The Organization for Economic Cooperation and Development (OECD) warned that recent escalations in trade tensions between the US and China had stalled global growth.

It seems this year’s major theme from the OECD is the deepening of the trade war starting to disrupt the volume of global trade (something we highlighted in a piece called: Global Trade Collapsing To Depression Levels), weighing on consumer demand worldwide, and hurting economic output in both developed and emerging markets.

“Let’s avoid complacency at all costs,” OECD Secretary-General Angel Gurria said. “Clearly the biggest threat is through the escalation of trade restriction measures, and this is happening as we speak. This clear and present danger could easily have knock-on effects.”

Relations between both countries deteriorated earlier this month when President Trump announced that he would increase tariffs on $200 billion in goods from 10% to 25%. In a tit-for-tat effort, China responded by raising the tariffs on $60 billion of US goods.

The OECD suggests that a re-escalation of the trade war could damage smaller economies and accelerate the global synchronized decline.

OECD experts warn trade tensions are unraveling complex global supply chains, could wipe out entire industries in less developed countries as three decades of globalization are reversed.

In a CNBC interview last week, Gurria said the OECD had cut 1% of its global growth predictions over the previous 12 months. Last year, it forecasted a 3.9% growth rate in 2019, but now, it has been reduced to 3.1% amid trade tensions.

“Uncertainty is the greatest enemy of growth and when you don’t have investment because of trade uncertainties, then of course as a rule of thumb, growth will come down and this is what’s happened in a relatively short period of time. It’s really a very bad scene today, it’s a very great source of concern,” he said.

“Why do you invest? You invest to produce, to sell, to get a reasonable profit. But if you do not know if you’re going to have access to the market, you don’t know what tariff you’re going (to face) or whether there will be access at all, then what you do then if you’re a responsible investor is that you hold back, if you’re a responsible consumer you hold back,” Gurria said.

“Investment is the seed of the growth of tomorrow and this is why, after a short period of time, we’ve had this enormous cut in the projections of growth going forward.”

OECD experts warn if President Trump slaps a 25% tariff on additional $300 billion of imported Chinese goods, many third-world countries’ economies would collapse.

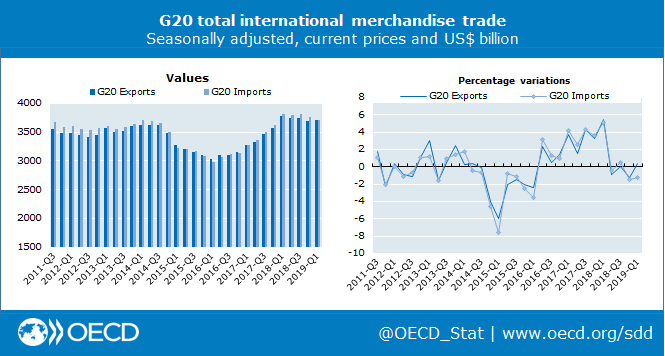

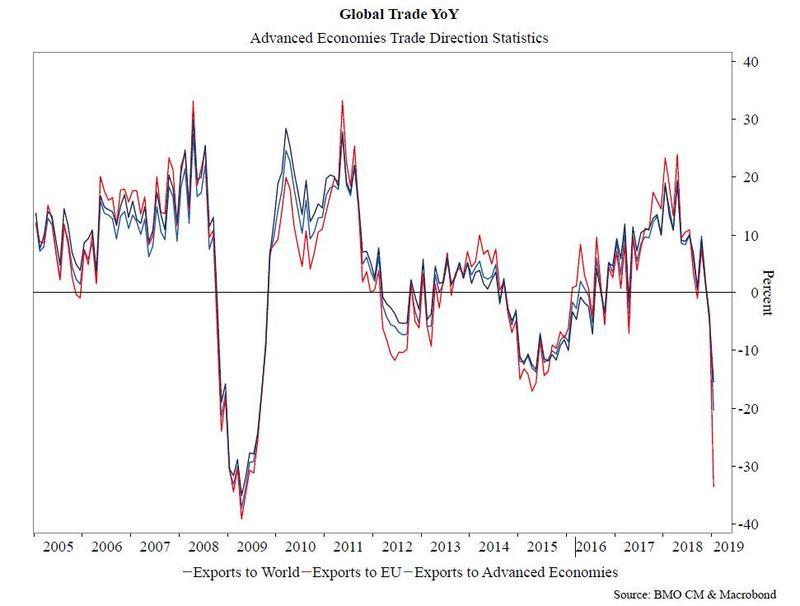

And the best way to visualize the OECD’s warning about the global slowdown is through a chart on the YoY changes in global trade as measured by the IMF’s Direction of Trade Statistics, courtesy of BMO’s Ian Lyngern. It shows the collapse in global exports as broken down into three categories:

Exports to the world (weakest since 2009),

Exports to advances economies (also lowest since 2009), and

Exports to the European Union (challenging 2009 lows).

In short, even before the latest round of trade escalation, global trade had tumbled to levels last seen during the financial crisis. One can only wonder what happens to global trade and smaller economies along critical supply chains after the latest escalation in the US and China trade war…

via ZeroHedge News http://bit.ly/2YY0A4e Tyler Durden

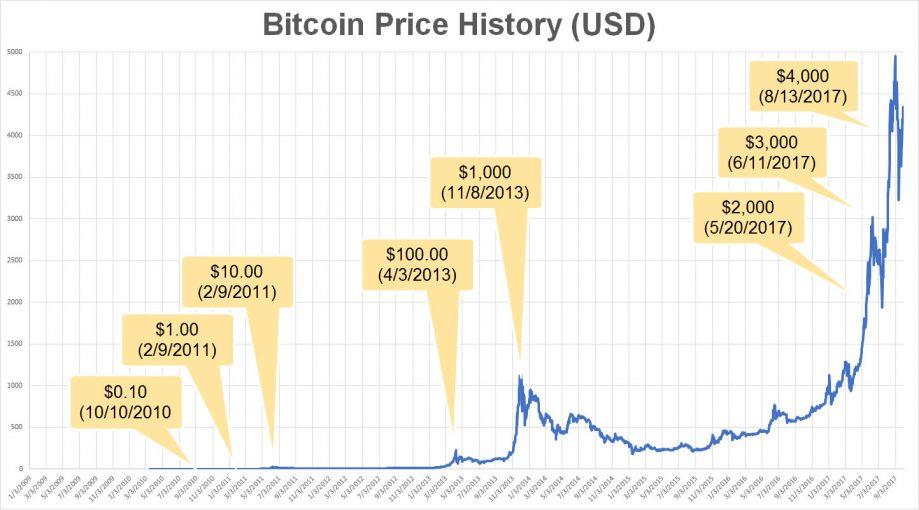

I meant to write this back around May 7th or so, after I listened to “What Bitcoin Did #104” with Tuur Demester and then read his “Bitcoin in Heavy Accumulation” paper. The title of my post was supposed to be “Is Bitcoin finally putting in a bottom?” Real life got in the way of my writing, for a few weeks and then Bitcoin went and did this

I saw a thread in a crypto group on Facebook polling the members, “What is the catalyst behind the Bitcoin price surge” and I personally think it was the release of that Tuur Demester paper. Until then, there were too many head fakes and too much volatility but he made a cogent case that overall, the whales were back in accumulation mode.

Bitcoin’s inelasticity of units

One of the more interesting takeaways from the “What Bitcoin Did” podcast interview was his observation that, with a max 21 million Bitcoin that will ever exist, and an estimated 3 million Bitcoin lost forever through various forms of misadventure, that leaves 17 million BTC now with a global population of millionaires somewhere around 20 million. That means that there is not enough Bitcoin in existence for each millionaire in the world to possess one full BTC.

This leads to the dynamic Kurt Schlichter predicted in his Paper Money Collapse when he thoroughly debunked the objection that money can never return to a hard-backed currency because of there being a shortage of a fixed unit currency like gold to fulfill all of an economy’s transaction volume.

Said differently, one of the arguments against an inelastic currency, such as Bitcoin – is that there isn’t enough of the monetary unit to go around to accommodate an expanding economy.

According to Schlichter:

“A monetary system with a money commodity of essentially fixed supply will experience secular deflation. A growing economy, with an entirely inflexible money supply will exhibit a tendency for prices to decline on trend, and for money’s purchasing [power] to steadily increase. But the key question now, is why should this be a problem? We have already seen that historically secular deflation was rather minor and that it certainly never appeared to present any economic difficulties. No correlation between deflation or recession or stagnation is evident under commodity money systems. [T]here are no reasons on conceptual grounds to consider deflation to be a problem”

The ostensible reason why central bankers and policy makers target inflation is to expand the number of currency units to service the economy. But that’s disingenuous, and the real reason inflation is targeted is because it enables various governments to borrow more than they should, and then pretend to pay it off in currency units with diminished purchasing power. Inflation is theft, yet very few people understand this (not the least of which is “Politics of Bitcoin” author David Golumbia, who insists that inflation increases purchasing power).

What actually happens in terms of an inelastic currency, is that prices go down over time. We would also expect to see the currency unit itself sub-divide into smaller denominations, something which Bitcoin and crypto-currencies are uniquely suited toward.

Should the ascent of crypto currencies continue, we should expect see the subdivisions of bitcoin being used in everyday parlance and transactions reference smaller subdivisions of BTC, from bitcents (0.01 BTC, or cBTC) to millibits (0.001 BTC or mBTC), then microbits (0.000001) or eventually even satoshis themselves (“sat”, 0.00000001 BTC).

What makes a secular cycle in crypto?

“Systems like Ethereum (and Bitcoin and NXT, and Bitshares, etc) are a fundamentally new class of cryptoeconomic organisms — decentralized, jurisdictionless entities that exist entirely in cyberspace, maintained by a combination of cryptography, economics and social consensus”

– Vitalik Buterin

One thing Demester said in passing was that we are in still in an intact singular secular bull market in Bitcoin, which started in 2008. When I wrote “Welcome to Bitcoin’s Trough of Disillusionment” I posited that the secular bull market ended in 2017, making for a 9-year secular run. My best guess was that we were then entering a secular bear market in crypto and that would need to be measured in years, not months.

I get hung up on this because as I’ve previously wondered, if crypto-currencies are indeed a new form of asset class, and I posited in “This Time is Different: What Bitcoin Actually Is” that they are, then I would expect them to behave like other asset classes, and switch leadership between secular bull cycles.

That’s not a law by any means. But in general, whatever lead the market up in the previous bull (think Nifty 50, .COMs, housing and now the FAANGs), leadership shifts to different sectors on subsequent bull cycles within the asset class. Each bull market has a defining narrative unto itself (mostly variations on a “this time it’s different”). When the narrative changes, the sectors that lead the bull are the ones that correspond to that new mythology. The next equities bull may be biotech, or nanotech.

But crypto is so new, what are “the sectors”? Was the last spike defined by the ICO craze, and the next one, if and when it occurs, will be defined by something else? Whatever it will be may not even exist yet. With crypto we repeatedly find ourselves in uncharted territory. To paraphrase William Gibson,

Crypto-currencies were like a deranged experiment in social Darwinism, designed by a bored researcher who kept one thumb permanently on the fast-forward button.

Events move faster in this space, and it’s still early going. Maybe each successive all-time high in the price of Bitcoin in USD terms was a secular cycle unto itself?

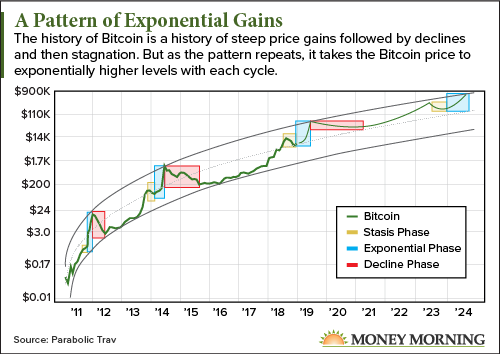

It is tempting, to look at this recurring pattern of Bitcoin price spikes and extrapolate into the future and envision yet another one that will dwarf the 2017 high in manner congruent with previous bull cycles. Where that would put it is almost impossible to guess, the following chart from the same article as the one above extrapolates the trend of “exponentially higher all-time-highs”:

But extrapolation of the past is one of the primary fallacies of investing. And, I think Demester said as much as well, that eventually Bitcoin volatility will settle out and into more normal ranges and away from these periodically expanding super-spikes. I actually think it would be better for the space and open the door to wider penetration among the general economy if that happens.

As interesting as you might find all of the forgoing, none of it is useful. Does it mean you should back up the truck and buy Bitcoin before the next super-spike? Or has it gone up too much, too soon and now it’s a screaming short?

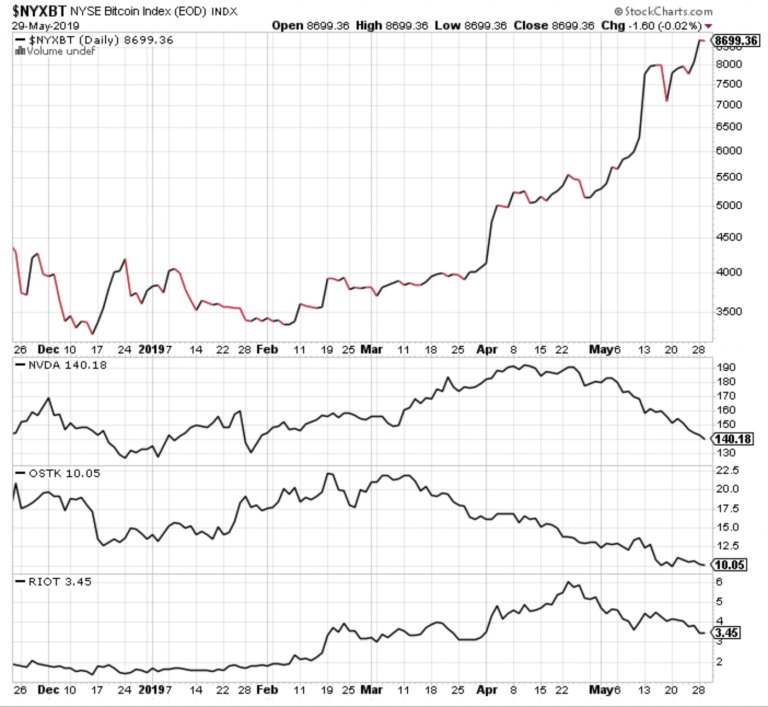

Bitcoin stocks are not confirming this move

The Bitcoin equities, if we can actually point at any stocks and call them that, maybe OSTK, NVDA, possibly RIOT, don’t seem to be confirming the move. When that happens in precious metals it usually means the rally is a head fake or destined to stall out.

Any other “Bitcoin equities” have been ground all the way down into penny stock dust. MGTI and DPW Holdings are beyond trainwrecks. HIVE was the only penny stock I found whose chart doesn’t look absolutely terrible, but the fundamentals are a disaster.

GBTC is moving in tandem with Bitcoin, which makes sense, yet the premium is currently around 33%, not the completely insane 70% or 80% that it commanded during the blow off top of 2017, further the premium to NAV has actually dropped a few points since this BTC move really took off:

Overall, the bitcoin stocks space is too new and too damaged to be able to tell us anything useful, other than making note that at least here, there is a conspicuous absence of exuberance.

Bitcoin on the other hand, is enjoying a lot of optimism right now and it’s not uncommon to see lofty price targets being bandied around in social media again.

That said, I am tentatively in agreement that winter is over for Bitcoin, and that we are at least entering a basing phase ahead of a new bull cycle. Remember what I warned when I wrote Welcome to Bitcoin’s Trough of Disillusionment:

I have personally and notoriously been “too early” calling bottoms of gold bears since 2003. Possibly profitable advice would be: wait until I call for a bottom in Bitcoin and then wait another year.

It’s impossible for anybody to tell you how to the future will pan out, but I can tell you what we’re doing, how I’ve played it until now, and the approach that has worked for me in the past and never let me down:

Don’t buy Bitcoin. Earn it.

The best way I’ve found to invest in something like Bitcoin was an approach we took going back to the digital gold currency days of yore, when e-gold was a thing, and we became the first and only ICANN accredited registrar who would accept it as a payment method. Instead of converting those sales to fiat, the transaction volume was comparatively small enough that it wasn’t material to our cashflow. We could accumulate it, and over time, it added up to a few pounds of bullion, which we were diligently converting to physical via the secondary market.

In 2013 we ran the same play again, becoming effectively the first ICANN registrar to accept Bitcoin (and then Ethereum, and lately we dropped Bitcoin Cash and added Litecoin). From 2013 through to the super-spike in 2017, we for the most part accumulated it.

After the bubble peaked out, we kept accepting Bitcoin, but switched gears to converting half of it into gold, again, this time using Goldmoney / Bitgold. We don’t look at things as Bitcoin vs gold. We look at global financial repression and economic rigging as a situation that one defends against with Bitcoin and gold. They are natural compliments and not at all orthogonal to each other.

We’ve since shifted our weighting and are back in 100% accumulation mode for crypto-currencies. On this stretch of the crypto-currency journey I am talking to more business owners who want to do the same thing: offer Bitcoin as payment option to their customers.

If you own a business and want to add Bitcoin as a payment method so that you can essentially dollar cost average your way into a decent position, it may be a fortuitous time to start. Every bit of Bitcoin you earn now has that inexorable deflationary wind at its back that will hold and gain value in fiat money terms over time. Given global debasement of worldwide fiat currencies, perhaps spectacularly so.

As an example, during the blow off top in December 2017 I remember logging into a wallet I had setup for a tipjar on an old blog that had received a single tip, something like $2 or $5 (maybe even less), and was astounded to realize it had become worth $1500 or so. Think of that every time you accept a $5 or $20 or $150 payment from your business in Bitcoin, and if you’re doing that, as we were for years between 2013 and 2017, several times a day, you start to get that snowball effect.

* * *

If you don’t have the technical time or inclination to dig into this and set it all up, fear not, easyDNS is launching a fully managed easyCrypto Payment Gateway, which runs under your own domain and collects Bitcoin into your own wallet. You can sign up here for an invite.

via ZeroHedge News http://bit.ly/2JPYTm2 Tyler Durden

Facebook is facing a new round of criticism this week for its refusal to send CEO Mark Zuckerberg and COO Sheryl Sandberg to testify at a hearing in Canada’s House of Commons. That criticism is unfair—their refusal to testify in front of the Canadian legislature, like their refusal to testify in the U.K.. last November—is at the very least a prudent decision. But it’s arguably a principled one.

Don’t get me wrong: I don’t embrace the idea, currently fashionable in some chambers of government and sectors of the punditocracy, that complying with a subpoena should be fundamentally voluntary. When Zuckerberg was summoned directly by congressional lawmakers last year to answer a full range of political questions, he was right to attend. And if for some reason he had resisted, Congress would have been within its authority to subpoena him and compel him to attend.

But neither Canada, which Zuckerberg and Sandberg officially disappointed this week by sending two senior Facebook executives in their stead, nor the United Kingdom, where Zuckerberg similarly refused to appear last fall, has the same power that the U.S. government has over an American citizen and a company that’s incorporated in the United States. What’s more, the jurisdictional question is the least relevant aspect of those two no-shows. Far more important is the fact that the Canadian hearing, like the U.K. hearing before it, was intended to function as a kind of show trial.

How do we know it would have been a show trial? Here’s the tell: “Lawmakers from nearly a dozen countries used Tuesday’s forum in Ottawa to press tech companies about privacy violations, hate speech, and the spread of misinformation,” Politicoreported Tuesday. The U.K. hearing was similarly international—representatives from at least nine other countries attended the event last fall at the British Parliament, hoping to grill Zuckerberg about Facebook’s sins against democracy and the international order. In a move perhaps inspired by Clint Eastwood, Zuckerberg was represented at both the U.K. and Canadian events by an empty chair. The parliamentarians refined Eastwood’s dramaturgy by putting Zuckerberg’s name on the chair.

The takeaway from both events: If a parliament is inviting lawmakers from other countries into its chambers in order to allow them to cross-examine a witness—also from another country—then whatever that process is, it isn’t lawmaking or evidence-gathering. It isn’t even an effort to communicate information or political positioning to one’s home constituencies. Its purpose is retributive theater aimed at humiliating the presumptively guilty witness.

To be clear, most legislative hearings are political theater. Everyone familiar with the workings of representative government knows that the gathering of information is a secondary function of a legislative hearing. Its primary function is communicating to the public that legislators are on the case. But to show that, you don’t need to invite parliamentarians from elsewhere in the world to quiz the witness; domestic lawmakers, assisted by staff, can do that themselves. That is, after all, part of what they’re elected and paid to do. No need to import legislative guest workers.

Sometimes that political theater even works to public benefit. When Zuckerberg testified before Congress last summer, he faced a range of questions that spanned the political spectrum. Democrats quizzed the CEO about his company’s handling of private information, and about political actors (domestic and foreign, legitimate and otherwise) who use the platform to sway elections and other political outcomes. Republicans in Congress, many of whom have embraced the myth that tech companies have an agenda to suppress conservative content, sought to pin Zuckerberg down on charges of political bias or the question of whether Section 230 obligates Facebook and other tech platforms to be neutral. (News Flash: Section 230 was designed to do just the opposite, for good public policy reasons.)

Zuckerberg’s answers to House and Senate members weren’t always perfect and they didn’t make everyone happy, but quite often they were genuinely informative, both in sharing how Facebook actually operates and in communicating to the public how Facebook regards its services and its role. Disturbingly, Zuckerberg began to signal his willingness to accept more regulation, including stronger obligations to police content, in compliance with U.S. regulation as well as that of (appropriately harmonized) international regulation governing illegal content, election meddling, and privacy protection. That fullest flower from that seed of willingness was Zuckerberg’s Washington Post op-ed in March.

The tone of that op-ed suggests that Zuckerberg and Facebook may be willing to bail themselves out of their current P.R. nightmare by embracing some kind of regulated-industry status. That’s a bad idea not only because Facebook isn’t particularly adept at content-moderation now (and likely won’t be much better in the future), but also because their content-curation and privacy policies will function as a kind of private law that affects what we see and what can be known about us but without the transparency of public law and regulation.

And at this week’s hearing in Canada, the executives Facebook actually stuck to their jump-and-we’ll-ask-how-high message. As Politicoreports, “The two Facebook executives who did show up—one based in Canada, the other in the U.S.—defended the company and promised to comply with new ethics standards and to collaborate in the development of future ones around the world.”

Lost in the complaints about whether Facebook’s top brass show up for show trials is the fact that Facebook is already working toward a coherent, consistent message that, depending on how it plays out, should either hearten us or concern us. Facebook’s overt commitment to develop an ethical code and stick to it is a good sign—I’ve argued for that myself. But the risks are also serious: if the resulting code of ethics is burdensome enough to impose a high barrier to entry for future social-media competitors, Facebook’s commitment will have the extra added benefit (to Facebook) of locking in its market dominance.

That doesn’t have to be the result. It’s possible, after all, to create ethical frameworks that function up and down the scale—doctors and lawyers who are solo practitioners have the same capacity to obey professional-ethics imperatives that hospitals and big firms do. But that’s because they were designed to scale—whatever new rules tech companies offer, or that we suggest to them, need to scale up and down as well. The tech industry, working in consultation with civil society and multistakeholder forums, shouldn’t wait for governments to hand down what bureaucrats—ungrounded in direct experience of the industry—think the rules should be. A better approach is to work out the ethical rules much the way that doctors, lawyers, and other professions have done, and evolve them, in consultation as situations and problems change.

Mark Zuckerberg is the whipping boy of the moment. But it may be Jack Dorsey of Twitter tomorrow, or Sundar Pichai of Google or Apple’s Tim Cook the day after that. And when (it’s probably not “if”) one of the other CEOs angers lawmakers, it will be heard as the other shoe dropping for Big Tech. That’s why, if Facebook and other tech companies who want to get themselves out of the legislative crosshairs, both here and abroad, need to be proactive, not reactive, and to position themselves as vigorous tribunes and advocates for user interests, not just targets for complaints. We’ve already seen examples of this, such as Apple’s resistance to government demands to hack iPhone security and Google’s game-changing adoption of the transparency-report paradigm. If the companies apply the same kind of creativity to becoming users’ advocates that they already have applied to feeding users what (they imagine) we want, Zuckerberg and other CEOs will start actively seeking opportunities to show up at more hearings. They’ll seize the chance to brag.

from Latest – Reason.com http://bit.ly/2IeglNN

via IFTTT

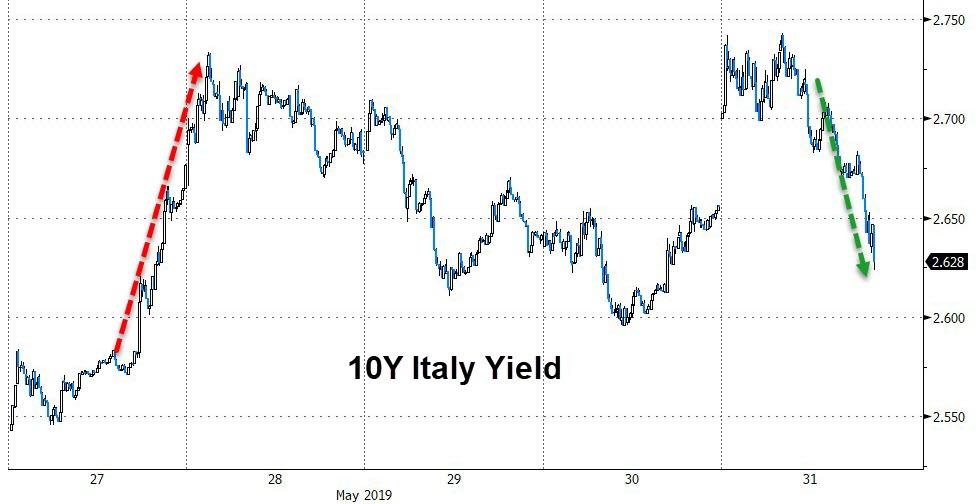

Euro is rallying against the dollar and BTP yields are tumbling after the Italian government has responded to EU concerns (threats of fines) about the southern European nation’s surging debtload.

In what appears like a “say whatever they want to hear” statement, Italian officials promised that the country is planning to reduce the cost of new welfare measures for income support (“citizens income”) and earlier retirement age in 2020-2022, Italian news agency Adnkronos reports.

Additionally, Italy will reportedly tell the EU that its structural deficit can improve without a rise in VAT:

The government is “launching a new spending review and we believe that it will be possible to reduce spending projections for new welfare policies,” news wire cites the letter as saying.

And sure enough, the market is buying it…

Italy told the EU that it expects a drop in bonds yields, lowering borrowing costs as a consequence:

“We are convinced that once the budget program will be finalized in agreement with the European Commission, yields on Italian government bonds will decrease and interest expenditure projections will be revised downwards”

And as can be seen – whether or not Treasury is buying again – that is happening right on cue.

via ZeroHedge News http://bit.ly/2EL9H0x Tyler Durden

Facebook is facing a new round of criticism this week for its refusal to send CEO Mark Zuckerberg and COO Sheryl Sandberg to testify at a hearing in Canada’s House of Commons. That criticism is unfair—their refusal to testify in front of the Canadian legislature, like their refusal to testify in the U.K.. last November—is at the very least a prudent decision. But it’s arguably a principled one.

Don’t get me wrong: I don’t embrace the idea, currently fashionable in some chambers of government and sectors of the punditocracy, that complying with a subpoena should be fundamentally voluntary. When Zuckerberg was summoned directly by congressional lawmakers last year to answer a full range of political questions, he was right to attend. And if for some reason he had resisted, Congress would have been within its authority to subpoena him and compel him to attend.

But neither Canada, which Zuckerberg and Sandberg officially disappointed this week by sending two senior Facebook executives in their stead, nor the United Kingdom, where Zuckerberg similarly refused to appear last fall, has the same power that the U.S. government has over an American citizen and a company that’s incorporated in the United States. What’s more, the jurisdictional question is the least relevant aspect of those two no-shows. Far more important is the fact that the Canadian hearing, like the U.K. hearing before it, was intended to function as a kind of show trial.

How do we know it would have been a show trial? Here’s the tell: “Lawmakers from nearly a dozen countries used Tuesday’s forum in Ottawa to press tech companies about privacy violations, hate speech, and the spread of misinformation,” Politicoreported Tuesday. The U.K. hearing was similarly international—representatives from at least nine other countries attended the event last fall at the British Parliament, hoping to grill Zuckerberg about Facebook’s sins against democracy and the international order. In a move perhaps inspired by Clint Eastwood, Zuckerberg was represented at both the U.K. and Canadian events by an empty chair. The parliamentarians refined Eastwood’s dramaturgy by putting Zuckerberg’s name on the chair.

The takeaway from both events: If a parliament is inviting lawmakers from other countries into its chambers in order to allow them to cross-examine a witness—also from another country—then whatever that process is, it isn’t lawmaking or evidence-gathering. It isn’t even an effort to communicate information or political positioning to one’s home constituencies. Its purpose is retributive theater aimed at humiliating the presumptively guilty witness.

To be clear, most legislative hearings are political theater. Everyone familiar with the workings of representative government knows that the gathering of information is a secondary function of a legislative hearing. Its primary function is communicating to the public that legislators are on the case. But to show that, you don’t need to invite parliamentarians from elsewhere in the world to quiz the witness; domestic lawmakers, assisted by staff, can do that themselves. That is, after all, part of what they’re elected and paid to do. No need to import legislative guest workers.

Sometimes that political theater even works to public benefit. When Zuckerberg testified before Congress last summer, he faced a range of questions that spanned the political spectrum. Democrats quizzed the CEO about his company’s handling of private information, and about political actors (domestic and foreign, legitimate and otherwise) who use the platform to sway elections and other political outcomes. Republicans in Congress, many of whom have embraced the myth that tech companies have an agenda to suppress conservative content, sought to pin Zuckerberg down on charges of political bias or the question of whether Section 230 obligates Facebook and other tech platforms to be neutral. (News Flash: Section 230 was designed to do just the opposite, for good public policy reasons.)

Zuckerberg’s answers to House and Senate members weren’t always perfect and they didn’t make everyone happy, but quite often they were genuinely informative, both in sharing how Facebook actually operates and in communicating to the public how Facebook regards its services and its role. Disturbingly, Zuckerberg began to signal his willingness to accept more regulation, including stronger obligations to police content, in compliance with U.S. regulation as well as that of (appropriately harmonized) international regulation governing illegal content, election meddling, and privacy protection. That fullest flower from that seed of willingness was Zuckerberg’s Washington Post op-ed in March.

The tone of that op-ed suggests that Zuckerberg and Facebook may be willing to bail themselves out of their current P.R. nightmare by embracing some kind of regulated-industry status. That’s a bad idea not only because Facebook isn’t particularly adept at content-moderation now (and likely won’t be much better in the future), but also because their content-curation and privacy policies will function as a kind of private law that affects what we see and what can be known about us but without the transparency of public law and regulation.

And at this week’s hearing in Canada, the executives Facebook actually stuck to their jump-and-we’ll-ask-how-high message. As Politicoreports, “The two Facebook executives who did show up—one based in Canada, the other in the U.S.—defended the company and promised to comply with new ethics standards and to collaborate in the development of future ones around the world.”

Lost in the complaints about whether Facebook’s top brass show up for show trials is the fact that Facebook is already working toward a coherent, consistent message that, depending on how it plays out, should either hearten us or concern us. Facebook’s overt commitment to develop an ethical code and stick to it is a good sign—I’ve argued for that myself. But the risks are also serious: if the resulting code of ethics is burdensome enough to impose a high barrier to entry for future social-media competitors, Facebook’s commitment will have the extra added benefit (to Facebook) of locking in its market dominance.

That doesn’t have to be the result. It’s possible, after all, to create ethical frameworks that function up and down the scale—doctors and lawyers who are solo practitioners have the same capacity to obey professional-ethics imperatives that hospitals and big firms do. But that’s because they were designed to scale—whatever new rules tech companies offer, or that we suggest to them, need to scale up and down as well. The tech industry, working in consultation with civil society and multistakeholder forums, shouldn’t wait for governments to hand down what bureaucrats—ungrounded in direct experience of the industry—think the rules should be. A better approach is to work out the ethical rules much the way that doctors, lawyers, and other professions have done, and evolve them, in consultation as situations and problems change.

Mark Zuckerberg is the whipping boy of the moment. But it may be Jack Dorsey of Twitter tomorrow, or Sundar Pichai of Google or Apple’s Tim Cook the day after that. And when (it’s probably not “if”) one of the other CEOs angers lawmakers, it will be heard as the other shoe dropping for Big Tech. That’s why, if Facebook and other tech companies who want to get themselves out of the legislative crosshairs, both here and abroad, need to be proactive, not reactive, and to position themselves as vigorous tribunes and advocates for user interests, not just targets for complaints. We’ve already seen examples of this, such as Apple’s resistance to government demands to hack iPhone security and Google’s game-changing adoption of the transparency-report paradigm. If the companies apply the same kind of creativity to becoming users’ advocates that they already have applied to feeding users what (they imagine) we want, Zuckerberg and other CEOs will start actively seeking opportunities to show up at more hearings. They’ll seize the chance to brag.

from Latest – Reason.com http://bit.ly/2IeglNN

via IFTTT

WikiLeaks founder Julian Assange is suffering from “intense psychological trauma” in a British prison and should not be extradited to the United Sates to face a “politicized show trial,” according to a UN human rights investigator.

UN torture expert Nils Melzer visited Assange in a high-security London prison on May 9 along with two medical experts, only to find the journalist under severe stress, agitated, and unable to cope with his complex legal case amid chronic anxiety, according to Reuters.

“Our finding was that Mr. Assange shows all the symptoms of a person who has been exposed to psychological torture for a prolonged period of time. The psychiatrist who accompanied my mission said that his state of health was critical,” he told Reuters in an interview in Geneva, adding “But my understanding is that he has now been hospitalized and that he is not able to stand trial.”

Melzer’s comments come after Assange’s attorney said he was unwell when he failed to show up for a London court hearing Thursday regarding his extradition battle. The 47-year-old is currently serving a 50-week sentence in the UK’s Belmarsh jail for skipping bail. According to WikiLeaks he has been moved to the prison’s health ward.

“Mr. Assange has been deliberately exposed, for a period of several years, to progressively severe forms of cruel, inhuman or degrading treatment or punishment, the cumulative effects of which can only be described as psychological torture,” said Melzer.

Melzer, a Swiss law professor, did not say which judges or senior politicians had been defaming Assange, but that “dozens if not hundreds of individuals” had expressed themselves inappropriately.”

“Here we are not speaking of prosecution but of persecution. That means that judicial power, institutions and proceedings are being deliberately abused for ulterior motives,” he added.

British Foreign Minister Jeremy Hunt, in a tweet posted within minutes of Melzer’s statement, said: “This is wrong. Assange chose to hide in the embassy and was always free to leave and face justice.

“The UN Special Rapporteur should allow British courts to make their judgments without his interference or inflammatory accusations,” he said. –Reuters

Assange was charged by the United States last week with 18 new counts related to conspiring to obtain and disclose classified information, endangering national security. He has been accused of unlawfully publishing the names of classified sources, and conspiring and with ex-Army intelligence analyst Chelsea Manning to obtain the classified information. He faces decades in prison if convicted.

“I am seriously, gravely concerned that if this man were to be extradited to the United States, he would be exposed to a politicized show trial and grave violations of his human rights,” said Melzer, adding “The main narrative in this affair really is the United States wanting to make an example of Mr. Assange in order to deter other people from following his example.”

Melzer also said that he didn’t expect Assange to be tortured using traditional methods.

“I would much more expect him to be subjected to prolonged solitary confinement, to very harsh detention conditions and to a psychological environment which would break him eventually.“

via ZeroHedge News http://bit.ly/2KiLEtw Tyler Durden

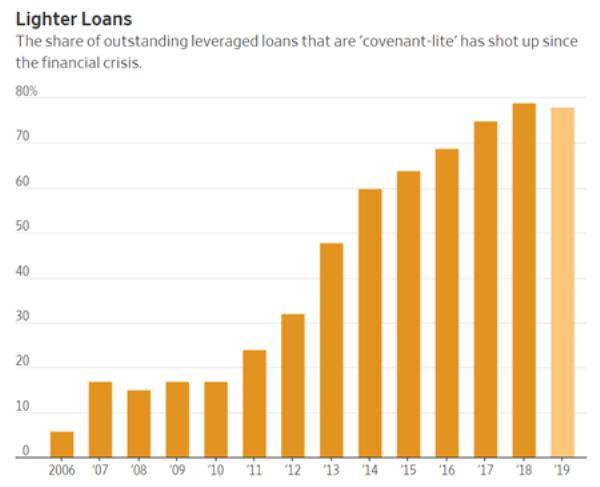

One of the lessons of the past few decades’ boom/bust cycles is that each financial bubble emerges in a different asset class. In the 1970s it was precious metals, in the 1980s junk bonds, in the 1990s tech stocks and in the 2000s mortgage-backed bonds.

Today the only one of these with a reasonable chance of blowing up the economy is Big Tech, which is wildly overvalued by any historical measure.

But a better candidate for the title of most dangerous bubble is emerging: Corporate debt, specifically the “almost junk” portion of that market.

Let’s start with the ongoing surge in overall corporate borrowing, which as a percentage of GDP is now back to the high achieved during the Great Recession, and higher than before the previous two recessions:

But not all corporations are misbehaving. The clear and present danger is coming from BBB rated debt, which means low-rated borrowers that aren’t quite as dicey as actual junk borrowers. This category was less than $1 trillion in the 2000s housing bubble and has since about tripled.

Meanwhile, the terms of these loans are increasingly of the “covenant-lite” variety that don’t require companies to keep their finances within reasonable boundaries. This kind of bond is now 80% of the speculative-grade, or leveraged, loan market, up from just 6% in 2006.

Here’s how this probably plays out. As low-quality borrowers’ interest costs soak up an ever-larger share of their earnings, they’ll start dropping into junk status. This will lead investors to demand higher yields for the remaining BBB bond issuers. Higher borrowing costs will then push more iffy companies into junk, and so on, until lenders stampede for the exits, shutting off access to capital for all but the top corporate borrowers.

Credit-starved companies will start dying, spooking the stock market, and that will be that for this expansion.

The new problem this time around is that potentially bad debts are everywhere, from emerging market dollar-denominated bonds to Italian sovereign debt, Chinese shadow banks, US subprime auto loans, and US student loans. All are teetering on the edge, just waiting to be nudged into the abyss by some external crisis.

So trouble in one sector can metastasize in ways that the global financial system hasn’t seen since the 1930s, forcing central banks to do some truly extraordinary things. Which is the real story here: Not the coming crisis but the monetary authorities’ reaction to the crisis.

via ZeroHedge News http://bit.ly/2QA8Ft3 Tyler Durden

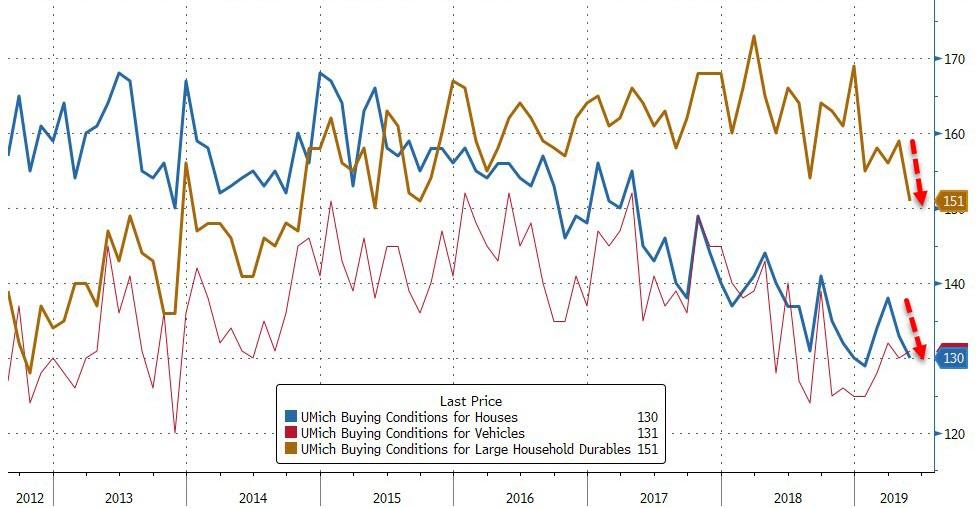

UMich Sentiment survey ‘expectations’ soared in the preliminary data sending the headline to its highest since Jan 2004, but the final prints were marked down notably.

Against expectations of 101.5, and flash print of 102.4 (highest since Jan 2004), the final data for UMich sentiment printed 100.0 (the highest since Aug 2018 only)

This is still the highest “expectation” print since Dec 2003 (albeit notably lower from 96.0 flash to 93.5 final) and current conditions slipped from 112.3 in April (112.4 flash) to 110.0 final for May.

Middle-income Americans saw sentiment weaken as the top and bottom income cohorts rose…

Buying attitudes towards homes and household durables tumbled…

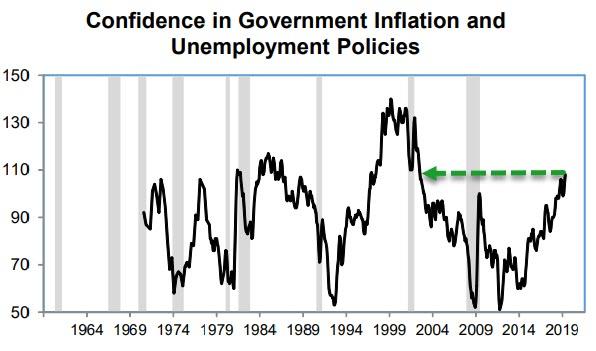

As UMich notes, the combination of higher inflation and lower spending provide conflicting signals for monetary policy, with the divergence further heightening if, as is likely, the trade war escalates. Will the Fed risk higher inflation with lower interest rates, or risk higher unemployment with higher interest rates? Either choice would threaten the highest level since 2002 in consumer confidence in the government’s policies to keep both unemployment and inflation at reasonably low levels (see the chart below).

The economic optimism now expressed by consumers is characteristically different than when the Index first reached the May level in the mid 1960s.

In the earlier era, optimism was primarily based on expected growth in incomes, in the current era, optimism is based more on expected income and job security. The shift is partly the legacy of the Great Recession and partly due to an aging population. This shift has been reflected in personal economic evaluations as well as in political choices.

The proportion of consumers who anticipated an economic downturn during the next five years fell to 38%, the lowest level since 2004.

via ZeroHedge News http://bit.ly/2YWK4RX Tyler Durden

Trump plans to make Americans pay until “illegal migrants coming through Mexico” stop. The president tweeted Thursday night that starting soon, every single item imported from Mexico will be subject to a five percent tariff—a rate that “will gradually increase” until undocumented border crossings end. In August it would rise to 15 percent and then to 25 percent in October. When “the Illegal Immigration problem is remedied,” Trump tweeted, “the Tariffs will be removed.”

By this morning, stocks are tumbling and pretty much everyone is asking, basically, wtf?

“Trade policy and border security are separate issues. This is a misuse of presidential tariff authority and counter to congressional intent,” says Sen. Chuck Grassley (R–Iowa), who chairs the Senate Finance Committee, in a statement.

On June 10th, the United States will impose a 5% Tariff on all goods coming into our Country from Mexico, until such time as illegal migrants coming through Mexico, and into our Country, STOP. The Tariff will gradually increase until the Illegal Immigration problem is remedied,..

In a nutso White House press release, Trump whines that “for years, Mexico has not treated us fairly” and declares we are “now asserting our rights as a sovereign Nation.” He continues:

To address the emergency at the Southern Border, I am invoking the authorities granted to me by the International Emergency Economic Powers Act. Accordingly, starting on June 10, 2019, the United States will impose a 5 percent Tariff on all goods imported from Mexico. If the illegal migration crisis is alleviated through effective actions taken by Mexico, to be determined in our sole discretion and judgment, the Tariffs will be removed. If the crisis persists, however, the Tariffs will be raised to 10 percent on July 1, 2019. Similarly, if Mexico still has not taken action to dramatically reduce or eliminate the number of illegal aliens crossing its territory into the United States, Tariffs will be increased to 15 percent on August 1, 2019, to 20 percent on September 1, 2019, and to 25 percent on October 1, 2019. Tariffs will permanently remain at the 25 percent level unless and until Mexico substantially stops the illegal inflow of aliens coming through its territory. Workers who come to our country through the legal admissions process, including those working on farms, ranches, and in other businesses, will be allowed easy passage.

Those are the only real details offered in the 15-paragraph statement, which is mostly the same TV tough-guy caricature meets crime-panic fever dream that the president rambles out on the regular.

Trump has always loved tariffs because Trump has never understood trade.

But the tariffs would be anything but business as usual, of course. They could “throw into chaos corporate and agricultural supply chains that have essentially worked in a system without tariffs since the 1994 North American Free Trade Agreement,” writeWashington Post financial reporters David J. Lynch and Kevin Sieff. “Mexico is on track to become the United States’ largest trading partner, ahead of China and Canada, according to census data through March.”

How many times will Congress let the president unilaterally raise taxes on Americans? All the times. https://t.co/hJtaKly92K

After getting a complaint that she was working without a license, Florida officials sent a cease-and-desist order and fined her $750. Del Castillo sued, saying her free speech rights were violated. Now, a federal court is expected to rule on her lawsuit as other states weigh regulations on professional dietary advice.

The case highlights the confusion around dietitians and health coaches, and how their qualifications differ.

“I literally didn’t even know I was doing anything that was wrong,” said Del Castillo, who noted her business was legal when she was living in California.

FREE MARKETS

California lawmakers are once again taking aim at independent contractors. A bill that passed the California State Assembly this week would create new standards for determining whether workers are independent contractors or employees. From Vox:

To hire an independent contractor, businesses must prove that the worker (a) is free from the company’s control, (b) is doing work that isn’t central to the company’s business, and (c) has an independent business in that industry. If they don’t meet all three of those conditions, then they have to be classified as employees.

This could radically upend so many different industries and businesses. Of course lawmakers are handing out exemptions to those they like:

The state’s Chamber of Commerce and dozens of industry groups have been lobbying for exemptions, and a long list of professions were excluded from the bill: doctors, dentists, lawyers, architects, insurance agents, accountants, engineers, financial advisers, real estate agents, and hairstylists who rent booths at salons.

But “Uber and Amazon drivers…manicurists and exotic dancers” and many others that politicians disfavor would be screwed.

Ted Cruz and Alexandria Ocasio-Cortez may team up to limit lawmakers’ post-Congress options:

Senator @tedcruz has agreed to co-lead a “clean” bill with Rep. @AOC to ban members of Congress from becoming paid lobbyists once they leave Congress. pic.twitter.com/4en9biU2xt

.@Newsy investigation shows that the NYPD has systemically underreported rape by excluding oral and anal rape from their CompStat numbers. https://t.co/nOHXQhCcym

Most analysts –and the Fed – don’t understand that inflation cycles are different from business cycles. Understanding this key reality allowed our clients to be properly positioned for the drop in bond yields.

ECRI’s co-founder, Geoffrey H. Moore, who created the original leading index of the business cycle over half a century ago, developed the U.S. Future Inflation Gauge (USFIG) to predict those separate inflation cycle turning points. The USFIG also leads inflation expectations (see chart).

The USFIG turned down early last year, and by summertime, it was clear that a fresh inflation cycle downturn was taking hold. That inflation cycle downturn wasn’t obvious to the Fed, which hiked rates in September and December. Despite being forced to pivot hard early this year, Fed Chairman Powell just this month called low inflation “transitory.” Bond markets were also caught flat-footed, with the 10-year treasury yield around 3¼% in October, and again in November, as inflation expectations remained high through last fall.

Highlight: @businesscycle’s Lakshman Achuthan on the economy: “I don’t think there’s a recession imminent, but there’s also no clear signs — at least in the US — of a strong revival ahead, which had been kind of the exception after the Fed pivoted earlier this year.” pic.twitter.com/qHlkQzUIWz