North Korea Says “Will Not Offer Anything For Trump To Brag About” Without Receiving In Return

Reuters has quoted Korean Central News Agency (KCNA) on Monday as saying North Korea has zero interest in giving President Trump future meetings to brag about unless it receives something in return.

N.KOREA SAYS WILL NOT OFFER ANYTHING FOR US PRESIDENT TRUMP TO BRAG ABOUT – KCNA

N.KOREA SAYS URGES US TO DROP HOSTILE POLICY AGAINST IT IF IT WANTS TO CONTINUE DIALOGUE – KCNA

Statements from KCNA were made via Foreign Ministry adviser Kim Kye Gwan, who has recently called for US concessions ahead of a December deadline set by Kim Jong Un for President Trump to provide favorable terms to restore nuclear talks.

Gwan said North Korea wasn’t interested in a summit with the US and called any future talks with the Trump administration “useless.”

“If the US does not really want to let go of its dialogue with us, it should make a decision to withdraw its hostile policy of viewing us as an enemy,” the KCNA statement said.

Gwan’s statements came after the Trump administration canceled joint military exercises with South Korea. President Trump tweeted that Kim Jong Un needs to “act quickly, get the deal done” and suggested a summit could be nearing, saying, “See you soon!”

Gwan said, “Although (North Korea and the US) held three summits and other meetings since June last year, there hasn’t been much improvement in relations, and the US has been just trying to buy time to its favor.”

“We are no longer interested in such meetings that provide us no benefit,” he added.

Negotiations have collapsed since a February summit between both countries in Vietnam after the US rejected North Korean demands for sanction relief for partial abandonment of its nuclear weapons.

It seems that Kim understands ahead of an election year, President Trump will want to showboat any progress made on the Korean Peninsula, even though it might not be beneficial for both countries in the long run.

JPMorgan Asset Management ‘Outs’ Jeff Gundlach As The King Of The Armageddonists

As bearish-biased analysts, strategists, and investors throw in the towel amid the market’s incessant FOMO-driven melt-up in the face of record global policy uncertainty, declining earnings, and a global economy showing anything but ‘troughing’; it seems JPMorgan’s Asset Management group has decided now is the time to name names and call out the last decade’s so-called “Armageddonists”…

Authored by Michael Cembalest, CIO JPMorgan Private Bank,

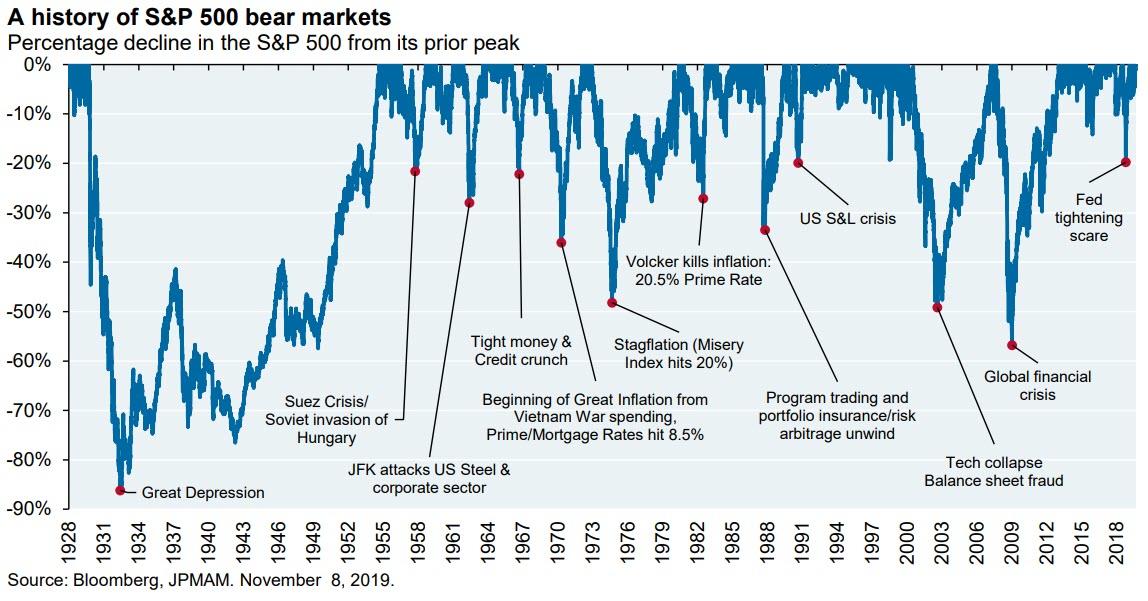

While recessions and bear markets are a fact of life, something peculiar happened after the Global Financial Crisis: the rise of the Armageddonists, which refers to the market-watchers, forecasters and money managers whose apocalyptic comments spread like wildfire in print and online financial news. I understand why: by 2010, investors had experienced two consecutive bear markets, each with equity declines of over 40%. It took several years for equity markets to recover each time, unlike the shallower, faster-recovering bear markets of the 1960’s and 1980’s. The dismal performance of consecutive 2001/2008 bear markets hadn’t been seen in decades, and is only comparable to parts of the Great Depression.

I also understand that mega-bearish news appeals to human negativity bias, a topic examined by Nobel Prize winner Daniel Kahneman in his 2011 book on the brain and human survival instincts, by political scientist Stuart Soroka who has illustrated the inverse relationship between magazine sales and the positivity of a magazine’s cover, and in a 2014 experiment in which a city newspaper lost two thirds of its readers on a day when it deliberately only published positive news. That said, what are the consequences for investors that reacted to dire Armageddonist predictions which have flooded the airwaves and internet since 2010?

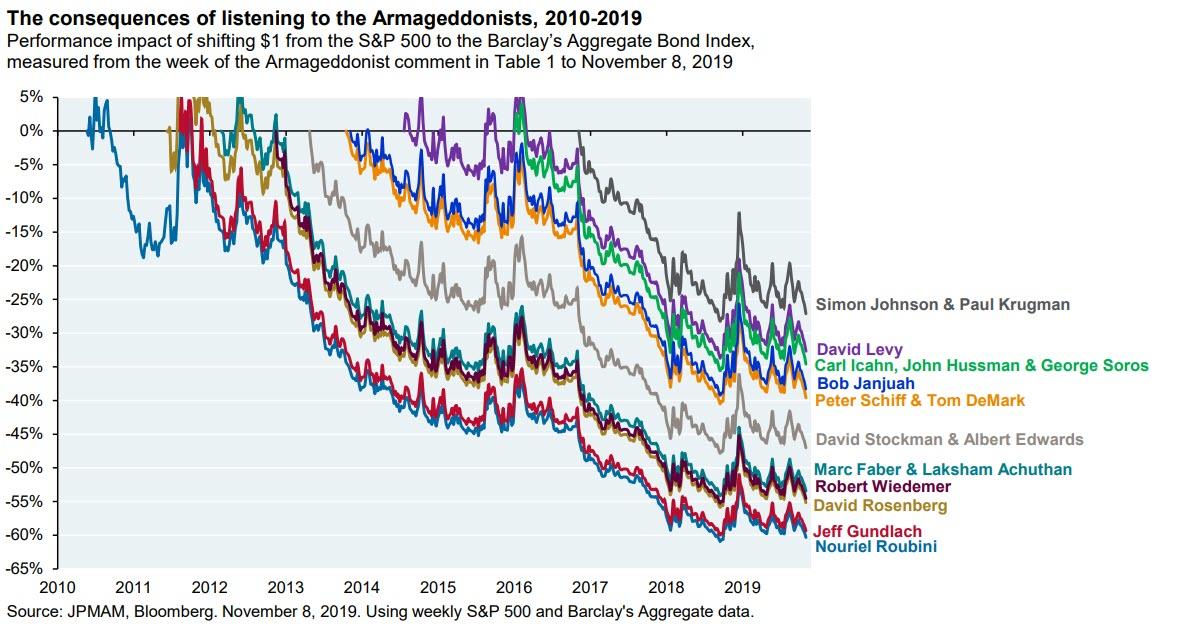

We pulled together comments made by well known Armageddonists since 2010, a few of whom are on record as having anticipated the prior bear market and recession.

We measured the impact on an investor deciding to shift a dollar from equities to diversified government, mortgage-backed and corporate bonds after reading the post-2010 comments. To be clear, this isn’t about whether the Armageddonist at some point became more optimistic. This chart is about the opportunity loss for investors that acted upon seeing their comments at the time. One example: $1 shifted from equities to bonds in 2014 in response to mega-bearish commentary would have underperformed equities by around 40% as the S&P 500, propelled more by earnings growth than by multiple expansion, rolled on.

[ZH: It seems DoubleLine’s Jeff Gundlach shares the dubious award for ‘worst’ Armageddonist, with none other than Dr.Doom – Nouriel Roubini]

One day, of course, Armageddonists will be rewarded with a recession.

Partly as a consequence of the China-US Trade War, equity outperformance vs bonds reached a peak in early 2018 and has been treading water since; CEO Confidence has plunged to its lowest level since the financial crisis; the US is now in an earnings recession; and 67% of respondents to the Duke CFO Survey believe the US will be in recession by the end of 2020 (despite all of this, institutional investor positioning in equity futures is close to its highest/most bullish level since 2007). I believe that the health of the US consumer, strong labor and housing markets and a modest rebound in manufacturing will prevent a recession from happening in 2020, but I could be wrong. In any case, for investors that reacted to Armageddonist comments, the larger issue is this: the next recession and bear market will have to be quite severe to earn back what was sacrificed along the way. Using rough math, a sustained, multi-year bear market with 35%-45% declines from peak levels would be needed to reverse many of the opportunity losses shown in the chart above.

How severe will the next bear market be?

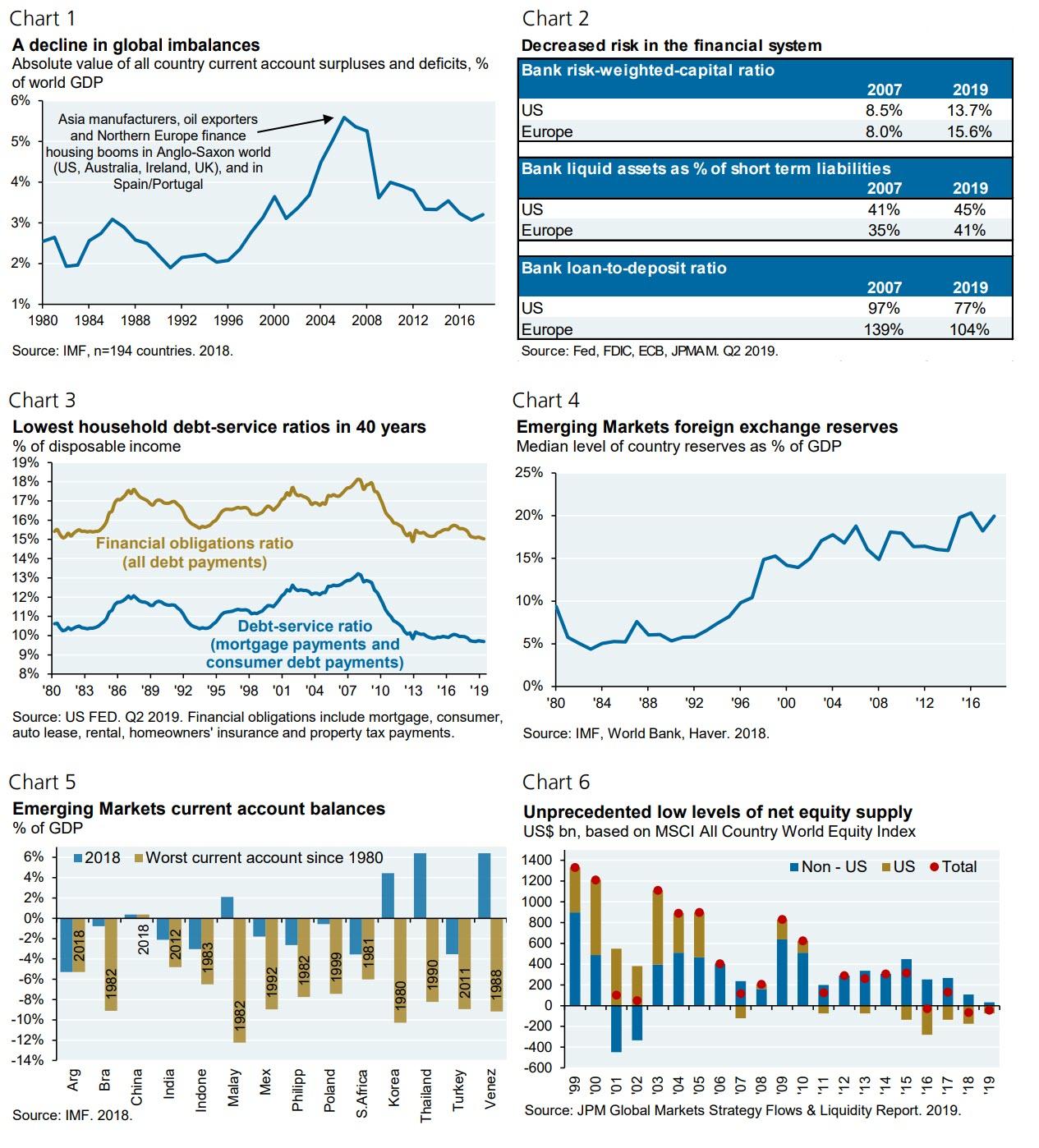

I believe it won’t be as bad as the prior two, due to the following:

a reduction in global economic imbalances,

higher levels of capital and decreased funding risks in US and European banks,

stronger balance sheet fundamentals of US households,

reduced risk in most Emerging Markets due to higher levels of foreign exchange reserves and less reliance on foreign capital,

and the low level of new US equity supply since buybacks and M&A have exceeded new equity issuance for the last five years.

What are the mega-bearish counterpoints?

US equity valuations are well above median, underwriting standards in the leveraged loan market have declined to disturbing levels, and deficits are financing a large part of US growth this late in the cycle. And, as discussed in our October Eye on the Market, there could be a seismic shift in Washington in 2020 that imposes substantial taxes, bans on share repurchases and regulatory costs on tech, energy, healthcare, financials, biotech, wireless, chemicals and more. Too soon to assess in terms of probabilities, but chances of a fundamental re-ordering of the US economy are rising.

All things considered, I think the next recession and bear market will not be as severe or long-lasting as the worst ones shown above. If that’s the case, it would ratify the approach of money managers that maintained normal exposures to risky assets in diversified portfolios since 2010, even as the business cycle aged and apocalyptic commentary swirled around them.

* * *

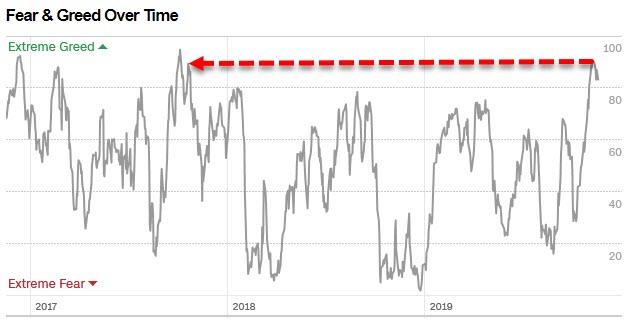

Having said all that, who could have seen this coming?

Source: Bloomberg

Of course, we suspect the fact that Michael Cembalest has decided to issue this report, “outing” the Armageddonists, will only fuel the calls for a top in complacency… just remember if greed is good, extreme greed must be awesome for everyone…

South Dakota has employed a very unique advertising strategy to combat meth use in the state. The slogan for the state’s new anti-drug campaign is “Meth. We’re on it.”

In announcing the campaign, Gov. Kristi Noem (R) wrote that last year, 13 South Dakotans lost their lives because of methamphetamines and 3,366 were arrested on related offenses. To curb usage, Noem announced on Monday the state’s “largest and most aggressive” campaign yet.

As with many aspects of our seemingly endless drug war, South Dakota’s campaign has good intentions. But it’s not the intention that has people talking.

“Meth. We’re on it,” reads the campaign’s logo in big, bold lettering that are plastered over an outline of the state. If that wasn’t enough to grab attention, the campaign and its logo can be viewed at the website onmeth.com.

A company called Broadhead LLC received $448,914 to design the campaign. The state is now running ads and posters featuring a diverse group of South Dakotans saying, “I’m on meth.”

Whether the state succeeds in reducing meth use and helping people who want to quit do so, they’ve already succeeded in “raising awareness.”

South Dakota has launched a campaign to combat meth.

According to Facebook, this campaign is a refresh of the state’s “Meth Changes Everything” marketing strategy.

The new campaign directs people to a tipline where residents can report suspected drug activity to the state attorney general. It also includes classroom resources reminiscent of a certain other anti-drug campaign aimed at young people.

But lest this seem only like a hilarious way to lock more people up, the campaign also includes funding for substance abuse treatment facilities and a confidential locator for connecting with those facilities. South Dakotans can also receive financial assistance for treatment.

Reason has reached out to the South Dakota Department of Social Services for comment on the campaign, the treatment facilities, and literally anything about this campaign other than the insane slogan that is currently breaking the internet. The story will be updated with comment.

from Latest – Reason.com https://ift.tt/2qgkmfO

via IFTTT

South Dakota has employed a very unique advertising strategy to combat meth use in the state. The slogan for the state’s new anti-drug campaign is “Meth. We’re on it.”

In announcing the campaign, Gov. Kristi Noem (R) wrote that last year, 13 South Dakotans lost their lives because of methamphetamines and 3,366 were arrested on related offenses. To curb usage, Noem announced on Monday the state’s “largest and most aggressive” campaign yet.

As with many aspects of our seemingly endless drug war, South Dakota’s campaign has good intentions. But it’s not the intention that has people talking.

“Meth. We’re on it,” reads the campaign’s logo in big, bold lettering that are plastered over an outline of the state. If that wasn’t enough to grab attention, the campaign and its logo can be viewed at the website onmeth.com.

A company called Broadhead LLC received $448,914 to design the campaign. The state is now running ads and posters featuring a diverse group of South Dakotans saying, “I’m on meth.”

Whether the state succeeds in reducing meth use and helping people who want to quit do so, they’ve already succeeded in “raising awareness.”

South Dakota has launched a campaign to combat meth.

According to Facebook, this campaign is a refresh of the state’s “Meth Changes Everything” marketing strategy.

The new campaign directs people to a tipline where residents can report suspected drug activity to the state attorney general. It also includes classroom resources reminiscent of a certain other anti-drug campaign aimed at young people.

But lest this seem only like a hilarious way to lock more people up, the campaign also includes funding for substance abuse treatment facilities and a confidential locator for connecting with those facilities. South Dakotans can also receive financial assistance for treatment.

Reason has reached out to the South Dakota Department of Social Services for comment on the campaign, the treatment facilities, and literally anything about this campaign other than the insane slogan that is currently breaking the internet. The story will be updated with comment.

from Latest – Reason.com https://ift.tt/2qgkmfO

via IFTTT

‘The Horowitz Report Is Coming, The Horowitz Report Is Coming’ – Lindsay Graham Signals Early Dec. Release

For over a year, Department of Justice Inspector General Michael Horowitz has been ‘investigating the investigators’ – as has become the common parlance – and the last few months have seen growing angst among those on the left about what (and who) his report on FISA abuse and the origins of the Russia investigation may include.

As Townhall reports, investigations for the report have been concluded since September and have been reviewed by DOJ for classified information; and today, we get a step closer to finding out as Senate Judiciary Committee Chairman Lindsey Graham released a statement confirming the dates for Horowitz’s testimony.

“I appreciate all the hard work by Mr. Horowitz and his team regarding the Carter Page FISA warrant application and the counterintelligence investigation of the Trump campaign,” Graham said.

“Mr. Horowitz will be appearing before the Senate Judiciary Committee on December 11, where he will deliver a detailed report of what he found regarding his investigation, along with recommendations as to how to make our judicial and investigative systems better.”

Graham concluded…

“I look forward to hearing from him. He is a good man that has served our nation well.”

As do many others.

The timing of Horowitz’ testimony indicates a release for the highly anticipated report during the first week of December – which makes sense given this week’s impeachment circus will suck all the oxygen out of the room and next week is Thanksgiving.

Democrats are pouring it on this week ahead of a post-Thanksgiving cold water deluge of bad news that will detail charges against the progenitors of RussiaGate. The roll-call may be a long one, including many actors whose turpitudes have been publicly and richly documented for many months – Messers, Brennan, Clapper, Comey, Rosenstein, McCabe, Strzok, Halper, Ms. Page, et. al – and, if real justice is on order, not a few figures lurking in the Deep State deep background — John Carlin, Bill Priestap, Dana Boente, Michael Gaeta, Sally Yates, Loretta Lynch, Susan Rice, Samantha Power, and perhaps even the archangel Barack Obama, just in time for Christmas, too. Robert Mueller and Andrew Weissmann deserve to be included for what amounted to a blatant, arrantly mendacious malicious prosecution, knowing that they had no case and proceeding anyway for two whole years.

I hope the roundup will extend to the very latest ploys leading to RussiaGate’s successor subterfuge, UkraineGate, namely the exploits of “whistleblower” Eric Ciaramella, his handlers and enablers in Mr. Schiff’s office, and the actions of his accomplice, Michael Atkinson, the current Intelligence Community Inspector General, with obvious conflicts of interests as a major player in the previous RuissiaGate dodge — he was legal counsel to Assistant Attorney General John Carlin, who headed the Department of Justice’s National Security Division at the birth of the FBI’s “Crossfire Hurricane” gambit, and before that he was Robert Mueller’s chief of staff at the FBI.

But, hoping for all those names above to face some perp walks may well be wishful thinking, but for now, we are sure they will be sweating.

Of course, given Graham’s suggested release schedule, that’s just enough time for Comey and Clapper to book their flights to Caracas.

PG&E Probing “Suspicious” Monetary Claims From Fire Victims, Including A $280 Million Emerald

While lawyers tap dance in the background, thinking about the hundreds of thousands of billable hours they are racking up, things at PG&E, which is left dealing with billions worth of damaged goods claims one at a time, are not as optimistic.

Among the latest “suspicious” claims the company has come across while sifting through the dragnet of victims is one man who says the company’s Camp Fire wildfire destroyed his 500 pound emerald, worth $280 million.

In addition to seeking a claim for the emerald, the man and his wife have submitted four duplicate claims for $4.5 million each, according to PG&E. PG&E is probing this and other “exceptionally large monetary claims, which appear suspicious,” according to Bloomberg.

The probe is part of a court process that is attempting to determine the company’s potential losses from wildfires caused by its infrastructure. U.S. District Judge James Donato is set to weigh in early this week at a regularly scheduled hearing.

In the case of the emerald, PG&E is seeking appraisal reports and receipts to back up the claims. The company said in a legal filing:

“With respect to the claim for the $280 million emerald, the company wants proof the owner made an effort to secure and protect the emerald and documents showing that the emerald was damaged or destroyed.”

Information from several large claims that total about $370 million will be used to try and figure out whether or not a discount should be applied to false or overvalued claims.

PG& did not identify the owner of the emerald or name specifics about those submitting dubious claims. A committee representing fire victims argue that the company is spotlighting information about individuals who aren’t part of the proceeding in front of Judge Donato. The committee also says that PG&E’s probing of the claims, in general, is improper. Many victims have been displaced from their homes, have lost family members and are getting psychological treatment, the committee lawyers argued.

Committee lawyers representing the victims said in a filing: “Asking these fire victims to produce financial back-up for their claims and be deposed on the details of this backup is unduly burdensome and should not be permitted.”

Schiff Leaked Disinfo To Politico As Part Of ‘Impeachment Scheme’, Lawsuit Claims

A senior White House official has claimed in a lawsuit that Rep. Adam Schiff (D-CA) “acted in concert” with Politico by leaking false information from closed-door impeachment testimony to journalist Natasha Bertrand with the goal of undermining President Trump’s confidence in him “and to further Schiff’s impeachment inquisition.”

According to the lawsuit, Schiff or his staff gave Bertrand closed-door impeachment testimony by former adviser Fiona Hill and Lt. Col. Alexander Vindman – who told lawmakers that he was told “at the last second” not to debrief President Trump after attending Ukrainian President Volodomyr Zelensky’s May inauguration. Instead, Trump was debriefed by Kashyap Patel, a senior counterterrorism official on the National Security Council (NSC) and longtime staffer for Rep. Devin Nunes (R-CA).

Kash Patel (right) with White House Social Media Director Dan Scavino. | Andrew Harnik/AP Photo

During his testimony, Vindman accused Patel of misrepresenting himself as a Ukraine expert, and said he was feeding the president misinformation about the country – which Bertrand then published in Politico.

According to GOP strategist and White House regular Arthur Schwartz, “Both Vindman and Fiona Hill appear to have lied about a number of the same things.”

Both Vindman and Fiona Hill appear to have lied about a number of the same things. Hill is represented by Harvey Weinstein’s lawyers. Is former Obama admin hack @LeeWolosky suborning perjury? https://t.co/5E3zp4kWpT

Patel claims he has never spoken with Trump about Ukraine. He is seeking at least $25 million for defamation and “presumed damages and actual damages, including, but not limited to, insult, pain, embarrassment, humiliation, mental suffering, injury to his reputation, special damages, costs, and other out-of-pocket expenses.” He has requested a trial by jury.

According to the lawsuit:

Between October 14, 2019 and November 8, 2019, Politico and Bertrand colluded, collaborated and conspired with Schiff to defame Kash. Schiff, or members of his staff or aides acting at his direction, leaked to Bertrand the closed-door testimony that [former former senior advisor and European and Russian affairs specialist who served on the NSC Fiona] Hill and [NSC Director of European Affairs Lt. Col. Alexander] Vindman gave in the subfloor of the Capitol Visitor Center. The leaks occurred in real-time. Schiff leaked the testimony to Bertrand because Schiff knew that it would be a violation of House Rules and Committee Rules for Schiff to publish the substance of the testimony himself.

The joint collaborative purpose of the leaks was to publish Hill and Vindman’s false and defamatory statements, including Hill and Vindman’s egregious personal attacks on Kash, so as to further Schiff and Politico’s interests in harming the President and advancing the impeachment inquisition. In furtherance of the conspiracy, Bertrand secretly communicated with Schiff or his staff via encrypted email, including proton-mail, and messaging services, such as Signal.

Kash accused Politico of ‘intentionally employing a scheme’ and abandoning ‘all journalistic integrity.’

Defendants intentionally employed a scheme or artifice to defame Kash with the intent to undermine the President’s confidence in Kash and to further Schiff’s impeachment inquisition. Defendants acted in concert with Schiff to accomplish an unlawful purpose through unlawful means, without regard for Kash’s rights and interests.

…

Defendants abandoned all journalistic integrity and violated their own code of ethics in order to further the conspiracy with Schiff. Defendants did not seek truth; report truth; minimize harm; act independently; and they most certainly were not transparent.

According to Breitbart, a source close to the president said of Bertrand’s article “This story is patently false,” adding “The president is well aware of Patel’s expertise and background. At no time has the president ever indicated to anyone including Kash that he believed that Kash was any sort of Ukraine expert or had any views on Ukraine at all for that matter. Their discussions were about something entirely unrelated to Ukraine, and Democrats and these witnesses know this but keep perpetuating this lie anyway.“

Every few days another country blows up, as their citizens take to the streets with little warning and no apparent interest in a quick settlement. Here’s the first part of the “War…Civil Unrest” section of today’s DollarCollapse.com links list. As you can see, the peasants have grabbed their pitchforks and besieged their betters on four continents over a wide range of issues, which implies that the stated cause in each case is just an excuse.

The real grievance is the sense that an unresponsive elite are sucking up all the available wealth, leaving the vast majority with (at best) zero upward mobility and at worst a return to the servitude their parents only recently escaped. To test the truth of this, watch what happens when a chastened government caves on the initial issue — and instead of heading back home the protesters ramp it up.

Who even remembers what pulled France’s Yellow Vests into the streets? The Macron government has spent months apologizing and offering big new spending programs aimed at the protesters’ stated concerns. Yet today’s headline is about water cannons and flipped cars. Hong Kong repealed the law that ignited its riots back in June, yet today the story is protesters shooting police with arrows (!) and Chinese soldiers deploying to help “clean up the streets.” Uh huh.

Why is this happening now?

Because artificially easy money enriches the people who own the stocks, bonds and real estate that rise in value when interest rates go down. This expands the already painfully wide gap between rich and poor and turns the already high level of background resentment into a powder keg. Then it’s just a matter of a provocation. And there’s always another provocation coming.

Looked at this way, the current wave of unrest is not easily fixed because the immediate remedy is even more easy money. In other words, reinstate the gas price subsidy and borrow whatever is necessary to cover the cost. Or increase welfare spending to make life slightly easier for protesters, at the cost of higher deficits. Then cut interest rates to finance all the new debt.

The result? Even more new money flowing into the elite via rising financial asset prices. Which further widens the gap between rich and poor.

Not a single government is responding to protests with “Ok, we’ll take a bunch of real wealth from the oligarchs and give it to the protesters.” That solution obviously won’t fly with the various versions of deep state/military industrial complex that are in charge out there. Easy money, in contrast:

1) is technically doable,

2) appears at first glance to help the 99%, and

3) actually further enriches the 1%.

So no one objects, the problem gets worse, and the next round of unrest is even bigger.

This may not be immediately apparent, but most people will get it eventually, by which time a peaceful solution will be far out of reach. Civil unrest is our new normal.

Tesla Supercharger Erupts In Flames At New Jersey Wawa

Nothing puts the “convenience” in “convenience store” like your car possibly going up in flames while you run inside for milk and eggs, but that’s exactly what happened Sunday when a Tesla Supercharger at a Parsippany, New Jersey Wawa caught fire on Sunday afternoon, according to CNBC.

A spokesperson for Wawa stated: “Tesla had an issue with their cabinet and the power has been shut off while they are investigating. Our store was unaffected as it is on a completely separate power line.” Great – but how’s the car?

A witness who asked to remain unidentified because they were not authorized to speak with press (i.e. very likely a Wawa employee) told CNBC that flames were noticed by a neighbor across the street from the store, who reported it to the fire department and store employees.

Wawa has announced plans to increase the number of its stores that feature Supercharger stations from 16 to more than 30 by the end of next year. At the store where the fire occurred, Tesla said it had installed eight 120 Kw Superchargers, which were available around the clock to drivers.

Earlier this year, Tesla added a “V3 Supercharger” to its arsenal of charging stations that is supposed to enable drivers to add up to 75 miles of charge in just five minutes – with the small side effect of possible setting your car, and everything around it and in it, on fire.

Tesla has said it is still under pressure to expand its Supercharger network to keep pace with the increasing number of its cars on the road (or sitting in vacant lots).

“If we fail to do so in a timely manner, our customers could become dissatisfied, which could adversely affect sales of our vehicles,” the company said in its most recent regulatory filing.

We wonder if cars bursting into flames could adversely affect sales of their vehicles, as well? Just a thought.

On the 40th anniversary of the first world climate conference in 1979, the journal Bioscience published the ominously titled “World Scientists’ Warning of a Climate Emergency.” “Scientists,” the Warning begins, “have a moral obligation to clearly warn humanity of any catastrophic threat and to ‘tell it like it is.’ On the basis of this obligation…we declare, with more than 11,000 scientist signatories from around the world, clearly and unequivocally that planet Earth is facing a climate emergency.” Addressing this emergency, the Warning continued, will require a stunning prescription: “the world population must be stabilized – and, ideally, gradually reduced.”

The Warning itself might have gone the way of most academic editorializing, but the 11,000 “scientists” who added their names and reputations to the effort caught the public imagination. The press picked it up and everyone was off to the races. Right until people started looking at the credentials of the more than 11,000 signatories.

The list includes shockingly few climate scientists. It does include people who describe themselves as “PHD Student,” “MD,” and “Zoo keeper,” though. And those were drawn just from people with last names beginning with A. Critics had a field day with this, but they had more fun with signatories Mickey Mouse and Albus Dumbledore, who also signed on.

That 11,000 academics of any description would sign off this sort of thing is what’s most telling, and most damning. What do the 11,000 suggest? Quickly implementing “massive energy efficiency and conservation practices,” “eating mostly plant-based foods,” creating a “carbon-free economy,”and “reducing population,” among other things, all with the goal of bringing about “major transformations in the way our global society functions.”

Is that all?

Their set of recommendations follows almost perfectly from a strange obsession economists have had for over two centuries, which holds the threat of “overpopulation” imperils humanity’s very existence. In past variants, this threat entailed resource depletion that would supposedly condemn most of the world to misery and starvation.

Today’s scientists have adapted identical reasoning to climate change. In each instance, scholars claiming the mantle of scientific expertise have enlisted apocalyptic fears of a coming “population crisis” to advance sweeping programs of social engineering as a way to alter the course. But curiously, the predicted population catastrophe never comes. We are simply expected to believe that, for some reason, this time things are different even if the prescription is the same.

The root of this idea traces to eighteenth-century economist Thomas Malthus, who began with a simple, intuitively plausible observation: the population of human beings expands at a faster rate than food production increases, ensuring that the typical person’s quality of life ultimately decreases to the point of misery as a result. He was so persuasive on this count that the process became known as the “Malthusian catastrophe.”

While Malthus’s religiosity constrained him from taking this intuition to its full prescriptive end, his followers in the nineteenth and twentieth centuries attempted to mechanize a “scientific” solution by enlisting the powers of the state to socially plan and control population rates.

Before his name became synonymous with his macroeconomic diagnosis of the Great Depression, the British economist John Maynard Keynes attained fame as one of the world’s most prominent neo-Malthusians. “There is no more important object of deliberate state policy,” Keynes wrote in 1924, “than to secure a balanced budget of population.” Indeed, Keynes prescribed population control as a “solution” to the underlying political causes of World War I, to the Soviet Union’s food and political crises, and even to the economic malaise of interwar Germany.

In a heretofore unpublished speech given before the Malthusian League in London in 1927, Keynes contended that a proper population policy must not only achieve population stability but continue to maintain and cultivate a population of a certain character after the growth pattern had been reversed. At first he spoke of birth control, but almost seamlessly slipped into the pseudoscience of hereditary social planning known as Eugenics.

“Within our own lifetime,” Keynes predicted, “the population of [Great Britain] will cease to increase and will probably diminish.” Following Malthusian logic to its end, Keynes thought this both good and necessary, even if the nations of the earth “are now faced with a greater problem, which will take centuries to solve.” The solution? Keynes concluded, “I believe that for the future the problem of population will emerge in the much greater problem of heredity and Eugenics.” As a scribbled line on his notes further acknowledged, “Quality must become the preoccupation.”

What we needed to address the Malthusian catastrophe, according to Keynes, was a smaller and “better” population, cultivated by “the powerful weapon of the preventive check” and administered through a state-directed population policy. This is the ugly intellectual heritage – and hubris – behind today’s population planners in the climate activist movement.

Because this time, they tell us, it’s different. But it would have to be, because when Malthus penned his original prediction more than 95 percent of the world’s population of one billion lived in extreme poverty. That population has grown more than seven fold, but only about one third of it lives in extreme poverty today. The Malthusian catastrophe never came. Instead, we got growing wealth and comfort on a global scale, a process that continues unabated.

Yet according to the 11,000 signatories, a new Malthusian tipping point is approaching. This time the cause is not impoverishing resource depletion itself, but the belief that too many people are enjoying the fruits of prosperity. Electricity, affordable and accessible transportation, and even the consumption of meat are recast from signs of unprecedented global prosperity and into “strains” on the climate. The sky is falling now, and once again governments must turn to seldom-elaborated forms of social engineering aimed at reducing the global birth rate.

And here is where the pedigree of the 11,000 matters. They urge us to uproot nearly the entirety of human life using an argument that has never, in over 200 years, been correct. And they are absolutely unqualified as a group to do so. The ever present danger is that politicians will take cover behind them and their bad ideas, which is not at all a far-fetched concern.

Presidential candidate Bernie Sanders, in a recent town hall meeting on climate change, went right back to the same Mathusian well. In response to a question on global overpopulation he said that women “in the United States…have a right to control their own bodies and make reproductive decisions. The Mexico City agreement, which denies American aid to those organizations around the world that allow women to have abortions or even get involved in birth control, to me is totally absurd.” Such measures, he continued, were needed “especially in poor countries.”

A candidate for the presidency of the United States thinks it is absurd that the American people should be cautious in inflicting schemes of population control on impoverished nations. What he means but will not say is that he thinks Keynes was right. He thinks that we, in the developed West, need to decide how many and what kind of people should be born in less developed countries.

Because the environment. Because this time it’s different.

{kind=link}