This spring has seen a spike in families fleeing Central America and flocking to the U.S. border seeking asylum. Contrary to President Donald Trump’s claims, this isn’t a crisis. But the situation is straining the resources of frontline border agencies that are running out of space to process and house these migrants, partly because the president has been wasting resources on a useless wall rather than hiring judges and personnel for quick processsing.

Further, Trump’s proposed solutions will be too costly or unworkable or both.

There is, however, a costless fix: Hand these migrants a work permit right off the bat, but with a condition. Reason Foundation Senior Analyst Shikha Dalmia explains.

John Solomon published another blockbuster investigation Sunday on possible alleged interference in the 2016 election involving Ukraine.

Ukrainian sources told Solomon that the Trump Justice Department has allegedly not followed up on evidence given to the department by Ukrainian law enforcement officials.

Those Ukrainian officials said they have evidence showing that American Democrats, along with allies in Kiev, sought to interfere in the 2016 U.S. elections and obstruct ongoing criminal probes.

Solomon interviewed Kostiantyn Kulyk, deputy head of the Prosecutor General’s International Legal Cooperation Department. He told The Hill that he, along with other senior law enforcement officials, have tried since last year to get visas from the U.S. Embassy “in Kiev to deliver their evidence to Washington.”

Kulyk told Solomon, “we were supposed to share this information during a working trip to the United States. However, the (U.S.) ambassador blocked us from obtaining a visa. She didn’t explicitly deny our visa, but also didn’t give it to us.”

According to Solomon’s interview with Kulyk,

Ukrainian businessmen “authorized payments for lobbying efforts directed at the U.S. government. In addition, these payments were made from funds that were acquired during the money-laundering operation. We have information that a U.S. company was involved in these payments.”

Kulyk said the company is tied to one or more prominent Democrats, Ukrainian officials insist, as reported by The Hill.

To read more on this in-depth investigation go to The Hill…

via ZeroHedge News http://bit.ly/2KeagVI Tyler Durden

The White House has joined other international voices in urging Benghazi-based renegade General Khalifa Haftar tohalt his ongoing assault on the country’s capital — this as the United Nations-backed Government of National Accord (GNA) in Tripoli has already spent days battling Haftar’s Libyan National Army (LNA), which has included the use of air power.

Late in the day Sunday, Secretary of State Michael Pompeo said in a statement, “We have made clear that we oppose the military offensive by Khalifa Haftar’s forces and urge the immediate halt to these military operations against the Libyan capital.”

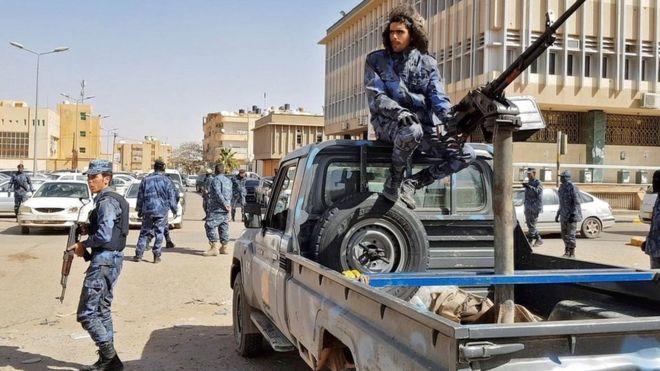

Gen Haftar’s forces in the southern town of Sebha last month, via AFP/BBC

And additionally Pompeo stated, “There is no military solution to the Libya conflict” — an absurd and ironic line for a top US official, given it was the US-NATO led 2011 war on Libya’s Gaddafi that plunged the country into years of internecine civil war and violence in the first place.

“A political solution is the only way to unify the country and provide a plan for security, stability and prosperity for all Libyans,” Pompeo said further.

Over the weekend US Africa Command said it was withdrawing a small contingency of Marines in Libya due to “security conditions on the ground.” US forces had reentered Libya in larger numbers during a 2016 campaign to oust ISIS terrorists from their stronghold in Sirte (notably Sirte had been Gaddafi’s favored town and the place of his execution at the hands of NATO-backed Islamists).

“The security realities on the ground in Libya are growing increasingly complex and unpredictable,” said AFRICOM commander Marine Corps Gen. Thomas Waldhauser, announcing the move. “Even with an adjustment of the force, we will continue to remain agile in support of existing U.S. strategy.”

The LNA has conducted air strikes on the south of the city as it seeks to advance into the center from a disused airport.

But the government of Prime Minister Fayez al-Serraj has armed groups arriving from nearby Misrata to help block the LNA.

It reported 11 deaths without saying on which side.

Al-Serraj, 59, who comes from a wealthy business family, has run the Tripoli government since 2016 as part of a U.N.-brokered deal boycotted by Haftar. — Reuters

Haftar – who solidified control of Eastern Syria and swept through the south in January, seeks to capture Tripoli and seize military control of the entire country, after his LNAcaptured a section aroundTripoli’s international airport.

As we noted earlier Sunday, some international reports confirmed that the LNA gained full control of the airport later in the day Saturday, but other conflicting reports say that this was premature, which could mean only a section what’s called the “old airport” was wrested from Tripoli forces — not the operational international side. Video purporting to be from the inside the Tripoli airport was posted on social media Saturday.

The U.N. Security Council fears that the Libyan National Army’s advances toward Tripoli –– where the U.N.-backed government is –– could lead to a military showdown.https://t.co/Htb5xrPhM9

The renegade general, who for about two decades previously lived in exile in the US a mere few miles from CIA headquarters in Virginia, is unlikely to halt the assault, which has the UN fearing a new major war that could further rip Libya apart.

#Libya– video of LNA fighting near Khallet Alforjan, Ain Zara, outskirts of #Tripoli.

Classic combined-arms tactics:

-Couple of dudes taking potshots with an MG in general direction of enemy

-Tank doing donuts

-Someone walking by with an RPG

-A guy on his back filming it all pic.twitter.com/USLo4i026e

One political commentator and historian, Gerald Horne, placed the latest events within the context of the prior NATO intervention: “You may well expect a bloodbath to unfold in Tripoli. Which is quite tragic and unfortunate, but I’d say it’s the inevitable outcome of the ill-advised attack by NATO, led by the US, that resulted in the 2011 overthrow of Gaddafi,” he told Russia’s RT.

As Libya descends even further into anarchy, violence & instability, here was the reaction of Hillary Clinton – a leading advocate of that “humanitarian bombing” – after learning Gaddafi was murdered (he was raped with a bayonet by a mob as he was killed). “Humanitarian wars”: pic.twitter.com/GFjPnaQKny

Based in Libya’s oil-rich east, Haftar’s militia has already captured much of the country’s oil resources, especially after a successful blitz to take much of the south over the past year.

And now he stands ready to take the capital of Tripoli in the west — home to Libya’s state-run National Oil Corporation, which when combined with small subsidiaries under its direction accounts for some 70% of the country’s oil output.

* * *

Bloomberg’s Salma El Wardany considers the potential impact on global oil markets and asks, will this impact oil exports?

Not immediately. Major oilfields and export terminals are

far from the clashes. But history shows that fighting anywhere

in Libya can cause dramatic swings in output. In June, Libya’s

crude shipments were suspended for weeks after Haftar captured

two export terminals and transferred them to an oil authority in

eastern Libya. Exports dropped by 800,000 barrels a day and

Libya lost almost $1 billion before he handed the terminals back

to the Tripoli-based National Oil Corp. “Oil operations have

been largely normal but any sustained fighting could quickly

bring Libya back below one million barrels a day,” Darwazah

said.

Concerning oil facilities in the west of the country:

Any disruption at Zawiya port, the main export terminal for

Sharara, would cause a partial or a complete shutdown of the

300,000 barrel-a-day oil field. Zawiya is scheduled to load 6

million barrels of crude in April. If Haftar takes control of

the terminal, he will virtually control Libya’s oil industry.

Prior the 2011 Libyan war and NATO military intervention which ultimately led to the overthrow and killing of longtime ruler Muammar Gaddafi, Libya produced about 1.6 million bpd, but years of turmoil and political instability in the aftermath have slashed that to 550,000 barrels per day as of 2018 output numbers.

via ZeroHedge News http://bit.ly/2OVx5fD Tyler Durden

An impossible job? Kirstjen Nielsen announced Sunday that on April 10, she’ll be stepping down as head of the Department of Homeland Security (DHS). Customs and Border Protection chief Kevin McAleenan will then become acting secretary of DHS.

Nielsen’s resignation comes less than a year and a half after she replaced John Kelly. Kelly went on to become President Donald Trump’s chief of staff, but he left that position in January. “With McAleenan’s appointment, Trump now has an acting homeland security secretary, defense secretary, interior secretary and chief of staff,” notesAxios.

Secretary of Homeland Security Kirstjen Nielsen will be leaving her position, and I would like to thank her for her service….

Nielsen “has arguably been the most aggressive secretary in the department’s short history in cracking down on immigration—with her legacy likely to be defined among progressives by the ‘zero tolerance’ prosecution policy of late spring and early summer 2018 that resulted in the separation of thousands of families at the US-Mexico border,” writes immigration reporter Dara Lind. Alas:

None of it appears to have been enough for Trump.

Nielsen’s resignation was preceded on Thursday night by the abrupt withdrawal of the nomination of acting Immigration and Customs Enforcement director Ron Vitiello to formally lead the agency, with Trump telling reporters Friday morning that he wanted to go in a “tougher direction.” While it’s not yet clear whether Trump requested Nielsen’s resignation or not, it certainly appears as if that “tougher direction” is extending to a new DHS secretary….

[W]ith nearly 100,000 migrants apprehended by Border Patrol agents along the US-Mexico border in March, Trump is yet again ruminating angrily and obsessively over immigration, riffing in speeches about telling migrants “we’re full” and “go back.”

Nielsen couldn’t make that happen, because no one could, because it’s impossible. The US can’t—even with a wall—physically prevent the entry of unauthorized immigrants onto US soil. And once on US soil, they have certain rights—including the right to request asylum.

The one silver lining here seems to be that there’s not much more McAleenan, or any Nielsen replacement, can legally do.

Even during Kelly’s tenure as DHS head, “the low-hanging fruit of deterrent immigration policies had been picked a long time ago,” writes Lind. She continues:

US immigration law is a balance between the desire to minimize unauthorized entry into the United States and the desire to protect vulnerable people who may be fleeing harm and persecution. Both US and international law prohibit the US from refusing entry to people who are in danger of prosecution in their home countries; both US statute and court settlements offer extra due-process protections to asylum seekers, children, and families.

The policies Trump wants, and the outcomes he has promised, aren’t within the power of the White House or the Department of Homeland Security.

As for Acting Secretary McAleenan’s prospects: He’s shown no particular signs of being better or worse than the average border hawk. He has presided over some of the worst immigration actions and abuses of the Trump administration, while refusing to endorse the very worse of Trump’s rhetoric. He’s “not an ideologue or fire breather,” an anonymous DHS officially tells CNN.

Kevin McAleenan is a career border officer. He “looks the part” better than Nielsen. But he’s not the dude who blames Ds for everything or talks of “invasion.” & he—like any other human on earth—can’t physically stop migrants from setting foot on US soil. https://t.co/YMKG55w4Pi

“The safest place in the world to be online.” A new internet regulation proposal backed by U.K. Prime Minister Theresa May would give regulatory bodies there “unprecedented powers to issue fines and other punishments if social-media sites don’t swiftly remove” offending content. British authorities are touting it as a way to ensure the U.K. is “the safest place in the world to be online.” Right now, the proposal “comes in the form of a white paper that eventually will yield new legislation,” reportsThe Washington Post:

Early details shared Sunday proposed that lawmakers set up a new, independent regulator tasked to ensure companies “take responsibility for the safety of their users.” That oversight—either through a new agency or part of an existing one—would be funded by tech companies, potentially through a new tax.

The agency’s mandate would be vast, from policing large social-media platforms such as Facebook to smaller web sites’ forums or comment sections. Much of its work would focus on content that could be harmful to children or pose a risk to national security. But regulators ultimately could play a role in scrutinizing a broader array of online harms, the U.K. said, including content “that may not be illegal but are nonetheless highly damaging to individuals or threaten our way of life in the U.K.” The document offers a litany of potential areas of concern, including hate speech, coercive behavior and underage exposure to illegal content such as dating apps that are meant for people over age 18.

FREE MINDS

Raunch-rhetoric realignment? These are words I never thought I’d type but…an interesting Matthew Yglesias thread:

Here’s a hypothesis I have without much hard data.

There’s been a decades-long debate in the US between Christian conservatives and feminists but also a third force in the debate that rarely articulates a self-conscious ideology — a sort of raunch culture.

“A pregnant mother is facing disorderly conduct charges in Georgia for allowing her 3-year-old son to relieve himself in public,” reports AP.

“When people ask me, how the Trump era is adjusting my political views, my answer is simple: It’s making me more libertarian,” writes David French at National Review. “It’s making me more concerned about the fate of the Constitution. I trust the government less, I’m more appalled at its sweeping assumptions of power, and I see more clearly what happens when its leaders—possessed with unwavering self-righteousness—believe that the ends justify the means.”

In China, a new app called Study the Great Nation pumps out Communist propaganda all day, directly to citizens’ smartphones, and awards them for reading. “Many employers now require workers to submit daily screenshots documenting how many points they have earned,” saysThe New York Times.

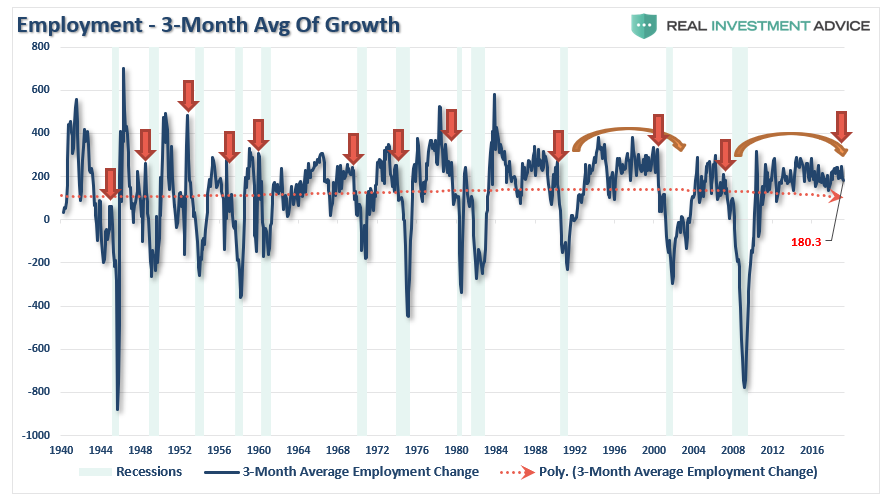

Last week, the Bureau of Labor Statistics (BLS) published the March monthly “employment report” which showed an increase in employment of 196,000 jobs. As Mike Shedlock noted on Friday:

“The change in total non-farm payroll employment for January was revised up from +311,000 to +312,000, and the change for February was revised up from +20,000 to +33,000. With these revisions, employment gains in January and February combined were 14,000 more than previously reported. After revisions, job gains have averaged 180,000 per month over the last 3 months.

Baseline Unemployment Rate: Unchanged at 3.8% – Household Survey

U-6 unemployment: Unchanged at 7.3% – Household Survey

Civilian Non-institutional Population: +145,000

Civilian Labor Force: -224,000 – Household Survey

Not in Labor Force: +369,000 – Household Survey

Participation Rate: -0.2 to 63.0– Household Survey”

There is little argument the streak of employment growth is quite phenomenal and comes amid hopes the economy will continue to avoid a recessionary contraction. When looking at the average rate of employment growth over the last 3-months, as Mike noted at 180,000, there is a clear slowing in the trend of employment. It is this “trend” we will examine more closely today.

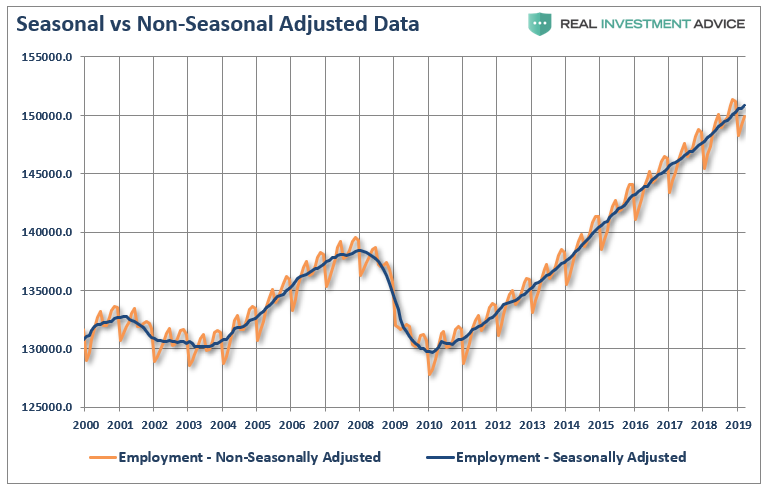

While a tremendous amount of attention is focused on the monthly employment numbers, the series is one of the most highly manipulated, guesstimated, and annually revised series produced by any agency. The whole issue of seasonal adjustments, which try to account for temporary changes to employment due to a variety of impacts, is entirely too systematic to be taken at face value. The chart below shows the swings between the non-seasonally adjusted and seasonally adjusted data – anything this rhythmic should be questioned rather than taken at face value as “fact.”

As stated, while most economists focus at employment data from one month to the next for clues as to the strength of the economy, it is the “trend” of the data which is far more important to understand.

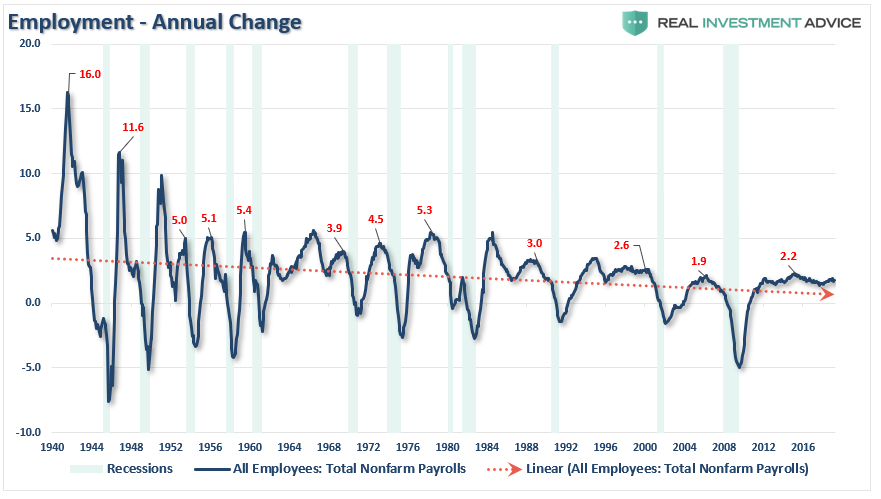

The chart below shows the peak annual rate of change for employment before the onset of a recession. The current annual rate of employment growth is 1.4% which is lower than any previous employment level prior to a recession in history.

But while this is a long-term view of the trend of employment in the U.S., what about right now? The chart below shows employment from 1999 to present.

While the recent employment report was slightly above expectations, the annual rate of growth is slowing. The chart above shows two things. The first is the trend of the household employment survey on an annualized basis. Secondly, while the seasonally-adjusted reported showed 196,000 jobs created, the actual household survey showed a loss of 200,000 jobs.

Many do not like the household survey for a variety of reasons but even if we use the 3-month average of seasonally-adjusted employment we see the same picture. (The 3-month average simply smooths out some of the volatility.)

But here is something else to consider.

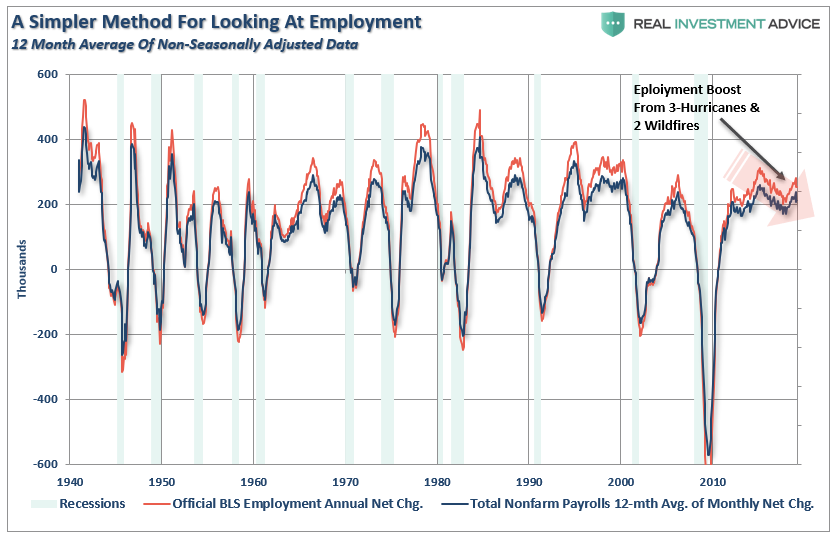

While the BLS continually adjusts and fiddles with the data to mathematically adjust for seasonal variations,the purpose of the entire process is to smooth volatile monthly data into a more normalized trend. The problem, of course, with manipulating data through mathematical adjustments, revisions, and tweaks, is the risk of contamination of bias. A simpler method to use for smoothing volatile monthly data is using a 12-month moving average of the raw data as shown below.

Notice that near peaks of employment cycles the employment data deviates from the 12-month average but tends to reconnect as reality emerges. (Also, note the pickup in employment due to the slate of “natural disasters” in late 2017 which are now fading as reconstruction completes)

Sometimes, “simpler” gives us a better understanding of the data.

Importantly, there is one aspect to all the charts above which remains constant. No matter how you choose to look at the data, peaks in employment growth occur prior to economic contractions rather than an acceleration of growth.

However, there is more to this story.

A Function Of Population

One thing which is never discussed when reporting on employment is the “growth” of the working age population. Each month, new entrants into the population create “demand” through their additional consumption. Employment should increase to accommodate the increased demand from more participants in the economy. Either that or companies resort to automation, off-shoring, etc. to increase rates of production without increases in labor costs. The chart below shows the total increase in employment versus the growth of the working age population.

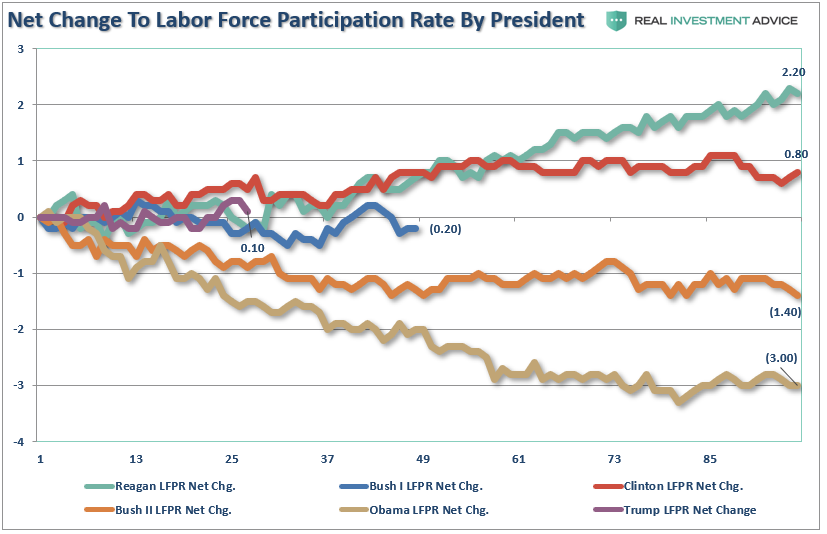

The missing “millions” shown in the chart above is one of the “great mysteries” about one of the longest economic booms in U.S. history. This is particularly a conundrum when the Federal Reserve talks about the economy nearing “full employment.” The Labor Force Participation Rate below shows this great mystery.

Since many conservatives continue to credit President Trump with a booming economy and employment gains, we can look at changes to the labor force participation rate by President as a measure of success. Currently, Trump’s gains are either less than Clinton, the same as Reagan, or tracking Bush Sr.; “spin it” as you will.

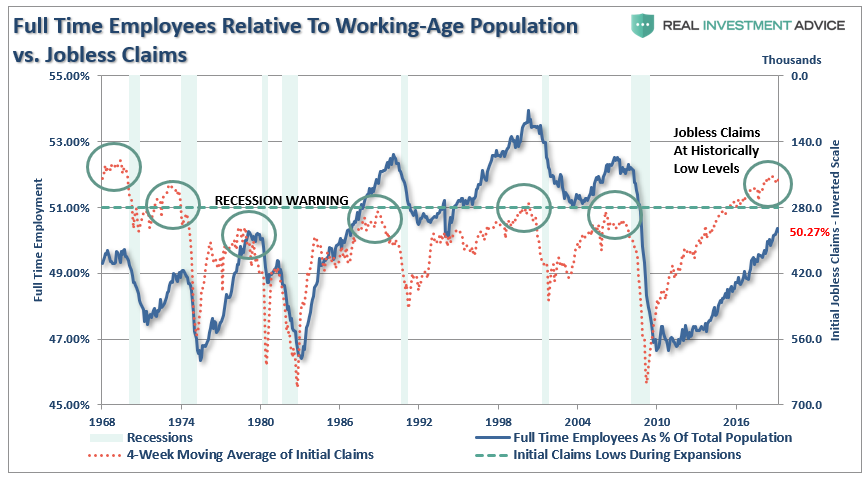

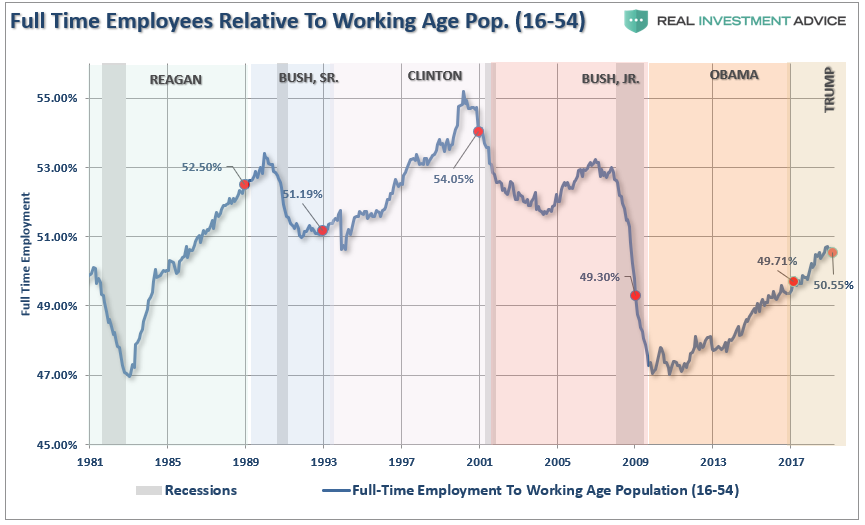

Of course, as we are all very aware, there are many people who are working part-time, going to school, etc. But even when we consider just those working “full-time” jobs, particularly when jobless claims are reaching record lows, the percentage of full-time employees is still well below levels of the last 35 years.

“With jobless claims at historic lows, and the unemployment rate at 4%, then why is full-time employment relative to the working-age population at just 50.27% which is down from 50.5% last month?”

It’s All The Baby Boomers Retiring

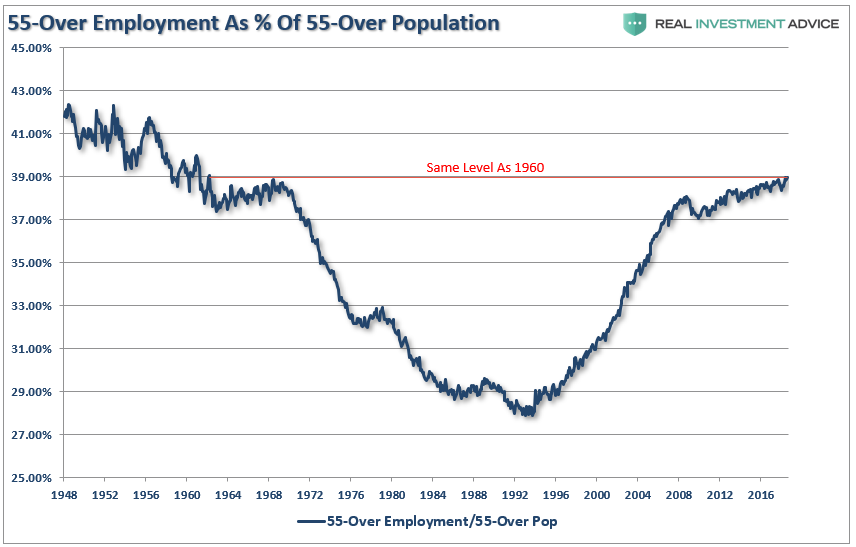

One of the arguments often given for the low labor force participation rate is that millions of “baby boomers” are leaving the workforce for retirement. This argument doesn’t carry much weight given that the “Millennial” generation, which is significantly larger, is simultaneously entering the workforce. The other problem is shown below, there are more individuals over the age of 55, as a percentage of that age group, in the workforce today than in the last 50-years.

Of course, the reason they aren’t retiring is that they can’t. After two massive bear markets, weak economic growth, questionable spending habits,and poor financial planning, more individuals over the age of 55 are still working because they simply can’t “afford” to retire.

However, for argument sake, let’s assume that every worker over the age of 55 retires. If the “retiring” argument is valid, then employment participation rates should soar once that group is removed. The chart below is full-time employment relative to the working-age population of 16-54.

Importantly, note in the first chart above the number of workers over the age of 55 increased last month. However, employment of 16-54 year olds declined from 50.78% to 50.55%. It is also, the lowest rate since 1985, which was the last time employment was increasing from such low levels.

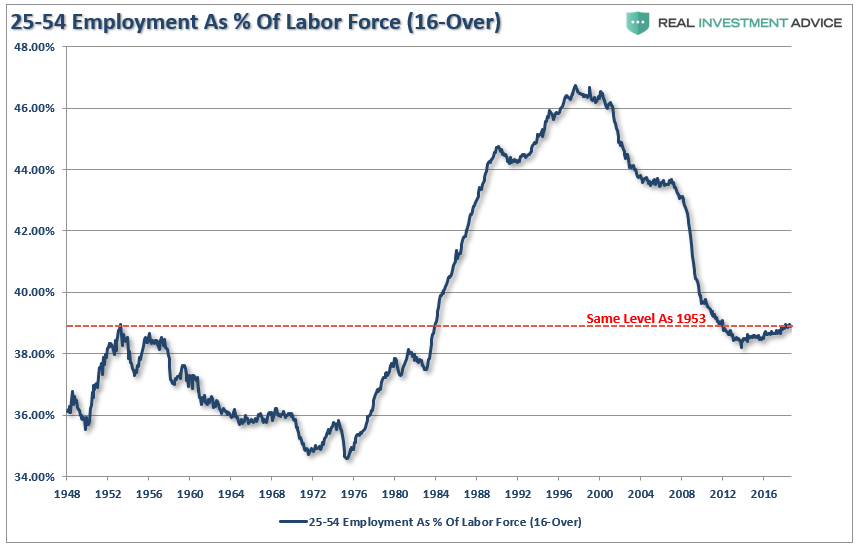

The other argument is that Millennials are going to school longer than before so they aren’t working either.(We have an excuse for everything these days.) The chart below strips out those of college age (16-24) and those over the age of 55. Uhm…

Here is the same chart of employed 25-54 year olds as a percentage of just that group.

When refined down to this level, talk about data mining, we do actually see recovery, however, after the longest economic expansion on record, a record stock market, and record levels of corporate debt to fund expansions and buybacks; employment ratios for this group are at the same level as seen in 1988. Such should raise the question of just how robust the labor market actually is?

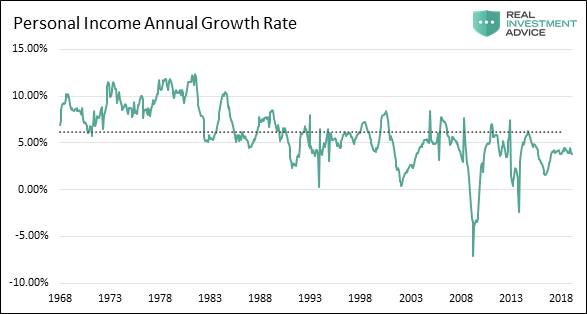

Low initial jobless claims coupled with the historically low unemployment rate are leading many economists to warn of tight labor markets and impending wage inflation. If there is no one to hire, employees have more negotiating leverage according to prevalent theory. While this seems reasonable on its face, further analysis into the employment data suggests these conclusions are not so straightforward.

Strong Labor Statistics

Michael Lebowitz recently pointed out some important considerations in this regard.

“The data certainly suggests that the job market is on fire. While we would like nothing more than to agree, there is other employment data which contradicts that premise.”

For example, if there are indeed very few workers in need of a job, then current workers should have pricing leverage over their employers. This does not seem to be the case as shown in the graph of personal income below.

Furthermore, a closer inspection of the BLS data reveals that, since 2008, 16 million people were reclassified as “leaving the workforce”. To put those 16 million people into context, from 1985 to 2008, a period almost three times longer than the post-crisis recovery, a similar number of people left the workforce.

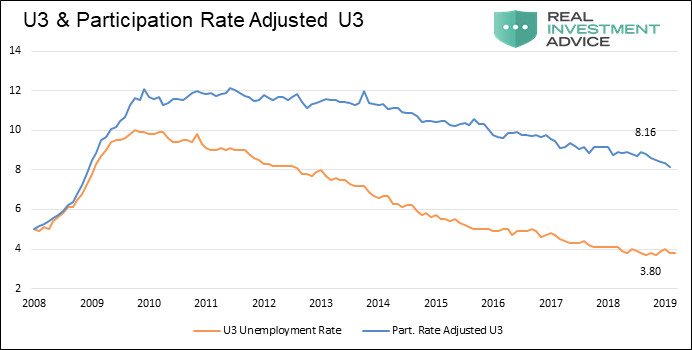

Why are so many people struggling to find a job and terminating their search if, as we are repeatedly told, the labor market is so healthy? To explain the juxtaposition of the low jobless claims number and unemployment rate with the low participation rate and weak wage growth, a calculation of the participation rate adjusted unemployment rate is revealing.

When people stop looking for a job, they are still unemployed, but they are not included in the U-3 unemployment calculation. If we include those who quit looking for work in the data, the employment situation is quite different. The graph below compares the U-3 unemployment rate to one that assumes a constant participation rate from 2008 to today. Contrary to the U-3 unemployment rate of 3.90%, this metric implies an adjusted unemployment rate of 8.69%.

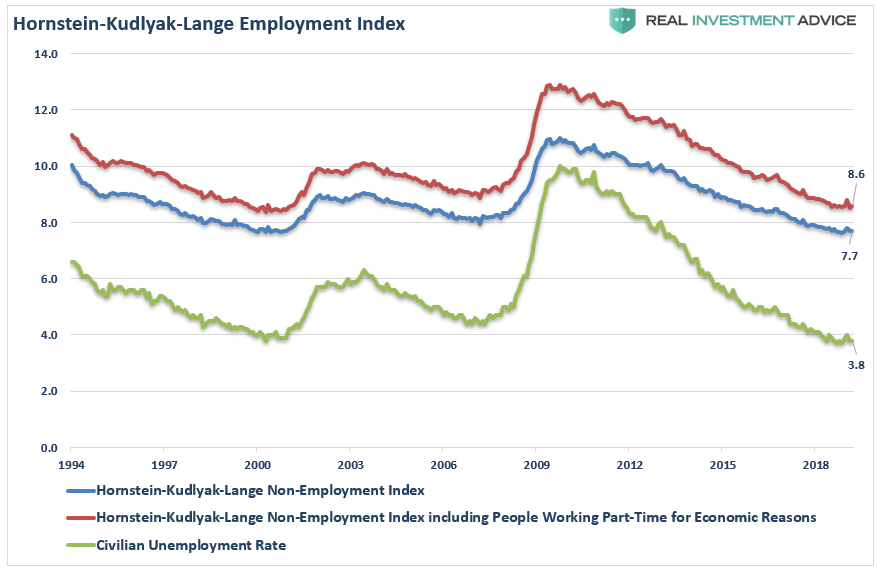

Importantly, this number is much more consistent with the data we have laid out above, supports the reasoning behind lower wage growth, and is further confirmed by the Hornstein-Kudlyak-Lange Employment Index.

(The Hornstein-Kudlyak-Lange Non-Employment Index including People Working Part-Time for Economic Reasons (NEI+PTER) is a weighted average of all non-employed people and people working part-time for economic reasons expressed as the share of the civilian non-institutionalized population 16 years and older. The weights take into account persistent differences in each group’s likelihood of transitioning back into employment. Because the NEI is more comprehensive and includes tailored weights of non-employed individuals, it arguably provides a more accurate reading of labor market conditions than the standard unemployment rate.)

One of the main factors driving the Federal Reserve to raise interest rates and reduce its balance sheet is the perceived low level of unemployment. Simultaneously, multiple comments from Fed officials suggest they are justifiably confused by some of the signals emanating from the jobs data. As we have argued in the past, the current monetary policy experiment has short-circuited the economy’s traditional traffic signals.None of these signals is more important than employment.

As Michael noted:

“Logic and evidence argue that, despite the self-congratulations of central bankers, good wage-paying jobs are not as plentiful as advertised and the embedded risks in the economy are higher. We must consider the effects that these sequences of policy error might have on the economy – one where growth remains anemic and jobs deceptively elusive.

Given that wages translate directly to personal consumption, a reliable interpretation of employment data has never been more important. Oddly enough, it appears as though that interpretation has never been more misleading. If we are correct that employment is weak, then future rate hikes and the planned reduction in the Fed’s balance sheet will begin to reveal this weakness soon.”

As an aside, it is worth noting that in November of 1969 jobless claims stood at 211,000, having risen slightly from the lows recorded earlier that year. Despite the low number of claims, a recession started a month later, and jobless claims would nearly double within six months. This episode serves as a reminder that every recession followed interim lows in jobless claims and the unemployment rate. We are confident that the dynamics leading to the next recession will not be any different.

But then again, maybe the yield-curve is already giving us the answer.

via ZeroHedge News http://bit.ly/2OUaWya Tyler Durden

“It will be definitely a jumbo deal with at least four tranches,” said Sergey Dergachev senior portfolio manager at Union Investment Privatfonds GmbH in Frankfurt. “Demand should be huge.”

Demand for the most highly anticipated sale of the year already totaled $30 billion, Aramco Chairman and Saudi Energy Minister Khalid Al-Falih told Bloomberg TV early on Monday, but it has already rep[ortedly surpassed that.

Dergachev speculated that demand could even surpass the record $53 billion in bids that Qatar received for its $12 billion bond sale last year.

Entering the bond market has forced Aramco to open its books after decades of speculation about its earnings and production. The company got the fifth-highest investment-grade ratings at both Moody’s Investors Service and Fitch Ratings, matching Saudi Arabia’s sovereign grade.

Bloomberg reports that the oil giant is offering six-tranche debt, according to the people familiar with the matter, who asked not to be identified. The world’s most profitable company is tapping the market ahead of a planned $69 billion acquisition.

Initial Price Thoughts:

USD 3Y Fixed — T+75 area

USD 3Y Floating Rate Notes — Libor + equivalent

USD 5Y Fixed — T+95 area

USD 10Y Fixed — T+125 area

USD 20Y Fixed — T+160 area

USD 30Y Fixed — T+175 area

Aramco may raise about $10 billion from the sale, the kingdom’s energy minister said in January, as Saudi Arabia combines the oil producer with chemical maker Saudi Basic Industries Corp.

The deal is expected to price tomorrow, so we would not be surprised to see leakage higher in Treasury yields on rate-locks and rotation.

via ZeroHedge News http://bit.ly/2uRQq8f Tyler Durden

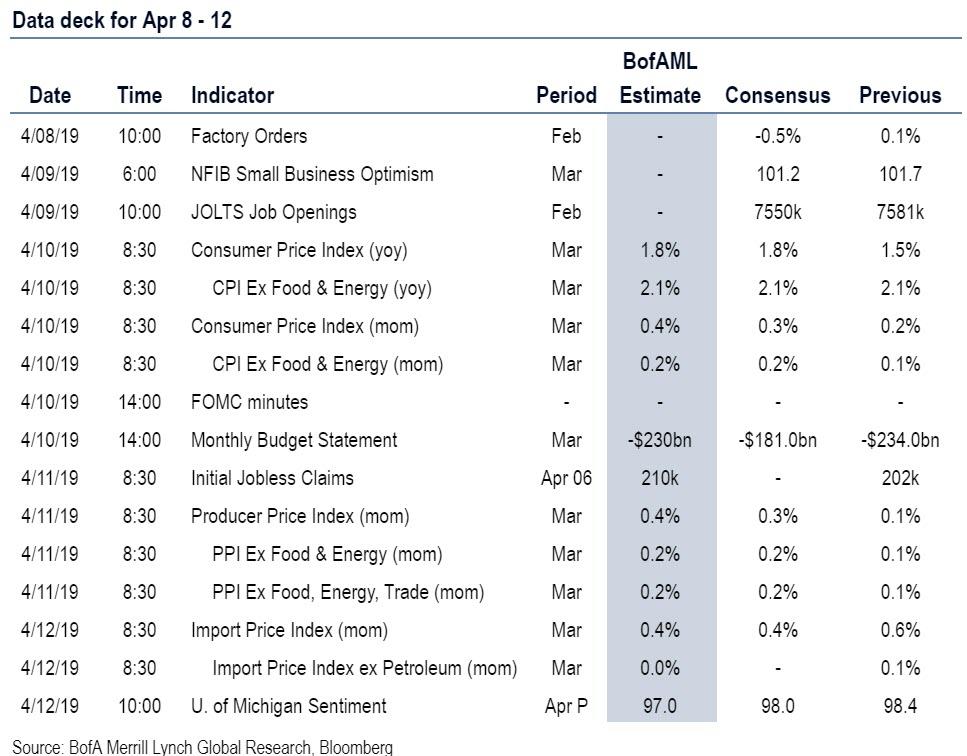

While the week starts off slowly, traders will look forward to a “Super Wednesday” with the EU emergency Brexit summit, ECB meeting, US CPI report and FOMC minutes all slated for that day. According to DB’s Craig Nicol, “that should be the highlight of the week ahead however we’ve also got a busy week for data out of China, as well as a number of scheduled Fed speakers, the annual IMF and World Bank Spring Meetings and China-EU Summit. If that wasn’t enough, US banks also kick off earnings season next week.”

Starting with Brexit, the latest in the neverending divorce saga is the UK seeking an extension of the Brexit deadline until June 30, with a further headline suggesting that PM May is aiming to ratify the divorce deal before May 23. The PM’s letter also announced that the UK will hold European Parliamentary elections on May 23 if a deal hasn’t been ratified by then. So markets will now await the EU response with an emergency Summit scheduled for next Wednesday. PM May will reportedly not bring any Brexit plan to a vote before the Summit which means the EU will need to come to a unanimous agreement that a clear plan on a way forward is being proposed, to allow the EU to come to a common position and offer the extension.

For the ECB, after markets were left puzzled by the messaging from the previous meeting and with the subsequent moves in bond markets which has seen Bunds turn negative again, expect there to be plenty of questions directed at Draghi both on the TLTRO details and also the impact of negative rates. Newsflow on tiering has picked up in recent days including an acknowledgement in the latest meeting minutes, with the latest report suggesting that the tiering trial balloon was not quite as successful and the ECB may hold off on announcing details. So markets will particularly be looking for clues as to where the internal debate on persistent low rates on bank margins and profitability now lies.

Shortly after the ECB on Wednesday we’ll get the March CPI report in the US. The consensus is for a +0.2% mom core reading which would be enough to hold the annual rate at a relatively solid +2.1% yoy. In the evening we then get the FOMC minutes from the March meeting. A reminder that the message from this meeting was undeniably dovish. The median dot moved to no rate hikes this year with seven officials also seeing the Fed on hold at least through the end of 2020. Deutsche Bank economists made the point that it is clear that the Committee no longer has a strong tightening bias and patience remains the order of the day for some time. With that in mind, expect the minutes to reiterate this more dovish tone, with readers also likely to look out for hints on the composition and duration of the balance sheet.

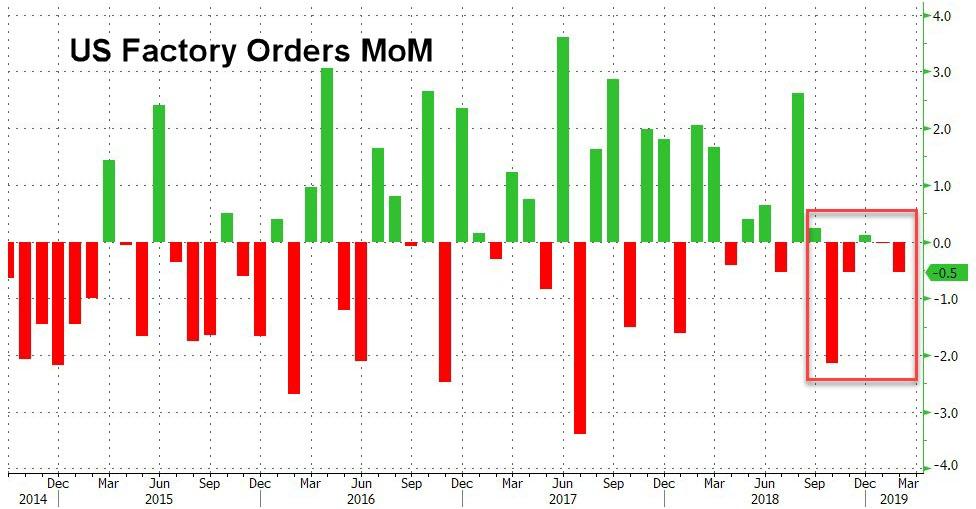

Elsewhere, as well as the CPI report in the US next week we’ll also get the March PPI report on Thursday. Outside of that it’s fairly light for data in the US though with only final February factory, durable and capital goods orders due on Monday, the March monthly budget statement on Wednesday, claims on Thursday and the preliminary April University of Michigan consumer sentiment survey on Friday worth flagging.

In Europe expect there to be some focus on the February industrial production reports next week with data due for the UK and France on Wednesday and the Euro Area on Friday. We’ll also get the February GDP reading for the UK on Wednesday while Thursday will see final March CPI revisions made in Germany and France. Meanwhile in Asia it’s a busy week for data out of China with March foreign reserves due on Sunday, March CPI and PPI due on Thursday and March trade data due on Friday. We’re also expecting to get the latest money and credit aggregates data covering March at some stage next week.

As for the Fedspeak, we got confirmation that Chair Powell is to address the House Democratic Retreat which takes place over three days from Wednesday to Friday next week. Other speakers include Clarida late on Tuesday, and Clarida again on Thursday along with Bullard, Quarles, Kashkari and Bowman – all at separate events.

At a more micro level next week will also see an early drip feed of Q1 earnings in the US including the banks with both JP Morgan and Wells Fargo due to report on Friday. The quarter is expected to be a dud, with consensus now expecting a sharp drop in EPS growth, the first decline since 2016.

Finally, other things to potentially watch out for next week include China Premier Li Keqiang travelling to Brussels for the five day China-EU Summit on Monday, the annual week long Spring Meetings of the World Bank/IMF also kicking off Monday, Israel’s general election on Tuesday, the IMF’s latest World Economic Outlook update on Tuesday, the US Congressional Committee holding a hearing on Wednesday with the chiefs of the biggest US banks on “Holding Megabanks Accountable”, the OPEC monthly oil market report on Wednesday, South Korea President Moon Jae-in meeting President Trump on Thursday, and India heading to the polls on Thursday (albeit voting in phases with results in late May).

Summary of key events by day, courtesy of Deutsche Bank

Monday: A fairly light day for data, with March consumer confidence due in Japan overnight followed by February trade data in Germany, March industry sentiment data in France and the Sentix investor confidence reading for the Euro Area. In the US we’ll get February factory orders and final durable and capital goods orders revisions. Elsewhere, the BoJ’s Kuroda and ECB’s Villeroy are due to speak, while China Premier Li Keqiang is due to travel to Brussels for the China-EU Summit. The annual IMF/World Bank Spring Meetings also kick off.

Tuesday: A very quiet day for data releases with the UK’s March BRC sales data, and March NFIB small business optimism print and February JOLTS report in the US the only releases of note. The Fed’s Clarida speaks in the evening while the IMF’s latest World Economic Outlook update is due.

Wednesday: The big highlight is the ECB meeting in the early afternoon followed by Draghi’s press conference. Not long after that we’ll also get the March CPI report in the US. Also high on the agenda will be the emergency EU Brexit Summit. Other data releases of note include February industrial production prints in France and the UK, as well as the February GDP reading in the latter. The March monthly budget statement is also due in the US along with the latest FOMC meeting minutes. The OPEC monthly oil report is due while the US Congressional Committee is due to hold a hearing with chiefs of the biggest US banks on “Holding Megabanks Accountable”.

Thursday: Inflation releases should be the main focus with March CPI/PPI in China, final March CPI revisions in Germany and France and the March PPI report in the US all due. The latest initial jobless claims reading in the US will also be out. It’s also a busy day for Fedspeak with Clarida, Bullard, Quarles, Kashkari and Bowman all due to speak. Meanwhile, South Korea President Moon Jae-in will meet with President Trump. India will also go to the polls.

Friday: Another quiet day for data with the February industrial production report for the Euro Area, and March import price index and preliminary University of Michigan consumer sentiment readings in the US due. March trade data in China is also likely to be out at some stage. Away from that the BoE’s Carney is due to speak at the IMF/World Bank Spring Meetings.

Looking at just the US, Goldman writes that the key economic data releases this week are the CPI report on Wednesday and the PPI report on Thursday. In addition, minutes from the March FOMC meeting will be released on Wednesday. There are several scheduled speaking engagements by Fed officials this week, including two by Vice Chairman Richard Clarida on Tuesday and Thursday.

Monday, April 8

10:00 AM Factory Orders, February (GS -0.5%, consensus -0.5%, last +0.1%); Durable goods orders, February final (last -1.6%); Durable goods orders ex-transportation, February final (last +0.1%); Core capital goods orders, February final (last -0.1%); Core capital goods shipments, February final (last flat): We estimate factory orders decreased 0.5% in February following a 0.1% increase in January. Durable goods orders declined in the February advance report, driven primarily by a decline in aircraft orders.

Tuesday, April 9

06:00 AM NFIB small business optimism, March (consensus 101.2, last 101.7)

10:00 AM JOLTS Job Openings, February (consensus 7,550 last 7,581k)

6:45 PM Fed Vice Chairman Clarida (FOMC voter) speaks: Fed Vice Chairman Richard Clarida will speak at a Fed Listens event to discuss the review of the monetary policy framework at the Minneapolis Fed.

Wednesday, April 10

08:30 AM CPI (mom), March (GS +0.35%, consensus +0.3%, last +0.2%); Core CPI (mom), March (GS +0.13%, consensus +0.2%, last +0.1%); CPI (yoy), March (GS +1.82%, consensus +1.8%, last +1.5%); Core CPI (yoy), March (GS +2.03%, consensus +2.1%, last +2.1%): We estimate a 0.13% increase in March core CPI (mom sa), which would lower the year-over-year rate by a tenth to +2.0%. Our forecast reflects an expected drag from residual seasonality in the apparel category from methodological changes. We also expect softness in the used cars and lodging away from home categories. On the positive side, we expect a relatively stable pace of monthly shelter inflation, as alternative rent measures have picked back up, apartment completions have peaked, and aggregate vacancy rates remain low. Rebounding oil prices could also boost airfares in the upcoming report. We look for a 0.35% increase in headline CPI (mom sa), reflecting a boost from higher gasoline prices.

2:00 PM Minutes from the March 19-20 FOMC meeting: At its March meeting, the FOMC left the target range for the policy rate unchanged at 2.25-2.50%, as widely expected. The median dot in the Summary of Economic Projections showed a 0-1 baseline for rate hikes in 2019-2020, compared to 2-1 in December, and the average dots declined significantly. The FOMC also announced that portfolio runoff will stop at the end of September and that the pace of Treasury runoff will be tapered in the interim. In the minutes, we will look for further discussion of inflation, the path of the policy rate, the review of the monetary policy framework, and balance sheet normalization.

Thursday, April 11

08:30 AM PPI final demand, March (GS +0.4%, consensus +0.3%, last +0.1%); PPI ex-food and energy, March (GS +0.2%, consensus +0.2%, last +0.1%); PPI ex-food, energy, and trade, March (GS +0.2%, consensus + 0.2%, last +0.1%): We estimate a 0.4% increase in headline PPI in February, reflecting relatively firm core prices and energy prices. We expect a 0.2% increase in the core measure excluding food and energy, and also a 0.2% increase in the core measure excluding food, energy, and trade.

08:30 AM Initial jobless claims, week ended April 6 (GS 210k, consensus 210k, last 202k); Continuing jobless claims, week ended March 30 (last 1,717k): We estimate jobless claims increased by 8k to 210k in the week ended April 6, following a 10k decline in the prior week.

09:30 AM Fed Vice Chairman Clarida (FOMC voter) speaks: Fed Vice Chairman Richard Clarida will speak with Institute of International Finance President Tim Adams at a policy summit in Washington.

09:40 AM St. Louis Fed President James Bullard (FOMC voter) speaks: St. Louis Fed President James Bullard will discuss the US economy and monetary policy in Tupelo, Mississippi. Prepared text and audience and media Q&A are expected.

Friday, April 12

08:30 AM Import price index, March (consensus +0.4%, last +0.6%)

10:00 AM University of Michigan consumer sentiment, April preliminary (GS 97.0, consensus 98.0, last 98.4): We expect the University of Michigan consumer sentiment index to decrease by 1.4pt to 97.0. The measure appears elevated compared to similar measures such as the Conference Board consumer confidence index.

Source: Deutsche Bank, Goldman, BofA

via ZeroHedge News http://bit.ly/2VvrHCr Tyler Durden

A Russian-born academic accused of being a Kremlin operative claims she was “used” to smear former National Security Adviser Michael Flynn over an unplanned contact they had at a 2014 dinner at the University of Cambridge, England when Flynn was the Director of the Defense Intelligence Agency under President Obama.

38-year-old Svetlana Lokhova met Flynn at the February 2014 Cambridge dinner organized by Sir Richard Dearlove – a former head of MI6 who was launching an organization called the Cambridge Security Initiative, according to the BBC. Also part of the organizing group was alleged American spy Stefan Halper, a longtime spook and then-Cambridge professor emeritus widely reported to have infiltrated the Trump campaign and spied on several aides during the 2016 US election.

Svetlana Lokhova

“General Flynn was the guest of honor and he sat on one side of the table in the middle. I sat on the opposite side of the table to Flynn next to Richard Dearlove because I was the only woman at dinner, and it’s a British custom that the only woman gets to sit next to the host,” Lokhova told Fox News, who added that she has never been alone with Flynn.

As an expert on Soviet intelligence in the 1930s, Lokhova says she was asked to present some of her research. “The idea was that I would impress the DIA with the Cambridge pedigree of research.”

Lokhova showed Flynn a 1912 postcard from Stalin to the fiancee of his best friend. The fiancee was helping Stalin obtain a fake passport to escape surveillance when he was an early revolutionary working against the Tsarist regime.

…

She says Flynn asked her to send the document to him. This was because he was expecting some senior officials visiting Washington from Russia. At this point, there was a move towards trying to increase co-operation with Russia in the field of counter-terrorism, as it had recently emerged that those involved in the 2013 Boston bombing had been known to the Russians.

Lokhova says both Flynn and his assistant provided their emails, looking forward to using the postcard to break the ice when the Russian officials arrived in Washington. –BBC

Lokhova’s contact with Flynn at the dinner was used in several 2017 media reports to suggest that he had been “gotten to” by the Russians, while pundits and social media commentators suggested she was a Kremlin “honeypot.”

Hi @MalcolmNance@MSNBC, I have not forgotten how you told American people and the world a whole packs of lies about me based on your racist and sexist views. The tide has turned. https://t.co/iZnkX9Hqb6

I’m not a Russian spy and I have never worked for the Russian government,” said Lokhova, adding “I believe that General Flynn was targeted and I was used to do it.”

Of note, Halper – the ex-son-in-law of former CIA Director Ray Cline, was paid over $1 million by the Obama Defense Department between 2012 and 2018, with nearly half of it surrounding the 2016 US election.

Michael Flynn is pictured at a 2014 dinner at the University of Cambridge. (Courtesy of Svetlana Lokhova)

In December, 2016 – weeks after President Trump won the US election, event organizers Dearlove and Halper suddenly resigned from their positions at the Cambridge Intelligence Seminar (CIS) – an academic forum on the Western Spy World – due to what Halper called “unacceptable Russian influence” on the group.

According to journalist Sara Carter, however, Halper is steeped in Kremlin contacts.

Ironically, documents obtained by SaraACarter.com suggest that Halper also had invited senior Russian intelligence officials to co-teach his course on several occasions and, according to news reports, also accepted money to finance the course from a top Russian oligarch with ties to Putin.

Several course syllabi from 2012 and 2015 obtained by this outlet reveal Halper had invited and co-taught his course on intelligence with the former Director of Russian Intelligence Gen. Vladimir I. Trubnikov.

…

Even more interesting are reports from the British Media outlet, The Financial Times, that state Halper received funds for the Cambridge seminar from Russian billionaire Andrey Cheglakov, who has close ties to Russian President Vladimir Putin. –Sara A. Carter

Stefan Halper

On Sunday, Lokhova took to Twitter for a massive thread to slam Washington Post journalists David Ignatius and Tom Hamburger for what she said was covering up for “Halper’s mess.”

Remember, you must not never ever under any circumstances whatsoever called a spy on Trump campaign Halper, ‘a spy on Trump campaign’. Washington Post wants you to refer to Halper as ‘the FBI source who assisted the Russia investigation’ Got it? (4)

I never heard of Ignatius. But some reason my university professor, who I now understand is a friend of Ignatius, gave him my personal email address. Which was very nice as I have given birth few weeks earlier and still recovering from a shock of the WSJ attack (6)

I never heard of Ignatius. But some reason my university professor, who I now understand is a friend of Ignatius, gave him my personal email address. Which was very nice as I have given birth few weeks earlier and still recovering from a shock of the WSJ attack (6)

Ignatius responded he understood. And nothing was published, because as he told me later, he interviewed witnesses at the ‘Flynn dinner’ and found nothing (10).

Roll forward May 2018, and Halper is exposed as FBI operative. Ignatius writes ‘I’d like very much to ask you about Halper’. We spoke, & I caught him off-guard with a direct question: did he know he was a spy? To which he said ‘I always found him very reliable’, then hung up(12)

Hamburger tries to interrogate me AGAIN over the Flynn dinner. I refer him to Ignatius. Then he tries the Kremlin penetration of the Cambridge Seminar line. I read him out Halper resignation email proving that Halper did not tell the truth (14)

I told Hamburger (&have it time-stamped): ‘You reveal you have not had contact with Dearlove. So if the principals in the story have not confirmed their knowledge/statements personally, then the journalists do not have evidence, but only hearsay, and this should be stressed. (16

I also confirmed that Gen Flynn DIA liaison Dan O’Brien had been on the record with WaPo to confirm he left 2014 dinner with Flynn and nothing happened. Now let’s turn to what Hamburger wrote (18)

I’ve previously made numerous complaints to the WaPo and have been ignored. So now I call on the @washingtonpost to retract the story by Tom Hamburger and print everything they know about the #Russiagate hoax. (22)

Separately, there has to be a public inquiry into the alarming links between WaPo reporters and those with access to Classified Information. (23). THE END

In the aftermath of last weekend’s local elections in Turkey, which saw Erdogan’s ruling AKP party lose control of Turkey’s two main cities, Ankara and Istanbul, on Monday President Erdogan demanded that the country’s election board investigate “widespread irregularities” in local elections in Istanbul, where a partial recount is already underway after the ruling party contested its defeat, sending the lira tumbling to the lowest level since March 25.

“There is stealing from the boxes,” Erdogan said, adding that “we’re applying to the YSK against that organized intervention at the ballot box,” referring to the High Election Board. In the U.S. “they renew elections when there is a one percentage point difference,” the president said in what appeared to signal a push for a new election in the city.

“Given the huge economic challenges facing Turkey, this is the last thing Turkey needs at this stage,” said Tim Ash, senior strategist at BlueBay Asset Management LLP in London, said by email.

As we reported at the time, the March 31 municipal vote ended a quarter century of rule by Erdogan’s movement in Ankara, the capital. But it was the defeat in Istanbul that has galvanized his ruling AK Party into refuting the preliminary results. As a reminder, the AK Party and its predecessors have been holding Istanbul since Erdogan won the mayor’s office in 1994, and a defeat there would hinder social policies that rally the support of poorer citizens.

“No one has the right to claim victory in Istanbul with just a 13,000 to 14,000 vote difference,” Erdogan said, referring to the gap between the candidate of the opposition CHP, who was initially declared winner, and the AKP’s pick for mayor.

Erdogan’s party has already sought the cancellation of voting in Istanbul’s Buyukcekmece district and applied to the election board for a recount of all votes in the remaining 38 districts across the country’s largest city of 16 million people.

The news that Erdogan would challenge the Istanbul vote, adding to the country’s political instability, sent the lira sliding, with negative FX sentiment boosted when the Turkish central bank cut the interest rates it offers on lira leg of FX swaps with commercial lenders to 24% from 25.5%; in doing so it revered an increase in rate to 25.5% from 24% on March 25, when it ceased to offer any funding to commercial banks through its one- week repo facility

In addition to the slide in the lira, Turkish bonds and stocks also fell on Monday: yields on 10-year local-currency bonds jumped 21 basis points to 17.49%, the highest in a week, while five-year CDS climbed above 400 bps. In equities, the Borsa Istanbul benchmark stock index dropped 1.8% the first retreat in four days, after gaining 5.3% last week.

via ZeroHedge News http://bit.ly/2I4phaL Tyler Durden

This spring has seen a spike in families fleeing Central America and flocking to the U.S. border seeking asylum. Contrary to President Donald Trump’s claims, this isn’t a crisis. But the situation is straining the resources of frontline border agencies that are running out of space to process and house these migrants, partly because the president has been wasting resources on a useless wall rather than hiring judges and personnel for quick processsing.

This spring has seen a spike in families fleeing Central America and flocking to the U.S. border seeking asylum. Contrary to President Donald Trump’s claims, this isn’t a crisis. But the situation is straining the resources of frontline border agencies that are running out of space to process and house these migrants, partly because the president has been wasting resources on a useless wall rather than hiring judges and personnel for quick processsing.

An impossible job? Kirstjen Nielsen

An impossible job? Kirstjen Nielsen

{kind=link}

{kind=link}

{kind=link}

{kind=link}