South Dakota Governor Bans TikTok From State-Owned Devices

Government employees in South Dakota will no longer be allowed to have TikTok installed on government devices due to security concerns.

“Because of our serious duty to protect the private data of South Dakota citizens, we must take this action immediately,” said Republican Governor Kristi Noem in a statement. “I hope other states will follow South Dakota’s lead, and Congress should take broader action, as well.”

Noem made the ban official in a Tuesday executive order.

The move comes roughly a month after FCC commissioner Brendan Carr told Axios that the Biden administration’s Council on Foreign Investment in the US (CFIUS) should take action against the hugely popular Chinese-owned app which allows users to post short videos, adding that it poses a “national security concern.”

“I don’t believe there is a path forward for anything other than a ban,” said Carr.

Axios said TikTok is in discussions with CFIUS about whether it can be divested from ByteDance, a Chinese company, to an American company to remain operational in the US.

In addition to their general concerns about all social media companies, US officials worry about TikTok’s data collection polices and its relationship to the Chinese government. That’s prompted calls from US Senators to fully ban the app. TikTok has said it is confident it will reach a resolution with US officials that allows the app to remain in the country. -Bloomberg

On Wednesday, Treasury Secretary Janet Yellen – chair of the CFIUS, told a conference hosted by the New York Times: “I think there are legitimate national security considerations. “

Meanwhile in late October, Sen. Mark Warner (D-Va.), head of the US Senate intelligence committee, admitted that President Trump was right regarding the security risks surrounding the video app.

Across the political spectrum, Republican lawmakers are in line with Democrats about TikTok:

“No surprise there,TikTok is just another invasive tool for communist China to infiltrate Americans‘ personal and proprietary information,” Rep. Ken Buck (R-Colo.) told The Epoch Times. “This app presents a very real threat to our national security, and the United States should take strong action to stop the CCP’s espionage campaign.”

And in another October interview, China-In-Focus’ Tiffany Meier sat down with Casey Fleming, CEO of intelligence and security strategy firm BlackOps Partners, who said:

“What people need to understand is that TikTok is a military application.

It’s a weaponized espionage application to get every bit of information they possibly can off the phone, which they do – your whereabouts, how you go about your day, your access to other people, access to technology, intellectual property, and things that you can be blackmailed on, and so on.

So people need to understand that TikTok is a weaponized military application in the hands of our middle schoolers, our kids, our high school kids, and our young adults.”

As a reminder, India banned TikTok in 2020 “to protect the data and privacy of its 1.3 billion citizens” and to put a stop to technology that was “stealing and surreptitiously transmitting users’ data in unauthorized servers outside India.”

Today I will offer a progress report on the Federal Open Market Committee’s (FOMC) efforts to restore price stability to the U.S. economy for the benefit of the American people. The report must begin by acknowledging the reality that inflation remains far too high. My colleagues and I are acutely aware that high inflation is imposing significant hardship, straining budgets and shrinking what paychecks will buy. This is especially painful for those least able to meet the higher costs of essentials like food, housing, and transportation. Price stability is the responsibility of the Federal Reserve and serves as the bedrock of our economy. Without price stability, the economy does not work for anyone. In particular, without price stability, we will not achieve a sustained period of strong labor market conditions that benefit all.

We currently estimate that 12-month personal consumption expenditures (PCE) inflation through October ran at 6.0 percent (figure 1).1 While October inflation data received so far showed a welcome surprise to the downside, these are a single month’s data, which followed upside surprises over the previous two months. As figure 1 makes clear, down months in the data have often been followed by renewed increases. It will take substantially more evidence to give comfort that inflation is actually declining. By any standard, inflation remains much too high.

For purposes of this discussion, I will focus my comments on core PCE inflation, which omits the food and energy inflation components, which have been lower recently but are quite volatile. Our inflation goal is for total inflation, of course, as food and energy prices matter a great deal for household budgets. But core inflation often gives a more accurate indicator of where overall inflation is headed. Twelve-month core PCE inflation stands at 5.0 percent in our October estimate, approximately where it stood last December when policy tightening was in its early stages. Over 2022, core inflation rose a few tenths above 5 percent and fell a few tenths below, but it mainly moved sideways. So when will inflation come down?

I could answer this question by pointing to the inflation forecasts of private-sector forecasters or of FOMC participants, which broadly show a significant decline over the next year. But forecasts have been predicting just such a decline for more than a year, while inflation has moved stubbornly sideways. The truth is that the path ahead for inflation remains highly uncertain. For now, let’s put aside the forecasts and look instead to the macroeconomic conditions we think we need to see to bring inflation down to 2 percent over time.

For starters, we need to raise interest rates to a level that is sufficiently restrictive to return inflation to 2 percent. There is considerable uncertainty about what rate will be sufficient, although there is no doubt that we have made substantial progress, raising our target range for the federal funds rate by 3.75 percentage points since March. As our last postmeeting statement indicates, we anticipate that ongoing increases will be appropriate. It seems to me likely that the ultimate level of rates will need to be somewhat higher than thought at the time of the September meeting and Summary of Economic Projections. I will return to policy at the end of my comments, but for now, I will simply say that we have more ground to cover.

We are tightening the stance of policy in order to slow growth in aggregate demand. Slowing demand growth should allow supply to catch up with demand and restore the balance that will yield stable prices over time. Restoring that balance is likely to require a sustained period of below-trend growth.

Last year, the ongoing reopening of the economy boosted real gross domestic product (GDP) growth to a very strong 5.7 percent. This year, GDP was roughly flat through the first three quarters, and indicators point to modest growth this quarter, which seems likely to bring the year in with very modest growth overall. Several factors contributed to this slowing growth, including the waning effects of reopening and of pandemic fiscal support, the global implications of Russia’s war against Ukraine, and our policy actions, which tightened financial conditions and are affecting economic activity, particularly in interest-sensitive sectors such as housing. We can say that demand growth has slowed, and we expect that this growth will need to remain at a slower pace for a sustained period.

Despite the tighter policy and slower growth over the past year, we have not seen clear progress on slowing inflation. To assess what it will take to get inflation down, it is useful to break core inflation into three component categories: core goods inflation, housing services inflation, and inflation in core services other than housing (figure 2).

Core goods inflation has moved down from very high levels over the course of 2022, while housing services inflation has risen rapidly. Inflation in core services ex housing has fluctuated but shown no clear trend. I will discuss each of these items in turn.

Early in the pandemic, goods prices began rising rapidly, as abnormally strong demand was met by pandemic-hampered supply. Reports from businesses and many indicators suggest that supply chain issues are now easing. Both fuel and nonfuel import prices have fallen in recent months, and indicators of prices paid by manufacturers have moved down. While 12-month core goods inflation remains elevated at 4.6 percent, it has fallen nearly 3 percentage points from earlier in the year. It is far too early to declare goods inflation vanquished, but if current trends continue, goods prices should begin to exert downward pressure on overall inflation in coming months.

Housing services inflation measures the rise in the price of all rents and the rise in the rental-equivalent cost of owner-occupied housing. Unlike goods inflation, housing services inflation has continued to rise and now stands at 7.1 percent over the past 12 months. Housing inflation tends to lag other prices around inflation turning points, however, because of the slow rate at which the stock of rental leases turns over.2 The market rate on new leases is a timelier indicator of where overall housing inflation will go over the next year or so. Measures of 12-month inflation in new leases rose to nearly 20 percent during the pandemic but have been falling sharply since about midyear (figure 3).

As figure 3 shows, however, overall housing services inflation has continued to rise as existing leases turn over and jump in price to catch up with the higher level of rents for new leases. This is likely to continue well into next year. But as long as new lease inflation keeps falling, we would expect housing services inflation to begin falling sometime next year. Indeed, a decline in this inflation underlies most forecasts of declining inflation.

Finally, we come to core services other than housing. This spending category covers a wide range of services from health care and education to haircuts and hospitality. This is the largest of our three categories, constituting more than half of the core PCE index. Thus, this may be the most important category for understanding the future evolution of core inflation. Because wages make up the largest cost in delivering these services, the labor market holds the key to understanding inflation in this category.

In the labor market, demand for workers far exceeds the supply of available workers, and nominal wages have been growing at a pace well above what would be consistent with 2 percent inflation over time.3 Thus, another condition we are looking for is the restoration of balance between supply and demand in the labor market.

Signs of elevated labor market tightness emerged suddenly in mid-2021. The unemployment rate at the time was much higher than the 3.5 percent that had prevailed without major signs of tightness before the pandemic. Employment was still millions below its level on the eve of the pandemic. Looking back, we can see that a significant and persistent labor supply shortfall opened up during the pandemic—a shortfall that appears unlikely to fully close anytime soon.

Comparing the current labor force with the Congressional Budget Office’s pre-pandemic forecast of labor force growth reveals a current labor force shortfall of roughly 3-1/2 million people (figure 4, left panel).4 This shortfall reflects both lower-than-expected population growth and a lower labor force participation rate (figure 4, right panel). Participation dropped sharply at the onset of the pandemic because of many factors, including sickness, caregiving, and fear of infection. Many forecasters expected that participation would move back up fairly quickly as the pandemic faded. And for workers in their prime working years, it mostly has. Overall participation, however, remains well below pre-pandemic trends.

Some of the participation gap reflects workers who are still out of the labor force because they are sick with COVID-19 or continue to suffer lingering symptoms from previous COVID infections (“long COVID”).5 But recent research by Fed economists finds that the participation gap is now mostly due to excess retirements—that is, retirements in excess of what would have been expected from population aging alone.6 These excess retirements might now account for more than 2 million of the 3‑1/2 million shortfall in the labor force.7

What explains these excess retirements? Health issues have surely played a role, as COVID has posed a particularly large threat to the lives and health of the elderly.8 In addition, many older workers lost their jobs in the early stages of the pandemic, when layoffs were historically high. The cost of finding new employment may have appeared particularly large for these workers, given pandemic-related disruptions to the work environment and health concerns.9 Also, gains in the stock market and rising house prices in the first two years of the pandemic contributed to an increase in wealth that likely facilitated early retirement for some people.

The data so far do not suggest that excess retirements are likely to unwind because of retirees returning to the labor force. Older workers are still retiring at higher rates, and retirees do not appear to be returning to the labor force in sufficient numbers to meaningfully reduce the total number of excess retirees.10

The second factor contributing to the labor supply shortfall is slower growth in the working-age population. The combination of a plunge in net immigration and a surge in deaths during the pandemic probably accounts for about 1-1/2 million missing workers.11

Policies to support labor supply are not the domain of the Fed: Our tools work principally on demand. Without advocating any particular policy, however, I will say that policies to support labor force participation could, over time, bring benefits to the workers who join the labor force and support overall economic growth. Such policies would take time to implement and have their effects, however. For the near term, a moderation of labor demand growth will be required to restore balance to the labor market.

Currently, the unemployment rate is at 3.7 percent, near 50-year lows, and job openings exceed available workers by about 4 million—that is about 1.7 job openings for every person looking for work (figure 5). So far, we have seen only tentative signs of moderation of labor demand. With slower GDP growth this year, job gains have stepped down from more than 450,000 per month over the first seven months of the year to about 290,000 per month over the past three months. But this job growth remains far in excess of the pace needed to accommodate population growth over time—about 100,000 per month by many estimates. Job openings have fallen by about 1.5 million this year but remain higher than at any time before the pandemic.

Wage growth, too, shows only tentative signs of returning to balance. Some measures of wage growth have ticked down recently (figure 6). But the declines are very modest so far relative to earlier increases and still leave wage growth well above levels consistent with 2 percent inflation over time. To be clear, strong wage growth is a good thing. But for wage growth to be sustainable, it needs to be consistent with 2 percent inflation.

Let’s sum up this review of economic conditions that we think we need to see to bring inflation down to 2 percent. Growth in economic activity has slowed to well below its longer-run trend, and this needs to be sustained. Bottlenecks in goods production are easing and goods price inflation appears to be easing as well, and this, too, must continue. Housing services inflation will probably keep rising well into next year, but if inflation on new leases continues to fall, we will likely see housing services inflation begin to fall later next year. Finally, the labor market, which is especially important for inflation in core services ex housing, shows only tentative signs of rebalancing, and wage growth remains well above levels that would be consistent with 2 percent inflation over time. Despite some promising developments, we have a long way to go in restoring price stability.

Returning to monetary policy, my FOMC colleagues and I are strongly committed to restoring price stability. After our November meeting, we noted that we anticipated that ongoing rate increases will be appropriate in order to attain a policy stance that is sufficiently restrictive to move inflation down to 2 percent over time.

Monetary policy affects the economy and inflation with uncertain lags, and the full effects of our rapid tightening so far are yet to be felt. Thus, it makes sense to moderate the pace of our rate increases as we approach the level of restraint that will be sufficient to bring inflation down. The time for moderating the pace of rate increases may come as soon as the December meeting. Given our progress in tightening policy, the timing of that moderation is far less significant than the questions of how much further we will need to raise rates to control inflation, and the length of time it will be necessary to hold policy at a restrictive level. It is likely that restoring price stability will require holding policy at a restrictive level for some time. History cautions strongly against prematurely loosening policy. We will stay the course until the job is done.

1. Throughout this discussion, PCE data for October are estimates based on the October consumer price index and producer price index data. Return to text

2. Rental lease data are also the main input into the measurement of owner-occupied housing prices. Return to text

3. The pace of wage inflation affects all sectors of the economy, but wages are a particularly large share of costs in core services ex housing and, thus, particularly important for inflation in this category. Return to text

4. See Congressional Budget Office (2020). To account for the effect of population controls on the level of the labor force, the shortfall is calculated by appending the Congressional Budget Office’s January 2020 projected labor force growth over the years 2020–22 onto the level of the labor force in 2019:Q4 that is adjusted for population controls. Return to text

5. Recent research suggests that long COVID may be keeping 280,000 to 680,000 individuals aged 16 to 64 out of the labor force (Sheiner and Salwati, 2022), and long COVID may explain why the percentage of those aged 18 to 64 not in the labor force due to a disability has stalled over the past two years rather than continuing its pre-pandemic decline (see also Price, 2022). Return to text

6. See Montes, Smith, and Dajon (2022). Return to text

7. This analysis adjusts for population controls to the Current Population Survey. This adjustment is important, because while the unadjusted data show a marked decline in the retired share in January 2022, this drop is entirely an artifact of new population controls introduced in January. A proper assessment of the effects of retirements since the start of the pandemic needs to adjust the historical data for the effects of these population controls. See Montes, Smith, and Dajon (2022). Return to text

8. For example, see Goda and Soltas (2022). Return to text

9. Displaced workers aged 65 and over had markedly lower reemployment rates and markedly higher rates of labor force exit than did similarly aged displaced workers in the years just before the pandemic. See Bureau of Labor Statistics (2022). Return to text

10. Among those 55 and over, transitions into retirement are currently well above the average rate in the three years before the pandemic (after adjusting for population controls). At the same time, retirees are returning to the labor force at a rate similar to that before the pandemic. Return to text

11. First, due primarily to COVID, mortality over the past few years has far exceeded what had been expected before the pandemic. This channel accounts for about 400,000 of the labor force shortfall. Total deaths due to COVID are much larger—about 1 million people. However, the effect on the labor force is smaller than this because COVID deaths have mostly been among older people, who participate in the labor force at lower rates than younger people.

Second, due, at least in part, to pandemic-related restrictions on entry into the United States, total immigration has slowed substantially since the start of the pandemic, lowering the labor force by about 1 million people relative to pre-pandemic trends. While lawful, nonpermanent immigration (for example, H-1B and H-2B visa holders) has bounced back considerably since earlier in the pandemic, these categories of immigration are generally still below 2019 levels. Meanwhile, lawful permanent immigration (that is, new green card holders) is also somewhat lower than in 2019 and well below levels that prevailed earlier in the 2010s. Regarding undocumented immigration, while migrant encounters at the U.S.–Mexico border have been high lately, some estimates suggest the number of undocumented immigrants in the United States is not much different than in 2019. (For data on legal immigration, see U.S. Department of Homeland Security, 2022; for data on border encounters, see U.S. Customs and Border Protection, 2022; for estimates of the number of undocumented immigrants, see Camarota and Zeigler, 2022.). Return to text

* * *

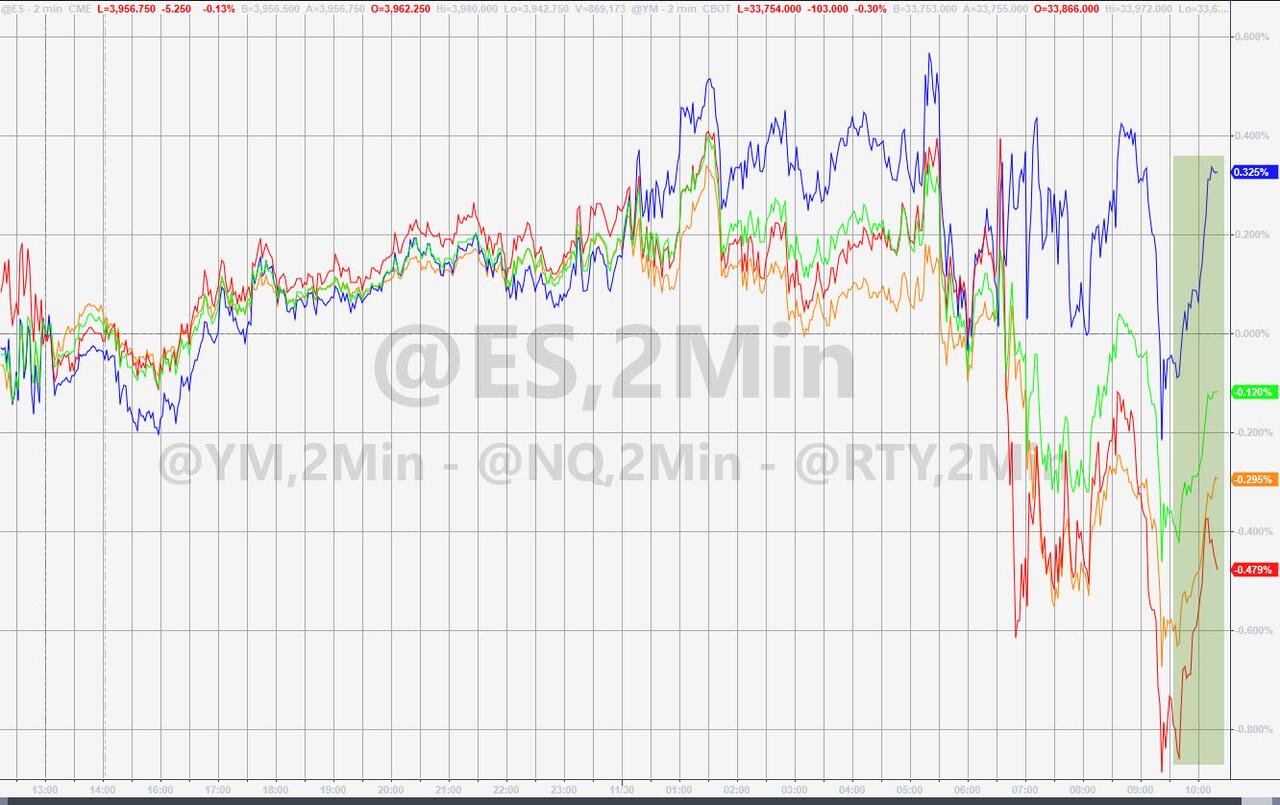

When we previewed Jay Powell’s speech yesterday, we explained both why the market has been so nervous heading into (PTSD from his Jackson Hole market mauling) as well as why the blackout period that follows Powell’s speech and lasts through the middle of December will be far more important for the market over the next two weeks.

Looking at today’s jitteryness, the market is clearly still on edge, so below we share two Powell previews as of this morning, one from Goldman bankers, the other from JPMorgan.

We start with JPMorgan trader Andrew Tyler who has a neutral view of what to expect from the Fed chair today:

While Equities saw a lift on Weds following Fed Minutes, this week have multiple Fed speakers, none more important that Powell’s speech Weds at 1.30pm. Should the market be bracing for a repeat of Jackson Hole? When Powell gave his Jackson Hole speech Fed Funds were 2.25% – 2.50% and now they are 3.75% – 4.00%; but financial conditions have loosened considerably following the tightening that we experienced in Sept and Oct, though the financial conditions index is tighter (higher) now than in August. While mortgage rates have come off their highs, the 6.78% rate compares to 5.89% during Jackson Hole.

Given that background, it is unclear what more Powell could say that we have not heard from recent Fed speakers:

(i) terminal rate 4.75% – 5.25% seems to be an acceptable place to pause;

(ii) once at that ~5% level, data will determine the next moves. Currently, the market is pricing in a 5% terminal rate, and it feels unlikely that the bond market would have a material repricing ahead of Friday’s NFP, the Dec 12 CPI print, and Dec 13 Fed announcement. For reference, the Monday of Powell’s Jackson Hole speech, the terminal rate expectation was 3.74% and the Monday following, the terminal rate moved to 3.84%; and the 10Y yield moved from 3.01% to 3.10% over the same period. The SPX fell 3.4% the day of the speech, NDX was -4.1%, RTY was -3.3%. The market feels less offsides now with a higher-for-longer view becoming consensus, so moves of that magnitude do not appear to be very likely.

Our tactical view is that Equity market moves are likely lower from here given the number of clients who want to sell stock around the 4,000 level in the SPX; many clients feel the 3700 – 3900 range is appropriate absent a material change in the data (e.g., NFP under 100k or CPI falls another 50bps, or more). While a Fed pivot is currently off the table, investors looking for a pause are unlikely to find that support from Powell this week.

So while JPM notes that its clients are generally bearish, there is nothing in what Powell will say that could precipitate a selloff. Not surprisingly, Goldman agrees, and as Goldman’s Michael Nocerino notes the market has “somewhat de-risked heading into the event after Fed Speakers this week dropped the hawkish tone on the market”

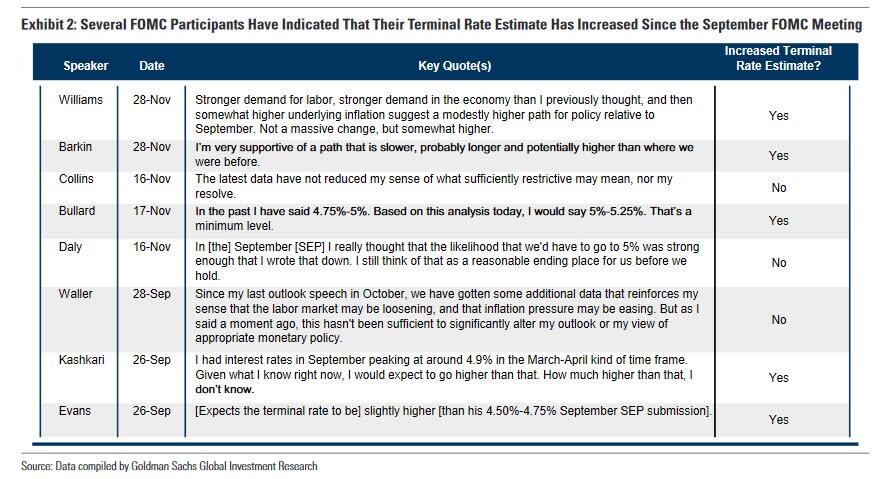

James Bullard said markets are underestimating the chances that the FOMC will need to be more aggressive next year, adding tightening may go into 2024;

John Williams said “there’s still more work to do” to get inflation down;

Loretta Mester told the FT that the central bank isn’t near a pause.

Here is some additional color from Goldman trader Mike Cahill, who says that Powell’s speech is important for two reasons. :

First, the focus on the labor market is critical for assessing the how Powell views the Committee’s task ahead. Does he think it is likely the Fed can cool the labor market without a significant rise in the unemployment rate? And why did the September projections show such a sharp fall in inflation with only a modest rise in unemployment?

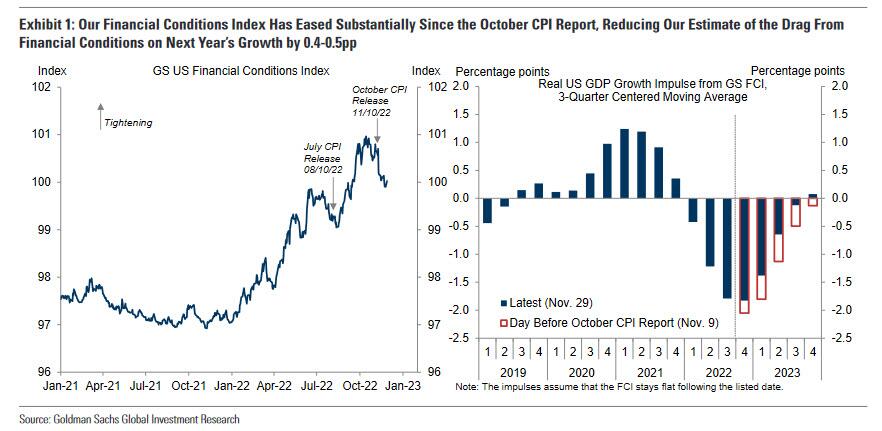

Second, this is a chance for Powell to comment on the substantial easing in financial conditions since the CPI print. Lower inflation is a better fundamental reason for the market to price less tightening, but our FCI has unwound half the tightening since Powell’s JH speech and is now essentially flat since June. Is he ok with this? Vast majority of FCI tightening has been pre June versus 80% of rate hikes. But we think FCI is how policy translates to the economy (the change and not the level). The easing in FCI now means that the FCI drag to growth peaks this quarter and is now roughly flat as of middle of the year – see 2nd chart below. Overall we think that FC will need to act as a restraint to the economy throughout 2023 to achieve a soft landing.

Finally, here is an extended preview excepted from Jan Hatzius at Goldman’s research desk (full note available to pro subscribers in the usual place).

At 1:30pm ET today, Chair Powell will deliver prepared remarks on “then economic outlook, inflation, and the labor market.” Since the October CPI print, our financial conditions index (FCI) has eased substantially, which has reduced our estimate of the drag from financial conditions on next year’s growth by 0.4-0.5pp.

The key question for markets is therefore to what degree he will try to push back against the recent FCI easing by striking a hawkish tone.

Powell is likely to hint that the FOMC will slow the pace of rate hikes at then December meeting but push back against the recent easing in financial conditions with two hawkish counterpoints.

First, Powell is likely to suggest that the FOMC will need to raise the funds rate to a higher peak than it projected at the September meeting, echoing his remarks at the November press conference and following similar comments from several other FOMC members over the last few weeks.

Second, he is likely to reiterate that inflation remains too high and the labor market remains extremely tight. At the November press conference, he acknowledged that job growth had slowed and that job openings had started to decline, but stressed that the labor market remained “out of balance” and noted that the participation rate had been “little changed since the beginning of the year.” That said, the fact that financial conditions are meaningfully tighter today than when he pushed back against easing financial conditions in his Jackson Hole speech should reduce the impetus for an overly hawkish message in today’s speech

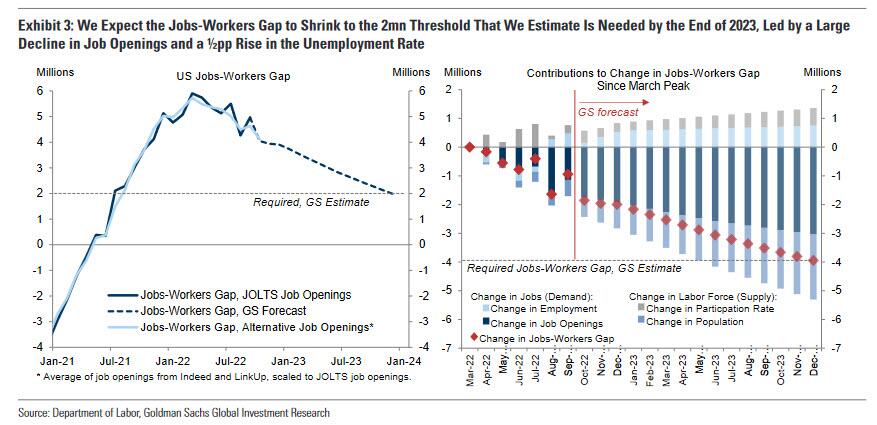

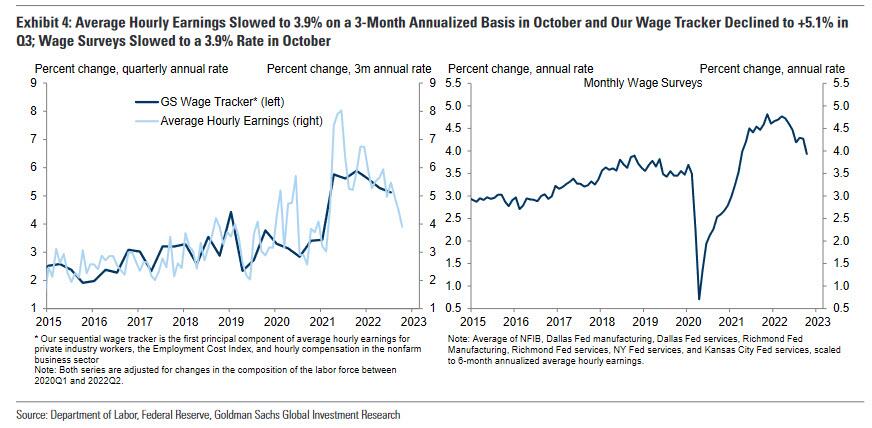

While Powell will likely try to avoid a further counterproductive easing in financial conditions by signaling that the FOMC will keep hiking well into 2023, recent data have shown encouraging signs that labor-market rebalancing is underway, and the reasons to expect lower future inflation have continued to strengthen. Our jobs-workers gap has closed 45% of the distance between its March peak and the level we think is necessary to restore balance to the labor market, recent indicators of wage growth have softened on net, and alternative web-based measures of rent growth for new tenants have decelerated substantially.

The recent news on inflation has also been encouraging. Core CPI inflation slowed in October and we expect core PCE inflation to decelerate to 0.25% (m/m) in Thursday’s release (vs. 0.45% in September). In addition, the reasons to expect lower future inflation have strengthened further.

First, leading indicators of core goods prices — especially the supplier deliveries and prices paid components of the ISM as well as used car auction prices—have declined sharply. Second, asking rents on new leases slowed further in October, and data from Apartment List indicate that asking rents declined 0.2% in November. While Powell endorsed the official CPI/PCE rental components as the best measures of housing inflation for monetary policy purposes, he did note that the committee is “considering that we also know that at some point you’ll see rents coming down” because of the signal from the alternative measures.

We continue to expect the FOMC to slow the pace of rate hikes to 50bp inn December and to 25bp in February, March, and May, raising the funds rate to a peak of 5-5.25%.

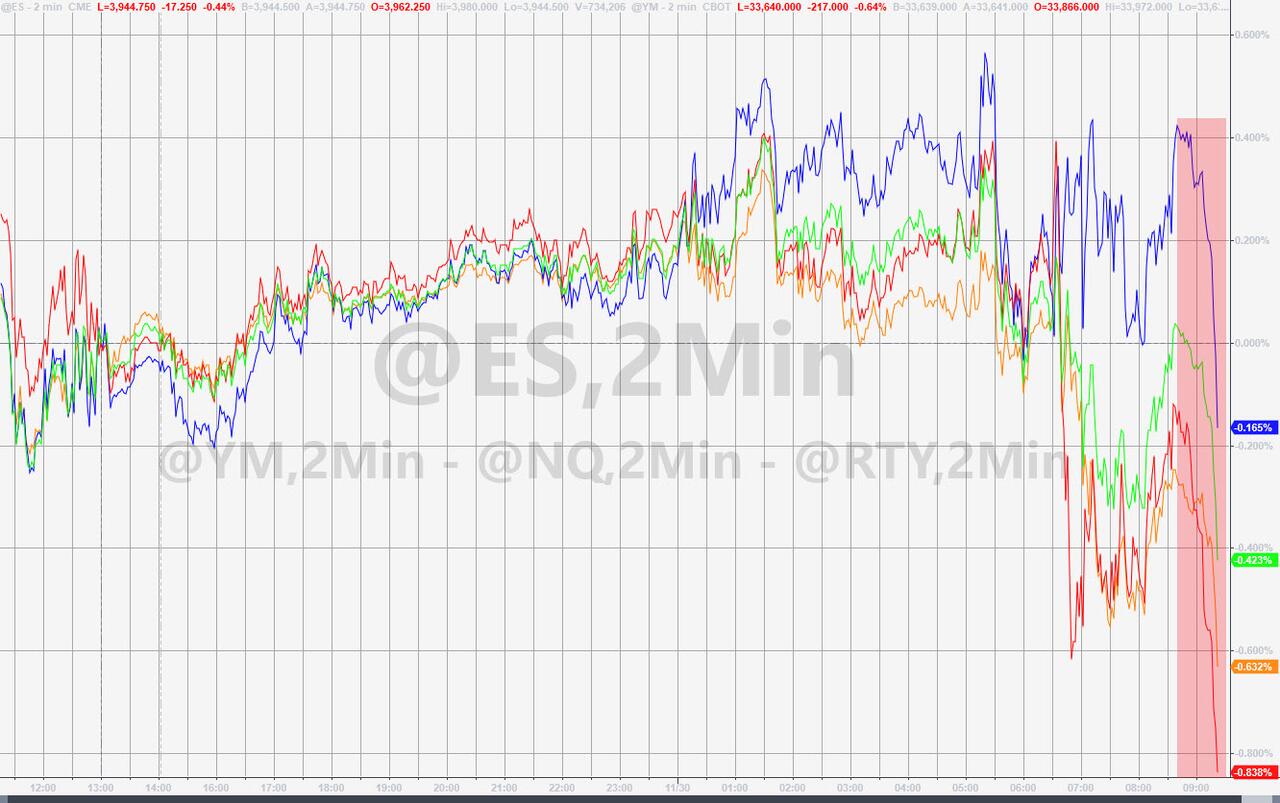

Democrat-Run House Votes To Push Labor Deal Down Railroad Unions’ Throats

Update (1315ET): As expected, Democrats have ‘crossed a line’ and voted to remove labor unions’ leverage by approving a bill to force them to accept the railroad labor deal.

Pelosi said in a letter to her colleagues last night that Democrats have stood with “hard-working railroaders in their fight against greedy railroad corporations for fairer wages, benefits and working conditions,” she said in the letter.

“However, we must act to prevent a catastrophic strike that would touch the lives of nearly every family: erasing hundreds of thousands of jobs, including union jobs; keeping food and medicine off the shelves; and stopping small businesses from getting their goods to market.”

House lawmakers voted 290 to 137 on legislation that would force the adoption of a tentative labor agreement by rail workers, using the power of a 1926 law that allows Congress to intervene in railroad disputes that threaten to disrupt the U.S. economy.

US equities have rebounded on the news…

Any legislation that passes the House will have to be approved by the Senate as well. Sen. Bernie Sanders (I., Vt.) proposed a similar sick-leave measure.

As we detailed yesterday, union leaders have already expressed their ire at the intervention.

Michael Paul Lindsey, a locomotive engineer in Idaho and steering committee member for Railroad Workers United, told Insider it was a “blatant betrayal,” but he wasn’t surprised.

“I thought it was kind of laughable that anyone would think that either the Democrats or the Republicans actually cared. Bottom line, they care about money,” he said.

Even so, “there was always that hope in the back of my mind that maybe someone would do something that was actually right for the American worker for once — instead of just what’s right for corporate America.”

Republicans have traditionally philosophically-opposed government intervention into private contractual obligations, and Senator Marco Rubio has vociferously defended the workers’ rights:

“Just because Congress has the authority to impose a heavy-handed solution does not mean we should,” he said.

“It is wrong for the Biden administration, which has failed to fight for workers, to ask Congress to impose a deal the workers themselves have rejected.”

House lawmakers are also expected to vote on a second bill that would increase paid sick leave to seven days.

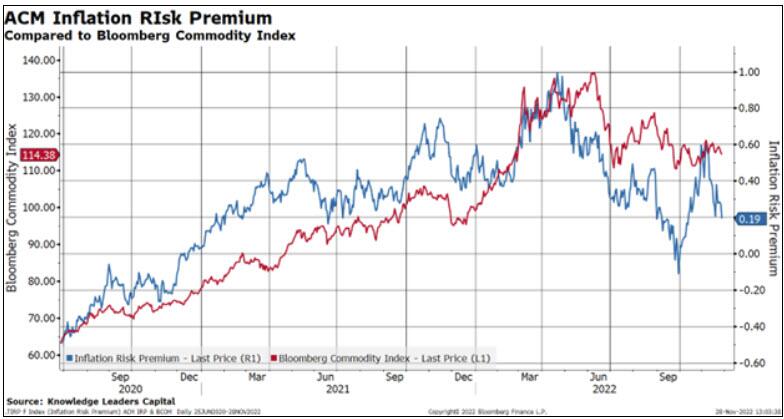

There are many ways to decompose the bond market to identify the component pieces to infer what the market is pricing in.

The nominal long US Treasury bond is a function of two things:

1) the average expected future nominal short-term interest rate, and

2) the term premium.

The term premium can then be decomposed into two parts:

1) the inflation risk premium, and

2) the real risk premium.

With a little bit of algebra, bringing in some other independent variable like the inflation swap, breakeven inflation and TIPS yield, we can calculate the inflation risk premium.

The inflation risk premium tends to move in step with commodity prices whereas the real risk premium tends to move more in step with Federal Reserve policies and expectations.

What’s catching our attention is the recent plunge in the inflation risk premium and what it may mean for commodity prices.

After peaking soon after Russia’s invasion of Ukraine, the inflation risk premium signaled the peak in the Bloomberg Commodity Index in June.

Recently, since the first week of November, the inflation risk premium has dropped from 60bps to 19bps. This has coincided with mostly sideways action in the commodity index so far. But we think it does signal downside risk to commodities in the near future.

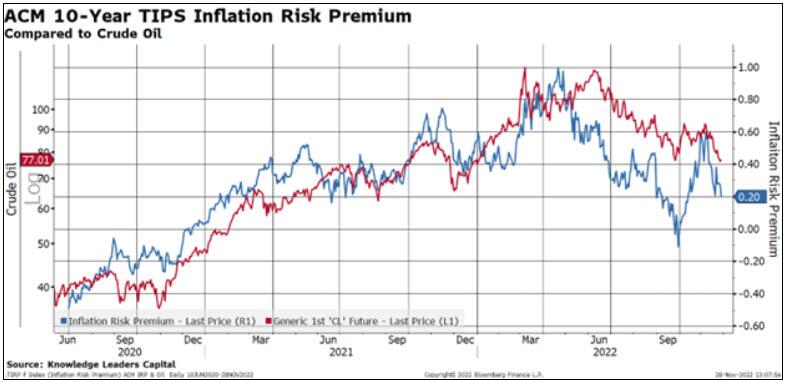

Oil is a component of the Bloomberg Commodity index, probably the most important one. It spiked on news of the Russian invasion of Ukraine but the inflation risk premium had been rising all February signaling higher oil prices ahead. Then the inflation risk premium peaked in late April, which preceded the double top in oil in June.

The signal to us from the US bond market is that oil prices may be set to fall further. The last time the inflation risk premium was around 20bps, oil prices were $64-$70/barrel.

Twitter owner Elon Musk on Wednesday confirmed what everyone with two functioning brain cells and intellectual honesty already knew; the social media giant has “interfered in elections.”

In a discussion over a Reuters article in which the company’s former head of trust and safety says Twitter is ‘not safer’ under Musk, user @EvaFoxU posted: “Twitter has shown itself to be not safe for the past 10 years and has lost users’ trust. The past team of “trust and safety” is a disgrace, so it doesn’t have any right to judge what is being done now,” adding “They had a chance, but they sold their souls to a corporation.”

To which Musk replied, “Exactly. The obvious reality, as long-time users know, is that Twitter has failed in trust & safety for a very long time and has interfered in elections.”

Musk then said that “Twitter 2.0 will be far more effective, transparent and even-handed.”

Twitter has shown itself to be not safe for the past 10 years and has lost users’ trust. The past team of “trust and safety” is a disgrace, so it doesn’t have any right to judge what is being done now. They had a chance, but they sold their souls to a corporation.

Exactly. The obvious reality, as long-time users know, is that Twitter has failed in trust & safety for a very long time and has interfered in elections.

Twitter 2.0 will be far more effective, transparent and even-handed.

Musk’s comments come days after he agreed with formerly banned news personality Alex Lorusso that releasing Twitter’s internal discussions about the decision to censor the Hunter Biden laptop story right before the 2020 US election is “necessary to restore public trust.”

As we noted last week, the Post had its Twitter account locked in October 2020 for reporting on the now-confirmed-to-be-real “laptop from hell,” which contains unprosecuted evidence of foreign influence peddling through then-Vice President Joe Biden – including a meeting between Joe and an executive of Ukrainian gas giant Burisma, in 2015.

The laptop contained caches of emails detailing business dealings with Burisma and state-owned CEFC China Energy Co, from which his firms received $4.8 million in wire transfer payments from its founder, Ye Jianming, according to a Senate report. -Daily Caller

Twitter had restricted any user from sharing links of the Post‘s coverage, both publicly or via direct message – while the social media giant also locked out former White House spox Kayleigh McEnany’s personal account, as well as former President Trump’s campaign account, for sharing the link.

In the ensuing years, the authenticity of the laptop has been confirmed by both the Washington Post and the New York Times, while CBS News authenticated the laptop on Monday.

Musk in April spoke out in opposition to Twitter’s decision to temporarily suspend New York Post’s Twitter account.

“Suspending the Twitter account of a major news organization for publishing a truthful story was obviously incredibly inappropriate,” Musk said in April, responding to a post about the Hunter Biden laptop story.

Musk, who took over Twitter in late October, has vowed to make the platform into a politically unbiased bastion of free speech.

He said in an open letter following his acquisition of Twitter that he bought it because “it is important to the future of civilization to have a common digital town square, where a wide range of beliefs can be debated in a healthy manner, without resorting to violence.”

“There is currently great danger that social media will splinter into far right wing and far left wing echo chambers that generate more hate and divide our society,” Musk added.

Indeed:

MEDIA 2022: Hunter Biden’s laptop is real.

MEDIA 2020: RUSSIAN DISINFORMATION! pic.twitter.com/O66PJZNxlN

Amazon CEO Andy Jassy was speaking live during the DealBook Summit and let some uncomfortable truths loose:

Jassy began by noting that they had done a lot of hiring and realized it was time to “streamline costs” adding that it was “clear that consumers are spending but being careful.”

Finally, Jassy warned that the economy is a “lot more uncertain than previously thought.”

These comments weighed on AMZN (and AAPL)…

This sent the broad markets lower…

Not exactly a sign of the soft-landing so many are hoping for.

by Elwin de Groot, Head of Macro Strategy at Rabobank

French president Macron and his wife have arrived in Washington for a two-day state visit to the White House. After a joint press conference with President Biden, dinner will be served on Thursday. We may not be in for the same intense moments that Macron had in his encounters with Biden’s predecessor. Take that famous handshake moment with Trump in May 2017, just after Macron’s election, with which Macron intended to show that he was not somebody to mess with. But the to-and-fros were mutual and over time the relationship between the two remained volatile. During Macron’s state visit in 2018, Trump said: “We have a very special relationship, in fact I’ll get that little piece of dandruff off,” Trump said. “We have to make him perfect — he is perfect.” In reality, they already were miles apart. At a G7 meeting in June 2018, Macron threatened to exclude Trump from participating in a joint declaration with other leaders. The tariff wars, including steel and aluminium tariffs on Europe were also a drag on the relationship. In December 2019, Trump called Macron “very, very nasty” after the French leader criticized the US for withdrawing troops from Syria.

This week’s state visit is seen as a possibility to reset those relations and “orient squarely towards the future”, as White House spokesman John Kirby put it on Monday. Yet, from a geo-political (or should we say, geo-powerful) perspective, the French president is starting from an underdog position. Aside from the painful decision by Australia in September 2021 to engage in a trilateral security pact with the UK and US for the Indo-Pacific region that would help Australia to acquire nuclear-powered submarines from the US rather than French diesel-propelled subs as per the original plan, the biggest sting at the moment is the Inflation Reduction Act (IRA) that was signed into law by President Biden on August 16 and aims to address climate change. France and many of its European partners, however, argue that parts of that Act violate WTO rules. In particular subsidies for electric vehicle purchases are seen as unfair competition as they discriminate against foreign (car) producers. Under the IRA, electric car buyers are eligible for a tax credit of up to $7,500 as long as the vehicle has a battery that is built in North America, with minerals mined or recycled on the continent.

One option for Europe is to engage in a ‘tit-for-tat’ strategy, by launching similar subsidies and regulations for European manufacturers. In a recent interview with French daily Les Echos, Macron said: “I strongly defend a European preference in this area and strong support for the automotive industry. We must stand by this and it must happen as soon as possible […] We must wake up, neither the Americans nor the Chinese will give us such gifts! Europe must prepare a strong response and move very quickly. […] I have been pushing for more European sovereignty for five years. The software of many Europeans is changing,”

Some commentators suggest that by asking President Biden for ‘permission’ to engage in a similar type of subsidies scheme, Europe could re-invigorate its goals of achieving form of ‘(open) strategic autonomy’. Yet, the fact that Macron’s meeting with Biden is being perceived by some as asking for permission, that very much underscores Europe’s current lack of strategic autonomy and the power to pursue it on its own.

Moreover, there are numerous risks attached to such a tit-for-tat strategy. By openly going against WTO rules themselves, the EU would undermine the “open” part of its strategic autonomy strategy. As recently as February 2019 it signed a significant Economic Partnership Agreement with Japan, on which the EU themselves note that it “removes tariffs and other trade barriers and creates a platform to cooperate in order to prevent obstacles to trade; and helps us shape global trade rules in line with our high standards and shared values, and; sends a powerful signal that two of the world’s biggest economies reject protectionism.” Clearly, agreeing with the US to erect trade barriers goes against the grain of such views.

Another question is whether the US would play ball. In fact, why would they? As Europe is puffing under the weight of potential energy shortages and high energy costs, its (energy-intensive) industry already has a significant competitive disadvantage vis-à-vis US producers. Plus, Europe will need significant additional US LNG supplies in the coming years. The US has also provided the majority of military equipment and funding for the Ukraine to fend of Russia; the EU has been playing second fiddle. Even though Biden may not be as inclined as Trump to make French toast of Macron if he doesn’t like his proposals, he does not have many reasons to agree to them

Bombing At Ukrainian Embassy In Madrid Has Diplomats On High Alert

Ukrainian diplomats around the world are on high alert after a small bomb went off at Ukraine’s embassy in Madrid on Wednesday, injuring a diplomatic staff member.

The embassy had received an envelope that exploded when it was either moved or opened, and the package was addressed to Ambassador Serhii Pohoreltsev, a statement released by the Spanish government confirmed.

Ukrainian Foreign Minister Dmytro Kuleba soon after the mail bomb attack which appeared to target the country’s ambassador to Spain said he has “issued an urgent instruction to step up security at all Ukrainian embassies abroad.”

A foreign ministry statement additionally said: “Whoever is behind this explosion they will not succeed in intimidating Ukrainian diplomats or stopping their daily work to strengthen Ukraine and to counter Russian aggression.”

It’s unclear whether Ambassador Serhii Pohoreltsev was at the embassy at the time, or how close in proximity he was to the explosion. Spain’s Foreign Affairs Minister Jose Manuel Albares held a phone call with Amb. Pohoreltsev wherein the latter confirmed the injured person was a Ukrainian worker.

Spanish FM Albares is currently in Romania, where he’s visiting Spanish troops there on a NATO mission. Spain is among Western European countries which have from the beginning been sending consistent defense and foreign aid to Kiev.

The mail bombing is under investigation, and at this point there have been no statements to suggest the police or Spanish government have any leads at this time.

Within hours after the incident, Spanish police have established a stronger security perimeter with vehicles completely surrounding the embassy location in the Hortaleza district of northeastern Madrid.

My trip from Cancún to Puerto Rico on Monday was a smooth journey, which is fortunate given that I was traveling with my extended family in tow, including two babies, plus my wife’s family from Ukraine.

We had managed to get them out of Ukraine several weeks ago and into Mexico, where we had been staying for the past several months.

The fact that both of my children were born in Mexico was extremely helpful to getting my in-laws out of Ukraine; under Mexico’s nationality law, children born in Mexico are automatically Mexican citizens. Plus both parents, as well as both sets of grandparents, are awarded permanent residency.

We were able to process their Mexican residency before they even left Ukraine. And having that foreign residency really helped smooth their train border crossing on their way from Kiev into Poland, before eventually boarding their flight from Warsaw to Cancún.

Once they were in Mexico, we then applied for two-year refugee visas to the US under a program called Uniting for Ukraine.

To give credit where credit is due, the US State Department and Department of Homeland Security made this program remarkably easy.

Uniting for Ukraine requires a US sponsor who commits to providing financial support for eligible Ukrainians who are approved under the program. I’m obviously the sponsor, so I filled out the application on their behalf and enclosed some reasonable documentation — two tax returns and a letter from my accountant — demonstrating my ability to support them financially.

The approval came back within two weeks… which is crazy fast for any government program.

So with visas in hand, my extended family and I were on a plane Monday morning, bound for Puerto Rico (which is a US territory, so all foreigners require a US visa to enter).

And I’m happy to report that everyone is settled in their new home.

Quite comically, though, we weren’t on the ground for even 24 hours before the power went out in my neighborhood.

I’ve written about this before; the power grid in Puerto Rico is tragic farce of corruption and incompetence, and it is about as reliable as a member of Congress.

Despite paying some of the highest electricity prices in the US (~30c per kWh), Puerto Ricans frequently suffer power outages. And when I say ‘frequently’, I mean every few days.

The median age of Puerto Rican power plants is about 45 years, compared to about 18 years on the US mainland; most power plants here on the island are operating far beyond their useful life, which is why they tend to break down all the time, literally leaving people in the dark.

The state-owned electrical company (PREPA) mismanaged the grid for decades, and then took on a total of $9 billion in debt, supposedly to fix the grid. The federal government pumped in billions more.

Now, that money should have been enough to build at least 8,000 MW of electrical production capacity on the island… from scratch. That’s literally twice as much electricity as the island requires.

But instead, PREPA squandered the money. Nobody really quite knows where it all went… but there were a number of bidding scandals and rumors of financial impropriety.

PREPA ultimately declared bankruptcy, and the government then awarded the island’s electricity monopoly to a new company after a secretive bidding process which was not open to the public.

Unsurprisingly, the grid still isn’t fixed… but Puerto Ricans have become accustomed to this inconvenience.

I was in the gym yesterday when the lights went off. Suddenly it was pitch black. But everyone just shrugged it off and kept working out.

It made me marvel at human beings’ capacity to adapt to adverse circumstances, and to eventually normalize them.

Puerto Ricans have completely normalized living without reliable electricity, in the same way that most of the world normalized COVID lockdowns in 2020, and how my in-laws normalized the war while they were still living in Ukraine.

Eventually they just got used to the shelling, the rockets, and the armed gangs roaming the streets.

This ability to adapt quickly is a remarkable attribute of our species, and one that is not terribly common in the animal kingdom.

But it’s also a double-edged sword, because normalization can often come at a high opportunity cost.

In other words, constantly having to normalize conditions which are rapidly deteriorating means that we aren’t putting any energy into improving our circumstances.

This is a classic ‘boiling frog’ mentality; we continually become accustomed to higher and higher temperatures until it’s too late to jump out of the pot.

I know a lot of people have been shocked… and dismayed… at how rapidly their country has deteriorated in a very short period of time.

COVID lockdowns, followed by mostly peaceful protests, followed by woke insanity, followed by some of the most incompetent leadership in history, followed by record-high inflation and a looming energy crisis. . .

Many of us have normalized these trends. In fact we regularly hear that term “new normal” as if we’re all just supposed to accept that this is how it’s going to be from now on.

Well, first of all, that “new normal” view is bullshit. This is not how it’s going to be from now on.

5,000+ years of human history show that incompetence and insanity eventually and always give way to growth and reason. These cycles are just a matter of time.

More importantly, this idea underscores the importance of having a Plan B.

Rather than normalize bad circumstances, it’s much more effective to take back control where you can and ensure that you’ll be able to maintain a position of strength.

For instance, when a government in decline is hellbent on raising taxes so that they can squander more money on disastrous ideas (like paying people to not work!), there’s zero downside in taking completely legal steps to reduce or eliminate your tax bill.

This is a much better approach than simply normalizing a higher tax bill.

Taxes are obviously just one example; there are countless more. The central idea is that you are still in the driver’s seat.

Since Fringe Finance has started, I’ve scoured the Earth far and wide to try and bring a perspective on real estate to the blog that is going to be both no bullshit and an unfiltered on-the-ground opinion that I know and trust (and could add value to my readers).

And to be honest, I didn’t have to scour much, as a good friend of mine is a brilliant up and comer in the world of real estate in Philadelphia. I’ve worked with her several times and have known her for years – she’s insightful, pragmatic, conscientious and has a serious pulse on the industry. I know for a fact that she eats, sleeps and breathes the industry.

As such, my kind friend, award-winning realtor Kira Mason, has agreed to drop in once in a while to offer up her take on the pulse of the industry for benefit of my readers. Kira runs the Substack Gritty City Real Estate, which you can read & follow free here and she is @kmasonrealtor on Twitter.

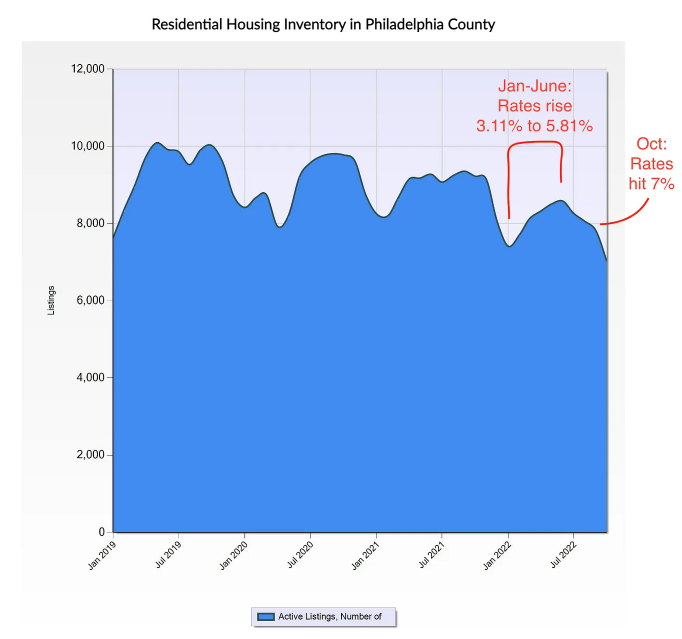

Post-Holiday Inventory Increase Fixed to Add Insult to Injury for the Housing Market

I’m beginning to think that the timing of the interest rate hike this fall has prevented us from experiencing the full effects of deteriorating buyer demand.

Every year, housing inventory gears down for real estate’s dormant period through the holiday season. After the new year begins, inventory then begins its slow hike towards peak in the spring and summer. It was approaching the time when inventory typically begins its final annual descent that rates hit 7% and demand vaporized.

With low inventory the belt keeping the emaciated real estate market’s pants up, I’m nervous about what could happen once more homes hit the market in Q1 and Q2 of 2023.

The inventory decline this year came in two distinct phases. Between January and July, mortgage interest rates rose from 3.11% to 5.81%: a 270 basis point increase representing a roughly 32% increase in one’s monthly mortgage payment.

Market behavior started shifting significantly once rates passed 5.5% in June. By July, inventory began its seasonal downturn…four months early. When rates finally reached and surpassed 7% in October (by which time monthly payments were up a nauseating 47%), inventory began to decline more steeply. Though steeper, inventory declined at more more moderate pace than it usually does at this time of year. This was an effect of reduced demand; despite fewer new listings being added to the market, the dearth of sales caused a relative buildup of older listings.

The perennial reason for the seasonal decline is that few people are interested in house hunting, going through stressful real estate transactions, and moving during the holiday season.

Sellers know that this will affect demand, not to mention the fact that they’ll face the same inconveniences on the buy side, so most choose to hold off on listing their homes until after New Year’s Eve. This holiday season, we can add an additional “inconvenience” to the list: mortgage interest rates at their highest level in 20 years, and affordability at an all time low. With 92% of homeowners enjoying mortgage interest rates under 5%, and 62% with rates under 3.75%, nobody is putting their home on the market unless they absolutely must.

While resale inventory isn’t likely to fully rebound until rates and prices both come down and affordability improves, we will still be seeing inventory start climbing up again in the new year. There’s also a pipeline of specs under construction that, when combined with built-to-order homes, is close to the record highs recorded in 2006. When these hit the market and are combined with whatever little burst of resale listings our homeowners can muster up, we will be experiencing the effects of today’s interest rates in a rising inventory environment for the first time.

Get 50% off: If you enjoy this article, would like to support my work and have the means, I can offer you 50% off for life: Get 50% off forever

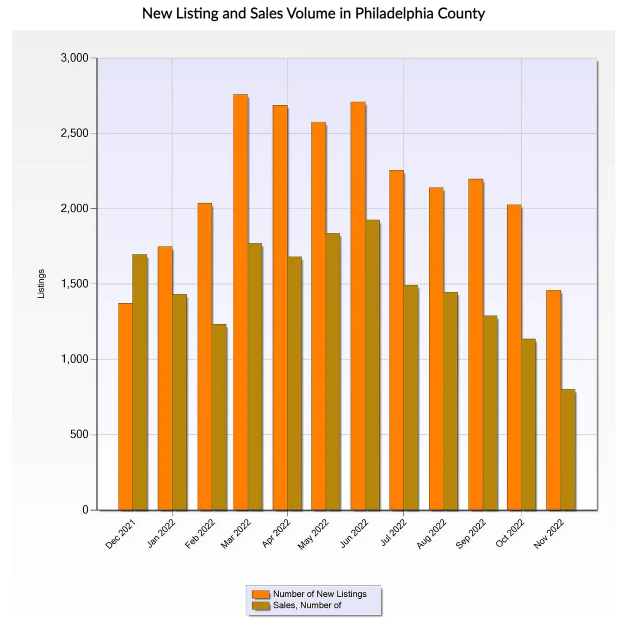

The fact that the market has shifted so dramatically, even in a declining inventory environment, is testament to the 180-degree turn that buyers have taken at the tail end of this year.

And no wonder: with overvalued real estate and record high interest rates, housing affordability is at an all time low. As a result, transaction volume in Philadelphia plummeted 40% from June to October of this year. One might try to attribute this to normal seasonality, but the same period in 2021 saw only a 27% drop.

Just this past summer, buyers were catering to the whims of sellers with waived inspections, above-asking offers, and all the housing boom tricks you’re probably well acquainted with at this point. Bidding wars were still an expected and despised part of the home buying process.

By October, buyer activity had dried up, and sellers were placing reverse offers.

These days, one can hardly show a home to their buyer client without fielding a series of calls from the listing agent offering escalating concessions in a desperate attempt to bring in an offer. The change has been stark and sudden, with housing market analyst Ivy Zelman declaring that the rate of change is “faster than she’s ever seen”.

It’s important to note that not only did 7% rates hit when inventory was on its way down- peak inventory in 2022, which was reached in June, was the lowest annual peak since 2018, with only 8,582 listings. So when inventory fell this year, it was falling from already depressed levels.

If this is the way the market behaves when already low inventory goes into hibernation mode for the holiday season, how will it behave during the uptick we traditionally see after the new year? Even if we don’t get the panic selling that some are anticipating, our normal seasonal inventory increase, paired with new construction entering the market, could be enough to exert additional downwards pressure on prices that are already falling.

About Kira Mason

Kira is a realtor with Berkshire Hathaway Fox & Roach and The Kevin McGillicuddy Team, winner of the 2021 Chairman’s Circle award and ranked within the top 1% of the national Berkshire Hathaway HomeServices network. She independently won Homesnap’s “Fastest Growing Agent” award in 2021 and specializes in the purchase and sale of residential real estate in Philadelphia.

Kira runs the Substack Gritty City Real Estate, which you can read & follow free here and she is @kmasonrealtor on Twitter. She can be reached via e-mail at the address: contact@kiramasonrealtor.com.

QTR’s Disclaimer:I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. This is not a recommendation to buy or sell any stocks or securities or any asset class – just my opinions of me and my guests. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. Positions can change immediately as soon as I publish this, with or without notice. You are on your own. Do not make decisions based on my blog. I exist on the fringe. The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. Also, I just straight up get shit wrong a lot. I mention it three times because it’s that important.