Bonds erased early losses and stocks give back opening gains, drifting back within Wednesday’s trading range as traders paused to asses the rollercoaster of the past three days which saw the biggest first day drop of the year since the dot com bubble followed by a surge as Democrats took Congress following Senate wins in Georgia, sparking expectations of massive stimulus.

S&P 500 futures were up 0.4% and most stock benchmarks across Asia and Europe were in the green. Treasury yields held above 1%, while the dollar strengthened against all its major peers. In a sign that traders are still willing to pile on risk, Bitcoin shot above $38,000 to another record high.

At 07:40 a.m., Dow E-minis were up 91 points, or 0.31%, S&P 500 E-minis were up 18.5 points, or 0.49%, and Nasdaq 100 E-minis were up 91.5 points, or 0.8%. Among the notable movers, Bank of America Corp, Citigroup, JPMorgan Chase and Goldman continued to climb in pre-market trading as the benchmark 10-year Treasury yield hovered near 1%. Shares of Twitter Inc. dropped 1.3% in U.S. pre-market trading after the platform suspended Trump’s account. Tesla Inc. added 2.9% as analysts at RBC upgraded the stock, saying they were “completely wrong” with their previously bearish views.

Overnight, Joe Biden was formally recognized by Congress as the next U.S. president early Thursday, a day after demonstrators overpowered police and stormed through the Capitol building in a scene of unprecedented turmoil in Washington. Present Donald Trump released a statement pledging “an orderly transition” after Congress certified the results. Stunning images of the assault on Congress had earlier knocked sentiment, though markets focused on the implications of the Democrat blue wave.

Despite the disruption, markets showed little sign of worry and trading throughout the day was normal. Bullish themes, such as the prospect for more U.S. stimulus spending in a Democrat-controlled Congress and the vaccine rollout, have dominated investor attention.

“The market is confident that there will be an orderly transition of power,” said Christoph Rieger, head of fixed-rate strategy at Commerzbank AG. “What matters more are the near-term prospects of a transition of power and more fiscal stimulus under a Democrat-led Senate.”

After a dour start to the week, financials and industrial stocks powered the Dow and the S&P 500 to all-time highs on Wednesday in hopes that some of President-elect Joe Biden’s policies could speed up a vaccine-driven recovery from the steepest downturn in decades. But the Nasdaq, dominated by FAANG stocks that had led Wall Street’s rally from the pandemic lows, closed lower on fears some of them could face antitrust scrutiny while the coming inflation wave would hit deflationary assets.

“The market is saying the reflation trade is on,” said Justin Onuekwusi, portfolio manager at Legal & General Investment Management. “The Democrat sweep means there will be more flexibility and speed to writing a fiscal check so a one-off U.S. fiscal boost as a bridge to a post-vaccine world is definitely on the cards.”

In Europe, the Stoxx 50 was little changed, the DAX outperforming with a 0.4% gain while FTSE 100 lags having outperformed at the open. European sentiment was boosted by an unexpected rise in German factory orders pre-lockdown in November. U.K. grocer J Sainsbury Plc shares rallied 4.1% after seeing its strongest Christmas on record. On the downside, Ryanair Holdings Plc declined 2.8% after the budget airline operator cut its full-year traffic forecast, citing new coronavirus restrictions. U.S.-listed shares of German biotech firm CureVac NV surged 20% after it struck an alliance with drugmaker Bayer to help it seek regulatory approval for its experimental COVID-19 vaccine and distribute doses.

Asian stocks joined the global reflation trade with more stimulus spending likely on the horizon after the Democrats won control of the Senate. The MSCI Asia Pacific Index gained as much as 1.4%, set for another record close. Material and industrial stocks led the gains, followed by financials which were boosted by a steepening yield curve. Environmental and cannabis-related stocks, which are seen to benefit from U.S. President-elect Joe Biden’s agenda, also outperformed. Alibaba Group and Tencent led a selloff in internet stocks as the Trump administration considers barring investments in China’s two most valuable companies. Three major Chinese telecommunications companies also slumped as NYSE reversed again with a plan to delist them. North Asian markets led the charge, with Korea’s benchmark gauge and Japan’s Topix closing 2.1% and 1.7% higher, respectively. Miners Rio Tinto and BHP earlier surged to all-time highs while chipmakers Samsung and SK Hynix drove South Korean stocks to a record high. Malaysia’s benchmark gauge dropped as much as 1.2% before recouping the losses as the country recorded its highest-single day increase in new coronavirus cases on Wednesday.

In rates, Wednesday’s bond sell-off pushed the yield on benchmark 10-year U.S. Treasuries over 1% for the first time since March. It rose as high as 1.0660% on Thursday before slipping back, and was last trading around 1.0524% after earlier weakness during Asia session pushed 10-year to 1.064%, exceeding Wednesday’s high. Euro zone government bonds followed suit, with Germany’s 10-year Bund yield up slightly to -0.55%. Japanese government bonds also slipped.

The Democrat victory also reverberated in currency markets, sending the dollar to a near-three year low against a basket of six major currencies, with traders betting growing U.S. trade and budget deficits would weigh on a greenback already bruised. On Thursday the Dollar index bounced 0.6% to 89.780, on track for its biggest one-day gain since October. The euro clawed away from an almost three-year high of $1.22, and also languished near recent multi-year troughs against the Aussie, kiwi and Swiss franc. That said, some analysts said rising bond yields may help the dollar’s fortunes. The Polish zloty appreciated as much as 0.6% to trade below 4.50 per euro, a level that’s seen as a possible trigger-point for central bank intervention.

“Higher Treasury yields should benefit the dollar against the euro and the yen,” said Masafumi Yamamoto, chief currency strategist at Mizuho Securities in Tokyo.“However, the dollar will remain weaker against commodity currencies like the Aussie and emerging market currencies.” Other risk assets climbed, with safe havens like the Japanese yen losing ground.

In commodities, Copper, a barometer for global growth, gained 0.3% to hover near an 8-year high. Oil prices held around a 10-month high, basking in the afterglow of a production cut promised by Saudi Arabia. Brent crude futures were flat at $54.25 a barrel. Gold was steady at $1,921 an ounce, and bitcoin firm after hitting a fresh record high just over $38,000. The cryptocurrency has soared over a quarter already this month after almost quadrupling last year.

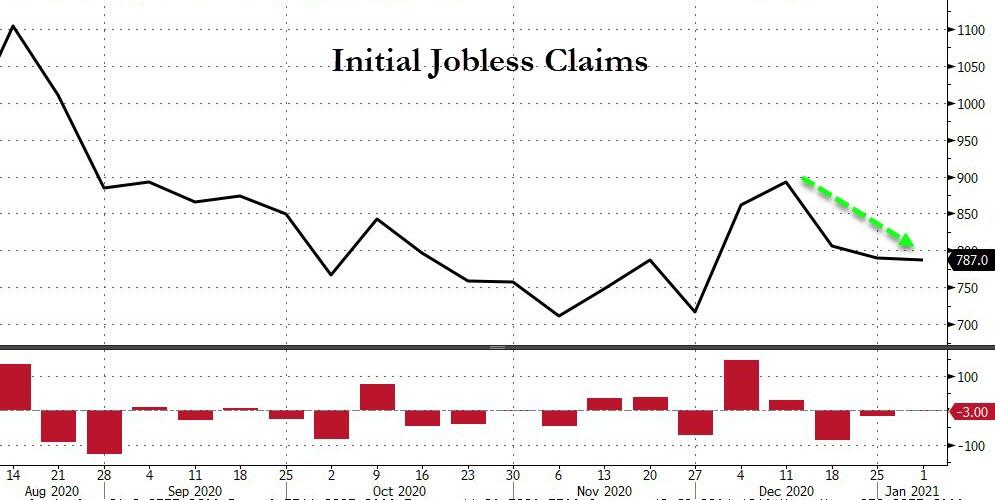

The first weekly initial claims report of 2021 due at 830am ET is expected to show the number of Americans filing for unemployment benefits rose to 800,000 last week, likely due to increased restrictions to keep the spread of coronavirus infections in check. The more comprehensive jobs report for December is expected on Friday.

Market Snapshot

- S&P 500 futures up 0.5% to 3,758.50

- STOXX Europe 600 up 0.1% to 406.92

- MXAP up 0.9% to 204.02

- MXAPJ up 0.6% to 679.16

- Nikkei up 1.6% to 27,490.13

- Topix up 1.7% to 1,826.30

- Hang Seng Index down 0.5% to 27,548.52

- Shanghai Composite up 0.7% to 3,576.21

- Sensex up 0.01% to 48,181.06

- Australia S&P/ASX 200 up 1.6% to 6,711.95

- Kospi up 2.1% to 3,031.68

- German 10Y yield rose 0.2 bps to -0.518%

- Euro down 0.3% to $1.2286

- Italian 10Y yield unchanged at 0.456%

- Spanish 10Y yield rose 1.1 bps to 0.057%

- Brent futures up 0.3% to $54.46/bbl

- Gold spot down 0.2% to $1,915.26

- U.S. Dollar Index up 0.2% to 89.67

Top Overnight News from Bloomberg

- Joe Biden was formally recognized as the next U.S. president early Thursday, ending two months of failed challenges by his predecessor that exploded into violence at the Capitol as lawmakers met to ratify the election result

- Trump, hours after his supporters broke into the Capitol, pledged “an orderly transition”

- The total market value of cryptocurrencies surpassed $1 trillion for the first time amid a frenzied and volatile rally in Bitcoin

A quick look at global markets courtesy of Newsquawk

Asia-Pac bourses traded mostly higher as the region reacted to the Democrats winning control of the Senate which lifted most major indices on Wall St and buoyed cyclicals on anticipation of greater stimulus measures, with US equity futures also underpinned after the earlier siege on Capitol Hill was eventually resolved. Congress was evacuated earlier after pro-Trump protesters stormed buildings and halted the election certification procedure with reports of gunfire and suspected explosive devices in Washington D.C adding to the pandemonium, prompting the activation of the National Guard, although police have since taken back control and Senate has reconvened to certify the Presidential election results with many also blaming President Trump for inciting the insurrection. ASX 200 (+1.6%) and Nikkei 225 (+1.6%) surged with the sectors in Australia mirroring their stateside counterparts whereby cyclicals outperformed and tech suffered, while sentiment in Tokyo stocks also took its cue from global peers which overshadowed weaker wage data and a looming state of emergency decision. Hang Seng (-0.5%) and Shanghai Comp. (+0.7%) were indecisive and swung between gains and losses with heavy pressure in the telecom and tech giants after the NYSE and S&P Dow Jones announced to remove the major Chinese telecom firms and with US reportedly mulling prohibiting Americans from investing in Alibaba and Tencent Holdings. Finally, 10yr JGBs were lower with prices trickling further beneath the 152.00 level amid the gains in stocks, spillover selling from bear steepening in USTs and with the absence of BoJ purchases in the market today.

Top Asian News

- Japan Declares Virus Emergency for Tokyo Amid Record Cases

- Ant Plans Credit Unit Revamp to Avoid Sharp Drop in Loans

- India Approves $4 Billion to Boost Industries in Kashmir

- China Sentences Ex-State Bank Chief to Life on Bribery

European bourses see somewhat of a mixed session thus far (Euro Stoxx 50 Unch), as the Georgia-driven optimism in APAC hours fizzled out in early European trade amid a lack of fresh catalysts ahead of tomorrow’s US jobs data, and today’s IJC and Services PMI releases, while US equity futures post modest gains with the E-mini S&P matching its intraday record high of 3773.25 as European player entered the fray. Sectors in Europe also vary with no clear risk tone portrayed; though, around the cash open the sector breakdown did favour cyclicals, though the magnitudes were more contained than yesterday. Materials and Industrial names lead the gains whilst Healthcare, Travel and IT lag, and Energy alongside Banks take breathers after yesterday’s sizeable gains. Delving deeper into the sectors, Materials track upside in the base metals complex while Travel & Leisure is dented by airliners amid firmer oil prices alongside Ryanair (-2.9%) cutting its FY traffic forecast and significantly dropping its flight schedules from January 21st. As such, sympathy play is seen among peers including easyJet (-3.2%), IAG (-2.9%), Deutsche Lufthansa (-1.5%) and Air France (-1.5%); albeit, for the latter, French press Le Parisie noted that Air France will be provided further state aid this year. In terms of individual movers, Saint Gobain (+7.5%) leads the gains in the CAC after upping its Q4 and H2 2020 forecasts while guiding operating margin at a “record level”. German-heavyweight Bayer (+3.3%) lifts the DAX after CureVac (+12.7%) agreed to an alliance with Bayer to get global support in seeking approval for its experimental COVID-19 vaccine and for distribution. On the other end of the spectrum, Delivery Hero (-1.6%) is softer after it launched a cash capital increase via the issuance of around 9.4mln shares, equating to 4.7% of share capital.

Top European News

- Denmark Charges Two Britons Over $1.6 Billion Cum-Ex Fraud

- Euro- Area Economic Confidence Rises Despite Fresh Virus Curbs

- Goldman Sees BOE Fighting New Recession With More Bond Buying

- Johnson Vows to Slash Business Rules, Asking U.K. Bosses to Help

In FX, the Dollar remains in recovery mode, with the DXY rebounding from sub-89.500 lows, albeit in somewhat quieter and more measured fashion compared to Wednesday’s frantic price action awaiting confirmation of the Georgia run-off results and certification of Electoral College votes that was derailed by the siege on Capitol Hill before resuming to seal victory for President-in-waiting Biden. For the record, FOMC minutes were largely taken in stride, but upcoming IJC, trade and non-manufacturing ISM releases could be more market moving either side of comments from Fed’s Harker and Evans. Meanwhile, after extending losses on the Blue banner of fiscal and deficit excesses among other bearish factors, the Buck seems to have gleaned a degree of traction from the ongoing ramp up in US Treasury yields as 10 year cash inches further above 1% and the index hovers near the top of a 89.949-294 band.

- JPY/CHF/AUD – Not much to chose between the Yen, Franc and Aussie in percentage terms at foot of the major leagues as they all continue to fall prey to the Greenback revival. However, the rebounds in Usd/Jpy and Usd/Chf through 103.65 and 0.8840 respectively alongside Aud/Usd relinquishing 0.7800+ status will be welcomed by the respective monetary authorities, especially as Aussie trade data disappointed overnight. Moreover, the BoJ and MoF have stressed the need for market stability and SNB remains fully committed to intervention as Japan and Switzerland battle against the latest spread of COVID-19.

- EUR/NZD – The next weakest G10 links or least resilient to the Buck bounce, with the Euro topping out around 1.2350 again and not able to rely on underlying support from 1.2300 option expiries today, while the Kiwi has lost grip of the 0.7300 handle, albeit still holding up a bit better than its Antipodean counterpart as the Aud/Nzd cross stays mostly south of 1.0700.

- CAD/GBP – Looming Canadian trade and Ivey PMIs may provide the Loonie with some independent inspiration, but for now Usd/Cad is hovering around 1.2700 and weighing firm crude prices vs relative US Dollar strength, and it’s a similar story for Sterling as Cable pivots 1.3600 assessing pandemic implications for the UK economy, Government finances and BoE policy in addition to external impulses.

- SCANDI/EM – Oil’s exertions over Usd 51/brl in WTI terms and close to Usd 55 for Brent are keeping the Nok in the ascendency comfortably above 10.4000 vs the Eur, though the Sek is still struggling to mount a serious test of 10.0000 in wake of a slowdown in Sweden’s services PMI. Elsewhere, the Try continues its impressive comeback even though the EU has sanctioned Turkey, and in stark contrast to the Zar that has been hit even harder by reports about vaccinations not being effective against SA’s new virus strain

In commodities, WTI and Brent front month futures consolidate and trade off best levels, as the former briefly topped USD 51/bbl and the latter meanders around USD 54.50/bbl with prices underpinned by the OPEC+ meeting earlier this week and positive risk tone amid expectations of greater stimulus following the blue sweep in the Georgia Senate Run-offs. News flow for the complex has been light in European hours, although from a demand standpoint, Ryanair has cut its FY traffic forecast to 26-30mln passengers vs prev. guided below 35mln and will be significantly cutting its flight schedules from 21st January, thus the jet fuel demand aspect is on watch. Elsewhere, spot gold prices declined yesterday and tested USD 1900/oz to the downside as prices tracked real yields in US trade, with the yellow nursing some of its wounds overnight to stabilise around USD 1920/oz in European trade. Similarly, spot silver briefly dipped below USD 27/oz yesterday but replaced the status in overnight trade. Base metal prices further advanced overnight in a continuation of the Georgia run-off hype and reflationary play. LME copper meanwhile continues to extend gains above USD 8,100/t hitting levels last seen in 2013. Finally, Shanghai stainless steel futures extended gains overnight amid higher nickel feedstock costs coupled with tighter supply woes.

US Event Calendar

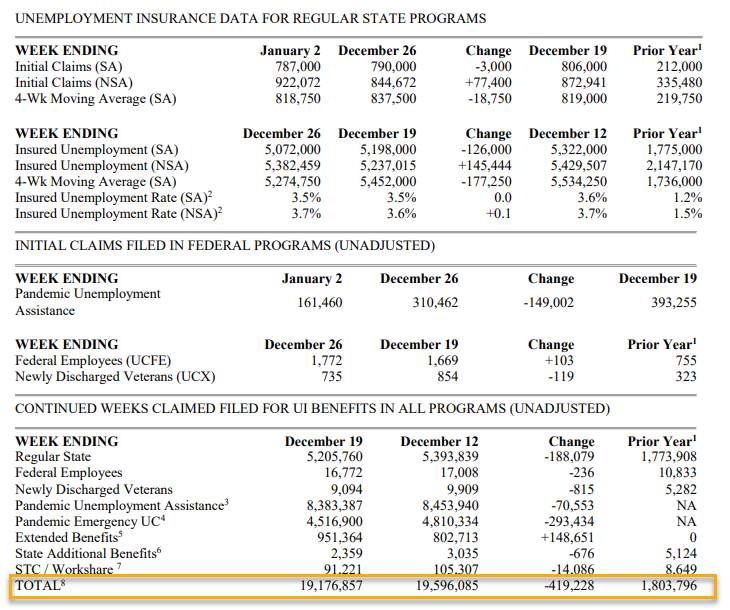

- 8:30am: Initial Jobless Claims, est. 800,000, prior 787,000; Continuing Claims, est. 5.2m, prior 5.22m

- 8:30am: Trade Balance, est. $67.3b deficit, prior $63.1b deficit

- 9:45am: Bloomberg Consumer Comfort, prior 44.6

- 10am: ISM Services Index, est. 54.5, prior 55.9

DB’s Jim Reid concludes the overnight wrap

Regular readers over the last year will be aware that the soundtrack to my WFH has been “Chill Acoustic” radio. I work better with mellow music on in the background. However after 9 months I’ve become slightly bored of what is a rotation of exactly the same songs on an albeit long loop. As such I’ve imaginatively moved to “Smooth Chill” radio this week and to be honest I now constantly feel like I’ve left an Ibiza nightclub at 5am with the warm sun rising over the horizon rather than the dark, wet and cold Surrey mornings we’ve been having. It’s very ambient! So bear that in mind as you read my output. In fact there is no guarantee I won’t fall back to sleep before I finish this!

Markets certainly woke up for the year yesterday and reacted strongly after the final votes from the Georgia Senate races put the Democrats over the top in both contests, with cyclical assets in particular seeing large outperformance. However remarkable scenes from protestors storming the US Capitol in protest at Trump’s election defeat took the shine off the session (more below).

Nevertheless the Senate results mean that the so-called ‘Blue Wave’ scenario has finally come about, albeit via a tortuous journey, resulting in a slim Democratic majority in both chambers of Congress. The main implication being the prospect of a substantially larger US stimulus package once President-elect Biden comes to office, and giving further support to the reflation trade.

As investors anticipated further stimulus ahead, yesterday saw a substantial selloff in US Treasuries, with 10yr yields up +8.1bps to 1.036%. That takes them above the 1% barrier for the first time since mid-March, back when Treasury yields sunk to all-time lows as the coronavirus pandemic took hold around the world. Alongside this, there was a sizeable steepening in the yield curve, with the 2s10s curve up +6.3bps to 89.5bps, which is the steepest level in 3 years, while the 5s30s hit its steepest in 4 years. Notably, it was rising inflation expectations that drove the bulk of the increase in yields, with 10yr US breakevens up +4.1bps to 2.07%, taking them back to levels not seen since late-2018. This hit a low of 0.55% back in March so inflation expectations on this measure have been totally reappraised.

In more jarring US political news, the election certification process, which is normally fairly straight forward and ceremonial, was first interrupted by objections from Republican lawmakers, but then stopped altogether by protestors breeching the US Capitol Building. This followed a rally by President Trump in the morning, before the crowd started marching through the streets of Washington DC to Congress where the Senate and House were holding the joint session. Congress reconvened later in the evening in order to finish the certification process of the Presidential election which is still continuing as we go to print. The accepted electoral count is currently frozen at 244 to 157 while Pennsylvania is debated. In a sign of how extraordinary times are, Twitter, Facebook and Instagram temporarily blocked President Trump’s accounts overnight.

The protests and occupation of the Capitol moderated some of the initial market moves of the day with the S&P 500 (+0.57%) off the days highs of around +1.5%. Notwithstanding this set back, the Dow Jones (+1.44%) climbed to fresh all-time highs, as the small-cap Russell 2000 surged an even-stronger +3.98%. Cyclical sectors led the advance, with financials (+4.36%) and materials (+4.09%) the strongest-performing S&P 500 industry groups, in a broad-based move that saw over 80% of the index close higher on the day. Tech stocks strongly underperformed however, with the NASDAQ falling -0.61% thanks to the combination of rising bond yields and fears that a Democratic Washington means higher taxes and new regulations for big tech. The equal weight S&P 500 (+2.37%) saw its biggest out-performance of the main parent index since November 9, when the results of the US general election were finally called.

In terms of the ramifications, the Georgia results mean that President-elect Biden will now have united control of government at the start of his term, making another large fiscal stimulus package a likely outcome. It also gives Biden a lot more flexibility in his appointments to senior positions, because the Senate approves an array of posts including the cabinet, ambassadors, judges and the Federal Reserve Board of Governors. Indeed, had the Republicans kept control of the Senate, that would have made Biden the first president since George H. W. Bush in 1989 to not have his party controlling both houses of Congress at the start of his term of office, constraining his room for manoeuvre from the start.

This rotation out of safe havens into risk assets was seen across multiple asset classes yesterday. European equities surged alongside their US counterparts, with the STOXX 600 (+1.36%) hitting a post-pandemic high led by banks (+5.56%), whilst oil prices benefited too, with both Brent Crude (+1.31%) and WTI Oil (+1.40%) reaching their own post-pandemic highs of $54.30/bbl and $50.63/bbl respectively. Peripheral sovereign bonds in Europe were another to benefit from this pattern, with the spread of 10yr Italian debt over bunds (-5.7bps) tightening to a 4-year low of 1.09%, as the 10yr Spanish spread fell -4.6bps to its lowest in over a decade. Yields were still up across the board however, with those on bunds (+5.7bps), gilts (+3.4bps) and OATs (+1.7bps) all moving higher. Meanwhile, the traditionally haven Japanese Yen was the worst-performing among the G10 currencies (-0.31% vs USD), as precious metals including gold (-1.61%) and silver (-0.95%) similarly lost ground. On the other hand Bitcoin rose sharply, gaining +6.35% on the day and is up another +4.96% overnight to over $37,500.

Overnight in Asia markets have moved higher in tow with Wall Street’s moves outside of the Hang Seng (-0.38%) which is down on news that the Trump administration may bar investments in China’s Alibaba Group and Tencent. Investors might have difficulty unwinding their positions in these companies if this indeed happens as at $1.3tn, the combined market value of their primary listings is nearly twice the size of Spain’s stock market, while the firms together account for about 11% of the weighting for MSCI Inc.’s emerging markets benchmark. Sentiment for the Hang Seng was also sapped as the NYSE took a second U-turn this week saying that it now plans to go ahead with delisting China’s three major telecommunication companies after US Treasury Secretary Steven Mnuchin disagreed with its earlier decision to give the firms a reprieve. The Nikkei (+1.38%), Shanghai Comp (+0.18%) and Kospi ( +2.40%) are all up. Futures on the S&P 500 (+0.50%) and Nasdaq (+0.67%) are also trading higher.

In terms of the coronavirus pandemic, the drumbeat of negative news continued as we await the rollout of vaccination programmes. In the UK, another record number of cases were reported yesterday, at over 62k, along with more than a thousand daily deaths for the first time since the original wave back in April. Meanwhile in Ireland, new restrictions were announced, with the cabinet agreeing to keep most students out of school until at least the end of January, while non-essential construction projects will stop from Friday evening. Separately, yesterday saw the Moderna vaccine win approval in the EU, which comes as leaders on the continent have faced strong pressure to speed up the vaccination programme, with the numbers so far lagging well behind the US and the UK.

Fed minutes from the December meeting were released last night and some of the content is already well out of date. Many members referenced the downside risks of ending government support, but Congress has since agreed to fresh fiscal stimulus, with more likely on the way, following the Georgia runoffs. The virus and growing case counts were the other material down-side risk discussed, while upside risks remain pent-up demand and a robust vaccine rollout. The committee remained unconcerned with inflation and stressed that the new guidance is “qualitative” and that there would not be simple numerical targets at this time to trigger changes to monetary policy.

On the data front, the final Euro Area services PMI was revised down from the flash reading to 46.4 (vs. flash 47.3), while the composite number was also revised down to 49.1 (vs. flash 49.8). Nevertheless, despite the downward revisions from the flash prints, they’re still a lot stronger than the market was originally expecting for December. Elsewhere in the US ahead of tomorrow’s December jobs report, the ADP’s employment reading for December showed a -123k reduction in private payrolls (vs +75k expected), which was the first decline in that reading since April. However, US factory orders in November surprised to the upside, rising by +1.0% (vs. +0.7% expected).

To the day ahead now, and data releases include December’s construction PMI from the UK and Germany, German factory orders for November, Italy’s preliminary December CPI reading and Euro Area retail sales for November. Meanwhile from the US, there’s the weekly initial jobless claims, the ISM services index for December, along with the November trade balance. Finally, central bank speakers today include the Fed’s Harker, Barker, Bullard, Evans and Daly.