Futures Meltup To New All Time High As November Begins With A Bang

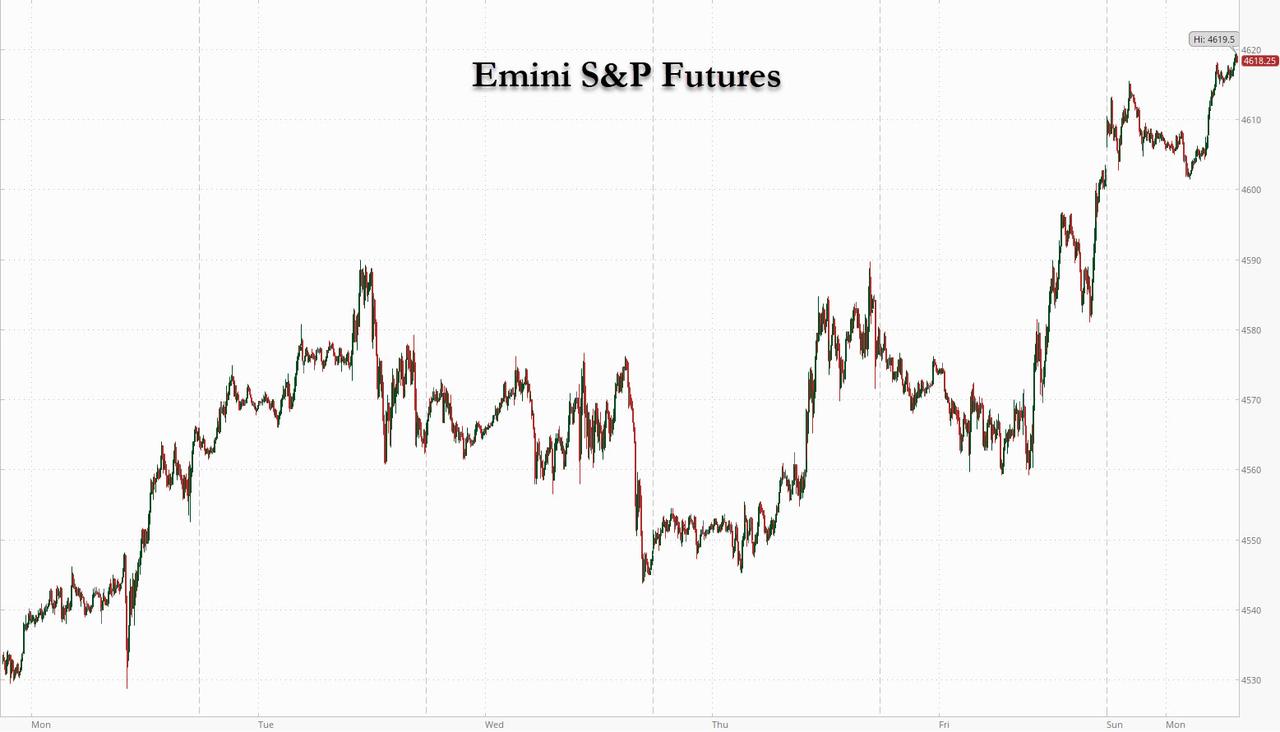

US futures and European stocks rose to a new record high to start the historically stellar month of November…

… and Asian markets jumped amid positive earnings surprises and as concerns of a global stagflation and central bank policy error faded for a few hours (they will return shortly). TSLA melted up by another $35BN in market cap “because gamma.” S&P 500 futures climbed 0.4% after the cash index posted the biggest monthly gain since last November. Treasury Secretary Janet Yellen expressed confidence in the continuing recovery from the pandemic, helping spur gains in equity markets. Health-care shares rallied in Europe. The dollar and Treasury yields advanced as investors awaited this week’s Federal Reserve meeting to announce the start of tapering (which will then lead to rate hikes next July according to Goldman). Oil rebounded on fresh supply concerns.

In addition to the now absolutely batshit insane meltup in Tesla, which won’t end until the SEC cracks down on gamma squeeze manipulation, other mega-cap technology stocks such as Google, Meta, Microsoft, Amazon.and Apple, aka oddly enough GAMMA, traded mixed. Exxon and Chevron added about 0.7% each as JP Morgan raised its price target on the oil majors following their strong quarterly results last week. Major Wall Street banks gained between 0.2% and 0.8%. The broader S&P 500 financials sector slipped last week, breaking a three-week winning streak. Lucid Group Inc. rose 4.8% in premarket, extending its advance from last week, after the new U.S. tax plan included a proposal to make EV tax credits more widely available. Harley-Davidson Inc jumped 8.2% after the European Union removed retaliatory tariffs on U.S. products including whiskey, power boats and company’s motorcycles. Here are the most notable pre-market movers:

- Tesla shares rise 2.3% in U.S. premarket trading after their biggest monthly gain in almost a year in October

- ABVC BioPharma jumps more than 700% as thelittle known biotechnology company garners attention from retail traders on social media

- Ocugen and Zosano (ZSAN US) are some other top gainers among retail trader stocks in premarket

A largely upbeat earnings season has helped investors look past a mixed-macro economic picture, with the benchmark S&P 500 and the tech-heavy Nasdaq recording their best monthly performance since November 2020 in October. Of the 279 S&P 500 companies that have reported quarterly results, 87% have met or exceeded estimates. Among members of Europe’s Stoxx 600 index, 68% surpassed expectations. On the economic data front, readings on October factory activity data from IHS Markit and ISM are due after market open, followed by non-farm payrolls on Friday.

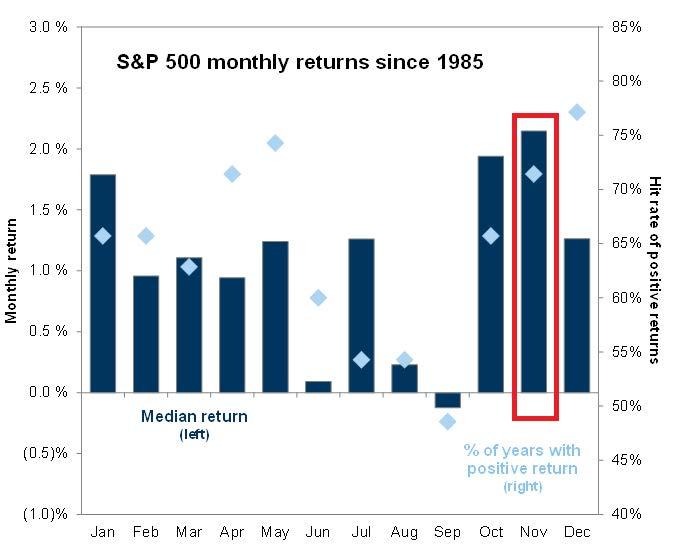

Focus is now on the Fed’s two-day policy meeting which concludes at 2pm on Nov 3, where the central bank will announce the tapering of its $120 billion monthly bond buying program by $15 billion. With recent U.S. data showing inflation pressures building, the market has also started pricing in rate hikes next year. November and December tend to be among the strongest months for stocks and any hawkish tilt in the Fed’s message could catch equities by surprise. Meanwhile, Biden’s economic agenda seemed to be on track as Democratic lawmakers worked to overcome their differences on a $1.75 trillion social-spending plan.

“Depending on where you are looking, you are getting very different stories on the outlook for global markets,” Kerry Craig, global market strategist at JPMorgan Asset Management, said on Bloomberg Television. “If you look at equities and the rally you are seeing, you think everything is OK. If you look at the bond market and how yields are moving, there’s obviously a lot more concern around inflation and policy normalization.”

European stocks hit the afterburner out of the gate with the Euro Stoxx 50 adding as much as 1% before drifting off best levels. FTSE MIB and IBEX outperform, FTSE 100 lags slightly. Banks, construction and travel are the strongest sectors; tech the sole Stoxx 600 sector in the red. Barclays Plc fell 1.5%. Chief Executive Officer Jes Staley stepped down amid a U.K. regulatory probe into how he characterized his ties to the financier and sex offender Jeffrey Epstein.

Asian stocks were poised to snap a three-day decline thanks to a rally in Japanese equities, which got a boost from an election victory for the country’s ruling party and Prime Minister Fumio Kishida. The MSCI Asia Pacific Index advanced as much as 0.6%, while Japan’s benchmark Topix and the blue-chip Nikkei 225 Stock Average each added more than 2%. Sony Group, Toyota Motor and Tokyo Electron were among the single-largest contributors to the regional measure’s rise. By sector, industrials and information-technology companies provided the biggest boosts. Japan’s ruling Liberal Democratic Party defied worst-case scenarios to secure a majority by itself in a closely-watched election Sunday. Analysts said the outcome signals political stability, paving the way for economic stimulus to be executed as anticipated (see Street Wrap). “Indicators of market activity show that there will be a positive market impact to the election, as although it was not greatly different than expectations, the LDP clearly surpassed some of the more dire polls of last week and there will not likely be any party shake-up in the intermediate-term,” John Vail, Tokyo-based chief global strategist at Nikko Asset Management wrote in a note. The market is also “reacting positively” to Friday’s share-price gains in the U.S., Vail said. Futures on the S&P 500 rose during Asian trading hours after the underlying gauge added 0.2%. Asia’s regional benchmark capped a weekly drop of 1.5%, its worst such performance since early October, as disappointing results weighed on big technology stocks. More than half of the companies on the MSCI Asia Pacific Index have reported results for the latest quarter with about 37% posting a positive surprise, according to data compiled by Bloomberg.

Australia’s S&P/ASX 200 index rose 0.6% to 7,370.80, recouping some losses after Friday’s 1.4% plunge. Health and consumer discretionary stocks contributed the most to the benchmark’s gain. WiseTech was among the top performers, snapping a four-day losing streak. Westpac was the worst performer after the bank delivered a smaller share buyback than some had expected. In New Zealand, the S&P/NZX 50 index fell 0.5% to 13,030.31.

In rates, fixed income trades heavy with gilts leading the long end weakness. Treasuries were slightly cheaper on the long-end of the curve as S&P 500 futures exceed last week’s record highs. Yields are cheaper by 2bp to 2.5bp from belly out to long-end, with front-end slightly outperforming and steepening 2s10s spread by 1.7bp; 10-year yields around 1.58% with gilts underperforming by 1.1bp, Italian bonds by 3.5bp. Gilts and Italian bonds lag, with Bank of England rate decision due Thursday. In the U.S., weekly highlights include refunding announcement and FOMC Wednesday and Friday’s October jobs report. Bund and gilt curves bear steepen with gilts ~1bps cheaper to bunds. Peripheral spreads swing an early tightening to a broad widening to core with Italy the weakest performer. Overnight futures and options flows included block seller in 5-year note futures (3,900 at 3:09am ET) and a buyer of TY Week 1 129.00 puts at 3 on 10,000, says London trader.

In FX, the Bloomberg dollar index held a narrow range. SEK and CHF top the G-10 score board, GBP lags with cable snapping below 1.3650. TRY outperforms EMFX peers.

- The BBDXY inched up and the greenback traded mixed against its Group-of-10 peers, with many of the risk-sensitive currencies leading gains

- The pound retraced some losses against the dollar, after dipping earlier in the European session. The yield on 2-year gilts hit the highest since May 2019. Financial markets are almost fully pricing in a 15-basis point increase in the Bank of England’s benchmark lending rate on Nov. 4, while economists increasingly share that view, even as they see the decision as a far closer call. A record share of U.K. businesses are expecting to increase prices, adding to the inflationary pressures confronting Bank of England policy makers ahead of their meeting on Thursday

- Australian bonds extended opening gains as traders positioned for the Reserve Bank’s policy decision Tuesday. The Aussie fell, tracking losses in iron ore prices following a weak China PMI, which showed signs of further weakness in October

- The yen fell for a second day after the ruling Liberal Democratic Party retained its outright majority in a lower-house election, reinforcing bets for fiscal stimulus and reforms. Hedge funds boosted net short positions on the yen to the most since January 2019, raising the risk of a squeeze should risk appetite deteriorate suddenly and demand for havens rise

- The Turkish lira edged higher after Turkish President Recep Tayyip Erdogan said he had “positive” talks with U.S. President Joe Biden

In commodities, crude futures drift higher. WTI adds 40c to trade near $84; Brent rises ~1% near $84.50. Spot gold is quiet near $1,786/oz. Base metals are mixed: LME nickel and tin outperform, zinc lags.

Looking at today’s calendar, earnings continue on Monday with PG&E and ON Semiconductor reporting pre-market, and NXP Semiconductors post-market. We also get the latest Mfg PMI print and the October Mfg ISM print.

Market Snapshot

- S&P 500 futures up 0.3% to 4,612.25

- STOXX Europe 600 up 0.8% to 479.40

- MXAP up 0.4% to 198.04

- MXAPJ down 0.3% to 645.49

- Nikkei up 2.6% to 29,647.08

- Topix up 2.2% to 2,044.72

- Hang Seng Index down 0.9% to 25,154.32

- Shanghai Composite little changed at 3,544.48

- Sensex up 1.3% to 60,079.40

- Australia S&P/ASX 200 up 0.6% to 7,370.78

- Kospi up 0.3% to 2,978.94

- Brent Futures up 0.3% to $83.95/bbl

- Gold spot down 0.0% to $1,783.20

- U.S. Dollar Index little changed at 94.14

- German 10Y yield little changed at -0.091%

- Euro up 0.1% to $1.1571

Top Overnight News from Bloomberg

- House Democratic leaders are pushing hard to get Biden’s package finalized, with votes on both that bill and a smaller infrastructure plan this week — the latest in a string of self- imposed deadlines. The Senate, which already approved the public-works bill, is likely to vote on the larger package later in the month

- Leaders of the Group of 20 countries agreed on a climate deal that fell well short of what some nations were pushing for, leaving it to negotiators at the COP26 summit in Glasgow this week to try to achieve a breakthrough

- The U.K. said it will trigger legal action against France within 48 hours unless a dispute over post-Brexit fishing rights is resolved, as the growing spat threatens to overshadow the United Nations’ climate summit

- Treasury Secretary Janet Yellen said she believes Federal Reserve Chair Jerome Powell has taken “significant action” in the wake of revelations over the personal investments of U.S. central-bank policy makers; Yellen dismissed recent moves in the bond market that have signaled concern about monetary policy makers squelching economic growth, and expressed confidence in the continuing recovery from the Covid-19 pandemic

- The U.S. and the European Union have reached a trade truce on steel and aluminum that will allow the allies to remove tariffs on more than $10 billion of their exports each year

Asia-Pac bourses traded mostly higher amid tailwinds from last Friday’s fresh record highs in the US where Wall St. topped off its best monthly performance YTD, but with some of the advances in the region capped as participants digested mixed Chinese PMI data and ahead of this week’s slew of key risk events including crucial central bank policy announcements from the RBA, BOE and FOMC, as well as the latest NFP jobs data. ASX 200 (+0.8%) was led higher by the consumer-related sectors amid a reopening play after Australia permitted fully vaccinated citizens to travel internationally again and with several M&A related headlines adding to the optimism including the Brookfield-led consortium acquisition of AusNet Services and Seven West Media’s takeover of Prime Media. Conversely, the largest weighted financials sector failed to join in on the spoils with Westpac shares heavily pressured following its FY results which fell short of analyst estimates despite more than doubling on its cash earnings. Nikkei 225 (+2.5%) was the biggest gainer with the index underpinned by favourable currency flows and following the general election in which the ruling LDP maintained a majority in the lower house although won fewer seats than previously for its slimmest majority since 2012, while the KOSPI (+0.4%) was kept afloat but with upside limited by slightly softer than expected trade data. Hang Seng (-1.5%) and Shanghai Comp. (+0.1%) were subdued amid a slew of earnings releases and following mixed Chinese PMI data in which the official Manufacturing and Non-Manufacturing PMIs disappointed analysts’ forecasts with the former at a second consecutive contraction, although Caixin Manufacturing PMI was more encouraging and topped market consensus. Finally, 10yr JGBs initially declined amid gains in stocks and recent pressure in T-notes due to rate hike bets with analysts at Goldman Sachs bringing forward their Fed rate hike calls to July 2022 from summer 2023 citing inflation concerns, although 10yr JGBS then recovered despite the mixed results from the 10yr JGB auction which showed a higher b/c amid lower accepted prices and wider tail in price.

Top Asian News

- Japan’s Kishida Mulls Motegi for LDP Secretary General: Kyodo

- Home Sales Slump; Another Bond Deadline Looms: Evergrande Update

- Two Thirds of China’s Top Developers Breach a ‘Red Line’ on Debt

- Hedge Fund Quad Sells Memory Stocks Citing Demand Uncertainty

European equities (Stoxx 600 +0.6%) have kicked the week off on the front-foot with the Stoxx 600 printing a fresh all-time-high. The handover from the APAC session was a largely constructive one with the Nikkei 225 (+2.6%) the best in class for the region amid favourable currency flows and the fallout from the Japanese general election which saw the ruling LDP party maintain a majority in the lower house. Elsewhere, performance for the Shanghai Composite (-0.1%) and Hang Seng (-0.9%) was less impressive amid a slew of earnings releases and mixed Chinese PMI data in which the official Manufacturing and Non-Manufacturing PMIs disappointed analysts’ forecasts. US equity index futures are trading on a firmer footing (ES +0.5%) ahead of Wednesday’s FOMC announcement and Friday’s NFP data. The latest reports from Washington suggest that House Democrats are hoping to pass the social spending and bipartisan infrastructure bills as soon as Tuesday. Back to Europe, a recent note from JPM stated that Q3 European earnings “are coming in well ahead of expectations in aggregate”, adding that results are healthy when considering the “trickier operating backdrop”. Sectors in the region are higher across the board with Auto names top of the leaderboard. Renault (+3.3%) sits at the top of the CAC 40 with the name potentially gaining some reprieve from agreement to resolve the US-EU steel and aluminium trade dispute (something which the Co. has previously noted as a negative). Also following the resolution, Thyssenkrupp (+2.8%) and Salzgitter (+4.5%) are both trading notably higher. Barclays (-2.0%) shares are seen lower after news that CEO Staley is to step down with immediate effect following the investigation into his relationship with sex offender Jeffrey Epstein; Barclays’ Global Head of Markets, Venkatakrishnan is to take over. UK homebuilders (Persimmon -2.1%, Taylor Wimpey -1.9%, Barratt Developments -1.9%, Berkeley Group -1.7%) are softer on the session amid concerns that the sector could fall victim to higher mortgage rates given the shape of the UK yield curve. Ryanair (+1%) shares are higher post-earnings which saw the Co. continue its recovery from the pandemic, albeit still expects a loss for the year. Furthermore, the board is considering the merits of retaining its standard listing on the LSE. Finally, BT (+4.2%) is the best performer in the Stoxx 600 ahead of earnings on Thursday with press reports suggesting that the Co. could announce that its GBP 1bln cost savings target will be met a year earlier than the guided March 2023.

Top European News

- SIG Proposed Offering for EU300m Senior Secured Notes Due 2026

- Delivery Hero’s Turkey Unit CEO Nevzat Aydin to Step Down

- Goldman Sachs Says ‘Lost Decade’ Is Looming for 60/40 Portfolios

- URW Sells Stake in Paris Triangle Tower Project to AXA IM Alts

In FX, the Greenback is holding above 94.000 in index terms and gradually ground higher after pausing for breath and taking some time out following its rapid resurgence last Friday to eclipse the 94.302 month end best at 94.313 before waning again. Hawkish vibes going into the FOMC are underpinning the Dollar and helping to offset external factors that are less supportive, including ongoing strength in global stock markets on solid if not stellar Q3 earnings and economic recovery from COVID-19 lockdown or restricted levels. Hence, the DXY is keeping its head above the round number and outperforming most major peers within and beyond the basket, awaiting Markit’s final manufacturing PMI, the equivalent ISM and construction spending ahead of the Fed on Wednesday and NFP on Friday.

- JPY/AUD – Little sign of relief for the Yen from victory by Japan’s ruling LDP part at the weekend elections as the 261 seat majority secured is down from the previous 276 and the tightest winning margin since 2012. Moreover, Security General Amari lost his constituency and new PM Kishida concedes that this reflects the public’s adverse feelings towards the Government over the last 4 years. Usd/Jpy is eyeing 114.50 as a result and the Aussie is looking precarious around 0.7500 against the backdrop of weakness in commodity prices even though perceptions for the upcoming RBA have turned markedly towards the potential for YCT to be withdrawn following firm core inflation readings and no defence of the 0.1% April 2024 bond target.

- NZD/EUR/CHF/CAD/GBP – All narrowly mixed vs their US counterpart, and with the Kiwi also taking advantage of the aforementioned apprehension in the Aud via the cross, while the Euro has pared declines from just under 1.1550, but still looks top-heavy into 1.1600. Elsewhere, the Franc is pivoting 0.9160 and 1.0600 against the Euro with more attention on a rise in Swiss sight deposits at domestic banks as evidence of intervention than a fractionally softer than expected manufacturing PMI, the Loonie is keeping afloat of 1.2400 ahead of Markit’s Canadian manufacturing PMI and Sterling is striving to stay above 1.3600, but underperforming vs the Euro circa 0.8470 amidst the ongoing tiff between the UK and France over fishing rights.

- SCANDI/EM – Robust Swedish and Norwegian manufacturing PMIs plus broad risk appetite is underpinning the Sek and Nok, in contrast to the Cnh and Cny following disappointing official Chinese PMIs vs a more respectable Caixin print, but the EM laggard is the Zar in knock-on reaction to Gold’s fall from grace on Friday, increasingly bearish technical impulses and SA energy supply issues compounded by Eskom’s load-shedding. Conversely, the Try has pared some declines irrespective of a slowdown in Turkey’s manufacturing PMI as the CBRT conducted a second repo op for Lira 27 bn funds maturing on November 11 at 16%.

In commodities, WTI and Brent are firmer this morning with gains of between USD 0.50-1.00/bbl, this upside is in-spite of a lack of fundamental newsflow explicitly for the complex and is seemingly derived from broader risk sentiment, as mentioned above. Nonetheless, Energy Ministers are beginning to give commentary ahead of Thursday’s OPEC+ event and so far Angola, Kuwait and Iraq officials have voiced their support for the planned 400k BPD hike to production in December. This reiteration of existing plans is in opposition from calls from non-OPEC members such as the US and Japan that the group should look to increase production quicker than planned, in a bid to quell rising prices. Separately, Saudi Aramco reported Q3 earnings over the weekend in which its net profit doubled given strong crude prices and sales volumes improving by 12% QQ; subsequently, some analysts have highlighted the possibility for a end-2021 special dividend. Elsewhere, base metals are mixed and fairly contained in-spite of the EU and US announcing an agreement to resolve the ongoing aluminium and steel trade dispute. While spot gold and silver are modestly firmer this morning as the yellow metal remains contained after its slip from the USD 1800/oz mark in the tail-end of last week. Currently, spot gold is pivoting its 100-DMA at USD 1786 with the 50- and 200-DMAs residing either side at USD 1780/oz and USD 1791/oz respectively.

US Event Calendar

- 9:45am: Oct. Markit US Manufacturing PMI, est. 59.2, prior 59.2

- 10am: Oct. ISM Manufacturing, est. 60.5, prior 61.1

- 10am: Sept. Construction Spending MoM, est. 0.4%, prior 0%

DB’s Jim Reid concludes the overnight wrap

Welcome to November. I had three halloween parties over the weekend which is probably more than the entire number I went to before I had kids. I still have some spooky make up on this morning that I just couldn’t get off from last night. So there’s a reason alone to zoom into the call at 3pm today.

As it’s the 1st of November Henry is about to publish our monthly performance review. It was a hectic month of higher inflation expectations and commodities, and also the best S&P 500 month of the year. Bonds underperformed across the board but these small negatives masked great volatility and stress under the surface, especially in the last week. See the report that should be out in the next 30-60mins.

With all due respect to our readers in Australia, I’m going to open the market section this morning with a line I don’t think I’ve written in 27 years of market commentary and probably won’t again. And it’s not about England thrashing Australia at cricket on Saturday. Yes the most important event of the week could be the RBA meeting tomorrow. 2 year yields last week rose from 0.15% on Wednesday morning to 0.775% at the close on Friday as the RBA were conspicuous by their absence in defending the 0.1% target on the April 24 bond. I’ve absolutely zero idea what they are going to do tomorrow which should help you all tremendously but their absence again this morning gives a decent indication. I was taught economics in an era where central banks liked to keep an element of mystery and surprise. As such I’ve always disliked the forward guidance era as it encourages markets to pile on to much riskier, one way positions that a normally functioning market should naturally allow. But to go from forward guidance to silence (that rhymes) is a recipe for huge market turmoil if the facts change. It’s unclear if the full implications of last week’s carnage at the global front end has yet been cleared out. There is lots of speculation about large unwinds, big stop losses etc. Liquidity was also awful last week. Much might depend on central banks this week. Make no mistake though there is considerable pain out there.

The latest this morning in Aussie rates is that the 2y yield is down around -7bps while the 10y yield is down -19.0bps. So we wait with baited breath for tomorrow. Elsewhere in Asia, the Nikkei 225 (+2.42%) is charging ahead this morning as Japan’s Liberal Democratic Party kept its majority after lower house elections, thus boosting optimism about a potential fiscal stimulus. Elsewhere, the KOSPI (+0.43%) and the Shanghai composite (+0.07%) are outperforming the Hang Seng (-1.10%). In terms of data, China’s official manufacturing PMI fell from 49.6 to 49.2 (49.7 expected), not helped by commodities price rises and electricity shortages. The non-manufacturing PMI also fell to 52.4 from 53.2 (consensus 53). The Caixin manufacturing PMI did beat at 50.6 this morning (consensus 50). In terms of virus developments in the region, Shanghai Disneyland is closed amid recent COVID outbreaks, while Singapore is adding ICU beds in response to high levels of serious cases. The S&P 500 mini futures is up +0.23% this morning, the US 10y Treasury is at 1.56% (+1.2bps).

It’s strange to have a likely Fed taper announcement on Wednesday be third billing for the week but the BoE on Thursday might be the next most important meeting as it’s still a finely judged call as to whether they hike this week or not. DB (preview here) think they will raise rates by 15bps with two 25bps hikes in February and May. They’ll also end QE a month earlier than planned.

So over to the third billing, namely the Fed. They will announce a well flagged taper on Wednesday. In line with recent guidance, DB expect that the Fed will announce monthly reductions of $10bn and $5bn of Treasury and MBS purchases, respectively. With the first cut to purchases coming mid-November, this will bring the latest round of QE to a conclusion in June 2022.

The Fed has some flexibility with this timetable but it will be interesting to hear how much Powell pushes back on markets that price in two hikes in 2022, including one almost fully priced for before the taper ends. If markets attacked the Fed in the same way they have the RBA the global financial system would have a lot of issues so it’s a fine balance for the Fed. They won’t want to push back too aggressively on market pricing given the uncertainty but they won’t want an outright attack on forward guidance.

Moving on, a lowly fourth billing will be reserved for US payrolls on Friday. DB expect the headline gain (+400k forecast, consensus +425k vs. +194k previously) to modestly outperform that of private payrolls (+350k vs. +317k) and for the unemployment rate to fall by a tenth to 4.7% and average hourly earnings to post another strong gain (+0.4% vs. +0.6%) amidst still-elevated hours worked (34.8hrs vs. 34.8hrs).

Outside of all this excitement, we have the COP26 which will dominate all your news outlets. The other main data highlight are the global PMIs (today and Wednesday mostly) which will give insight into how the economic recovery has progressed in the first month of Q4 with the surveys shedding light onto how inflation is affecting suppliers. There is lots more in store for us this week but see the day by day calendar at the end for the full run down

The market also enters the second half of the 3Q earnings season. There are 168 S&P 500 and 85 Stoxx 600 companies reporting this week with 52% of the S&P 500 and 48% of the STOXX 600 having already reported.

DB’s Binky Chadha published an update on earnings season over the weekend (link here). In the US, the size of the earnings beat has declined over the course of the season and is on track to hit 7%, well below the record 14-20% range post pandemic. Excluding the lumpy loan-loss reserve releases by banks, the beat is even lower at 5%, bringing it back in line with the historical norm. Quarterly earnings are on track to be down sequentially from Q2 to Q3 by -1.1% (qoq seasonally adjusted), the first drop since Q2 2020. The flat to down read of earnings is broad based across sector groups. Forward consensus estimates have fallen outside of the Energy sector. The S&P 500 nevertheless has seen one of the strongest earning season rallies on record. See much more in Binky’s piece.

This week’s highlights include NXP Semiconductors, Zoom, and Tata Motors today before Pfizer, T-Mobile, Estee Lauder, BP, Mondelez, Activision Blizzard, and AP Moller-Maersk tomorrow. Then on Wednesday we’ll hear from Novo Nordisk, Qualcomm, CVS, Marriott, Albemarle, and MGM resorts. Thursday sees reports from Toyota, Moderna, Square, Airbnb, Uber, and Deutsche Post and then a busy Friday with Alibaba Group, Dominion Energy, Honda, and Mitsubishi.

Looking back now and reviewing last week in numbers, it was a week of heightened intraday volatility within rates, as markets brought forward the expected timing of central bank policy actions across advanced economies while revising down growth expectations. Position stop outs almost certainly played a role as the magnitude of the moves were out of sync with macro developments while FX and equity markets were not nearly as volatile.

Global front end rates started moving in earnest on Wednesday, following the Bank of Canada’s surprise decision to end net asset purchases, while bringing forward the timing of liftoff, which sent 2yr Canadian bonds more than +20bps higher. In the following days, the RBA opted not to defend their yield curve control target, and ECB President Lagarde did not use her press conference to provide much of a forceful pushback on recent repricing.

All told, almost every DM economy saw their 2 yr bond selloff, including the US (+4.4 bps, +0.8 bps Friday), UK (+4.9 bps, +5.9 bps Friday), Germany (+5.2 bps, +3.2 bps Friday), Canada (+23bps) and Australia (+65bps). The long end went the other direction in the core countries, with many curves twist flattening over the week as negative growth sentiment weighed on the back end. Nominal 10yr yields declined -6.2 bps (-2.8 bps Friday) in the US, -11.1 bps (+2.5 bps Friday) in the UK, and were flat in Germany (+3.0 bps Friday). Unlike the rest of October, the decline in nominal yields coincided with declining inflation breakevens (albeit from historically high levels), with 10yr breakevens declining -5.2 bps (-0.6 bps Friday) in the US, -25.4 bps (-8.5 bps Friday) in the UK, and -16.3 bps (-11.5 bps Friday) in Germany. Note that outside the core there were some bond markets that moved higher in yield with 10yr bonds in Canada (+7bps), Australia (+30bps) and Italy (+19bps) all higher for different reasons. Some of the bond moves above don’t do the intra-day volatility any justice though.

Elsewhere Crude oil prices dipped to close out what was otherwise another very good month, with Brent and WTI -1.34% (+0.07% Friday) and -0.23% (+0.92% Friday) lower.

Meanwhile, equity markets marched to the beat of a different drum. The S&P 500 (+1.33%, +0.19% Friday), Nasdaq (+2.71%, +0.33% Friday), and DJIA (+0.40%, +.25% Friday) all set new all-time highs, while the STOXX 600 increased +0.77% (+0.07% Friday), cents below the all-time high set in August. Generally strong earnings relative to a worried market prior to the season again supported equity markets. Calls were replete with mentions of supply chain woes and labour shortages though, but companies sounded an optimistic note on end-user demand. Many big tech stocks reported, to more mixed results than the broader index. Alphabet and Microsoft beat on both revenue and earnings, Facebook and Apple missed analyst revenue estimates, while Amazon and Twitter missed revenue and earnings estimates. Ford and Caterpillar, two bellwethers particularly exposed to current supply chain and labour maladies, fared especially well. So far this season 279 companies have reported, with 206 beating on revenue and 237 beating on earnings

Out of D.C., after prolonged negotiations within the Democratic Party, US President Biden unveiled a new social and climate spending framework, containing $1.75 trillion in spending measures as well as revenue-raising offsets. Once the text is finalized, it should enable a vote on the social spending package as well as the separately-negotiated bi-partisan infrastructure bill. More is likely to come this week.

Tyler Durden

Mon, 11/01/2021 – 07:59

via ZeroHedge News https://ift.tt/3GEg97U Tyler Durden