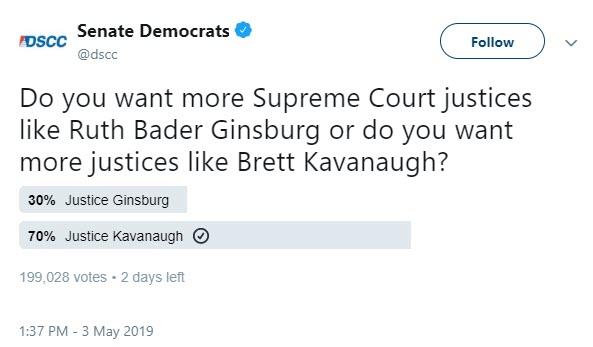

Assuming their own echo chamber would provide an ‘obvious’ conclusion, providing self-aggrandizing virtue signaling ammunition for the next news cycle attack on the vast right-wing conspiracy, the Democratic Senatorial Campaign Committee tweeted out a simple poll to its 107,000 followers:

“Do you want more Supreme Court justices like Ruth Bader Ginsburg or do you want more justices like Brett Kavanaugh?”

Do you want more Supreme Court justices like Ruth Bader Ginsburg or do you want more justices like Brett Kavanaugh?

Is the never ending rally ready to blast off or is it running out of steam setting up to finally correct? Let’s first separate facts from fiction.

Forget data and earnings, only 3 things truly mattered this past week: The Fed, the incessant efforts to verbally hype markets into a frenzy every single day (China, China, China), and magic risk free Friday once again saving the week into a marginally positive close with a magic gap, ramp and camp.

The result: Talk of a never ending rally and emerging narratives to support the very idea:

Inflation is dead. Debt doesn’t matter. The bull market lasts forever. Central banks have eliminated recessions. The U.S. stock market can’t stop, won’t stop its endless rally.

This is not me being facetious, these are actual headlines and phrases permeating the current investing landscape. Four months after a 20% correction which is now long forgotten. New all-time human history highs on $SPX and $NDX. Unemployment rate at 3.6%, the lowest in 50 years.

Party like its 1999, an almost circus like atmosphere. Let me humbly suggest: A true bull market would not require constant hyping and daily verbal neck rubs to push prices higher which bring us back to the question of sustainability of new highs.

I’ve called this the most jawboned rally in history, but it is rapidly devolving into the most hyped rally in history. And yet gains were modest. On the week $DJIA was actually down 30 points and $SPX gained 5 handles with a now standard closing squeeze in the last seconds of trading.

Things are so awesome let’s cut rates. No really, rate cut calls not only by the administration (think Kudlow, Trump and Pence,) but by the end of the week various Fed officials were sending the same message:

Yes, some people just like to throw gasoline on a fire to see what happens.

Is the Fed still pretending to be independent? Succumbing to political pressure in December and caving on the balance sheet and rate hikes they suddenly seemed to fall in line with almost daily calls for rate cuts by the administration. While the Fed statement expressed neutrality Friday’s speeches sent a different signal.

Friday’s parade of dovish Fed speakers of course aided in damage control from Jay Powell’s slip-up during the week which produced a sizable dip courtesy one word: “Transitory” by Jay Powell. Another communication error and in process markets broke the 2019 up trends.

Downside was not scheduled to happen and hence pity was taken on good old Jerome Powell:

You have to feel sorry for #Fed Chair #Powell:

In his press conference, he again–inadvertently–found a way to turn a rather uneventful market reaction into notable price movements.

In December it was his emphasis on “auto pilot:” this afternoon, it was his use of “transitory.” pic.twitter.com/VqPwcmjrxo

My response to this: Reason to feel sorry? Why? Because markets reveal themselves to be entirely dependent on the Fed to be dovish 100% of the time?

Any slight hawkish hint and we sell off? What’s that say about the entire construct? A market beholden to central committee planning. On January 4 Powell’s “Flexible on balance sheet” speech caused a “notable price movement” of +3.4% on $SPX. Nobody felt sorry for him then. Are we to feel sorry for Fed chairs when their communications produce downside i.e. in December and this week?

Or a better point yet via Guy Adami:

I understand what you are saying @elerianm , but I find my sympathy aimed towards the 100 of millions US citizens that Fed policy has disenfranchised over the last decade. The wealth gap has never been greater, and the Fed is almost entirely to blame… in my opinion https://t.co/wByGEo1PD8

Look, these are really important issues that keep getting pushed under the rug. Once again the Fed has revealed itself to be the biggest price driver of markets if only for a mistake in communication. Markets remain entirely dependent on a dovish Fed and hence Friday’s parade of 8 Fed speakers offered comfort.

The Fed of course is aware that things are not as rosy as they appear and their downside risk concerns are well founded and persistent low inflation readings giving the excuse to not raise rates while unemployment is at 50 year lows and the tech bubble and wealth inequality keep expanding.

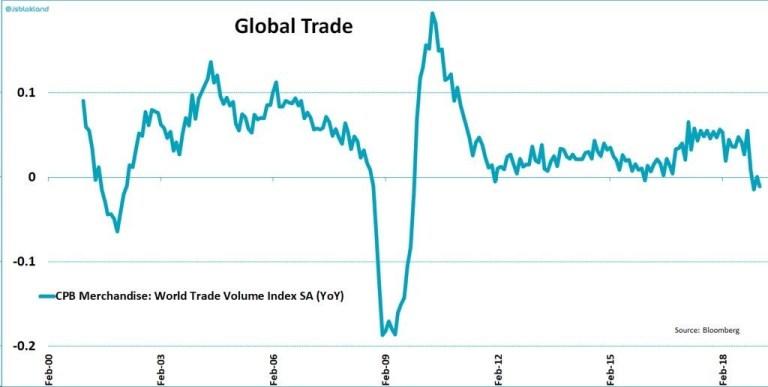

Global trade continues to languish:

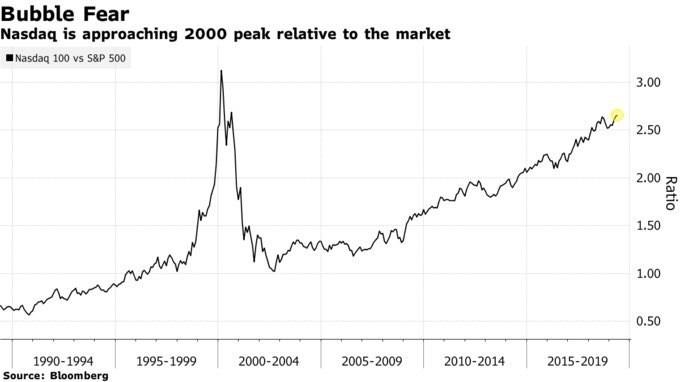

..while market advances are very much dependent on 6 stocks:

The same 6 stocks that have helped drive tech valuations to a disconnect from the larger market at levels not seen since the dot.com bubble:

But earnings are so much better this time. True, but many of these companies are running into slowing growth issues of their own. $GOOGL was an example this week and got punished. Slowing growth has so far been ignored with $AAPL and $AMZN. $NFLX is a debt bomb ticking and $FB continues to face regulatory and political backlash. The market caps of these companies ($3.7 trillion) is so outsized any switch in sentiment as we saw in Q4 can produce sizable downside.

So sentiment must be maintained. With this backdrop of a never ending rally is the blast-off inevitable? Is the Fed, impotent to have a backbone, content to let the bubble lead to its inevitable conclusion?

And, speaking of sentiment, if only the Fed would gear its communication to not screw up then nothing bad would happen. This at least seems to have been the message implied by Mohamed A. El-Erian:

“The fact that it ended up moving markets suggests that the Fed needs to develop a better understanding of market technicals — or what some call a ‘feel’ for the markets. Without that, an important part of its policy arsenal — that is, policy guidance which ensures that markets do some, if not all of the heavy lifting — will become less effective,” he said.

Well, there you have it. So much for being data dependent or economy focused. But it is an important implicit admission: The Fed’s role is to guide markets. Higher. Communications that lead to downside are mistakes.

But Jay Powell’s communication error notwithstanding, by Friday ‘the program’ was back in full swing, magic risk free Friday for the win:

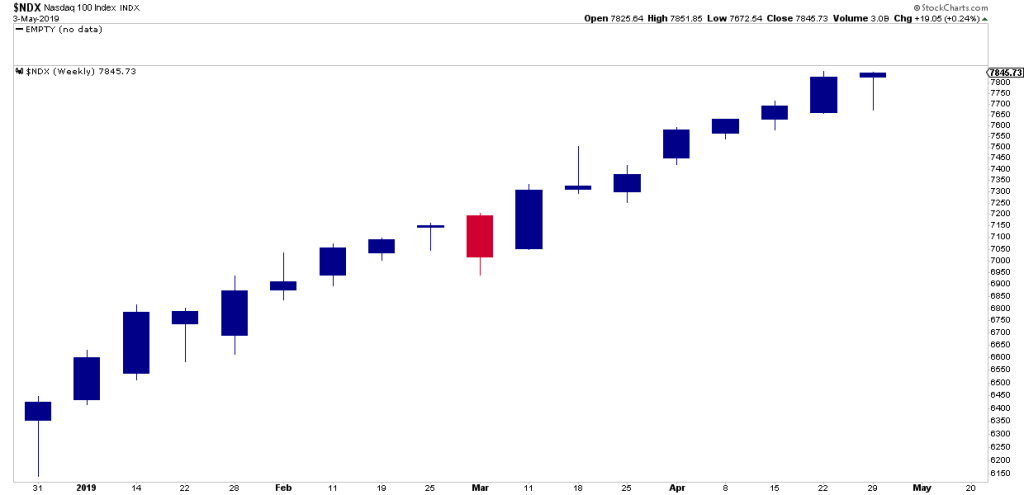

While the Fed may not be yet focusing on market technicals we are. Last week saw a break of some trends and the never ending rally produced an interesting candlestick on the $NDX:

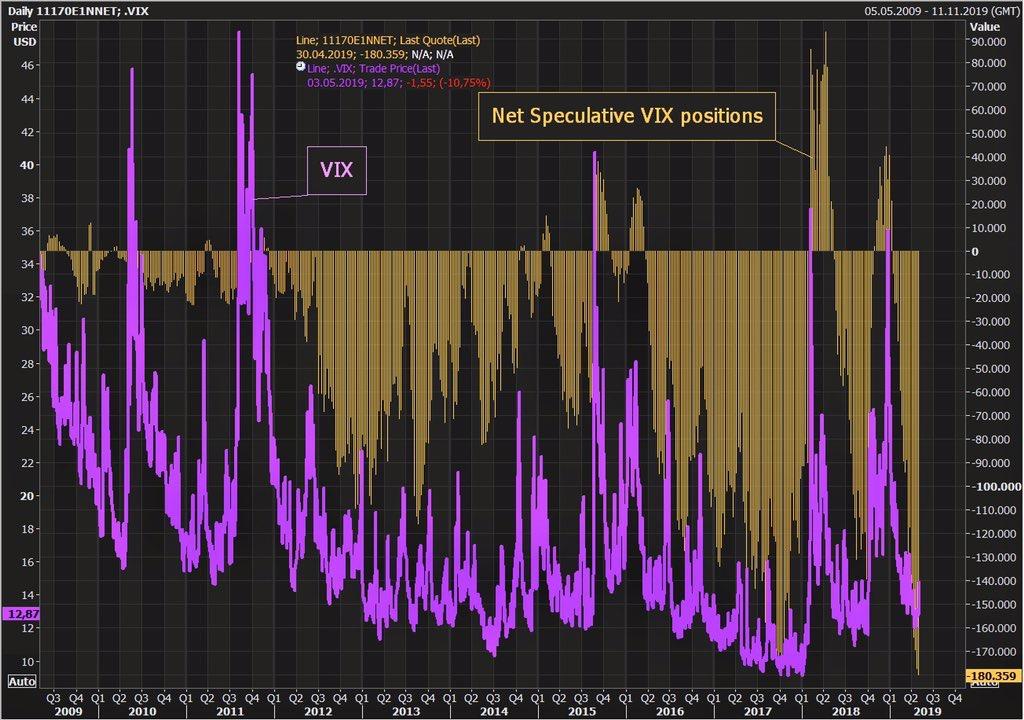

That looks auspiciously like a bearish hanging man potentially signaling the end of a trend, an interesting spot to now see record short positioning on the $VIX:

Which brings us back to the question from the outset: Is the never ending rally ready to blast off or is it running out steam setting up to finally correct?

Let’s run through the charts and technicals:

* * *

To get notified of future videos feel free to subscribe to our YouTube Channel.

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

via ZeroHedge News http://bit.ly/2H3jdOc Tyler Durden

So much for months and months of constant leaks, headlines, tweets, and press reports that US-China trade talks are going great amid an ocean of “optimism” (meant solely to sucker in amateurs into the most obvious bull headfake since 1987).

Just after noon on Sunday, President Trump tweeted that 10% tariffs paid by China on $200 billion in goods will rise to 25% on Friday, and that – contrary to what he himself and his chief economist, Larry Kudlow has said for months, talks on a trade deal have been going too slowly.

And, just to underscore his point, Trump also threatened to impose 25% tariffs on an additional $325 billion of Chinese goods “shortly.”

….of additional goods sent to us by China remain untaxed, but will be shortly, at a rate of 25%. The Tariffs paid to the USA have had little impact on product cost, mostly borne by China. The Trade Deal with China continues, but too slowly, as they attempt to renegotiate. No!

With the tariff rate on numerous goods originally set at 10% and set to more than double in 2019, Trump postponed that decision after China and the US agreed to sit down for trade talks; following Trump’s tweet it is now confirmed that trade talks have hit an impasse and that escalation will be needed to break the stalemate.

It was as recently as Friday that Vice President Mike Pence told CNBC that Trump remained hopeful that he could strike a deal with China (at the same time as he was urging for a rate cut from the Fed).

Curiously, on Wednesday, the White House – clearly hoping to sucker in even more naive bulls to buy stocks at all time highs – said the latest round of talks had moved Beijing and Washington closer to an agreement. Press secretary Sarah Sanders said, “Discussions remain focused toward making substantial progress on important structural issues and re-balancing the US-China trade relationship.”

In recent weeks there were multiple reports that China and U.S. were close to a trade deal, and an agreement could come as soon as Friday. Major sticking points the U.S. and China have been intellectual property theft and forced technology transfers. There has also been disagreement as to whether tariffs be removed or remain in place as an enforcement mechanism.

While it was not clear why Trump has decided to escalate his tariff policy, the most obvious explanation is that for a White House, which has been obsessed with pushing the S&P to record levels, this was the last lever it had at its disposal. And now that the S&P is back at all time highs, the lies can end, if only for the time being.

via ZeroHedge News http://bit.ly/2LpLnHr Tyler Durden

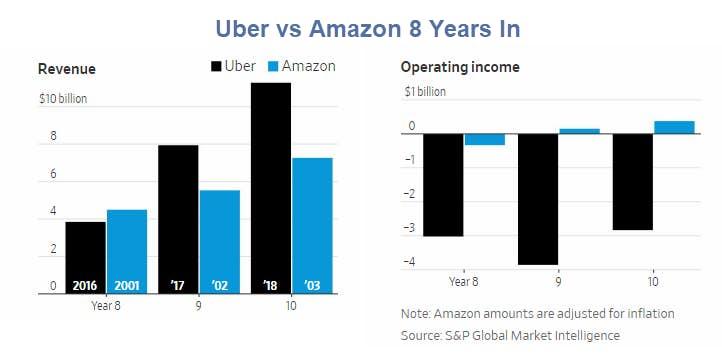

Analysts are questioning Uber’s viability. Many are concerned it will never make a profit. There’s too much competition.

Grandiose Plans

Uber wants to become the Amazon of everything transportation related. But a key question remains: Can Uber Ever Make a Profit?

In Uber’s vision of the future, most people won’t own cars. Riders will hop on electric bikes and scooters for short distances, and summon cars with drivers for longer rides. Takeout dinner will become a vestige, replaced by hand-delivered meals. Garages will empty and parking lots will be ripped up and transformed into grassy parks.

Eventually, robots will rule. Self-driving cars will shuttle people around the roads—and in the air—while drones will make the deliveries. Robotrucks will roam the highways. And Uber will be at the center of it all.

As Uber gets set to go public next Friday in one of the largest tech IPOs ever, Chief Executive Dara Khosrowshahi is trying to sell Wall Street on his vision that Uber will become the dominant force in all forms of transportation.

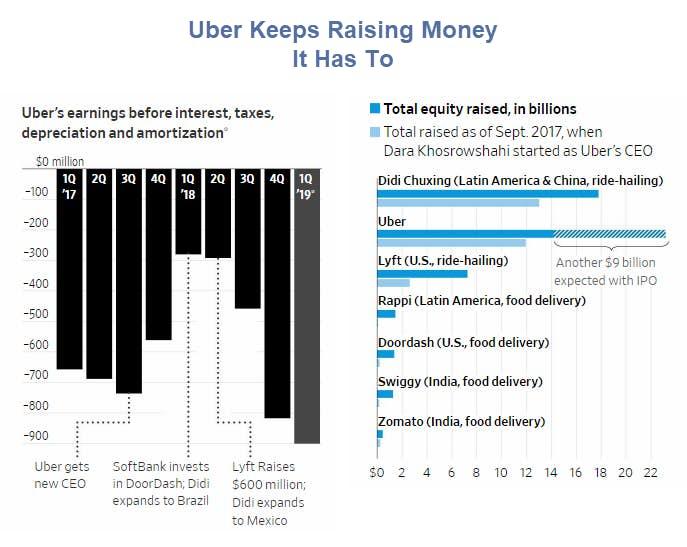

That mission is threatened by an onslaught of competition from all sides that has intensified in recent months and caused Uber’s loss to balloon to more than $3.7 billion in the 12 months through March—by far the largest loss ever for a U.S. startup in the year before an IPO, according to S&P Global Market Intelligence.

Uber vs Amazon

Amazon started making profits eight years in. Uber is bleeding money badly.

Uber Has to Continually Raise Money

There are no barriers to entry other than raising money. The competition is intense and competitors have learned from Uber’s mistakes.

Note the four food delivery competitors in the right panel in the lead chart. There are competitors in the scooter business as well.

Uber has a deal with McDonald’s. Uber used to get a 20% commission on deliveries. McDonald’s renegotiated the deal. Uber now gets a 15% commission.

Is that enough to make a profit? Year-to-date number provide a resounding no.

Uber Does Many Related Things, All Poorly

If Uber made money in one place it could afford to have cash drains elsewhere.

Compare Google to Uber. Google makes massive amounts of money off search engine advertising. It uses that free cash flow to fund many other endeavors, notable driverless car technology.

In contrast, Uber loses money at everything it does. It is also far behind Google (Waymo) in driverless technology.

Uber’s Survival

As long as Uber has the confidence of investors, it can survive by raising money. But if that confidence wanes before Uber makes enough to pay interest on accumulated debt, Uber is toast.

Right now, Uber is a zombie corporation, totally dependent on investors’ willingness to keep funding Uber’s cash needs.

via ZeroHedge News http://bit.ly/2H6PVON Tyler Durden

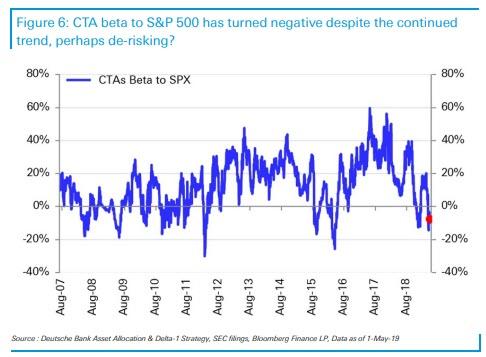

Not only is this the most hated, not to mention fake, bull market in history (thanks to some $15 trillion in central bank liquidity), it is also the most frustrating one: as the following chart from Deutsche Bank shows, even with the S&P back at all time highs, equity long short funds have absolutely no faith in the underlying drivers and their net beta exposure to US equities is the approaching a record low.

It’s not just carbon-based active investors that have no faith in continued levitation: trend-following CTAs and other systematic funds which buy or sell based on trigger prices, have also started to derisk in recent days…

… while Risk Parity funds are a long away from from peak equity exposure.

To a large degree this ongoing divergence in which stocks have continued to rise even as investors pull back, is the result of what Goldman’s David Kostin called a “disharmony of mixed economic data and Fed messaging” with the Goldman equity strategist noting that “equities struggled to digest the conflicting messages from strong payroll growth and a dovish FOMC statement with weak ISM prints and Chair Powell’s relatively hawkish press conference.”

To be sure, last week’s conflicting data has come on the heels of what many dubbed a renaissance in green shoots (largely the result of a massive credit injection and a fresh stimulus out of China), and follows what has largely been interpreted as favorable economic data, which together with continued record buybacks, has helped push the S&P 17% higher YTD

And yet, as Kostin writes, “beneath an equity market at record highs, thematic rotations indicate a still-cautious investor mindset.”

Which has also led Goldman’s clients to become increasingly confused, or as the strategist puts it – frustrated. Specifically, as Kostin explains, “the cyclical-led market rally has not coincided with a rotation to value stocks, leading some frustrated clients to ask why “catch up” trades are not working with the S&P 500 back at record highs.”

Call it the latest unexplained consequence of central planning: consider this example from Goldman:

in the past, environments of accelerating economic growth have typically supported the outperformance of both value stocks and cyclicals. In 2H 2016, for example, the Cyclical/Defensive pair rose by 18 percentage points and our sector-neutral, long/short Value factor rose by 17 pp. This year, in contrast, value stocks have lagged, as they have for most of the past two years (Ex. 1 and 2).

As Kostin notes, “the underperformance of value stocks is just one reflection of the ongoing market preference for growth and quality. In addition to cyclicals, a variety of “high quality” themes led the market as it rallied in 1Q 2019, including stocks with

strong balance sheets and firms with high pricing power. Likewise, the YTD outperformance of our basket of stocks with high revenue growth reflects an investor desire for idiosyncratic growth that is unusual in an environment of economic acceleration, which would normally erode the scarcity premium carried by such firms. The relative sluggishness of the typically high-beta Russell 2000 small-cap index is another manifestation. While the quality themes have generally traded sideways during the past month, growth stocks have continued to outperform. “

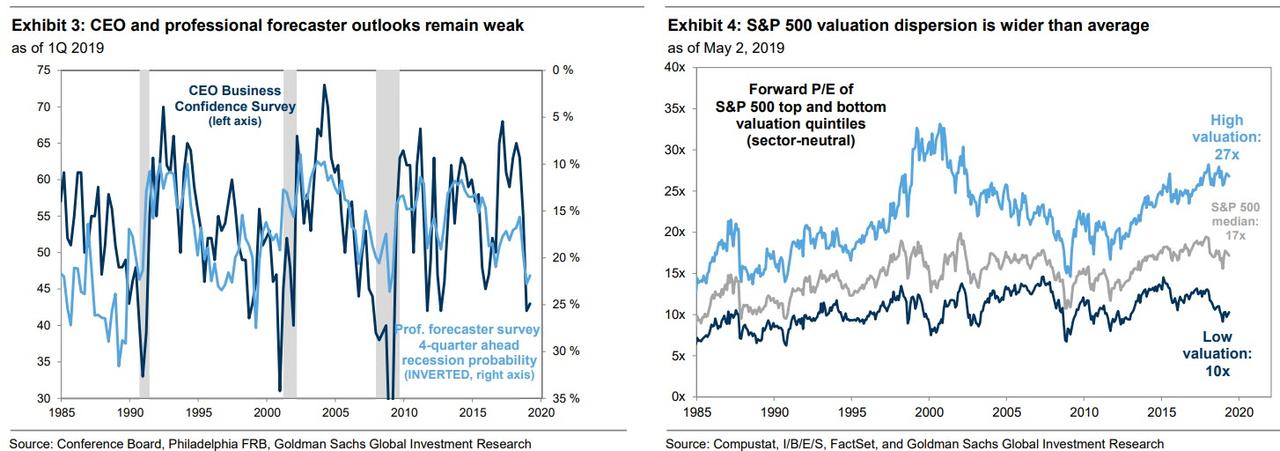

There are several reasons why Goldman believes there has been no rotation into value stocks: for one, although improved economic data and Fed dovishness helped allay investor concerns of a recession in the near term, most of Goldman’s clients “remain in a relatively cautious “late cycle” mindset. Economic data have improved, but the unemployment rate is 3.6% and the current economic cycle will match the longest on record next month.” Furthermore, the early 2019 slowdown in US corporate earnings growth “has likely also contributed to the underperformance of value, as has the exceptional combination of growth, profitability, and momentum displayed by the market-leading growth stocks.”

And speaking of late cycle, one can argue that the biggest concern most investor share is that the business cycle is long, long overdue for a recession. To be sure, the fed funds market shows a 50% likelihood of Fed rate cut by year-end. The CEO Business Confidence survey improved modestly in 1Q 2019 relative to 4Q 2018, but otherwise registers the lowest reading since 2012. And the Philly Fed’s Anxious Index shows that professional forecasters assign a 22% probability of recession within the next four quarters, the highest reading this cycle outside of the 23% print in 4Q 2018 (see Exhibit 3).

Confirming the ongoing investor boycott, Kostin points out several things we have repeatedly discussed: namely, that although investor equity positions have increased this year, they remain far from the highs of early 2018; US equity mutual funds and ETFs have experienced $38 billion of outflows YTD ; and VIX ETPs show record long volatility positions.

As a result of all this, Kostin writes that the bank’s clients and investors in general now have to decide which is most likely among three potential outcomes:

economic growth fades, reversing the cyclical rally and likely supporting the continued outperformance of quality stocks;

the outlook improves enough to ease late cycle concerns and spark a rotation to value and lower quality laggards;

the combination of healthy but unspectacular economic growth and a patient Fed inclines investors to continue to reward firms with superior idiosyncratic growth profiles despite premium valuations.

For what it’s worth, Goldman says that it falls “in the third camp” as the bank’s economist s predict US GDP growth of 2.8% in full- year 2019 and expect that growth will remain modestly above-trend in the 2%-2.5% range through the end of 2021. As a result, “S&P 500 EPS growth should accelerate in 2H 2019, as expected by most analysts, but the consensus forecast of 12% EPS growth in 2020 looks overly optimistic (our top-down estimate is +4%).”

That said, last December Goldman predicted that there would be 4 rate hikes in 2019. Now it does not expect a rate hike until the very end of 2020 so take any Goldman forecast with a mountain of salt.

And speaking of trade recos from Goldman, the bank’s equity strategist urges clients to focus on dispersion, which “

today is close to the widest level this cycle and according to some measures the widest since the Tech Bubble. As a result, we would continue to focus on growth but avoid the stocks with the most extreme valuations.”

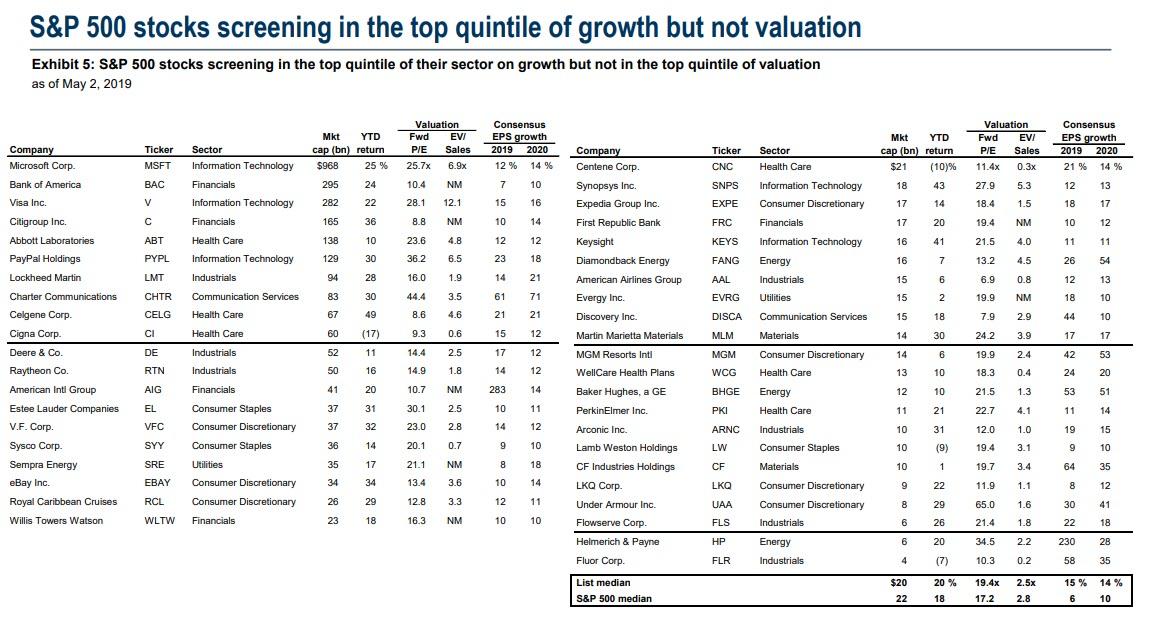

Putting this in practical terms, Goldman shows the chart below, which shows 42 stocks that rank in the top 20% of their S&P 500 sectors on sales and EPS growth but not in the top quintile on valuation, based on the combination of metrics we use to create our factors. These stocks trade at roughly the same median valuation as the typical S&P 500 stock with substantially faster expected EPS and sales growth through 2020. YTD the median stock on the list has outperformed the median S&P 500 stock 20% vs. 18%.

via ZeroHedge News http://bit.ly/2Y1B51o Tyler Durden

A detailed plan from “UNITED STATES SOUTHERN COMMAND” dated “23 FEBRUARY 2018” was issued with the title “PLAN TO OVERTHROW THE VENEZUELAN DICTATORSHIP ‘MASTERSTROKE’” and is here presented complete.

This document was personally signed by Admiral Kurt W. Tidd, who was the Commander (the chief), at SOUTHCOM, and he was thus the top U.S. military official handling Venezuela. But this was far more than just a military plan.

It was comprehensive — directing military, diplomatic, and propaganda, policies — regarding the Trump Administration’s planned “Overthrow” of Venezuela’s Government. His plan has since guided the Administration’s entire operation, including “the capacities of the psychological war,” regarding Venezuela.

It instructed SOUTHCOM:

Encouraging popular dissatisfaction by increasing scarcity and rise in price of the foodstuffs, medicines and other essential goods for the inhabitants. Making more harrowing and painful the scarcities of the main basic merchandises.” …

intensifying the undercapitalization of the country, the leaking out of foreign currency and the deterioration of its monetary base, bringing about the application of new inflationary measures.” …

Fully obstruct imports, and at the same time discouraging potential foreign investors in order to make the situation more critical for the population.” …

compelling him to fall into mistakes that generate greater distrust and rejection domestically” …

To besiege him, to ridicule him and to pose him as symbol of awkwardness and incompetence. To expose him as a puppet of Cuba.” …

Appealing to domestic allies as well as other people inserted from abroad in the national scenario in order to generate protests, riots and insecurity, plunders, thefts, assaults and highjacking of vessels as well as other means of transportation, with the intention of deserting this country in crisis through all borderlands and other possible ways, jeopardizing in such a way the National Security of neighboring frontier nations. Causing victims and holding the Government responsible for them. Magnifying, in front of the world, the humanitarian crisis in which the country has been submitted to.”

Structuring a plan to get the profuse desertion of the most qualified professionals from the country, in order ‘to leave it with no professionals at all’, which will aggravate even more the internal situation and along these lines putting the blame on of Government.”

the presence of combat units from the United States of America and the other named countries, under the command of a Joint General Staff led by the USA.”

It was posted online at the Voltairenet site, and was first copied to a web archive on 14 May 2018. So, it has been online since at least that date. However, because the photo in it of the document wasn’t made available via software which includes the individual symbols, but presented only the full visual image of the paper document, it still hasn’t yet gone viral on the Web.

Here, therefore, is the first appearance, on the Web, of the full document, that’s manually copied, character-by-character, so that each phrase in this document becomes, for the first time, web-searchable, and thereby conveniently available for journalists and historians to quote from.

This prophetic document — the source for what has happened afterward in and to Venezuela — might therefore finally receive the public attention that it so clearly merits.

The document starts with propaganda against Venezuela’s existing Government (and it totally ignores the extent to which the pre-existing U.S. economic sanctions against Venezuela had actually caused these problems), and it then proceeds to present the U.S. plan to overthrow the ‘dictatorship’. (Tidd refers to Maduro only as “the Dictator,” except at the very start and very end.

At the end, he commands “the denouncement toward Maduro’s regimen” and he also uses the phrase “the enemy” to refer to him — as if there had been the U.S. Constitutionally required authorization, by the U.S. Congress, of this “war.” The close urges “the dispatch of a UNO military force for the imposition of peace, once Nicolas Maduro’s corrupt dictatorship is defeated.” The U.N. is militarily to “impose” “peace,” after the U.S. and its allies have conquered Venezuela.)

Although Tidd placed 100% of the blame for Venezuela’s problems upon Maduro, and ignored the crucial extent to which U.S. economic sanctions had caused them, his plan emphasized that the U.S. must actively make things even worse for the Venezuelan public than America’s economic sanctions had yet done.

His coup-plan is loaded with such statements, and, in fact, opens with one:

“Encouraging popular dissatisfaction by increasing scarcity and rise in price of the foodstuffs, medicines and other essential goods for the inhabitants. Making more harrowing and painful the scarcities of the main basic merchandises.”

So: he wasn’t naive. America’s induced suffering upon Venezuelans was part of his plan for Venezuelans, in order to get them to do what the U.S. regime wants them to do — overthrow Maduro. Furthermore, the United States Government has had extensive successes in previous such operations. One example is that this was how Chile’s Salvador Allende was brought down in 1973 (at a time when the U.S. Government’s claims to have done it for ‘national security’ reasons had much more credibility than its current excuse of helping the Venezuelan people does, because the supposedly ideological Cold War was still on).

The only excuse that the perpetrators can come up with, this time around, is “to put an end to the Venezuelan nightmare and the awakening of theirs beloved nation at a luminous dawn, in which the vision of fortune, true peace and tranquility predominate for their fellow citizens.”

Impoverish the nation, in order to help Venezuelans attain “true peace and tranquility.” That’s the plan.

Here is the document’s entire text:

SOUTHCOM

TOP SECRET

23 FEB 2018

PLAN TO OVERTHROW THE VENEZUELAN DICTATORSHIP “MASTERSTROKE”

UNITED STATES SOUTHERN COMMAND 23 FEBRUARY 2018

TOP SECRET/20180223

CURRENT SITUATION

The Venezuelan Chavista dictatorship staggers as a result of its frequent internal problems; there is a great shortage of foodstuffs, an exhaustion of the sources of foreign currency and a rampant corruption. The international support, won with petrodollars, becomes scarcer each time and the purchasing power of its national currency is in a constant downfall.

Such scenario is not supposed to change, but the Venezuelan present-day leaders, as they usually do, in their despair to preserve their power, are capable to appeal to new populist measures that perpetuate their positions of privilege; the only mechanism that sustains them obstinate to the struggle to hold on their positions.

Maduro’s corrupt regimen will collapse but regrettably, the divided opposing forces, legitimate defenders of democracy and the well-being of their people, do not have power enough to put an end to the Venezuelan nightmare and the awakening of theirs beloved nation at a luminous dawn, in which the vision of fortune, true peace and tranquility predominate for their fellow citizens.

The internal disputes, the supreme particular likings, the corruption similar to the one of their rivals, as well as the scarcity of rooting, do not grant them the opportunity to make the most of this situation and to give the necessary step to overturn the state of penury and precariousness in which the pressure group, that exercises the leftist dictatorship, has submerged the country. We are at the presence of an unprecedented criminal action in Latin America.

This affects the entire region, there is no respect to international right and local political alternatives are unacceptable.

Democracy spreads out in America, continent in which radical populism was intended to take over. Argentina, Ecuador and Brazil are examples of it. The rebirth of democracy has the support of the most valuable determinations, and the conditions in the regions run in its favour.

It is the time for the United States to prove, with concrete actions, that they are implicated in that process, where overthrowing Venezuelan dictatorship will surely mean a continental turning point.

It is the first opportunity of the Trump Administration to bring forward the vision in reference to security and democracy. Showing its active commitment is crucial, not only for the administration, but also for the continent and for the world.

The time has come to

Step to speed up the definite overthrow of Chavismo and the expulsion of its representative:

Undermining the decadent popular support to Government.

Encouraging popular dissatisfaction by increasing scarcity and rise in price of the foodstuffs, medicines and other essential goods for the inhabitants. Making more harrowing and painful the scarcities of the main basic merchandises.

Securing he the present-day dictator’s irreversible deterioration

Developing actions to encourage the egocentrism and the verbal incontinence of the Dictator, compelling him to fall into mistakes that generate greater distrust and rejection domestically, while continuing to minimize the international significance of his public figure.

To beseige him, to ridicule him and to pose him as symbol of awkwardness and incompetence. To expose him as a puppet of Cuba. Exacerbating the division among members of the governing group. Revealing the differences in his living conditions with respect to those of his followers, at the same time to incite them to keep on increasing those divergences. Highlighting examples as the ones of Rafael Ramirez from PDVSA and Nelson Mercengtes from gthe BCV.

Making his government unsustainable, forcing him to claudication, to negotiate or to run away, as other close collaborators have done.

Making provisions for a back or escaping door, in case he finally chooses to look for a safe port out of his country.

Increasing the internal instability to a critical level.

Intensifying the undercapitalizatioin of the country, the leaking out of foreign currency and the deterioration of its monetary base, bringing about the application of new inflationary measures that increase its deterioration and that simultaneously provoke the citizens with less access — who support the present-day rulers — and those who are best positioned, to see their social status threatened or affected. Establishing that the use of bitcoin, Petro, is a key element in the deterioration of the economy, which is an unconstitutional and illegal manipulation of the national currency, useable for money laundering.

Fully obstructing imports, and at the same time, discouraging potential foreign investors in order to contribute to make more critical the situation of the population — mainly in the sphere of oil, essential for any attempt of recuperation of the national economy.

Appealing to domestic allies as well as other people inserted from abroad in the national scenario in order to generate protests, riots and insecurity, plunders, thefts, assaults and highjacking of vessels as well as other means of transportation, with the intention of deserting this country in crisis through all borderlands and other possible ways, jeopardizing in such a way the National Security of neighboring frontier nations. Causing victims and holding the Government responsible for them. Magnifying, in front of the world, the humanitarian crisis in which the country has been submitted to.

Making use of the generalized corruption and the originating profits from their operations with prohibited drugs, to do away with their image in front of the world and their domestic followers.

Promoting fatigue inside the members of the PSUV, inciting the annoyance and nonconformity among themselves, for them to break noisily away from the line of the Government; for them to refuse the measures and restrictions which also affect them, inciting the rising of internal politic factions, which divides it in its schism, making it as weak as the the opposition is. Creating frictions between the PSUV and “Somos Venezuela”.

Structuring a plan to get the profuse desertion of the most qualified professionals from the country, in order “to leave it with no professionals at all”, which will aggravate even more the internal situation and along these lines putting the blame on of Government.

Using the army officers as an alternative of definite solution.

Continuing hardening the conditions inside the Armed Forces to carry out a coup d’etat before concluding 2018, if the crisis does not make the dictatorship to collapse or the dictator does not decide to move aside.

Continuing setting fire to the common frontier with Colombia. Multiplying the traffic of fuel and other goods. The movement of paramilitaries, armed raids and drug trafficking. Provoking armed incidents with the Venezuelan frontier security forces.

Recruiting paramilitaries mainly in the campsites of refugees in Cucuta, La Guajira and the north of Santander, areas largely populated by Colombian citizens who emigrated to Venezuela and now return, run away from the regimen to intensify the destabilizing activities in the common frontier between both countries. Making use of the empty space left by the FARC, the belligerency of the ELN and the activities in the area of the Gulf Clan.

Preparing the involvement of allied forces in support of the Venezuelan army officers or to control the internal crisis, in the event they delay too much in taking the initiative.

Establishing a speedy time line that prevents the Dictator to continue winning control on the internal scenario. If it’s necessary, act before the elections stipulated for next April.

Getting the support of the allied authorities of friendly countries (Brazil, Argentina, Colombia, Panama and Guyana).

Organizing the provisioning, relief of troops, medical and logistic support from Panama. Making good use of the facilities of electronic surveillance and signals intelligence, the hospitals and its deployed endowments in Danen, the equipped airdromes for the Colombian Plan, as well as the landing fields of the old-time military bases of Howard and Albrook, as well as the one belonging to “Rio Halo”. In addition, the Humanitarian Regional Center of the United Nations, designed for situations of catastrophes and humanitarian emergency, which has an aerial landing field and its own warehouses.

Moving on the basification of combat airplanes and choppers, armored conveyances, intelligence positions, and special military and logistics units (police and military district attorneys and prisons).

Developing the military operation under international flag, patronized by the Conference of American Armies, under the protection of the OAS and the supervision, in the legal and media context, of the Secretary General Luis Almagro. Declaring the necessity that the continental commandment be strengthened to act, using the instrument of the Inter-American Democratic Charter, in order to avoid the democratic rupture.

Binding Brazil, Argentina, Colombia and Panama to the contribution of greater number of troops, to make use of their geographic proximity and experience in operations in forest regions. Strengthening their international condition with the presence of combat units from the United States of America and the other named countries, under the command of a Joint General Staff led by the USA.

Using the facilities at Panamanian territory for the rear guard and the capacities of Argentina for the securing of the ports and the maritime positions.

Leaning on Brazil and Guyana to make use of the migratory situation that we intend to encourage in the border with Guyana.

Coordinating the support to Colombia, Brazil, Guyana, Aruba, Curacao, Trinidad and Tabago and other States in front of the flow of Venezuelan immigrants in the event of the crisis. Promoting international participation in this effort, as part of the multilateral operation with contribution of the States, Non-Profit Organizations and international bodies. Supplying the adequate logistic, intelligence, surveillance and control support.

Anticipating, specially, the most vulnerable points in Arauca, Puerto Carreno and Ininda, Maicao, Barranquilla and Sincelejo, in Colombia, and Roramia, Manaos and Boa Vista, in Brazil.

Information Strategie

Silencing the symbolic presence of Chavez-representative of unit and popular support-, and in the other way around, keeping the harassment to the Dictator as the only responsible of the crisis in which he has submerged the nation.

Holding the Dictator and his closer followers responsible, in the first place, for the prevailing crisis due to his inability to find the way out that the Venezuelans are in need of.

Intensifying the media denouncement about the cubanization of Venezuela.

Outstandingly intensifying the denouncement toward Maduro’s regimen, considering him:

A criminal

A illegitimate

A thief of the wealth of the Venezuelan people

Someone who plunders the national treasury to carry out his evasion

Highlighting the incompetence of the mechanisms of integration created by the regimens of Cuba and Venezuela, specially the ALBA and PETROCARIBE, in order to tackle the situation of the country and their inability to find solutions to the problems that the citizens are facing.

Increasing, inside the country and through the mass media established abroad, the dissemination of designed messages based on testimonies and publications originated in the country, making use of all the possible capacities, including the social networks.

Claiming, through that mass media, the need to put an end to this situation because of its unsustainable essence.

Justifying and assuring through violent means the international backup to the deposal of the dictatorship, displaying an extensive dissemination, inside the country and to the entire world, through all the open means and the capacities of the psychological war of the US ARMY.

Assuring that the disclosed images and reports of the military actions are approved by the General Staff to prevent their manipulation and use by the enemy.

The United States should entirely back up the OAS, strengthening the image of the OAS and other multilateral institutions for the inter-American system, as instruments for the solution to the regional problems.

Promoting the request of the the dispatch of a UNO military force for the imposition of peace, once Nicolas Maduro’s corrupt dictatorship is defeated.

[signature]

K.W. TIDD

Admiral, USN

COMMANDER

via ZeroHedge News http://bit.ly/2LoD7ak Tyler Durden

The UK’s tax collector – HM Revenue and Customs (HMRC) has been forced to delete the biometric voice records of five million people because they did not have clear consent from customers to have them in the first place, according to ZDNet.

HMRC uses the Voice ID biometric voice security system to make it easier for callers to fast-track security processes while discussing their account. The system promises to reduce wait times and prevent unauthorized people from accessing accounts.

The UK’s data privacy watchdog, however – the Information Commissioner’s Office (ICO) sways that HMRC failed to properly inform customers about how their biometric data would be processed, and did not allow them to give or withhold consent in a “breach of the General Data Protection Regulation,” according to the ICO.

ICO Deputy Commissioner Steve Wood said “We welcome HMRC’s prompt action to begin deleting personal data that it obtained unlawfully. Our investigation exposed a significant breach of data protection law – HMRC appears to have given little or no consideration to it with regard to its Voice ID service.”

Under the GDPR, biometric data is subject to stricter conditions as it is placed in a special category of information.

“Innovative digital services help make our lives easier but it must not be at the expense of people’s fundamental right to privacy. Organisations must be transparent and fair and, when necessary, obtain consent from people about how their information will be used. When that doesn’t happen, the ICO will take action to protect the public,” Wood added.

HMRC’s the scheme was criticised last year by privacy campaigners Big Brother Watch who said there was no option for callers to opt out of the ID scheme, or have their voiceprint deleted. A complaint by Big Brother Watch prompted the ICO investigation.

HMRC has written to the Information Commissioners Office (ICO) and said it will now only keep Voice ID enrolments where it holds explicit consent. That accounts for around 1.5 million customers, who have used the service since HMRC introduced changes in October 2018 to comply with GDPR requirements. –ZDNet

HMRC will now delete all records where they do not have explicit consent by June 5th, 2019 – a deadline set by the ICO.

According to Silkie Carlo, director of Big Brother Watch, “To our knowledge, this is the biggest ever deletion of biometric IDs from a state-held database. This sets a vital precedent for biometrics collection and the database state, showing that campaigners and the ICO have real teeth and no government department is above the law.”

HMRC CEO Jonathan Thompson said “These total around 5 million customers who enrolled in the Voice ID service before October 2018 and have not called us or used the service since to reconfirm their consent.”

Of note, there are around 30 million taxpayers in the UK.

The agency will still continue to use Voice ID, which has shown to be popular with customers.

“HMRC has worked hard to ensure the system complies with GDPR requirements around explicit consent and our published privacy notice already makes clear that we will not use voice identification data for any other purposes,” added Thompson.

via ZeroHedge News http://bit.ly/2ZUGBox Tyler Durden

Fortunately, the market rallied on Friday as traders scrambled to hold important support levels following confirmation from Richard Clarida that the Fed has no intention of moving interest rates anytime soon. Via Bloomberg:

CLARIDA: WE’LL WEIGH `WHAT, IF ANY, FURTHER ADJUSTMENTS’ NEEDED

CLARIDA: FED FUNDS RATE NOW IN RANGE OF NEUTRAL ESTIMATES

CLARIDA SAYS FED CAN AFFORD TO BE DATA DEPENDENT

FED’S CLARIDA SAYS U.S. ECONOMY IS IN A `VERY GOOD PLACE’

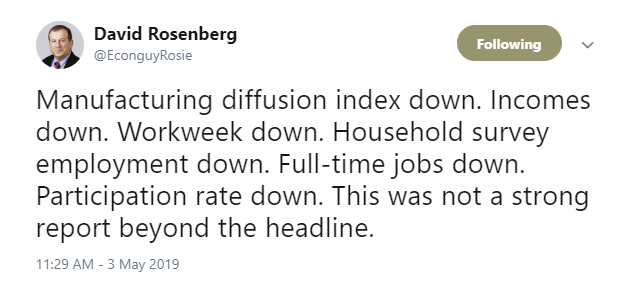

Despite headlines to the contrary, the employment report on Friday was NOT good and we will likely see a good bit of payback next month. David Rosenberg summed it up well:

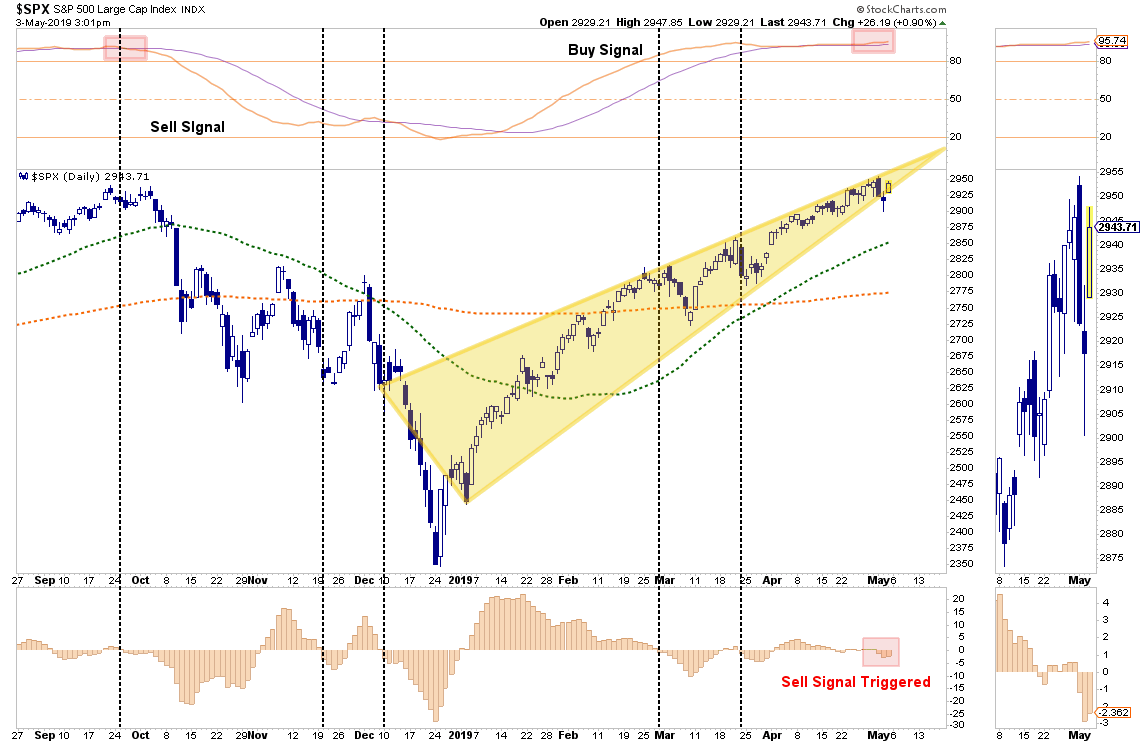

“While that break to the upside was indeed bullish, the market remains very confined to a rising consolidation pattern and failed to close above the intraday all-time highs from last September. With the markets trading on VERY light volume on Friday, combined short-term ‘sell signals’ forming, and pushing more extreme overbought conditions, it is too early to completely remove all risk management controls in portfolios.”

The chart below is updated from last week.

While the market did hold inside of its consolidation pattern, we are still lower than the previous peak suggesting we wait until next week for clarity. However, a bit of caution to overly aggressive equity exposure is certainly warranted.I say this for a couple of reasons.

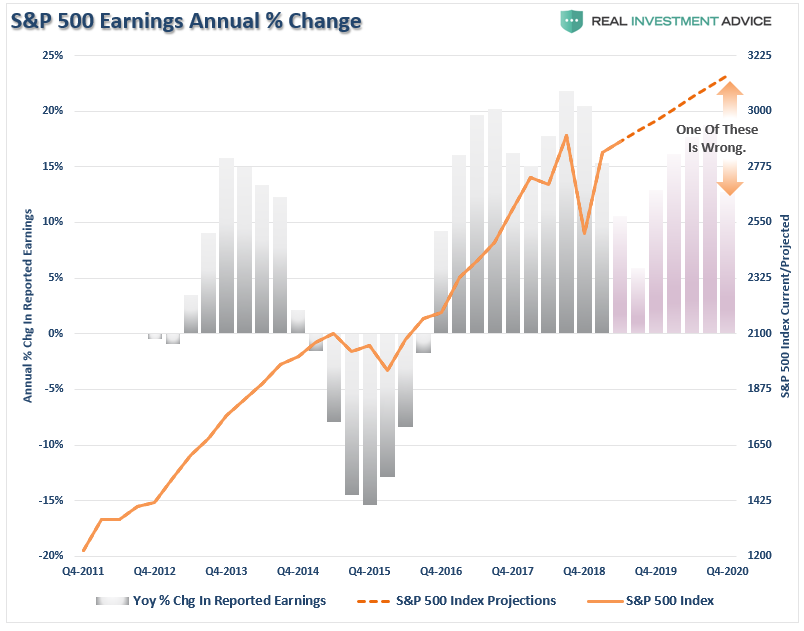

The market has had a stellar run since the beginning of the year and while earnings season is giving a “bid” to stocks currently, both current and forecast earnings continue to weaken.

We are at the end of the seasonally strong period for stocks and given the outsized run since the beginning of the year a decent mid-year correction is not only normal, but should be anticipated.

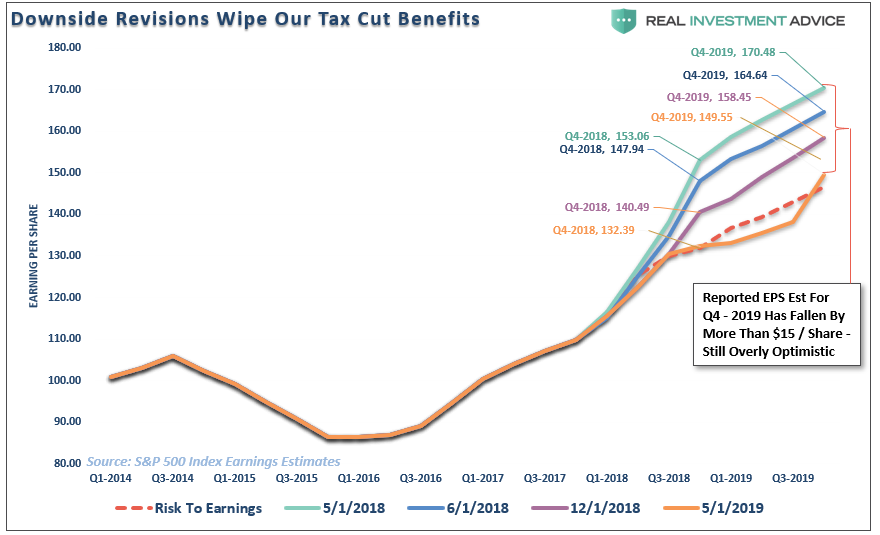

With respect to earnings, and as we have stated many times previously, estimates continue to be revised lower, and have now exceed our original revision target (red dashed line) set out in early 2018.

Note: The Q4-2019 hockey-stick earnings jump WILL BE revised down markedly over the next few months.

Why do I say that?

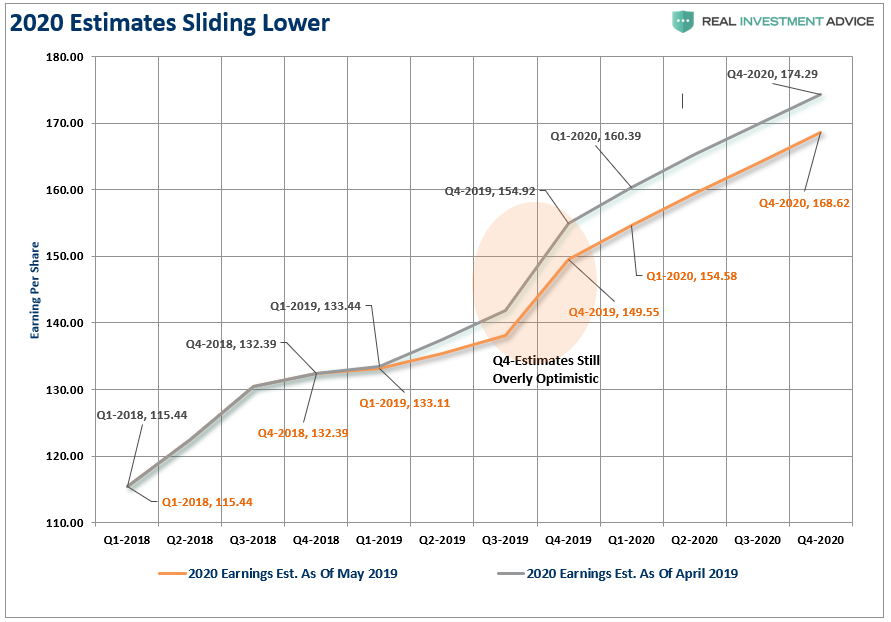

Because 2020 estimates are already being revised down rather sharply as well.

This is important as markets push all-time highs at a time when forward earnings estimates for the next 18-months are all lower than previously estimated. Despite the rise in expected earnings in 2020, the peaks of those expectations (which are predictably about 33% too high currently) are all lower than the 2018 earnings peaks.

In other words, further increases in the markets over the next two years will be a function of multiple expansion rather than increased “value.”

Such an environment tells us a few things about the market.

In the short-term prices will be driven by momentum and optimism. (1-3 months)

Over the intermediate-term prices will become more subject to higher volatility due to potential disappointments as “bad news” is treated as “bad news” (4-9 months)

Longer-term the market is simply a weighing machine and current expectations of 8% annual growth rates in asset prices will be realigned with weaker earnings prospects (10-24 months)

As noted above, the market’s stellar run is set for a breather over the next couple of months. Specifically, as we approach the end of the seasonally strong period, the odds of a “reset” rise markedly. As noted on Thursday by StockTraders Almanac the seasonal “sell” signal has also been triggered. To wit:

“Yesterday after the market closed, we sent out our Tactical Seasonal Switching Strategy Sell Alert for DJIA and S&P 500…we are shifting the ETF Portfolio to a market-neutral position by adding some exposure to short and longer duration bonds.”

Never Hurts To Ring The Cash Register

This brings me to what we did with our equity portfolios last Tuesday and subsequently reported to our RIA PRO subscribers on Wednesday morning. (Try NOW and get 30-days FREE)

“A common theme through today’s report is ‘Profit Taking.’ Over the last couple of weeks, we have continued to discuss taking profits and rebalancing risks. Yesterday we sold 10% of our many of holdings prior to earnings to capture some profits. We also added to some of our Healthcare holdings which have been under undue pressure and represent value in a market that has little value currently.”

This was also a point Jim Cramer reiterated on CNBC on Thursday:

“Any time you have a remarkable run, it never hurts to take something off the table. Nobody ever got hurt ringing the register,” – Jim Cramer, CNBC

As the old Wall Street saying goes:

“Bulls make money. Bears make money. Hogs get slaughtered.”

Yes, markets are hovering near all-time highs and everything certainly seems to be firing on all cylinders. However, such is ALWAYS the case before a correction begins. Such is the nature of markets.

Currently, the markets have had a stellar run since the beginning of the year, and as we wrote previously if you sold everything today, and went to cash, it is unlikely you will miss much between now and the end of the year. (We aren’t recommending you do that, it is just to illustrate a point)

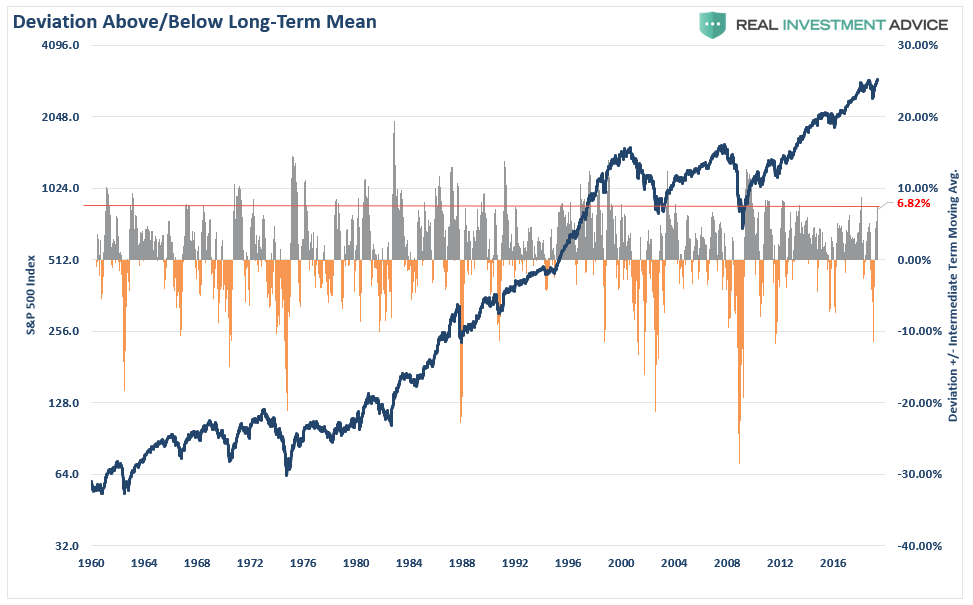

“At almost 7% above the long-term weekly moving average, the market is currently pushing the upper end of historical deviations.”

The important point to take away from this data is that “mean reverting” events are commonplace within the context of annual market movements.

Currently, investors have become extremely complacent with the rally from the beginning of the year and are quick extrapolating current gains through the end of 2019.

As shown in the chart below this is a dangerous bet. In every given year there are drawdowns which have historically wiped out some, most, or all of the previous gains. While the market has ended the year, more often than not, the declines have often shaken out many an investor along the way.

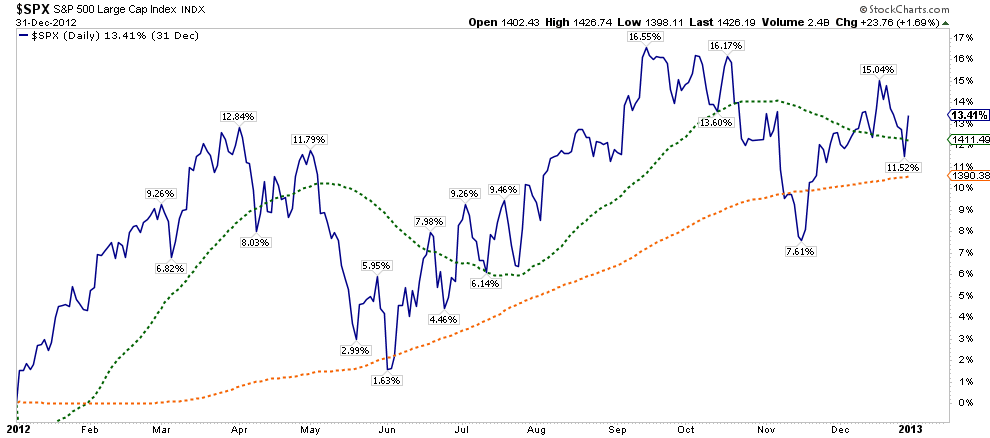

Let’s take a look at what happened the last time the market started out the year up 13% in 2012.

So far, it looks a whole lot like this year.

“From a portfolio management standpoint, the reality is that markets are very extended currently and a decline over the next couple of months is highly likely. While it is quite likely the year will end on a positive, particularly after last year’s loss, taking some profits now, rebalancing risks, and using the coming correction to add exposure as needed will yield a better result than chasing markets now.”

Given that every given year has some sort of corrective action in it, betting this year will be different is a low probability event.

Slowing Domestic Economic Growth: I see going forward nominal GDP in the U.S. at nearly recessionary growth levels. There was less than meets the eye in the first-quarter headline Real GDP growth rate of 3.2%. The accumulation of inventories, large doses of government spending and a sharp improvement in exports will likely subtract from the second-quarter growth rate. Moreover, consumer spending is clearly slowing (first-quarter consumer durable spending was down 5%), along with housing and non-residential construction now. Commodities are down in each of the last five days and are now at a seven-week low. Finally, credit card charge-off rates are rising sequentially, as are delinquency rates.

Slowing Non-U.S. Economic Growth: Economic confidence in the European Union has hit a 10-month low. Hong Kong exports to China are falling post haste (down 10% in March). Finally, last night’s disappointing Chinese data questions the foundation of growth in that region.

The Earnings Recession: A strengthening currency, sub-4% nominal U.S. GDP growth and rising wage and salary costs pose threats to corporate profitability this year. While estimates have improved from year-end, first-quarter profits still look to be down by more than 2%. According to Rosie (David Rosenberg), fully 84% of those companies issuing guidance have been negative. Second-quarter profits look negative, again. As I have chronicled, profit margins peaked several quarters ago (3Q 2018). Going forward, it seems to me that commodities and interest expenses are likely troughing and that wage growth may accelerate from here, pressing margins. Finally, don’t fall for the fact that 77% of the reporting companies have beat “estimates.” This is what I refer to as the “Twit Olympics” where estimates are taken down and guided to levels that almost certainly will be beat.

The Last Two Times the Fed Ended Its Rate Hike Cycle, a Recession and Bear Market Followed

The Strengthening U.S. Dollar: More than 40% of the S&P component’s sales are non U.S.-based. A strong U.S. currency will be a profits headwind over the remainder of 2019.

Message of the Bond Market: Stated simply, the 10-year U.S. note is sending the message of slowing global economic growth.

Untenable Debt Levels: I have already spent quite a lot of time making the case that debt is a governor to growth. The greatest subset threat is sovereign debt, which for now is being ignored.

Credit Is Already Weakening: With GDP up by more than 3% in real terms in the first quarter, one should be asking, “Why are bank credit and leveraged loans weakening?” The proliferation of “covenant lite” financing and the existence of increasingly excessive leverage are worrisome. Bankwide loans are weakening (are inventories bloated?); it’s the most sluggish trend seen since 2016. The ratio of debt upgrades to downgrades this year is also at the worst level in three years. As well, the leveraged loan market is seeing outflows and distressed debt is beginning to see an acceleration in write-offs. Finally, the search for yield, coupled with low interest rates, causes mischief and the misallocation of resources — for example, the silly issuance of 100-year Argentina bonds that now sell for about 66 cents on the dollar (they were issued at par).

Valuation: Many claim that the “Powell Pivot” and its likely ramifications of lower rates for longer provides a cover for equities. But stocks, currently valued at 17x forward earnings, are now more than two price-to-earnings (P/E) multiple points above the average level of the last decade — a period of time in which rates were mostly at or near generational lows.

Positioning Is to the Bullish Extreme: As noted last week by my pal Peter Boockvar, chief investment officer at Bleakley Advisory Group, the net speculative position in short VIX futures is at an all-time high. And all-time is a long time.

Rising Bullish Sentiment (and The Bull Market in Complacency): The CNN Fear & Greed Index is extended toward Greed now. Barron’s Big Money Poll lists only about one-sixth of the respondents as bearish.

Non-Conformation of Transports: The Dow Theory is shining an amber light in 2019’s sea of market green. I am surprised so few technicians have mentioned this warning flag.

It’s a lot.

However, where that laundry list of worries is long, none of them are going to be the “one” which gets the market. It is the combination of these issues which provide the “fuel” to amplify the impact of an unexpected, exogenous event which ignites selling in the markets.

Since it is ALWAYS an unexpected event which causes sharp declines in asset prices, this is why advisors typically tell their clients “since you can’t predict it, all you can do is just ride it out.”

This is not only lazy, but ultimately leads to the unnecessary destruction of capital and the investors time horizon.

via ZeroHedge News http://bit.ly/2VHXAuV Tyler Durden

Analysts have studied a report from North Korea’s Korean Central News Agency, which was accompanied by a few images, and determined that the “projectile” fired by North Korea Saturday morning, was, in fact, a short-range ballistic missile.

In addition to images released by KCNA, independent analysts managed to capture images of the launch.

Lucky shot! Captured by @planetlabs Planetscope satellite at 0154 UTC (1054 local) on Saturday as it overflew Wonsan, North Korea. pic.twitter.com/g5QgVI8hJf

But before Korea hawks in the US start accusing Kim Jong Un of playing Washington with his pursuit of denuclearization, Bloomberg reports that, while the test may have violated United Nations sanctions on North Korea, it appears to have stopped short of breaking Kim’s promise to Trump to refrain from testing long-range missiles that could threaten the US. This would suggest that the launch was merely a sign of frustration and a warning by the North.

In a Saturday tweet, Trump brushed off reports about the missile launch, insisting that Kim wouldn’t do anything to jeopardize talks. It appears he was correct in that assessment.

South Korea’s Defense Ministry issued a statement on Sunday saying “based on what was analyzed until now, what we understand is that (North Korea) launched many 240mm, 300mm multiple rocket launchers including new model of tactical guided weapons & assess that the range is about 70-240km.”

Lindsey Graham, one of the most prominent North Korea hawks, warned in a tweet that the launches could “change the equation in a dangerous and dramatic fashion.”

I appreciate the historic efforts President Trump and his team have made to solve the North Korean nuclear threat peacefully.

The President has been personally engaged in an unprecedented manner and shown a willingness to find a win-win solution. https://t.co/2eFBr6TC0e

One analysts claimed that while the launch was undoubtedly the most significant provocation from the North since hostilities were put on hold in late 2017, South Korea appeared to be backing away from forcefully condemning its northern neighbor with its language describing the missile as a “projectile,” which appeared to suggest that the launch might have just been an artillery drill. Though a spokeswoman for South Korea’s president did condemn the launch for threatening the carefully constructed peace between the two powers.

Nathan Hunt, an independent defense researcher, said the South Korean statement was “skirting over” North Korea’s ballistic missile launch. “They did indeed test a new short-range missile, or as others call close-range ballistic missile, and this was not just an artillery drill,” Hunt said.

Either way, the exercise was Kim’s most significant provocation since he launched an intercontinental ballistic missile in November 2017, declared his nuclear weapons program “complete” and opened talks. Kim has expressed increasing frustration since Trump refused his demands for sanctions relief and walked out of their second summit in Hanoi in February.

During a meeting with Russian President Vladimir Putin last month, Kim accused the US of acting in “bad faith” by refusing to compromise in its talks with the North, which were stalled even before Trump walked away from the table during a summit between the two leaders in Hanoi.

Another analyst said the missile appeared to be a short-range weapon similar to a Russian Iskander. She also slammed Trump for trying to “pretend” he’s making progress with North Korea.

The weapon featured in the KCNA photograph appeared to be a solid-fuel ballistic missile similar to a Russian Iskander, said Melissa Hanham, a non-proliferation expert and director of the One Earth Future Foundation’s Datayo Project. North Korea had unveiled a similar weapon, which could be stored while fueled, deployed and fired with less detection time, during a military parade in February 2018.

“Looks like Donald Trump is ignoring it, because it doesn’t fit into his narrative,” Hanham said. “He wants to pretend that he is making progress in North Korea and that they wouldn’t test a new missile.”

The timing of the launch was also significant: It came days ahead of a visit by US Special Representative Stephen Biegun to South Korea and Japan. Some also speculated that it could have been a gesture of contempt ahead of the restart of joint military exercises between South Korea and the US.

via ZeroHedge News http://bit.ly/2Y75Vpl Tyler Durden

When Tesla announced during its last earnings report that it was considering entering the insurance business (because that’s clearly an organic pivot to making electric cars and batteries), some people were surprised, others weren’t. Supporters of the company, clinging to Elon Musk’s every desperate business model pivot, applauded the idea. “Great way to diversify, Elon,” they likely thought. Skeptics and – well, pretty much anybody else – were immediately critical of the idea, including the Oracle From Omaha himself, Warren Buffett.

Buffett said at Berkshire’s annual meeting that Tesla will struggle if it goes into the insurance business, a field where Buffett just happens to be a bit of an expert, according to CNBC. Musk has been called out in the past (see here and here and here) by experts in fields of study that he claims to understand but doesn’t, and it’s happening yet again.

Buffett said: “It’s not an easy business. The success of the auto companies getting into the insurance business is probably as likely as the success of the insurance companies getting into the auto business.”

As a reminder, Musk told analysts last month that Tesla would be launching an insurance product in May. He claimed that his company has direct knowledge of a person’s risk profile “based on the car” which gives it an “information arbitrage” opportunity. Because, you know, “traditional” non-disruptive auto insurance actuaries don’t take into account what kind of car you drive. Warren Buffett – again, a finely tuned expert in the insurance industry – called Musk on that bulls*it.

“I’d bet against any company in the auto business…” Buffett also commented.

About 1/3 of Berkshire Hathaway’s business is in insurance, including Geico, whose value has risen more than $50 billion since Berkshire acquired it.

And in terms of Tesla getting its insurance product off the ground, PlainSite tweeted out that the company has had the name “Tesla Insurance Services” registered since 2017. According to PlainSite, they have 1 registered agent working out of San Francisco. This compares to Geico, who has 499 agents whose names just begin with the letters A, B and C.

It has one (1) endorsed agent who works out of a shared office in San Francisco.

On the other hand, insurance is a great industry for playing accounting tricks and collecting cash up front – two things Tesla has been honing its expertise in.

via ZeroHedge News http://bit.ly/2VK1ljs Tyler Durden