“Escalator Up, And Elevator Down” – 60:40 Isn’t Dead, Just Resting

By Andrew Sheets, Chief Cross-Asset Strategist for Morgan Stanley

Among other things, 2022 remains a reminder to be careful what you wish for. Over the last decade, it’s been common to hear “yields are too low”, “spreads are too tight”, “valuations are too high”, “value never works” and “central bank policy is steamrolling everything”. But then a year came along that gave us higher yields, wider spreads, cheaper valuations, value outperformance and policy reversal…and it hasn’t exactly been a day at the beach.

All this comes to mind when we think about the long-term outlook for cross-asset performance. Over the years, we (and many others) have talked about how our estimates suggested historically low returns for a 60:40 portfolio. And frequently, it just didn’t matter. Global stocks and bonds continued to hum away nicely, delivering unusually strong returns and diversification.

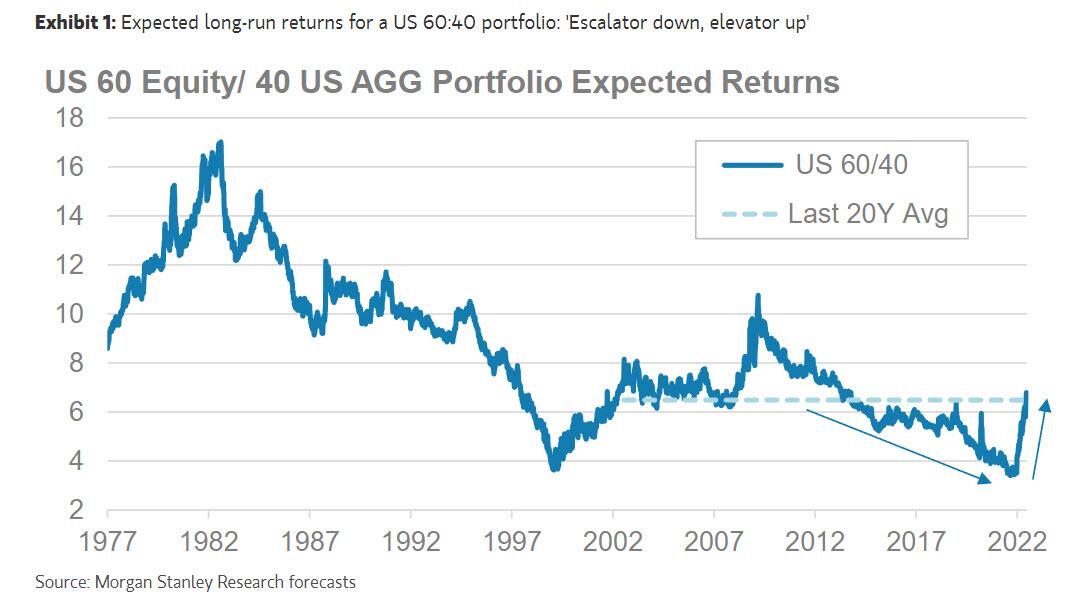

But then, all at once, those dour long-term forecasts came true. From January 1 through June 30 of this year, a 60:40 portfolio of US equities and the Aggregate Bond Index lost ~16% of its value, wiping out all 60:40 gains since September 2020. Portfolios in Europe suffered a similar fate. It’s often said that monetary policy is “an escalator up, and an elevator down”. Expected returns for a 60:40 portfolio were an escalator down and an elevator up.

Such extreme moves raise an obvious question: do these large losses, and the fact that they involved stock and bond prices moving in the same direction, mean that diversified portfolios of stocks and bonds are fundamentally broken in an era of tighter policy?

One way that 60:40 portfolios could be ‘broken’ is that they simply can’t generate reasonable returns going forward. But on our return estimates, this isn’t the case. Lower prices have raised our long-term return estimates for US and European equities, while higher yields have boosted our estimates for US and European bonds. For a 60:40 portfolio of US equities and Aggregate bonds, for example, we forecast a 10-year return of +6.2% per annum, or 3.9pp above expected inflation.

Could our estimates be wrong? Certainly. Any projection of market performance is uncertain, especially in the short run. But we think that our process, built by my colleague Serena Tang, is solid, and it has been effective in explaining historical returns over the long run.

I sense that an even bigger investor concern, however, is the relevance of diversification. The drawdown of a 60:40 portfolio this year isn’t necessarily extreme in its magnitude (2002 and 2008 were worse) but rather its uniformity, as almost every asset class (barring commodities) lost money. Whereas those previous large drawdowns left investors wishing they had held more fixed income, this year has left investors wishing they didn’t own anything.

These fears have been given a face: bond-equity correlation. The story goes something like this: for most of the last 20 years, bond and equity returns were negatively correlated, moving in opposite directions and diversifying each other. But since the large policy interventions of 2020, this correlation has turned positive. Stock and bond prices are now moving in the same direction. The case for diversification is over.

This is a good story, and like all good stories, it contains a grain of truth. The largest expansion of central bank support in history in 2020-21 did boost both stocks and bonds, support that is now reversing. But there is also a risk of confusing direction and magnitude: bonds can still be good diversifiers, even if they aren’t as good as before.

The reason is some relatively simple math. Even if stocks and bonds are now positively correlated, that correlation is well below 1. There are still plenty of days where they don’t move together. That matters, as even ‘positive’ correlation can still have a dampening effect on volatility. Based on average volatility over the last decade, raising the stock-bond correlation from -0.2 to +0.2 would only increase the volatility of a US 60:40 portfolio from 10.2% to 10.8%. That’s hardly cataclysmic.

The reason why the correlation effect can be small is that the volatility impact can be large. The last six months have seen the worst drawdown in bond prices in 40 years, and unusually high levels of implied volatility. Bonds have been riskier than at any point in most investors’ careers.

Yet even then, the trailing 1-year volatility on the US Aggregate Bond index is ~6%, less than a third of the volatility of US equities over the same period. And for portfolio construction, that matters, as having 40% of a portfolio in anything with one-third the volatility of the other 60% will absolutely dampen overall fluctuations. Hence, despite recent struggles, the case for 60:40-type approaches endures, with higher estimated long-term returns in the US and Europe over the next decade than at most points over the last 10 years.

Tyler Durden

Sun, 07/24/2022 – 13:30

via ZeroHedge News https://ift.tt/DklYAvG Tyler Durden