Iran has again rejected the prospect of new negotiations with the White House “under any circumstances,” according to an interview with Supreme Leader Ayotallah Ali Khamenei’s Military Adviser Hossein Dehghan, cited in Al Jazeera.

The Islamic Republic’s top military adviser further warned Iran and its regional allies will target all American bases in the region should the US launch war plans, while reiterating Iran’s ability to block the vital Strait of Hormuz to global oil transit. Everyone must be able to freely transit the Persian Gulf waterway or no one at all, Dehghan warned.

File photo of US troops in Iraq, via the AP

Yesterday, Iranian vice-president, Eshaq Jahangiri, said that Iranrejects UK-led attempts to establish a “joint European task force” to monitor and patrol the Persian Gulf in order to protect international shipping, countering that it would only bring “insecurity”.

“There is no need to form a coalition because these kinds of coalitions and the presence of foreigners in the region by itself creates insecurity,” he said. And added, “And other than increasing insecurity it will not achieve anything else.” France, Italy, the Netherlands and Denmark indicated Tuesday they would support a European-led naval mission to ensure international vessels’ safe passage in the gulf.

Iran’s Deputy Foreign Minister further informed France directly while in Paris meeting with top French officials including the president, that Iran’s own military forces will “secure” the Strait of Hormuz and will “not allow disturbance in shipping in this sensitive area,” Reutersreported earlier.

Meanwhile, threats and counter threats have continued to fly between London and Tehran, with each demanding the release of their tanker while accusing the other of “piracy”. Early this month the Royal Navy seized the Grace 1, carrying 2 million barrels of oil, off Gibraltar; and in turn Iran last Friday captured the British-flagged Stena Impero in the Strait of Hormuz.

On Wednesday Iran’s Hassan Rouhani appeared to offer a new deal that could break the stalemate, suggesting that should the UK release the Grace 1, Iran would reciprocate by releasing the Stena Impero.

“If Britain steps away from the wrong actions in Gibraltar, they will receive an appropriate response from Iran,” Rouhani said Wednesday addressing a weekly cabinet meeting. The words came the same day Britain reportedly sent a mediator to Iran seeking the release of the Stena Impero.

via ZeroHedge News https://ift.tt/2GmyWqP Tyler Durden

Former Special Counsel Robert Mueller is testifying before two Congressional committees today, offering his first public testimony since submitting his 448-page report on the 2016 US election. Testimony is scheduled to begin in the House Judiciary Committee at 8:30 a.m. to 11:30 a.m., followed by the smaller House Intelligence Committee from noon to 2 p.m.

Watch live:

Mueller is expected follow guidance from the Justice Department and stick to the ‘four corners’ of his report, and he has made clear that he won’t answer hypothetical questions. That said, as a private citizen there is nothing stopping Mueller from answering questions outside the report.

What to watch for

House Democrats – looking for anything they can use to launch an impeachment, will undoubtedly focus on having Mueller refute President Trump’s oft-repeated “no collusion, no obstruction” claim. While the Mueller report did not find evidence of collusion, he left the question of obstruction to Attorney General William Barr and former Deputy AG Rod Rosenstein – who found no collusion.

The Mueller report contains at least 10 alleged acts by Trump that could constitute obstruction of his investigation, which Democrats will likely push for him to elaborate on.

Mueller may provide fresh momentum for congressional Democrats to open proceedings to impeach the president. Impeachment is an option that House Speaker Nancy Pelosi has resisted so far because of her belief it would prove futile, and politically damaging to her party, unless dramatic new evidence emerges that would lead to Trump’s removal from office by the Republican-controlled Senate. –Bloomberg

Republicans, meanwhile, will likely focus on the origins of the Russia investigation – as well as the anti-Trump text messages exchanged between FBI officials Peter Strzok and Lisa Page, who were key investigators of both Donald Trump and Hillary Clinton. GOP House members will also likely ask about the so-called Steele dossier which contains salacious and unverified allegations about President Trump and his aides.

via ZeroHedge News https://ift.tt/2LDPKh3 Tyler Durden

For the first time in history, the yield on Greece’s 10Y sovereign bonds dropped below 2.00% – having crashed from around 4.00% at the start of the year – and is below US Treasury debt costs.

Greece’s 10-year yield fell 7bps to a record low of 1.984% (and Greek five-year yield falls 4bps to 1.03%, nearing July 3 record low at 1.028%)

Finally, do you think Greek debt ‘deserves’ a sub-2% yield?

Debt doesn’t matter stupid!

via ZeroHedge News https://ift.tt/2OclrQK Tyler Durden

This post discusses the Whig executive and the available records of the Constitution’s drafting history. Those records show that the delegates were familiar with the limited understanding of executive power. They also support the conclusion that the delegates wanted to give the President that limited form of the power, and drafted accordingly.

On May 29, 1787, Edmund Randolph presented to the Federal Convention several resolutions on behalf of the Virginia delegation. Two are critical to understanding the Constitution’s executive power. One proposed to confer on a new “National Legislature” the “legislative rights” then given to Congress by the Articles of Confederation. The other gave a new “National Executive” a “general authority to execute the national laws” and also “the executive rights vested in Congress by the Confederation.”

On June 2, the Convention turned to the national executive. According to Madison’s notes, the younger Pinckney of South Carolina stated his support for a vigorous executive, but feared that the powers in the resolution would include peace and war, which would create an elective monarchy. John Rutledge of South Carolina opposed giving the executive the powers of peace and war. Roger Sherman of Connecticut said that the executive should be chosen by the legislature, because “he considered the executive magistracy as nothing more than an institution for carrying the will of the legislature into effect.”

James Wilson of Pennsylvania then propounded a Whig-type limited conception of executive power. He “did not consider the prerogatives of the British monarch as a proper guide in defining the executive powers. Some of these prerogatives were of a legislative nature. Among others that of war & peace etc. The only powers he conceived strictly executive were those of executing the laws, and appointing officers, not {appertaining to and} appointed by the legislature.” (Braces indicate Madison’s later emendations.) After some back and forth, the Convention modified the resolution along the lines Wilson supported. It deleted reference to the executive rights of Congress, and gave the new national executive “power to carry into effect. the national laws. to appoint to offices in cases not otherwise provided for.”

Wilson wanted and got a chief magistrate who would carry out the laws but not have Congress’s “executive rights.” (As Wilson’s later Lectures on Law show, he had a worked-out view of the Whig executive power.) How could it make sense to have an executive without executive rights? Very likely because of a crucial ambiguity in many uses of “executive” that derived from British practice. The King was chief executive: he administered the government. He had many other powers too, like deciding on war and peace and making treaties. Powers of the executive, or executive rights, might mean the powers of the officer in the British system who held the power to carry out the law, including other powers that person held. Deciding on war was an executive power in that sense but was not within the executive power in Wilson’s sense. When the delegates rejected the grant of Congress’s executive rights, they decided not to use the powers of the British chief executive as the model of theirs.

Deliberations in the Convention continued through June and July, but the delegates did not reconsider their June 2 vote on the powers of the executive. At the end of July, the Convention committed its decisions up to that point to the Committee of Detail, which was to produce a draft constitution. Wilson served on the committee and was probably its scribe.

The Committee of Detail made a verbal change of considerable importance. Instead of creating an officer called “the executive,” and giving that officer stated powers, the committee adopted the approach now found in Article II. It created an officer called the President and gave that officer “the executive power.” Although the move did not completely clear up the ambiguity associated with “executive,” it did move the text in Wilson’s direction. Calling an officer a President says nothing about the officer’s powers, so those powers must be separately granted. If the executive power is one but only one of them, that suggests that it is the narrower power to carry out the laws and not the broader collection held by the British officer who performed that function and also, for example, could give pardons. “The executive” in the British system was unquestionably the monarch, but the “executive power” could refer to only the narrow Whig-type authority, and Wilson at least thought that it did.

Later decisions by the convention increased the power of the President, notably with respect to treaties, but did not affect the executive power. The ultimate form of Article II’s vesting clause is a slightly modified version of the Committee of Detail’s proposal. As I have argued, its text and the Constitution’s tripartite system of powers indicate that the clause uses Wilson’s conception of executive power. The Convention’s decisions (which are much better documented than its debates) indicate that the delegates’ goal was to create a President with the Whig executive power and some additional authority, like making treaties, that had been part of the King’s non-executive power.

In September, the Convention referred its nearly-completed work, based on the report of the Committee of Detail, to the Committee of Style and Arrangement. The latter committee produced the now-familiar version of the Vesting Clause of Article I, which has figured in debates about Article II. Article I gives Congress “all legislative powers herein granted,” while Article II gives “the executive power.” Proponents of a more-than-Whig executive power, like Alexander Hamilton as Pacificus, have relied on the contrast. The President, they argue, has all executive powers, enumerated and unenumerated, not only those herein granted.

Whether the Committee of Style, or at least Gouverneur Morris of that committee, meant to facilitate that reading is one of the great questions about the Federal Convention. If the committee had that plan, it was not in response to a recorded choice made by the convention as a whole, like the choice to reject the Virginia Plan’s grant of “executive rights.” Whatever the committee’s plan may have been, the inference from the contrast between the two Vesting Clauses to a non-Whig executive power is weak. The King had many powers, and so in Britain there were many powers of the executive, but there is only one executive power. It may seem multiple because it can interact with all kinds of legal rules that it implements, but in all those interactions it remains itself: the capacity to use the resources of the government to pursue the goals given by the law, subject to the constraints found in the law. Article II confers no unenumerated executive powers, because like the executive branch, the executive power is unitary. That power, the capacity to carry out the law, is the executive power James Wilson wanted to give the new chief magistrate. Wilson proposed that understanding, and there is good reason to conclude that the delegates in general agreed with him and approved language that implemented that decision.

from Latest – Reason.com https://ift.tt/30Rdjqn

via IFTTT

Earnings season always features more than a couple of surprises, and on Wednesday morning, the most shocking numbers were released by two of America’s iconic industrial giants: Boeing and Caterpillar.

But while Boeing shares swiftly recovered from their initial earnings inspired selloff as analysts and algos found some redeeming information in the company’s services and defense business, for shares of CAT, it was mostly a one-way move, as the company, which constitutes 3.4% of the Dow, missed on both the top and bottom line – though the company’s warning that it now sees full-year EPS coming in at the lower end of its range, citing rising costs and falling sales in Asia, is what grabbed investors’ attention.

It’s the latest sign that the blowback from President Trump’s trade war might be even more severe than many had anticipated. And after the IMF’s dismal economic projections (released yesterday), the results from the global belwether are the second significant sign this week that global economic growth and trade are slowing.

“The increase in manufacturing costs was primarily due to higher material costs, including tariffs, variable labor and burden and warranty expense,” the company said in a statement Wednesday.

Analysts highlighted the whiplash created by CAT’s earnings outlook after several quarters of raising guidance.

“Cracks are showing,” said BI’s Karen Ubelhart. “Outlook unchanged, but Caterpillar emphasized lower end of forecast after a string of quarters of raising guidance.”

Here are the highlights:

Adj EPS: $2.83 (est $3.12)

Rev: $14.43B (est $14.45B)

Still Sees FY Adj EPS: $12.06-$13.06 (est $13.29)

Expects To Be At Lower End Of FY Adj EPS Range

CAT also reported its weakest sales since 2017.

Twitter wits were quick to crack a few jokes.

Headline should be: Boeing and Cat earnings so bad it pushed ES and nasdaq up https://t.co/jRQn9VvW8S

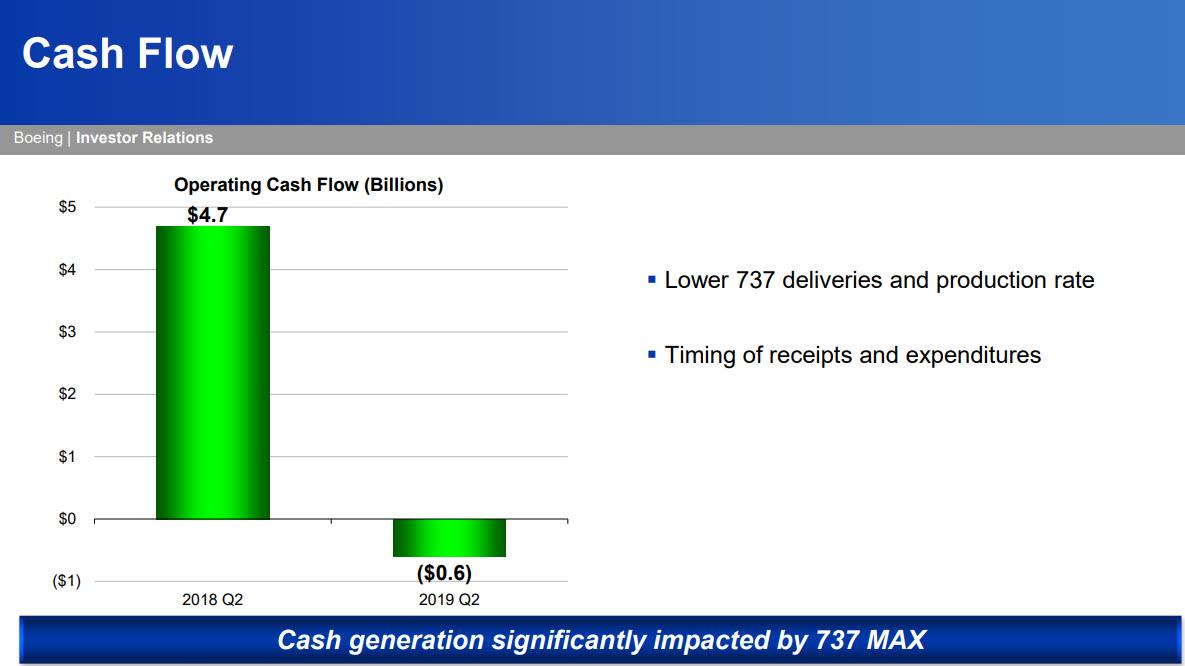

With the storm clouds over the grounded 737 MAX gathering patiently for the past 5 months, it was only a matter of time before the torrential downpour arrived, which it did just before 730am, when Boeing reported shocking numbers, with Q2 EPS printing at a stunning loss of $5.82, far below the expected profit of $1.98 per share and last year’s profit of $3.33 with revenue plunging 35% Y/Y to $15.75BN, some $5 billion below the expected $20.45 billion.

The company listed the following reasons for this surprising loss:

Recorded lower BCA revenue and operating earnings due to fewer 737 deliveries

Booked $4.9B after-tax charge related to estimated potential concessions and other considerations

Included $1.7B increased costs to produce aircraft in the 737 program accounting quantity

The 737 MAX fiasco meant that Boeing actually tipped into cash flow negative, reporting $600 million in cash burn, a far cry from the $4.68BN a year ago, while the company’s backlog dropped 2.9% to $474 billion.

Trying to put some lipstick on the pig, Boeing said it delivered 90 airplanes, including 42 787s, and noted that it had received a letter of intent from IAG for 200 737 MAX planes.

Commenting on the ongoing 737 MAX troubles, Boeing said that “disciplined development and testing is underway and we will submit the final software package to the FAA once we have satisfied all of their certification requirements.” Boeing also remains “focused on 737 MAX safe return to service; results significantly impacted.”

For now, and until there is clarity on the future of the 737 MAX, Boeing pulled all forecasts, saying that the previously issued 2019 financial guidance does not reflect 737 MAX impacts, and that due to uncertainty of timing and conditions on 737 MAX return to service, new guidance will be issued at future date. This is what the company said:

“Due to the uncertainty of the timing and conditions surrounding return to service of the 737 MAX fleet, new guidance will be issued at a future date. Boeing is working very closely with the FAA on the process they have laid out to certify the 737 MAX software update and safely return the MAX to service. Disciplined development and testing is underway and we will submit the final software package to the FAA once we have satisfied all of their certification requirements. Regulatory authorities will determine the process for certifying the MAX software and training updates as well as the timing for lifting the grounding order.”

The silver lining, of course, is that Boeing is also a bullish bet on war, and at least in that regard it did not disappoint, as sales in the offense “defense” unit rose 8% to $6.6 billion. As Bloomberg notes, no surprise that that would be up if you’ve been paying attention to other earnings this week, as Pentagon contractors Lockheed Martin, United Technologies and Northrop Grumman all beat expectations.

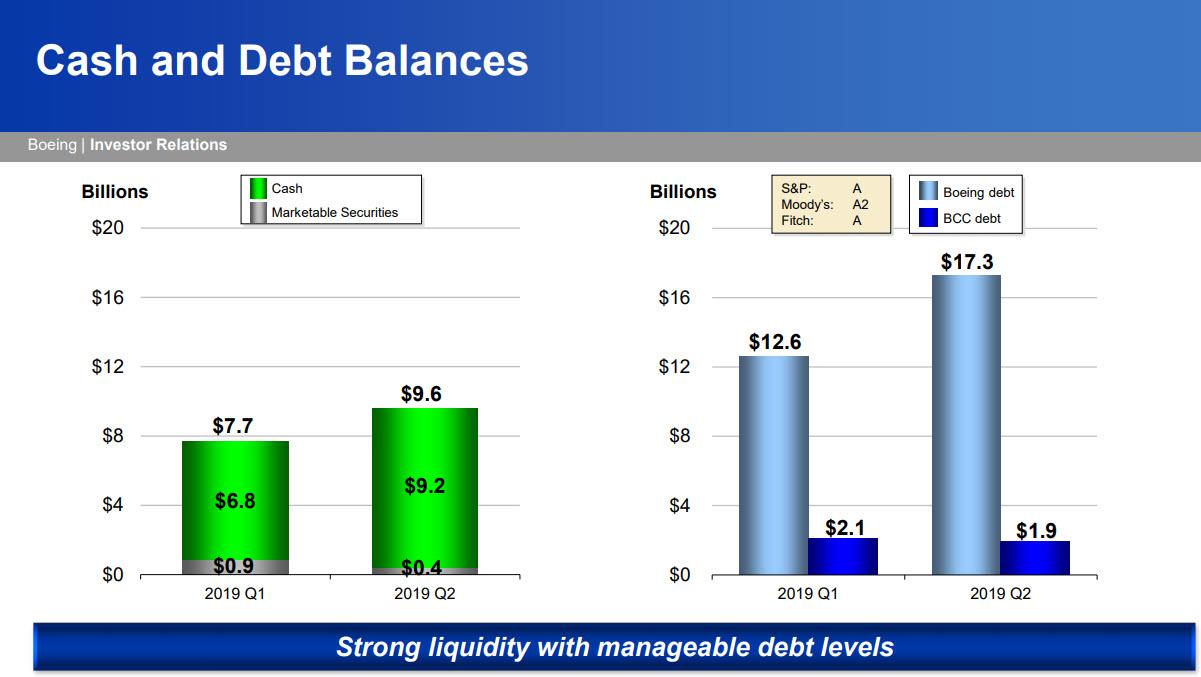

Meanwhile, even as Boeing’s net cash balance prudently rose by $2 billion, its debt increased by a far more ominous $4.7 billion, which will be a problem now that Fitch, and soon other rating agencies, are preparing to cut Boeing from single A and push it into the triple Bs.

In kneejerk reaction, Boeing shares – which have the highest weighing in the Dow Jones – tumbled as much as 1.8% before regaining much of their early losses.

Boeing’s full Q2 invester presentation is below

via ZeroHedge News https://ift.tt/2GpbYPW Tyler Durden

This post discusses the Whig executive and the available records of the Constitution’s drafting history. Those records show that the delegates were familiar with the limited understanding of executive power. They also support the conclusion that the delegates wanted to give the President that limited form of the power, and drafted accordingly.

On May 29, 1787, Edmund Randolph presented to the Federal Convention several resolutions on behalf of the Virginia delegation. Two are critical to understanding the Constitution’s executive power. One proposed to confer on a new “National Legislature” the “legislative rights” then given to Congress by the Articles of Confederation. The other gave a new “National Executive” a “general authority to execute the national laws” and also “the executive rights vested in Congress by the Confederation.”

On June 2, the Convention turned to the national executive. According to Madison’s notes, the younger Pinckney of South Carolina stated his support for a vigorous executive, but feared that the powers in the resolution would include peace and war, which would create an elective monarchy. John Rutledge of South Carolina opposed giving the executive the powers of peace and war. Roger Sherman of Connecticut said that the executive should be chosen by the legislature, because “he considered the executive magistracy as nothing more than an institution for carrying the will of the legislature into effect.”

James Wilson of Pennsylvania then propounded a Whig-type limited conception of executive power. He “did not consider the prerogatives of the British monarch as a proper guide in defining the executive powers. Some of these prerogatives were of a legislative nature. Among others that of war & peace etc. The only powers he conceived strictly executive were those of executing the laws, and appointing officers, not {appertaining to and} appointed by the legislature.” (Braces indicate Madison’s later emendations.) After some back and forth, the Convention modified the resolution along the lines Wilson supported. It deleted reference to the executive rights of Congress, and gave the new national executive “power to carry into effect. the national laws. to appoint to offices in cases not otherwise provided for.”

Wilson wanted and got a chief magistrate who would carry out the laws but not have Congress’s “executive rights.” (As Wilson’s later Lectures on Law show, he had a worked-out view of the Whig executive power.) How could it make sense to have an executive without executive rights? Very likely because of a crucial ambiguity in many uses of “executive” that derived from British practice. The King was chief executive: he administered the government. He had many other powers too, like deciding on war and peace and making treaties. Powers of the executive, or executive rights, might mean the powers of the officer in the British system who held the power to carry out the law, including other powers that person held. Deciding on war was an executive power in that sense but was not within the executive power in Wilson’s sense. When the delegates rejected the grant of Congress’s executive rights, they decided not to use the powers of the British chief executive as the model of theirs.

Deliberations in the Convention continued through June and July, but the delegates did not reconsider their June 2 vote on the powers of the executive. At the end of July, the Convention committed its decisions up to that point to the Committee of Detail, which was to produce a draft constitution. Wilson served on the committee and was probably its scribe.

The Committee of Detail made a verbal change of considerable importance. Instead of creating an officer called “the executive,” and giving that officer stated powers, the committee adopted the approach now found in Article II. It created an officer called the President and gave that officer “the executive power.” Although the move did not completely clear up the ambiguity associated with “executive,” it did move the text in Wilson’s direction. Calling an officer a President says nothing about the officer’s powers, so those powers must be separately granted. If the executive power is one but only one of them, that suggests that it is the narrower power to carry out the laws and not the broader collection held by the British officer who performed that function and also, for example, could give pardons. “The executive” in the British system was unquestionably the monarch, but the “executive power” could refer to only the narrow Whig-type authority, and Wilson at least thought that it did.

Later decisions by the convention increased the power of the President, notably with respect to treaties, but did not affect the executive power. The ultimate form of Article II’s vesting clause is a slightly modified version of the Committee of Detail’s proposal. As I have argued, its text and the Constitution’s tripartite system of powers indicate that the clause uses Wilson’s conception of executive power. The Convention’s decisions (which are much better documented than its debates) indicate that the delegates’ goal was to create a President with the Whig executive power and some additional authority, like making treaties, that had been part of the King’s non-executive power.

In September, the Convention referred its nearly-completed work, based on the report of the Committee of Detail, to the Committee of Style and Arrangement. The latter committee produced the now-familiar version of the Vesting Clause of Article I, which has figured in debates about Article II. Article I gives Congress “all legislative powers herein granted,” while Article II gives “the executive power.” Proponents of a more-than-Whig executive power, like Alexander Hamilton as Pacificus, have relied on the contrast. The President, they argue, has all executive powers, enumerated and unenumerated, not only those herein granted.

Whether the Committee of Style, or at least Gouverneur Morris of that committee, meant to facilitate that reading is one of the great questions about the Federal Convention. If the committee had that plan, it was not in response to a recorded choice made by the convention as a whole, like the choice to reject the Virginia Plan’s grant of “executive rights.” Whatever the committee’s plan may have been, the inference from the contrast between the two Vesting Clauses to a non-Whig executive power is weak. The King had many powers, and so in Britain there were many powers of the executive, but there is only one executive power. It may seem multiple because it can interact with all kinds of legal rules that it implements, but in all those interactions it remains itself: the capacity to use the resources of the government to pursue the goals given by the law, subject to the constraints found in the law. Article II confers no unenumerated executive powers, because like the executive branch, the executive power is unitary. That power, the capacity to carry out the law, is the executive power James Wilson wanted to give the new chief magistrate. Wilson proposed that understanding, and there is good reason to conclude that the delegates in general agreed with him and approved language that implemented that decision.

from Latest – Reason.com https://ift.tt/30Rdjqn

via IFTTT

S&P futures reversed a two-day rally, dropping alongside European stocks, led by the tech sector after the DOJ announced it was launching a broad, anti-trust review of the mega-tech (FANG) names, while weaker-than-expected composite PMIs in the Eurozone weighed on equities and sent bond yields to new all time lows, with manufacturing readings in Germany and France standing out. The dollar slumped while cable spiked one day after BoJo was elected as the next prime minister.

Weaker-than-expected composite PMIs in Germany and France weighed on equities and lifted bond prices, with manufacturing readings in Germany and France standing out, as the recession in Germany’s manufacturing sector worsened in July with the performance of goods producers dropping to the lowest level in seven years while French business growth slowed unexpectedly, the latest PMIs showed.

Trade tensions, weaker demand abroad and the travails of the car industry have built up over the past year to take a toll on the engine of Europe’s economy. They’ve dragged manufacturing into its deepest slump in seven years, and some of the nation’s biggest corporate names from BASF SE to Daimler AG and Continental AG have had to come to terms with a new reality for business. As one of the world’s biggest exporters, Germany is paying a high price for the the slowdown in global trade. The economy is forecast to grow the least in six years in 2019, the Bundesbank sees no sign of an export recovery and some are even saying there’s a risk of recession.

Beyond manufacturing, Germany’s image has also been dented by the troubles at Deutsche Bank AG, which is cutting thousands of jobs, and warned Wednesday that its trading slump deepened sending its stock sharply lower.

Downbeat earnings as well as the weaker-than-expected Eurozone manufacturing surveys took European shares and the euro a leg lower, with the single currency hitting two-month lows. Following strentgh in Asia, MSCI’S All-Country World index extended its previous day’s gains by a whisker, rising 0.02%. Sentiment was boosted by a Bloomberg report that U.S. Trade Representative Robert Lighthizer would travel to Shanghai next week for meetings with Chinese officials.

“While the resumption of trade talks appears to mitigate any near-term deterioration in US-China tensions, prudent investors will not get carried away, seeing as a meaningful deal still seems a long way off,” said Han Tan, market analyst at FXTM.

Asian stocks climbed for a second day, led by communications firms, as U.S. officials prepare to travel to China next week for trade negotiations. Markets in the region were mixed, with China and Australia advancing and India retreating. The Shanghai Composite Index rose 0.8% for its biggest gain in three weeks, as large insurers and banks offered strong support. The Topix added 0.4%, driven by Toyota Motor and Sony. SoftBank gained 1% following a report that it’s close to announcing the launch of a new technology investment vehicle modeled on its giant $100 billion Vision Fund. The Bank of Japan may lower its inflation forecast for this fiscal year and downgrade some of its economic growth projections. India’s Sensex slipped 0.2%, with Reliance Industries and Larsen & Toubro among the biggest drags, as investors judged bad debt risks at some financial companies.

With the latest PMIs confirming Europe is on the edge of recession, the ECB is thought likely to at least offer a nod to easier policy at its meeting on Thursday. Meanwhile, in the US, futures remain 100% priced for a rate cut of 25 basis points from the Federal Reserve next week, and even imply an 18% chance of 50 basis points. The prospect of widespread central bank largesse helped take the sting out of a downgrade to the IMF’s global growth forecasts.

“There are two conflicting catalysts for stock traders right now: on one hand, central banks around the world are about to embark on an easing initiative…,” said Konstantinos Anthis, head of research at ADSS. “On the other though, the slowdown in growth on a global scale and various geopolitical factors keep weighing down on corporate profitability, asking questions on whether equities have peaked.”

In FX, the euro declined for a fourth day after manufacturing gauges in Europe came in weaker than forecast. The common currency hit a two-month lows at $1.1127, falling further after the weak PMIs. It also hit a near seven-month trough against the yen at 120.19 though it recovered from a two-year low versus the Swiss franc. The Australian dollar tumbled after a domestic bank that has correctly called previous policy decisions flagged two more rate cuts. The pound reversed losses before Boris Johnson was set to be appointed U.K. prime minister, with a cabinet reshuffle expected later Wednesday, with investors unclear as to whether he will lead the country to a no-deal EU exit or find a compromise.

“We believe that in the short term the market is overstating the risk of a no deal,” said Mark Haefele, chief investment officer at UBS Global Wealth Management. “While a no-deal Brexit remains possible over the longer term, our view is that the most likely path in the short term is for a further extension to the UK’s 31 October exit day, either due to a change in stance from PM Johnson, or in the case of a general election.”

In rates, fears of a European recession sent investors toward the safety of German bunds, with Treasury and gilt yields also sliding lower in unison. European bond yields lower across the curves, also dragging down UST yields, with BTPs and Bonos outperforming.

Expected data include PMI readings, mortgage applications and new home sales. AT&T, Boeing, Caterpillar, UPS, Facebook, Ford, and Tesla are among companies reporting earnings

Market Snapshot

S&P 500 futures down 0.3% to 2,998.25

STOXX Europe 600 down 0.1% to 391.14

MXAP up 0.2% to 160.97

MXAPJ down 0.03% to 528.60

Nikkei up 0.4% to 21,709.57

Topix up 0.4% to 1,575.09

Hang Seng Index up 0.2% to 28,524.04

Shanghai Composite up 0.8% to 2,923.28

Sensex down 0.3% to 37,881.58

Australia S&P/ASX 200 up 0.8% to 6,776.67

Kospi down 0.9% to 2,082.30

German 10Y yield fell 2.6 bps to -0.381%

Euro down 0.1% to $1.1137

Italian 10Y yield fell 5.0 bps to 1.25%

Spanish 10Y yield fell 3.1 bps to 0.363%

Brent futures up 0.4% to $64.11/bbl

Gold spot up 0.4% to $1,423.97

U.S. Dollar Index little changed at 97.71

Top Overnight News from Bloomberg

European Central Bank policy makers have plenty of reasons to wait until September before committing to more stimulus; in the run-up to their meeting, Governing Council members have said that additional support measures are available, if needed, to boost the euro zone’s ailing economy

U.S. Trade Representative Robert Lighthizer and senior U.S. officials are set to travel to China next Monday for the first high-level, face-to-face trade negotiations between the world’s two biggest economies since talks broke down in May

Boris Johnson will formally take office as U.K. prime minister Wednesday and seek to build a government that will bring his Conservative Party together and deliver Brexit The new leader will give hardline Brexiteer Priti Patel a cabinet role and promote politicians of all stripes to try to reflect modern Britain, according to a person familiar with his plans

U.K. businesses urges Johnson to soften “hugely worrying” Brexit stance

China’s central bank governor said the country’s current interest rates are at an appropriate level, and policy will reflect domestic considerations

Bank of Japan will probably lower its inflation forecast for this fiscal year and may also downgrade some of its economic growth projections at its meeting next week, according to people familiar

Oil rallied as plans for a meeting between the U.S. and China offered a hint of progress in the trade war dividing the world’s two biggest economies

Speaker Nancy Pelosi says the House will have the votes to pass the budget, debt limit deal

Asian equity markets traded mostly higher with sentiment lifted by US-China trade hopes after reports US Trade Representative Lighthizer will lead a small team of negotiators to China next Monday for trade discussions. This underpinned major indices on Wall St. with outperformance seen in the trade sensitive sectors such as materials and industrials, although futures pared some of the gains after-market on news the DoJ is to open a broad antitrust review on the large tech firms. Nonetheless, ASX 200 (+0.8%) and Nikkei 225 (+0.4%) were higher with broad strength seen in Australia aside from the mining sector, while gains in Tokyo were capped amid a downturn among JPY-crosses. Hang Seng (+0.3%) and Shanghai Comp. (+0.8%) showed a strong performance on the trade optimism which was also helped by US Commerce Secretary Ross who said he will deal with Huawei waiver applications within the next few weeks, while China was also said to be looking to make more agricultural purchases as a goodwill gesture. Finally, 10yr JGBs were uneventful with demand sapped following similar uninspiring trade in USTs amid the positive risk tone and with the BoJ also absent from the market today.

Top Asian News

World’s Top Toymaker Joins Companies Leaving China’s Factories

Japan May Soon Gain A Powerful Trade Weapon Against South Korea

Hong Kong’s NWS Is Said to Mull Sale of Public Transport Assets

Malaysia’s PE Fund Said to Weigh Options for Oil Tanker Operator

Major European bourses are marginally lower [Eurostoxx 50 -0.2%] following on from a relatively flat open as overall downbeat flash PMIs from Europe weighted on the region. UK’s FTSE 100 (-1.0%) lags its peers amid unfavourable currency action coupled with underperformance in heavyweight mining names following a barrage of broker downgrades. As such, Rio Tinto (-4.0%), BHP (-3.4%) and Anglo American (-3.1%) all rest at the foot of the index. Sectors are mixed with defensive sectors supported due to the current cautious risk tone. In terms of individual movers, ASM (+7.3%), ITV (+6.1%) and Akzo Nobel (+4.1%) shares are all fuelled by earnings and trade at the top of the Stoxx 600. On the flip side, Deutsche Bank (-3.7%) shares plumbed the depths post-earning after the German lender reported a larger than expected net loss and cut its FY 19 revenue guidance.

Top European News

Euro Area’s Economic Struggles Persist as Industry Slump Deepens

Dovish ECB Renders More Czech Rate Hikes Pointless for Michl

Paris Scorches in Historic Drought as Heatwave Fries Europe

Repsol Announces Buyback Plan as Oil Earnings Kick Off

In FX, dollar bulls have gleaned even more encouragement from unfolding US-China trade developments given that face-to-face talks look set to resume early next week, and Beijing offers to buy more agricultural goods as a good will gesture in response. Moreover, the Dollar continues to proffer from the demise of others and increasingly constructive technical impulses with the DXY eclipsing a Fib retracement level and inching closer towards the psychological 98.000 mark.

AUD/NZD – The Aussie has given up 0.7000+ status and is now threatening to slide below 0.6975 in wake of slowdowns in all CBA PMI readings overnight and yet another dovish RBA policy call looking for 2 further cuts in the OCR (Westpac this time eyeing moves in October and February 2020). All this ahead of comments from RBA Lowe in the early hours on Thursday and in contrast to the Kiwi that is keeping in contact with 0.6700 after a wider than forecast NZ trade balance, albeit due to a bigger miss on the import side vs exports.

EUR/CHF/CAD – The single currency has also been undermined by PMI surveys, and in particular the manufacturing prints showing France on the 50 threshold and Germany sinking deeper into contraction. With Eurozone M3 also softer than expected, rate cut odds have now tipped in favour of 10 bp for tomorrow’s ECB meeting and Eur/Usd is losing sight of decent option expiry interest at 1.1150 (1 bn) as a result, but holding above the ytd base and 1.1100 where big barriers lie. Meanwhile, the Franc has retreated further vs the Buck within a 0.9850-75 band, but remains above 1.1000 against the Euro pending Thursday’s ECB policy pronouncements and the SNB’s response, but the Loonie has clawed back some lost ground vs its US counterpart to meander between 1.3129-47 compared to 1.3164 or so at one stage on Tuesday.

GBP/JPY – Relative outperformers and bucking the overall trend, as the Pound maintains its recovery momentum following confirmation that Boris Johnson will take over the reins from Theresa May as Tory Party head. Cable has extended its rebound from near 1.2400 to 1.2480+ awaiting the official unveiling of the new PM and his Cabinet line up, with Eur/Gbp down towards 0.8925 and early July mtd lows. Similarly, the Yen is still displaying resilience in the face of overall Usd strength and upbeat risk sentiment despite ongoing geopolitical tensions, with a reluctance to stray too far from 108.00 where massive expiries roll off (4.3 bn) and technical resistance capping the upside (108.31 Fib).

EM – The Rand remains in the spotlight amidst comments from SARB Governor Kganyago underlining post-rate cut guidance for limited additional monetary stimulus and CPI data that was slightly firmer than anticipated in m/m terms. Usd/Zar is hovering just below 13.9500 as the Central Bank head highlights the fact that neutral rates have risen due to risk premia of late and this makes it tougher for further easing.

In commodities, WTI and Brent futures are taking a breather from last night’s geopolitical-induced gains in which the benchmarks reclaimed USD 57/bbl and USD 64/bbl to the upside on reports that UK approached EU nations to join a European-led mission for safe shipping via the Strait of Hormuz. Furthermore, reports of a US delegation heading to China on Monday exacerbated upside in the complex on sentiment. Meanwhile, the mammoth drawdown in API crude stocks (-10.96mln vs. Exp. -4.0mln) added further fuel to the upside for oil, although the immediate jolt was quickly faded due to bearish components of the release including a surprise build in gasoline inventories, it’s worth noting that this week’s inventory data also captures the late effects of Storm Barry. Elsewhere, spot gold in is crawling higher as the yellow metal consolidates following its recent decline from 6yr highs. Copper prices are marginally lower amid the cautious risk tone, albeit remain above USD 2.70/lb, while Dalian Iron ore extended losses amid slowing demand in the wake of output restrictions on steel producers in China’s top steel-making city Tangshan.

US Event Calendar

7am: MBA Mortgage Applications, prior -1.1%

9:45am: Markit US Manufacturing PMI, est. 51, prior 50.6; Services PMI, est. 51.8, prior 51.5

10am: New Home Sales, est. 658,000, prior 626,000; est. 5.11%, prior -7.8%

DB’s Jim Reid concludes the overnight wrap

I’ve been promised the hottest night of my life this week. For the avoidance of doubt, meteorologists have suggested that this week will likely see the hottest overnight temperatures on record here in the UK and the hottest July day on record and possibly a new overall record. I must admit the more I read about climate change the more worried I get. However all I will say is that since we moved house three months ago we must have eaten outside in the evening 90% of the time I’ve been around. It’s been absolutely fantastic. Not even a swarm of flying ants could stop us last night. The only thing missing was a glass of Rose. Interestingly flying ants have been so prevalent over the last week in the South of England that they’ve appeared on weather radars and some forecasters initially mistook them for a band of rain!

As well as potentially being the hottest day ever tomorrow, it’s possible we’ll also start the latest round of global monetary stimulus or at least get new dovish forward guidance from the ECB. Given we’re on the eve of such an event and given that we have seen a big rally in global assets as a prelude, I found it interesting to read DB’s Binky Chadha’s latest asset allocation piece yesterday (see link here). In it he showed that since the 1950s, the Fed has embarked on 19 easing cycles, including the unconventional easing measures adopted during the course of this economic recovery. However of these, 9 or almost half, saw the economy eventually slip into recession. The episodes that ended in recession saw the ISM continue to weaken, eventually bottoming – 8 months after the Fed began cutting – at low levels (median 36). In these recession episodes, the S&P 500 saw a full bear market, typically falling -27% from peak to trough, with a bulk of the decline occurring after the Fed had started easing. Indeed, on average, the S&P 500 did not bottom until 5 months after the Fed started cutting. The distinguishing characteristic of the episodes that did not end in recessions was that after a moderate further decline in growth (to a median ISM 48), on average within 2-3 months after the Fed began easing, growth rebounded quickly. The equity market typically fell -7% after the Fed began easing, but bottomed quickly with growth. The S&P 500 ended above the pre-easing level within 6 months each and every time, rising a robust 12% on average. So my take on this is that history suggests a much higher probability of an imminent recession than markets do and also that we’re at quite a binary moment for markets as the Fed (and other central banks) embark on a fresh easing cycle. See the piece for much more detail.

In terms of markets yesterday, the focus was a further rally for equities across the world, with the S&P 500 closing +0.69% higher and above the 3000 level for only the fourth time in history. Elsewhere, the DOW and NASDAQ advanced +0.65% and +0.58%. After US markets closed, the Justice Department said it is investigating tech firms for antitrust violations, which caused the Nasdaq to retrace a bit more than half of its gains from yesterday, with futures down -0.18% overnight. Shares of Amazon (-0.95%), Alphabet (-0.96%) and Facebook (-1.54%) declined c.1% in after-hours trading. Prior to that, indexes were supported by strong earnings reports, as well as positive news on the trade front after Europe went home. USTR Lighthizer and other senior officials will reportedly travel to China on Monday for face-to-face talks, likely staying through Wednesday. European equities rallied as well before this news, with the STOXX 600 up +0.98% and the DAX trading +1.64%.

The positive trade news has also supported the Asian session overnight with Chinese markets leading advances – the CSI (+1.03%), Shanghai Comp (+1.01%) and Shenzhen Comp (+1.39%) are all up over 1%. The Nikkei (+0.46%) and Hang Seng (+0.93%) are also up while the Kospi is down -0.25%. Elsewhere, futures on the S&P 500 are trading largely unchanged while crude oil prices (WTI +0.41%, Brent +0.27%) are up for the fourth day in a row on a report from the American Petroleum Institute which showed a 10.96 million barrel decline in US crude stockpiles last week. In terms of overnight data releases Japan’s preliminary July manufacturing PMI came in at 49.6 (vs. 49.3 last month) while the services PMI stood at +52.3 (vs. 51.9 last month) bringing the composite PMI print to 51.2 (vs. 50.8 last month).

Ahead of tomorrow’s ECB meeting the next test will be the rest of today’s flash global PMIs. The last few months have seen some stabilisation in the data with the manufacturing PMI for the Euro Area hitting 47.6 in June (vs. 47.7, 47.9 and 47.5 in the three months prior). The consensus expects a 47.7 reading for July. As for the services reading the consensus expects a 53.3 print which compares to 53.6 last month. We should note that we’ll also get country level PMI data for Germany, France, and also the US.

Turning back to the earnings reports from yesterday, Coca-Cola (+6.07%) and United Technologies (+1.50%) led gains. Coca-Cola shares climbed to a record high after their results showed a strong increase in demand, with full-year revenue growth estimated to grow 5%, up 1pp from the previous guidance. Demand from China has been a key driver of that growth, with sales volumes up 7% in Asia’s largest economy. United Technologies also raised their guidance, citing strong jet engine sales. After hours, Texas Instruments (+7.01%) and Snap (+9.10%) rallied strongly, as the former raised its guidance and the latter increased its daily user count to 203 million, compared to consensus estimates for 192 million.

The risk-on sentiment bled over into fixed income markets, where 10-year treasury yields rose +2.6bps. Two-year yields rose +2.5bps, leaving the 2y10y curve roughly flat. Earlier in the session, European yields rallied with bund yields down -0.9bps to -0.355%. BTPs outperformed, gaining -5.1bps. In the UK, gilt yields fell -1.6bps and the Treasury sold new 10-year notes at their second lowest ever yield at 0.789%, above only the September 2016 auction. In credit, HY spreads tightened -3.6bps and -4.7bps in Europe and the US. This morning we have published an update of our analysis looking at relative value between the EUR and USD HY markets. EUR HY has generally outperformed since February and within the note we assess whether USD HY is now starting to look relatively more attractive ( link here).

As widely expected, Boris Johnson was elected the leader of the Conservative Party yesterday, and as such will become the new UK PM this afternoon. While journals stretching to the moon and back have been written on the Brexit implications, less has been written on the wider economic policy mix of the incoming government. DB’s Oli Harvey wrote on this yesterday (see link here) and thinks that if the new administration survives or wins an election we could have a sizeable departure from the post 2010 regime. Indications are that Borisnomics may represent a significant relaxing of fiscal policy leading to materially higher borrowing and hence issuance. At the same time, we think there is at least some possibility the Bank of England’s mandate could be adapted to provide the bank more flexibility over inflation. This policy move is likely to be more extreme in a hard Brexit scenario but fiscal policy is likely going to take the strain in all reasonable scenarios. Oli thinks the best trades are forward steepeners such as 2s10s 2 year forward. As I’ve repeatedly suggested the UK could start the helicopter money experiment (on a hard Brexit) that I think is likely across the globe in the years ahead.

Elsewhere in the UK, there was some attention paid to two BoE speakers, Saunders and Haldane, who both leaned dovishly. Saunders is possibly the biggest hawk on the MPC, but he said that the economy looks weak and “is clearly not overheating,” suggesting potential support for policy easing. Similarly, Haldane said that uncertainty is high and “the case for holding rates until the road becomes clearer is strong.” Considering that he had previously argued for higher rates before the June policy meeting, this was a decidedly dovish shift as well. At the same time, the UK’s CBI manufacturing orders index fell to -34, its lowest level in over 9 years and far worse than the expected -15. The cocktail of dovish signals and weak data pushed the pound -0.31% weaker versus the dollar.

Away from markets, the IMF updated its World Economic Outlook and cut its forecast for global growth by -0.1pp for both 2019 and 2020, to 3.2% and 3.5%, respectively. The update described growth as “sluggish” and “subdued” and also noted that risks are tilted to the downside, emphasizing trade tension uncertainties. Nevertheless, the forecast for the US rose +0.3pp to 2.6% for this year, while Europe’s stayed steady at 1.3%. The forecast for China was revised down -0.1pp, to 6.2%, while India’s was trimmed -0.3pp to 7.0%. The IMF also revised down its forecast for 2019’s growth in world trade volumes by c.1pp, to 2.5%.

To wrap up yesterday’s economic data, in the US it was mostly disappointing, with the Richmond Fed manufacturing index down to -12 versus expectations for a positive print of 5. That contrasts with the recent rebound in surveys from the Philadelphia and New York Feds, giving a cloudier picture ahead of today’s flash PMI. Existing home sales slowed further in June to 5.27mn, weaker than expected, while the FHFA house price index rose only 0.1%, the weakest pace since early 2017 and fourth weakest since 2012. In Europe, consumer confidence improved slightly to -6.6 from -7.2.

Turning to the day ahead, the July flash PMIs in Europe and the US will be the main data focus. Away from that, July confidence indicators are due in France, June M3 money supply data due for the Euro Area and June new home sales data due in the US. Earnings highlights include Boeing, Caterpillar, Ford, Facebook and AT&T. Former Special Counsel Mueller will testify before the House Judiciary and Intelligence committees on Russian election interference.

via ZeroHedge News https://ift.tt/2OdfNxR Tyler Durden

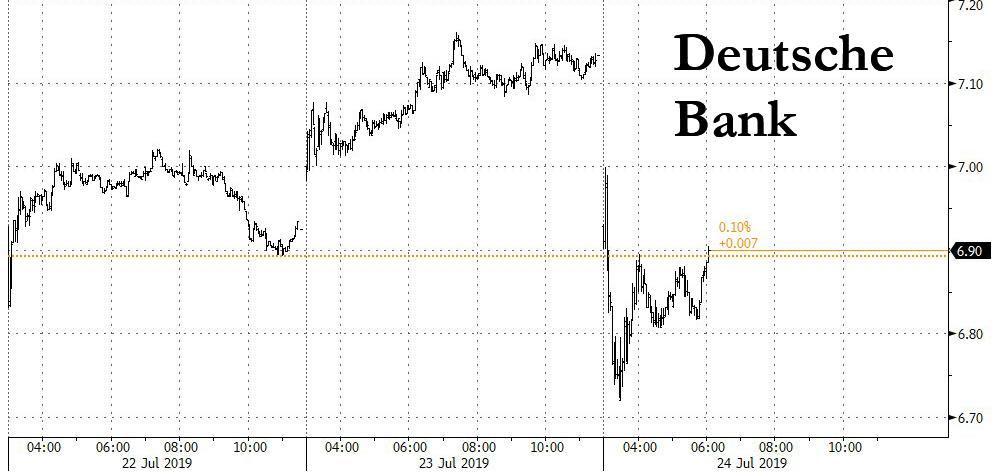

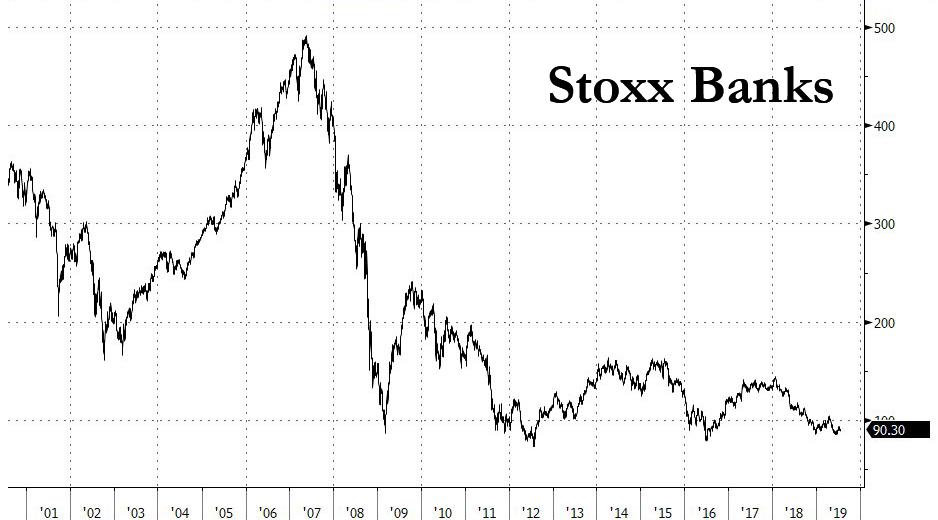

If one ever needed evidence that such a thing as bank karma exists, look no further than Deutsche Bank, which after manipulating and rigging every market it traded in, violating virtually every regulation and anti-money laundering rule in existence, and quietly witnessing the bizarre, unexplained suicide by more than one senior official, has been caught in a downward spiral of spectacular collapse which culminated recently with the biggest corporate restructuring and mass layoff announced by a major bank. And then there are the earnings.

On Wednesday, the bank that is set to layoff over 20% of its workforce, reported a dramatic decline in trading revenue resulting in a far bigger than expected €3.16 billion net loss, a far cry from the €361MM profit a year ago. While the revenue of €6.2 billion was in line with the preliminary release from July 7, the bank warned that 2019 group revenue would be lower than 2018, blaming lower interest rates on increasing pressure on revenue after trading slump deepened in the second quarter, adding urgency to Chief Executive Officer Christian Sewing’s overhaul plans.

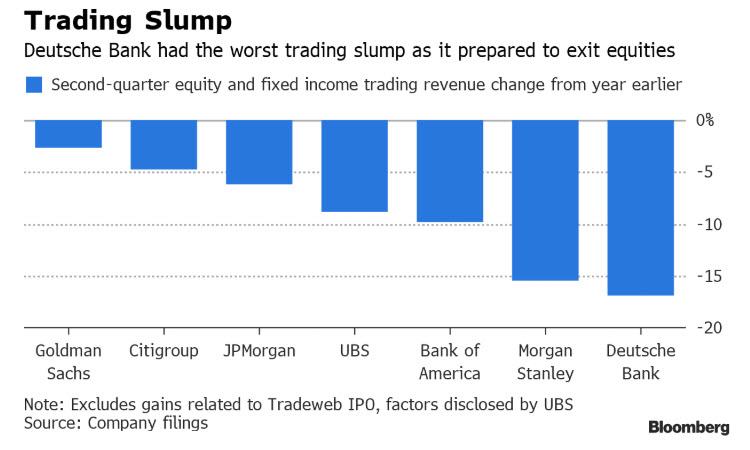

As many expected – largely since it is now firing front-line traders – the bank again underperformed Wall Street peers in trading, with income from buying and selling securities slumping 12%, led by a decline of about a third in the now defunct equities business. While Q2 FICC sales & trading revenue of €1.32 billion was a fraction better than the company-compiled estimate EU1.31 billion, equities sales & trading revenue €369 million badly missed the estimate of €480 million. Fixed income trading declined 11% when adjusting for the TradeWeb IPO. While Sewing is keeping that business, he is reducing the amount of capital it uses.

The resulting total Q2 trading revenue of €1.69 billion not only missed the average estimate of €1.79 billion, but the 17% decline in trading revenue was the worst of all major Wall Street peers.

Deutsche Bank’s dismal trading Q2 results compared with a decline of around 8% at the five biggest Wall Street banks. UBS Group on Tuesday reported a 9% slump in equities trading and 7% lower revenue from fixed income, which however was better than expected and lifted DBK shares sharply higher. Oops.

Deutsche Bank said it started losing business during the quarter as it became clear it would exit equities trading. Sergio Ermotti, the UBS CEO, said Tuesday that some of the balances from the German lender’s business are coming to his bank’s prime brokerage unit; as a reminder, last week we reported that Deutsche was seeing a whopping €1 billion in daily outflows, as part of its exit from equities, in which the German lender had agreed to transfer some 150 billion euros of balances linked to hedge funds to French rival BNP Paribas SA. Additionally, Deutsche Bank is planning to auction its equity derivatives portfolio and kick off the process in the coming weeks, Bloomberg reports.

At the global transaction bank, which CEO Sewing is separating from the investment bank to make it the centerpiece of a new corporate bank division headed by Stefan Hoops, revenue was essentially flat when adjusting for a one-time gain a year earlier.

Elsewhere, Q2 Private & Commercial Bank revenue of €2.49 billion was in line with the company-compiled estimate EU2.49 billion; meanwhile Asset Management revenue €593 million was slightly ahead of estimates.

But wait, there’s more: after warning of about a €2.8 billion charge just a few weeks back, Deutsche decided to make Q2 into yet another kitchen sink quarter, as the bottom line result also included a bigger than expected €3.4 billion restructuring charge. How DB found an additional several hundred million in “one-time expenses” to lump into the charges in under a month is somewhat perplexing, yet traders would have likely let it slide… if only such “kitchen sinking” wasn’t now a regular, quarterly event at Deutsche Bank.

The pain was not over yet, as CFO James von Moltke had even more surprises in store, when he suggested the outlook for lower rates add further downside pressure on revenues: “Frankly it does represent a revenue pressure for us and all of the banks if rates from here go down further,” von Moltke said in an interview with Bloomberg Television. “It’s something that, as you say, is a significant risk to us.”

Von Moltke said earlier this month that the goal of lifting return on tangible equity to 8% in 2022 “is realistic given the interest rate environment we’re facing.” The bank wants to boost its annual revenue by 2 billion euros through 2022, helped by a “modest improvement” in rates.

“We provided a set of numbers,” von Moltke said on Wednesday. “As one always does, one has to make some planning assumptions, those happened to be at the end of May and we are very aware that the outlook deteriorated during June.”

The CFO also said he expected another €2 billion in second half charges, as he hopes to stabilize and grow revenue in the core bank. He also said that the bank would like to have job numbers in the high 80,000s by the end of the year, down from above 90,000 at present, and has given job notifications to about 900 equities staff.

Moltke said that if the European Central Bank does lower rates, he expects it to shield commercial banks from further harm through deposit tiering, in which some overnight deposits that banks park at the ECB are excluded or charged a less punitive rate. We explained last night why absent tiering, the ECB risked crushing Europe’s already suffering banks.

Attempts to put a favorable spin on the latest disastrous numbers fell far short alas, and as Thomas Hallett, bank analyst at Keefe, Bruyette & Woods in London, wrote, “client retention risks, an unfavorable interest rate environment and negative secular trends across divisions present material headwinds to management plans. These results do little to allay market concerns on the ability to deliver on those targets.”

Citi’s Andrew Coombs said he is “most cautious” on the ~€25b revenue assumption the bank has for its 2022 targets. The analyst estimates a greater risk of revenue attrition in the investment bank and believes the bank might need to factor in lower rates at its corporate and retail division

How DB will turnaround the ship with what is increasingly looking like a sub-skeleton crew of workers remains unknown: the German lender’s overhaul resulted in the departure of investment banking head Garth Ritchie. Sewing has taken over oversight over the division at the management board level while operational oversight has been split between Hoops; Mark Fedorcik, head of the investment bank; and Ram Nayak, in charge of fixed-income trading. Christiana Riley, who’s running the bank’s U.S. operations, will join the management board pending regulatory approval.

Deutsche Bank shares fall as much as 5.3% in early Frankfurt trading after the lender reported the disappointing results, and guided to even lower revenue. The move followed an odd gain of 3% on Tuesday after results from UBS and a lift in macro sentiment gave banking stocks a boost.

via ZeroHedge News https://ift.tt/2Yqqdhr Tyler Durden

For the first time since President Xi began his second term in 2017, China has released a defense white paper that doesn’t elaborate on the country’s military priorities so much as it criticizes Beijing’s chief political adversary – the US – while defending the Communist Party’s right to impose its rule over China’s wayward provinces, including Hong Kong, which is still being rattled by protests, and Taiwan.

It’s the latest sign that tensions between Beijing and Washington over the latter’s support for Taiwan – Washington recently approved the sale of $2 billion in tanks and anti-aircraft missiles – might not only scupper trade talks, they could be the spark that ignites World War III. And what’s more, it comes hours after the White House confirmed that the next round of in-person trade talks had been set for next week. Remember, Beijing has repeatedly threatened to use military force against any foreign power who interferes in its relationship with Taiwan, while Taiwan’s leaders have insisted that they would never submit to Communist Party rule, Bloomberg reports.

The paper, titled “China’s National Defense in the New Era” – in a reference to a popular Xi slogan – accused the US of provoking competition among major countries, and noted that the “international security system and order are undermined by growing hegemonism, power politics, unilateralism and constant regional conflicts and wars.”

“(The US) has provoked and intensified competition among major countries, significantly increased its defense expenditure, pushed for additional capacity in nuclear, outer space, cyber and missile defense,” the paper said.

The white paper noted recent patrols by Chinese warships and warplanes around Taiwan, insisting that the operation was intended to send a “stern warning” to Taipei. Oddly, given Beijing’s heated response to the Navy’s “freedom of navigation” operations, the white paper also described the situation in the South China Sea as “generally stable and improving” (despite the international legal battle over which country actually has sovereignty). Though the paper did describe American patrols in the area as “destabilizing.”

As Beijing has often done, the paper criticized foreign forces – a euphemism for the US and UK – for the recent bouts of instability witnessed in Hong Kong, where demonstrations over the hated extradition bill are still going on. On Sunday, 100,000 people rallied in down town Hong Kong for a demonstration that quickly devolved into violence, with police firing tear gas at unruly protesters.

During the press conference introducing the paper, Wu Qian, a spokesman for China’s defense ministry, echoed recent state media reports by insisting that the vandalism of a central government liaison office in Hong Kong was a direct challenge to the Chinese system, and that the PLA garrison in Hong Kong could intervene to end the demonstrations if it is asked by the city’s Beijing-controlled government, the SCMP reports.

“We are closely following the developments in Hong Kong, especially the violent attack against the central government liaison office by radicals on July 21,” Wu said at the briefing.

“Some behaviour of the radical protesters is challenging the authority of the central government and the bottom line of one country, two systems. This is intolerable.”

Foreign Minister Wang Yi blamed the “black hand” of the West for creating trouble in Hong Kong, though he didn’t specifically single out the US.

As CNN pointed out, one change in the 2019 report, compared with the last defense report, published in 2015, is the tight grip that President Xi has over China’s military: It included copious references appearing in the white paper to the “new era” of Xi’s signature ideology.

“Guided by Xi Jinping’s thinking on strengthening the military, China’s national defense in the new era will stride forward along its own path to build a stronger military.”

We imagine analysts at the Pentagon are picking through the report now, trying to suss out exactly what it means for US-China bilateral relations.

via ZeroHedge News https://ift.tt/2MiS8tt Tyler Durden

{kind=link}