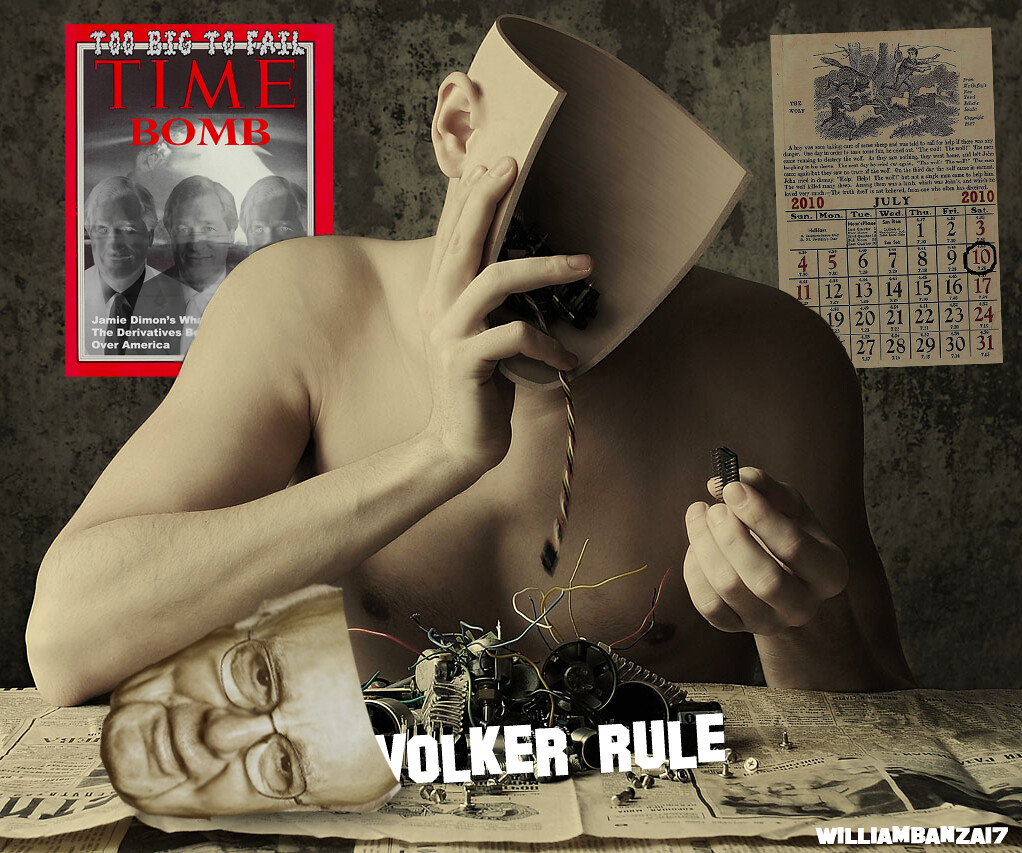

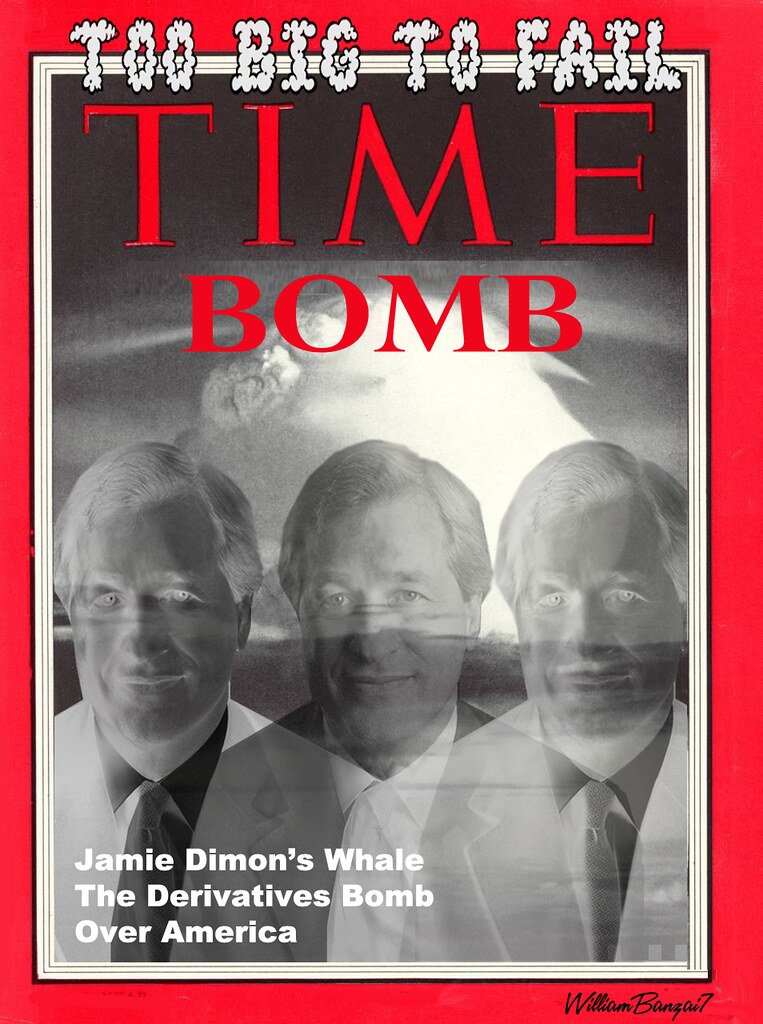

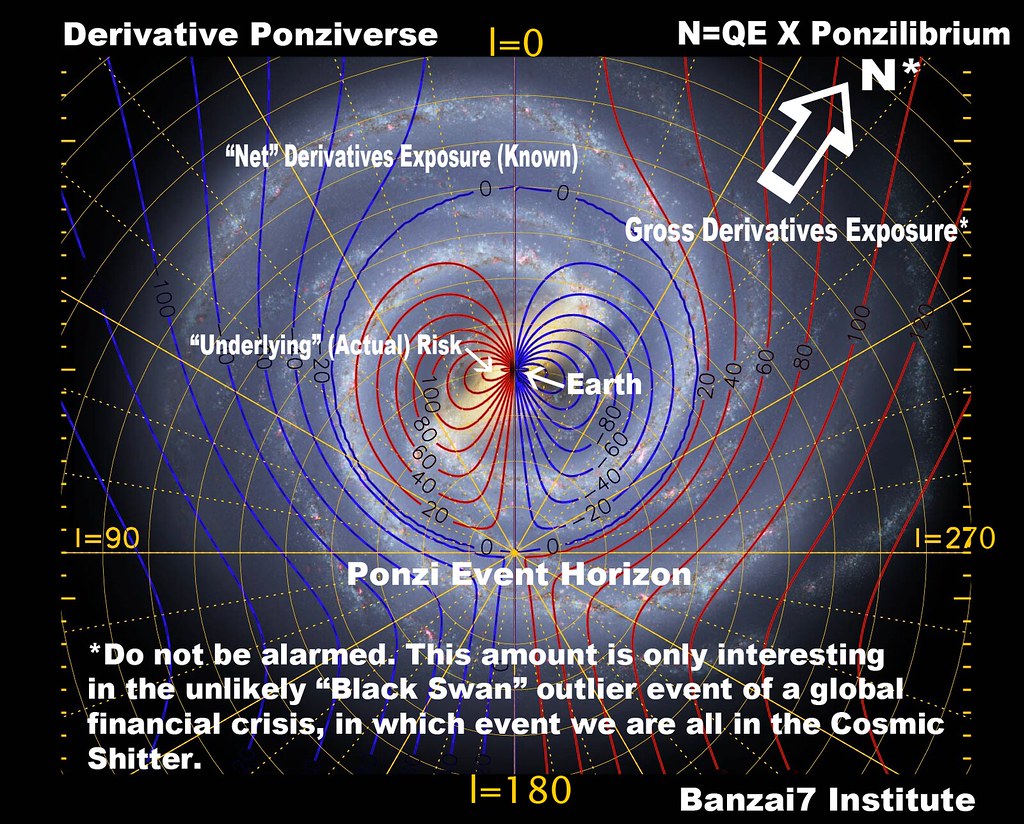

.

.

.

.

.

.

![]()

|

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/Dtlnb7HHmMk/story01.htm williambanzai7

another site

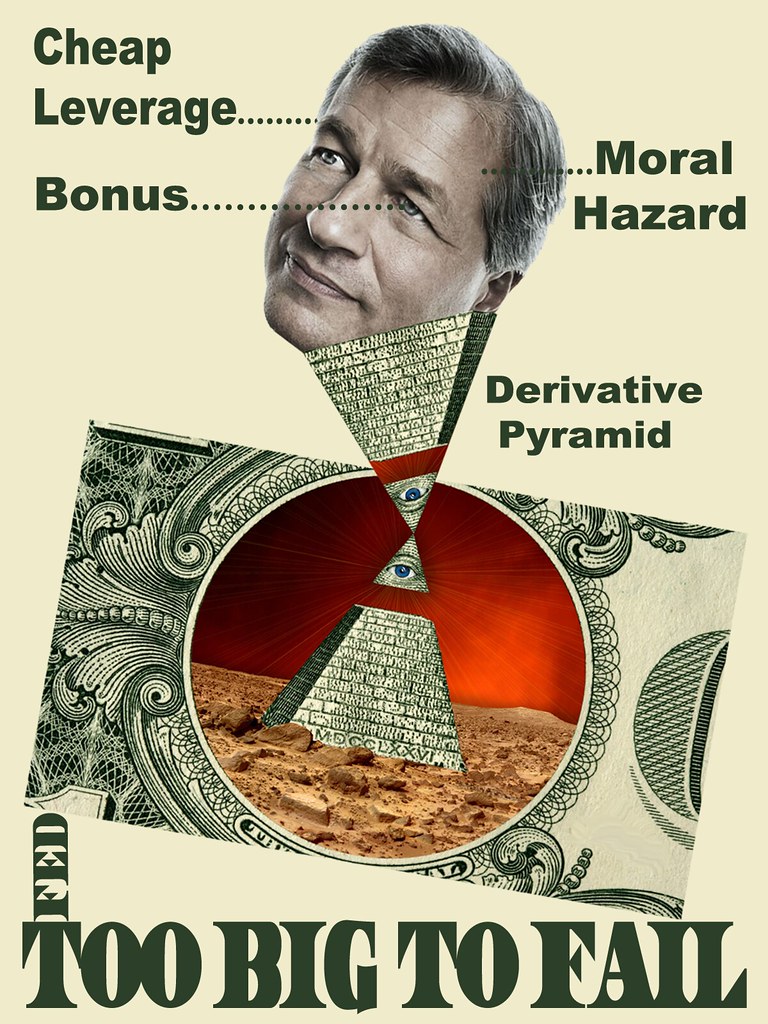

.

.

.

.

.

.

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/Dtlnb7HHmMk/story01.htm williambanzai7

In the wake of the news of Nelson Mandela’s

In the wake of the news of Nelson Mandela’s

death some people predictably hastened to remind us that despite

his status as a symbol of peace, reconciliation, and freedom

Mandela had associations with groups that were not

sympathetic to capitalism and were hardly afraid of committing

acts of violence. Comments criticizing Sen. Ted Cruz’s Facebook

post after Mandela’s death in particular were

widely reported.

Over at The New York Times’

DealBook, Andrew Ross Sorkin notes that while Mandela may have

believed in the nationalization of industries after his release in

1990, his attitude towards markets did change, ironically thanks in

part to talks with Chinese and Vietnamese communists at the 1992

meeting of the World Economic Forum:

But as the five-day conference of high-level speed-dating wore

on, Mr. Mandela soon decided he needed to reconsider his long-held

views: “Madiba then had some very interesting meetings with the

leaders of the Communist Parties of China and Vietnam,” Mr. Mboweni

wrote, using Mr. Mandela’s clan name. “They told him frankly as

follows: ‘We are currently striving to privatize state enterprises

and invite private enterprise into our economies. We are Communist

Party governments, and you are a leader of a national liberation

movement. Why are you talking about nationalization?’ ”“It was those decisive moments which made him think about the

need for our movement to seriously rethink the issue,” Mr. Mboweni

said.Mr. Mandela’s push toward free markets opened up his country to

become the fastest growing in Africa and eventually brought in

billions of dollars of investment from large companies outside the

country. Barclays, for example, acquired Absa, South Africa’s

largest consumer bank, in 2005. Iscor, the country’s largest steel

maker, was sold to Lakshmi Mittal’s LNM in 2004. Industrial and

Commercial Bank of China bought a big stake in Standard Bank, South

Africa’s largest financial services company, in 2008. And Massmart,

a South African supermarket chain, sold a majority stake to Walmart

in 2011.

After former House Speaker Newt Gingrich received hostile

reactions to a personal statement he made expressing his

condolences to South Africans and Mandela’s family following

Mandela’s death he wrote

a response in which he addressed Mandela’s connections to

communism and armed struggle. In the statement, Gingrich rightly

asks those who criticize Mandela’s actions before his imprisonment

on Robben Island to consider not only how they would have acted in

the same situation but also how some of the Founding Fathers

behaved in response to British tyranny. Gingrich’s response was

praised by

Jim Antle at The American Conservative, who wrote:

The Founders’ sins are worthy topics of discussion that should

not be whitewashed out of American history. But neglecting the

context of the times, the specific injustices they fought, the

institutions they built, and the principles they imperfectly

embodied is ideologically motivated malpractice.Similarly, it is right to point out that many fawning Mandela

obituaries ignore the injustices he tolerated himself, his kind

words for terrorists and dictators, the violence of the ANC toward

blacks as well as whites, even the sins of post-apartheid South

Africa and the virtues of the country before it was transformed.

But any reference to these things that neglects or minimizes the

injustices of apartheid is woefully incomplete—and unlikely to

result in a meaningful dialogue about the very facts such

contrarian commentary hopes to expose.

Too often prominent political figures are lazily characterized

both during their lives and after their deaths, whether it is

calling Obama a “socialist,” Thatcher a “fascist,” or Tea Partiers

“anarchists.” It’s a shame to see Mandela, a praiseworthy as well

as imperfect man, being given similar treatment.

from Hit & Run http://reason.com/blog/2013/12/10/chinese-and-vietnamese-communists-helped

via IFTTT

The % of NYSE stocks above their 200-day moving averages has a strong bearish divergence similar to previous plunge-preceding divergences. As BofAML notes, this points to diminishing momentum for market breadth and preceded pullbacks in the range of 15%-20% in 2010 and 2011; increasing the risk for a US equity market pullback in 2014.

It would take a break below 60% for the % of NYSE stocks above 200-day MAs to provide a more dire warning for US equities.

Source: BofAML

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/OvvIsXHB-ps/story01.htm Tyler Durden

The % of NYSE stocks above their 200-day moving averages has a strong bearish divergence similar to previous plunge-preceding divergences. As BofAML notes, this points to diminishing momentum for market breadth and preceded pullbacks in the range of 15%-20% in 2010 and 2011; increasing the risk for a US equity market pullback in 2014.

It would take a break below 60% for the % of NYSE stocks above 200-day MAs to provide a more dire warning for US equities.

Source: BofAML

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/OvvIsXHB-ps/story01.htm Tyler Durden

Submitted by Howard Kunstler of Kunstler.com,

“Federal Reserve officials are closer to winding down their controversial $85 billion-a-month bond-purchase program, possibly as early as December, in the wake of Friday’s encouraging jobs report.”

That from the much-deservedly maligned John Hilsenrath, widely regarded to be the Federal Reserve’s ventrioloquist dummy over at the Wall Street Journal, as in, from God’s mouth to the jittery multitudes. Of course the jobs number was just another highly seasoned and over-leavened cupcake from the Bureau of Labor Statistic’s magic hedonic oven, so you can be sure that the predicate of that statement is… how to put it delicately… the latest arrant lie with hypothetical icing on top.

Everybody knows that the Federal Reserve’s money-pumping operations have become a replacement for what used to be an economy. Therefore, no more money pumping = no more so-called economy. It’s that simple. But it doesn’t mean that the Federal Reserve won’t make a gesture and I wouldn’t be surprised if they try it during the season that Santa Claus hovers over the national consciousness — or what little of that remains when you subtract the methedrine, the Kanye downloads, the fear of an $11,000 bill for an emergency room visit requiring three stitches, and all the other epic distractions of our time.

The next meeting of the Fed’s Open Market Committee (FOMC), where such things as taper-or-not are considered, is Dec. 17. The Fed has to make some kind of gesture to retain any credibility, so I suspect they’ll go for a symbolic shaving of five or ten billion a month off the current official bond-buying operation number of $85 billion a month (or $1.2 trillion a year). If they don’t do it, no one will ever believe them again. I call it the “head-fake” taper, because it is essentially a false move.

The catch is that the Fed has more than one back door for vacuuming up all sorts of other miscellaneous financial trash paper securitized by promises already broken, moldy sheet-rock housing, college loans defaulted on, car payments that stopped arriving eighteen months ago, credit cards maxed to oblivion, sovereign foreign economies visibly whirling down the drain, and untold casino bet derivative hedges. Loose talk has it that the Fed is buying up way more dodgy debt than the official number of $85 billion a month. And why not? They bailed out way more than the $700 billion official TARP figure back in 2009 — everything from insolvent European banks to Floridian motels on the REO junk-pile — so nobody should take any particular taper number seriously. They’ll just backfill as necessary.

But even in a world of seemingly no consequence, things happen. One pretty sure thing is rising interest rates, especially when, at the same time as a head-fake taper, foreigners send a torrent of US Treasury paper back to the redemption window. This paper is what other nations, especially in Asia, have been trading to hose up hard assets, including gold and real estate, around the world, and the traders of last resort — the chumps who took US T bonds for boatloads of copper ore or cocoa pods — now have nowhere else to go. China alone announced very loudly last month that US Treasury debt paper was giving them a migraine and they were done buying anymore of it. Japan is in a financial psychotic delirium scarfing up its own debt paper to infinity. Who’s left out there? Burkina Faso and the Kyrgystan Cobblers’ Union Pension Fund?

The interest rate on the US 10-year bond is close to bumping up on the ominous 3.0 percent level again. Apart from the effect on car and house loans, readers have pointed out to dim-little-me that the real action will be around the interest rate swaps. Last time this happened, in late summer, the too-big-to-fail banks wobbled from their losses on these bets, providing a glimpse into the aperture of a black hole compressive deflation where cascading chains of unmet promises blow financial systems past the event horizon of universal default and paralysis where money stops moving anywhere and people must seriously reevaluate what money actually is.

I think we’ll see them try the head-fake taper. They must. It will be backstopped by and saturated in statistical lying, and everyone will have trouble parsing the probable effect because the chronic dishonesty loose in this land will have deformed and impaired all metrics of true value. At the heart of whatever remains of this economy is fire, and the officers of the Federal Reserve are playing with it. Pretty soon, we’ll get the un-taper, the final surrender to the crack-up boom that awaits before the western world has to go medieval.

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/kGdFMhV0-i8/story01.htm Tyler Durden

Tapering may not be tightening, as the Fed will keep repeating until someone actually believes it (the Fed may be right, however it’s not what the Fed thinks or does, but the next most levered counterparty who is the risk factor, and whose potential selling is what is keeping everyone on their toes), but the just completed 3 Year auction just priced at a yield of 0.631%, precisely where it priced in August, the month before the last “consensus” taper announcement at the September FOMC, and above the 0.581% where the 3 Year was in June when the Taper Tantrum peaked. The short-end may not be panicking yet, but the enthusiasm for bonds is certainly not where it used to be, especially when one considers 3 Years priced in the mid-0.3% range from September 2011 until May 2013.

That said, the auction showed stable demand, with the High Yield pricing through the 0.637% When Issued. Demands was even stabler when one looks at the Bid to Cover, which at 3.553 was the highest since the 3.587% in February, and continues to break the trend of declining BTCs seen over the past year, until the sharp jump in November.

Finally, the allocation was as follows: Primary Dealers: 49.6%, promptly to be flipped to the Fed, Indirects 38.4%, well above the 29.1% TTM average, and Directs taking down just 12.0%, the lowest since June, and far below the 18.9% average.

While overall the auction priced without any glitches or complications, should the Fed indeed proceed to Taper, the January 3 Year will hardly be a cool, calm and collected.

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/2uFrPQ_vFDA/story01.htm Tyler Durden

While much has been said about the benefits of Bernanke’s wealth effect to the asset-owning “10%”, just as much has been said about the ever deteriorating plight of the remaining debt-owning 90%, who are forced to resort to labor to provide for their families, and more specifically how their living condition has deteriorated over not only the past five years, since the start of the Fed’s great experiment, but over the past several decades as well. However, in the case of America’s “servant” class, Al Jazeera finds that their plight is now worse than it has been at any time over the past century, going back all the way to 1910!

According to Al Jazeera, “at least one class of American workers is having a much harder time today than a decade ago, than during the Great Depression and than a century ago: servants. The reason for this, surprisingly enough, is outsourcing. Let me explain. Prosperous American families have adopted the same approach to wages for servants as big successful companies, hiring freelance outside contractors for all sorts of functions from child care and handyman chores to gardening and cleaning work to reduce costs. Instead of the live-in servants, who were common in the prosperous households of America before World War II, better off families now outsource the family cook, maid and nanny. It is part of a global problem in developed countries that is getting more attention worldwide than in the U.S.”

The reality is that the modern servant is also known as the minimum-wage burger flipper, whose recent weeks have been spent in valiant, if very much futile, strikes in an attempt to increase the minimum wage their are paid. Futile, because recall that in its first “national hiring day” McDonalds hired 62,000 workers…. and turned down 938,000! Such is the sad reality of the unskilled modern day worker at the bottom the labor pyramid.

Unfortunately, we anticipate many more strikes in the future of America’s disenfranchised poorest, especially once they realize that their conditions are worse even than compared to live in servants from the turn of the century.

Al Jazeera crunches the numbers:

Consider the family cook. Many family cooks now work at family restaurants and fast food joints. This means that instead of having to meet a weekly payroll, families can hire a cook only as needed.

A household cook typically earned $10 a week in 1910, century-old books on the etiquette of hiring servants show. That is $235 per week in today’s money, while the federal minimum wage for 40 hours now comes to $290 a week.

At first blush that looks like a real raise of $55 a week, or nearly a 25-percent increase in pay. But in fact, the 2013 minimum wage cook is much worse off than the 1910 cook. Here’s why:

- The 1910 cook earned tax-free pay, while 2013 cook pays 7.65 percent of his income in Social Security taxes as well as income taxes on more than a third of his pay, assuming full-time work every week of the year. For a single person, that’s about $29 of that $55 raise deducted for taxes.

- Unless he can walk to work, today’s outsourced family cook must cover commuting costs. A monthly transit pass costs $75 in Los Angeles, $95 in Atlanta and $122 in New York City, so bus fare alone runs $17 to $25 a week, eating up a third to almost half of the seeming increase in pay, making the apparent raise pretty much vanish.

- The 1910 cook got room and board, while the 2013 cook must provide his own living space and food.

More than half of fast food workers are on some form of welfare, labor economists at the University of California, Berkeley and the University of Illinois reported in October after analyzing government economic statistics.

Data on domestic workers is scant because Congress excludes them from both regular data gathering by the Bureau of Labor Statistics and laws giving workers rights to rest periods and collective bargaining.

Nevertheless, what we do know is troubling. These days 60 percent of domestic workers spend half of their income just on housing and a fifth run out of food some time each month.

A German study found that in New York City domestic workers pay ranges broadly, from an illegal $1.43 to $40 an hour, with a quarter of workers earning less than the legal minimum wage. The U.S. median pay for domestic servants was estimated at $10 an hour.

The conclusion?

We are falling backwards in America, back to the Gilded Age conditions a century and more ago when a few fortunate souls grew fabulously rich while a quarter of families had to take in paying boarders to make ends meet. Only back then, elites gave their servants a better deal.

Thorstein Veblen, in his classic 1899 book “The Theory of the Leisure Class,” observed that “the need of vicarious leisure, or conspicuous consumption of service, is a dominant incentive to the keeping of servants.” Nowadays, servants are just as important to elites, except that they are conspicuous in their competition to avoid paying servants decent wages.

But… but… how is that possible if the stock market is at all time highs and the wealth is US households just rose by $1.9 trillion in one short quarter. Oh wait, what they meant is “some” households.

And, of course if all else fails, America’s “free” servants, stuck in miserable lives working minimum wage jobs for corporations where the only focus in on shareholder returns and cutting overhead, can volunteer to return to a state of “semi-slavery” (while keeping the iPhones and apps of course, both paid on credit) and become live-in servants for America’s financial oligarchy and the like. We hear the numerous apartments of Wall Street’s CEOs have quite spacious servants’ quarters.

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/VRZU_zGgSf0/story01.htm Tyler Durden

While much has been said about the benefits of Bernanke’s wealth effect to the asset-owning “10%”, just as much has been said about the ever deteriorating plight of the remaining debt-owning 90%, who are forced to resort to labor to provide for their families, and more specifically how their living condition has deteriorated over not only the past five years, since the start of the Fed’s great experiment, but over the past several decades as well. However, in the case of America’s “servant” class, Al Jazeera finds that their plight is now worse than it has been at any time over the past century, going back all the way to 1910!

According to Al Jazeera, “at least one class of American workers is having a much harder time today than a decade ago, than during the Great Depression and than a century ago: servants. The reason for this, surprisingly enough, is outsourcing. Let me explain. Prosperous American families have adopted the same approach to wages for servants as big successful companies, hiring freelance outside contractors for all sorts of functions from child care and handyman chores to gardening and cleaning work to reduce costs. Instead of the live-in servants, who were common in the prosperous households of America before World War II, better off families now outsource the family cook, maid and nanny. It is part of a global problem in developed countries that is getting more attention worldwide than in the U.S.”

The reality is that the modern servant is also known as the minimum-wage burger flipper, whose recent weeks have been spent in valiant, if very much futile, strikes in an attempt to increase the minimum wage their are paid. Futile, because recall that in its first “national hiring day” McDonalds hired 62,000 workers…. and turned down 938,000! Such is the sad reality of the unskilled modern day worker at the bottom the labor pyramid.

Unfortunately, we anticipate many more strikes in the future of America’s disenfranchised poorest, especially once they realize that their conditions are worse even than compared to live in servants from the turn of the century.

Al Jazeera crunches the numbers:

Consider the family cook. Many family cooks now work at family restaurants and fast food joints. This means that instead of having to meet a weekly payroll, families can hire a cook only as needed.

A household cook typically earned $10 a week in 1910, century-old books on the etiquette of hiring servants show. That is $235 per week in today’s money, while the federal minimum wage for 40 hours now comes to $290 a week.

At first blush that looks like a real raise of $55 a week, or nearly a 25-percent increase in pay. But in fact, the 2013 minimum wage cook is much worse off than the 1910 cook. Here’s why:

- The 1910 cook earned tax-free pay, while 2013 cook pays 7.65 percent of his income in Social Security taxes as well as income taxes on more than a third of his pay, assuming full-time work every week of the year. For a single person, that’s about $29 of that $55 raise deducted for taxes.

- Unless he can walk to work, today’s outsourced family cook must cover commuting costs. A monthly transit pass costs $75 in Los Angeles, $95 in Atlanta and $122 in New York City, so bus fare alone runs $17 to $25 a week, eating up a third to almost half of the seeming increase in pay, making the apparent raise pretty much vanish.

- The 1910 cook got room and board, while the 2013 cook must provide his own living space and food.

More than half of fast food workers are on some form of welfare, labor economists at the University of California, Berkeley and the University of Illinois reported in October after analyzing government economic statistics.

Data on domestic workers is scant because Congress excludes them from both regular data gathering by the Bureau of Labor Statistics and laws giving workers rights to rest periods and collective bargaining.

Nevertheless, what we do know is troubling. These days 60 percent of domestic workers spend half of their income just on housing and a fifth run out of food some time each month.

A German study found that in New York City domestic workers pay ranges broadly, from an illegal $1.43 to $40 an hour, with a quarter of workers earning less than the legal minimum wage. The U.S. median pay for domestic servants was estimated at $10 an hour.

The conclusion?

We are falling backwards in America, back to the Gilded Age conditions a century and more ago when a few fortunate souls grew fabulously rich while a quarter of families had to take in paying boarders to make ends meet. Only back then, elites gave their servants a better deal.

Thorstein Veblen, in his classic 1899 book “The Theory of the Leisure Class,” observed that “the need of vicarious leisure, or conspicuous consumption of service, is a dominant incentive to the keeping of servants.” Nowadays, servants are just as important to elites, except that they are conspicuous in their competition to avoid paying servants decent wages.

But… but… how is that possible if the stock market is at all time highs and the wealth is US households just rose by $1.9 trillion in one short quarter. Oh wait, what they meant is “some” households.

And, of course if all else fails, America’s “free” servants, stuck in miserable lives working minimum wage jobs for corporations where the only focus in on shareholder returns and cutting overhead, can volunteer to return to a state of “semi-slavery” (while keeping the iPhones and apps of course, both paid on credit) and become live-in servants for America’s financial oligarchy and the like. We hear the numerous apartments of Wall Street’s CEOs have quite spacious servants’ quarters.

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/VRZU_zGgSf0/story01.htm Tyler Durden

Same Shit, Different Day; yet again the S&P 500 is trading tick-for-tick with the all-important EURJPY cross rate. As the following chart shows, its all about fun-durr-mentals…

Fun-Durr-Mentals….

(h/t @Not_Jim_Cramer)

Same Shit Different Day…

and longer-term…

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/FM0LN-8avao/story01.htm Tyler Durden

If you can’t beat ’em, join ’em, copy ’em, and then beat ’em. While everyone’s attention has been glued to Bitcoin (and its various smaller and less viable for now alternative digital currencies), JPMorgan has submitted a patent which appears to set the scene for a competing centralized network to Bitcoin. As LetsTalkBitcoin noted first, the “Method and system for processing internet payments using the electronic funds transfer network,” states that Chase’s technology is a “new paradigm.” Moreover that it permits the creation of “virtual cash” (also referred to as “web cash”) with a “real-time digital exchange of value.”

Imagine paying for some product in a transaction directly with the seller that doesn’t include a costly third-party fee or the revelation of a personal account number — the current components that comprise credit card and debit card purchases. Imagine this system with a “real-time digital exchange of value.” And imagine that you can archive all the transactions in a personal digital wallet, with its own “Internet Pay Anyone (IPA)” account and inherent safeguards built-in, something that you could call “Virtual Private Lockbox (VPL),” according to JPMorgan’s patent.

If this “web cash” system — as JPMorgan Chase calls it — seems familiar, it should. It smacks of the peer-to-peer transactions of bitcoins and other cryptocurrencies that increasingly are making the world’s biggest banks uneasy about the future of e-commerce.

The patent, first revealed by LetsTalkBitcoin.com, is a fascinating look into JPMorgan’s veiled outlook on the evolving but growing bitcoin universe, and other more widely-accepted payment systems.

JPMorgan’s proposed system offers another eerily familiar component, which seemingly mimics “blockchain,” a publicly available, permanent ledger of bitcoin transactions.

…

Without naming the virtual currency or any competing payments system by name, the bank takes a swipe at the crytocurrency model.

“None of the emerging efforts to date have gotten more than a toehold in the market place and momentum continues to build in favor of credit cards,” according to Chase’s patent application published by The United States Patent and Trademark Office (USPTO). It was filed August 5th, 2013.

…

JPMorgan Chase sees “a new marketplace” emerging for “low dollar, high volume, real-time payments with payment surety for both consumers and producers.”

As LetsTalkBitcoin.com points out, “Bitcoin has also been ballyhooed for it use with micro-payments and payments under ten dollars due to its zero to negligible fee structure.”

JPMorgan Chase: “The present invention further enables small dollar financial transactions, allows for the creation of ‘web cash’ as well as provides facilities for customer service and record-keeping.”

While naming protocols for these vitual currencies is uncertain, we can’t help but think “Dimons” would be appropriate as the web cash becomes increasingly more trusted.

LetsTalkBitcoin discusses how JPMorgan’s proposed system works:

Under The Hood: Internet Pay Anyone

“…The structural components to the system of the present invention include:

a Payment Portal Processor; a digital Wallet;

an Internet Pay Anyone (IPA) Account;

a Virtual Private Lockbox (VPL);

an Account Reporter;

the existing EFT networks;

and a cash card.

“…The Payment Portal Processor (PPP) is a software application that augments any Internet browser with e-commerce capability. The PPP software sits in front of and provides a secure portal for accessing (finking to) the user’s. Demand Deposit Accounts (DDA) and IPA accounts. The PPP enables the user to push electronic credits from its DDA and IPA accounts to any other accounts through the EFT network…”

“…The {technology} …includes freely publishing the payment address and making it available to users of an internet portal or search engine…”

“…Currently, all Internet transactions use “pull” technology in which a merchant must receive the consumer’s account number (and in some cases PIN number) in order to complete a payment. The payment methods of the present invention conversely use “push” technology in which users (consumers or businesses) push an EFT credit from their IPA or DDA accounts to a merchant’s account, without having to provide their own sensitive account information…”

A New Paradigm

“…The present invention represents a new paradigm for effectuating electronic payments that leverages existing platforms, conventional payment infrastructures and currently available web-based technology to enable e-commerce in both the virtual and physical marketplace. The concept provides a safe, sound, and secure method that allows users (consumers) to shop on the Internet, pay bills, and pay anyone virtually anywhere, all without the consumer having to share account number information with the payee. Merchants receive immediate payment confirmation through the Electronic Funds Transfer (EFT) network so they can ship their product with confidence that the payment has already been received. The present invention further enables small dollar financial transactions, allows for the creation of “web cash” as well as provides facilities for customer service and record-keeping…”

and the implications:

I view this technology and patent application as an overwhelming good thing. Bitcoin is driving Innovation. It has been said that credit cards and the legacy banking system in use today was never meant for use over the internet. Chase’s updated Internet Pay Anyone technology appears to come head to head with Bitcoin.

…

While it remains to be seen if this technology is a “Bitcoin Killer,” other players such as eBay/PayPal (which have been riding under Bitcoin’s coattails through marketing gimmicks) ought to pay close attention to this emerging technology. If Bitcoin does get a “toehold” in the marketplace, we just might see this technology activated. The Chase is on.

Finally, the patent application itself (source USPTO):

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/sdGi5WoIMkg/story01.htm Tyler Durden