Shakespeare’s undiscovered Play: “The Tragedy of Boris Johnson”

You have to give the UK credit for doing High Drama extremely well. This is Downton on Speed. George Martin never wrote anything this good for Game of Thrones. Even Shakespeare could not have written it better.

Is this the final act? Brought low by a brother, a fainting policeman, the Iago(s) in the office – Does Birnam Wood now march on high Dunsinane? For foreign readers… I do hope it’s entertaining, because frankly, it’s becoming a complete p*sser for us.

When are we going to get out markets back? Yesterday my phone was swirling with multiple rumours from the Westminster end of town. At one point I was told Labour Whips had agreed to an October 15th Election if the No Vote bill gets royal assent. Then it was an October 29th date agreed between Corbyn and the SNP. Next the rumours were of ministers looking to flee the Boris Bunker, while another senior figure is in the paper saying Boris should readmit the Remoaners he threw out the party earlier this week. Yesterday Boris looked confused and lonely.

The recent rally in the GB Peso looks likely to prove short-lived. Short-term, look for further volatility. Long-term, can we ever get back to stability? How do we get over this and allow the UK economy to grow, sterling to settle, house-prices to rise (a critical factor for UK feelgood), and everyone to start playing nice again?

Well…. Maybe, just maybe there is light at the end of the tunnel. It will require some creative destruction and not a few political sacrifices – meaning heads have to roll….

The reason I’m feeling slighty more positive is because – to be brutally honest – for all their good intentions, even the Remainers must soon realise they are wasting their time. They may well be right that Brexit was a really bad idea, but if you were leading Europe would you want the UK to remain a member?

Of course not. Don’t discount the very real possibility Europe refuses an extension past Oct 31st and demands we ***k **f with either the offered deal or no-deal on the agreed date. Macron, et al, are not going to risk the political future of Europe to help out the UK. Whatever the lunatic right or left may tell us, Brussels is fed up to the back teeth with the UK. They are just as keen as Boris that we leave – they don’t want the UK to play any future role in Europe. They have too many other issues to address and solve. The UK is not reliable – if we stay Brexit would continue to fester. We are a canker that must be lopped off. If Britain doesn’t exit now, the EU should throw us out – because Brexit won’t ever go away.

Instead, Remainers would do best to employ their considerable energies on campaigning for the UK to take the best possible deal that’s on offer – which, if Europe plays tough, will pretty much be the one proposed to Theresa May.

And maybe that’s a way out the Brexit labyrinth: Torch the Boris Government and find a very deep ditch to bury him, Mogg, and the rest. Accept Europe letting us leave with the deal, and let the bulk of Labour and Rump Conservative MPs – who are honourable men and women – accept it. We can sort out the Scots later.. The Liberals? C’mon… you can’t fix everything..

The bulk of parliament are – like Boris’ “honourable” and now resigned brother, Jo Johnson – Remainers deep within their souls. They must now accept the inevitable. Maybe the Play could end with Jo Johnson being handed the Crown by an MP who picks it from his brother’s body lying in that ditch of his own choosing. What a finish that would be… Jo goes on to unite the fractured tribes of Albion.. Yeah? It works for me.. (and curiously, makes the tragedy even more moving.. Boris may end up in the ditch, but he will have achieved Brexit.)

Meanwhile… Boris’ rump Tory government is now held hostage by the opposition – trapped in the Boris Bunker. Effectively Jeremy Corbyn can choose when the next election will be held. Why go early? If Corbyn was smart he’d wait, then wait some more. Every day the atmosphere in the Bunker will become more foetid and treacherous.

This is where is might get interesting. If Europe won’t give us an extension, or says something like: “You have till November 31st to Agree the Deal or leave with a No Deal”, then Boris can whimper something about Europe trying to bully the UK.

In such a circumstance Corbyn waits and enables an election post October 31st. That crushes Boris’ first big promise to the electorate – that we were leaving no matter what on Halloween.

Any election will leave Labour facing the question they have so far avoided: what do they want? The Deal offered to Theresa? A new deal they aren’t going to get from Europe? A pointless Second Referendum because we aren’t getting a second chance? Or a No Deal? At that point Labour faces the same problem Boris faced – getting the political sheep to make pragmatic decisions. Good luck to him. We could well get a Part II to this play.

Back on the front lines outside the bunker… Corbyn could well decide to keep Boris in Limbo as long as possible – steadily eroding any “new leader” electoral advantage he held, deepening the festering divisions within the already fractured conservative party and letting their own discord unravel the party. New leaders would arise to replace him – Boris might not even make the election if someone senior mounts an effective coup. Corbyn could use the next few weeks to stir up the Cummings vs the Party discontent, make reassuring noises to the city and announce clever new Labour spending plans. It would give him, the Liberals and SNP the opportunity to carve up the country into anti-Tory tactical voting constituencies. Even Jeremy Corbyn will look electable after Boris spends a few more weeks trapped in his No 10 Bunker.

At the moment the numbers suggest the Tories would be the largest party, but without an overall majority. It’s conceivable Boris could do a deal with Farage and field Brexit Tories across the country. But that would be on a pure No-Deal basis – which may lose as many votes as it gains, and possibly trigger another mass Tory Defection from the Bunker.

Of course, Brussels may decide to deny the UK any extension – telling the UK to take the Backstop Theresa May deal offered last year by October 31st, in which case an October 15th or 29th Election is probably too late… Boris’ head will still end up on a pole, but he’ll have got his No-Deal Brexit… and the rest of us will have to cope with it.

I was going to write about We-Work this morning as a wake up and smell the coffee moment for global stocks.. but that will be just as bad next week!

Have a great weekend.. and off to do the day job.

via ZeroHedge News https://ift.tt/2ZEGNM3 Tyler Durden

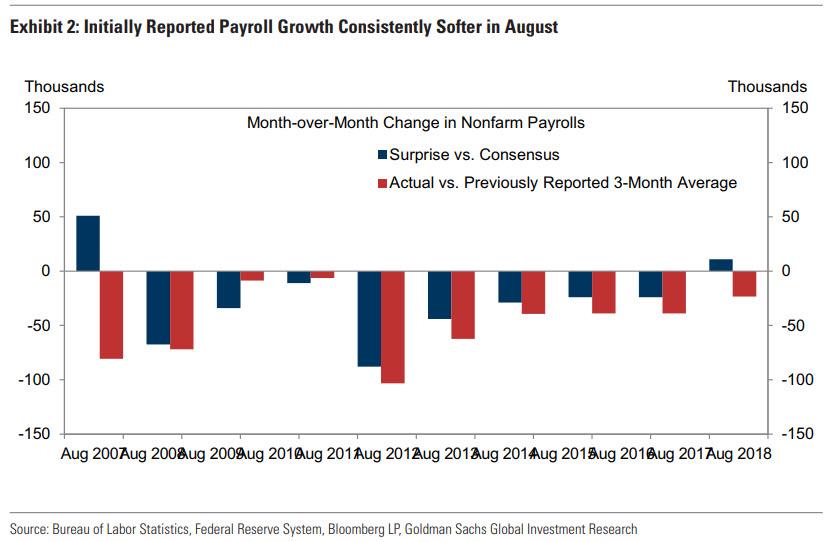

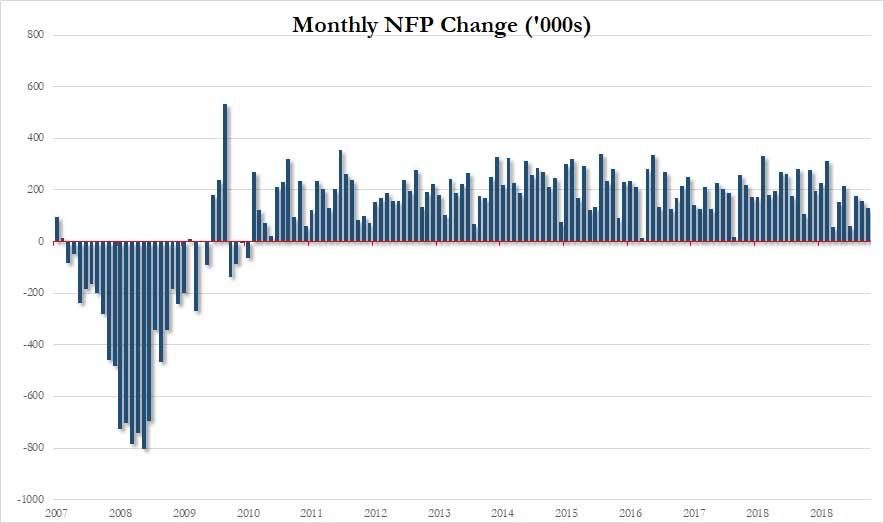

In our preview of the August jobs report we warned that while census hiring was a potential positive wildcard to today’s print, it was the seasonals that were a major negative risk, with August jobs missing consensus in 8 of the past 10 August prints.

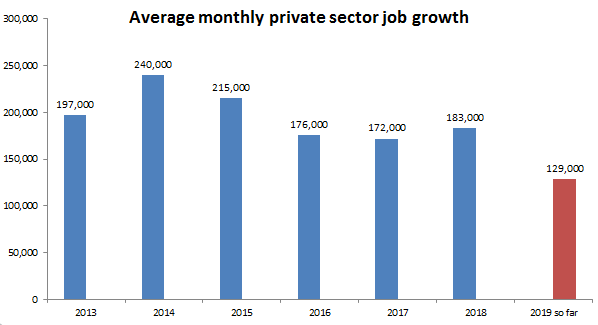

Well, make that 9 of the past 11, because moments ago the BLS reported that in August, a total of just 130K payrolls were added, with hiring for census accounting for 25,000 of that; As a result private employment rose just 96,000, with both counts the weakest in three month.

The private payroll miss was especially bad, with the 96K print far below the 150K expected. Worse, on a YTD basis, the number of private jobs created in 2019 is the worst going back at least 6 years.

That was the bad news, the good news is that average hourly earnings, were stronger than expected on both a sequential and annual basis – rising 3.2% YoY and 0.4% MoM, for all workers. Earnings for production/non-supervisory workers also rose 3.5% YoY after 3.4% in July.

Some more good news: the unemployment rate held steady at 3.7%, with the black unemployment dropping to a new all time low.

Developing.

via ZeroHedge News https://ift.tt/2PSXC1p Tyler Durden

A previously low-profile labor dispute between American Airlines mechanics and the airlines was thrust into the spotlight on Friday following reports that one of the airline’s mechanics deliberately sabotaged a flight –allegedly in an attempt to force the airline to pay out more overtime, CNBC reports.

The incident, which amounts to a federal offense that could be tantamount to terrorism, occurred back in July. The mechanic deliberately inserted a piece of foam into the plane’s air data module, a sensor that measures the plane’s pitch, speed and other information, according to the affidavit.

The mechanic, Abdul-Majeed Marouf Ahmed Alani, is set to appear in court on Friday, the US Attorney’s Office in Miami said. He told investigators that he decided to sabotage the flight because the ongoing labor dispute had “affected him financially.”

Notably, Alani’s decision to tamper with the plane’s sensors comes at a particularly sensitive time for the industry. Faulty sensors were blamed for contributing to the two deadly crashes of Boeing 737 MAX 8s that forced the global grounding of the planes.

According to Alani, “his intention was not to cause harm to the aircraft or its passengers” but to “cause a delay or have the flight cancelled in anticipation of obtaining overtime work,” per the affidavit.

AA Flight 2834 was about to depart for Nassau, Bahamas on July 17. 150 people were on board. Suddenly, an error message appeared on the plane’s monitors after the engines had been started up. The crew decided to abort takeoff and returned to the gate.

The plane was taken out of service for maintenance. Passengers deplaned and boarded a different aircraft for the flight.

During an inspection, one of Alani’s fellow mechanics noticed certain irregularities, and notified management, who reported the issue to federal law enforcement. Specifically, the mechanic found a loose pitot tube, a critical component that connects to the plane’s data module. He soon discovered that the system had been obstructed, which was suspicious.

According to CNBC, AA characterized this as an unprecedented escalation in a labor dispute that has seen mechanics routinely engage in conduct intended to slow or stop the return of aircraft to service. These small-scale sabotage attempts have led to the cancellation or delay of hundreds of flights.

The union said it couldn’t condone Alani’s behavior.

“From a union standpoint we wouldn’t condone even the thought of doing this,” said Gary Peterson, a vice president at the Transport Workers Union, which represents American’s mechanics.

via ZeroHedge News https://ift.tt/2UEcTBN Tyler Durden

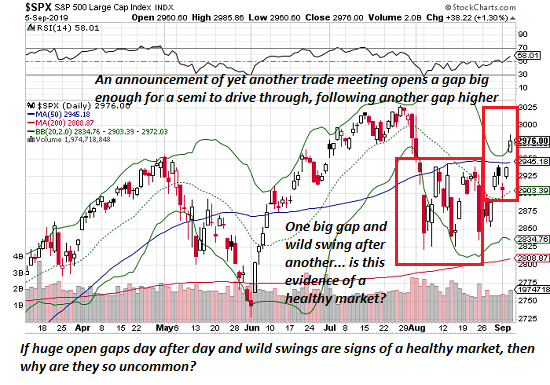

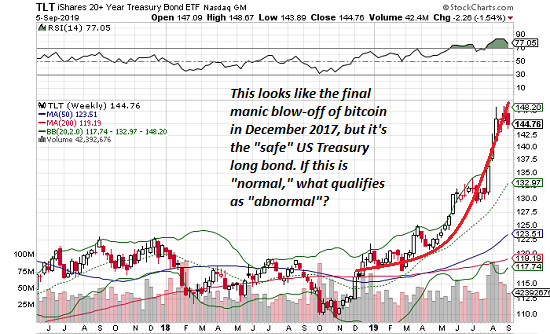

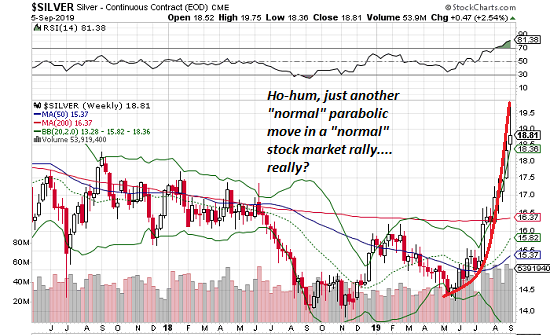

If these three charts reflect a “normal” “healthy” Bull market, then why are they so uncommon?

The implicit narrative of the latest rally in stocks is that this is just another normal rally in the ongoing 10-year long Bull market. Nice, but do these three charts look “normal” to you? Let’s take a quick glance at a daily chart of the S&P 500 (SPX), a weekly chart of TLT, the exchange-traded fund of the US Treasury 20-year bond, and silver.

In other words, let’s look at three different assets: stocks, bonds and one of the precious metals.

Even the most cursory glance reveals there is nothing normal about any of these charts. The recent action in the SPX is anything but normal: yet another announcement of yet another (low-level nothing-burger) trade meeting opens a gap big enough for a semi to drive through, punching through the upper Bollinger Band, and on the heels of a previous big gap up, also on no fundamental news.

Look at August: if a month of nearly daily open gaps and manic swings is “normal,” why are such periods so uncommon in “normal” rallies? Looking at August’s wild schizophrenia, does this strike you as “normal” market action in an ongoing Bull market? If so, perhaps you should dial back your Ibogaine consumption.

Next up, TLT, the US Treasury long bond. You know, the “safe” long bond, which moves glacially compared to risk-on stocks.

If we dare to be honest (risky in a world terrified of honesty), this looks like the blow-off topping move of risk-on bitcoin in December 2017. There is nothing “normal” about this parabolic move in Treasury bonds.

Now let’s consider silver, like its precious metal sibling gold, traditionally a hedge against currency devaluations and other risky spots of bother. Since when is a parabolic move higher in the precious metals a sign of a healthy stock market rally or healthy economy?

Um, how about “never”? Let’s face it, these are not charts of a healthy stock market. They’re signs of the manic uncertainty and frenzied churn of traders desperately seeking the next parabolic rally in risk-off hedges.

Again–if these three charts reflect a “normal” “healthy” Bull market, then why are they so uncommon? Quick, let’s talk about liquidity (good), dovish central banks (better) and trade deal rumors (best).

That the entire stock market rally rests on empty rumors and recycled central bank happy talk is beyond pathetic. There is nothing normal or healthy in these charts or in a pathological reliance on addled double-speak to push stocks higher.

Thanks to a generous grant from the Stanton Foundation, and to the video production work of Meredith Bragg and Austin Bragg at Reason.tv, I’m putting together a series of 10 short, graphical YouTube videos explaining free speech law. Our first five videos were

As usual for our episodes, the full script is also posted right below the video on YouTube.

We’d love it if you

Watched this.

Shared this widely.

Suggested people or organizations whom we might be willing to help spread it far and wide (obviously, the more detail on the potential contacts, the better).

Gave us feedback on the style of the presentation, since we’re always willing to change the style as we learn more.

Please post your suggestions in the comments, or e-mail me at volokh at law.ucla.edu.

Future videos in the series will likely include most of the following, plus maybe some others:

Free speech at college.

Speech and privacy.

Speech on or with government property.

Alexander Hamilton: free press pioneer.

from Latest – Reason.com https://ift.tt/30Zl7GR

via IFTTT

Thanks to a generous grant from the Stanton Foundation, and to the video production work of Meredith Bragg and Austin Bragg at Reason.tv, I’m putting together a series of 10 short, graphical YouTube videos explaining free speech law. Our first five videos were

As usual for our episodes, the full script is also posted right below the video on YouTube.

We’d love it if you

Watched this.

Shared this widely.

Suggested people or organizations whom we might be willing to help spread it far and wide (obviously, the more detail on the potential contacts, the better).

Gave us feedback on the style of the presentation, since we’re always willing to change the style as we learn more.

Please post your suggestions in the comments, or e-mail me at volokh at law.ucla.edu.

Future videos in the series will likely include most of the following, plus maybe some others:

Free speech at college.

Speech and privacy.

Speech on or with government property.

Alexander Hamilton: free press pioneer.

from Latest – Reason.com https://ift.tt/30Zl7GR

via IFTTT

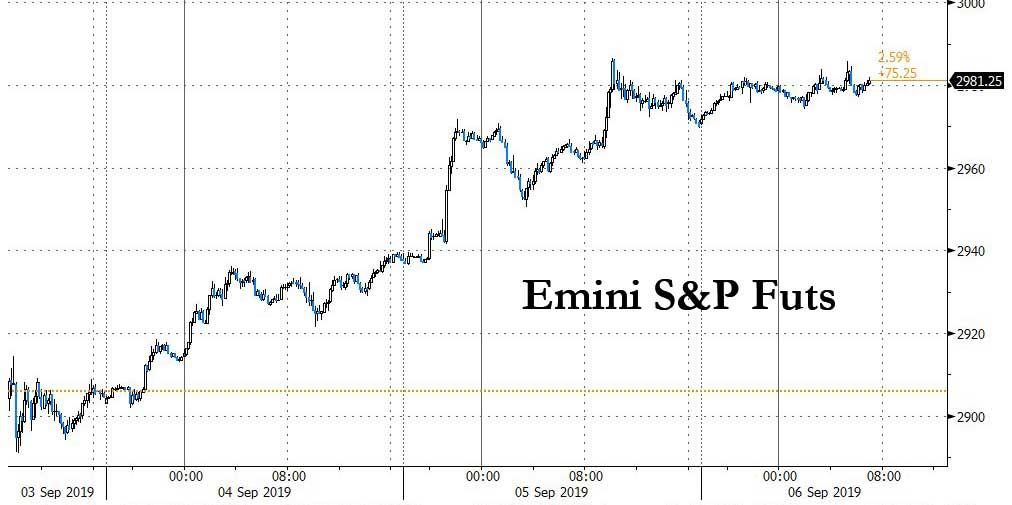

US equity futures and global stocks were drifting rangebound ahead of today’s key payrolls data and Powell speech, when news of a targeted and broad RRR stimulus from China just after 5am ET helped cap a strong week for global markets while bond buyers and dollar dealers were patiently waiting for a major disappointment in today’s economic data after their first significant selloffs in months.

S&P 500 futures rose, pushing the broad US equity index to within 2% of its all-time high, although they have found some resistance just around 2,980, while Europe’s Stoxx 600 fluctuated, with automakers rising as energy shares fell on a drop in oil prices. Equities pared some gains after jumping briefly as China cut the amount of cash banks must hold as reserves, injecting liquidity into an economy facing headwinds to growth. The MSCI Asia Pacific Index headed for its biggest weekly advance since June.

After a roller-coaster week dominated by UK and Italian political drama, Washington and Beijing trade talk, global monetary stimulus and Argentina’s imposing capital controls, calm looked to have returned. Then Beijing cut in. Just as Chinese markets were closing, the country’s central bank said it was slashing the amount of cash that banks must hold as reserves for the third time this year and the first time since 2015 that Beijing announced a broad and targeted RRR cut. That released a total of 900 billion yuan ($126.35 billion) to shore up the slowing economy.

“It feels to me like the air is coming out of it a bit,” Societe Generale strategist Kit Juckes said, referring to the recent surge in volatility. “So we will see what we get from the payrolls.”

Light volumes and sluggish price action dominated the European morning’s wait ahead of payrolls and scheduled comments from Fed’s Powell. Europe’s pan-region Stoxx 600, London FTSE, Paris CAC 40 and DAX in Frankfurt were all higher, after rising to their highest in more than month on Thursday.

Asian equities followed Wall Street higher as trade war angst subsides; MSCI Asia-Pacific index ex Japan rose for a third day, adding 0.6% and giving it a 2.4% weekly gain, its best week since mid-June. The rise in Asian stocks was led by financial firms and energy producers, following a U.S. rally supported by strong jobs data. Almost all markets in the region were up, with India and Hong Kong among the top performers. The Topix advanced 0.2%, driven by automakers and electronics firms. Japanese households increased spending again in July despite poor weather, showing solid consumer confidence ahead of a sales-tax hike in October. The Shanghai Composite Index added 0.5%, with Ping An Insurance Group and CSC Financial among the biggest boosts. The gauge climbed for a fifth straight day to finish its best week since June. India’s Sensex rose 0.7%, buoyed by Reliance Industries and HDFC Bank. Automakers rallied as the government considered more measures including lower taxes to boost vehicle sales.

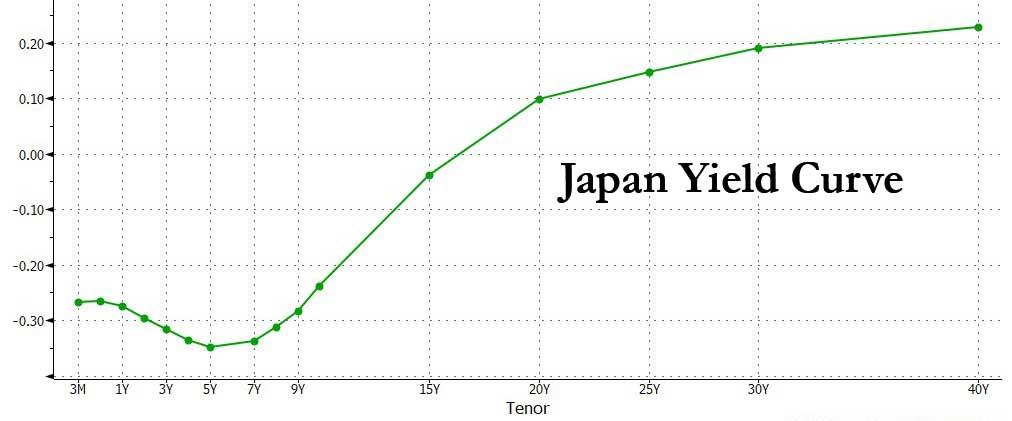

In rates, Treasuries fell, with 10-yr yield higher at 1.60% while JGB futures dipped. Euro zone bond yields steadied after their worst one-day selloff in more than a year. Bunds/USTs dipped after a choppy start, while peripheral spreads broadly tightened to core bonds. Italian short-end outperformed with 2y and 5y yields off 4.5bps, with Moody’s scheduled to review Italy later Friday. Long-end JGB yields rise ~7bps, digesting commentary from BOJ’s Kuroda who earlier in the session said yields on 20-, 30-year JGBs have “fallen a bit too far” noting that returns for life insurers and pension funds have fallen significantly, negatively impacting consumer sentiment.

In FX, the Yen was steady with the Bloomberg dollar index while the euro and pound saw weekly gains after the biggest drop for the dollar in a month. In Asia, the Aussie was 0.1% higher, while the CNY gained notably after the RRR Cut announcement.

In commodities, WTI crude steady near $56.37; while brent oil futures were little changed at $60.97 per barrel. Brent had climbed to a one-month peak of $62.40 per barrel on Thursday after data showed U.S. crude stockpiles decline and the news about U.S.-China trade talks. Gold retreated after reaching a 2019 high earlier in the week. Meanwhile, Hurricane Dorian threatens to hit cotton, tobacco, hemp and corn in the U.S. Southeast.

In other overnight news, Fitch downgraded Hong Kong’s rating to ‘AA’ from ‘AA+’ and kept the outlook negative due to protests related to the extradition bill. Fitch said in a statement that months of persistent conflict and violence are testing the perimeters and pliability of the “one country, two systems” framework that governs Hong Kong’s relationship with China.

With a barrage of news in the rearview mirror, the closely watched U.S. non-farm payrolls report due at 830 am is expected to show 160,000 jobs were added in August and the unemployment rate was unchanged at 3.7% (see our full preview here). Surveys on Thursday had suggested the U.S. may be in better shape than investors have been fearing. Services activity accelerated in August and private employers increased hiring more than expected. Despite the reassuring signs, bond markets still expect the Federal Reserve to cut U.S interest rates this month and a total of 55 basis points of cuts by the end of the year.

In terms to what the market wants from today’s payroll, DB’s Jim Reid notes that it’s hard to know where the ‘risk-friendly’ number lies. With all the concerns about the economy in recent weeks, we’re probably still in a period where good is good for risk, even if it will price out the more extreme central bank action. This week we’ve already seen markets respond negatively to a weak ISM manufacturing and then positively to strong ISM non-manufacturing yesterday. So it appears that we’re treating data on its merit again. DB economists expect a below consensus NFP print of 140k, partly reflecting a one-tenth increase in average weekly hours. DB also notes that headline and private payrolls have missed the consensus forecast in four of the last five August numbers with the median miss being 38k. For wages, they expect average hourly earnings to have increased +0.3% mom, which is in-line with the market although the risk is that the annual rate rounds down to +3.0% yoy. The unemployment rate is expected to hold steady at 3.7%.

“The strong U.S. data are the main part of the latest turn in markets as they are key factors impacting equities and U.S. yields, therefore determining how long this ‘risk on’ phase will last,” said Junichi Ishikawa, senior FX strategist at IG Securities in Tokyo. The August payrolls report “will get more attention than usual as it could further fuel the risk-on phase, which in turn would boost the dollar,” Ishikawa said.

Also on deck today, Powell is slated to speak on the economic outlook at an event in Zurich at 12:30pm ET. “While this has been some positive economic data, it makes it a little more difficult for the Fed to cut rates,” Kristina Hooper, chief global market strategist at Invesco, told Bloomberg TV. “I suspect what we will hear from Powell is a very tepid commentary on the Fed’s ability to provide monetary policy accommodation.”

A reminder that the Fed’s media blackout period kicks in at the weekend so it’s a last opportunity for the Fed and Powell to get a message across, if they want to. Consensus expects Powell’s comments to largely mirror his Jackson Hole speech which was broadly dovish in acknowledging the argument for future policy accommodation but not pre-committing to any specific policy actions.

Top Overnight News

Boris Johnson’s opponents are seeking ways to outmaneuver him on Brexit. Their latest idea is to hold a U.K. election in late October

The Bank of England will start topping up its 10 billion-pound ($12 billion) corporate-bond holdings next week, providing a test of its ability to support credit markets just weeks before a potential no-deal Brexit.

German industrial production unexpectedly declined further in July as trade tensions and waning business confidence continued to weigh on global demand.

Mario Draghi is expected to go big in a final stimulus push as European Central Bank president, overriding protests from among his ranks that tools such as bond purchases aren’t yet needed.

The EU still doesn’t know whether Boris Johnson is bluffing when he says he wants to leave the bloc with a deal, according to officials close to the Brexit negotiations

Mario Draghi is expected to go big in a final stimulus push as European Central Bank president, overriding protests from among his ranks that tools such as bond purchases aren’t yet needed.

After August’s historic drop, it was starting to seem like Treasury yields could only fall. And then came Thursday, when an enormous surge reminded bulls the world’s biggest bond market isn’t a one-way street

Fitch Ratings downgraded Hong Kong as an issuer of long-term, foreign currency debt for the first time since 1995, saying that recent political turmoil raises doubts about its governance

Oil is heading for the biggest weekly advance since mid-July as American crude stockpiles shrunk more than forecast, while U.S.-China trade talks look set to continue in Washington next month

Market Snapshot

S&P 500 futures up 0.2% to 2,978.50

STOXX Europe 600 down 0.04% to 385.78

MXAP up 0.5% to 156.04

MXAPJ up 0.6% to 506.49

Nikkei up 0.5% to 21,199.57

Topix up 0.2% to 1,537.10

Hang Seng Index up 0.7% to 26,690.76

Shanghai Composite up 0.5% to 2,999.60

Sensex up 0.8% to 36,937.75

Australia S&P/ASX 200 up 0.5% to 6,647.33

Kospi up 0.2% to 2,009.13

Brent Futures down 0.03% to $60.93/bbl

Gold spot down 0.7% to $1,507.92

U.S. Dollar Index down 0.02% to 98.39

German 10Y yield fell 0.2 bps to -0.596%

Euro up 0.06% to $1.1042

Brent Futures down 0.03% to $60.93/bbl

Italian 10Y yield rose 13.2 bps to 0.604%

Spanish 10Y yield fell 3.2 bps to 0.203%

Asian equity markets traded higher after sustaining the momentum from Wall St. where all major indices rallied and the S&P 500 notched a 1-month high amid US-China trade hopes, while better than expected ISM Non-Manufacturing and ADP jobs data ahead of today’s NFP report added to the optimism. ASX 200 (+0.5%) and Nikkei 225 (+0.5%) were higher with the gains in Australia led by tech following similar outperformance of the trade-sensitive sector stateside and with the JPY-risk dynamic at play in Tokyo. Hang Seng (+0.7%) and Shanghai Comp. (+0.5%) conformed to the global optimism although gains in the region were somewhat capped ahead of the key US jobs data and after a mostly inactive PBoC this week resulted to a net weekly liquidity drain of CNY 100bln. Finally, 10yr JGBs were lower following the extended its slide below 155.00 after-hours yesterday as the heightened risk appetite triggered declines across global bonds. However, downside has since been stemmed on selling fatigue and with the BoJ present in the market for over JPY 1.2tln of JGBs heavily concentrated on 1yr-10yr maturities, while BoJ Governor Kuroda also reiterated that lowering rates further into negative territory is always an option and noted both 20yr and 30yr yields have declined a bit too far.

Top Asian News

Axiata, Telenor Call Off Talks on Forming Asian Mobile Giant

Bali Beaches, Thai Temples Go Quiet as Chinese Stay at Home

Bank Bonds Gain in India as Mergers Set to Boost Credit Profiles

Hong Kong ‘Will Be Done’ If China Deploys Troops, Jimmy Lai Says

Major European bourses are flat [Eurostoxx 50 +0.1%] after the region saw a tentative open ahead of today’s key risk events (US Jobs data, Fed Chair Powell to speak on economic outlook and monetary policy). Bourses experienced some short-lived upside upon the PBoC’s announcement of its 50bps RRR cut effective Sep 16th. Further RRR cuts will be implemented on some banks in two phases of 50bps each on October 15th and November 15th. The PBoC estimates a release of CNY 900bln in liquidity. Sectors are mixed with marginal outperformance in consumer discretionary names whilst utilities lag. Looking at individual movers Telenor (-4.3%) are subdued after the Co. and Axiata agreed to end discussions regarding a non-cash combination of their telecom infrastructures. Meanwhile Sodexo (-3.7%) is just below on the Stoxx 600 on the back of a broker move. On the flip side, Thyssenkrupp (+2.2%) share continues its ascent amid constructive comments from Kone (+2.0%) regarding the former’s elevator unit, with indicative bids for this unit to be submitted by Wednesday.

Top European News

Markets Are Expecting Too Much From the ECB, Constancio Says

Aviva Chairman to Lead U.K. Finance Lobby’s Advisory Council

In FX, pre-NFP caution and consolidation has curtailed the Dollar’s recovery, with the index churning within a tight 98.309-463 range just shy of Thursday’s post-ADP and non-manufacturing ISM high (98.538). In terms of Friday’s fundamental drivers, the data spotlight falls on US jobs ahead of Fed chair Powell ahead of the September FOMC and pre-policy meeting purdah, but from a technical perspective the DXY is delicately placed between 10 and 20 DMAs at 98.480 and 98.210 respectively.

NZD/AUD/CAD – In keeping with this week’s evolving and improving risk tone, supplemented by 50-100 BP PBoC RRR cuts, high beta and more sensitive to overall sentiment G10 currencies have forged further gains, with Nzd/Usd managing to clamber back above 0.6400 and overtaking Aud/Usd in the process as the cross fades after several 1.0700+ forays. However, the Aussie has formed a firmer footing vs its US counterpart and nibbled through buy-stops between 0.6830-35 alongside a more pronounced bounce in the Yuan (Usd/Cnh eyeing 7.1100 compared to highs not far from 7.2000 recently). Meanwhile, Usd/Cad has slipped back to test 1.3200 after comments from BoC’s Schembri basically underscored Wednesday’s rates appropriate for now guidance, albeit adding more emphasis on weak commodity prices and not ruling out NIRP in extreme circumstances. Next up for the Loonie, Canadian labour data alongside US NFP, and then IVEY PMI after this week’s sub-50 Markit manufacturing print.

EUR – The single currency is holding rock steady against the Greenback between 1.1030-50 and may not venture much further ahead of the aforementioned US labour report, or after given hefty option expiry interest at 1.1045-55 (1.8 bn) and Fib resistance near the middle of that band (1.1049).

JPY/GBP/CHF – All on the back foot, with the Yen pivoting 107.00 and wary of decent expiries between the big figure and 107.05 (1.7 bn), but cushioned by bids reportedly layered from 107.10 to 107.20 ahead of corporate supply at 107.50. Elsewhere, Sterling has been more volatile amidst the ongoing UK political and Brexit uncertainty, with Cable waning ahead of 1.2350 and losing grip of the 1.2300 handle again before gleaning some traction on the High Court’s ruling that PM Johnson’s Parliament suspension is not unlawful. Conversely, the Franc is underperforming around 0.9900 and under 1.0900 vs the Euro after reiterations from SNB head Jordan that sub-zero Swiss interest rates are still required, and in advance of another scheduled appearance by the chief alongside his US peer.

EM – Try aside, regional currencies are revelling in the stronger appetite for risk, and the Rub is now exception even though the CBR is widely expected to lower rates by 25 bp shortly.

In commodities, WTI and Brent crude futures are lower on the day thus far, as is usually the case on US jobs report day, with participants also awaiting Fed Chair Powell’s speech on economic outlook and monetary policy. WTI futures reside under the 55.50/bbl mark after it failed to convincingly breach its 100 DMA to the upside yesterday whilst today breaching both its 50 and 200 DMAs to the downside (both at 56.15/bbl). Meanwhile, Brent futures trade below 60.00/bbl at time of writing. In terms of weekly performance, both energy benchmarks were swayed by the flip-flop in risk sentiment over the week, WTI futures fluctuated in-between its 50 WMA (57.63/bbl) and 200 WMA (53.25/bbl), whilst its Brent counterpart printed a weekly range of 57.26-60.90/bbl for now. Elsewhere, gold prices remain on the backfoot despite a weaker Buck as the recent bout of risk appetite (driven by US/China trade hopes and better-than-forecast ISM N-manufacturing) took the yellow metal closer to the 1500/oz mark (vs. weekly high at 1557/oz). Meanwhile, as it stands, copper is poised to end the week on a more positive note as prices remain above the 2.60/lb level (vs. sub-2.50/lb low). Finally, nickel ore prices saw a correction of around 3.0% amid supply glut concerns followings its recent rally with downside attributed to Indonesia stated that nickel miners can apply for new export quotas for the rest of the year in addition to their already approved quotas.

US Event Calendar

8:30am: Change in Nonfarm Payrolls, est. 160,000, prior 164,000

Unemployment Rate, est. 3.7%, prior 3.7%

Average Hourly Earnings MoM, est. 0.3%, prior 0.3%

Average Hourly Earnings YoY, est. 3.0%, prior 3.2%

Average Weekly Hours All Employees, est. 34.4, prior 34.3

Labor Force Participation Rate, prior 63.0%

Underemployment Rate, prior 7.0%

12:30pm: Powell Speaks in Zurich on Economic Outlook

DB’s Jim Reid concludes the overnight wrap

15 years ago today, I met my current long-term partner after breaking up with my previous partner of 9 years – my first relationship. Having never been with anyone else, I didn’t really know what to expect. Was it love at first sight? I wouldn’t say so but love has subsequently blossomed. I’ve no idea if they’ve ever wanted to divorce me but probably best I don’t know. There have been rows, tensions and disagreements but over the years a great mutual respect has developed. Yes, on September 6th 2004 I joined DB and to a great bunch of people in research. The previous week, I’d climbed Kilimanjaro at the end of my gardening leave, so the last 15 years have been pretty straightforward relative to that.

After one of the biggest bond routs yesterday for years in some cases, it’s amusing to reflect that when I started at DB, 10yr yields in the US, Germany and the UK were all comfortably above 4%. Will I see such yields in my career again? Anyway, today’s payrolls report comes at a fascinating time given yesterday’s move. 10y and 2y Treasury yields rose +9.8bps (a further +1bps this morning) and +10.2bps (a further +0.5bps) – both the sharpest sell-offs since January 4. Europe saw similar moves. In fact, 30y Bunds (+14.2bps) had their sharpest sell-off in 4 years and even briefly turned positive again having touched a low of -0.311% as recently as August 16. In the end, 10y Bunds rose +8.1bps and back to the gravity-defying heights of -0.594% while BTPs were up +13.5bps. The bond moves helped US and European Banks to rally +2.46% and +3.35%, respectively.

Firmer data and the positive trade war news we mentioned yesterday appeared to cause the mini-shockwave through the bond market. As we’ve also been highlighting this week, it’s been a bumper few days for US IG supply with $74bn of issuance so far since Monday already eclipsing the previous weekly record of $66bn in September 2013. There was also some attention paid to a WSJ article from chief economic correspondent Nick Timiraos, who has developed a reputation for being well connected to the Fed. The article said that “the idea of an aggressive half-point cut to battle the slowdown hasn’t gained much support inside the central bank,”. This helped spark a sell-off in fed funds futures with implied odds of 12% for the larger 50bps cut this month, down from 30% on Wednesday. Through year-end, there are now 60bps of cuts priced, down -7.5bps yesterday.

In terms to what the market wants from today’s payroll, it’s hard to know where the ‘risk-friendly’ number lies. With all the concerns about the economy in recent weeks, we’re probably still in a period where good is good for risk, even if it will price out the more extreme central bank action. This week we’ve already seen markets respond negatively to a weak ISM manufacturing and then positively to strong ISM non-manufacturing yesterday. So it appears that we’re treating data on its merit again. The consensus expects a 160k reading, which is broadly in line with last month’s 164k reading. Our economists are, however, below consensus at 140k, partly reflecting a one-tenth increase in average weekly hours. Our colleagues also make the point that headline and private payrolls have missed the consensus forecast in four of the last five August numbers with the median miss being 38k. For wages, they expect average hourly earnings to have increased +0.3% mom, which is in-line with the market although the risk is that the annual rate rounds down to +3.0% yoy. The unemployment rate is expected to hold steady at 3.7%.

If the data fails to provide much direction, then there’s always Fed Chair Powell speaking at 5.30pm BST/12.30pm EST in Zurich at a SNB event. A reminder that the media blackout period kicks in at the weekend so it’s a last opportunity for the Fed and Powell to get a message across, if they want to. Our colleagues expect Powell’s comments to largely mirror his Jackson Hole speech which was broadly dovish in acknowledging the argument for future policy accommodation but not pre-committing to any specific policy actions.

Risk assets go into these two big events on the back of a decent two-day rally with a +1.30% return for the S&P 500 yesterday putting it back to within 1.65% of the all-time highs. That’s also now six positive days out of the last eight. The DOW (+1.41%) and NASDAQ (+1.75%) also had strong days while in credit US HY spreads finished -13bps tighter. The incrementally positive news about trade including the announcement from Chinese Vice Premier Liu He (from the Asian session yesterday) about agreeing to a visit in early October was a driver, as was the data.

The headline news though was the better-than-expected ISM non-manufacturing where the August reading bounced +2.7pts to 56.4 (vs. 54.0 expected). New orders (60.3 vs. 54.1) were a big driver; however, it didn’t go unnoticed that the employment component slid over 3pts to 53.1 and to the lowest level since December 2017. That was somewhat countered by a strong ADP reading where the August print of 195k bettered expectations for 148k even though revisions subtracted -14k from July’s figure. An interesting divergence also opened between the ISM manufacturing employment index and manufacturing hiring in ADP. Historically these two series have been fairly well correlated.

Asian markets are following Wall Street’s lead this morning with the Nikkei (+0.60%), Hang Seng (+0.64%), Shanghai Comp (+0.16%) and Kospi (+0.17%) all up. Futures on the S&P 500 are +0.22% higher while spot gold prices are down -0.30% to 1514.50/ troy ounce. 10y JGB yields have tracked up +2.1bps this morning to -0.253%. As for overnight data releases, Japan’s July household spending came in line with consensus at +0.8% yoy, marking the 8th straight increase and the longest streak on record in comparable data dating back to 2000, as consumer spending remains elevated ahead of the planned October sales tax hike. Real labour cash earnings surprised on the downside though with the reading at -0.9% yoy (vs. -0.7% yoy expected).

In other overnight news, Fitch have downgraded Hong Kong’s rating to ‘AA’ from ‘AA+’ and kept the outlook negative due to protests related to the extradition bill. Fitch said in a statement that months of persistent conflict and violence are testing the perimeters and pliability of the “one country, two systems” framework that governs Hong Kong’s relationship with China.

In terms of Brexit developments yesterday, there were none really. All eyes will be on Monday when Mr Johnson will try to get an election vote through and all depends on whether the Labour and/or SNP party support it. Overnight, Bloomberg and other news outlets have reported that Labour’s Corbyn is in talks with the SNP’s leadership over pushing for a delay with their preference being October 29th and thus trying to force Mr Johnson to go to Brussels, against his will, to ask for an extension. I’m sure they’ll be lots of rumours in the weekend papers.

As for the rest of the US data yesterday, jobless claims remained low at 217k and are still yet to show any signs of meaningful deterioration. The services PMI was revised down 0.2pts to 50.7 while nonfarm productivity and unit labour costs were revised up one-tenth and two-tenths, respectively, to 2.3% and 2.6% for Q2. Elsewhere, factory orders were reported as rising a slightly better-than-expected +1.4% mom in July while core capital goods orders were revised down two-tenths to +0.2% mom.

In Europe the only data of note was the volatile factory orders series in Germany, where orders were reported as falling -2.7% mom in July (vs. -1.4% expected). That didn’t stop the STOXX 600 from climbing +0.72%.

Onto the day ahead, where the obvious focus is the US employment report this afternoon. Prior to that we’ll get July industrial production and Q2 labour costs data in Germany this morning along with the July trade balance in France. Not long afternoon we’ll get the final Q2 GDP revisions for the Euro Area where the last estimate pegged growth at +0.2% qoq. The other potentially important event for markets is Powell’s speech tonight in Zurich.

via ZeroHedge News https://ift.tt/2ZPAgsX Tyler Durden

For a sense of the endless political resources that California’s left-leaning groups have at their ready, consider this recent turn of events. After having spent $3.45 million last year to qualify a tax-hike measure on the 2020 general-election ballot, activists have decided to start from scratch on a “new and improved” version. Given the higher vote totals that they now need, they’ll have to spend at least $5 million on the new signature drive.

This would be chump change for labor groups such as the California Teachers’ Association and the Service Employees International Union—and other prominent backersof an initiative that will obliterate Proposition 13’s tax protections on commercial property owners and small businesses. Consider $5 million a small investment given the likely payout if voters are foolish enough to embrace this record-setting property tax boost.

According to the filing at the California Secretary of State’s office, the currently qualified “split rolls” initiative will result in a “Net increase in annual property tax revenues of $6.5 billion to $10.5 billion in most years, depending on the strength of the real estate markets.” The bulk of the money “would be allocated to schools (40 percent) and other local governments (60 percent).” There are no revisions that can alter the fundamental nature of this stinker.

A spokesman for the campaign toldPolitico that it refiled the initiative to create “improvements to implementation dates, expansive new small business tax relief, clarified education financing and stronger zoning language to ensure large corporations cannot avoid reassessment.” He said changes will “substantially strengthen the measure” and “widen the path to victory.” I would have loved to have seen the polling that led to this costly reboot.

The proposal is known as “split rolls,” because it splits away commercial property tax protections from residential ones. Public-sector unions and Democratic officials have been gunning for Proposition 13 since its passage in 1978 amid a tax revolt. Californians were furious at rapidly rising tax bills. Elderly people were being taxed out of their homes.

The measure capped property tax rates at 1 percent of the sales price and limited increases to 2 percent a year (plus local bonds). Prop. 13 has been the third rail of California politics—you don’t touch it, if you want to live—since then.

Californians’ tax rates are among the nation’s highest in almost every category, but their property tax levels have remained reasonable. Given high home values, the state still gets a hefty share of those dollars. According to a calculator from the Howard Jarvis Taxpayers Association, the annual property taxes on my modest home would increase $15,000 if Proposition 13 were eliminated. I’d be moving out of state.

Liberals have long blamed Prop. 13 for destroying public services, but that’s malarkey. The state’s total tax take has increased significantly, even on a per-capita basis, over that time. Our government employees are the best paid in the nation, and they receive pension deals that boggle the mind. State budgets have set spending records and schools received a 66-percent funding boost over six years. Services are crummy because of bureaucratic priorities—not funding shortages.

You can consider any new property taxes as pension taxes. The California Public Employees’ Retirement System (CalPERS) and the California State Teachers’ Retirement System (CalSTRS) are vastly underfunded even after years of record stock-market gains. If recession hits, they could get sucked into an inextricable hole. This is because for years cities and school districts have been passing unaffordable pension increases. Money is fungible, so new property tax dollars—however they are earmarked—will cover up this problem.

Such a large tax increase could be economically devastating. “Increased business taxes ultimately are passed on either to consumers as higher prices, to employees as less compensation, or the general community as less business activity,” explains the California Chamber of Commerce. Higher property taxes will diminish commercial property values, which could spark another real-estate bust. That’s one of my fears as the owner of an office building.

Progressive strategy has been to chip away at Prop. 13 protections by assuring one set of property owners that they’re only coming after another set—to make “them” pay their fair share. First, they called for tightening up so-called loopholes during property transfers. Now, they want to eliminate protections from many commercial properties. Eventually, they’ll be gunning for your home. No matter how much you give them, these activists will never stop until they’ve bled your bank account dry.

Fortunately, the initial 2020 tax-hike initiative was such a mess that its backers have to start again with a new measure that is supposed to be more appealing. But polling remains dismal for them because there really is no way to put lipstick on this pig. The only way to keep such activists from the trough is to refuse to vote to increase your own taxes.

This column was first published by the Orange County Register.

from Latest – Reason.com https://ift.tt/2ZyI4nQ

via IFTTT

For a sense of the endless political resources that California’s left-leaning groups have at their ready, consider this recent turn of events. After having spent $3.45 million last year to qualify a tax-hike measure on the 2020 general-election ballot, activists have decided to start from scratch on a “new and improved” version. Given the higher vote totals that they now need, they’ll have to spend at least $5 million on the new signature drive.

This would be chump change for labor groups such as the California Teachers’ Association and the Service Employees International Union—and other prominent backersof an initiative that will obliterate Proposition 13’s tax protections on commercial property owners and small businesses. Consider $5 million a small investment given the likely payout if voters are foolish enough to embrace this record-setting property tax boost.

According to the filing at the California Secretary of State’s office, the currently qualified “split rolls” initiative will result in a “Net increase in annual property tax revenues of $6.5 billion to $10.5 billion in most years, depending on the strength of the real estate markets.” The bulk of the money “would be allocated to schools (40 percent) and other local governments (60 percent).” There are no revisions that can alter the fundamental nature of this stinker.

A spokesman for the campaign toldPolitico that it refiled the initiative to create “improvements to implementation dates, expansive new small business tax relief, clarified education financing and stronger zoning language to ensure large corporations cannot avoid reassessment.” He said changes will “substantially strengthen the measure” and “widen the path to victory.” I would have loved to have seen the polling that led to this costly reboot.

The proposal is known as “split rolls,” because it splits away commercial property tax protections from residential ones. Public-sector unions and Democratic officials have been gunning for Proposition 13 since its passage in 1978 amid a tax revolt. Californians were furious at rapidly rising tax bills. Elderly people were being taxed out of their homes.

The measure capped property tax rates at 1 percent of the sales price and limited increases to 2 percent a year (plus local bonds). Prop. 13 has been the third rail of California politics—you don’t touch it, if you want to live—since then.

Californians’ tax rates are among the nation’s highest in almost every category, but their property tax levels have remained reasonable. Given high home values, the state still gets a hefty share of those dollars. According to a calculator from the Howard Jarvis Taxpayers Association, the annual property taxes on my modest home would increase $15,000 if Proposition 13 were eliminated. I’d be moving out of state.

Liberals have long blamed Prop. 13 for destroying public services, but that’s malarkey. The state’s total tax take has increased significantly, even on a per-capita basis, over that time. Our government employees are the best paid in the nation, and they receive pension deals that boggle the mind. State budgets have set spending records and schools received a 66-percent funding boost over six years. Services are crummy because of bureaucratic priorities—not funding shortages.

You can consider any new property taxes as pension taxes. The California Public Employees’ Retirement System (CalPERS) and the California State Teachers’ Retirement System (CalSTRS) are vastly underfunded even after years of record stock-market gains. If recession hits, they could get sucked into an inextricable hole. This is because for years cities and school districts have been passing unaffordable pension increases. Money is fungible, so new property tax dollars—however they are earmarked—will cover up this problem.

Such a large tax increase could be economically devastating. “Increased business taxes ultimately are passed on either to consumers as higher prices, to employees as less compensation, or the general community as less business activity,” explains the California Chamber of Commerce. Higher property taxes will diminish commercial property values, which could spark another real-estate bust. That’s one of my fears as the owner of an office building.

Progressive strategy has been to chip away at Prop. 13 protections by assuring one set of property owners that they’re only coming after another set—to make “them” pay their fair share. First, they called for tightening up so-called loopholes during property transfers. Now, they want to eliminate protections from many commercial properties. Eventually, they’ll be gunning for your home. No matter how much you give them, these activists will never stop until they’ve bled your bank account dry.

Fortunately, the initial 2020 tax-hike initiative was such a mess that its backers have to start again with a new measure that is supposed to be more appealing. But polling remains dismal for them because there really is no way to put lipstick on this pig. The only way to keep such activists from the trough is to refuse to vote to increase your own taxes.

This column was first published by the Orange County Register.

from Latest – Reason.com https://ift.tt/2ZyI4nQ

via IFTTT

Hysterical Democrats who nearly had a stroke earlier this year when former Starbucks CEO Howard Schultz declared his intention to run as an independent can rest easy: The corporate titan revealed in a letter to his “supporters” on Friday that he had decided not to pursue a self-financed third-party run.

The Washington Post reports that recruiting moderate voters was more difficult than he had imagined, and that he didn’t want to risk being the ‘spoiler’ who handed Trump a second term.

Howard Schultz

Schultz’s decision comes after he spent months out of the spotlight because of an unspecified health issue. The many candidates vying for the Democratic nomination will undoubtedly celebrate Schultz’s decision. The billionaire executive added that he was ending his campaign now because he didn’t want to risk his name showing up on the ballot if a moderate like Joe Biden won the Democratic nomination.

In a three-page letter to supporters Schultz outlined his reasons for abandoning his presidential bid and sketched his plans for the future. Moderate voters, who he had hoped would have been his constituency, “has largely tuned out of political life,” he wrote, and many other potential supporters would not back him because of their concern that he would aide Trump’s reelection.

The calendar also worked against his ambitions, complicating Schultz’s commitment to withdraw his candidacy before a general election if a centrist like former vice president Joe Biden won the Democratic nomination.

“If I went forward, there is a risk that my name would appear on ballots even if a moderate Democrat wins the nomination, and that is not a risk I am willing to take,” he wrote.

Schultz, 66, burst on the political scene in January, when he announced on CBS’s “60 Minutes” that he was considering an independent campaign, days after the news broke that his advisers were exploring the possibility of a third-party run.

Initially, Schultz said he would run to try to tap into the large swath of moderates across the US who don’t like President Trump, but also felt left behind by the Democratic Party’s tilt toward socialism.

He called this group the “exhausted majority,” a term that has so far failed to gain traction.

“Eighty-four percent of Americans do not consider themselves far right or far left,” Schultz wrote to supporters Friday. “Among them are an exhausted majority who want common sense, collaborative and truthful government.”

Shortly after Schultz launched his campaign early this year, top Democrats joined together to denounce him as “dangerous” and unable to win, while President Trump mocked and taunted him.

“Here is what is going to happen: He is going to spend hundreds of millions of dollars, and he is going to get into September or October of 2020, and he is going to realize he can’t win,” said Jim Messina, President Barack Obama’s 2012 campaign manager. “He is going to endorse the Democrat or he will accidentally elect Donald Trump.”

After dropping out, Schultz declared his intentions to use the money he had planned to commit to the campaign to invest in people and organizations that would help “move the country beyond two-party gridlock.”

via ZeroHedge News https://ift.tt/2ZRqiY8 Tyler Durden