Key Events This Week: Things Finally Quiet Down

After a whirlwind two weeks which saw both the latest FOMC decision and the April jobs report, not to mention the peak of earnings season when all of the top tech companies reported, the calendar takes a quieter turn after the deluge of macro events last week, and the focus shifts on whether markets can continue to find a more solid footing. The latter half of last week saw strong gains for most asset classes thanks to an FOMC meeting that avoided hawkish surprises coupled with a softer payrolls report on Friday that reignited hopes of a soft landing for the US economy. 10yr Treasury yields saw their largest weekly decline of the year so far (-15.5bps) while the S&P 500 posted its best 2-day run in 10 weeks (+2.18%).

Looking forward, the health of the US economic cycle will remain in focus with today’s Senior Loan Officer Survey from the Fed. The SLOOS has seen a gradual improvement in the past few quarters after the sharp tightening following the regional banking stress last March. A key question is whether the rise in yields since the start of the year could derail the nascent improvement in bank credit conditions. Later in the week, the University of Michigan consumer survey will attract attention on Friday given the recent softening in US consumer confidence indicators.

The main macro event in Europe will be the latest BoE decision on Thursday. Our UK economist expects this week’s meeting to set the stage for the first rate cut in June and foresees dovish shifts in the MPC’s modal CPI projections and its forward guidance. You can see the full preview here. We will also have the RBA decision on Tuesday (see our economists’ preview here), while on Wednesday the Riksbank could deliver the first rate cut of the cycle there. Finally, we’ll have the accounts of April ECB meeting due on Friday. These are unlikely to deliver major surprises, with April’s clear if conditional signal of a June rate cut having solidified in recent ECB commentary. But we will watch for any hints on the ECB reaction function beyond June, including on what sort of data might justify consecutive ECB cuts.

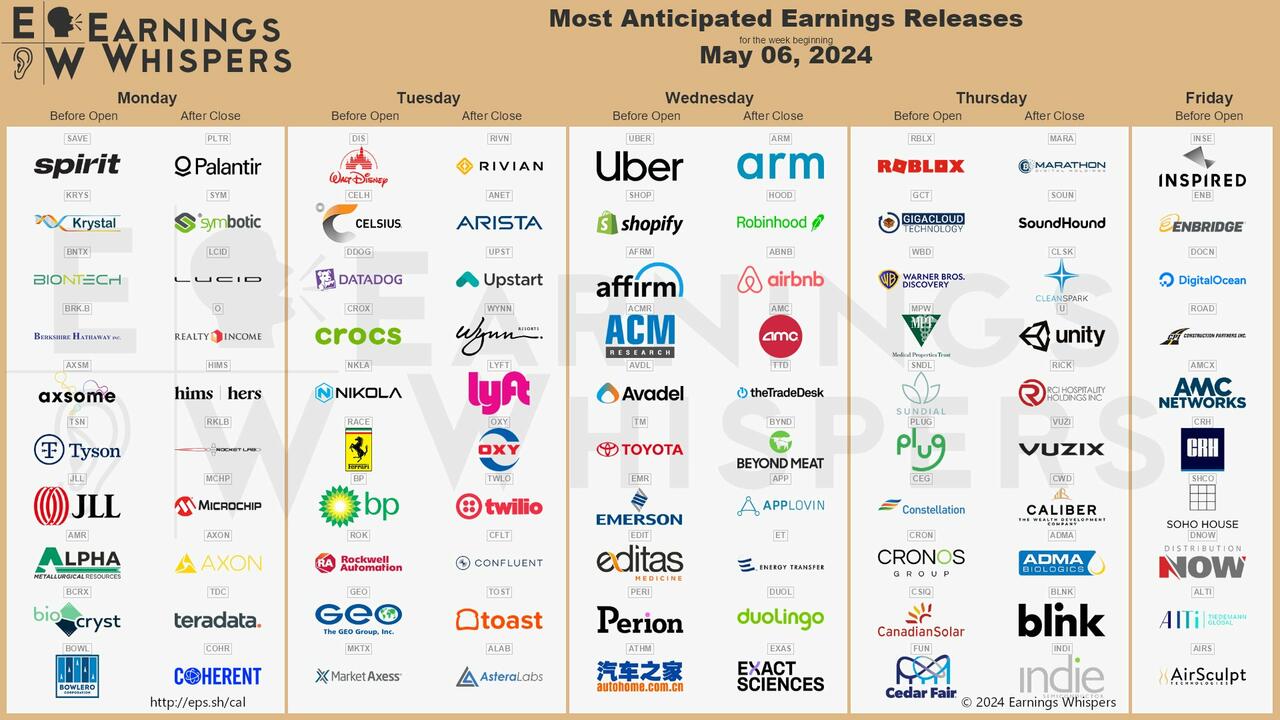

The earnings season will begin to taper off this week, with almost 400 of S&P 500 members having already reported. Notable releases will include Walt Disney, Vertex, Uber and Airbnb in the US, Ferrari, Telefonica and Leonardo in Europe and Toyota and Nintendo in Japan.

Day-by-day calendar of events

Monday May 6

- Data : China April Caixin services PMI, Italy April services PMI, Eurozone March PPI

- Central banks : Fed’s SLOOS, Barkin and Williams speak, ECB’s Villeroy, Nagel and Panetta speak

- Earnings : Vertex, Palantir, Williams Cos, Simon Property Group, Realty Income

Tuesday May 7

- Data : US March consumer credit, UK April construction PMI, new car registrations, China April foreign reserves, Germany March trade balance, factory orders, April construction PMI, France Q1 wages, private sector payrolls, March trade balance, current account balance, Eurozone March retail sales, Switzerland April unemployment rate

- Central banks : Fed’s Kashakari speaks, ECB’s De Cos speaks, RBA decision

- Earnings : Walt Disney, BP, Arista Networks, Duke Energy, McKesson, Occidental Petroleum, Kenvue, Nintendo, Ferrari, Electronic Arts, Rockwell Automation, Leonardo, Reddit, Lyft

- Auctions : US 3-yr Notes ($58bn)

Wednesday May 8

- Data : US March wholesale trade sales, Italy March retail sales, Germany March industrial production

- Central banks : Fed’s Cook, Jefferson and Collins speak, ECB’s Wunsch speaks , Riksbank decision

- Earnings : Toyota, Arm, Uber, Airbnb, Emerson Electric, Teva, Shopify, Vistra, Affirm, Siemens Energy, AB InBev

- Auctions : US 10-yr Notes ($42bn)

Thursday May 9

- Data : US initial jobless claims, UK RICS house price balance, China April trade balance, Japan March leading and coincident index, labor cash earnings

- Central banks : BoE decision, April DMP survey, Pill speaks, BoJ summary of opinions April MPM, ECB’s Cipollone and Guindos speak, BoC’s financial system review

- Earnings : Constellation Energy, Roblox, Telefonica, Enel, Warner Bros Discovery, Warner Music Group

- Auctions : US 30-yr Bonds ($25bn)

Friday May 10

- Data : US May University of Michigan survey, April monthly budget statement, UK Q1 GDP, March monthly GDP, trade balance, industrial production, index of services, construction output, China Q1 current account balance, Japan March trade balance, current account, household spending, April Economy Watchers survey, bank lending, Italy March industrial production, February industrial sales, Canada April jobs report, Norway, Denmark April CPI

- Central banks : Fed’s Goolsbee, Barr and Bowman speak, ECB’s account of the April meeting, Cipollone speaks, BoE’s Pill speaks

- Earnings : Tokyo Electron

* * *

Finally, looking at just the US, Goldman notes that the key economic data release this week are the University of Michigan report on Friday. There are several speaking engagements by Fed officials this week, including remarks from Vice Chair Jefferson, Vice Chair for Supervision Barr, Governors Cook and Bowman, and Presidents Barkin, Williams, Kashkari, Collins, and Goolsbee.

Monday, May 6

- 12:50 PM Richmond Fed President Barkin (FOMC voter) speaks: Richmond Fed President Thomas Barkin will deliver a speech on the economic outlook in Columbia, South Carolina. Audience and media Q&A are expected. On April 10, Barkin said “of course it’s conceivable that we’re going to get to a soft landing, the numbers in a big picture have been great… We need to be humble about how easy it is to get there.”

- 01:00 PM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will participate in a fireside chat conversation at the Milken Institute Global Conference. A Q&A is expected. On April 18, Williams said “I definitely don’t feel urgency to cut interest rates.” He went on to say, “I think interest rates will need to be lower at some point but the timing of that will be based on the economy.”

- 02:00 PM Senior Loan Officer Opinion Survey 2023Q4

Tuesday, May 7

- There are no major economic data releases scheduled.

- 11:30 AM Minneapolis Fed President Kashkari (FOMC non-voter) speaks: Minneapolis Fed President Neel Kashkari will participate in a fireside chat at the Milken Institute Global Conference. A Q&A is expected. On April 4, Kashkari said “in March I jotted down 2 rate cuts this year. But if inflation continues moving sideways, that would make me question whether we need to do those rate cuts at all.”

Wednesday, May 8

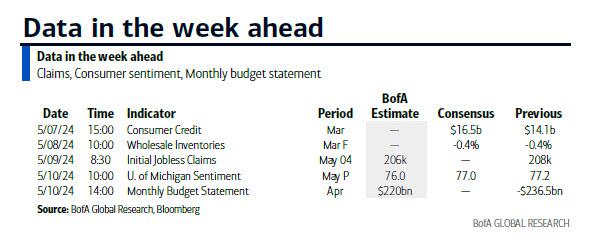

- 10:00 AM Wholesale inventories, March final (consensus -0.4%, last -0.4%)

- 11:00 AM Fed Vice Chair Jefferson speaks: Vice Chair Philip Jefferson will participate in a moderated discussion on careers in economics. On April 16, Jefferson said “my baseline outlook continues to be that inflation will decline further, with the policy rate held steady at its current level, and that the labor market will remain strong, with labor demand and supply continuing to rebalance.” He went on to say that “the outlook is still quite uncertain, and if incoming data suggests that inflation is more persistent than I currently expect it to be, it will be appropriate to hold in place the current restrictive stance of policy for longer.”

- 11:45 AM Boston Fed President Collins (FOMC non-voter) speaks: Boston Fed President Susan Collins will provide remarks to MIT students followed by a fireside discussion. Speech text and a Q&A are expected. On April 11, Collins said “I expect to see further evidence that inflation is durably, if unevenly, returning toward 2 percent, and that the economy is coming into better balance, with demand and supply more closely aligned amid a healthy labor market.”

- 01:30 PM Fed Governor Cook speaks: Fed Governor Lisa Cook will discuss the Fed’s latest semi-annual Financial Stability Report at an event hosted by Brookings. Remarks will be followed by a panel discussion. A Q&A is expected. On March 25, Cook said “the path of disinflation, as expected, has been bumpy and uneven, but a careful approach to further policy adjustments can ensure that inflation will return sustainably to 2% while striving to maintain the strong labor market.”

Thursday, May 9

- 08:30 AM Initial jobless claims, week ended May 4 (GS 215k, consensus 212k, last 208k): Continuing jobless claims, week ended April 27 (consensus 1,785k, last 1,774k)

Friday, May 10

- 09:00 AM Fed Governor Bowman speaks: Fed Governor Michelle Bowman will speak on financial stability risks at the Texas Bankers Association Annual Convention. Speech text and a moderated Q&A are expected. On May 3, Bowman said “with annualized 3-month core PCE inflation jumping to 4.4 percent in March, well above average inflation in the second half of last year, I expect inflation to remain elevated for some time,” but went on to say “my baseline outlook continues to be that inflation will decline further with the policy rate held steady, but I still see a number of upside inflation risks that affect my outlook.”

- 10:00 AM Dallas Fed President Logan (FOMC non-voter) speaks: Dallas Fed President Lorie Logan will speak in a moderated Q&A to the Louisiana Bankers Association Annual Conference in New Orleans. On April 5, Logan said “I’m increasingly concerned about upside risks to the inflation outlook. To be clear, the key risk is not that inflation might rise – though monetary policymakers must always remain on guard against that outcome – but rather that inflation will stall out and fail to follow the forecast path all the way back to 2 percent in the timely way.”

- 10:00 AM University of Michigan consumer sentiment, May preliminary (GS 76.2, consensus 76.8, last 77.2); University of Michigan 5-10-year inflation expectations, May preliminary (GS 3.1%, consensus 3.0%, last 3.0%): We expect the University of Michigan consumer sentiment index decreased to 76.2 in the preliminary May reading. We estimate the report’s measure of long-term inflation expectations rose 0.1pp to 3.1%, reflecting higher gasoline prices and the higher-than-expected price data reported in 2024. The transition to web-based interviews could also exert upward pressure.

- 12:45 PM Chicago Fed President Goolsbee (FOMC non-voter) speaks: Chicago Fed President Austan Goolsbee will speak in a moderated Q&A at the Economic Club of Minnesota luncheon. On April 19, Goolsbee said “so far in 2024, that progress on inflation [we saw in 2023] has stalled. You never want to make too much of any one month’s data, especially inflation, which is a noisy series, but after three months of this, it can’t be dismissed.”

- 01:30 PM Fed Vice Chair for Supervision Barr speaks: Fed Vice Chair for Supervision Michael Barr will give a commencement speech for American University School of Public Affairs Graduation.

Source: DB, Goldman

Tyler Durden

Mon, 05/06/2024 – 10:55

via ZeroHedge News https://ift.tt/6NVg7He Tyler Durden