US PMIs Surprisingly Surge Despite Plummeting ‘Hard Data’, EU PMIs Slump

After this morning’s ugly picture across European PMIs, preliminary June US PMIs were also expected to decline modestly, but remain in expansion (above 50) for both manufacturing and services.

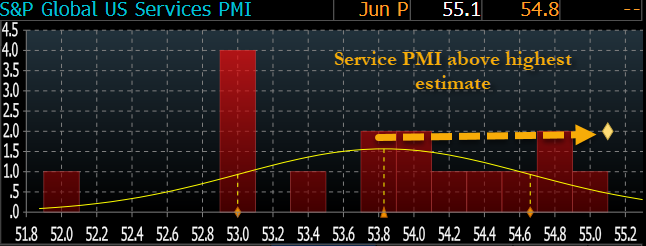

But, in the face of puking US hard macro data, the soft survey data surprised to the upside with Manufacturing at 51.7 (51.3 prior, 51.0 exp) and Services at 26-month highs at 55.1 (54.8 prior, 54.0 exp)…

Source: Bloomberg

The US Services print is above all analysts’ estimates…

Source: Bloomberg

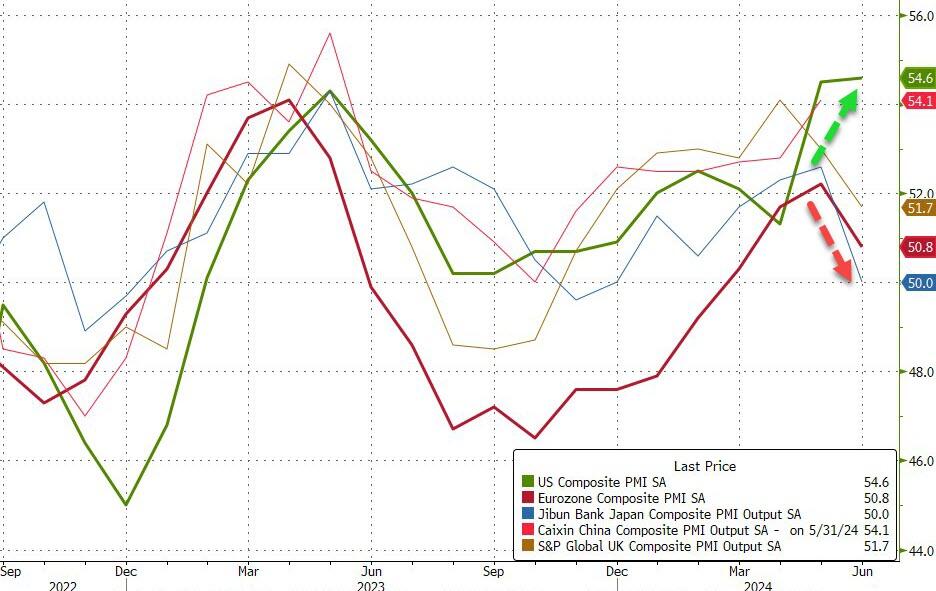

Quite a divergence from the rest of the world…

Source: Bloomberg

Commenting on the data, Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said:

“The early PMI data signal the fastest economic expansion for over two years in June, hinting at an encouragingly robust end to the second quarter while at the same time inflation pressures have cooled.

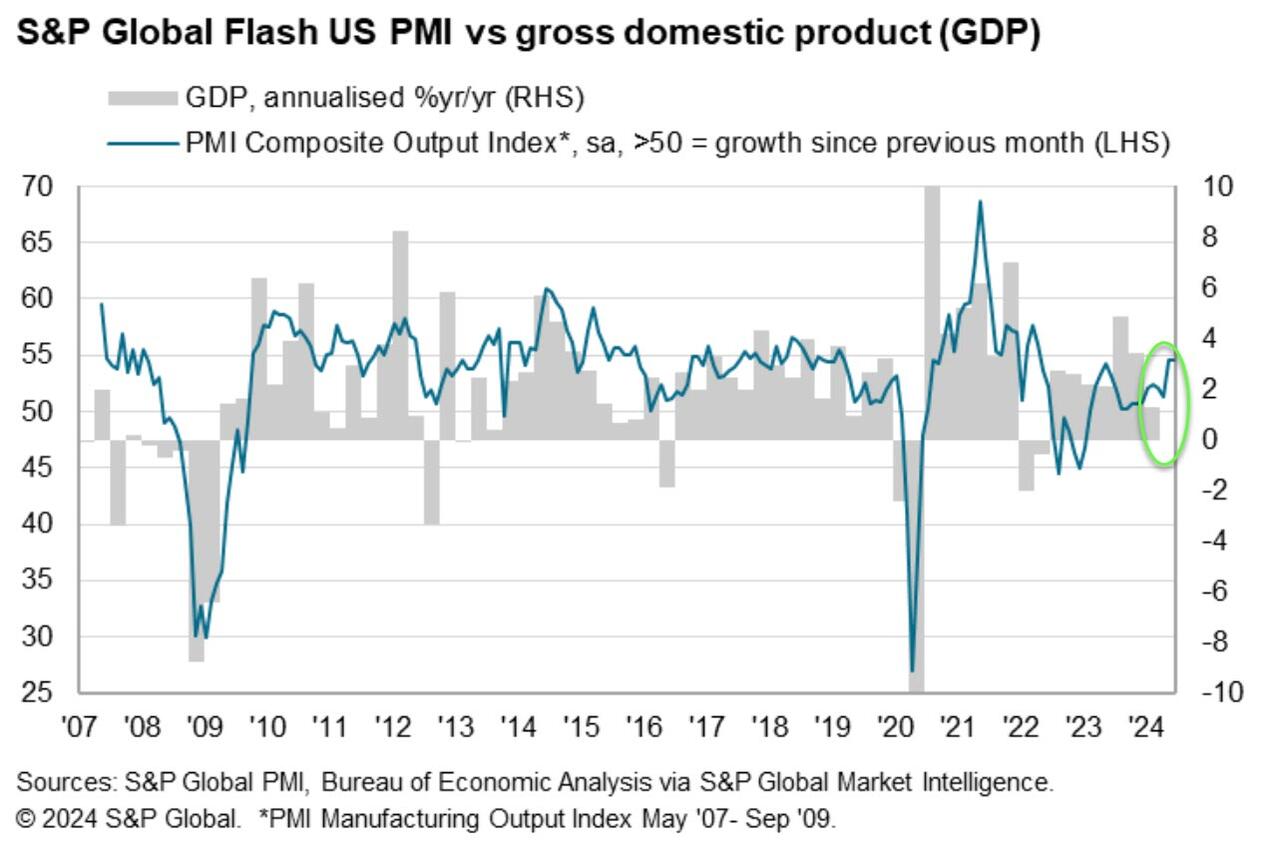

“The PMI is running at a level broadly consistent with the economy growing at an annualized rate of just under 2.5%. The upturn is broad-based, as rising demand continues to filter through the economy. Although led by the service sector, reflecting strong domestic spending, the expansion is being supported by an ongoing recovery in manufacturing, which so far this year is enjoying its best growth spell for two years.

“The survey also brings welcome news in terms of job gains, with a renewed appetite to hire being driven by improved business optimism about the outlook.

“Selling price inflation has meanwhile cooled again after ticking higher in May, down to one of the lowest levels seen over the past four years. Historical comparisons indicate that the latest decline brings the survey’s price gauge into line with the Fed’s 2% inflation target.”

Not exactly a Fed rate-cutting scenario!!

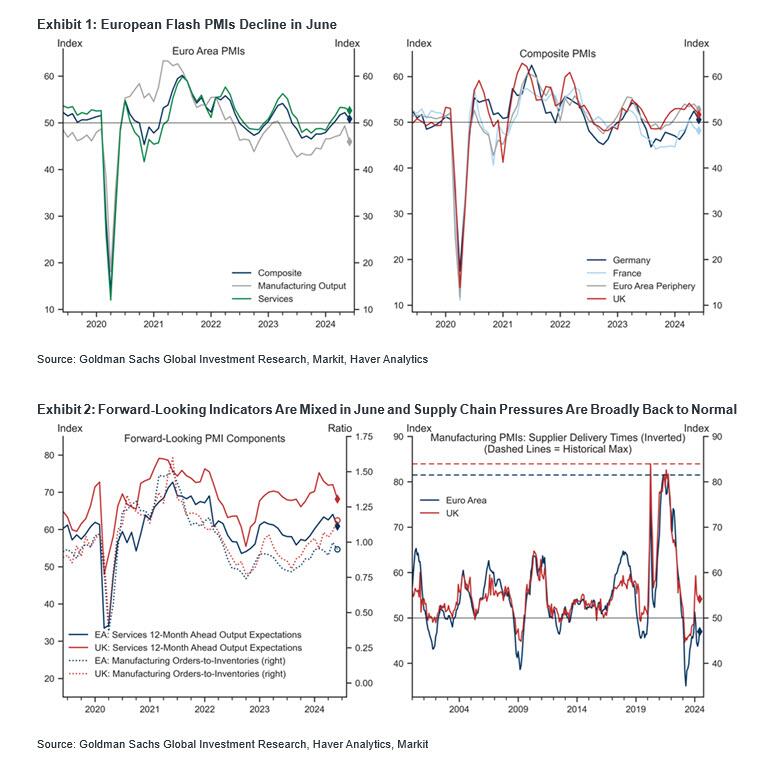

As we detailed earlier, judging by the unexpected freefall and across-the-board miss in Europe’s PMIs this morning, the ECB may have cut rates too little, too late.

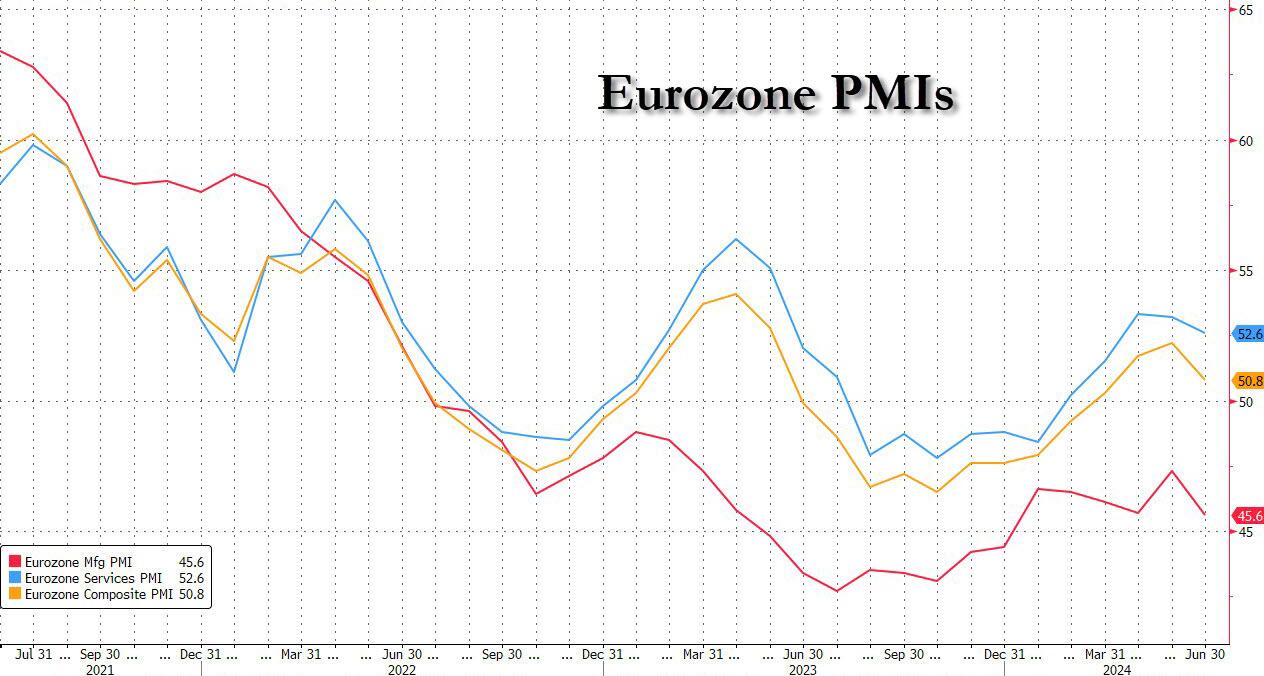

The Euro area composite flash PMI declined by 1.3pt to 50.8, below consensus expectations of 52.5, prompting analysts to comment that “this should be a further reason for the ECB to proceed cautiously with interest rate cuts.”

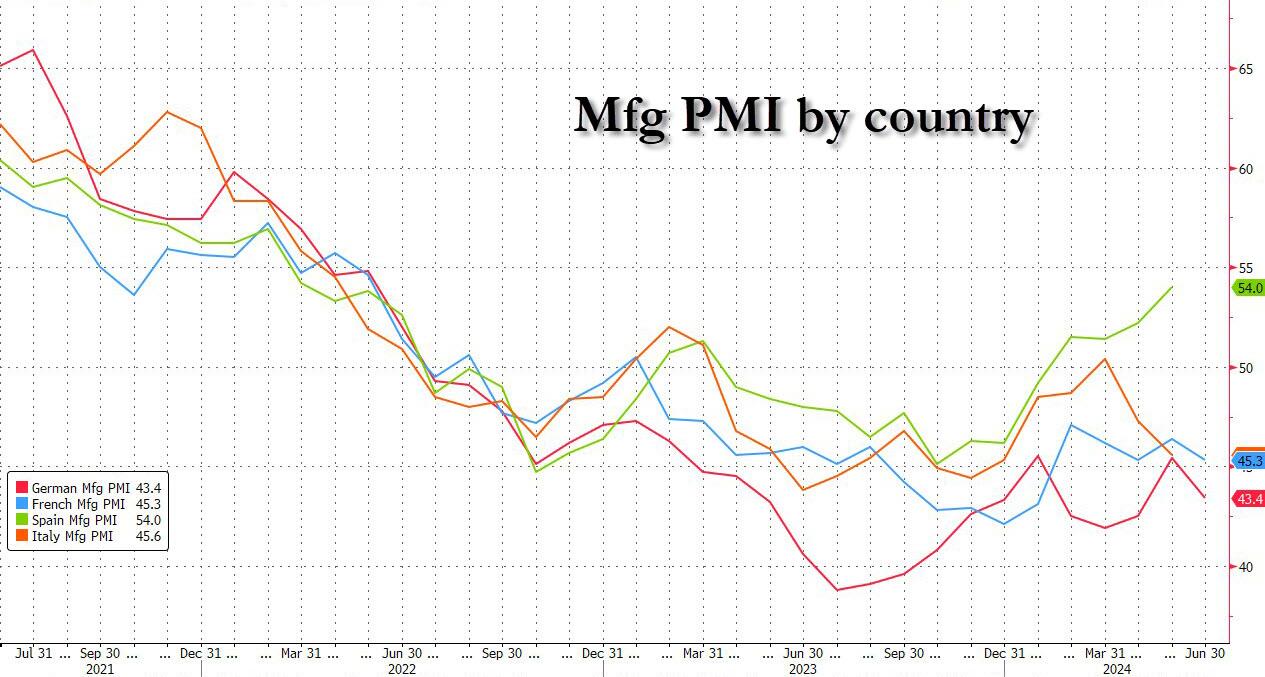

According to Goldman, the deceleration in the composite index was broad-based across sectors, though skewed towards the manufacturing sector, where the output index fell (by 3.4pt) to 46.0. Here is a snapshot of the reports:

-

Euro Area Composite PMI (June, Flash): 50.8, missing consensus 52.5, last 52.2.

-

Euro Area Manufacturing PMI (June, Flash): 45.6, missing consensus 47.9, last 47.3.

-

Euro Area Services PMI (June, Flash): 52.6, missing consensus 53.4, last 53.2.

-

-

France Composite PMI (June, Flash): 48.2, missing consensus 49.4, last 48.9.

-

Germany Composite PMI (June, Flash): 50.6, missing consensus 52.7, last 52.4.

-

UK Composite PMI (June, Flash): 51.7, missing consensus 53.0, last 53.0.

Across countries, the decline in the area-wide index was broad-based.

- France: The French composite flash PMI decreased by 0.7pt to 48.2 in June, notably below consensus and our expectations. The decline was driven by both sectors, with the services index falling (by 0.5pt) to 48.8, and the manufacturing output series dropping (by 1.7pt) to 45.3. The press release state that “the level of incoming new business weighed on activity, [with] some panel members linking lower output volumes to the upcoming election”.

- Services Flash PMI (Jun) 48.8 vs. Exp. 50.0 (Prev. 49.3);

- Manufacturing Flash PMI (Jun) 45.3 vs. Exp. 46.8 (Prev. 46.4)

- Germany: The German composite flash PMI decreased by 1.9pt to 50.6 in June, below consensus and our expectations. The deceleration was broad-based across sectors, though skewed heavily towards the manufacturing sector, where the output index fell (by 4.0pt) to 44.9.

- Services Flash PMI (Jun) 53.5 vs. Exp. 54.4 (Prev. 54.2);

- Manufacturing Flash PMI (Jun) 43.4 vs. Exp. 46.4 (Prev. 45.4).

- Periphery: The periphery composite PMI decreased by 1.2pt to 52.8, driven by a decline across both sectors, skewed notably towards manufacturing, where the output index fell (by 3.4pt) to 47.1.

- In the UK, the composite flash PMI declined to 51.7, below consensus expectations of a flat reading, on the back of a deceleration in services activity, where the index fell by 1.7pt to 51.2, only partly offset by a slight improvement in manufacturing activity.

In its commentary on the results, Goldman said it sees three main takeaways from today’s data.

- First, a loss of momentum in both the Euro area and the UK headline numbers. Despite expanding activity overall, Q2 growth momentum appears to be weaker than at the beginning of the year.

- Second, the drivers of the slowdown appear to be different, with the UK recording strong and expanding manufacturing sector activity, as opposed to the broad-based decline in manufacturing seen across the Euro area.

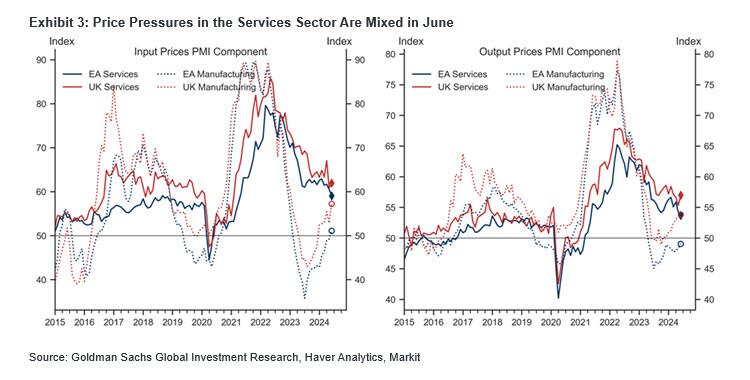

- Third, the PMI price components showed a slight divergence this month, with the Euro area mostly seeing benign price developments, following the ECB cut earlier this month, but UK prices gaining strength, driven in part by stronger demand expectations.

In response to the ugly PMI prints, European bond yields slumped and also dragged down the EUR, while pushing the USD higher. Curiously, despite the virtual assurance of much more QE coming, both gold and crypto also slumped to session lows after the dismal numbers. Expect that to reverse once the selling momentum ignition algos are exhausted.

Tyler Durden

Fri, 06/21/2024 – 09:55

via ZeroHedge News https://ift.tt/AJiF81T Tyler Durden