Course Reversal: When And Where Will The Treasury Make Coupon Cuts

This Friday, the Treasury will kick start its upcoming quarterly refunding meeting with the release of the primary dealer questionnaire at noon. An area rates traders will be closely focused on is the potential cuts to coupon issuance – when, how big, and what maturities?

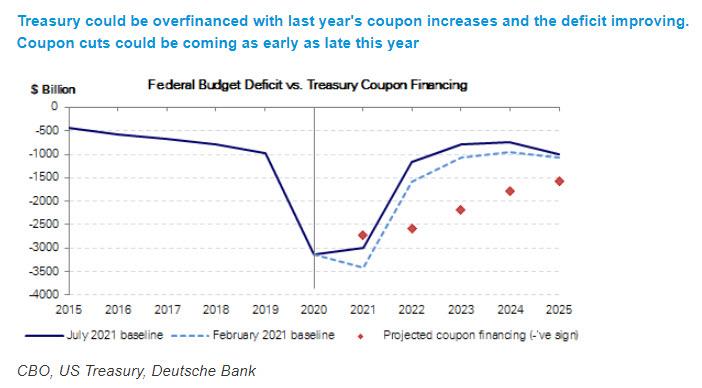

Such a move would represent a material reversal to a long-running trend: As DB’s Steven Zend reminds us, between April and November 2020, the Treasury rapidly raised issuance sizes for coupon securities, taking gross monthly sales from around $225BN before Covid to currently around $370BN. As a result, at the current juncture, and absent any future fiscal “shocks”, the Treasury stands to be overfinanced in the next few years.

This month, the CBO updated its baseline long-term deficit projections. As noted previously, relative to its March projections, the Congressional beancounters now project smaller deficits due to higher revenues from a stronger economy. As a result, after 2021, deficits are expected to fall significantly and average $1.2 trillion annually. In comparison, the Treasury’s coupon financing capacity looks too big, and according to Zeng’s estimates it will generate $2.6 trillion in net issuance in FY2022, $2.2 trillion in FY2023, and $1.8 trillion in FY2024. All else equal, this suggests there is room to reduce coupon issuance as soon as this year and by half a trillion or more per year in the first two years.

So how should these cuts be allocated?

Answering this question, Zeng writes that reducing the issuance of short maturities has the benefit of allowing the Treasury to extend the average maturity of its debt and reduce future rollover risk. But cutting the long-end may be needed to address liquidity issues that have arisen with last year’s size increases, particularly in the 20yr sector. Additionally, large cuts to the long-end could also have market implications. Depending on the amount the Treasury ultimately decides, the DB strategists concludes that cuts could be allocated across the curve but skew to the long-end.

In any case, while the upcoming refunding is too early for this to happen, the Treasury will send a strong signal if it has these cuts planned for November, which Zeng thinks is realistic.

Tyler Durden

Wed, 07/14/2021 – 14:27

via ZeroHedge News https://ift.tt/3eiG20w Tyler Durden