An impossible job? Kirstjen Nielsen announced Sunday that on April 10, she’ll be stepping down as head of the Department of Homeland Security (DHS). Customs and Border Protection chief Kevin McAleenan will then become acting secretary of DHS.

Nielsen’s resignation comes less than a year and a half after she replaced John Kelly. Kelly went on to become President Donald Trump’s chief of staff, but he left that position in January. “With McAleenan’s appointment, Trump now has an acting homeland security secretary, defense secretary, interior secretary and chief of staff,” notesAxios.

Secretary of Homeland Security Kirstjen Nielsen will be leaving her position, and I would like to thank her for her service….

Nielsen “has arguably been the most aggressive secretary in the department’s short history in cracking down on immigration—with her legacy likely to be defined among progressives by the ‘zero tolerance’ prosecution policy of late spring and early summer 2018 that resulted in the separation of thousands of families at the US-Mexico border,” writes immigration reporter Dara Lind. Alas:

None of it appears to have been enough for Trump.

Nielsen’s resignation was preceded on Thursday night by the abrupt withdrawal of the nomination of acting Immigration and Customs Enforcement director Ron Vitiello to formally lead the agency, with Trump telling reporters Friday morning that he wanted to go in a “tougher direction.” While it’s not yet clear whether Trump requested Nielsen’s resignation or not, it certainly appears as if that “tougher direction” is extending to a new DHS secretary….

[W]ith nearly 100,000 migrants apprehended by Border Patrol agents along the US-Mexico border in March, Trump is yet again ruminating angrily and obsessively over immigration, riffing in speeches about telling migrants “we’re full” and “go back.”

Nielsen couldn’t make that happen, because no one could, because it’s impossible. The US can’t—even with a wall—physically prevent the entry of unauthorized immigrants onto US soil. And once on US soil, they have certain rights—including the right to request asylum.

The one silver lining here seems to be that there’s not much more McAleenan, or any Nielsen replacement, can legally do.

Even during Kelly’s tenure as DHS head, “the low-hanging fruit of deterrent immigration policies had been picked a long time ago,” writes Lind. She continues:

US immigration law is a balance between the desire to minimize unauthorized entry into the United States and the desire to protect vulnerable people who may be fleeing harm and persecution. Both US and international law prohibit the US from refusing entry to people who are in danger of prosecution in their home countries; both US statute and court settlements offer extra due-process protections to asylum seekers, children, and families.

The policies Trump wants, and the outcomes he has promised, aren’t within the power of the White House or the Department of Homeland Security.

As for Acting Secretary McAleenan’s prospects: He’s shown no particular signs of being better or worse than the average border hawk. He has presided over some of the worst immigration actions and abuses of the Trump administration, while refusing to endorse the very worse of Trump’s rhetoric. He’s “not an ideologue or fire breather,” an anonymous DHS officially tells CNN.

Kevin McAleenan is a career border officer. He “looks the part” better than Nielsen. But he’s not the dude who blames Ds for everything or talks of “invasion.” & he—like any other human on earth—can’t physically stop migrants from setting foot on US soil. https://t.co/YMKG55w4Pi

“The safest place in the world to be online.” A new internet regulation proposal backed by U.K. Prime Minister Theresa May would give regulatory bodies there “unprecedented powers to issue fines and other punishments if social-media sites don’t swiftly remove” offending content. British authorities are touting it as a way to ensure the U.K. is “the safest place in the world to be online.” Right now, the proposal “comes in the form of a white paper that eventually will yield new legislation,” reportsThe Washington Post:

Early details shared Sunday proposed that lawmakers set up a new, independent regulator tasked to ensure companies “take responsibility for the safety of their users.” That oversight—either through a new agency or part of an existing one—would be funded by tech companies, potentially through a new tax.

The agency’s mandate would be vast, from policing large social-media platforms such as Facebook to smaller web sites’ forums or comment sections. Much of its work would focus on content that could be harmful to children or pose a risk to national security. But regulators ultimately could play a role in scrutinizing a broader array of online harms, the U.K. said, including content “that may not be illegal but are nonetheless highly damaging to individuals or threaten our way of life in the U.K.” The document offers a litany of potential areas of concern, including hate speech, coercive behavior and underage exposure to illegal content such as dating apps that are meant for people over age 18.

FREE MINDS

Raunch-rhetoric realignment? These are words I never thought I’d type but…an interesting Matthew Yglesias thread:

Here’s a hypothesis I have without much hard data.

There’s been a decades-long debate in the US between Christian conservatives and feminists but also a third force in the debate that rarely articulates a self-conscious ideology — a sort of raunch culture.

“A pregnant mother is facing disorderly conduct charges in Georgia for allowing her 3-year-old son to relieve himself in public,” reports AP.

“When people ask me, how the Trump era is adjusting my political views, my answer is simple: It’s making me more libertarian,” writes David French at National Review. “It’s making me more concerned about the fate of the Constitution. I trust the government less, I’m more appalled at its sweeping assumptions of power, and I see more clearly what happens when its leaders—possessed with unwavering self-righteousness—believe that the ends justify the means.”

In China, a new app called Study the Great Nation pumps out Communist propaganda all day, directly to citizens’ smartphones, and awards them for reading. “Many employers now require workers to submit daily screenshots documenting how many points they have earned,” saysThe New York Times.

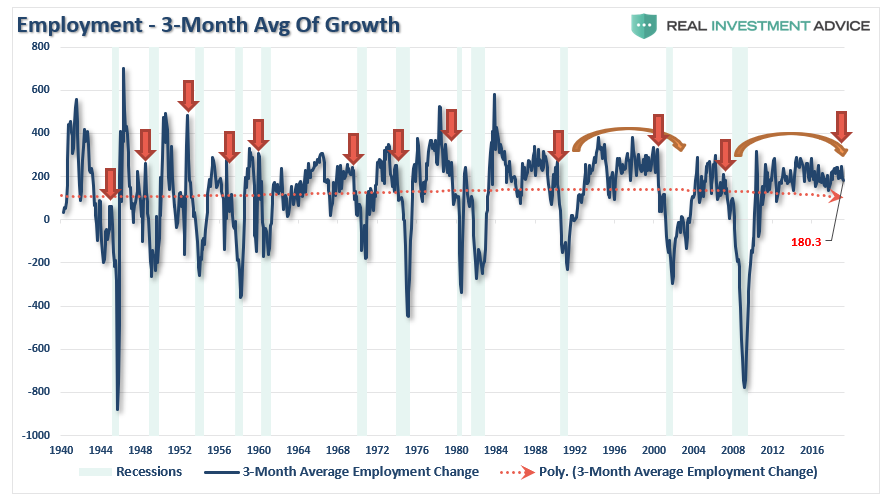

Last week, the Bureau of Labor Statistics (BLS) published the March monthly “employment report” which showed an increase in employment of 196,000 jobs. As Mike Shedlock noted on Friday:

“The change in total non-farm payroll employment for January was revised up from +311,000 to +312,000, and the change for February was revised up from +20,000 to +33,000. With these revisions, employment gains in January and February combined were 14,000 more than previously reported. After revisions, job gains have averaged 180,000 per month over the last 3 months.

Baseline Unemployment Rate: Unchanged at 3.8% – Household Survey

U-6 unemployment: Unchanged at 7.3% – Household Survey

Civilian Non-institutional Population: +145,000

Civilian Labor Force: -224,000 – Household Survey

Not in Labor Force: +369,000 – Household Survey

Participation Rate: -0.2 to 63.0– Household Survey”

There is little argument the streak of employment growth is quite phenomenal and comes amid hopes the economy will continue to avoid a recessionary contraction. When looking at the average rate of employment growth over the last 3-months, as Mike noted at 180,000, there is a clear slowing in the trend of employment. It is this “trend” we will examine more closely today.

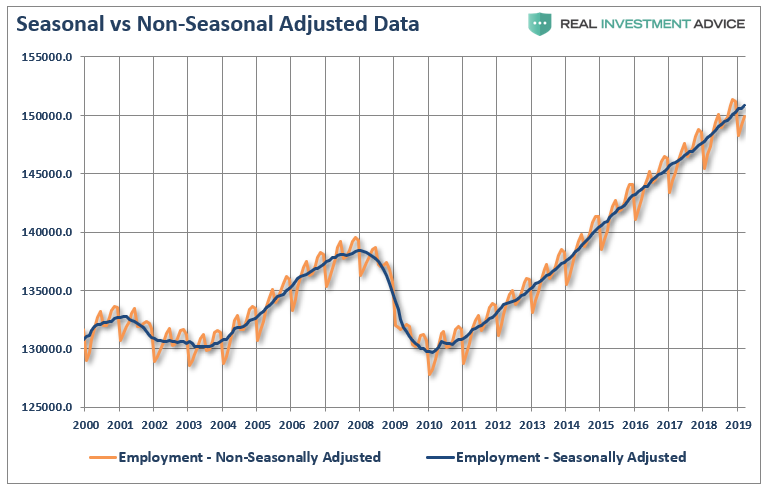

While a tremendous amount of attention is focused on the monthly employment numbers, the series is one of the most highly manipulated, guesstimated, and annually revised series produced by any agency. The whole issue of seasonal adjustments, which try to account for temporary changes to employment due to a variety of impacts, is entirely too systematic to be taken at face value. The chart below shows the swings between the non-seasonally adjusted and seasonally adjusted data – anything this rhythmic should be questioned rather than taken at face value as “fact.”

As stated, while most economists focus at employment data from one month to the next for clues as to the strength of the economy, it is the “trend” of the data which is far more important to understand.

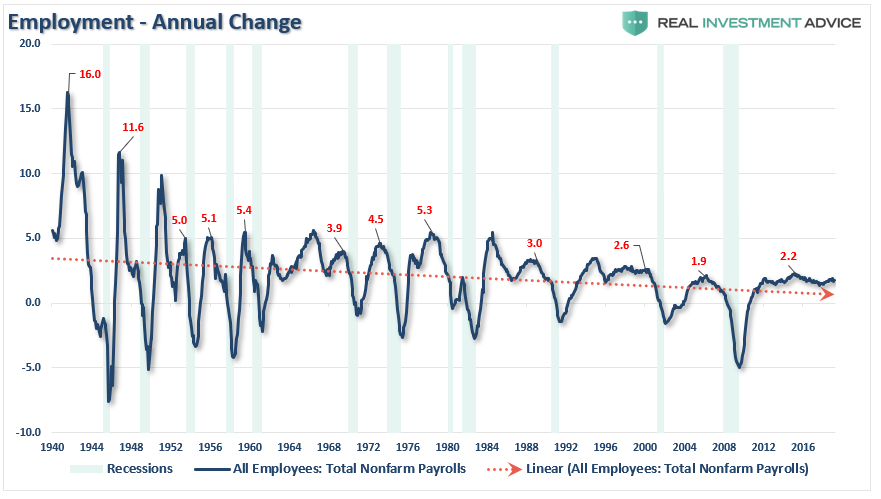

The chart below shows the peak annual rate of change for employment before the onset of a recession. The current annual rate of employment growth is 1.4% which is lower than any previous employment level prior to a recession in history.

But while this is a long-term view of the trend of employment in the U.S., what about right now? The chart below shows employment from 1999 to present.

While the recent employment report was slightly above expectations, the annual rate of growth is slowing. The chart above shows two things. The first is the trend of the household employment survey on an annualized basis. Secondly, while the seasonally-adjusted reported showed 196,000 jobs created, the actual household survey showed a loss of 200,000 jobs.

Many do not like the household survey for a variety of reasons but even if we use the 3-month average of seasonally-adjusted employment we see the same picture. (The 3-month average simply smooths out some of the volatility.)

But here is something else to consider.

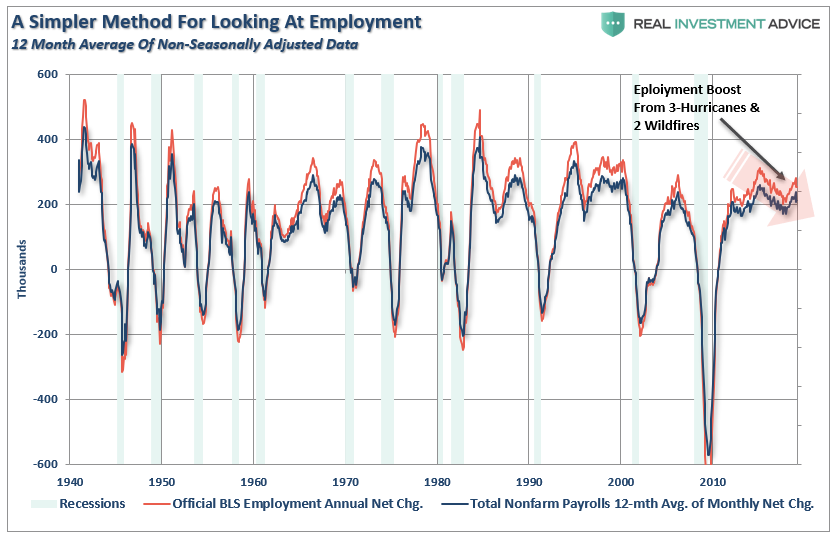

While the BLS continually adjusts and fiddles with the data to mathematically adjust for seasonal variations,the purpose of the entire process is to smooth volatile monthly data into a more normalized trend. The problem, of course, with manipulating data through mathematical adjustments, revisions, and tweaks, is the risk of contamination of bias. A simpler method to use for smoothing volatile monthly data is using a 12-month moving average of the raw data as shown below.

Notice that near peaks of employment cycles the employment data deviates from the 12-month average but tends to reconnect as reality emerges. (Also, note the pickup in employment due to the slate of “natural disasters” in late 2017 which are now fading as reconstruction completes)

Sometimes, “simpler” gives us a better understanding of the data.

Importantly, there is one aspect to all the charts above which remains constant. No matter how you choose to look at the data, peaks in employment growth occur prior to economic contractions rather than an acceleration of growth.

However, there is more to this story.

A Function Of Population

One thing which is never discussed when reporting on employment is the “growth” of the working age population. Each month, new entrants into the population create “demand” through their additional consumption. Employment should increase to accommodate the increased demand from more participants in the economy. Either that or companies resort to automation, off-shoring, etc. to increase rates of production without increases in labor costs. The chart below shows the total increase in employment versus the growth of the working age population.

The missing “millions” shown in the chart above is one of the “great mysteries” about one of the longest economic booms in U.S. history. This is particularly a conundrum when the Federal Reserve talks about the economy nearing “full employment.” The Labor Force Participation Rate below shows this great mystery.

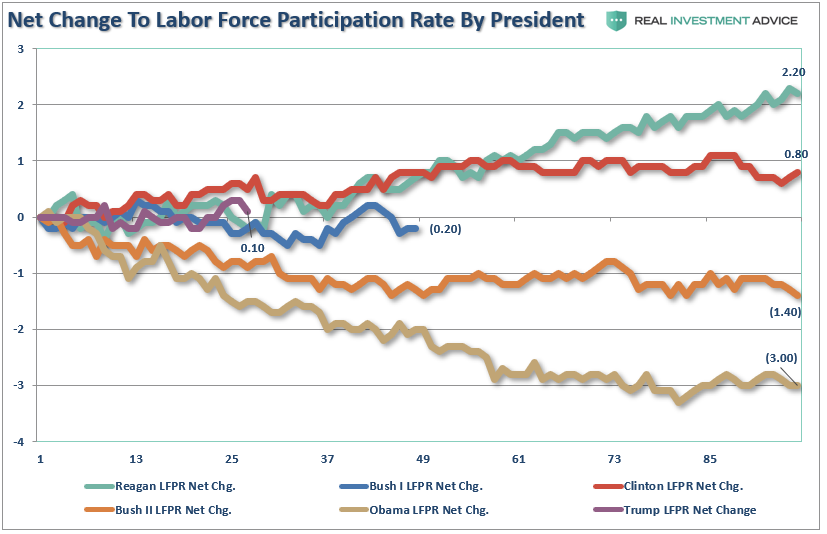

Since many conservatives continue to credit President Trump with a booming economy and employment gains, we can look at changes to the labor force participation rate by President as a measure of success. Currently, Trump’s gains are either less than Clinton, the same as Reagan, or tracking Bush Sr.; “spin it” as you will.

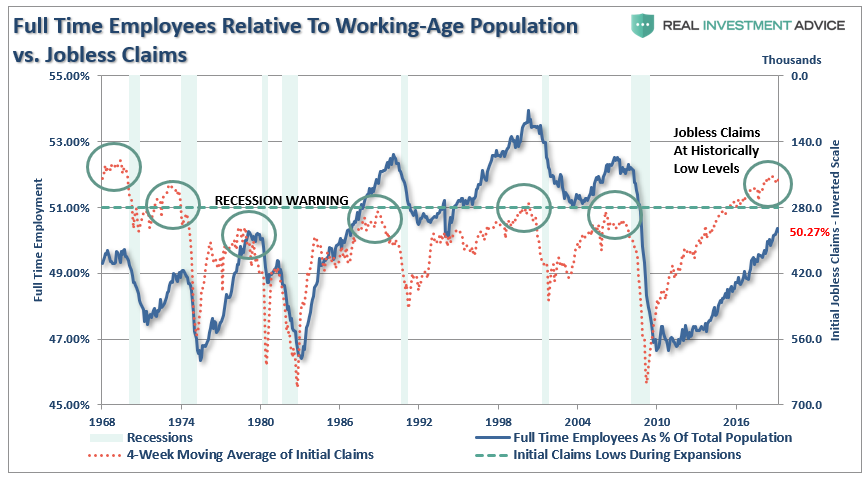

Of course, as we are all very aware, there are many people who are working part-time, going to school, etc. But even when we consider just those working “full-time” jobs, particularly when jobless claims are reaching record lows, the percentage of full-time employees is still well below levels of the last 35 years.

“With jobless claims at historic lows, and the unemployment rate at 4%, then why is full-time employment relative to the working-age population at just 50.27% which is down from 50.5% last month?”

It’s All The Baby Boomers Retiring

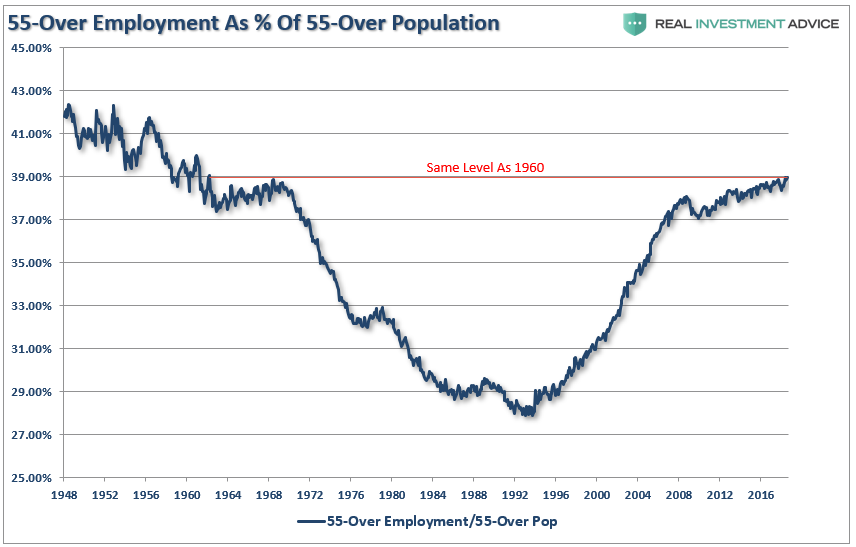

One of the arguments often given for the low labor force participation rate is that millions of “baby boomers” are leaving the workforce for retirement. This argument doesn’t carry much weight given that the “Millennial” generation, which is significantly larger, is simultaneously entering the workforce. The other problem is shown below, there are more individuals over the age of 55, as a percentage of that age group, in the workforce today than in the last 50-years.

Of course, the reason they aren’t retiring is that they can’t. After two massive bear markets, weak economic growth, questionable spending habits,and poor financial planning, more individuals over the age of 55 are still working because they simply can’t “afford” to retire.

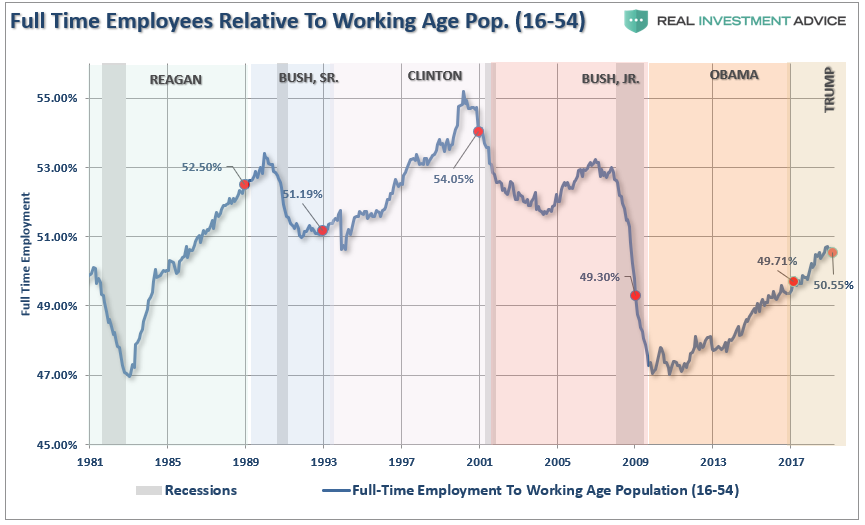

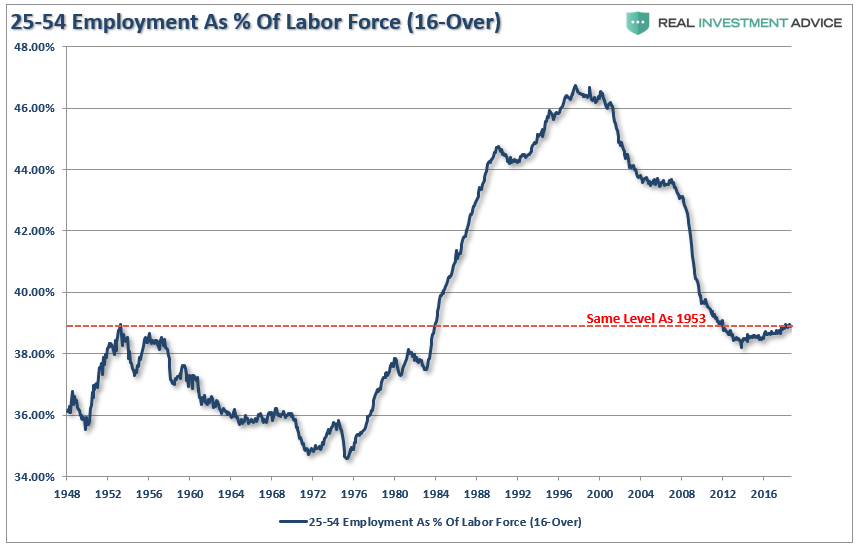

However, for argument sake, let’s assume that every worker over the age of 55 retires. If the “retiring” argument is valid, then employment participation rates should soar once that group is removed. The chart below is full-time employment relative to the working-age population of 16-54.

Importantly, note in the first chart above the number of workers over the age of 55 increased last month. However, employment of 16-54 year olds declined from 50.78% to 50.55%. It is also, the lowest rate since 1985, which was the last time employment was increasing from such low levels.

The other argument is that Millennials are going to school longer than before so they aren’t working either.(We have an excuse for everything these days.) The chart below strips out those of college age (16-24) and those over the age of 55. Uhm…

Here is the same chart of employed 25-54 year olds as a percentage of just that group.

When refined down to this level, talk about data mining, we do actually see recovery, however, after the longest economic expansion on record, a record stock market, and record levels of corporate debt to fund expansions and buybacks; employment ratios for this group are at the same level as seen in 1988. Such should raise the question of just how robust the labor market actually is?

Low initial jobless claims coupled with the historically low unemployment rate are leading many economists to warn of tight labor markets and impending wage inflation. If there is no one to hire, employees have more negotiating leverage according to prevalent theory. While this seems reasonable on its face, further analysis into the employment data suggests these conclusions are not so straightforward.

Strong Labor Statistics

Michael Lebowitz recently pointed out some important considerations in this regard.

“The data certainly suggests that the job market is on fire. While we would like nothing more than to agree, there is other employment data which contradicts that premise.”

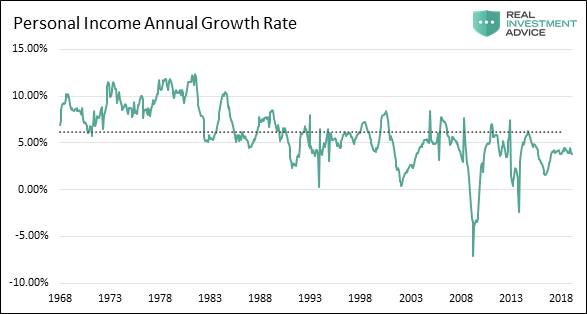

For example, if there are indeed very few workers in need of a job, then current workers should have pricing leverage over their employers. This does not seem to be the case as shown in the graph of personal income below.

Furthermore, a closer inspection of the BLS data reveals that, since 2008, 16 million people were reclassified as “leaving the workforce”. To put those 16 million people into context, from 1985 to 2008, a period almost three times longer than the post-crisis recovery, a similar number of people left the workforce.

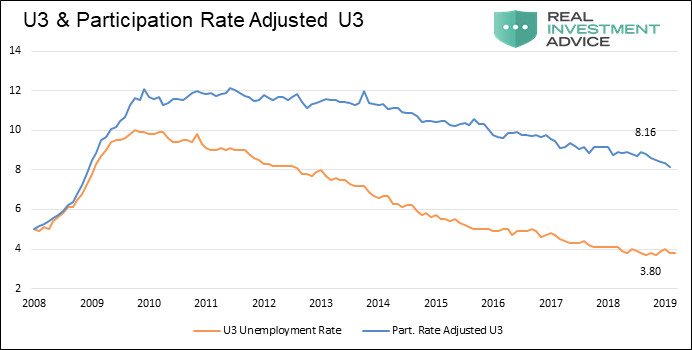

Why are so many people struggling to find a job and terminating their search if, as we are repeatedly told, the labor market is so healthy? To explain the juxtaposition of the low jobless claims number and unemployment rate with the low participation rate and weak wage growth, a calculation of the participation rate adjusted unemployment rate is revealing.

When people stop looking for a job, they are still unemployed, but they are not included in the U-3 unemployment calculation. If we include those who quit looking for work in the data, the employment situation is quite different. The graph below compares the U-3 unemployment rate to one that assumes a constant participation rate from 2008 to today. Contrary to the U-3 unemployment rate of 3.90%, this metric implies an adjusted unemployment rate of 8.69%.

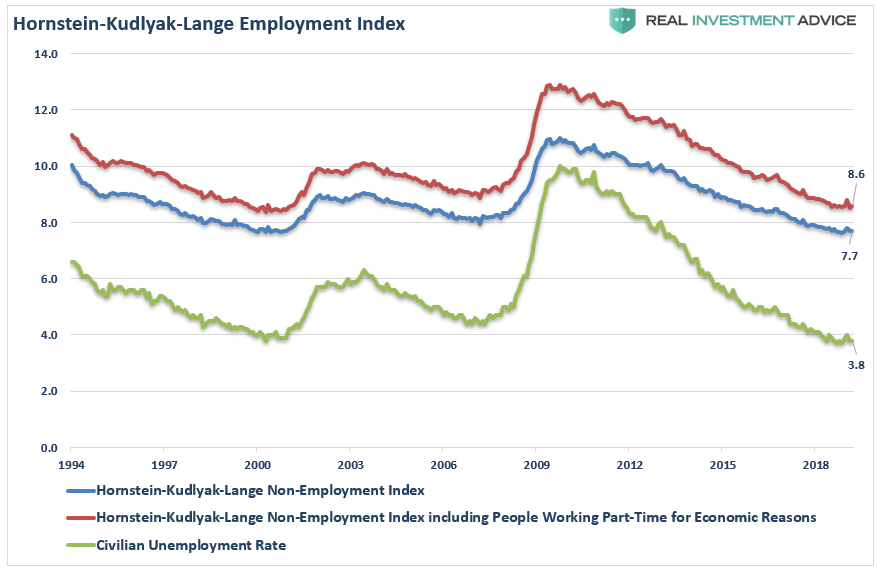

Importantly, this number is much more consistent with the data we have laid out above, supports the reasoning behind lower wage growth, and is further confirmed by the Hornstein-Kudlyak-Lange Employment Index.

(The Hornstein-Kudlyak-Lange Non-Employment Index including People Working Part-Time for Economic Reasons (NEI+PTER) is a weighted average of all non-employed people and people working part-time for economic reasons expressed as the share of the civilian non-institutionalized population 16 years and older. The weights take into account persistent differences in each group’s likelihood of transitioning back into employment. Because the NEI is more comprehensive and includes tailored weights of non-employed individuals, it arguably provides a more accurate reading of labor market conditions than the standard unemployment rate.)

One of the main factors driving the Federal Reserve to raise interest rates and reduce its balance sheet is the perceived low level of unemployment. Simultaneously, multiple comments from Fed officials suggest they are justifiably confused by some of the signals emanating from the jobs data. As we have argued in the past, the current monetary policy experiment has short-circuited the economy’s traditional traffic signals.None of these signals is more important than employment.

As Michael noted:

“Logic and evidence argue that, despite the self-congratulations of central bankers, good wage-paying jobs are not as plentiful as advertised and the embedded risks in the economy are higher. We must consider the effects that these sequences of policy error might have on the economy – one where growth remains anemic and jobs deceptively elusive.

Given that wages translate directly to personal consumption, a reliable interpretation of employment data has never been more important. Oddly enough, it appears as though that interpretation has never been more misleading. If we are correct that employment is weak, then future rate hikes and the planned reduction in the Fed’s balance sheet will begin to reveal this weakness soon.”

As an aside, it is worth noting that in November of 1969 jobless claims stood at 211,000, having risen slightly from the lows recorded earlier that year. Despite the low number of claims, a recession started a month later, and jobless claims would nearly double within six months. This episode serves as a reminder that every recession followed interim lows in jobless claims and the unemployment rate. We are confident that the dynamics leading to the next recession will not be any different.

But then again, maybe the yield-curve is already giving us the answer.

via ZeroHedge News http://bit.ly/2OUaWya Tyler Durden

“It will be definitely a jumbo deal with at least four tranches,” said Sergey Dergachev senior portfolio manager at Union Investment Privatfonds GmbH in Frankfurt. “Demand should be huge.”

Demand for the most highly anticipated sale of the year already totaled $30 billion, Aramco Chairman and Saudi Energy Minister Khalid Al-Falih told Bloomberg TV early on Monday, but it has already rep[ortedly surpassed that.

Dergachev speculated that demand could even surpass the record $53 billion in bids that Qatar received for its $12 billion bond sale last year.

Entering the bond market has forced Aramco to open its books after decades of speculation about its earnings and production. The company got the fifth-highest investment-grade ratings at both Moody’s Investors Service and Fitch Ratings, matching Saudi Arabia’s sovereign grade.

Bloomberg reports that the oil giant is offering six-tranche debt, according to the people familiar with the matter, who asked not to be identified. The world’s most profitable company is tapping the market ahead of a planned $69 billion acquisition.

Initial Price Thoughts:

USD 3Y Fixed — T+75 area

USD 3Y Floating Rate Notes — Libor + equivalent

USD 5Y Fixed — T+95 area

USD 10Y Fixed — T+125 area

USD 20Y Fixed — T+160 area

USD 30Y Fixed — T+175 area

Aramco may raise about $10 billion from the sale, the kingdom’s energy minister said in January, as Saudi Arabia combines the oil producer with chemical maker Saudi Basic Industries Corp.

The deal is expected to price tomorrow, so we would not be surprised to see leakage higher in Treasury yields on rate-locks and rotation.

via ZeroHedge News http://bit.ly/2uRQq8f Tyler Durden

While the week starts off slowly, traders will look forward to a “Super Wednesday” with the EU emergency Brexit summit, ECB meeting, US CPI report and FOMC minutes all slated for that day. According to DB’s Craig Nicol, “that should be the highlight of the week ahead however we’ve also got a busy week for data out of China, as well as a number of scheduled Fed speakers, the annual IMF and World Bank Spring Meetings and China-EU Summit. If that wasn’t enough, US banks also kick off earnings season next week.”

Starting with Brexit, the latest in the neverending divorce saga is the UK seeking an extension of the Brexit deadline until June 30, with a further headline suggesting that PM May is aiming to ratify the divorce deal before May 23. The PM’s letter also announced that the UK will hold European Parliamentary elections on May 23 if a deal hasn’t been ratified by then. So markets will now await the EU response with an emergency Summit scheduled for next Wednesday. PM May will reportedly not bring any Brexit plan to a vote before the Summit which means the EU will need to come to a unanimous agreement that a clear plan on a way forward is being proposed, to allow the EU to come to a common position and offer the extension.

For the ECB, after markets were left puzzled by the messaging from the previous meeting and with the subsequent moves in bond markets which has seen Bunds turn negative again, expect there to be plenty of questions directed at Draghi both on the TLTRO details and also the impact of negative rates. Newsflow on tiering has picked up in recent days including an acknowledgement in the latest meeting minutes, with the latest report suggesting that the tiering trial balloon was not quite as successful and the ECB may hold off on announcing details. So markets will particularly be looking for clues as to where the internal debate on persistent low rates on bank margins and profitability now lies.

Shortly after the ECB on Wednesday we’ll get the March CPI report in the US. The consensus is for a +0.2% mom core reading which would be enough to hold the annual rate at a relatively solid +2.1% yoy. In the evening we then get the FOMC minutes from the March meeting. A reminder that the message from this meeting was undeniably dovish. The median dot moved to no rate hikes this year with seven officials also seeing the Fed on hold at least through the end of 2020. Deutsche Bank economists made the point that it is clear that the Committee no longer has a strong tightening bias and patience remains the order of the day for some time. With that in mind, expect the minutes to reiterate this more dovish tone, with readers also likely to look out for hints on the composition and duration of the balance sheet.

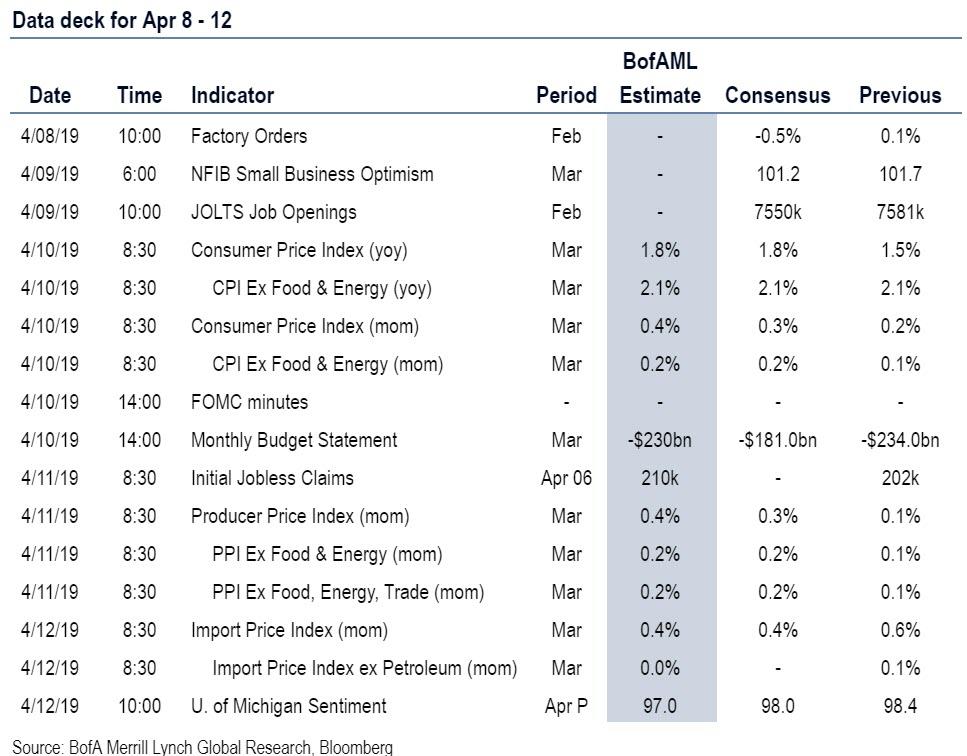

Elsewhere, as well as the CPI report in the US next week we’ll also get the March PPI report on Thursday. Outside of that it’s fairly light for data in the US though with only final February factory, durable and capital goods orders due on Monday, the March monthly budget statement on Wednesday, claims on Thursday and the preliminary April University of Michigan consumer sentiment survey on Friday worth flagging.

In Europe expect there to be some focus on the February industrial production reports next week with data due for the UK and France on Wednesday and the Euro Area on Friday. We’ll also get the February GDP reading for the UK on Wednesday while Thursday will see final March CPI revisions made in Germany and France. Meanwhile in Asia it’s a busy week for data out of China with March foreign reserves due on Sunday, March CPI and PPI due on Thursday and March trade data due on Friday. We’re also expecting to get the latest money and credit aggregates data covering March at some stage next week.

As for the Fedspeak, we got confirmation that Chair Powell is to address the House Democratic Retreat which takes place over three days from Wednesday to Friday next week. Other speakers include Clarida late on Tuesday, and Clarida again on Thursday along with Bullard, Quarles, Kashkari and Bowman – all at separate events.

At a more micro level next week will also see an early drip feed of Q1 earnings in the US including the banks with both JP Morgan and Wells Fargo due to report on Friday. The quarter is expected to be a dud, with consensus now expecting a sharp drop in EPS growth, the first decline since 2016.

Finally, other things to potentially watch out for next week include China Premier Li Keqiang travelling to Brussels for the five day China-EU Summit on Monday, the annual week long Spring Meetings of the World Bank/IMF also kicking off Monday, Israel’s general election on Tuesday, the IMF’s latest World Economic Outlook update on Tuesday, the US Congressional Committee holding a hearing on Wednesday with the chiefs of the biggest US banks on “Holding Megabanks Accountable”, the OPEC monthly oil market report on Wednesday, South Korea President Moon Jae-in meeting President Trump on Thursday, and India heading to the polls on Thursday (albeit voting in phases with results in late May).

Summary of key events by day, courtesy of Deutsche Bank

Monday: A fairly light day for data, with March consumer confidence due in Japan overnight followed by February trade data in Germany, March industry sentiment data in France and the Sentix investor confidence reading for the Euro Area. In the US we’ll get February factory orders and final durable and capital goods orders revisions. Elsewhere, the BoJ’s Kuroda and ECB’s Villeroy are due to speak, while China Premier Li Keqiang is due to travel to Brussels for the China-EU Summit. The annual IMF/World Bank Spring Meetings also kick off.

Tuesday: A very quiet day for data releases with the UK’s March BRC sales data, and March NFIB small business optimism print and February JOLTS report in the US the only releases of note. The Fed’s Clarida speaks in the evening while the IMF’s latest World Economic Outlook update is due.

Wednesday: The big highlight is the ECB meeting in the early afternoon followed by Draghi’s press conference. Not long after that we’ll also get the March CPI report in the US. Also high on the agenda will be the emergency EU Brexit Summit. Other data releases of note include February industrial production prints in France and the UK, as well as the February GDP reading in the latter. The March monthly budget statement is also due in the US along with the latest FOMC meeting minutes. The OPEC monthly oil report is due while the US Congressional Committee is due to hold a hearing with chiefs of the biggest US banks on “Holding Megabanks Accountable”.

Thursday: Inflation releases should be the main focus with March CPI/PPI in China, final March CPI revisions in Germany and France and the March PPI report in the US all due. The latest initial jobless claims reading in the US will also be out. It’s also a busy day for Fedspeak with Clarida, Bullard, Quarles, Kashkari and Bowman all due to speak. Meanwhile, South Korea President Moon Jae-in will meet with President Trump. India will also go to the polls.

Friday: Another quiet day for data with the February industrial production report for the Euro Area, and March import price index and preliminary University of Michigan consumer sentiment readings in the US due. March trade data in China is also likely to be out at some stage. Away from that the BoE’s Carney is due to speak at the IMF/World Bank Spring Meetings.

Looking at just the US, Goldman writes that the key economic data releases this week are the CPI report on Wednesday and the PPI report on Thursday. In addition, minutes from the March FOMC meeting will be released on Wednesday. There are several scheduled speaking engagements by Fed officials this week, including two by Vice Chairman Richard Clarida on Tuesday and Thursday.

Monday, April 8

10:00 AM Factory Orders, February (GS -0.5%, consensus -0.5%, last +0.1%); Durable goods orders, February final (last -1.6%); Durable goods orders ex-transportation, February final (last +0.1%); Core capital goods orders, February final (last -0.1%); Core capital goods shipments, February final (last flat): We estimate factory orders decreased 0.5% in February following a 0.1% increase in January. Durable goods orders declined in the February advance report, driven primarily by a decline in aircraft orders.

Tuesday, April 9

06:00 AM NFIB small business optimism, March (consensus 101.2, last 101.7)

10:00 AM JOLTS Job Openings, February (consensus 7,550 last 7,581k)

6:45 PM Fed Vice Chairman Clarida (FOMC voter) speaks: Fed Vice Chairman Richard Clarida will speak at a Fed Listens event to discuss the review of the monetary policy framework at the Minneapolis Fed.

Wednesday, April 10

08:30 AM CPI (mom), March (GS +0.35%, consensus +0.3%, last +0.2%); Core CPI (mom), March (GS +0.13%, consensus +0.2%, last +0.1%); CPI (yoy), March (GS +1.82%, consensus +1.8%, last +1.5%); Core CPI (yoy), March (GS +2.03%, consensus +2.1%, last +2.1%): We estimate a 0.13% increase in March core CPI (mom sa), which would lower the year-over-year rate by a tenth to +2.0%. Our forecast reflects an expected drag from residual seasonality in the apparel category from methodological changes. We also expect softness in the used cars and lodging away from home categories. On the positive side, we expect a relatively stable pace of monthly shelter inflation, as alternative rent measures have picked back up, apartment completions have peaked, and aggregate vacancy rates remain low. Rebounding oil prices could also boost airfares in the upcoming report. We look for a 0.35% increase in headline CPI (mom sa), reflecting a boost from higher gasoline prices.

2:00 PM Minutes from the March 19-20 FOMC meeting: At its March meeting, the FOMC left the target range for the policy rate unchanged at 2.25-2.50%, as widely expected. The median dot in the Summary of Economic Projections showed a 0-1 baseline for rate hikes in 2019-2020, compared to 2-1 in December, and the average dots declined significantly. The FOMC also announced that portfolio runoff will stop at the end of September and that the pace of Treasury runoff will be tapered in the interim. In the minutes, we will look for further discussion of inflation, the path of the policy rate, the review of the monetary policy framework, and balance sheet normalization.

Thursday, April 11

08:30 AM PPI final demand, March (GS +0.4%, consensus +0.3%, last +0.1%); PPI ex-food and energy, March (GS +0.2%, consensus +0.2%, last +0.1%); PPI ex-food, energy, and trade, March (GS +0.2%, consensus + 0.2%, last +0.1%): We estimate a 0.4% increase in headline PPI in February, reflecting relatively firm core prices and energy prices. We expect a 0.2% increase in the core measure excluding food and energy, and also a 0.2% increase in the core measure excluding food, energy, and trade.

08:30 AM Initial jobless claims, week ended April 6 (GS 210k, consensus 210k, last 202k); Continuing jobless claims, week ended March 30 (last 1,717k): We estimate jobless claims increased by 8k to 210k in the week ended April 6, following a 10k decline in the prior week.

09:30 AM Fed Vice Chairman Clarida (FOMC voter) speaks: Fed Vice Chairman Richard Clarida will speak with Institute of International Finance President Tim Adams at a policy summit in Washington.

09:40 AM St. Louis Fed President James Bullard (FOMC voter) speaks: St. Louis Fed President James Bullard will discuss the US economy and monetary policy in Tupelo, Mississippi. Prepared text and audience and media Q&A are expected.

Friday, April 12

08:30 AM Import price index, March (consensus +0.4%, last +0.6%)

10:00 AM University of Michigan consumer sentiment, April preliminary (GS 97.0, consensus 98.0, last 98.4): We expect the University of Michigan consumer sentiment index to decrease by 1.4pt to 97.0. The measure appears elevated compared to similar measures such as the Conference Board consumer confidence index.

Source: Deutsche Bank, Goldman, BofA

via ZeroHedge News http://bit.ly/2VvrHCr Tyler Durden

A Russian-born academic accused of being a Kremlin operative claims she was “used” to smear former National Security Adviser Michael Flynn over an unplanned contact they had at a 2014 dinner at the University of Cambridge, England when Flynn was the Director of the Defense Intelligence Agency under President Obama.

38-year-old Svetlana Lokhova met Flynn at the February 2014 Cambridge dinner organized by Sir Richard Dearlove – a former head of MI6 who was launching an organization called the Cambridge Security Initiative, according to the BBC. Also part of the organizing group was alleged American spy Stefan Halper, a longtime spook and then-Cambridge professor emeritus widely reported to have infiltrated the Trump campaign and spied on several aides during the 2016 US election.

Svetlana Lokhova

“General Flynn was the guest of honor and he sat on one side of the table in the middle. I sat on the opposite side of the table to Flynn next to Richard Dearlove because I was the only woman at dinner, and it’s a British custom that the only woman gets to sit next to the host,” Lokhova told Fox News, who added that she has never been alone with Flynn.

As an expert on Soviet intelligence in the 1930s, Lokhova says she was asked to present some of her research. “The idea was that I would impress the DIA with the Cambridge pedigree of research.”

Lokhova showed Flynn a 1912 postcard from Stalin to the fiancee of his best friend. The fiancee was helping Stalin obtain a fake passport to escape surveillance when he was an early revolutionary working against the Tsarist regime.

…

She says Flynn asked her to send the document to him. This was because he was expecting some senior officials visiting Washington from Russia. At this point, there was a move towards trying to increase co-operation with Russia in the field of counter-terrorism, as it had recently emerged that those involved in the 2013 Boston bombing had been known to the Russians.

Lokhova says both Flynn and his assistant provided their emails, looking forward to using the postcard to break the ice when the Russian officials arrived in Washington. –BBC

Lokhova’s contact with Flynn at the dinner was used in several 2017 media reports to suggest that he had been “gotten to” by the Russians, while pundits and social media commentators suggested she was a Kremlin “honeypot.”

Hi @MalcolmNance@MSNBC, I have not forgotten how you told American people and the world a whole packs of lies about me based on your racist and sexist views. The tide has turned. https://t.co/iZnkX9Hqb6

I’m not a Russian spy and I have never worked for the Russian government,” said Lokhova, adding “I believe that General Flynn was targeted and I was used to do it.”

Of note, Halper – the ex-son-in-law of former CIA Director Ray Cline, was paid over $1 million by the Obama Defense Department between 2012 and 2018, with nearly half of it surrounding the 2016 US election.

Michael Flynn is pictured at a 2014 dinner at the University of Cambridge. (Courtesy of Svetlana Lokhova)

In December, 2016 – weeks after President Trump won the US election, event organizers Dearlove and Halper suddenly resigned from their positions at the Cambridge Intelligence Seminar (CIS) – an academic forum on the Western Spy World – due to what Halper called “unacceptable Russian influence” on the group.

According to journalist Sara Carter, however, Halper is steeped in Kremlin contacts.

Ironically, documents obtained by SaraACarter.com suggest that Halper also had invited senior Russian intelligence officials to co-teach his course on several occasions and, according to news reports, also accepted money to finance the course from a top Russian oligarch with ties to Putin.

Several course syllabi from 2012 and 2015 obtained by this outlet reveal Halper had invited and co-taught his course on intelligence with the former Director of Russian Intelligence Gen. Vladimir I. Trubnikov.

…

Even more interesting are reports from the British Media outlet, The Financial Times, that state Halper received funds for the Cambridge seminar from Russian billionaire Andrey Cheglakov, who has close ties to Russian President Vladimir Putin. –Sara A. Carter

Stefan Halper

On Sunday, Lokhova took to Twitter for a massive thread to slam Washington Post journalists David Ignatius and Tom Hamburger for what she said was covering up for “Halper’s mess.”

Remember, you must not never ever under any circumstances whatsoever called a spy on Trump campaign Halper, ‘a spy on Trump campaign’. Washington Post wants you to refer to Halper as ‘the FBI source who assisted the Russia investigation’ Got it? (4)

I never heard of Ignatius. But some reason my university professor, who I now understand is a friend of Ignatius, gave him my personal email address. Which was very nice as I have given birth few weeks earlier and still recovering from a shock of the WSJ attack (6)

I never heard of Ignatius. But some reason my university professor, who I now understand is a friend of Ignatius, gave him my personal email address. Which was very nice as I have given birth few weeks earlier and still recovering from a shock of the WSJ attack (6)

Ignatius responded he understood. And nothing was published, because as he told me later, he interviewed witnesses at the ‘Flynn dinner’ and found nothing (10).

Roll forward May 2018, and Halper is exposed as FBI operative. Ignatius writes ‘I’d like very much to ask you about Halper’. We spoke, & I caught him off-guard with a direct question: did he know he was a spy? To which he said ‘I always found him very reliable’, then hung up(12)

Hamburger tries to interrogate me AGAIN over the Flynn dinner. I refer him to Ignatius. Then he tries the Kremlin penetration of the Cambridge Seminar line. I read him out Halper resignation email proving that Halper did not tell the truth (14)

I told Hamburger (&have it time-stamped): ‘You reveal you have not had contact with Dearlove. So if the principals in the story have not confirmed their knowledge/statements personally, then the journalists do not have evidence, but only hearsay, and this should be stressed. (16

I also confirmed that Gen Flynn DIA liaison Dan O’Brien had been on the record with WaPo to confirm he left 2014 dinner with Flynn and nothing happened. Now let’s turn to what Hamburger wrote (18)

I’ve previously made numerous complaints to the WaPo and have been ignored. So now I call on the @washingtonpost to retract the story by Tom Hamburger and print everything they know about the #Russiagate hoax. (22)

Separately, there has to be a public inquiry into the alarming links between WaPo reporters and those with access to Classified Information. (23). THE END

In the aftermath of last weekend’s local elections in Turkey, which saw Erdogan’s ruling AKP party lose control of Turkey’s two main cities, Ankara and Istanbul, on Monday President Erdogan demanded that the country’s election board investigate “widespread irregularities” in local elections in Istanbul, where a partial recount is already underway after the ruling party contested its defeat, sending the lira tumbling to the lowest level since March 25.

“There is stealing from the boxes,” Erdogan said, adding that “we’re applying to the YSK against that organized intervention at the ballot box,” referring to the High Election Board. In the U.S. “they renew elections when there is a one percentage point difference,” the president said in what appeared to signal a push for a new election in the city.

“Given the huge economic challenges facing Turkey, this is the last thing Turkey needs at this stage,” said Tim Ash, senior strategist at BlueBay Asset Management LLP in London, said by email.

As we reported at the time, the March 31 municipal vote ended a quarter century of rule by Erdogan’s movement in Ankara, the capital. But it was the defeat in Istanbul that has galvanized his ruling AK Party into refuting the preliminary results. As a reminder, the AK Party and its predecessors have been holding Istanbul since Erdogan won the mayor’s office in 1994, and a defeat there would hinder social policies that rally the support of poorer citizens.

“No one has the right to claim victory in Istanbul with just a 13,000 to 14,000 vote difference,” Erdogan said, referring to the gap between the candidate of the opposition CHP, who was initially declared winner, and the AKP’s pick for mayor.

Erdogan’s party has already sought the cancellation of voting in Istanbul’s Buyukcekmece district and applied to the election board for a recount of all votes in the remaining 38 districts across the country’s largest city of 16 million people.

The news that Erdogan would challenge the Istanbul vote, adding to the country’s political instability, sent the lira sliding, with negative FX sentiment boosted when the Turkish central bank cut the interest rates it offers on lira leg of FX swaps with commercial lenders to 24% from 25.5%; in doing so it revered an increase in rate to 25.5% from 24% on March 25, when it ceased to offer any funding to commercial banks through its one- week repo facility

In addition to the slide in the lira, Turkish bonds and stocks also fell on Monday: yields on 10-year local-currency bonds jumped 21 basis points to 17.49%, the highest in a week, while five-year CDS climbed above 400 bps. In equities, the Borsa Istanbul benchmark stock index dropped 1.8% the first retreat in four days, after gaining 5.3% last week.

via ZeroHedge News http://bit.ly/2I4phaL Tyler Durden

For the two decades that he’s edited the scabrous and insightful U.K.-based web magazine Spiked, Brendan O’Neill, an occasional Reason contributor, has described himself—perhaps with a wee bit of provocation—as a “libertarian Marxist.” That is, until the populist uprisings in Europe last year.

“The thing that’s different now than it would have been six months ago,” O’Neill told me during a February episode of the Fifth Column podcast, “is that I’ve increasingly gone off the word libertarian.” The Brexit vote in England, the Yellow Vest protests in France, various anti-elitist spasms across the globe—these have packed more of a punch in two short years than four decades’ worth of classical liberal think-tank thumbsucking, he said: “I think other things more interesting than libertarianism are happening in the world right now.”

Individualists fond of Enlightenment rationalism do not generally hasten toward the excitement of street mobs or even electoral majorities. But the global rise in nationalist politics, from Viktor Orbán’s Hungary to Donald Trump’s America, has tempted many commentators with the thrills of revolution and machinations of power. Unsurprisingly, they are shedding their libertarianism along the way, writes Matt Welch.

“The eggs chase the bacon round the frying pan.. ”

News over the weekend leave me un-enlightened:

The denouement of the Brexit crisis on Thursday? Who knows..?

Kudlow saying its “closer” gives us no reason to think China and the US will actually sign a trade deal – it seems to be wallowing. Does it matter?

Saudi Arabia’s Aramco attracting a $30 bln book for its new bond. How quickly we forget..

Earnings kick off this week in the US – some say lower numbers will likely to test the stock market’s resolve and the current high valuations. Test, but unlikely to break?

How much are consumers over-levered across global housing, and personal lending? Lots, but rates are lower for longer.. until.

The global economy continues to look like its slowing..

Politics remains febrile (what a great word..) around the globe: a Salvini Le Pen love in, Trump vs Democrats, Trump losing Homeland chief, and the AfD.

Is the great Asset Reset button about to be pressed? What ARB?

Hilarious article on Zerohedge has a senior Blackrock exec calling for ECB to start buying European equities as next stage of boosting Europe’s recovery and inflation. Really? Because it’s worked so well in Japan?

Despite all the above, markets feel unconcerned. Speaking to clients there is a distinct “been here before” mood. Is it complacency, or is it an understanding that uncomfortable news might be hyped and fake, and signals often mislead? Despite all the negativity – investment managers tend to discount the known bad news. It’s the unknowns that sink markets. This is the last full week before the Easter break.

There are three things I’ve got on my watch list for the coming week:

FED Minutes on Wednesday – what do they think?

European banking – ECB lower for longer rates, further slowdown in Europe, (German industrial orders slipping by nearly 5%), money laundering, competition policy, and competition; just how dismal are prospects for the sector?

Boeing – stock price actually bounced on the back of the pilots not being to blame for Ethiopian Airlines crash. But long-term?

European Banks

European Bank stocks are among the worst performing asset class – only cars are worse. Low rates, margin pressure and the deepening downturn in Europe don’t help. A host of names are trading below asset value – which tells you one of two things: either they are cheap, or the market doesn’t believe where the banks have marked their assets. (I go with the latter.)

Who is comfortable with European banks? While they might not be the trigger they will be part of the next European crisis. But now? I’m just trying to rationalise them. There are really three big negatives when it comes to European banking: i) the banks themselves, ii) the European economy and iii) the who needs banks anyway argument.

When it comes to European banks, I’m struggling to come up with a single name I could point to and say: “that’s a great bank: well managed, sound business, and meets the dream “dull and predictable” investor nirvana.” None of them pass – but I’m willing to stand corrected if readers think I’m missing something and there are names to buy.

Sentiment towards European banks is coloured by the current tumble of fines against them. They have paid out over $16 bin in money laundering and regulatory fines over the past 10years. (And that number excludes the UK banks who are well over $10 bin themselves.) Although I’d split UK banks out as separate from Europe, Standard Chartered faces a multi-hundred million fine for Iranian sanctions breaking just as their current “deferred prosecution agreement” with the US authorities expires- under which it has promised to be good – ends.

The StanChart fines relate to activities between 2007-2014, but since then I’ve met many Iranians, (another story), who are clearly well banked and in possession of multiple credit cards, so it’s pretty clear Iran sanctions remain an open book for the SEC and guess who they are looking at. Oh? The rest of the world wants to deal with Iran? Better not say anything more… but I’d start in Paris..

Then there is the slew of Baltic money laundering charges engulfing Scandinavian banks (and maybe Deutsche). Despite the fact European banks have paid over $12 bln to Uncle Sam in Money Laundering fines, the EU has proved unable to agree on a list of money laundering jurisdictions and doesn’t even check money laundering at an EU level. Why? Some counties (including one beginning with G), enable their banks to not disclose fines (for reputational reasons). Neither can the EU agree on Banking Union or a single European Deposit Insurance Scheme; the French are in favour, everyone else who matters is against.

Meanwhile, you really can’t make up the current headlines about the political driven merger between Deutsche and Commerzbank, and the lack of progress (some would say reversal) towards European Banking Union. While banks are expected to work under the rules of the ECB, no one has agreed common rules, while ECB policy means banks struggles with margins, returns and profitability, and the legacy of broken bank lending practices essentially still unfixed since 2007. Season with economic downturn, and overlay with a layer of ECB bureaucracy and regulation to the mix and it doesn’t get any better.

The “successes” of European Banking Union has been extraordinary (US Readers: Sarcasm Alert): cross border banking isn’t happening (actively opposed by many), banks are being dragged down to the lowest common denominator, bad lending is unresolved, too-big-to-fail remains strongly entrenched as domestic vs European banking policy remains in the ascendant. When the Germans say they are against cross-border banking in order to create a German banking champion by merging Deutsche and Commerz, I can’t help but giggle.

Why bother with European banks? What is the purpose and goal of banking? It’s difficult to say anymore… banks don’t fill the same irreplaceable niche they once did in our financial ecosystem. (Global regulators can probably claim a minor success in that regard.)

Effectively banks have either become brands – with franchises in private banking (whatever that means), wealth management, less so in retail banking where actually meeting a bank clerk is less likely than meeting the tooth fairy, or they are processors of cash flows like mortgages or credit cards. Many SMEs complain their banks don’t understand their business needs, and are slow to address them. That’s particulary true when banks are in trouble, under the regulatory cosh and distrusted.

The future of banking is unclear. There are many routes: one is to optimise capital to make returns as efficient as possible, but that doesn’t neccessarilly work as it means cutting out extraneous risks, activities and services based on capital charges – not on the business case. Customers don’t respond well to organisations that drop them. Or the bank might claim to be client centric – which basically means: find them, grab them and retain them – something that’s about service, which is generally poor across Europe – especially in UK!

While Europe’s banking dinosaurs continue to cut costs and respond to regulatory fiat, we’ve got serious competition on the horizon. It’s about competing direct with the bright new service and cost focused FinTecs, reaching their market through digitisation (which financials seem genetically incapable of doing well…), and simple to use digital systems – which in many banks despair of. (We are all aware most banks are held together by slew of antique systems held together by “Dave from IT” who has been wearing the same T-shirt for over a month, but is the only person in the bank who speaks Klingon and archaic programming languages from 1986. Sorry Dave.)

My point on European banks boils down to dinosaurs trying to survive in an environment that’s moving against them, and is under competitive threat.

Boeing

Interesting to note how the Boeing stock price has performed – up then flat – since the preliminary investigation into the Ethiopian Airlines flight concluded it wasn’t pilot error and pointed to a fail on the MCAS anti-stall system – clearly Boeing’s problem.

The costs we’d expect investors to ask about Boeing’s potential future liabilities from a plane that’s proved dangerous seem to have been discounted. The effect on profitability of cutting 20% of production (the Boeing 737 Max series produces 1/3 of Boeing profits), and questions to management about the long-term policy towards developing new aircraft rather than simply updating old ones, aren’t at the forefront.

Instead, it seems the market has decided the 5000 plane 737 Max order book is too large a future income stream to be worried about. They assume the company is set to deal with any costs relating to the two crashes, that the MAX series will soon be cleared for flight operations again, and that there will be no long-term repetitional damage to the aircraft maker.

I do hope the market is right – Boeing, by default is a major part of any tracker fund. But, there are risks – including what is thrown up in the full investigation and in subsequent litigation. I heard it suggested Boeing will seek to make cases “go-away” by offering swift settlements, but we really do need to find out if they compromised on the design of the plane, investigate the claims no training was required, the complexity of the systems and how they explained these systems to crew.

I ask because I fly…. So should you!

via ZeroHedge News http://bit.ly/2YWWWbH Tyler Durden

Dealing another blow to public confidence in Boeing’s ability to swiftly reassure regulators that its 737 MAX 8 can be made safe for passenger travel, the South China Post on Monday reported that China Aircraft Leasing Group Holdings has put an order for 100 new 737s on hold, until it can be assured of the aircraft’s safety.

China was the first country to ground the 737s after Ethiopian Airlines flight ET302 crashed just minutes after takeoff – the second deadly incident involving the planes in just 5 months. A preliminary report from investigators found that the pilots followed Boeing’s safety procedures, but were still unable to right the plane.

Boeing is working on an update of its MCAS anti-stall software, which is believed to have contributed to both the crash of ET302 and a deadly Lion Air crash that occurred just five months earlier, but the fix is taking longer than anticipated.

Per its original delivery schedule, the first 737 was supposed to be delivered to the aircraft lessor in Q3 of this year. Originally, the lessor signed its contract with Boeing in June 2017, ordering 50 aircraft, then increasing it by 25 with an option for another 25. The order for the initial 50 aircraft was valued at $5.8 billion.

The company said it has stopped paying installments on the planes it has ordered.

The Hong Kong-listed lessor, controlled by the state-owned conglomerate China Everbright Group, placed an order for 50 aircraft in June 2017. CALC then increased it by another 25 in December with an option for 25 more as part of its plan to grow its overall fleet from 133 in 2018 to 232 by 2023. According to the original schedule, the first MAX jet was expected to be delivered to CALC in the third quarter of this year and continue up to 2023.

“The purchase has been suspended and we have stopped paying the installments,” said Chen Shuang, chairman of CALC and chief executive of China Everbright, the financial arm of China Everbright Group.

Airlines around the world have grounded the 737s, and last week, the FAA set up a joint review task force that is expected to include other aviation regulators, including possibly China’s, which has been invited to join.

Most of the deliveries weren’t expected until 2021, so the hold won’t impact the lessor’s operations, its spokesman said.

A CALC spokeswoman said that since most of the deliveries to the company were to be made from 2021, “so we see little or no impact on our operations.”

Chen said that they have received assurances from Boeing that “a better solution will be submitted to CALC within two months”, adding that they have not yet discussed compensation.

Chen said both sides are actively seeking a solution to the problem.

“One option being considered is to replace it with other aircraft. But there aren’t too many options,” said Chen.

Of course, the last thing Boeing shareholders wanted to hear after last week’s string of negative headlines was more bad news. And following the revelation that Boeing might soon have a second large cancellation on its hands, its shares – already lower – have sunk even further in premarket trading, weighing on the Dow.

via ZeroHedge News http://bit.ly/2Vwn0Iq Tyler Durden

If Boeing thought it could sweep its Boeing 737 MAX production cut under the rug with a late Friday announcement it failed: the company’s decision to cut 737 production by 20% sent BA shares 4% lower in pre-market trading with a BofA downgrade to Neutral not helping, and hit the shares of its suppliers including Meggitt, Melrose and Safran, which all fell between 1 percent and 2.5 percent. More importantly, since Boeing is the biggest component of the Dow, futures on the ‘industrial average’ were lower, with the implied open down more than 100 points, while global market and government bonds also drifted lower as progress toward a trade deal between America and China continued to drag. Oil rose as fighting in Libya raised the risk of supply outages.

As a reminder, on Friday Boeing announced that 737 production will be cut to 42 airplanes per month from 52 starting in mid-April, without giving an end date. Investment bank Cowen said Boeing’s decision to cut the production of the 737 was the right thing to do. “The 737 rate cut to 42/month should help resolve the MAX crisis but with a large 2019 cash hit,” wrote Cowen in a note.

Boeing’s latest woes did not help equity markets around the world, as last week’s global stock rally hit the pause button with MSCI’s world equity index flat as potential flashpoints including a crucial Brexit summit and central bank meetings loomed, and investors began to look ahead to an earnings season that would usher in an earnings recession according to Morgan Stanley.

While Dow futures took the brunt of the hit due to Boeing’s dominant position in the index, S&P 500 futs were also lower after the biggest US benchmark rounded out last week with gains that took it to a six-month high, while the Stoxx Europe 600 also nudged into the red. A rally in Shanghai fizzled out, and equities fell in Tokyo as the yen pushed higher.

China equity markets reopened after Friday’s holiday with handsome gains, but they were wiped out by midday with traders awaiting more “optimism” from U.S.-China trade talks; as a result the Shanghai Composite closed 0.1% lower after rising as much as 1.3% earlier; ChiNext index slides 2.1% while the MSCI Asia Pacific index was little changed. Early optimism emerged after a document was published on the central government’s website late on Sunday, in which Beijing said it would step up a policy of targeted cuts to banks’ required reserve ratios to encourage financing for small and medium-sized businesses. Shares rose in Sydney and saw modest gains in Hong Kong.

Early trading in Europe was also muted, with German exports and imports both falling more than expected in February, the latest sign that Europe’s largest economy will likely have meager growth in the first quarter amid increased headwinds from abroad. European stocks slipped 0.2% in early trading, as the weak German data and investor caution ahead of a string of political and monetary policy events held the market back. However, since then the Stoxx 600 index has pared losses and turns slightly positive, as the euro climbs against the dollar ahead of the EU summit. Healthcare (+0.5%) and oil & gas (+0.5%) lead gains, while Travel (-0.5%), construction (-0.5%) and financial services (-0.5%) the main laggards.

Euphoria was also muted due to lack of new trade deal developments, even though Trump’s top economic adviser Larry Kudlow said the two sides are “closer and closer” to a deal, and that top-tier officials would be talking this week. A strong U.S. jobs report Friday didn’t stop President Trump from suggesting the Fed should cut interest rates and stop shrinking its balance sheet.

“Today’s very minor move down has to be seen in light of recent developments,” said Britta Weidenbach, head of European equities at DWS. “We’re back at the levels where the correction started last year. So now the question certainly is, what’s next?”

Quite a few things are next, in fact, as Wednesday is a blockbuster day. We have the EU emergency Brexit summit where they will decide whether to grant the U.K. a further extension and on what terms, an ECB meeting a day earlier than normal, the US CPI report and FOMC minutes all slated for that day. That should be the highlight of the week ahead however we’ve also got a busy week for data out of China, as well as a number of scheduled Fed speakers, the annual IMF and World Bank Spring Meetings and a China-EU Summit. If that wasn’t enough, US banks also kick off earnings season at the end of the week. Oh and Friday also marks the revised point that the U.K. leaves the EU if no extension is given this week.

Investors will also focus on the upcoming earnings season, which kicks off at the end of this week with U.S. banks reporting, and which will be a reality check for markets as analysts now expect a roughly 4% drop in EPS Y/Y, the first such drop since 2016.

“Q1 will definitely not be a good quarter for corporates, and it might well be that the market turns back to fundamentals whereas a lot of hope on China/U.S. trade deals and developments on the interest rate front had driven markets up year-to-date,” said DWS’ Weidenbach.

Bond markets were being squeezed by investors’ search for yield after benchmark German Bunds fell into negative territory. Greece’s 10-year government bond yields were within a shade of their lowest level in over 13 years as a cocktail of positive headlines boosted sentiment towards the country and zero percent Bund yields push investors to riskier investments. German bund yields traded at 1 basis point, just holding in positive territory, while US Treasuries and the dollar were steady after President Donald Trump stepped up pressure on the Federal Reserve to sustain growth.

Looking ahead, though, optimism persists: “Valuations are OK, global growth is expected to improve into the second half of the year, monetary and fiscal policy has become more supportive of markets and the trade war is receding,” said Shane Oliver, investment strategist at AMP Capital Investors Ltd. This “should support decent gains for share markets through 2019 as a whole,” he said.

In the latest Brexit news, UK PM May could offer the Labour Party a post-Brexit customs union today, prior to this The Times reports that PM May is set to offer Jeremy Corbyn a legally binding soft Brexit deal with a “Boris lock” that would make it difficult for a future Eurosceptic prime minister to tear up after she leaves No 10. (Newswires/Times) Separately, UK Labour party want a firm indication that the government is prepared to reopen the political declaration, there may be some movement later (either talks or a new offer), according to BBC’s Nick Eardley. Conservative MPs are warning that they will move to remove UK PM May within weeks if the UK is forced to partake in EU elections and extend membership beyond the end of June.

In FX, we saw some more risk-aversion, as the dollar slipped 0.1% to 97.269 against a basket of currencies, while the euro inched up 0.1%, but hovered near a one-month low at $1.1229 ahead of the ECB meeting later this week. The pound edged higher as British Prime Minister Theresa May appealed to both the public and politicians in search of support for a compromise Brexit plan; whe needs to come up with a new plan to secure a delay from EU leaders at a summit on Wednesday as a deadline of this Friday draws ever closer. In Turkey, President Recep Tayyip Erdogan cited “widespread irregularities” in local elections in Istanbul, sending the lira lower.

In commodities, crude extended gains as an escalation of fighting in OPEC producer Libya overshadowed the biggest increase in U.S. active rigs since May. WTI and Brent prices are revisiting levels last seen in November 2018 (USD 63/bbl and USD 70/bbl respectively). Gains are spurred as conflict in Libya escalates, with Hafta ordering his troops to march towards Tripoli. The fight has not yet effected oil supply, with Port Zawiya closely monitored by oil traders as it is the closest to the conflict. In metals, London copper prices rose as much as 1 percent on Monday, snapping two days of declines.

Expected data include factory orders and durable-goods orders. Kenon Holdings is reporting earnings.

Market Snapshot

S&P 500 futures down 0.2% to 2,891.75

STOXX Europe 600 down 0.2% to 387.57

MXAP up 0.08% to 162.65

MXAPJ up 0.2% to 540.47

Nikkei down 0.2% to 21,761.65

Topix down 0.4% to 1,620.14

Hang Seng Index up 0.5% to 30,077.15

Shanghai Composite down 0.05% to 3,244.81

Sensex down 0.5% to 38,652.54

Australia S&P/ASX 200 up 0.7% to 6,221.35

Kospi up 0.04% to 2,210.60

German 10Y yield unchanged at 0.008%

Euro up 0.2% to $1.1234

Italian 10Y yield fell 4.1 bps to 2.124%

Spanish 10Y yield fell 0.4 bps to 1.101%

Brent futures up 0.7% to $70.81/bbl

Gold spot up 0.4% to $1,297.25

U.S. Dollar Index down 0.2% to 97.24

Top Overnight News

U.S. President Donald Trump’s frustration over his inability to fulfill his signature 2016 campaign promise to curb illegal immigration led him to oust his second homeland security chief, as the president eyes his re-election prospects next year; Homeland Security Secretary Kirstjen Nielsen resigned at Trump’s request after meeting with him Sunday, according to people familiar with the matter

A long but flexible extension to the Brexit process proposed by the European Union was denounced as “like purgatory” by a leading U.K. lawmaker, as Prime Minister Theresa May sought to gain support for a compromise departure plan

Larry Kudlow says the U.S. and China are “closer and closer” to a trade deal, and that top-tier officials would be talking again this week via “a lot of teleconferencing”

Bank of Japan Governor Haruhiko Kuroda says the economy is expanding moderately though weakness in overseas economies is weighing on exports and production

Oil extended its rally to a five-month high as conflict in major producer Libya increased the risk of new supply outages. Libya’s internationally-recognized government vowed to counterattack against forces loyal to strongman Khalifa Haftar

Japanese investors turned net buyers of German sovereign bonds in February, ending a four-month selling streak, according to balance-of-payments data

China’s foreign-currency holdings rose as lower government bond yields in developed markets lifted valuations. Reserves increased by $8.58b to $3.0988t in March, the People’s Bank of China said

Theresa May is hoping to re-start stalled Brexit negotiations with her chief political rival Jeremy Corbyn, in her search for a compromise plan she can sell to European leaders at a crucial summit this week

Japanese investors bought German and French bonds in February, when deepening concern over Europe’s economic slowdown spurred speculation the region’s central bank would join the Federal Reserve in turning dovish on monetary policy

Turkish President Recep Tayyip Erdogan urged the country’s election board to investigate “widespread irregularities” in local elections in Istanbul, where a partial recount is already underway after the ruling party contested its defeat. The lira declined on the remarks

According to a BOE survey released Monday, 47% of people see rates going up in the next 12 months, compared with 53% in November. Markets are also increasingly pessimistic of a hike amid increased Brexit uncertainty, and see a less than 10% chance of a move in the next year

Asian equity markets began the week mixed as the region somewhat failed to sustain the initial momentum from last Friday’s gains on Wall St, where all majors edged higher and the S&P 500 notched a 7-day win streak after the latest NFP data. ASX 200 (+0.6%) and Nikkei 225 (-0.2%) both opened higher with commodity-related sectors among the biggest gainers in Australia due to strength in metal prices and after WTI crude rallied to fresh YTD highs above the USD 63.00/bbl level, while risk appetite in Japan was less decisive and eventually waned as exporters contended with flows into JPY. Hang Seng (+0.4%) and Shanghai Comp. (U/C) were initially buoyed on return from their extended weekend as they played catch up to the optimism from last week’s US-China trade talks in which both sides noted significant progress was made and with discussions to continue via teleconference this week, while China also plans to ease the burden on businesses in which it will reduce companies’ social insurance contributions by CNY 300bln. However, the mainland gradually deteriorated as some were kept cautious by reports that plans for a US-China joint statement hit a stalemate due to differences regarding access to China’s market. Finally, 10yr JGBs were mildly higher with prices supported as the initial positive momentum in the region waned and with the BoJ present in the market for JPY 280bln in JGBs, while prices also tracked the rebound seen in T-notes in the wake of the US jobs data where weak wage growth subsequently saw the probability of a Fed rate cut this year increase to 75% before paring back to 50%.

Top Asian News

China Steps Up Gold-Buying Spree as PBOC’s Hoard Rises Again

UniCredit China Employee Said to Allegedly Embezzle $15 Million

India’s Cash Crunch Is Weighing on Financial Health of Firms

Lira Falls as Erdogan Demands Probe Into Lost Istanbul Vote

A subdued start to the week for European equities [Stoxx 600 unch] following on from a mixed Asia-Pac session as Friday’s NFP optimism waned ahead of another week filled with risk events. Broad-based losses are being experienced across major indices, whilst sectors are relatively mixed with energy names outperforming after WTI and Brent crude rallied to fresh YTD highs. In terms of individual movers, BMW (-0.4%) shares have nursed some losses after opening lower in excess of 2% amid reports that its Q1 results will be impacted by the EU fines into antitrust proceedings. This initially pressured its fellow German peers in sympathy [Daimler (-0.2%), Volkswagen (+0.4%)] who later climbed back above break-even. Sticking with Germany, Dialog Semiconductor (+1.1%) shares were bolstered amid news that the company closed a deal with US tech giant Apple (-0.4% pre-market), ahead of schedule. Finally, Fiat Chrysler (+1.3%) rose to the top of the FTSE MIB following reports the Co. signed a deal with Tesla to bypass EU emission rules. Elsewhere, Boeing (BA) CEO says they plan to cut their 737 Max monthly production by just under 20%. As such Co. are lower by 2.6% in the pre-market.

Top European News

Swedbank’s Debt Headache Reveals a ‘Remarkable’ Bond Outlier

Fiat to Pool Cars With Tesla to Meet EU Emissions Targets on CO2

Ashley Floats New Plan to Stave Off Debenhams Equity Wipeout

In FX, the Dollar continues to drift down from initial post-NFP highs as global stocks wobble and oil climbs to fresh ytd peaks. The DXY remains relatively rangebound, however, and ‘comfortably’ above the 97.000 handle within 97.230-384 parameters.

JPY/GBP – The Yen has regained a safe-haven bid and rebounded from circa 111.80 lows through 111.50 and close to the 200 DMA (111.495) vs the Greenback, while technical buying was also noted during the Asia-Pacific session in several Jpy crosses including Eur/Jpy and Nzd/Jpy that tested psychological/round number levels at 125.00 and 75.00 respectively. Meanwhile, Sterling retains an underlying bid vs the Buck above 1.3000 and is straddling 1.3050, as Eur/Gbp pivots 0.8600 in the run up to Wednesday’s EU Brexit Summit when UK PM May will present the case for another A 50 extension backed by a withdrawal plan or at least a strategy to avert no deal on April 12. On that note, she will resume talks with the Labour Party in an effort to find a compromise amidst reports that the opposition want a firm commitment to re-opening the PD rather than additions to the existing document.

EUR – The single currency is also holding above a big figure mark vs the Dollar and 2019 lows not far below 1.1200, but chart resistance around 1.1250 and a key Fib is still capping the upside, while hefty option expiry interest at 1.1225 (1.4 bn) is also weighing on the headline pair.

NZD/CAD/AUD/CHF – All relatively flat and narrowly mixed vs the Usd, as the Kiwi meanders between 0.6723-37 and also has expiries close by to exert some influence into the NY cut (1 bn at 0.6725). Elsewhere, another upturn in oil prices has helped the Loonie reverse some post-Canadian jobs data losses within a 1.3390-70 band, and is also supporting the NOK vs the Eur with the cross back down through 9.6500. Note, Barclays has shorted Eur/Nok and is looking for a move to 9.5908 with a 9.7100 stop. Elsewhere, the Aussie is hovering around 0.7100 and Franc is sitting tight near parity.

EM – The Lira has weakened even further vs the Dollar as municipal election results are recounted in Istanbul and Turkey mulls military action in Syria, while the CBRT has cut its FX swap rate by 150 bp and decided to restart 1 week refunding operations. Usd/Try up over 5.7000 and 5.7100+ at one stage.

In commodities, further supply-side woes have bolstered the energy complex to YTD highs with WTI and Brent futures revisiting levels last seen in November 2018 (USD 63/bbl and USD 70/bbl respectively). Gains are spurred as conflict in Libya escalates, with Hafta ordering his troops to march towards Tripoli. The fight has not yet effected oil supply, with Port Zawiya closely monitored by oil traders as it is the closest to the conflict. The port is scheduled to load 6mln barrels of crude in April which is subject to change if shipments are delayed. Amidst this, the oil complex last week saw speculators adding to their net long positive positions, with managed money positions in ICE Brent rising by just under 27k to result in net long speculative positions at almost 350k lots, the largest since the end of October 2018. Elsewhere, Saudi Energy Minister noted that he does not believe the Kingdom needs to cut output below its target, whilst a key architect of Russia’s OPEC+ deal said that the members could raise oil output in its June meeting. On the Aramco front, Saudi Energy Minister Al-Falih stated that the Aramco bond could attract demand north of USD 30bln (vs. touted USD 10bln) which will be used as part of a payment for the 70% purchase of Sabic (valued at USD 6.9bln). In the metals complex, gold prices are underpinned as the Greenback softened overnight and continues to pull back during the European session thus far. Demand for the yellow metal was also reflected in an increase in China’s gold reserves which showed the fourth consecutive month of gold purchases. Elsewhere, copper benefitted amid overnight gains across Chinese commodity prices in which Dalian iron ore futures extended on record highs, while Shanghai rebar and hot rolled coil rallied over 3% shortly after the open.

US Event Calendar

10am: Factory Orders, est. -0.5%, prior 0.1%; Factory Orders Ex Trans, prior -0.2%

10am: Durable Goods Orders, est. -1.6%, prior -1.6%; Durables Ex Transportation, est. 0.1%, prior 0.1%

10am: Cap Goods Orders Nondef Ex Air, prior -0.1%; Cap Goods Ship Nondef Ex Air, prior 0.0%

DB’s Jim Reid concludes the overnight wrap

This week is set to be busy but get an early night on Tuesday (I can’t due to Champions League football. Exciting!) as Wednesday is a blockbuster day. We have the EU emergency Brexit summit where they will decide whether to grant the U.K. a further extension and on what terms, an ECB meeting a day earlier than normal, the US CPI report and FOMC minutes all slated for that day. That should be the highlight of the week ahead however we’ve also got a busy week for data out of China, as well as a number of scheduled Fed speakers, the annual IMF and World Bank Spring Meetings and a China-EU Summit. If that wasn’t enough, US banks also kick off earnings season at the end of the week. Oh and Friday also marks the revised point that the U.K. leaves the EU if no extension is given this week.

We may also see more US/China trade headlines this week and as a start over the weekend, President Trump’s economic adviser Larry Kudlow said that the US and China are getting “closer and closer” to a trade deal, and that top-tier officials would be talking again this week via “a lot of teleconferencing.” He added that “we’ve made great progress on the IP theft. We’ve made good progress on the forced transfer of technology,” the Chinese have acknowledged their problems, which was a very big hurdle, and “what wasn’t on the table, is on the table.” However, China’s state run news agency Xinhua had said on Friday that “the remaining issues are all hard nuts to crack” while the White House official statement post last week’s trade talks suggested that “significant work remains, and the principals, deputy ministers, and delegation members will be in continuous contact to resolve outstanding issues.” At the moment though it still seems like we are slowly inching towards a deal.

Asian markets have started the week on a mixed note with the Hang Seng (+0.30%) up while the Nikkei (-0.21%) and Kospi (-0.05%) are down erasing early gains. China’s Shanghai Comp was up as much as +0.76% in early trading but is now down (-0.09%) with semiconductor and chip makers stocks weighing on the index (down -3.30%). Elsewhere, futures on the S&P 500 are down -0.17% while the Japanese yen is up +0.31% this morning. Oil prices (WTI +0.54% and Brent +0.51%) are also extending gains this morning as an escalation of fighting in Libya is threatening further supply cuts. In terms of data releases, we saw China’s March foreign reserves at $3.099tn (vs. $3.090tn expected). China’s onshore yuan is trading -0.17% this morning.