Canada declared a national climate emergency on Monday. The next day, Prime Minister Justin Trudeau gave the greenlight to a massive oil sands pipeline.

The House of Commons, with strong support declared climate change a “real and urgent crisis.” A week before, Justin Trudeau proposed a ban on single-use plastics, which, if implemented, would be the latest in a growing number of bans on plastic that could put multibillion-dollar bets on plastics and petrochemicals by the oil industry at risk.

But Trudeau has never really stood in the way of Canada’s oil industry, despite years of platitudes about addressing climate change. That was clear on June 18, when he gave the approval to the Trans Mountain Expansion (not for the first time), a $4.5 billion twin pipeline that would run along an existing line from Alberta to the Pacific Coast in British Columbia.

The Trans Mountain Expansion is one of a few high-profile pipeline projects that have run into serious trouble. Trudeau first gave the greenlight in 2016, but the project ran aground amid legal challenges from First Nations and environmental groups. Last year, Kinder Morgan, the original owner of the project, headed for the exit, threatening the cancel the project altogether.

Desperate to keep it alive – and the clearest example imaginable of how much the Canadian government depends on the oil industry – Trudeau moved to nationalize the project in mid-2018, buying it off of Kinder Morgan’s hands. A year later, here we are, with Ottawa once again trying to push it forward.

“This isn’t an either/or proposition. It is in Canada’s national interest to protect our environment and invest in tomorrow, while making sure people can feed their families today,” Trudeau said on Tuesday. Despite Trudeau’s plea, many see it precisely as an either/or proposition. Faced with a binary choice, Trudeau could either anger the oil industry, or anger First Nations and environmental groups. He chose the former, even though that was mostly expected.

“The approval comes as no surprise—the federal government owns the pipeline after all,” Scotiabank’s Rebekah Young wrote in a note. The Canadian government has vowed to build the project with a Crown corporation, then turn it over to private investors or some other company.

But the next step is unclear.

The approval from Trudeau’s government is a “positive step” for the project, but “project execution risk remains elevated,” Goldman Sachs wrote in a note to clients. The investment bank said that while the government plans to begin construction this year, Goldman is not factoring the project into its base-case forecasts, “given prior uncertainty in the outlook of this project.”

“Today’s decision is a positive development for Canada’s western oil sector, but it will have little impact on short term production,” Rebekah Young for Scotiabank said. The expansion will triple the pipeline system’s current capacity, taking it up to 890,000 bpd.

“However, with the earliest completion date only by 2022,” Young added.

Still, commencing construction on the project would be seen as a breakthrough for Canada’s oil industry.

“We would also anticipate that reaching surety in construction of TMX would provide oil sand producers confidence to commence re-investing in production growth, given the capital constrained budgets most companies are now operating under,” Goldman analysts said.

“That said, we continue to see pipeline shortages until at least 2022…and during this period from now until then, see light-heavy differentials wider than pipeline economics.”

The inability to build a new pipeline had diminished production growth in Canada’s oil sands, and could limit output in the long run. The Canadian Association of Petroleum Producers (CAPP) just released its 2019 Crude Oil Forecast, and lowered its estimate for production growth to 1.44 percent annually through 2035, less than half its prior estimate from 2014.

“Pipeline constraints, a lack of market diversity, and inefficient regulations are largely responsible for holding back Canada’s oil sector,” CAPP said.

Oil forecasts aside, the Trans Mountain Expansion will still run into stiff resistance from First Nations and environmental groups. “The Trudeau government does not have the right to put a pipeline through unceded Secwepemc land,” spokeswoman Kanahus Manuel said, according to Reuters. More lawsuits and protests are inevitable.

Moreover, the pipeline needs permits from British Columbia, where the government has opposed the project.

“[T]he project still faces significant political, regulatory, and judicial challenges, and ultimately we see a tremendous amount of execution risk up until the oil starts flowing,” Gavin MacFarlane, a VP with Moody’s Investors Service, said in comments circulated to reporters.

Meanwhile, the other pipeline that could potentially add takeaway capacity from Alberta – Enbridge’s Line 3 replacement – hit another snag. State agencies in Minnesota said on Tuesday that they would not issue permits until a revised environmental review was completed, following a recent court order that said the state had failed to adequately assess the potential impact of an oil spill. In short, permits could be delayed longer than expected.

If Line 3 fails to move forward for any reason, that increases the stakes and importance for the Trans Mountain Expansion as the only route left for new pipeline capacity. And vice versa.

via ZeroHedge News http://bit.ly/2Rsx6Jc Tyler Durden

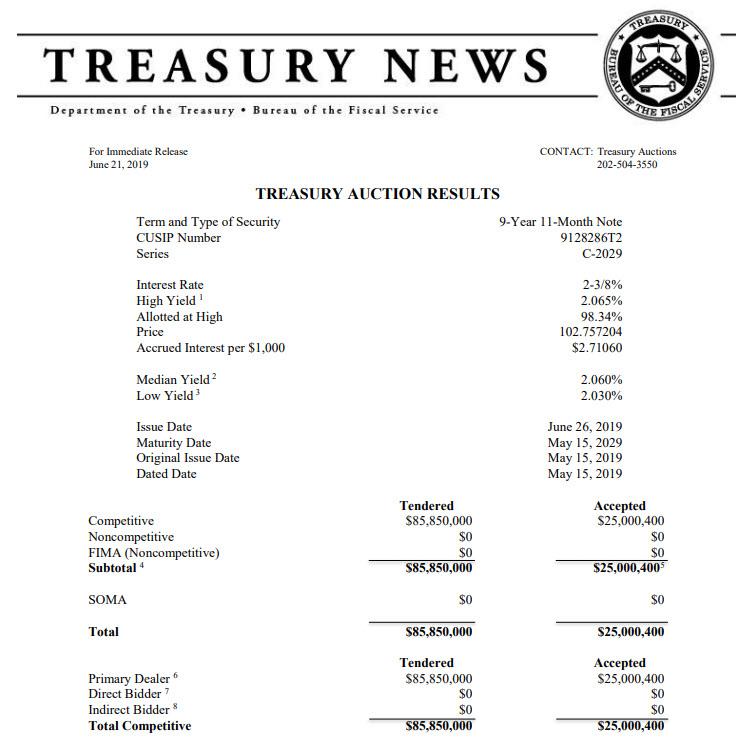

There was some confusion this morning when the US Treasury announced it would auction off a 10Year reopening (9-Years, 11-Months), at the odd time and date of noon on Friday, unlike the traditional time of 2pm on Thursday.

So what’s going on. Well, on Thursday, the Treasury Department reminded investors that it announced on May 1, 2019, its intent to conduct a live small-value contingency auction operation in the second calendar quarter of 2019.

The reason: “Treasury believes that it is prudent to regularly test its contingency auction infrastructure. This small-value contingency auction operation will be on June 21, 2019. This will be a 9-year 11-month note auction.” Unlike traditional auctions, this was a small test to make sure the Treasury’s emergency infrastructure is operational, and as the Treasury disclosed, for this live “small-value contingency auction operation”, the following conditions applied:

Bids shall be submitted by telephone to Treasury’s fiscal agent the Federal Reserve Bank of New York (FRBNY).

Only primary dealers, as designated by FRBNY, may submit bids.

Each primary dealer can submit up to 5 competitive bids.

Net long position (NLP) reporting will not be required for this coupon.

Each competitive bid must be at a separate yield.

Customer bids will not be accepted.

Noncompetitive tenders, including FIMA tenders, will not be accepted.

SOMA will be accepted.

Moments ago the results were announced, and the details were as follows:

Size: 25 million

Maturity date: May 15, 2029 (9-year, 11-month reopening on Cusip 6T2)

Yield allotted at high: 2.065%

Bid to Cover 3.43

Awarded to Primary Dealers: 100%

By implication, awarded to Directs and Indirects: 0%

So while the auction was immaterial from a gross or net debt issuance standpoint, it confirmed that its “contingency auction infrastructure” is operational, which means that under emergency conditions where dealers can only buy US Treasuries via telephone – needless to say those conditions would be especially concerning for the broader US and global economy – the US government will still be able to fund itself.

via ZeroHedge News http://bit.ly/2N0asJH Tyler Durden

Rose Mary Knick, the plaintiff in Knick v. Township of Scott, with her lawyers from the Pacific Legal Foundation.

In Knick v. Township of Scott, an important decision issued this morning, the Supreme Court overruled a precedent that creates a Catch-22 blocking property owners from bringing takings cases against state and local governments in federal court.

The main point at issue in Knick was whether the Court should overrule Williamson County Regional Planning Commission v. Hamilton Bank (1985). Under Williamson County, a property owner who contends that the government has taken his property and therefore owes “just compensation” under the Fifth Amendment, could not file a case in federal court until he or she first secured a “final decision” from the relevant state regulatory agency and “exhausted” all possible remedies in state court. Even then, it was still often impossible to bring a federal claim, because various procedural rules preclude federal courts from reviewing final decisions in cases that were initially brought in state court. I discussed the issues at stake in the case in a Wall Street Journal op ed, and more fully here, and in an amicus brief I coauthored on behalf of the Cato Institute, the National Federation of Independent Business, the Southeastern Legal Foundation, the Beacon Center of Tennessee, the Reason Foundation (which publishes Reason magazine and this website), and myself.

The majority opinion by Chief Justice John Roberts overrules Williamson County and eliminates the Catch-22 that we highlighted in our brief, and which has long been heavily criticized by legal scholars and others. Here is the key part of the opinion:

In Williamson County Regional Planning Comm’n v. Hamilton Bank of Johnson City, 473 U. S. 172 (1985), we held that a property owner whose property has been taken by a local government has not suffered a violation of his Fifth Amendment rights—and thus cannot bring a federal takings claim in federal court—until a state court has denied his claim for just compensation under state law….

The Williamson County Court anticipated that if the property owner failed to secure just compensation understate law in state court, he would be able to bring a “ripe” federal takings claim in federal court. See id., at 194. But as we later held in San Remo Hotel, L. P. v. City and County of San Francisco, 545 U. S. 323 (2005), a state court’s resolution of a claim for just compensation under state law generally has preclusive effect in any subsequent federal suit. The takings plaintiff thus finds himself in a Catch-22: He cannot go to federal court without going to state court first; but if he goes to state court and loses, his claim will be barred in federal court. The federal claim dies aborning.

The San Remo preclusion trap should tip us off that the state-litigation requirement rests on a mistaken view of the Fifth Amendment. The Civil Rights Act of 1871, after all, guarantees “a federal forum for claims of unconstitutional treatment at the hands of state officials,” and the settled rule is that “exhaustion of state remedies ‘is not a prerequisite to an action under [42 U. S. C.] §1983….'” But the guarantee of a federal forum rings hollow for takings plaintiffs, who are forced to litigate their claims in state court.

We now conclude that the state-litigation requirement imposes an unjustifiable burden on takings plaintiffs, conflicts with the rest of our takings jurisprudence, and must be overruled. A property owner has an actionable Fifth Amendment takings claim when the government takes his property without paying for it. That does not mean that the government must provide compensation in advance of a taking or risk having its action invalidated: So long as the property owner has some way to obtain compensation after the fact, governments need not fear that courts will enjoin their activities. But it does mean that the property owner has suffered a violation of his Fifth Amendment rights when the government takes his property without just compensation, and therefore may bring his claim in federal court under §1983 at that time.

Chief Justice Roberts also emphasized that Williamson County created a double standard under which Takings Clause claims are subjected to a perverse requirement that is not imposed on other constitutional claims against state and local governments:

The state-litigation requirement relegates the Takings Clause “to the status of a poor relation” among the provisions of the Bill of Rights. Dolan v. City of Tigard, 512

U. S. 374, 392 (1994). Plaintiffs asserting any other constitutional claim are guaranteed a federal forum under §1983, but the state-litigation requirement “hand[s] authority over federal takings claims to state courts.” San Remo, 545 U. S., at 350 (Rehnquist, C. J., concurring in judgment). Fidelity to the Takings Clause and our cases construing it requires overruling Williamson County and restoring takings claims to the full-fledged constitutional status the Framers envisioned when they included the Clause among the other protections in the Bill of Rights.

As emphasized in our amicus brief, one of the main reasons why the framers of the Fourteenth Amendment chose to “incorporate” the Bill of Rights against the states in 1868 was to preclude abuses by state governments, and to ensure that these rights could be vindicated in federal court. State courts can be and sometimes are tilted in favor of their own state and local governments. Particularly in the many states where state judges are elected, they may be part of the same political coalition as the state and local government officials who adopted the policy that may have violated the Takings Clause. In many—perhaps even most—situations, it will make little difference whether a takings claim is heard in state court or federal court. But sometimes, a federal forum is essential to ensuring fair consideration of the property owner’s claims.

The standard rationale for Williamson County, defended in Justice Elena Kagan’s dissent today, is that the state has not really “taken” property without just compensation until a state court has reached a final decision upholding the government’s actions. Chief Justice Roberts nicely dispenses with that theory:

Contrary to Williamson County, a property owner has a claim for a violation of the Takings Clause as soon as a government takes his property for public use without paying for it. The Clause provides: “[N]or shall private property be taken for public use, without just compensation.” It does not say: “Nor shall private property be taken for public use, without an available procedure that will result in compensation.” If a local government takes private property without paying for it, that government has violated the Fifth Amendment—just as the Takings Clause says—without regard to subsequent state court proceedings….

The Fifth Amendment right to full compensation arises at the time of the taking, regardless of post-taking remedies that may be available to the property owner. That principle was confirmed in Jacobs v. United States, 290 U. S. 13 (1933), where we held that a property owner found to have a valid takings claim is entitled to compensation as if it had been “paid contemporaneously with the taking”—that is, the compensation must generally consist of the total value of the property when taken, plus interest from that time.

I would add that the same reasoning could be used to deny a federal forum for numerous other constitutional rights claims. By the logic of Williamson County, a state government has not really censored speech until a state court upholds the censorship policy. It has not really engaged in unconstitutional racial discrimination in hiring until a state court issues a “final decision” holding that the challenged hiring rules are legal. And so on.

Chief Justice Roberts’ opinion also effectively explains why Williamson County should be overruled based on the Supreme Court’s far from precise criteria for reversing precedent. As he emphasizes, “Williamson County was not just wrong. Its reasoning was exceptionally ill founded and conflicted with much of our takings jurisprudence.” He also notes that the ruling “has come in for repeated criticism over the years from Justices of this Court and many respected commentators,” that it has “become unworkable in practice,” and that “there are no reliance interests on the state-litigation requirement” because allowing takings cases to go to federal court would not lead to the invalidation of otherwise lawful state and local government policies.

Given the serious flaws of Williamson County, it is unfortunate that Knick turned out to be a close 5-4 decision, with the justices divided along ideological lines—the five conservatives in the majority and four liberals in dissent. Indeed, the case was reargued in order to include Justice Brett Kavanaugh, who had not yet been confirmed at the time of the initial oral argument. It now seems highly likely that the Court took this step because the justices were previously split 4-4. I would add, however, that Kavanaugh’s participation ultimately led to the same outcome as what likely would have occurred had Justice Anthony Kennedy remained on the Court. Kennedy was a critic of Williamson County, and had joined a 2005 concurring opinion urging the Court to consider reversing it.

The dissent by Justice Elena Kagan fails to provide any good justification for keeping Williamson County in place. Much of it seems to assume that the majority requires immediate payment of compensation any time a state or local government adopts any policy that might potentially qualify as a taking:

[A] government actor usually cannot know in advance whether implementing a regulatory program will effect a taking, much less of whose property. Until today, such an official could do his work without fear of wrongdoing, in any jurisdiction that had set up a reliable means for property owners to obtain compensation. Even if some regulatory action turned out to take someone’s property, the official would not have violated the Constitution. But no longer. Now, when a government undertakes land-use regulation (and what government doesn’t?), the responsible employees will almost inescapably become constitutional malefactors. That is not a fair position in which to place persons carrying out their governmental duties.

But in fact the majority in no way turns government officials into “constitutional malefactors” merely because they enact a “regulatory program.” It just holds that aggrieved property owners can then bring a takings case in federal court. There is no constitutional violation, however, unless the court finds that the program in question effects a taking and the state didn’t pay. Exactly the same thing happens when the regulatory program in question is challenged in state court, and the latter rules that it was a taking.

Justice Kagan also argues that the Williamson County rule is supported by a “mountain of precedent” going back to the nineteenth century. But, as the majority points out, those cases addressed situations where the plaintiff sued for injunctive relief blocking a taking, rather than for monetary compensation. Once mechanisms for providing monetary compensation were established after 1870, injunctive relief was not an appropriate remedy for a Takings Clause claim. Thus, “every one of the cases cited by the dissent would come out the same way—the plaintiffs would not be entitled to the relief they requested because they could instead pursue a suit for compensation.”

I would add that there is a crucial distinction between a situation where the state does not deny that a taking has occurred, but establishes a compensation procedure that does not provide immediate payment, and one where the state argues that there was no taking in the first place. As Roberts notes, the former scenario does not amount to a violation of the Takings Clause, so long as the state ultimately pays full compensation—including accumulated interest for the period that elapses between the moment when the taking took place and the time when compensation was actually paid. The latter case, by contrast, is no different from any other situation where a citizen claims the state has violated the federal Constitution, and the government denies it. Such cases can and should be entitled to a forum in federal court.

Justice Kagan even defends the “Catch-22” created by Williamson County, arguing that it is actually a feature rather than a bug, because it allows state courts to address issues on which they have greater expertise than federal courts. For reasons I explained in this article, the same superior expertise rationale can be used to justify consigning a wide range of other federal constitutional claims to state court, in situations where state judges are likely to have greater expertise than federal ones.

Finally, I am happy to report that the federal government’s strange “Klingon forehead” rationale for retaining large parts of Williamson County ended up playing no part in the Court’s decision. Neither the majority justices nor the dissenters endorse it. Indeed, they barely even mention it (the majority dispenses with it in a footnote).

from Latest – Reason.com http://bit.ly/2L65YOZ

via IFTTT

Rose Mary Knick, the plaintiff in Knick v. Township of Scott, with her lawyers from the Pacific Legal Foundation.

In Knick v. Township of Scott, an important decision issued this morning, the Supreme Court overruled a precedent that creates a Catch-22 blocking property owners from bringing takings cases against state and local governments in federal court.

The main point at issue in Knick was whether the Court should overrule Williamson County Regional Planning Commission v. Hamilton Bank (1985). Under Williamson County, a property owner who contends that the government has taken his property and therefore owes “just compensation” under the Fifth Amendment, could not file a case in federal court until he or she first secured a “final decision” from the relevant state regulatory agency and “exhausted” all possible remedies in state court. Even then, it was still often impossible to bring a federal claim, because various procedural rules preclude federal courts from reviewing final decisions in cases that were initially brought in state court. I discussed the issues at stake in the case in a Wall Street Journal op ed, and more fully here, and in an amicus brief I coauthored on behalf of the Cato Institute, the National Federation of Independent Business, the Southeastern Legal Foundation, the Beacon Center of Tennessee, the Reason Foundation (which publishes Reason magazine and this website), and myself.

The majority opinion by Chief Justice John Roberts overrules Williamson County and eliminates the Catch-22 that we highlighted in our brief, and which has long been heavily criticized by legal scholars and others. Here is the key part of the opinion:

In Williamson County Regional Planning Comm’n v. Hamilton Bank of Johnson City, 473 U. S. 172 (1985), we held that a property owner whose property has been taken by a local government has not suffered a violation of his Fifth Amendment rights—and thus cannot bring a federal takings claim in federal court—until a state court has denied his claim for just compensation under state law….

The Williamson County Court anticipated that if the property owner failed to secure just compensation understate law in state court, he would be able to bring a “ripe” federal takings claim in federal court. See id., at 194. But as we later held in San Remo Hotel, L. P. v. City and County of San Francisco, 545 U. S. 323 (2005), a state court’s resolution of a claim for just compensation under state law generally has preclusive effect in any subsequent federal suit. The takings plaintiff thus finds himself in a Catch-22: He cannot go to federal court without going to state court first; but if he goes to state court and loses, his claim will be barred in federal court. The federal claim dies aborning.

The San Remo preclusion trap should tip us off that the state-litigation requirement rests on a mistaken view of the Fifth Amendment. The Civil Rights Act of 1871, after all, guarantees “a federal forum for claims of unconstitutional treatment at the hands of state officials,” and the settled rule is that “exhaustion of state remedies ‘is not a prerequisite to an action under [42 U. S. C.] §1983….'” But the guarantee of a federal forum rings hollow for takings plaintiffs, who are forced to litigate their claims in state court.

We now conclude that the state-litigation requirement imposes an unjustifiable burden on takings plaintiffs, conflicts with the rest of our takings jurisprudence, and must be overruled. A property owner has an actionable Fifth Amendment takings claim when the government takes his property without paying for it. That does not mean that the government must provide compensation in advance of a taking or risk having its action invalidated: So long as the property owner has some way to obtain compensation after the fact, governments need not fear that courts will enjoin their activities. But it does mean that the property owner has suffered a violation of his Fifth Amendment rights when the government takes his property without just compensation, and therefore may bring his claim in federal court under §1983 at that time.

Chief Justice Roberts also emphasized that Williamson County created a double standard under which Takings Clause claims are subjected to a perverse requirement that is not imposed on other constitutional claims against state and local governments:

The state-litigation requirement relegates the Takings Clause “to the status of a poor relation” among the provisions of the Bill of Rights. Dolan v. City of Tigard, 512

U. S. 374, 392 (1994). Plaintiffs asserting any other constitutional claim are guaranteed a federal forum under §1983, but the state-litigation requirement “hand[s] authority over federal takings claims to state courts.” San Remo, 545 U. S., at 350 (Rehnquist, C. J., concurring in judgment). Fidelity to the Takings Clause and our cases construing it requires overruling Williamson County and restoring takings claims to the full-fledged constitutional status the Framers envisioned when they included the Clause among the other protections in the Bill of Rights.

As emphasized in our amicus brief, one of the main reasons why the framers of the Fourteenth Amendment chose to “incorporate” the Bill of Rights against the states in 1868 was to preclude abuses by state governments, and to ensure that these rights could be vindicated in federal court. State courts can be and sometimes are tilted in favor of their own state and local governments. Particularly in the many states where state judges are elected, they may be part of the same political coalition as the state and local government officials who adopted the policy that may have violated the Takings Clause. In many—perhaps even most—situations, it will make little difference whether a takings claim is heard in state court or federal court. But sometimes, a federal forum is essential to ensuring fair consideration of the property owner’s claims.

The standard rationale for Williamson County, defended in Justice Elena Kagan’s dissent today, is that the state has not really “taken” property without just compensation until a state court has reached a final decision upholding the government’s actions. Chief Justice Roberts nicely dispenses with that theory:

Contrary to Williamson County, a property owner has a claim for a violation of the Takings Clause as soon as a government takes his property for public use without paying for it. The Clause provides: “[N]or shall private property be taken for public use, without just compensation.” It does not say: “Nor shall private property be taken for public use, without an available procedure that will result in compensation.” If a local government takes private property without paying for it, that government has violated the Fifth Amendment—just as the Takings Clause says—without regard to subsequent state court proceedings….

The Fifth Amendment right to full compensation arises at the time of the taking, regardless of post-taking remedies that may be available to the property owner. That principle was confirmed in Jacobs v. United States, 290 U. S. 13 (1933), where we held that a property owner found to have a valid takings claim is entitled to compensation as if it had been “paid contemporaneously with the taking”—that is, the compensation must generally consist of the total value of the property when taken, plus interest from that time.

I would add that the same reasoning could be used to deny a federal forum for numerous other constitutional rights claims. By the logic of Williamson County, a state government has not really censored speech until a state court upholds the censorship policy. It has not really engaged in unconstitutional racial discrimination in hiring until a state court issues a “final decision” holding that the challenged hiring rules are legal. And so on.

Chief Justice Roberts’ opinion also effectively explains why Williamson County should be overruled based on the Supreme Court’s far from precise criteria for reversing precedent. As he emphasizes, “Williamson County was not just wrong. Its reasoning was exceptionally ill founded and conflicted with much of our takings jurisprudence.” He also notes that the ruling “has come in for repeated criticism over the years from Justices of this Court and many respected commentators,” that it has “become unworkable in practice,” and that “there are no reliance interests on the state-litigation requirement” because allowing takings cases to go to federal court would not lead to the invalidation of otherwise lawful state and local government policies.

Given the serious flaws of Williamson County, it is unfortunate that Knick turned out to be a close 5-4 decision, with the justices divided along ideological lines—the five conservatives in the majority and four liberals in dissent. Indeed, the case was reargued in order to include Justice Brett Kavanaugh, who had not yet been confirmed at the time of the initial oral argument. It now seems highly likely that the Court took this step because the justices were previously split 4-4. I would add, however, that Kavanaugh’s participation ultimately led to the same outcome as what likely would have occurred had Justice Anthony Kennedy remained on the Court. Kennedy was a critic of Williamson County, and had joined a 2005 concurring opinion urging the Court to consider reversing it.

The dissent by Justice Elena Kagan fails to provide any good justification for keeping Williamson County in place. Much of it seems to assume that the majority requires immediate payment of compensation any time a state or local government adopts any policy that might potentially qualify as a taking:

[A] government actor usually cannot know in advance whether implementing a regulatory program will effect a taking, much less of whose property. Until today, such an official could do his work without fear of wrongdoing, in any jurisdiction that had set up a reliable means for property owners to obtain compensation. Even if some regulatory action turned out to take someone’s property, the official would not have violated the Constitution. But no longer. Now, when a government undertakes land-use regulation (and what government doesn’t?), the responsible employees will almost inescapably become constitutional malefactors. That is not a fair position in which to place persons carrying out their governmental duties.

But in fact the majority in no way turns government officials into “constitutional malefactors” merely because they enact a “regulatory program.” It just holds that aggrieved property owners can then bring a takings case in federal court. There is no constitutional violation, however, unless the court finds that the program in question effects a taking and the state didn’t pay. Exactly the same thing happens when the regulatory program in question is challenged in state court, and the latter rules that it was a taking.

Justice Kagan also argues that the Williamson County rule is supported by a “mountain of precedent” going back to the nineteenth century. But, as the majority points out, those cases addressed situations where the plaintiff sued for injunctive relief blocking a taking, rather than for monetary compensation. Once mechanisms for providing monetary compensation were established after 1870, injunctive relief was not an appropriate remedy for a Takings Clause claim. Thus, “every one of the cases cited by the dissent would come out the same way—the plaintiffs would not be entitled to the relief they requested because they could instead pursue a suit for compensation.”

I would add that there is a crucial distinction between a situation where the state does not deny that a taking has occurred, but establishes a compensation procedure that does not provide immediate payment, and one where the state argues that there was no taking in the first place. As Roberts notes, the former scenario does not amount to a violation of the Takings Clause, so long as the state ultimately pays full compensation—including accumulated interest for the period that elapses between the moment when the taking took place and the time when compensation was actually paid. The latter case, by contrast, is no different from any other situation where a citizen claims the state has violated the federal Constitution, and the government denies it. Such cases can and should be entitled to a forum in federal court.

Justice Kagan even defends the “Catch-22” created by Williamson County, arguing that it is actually a feature rather than a bug, because it allows state courts to address issues on which they have greater expertise than federal courts. For reasons I explained in this article, the same superior expertise rationale can be used to justify consigning a wide range of other federal constitutional claims to state court, in situations where state judges are likely to have greater expertise than federal ones.

Finally, I am happy to report that the federal government’s strange “Klingon forehead” rationale for retaining large parts of Williamson County ended up playing no part in the Court’s decision. Neither the majority justices nor the dissenters endorse it. Indeed, they barely even mention it (the majority dispenses with it in a footnote).

from Latest – Reason.com http://bit.ly/2L65YOZ

via IFTTT

Thousands of people took to the streets of Hong Kong on Friday for the third time in less than a week, calling for the city-state’s chief executive Carrie Lam to resign, while demanding that the government drop a controversial extradition bill which would allow Hong Kong to extradite people who are wanted for crimes in mainland China.

Arsenal St out front of #HK police HQ is really packed and LOUD right now. Main call: Release them! pic.twitter.com/SV8gMieLhP

— Kong Tsung-gan / 江松澗 (@KongTsungGan) June 21, 2019

The mostly young protesters surrounded the police headquarters in the city’s Wan Chai district on Friday – blocking roads and staging a sit-in less than half-a-mile from legislative offices.

Thousands of demonstrators again occupied Hong Kong’s downtown area on Friday [Euan McKirdy/Al Jazeera]

— Kong Tsung-gan / 江松澗 (@KongTsungGan) June 21, 2019

One of the group’s leaders is activist Joshua Wong, who was recently released from prison after rising to prominence during the 2014 Umbrella Revolution. Wong told Al Jazeera that he risks rearrest under the “hardline suppression of the police force,” for participating in an unauthorized protest.

Joshua Wong (Euan McKirdy/Al Jazeera)

Wong said the demonstration at police headquarters showed the anger of the protesters at the treatment of their comrades at the hands of riot officers after violent clashes last week.

He said, however, Friday’s actions were a peaceful occupation of the roads around the building, and protesters would not try to storm the complex.

Wong said his organisation, Demosisto, encouraged people to join the demonstration, and the past two weeks encouraged his view of Hong Kongers’ political and civil sense.

“It’s the miracle of Hong Kong,” said Wong. –Al Jazeera

Local police have asked the protesters to leave the area, however they are not planning a “clearance operation” according to a spokeswoman. “We respect the rights of the public to express their views in a peaceful manner,” she said.

A new flag’s just appeared in the crowd to much applause: a white bauhinia on black background dripping w red blood. (The #CCP-imposed ‘official’ flag is white bauhinia on Communist red background.) pic.twitter.com/xjZWj160cx

— Kong Tsung-gan / 江松澗 (@KongTsungGan) June 21, 2019

Now the last remaining police outside, at the top of the escalator, are getting pelted w what must be apples or tomatoes, but they refuse to go in behind the rolling steel shutter behind them. pic.twitter.com/s0kwdrlKKW

— Kong Tsung-gan / 江松澗 (@KongTsungGan) June 21, 2019

Lam apologizes

On Tuesday Lam issued a rare public apology, saying she was “sincerely sorry” for her handling of the extradition bill which resulted in two prior protests which attracted over 1 million and 2 million participants respectively according to organizers.

“I have heard you loud and clear and have reflected deeply on all that has transpired,” said Lam, adding “The concerns over the last few months have been caused by the deficiencies of the (Hong Kong) government.”

That said, while Lam committed to indefinitely suspend (pause) the extradition bill last Sunday, she did not respond to demands that Hong Kong completely withdraw. She has also failed to call for an investigation into allegations of police brutality during a protest on June 12 which turned violent.

Hong Kong police were criticised for their heavy-handed response to last week’s protests but were subdued on Friday [Euan McKirdy/Al Jazeera]

“The chief executive said that the bill would be delayed. It needs to be scrapped and we are also protesting the violent reaction of the Hong Kong police,” 21-year-old City University student ‘Cheung,’ who said there are “numerous issues” that Hong Kong residents are angry over. Cheung suggested that “both” peaceful protest and more direct action are needed, according to Al Jazeera.

“I won’t judge anyone who uses violence. They just want to support Hong Kong,” she added.

Student and pro-democracy groups had given Lam until 5 p.m. Thursday to respond to those demands, saying they would stage further protests Friday if she did not. Those protests began with a peaceful sit in outside the legislature and central government offices, which have been closed to all business, before demonstrators escalated by seizing Harcourt Road.

Some of the protesters brought signs imploring the police not to shoot at them – referring to the violence that broke out last week when police deployed rubber bullets, tear gas and bean bags against the protesters, enraging many.

“In the last few days, police officials have said that they haven’t done anything wrong,” one 20-year-old protester named Kong told Al Jazeera. “We no longer have confidence in the police, and we won’t allow the incident to be forgotten.”

via ZeroHedge News http://bit.ly/2KrIqEI Tyler Durden

There’s plans in the works to cover a mural of George Washington from the halls of George Washington High School in San Francisco due to complaints that it’s offensive and demeaning to Native Americans and African Americans.

The San Francisco school board is expected to decide next week whether to cover the image or paint over it, but there’s no plans among top officials to leave the imagery in the open for students to view, according to several Bay Area news reports.

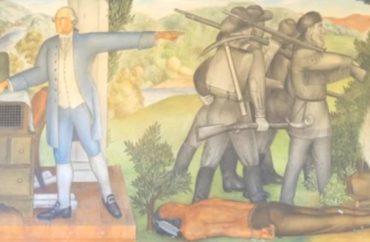

Board members appear to agree with a working group’s determination that the mural “traumatizes students and community members.” The “Life of Washington” mural, which consists of 13 panels, was painted in 1936. One of the images involves Washington gesturing toward a group of explorers who are walking by the body of a presumably deceased Native American. Another depicts Washington next to several slaves performing various types of manual labor.

At a June 18 special meeting to consider the controversial paintings, “not one school board member advocated to keep the mural,” reportsSF Weekly.

“Instead, Commissioners Gabriela Lopez, Alison Collins, Stevon Cook, and Mark Sanchez commented on how emotionally draining it was to hear — and have other rehash for them — the pain they know firsthand comes from violent, demeaning imagery like this.”

The three options before the board are to obscure the mural with curtains, create acoustic panels to cover it up, or paint over it; each option would costs anywhere from 300,000 to $800,000 to complete, the San Francisco Chroniclereports.

District spokeswoman Gentle Blythe told the Chroniclethe mural is “huge and complicated,” and that even though it consists of only a couple of controversial images the board’s decision will impact the entire fresco.

About 100 people packed the recent school board meeting to weigh in on the issue, many of whom spoke against covering the mural up.

“We should be teaching about the mural and what it means. I’m half native American. I have no problem with the mural. It depicts what happened,” said one mural proponent, reports FOX KTVU 2.

Writing in National Review, James Sutton reportsthe mural was never really a bother at the high school.

“The mural (which lies about 20 blocks from my house) wasn’t even particularly opposed by the student body. According to teachers who attended the public hearings over the mural, the majority of students were against its removal or just apathetic. But a small group of outside busybodies joined with a few students to ensure that it would be removed from the public’s sight.

Once the words ‘racist’ or ‘white supremacist’ are attached to something, no matter how inaccurate, liberals will not risk their reputation by defending it,” Sutton wrote.

via ZeroHedge News http://bit.ly/2RsVJoY Tyler Durden

It turns out that public schools aren’t actually free and open to all. One Texas district, Lovejoy Independent School District, has been collecting tuition from students living outside of district boundaries since 2013—with current annual rates sitting as high as $14,000 per student. The district only offers a limited number of spots to paying outsiders and selects finalists based on their academic performance and disciplinary records. Even then, the lucky students still have to reapply each year, there is no guarantee that their siblings will be admitted, and transportation isn’t provided.

Lovejoy isn’t alone, as districts around the country use a similar tactic. Just in Texas, the school districts in Sharyland, Rockwall, and Magnolia all have their own policies demanding thousands from students coming from outside the district. They justify these restrictive policies and fees by arguing that outside students don’t contribute to the district’s local tax base. This is true—but it points to a deeper problem. The current public school system only gives freedom to wealthy families that can afford to get their child enrolled in the right school, making school choice a luxury rather than a basic right.

Texas law allows districts to be selective with transfers, to cap them, or to shut them out entirely. Unsurprisingly, these types of restrictions cater to political motivations over student needs—hurting disadvantaged families the most. A 2017 study of Ohio, which has restrictive enrollment policies similar to those in Texas, found that wealthy suburban school districts are far less likely than other types of districts to accept students from outside district boundaries. The report refers to these districts as “walled” districts because they surround the state’s largest inner cities—such as Cleveland and Cincinnati—and trap disadvantaged students in those inner-city districts.

When districts do accept outside students, they often do so only as long as it benefits them financially. Lovejoy first rolled out its inter-district enrollment program in 2013 because it wanted to generate more revenue. Ted Moore, the district superintendent at the time, announced the strategy as a way to counteract a recent $2.5 million cut in state funding. He further added that the district would “get out of the transfer business” once Lovejoy’s schools were filled by district residents.It’s understandable that schools would be concerned about their bottom lines, but the perverse incentives created by this government system favor those least in need.

It doesn’t have to be this way. Many states offer open enrollment policies. Florida, for instance, implemented a choice-friendly law in 2017 that requires districts to accommodate outside students. Any schools in the state with the space must let kids in via a lottery process, and must give priority to certain types of disadvantaged students. Those schools are not allowed to charge tuition.

Another way to knock down the perverse incentives that restrict choice for disadvantaged students is to reduce the school system’s reliance on local tax revenues. Local dollars usually don’t follow students across district lines, making it so that many districts—especially property-wealthy ones that don’t receive as much state funding—have little incentive to accept outsiders. States that reform their school finance systems so that they are less dependent on local taxes often see families choosing schools outside their home districts—a phenomenon that’s been observed in Indiana. Once local revenues stop being a factor, state dollars more easily follow students across district lines—giving educational freedom to more families.

Even with the high tuition rates and the competitive application process, the Lovejoy Independent School District reports that its open enrollment program is still popular. One look at the district’s accolades explains it all—it boasts test performance scores in the top 1 percent of Texas districts, and provides a robust college preparatory curriculum. While it’s hard not to be happy for the families that do get access to a quality education, that access shouldn’t be determined by a public school system that favors deep pockets and political leverage.

from Latest – Reason.com http://bit.ly/2Y05UnA

via IFTTT

It turns out that public schools aren’t actually free and open to all. One Texas district, Lovejoy Independent School District, has been collecting tuition from students living outside of district boundaries since 2013—with current annual rates sitting as high as $14,000 per student. The district only offers a limited number of spots to paying outsiders and selects finalists based on their academic performance and disciplinary records. Even then, the lucky students still have to reapply each year, there is no guarantee that their siblings will be admitted, and transportation isn’t provided.

Lovejoy isn’t alone, as districts around the country use a similar tactic. Just in Texas, the school districts in Sharyland, Rockwall, and Magnolia all have their own policies demanding thousands from students coming from outside the district. They justify these restrictive policies and fees by arguing that outside students don’t contribute to the district’s local tax base. This is true—but it points to a deeper problem. The current public school system only gives freedom to wealthy families that can afford to get their child enrolled in the right school, making school choice a luxury rather than a basic right.

Texas law allows districts to be selective with transfers, to cap them, or to shut them out entirely. Unsurprisingly, these types of restrictions cater to political motivations over student needs—hurting disadvantaged families the most. A 2017 study of Ohio, which has restrictive enrollment policies similar to those in Texas, found that wealthy suburban school districts are far less likely than other types of districts to accept students from outside district boundaries. The report refers to these districts as “walled” districts because they surround the state’s largest inner cities—such as Cleveland and Cincinnati—and trap disadvantaged students in those inner-city districts.

When districts do accept outside students, they often do so only as long as it benefits them financially. Lovejoy first rolled out its inter-district enrollment program in 2013 because it wanted to generate more revenue. Ted Moore, the district superintendent at the time, announced the strategy as a way to counteract a recent $2.5 million cut in state funding. He further added that the district would “get out of the transfer business” once Lovejoy’s schools were filled by district residents.It’s understandable that schools would be concerned about their bottom lines, but the perverse incentives created by this government system favor those least in need.

It doesn’t have to be this way. Many states offer open enrollment policies. Florida, for instance, implemented a choice-friendly law in 2017 that requires districts to accommodate outside students. Any schools in the state with the space must let kids in via a lottery process, and must give priority to certain types of disadvantaged students. Those schools are not allowed to charge tuition.

Another way to knock down the perverse incentives that restrict choice for disadvantaged students is to reduce the school system’s reliance on local tax revenues. Local dollars usually don’t follow students across district lines, making it so that many districts—especially property-wealthy ones that don’t receive as much state funding—have little incentive to accept outsiders. States that reform their school finance systems so that they are less dependent on local taxes often see families choosing schools outside their home districts—a phenomenon that’s been observed in Indiana. Once local revenues stop being a factor, state dollars more easily follow students across district lines—giving educational freedom to more families.

Even with the high tuition rates and the competitive application process, the Lovejoy Independent School District reports that its open enrollment program is still popular. One look at the district’s accolades explains it all—it boasts test performance scores in the top 1 percent of Texas districts, and provides a robust college preparatory curriculum. While it’s hard not to be happy for the families that do get access to a quality education, that access shouldn’t be determined by a public school system that favors deep pockets and political leverage.

from Latest – Reason.com http://bit.ly/2Y05UnA

via IFTTT

Curtis Flowers, a black man tried six times for the same 1996 quadruple murder, will get a seventh trial, the Supreme Court ruled Friday.

Writing for the majority, Justice Brett Kavanaugh said that prosecutor Doug Evans—who oversaw all six trials—violated Flowers’ constitutional rights when he sought to keep African-Americans off of the jury. Evans struck 41 out of 43 potential black jurors over the course of the legal proceedings, including five out of six in the final trial. Such conduct is in contention with precedent outlined in Baston v. Kentucky, he said, a Supreme Court decision that ruled that peremptory challenges—in which a prosecutor may strike a juror without reason—cannot be racially biased.

“The numbers speak loudly,” Kavanaugh wrote. “Over the course of the first four trials, there were 36 black prospective jurors against whom the State could have exercised a peremptory strike. The State tried to strike all 36.”

Flowers is currently on death row. Two of his trials ended in hung juries, and with the high court’s latest decision, all four convictions have been overturned on appeal.

Justices Clarence Thomas and Neil Gorsuch dissented. “The majority builds its decision around the narrative that this case has a long history of race discrimination,” Thomas wrote. “This narrative might make for an entertaining melodrama, but it has no basis in the record.” It’s hard to see how he arrived at that conclusion, though, when considering the years-long history of bias against African-American would-be jurors.

Evans has also garnered attention for allegations of further prosecutorial misconduct—such as introducing evidence unrelated to the crimes on trial—which contributed to Flowers’ first two reversed convictions. But it doesn’t stop there. I wrote back in April:

Evans has committed a slew of prosecutorial infractions, including the use of faulty testimony from Odell Harmon, a jailhouse snitch who falsely implicated Flowers after the state offered him a deal. He has since recanted. That drew mainstream outrage after the release of the second season of “In the Dark,” a podcast profiling Flowers’s jaw-dropping journey through the legal system.

Gasoline futures for July delivery were up more than 4% on the NY Mercantile Exchange, overtaking an increase in WTI, as an inferno continues to burn through the Philadelphia Energy Solutions oil refinery in South Philadelphia on Friday.

The Philadelphia refinery is “the largest such plant on the U.S. East Coast and the main supplier to the local gasoline market” according to Bloomberg. As of 10AM, the fire was still not under control, according to the Philadelphia Fire Department.

The PES complex handles up to 335,000 barrels of crude per day and is the main supplier of fuel to the New York Harbor market, where inventory is already below average seasonal levels. The complex has plants at Point Breeze and Girard Point in Philadelphia.

After a leak in an alkylation unit, an explosion sent the complex ablaze, forcing the Girard Point section to shut down. The Point Breeze section had already been under repair due to a fire earlier this month. Due to the fact that it is a chemical fire, officials are saying it could burn all day.

— hood’s favorite vegan (@1nicetownbean) June 21, 2019

Joe Brusuelas, Chief Economist at RSM US LLP said: “Any shortage ahead of the peak of the summer driving season does not bode well for U.S. consumer pocketbooks. The video of the early morning explosion is horrific.”

Gasoline demand nationwide was already at a record last week, nearing 10 million barrels per day.

There was a shelter-in-place for parts of South Philadelphia due to the smoke plume from the fire, but it has since been lifted. The site has been home to refining operations for more than 150 years. Prior to PES, the site was owned by Chevron and Sunoco.

via ZeroHedge News http://bit.ly/2L4ZEHz Tyler Durden

{kind=link}

{kind=link}

{kind=link}