The system of higher education in the United States is being rebuilt from the foundation and we’ve only just started to see the impact of this dramatic transformation.

The way students and parents pay for college is changing

The methods and the places students learn are changing (and have been for a while)

Our culture is changing to finally accept that “traditional” 4-year college isn’t the answer for everyone

But before we talk about all of the changes that are happening in higher education right now, let’s talk about why college is, to put it simply, broken in the United States.

College is Broken.

It’s impossible to miss the many ways college is broken today. And I’m not just talking about the high profile bribery scandal that broke several weeks ago.

While parents paying hundreds of thousands to millions of dollars to guarantee college admission through a “side door” is concerning, it pales in comparison to these other indicators of college broken-ness.

1. Student Loans Are Crippling Tens of Millions

44.2 Million Americans currently are carrying close to $1.5 Trillion in student loan debt (this is ~20% of the US adult population).

Even more astonishing, over 11% of these loans are delinquent (90+ days without payment or in default).

This delinquency rate is >5x the credit card delinquency rate!

Student loans have become such a burden that companies have been started to offer student loan repayment as a fringe benefit: Goodly.

Shout out to Goodly for helping the many already in debt, but we need to stop the problem at the source too!

From 1988 to 2008, tuition increased on average by 3.5% per year. From 2008 to 2018, tuition continued to increase at a still-suffocating 3% per year.

In 1998, tuition at a private 4-year college was 77% of the average male income in the United States.

By 2016, this had increased to 116%.

On the public college side, the increase is even more dramatic. In 1998, the costs averaged 29% of the average male income in the United States,increasing to 52% in 2016.

Incomes simply have not kept pace with tuition increases.

3. Incentives Are Distorted Between Colleges and Students

Students continue to attend college and continue to take on these significant loans because they believe they are making a good investment. College graduates earn substantially more than High School graduates over the course of their career, right? Correct, but…

The fundamental problem is that if the college they attend turns out to be a bad investment, as a growing number of private 4-year colleges do, only the student pays this penalty (and they pay a BIG, often lifelong, one).

The college already got paid by either the government or the student loan company and there is simply no penalty for their lack of performance in student education and career placement (save for some very limited publicly funded university penalties).

There are also no meaningful incentives from the government to provide education in areas where jobs are in the highest demand.

The only true incentive these colleges have is one that is too distant for many: The ability to continue to recruit new students who will pay their ever-increasing tuition rates.

How College is Changing Right Now

Where And How You Learn

MOOCs: Massive Open Online Courses aren’t new, but the depth of courses they offer continues to increase dramatically. Between EdX, Coursera, Khan Academy, and Udacity you can learn almost anything from anywhere for free.

Code Schools (v2!): Code Schools have already gone through one wave of evolution with ineffective programs and schools failing, new models for sustainable funding and profitability emerging and consolidation accelerating.

Technical Trade Schools: Technical school used to mean learning a trade like Carpentry or studying as an Electrician’s apprentice. This concept has been reinvigorated with companies like NextGenT that offer many technical certificate programs in high demand fields like cybersecurity.

How You Pay

ISAs: Income Share Agreements. Instead of paying tuition up front, a student agrees to pay a percentage of their future income to the school or lender. There is usually an income “floor” that the student must be above in order for the income share to take effect after graduation. There is also usually a repayment “ceiling” (so the former student doesn’t end up paying an obscene amount if they get a high-salary position immediately out of school). Companies like Vemo Education have started to bring this payment model to significant numbers of both code schools and traditional 4-year colleges.

Get Paid to Learn: Several companies are taking the idea of the ISA a step further. In addition to paying nothing upfront, these companies are actually paying you a salary to learn. They are betting on high demand career fields like software development and data science and trying to make it as easy as possible for top candidates to join their schools. Several “get paid to learn” companies include Lambda School, Modern Labor, and CareerKarma.

Cultural Changes and Pressures

Reducing the 4 Year College “Pressure”: It’s taken a long time, and particularly affluent parts of our country are still pretty resistant, but code schools and alternative higher education options have begun to gain acceptance as a better option for meaningful percentages of high school graduates.

Thank you for reading. If you’re enjoying this post so far, I think you would enjoy my new book, Disrupt Yourself. For a limited time, I’m offering a free pre-release chapter.

Code schools will (continue to) consolidate dramatically

All colleges remaining offer ISAs and many offer “get paid to learn” options

Community College still exists as the low cost higher education option and may even grow in influence and size

A small set of top code schools achieve “Ivy League” status and diversify to offer robust curriculum for developers, data scientists, designers, product managers and more (essentially the tech company talent stack)

Student loan debt collapses in value as defaults skyrocket

Prediction: College in 20 Years…

Ivy League and top research universities are only “old guard” that remain

Community college is free everywhere in the USA as a guaranteed, robust, public secondary education (in many states this is the case already)

All colleges that remain offer both ISAs and “you get paid to learn” options

Code schools look like colleges and colleges look like code schools to the point where they are hard to differentiate

College is Changing and It’s a Good Thing

College is broken today.

But fortunately, many startups, companies, and public figures are starting to pay attention and build the next generation of higher education.

It’s going to be disruptive, it’s going to be scary (at times), but with the right minds focused on this huge problem, our country will build a secondary education system that has:

Free options that are robust (Community College)

Stronger alignment with high-demand careers

True incentive alignment between students and education providers

Little to no debt for students (!)

via ZeroHedge News http://bit.ly/2X4P3iy Tyler Durden

Amidst the ongoing nuclear negotiation standoff with the United States, North Korean leader Kim Jong Un has initiated a large-scale military shakeup, bolstering his general officers corps with a wave of promotions.

The move is said to mark the upcoming birthday of his grandfather and North Korea founder Kim Il Sung, according to state media, but more significantly Kim used the occasion to extend another hand to Washington, signaling he’s not given up after the disappointing failed February talks with Trump in Hanoi, which rapidly broke down.

File photo via KCNA/Reuters

Kim said on Saturday during a speech on state television he would be willing to hold a third summit with Trump, and said Washington has until the end of the year to make a nuclear deal happen.

Crucially, Trump responded quickly and in the affirmative, tweeting Saturday that a third summit “would be good” and noted warmly “we fully understand where we each stand” in terms of the two leaders’ personal relationship.

“I agree with Kim Jong Un of North Korea that our personal relationship remains very good, perhaps the term excellent would be even more accurate, and that a third Summit would be good in that we fully understand where we each stand,” Trump posted to Twitter.

I agree with Kim Jong Un of North Korea that our personal relationship remains very good, perhaps the term excellent would be even more accurate, and that a third Summit would be good in that we fully understand where we each stand. North Korea has tremendous potential for…….

“North Korea has tremendous potential for……. …extraordinary growth, economic success and riches under the leadership of Chairman Kim,” Trump continued. “I look forward to the day, which could be soon, when Nuclear Weapons and Sanctions can be removed, and then watching North Korea become one of the most successful nations of the World!”

….extraordinary growth, economic success and riches under the leadership of Chairman Kim. I look forward to the day, which could be soon, when Nuclear Weapons and Sanctions can be removed, and then watching North Korea become one of the most successful nations of the World!

The significant public breakthrough in direct public dialogue following Hanoi was coupled Kim ordering three people to be promoted to full general with 33 others raised to the rank major general on Sunday.

The promotions come shortly after Kim reaffirmed his faith in top aides involved in nuclear talks with the U.S. In a Supreme People’s Assembly meeting earlier this month, North Korea reappointed Kim Yong Chol as a member of the State Affairs Commission led by Kim Jong Un himself. The country has also promoted Choe Son Hui to first vice foreign minister.

Importantly it was Kim Yong Chol that met with Trump at the White House earlier this year, who also had a key role in paving the way for talks with the US in Vietnam.

This second summit ended badly when Trump walked out of the meeting after it was clear not deal would be reached. “Sometimes you have to walk, and this was just one of those times,” President Trump had said at the time of his cutting short the Vietnam summit.

via ZeroHedge News http://bit.ly/2XdzOUO Tyler Durden

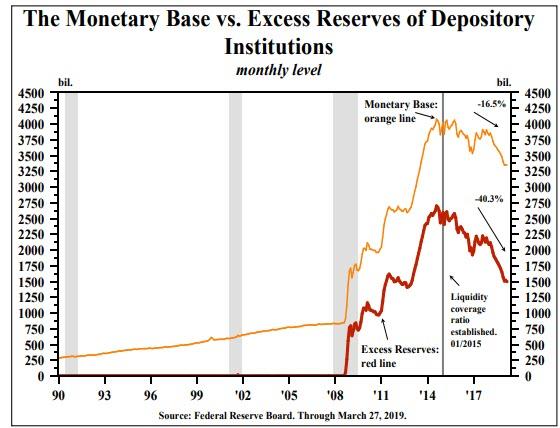

Under existing statutes, Fed liabilities, which they can create without limits, are not permitted to be used to pay U.S. government expenditures. As such, the Fed’s liabilities are not legal tender. They can only purchase a limited class of assets, such as U.S. Treasury and federal agency securities, from the banks, who in turn hold the proceeds from this sale in a reserve account at one of the Federal Reserve banks. There is currently, however, a real live proposal to make the Fed’s liabilities legal tender so that the Fed can directly fund the expenditures of the federal government – this is MMT – and it would require a change in law, i.e. a rewrite of the Federal Reserve Act.

This is not a theoretical exercise. Harvard Professor Kenneth Rogoff, writing in ProjectSyndicate.org (March 4, 2019), states “A number of leading U.S. progressives, who may well be in power after the 2020 elections, advocate using the Fed’s balance sheet as a cash cow to fund expansive new social programs, especially in view of current low inflation and interest rates.” How would MMT be implemented and what would be the economic implications? The process would be something like this: The Treasury would issue zero maturity and zero interest rate liabilities to the Fed, who in turn, would increase the Treasury’s balances at the Federal Reserve Banks. The Treasury, in turn, could spend these deposits directly to pay for programs, personnel, etc. Thus, the Fed, which is part of the government, would be funding its parent with a worthless IOU. In historical cases of money printing, the countries were not the reserve currency of the world, as the U.S. is today. Thus, the entire global system could be destabilized in very short order if this were to occur.

There would be no real increase in services or money since very little time would lapse before people realized increasing inflation was not increasing real purchasing power. If the government responded by issuing more central bank legal tender, the inflationary process would become self-perpetuating, and as was the case in numerous historical instances this would lead to hyper-inflation. Moreover, the central bank would have no capability of reducing the money supply. All they could offer would be the zero maturity, zero interest liabilities of the government, but there would be no buyers. This would mean that hyper-inflation would be difficult to stop.

Rates Too High Already

Presently, the Treasury market, by establishing its rate inversion, is suggesting that the Fed’s present interest rate policy is nearly 50 basis points too high and getting wider by the day. A quick reversal could reverse the slide in economic growth, but the lags are long. It appears that history is being repeated – too tight for too long, slower growth, lower rates.

Velocity

In the article, Lacy also touched on the velocity of money. While I agree with Hunt that velocity has generally been falling, the equation itself is useless.

As I have pointed out, velocity can rise or far with rising or falling GDP. It is not an independent variable that can be tracked.

Velocity = Value of transactions/supply of money. This expression can be summarized as: V = P(T/M) , where V stands for velocity, P stands for average prices, T stands for volume of transactions, and M stands for the supply of money.

This expression can be further rearranged by multiplying both sides of the equation by M. This in turn will give the famous equation of exchange: M(V) = P(T).

Many economists employ GDP instead of P(T), thereby concluding that: M(V) = GDP = P x (real GDP).

Velocity Does Not Have an Independent Existence

Contrary to mainstream economics, velocity does not have a “life of its own.” It is not an independent entity–it is always value of transactions P(T) divided into money M, i.e., P(T/M). On this Rothbard wrote: “But it is absurd to dignify any quantity with a place in an equation unless it can be defined independently of the other terms in the equation.” (Man, Economy, and State, p. 735)

Since V is P(T/M), it follows that the equation of exchange is reduced to M(PxT)/M = P(T), which is reduced to P(T) = P(T), and this is not a very interesting truism. It is like stating that $10=$10, and this tautology conveys no new knowledge of economic facts.

In regard to hyperinflation, I have been asked many time what it would take for me to change my mind on that happening in the US. My response, has been unchanged for years: Give Congress Control of Money Supply.

MMT does precisely that. There is no project that could not be funded including AOCs absurd Green New Deal which might cost as mush as $200 trillion.

It would not stop there. Guaranteed “living wages” and “guaranteed jobs would finish it off. The amount needed to have a living wage could never be met. Prices would soar along with the guarantee.

What About Rate Cuts

Hunt says interest rates are 50 basis points too high. In relation to the Fed’s mandate, I believe Hunt is correct.

If one wants to factor in asset bubbles the Fed isn’t. Alternatively, the Fed should have started hiking in 2010 or 2011 and be cutting rates now.

The Fed is constantly chasing its own tail. I believe that is what Hunt means when he speaks of lags. If so, we are in agreement on that point as well.

Regardless, because of Fed actions and the lags, I am certain we are headed for another very deflationary asset bubble bust.

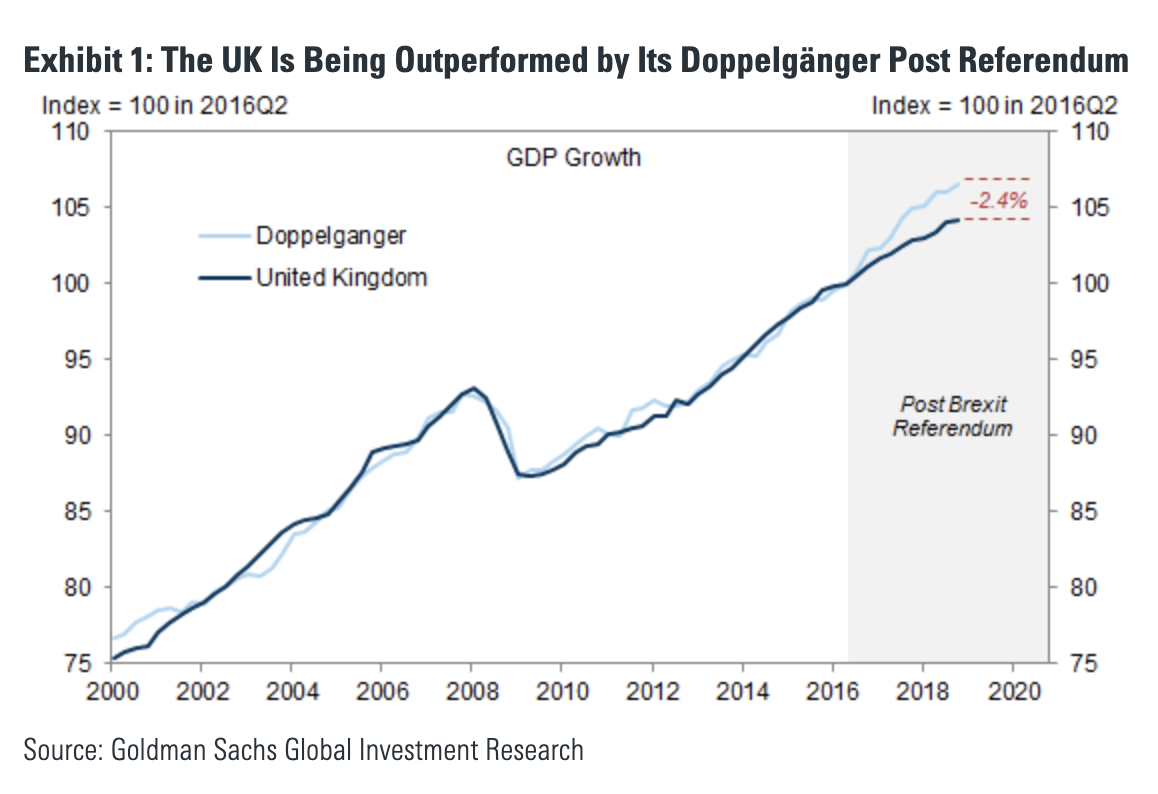

In his latest note published last week, SocGen’s Albert Edwards – never at a loss subjects that inspire his outrage – rages on the topic of Brexit, and specifically the often repeated assertion (as discussed here as well), that post-Brexit referendum UK has lost 2% of its GDP output, or about £800m a week.

We won’t dwell on that for a simple reason: as UBS’ chief economist Paul Donovan put is best last week, “A few things have happened in the EU-UK divorce. Does anyone care? No, they do not.” Another reason why Brexit is largely meaningless despite resulting in countless newswire headlines each and every day: the final outcome is clear – with Theresa May a remainer, and with both sides seeking to perpetuate the status quo by delaying and delaying and delaying some more until it appears that it’s the public’s desire to reverse the outcome of the 2016 referendum, it is just a matter of time before the entire idea of Brexit is scuttled.

Instead we will focus on an anecdote that Edwards brings up in relation to his now 30-year-old son, Newcome, who was 10 back in 1999, and was reportedly stealing Albert’s Financial Times “to look at Nasdaq share prices:”

It was at that point that I realised the tech bubble was really getting out of hand (I have reproduced part of this weekly explaining what happened, at the end of this note).

As Edwards further explains, “discovering my 10 year old son looking at Nasdaq share prices alerted me to the extent of the madness that had gripped the markets by end 1999. Similarly there are moments in this job when something you hadn’t been following particularly closely is highlighted to you and you stagger back in shock. At that point you realise that something has gone very wrong.”

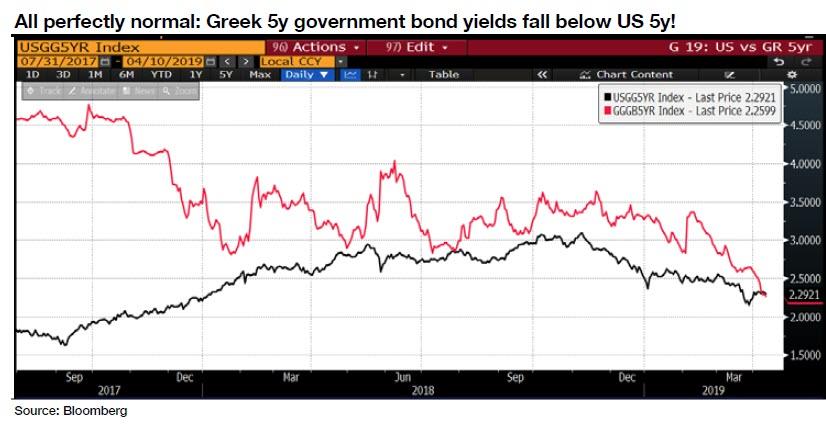

So unlike 1999, when it was Nasdaq prices that set Edwards off, this time it was the yield on the Greek 5Y government bond that inspired shock in the SocGen strategist, to wit: “I certainly think the decline in the 5y Greek government bond yield to 2.28%, below that of the US, counts as such an event (they were recently yielding 20%!). @mnicoletos on Twitter highlighted the chart below with the comment, “if you can’t find anything wrong with this chart then I’m afraid there isn’t much to say….”

Aside from the shock of 5Y Greek govt bonds yielding below their US equivalents, there were a few more topics that “surprised” Edwards when he returned from his latest business trip to the US, the first of which is that while fears of a global hard landing receded at the start of last week in the wake of the bounce in the official NBS Chinese PMI back above 50.0 in March, even though most of the components of the official manufacturing PM rose, the important employment component fell further to 47.2 (see chart below). As Edwards points out, “this has now slumped below the levels that helped trigger the 2015 Renminbi devaluation! In addition despite recovering, non-manufacturing employment remains below the critical 50 level, meaning employment is still contracting.”

And as the SocGen strategist correctly notes, “at the end of the day, what matters to the Chinese Government far more than the GDP growth numbers most commentators focus on, is employment growth. For it is job losses, rather than whether GDP grows at 6% or 5%, that might be a prelude to social unrest.“

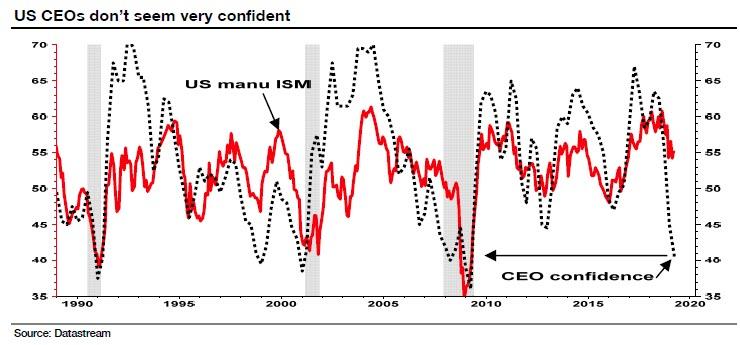

Besides the recent Chinese data, Edwards highlights the recent US Conference Board survey of CEO confidence as another “interesting datapoint” that was published while he was away. And while here, too, the headline measure ticked up a notch in Q1 to 43 from 42 in Q4 (a reading of more than 50 points reflects more positive than negative responses), the recent readings are consistent with an economy on the verge of recession and the manufacturing ISM at 45 rather than the current 55. There was one exception: “1998 Q4 which was a near death experience for the economy in the wake of the Asian/Russian/LTCM crises.”

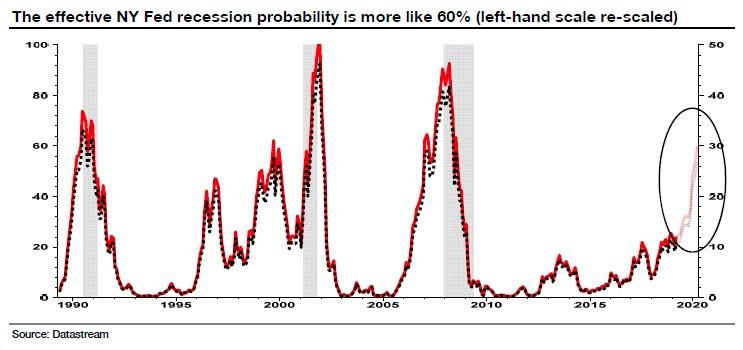

And speaking of the risk of an imminent US recession, Edwards brings attention to the surge in the NY Fed’s predictor of recession (based on the yield curve) which shows a latest reading of a 27% probability – the highest reading since 2008.

However this probability underestimates the chances, as the series typically peaks out at a 40-50% probability, even in the depths of a deep recession (see dotted line on right-hand scale below). So recalibrating the scale on the chart so the probability is nearer to 100% in the depths of previous recessions, the probability of recession later this year jumps up to 60% rather than the reported 27% (see red line and left-hand scale below, Datastream shows forward data plots in the circle as faint red and dotted lines).

Considering that in just two months, or June, the US expansion will become the longest economic up-cycle in history, Edwards points out that the fragility of the current economic situation is explained by this quote from former Fed Governor, Laurence Meyer: “A period of stability induces behavioural responses that erode margins of safety, reduce liquidity, raise cash flow commitments relative to income and profits, and raise the price of risky, relative to safe assets — all combining to weaken the ability of the economy to withstand even modest adverse shocks.”

He is, right of course, but as long as the Fed steps in every time there is an “adverse shock”, why should traders, investors or anyone else for that matter, be nervous?

* * *

Ainally, as Edwards promised at the start of his note, here is his Global Strategy “Weekly Failed as a Father”, published in Nov 1999, at the highest of the dot com bubble.

You’ve read about it in the papers. Child runs off with religious cult. It couldn’t happen to you of course. You understand your children. You’ve brought them up to know the difference between right and wrong.

But when it happens to you, the soul-searching starts. Was it me? Did I spend too long at work? Should I have seen it coming? Or was it the little things? Perhaps I was nagging too much about his diabolical table manners.

I blame the environment. He obviously wasn’t born with these problems. It must be the fault of television. There have been those adverts recently…

But it was only this Monday that I realised there was a problem at all.

Anyway, I thought it a bit odd. I came downstairs at about 8am to pick up the Financial Times off the doorstep and the paper-boy only seemed to have delivered the supplement but not the main body of the paper. Odd!

But the paper-boy had indeed been acting a little oddly recently. It was only the other day that he rang the door-bell at 6am. Rushing down and throwing open numerous bolts, I was confronted by a cowering boy who had, much to his horror, stuffed the wrong paper through the letter box and wanted it back.

My sense of irritation quickly passed. He looked scared. Perhaps the shock of him seeing a grown man in Marks and Spencer paisley pyjamas was enough punishment. Anyway after finding only the supplement on the doorstep last Monday, I had assumed he was wreaking some sort of retaliatory action. I wandered into the kitchen – to seek out my caffeine intake – only to discover the awful, disgusting truth.

On the kitchen sideboard I found the FT second section, open at the Nasdaq share prices.

Then it hit me. My son – my little boy – had turned into a bull market junkie. He had sneaked down while I was asleep to check the Nasdaq share prices. Why?

I suppose I wouldn’t have minded so much if he had been checking the Gilt pages or even the Building and Construction section – but why the Nasdaq?

I should have realised the day before. He asked me to show him the Nasdaq stocks in the FT. I tried to shrug it off, as I did the recent one about transsexuals, but he persisted. Of course when I went to find it in the paper I couldn’t! I didn’t feel bad. I didn’t feel inadequate as a father. After all I had recently taken him to the park and repeatedly shown him how to do head on rugby tackles. I had the ball and was Jonah Lomu. He seemed to enjoy that! Surely that’s what modern fathers do!

But apparently the boys are discussing the Nasdaq at school after having seen “those” adverts on television. Chancellor Gordon Brown better watch out. “New” Labour’ schmoozing of all that is American could potentially turn a whole generation of UK children into “growth” junkies.

And this is how Edwards concludes: “Here we are in 2019 and looking at this chart, Im getting a strong sense of 1999 déjà vu!“

via ZeroHedge News http://bit.ly/2UyiUTT Tyler Durden

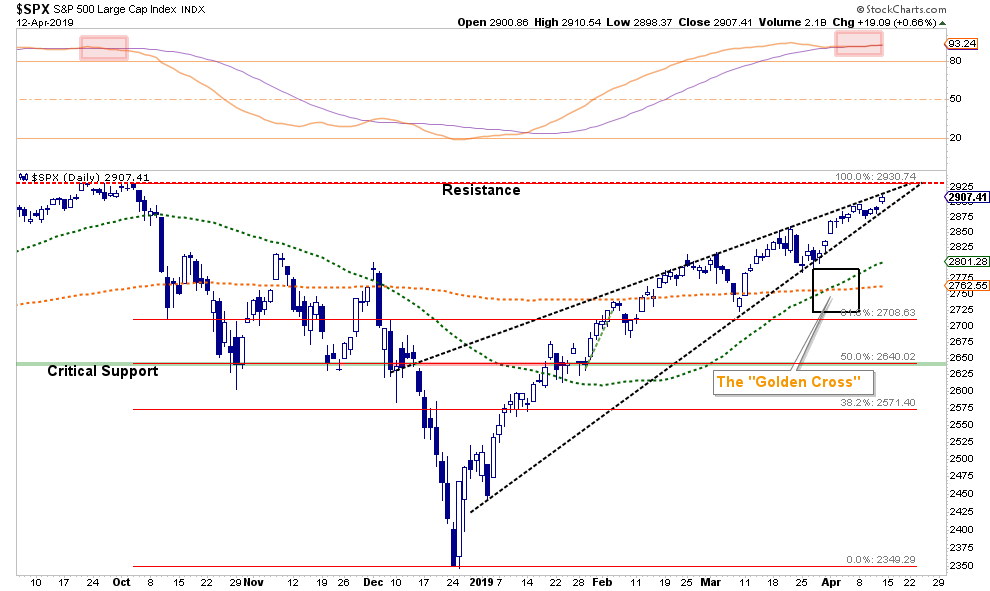

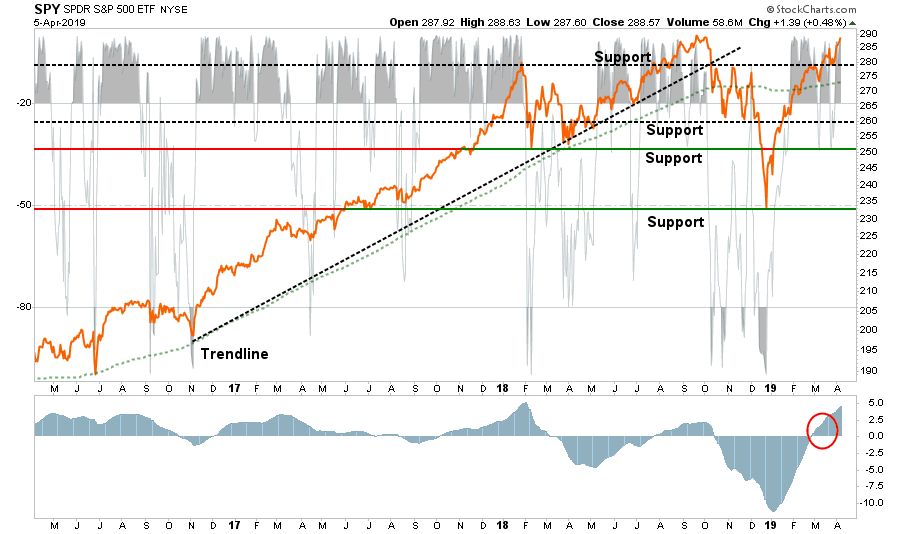

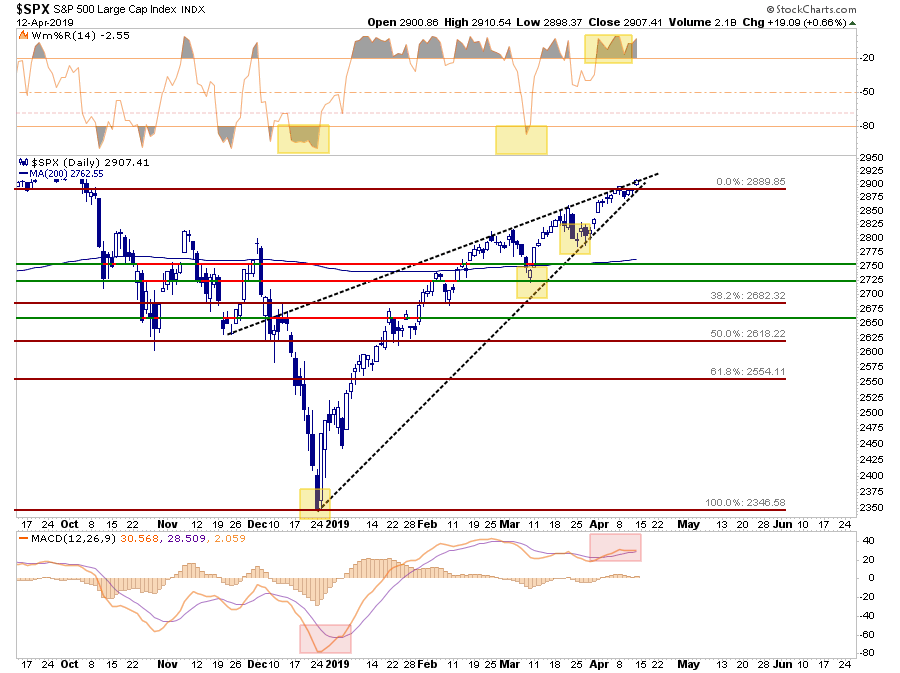

Markets Climb Above 2900, All-Time Highs Next Stop?

Over the last couple of weeks, we have been discussing the market’s advance from the lows and why retesting old highs was quite probable. To wit:

“The markets are close to registering a ‘golden cross.’ This is some of that technical ‘voodoo’ where the 50-day moving average (dma) crosses above the longer-term 200-dma. This ‘cross’ provides substantial support for stocks at that level and limits downside risk to some degree in the short-term.”

As I penned on Monday for our RIA PRO subscribers(Try it FREE for 30-days and get access to daily trading ideas on the markets, sectors, portfolio positions and long-short idea list):

“As we discussed last week, the rally above, and retest of support at 280 sets up a test of all-time highs. I expect that will occur early next week.SPY is extremely overbought, so a test and failure at the highs will not be surprising.

Short-Term Positioning: Bullish

Last Week: Previously increased sizing to full weight.

This Week: Hold

Stop-loss moved up to $280″

More importantly, on Friday, the markets broke above short-term resistance and the psychological barrier of 2900. This will likely get the bulls all excited over the weekend to make an attempt for all-time highs.

While the bullish bias is definitely behind investors currently, there are concerns relative to the current risk/reward backdrop.

As shown in the chart above, the market is not only back to more extreme overbought levels, it is also close to registering a short-term sell signal. With prices now compressed into a very tight range, the risk of a downside break has risen. Drew Zimmerman from Polar Futures Group also made some very astute observations on Friday.

“Is it the middle of April or the middle of August? The weekly trading volume of shares on the US indices and the number of futures contracts that traded this week was the lowest since last summer and among the lowest weekly levels of the past several years. This low volume has reduced price volatility with the VIX index trading back to down to levels not seen since the beginning of October last year before the equity price decline started. Even the volatility in the G7 currencies is the lowest it has been since the middle of 2014!

So, it’s quiet out there….what does that mean? Equity markets are only a couple of percentage points from all-time highs, things must be good! The central banks have done their job, they have all gone back to accommodative policy stances, and China easing more aggressively. We have gone from worries of a global slowdown to not worrying at all because the central banks have our back, and in that environment taking more risk pays. The central banks must know what is best right?

However, when we see broad markets get this quiet, it usually means we are about to get a rude surprise. When things coil up, it is common to see some explosive moves. Given the very low level of volatility, it may be an opportune time to buy some protection.”

We agree with the last statement. This is supported by the extreme level of the current “buy” signal as shown in the shaded orange bar graph in the chart below. These rare extreme extensions occur at extremes of sell-offs and rallies.

As stated, we definitely agree and as such are maintaining our current equity exposure, with an overweight positioning in cash and fixed income. While this allocation structure is currently providing some performance drag, it is also greatly reducing overall portfolio volatility which we think we will be well rewarded for over the next four to six months.

This is generally where someone with a reading disability sends me an email:

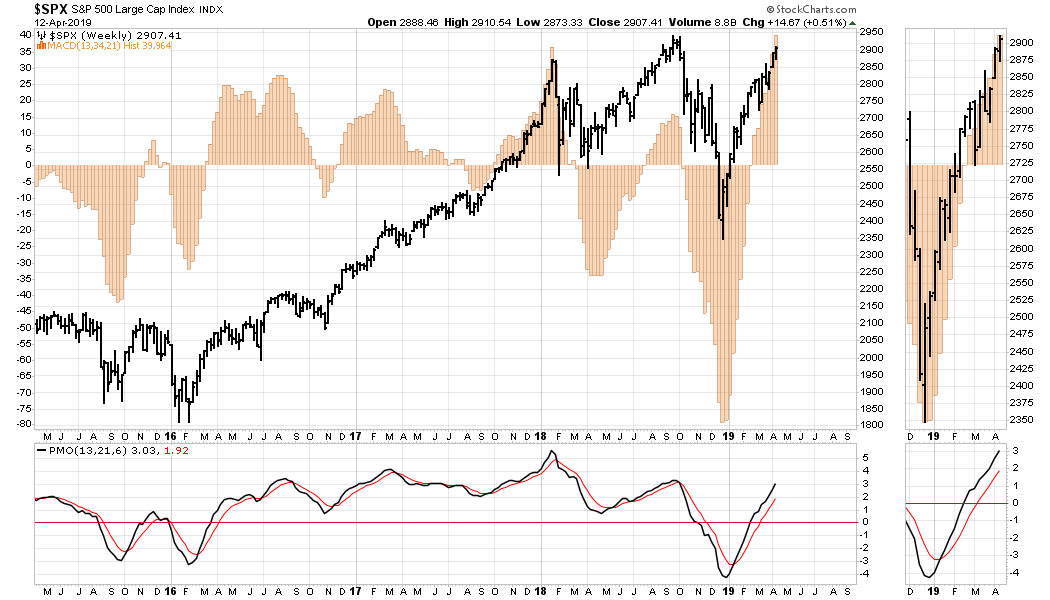

“The market has not been this oversold at any point in the last 20-years, on a monthly basis, as shown in the chart below.

The other bit of good cheer for the bulls is that unlike the previous two starts to more protracted bear markets, the long-term monthly uptrend has not been broken, yet. As noted above, the market is sitting on that uptrend support line which began in 2009.

At this point, the risk/reward for traders is clearly sided to the bulls…for now.”

So, for the reading impaired:

We are carrying reduced equity long positions, we are overweight cash, and fixed income because the deeply oversold condition which previously existed has been entirely reversed. This has occurred at a time where the earnings and economic backdrop are deteriorating, not improving.

Simply, the risk/reward setup is no longer as favorable as it was in December.

Make Stock Buybacks Illegal?

“Few topics prompt as powerful (and violent) a response from financial professionals as what the role of financial buybacks is in determining stock prices.

One group, largely those bulls who after a decade of central bank manipulation still believe that markets are efficient and unrigged, argue that stock buybacks have no impact on stock prices.

The other group, those who actually understand that if there is a trillion dollars in price indiscriminate stock bids is the single most effective way to boost stock prices, know that corporate buybacks, which until not too long ago were banned, and which over the past decade emerged as the single biggest source of stock purchases, are one of the two most important factors behind the all time highs in the stock market (the other being the Fed, whose policies have allowed companies to issue debt with record low yields, allowing them to fund these trillions in buybacks).” – Zerohedge, April 4, 2019

It is an interesting debate.

What makes this debate particularly notable, and as noted above, most people don’t remember that share repurchases were banned for decades prior to President Reagan in 1982.

So, why were they banned in the first place? Via Vox:

“Buybacks were illegal throughout most of the 20th century because they were considered a form of stock market manipulation. But in 1982, the Securities and Exchange Commission passed rule 10b-18, which created a legal process for buybacks and opened the floodgates for companies to start repurchasing their stock en masse.”

This isn’t the first time we have reversed policy previously put into place to avert Wall Street from taking advantage of the market to fill their own coffers.

The Crash of 1929

Leading up to the crash of 1929, banks, which were entrusted with people’s life savings, were on both sides of the investment game. They loaned money to investors to speculate with, and they were speculating in the markets themselves. What could possibly go wrong?

“Stocks are now at a permanently high plateau” – Dr. Irving Fisher, 1929

Following the crash, the SEC was formed to “police” the financial markets and protect investors from the predatory practices of Wall Street and the Banks. Part of that process was the passage of the Glass-Steagall act in 1933 to separate banking and brokerage activities in order to build a wall between the source of funds (bank deposits) and the use of funds (speculative investment.)

For nearly 70-years the markets functioned properly. However, in 1999, Congress repealed Glass-Steagall under tremendous pressure from the major banks who lobbied heavily to gain access to the massive revenue being generated from the “dot.com” mania.

It didn’t take long.

Just seven short years later, the world came apart in the biggest crisis/recession since the “Great Depression.” Not surprisingly, at the very center of the financial and economic destruction, were the major banks taking advantage of the investing public once again.

Coincidence?

“History may not repeat, but it often rhymes.” – Mark Twain

As noted, for decades stock buybacks were banned due to the problem of potential market manipulation. It is important to remember that regulations are NEVER passed in ADVANCE of a problem, they are always imposed in RESPONSE to a problem.

What Are We Talking About?

Like stock splits, share repurchases in and of themselves are not necessarily a bad thing, they are just the least best use of cash. Instead of using cash to expand production, increase sales, acquire competitors, or buy into new products or services, the cash is used to reduce the outstanding share count and artificially inflate earnings per share. Here is a simple example:

Company A earns $1 / share and there are 10 / shares outstanding.

Earnings Per Share (EPS) = $0.10/share.

Company A uses all of its cash to buy back 5 shares of stock.

Next year, Company A earns $0.20/share ($1 / 5 shares)

Stock price rises because EPS jumped by 100%.

However, since the company used all of its cash to buy back the shares, they had nothing left to grow their business.

The next year Company A still earns $1/share and EPS remains at $0.20/share.

Stock price falls because of 0% growth over the year.

This is a bit of an extreme example but shows the point that share repurchases have a limited, one-time effect, on the company. This is why once a company engages in share repurchases they are inevitably trapped into continuing to repurchase shares to keep asset prices elevated. Share repurchases divert ever-increasing amounts of cash from productive investments and takes away from longer-term profit and growth.

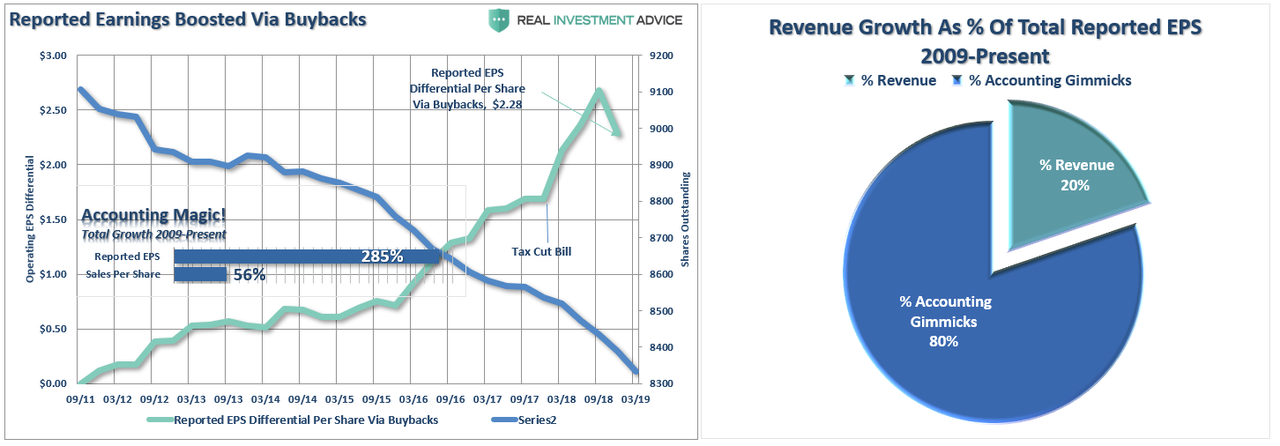

As we just discussed last week, since the recessionary lows, much of the rise in “profitability” has come from a variety of cost-cutting measures and accounting gimmicks rather than actual increases in top-line revenue. While tax cuts certainly provided the capital for a surge in buybacks, revenue growth, which is directly connected to a consumption-based economy, has remained muted.

The reality is that stock buybacks create an illusion of profitability. Such activities do not spur economic growth or generate real wealth for shareholders, but it does provide the basis for with which to keep Wall Street satisfied and stock option compensated executives happy.

Don’t believe me?

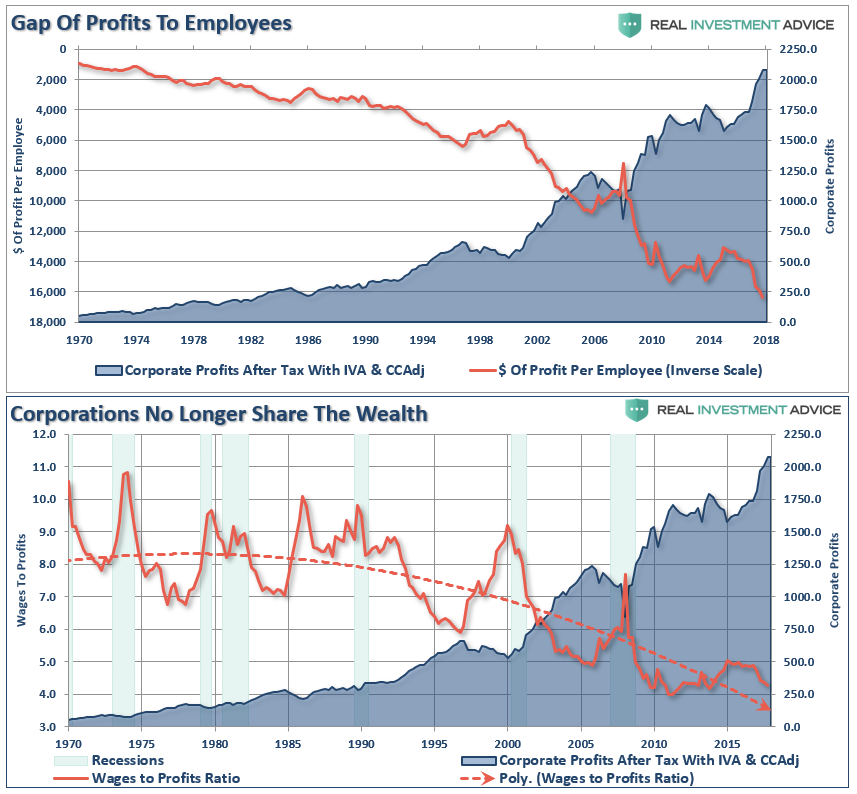

In 1982, according to the Economic Policy Institute, the average CEO earned 50 times the average production worker.Today, the CEO Pay Ratio’s increased to 144 times the average workerwith most of the gains a result of stock options and awards.

As shown in the chart below, clearly profits aren’t being shared with “working class stiffs.”

Tax Cuts For Corporations

As I wrote in early 2018. while it was widely believed that tax cuts would lead to rising capital investment, higher wages, and economic growth, it went exactly where we said it would. To wit:

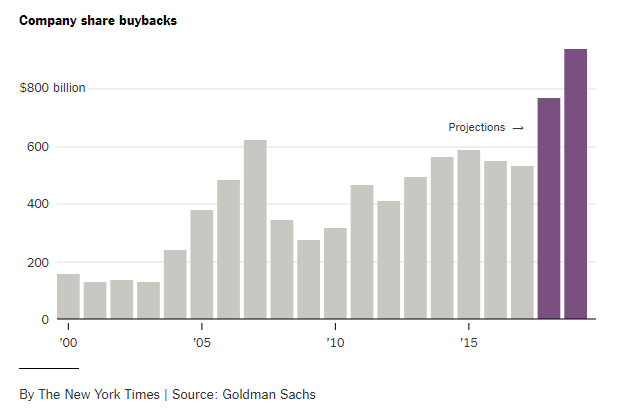

“Not surprisingly, our guess that corporations would utilize the benefits of ‘tax cuts’ to boost bottom line earnings rather than increase wages has turned out to be true. As noted by Axios, in just the first two months of this year companies have already announced over $173 BILLION in stock buybacks. This is ‘financial engineering gone mad’”

Share buybacks are expected to hit another new record by the end of 2019.

Let’s clear up a myth used to support the benefit of stock buybacks:

“Share repurchases aren’t bad. It is simply the company returning money to shareholders.”

Here is the issue:

Share buybacks only return money to those individuals who sell their stock. This is an open market transaction. For example, when Apple (AAPL) buys back some of their outstanding stock, the only people who receive any capital from the buyback are those who sold their shares.

So, who are the ones mostly selling their shares?

As noted above, it’s the insiders, of course, as changes in compensation structures since the turn of the century has become heavily dependent on stock issuance. Insiders regularly liquidate shares which were “given” to them as part of their overall compensation structure to convert them into actual wealth. As the Financial Times recently penned:

“Corporate executives give several reasons for stock buybacks but none of them has close to the explanatory power of this simple truth: Stock-based instruments make up the majority of their pay and in the short-term buybacks drive up stock prices.”

A recent report on a study by the Securities & Exchange Commission found the same:

SEC research found that many corporate executives sell significant amounts of their own shares after their companies announce stock buybacks, Yahoo Finance reports.

What is clear, is that the misuse and abuse of share buybacks to manipulate earnings and reward insiders has become problematic. As John Authers recently pointed out:

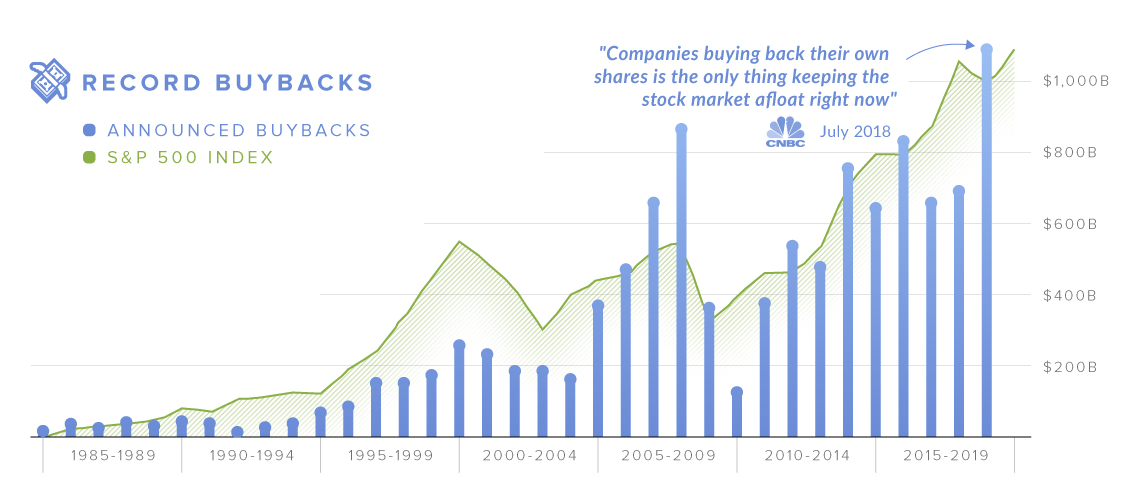

“For much of the last decade, companies buying their own shares have accounted for all net purchases. The total amount of stock bought back by companies since the 2008 crisis even exceeds the Federal Reserve’s spending on buying bonds over the same period as part of quantitative easing. Both pushed up asset prices.”

In other words, between the Federal Reserve injecting a massive amount of liquidity into the financial markets, and corporations buying back their own shares, there have been effectively no other real buyers in the market.

Don’t Have Cash, Use Debt

The other problem with the share repurchases is that is has increasingly been done with the use of leverage. The ongoing suppression of interest rates by the Federal Reserve led to an explosion of debt issued by corporations. Much of the debt was not used for mergers, acquisitions or capital expenditures but for the funding of share repurchases and dividend issuance.

Furthermore, with 62% of investment grade debt maturing over the next five years, there are a lot of companies that are going to wish they didn’t buy back so much stock. This debt load will become problematic if rates rise markedly, further deterioration in credit quality locks companies out of refinancing, or if there is a recessionary drag which forces liquidation of debt. This is something Dallas Fed President Robert Kaplan warned about:

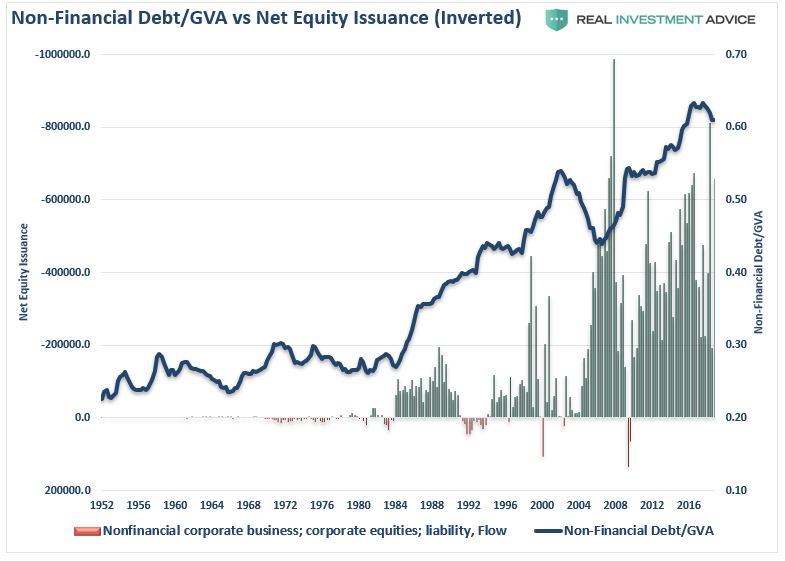

U.S. nonfinancial corporate debt consists mostly of bonds and loans. This category of debt, as a percentage of gross domestic product, is now higher than in the prior peak reached at the end of 2008.

A number of studies have concluded this level of credit could ‘potentially amplify the severity of a recession,’

The lowest level of investment-grade debt, BBB bonds, has grown from $800 million to $2.7 trillion by year-end 2018. High-yield debt has grown from $700 million to $1.1 trillion over the same period. This trend has been accompanied by more relaxed bond and loan covenants, he added.

This was recently noted by the Bank of International Settlements.

“If, on the heels of economic weakness, enough issuers were abruptly downgraded from BBB to junk status, mutual funds and, more broadly, other market participants with investment grade mandates could be forced to offload large amounts of bonds quickly. While attractive to investors that seek a targeted risk exposure, rating-based investment mandates can lead to fire sales.”

Make Stock Buybacks Illegal?

Now that you understand the background, and who share buybacks actually benefit, you can understand the reasoning behind wanting to ban them once again.

While share repurchases by themselves may indeed seem somewhat harmless, it is when they are coupled with accounting gimmicks, and massive levels of debt to fund them, in which they become problematic. This issue was noted by Michael Lebowitz:

“While the financial media cheers buybacks and the SEC, the enabler of such abuse idly watches, we continue to harp on the topic. It is vital, not only for investors but the public-at-large, to understand the tremendous harm already caused by buybacks and the potential for further harm down the road.”

However, there are significant consequences in resetting the system.

“Eliminating buybacks would immediately force firms to shift corporate cash spending priorities, impact stock market fundamentals, and alter the supply/demand balance for shares… The potential restriction on buybacks would likely have five implications for the US equity market: (1) slow EPS growth; (2) boost cash spending on dividends, M&A, and debt paydown; (3) widen trading ranges; (4) reduce demand for shares; and (5) lower company valuations.”– David Kostin, Goldman Sachs

If you are a short-term stock market bull, you will probably not want that. However, as my friend Doug Kass notes there are long-term benefits to reforming the system and putting corporations back onto a more “economically friendly” level:

My plan is simple.

Make buybacks illegal.

Allow companies to dividend out cash tax-free, like a buyback. This keeps companies out of the market and prevents them from manipulating their own stock, which often benefits company insiders who are selling.

Then the decision of what to do with corporate cash becomes more pure.

It no longer will be a choice of trying to prop up a stock versus spending it on the business.

Companies will still be left to do with their own cash what they want.

This is the other big problem, the fact that dividends are taxed, but buybacks are not.

That doesn’t make too much sense to me.”

In the end, the S.E.C. will move to once again ban stock buybacks as they did once before.

Unfortunately, it will be in response to (not to mention the pressure of public outrage) the next financial crisis that devastates a vast majority of the U.S. economy.

But that is just the way the system works.

via ZeroHedge News http://bit.ly/2KCM0wR Tyler Durden

Hundreds of people were ordered evacuated from homes, hospitals, and public buildings in the old city of Frankfurt on Sunday so a bomb disposal unit could detonate an old World War II era bomb discovered last week in the Main River.

The 250-kilogram U.S. Air Force bomb was reported successfully detonated, with dramatic photographs showing a massive wall of water spurting many stories high into the air.

A 250 kilogram American bomb from the Second World War was detonated in the Main River behind the Iron Bridge in Frankfurt, Germany on Sunday, April 14, 2019. Image source: EPA via AP

The “live” bomb had been discovered on Tuesday during a dive exercise in Frankfurt’s centrally located Main River, close to city residential buildings.

Both sides of the river were evacuated during Sunday’s detonation, which authorities said went off without any issues, and divers were again deployed to examine it to ensure it was safe and had fully exploded.

Mit einem lauten Knall und einer riesigen Wasserfontäne ist am Sonntag die #Weltkriegsbombe im Frankfurter Main auf spektakuläre Weise unschädlich gemacht worden. pic.twitter.com/Ib5lnAljDG

The BBC reported that “some 600 people were evacuated from parts of the city as bomb disposal experts got to work at about 08:00 local time (06:00 GMT) on Sunday.”

Now seven decades following the end of WWII, bombs and munitions turn up regularly throughout Germany, but such a large bomb located in the center of a major city is still considered rare.

However, this weekend’s evacuation pales in comparison to a similar detonation event almost exactly one year ago, in April 2018, when some 10,000 were ordered to leave central Berlin so that German police could defuse a WWII bomb there.

* * *

For comparison, here is a 250km WWII-era bomb detonated in Munich in 2012, conducted above ground/water. Essentially this is what happened at the bottom of the Main River in Frankfurt on Sunday.

via ZeroHedge News http://bit.ly/2DfrUCz Tyler Durden

I recently detailed why a recession is imminent based on a few factors, chiefly full employment among the working age segments of the population and minimal population growth among the same segments, detailed HERE. However, today I wanted to outline the impact that women moving into the labor force had on growing the labor force, but why this growth has ceased. I’ll also point out that the 2008-’09 financial crisis was a demographically driven crisis that was set decades earlier.

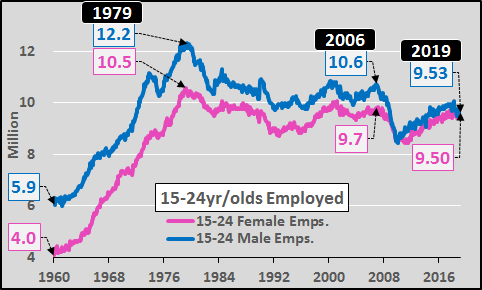

15 to 24 Year Olds

The chart below shows 15 to 24 year old employed males and females, from 1960 to present. Based on the peak 15 to 24 employment in 1979 (and subsequent four decades of decline), there was always sure to be a like peak (and like fall) among the 25 to 54 year old core population 30 years later…or 2009. Noteworthy is the relatively larger decline in employment among males than among females…and the fact that men and women make equal parts of the total employed persons.

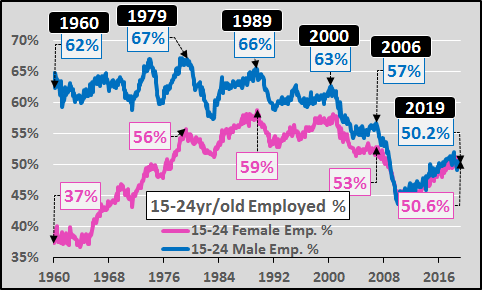

The 15 to 24 year old percentage of males and females employed, chart below. The peak in the percentage of males employed was in 1979 at 67% and 1989 at 59% for females. Both have been receding since and sit at 50%.

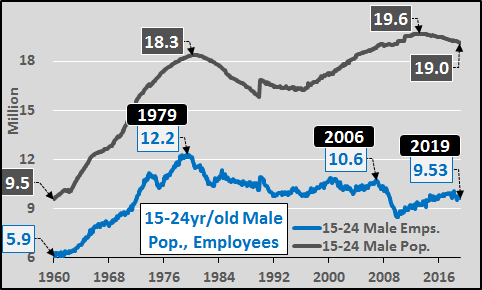

15 to 24 year old male population and employees, 1960 to present, below. While the total 15 to 24 population has essentially been unchanged since 1979, the total number of 15 to 24 employed males has consistently been in decline since 1979, a fall of 2.7 million (a 21% fall) over the last 40 years.

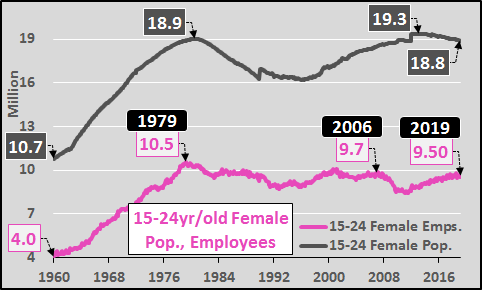

15 to 24 year old female population and employees below, 1960 to present. Peak 15 to 24 female employment came in 1979 and currently sits 1 million fewer than that peak (a 9% fall).

25 to 54 Year Olds

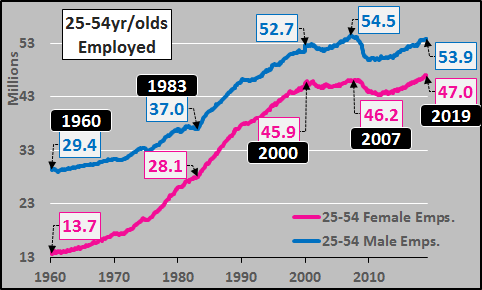

25 to 54 year old employed male and females, below. From 1960 to 2000, male employment rose 23 million while female employment rose a massive 32 million. Contrast that with since 2000, the quantity of employed males has increased by just 1.1 million and females by 1.3 million. Today, there are still 600 hundred thousand fewer employed males than in 2007 while employed females have increased by just 800 hundred thousand.

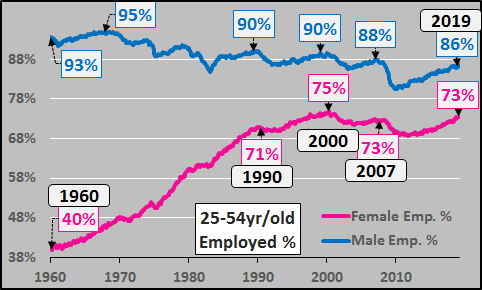

The percentage of 25 to 54 employed males has been in secular decline since mid-1960. However, the percentage of 25 to 54 females rose sharply from 1960 to 2000, but has like males, been in decline since 2000.

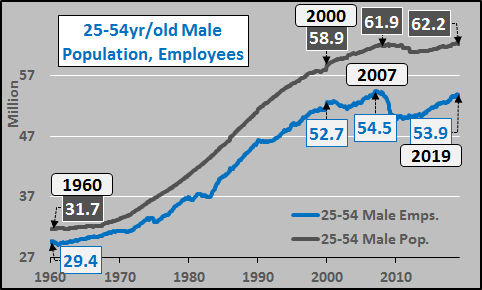

25 to 54 year old male population and employees, below. With minimal population growth and full employment, there is little chance for further growth in employment.

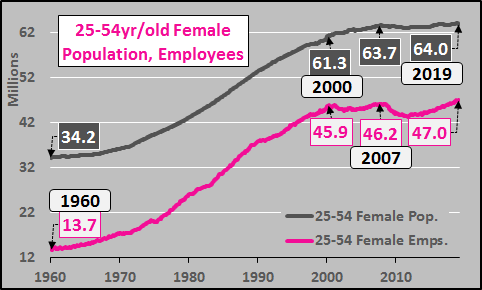

Chart below is 25 to 54 year old female population and employees. Ditto for the lack of population growth and minimal further employment growth.

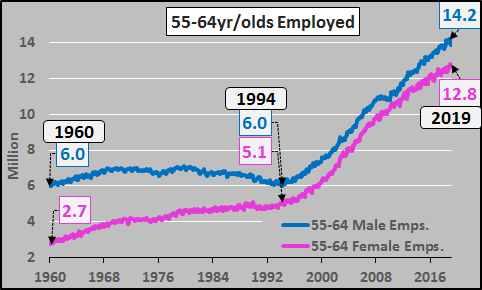

55-64 Year Olds

55 to 64 year old male and female employees, below. No growth among male employees from 1960 through 1994 while females rose by 2.4 million. Since 1994, male 55 to 64 employment has risen by over 8 million and female employment by 7.7 million.

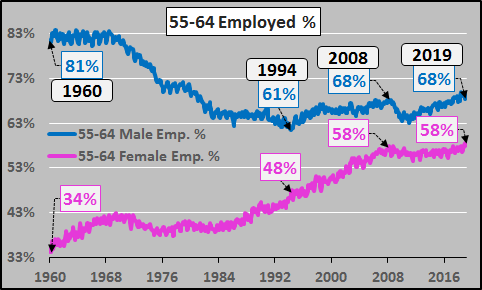

55 to 64 year old male and female employed percentages charted below. The decline in the percentage of males employed to 1994 and slight rise since. The percentage of 55 to 64 females employed consistently rose from ’60 to ’08, but like the percentage of males employed, appears to have hit peak employment since ’08.

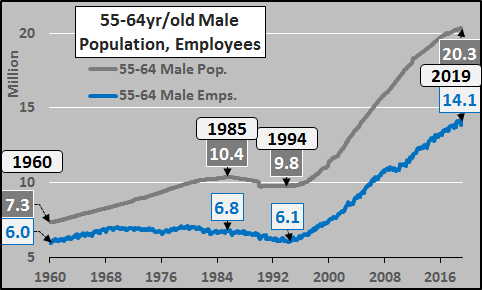

55 to 64 year old male population and employees, charted below. The growth of the 55 to 64 male/female population, and employed among them, has been the saving grace for the US over the past 25 years. However, the demographically driven 55 to 64 population growth impetus is fast coming to an end.

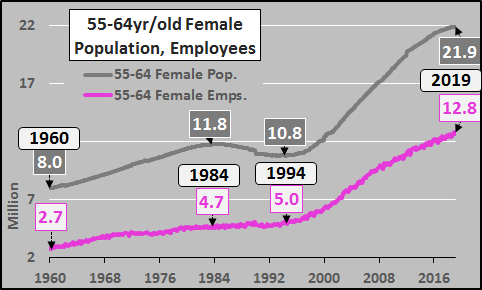

55 to 64 year old female population and employees, below.

65+ Year Olds

That tell-tale baby-boom population surge is now heading into the 75+ year old population segment (grey line below)…a group that has an 8% labor force participation rate. Even the 65 to 74 year old labor force participation rate is just 27%. Elderly population growth does not equate to employment or economic growth.

And finally, a juxtaposition of no rise (net) in births for five decades, (and now nearly a half million annual decline in births since 2007), versus a near doubling in total population. Big details, like the lack of working age population growth, subsequent employment growth, and resultant economic growth…can be hidden in big numbers.

Conclusion:

The possibility of the female working age population has been fully realized, and now appears to be at full employment. Population growth in America has shifted to the elderly, that have very low labor force participation rates. Presently, and for at least the next decade, there is no clear impetus for further growth in employment except participation rates moving well above historical norms or elderly remaining in the labor force far beyond expected levels. Without the growth in employment, there is no impetus for growth in consumption, new housing creation, or economic growth.

via ZeroHedge News http://bit.ly/2VJ2jt5 Tyler Durden

Democratic presidential candidate Cory Booker says that Americans would be “less safe” if illegal immigrants were released from locked detention centers into migrant-friendly American cities – a plan which President Trump has threatened to explore.

When asked by Face the Nation’s Margaret Brennan whether Trump’s threat was an empty one, or if he was simply trying to create friction, Booker replied: “You say ‘friction’ — I say he’s trying to pit Americans against each other and make us less safe.”

Following reports that the White House had discussed releasing a flood if migrants into Democratic-controlled, undocumented-friendly sanctuary cities, President Trump on Friday said that he was “giving strong considerations” to the idea.

….The Radical Left always seems to have an Open Borders, Open Arms policy – so this should make them very happy!

Earlier Friday, the Washington Post and ABC News reported that the Trump administration had twiced pushed for transferring migrants to sanctuary cities, citing anonymous senior government officials familiar with the matter.

In response to taking detained migrants and placing them in the care of cities which have pledged to protect them, Democrats lashed out.

“The extent of this Administration’s cynicism and cruelty cannot be overstated,” said Nancy Pelosi’s spokeswoman Ashley Etienne in a Friday statement. “Using human beings—including little children—as pawns in their warped game to perpetuate fear and demonize immigrants is despicable, and in some cases, criminal.”

Noting safety concerns, Pelosi’s aide added: “The American people have resoundingly rejected this Administration’s toxic anti-immigrant policies, and Democrats will continue to advance immigration policies that keep us safe and honor our values.”

Cory Booker says on @FaceTheNation that releasing illegal immigrants into sanctuary cities will “make us less safe.” Nice to see some hypocritical elected Democrats telling the truth now that they face a flood of illegals in their cities. pic.twitter.com/oFxqMsqBUz

On Saturday night, President Trump said over Twitter that “The USA has the absolute legal right to have apprehended illegal immigrants transferred to Sanctuary Cities,” and demanded that “they be taken care of at the highest level, especially by the State of California, which is well known or its poor management & high taxes!”

Just out: The USA has the absolute legal right to have apprehended illegal immigrants transferred to Sanctuary Cities. We hereby demand that they be taken care of at the highest level, especially by the State of California, which is well known or its poor management & high taxes!

On Sunday Rep. Bennie Thompson (D-MS) – chairman of the House Homeland Security Committee, said that he doesn’t “see a legal way” to release undocumented immigrants into sanctuary cities.

“More importantly, this is again his manufactured chaos he’s created over the last two years on the border,” said Thompson. “Before Donald Trump took office, we had a situation that was manageable. We had spikes, but it also went down, but what we have now is a constant pushing of the system so that it doesn’t work.”

House Homeland Security Committee chairman Rep. Bennie Thompson (D-MS)

Thompson added that transferring the migrants to sanctuary cities was “not about keeping the country safe, but about partisan politics and wantonly inflicting cruelty.”

Perhaps Thompson could explain how taking migrants out of locked facilities and placing them in the care of sanctuary cities constitutes cruelty?

California Governor Gavin Newsom called the idea “asinine” – adding that it is “unserious,” “illegal,” and “sophomoric.”

“It really is the sophistry of adolescence. It’s not serious. It lacks any rationale. It’s insulting to the American people and to the intelligence of the American people. It’s un-American. It’s illegal. It’s immoral. It’s rather pathetic. I don’t know what more I can say,” said Newsom.

Dems – Sanctuary cities: “compassionate and humane”

Also Dems – Releasing illegals into sanctuary cities: “uncompassionate and inhumane”

Dems – Green New Deal: “critical to Earth’s survival”

The US has been planning to have Julian Assange handed over for a longtime, that much is obvious. Mike Pence, the Vice President, was visiting Ecuador last year, notionally to discuss the Venezuela situation, and trade. But it was fairly obvious at the time, and even more so now, that they were discussing the details of Assange being handed over to UK authorities, and eventually extradited to the US.

“Trade”, indeed.

In terms of quid pro quo, the situation is clear-cut – In February, Ecuador got a $4.2 BILLION loan approved by the International Monetary Fund (amongst other pay-outs). Reuters reported on February 19th of this year:

Ecuador has reached a $4.2 billion staff-level financing deal with the International Monetary Fund (IMF), President Lenin Moreno said on Wednesday, as the Andean country grapples with a large fiscal deficit and heavy external debt.

The country will also receive $6 billion in loans from multilateral institutions including the World Bank, the Inter-American Development Bank, and the CAF Andean development bank…

So, less than 2 months ago, it was announced Ecuador was going to receive over 10 billion dollars of loans. Where all that money will eventually end up is anyone’s guess, it certainly isn’tbeing spent on infrastructure or state enterprise:

Moreno has begun to implement an austerity plan that includes layoffs of workers at state-owned companies and cuts to gasoline subsidies, also plans to find a private operator for state-run telecoms company CNT and other state-owned firms.

President Moreno has already been the subject of numerous corruption accusations. So these “loans”, nominally for “[creating] work opportunities for those who have not yet found something stable”, could more realistically be described as “a pay-off”.

More than just money, Lenin Moreno has been gifted something all insecure third-world leaders crave: Western approval.

The Economist ran a story on April 12th, the day after Assange was arrested, praising Lenin Moreno’s economic policies, and blaming the previous administration for the “mess” that Moreno has to clear ups. (Of course, the idea that Moreno is handling the economy brilliantly, but somehow also needs over $10 billion dollars in loans is never addressed. A tiny logical contradiction compared with the nonsense the MSM dish-up on a daily basis).

The basic structure of the give-and-take of this situation is fairly obvious.

Less on the nose, but still definitely present, is the slow-burn media-based campaign of defamation and smears directed at Assange. A campaign designed to weaken public support for him and lessen the potential outcry if/when the UK handed him to US authorities, who famously use “enhanced interrogation” on suspects.

Last October, just three months after Pence’s Ecuador visit, an Ecuadorian government memo was “leaked” claiming that Assange had bad personal hygiene habits, was hacking people’s electrical devices, and neglecting his cat. These charges, cynically designed to make Assange a figure of ridicule, got massive play in the media. The Guardian, ever at the vanguard of sticking the boot in on Assange, ran a gleeful opinion piece mocking him. As did many other publications.

To this day we have no way of knowing if there is any veracity to this “leaked” memo, but real or not, it served both to belittle Assange in the public mind, and provide Ecuador with an excuse to get rid of him (they set up “rules”, claim Assange wasn’t following them and THAT’s why they kicked him out – not the 10 billion dollars they got from international financial institutions).

The media are, of course, complicit in this lie.

Various outlets, from the Guardian, to CNN to the Australian have written “explainer” articles with headlines such as: ‘Rude, ungrateful and meddling’: why Ecuador turned on Assange.

Because – you know – ‘rude and ‘ungrateful’ people don’t deserve to have their human rights respected. There’s probably a clause in the UN charter to that effect.

Every step of this ignoble process, so far, has been based on lies. Let’s list them.

Lie #1: Assange hs been and is attacked as a “Russian agent” and “Putin’s stooge”. A “breaking news” story for the Guardian, written by an erstwhile plagiarist and a convicted forger, claimed Assange had worked with Paul Manafort to swing the US election for Trump.

No evidence for these claims has been supplied. It remains to date nothing more than a baseless allegation, and WikiLeaks is in the process of suing the Guardian over it. This lie paints Assange as an “enemy combatant”, and will be used to justify whatever happens to him.

Lie #2: Let’s all recall that, for months, we were told the US didn’t want Assange, that “the only barrier to him leaving the embassy was pride”. WikiLeaks claims that US had sealed indictments waiting for Assange were dismissed as “conspiracy theories”.

Lie #3: Just one week ago, the Ecuadorian government claimed they had NO plans to kick Assange out, and that WikiLeaks lied when they claimed as much.

They released Assange to UK police just six days later.

Equally obnoxious and dishonest is the ‘corporate concern trolling’ that allows faux-liberals to take up the craven position of “qualified support”, such as:

“You can think Assange is a liar, fascist and misogynist, but still think he shouldn’t be extradited”

This is the stance adopted by folks like Owen Jones in the Guardian, a position which claims to support one course of action, but is actually covertly arguing for the opposite. Damning Assange with the pretence of faint praise.

And ‘identity politics’ is also playing its part here – displaying its usefulness in clogging up public debate with shallow finger-pointing and Crucible-esque accusations of moral impurity. (Jones labels anyone who doesn’t believe the accusations against Assange “a misogynist”).

Suzanne Moore, the epitome of the liberal hypocrite, wrote a column for the New Statesmentalking quite a lot about totally unproven accusations of “molestation”, but breezing over the very-much-proven crimes against humanity.

Meanwhile seventy UK MPs, including “people’s champion” Jess Philips, and John Woodcock (who quit Labour over accusations of sexually inappropriate behaviour), signed a letter to Sajid Javiddemanding Assange be handed over to Sweden to face “justice”. A position marred only by the fact that Sweden haven’t actually asked for him yet. (This was aimed at Corbyn and Diane Abbott, whose support for Assange will be turned against them, and used to label Labour as being “soft on sexual predators” or “not supporting women” etc).

But this is all distraction and obfuscation – keeping the totally discredited accusations in the headlines, whilst avoiding the actual truth, which is:

Julian Assange was arrested for publishing evidence of US war crimes, after the US government bribed the Ecuadorian government to break international law.

That is what happened. And anyone who uses lies and distraction to deny this truth is on the wrong side of history.

via ZeroHedge News http://bit.ly/2IioG5l Tyler Durden

When President Trump demanded earlier this month that the Fed should cut interest rates to undo some of the damage it has done to the economy with its pernicious rate hikes, we pointed out the obvious dissonance between advocating for rate cuts while insisting that the economy is the strongest it has ever been.

TRUMP SAYS FED SHOULD DROP RATES, STOP QUANTITATIVE TIGHTENING

But the incongruity disappears when one considers that the central bank’s “dual mandate” simply masks its true purpose: To levitate asset prices and ensure that wealthy Americans get richer, while (at least for now) averting an all-out pension fund crisis.

Though the central bank’s “third mandate” is rarely, if ever, directly acknowledged, President Trump violated this convention in a tweet on Sunday, when he declared that the central bank, had it “done its job properly” would have sent the Dow another 5,000 to 10,000 points higher, and that GDP growth would have been “well over 4%”.

If the Fed had done its job properly, which it has not, the Stock Market would have been up 5000 to 10,000 additional points, and GDP would have been well over 4% instead of 3%…with almost no inflation. Quantitative tightening was a killer, should have done the exact opposite!

In essence, this is the president admitting that the Fed’s only job is to push stocks higher, damn the deteriorating fundamentals that make leave valuations increasingly divorced from reality.

According to Donald, the Fed’s job is now OFFICIALLY blowing even bigger stock market bubbles! https://t.co/mSUma4wuqO

While this tweet will almost certainly elicit howls from economists warning about the damage Trump is doing to the Fed’ precious ‘credibility’ (or whatever is left of it), we think it’s refreshing to finally hear the most powerful man in the free world speak openly about its most powerful central bank.

via ZeroHedge News http://bit.ly/2GbhNj0 Tyler Durden

{kind=link}

{kind=link}

{kind=link}