Submitted by John Rubino via The Dollar Collapse blog,

In one sense, the past couple of weeks’ debt ceiling debate was just one more in a long line of annoying-but-otherwise-pointless pieces of bad political theater. But in another sense it was a turning point, one that may have put the democrats completely in charge. Consider:

In a system with two viable parties, each side has to pretend to be more reasonable than it really is in order to attract just enough moderate votes to win the next election. So democrats pay lip service to fiscal responsibility and deficits – occasionally even signing bills like welfare reform that they find repugnant – when they’d much rather spend their days indiscriminately tossing other people’s money at new entitlement programs. Republicans, meanwhile, pretend to empathize with people they privately view as prey when they’d rather be cutting taxes and invading places that have oil.

We only rarely get to see the major parties’ true selves because the 20% of voters in the middle are turned off by displays of naked avarice, and in a two-party system elections go to whoever carries a majority of that block.

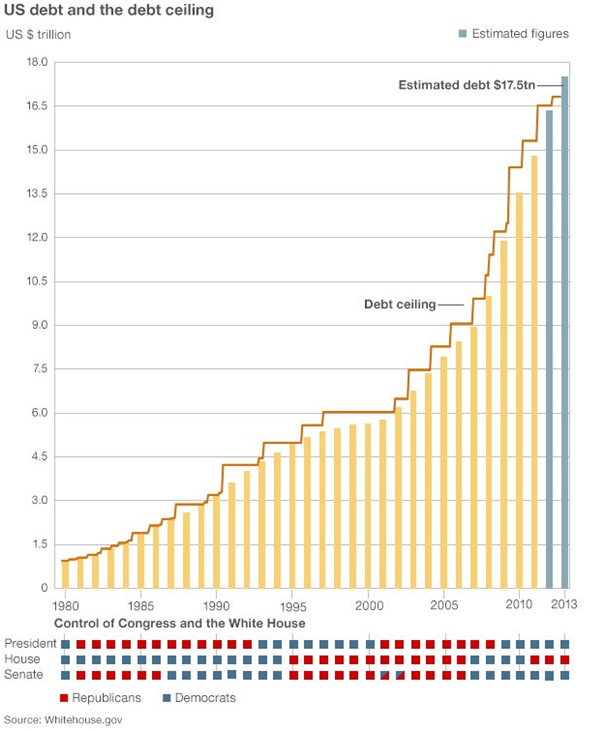

That’s why the latest debt ceiling debacle is such a big deal. Government shutdowns and related turmoil have become a standard bargaining chip lately, without affecting the make-up of either party. But this time the main conflict was not between republicans and democrats, but between mainstream, log-rolling, back-scratching, career-politician republicans and a handful of representatives and senators elected with Tea Party – i.e., highly ideological – support. The latter have no interest in raising the debt ceiling under any circumstances and see a government shutdown as a positive end in itself. Defunding Obamacare was just the excuse.

They got rolled, of course, as regular republicans chose to raise the debt ceiling without condition (as everyone always knew they would). But the cost of reopening the government is a republican civil war with only two likely outcomes: 1) The two groups stay in the big tent but challenge each other in primaries and intrigue over committee seats, etc., making a united, coherent policy front impossible and handing the next few elections to the democrats. 2) The Tea Party/libertarian republicans leave and either join the existing libertarian party or start one of their own, siphoning just enough votes from republicans in future elections to keep the democrats in charge.

Already, it has started. See this from today’s Bloomberg:

Republican Civil War Erupts: Business Groups v. Tea Party

A battle for control of the Republican Party erupted today as an emboldened Tea Party is moving to oust senators who voted to reopen the government, and business groups began mobilizing to defeat allies of the small-government movement.

“We are going to get engaged,” said Scott Reed, senior political strategist for the U.S. Chamber of Commerce. “The need is now more than ever to elect people who understand the free market and not silliness.” The chamber spent $35.7 million on federal elections in 2012, according to the Center for Responsive Politics, a Washington-based group that tracks campaign spending.

Meanwhile, two Washington-based groups that finance Tea Party-backed candidates said today they’re supporting efforts to defeat Mississippi Senator Thad Cochran, who voted this week for the measure ending the 16-day shutdown and avoiding a government debt default. Cochran, a Republican seeking a seventh term next year, faces a challenge in his party’s primary by Chris McDaniel, a state legislator.

McDaniel, who announced his candidacy today, “is not part of the Washington establishment and he has the courage to stand up to the big spenders in both parties,” Matt Hoskins, executive director of the Senate Conservatives Fund, said in a statement supporting him. Read more

Once the civil war costs the republicans control of the House of Representatives (November 4, 2014), the democrats will be relieved of the need to fool the middle about their commitment to fiscal sanity. The incoming Clinton administration and its congressional majorities will ramp up domestic spending and finance it with higher taxes, more borrowing and way more money printing. Janet Yellen (the perfect Fed chair for this transition) will expand QE and make it permanent. The Fed’s balance sheet will grow in trillion-dollar chunks as it buys up all the bonds issued by the government and the mortgage packagers and pretty much anybody else with paper to sell.

The resulting tidal wave of hot money will swamp emerging markets and drive Europe and Japan crazy, but the democrats won’t care because they’ll be favored by 20 points in the polls and in any event will be too busy hiring more staff to handle the upcoming legislative season to listen to non-believers. Oh, and they’ll counter any dissent with capital controls and stepped-up surveillance.

Could there be a better environment for gold? Not at first glance. But then almost the same could have been said two years ago when the Fed started buying $85 billion of bonds each month and bubbles began to form in stocks and houses. Some of that cash certainly should have found its way into precious metals. Instead the result was an epic correction. So logic isn’t necessarily our best guide here.

Still, the republican implosion/democrat ascendance comes after a two-year precious metals correction (during which China, India, and Russia bought something like 4,000 tons of gold, an amount greater than Germany’s entire gold reserves). So coming when it does, the combination of democrat dominance, an even more accommodating Fed and a growing shortage of Western gold to be shipped East…well, at the risk of being wrong again, this really does look like precious metals paradise.

![]()

|

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/oKAQvg6w7iY/story01.htm Tyler Durden

Submitted by John Rubino via The Dollar Collapse blog,

In one sense, the past couple of weeks’ debt ceiling debate was just one more in a long line of annoying-but-otherwise-pointless pieces of bad political theater. But in another sense it was a turning point, one that may have put the democrats completely in charge. Consider:

In a system with two viable parties, each side has to pretend to be more reasonable than it really is in order to attract just enough moderate votes to win the next election. So democrats pay lip service to fiscal responsibility and deficits – occasionally even signing bills like welfare reform that they find repugnant – when they’d much rather spend their days indiscriminately tossing other people’s money at new entitlement programs. Republicans, meanwhile, pretend to empathize with people they privately view as prey when they’d rather be cutting taxes and invading places that have oil.

We only rarely get to see the major parties’ true selves because the 20% of voters in the middle are turned off by displays of naked avarice, and in a two-party system elections go to whoever carries a majority of that block.

That’s why the latest debt ceiling debacle is such a big deal. Government shutdowns and related turmoil have become a standard bargaining chip lately, without affecting the make-up of either party. But this time the main conflict was not between republicans and democrats, but between mainstream, log-rolling, back-scratching, career-politician republicans and a handful of representatives and senators elected with Tea Party – i.e., highly ideological – support. The latter have no interest in raising the debt ceiling under any circumstances and see a government shutdown as a positive end in itself. Defunding Obamacare was just the excuse.

They got rolled, of course, as regular republicans chose to raise the debt ceiling without condition (as everyone always knew they would). But the cost of reopening the government is a republican civil war with only two likely outcomes: 1) The two groups stay in the big tent but challenge each other in primaries and intrigue over committee seats, etc., making a united, coherent policy front impossible and handing the next few elections to the democrats. 2) The Tea Party/libertarian republicans leave and either join the existing libertarian party or start one of their own, siphoning just enough votes from republicans in future elections to keep the democrats in charge.

Already, it has started. See this from today’s Bloomberg:

Republican Civil War Erupts: Business Groups v. Tea Party

A battle for control of the Republican Party erupted today as an emboldened Tea Party is moving to oust senators who voted to reopen the government, and business groups began mobilizing to defeat allies of the small-government movement.

“We are going to get engaged,” said Scott Reed, senior political strategist for the U.S. Chamber of Commerce. “The need is now more than ever to elect people who understand the free market and not silliness.” The chamber spent $35.7 million on federal elections in 2012, according to the Center for Responsive Politics, a Washington-based group that tracks campaign spending.

Meanwhile, two Washington-based groups that finance Tea Party-backed candidates said today they’re supporting efforts to defeat Mississippi Senator Thad Cochran, who voted this week for the measure ending the 16-day shutdown and avoiding a government debt default. Cochran, a Republican seeking a seventh term next year, faces a challenge in his party’s primary by Chris McDaniel, a state legislator.

McDaniel, who announced his candidacy today, “is not part of the Washington establishment and he has the courage to stand up to the big spenders in both parties,” Matt Hoskins, executive director of the Senate Conservatives Fund, said in a statement supporting him. Read more

Once the civil war costs the republicans control of the House of Representatives (November 4, 2014), the democrats will be relieved of the need to fool the middle about their commitment to fiscal sanity. The incoming Clinton administration and its congressional majorities will ramp up domestic spending and finance it with higher taxes, more borrowing and way more money printing. Janet Yellen (the perfect Fed chair for this transition) will expand QE and make it permanent. The Fed’s balance sheet will grow in trillion-dollar chunks as it buys up all the bonds issued by the government and the mortgage packagers and pretty much anybody else with paper to sell.

The resulting tidal wave of hot money will swamp emerging markets and drive Europe and Japan crazy, but the democrats won’t care because they’ll be favored by 20 points in the polls and in any event will be too busy hiring more staff to handle the upcoming legislative season to listen to non-believers. Oh, and they’ll counter any dissent with capital controls and stepped-up surveillance.

Could there be a better environment for gold? Not at first glance. But then almost the same could have been said two years ago when the Fed started buying $85 billion of bonds each month and bubbles began to form in stocks and houses. Some of that cash certainly should have found its way into precious metals. Instead the result was an epic correction. So logic isn’t necessarily our best guide here.

Still, the republican implosion/democrat ascendance comes after a two-year precious metals correction (during which China, India, and Russia bought something like 4,000 tons of gold, an amount greater than Germany’s entire gold reserves). So coming when it does, the combination of democrat dominance, an even more accommodating Fed and a growing shortage of Western gold to be shipped East…well, at the risk of being wrong again, this really does look like precious metals paradise.

![]()

|