Global Carmageddon Continues: Pirelli And VW Warn About “Worsening Market Scenario”

The automotive industry has been mired in recession for the better part of the last 18 months and still shows no signs of stopping. On Tuesday, comments from both VW’s CEO and from tire maker Pirelli, who cut its guidance for 2020, continue to exemplify an industry where the very worst of a recession may still be yet to come.

VW’s CEO said in an interview with Bloomberg early this week that he was cautious about “all regions except South America”, including major car markets like North America, Europe and China.

“We know what needs to be done – get our act together on vehicle launches and be very cautious on costs and expenses,” he commented. He also stated that he wasn’t surprised that PSA and Fiat Chrysler are in merger talks, given speculation about industry consolidation.

Volkswagen is expected to present a new five-year plan to its board in mid-November.

The shift to electric vehicles, more stringent emissions standards and a slowing global economy all continue to weigh on many auto manufacturers.

Tire maker Pirelli also warned about its operating profit margin and cash flow on Tuesday, saying it would delay the presentation of a new business plan while it works out scenarios for what it sees as a “worsening market scenario”, according to Reuters.

The company forecasted full year margin on adjusted EBIT of between 17% and 17.5%, much lower than already-lowered expectations of 18% to 19%. The company’s adjusted EBIT fell to 685 million euros for the nine months ended September 30, 2019. Pirelli also lowered its full year cash flow expectations to between 330 and 350 million euros, down from expectations of between 350 million and 380 million euros.

The company said that greater fixed costs and lowered production to reduce inventories both stung its guidance.

The company is set to present its industrial plans to 2022 in the first quarter of next year. This presentation was previously supposed to occur on December 11 of this year. Pirelli said the setback was due to the market being “more challenging compared with the forecasts of recent months”.

Chief Executive Marco Tronchetti Porvera said: “In this context, to protect our profitability we have to act deeper to reduce the cost of our products.”

You wouldn’t know it from today’s news headlines, but there’s a major scandal unfolding with potentially far-reaching consequences for the entire international community.

The political/media class has been dead silent about the fact that there are now two whistleblowers whose revelations have cast serious doubts on a chemical weapons watchdog group that is widely regarded as authoritative, despite the fact that this same political/media class has been crowing all month about how important whistleblowers are and how they need to be protected ever since a CIA spook exposed some dirt on the Trump administration.

When the Courage Foundation and WikiLeaks published the findings of an interdisciplinary panel which received an extensive presentation from a whistleblower from the Organization for the Prohibition of Chemical Weapons (OPCW) investigation of an alleged 2018 chlorine gas attack in Douma, Syria, it was left unclear (perhaps intentionally) whether this was the same whistleblower who leaked a dissenting Engineering Assessment to the Working Group on Syria, Propaganda and Media this past May or a different one. Subsequent comments from British journalist Jonathan Steele assert that there are indeed two separate whistleblowers from within the OPCW’s Douma investigation, both of whom claim that their investigative findings differed widely from the final OPCW Douma report and were suppressed from the public by the organization.

The official final report aligned with the mainstream narrative promulgated by America’s political/media class that the Syrian government killed dozens of civilians in Douma using cylinders of chlorine gas dropped from the air, while the two whistleblowers found that this is unlikely to have been the case. The official report did not explicitly assign blame to Assad, but it said its findings were in alignment with a chlorine gas attack and included a ballistics report which strongly implied an air strike (opposition fighters in Syria have no air force). The whistleblowers dispute both of these conclusions.

The drip-drip of revelations continues. Now a *second* whistleblower has come forward to say the OPCW concealed their findings clearing the Assad government of responsibility for an alleged chemical weapons attack in Douma last year https://t.co/HqnlvFYdBh

At the very least we can conclude from these revelations that the OPCW hid information from the public that an international watchdog organization has no business hiding about an event which led to an act of war in the form of an airstrike by the US, UK and France. We may also conclude that skepticism of their entire body of work around the world is perfectly legitimate until some very serious questions are answered. Right now no attempt is being made by the organization to bring about the kind of transparency which would help restore trust, with multiple journalists now reporting that the OPCW is refusing to answer their questions.

It is also not at all unreasonable to question whether the OPCW could have been influenced in some way by the United States behind the scenes, given how its now-dubious final report aligns so nicely with the narratives promoted by the CIA and US State Department, and given how we know for a fact that the US has aggressively manipulated the OPCW before in order to advance its regime change agendas.

In June of 2002, as the United States was preparing to invade Iraq, Mother Jones published an article titled “A Coup in The Hague” about the US government’s campaign to oust the OPCW’s very first Director General, José Bustani. If you’ve been following the recent OPCW revelations you will recall that Bustani was one of the panelists at the Courage Foundation whistleblower presentation in Brussels on October 15, after which he wrote the following:

“The convincing evidence of irregular behavior in the OPCW investigation of the alleged Douma chemical attack confirms doubts and suspicions I already had. I could make no sense of what I was reading in the international press. Even official reports of investigations seemed incoherent at best. The picture is certainly clearer now, although very disturbing.”

Mother Jones (which used to be a decent outlet for the record) breaks down how the US government was able to successfully bully the OPCW into ousting the very popular Bustani from his position as Director General in April 2002 by threatening to withdraw funding from the organization. This was done because Bustani was having an uncomfortable amount of success bringing the Saddam Hussein government to the negotiating table, and his efforts were perceived as a threat to the war agenda.

Friendly reminder that we know the USA has threatened to kill OPCW funding as leverage to achieve strategic goals. During the Bush administration it was to remove OPCW Director General Jose Bustani because he was interfering with the Iraq war agenda.https://t.co/757YaCLBZGpic.twitter.com/9rt3wXkA4e

“Indeed, US officials have offered little reason for its opposition to Bustani, saying only that they questioned his ‘management style’ and differed with several of Bustani’s decisions,” Mother Jones reports.

“Despite this, Washington waged an unusually public and vocal campaign to unseat Bustani, who had been unanimously reelected to lead the 145-nation body in May, 2000. Finally, at a ‘special session’ called after the US had threatened to cut off all funding for the organization, Bustani was sent packing.”

This happened despite broad international support for Bustani, including from then-Secretary of State Colin Powell who’d written to the renowned Brazilian diplomat praising his work in February 2001. According to the report’s author Hannah Wallace, the US was able to oust a unanimously re-elected Director General due to the disproportionate amount of financial influence America had over the OPCW.

“[I]n March of 2002, Bustani survived a US-led motion calling for a vote of no confidence in his leadership,” Wallace writes. “Having failed in that effort, Washington increased the pressure, threatening to cut off funding for the organization — a significant threat given that the US underwrites 22 percent of the total budget. A little more than a month later, Bustani was out.”

“Bustani suggests US officials were particularly displeased with his attempts to persuade Iraq to sign the chemical weapons treaty, which would have provided for routine and unannounced inspections of Iraqi weapons plants,” Wallace reported. “Of course, the Bush White House has recently cited Iraq’s refusal to allow such inspections as one justification for a new attack on Saddam Hussein’s regime.”

“Of course, had Iraq [joined the OPCW], a door would be opened towards the return of inspectors to Bagdad and consequently a viable, peaceful solution to the impasse,” Bustani told Mother Jones. “Is that what Washington wants these days?”

Panel Finds Gaping Holes in OPCW Report on Alleged Syrian Chemical Attack https://t.co/BIMiz4J3eH

Bustani told Mother Jones that he was already seeing a shift in the OPCW into alignment with US interests. Again, this was back in 2002.

“The new OPCW, after my ousting, is already undergoing radical structural changes, along the lines of the US recipe, which will strike a definitive blow to the post of the Director General, making it once and for all a mere figurehead of a sham international regime,” he said.

“Bustani traces the shift to the influence of several hawkish officials in the Bush State Department, particularly Undersecretary of State for Arms Control and International Security, John Bolton,” Wallace wrote.

Indeed, we’ve learned since that Bolton took it much further than that. Bustani reported to The Intercept last year that Bolton literally threatened to harm his children if he didn’t resign from his position as Director General.

“You have 24 hours to leave the organization, and if you don’t comply with this decision by Washington, we have ways to retaliate against you,” Bolton reportedly told him, adding after a pause, “We know where your kids live. You have two sons in New York.”

The Intercept reports that Bolton’s office did not deny Bustani’s claim when asked for comment.

It is worth noting here that John Bolton was serving in the Trump administration as National Security Advisor throughout the entire time of the OPCW’s Douma investigation. Bolton held that position from April 9, 2018 to September 10, 2019. The OPCW’s Fact-Finding mission didn’t arrive in Syria until April 14 2018 and didn’t begin its investigation in Douma until several days after that, with its final report being released in March of 2019.

“We Know Where Your Kids Live” John Bolton threatened head of chemical weapons commission as part of effort launch war against Iraq https://t.co/p8uluxbWGH

It is perfectly reasonable, given all this, to suspect that the US government may have exerted some influence over the OPCW’s Douma investigation. If they were depraved enough to not only threaten to withdraw funding from a chemical weapons watchdog in order to attain their warmongering agendas but actually threaten a diplomat’s family, they’re certainly depraved enough to manipulate an investigation into an alleged chemical weapons attack. This would explain the highly suspicious omissions and discrepancies in its report.

It is a well-established fact that the US government has long sought regime change in Syria, not just in 2012 with Timber Sycamore and the official position of “Assad must go”, but even before the violence began in 2011. I’ve compiled multiple primary source pieces of evidence in an article you can read by clicking here that the US government and its allies have been planning to orchestrate an uprising in Syria exactly as it occurred with the goal of toppling Assad, and a former Qatari Prime Minister revealed on television in 2017 that the US and its allies were involved in that conflict from the very moment it first started.

So to recap, we know that the US government has manipulated the OPCW in order to advance regime change agendas in the past, and we know that the US government has long had a regime change agenda against Syria. Many questions will need to be answered before we can rule out the possibility that these two facts converged in an ugly way upon the OPCW’s Douma investigation.

A Conflicted Kimbal Musk Was Facing SolarCity Margin Calls Before Tesla’s Bailout, Deposition Shows

More and more details to Tesla’s bailout of SolarCity are becoming clear. And the more details we get, the uglier things look.

The latest addition to the story was yesterday, when one well known Tesla skeptic took the time to lay out, in wonderful detail, the financial pressure that SolarCity’s tanking stock price was putting on the company’s directors – specifically, Elon’s brother Kimbal Musk – who faced multiple margin calls prior to the merger.

Using Kimbal Musk’s recently released deposition from the SolarCity lawsuit, the short seller known only as @TeslaCharts on Twitter, reconstructed the days leading up to Elon Musk pitching the SolarCity acquisition to the Tesla board. They detail a panicked Kimbal Musk, cursing about Tesla and blowing out his SpaceX shares to cover his SolarCity margin call – all while maintaining that he had zero conflict of interest in Tesla’s eventual bailout of SolarCity.

@TeslaCharts starts by layout out the context, reminding readers that Kimbal Musk was a large shareholder in SolarCity, as well as a board member of both Tesla and SpaceX at the time.

2/ A friendly reminder. At the time $TSLA is considering acquiring SolarCity, Kimbal is:

*A very large shareholder of SolarCity

*On the board of Tesla

*On the board of SpaceX

*CEO of The Kitchen

He is also Elon’s brother and cousin to Lyndon Rive, the CEO of SolarCity. $TSLAQ

He then makes note of Kimbal’s reasoning for not recusing himself regarding matters involving SolarCity. The only person who didn’t seem to think Kimbal had a conflict of interest was Kimbal himself.

3/ The attorney, who does a brilliant job, begins by asking Kimbal about why he didn’t recuse himself from the SolarCity deliberations. He also mentions the $TSLA code of conduct. Kimbal doesn’t know much about the code, but quickly denies he has a conflict of interest. $TSLAQpic.twitter.com/woG0uhHcL9

4/ Using Kimbal’s logic, it is impossible to have a conflict of interest as long as you are ‘representing the interests of Tesla shareholders’. $TSLAQpic.twitter.com/g8eFrXfFMA

He continues down this line of logic, noting that despite owning 141,541 shares of SolarCity, Kimbal still did not think he had a conflict of interest because he was representing “the best interests of the shareholders of Tesla”.

5/ Apparently, owning several million dollars worth of stock in a company you are considering acquiring is not a conflict of interest in Kimbal’s mind. $TSLAQpic.twitter.com/JuGh8waZrm

From there, @TeslaCharts starts to lay out a timeline. First, October 20, 2015, when Kimbal is facing a margin call due to SolarCity for the first time.

6/ On October 20th, 2015, SolarCity stock is starting to fall, and Kimbal is facing a potential margin call. He is asking Elon for a loan or considering selling SpaceX stock. He knows he is going to sell some $TSLA stock in November via his predetermined 10b5-1 plan. $TSLAQpic.twitter.com/nmJt2I0bpp

He then also lays out that many members of the Tesla and SolarCity boards are also on the Board of Directors of Kimbal’s company, the Kitchen.

7/ The SolarCity stock decline comes at a bad time for Kimbal. He is in the middle of a raise for his true passion, The Kitchen. Turns out, many members of the SolarCity and $TSLA boards are also investors in The Kitchen. No conflict there, right? $TSLAQpic.twitter.com/bhmX4fElfW

In fact, when Kimbal is seeking financing for his own company, SolarCity’s CEO tells him that he can’t participate because he is also facing his own margin calls. SolarCity is “seeing its ass”, CEO Lyndon Rive tells Kimbal. Of course, “seeing its ass” doesn’t appear in any SolarCity public filings around that time – this was information just for Kimbal.

8/ We are still on October 20, 2015. The CEO of SolarCity regretfully informs Kimbal that he can’t participate in this funding round of The Kitchen. Why? He has his own margin loans to worry about, of course! “SolarCity is seeing its ass” – didn’t see that in any filings. $TSLAQpic.twitter.com/2nsUPj5ysk

Then Kimbal winds up in a back and forth with the questioning attorney about the definition of a margin call, which he clearly doesn’t understand. The deposition shows that Kimbal used his Tesla line of credit to cover his SolarCity line – symbolic, of sorts, isn’t it?

9/ Apparently, Kimbal doesn’t know the definition of a margin call. Just because you can meet that call doesn’t mean it didn’t happen. Surreal. Oh, and he uses his $TSLA line to cover his SolarCity line often. He is keenly interested in the price of both stocks. $TSLAQpic.twitter.com/n6utsAONIs

Kimbal then faces a margin call on October 29, 2015 and uses his Tesla stock to again cover it.

10/ Having just testified that he doubted ever receiving a margin call, we find out that on October 29, 2015, Kimbal gets a margin call from Morgan Stanley. His loan collateralized by pledged $TSLA stock comes to the rescue again. $TSLAQpic.twitter.com/QGQcillK6A

Kimbal is then rebuffed by Elon after he hits Elon up for a loan to try and bail himself out of his margin call. “You know that I don’t actually have cash, right?” Elon says to his brother.

11/ Apparently Elon isn’t happy about being hit up for a loan by his brother. I can understand that. Pesky family members and all. Interesting that Elon had no cash all the way back in the fall of 2015. Kimbal better sell some SpaceX, I guess. pic.twitter.com/jk2gU0RKg8

So Kimbal shifts his attention to potentially selling some of his SpaceX stock to cover the call. It is also noted that Elon Musk had a LTV of just 5% for his SpaceX shares at Goldman.

12/ But Kimbal doesn’t want to sell his SpaceX stock. Why? Because stocks always go up and to the right. Maybe a pledged loan of his SpaceX shares? Elon only got a loan-to-value of 5% at Goldman for his SpaceX stock. I believe this is the first confirmation of that fact. $TSLAQpic.twitter.com/8Rz1e46dUn

By February 8, 2016, all hell is breaking loose. SolarCity’s stock is still falling and Kimbal is forced to offer some SpaceX stock at $110.

13/ On February 8, 2016, the SolarCity stock price is still cratering, and the margins calls are piling up. Time to sell some SpaceX at $110 a share. Is Elon getting margin calls too? Unclear. $TSLAQpic.twitter.com/no3x8YFPDm

On February 9, 2016, there’s a clear sense of urgency when SolarCity dips to $18 per share. Kimbal yanks the offer on his SpaceX stock from $110 to $95 over the course of just one day.

14/ Things get way worse on February 9, 2016. SolarCity dives to $18 a share. Kimbal is in deep now. Reduces his asking price on SpaceX shares to $95. Deep margin calls coming. What do Elon’s loans look like? $TSLAQpic.twitter.com/kIJx56eCxB

Kimbal then, frustrated, e-mails the CFO of his company, the Kitchen. “Motherfucker,” he says after describing Tesla’s 50% fall.

15/ Later on February 9th, Kimbal emails his frustrations to the CFO of The Kitchen. The $TSLA and SolarCity stock prices are stressing him out. $TSLAQpic.twitter.com/f7tKMz7nrq

So the next day, his brother Elon goes online and pulls forward the date for Model 3 reservations, announcing that more information on the unveil would be coming soon. Tesla stock moves higher and “margin loan pressure undoubtedly eases,” @TeslaCharts says.

16/ In the mother of all coincidences, the VERY NEXT DAY, Elon takes to twitter, surprises his team, and pulls forward the Model 3. The $TSLA stock price roars, margins loan pressure undoubtedly eases, and all is good for now. $TSLAQpic.twitter.com/ARu0IAjsRH

And just two weeks later, Elon calls a meeting to pitch the idea of acquiring SolarCity. To nobody’s surprise, the Board doesn’t even discuss Kimbal Musk’s potential conflict of interest.

17/ Fast forward two weeks later. Elon calls a special meeting of the $TSLA board on February 29, 2016, to press for the SolarCity acquisition. Does Kimbal recuse himself? No. Get this. THE BOARD DOESN’T EVEN DISCUSS HIS OBVIOUS CONFLICTS!!!!!!! $TSLAQpic.twitter.com/Ue12sUWgKr

The thread ends with @TeslaCharts saying what everyone else is thinking:

“The only thing surprising about this giant self-dealing Ponzi scheme is just how egregious it all is.”

The thread, in its entirety, can be read here. @TeslaCharts also appeared on a podcast on Sunday to lay out his thoughts both on Tesla’s recent quarterly results, and on the company’s claims about its “Version 3.0” of its solar roof tiles.

Recall, we noted yesterday that despite the company’s “headline” Q3 numbers, its U.S. sales actually plunged 39% in the quarter.

Chinese PMIs Unexpectedly Slide Further Into Contraction, Just Shy Of Post-Crisis Lows

If there was some hope that that today’s Fed rate cut would mark the bottom of the global economic slowdown and serve as the basis for even a modest recovery – after all, even Powell admitted that after this, nothing less than a full blown economic shitstorm would force the Fed to cut more – then Beijing promptly crapped all over any such optimism, when it reported that its latest official PMIs for the month of October not only missed by a mile, but were two of the worst prints since the financial crisis.

Early on Thursday, China’s National Bureau of Statistics reported that in October, China’s manufacturing PMI slumped deeper into contraction, dropping from 49.8 to 49.3, not only below the 49.8 consensus estimate, but also below the lowest sellside estimate (the range was 49.5-50.5). Worse, the Non-manufacturing PMI, which many had ignored for months because it was so deeply into expansionary territory, tumbled sharply, and after its biggest drop in almost a year, dipped to 52.8 from 53.6, and is now just shy of the lowest print since the financial crisis.

It gets even worse: whereas the contraction for large cap companies was modest, at just 49.9, down from 50.8, mid cap companies were worse, at 49.0, while small caps were dismal, at a paltry 47.9, down from 48.8.

Broken down by components, almost every index posted a decline, with the exception of the worst one, employment, which posted a modest increase:

Production 50.8, down from 52.3

New Orders 49.6, down from 50.5

Employment 47.3, up from 47.0

The above means that not only is the trade war with the US continuing to take its toll on China, but as long as Beijing refuses to spark a massive credit injection spree, which rebooted the global economy after the financial crisis, after the European sovereign debt crisis, and again after the Shanghai Accord…

… then the Fed’s hopes that its “insurance cuts” will amount to anything, will soon be drowned in the chaos of another global recession, but not before the Fed first cuts rates back to zero first, and then negative.

Killing Me Softly with Militarism – The Decay of Democracy in America

When Americans think of militarism, they may imagine jackbooted soldiers goose-stepping through the streets as flag-waving crowds exult; or, like our president, they may think of enormous parades featuring troops and missiles and tanks, with warplanes soaring overhead. Or nationalist dictators wearing military uniforms encrusted with medals, ribbons, and badges like so many barnacles on a sinking ship of state. (Was Donald Trump only joking recently when he said he’d like to award himself a Medal of Honor?) And what they may also think is: that’s not us. That’s not America. After all, Lady Liberty used to welcome newcomers with a torch, not an AR-15. We don’t wall ourselves in while bombing others in distant parts of the world, right?

But militarism is more than thuggish dictators, predatory weaponry, and steely-eyed troops. There are softer forms of it that are no less significant than the “hard” ones. In fact, in a self-avowed democracy like the United States, such softer forms are often more effective because they seem so much less insidious, so much less dangerous. Even in the heartland of Trump’s famed base, most Americans continue to reject nakedly bellicose displays like phalanxes of tanks rolling down Pennsylvania Avenue.

But who can object to celebrating “hometown heroes” in uniform, as happens regularly at sports events of every sort in twenty-first-century America? Or polite and smiling military recruiters in schools? Or gung-ho war movies like the latest version of Midway, timed for Veterans Day weekend 2019 and marking America’s 1942 naval victory over Japan, when we were not only the good guys but the underdogs?

What do I mean by softer forms of militarism? I’m a football fan, so one recent Sunday afternoon found me watching an NFL game on CBS. People deplore violence in such games, and rightly so, given the number of injuries among the players, notably concussions that debilitate lives. But what about violent commercials during the game? In that one afternoon, I noted repetitive commercials for SEAL Team, SWAT, and FBI, all CBS shows from this quietly militarized American moment of ours. In other words, I was exposed to lots of guns, explosions, fisticuffs, and the like, but more than anything I was given glimpses of hard men (and a woman or two) in uniform who have the very answers we need and, like the Pentagon-supplied police in Ferguson, Missouri, in 2014, are armed to the teeth. (“Models with guns,” my wife calls them.)

Got a situation in Nowhere-stan? Send in the Navy SEALs. Got a murderer on the loose? Send in the SWAT team. With their superior weaponry and can-do spirit, Special Forces of every sort are sure to win the day (except, of course, when they don’t, as in America’s current series of never-ending wars in distant lands).

And it hardly ends with those three shows. Consider, for example, this century’s update of Magnum P.I., a CBS show featuring a kickass private investigator. In the original Magnum P.I. that I watched as a teenager, Tom Selleck played the character with an easy charm. Magnum’s military background in Vietnam was acknowledged but not hyped. Unsurprisingly, today’s Magnum is proudly billed as an ex-Navy SEAL.

Cop and military shows are nothing new on American TV, but never have I seen so many of them, new and old, and so well-armed. On CBS alone you can add to the mix Hawaii Five-O (yet more models with guns updated and up-armed from my youthful years), the three NCIS (Naval Criminal Investigative Service) shows, and Blue Bloods (ironically starring a more grizzled and less charming Tom Selleck) — and who knows what I haven’t noticed? While today’s cop/military shows feature far more diversity with respect to gender, ethnicity, and race compared to hoary classics like Dragnet, they also feature far more gunplay and other forms of bloody violence.

Look, as a veteran, I have nothing against realistic shows on the military. Coming from a family of first responders — I count four firefighters and two police officers in my immediate family — I loved shows like Adam-12 and Emergency! in my youth. What I’m against is the strange militarization of everything, including, for instance, the idea, distinctly of our moment, that first responders need their very own version of the American flag to mark their service. Perhaps you’ve seen those thin blue line flags, sometimes augmented with a red line for firefighters. As a military veteran, my gut tells me that there should only be one American flag and it should be good enough for all Americans. Think of the proliferation of flags as another soft type of up-armoring (this time of patriotism).

Speaking of which, whatever happened to Dragnet’s Sergeant Joe Friday, on the beat, serving his fellow citizens, and pursuing law enforcement as a calling? He didn’t need a thin blue line battle flag. And in the rare times when he wielded a gun, it was .38 Special. Today’s version of Joe looks a lot more like G.I. Joe, decked out in body armor and carrying an assault rifle as he exits a tank-like vehicle, maybe even a surplus MRAP from America’s failed imperial wars.

Militarism in the USA

Besides TV shows, movies, and commercials, there are many signs of the increasing embrace of militarized values and attitudes in this country. The result: the acceptance of a military in places where it shouldn’t be, one that’s over-celebrated, over-hyped, and given far too much money and cultural authority, while becoming virtually immune to serious criticism.

Let me offer just nine signs of this that would have been so much less conceivable when I was a young boy watching reruns of Dragnet:

1. Roughly two-thirds of the federal government’s discretionary budget for 2020 will, unbelievably enough, be devoted to the Pentagon and related military functions, with each year’s “defense” budget coming ever closer to a trillion dollars. Such colossal sums are rarely debated in Congress; indeed, they enjoy wide bipartisan support.

2. The U.S. military remains the most trusted institution in our society, so say 74% of Americans surveyed in a Gallup poll. No other institution even comes close, certainly not the presidency (37%) or Congress (which recently rose to a monumental 25% on an impeachment high). Yet that same military has produced disasters or quagmires in Afghanistan, Iraq, Libya, Syria, Somalia, and elsewhere. Various “surges” have repeatedly failed. The Pentagon itself can’t even pass an audit. Why so much trust?

3. A state of permanent war is considered America’s new normal. Wars are now automatically treated as multi-generational with little concern for how permawar might degrade our democracy. Anti-war protesters are rare enough to be lone voices crying in the wilderness.

4. America’s generals continue to be treated, without the slightest irony, as “the adults in the room.” Sages like former Secretary of Defense James Mattis (cited glowingly in the recent debate among 12 Democratic presidential hopefuls) will save America from unskilled and tempestuous politicians like one Donald J. Trump. In the 2016 presidential race, it seemed that neither candidate could run without being endorsed by a screaming general (Michael Flynn for Trump; John Allen for Clinton).

5. The media routinely embraces retired U.S. military officers and uses them as talking heads to explain and promote military action to the American people. Simultaneously, when the military goes to war, civilian journalists are “embedded” within those forces and so are dependent on them in every way. The result tends to be a cheerleading media that supports the military in the name of patriotism — as well as higher ratings and corporate profits.

6. America’s foreign aid is increasingly military aid. Consider, for instance, the current controversy over the aid to Ukraine that President Trump blocked before his infamous phone call, which was, of course, partially about weaponry. This should serve to remind us that the United States has become the world’s foremost merchant of death, selling far more weapons globally than any other country. Again, there is no real debate here about the morality of profiting from such massive sales, whether abroad ($55.4 billion in arms sales for this fiscal year alone, says the Defense Security Cooperation Agency) or at home (a staggering 150 million new guns produced in the USA since 1986, the vast majority remaining in American hands).

7. In that context, consider the militarization of the weaponry in those very hands, from .50 caliber sniper rifles to various military-style assault rifles. Roughly 15 million AR-15s are currently owned by ordinary Americans. We’re talking about a gun designed for battlefield-style rapid shooting and maximum damage against humans. In the 1970s, when I was a teenager, the hunters in my family had bolt-action rifles for deer hunting, shotguns for birds, and pistols for home defense and plinking. No one had a military-style assault rifle because no one needed one or even wanted one. Now, worried suburbanites buy them, thinking they’re getting their “man card” back by toting such a weapon of mass destruction.

8. Paradoxically, even as Americans slaughter each other and themselves in large numbers via mass shootings and suicides (nearly 40,000 gun deaths in 2017 alone), they largely ignore Washington’s overseas wars and the continued bombing of numerous countries. But ignorance is not bliss. By tacitly giving the military a blank check, issued in the name of securing the homeland, Americans embrace that military, however loosely, and its misuse of violence across significant parts of the planet. Should it be any surprise that a country that kills so wantonly overseas over such a prolonged period would also experience mass shootings and other forms of violence at home?

9. Even as Americans “support our troops” and celebrate them as “heroes,” the military itself has taken on a new “warrior ethos” that would once — in the age of a draft army — have been contrary to this country’s citizen-soldier tradition, especially as articulated and exhibited by the “greatest generation” during World War II.

What these nine items add up to is a paradigm shift as well as a change in the zeitgeist. The U.S. military is no longer a tool that a democracy funds and uses reluctantly. It’s become an alleged force for good, a virtuous entity, a band of brothers (and sisters), America’s foremost missionaries overseas and most lovable and admired heroes at home. This embrace of the military is precisely what I would call soft militarism. Jackbooted troops may not be marching in our streets, but they increasingly seem to be marching unopposed through — and occupying — our minds.

The Decay of Democracy

As Americans embrace the military, less violent policy options are downplayed or disregarded. Consider the State Department, America’s diplomatic corps, now a tiny, increasingly defunded branch of the Pentagon led by Mike Pompeo (celebrated by Donald Trump as a tremendous leader because he did well at West Point). Consider President Trump as well, who’s been labeled an isolationist, and his stunning inability to truly withdraw troops or end wars. In Syria, U.S. troops were recently redeployed, not withdrawn, not from the region anyway, even as more troops are being sent to Saudi Arabia. In Afghanistan, Trump sent a few thousand more troops in 2017, his own modest version of a mini-surge and they’re still there, even as peace negotiations with the Taliban have been abandoned. That decision, in turn, led to a new surge (a “near record high”) in U.S. bombing in that country in September, naturally in the name of advancing peace. The result: yet higher levels of civilian deaths.

How did the U.S. increasingly come to reject diplomacy and democracy for militarism and proto-autocracy? Partly, I think, because of the absence of a military draft. Precisely because military service is voluntary, it can be valorized. It can be elevated as a calling that’s uniquely heroic and sacrificial. Even though most troops are drawn from the working class and volunteer for diverse reasons, their motivations and their imperfections can be ignored as politicians praise them to the rooftops. Related to this is the Rambo-like cult of the warrior and warrior ethos, now celebrated as something desirable in America. Such an ethos fits seamlessly with America’s generational wars. Unlike conflicted draftees, warriors exist solely to wage war. They are less likely to have the questioning attitude of the citizen-soldier.

Don’t get me wrong: reviving the draft isn’t the solution; reviving democracy is. We need the active involvement of informed citizens, especially resistance to endless wars and budget-busting spending on American weapons of mass destruction. The true cost of our previously soft (now possibly hardening) militarism isn’t seen only in this country’s quickening march toward a militarized authoritarianism. It can also be measured in the dead and wounded from our wars, including the dead, wounded, and displaced in distant lands. It can be seen as well in the rise of increasingly well-armed, self-avowed nationalists domestically who promise solutions via walls and weapons and “good guys” with guns. (“Shoot them in the legs,” Trump is alleged to have said about immigrants crossing America’s southern border illegally.)

Democracy shouldn’t be about celebrating overlords in uniform. A now-widely accepted belief is that America is more divided, more partisan than ever, approaching perhaps a new civil war, as echoed in the rhetoric of our current president. Small wonder that inflammatory rhetoric is thriving and the list of this country’s enemies lengthening when Americans themselves have so softly yet fervently embraced militarism.

With apologies to the great Roberta Flack, America is killing itself softly with war songs.

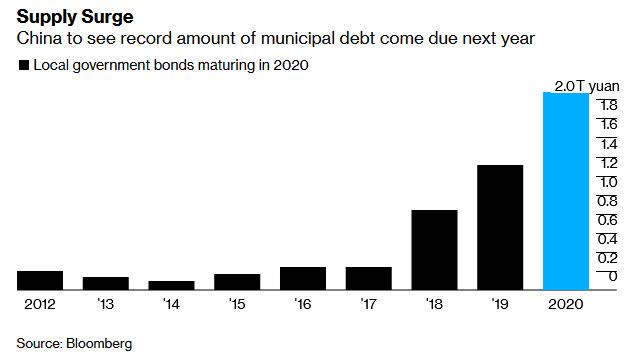

China’s Bond Market Faces Turmoil Amid Maturity Deluge

While the US bond market has had its share of harrowing slumps and vomit-inducing short squeezes in the past year as consensus shifted from one of “the neutral rate is far away” to “here comes NIRP”, China’s bonds have been a bastion of stability, trading in a tight range between 3% and 3.50% for the past year.

That may be about to change.

The reason: a wall of bond maturities is about to flood across China’s sovereign-bond market, which in the past three months has already been reeling from a global sell-off and rising inflation.

According to Bloomberg, more than 2 trillion yuan ($283 billion) of local-government notes will mature in 2020, a record and 58% more than this year’s level. This means fresh debt to refinance upcoming maturities will start hitting the market soon, with a the southern province of Guangdong expected to sell notes as early as November.

This is happening as China’s 10-year yield rose 3 basis points to 3.31%. the highest since late May, while the cost on 12-month interest rate swaps jumped 5 basis points to 2.92%. The yield on China Development Bank’s 3-year bonds due January 2022 rose 10 basis points to 3.25%.

Despite trading in a narrow range, China’s government bonds have been sliding for nearly two months, starting around the time a “growth shock” hit US rates and sparked the infamous quantastrophe, with the 10-year yield hitting the highest since May as selling momentum accelerated. Naturally, a flood of new supply will only exacerbate the weakness, especially as real, inflation-adjusted yields are barely above zero, a rarity for emerging markets.

“The large amount of supply that will be rolled over will weigh on China’s sovereign bonds,” Ken Cheung, chief Asia FX strategist at Mizuho Bank, told Bloomberg. The risk only grows when one considers the recent surge in food inflation as a result of “pig Ebola”, coupled with lower expectations of central bank stimulus.

To avoid a panic issuance scramble, Deputy Finance Minister Xu Hongcai said in September that China will grant part of a special bonds quota in advance to ensure that the funds raised can be used early in the year, Bloomberg reported, noting that so-called “special bonds have mostly been used for infrastructure spending, and the national limit could be raised from 2.15 trillion yuan.”

Earlier, in June, the State Council expanded the sectors that funds raised via the special bonds can be put toward. For 2020, they will include transport, energy, agriculture and forestry, vocational education and medical care. Overall fixed-asset investment has slowed this year amid pressure from the U.S. trade war.

Of course, there is only so much selling that the PBOC can take before it has to intervene, which is why so many China watchers have been stumped by the central bank’s lack of willingness to intervene so far.

Beijing’s decision to avoid conducting aggressive stimulus measures – even as China’s growth engine sputters, and the economy grows at the slowest pace since the early 1990s – has spooked bond investors. The central bank has held off from adding liquidity this week, instead allowing large short-term cash injections to mature. That’s effectively drained 500 billion yuan from the financial system. Meanwhile, China’s credit impulse which previously pulled the entire world out of a recessionary ditch, has barely pushed off the cycle lows.

Some analysts said the central bank could instead use a targeted tool to inject one-year cash, which it refrained from doing Wednesday. That said, there is also a limit how aggressive the PBOC can get: soaring consumer prices, fueled by the surging cost of pork, are seen capping how much liquidity Beijing can provide without further stoking inflation.

Which means that very soon, the PBOC will be forced to choose: risk runaway bond yields, tumbling risk prices and an even faster slowdown in the economy, or stimulate the economy, and watch as the yuan tumbles as inflation surges even more. The only question is whether this terminal dilemma will come before or after the US is faced with a roughly similar choice.

When the modern computer was first created in the 1960s, people soon started imagining a future with intelligent machines. Some of these visions were dystopic, like Skynet in the Terminator movies. Today, almost everyone takes it for granted that artificial intelligence (AI) on par with human cognition is just around the corner, but is it realistic? Surprisingly, there are good reasons to be pessimistic about the prospects of smart machines.

Materialism And Reductionism

The basis of AI optimism is the widespread conviction in materialism and reductionism. Materialism is the belief that everything is made from dead matter, that consciousness is an illusion, and that the human mind is the product of a machine – the brain. Reductionism is the belief that everything can be understood by chopping it up into its parts and only studying their properties as if it were machinery. It has been the backbone of many scientific and technological achievements.

Its success has led people to believe that it also applies to consciousness and intelligence. All we need to do is to write a clever program and run it on a sufficiently powerful computer and voila: It will be as bright as us.

The Limits Of Reductionism

Despite the utility of reductionism, it is a philosophical error to assume that everything is reducible. Consider the following analogy: 99.99% of the universe is an empty vacuum. Everywhere in the cosmos, we see only vast swaths of nothingness, punctuated by an odd galaxy. From our own Milky Way, we know that even galaxies are mostly empty. If you used this to conclude that the universe was void of content, you would almost be correct. Almost. But that speck of matter in the cosmos turns out to be immensely significant. We are made of it, and we live in a place where we are surrounded by vast amounts of it. Matter matters to us.

Thus, we cannot reduce the world to emptiness. We need to account for that exceptional state that we call matter. Similarly, almost all matter in the known universe is dead and unconscious, but we also by extraordinary coincidence happen to be alive and conscious. We know this from our direct experience, and no amount of peering into the dead material world can undo that fact. Consciousness is real and may not be reducible to material causes.

Evolution

In addition to our direct experience of consciousness, evolutionary theory provides compelling evidence that it is not merely an illusion. Anything that evolves through natural selection must be both heritable and objectively measurable. There is no way for consciousness to be selected for and evolve unless it does something.

So what is the biological function of consciousness? We don’t know for sure, but it likely plays a crucial role in intelligence. This can be demonstrated with a task that is simple for us: object recognition. At an early age, we recognize a panoply of objects with ease, which even the most powerful supercomputers are incapable of today.

The task is so trivial to us that scientists thought it would be easy for computers too. It turned out to be nearly impossible. Although computers can beat humans in highly specialized computationally intensive tasks such as chess, they are nowhere near the ability of even a toddler in categorizing and recognizing objects. The key ingredient seems to be consciousness, which enables powerful intelligence at a mere glance.

Computers will continue to get smarter in specialized domains, but they will never gain awareness because it is not an algorithm. Thus, they will have to emulate human intelligence without the power of consciousness. Don’t be surprised if AI continues to fall short of expectations.

Hong Kong Plunges Into Recession After Months Of Violent Protests Take Toll

Hong Kong has finally entered a recession after more than half a year of violent anti-government protests, the city’s Financial Secretary wrote in a blog post over the weekend, reported Reuters.

“The blow to our economy is comprehensive,” Paul Chan wrote, adding that upcoming economic data later this week will trigger a technical recession.

“The government will be announcing its advance estimates for the third quarter on Thursday. After seeing negative growth in the second quarter, the situation continued in the third quarter, meaning our economy has entered technical recession,” Chan wrote.

“It seems it will be extremely difficult for us to reach full-year economic growth of 0 to 1%. I would not rule out the possibility that the full-year economic growth will be negative.”

Protesters have frequently shut down popular shopping districts, something that we outlined last week, warning that the retail industry in Hong Kong is on the brink of collapse.

Tourism plunged 37% Y/Y in 3Q19, and the trend for 4Q19 is likely not to improve. The number of tourists for the first two weeks of October was down 50% on a Y/Y basis.

Rooms at the most high-end hotels, like Marco Polo Hongkong in Tsim Sha Tsui, are going for $72 per night, a 75% discount versus last year.

Anyone who wants to travel to Hong Kong this week, departing from New York City airports, can easily get roundtrip plane tickets for 50% off because air travel to Hong Kong remains depressed.

Local businesses are cutting back on their workforce as approximately 77% of all hotel workers have just been asked to go on leave without pay.

Chan said government officials had announced stimulative measures to support local small and medium-sized businesses as the recession is expected to deepen into 1H20.

Hong Kong billionaire Li Ka-shing pledged to give local businesses $128 million in support following the protests that have presented the city with “unprecedented challenges.”

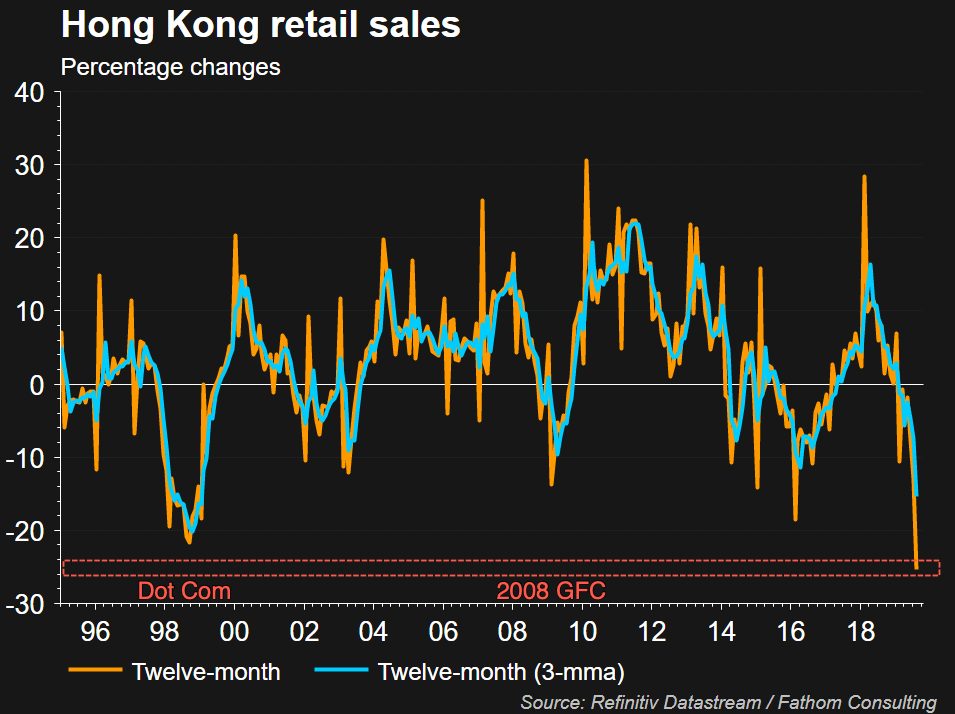

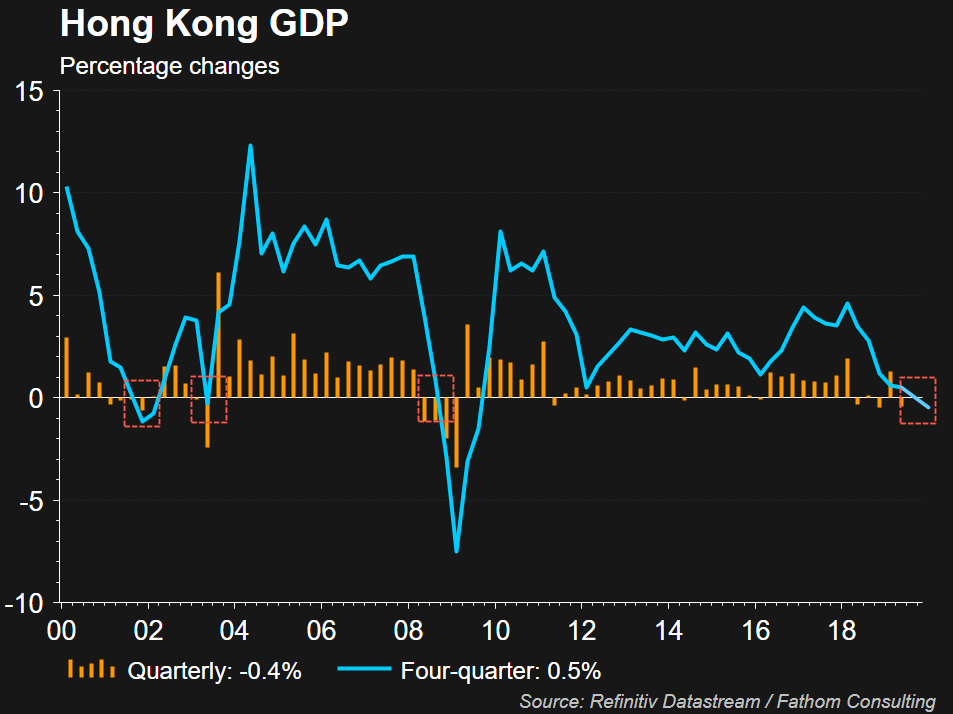

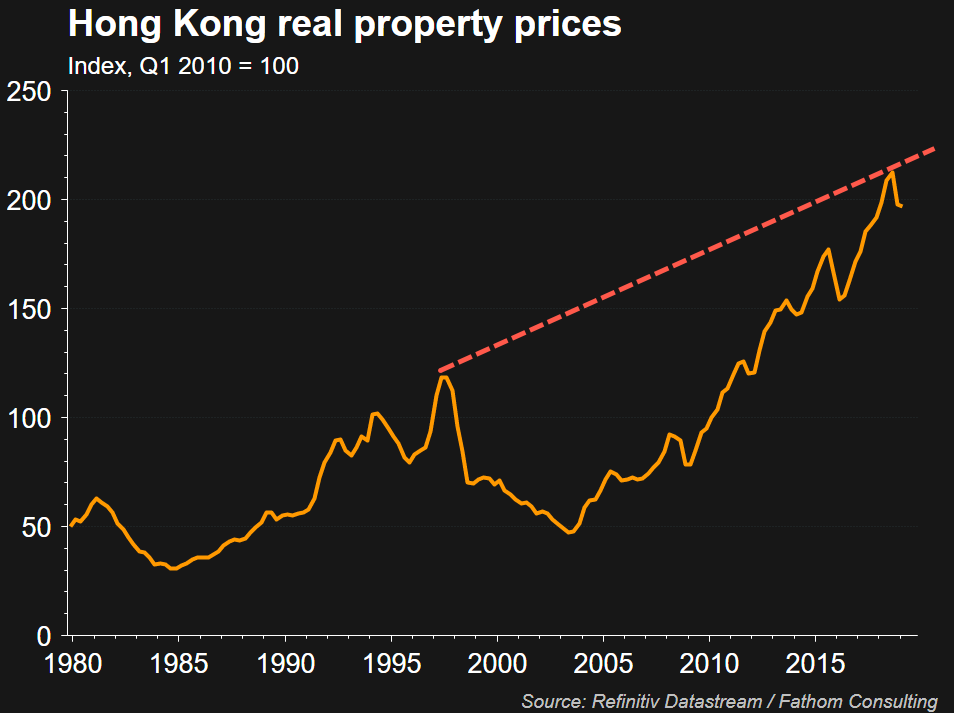

In a series of charts below, the city’s economic decline suggests a crisis has arrived:

In a 12-month and 3-month change, Hong Kong retail sales have absolutely crashed over the last half-year.

Hong Kong GDP is expected to print negative this Thursday for the first time since the financial crisis a decade ago.

Property prices in the city have stalled out in 2019.

The Hang Seng stock index is in a consolidation pattern. If economic deterioration continues, and or the recession worsens through 2020. Then it’s likely the stock index will break lower from the triangle.

Hong Kong is the first domino to drop. More emerging growth countries will fall under economic stress as the global recession is imminent, if not already arrived.

Renowned author and journalist James Howard Kunstler thinks what has been happening for the last few years with the mainstream media’s coverage of President Trump borders on criminal activity. Kunstler explains, “What I am waiting for is if and when indictments come down from Mr. Barr and Mr. Durham…”

“I am wondering whether the editors and publishers of the Washington Post and New York Times and the producers at CNN and MSNBC are going to be named as unindicted co-conspirators in this effort to gaslight the country and really stage a coup to remove the President and to nullify the 2016 election. I say this as someone who is not necessarily a Trump supporter. I didn’t vote for the guy. I am not a cheerleader for the guy, but basically I think the behavior of his antagonists has been much worse and much more dangerous for the nation and the American project as a long term matter. I really need to see some action to hold people responsible for the acts they have committed…

I am not an attorney, and I have never worked for the Department of Justice, but it seems to me that by naming the publishers and editors of these companies as unindicted co-conspirators that allows you to avoid the appearance of trying to shut down the press because you are not going to put them in jail, but you are going to put them in disrupt. That may prompt their boards of directors to fire a few people and maybe change the way they do business at these places.”

Kunstler says things look unlike anything we have seen in the past because we are approaching a day of reckoning in our debt based monetary system. Kunstler says, “Yeah, I think you can see it happening now…”

“What seems to be resolving is some movement to some sort of a crack up of the banking system. What we are really stuck in is a situation where we’ve got too many obligations we cannot meet and too many debts that will never be repaid. We have been trying to run the country for the past 15 or 20 years on debt because we can no longer provide the kind of industrial growth that we have been used to . . . and have this massive consumer spending industry. So, we have been borrowing from the future to pay our bills today, and we are running out of our ability to borrow more…

I think we are going to lose the ability to support a lot of activities that we have been doing. It starts with energy and its relationship to banking and our ability to generate the kind of growth you need to keep rolling over debt. The reason debt will never be paid and obligations will never be met is we are not generating that sort of growth. Were just generating frauds and swindles. Frauds and swindles are fun while you are doing them and they seem to produce a lot of paper profits, but after a while, they prove to be false. Then you have to do something else. A great deal about our economy and our way of life is false and is going to fail. Then we are going to have to make other arrangements for daily life. . . .It will probably mean we will be organizing our stuff at much more of a local scale.”

On the 2020 Presidential Election, Kunstler predicts, “When all is said and done, I am not convinced there is enough there to convict President Trump of anything…”

“At the same time, there is probably going to be a lot of legal actions brought against the people who started this coup against him, and that’s going to be extremely disturbing to the Left.

I think one of the possibilities is we may not have a 2020 election. In some way or another, the country may be so disorderly that we can’t hold an election. There may be so much strife that we cannot handle the legal questions around holding the election, and it may be suspended. I don’t know what that means, but I am very impressed of the disorder that we are already in. It’s more of a kind of mental disorder between the parties, but it could turn into a lot of kinetic disorder on the ground and a lot of institutional failure.”

Join Greg Hunter as he goes One-on-One with author and journalist James Howard Kunstler.

(You Tube has Demonetized this video – again. This means only long commercials play, if they play at all. (most skip long commercials) It must have some useful information in it, so, enjoy it!!)

Bill Ackman Says WeWork Is A “0”, SoftBank Should Cut Its Losses And Walk Away

How’s this for trenchant financial analysis from Bill Ackman, one of the boldest bold-faced names in the hedge fund business: SoftBank might end up writing down the entirety of its WeWork investment (including the $6 billion it just shelled out to wrest control of the firm away from Adam Neumann and his family).

Of course, that’s not exactly a cutting-edge call. WeWork’s unmatched fall from grace in August and September, which culminated with the shelving of its IPO and the collapse of a $6 billion JPM-led syndicated loan lifeline that was contingent on the offering, the company’s situation has gone from bad to worse. The company has been forced to put off a planned round of lease-signings and expansions, including possibly moving its headquarters to Manhattan’s Lord & Taylor Building, where the company holds an overpriced lease despite its former CEO owning a piece of the building. On the operations end, its business in China is bleeding capital, and the company has nearly $60 billion in long-term lease commitments, a number that is looking more daunting by the day.

But Ackman’s call arrives at a special time during the WeWork media dogpile. Ackman is only just recovering from a series of wrong-headed calls that nearly tanked his firm and career. Apparently, he thinks its finally “safe” to call WeWork a “0”, according to the FT. His LPs are no doubt watching.

And exactly how confident is Ackman? Pretty confident, he say.

“I think WeWork has a pretty high probability of being a zero for the equity, as well as for the debt,” the billionaire hedge fund manager said.

Ackman described Neumann as an amazing salesman (clearly, it takes a gifted charlatan to separate Masayoshi Son from his money), but that the company had become “enormously levered” too soon.

And speaking from experience, he warned SoftBank about continuing to throw good money after bad.

“As someone who has put good money after bad, I think this looks like putting good money after bad, and SoftBank should have walked away.”

At this point, Ackman and the others who have said SoftBank should expect to eat its entire investment are only a little more aggressive than the ratings agencies. Fitch Ratings warned on Tuesday that WeWork had “minimal headroom” to weather an economic slowdown or management misstep. SoftBank’s most recent cash infusion was “the effective minimum” the company needed to finance its existing operations and make it through a restructuring that is expected to cost 4,000 jobs.