Michael Burry, the physician and hedge fund manager who rose to fame as a character in Michael Lewis’s book “The Big Short” (he was one of a handful of investors who saw the housing market coming and bet against the investment-grade subprime mortgage bonds using credit default swaps), has found his next contrarian call: Going long shares of Gamestop.

Gamestop has consistently ranked among the most-shorted stocks listed in the US. But Burry told Barron’s that the market is overly pessimistic over the videogame retailer’s prospects, noting that both Sony’s and Microsoft’s next-gen consoles are likely to have physical optical disk drives. He also played down the threat from competition by new entrants, including Alphabet’s Stadia.

If the next-gen consoles expected to be released next year include optical disk drives, this “is going to extend GameStop’s life significantly,” Burry said. “The streaming narrative dovetailing with the cycle is creating a perfect storm where things look terrible. [But] it looks worse than it really is.”

Burry noted that 90% of GameStop’s ~5,700 stores are FCF positive. In prior console cycles, GS stores saw their FCF tumble before rebounding when the new consoles are released. Burry believes 2019 will mark a bottom for this cycle.

GS shares have slumped ~80%.

He added that much of the selling this year has been driven by technicals, thanks to a change in account rules that increased the company’s leverage ratio, though nothing has fundamentally changed.

“Technical factors driving the stock to lows has created an opportunity for substantial buybacks at below private market prices,” Burry said.

“There is no better use of capital [than buybacks].”

On Monday, Burry’s firm, Scion Asset Management, revealed that it had sent a letter to the board of GameStop, urging the company to finish executing the $237.6 million remaining from its $300 million share-buyback authorization. The letter marks the firm’s first foray into activist investing.

“We’re at low tide on the cash balance,” Burry said. “The balance sheet checks out for me.”

In the statement, Burry also disclosed that Scion now owns 3 million shares of GameStop, or about 3% of the company’s shares outstanding.

via ZeroHedge News https://ift.tt/2MHtx2v Tyler Durden

In a series of Friday evening tweets, President Donald Trump announced that he will hike existing tariffs on Chinese imports to 30 percent from 25 percent and will increase the next round of tariffs to 15 percent from 10 percent.

But at least he’s finally admitting that tariffs are taxes:

…Additionally, the remaining 300 BILLION DOLLARS of goods and products from China, that was being taxed from September 1st at 10%, will now be taxed at 15%. Thank you for your attention to this matter!

Trump was apparently unhappy with China’s decision to impose new tariffs on American automobiles, oil, and industrial exports starting September 1—tariffs that were a retaliation for Trump’s previous announcement that he would impose a new set of tariffs on Chinese imports on the same date.

Shortly after Trump’s tweets were issued, the Office of the U.S. Trade Representative clarified that the new 15 percent tariffs would be imposed “on the already scheduled dates” for implementation—in other words, the items that were supposed to remain tariff-free until after the holiday shopping season will still be held aside. That’s a minor reprieve for consumers, who figure to bear the brunt of the next set of tariffs.

The announcement of a new tax hike on Americans marked the end of a tumultuous week for the stock market, which had dropped sharply earlier on Friday after another set of Trump tweets in which he (ridiculously) “ordered” American businesses to pull back from doing business with China.

Trump’s rage-tweeting today and his impulsive decision to hike taxes on American businesses and consumers—at a time when he’s reportedly worried about a potential recession—is yet more evidence that the trade war with China is anything but “good and easy to win.”

For those keeping score at home, 30% tax on $250 billion imports+15% tax on $300 billion=$120 billion in taxes, or $941/household based on 127,586,000 households

— ???????????????????? ???????????????????? (@FreeTradeBryan) August 23, 2019

from Latest – Reason.com https://ift.tt/2MzXUrk

via IFTTT

In a series of Friday evening tweets, President Donald Trump announced that he will hike existing tariffs on Chinese imports to 30 percent from 25 percent and will increase the next round of tariffs to 15 percent from 10 percent.

But at least he’s finally admitting that tariffs are taxes:

…Additionally, the remaining 300 BILLION DOLLARS of goods and products from China, that was being taxed from September 1st at 10%, will now be taxed at 15%. Thank you for your attention to this matter!

Trump was apparently unhappy with China’s decision to impose new tariffs on American automobiles, oil, and industrial exports starting September 1—tariffs that were a retaliation for Trump’s previous announcement that he would impose a new set of tariffs on Chinese imports on the same date.

Shortly after Trump’s tweets were issued, the Office of the U.S. Trade Representative clarified that the new 15 percent tariffs would be imposed “on the already scheduled dates” for implementation—in other words, the items that were supposed to remain tariff-free until after the holiday shopping season will still be held aside. That’s a minor reprieve for consumers, who figure to bear the brunt of the next set of tariffs.

The announcement of a new tax hike on Americans marked the end of a tumultuous week for the stock market, which had dropped sharply earlier on Friday after another set of Trump tweets in which he (ridiculously) “ordered” American businesses to pull back from doing business with China.

Trump’s rage-tweeting today and his impulsive decision to hike taxes on American businesses and consumers—at a time when he’s reportedly worried about a potential recession—is yet more evidence that the trade war with China is anything but “good and easy to win.”

For those keeping score at home, 30% tax on $250 billion imports+15% tax on $300 billion=$120 billion in taxes, or $941/household based on 127,586,000 households

— ???????????????????? ???????????????????? (@FreeTradeBryan) August 23, 2019

from Latest – Reason.com https://ift.tt/2MzXUrk

via IFTTT

President Trump’s decision to link U.S. tariff negotiations to China’s handling of the ongoing Hong Kong protests seems like a smart move. It amply demonstrates the importance of Hong Kong in the eyes of America and other Western democracies. It would also seem to give Chinese leader Xi Jinping even less room to maneuver, and may add leverage to the U.S. negotiating position.

Furthermore, Trump’s offer to meet with the Chinese leader face-to-face to resolve the Hong Kong crisis peacefully focuses the world’s attention on Xi, rather than Trump, as the source of potential violence and intolerance. But these advantages may not have the impact that Trump hopes they will. There are a couple of possible reasons for this.

Waiting for 2020?

For one, it appears as if China may have decided to wait out Trump and his trade war policies. If true, the hope would be that Trump is be replaced in the 2020 presidential election by a more pliable American president.

But if that’s the case, there are some vulnerabilities to that strategy. The most obvious one is that Trumps may win re-election. Another is that two more years of tariffs will have inflicted more damage on China’s already limping economy, including an increase in the exodus of manufacturers and capital.

Europe is the Key to China’s Growth

That’s why Europe, not Trump’s tariffs, may be China’s bigger concern. Xi understands that focusing on European trade is the key to lessening the impacts of U.S. tariffs. About one billion euros in trade takes place every day between China and Europe, and China’s investment into the European Union (EU) almost doubled from 17.3 billion euros in 2017 to 29.1 billion in 2018. That trade flow is vitally important for both sides.

Trade also gives Beijing the opportunity to expand its relations with the EU. Not only are the Europeans a much more willing trading partner than the United States, but China and the EU both share recent experiences and viewpoints in their difficulties of working with Trump. Beijing sees increasing trade as a geopolitical opportunity to pull the EU further away from American influence.

Hong Kong Policy Poses Risk to Xi Jinping

Xi may not admit it, but his Hong Kong policy risks reversing the trading relations China worked so long and hard to establish with the EU. And economically, with U.S. trade relations continuing to deteriorate, China can ill-afford to lose trading deals with the Europeans as well.

But remaining in the Europeans’ good graces won’t be as easy for China as it has been in the past. The Huawei spyware scandal, for instance, remains a sore point with much of Western Europe and highlights the EU’s concern about Chinese takeovers of critical sectors. In response, the European Commission recently laid out a 10-point plan to address the trade imbalance and unfair and destructive trading practices by China. Notably, that was before the events in Hong Kong began.

China’s European Press Campaign

These objectives help explain Chinese ambassadors’ concerted efforts to persuade Europeans to side with Beijing and against the protesters in Hong Kong. What those efforts lack in subtlety, they make up for in intensity. China’s anti-protester campaign includes writing op-ed pieces condemning the Hong Kong protesters, as well as public criticisms against those European governments that do not.

But will that be enough to pull Europe out of its traditional Atlantic posture?

Europe Remains Suspicious of China

Like the United States, the EU is very sensitive to the threat that China and its technology theft and consistent cyberattacks pose to their long-term well-being. Perhaps just as important, the liberal democracies of Western Europe are closely watching China’s behavior toward the Hong Kong students, who are protesting against totalitarian China to preserve what’s left of their own liberal democracy.

Still, Europe has yet to choose sides in the U.S.-China trade war. Furthermore, some of the southern and eastern European nations are the beneficiaries of billions in Chinese investments and would welcome more. But it’s Germany and France—the leaders of the EU—that will determine its direction. And though British statements advising China to avoid violence in Hong Kong are met with Chinese rebukes, it would be wise for the Chinese Communist Party (CCP) to keep in mind that Hong Kong, with its highly efficient legal and financial systems, is a West European (British) creation—not communist China’s—and plays a huge role in China’s financial relations with the world.

CCP Divided on Xi’s Lack of a Plan

But there may be another, internal political reason for China’s overt efforts to bring Europe to their side. According to the Nikkei Asian Review, Xi’s position within the Party is not as secure as some would believe it to be. Some Party members are at odds with Xi’s devaluation of the yuan, disagree with his refusal to name a successor, his growing personality cult and his management of the economy.

Furthermore, there’s a growing concern within the CCP regarding Xi’s year-long delay in delivering the next five-year economic plan. The CCP has always planned China’s economy with a long-term horizon, but Xi’s foot-dragging is making Party members nervous. Some members view the lack of a formalized economic plan as the bigger obstacle to China’s continued economic growth than the U.S. tariffs. These factors magnify the importance of maintaining and growing trade relations with Europe support, both in trade and geopolitically against the United States.

Xi faces a delicate and perhaps uphill battle to bring Europe over to China’s side. He realizes that if he treats Hong Kong like Tiananmen Square, he could lose support for his “One Belt, One Road” (OBOR, also known as Belt and Road) initiative, jeopardize trade with Europe and other trade advantages China currently enjoys. Crushing the Hong Kong protesters won’t just degrade communist China’s already tarnished reputation, it will blacken Xi’s as well, and sink his signature international development plans.

Xi must surely be weighing these potentialities; otherwise, tanks from the People’s Liberation Army would have rolled into Hong Kong weeks ago.

via ZeroHedge News https://ift.tt/2Hpxft0 Tyler Durden

It’s becoming fashionable again to dismiss manufacturing. In 2015, we heard repeatedly how it represented only 12% of overall economic output. Any minor problems affecting such a small slice would surely be nothing much for the other seven-eights of the economy to overcome. There was no way Yellen’s rate hikes and the booming recovery they would anticipate would be derailed by such a trivial segment.

The idea has been given new life now that one rate cut has been undertaken. Last year, the downplaying had been more straightforward; there’s absolutely nothing wrong and nothing to stop a hawkish Powell. This year, maybe there is something wrong, but it’s only manufacturing. One-and-done rate cut should be sufficient.

IHS Markit reported yesterday its flash PMI numbers for the US economy in August. Sure enough, right off the top the manufacturing PMI dropped below 50 confirming continued weakness in the sector.

However, while it might be easy to dismiss this as just one problem, you have to acknowledge that it’s becoming a very big one even if it is only 12% of the economy. According to Markit, US manufacturing hasn’t been this bad off (below 50) since September 2009. We keep comparing the latest figure to that one month because each successive update drops a little more than the last one.

So, even if you don’t believe manufacturing accounts for much on its own you have to at least consider what must be going on in the other 88% which might leave the sector in such bad shape – without sight of a turnaround.

And it’s not the below 50 that should concern you. It’s more so that the trend keeps going after having confirmed (with other similar indications) that at least the goods economy smashed into a landmine back during the last quarter of 2018 absolutely must have suffered some substantial damage from doing so.

So, manufacturing is in really rough shape, but what about the larger maybe more pivotal service sector? That’s where the real bad news comes in. Markit’s Services PMI dropped from 53.0 in July to 50.9 August. It had rebounded last month which many believed would continue since it was, purportedly, the US economy finally showing its employment-based strength.

If not a second half rebound, then at least a second half stabilizing.

The flash August estimates pour a heavy dose of cold water on already tepid optimism. The composite PMI for August was just 50.9, matching May’s lowest in three years.

Should these estimates prove anywhere close to accurate, alongside the BLS’ benchmark revisions (which just subtracted one-fifth of the previously figured payroll gains between March 2018 and March 2019), the balance of risks are all wrong for either of those.

The most concerning aspect of the latest data is a slowdown in new business growth to its weakest in a decade, driven by a sharp loss of momentum across the service sector. Survey respondents commented on a headwind from subdued corporate spending as softer growth expectations at home and internationally encouraged tighter budget setting. [emphasis added]

What it suggests is quite apart from the idea of a narrow pocket of trouble due to trade wars and protectionist sentiment. There’s already broad-based weakness spreading throughout all of the US economy (not to mention everywhere else in the world). It may not yet add up to a full-scale recession, but all the signs keep pointing that way as does a wide array of indications which month after month continue inching closer and closer to a prospective date with one.

The longer it goes like this the greater the risk something just gives.

Jay Powell can declare “mid-cycle adjustment” all he wants. The data, including the revised labor data, just isn’t consistent with a one-and-done. Nor does it lead one to believe this is a limited 12% scenario. If nothing else, the downside risks keep rising and they were already substantial to start this month.

via ZeroHedge News https://ift.tt/2Zdz5bA Tyler Durden

Today Harris County, Texas, District Attorney Kim Ogg announced that Gerald Goines, the narcotics officer who instigated the disastrous January 28 drug raid that killed a middle-aged couple, has been charged with two counts of felony murder. The raid, which discovered no evidence of drug dealing, was based on an affidavit by Goines that cited a “controlled buy” of heroin that apparently never happened.

After defending the no-knock raid at 7815 Harding Street and describing Goines as a hero, Police Chief Art Acevedo revealed that investigators had been unable to identify the confidential informant who supposedly had bought heroin from Dennis Tuttle, a 59-year-old disabled Navy veteran who was killed by police along with his 58-year-old wife, Rhogena Nicholas. The investigators concluded that Goines, who retired in March after 34 years with the Houston Police Department (HPD), had lied in his search warrant affidavit.

Another narcotics officer involved in the raid, Steven Bryant, has been charged with evidence tampering for “knowingly providing false information” in a police report afterward. Goines claimed that Bryant, who retired three weeks before Goines, had verified that the “brown powder substance” supposedly purchased from Tuttle was black-tar heroin.

“These two charges of Felony Murder and Tampering with a Government Document against former Officers Goines and Bryant are the beginning of holding those responsible accountable,” Ogg said. “This is the start, the tip of the iceberg, in terms of how deep and wide we are investigating. We will find the truth about this entire matter.”

Ogg said “prosecutors are reviewing the events which preceded the deadly raid, including extraneous corruption allegations against Goines,” who had a history of questionable affidavits and testimony. The Houston Chroniclereports that Goines “is still under investigation over claims he stole guns, drugs and money.”

Ogg’s office also is reviewing “more than 14,000 previously filed criminal cases” involving the HPD Narcotics Division, including some 2,200 cases that were handled by Goines and Bryant. Dozens of pending cases already have been dismissed.

The HPD delivered the findings of its internal investigation to Ogg in May. The FBI is conducting a separate civil rights investigation, and last month two officers who responded to a January 8 call that supposedly implicated Tuttle and Nicholas in drug dealing testified before a federal grand jury. Contradicting Acevedo’s claim that the Harding Street home was known as a “drug house” and “problem location,” neighbors told local news outlets they had never noticed any suspicious activity there.

Tuttle and Nicholas were killed during an exchange of gunfire that also injured four narcotics officers, including Goines. According to police, the gunfire began after the first officer through the door use a shotgun to kill the couple’s dog.

from Latest – Reason.com https://ift.tt/2L36g7G

via IFTTT

Today Harris County, Texas, District Attorney Kim Ogg announced that Gerald Goines, the narcotics officer who instigated the disastrous January 28 drug raid that killed a middle-aged couple, has been charged with two counts of felony murder. The raid, which discovered no evidence of drug dealing, was based on an affidavit by Goines that cited a “controlled buy” of heroin that apparently never happened.

After defending the no-knock raid at 7815 Harding Street and describing Goines as a hero, Police Chief Art Acevedo revealed that investigators had been unable to identify the confidential informant who supposedly had bought heroin from Dennis Tuttle, a 59-year-old disabled Navy veteran who was killed by police along with his 58-year-old wife, Rhogena Nicholas. The investigators concluded that Goines, who retired in March after 34 years with the Houston Police Department (HPD), had lied in his search warrant affidavit.

Another narcotics officer involved in the raid, Steven Bryant, has been charged with evidence tampering for “knowingly providing false information” in a police report afterward. Goines claimed that Bryant, who retired three weeks before Goines, had verified that the “brown powder substance” supposedly purchased from Tuttle was black-tar heroin.

“These two charges of Felony Murder and Tampering with a Government Document against former Officers Goines and Bryant are the beginning of holding those responsible accountable,” Ogg said. “This is the start, the tip of the iceberg, in terms of how deep and wide we are investigating. We will find the truth about this entire matter.”

Ogg said “prosecutors are reviewing the events which preceded the deadly raid, including extraneous corruption allegations against Goines,” who had a history of questionable affidavits and testimony. The Houston Chroniclereports that Goines “is still under investigation over claims he stole guns, drugs and money.”

Ogg’s office also is reviewing “more than 14,000” previously filed criminal cases involving the HPD Narcotics Division, including some 2,200 cases that were handled by Goines and Bryant. Dozens of pending cases already have been dismissed.

The HPD delivered the findings of its internal investigation to Ogg in May. The FBI is conducting a separate civil rights investigation, and last month two officers who responded to a January 8 call that supposedly implicated Tuttle and Nicholas in drug dealing testified before a federal grand jury. Contradicting Acevedo’s claim that the Harding Street home was known as a “drug house” and “problem location,” neighbors told local news outlets they had never noticed any suspicious activity there.

Tuttle and Nicholas were killed during an exchange of gunfire that also injured four narcotics officers, including Goines. According to police, the gunfire began after the first officer through the door use a shotgun to kill the couple’s dog.

from Latest – Reason.com https://ift.tt/2L36g7G

via IFTTT

As widely expected, and as he himself previewed earlier in the day, Trump was set to unveil a major development in the US-China trade war this afternoon. That happened moments ago, when the president, in a series of 4 tweets, confirmed that he indeed was hiking tariffs on both existing and future China tariffs.

Specifically, Trump announced that in response to the $75 billion in tariffs that China just imposed on the US this morning – which “should not have” been put on as they were “politically motivated” – starting October 1, the existing 25% tariffs on $250BN in Chinese goods would rise to 30%, and the 10% tariffs on $300 billion in Chinese goods set to begin on September 1 will be 15%.

Here is the Trump announcement:

For many years China (and many other countries) has been taking advantage of the United States on Trade, Intellectual Property Theft, and much more.

Our Country has been losing HUNDREDS OF BILLIONS OF DOLLARS a year to China, with no end in sight.

Sadly, past Administrations have allowed China to get so far ahead of Fair and Balanced Trade that it has become a great burden to the American Taxpayer.

As President, I can no longer allow this to happen! In the spirit of achieving Fair Trade, we must Balance this very unfair Trading Relationship.

China should not have put new Tariffs on 75 BILLION DOLLARS of United States product (politically motivated!).

Starting on October 1st, the 250 BILLION DOLLARS of goods and products from China, currently being taxed at 25%, will be taxed at 30%.

Additionally, the remaining 300 BILLION DOLLARS of goods and products from China, that was being taxed from September 1st at 10%, will now be taxed at 15%. Thank you for your attention to this matter!

And the tweets themselves:

….Sadly, past Administrations have allowed China to get so far ahead of Fair and Balanced Trade that it has become a great burden to the American Taxpayer. As President, I can no longer allow this to happen! In the spirit of achieving Fair Trade, we must Balance this very….

…Additionally, the remaining 300 BILLION DOLLARS of goods and products from China, that was being taxed from September 1st at 10%, will now be taxed at 15%. Thank you for your attention to this matter!

And now we await China’s retaliation as Beijing has no choice but to retaliate again in tit-for-tat fashion, and is likely to hike the rate on its own tariffs targeting US goods, which will then prompt Trump to raise tariffs even more, at which point China will retaliate in kind, until eventually all trade between the US and China grinds to a halt, at which point the question is which country will succumb to recession and/or social unrest first.

Meanwhile, the real news this afternoon, is that there was still no announcement of currency intervention by Trump, or rather not yet. We expect that to come some time in the next 2-4 weeks.

via ZeroHedge News https://ift.tt/2TW4vxg Tyler Durden

Like Treasury Secretary Steven Mnuchin, Former White House Chief Strategist Steve Bannon has deep roots in Hollywood. And with the trade war with China now in full swing, Bannon has helped produce a dramatization of the conflict with Huawei that he hopes will help convince President Trump to stick to his guns, Bloomberg reports.

The film, entitled “Claws of the Red Dragon”, warily approaches the arrest of Huawei CFO Meng Wanzhou, who was arrested late last year by Canadian police after landing in Vancouver.

In particular, the film focuses on Beijing’s retaliation – that is, the arrest of a former Canadian diplomat, and a businessman who ran tours of North Korea for curious westerners, both of whom have been charged with espionage. Bannon told BBG that he hopes the film will convince Trump that Huawei must be shut down, and that it will help “steel Trump’s resolve”.

Bannon’s timing couldn’t be better, seeing as the administration granted Huawei another reprieve earlier this month as US markets logged some of their worst trperfo

“The central issue in the 2020 presidential campaign is going to be the economic war with China: manufacturing jobs, currency, capital markets and technology,” Bannon said in an interview. “Huawei is a key part of that, and this film will highlight why it must be shut down.”

Unlike most of Bannon’s earlier films, which were primarily documentaries about conservative icons like Ronald Reagan, as well as Bannon’s take on the factors that contributed to the financial crisis, “Claws of the Red Dragon” is a dark drama featuring professional actors.

“One of my objectives is to get a screening for President Trump at the White House,” Bannon said.

Watch the trailer for the film below:

via ZeroHedge News https://ift.tt/2ZxPyXz Tyler Durden

“A picture is worth a thousand words” is one of the dumbest aphorisms ever coined. Speaking as a former television producer, I’d say a picture takes a thousand words to explain. Take this much-circulated NASA satellite photo showing vast smoke plumes over the Amazon region:

Combined with a report from the Brazilian National Institute for Space Research that says the agency had detected 39,194 fires in the region, a 77 percent jump up from the same period in 2018, that picture has launched alarmed headlines around the world.

Interestingly, when NASA released the satellite image on August 21, it noted that “it is not unusual to see fires in Brazil at this time of year due to high temperatures and low humidity. Time will tell if this year is a record breaking or just within normal limits.”

So why are there so many fires? “Natural fires in the Amazon are rare, and the majority of these fires were set by farmers preparing Amazon-adjacent farmland for next year’s crops and pasture,” soberly explainsThe New York Times. “Much of the land that is burning was not old-growth rain forest, but land that had already been cleared of trees and set for agricultural use.”

It is routine for farmers and ranchers in tropical areas burn their fields to control pests and weeds and to encourage new growth in pastures.

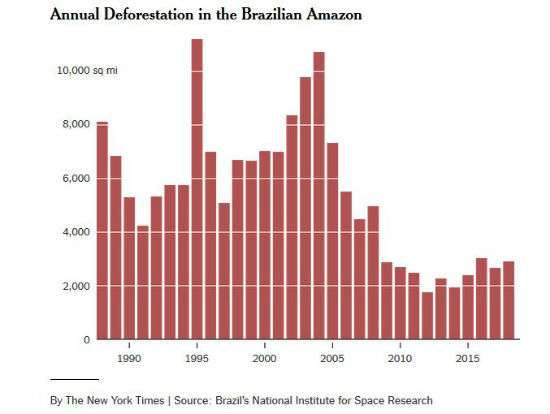

What about deforestation trends? Since the right-wing nationalist Jair Bolsonaro became Brazil’s president, rainforest deforestation rates have increased a bit, but they are still way below their earlier highs:

Various researchers have noted a U-shaped relation between environmental degradation and economic growth. As development takes off, levels of pollution and land degradation rise, but they begin to improve once certain thresholds of per capita incomes are attained. A 2012 study found, after parsing data from 52 developing countries between 1972 and 2003, that deforestation increases until average income levels reach about $3,100 per capita. As it happens, Brazilian per capita incomes reached $3,600 per capita in 2004,which is when deforestation rates began trending decisively downward.

While problematic deforestation is still taking place in the Amazon region, a 2018 study in Naturereported that the global tree canopy cover had increased by 865,000 square miles from 1982 to 2016. As Brazilians become wealthier, the deforestation trend in the Amazon will likely turn around toward afforestation, as it already has done many other countries.

As it happens, this post is only about 430 words.

from Latest – Reason.com https://ift.tt/2ZeOfNJ

via IFTTT