One day after a global “trade optimism”-inspired rally fizzled at the closing minute of US cash trading, European and Asian shares eased back from eight-month highs while bonds, the dollar and gold rallied as investors took money off the table amid, what else, “fresh concerns” about U.S.-China trade talks while dismal data from Germany signaled trouble for Europe as investors awaited further news from U.S.-China trade negotiations and tomorrow’s US jobs report.

US index futures were flat, while Asian markets and Europe’s Stoxx 600 index fell, led by declines in oil companies and miners.

The biggest economic news of the day was Germany’s latest industrial orders which tumbled at the fastest rate in over five years in February, driven largely by a collapse in foreign demand.

The report compounded fears that Europe’s largest economy, which yesterday slashed its GDP forecast by more than half from 1.9% to 0.8%, has had a feeble start to the year and left the euro stuck at $1.12, sent German Bund yields back below zero in the bond market and ended a four-day run of gains for share traders. Eslewhere, Italian shares and bonds also dropped after Bloomberg reported the country is set to slash this year’s growth forecast and raise the projected budget deficit.

In key company-related news, in the preliminary Ethiopian crash report of the Boeing 737 MAX, anti-stall software is not explicitly mentioned; Chief investigator says they cannot yet say if there is a structural problem with Max 8’s. Meanwhile, Tesla is tumbling after the company’s Q1 vehicle deliveries tumbled and missed badly, with just 63.0k deliveries vs. 90.7k previously.

Earlier in the session, the MSCI Asia index also lost 0.4% overnight after five straight days of gains had taken it to the highest level since late August. Losses were led by Australia and New Zealand while Hong Kong, the Philippines and Indian markets were also in red. The trend was bucked by Shanghai as Chinese shares rose 0.6% while Japan’s Nikkei paused near a recent one-month top.

Emerging-market stocks and currencies also lost momentum on Thursday after recent gains as investors awaited fresh good (or perhaps bad) data for signs the global economy is regaining a firmer footing (or else that central banks will ease more). The MSCI index of developing-market equities fell for a first day in six: the Indian rupee led declines among currencies following a rate cut and dovish outlook from the nation’s central bank. South Africa’s rand weakened after failing to strengthen beyond a key technical level, while the Indonesian rupiah rose after its monetary authority said it would allow further appreciation.

Analysts pointed to investor fatigue and a lack of fresh headlines on the Sino-U.S. trade talks for Thursday’s sell-off while disappointing U.S. economic data this week also weighed on sentiment. “We are expecting quite a constructive agreement between the U.S. and China when it comes to trade,” said AllianceBernstein China Portfolio Manager John Lin. He added it was probably now a consensus view among major investors and if it proved right, would raise other questions such as whether China’s government would “keep its foot on the (stimulus) pedal or ease off a bit.”

Risk sentiment has been supported by constant signs of progress in Sino-U.S. trade talks. White House economic adviser Larry Kudlow said on Wednesday the two sides aimed to bridge differences during talks, while Bloomberg reported that the US would grant China until 2025 to meet trade pledges. The plan would see China committing to buy more U.S. commodities, including soybeans and energy products, and allow full foreign ownership for U.S. companies operating in China as a binding pledge. Investors are also looking if ongoing talks lead to an earlier-than-anticipated meeting between U.S. President Donald Trump and his Chinese counterpart Xi Jinping to sign an accord.

At 2pm all eyes will be on the White House, where President Trump will meet Chinese Vice Premier Liu He as trade deal negotiations enter what could be the final stages.

While investors have become more optimistic that a trade deal will be signed, Bloomberg quotes Nick Twidale, chief operating officer at Rakuten Securities Australia, who said it “may just be another step in the process.” The implementation of any deal “will most probably provide obstacles in the process and may weigh on sentiment further down the track.”

“Also an important question would be whether an agreement would be sufficient to revive business sentiment and the global trade cycle,” J.P. Morgan Asset Management Asia Pacific Chief Market Strategist Tai Hui added. “We believe on the margin it would help, but practically all investors we’ve spoken to in Asia in the past six months believe friction will still flare up from time to time.

In FX, overnight moves were muted after bigger swings overnight when all major currencies gained against the safe-haven yen. The dollar gained broadly with Treasuries while Sterling dipped after U.K. lawmakers moved to block a no-deal Brexit; the euro largely shrugged off soft German data, and was waiting for the minutes of the European Central Bank’s last meeting, when it pushed back rate hike expectations. Euro-area bonds edged higher, and the yen and equities traded with a defensive tone

In commodities, oil prices slipped a second day, with Brent edging down further from the $70 mark after weekly U.S. oil data showed a surprise build up in crude inventories and record production; Global benchmark Brent has gained nearly 30 percent this year, while WTI has gained nearly 40 percent. Prices have been underpinned by tightening global supplies and signs of demand picking up. “There is a clear bias to the upside with the supply restrictions,” said Michael McCarthy, chief market strategist at CMC Markets in Sydney, pointing to supply cuts by OPEC and others, along with sanctions on Iran.

Spot gold traded lacklustre as markets were tentative ahead of the ECB minutes, US-China trade talks and payrolls, with investors pulling money out of gold ETFs with around $153MM removed out of the $10BN VanEck Vectors Gold Miners ETF over the last five days. Meanwhile, copper (-0.3%) succumbs to the cautious risk tone but remains above its 100 WMA of just under $2.90/lb. Finally, Dalian iron ore futures saw its best day in seven-weeks, extending its record-breaking rally, as supply-side woes (largely from cyclones in Western Australia) and a pick-up in demand (steel mills replenishing stocks) boosted the base metal to a new peak of USD 103.49/tonne.

On today’s docket, initial jobless claims are due, while companies reporting earnings include Constellation Brands and RPM International.

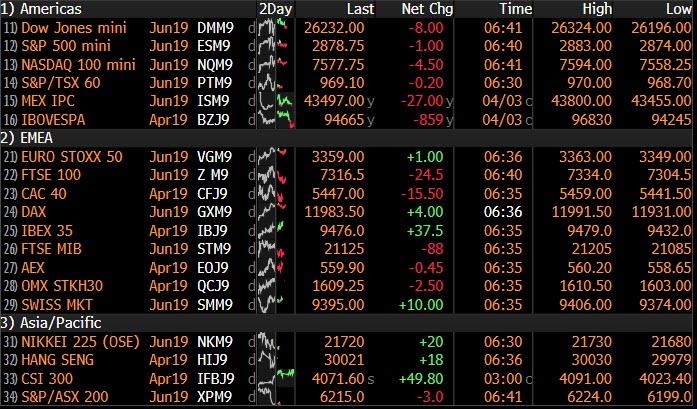

Market Snapshot

- S&P 500 futures down 0.1% to 2,876.25

- STOXX Europe 600 down 0.4% to 387.49

- MXAP down 0.2% to 162.37

- MXAPJ down 0.4% to 538.98

- Nikkei up 0.05% to 21,724.95

- Topix down 0.1% to 1,620.05

- Hang Seng Index down 0.2% to 29,936.32

- Shanghai Composite up 0.9% to 3,246.57

- Sensex down 0.3% to 38,761.75

- Australia S&P/ASX 200 down 0.8% to 6,232.80

- Kospi up 0.2% to 2,206.53

- German 10Y yield fell 0.9 bps to -0.001%

- Euro up 0.04% to $1.1237

- Brent Futures down 0.6% to $68.88/bbl

- Italian 10Y yield rose 1.5 bps to 2.186%

- Spanish 10Y yield fell 0.7 bps to 1.134%

- Brent Futures down 0.4% to $69.05/bbl

- Gold spot up 0.1% to $1,291.33

- U.S. Dollar Index unchanged at 97.10

Top Overnight News from Bloomberg

- U.S. President Donald Trump will meet Chinese Vice Premier Liu He at the White House on Thursday as speculation grows that negotiations over a trade deal are entering their final stages

- Britain took a decisive step away from a damaging no-deal Brexit as members of Parliament and political leaders backed efforts to prevent a disorderly departure from the EU

- Though the U.K. is better prepared for a no-deal Brexit than it was a number of months ago, it would still cause a large economic shock, the Times reports, citing Bank of England governor Mark Carney

- European Union increasingly sees a long Brexit delay as the most likely outcome of an emergency leaders’ summit next week, according to EU officials

- Trade deal that the U.S. and China are crafting would give Beijing until 2025 to meet commitments on commodity purchases and allow American companies to wholly own enterprises in the Asian nation, according to people familiar with the talks

- Bank of Japan is likely to unveil its lowest two-year inflation forecast under Haruhiko Kuroda’s governorship at a meeting later this month, according to a former chief economist of the central bank

- Trump administration is examining options for shutting entry points to the U.S. from Mexico in case the president follows through with his threat to close the border, a White House official said

- Nomura will fire about 100 workers at its troubled European business as Japan’s biggest brokerage embarks on its latest attempt to achieve sustained profitability overseas; the job cuts in Europe will mostly target rates and credit traders in London, one of the people said, asking not to be identified as the numbers aren’t public

- Italy is set to slash its growth forecast for this year and raise its projected budget deficit, according to two senior officials with knowledge of the draft outlook. Italy’s economy is set to grow just 0.1 percent this year, according to the draft, the officials said. The government’s previous forecast was for a 1 percent expansion

- India’s central bank delivered a back-to-back interest rate cut on Thursday and fueled speculation of more policy easing after lowering inflation and economic growth forecasts

Asian equity markets traded cautiously with the region tentative ahead of looming risk events and after a positive lead from Wall St. where US-China trade optimism kept stocks afloat despite poor ISM & ADP data. ASX 200 (-0.8%) and Nikkei 225 (Unch.) were subdued with broad weakness seen across all sectors in Australia as the post-budget euphoria faded and profit-taking set in following a 7-day win streak, while the Japanese benchmark was indecisive amid a choppy currency. Chinese markets were mixed ahead of an extended weekend in which the Hang Seng (-0.2%) stalled after it briefly rose above 30k for the first time since June last year, while the Shanghai Comp. (+0.9%) was boosted on hopes US and China are nearing a trade deal and with reports also suggesting a Trump-Xi meeting date to sign off on a deal could be announced as early as today. Finally, 10yr JGBs were lower as prices tracked the recent weakness in T-notes and as Japanese stock markets held above water for most the session, while mixed results at the 30yr auction also failed to spur demand.

Top Asian News

- India Central Bank Cuts Interest Rate to Boost Flagging Economy

- Bank Indonesia Chief Says Rate Is on Hold Amid Global Risks

- China Willing to Work With U.S. on Agreement Reached by Leaders

- Japan Post Insurance to Sell $3.7 Billion Shares in Global Deal

A subdued start to the fourth European session of the week with stocks treading water thus far [Eurostoxx 50 U/C] following a mixed Asia-Pac session, ahead of key risk events including the ECB minutes and US-Sino trade talks. The FTSE 100 (-0.6%) marginally lags in the equity-space as a slew of ex-divs [Direct Line (-5.0%), St James’ Place (-3.4%) and DS Smith (-2.4%)] coupled with a firmer Pound pressure the index. Broad-based losses are seen across European sectors, although energy names are faring slightly worse amidst marginal downside in the oil complex. In terms of individual movers, Commerzbank (+2.4%) trades near the top of the Stoxx 600 amid reports that UniCredit (-1.4%) may bid on the German bank if a Deutsche Bank (-1.7%) deal fails. Meanwhile, Software AG (+3.0%) shares were bolstered by a broker upgrade at UBS. On the flip side, Maersk (-11.2%) shares declined following the separate listing of its drilling unit.

Top European News

- Commerzbank Shares Rise on Report of Possible UniCredit Offer

- ICG Said to Near $1.2 Billion Deal for Italy’s Doc Generici

- German Institutes Slash 2019 Growth Forecast by More Than Half

- Miners Fall as Iron Ore Rally Pauses on Anglo and GS Warnings

In FX, the Dollar index is holding around the 97.000 level within an extremely narrow 97.013-225 range, and symptomatic of the listless tone in the G10 currency markets overall after choppy trade from Monday through Wednesday amidst fluctuating risk on, off and on again sentiment. However, today and Friday offer some prospect of more decisive moves or at least price action if not clear direction, with the ECB Minutes, Fed speakers and NFP on the agenda.

- GBP – The Pound remains underpinned as UK Parliament passed another motion to avoid a no deal Brexit and request that PM May go back to the EU seeking a further A 50 extension if no alternative is found to the WA by April 12 or May 22 (assuming no sudden change of heart and the current proposal with Brussels is accepted as the better of evils vs a CU). Cable has rebounded from yesterday’s sub or circa 1.3120 lows to retest 1.3200, but not quite as near the big figure this time as 21/30 DMA convergence around 1.3165 continues to exert some gravitational influence. Similarly, Eur/Gbp has retreated through 0.8550 towards 0.8500 again, though has not managed to get as close as it did on Wednesday.

- JPY/EUR – Both firmer vs the Greenback, albeit fractionally given the relatively constrained trade noted above, with the Jpy inching higher within a 111.50-35 band and potentially capped by decent option expiry interest from 111.50-60 (1.3 bn) and the 200DMA (111.49). Meanwhile, the single currency continues to meet resistance around 1.1250 and has not been helped by abysmal German industrial orders data or confirmation that the country’s group of Economic Institutes has become the latest to slash the 2019 GDP to under 1%.

- CHF/NZD/AUD/CAD – All underperforming, but again in context only marginally. Indeed, the Franc is meandering between 0.9987-72, Kiwi hovering from 0.6800 to 0.6773 and Aussie just keeping its head above 0.7100, and at this stage not looking likely to arouse expiry interest at 0.7140-50 in 1 bn. For choice, the Loonie is lagging against the backdrop of softer crude prices and back below 1.3350 ahead of Canada’s Ivey PMI.

- EM – Literally no respite for the Lira it seems, as economic, fiscal and political issues continue to weigh on the currency and Turkish assets in general. Indeed, Usd/Try has nudged up to 5.6600 again after Wednesday’s mixed inflation data and another hike in swap limits, as investors eye next week’s Economic Program conscious of the fact that the CBRT may not be able to loosen its grip on the monetary policy reins given that headline CPI remains so high.

In commodities, the energy complex had consolidated following yesterdays advances and was edging lower for the majority of the session, though WTI & Brent futures have recently reverted much of this downside and are now just edging into positive territory for the day. Brent and WTI are currently trading around sesson highs of USD 69.34 and USD 62.50 respectively. Earlier in the session, Brent prices edged lower after hitting resistance at its 200 DMA around USD 69.60/bbl, meanwhile WTI remains north of its 200 DMA (USD 61.40/bbl). Elsewhere, spot gold (+0.1) trades lacklustre as markets are tentative ahead of the ECB minutes, US-China trade talks and NFP. It is also worth noting that investors are pulling money out of gold ETFs with around USD 153mln removed out of the USD 10bln VanEck Vectors Gold Miners ETF over the last five days. Meanwhile, copper (-0.3%) succumbs to the cautious risk tone but remains above its 100 WMA of just under USD 2.90/lb. Finally, Dalian iron ore futures saw its best day in seven-weeks, extending its record-breaking rally, as supply-side woes (largely from cyclones in Western Australia) and a pick-up in demand (steel mills replenishing stocks) boosted the base metal to a new peak of USD 103.49/tonne.

US Event Calendar

- 7:30am: Challenger Job Cuts YoY, prior 117.2%

- 8:30am: Initial Jobless Claims, est. 215,000, prior 211,000; Continuing Claims, est. 1.75m, prior 1.76m

- 9:45am: Bloomberg Consumer Comfort, prior 60

DB’s Jim Reid concludes the overnight wrap

After a pause on Tuesday, Monday’s risk rally on stronger manufacturing PMIs extended further yesterday on the previous night’s trade news and then a mostly positive global round of non-manufacturing PMIs. It was so good that 10 year bund yields now give you a positive yield again (0.008% – up +5.7bps yesterday). Hurry while stocks last. It makes me want to work out how much the average person would have to invest in them to give them their required retirement income given the 1bps yield! The move was helped by signs of hope from the services PMIs in Europe (more on that below) and Kudlow’s comments that US and China negotiators are “making good headway”. Later in the session, Bloomberg reported that the US requested a six-year timetable for China to implement changes to its import purchases and market access reforms, possibly an indication that a deal is being formalised. The FT reported that there are still a couple of sizeable outstanding issues; 1) what happens to existing US levies on Chinese goods, which Beijing wants to see removed, and 2) the terms of a US enforcement mechanism that ensures that China abides by the deal. Overnight, the White House has said that President Trump will meet Chinese Vice Premier Liu He today in the Oval Office at 16:30 ET (21:30 UK Time). It really feels like progress is being made even if tough work remains.

The tech sector really led the charge yesterday with the NASDAQ closing up +0.60%, albeit off its highs of +1.14%, which means it’s now closed up four days in a row – good for a +2.95% spurt during that time. The FANGs weren’t to be left out with the NYSE FANG index rallying +0.93% – the fifth consecutive daily gain – to put it at the highest level since early October. Amazingly the NASDAQ is also back to being just 2.64% off its all-time highs from late August again. Meanwhile the S&P 500 climbed +0.21% and DOW +0.15%. The latter’s underperformance was entirely driven by Boeing’s -1.54% drop. The Wall Street Journal reported that last month’s 737 Max crash in Ethiopia came despite the fact that pilots followed Boeing’s instructions on how to compensate for a software defect. Ethiopian authorities will release their report on the crash today, potentially opening Boeing up to legal liability.

European equities had a better session, with the Stoxx 600 advancing +1.01% to its highest level since August 9th last year. Bourses rallied across the continent, led by the DAX (+1.70%), the IBEX (+1.33%), and by banks (+1.61%). The only major laggard was the FTSE 100 (+0.37%), which was pressured by the stronger pound on perceived positive Brexit news as well as by the sharp rise in gilt yields, which rose +9.4bps for their biggest selloff in 13 months. Treasury yields rose as well, climbing +4.5bps while the 2s10s curve steepened another 1.0bps to 18.0bps. High yield spreads were also 5bps tighter in both Europe and the US. Oil prices traded flat, though US inventory data showed a surprisingly large 7.2 million barrel increase in stockpiles last week, taking some air out of the narrative of robust demand so far this year.

On Brexit, Prime Minister May and Labour Leader Corbyn held discussions yesterday on a cross-party proposal that both sides described as “constructive” even if Mr Corbyn said that there had not been “as much change as (he) had expected” in Mrs May’s stance.

Their teams will continue negotiations today, and the most likely date for another vote is Monday or Tuesday next week. Last night, Parliament voted 313-312 to pass the Cooper-Letwin amendment, which would try to force a long Article 50 extension. The bill will now move to the House of Lords today and, assuming it is passed cleanly, will take no-deal Brexit off the table – from the U.K. side at least. That has enraged the hard-Brexit supporting wing of May’s party, but it could still push them to back her deal next week if she ends up bringing it to a vote. Prior to the May and Corbyn meeting, European markets were mostly busy watching any Parliament reaction to May’s pivot and any reaction from the EU. On the former two MPs resigned however significantly neither were Cabinet ministers. Is this the calm before the storm in terms of resignations? It’s fair to say that there are a vast number of unhappy Tory MPs over the talks with Mr Corbyn. On the latter there wasn’t too much to highlight. The EU seem to be mostly watching for now. Elsewhere, the Sun has reported overnight that PM May is likely to request 9 month delay to Brexit during the EU summit.

In Asia this morning markets are trading mixed with the Shanghai Comp (+0.56%) and Kospi (+0.19%) up while the Hang Seng (-0.52%) is down and the Nikkei is trading flat. Elsewhere, futures on S&P 500 are trading flattish (-0.06%).

Back to the PMIs where the big talking point, and in contrast to the manufacturing data, was the 0.6pt upward revision to the March services reading for the Euro Area to 53.3, helping to lift the composite to 51.6 (vs. 51.3 flash). With the services sector more domestically orientated than the manufacturing sector it helps to boost the case that the domestic European economy is generally doing ok. The positive revision was helped by a boost from most countries. Germany and France were revised up 0.5pts to 55.4 and 0.4pts to 49.1, respectively, while Italy (53.1 vs. 50.8 expected) and Spain (56.8 vs. 55.0 expected) both came in ahead of expectations.

Staying with the PMIs, yesterday DB’s Peter Sidorov highlighted the fascinating stat that while Germany’s manufacturing PMI is in the deepest downturn outside of the Great Recession, Germany’s services PMI is in the top 25% of readings since the start of the euro area recovery in late 2013. In standardised terms, that is the largest underperformance of manufacturing vs services we have seen since the start of the data in 1997.

Overall the data should be welcomed by the ECB however it doesn’t hide the fact that any recovery back to trend growth still requires the manufacturing sector to lift out of the doldrums. On the subject of the ECB yesterday we got a fresh story from MNI under the title “ECB tiering more likely if rates cut further”. A word of warning that MNI hasn’t proved to be the most reliable of sources in recent times. The headline seemed to be a bit punchier than the actual story too, with the main message being that the tiering debate is still in its infancy right now with no clear outcome.

There’s a chance that we learn a bit more about the ECB’s thinking today with the minutes from last month’s confused policy meeting. Confused in the sense that it felt like the ECB sent out various contradicting messages. A reminder that in the end that they opted to announce the bare bones of the new TLTRO replacement facility but downgraded growth and inflation without suggesting any cohesive future policy implications.

In contrast to the data in Europe yesterday it wasn’t quite so good a day for US data. The March ADP print came in at 129k versus 175k expected, and in fact was the lowest reading since September 2017. We should however caveat that the ADP reading overstated NFPs by 163k in February, which isn’t the first time we’ve seen such a big divergence. So there is a bit of a question about the ADP survey being a reliable spot indicator of payrolls. More important though was the miss in the March ISM non-manufacturing (56.1 vs. 58.0 expected) and -3.6pt drop from February. New orders was the big driver of the decline (59.0 from 65.2), however, the employment component did nudge up +0.7pts to 55.9. The gap between the US and the RoW is closing through a slight dip in the former and a welcome rise in the latter.

To the day ahead now where shortly after this hits your emails we’ll get February factory orders data out of Germany, followed by the March construction PMI. In the US this afternoon the early data release is March challenger job cuts before we get the latest weekly initial jobless claims reading. We’ve also got the aforementioned ECB minutes due out at lunchtime while the Fed’s Mester and Harker are speaking this evening. Keep an eye on potential trade headlines too with China Vice Premier Liu He now in Washington.

via ZeroHedge News https://ift.tt/2CVPnII Tyler Durden

As the saying goes, the definition of insanity is doing the same thing over and over again and expecting a different outcome. This is a perfect way to describe the current effort by Democrats and some conservatives to implement a federal paid leave program, writes Veronique de Rugy. If the United States implements this policy, they believe Americans will not suffer the same negative consequences suffered in every country that has such a policy on its books.

As the saying goes, the definition of insanity is doing the same thing over and over again and expecting a different outcome. This is a perfect way to describe the current effort by Democrats and some conservatives to implement a federal paid leave program, writes Veronique de Rugy. If the United States implements this policy, they believe Americans will not suffer the same negative consequences suffered in every country that has such a policy on its books.

Bethany, Oklahoma, police are investigating several teens for

Bethany, Oklahoma, police are investigating several teens for