Kolanovic Calls An End To The Covid Pandemic, Lays Out How To Trade The Energy Crisis

JPMorgan’s Marko Kolanovic, who late last month was promoted for the second time this year most recently being named co-head of all global research at the largest US bank, has not only been one of the most bullish Wall Street voices, but one of the most vocal covid optimists, frequently predicting that the end of the delta wave is just a matter of time and that markets should largely ignore it, to wit:

- JPM’s Kolanovic Finds Coronavirus Lockdowns “May Have Caused More Deaths Than Covid-19 Itself”

- JPM’s Kolanovic: Stop Freaking Out About The Delta Case Spike

- JPM’s Kolanovic: The Delta Variant Does Not Pose A Risk For Markets

… although to be fair, most if not all of these calls were self-serving and came in the context of his client recos to aggressively buy value stocks (while fading overvalued growth and tech stocks). That said, Kolanovic never actually called the end of the pandemic, but rather tentatively predicted its peak and decline.

That changed today when in his latest market note – in which he once again, surprise, urges clients to literally “buy the dip (ex high-multiple tech)”, the Croatian PhD has finally done it and has called for the official end of the pandemic, to wit:

Our core view remains that the COVID situation will continue improving driving a cyclical recovery. This will be the case for at least the next 3-4 months given COVID wave dynamics, but most likely also beyond that. We believe that this was the last significant wave, and an effective end to the pandemic – in the historical echo of the 1918/1919 pandemic (and a number of other pandemics in the last century) that also had ~4 waves and lasted about ~20 months. New COVID treatments are also supportive of this view.

And given the multi-decade lows in capex, inventories and what he calls “favorable conditions of consumer balance sheets”, Kolanovic believes the cyclical recovery “can run strongly for the next year or longer.”

Of course, markets have been bracing for the coming growth-to-value rotation, and as the JPM strategist notes this has manifested in a sharp spike in market volatility coupled with “a meaningful de-risking of systematic and discretionary managers. For instance, leverage in systematic strategies decreased from ~75th to ~45th percentile, and hedge fund betas declined to historical average levels.”

Always cheerful, Kolanovic – who in the past 5 years has not met a market he wouldn’t buy, unlike the skeptical Kolanovic of oil – believes “the recent pullback is an opportunity to buy the dip in cyclical assets – which would include all equities (EM and DM) apart from high-multiple growth sectors (e.g., Nasdaq 100).”

The reason for this is his view on intensifying energy issues, rising inflation and bond yields, “and still extreme overweights in growth and tech stocks, and underweights in value and cyclical stocks. Our highest conviction ideas remain energy (equities and commodity), materials, industrials and financials, and reopening, COVID-recovery, reflation and consumer themes.”

For what it’s worth, we completely agree with Kolanovic that while tech is massively overvalued and energy is the cheapest it has been on a relative basis perhaps ever, we are not as confident that the market will be quite so willing to rotate out of the five FAAMG stocks, which account for 25% of the S&P market cap, into the energy sector which in its entirety, accounts for just 4% of S&P market cap. Putting it mildly, such a rotation would leave countless casualties as there would be virtually no room to “rotate into.”

That challenging math however does not daunt the JPM quant, who believes that the current energy and supply chain issues “do not jeopardize, but in fact reinforce, our rotation thesis.” He explains why:

The current energy issues caught the attention of global investors over the past weeks. While some clients are calling these developments collectively ‘Greenflation,’ indicating green policies are the only driver of the current woes, we maintain these effects are not driven by a single cause, but by a more complex interplay of green energy policies (impacting capital flows), issues related to the onset and recovery from the COVID pandemic (demand, labor and supply chain frictions), as well as several current geopolitical developments (OPEC+, Russia, Iran, etc.).

That said, while Kolanovic disagrees with a recent take from DB (laid out in “Will ESG Trigger Energy Hyperinflation“) and argues that the crisis is not caused by green policies alone (also disagreeing with Vladimir Putin who earlier today said Europe’s soaring prices on the shift to renewable energy sources in Europe), he admits that it also “appears farfetched to think that green policies don’t play a role in the current crisis, as recently suggested by the IEA (here).” The reason, he said, is simple and can be explained in one sentence: Given that a goal of the ESG/green initiative is to divert capital from fossil fuels development, affected companies will not have sufficient capital to provide needed supply, or will require significantly higher profits to clear the (higher) cost of capital hurdle.

Yet while he himself admits that historically centrally planned economic transitions – such as this one – have contributed to large crises (e.g., here and here), Kolanovic does not believe “the current energy issues will evolve to such catastrophic dimensions, primarily because of democratic election processes and pragmatism of political parties to adjust the course, and market-based incentives.” While we admire the naivete of this view – especially since the bulk of global energy production is in countries which the West is quick to point out are anything by democracies – we hope he is correct in expecting that “at some (higher) energy price, traditional energy capex in the US will increase, which will ease the current crisis.” Because if he is wrong, the coming crisis will be greater than anything seen in recent history.

Having laid out his bigger picture argument why he does not expect the energy crisis to lead to catastrophe, Kolanovic next drills – pardon the pun – into why he does not believe that “the current price of energy will have a significant negative impact on the economy.” He starts of by arguing that the market can easily digest $130 or even $150 oil, an assumption which we are confident many energy analysts will find quite confusing:

For instance, the economy and consumer were functioning just fine in the period over 2010-15, when oil averaged above $100. Adjusting for inflation, consumer balance sheets, total oil expenditures, wages and prices of other assets (housing, stocks, etc.), we think even with oil at $130 or $150 equity markets and the economy could function well (with some rebalancing and capital rotations).

In fact, all of the major asset classes (bonds, stocks, real estate, etc.) have increased ~50% or more, while oil has declined 25% over the last decade. Oil is by all cross-asset comparisons cheap today, and one could argue that OPEC (and US producers) have been subsidizing global consumption over the past decade (and last year during near-zero oil prices, subsidizing retail flows into speculative products such as crypto and NFTs).

Additionally, ever optimistic, the Croatian also thinks that markets can easily absorb higher rates, and he does not expect a broad market selloff unless yields were to rise above 250-300 bps (US 10y), which he doesn’t foresee in the near term. To this one can of course counter that with 10Ys at 1.50% the FAAMGs are already nearly down 10% from their highs so once can only imagine what will happen when rates rise another 150bps. That said, this particular #timestamp from Kolanovic will be revisited once the 10Y does hit 2.50% and when, if Kolanovic is right, the S&P will be trading higher from current levels.

But what about the consumer tax that are soaring energy prices? Here Kolanovic has some soothing words too, arguing that “consumer balance sheets are now in a strong position and some reallocation of expenditures towards energy would not set back the economy and equity markets.” Well, maybe not very strong position, because in the very next sentence he claims that “at the low end of the income range, potential strain from high gas prices could be an issue” but he believes this can “easily be addressed with a small fraction of current stimulus plans.”

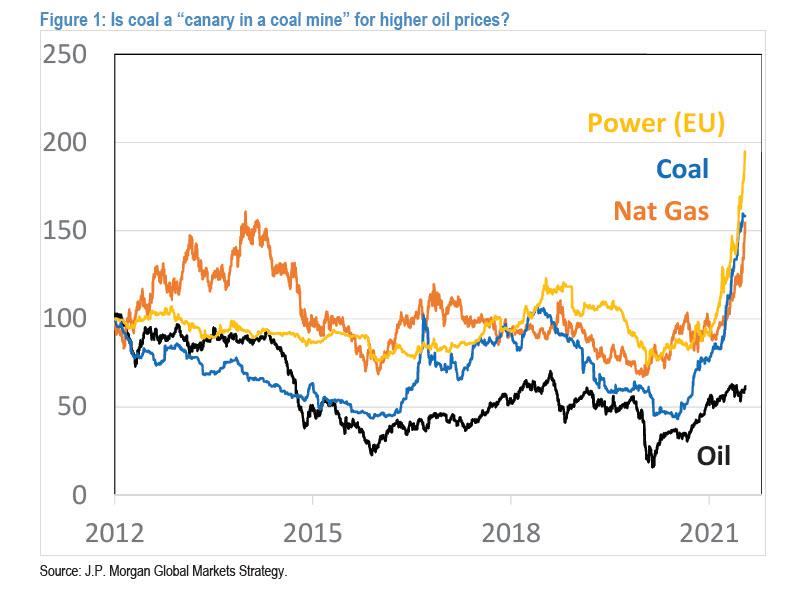

Finally, when looking at relative asset prices, Kolanovic claims that while oil is currently cheap relative to other assets “this is not the case with other forms of energy such as LNG, coal, natural gas, electricity, and uranium, which are all at or near all-time highs.” The JPM strategist believes that the evolution of coal prices might reflect supply, demand, cost of capital and energy transitioning issues for all fossil fuels, and as such, it would certainly be possible that oil prices will follow the same pattern (inflation adjusted for oil, that would be in a $150-200/bbl range).

And, in a faint glimpse of the old Kolanovic who looked at the future with great skepticism, the Croat then says that “the risk is that coal is a proverbial “canary in a coal mine” for the much more important commodity oil (figure below). Laws of physics (law of conservation of energy) would indicate that various forms of energy are interchangeable, as we are seeing currently with some oil for gas substitution, or firing up of coal plants above certain thresholds of electricity prices, private power generation, etc.”

Arguing that energy substitution is what really matters (even if once again energy analysts would have a field day with this “assumption”), and saying that “the linkage between various sources of energy has been true in financial markets as well, and historically energy assets have been correlated (averaging about 20-30% correlation of price returns)” the quant concludes that since oil is likely set to soar, “investors should consider hedging for higher oil prices, which can be expressed in asset class (long commodities, short bonds), sector (long energy), style (long value, short growth) or thematic form.”

His conclusion: “the most likely outcome of the current energy crisis is increased production at significantly higher energy prices, which would stabilize the global economy and energy infrastructure, but also temporarily slow down the energy transition.”

Tyler Durden

Wed, 10/06/2021 – 12:40

via ZeroHedge News https://ift.tt/3mw7vil Tyler Durden