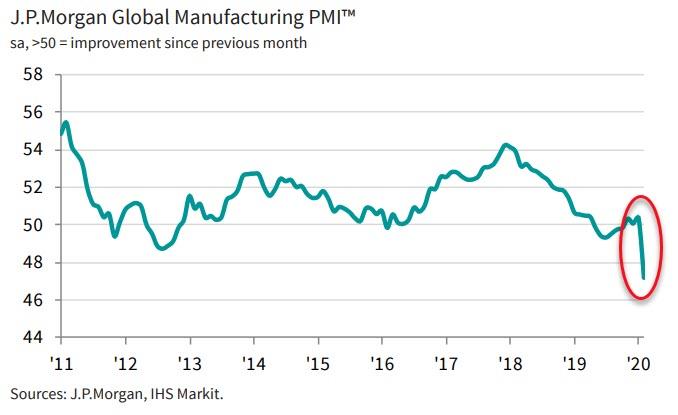

The global manufacturing sector suffered its steepest contraction since 2009 as demand, international trade and supply chains were severely disrupted by the COVID-19 outbreak.

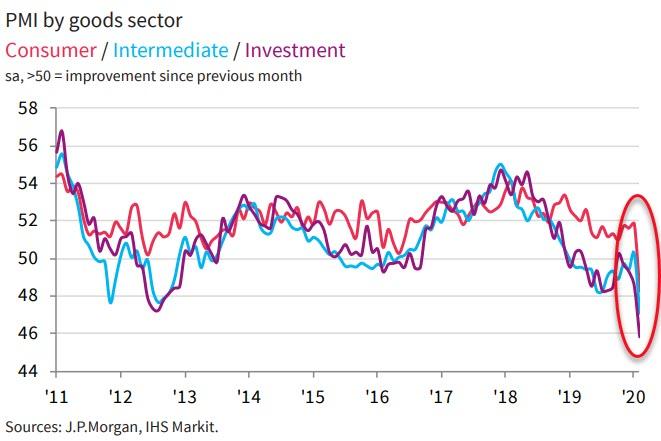

Output fell across the consumer, intermediate and investment goods industries, with the steepest drop at investment goods producers.

Manufacturing production and new orders registered their sharpest declines since April 2009.

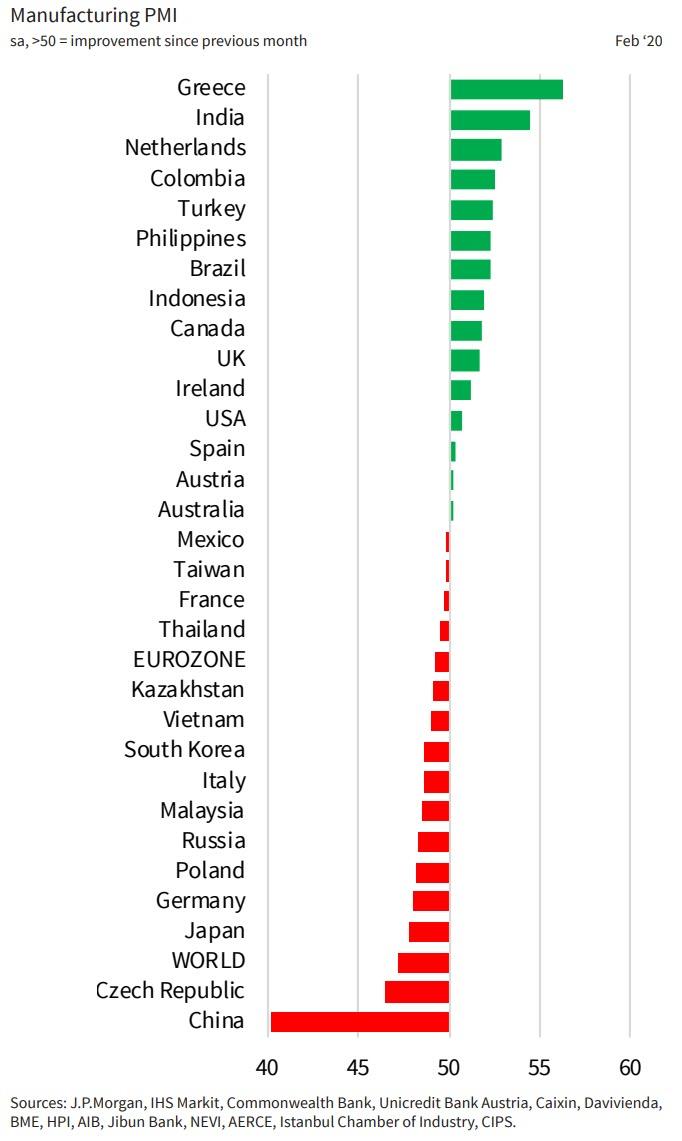

The downturns in both were quickest in China, where output and new business fell at survey-record rates. Of the 31 nations for which February data were available, 15 registered a contraction of output, including China, Japan, Germany, France, Italy, Taiwan, South Korea and Australia.

Clearly, the outbreak of COVID-19 had a marked impact on supply-chains during February… Just wait for the v-shaped recovery… any minute now!

Rabobank: An “Epoch-Marking” Moment In Treasury Yields Is Imminent

Submitted by Michael Every of Rabobank

The 1%

On Friday I was briefly conversing with the head of our Rates Strategy team about the virus and markets. As equities and US Treasury 10-year yields plummeted in tandem, we mused over how long it would be before we printed the psychological and epoch-marking sub-1% level. “Not long after the first US virus death,” was the conclusion.

Well, here we are. As the White House adopts a far more sombre tone, one US citizen has died from Covid-19, and clusters of cases continue to spread across the States with no link to China. Panic buying is being seen in places. In Iran, things are reported to be totally out of control, or so the social media rumors have it when the country is still closed off after the recent violent crackdown on protests, and when official news-flow is still Panglossian. In Europe, cases are also soaring exponentially and lockdowns are slowly spreading. No meetings of over 5,000 people now says France: because at 4,999 the virus isn’t transmissible, obviously. No cessation to free movement either, because EU27 > COVID19. In short, the virus trend surely says “sub-1%” imminently.

Indeed, Monday morning in Asia we saw the US 10-year hit 1.03% before rebounding back to 1.10% again, and 10-year Aussies trade at 0.68%, through the level of the OCR. In Japan, 10-year JGBs got to -0.18%.

The cause for the yield plunge was obvious. Saturday’s China PMI data were frankly shocking. Manufacturing was at 35.7 and services at 28.9: these are not recessionary levels, but outright depressionary. The private Caixin PMI was also awful at 40.3, again saying a deep downturn is biting. Of course, the real issue is if we get a V-shaped recovery in output – or in virus infections. Optimists, and Chinese stocks this morning, are cheering the former – and Chinese stocks are always freely traded and never, ever manipulated by the authorities, as well all know. Realists, and NASA satellite imagery of no pollution over China, lean towards the latter: as does one anecdotal, unsubstantiated report trending over the weekend that China has been ordering factories to leave the lights on to make them look busier from space and to boost electricity output in case pesky foreigners start trying to use that as a GDP proxy.

The cause for the yield bounce, apart from Potemkin Chinese stocks, purely technical functions, and Goldman Sachs saying they see this all as a brief blip, are remaining hopes that ‘central banks have this’. For example, Friday saw Fed Chairman Powell step in with a public statement: “The fundamentals of the U.S. economy remain strong. However, the coronavirus poses evolving risks to economic activity. The Federal Reserve is closely monitoring developments and their implications for the economic outlook. We will use our tools and act as appropriate to support the economy.” He didn’t actually do anything over the weekend, as the whispers had had it, but at least he mentioned that he has noticed what is going on. The BOJ this morning has also come out and made clear that it too has noticed that things are not going well (and recall Japan was already in recession, which today’s Q4 capex data at -5.0% only underlines). That is again being seen as positive. On such slim hopes are attempted market rallies based, it seems.

As the rest of the world outside China heads for the same kind of voluntary and obligatory virus lockdowns and NOT-BAU as are already the case in China, raising the question of who China will be selling all its output to once it finally gets up and running again, what is the Fed going to do and how is it going to help? Let’s say they do nothing: they look heartless. Through 1% we go. Let’s say they go 25bp: they look ridiculous. How does 25bp off Fed Funds compensate for a rolling economic panic and lockdown, and for simultaneous supply shocks and demand destruction? Through 1% we go. Let’s say they go 50bp: they then risk looking powerless. After a brief rally in stocks and yields, everything will reverse and the question will be asked “What difference does another 25bp on top of 25bp make?” – and that’s the Fed’s biggest gun being sniffed at. Through 1% we go.

Of course, with our equity-obsessed Fed it’s fairly clear what they will eventually do. Even more so when President Trump is of one mind with the Fed in that key regard, as he used a virus press briefing to lambast the central bank again, adding “We need a Fed that’s going to be a leader,” and asking why the US doesn’t have the lowest interest rates in the world, as if this were a competition. Which it may well soon be.

Talking of the 1%, there might also be some temporary lift for equities and yields today from the South Carolina Democratic primary results. There, voters resoundingly rejected an ageing, white, wealthy, handsy, gaffe-prone president surrounded by Ukraine-related family scandals… by opting for Joe “White Walker” Biden over Bernie Sanders and his anti-1% message. Expect much US media exhaling and talk of a Comeback even as Bernie remains ahead in 10 of the 14 states voting tomorrow on Super Tuesday.

Apart from viruses and caucuses, Europe wakes up today worrying about two other things: The UK and Turkey, and the two are arguably linked. Trade negotiations with the U.K. have started badly and are going to get worse now PM Johnson is allegedly playing hardball by making security contingent on trade access: no trade deal, no automatic UK military support for Europe. With the US also threatening the same, who will be defending Europe? Not Europe, based on its defence-spending plans under the proposed post-Brexit budget. For many countries the 1% figure of military spending to GDP is still closer than the 2% that NATO and the US would like to see.

Meanwhile, Turkey is threatening to reopen its borders and openly encourage Syrian refugees to flow West again: just what an increasingly-populist, virus-struck EU needs to see. President Erdogan has made clear the price for stopping this refugee flow: Europe and the US must give him military support vs Syria (read Russia), where he has just shot down two Syrian jets and blown up a Russian air defence system (not the expensive one he just bought from Russia, which has seen questions asked in the US over how Turkey can also stay in NATO). With the US leaving Afghanistan and in no mood to get dragged directly into a new pointless war, Turkey looks most unlikely to get the support it wants. In which case, what? Uncertainty and unpleasantness for the EU – and more reason to buy bonds.

Frankly, I am sure you can find 99 Dailies written in the Asian time-zone that are more upbeat than this one, especially the ones using official Chinese and/or Fed inputs as their output. In this regard (and only in this regard!) I am happy to be in the 1% – and let the rest eat cake.

“They’re Flying It In!” – Canadians Furious At Trudeau As Government Refuses To Stop Travelers From Iran

Furious Canadians slammed the government for failing to cancel flights from Iran, presently the country with the worst outbreak outside China, and other policies that suggest a dangerously blithe response from the government, perhaps as a consequence of PM Trudeau’s commitment to ‘woke’ policies (many have slammed travel bans as racist).

#COVID-19 is coming. With the explosion of the virus in Italy, Korea, China, and Iran, containment is no longer realistic.

It is however important to slow the spread so hospitals are not overwhelmed.

One critic even accused Ottawa of “flying in” the virus by refusing to cancel flights. Though, to be fair, while President Trump has cracked down on China and Iran, his reaction to Italy and South Korea has been slightly more mild (though the State Department has issued travel advisories targeting SK and Italy.

Can someone in Ottawa take this seriously already and shut down all flights and not allow anyone from key areas – China, Korea and Iran from entering Canada.

Yesterday, Canadian public health officials confirmed four new cases of the virus, each diagnosed at hospitals in Greater Toronto. That brought Canada’s total to 24.

“As a result of the co-ordinated efforts of our health care and public health system, all individuals who have tested positive have been quickly assessed and isolated,” the province’s ministry of health said in a statement.

All of Canada’s cases have been definitively tied to travelers. One patient, a man in his 50s who is a Toronto resident temporarily living in Vaughan, Ontario, where he is under self-isolation, is the brother of a Toronto man who had traveled to Iran recently, Global News reports.

Another man, this one in his 60s, was diagnosed at North York General Hospital after an emergency department visit with symptoms on Friday. He had also recently visited Iran.

And yet a third patient is the spouse of a woman who also contracted the virus. The couple recently traveled to Iran with their young daughter. He was tested at Mackenzie Health Hospital.

“As usual, Jay Powell and the Federal Reserve are slow to act. Germany and others are pumping money into their economies. Other Central Banks are much more aggressive. The U.S. should have, for all of the right reasons, the lowest Rate. We don’t, putting us at a competitive disadvantage. We should be leading, not following!”

But, Mizhuho rates strategist, Peter Chatwell, is concerned that The Fed will ‘deliver’ what Trump and the market is demanding, sending it even deeper into a liquidty trap…

Dear Fed,

On Friday you gave yourself the option to ease and provided a bit of calm to the stock market. It won’t work. Don’t make the mistakes the BoJ and ECB have made in trying to paper over structural problems with liquidity. If you do, your actions will be deflationary and you will devalue your monetary tools. Your real structural problems are rising inequality and the number of ‘zombie’ companies.

The virus will have a major economic impact. Global growth may fall on par with the GFC. It will, with a lag of 6-9 months, justify you easing through the employment dimension of your mandate. It will not, however, be disinflationary. Getting Fed Funds down to 1.25% would put your monetary policy back to a slightly accommodative setting.

However, moving too early, in order to support confidence (let’s admit it, stocks), will put you in a currency war you cannot win. Other central banks, who are missing their inflation targets will follow swiftly, reducing the FX benefit of your easing. By moving to support “confidence” (stocks) and “transmission” (spreads) you will in fact be generating deflationary forces.

Your easing since the GFC has allowed zombie companies to continue their lumbering, groaning, slow-motion takeover of the economy. By no means are we saying you need to shoot them (hike), but equally don’t support them just to satisfy your urges for a roaring SPX. Instead society needs them to bow out gracefully (let PE take the risk). Equities will perform better in the long run if you let the zombies die.

By cutting rates on March 18th, you will be telling the market a) that, all else equal, the underlying value from this level is dubious, and b) that you are determined to support asset bubbles. You will be advocating leveraged longs of failing companies. Your rate cuts will reduce the neutral Fed Funds rate once again. You are choosing to dive into a liquidity trap, racing to 0% Fed Funds and a QE restart. Yield curve control (another market vol killer) should also be avoided. Please learn the lessons from your international counterparts. The water in the liquidity trap isn’t lovely, don’t dive in!

Your attempt to change your inflation target becomes all the less credible in a liquidity trap. Instead of hitting the new target, you will be stuck answering the academic paradox of the reversal rate. As the central bank of the world’s largest economy, you set the tone for other central banks. Forcing them closer to their own reversal rates in this arms race is irresponsible, undermining fiat currency purely to attempt to put a base into equities.

US Manufacturing Growth Slows As New Orders, Imports Slump

Janaury’s (and preliminary February) data signaled mixed messages in the US manufacturing sector with ISM bouncing aggressively and PMI sliding for the 3rd straight month (but both in expansion – above 50).

Markit US Manufacturing PMI fell from 51.9 to 50.7 (below the flash print of 50.8) – 3rd straight month of declines – as new order growth slowed to nine-month lows.

ISM US Manufacturing survey disappointed, dropping from 50.9 to 50.1 (barely above contraction) amid contraction in new orders, and employment.

Source: Bloomberg

PMI remains very near the weakest levels since 2009…

And in the ISM data, three of five components fell, led by the biggest drop in production since 2018.

The gauge of supplier deliveries also rose to the highest level since 2018 — indicating slower delivery times that may be due to supply disruptions from the coronavirus.The imports index swung into contraction, falling the most on record to 42.6, the lowest reading since 2009. Export orders grew at a slower pace.

Supply chain delays stemming from supplier factory shutdowns in China and the outbreak of coronavirus led to a further deterioration in vendor performance, which reportedly held back output and the processing of backlogs due to a shortage of components. As a result, firms registered a renewed rise in outstanding business and a drop in pre-production inventories.

“Manufacturing production and order book trends deteriorated markedly in February as producers struggled against the double headwinds of falling export sales and supply chain delays, both in turn often linked to the coronavirus outbreak.

“Any growth in sales was once again largely driven by domestic consumers, though even here the rate of growth was weakened considerably compared to late last year.

“Historical comparisons against official data indicate that the survey is consistent with factory production and orders both falling at annualised rates of around 3%, with manufacturing jobs being lost at a monthly rate of roughly 20,000.

“While trade war fears have eased, helping push firms’ expectations for future growth to the highest since last April, coronavirus-related supply chain issues threaten to constrain production in coming months. At the same time, companies have become increasingly concerned that the COVID-19 outbreak will also hit demand, which is reportedly already cooling amid uncertainly leading up to the presidential election. Recent stock market volatility could also further dampen consumer spending and deter business investment.”

Sadly for the hopefuls, there is not enough here to shake The Fed’s confidence that

“the fundamentals of the U.S. economy remain strong” (Powell),

“I wouldn’t want to to prejudge the March meeting” (Bullard),

“there is some risk, but basically I think the U.S. outlook looks pretty good” (Yellen),

Millennials Marooned As RobinHood Experiences System-Wire Outage

Last week it was Fidelity shutting down, not allowing investors to trade during the historic market crash, now Robinhood trading app, popularized by millennials, has experienced trading issues on Monday morning.

“We are experiencing a system-wide outage. We are working to resolve this issue as soon as possible,” the company said.

Millennials are freaking out as the market could puke again…

@Robinhood is a joke. One of the biggest trading Mondays in recent history and the app is completely down and crashed since opening bell. People are losing THOUSANDS over this nonsense.

— Vivek Sevak _TLSM (@vivek_sevak_313) March 2, 2020

CDC Accidentally Releases ‘Diamond Princess’ Evacuee Who Tested Positive For The Virus

This doesn’t exactly inspire confidence in the federal government’s virus response, and certainly doesn’t bode well for American officials’ ability to suppress the virus.

Early Monday, the CDC admitted that it had mistakenly released an infected coronavirus patient from the San Antonio Texas Center for Infectious Disease the day prior after the patient twice tested negative for the virus. At that time the patient had no symptoms and technically met the criteria for release, and so was allowed to leave, ABC 7 reports.

However, the patient was soon returned to isolation after a subsequent lab test came back positive for the novel coronavirus, the virus that causes COVID-19. So the CDC decided to bring them back to quarantine “out of an abundance of caution.”

According to CNN, the patient was one of the evacuees from Wuhan, who was evacuated to Texas’s Lackland Air Force Base in San Antonio , been kept in quarantine on military bases in California, Texas and Nebraska.

So, why was the patient released if they still had a lab pending? The agency didn’t offer any kind of explanation.

“The fact that the CDC allowed the public to be exposed to a patient with a positive COVID-19 reading is unacceptable,” said San Antonio Mayor Ron Nirenberg said.

The CDC said the individual, who is currently being retested, had some “limited contact” with healthy individuals on the outside. The CDC said this wasn’t the first time a patient has seen back-to-back tests go from negative to positive. The agency is going to need to tighten its ‘criteria’ for what constitutes a ‘cured’ case. Hopefully they will before they really drop the ball, if it’s not already too late.

Today we learned that the CDC mistakenly released a patient from the Texas Center for Infectious Disease who later returned a positive COVID-19 reading.

The fact that the CDC allowed the public to be exposed to a patient with a positive COVID-19 reading is unacceptable.

— Mayor Ron Nirenberg (@Ron_Nirenberg) March 2, 2020

The CDC also released a statement:

The discharged patient had some contact with others while out of isolation, and CDC and local public health partners are following up to trace possible exposures and notify them of their potential risk

CDC is aware others have encountered similar situations where test results have alternated back & forth between negative & positive. That is part of why CDC criteria states a patient must have two negative test results from specimens taken more than 24 hrs apart.

With the federal quarantine period for the Diamond Princess evacuees coming to an end on Monday, Nirenberg said the city and health department will do all they can to keep the community safe.

“Our San Antonio Metro Health District and other local officials continue to address the situation with the utmost professionalism and care,” Nirenberg said.

Meanwhile, other local officials criticized the mayor and federal officials.

“This has been our biggest concern and now we will experience the consequences of no action,” said Bexar County Judge Nelson Wolff in a joint statement. “Time and time again, I have raised issues concerning evacuees, inappropriate accommodations, the risk of exposure during transporting and the need for additional monitoring and extended quarantine periods.”

Similarly, India reported a case on Monday involving an individual who tested negative for the virus, but later tested positive and was brought in for treatment, but only after being allowed to have contact with family and members of the public.

“I think this is serious in the sense that we can’t afford not to consider it as a serious threat.”

My Colleague James starts the day with a question: “Can a Cat with Coronavirus Bounce?” We shall find out shortly. Everyone expects coordinated action and support… Buying boots on?? Your call. I’d wait a bit.

Here’s my big tip for March 2020. This is likely to get worse, much much worse, BUT… buy banks on the dips and whenever they look cheap. I’m thinking not just the stock of the big dividend payers, but also the debt of the more questionable names with a bit of yield. I’m even thinking: Buy Cocos – the Tier 1 hybrid contingent capital monstrosities that combine all the downside of debt, and none of the equity upside. Why bullish on Banks? I’m not, but I’m pretty certain global authorities will do anything to avoid the Coronavirus morphing into financial catastrophe.

The last thing the authorities will countenance is any uncertainty around the likelihood a bank might be forced to trigger its CoCo debt. I’d even say bonds issued by the Worst Bank in the World – Deutsche Bank, might be worth a punt. That is a really difficult thing to write – I feel dirty just thinking it because it just feels so wrong – but it’s a call arrived at after calm and rational consideration of where the Coronavirus crisis goes next.

This morning the Bank of Japan pretty much said it would do “whatever it takes” to support markets and support liquidity. Gold star to me. I predicted they would: every other central bank will do the same. There are rumours the Fed could act as early as this week with a rate cut. Trump is gunning for them to act.

Thus far I think I’ve called this crisis pretty well. Back on Jan 20th I warned how a Meltup to Meltdown could happen quickly, before suggesting the virus could trigger it a few days later. (All the blogs are there on www.morningporridge.com.) Since then we’ve watched it escalate into a market event, despite the initial stock market indifference followed by a realisation of the economic damage, to the stage the markets are in reactive panic mode. But, unlike any other market shocker I’ve experienced, this one is a slow, grinding slow motion car crash of entirely predictable consequences. We don’t know where this goes, but we can make informed decisions.

The questions for investors are legion, but it’s possible to figure out a likely crisis roadmap round the following questions:

How effective will global central banks and regulators prove as they try to buoy markets through relaxing lending requirements, rate cuts, renewed Asset Purchase Programmes (QE), and even direct equity purchases?

How long-term will the damage to the global economy be from busted supply chains? The problem could be stay-at-home workers as much as anything else.

How much will corporate balance sheets be compromised by lost income? How is that likely to damage sentiment, impact investment, and create job losses? Can these be avoided?

How will the authorities pump liquidity direct to corporates – through bank lending forgiveness, extensions, etc?

If the virus becomes entrenched, how irrelevant will markets be when TV footage of hospitals in crisis dominates the agenda?

Where is this likely to go?

My own guess is that we aren’t yet ready for the likely social and market implications of a full blown pandemic. From reading over the weekend, it would appear 15-20% of cases turn serious, and of these, 20% require acute hospital care, including ventilating patients suffering deep-lung pneumonia. That’s 4% of patients. Yesterday, on the Andrew Marr show, the UK health minister stated the NHS has been able to make 500 acute beds capable of ventilating patients available. If 1 million Brits are affected, they will potentially need 40,000 beds. I understand the worst case scenario the govt is looking at is for 80% of the population, 45 million people, to become infected. Do the maths.

My conclusion is simple. If this becomes a Pandemic, there is likely to be a massive hospital and associated health crisis. The NHS will be forced to stop all other treatment to focus on the flu. As I can attest from a hospital appointment on Friday, the NHS is creaking at the seems at the best of times. If it happens, markets will be forced to react, and it won’t be a priority for global governments.

Meanwhile, back in Britain

Is the news Boris Johnson and his partner are to wed, and produce his unknownth child, supposed to generate a feel good for the UK economy? Boris and his squeeze are not Will and Kate. They aren’t even the latest desperately fondling Z-Listers from Love Island. He’s supposed to be our prime minister – guiding us through pestilence, plague and market meltdowns… Except, he’s not. The new government looks to be degenerating into a circus of political assassinations, blundering incompetence, self-entitled preening, and disruption for the sake of it.

And I voted for them…??? Was that a mistake? The alternative wasn’t great but neither is this.

A few years ago a government whip, Andrew Mitchell, was forced to resign after insulting a policeman by calling him a Pleb. Many people didn’t realise what the root of the insult told us about his mindset – a high class Tory Patrician who perceived himself entitled to rule, exercising his divine right to browbeat mere Plebeian servant. He may have forgotten the plebs also had the vote and elected officials. Quite properly he was slung out.

That was in another age. Today, politicians can get away with anything. The case against the home secretary, Pritti Patel, bears parallels. She has been accused of bullying her staff and conducting a media briefing campaign against her senior civil servant. He’s resigned, was offered a deal to stay quiet, but wants his day in court. Senior cabinet politicians have immediately rallied around her, hailing her as someone “determined” to change the civil service. She is hailed as an effective “distruptor” – suiting the Dominic Cummings agenda perfectly. That she comes across to sceptics like me as a crass political opportunistic is apparently neither here nor there.

Senior civil servants don’t resign over minor tiffs. They resign on matters of principal. For every cabinet source expressing confidence in the minister, there are dozens of insiders telling the press just how awful, self-centred, entitled and out of control she was. If she is a bully she must be dealt with – what signal would it send if she is not? But of course, she won’t be. She will get away with it because… because Cummings and Johnson don’t recognise that creating noise and bluster is not the same as getting stuff done. Disruption for disruptions sake is pointless, especially when done with malice. Check out Patel’s previous form – not good. Are these people you want in government?

And therein lies the problem. The key thing about any debt investment is that it be as “dull, boring and predictable” as possible. The UK fits the model. Over the past few days of crisis, Gilts and Sterling have proved something of a safe haven. We are perceived that way because of our political process and “strong and stable” government/administration. That’s in large part due to the civil service. Break it – and you break not only the country, but the perception of our global credit.

As Chairman Mao (actually it Zhou-Enlai) is rumoured to have said, “its too early” to comment on the French revolution… Its not too early to comment on the unacceptable behavior of Boris’ gang and the damage it might do to the UK’s global prestige long-term.

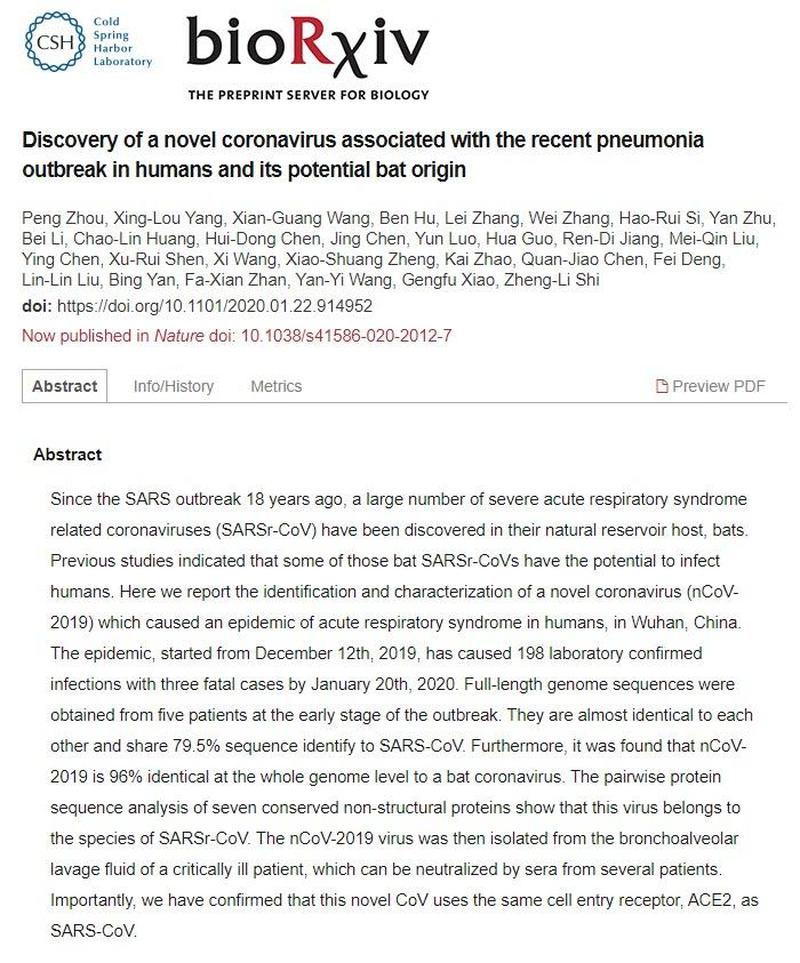

Scott Burke, CEO of crypto-related firm Groundhog, unleashed what we feel may be the most complete timelines of facts to help understand the controversial links between COVID-19 and HIV, and COVID-19 and Wuhan Institute of Virology.

Want to go down a (strictly fact-based) rabbit hole?

Here is the full slightly-edited-for-formatting twitter thread…

A disclaimer: I am not a virologist. This is me synthesizing what we have learned since the outbreak began and reviewing public scientific papers. I believe each of the following statements is a solid fact, backed up by a citation.

I also want to say that I understand some people are worried about blame being cast for this outbreak. Obviously we are all in this together, and my intention here is not to cast blame. These links overwhelmingly compel further scrutiny, but are not conclusive.

I do think however that information is being downplayed and suppressed by some scientists and media outlets and it’s our duty to find out the facts about this virus, do what we can to mitigate the outbreak, and prevent it from happening again.

Ready?…

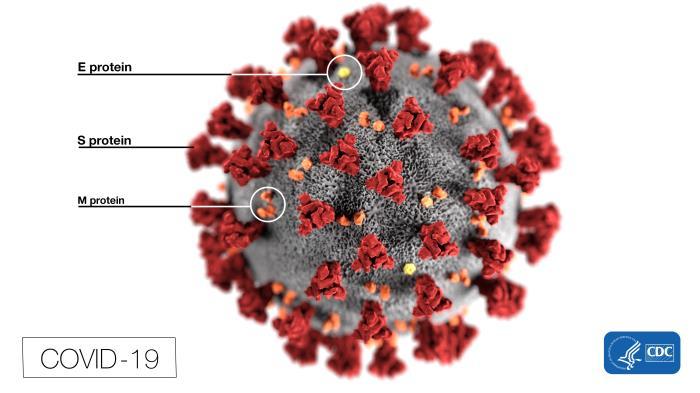

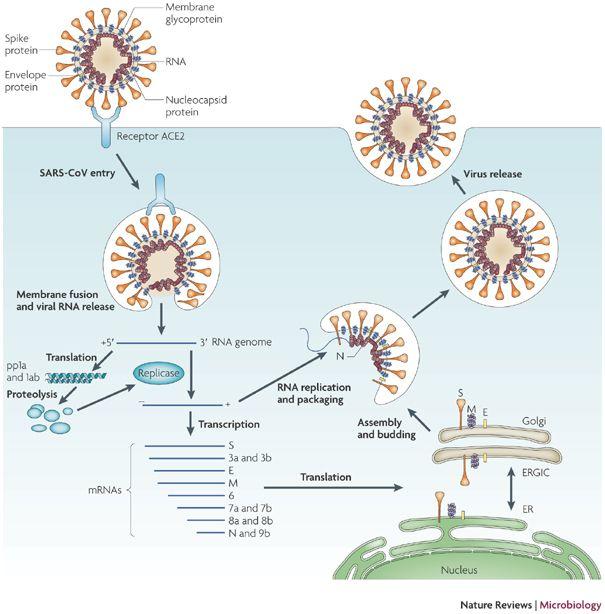

So there’s original SARS, which is a type of coronavirus. SARS infects cells through the ACE2 receptor in hosts.

The S spike protein plays a key role in how the virus infects cells. Each of the little spikes that surround the coronavirus is a spike protein (or S protein). That’s what gives the coronavirus it’s name – it’s “crown” of these spikes.

The S protein binds to the targeted cell through the ACE2 receptor, and boom, your cell is infected and becomes a virus replication factory.

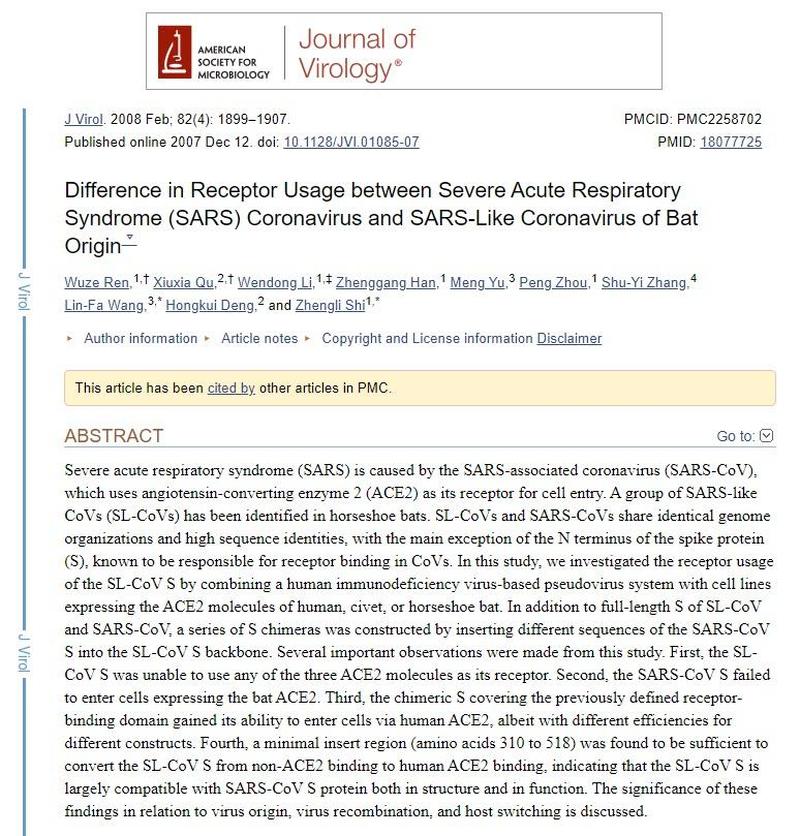

After the first SARS outbreak, there was a “land rush” to find other coronaviruses. A collection of SARS-*like* coronaviruses was isolated in several horseshoe bat species over 10 years ago, called SARS-like CoVs, or SL-CoVs. Not SARS exactly, but coronaviruses similar to SARS.

In 2007, a team of researchers based in Wuhan, in conjunction with an Australian laboratory, conducted a study with SARS, a SARS-like coronavirus, and HIV-1.

The researchers noted that if small changes were made to the S protein, it broke how SARS-CoV worked – it could no longer go in via ACE2. So they inferred the S protein was critical to the SARS attack vector.

They also predicted based on the S-ACE2 binding structure, that SARS-like CoVs were not able to use this same attack method (ACE2 mediation).

They decided to create a pseudovirus where they essentially put a SARS-like CoV in a HIV envelope.

It worked.

Using an HIV envelope, they replaced the RBD (receptor binding domain) of SL-CoV with that of SARS-CoV, and used it to successfully infect bats through ACE2 mediation.

12 years goes by…

A SARS-like CoV begins sweeping the globe that is far more infectious than previous outbreaks.

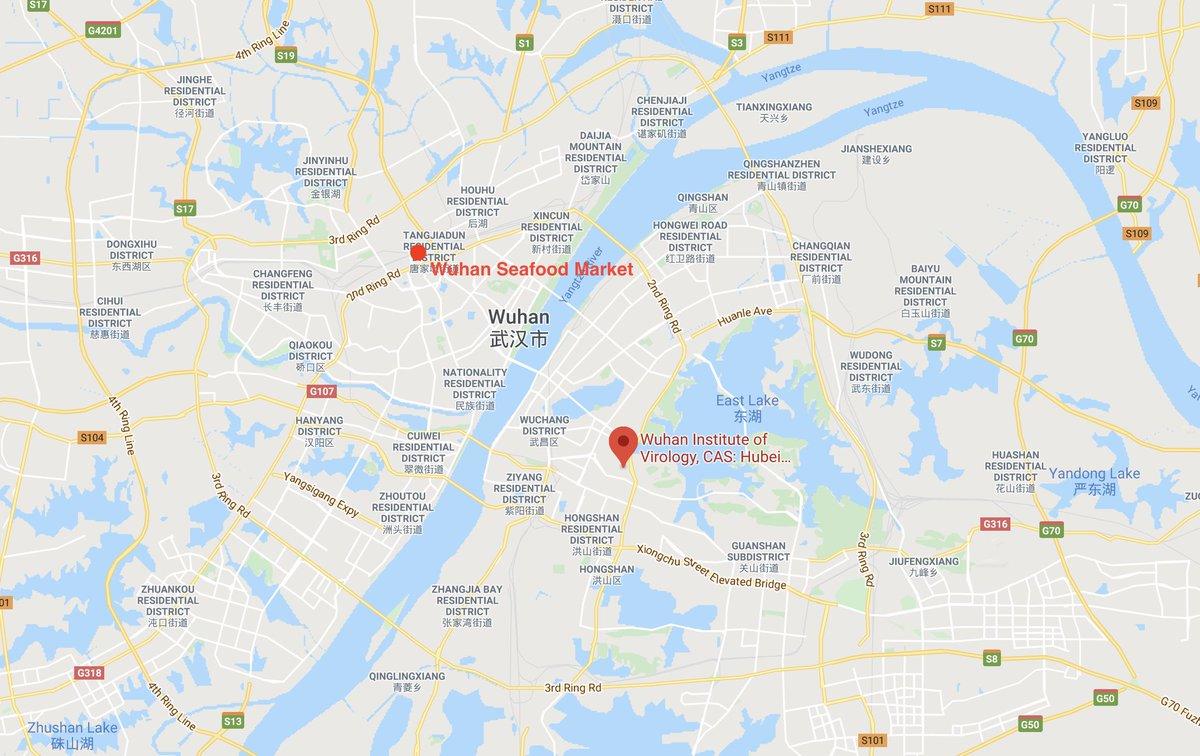

Ground Zero for this outbreak (not first human patient, but first spreading event) is considered to be Wuhan Seafood Market.

Wuhan Seafood Market is 20 miles from the National Biosafety Laboratory at Wuhan Institute of Virology.

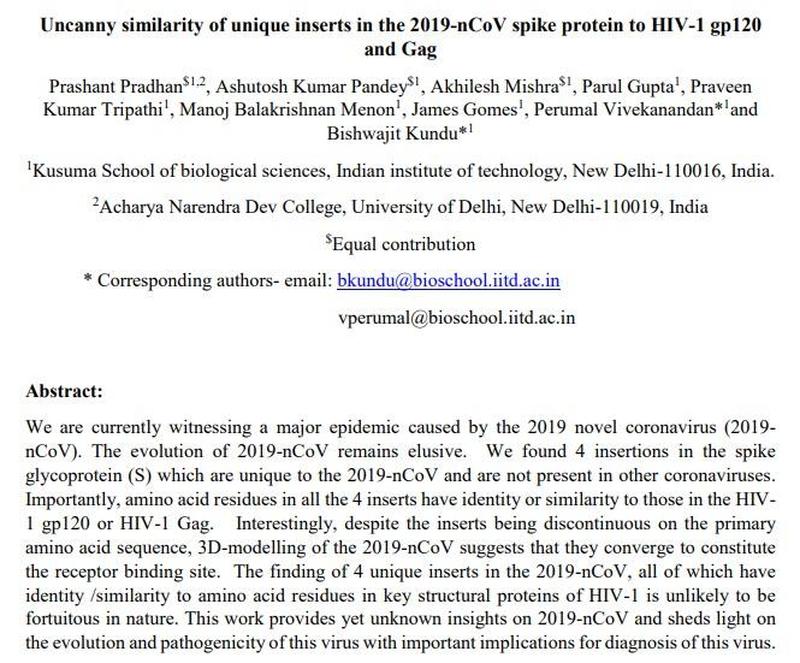

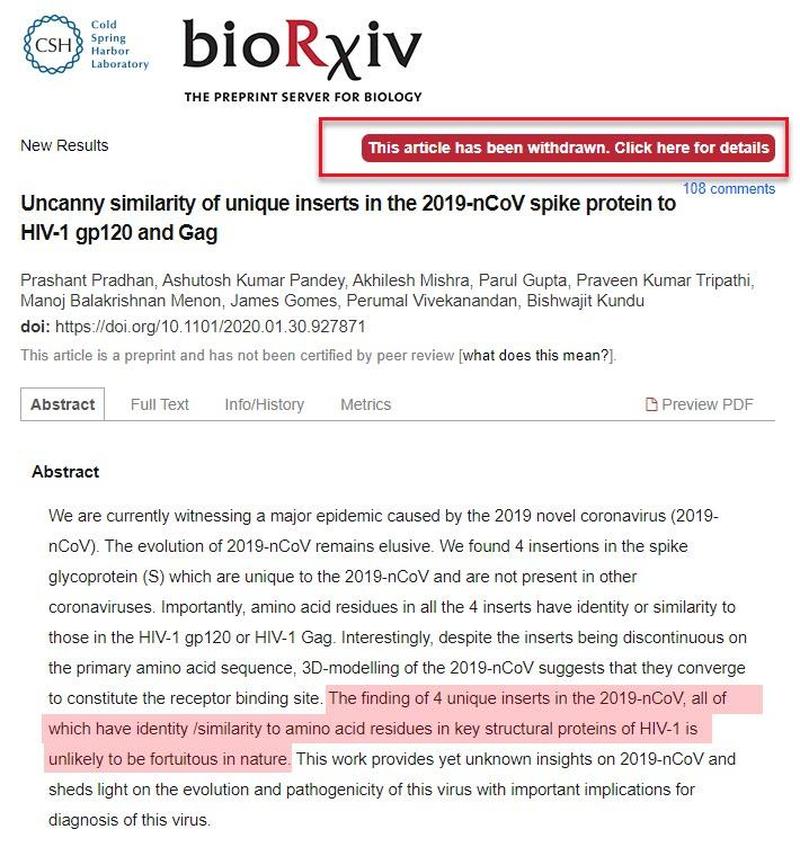

Amidst the outbreak, a team of Indian bioinformatics specialists at Delhi University released a paper pre-print…

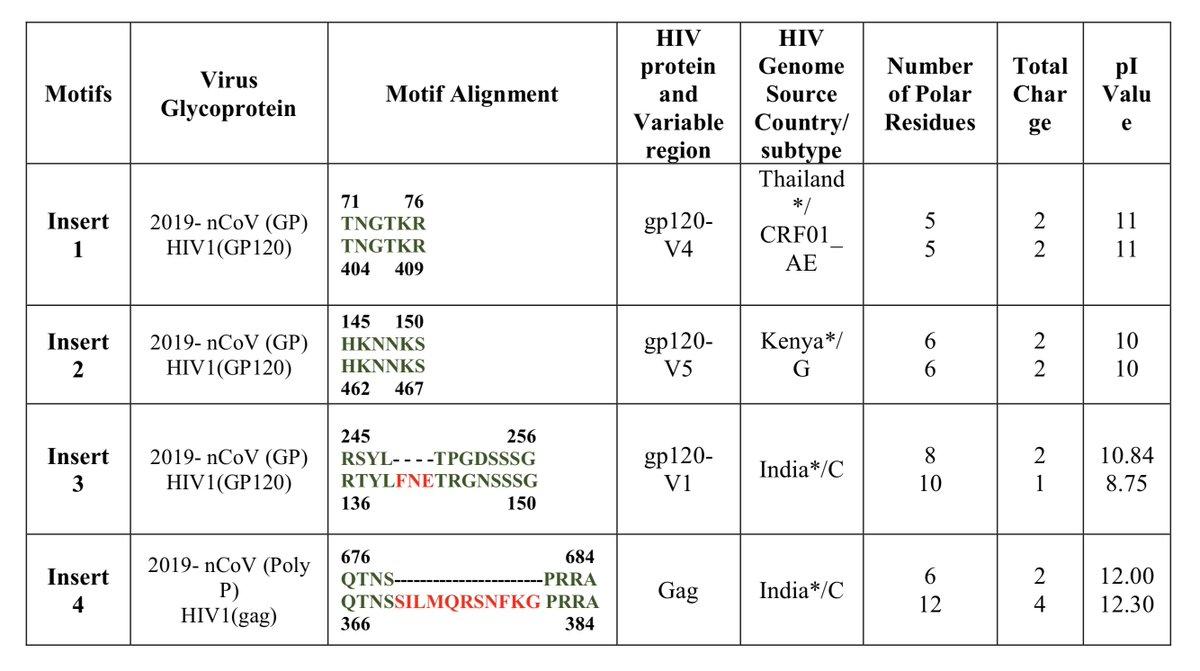

COVID-19 has a unique sequence about 1,378 nucleotide base pairs long that is not found in related coronaviruses. They claimed to identify genetic similarities in this unique material between COVID-19 and HIV-1.

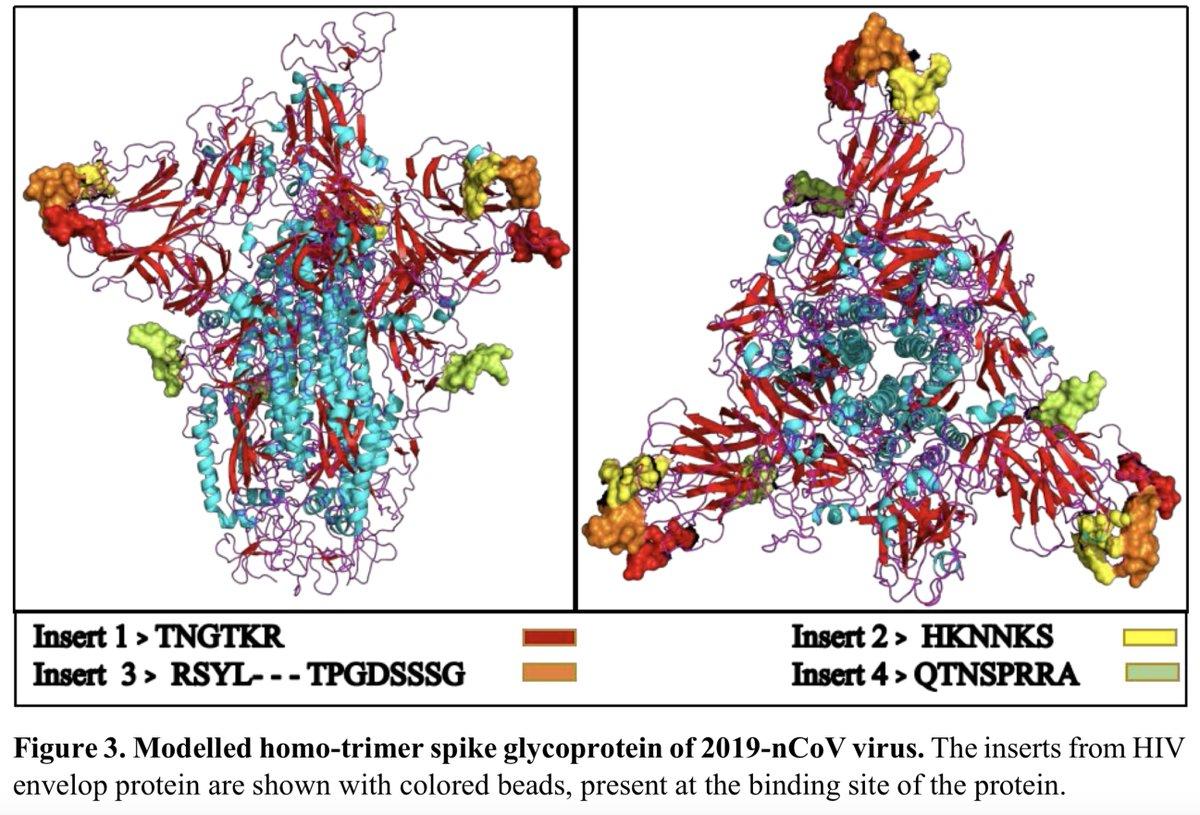

Specifically, they isolated 4 short genetic sequences in key protein structures (the receptor binding domain, or RBD).

Two of the sequences were perfect matches (albeit, short), and two of the sequences were matched but each with an additional string of non-matching material appearing in the middle of the sequence.

The paper was criticized and numerous attempts have been made to debunk it. After the criticism, the authors voluntarily withdrew it, intending to revise it based on comments made about their technical approach and conclusions.

One key debunking attempt claims this:

The same sequences are found in a variant called BetaCoV/bat/Yunnan/RaTG13/2013, which had been found “in the wild” in bats.

This is an attempt to prove that it was not engineered, but mutated naturally in the wild.

But there’s a problem…

This strain was only known by and studied at the Wuhan Virology Institute, and although they claim it was discovered in 2013, it wasn’t published or shared with the scientific community until immediately after the Indian paper, on January 27, 2020.

The RatG13 strain publication and the HIV research paper from 2008 share an author.

I discovered this on my own by comparing the two papers and then quickly realized this scientist’s contact information was the information that ZeroHedge was suspended from Twitter for sharing.

Their article identifies this author in question including some contact information from the Wuhan Virology Institute web site.

You can read the public comments and discussion of the original paper here:

There is a line of inquiry about how the sequences are remarkably stable in between the “bat” CoV and the nCoV, where in nature they would likely have mutated in between their shared evolution. Also a call for greater scientific evidence that the strain was collected in the wild.

Here is the only point in this thread where I will offer my opinion rather than a list of facts: In light of all the previous facts, the efforts to debunk the paper are not yet convincing in my view.

The RaTG13 paper makes the claim that, oh, that HIV-related material you identified that happens to protein fold to become a perfect attack vector for nCoV to attack ACE2?

It’s a relative of this other secret virus which came from the wild which we forgot to tell the scientific community about until now for no reason.

Here’s the secret virus – it came from bats – and here’s the new virus, see, they have the same HIV-related sequences… so… bats!

Totally not secret pathogen research which escaped the lab.

What are the odds that a SARS-like coronavirus with overlapping genetics from HIV mutated and crossed over into humans, next door to a laboratory which had been enhancing coronavirus with HIV for over a decade? And conversely, what are the odds it leaked out of the laboratory?

* * *

Finally, there is a great thread here by Trevor Bedford (@trvrb) examining the evidence for and against, with key replies challenging the conclusions made as well.

There is a nice “Bayesian” way to compare theories and think about evidence. I’m showing the probability of observing the data at hand given different theories. We want to compare the likelihood of observing this data, compared to other outcomes consistent with a theory. 3/21 pic.twitter.com/HaiNvCVxUo

Let’s learn! What do you think? Maybe I’m wrong! Can anyone disprove any of the links in the chain above? One thing is for sure, the science behind all this is fascinating.

But we need to make sure that if viruses are being secretly developed and accidentally released, that we learn about that and do our best to make sure it doesn’t happen again. @jonhoye@r_h_ebright@batresearch@nemopublius@JJ2000426