US Services Industry Slowed… And Accelerated… In September (You Decide) Tyler Durden

Mon, 10/05/2020 – 10:05

After a mixed picture (though uniformly disappointing) in Manufacturing surveys, analysts expected US Services surveys to show further deterioration from their post-COVID rebound peak.

Markit US Services 54.6 vs 54.6 flash vs 54.6 exp vs 55.0 prior

ISM US Service 57.8 vs 56.2 exp vs 56.9 prior

So Markit fell and ISM rose in September – choose which one you believe!

Source: Bloomberg

Under the hood of ISM Services:

Business activity rose to 63.0 vs 62.4 prior month

New orders rose to 61.5 vs 56.8

Employment rose to 51.8 vs 47.9; the highest since February

Supplier deliveries fell to 54.9 vs 60.5; the lowest level since February

Inventory change rose to 48.8 vs 45.8

Prices paid fell to 59.0 vs 64.2

Backlog of orders fell to 50.1 vs 56.6

New export orders fell to 52.6 vs 55.8

Imports fell to 46.6 vs 50.8

Inventory sentiment rose to 55.4 vs 52.5

ISM respondents were mostly optimistic:

“Business has been fairly stable over the summer; however, there is still a great deal of uncertainty as we move into fall and winter [and] how our sales volume will be.” (Agriculture, Forestry, Fishing & Hunting)

“Our industry is facing a bleak outlook, as the Hollywood studios have pulled back almost all of their content from October and November and moved it into next year. Coupled with the state health mandates restricting our attendance, we expect to operate at a loss in 2020 and 2021.” (Arts, Entertainment & Recreation)

“Work orders are improving rapidly. Lack of available labor is having a significant impact on our ability to fulfill orders.” (Construction)

“Insurance industry will experience some impact from weather- and protest-related property damage and business interruption.” (Finance & Insurance)

“The U.S. economy continued to rebound in September from the deep contraction seen at the height of the Covid-19 pandemic, with business activity rising across both manufacturing and services to round off the strongest quarter since early-2019.

“Covid-19 worries and social distancing continued to impact many businesses, however, especially in consumer-facing sectors, where demand for services fell once again. However, business and financial services, healthcare and housing sectors all fared well as the economy continued to revive, and exports of services also picked up as other countries continued to open up their economies.

“Encouragingly, new orders for services grew at an increased rate in September, putting additional pressure on operating capacity and fuelling another robust rise in employment. A further rise in backlogs of work bodes well for robust jobs growth to be sustained into October.

However, the slowdown in the Composite Index suggests this may be as good as it gets for US economic growth’s rebound…

“Sentiment on prospects for the coming year darkened significantly, however, linked to growing worries about virus numbers, uncertainty regarding the presidential election and fears that the economy is susceptible to weakening unless more support measures are put in place soon.”

via ZeroHedge News https://ift.tt/33vQvjX Tyler Durden

Key Events This Week: Powell, VP Debate, ISM And Fed Speakers Galore Tyler Durden

Mon, 10/05/2020 – 09:50

It’s a relatively quiet week event-wise, where outside of the VP debate on Wednesday we get the latest minutes from recent Fed (Weds) and ECB (Thurs) meetings, and also hear from both Fed Chair Powell (tomorrow) and ECB President Lagarde (tomorrow and Weds).

As DB’s Jim Reid notes, it’s also quiet for central banks, with the only G20 decision coming from the Reserve Bank of Australia tomorrow: economists expects no change in policy, but we will be watching for clues about whether a rate cut might yet be delivered by the end of the year.

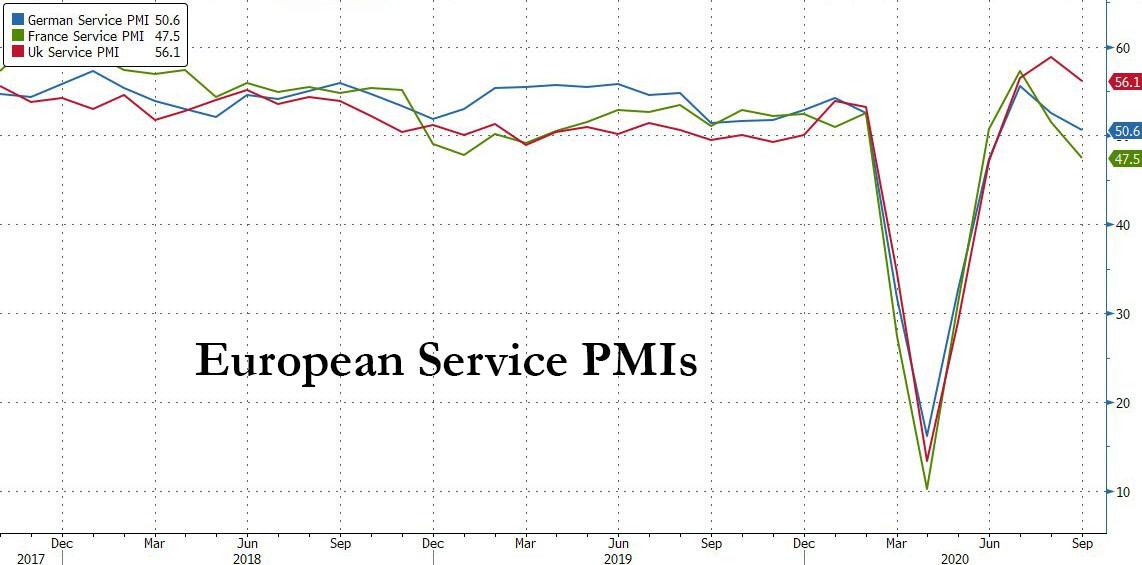

The main data highlight will likely be the release of the services and composite PMIs from around the world. Most are today but the U.K. comes tomorrow and China’s on Thursday after holidays. The flash readings showed clear signs of the services sector in Europe being affected by the second wave of Covid-19, with the flash Euro Area services PMI falling to 47.6, which is below the 50-mark that separates expansion from contraction, with both Germany (49.1) and France (48.5) also in contractionary territory. We will see if this trend is confirmed and whether there was any late month deterioration from the initial flash reading.

Some more observations courtesy of Anthony Cheung and Amplify Trading:

ASIA

Reminder, China on holiday until Friday.

TRUMP

Conflicting reports over the weekend on Trump’s health. Chief of staff, Mark Meadows after he said the president’s vital signs looked troubling which is contradictory to chief physician Sean Conley who said Trump had made “substantial progress” and “spent most of the afternoon conducting business.” He is now on dose two of five of the experimental antiviral drug Remdesivir and is not experiencing any side effects. If things continue to go well, he may be allowed to continue his treatment back at the White House on Monday, his team said.

Net net: Common belief is giving timing, the next few days are key as to whether the virus symptoms become more aggressive or not.

US CALENDAR

The US data focus will be the ISM services survey (Mon) and weekly jobless claims (Thu). Not expecting a great deal from FOMC mins where the Fed updated forward guidance with intro of AIT. Fed Chairman Powell (Tue) is among lots of Fed officials scheduled to give a keynote speech on the economic outlook this week (Weds), expect more calls for fiscal stimulus.

Last weeks markets were ultra sensitive to stimulus talk developments so the same level of vigilance is warranted this week. Pelosi on Sunday said progress was being made on coronavirus relief legislation. Following a contentious first presidential debate, focus will now shift to Wednesday’s VP debate between Mike Pence and Senator Kamala Harris (Wednesday).

ECB

Recent “sources” reported that splits among the Governing Council were already apparent at the last ECB meeting, so we may see more divergent opinions in the accounts from the Sept meeting. Apparently the hawks wanted to quietly slow the pace of PEPP buying and thought the macro forecasts were too pessimistic, while the doves wanted a stronger warning against EUR strength (TD). There will also be a whole host of ECB speakers running from Tuesday through Thursday. Lagarde speaks twice on Tuesday.

RBA

Speculation about a possible rate cut from the Reserve Bank of Australia has risen in the past few weeks, and next week’s RBA meeting will therefore be an important one. We do not expect a rate cut, although a shift to a more dovish rhetoric may be on the cards. The futures market seems to be pricing in around a 68% chance of a cut at this meeting, so we think the balance of risks for AUD is slightly tilted to the upside next week.

OIL

Libya’s oil output has risen to 295,000 barrels (eastern ports of Hariga, Brega and Zueitina) following a truce in the OPEC nation’s civil war and the lifting of a blockade on energy facilities. Saudi Arabia’s Finance Ministry sees oil prices at around $50 a barrel for the next three years, according to Goldman Sachs Group Inc.’s analysis of the kingdom’s pre-budget statement.

* * *

A day-by-day calendar of key events is below, courtesy of Deutsche Bank:

Monday October 5

Data: September services and composite PMIs from Japan, Russia, Italy, France, Germany, Euro Area UK, Brazil and US, Euro Area August retail sales, US September ISM services index

Central Banks: Fed’s Evans, Bostic speak

Tuesday October 6

Data: Germany August factory orders, September construction PMI, UK September construction PMI, Canada August international merchandise trade, US August trade balance, JOLTS job openings

Central Banks: Reserve Bank of Australia monetary policy decision, ECB President Lagarde, Chief Economist Lane, Fed Chair Powell, and Fed’s Harker, Bostic and Kaplan speak

Wednesday October 7

Data: Japan preliminary August leading index, Germany August industrial production, Italy August retail sales, US weekly MBA mortgage applications, August consumer credit

Central Banks: FOMC release meeting minutes, ECB President Lagarde, ECB’s Villeroy, Fed’s Rosengren, Bostic, Kashkari, Williams, Evans speak

Politics: US Vice Presidential Debate

Thursday October 8

Data: Japan August current account balance, China September services and composite PMI, Bank of France September industry sentiment indicator, Germany August trade balance, Canada September housing starts, US weekly initial jobless claims

Central Banks: ECB release monetary policy account, Bank of England Governor Bailey, Bank of Canada Governor Macklem, ECB’s Schnabel and Hernandez de Cos speak

Friday October 9

Data: UK August GDP, France August industrial production, Italy August industrial production, Canada September net change in employment, unemployment rate, US final August wholesale inventories

* * *

Looking at just the US, the key economic data releases this week are the ISM non-manufacturing index on Monday and initial jobless claims on Thursday. In addition, minutes from the September FOMC meeting will be released on Wednesday. There are numerous scheduled speaking engagements by Fed officials this week, including Fed Chair Powell on Tuesday and New York Fed President Williams on Wednesday.

Monday, October 5

09:45 AM Markit US services PMI, September final (consensus 54.6, last 54.6)

10:00 AM ISM non-manufacturing index, September (GS 55.9, consensus 56.1, last 56.9); While our non-manufacturing survey tracker increased (+1.3pt to 54.7), its level remains somewhat below the ISM non-manufacturing index. We also note scope for the ISM supplier deliveries component to retrench after its sharp rebound in last month’s report (+5.3pt to 60.5). Taken together, we estimate the ISM non-manufacturing index declined by 1.0pt to 55.9 in September.

10:45 AM Chicago Fed President Evans (FOMC non-voter) speaks; Chicago Fed President Charles Evans will give a luncheon address to the annual meeting of the National Association for Business Economics in Chicago. Prepared text is expected.

03:15 PM Atlanta Fed President Bostic (FOMC non-voter) speaks: Atlanta Fed President Raphael Bostic will speak on regulating fintech at a Fintech South event. Audience Q&A is expected.

Tuesday, October 6

08:30 AM Trade balance, August (GS -$66.4bn, consensus -$66.4bn, last -$63.6bn): We estimate the trade deficit increased by $2.8bn further in August, reflecting an increase in the goods trade deficit.

10:00 AM JOLTS job openings, August (consensus 6,500k, last 6,618k)

10:40 AM Fed Chair Powell (FOMC voter) speaks: Fed Chair Jerome Powell is the keynote speaker at the annual meeting of the National Association for Business Economics in Chicago. Powell will speak on the U.S. economic outlook and take questions from a moderator. Prepared text is expected.

11:45 AM Philadelphia Fed President Harker (FOMC non-voter) speaks: Philadelphia Fed President Patrick Harker will discuss machine learning in a webinar hosted by the Global Interdependence Center. Prepared text and audience Q&A are expected.

02:00 PM Atlanta Fed President Bostic (FOMC non-voter) speaks: Atlanta Fed President Raphael Bostic will speak to Leadership Florida about “An Inclusive Recovery.” Audience Q&A is expected.

04:00 PM Dallas Fed President Kaplan (FOMC voter) speaks: Dallas Fed President Robert Kaplan will discuss the U.S. and global economy with Bank of Mexico Governor Alejandro Díaz de Leónin in a webcast.

Wednesday, October 7

01:00 PM Boston Fed President Rosengren (FOMC non-voter), Atlanta Fed President Raphael Bostic (FOMC non-voter), and Minnesota Fed President Neel Kashkari (FOMC voter) speak; Boston Fed President Eric Rosengren, Atlanta Fed President Raphael Bostic, and Minnesota Fed President Neel Kashkari will host a virtual series titled “Racism and the Economy.”

02:00 PM Minutes from the September 15-16 FOMC meeting; At its September meeting, the FOMC left the target range for the policy rate unchanged at 0-0.25%, as widely expected. The FOMC also introduced new forward guidance which delays liftoff until the economy has reached maximum employment and inflation has risen to 2% and “is on track to moderately exceed 2 percent for some time.” The FOMC chose not to provide a timeline for asset purchases and did not change the composition of its Treasury purchases. In the minutes, we will look for further discussion on the forward guidance and asset purchase policies.

02:00 PM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will moderate a discussion with Henry Kissinger in an event hosted by the Economic Club of New York.

03:00 PM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will discuss flexible average inflation targeting with John Taylor at an event hosted by the Hoover Economic Policy Working Group.

04:30 PM Chicago Fed President Evans (FOMC non-voter) speaks: Chicago Fed President Charles Evans will discuss the U.S. economic outlook in a virtual event hosted by the Metals Service Center Institute. Prepared text is expected.

Thursday, October 8

08:30 AM Initial jobless claims, week ended October 3 (GS 810k, consensus 820k, last 837k); Continuing jobless claims, week ended September 26 (consensus 11,400k, last 11,767k): We estimate initial jobless claim decreased to 810k in the week ended October 3.

Friday, October 9

10:00 AM Wholesale inventories, August final (consensus +0.5%, last +0.5%)

12:10 PM Boston Fed President Rosengren (FOMC non-voter); Boston Fed President Eric Rosengren will speak on “Economic Fragility: Implications for Recovery from the Pandemic” at the virtual Marburg Memorial Lecture hosted by Marquette University. Prepared text and audience Q&A are expected.

02:00 PM Atlanta Fed President Bostic (FOMC non-voter) speaks; Atlanta Fed President Raphael Bostic will speak in a panel discussion to the Rework America Alliance group.

Source: Deutsche Bank, Goldman, BofA

via ZeroHedge News https://ift.tt/3nk2oSg Tyler Durden

Though I don’t follow the news in the Netherlands much, I happened to see something the other day that I think is a “beautiful” example of why so many countries get their “measures” wrong, their lockdowns, facemasks etc.

First of all, they all screwed up their initial lockdowns, which pretty much were March-June all over. And second lockdowns are more something they like to threaten people with than actually considered options. Unless things really get out of hand, if for instance numbers of deaths suddenly increase a lot, but given the change towards infections occurring in much younger people than before, that is not likely. Plus, of course, no-one wants even more economic damage.

And now what you see is the politicians don’t know what to do anymore. They turn to “their scientists” again, but many have before given advice that is different from what they say now, that hasn’t worked, and that often contradicts what their colleagues in other countries say. And so everyone starts blaming “the people”.

But the people have mostly obeyed the lockdowns and become experts themselves, or so they think, and seen them go nowhere. That makes the positions of politicians and “experts” much weaker than it was 6-7 months ago. It’s about credibility, and they’ve squandered it. Why “must we listen to the scientists” if that does us no good?

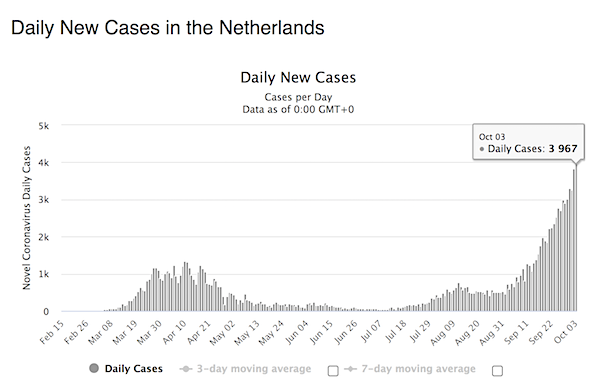

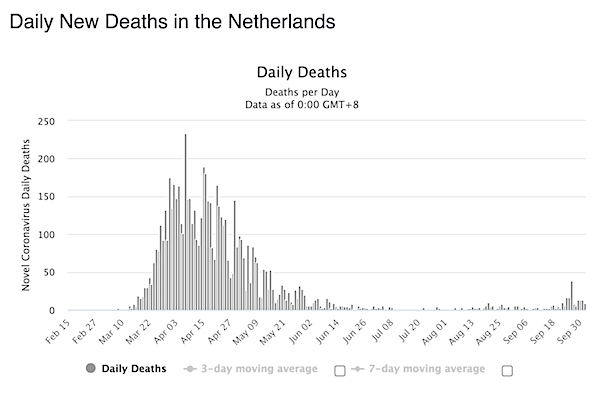

The Netherlands, like many European countries, is in a second wave that is seeing many more new daily cases than in spring. Partly due to more testing, but not entirely:

The number of deaths does not show a similar trend, which can be contributed to the infections mostly occurring in much younger people, and of course a better understanding in medical circles of the virus. However, hospitals are still filling up much faster than in June-July, and many younger people, too, end up with damaged brains, lungs, hearts etc.

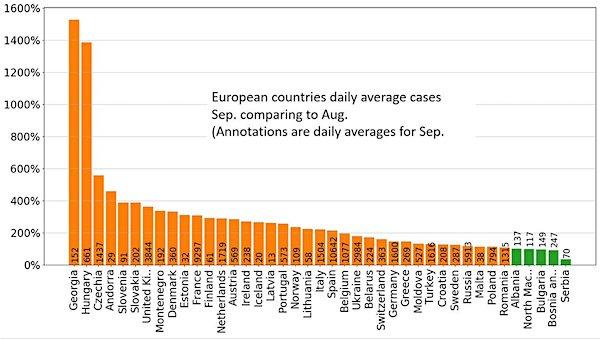

This recent chart of the difference between August and September infection numbers throughout Europe is skewed because of the insane increases in Hungary and Georgia, but it shows that a 300% increase was entirely normal in that timeframe.

So what now?

The Dutch government came with a whole new set of measures starting October 2. Because people “don’t obey the rules”. And people increasingly say: maybe the rules are not right. By the way, facemasks are not mandatory there in stores and other public places, there is only an “urgent” government advice to wear them. That is different from many other nations. Here are the new measures per Google Translate:

Work from home as much as possible.

Receive up to 3 guests at home.

Children up to and including 12 years are not included.

You may meet with a group of 4 people.

For example in a cinema or restaurant.

Children up to and including 12 years are not included.

A maximum of 30 people may be together in an indoor space.

Children count.

Cafes, bars and restaurants close at 10 p.m. You must be gone then. You can enter until 9 p.m.

You provide your name and telephone number. If someone gets sick who has been in the restaurant or cafe, you will receive a call.

You must make a reservation to visit a museum or library.

Stores only allow customers if there is enough space.

In supermarkets there will be special shopping hours for the elderly and the sick (people with poor health).

People with a contact profession must register customers. For example hairdressers.

The first reaction that I have, and I’m sure I’m not the only one: Why 3 people as house guests and not 4? Why 4 people at a restaurant table and not 5, or 30 total in an indoor space? There are family members we haven’t seen since Christmas, but a birthday party is out?

Where do those numbers come from? Did you just make them up? Also, closing bars and restaurants at 10 pm is going to be the death knell for many of the few that are left. Is that worth it?

About that number of 4 people at a restaurant table, the next article from NLTimes about worries in the hospitality sector says that in neighboring Germany and Belgium, 10 people can sit at that same -or preferably a bigger- table. Are Dutch people supposed to drive to those countries if they have a party of 8?

On Wednesday Prime Minister Mark Rutte issued the urgent advice for all Netherlands residents to wear masks in publicly accessible indoor spaces. This advice was met with skepticism, especially from the hospitality industry. Former RIVM director Roel Coutinho would rather have seen a mask obligation instead of advice.

Hospitality association KHN doubts whether the advice to wear masks in public makes sense, the association said in a press release. “The fact that there is still no scientific substantiation by the cabinet and RIVM about the proven usefulness of face masks certainly does not help to create and maintain support. Moreover, face masks still form an extra barrier to visiting establishments.”

If the government turns its advice into an obligation, the KHN wants the Netherlands to follow Germany and Belgium’s example. According to the association, in those countries up to 10 people are allowed at a restaurant table. “Then we will be open to it,” the association said. The KHN also wants extra financial support should masks become mandatory.

Roel Coutinho, who preceded Jaap van Dissel as head of public health institute RIVM, is pleased that the advice to wear masks indoors now applies to the whole of the Netherlands, but regrets that the government did not make it mandatory. “On the basis of all the literature, I am convinced that wearing a face mask is useful. But only advice makes it particularly difficult for people,” he said to Nieuwsuur. “An obligation, as is also happening in countries around us, gives everyone much more clarity.”

An obligation will also help the stores that have to enforce the face mask rule. “Because what exactly should those shops or supermarkets do?” Coutinho said. “Because it only concerns urgent advice, the responsibility now lies with shops, which makes it very difficult. An obligation is not always pleasant, but it is clear and easy to enforce.”

But the best part is the following, the initial piece that got me thinking about this.

Turns out that at the same moment the government issues an “urgent” advice to wear them, with a threat of making them mandatory, its chief Infectious Diseases expert, the Dutch Fauci, says he sees little benefit is wearing non-medical masks. As, ironically, Fauci, who used to say they were useless, now calls them very beneficial.

The frequent use of masks in other countries, the pressure of public opinion in his own country, or even a direct appeal from his famous American counterpart Anthony Fauci: Jaap van Dissel sticks to his position. When asked, the director of Infectious Diseases at the RIVM repeats that, according to him, masks have “an exceptionally small effect” on the attempts to contain the spread of the corona virus. In an interview with the NOS, he calls the cabinet’s recent decision to urgently recommend masks in public indoor spaces, therefore primarily a political decision rather than one based on medical grounds.

Since the start of the corona crisis, Van Dissel has emphasized that he sees little benefit in wearing non-medical face masks, especially because it could evoke a sense of false security and possibly divert attention from other rules. Although he acknowledges that there are studies that signal a positive effect of face masks, he believes they are difficult to extrapolate to the corona crisis.

“For example, medical mouth masks were often used in those studies and measures such as the one and a half meters are not taken into account,” he explains. There are also studies that are less positive about masks, he says. “That leads us to consider that we have not given a positive advice about it. That is just the story. That another decision is taken, based on political considerations, that it should be so.”

In addition, according to Van Dissel, the alleged effectiveness of non-medical face masks is nothing compared to the usefulness of other measures such as keeping sufficient distance from each other, washing hands regularly and staying at home in case of complaints. Earlier this week, the Outbreak Management Team, the advisory body of the cabinet which Van Dissel chairs, made some adjustments to the advice on face masks for the first time.

For example, the OMT wrote that masks could be recommended in places where sufficient distance from each other cannot always be kept “such as in busy shops”. For the same reason, a mask has been mandatory in public transport since June. According to Van Dissel, the change in the OMT advice has nothing to do with a changed view of mouth masks, but more to do with people’s sense of safety. “Of course, as OMT, we have also realized that some people would prefer to wear a mouth mask. If someone feels safer, we are fine with that,” he says.

The government says: wear a mask, and its chief scientific adviser says: don’t bother. Great message. And people don’t miss that. I’ve said it before: every government today should have a generous supply of N95 masks ready. They don’t because their experts long said they were not necessary. While some keep claiming cloth masks are useful, but “more to do with people’s sense of safety”.

I don’t know about you, but all these people with these useless masks on where they’re not needed, like outside, don’t make me feel safe at all. They make me think I’m surrounded by fools. And is anyone going to believe that 4 at a table is better than 10? How can they when just across the border the opinion is so different? If you ask me, the time of being able to order your citizens around on what to do and what not, may be ending for many governments. And they have only themselves to blame.

The only realistic thing to do at this point appears to be to give people back their own responsibility. If only because taking it away from them didn’t work.

Leaked Document Reveals Exxon’s Plan To Increase Emissions As Energy Space Prepares For Decarbonization Tyler Durden

Mon, 10/05/2020 – 09:19

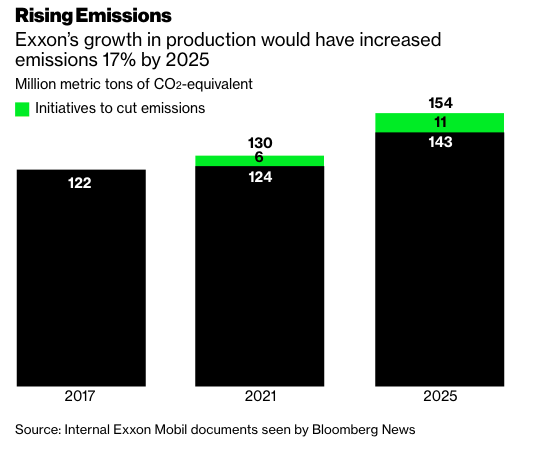

As oil majors prioritize their own decarbonization goals, an internal document viewed by Bloomberg reveals Exxon Mobil Corp. is planning to increase annual carbon-dioxide emissions output by as much as a small country like Greece.

Exxon is one of the biggest corporate emitters of greenhouse gasses globally, and the leak comes as the Texas-based company’s rivals, such as BP Plc and Royal Dutch Shell Plc, are planning, or have already begun, to shrink oil and gas operations to become net-zero on carbon by 2050 or before.

The internal document revealed Exxon’s stunning investment strategy of more than $200 billion in energy investments that would increase its emissions by about 17% through 2025. These investments are projected to drive higher cash flows and double earnings. However, much of the strategy was developed in pre-virus pandemic times and has yet to be revised for a post-pandemic world of lower oil demand and collapsing energy prices.

But the planning documents show for the first time that Exxon has carefully assessed the direct emissions it expects from the seven-year investment plan adopted in 2018 by Chief Executive Officer Darren Woods. The additional 21 million metric tons of carbon dioxide per year that would result from ramping up production dwarfs Exxon’s projections for its own efforts to reduce pollution, such as deploying renewable energy and burying some carbon dioxide.

These internal estimates reflect only a small portion of Exxon’s total contribution to climate change. Greenhouse gases from direct operations, such as those measured by Exxon, typically account for a fifth of the total at a large oil company; most emissions come from customers burning fuel in vehicles or other end uses, which the Exxon documents don’t account for.

That means the full climate impact of Exxon’s growth strategy would likely be five times the company’s estimate—or about 100 million tons of additional carbon dioxide—had the company accounted for so-called Scope 3 emissions. If its plans are realized, Exxon would add to the atmosphere the annual emissions of a small, developed nation, or 26 coal-fired power plants. –Bloomberg

Despite Exxon’s massive investment plan, plunging oil demand has resulted in a collapse in energy prices, which has in turn weighed on the company’s shares, as has being kicked out of the Dow. This drop in demand forced Exxon to slash its spending budget by a third in April, and its share price currently hovers around March lows.

The company recently warned of continued quarterly losses while using debt to pay capital expenditures and dividends. Over the summer, the company delayed oil and gas projects to preserve cash.

Exxon clearly lags behind other oil majors in addressing plans to tackle global warming, as the pandemic has forced many oil companies to start the transition toward developing energy with cleaner sources.

“It’s past time for Exxon Mobil to take responsibility for the harmful impacts of its oil and gas products,” said Mulvey of the Union on Concerned Scientists. “The world at large and its own investors would benefit from Exxon redirecting its strategy toward the energy we need in a low-carbon future.”

It’s also possible that Exxon’s strategy of going all-in on investment stems from the same trend that led to Rex Tillerson, the company’s former top executive, serving under the Trump administration as Secretary of State between 2017-18, as Exxon has sought to capitalize on Trump’s push to expand American “energy dominance”.

via ZeroHedge News https://ift.tt/33v47Mn Tyler Durden

“In Short Trump Is Really Sick; Or Trump Is Faking; Or Trump Is Recovering But Not Out Of The Woods Yet” Tyler Durden

Mon, 10/05/2020 – 09:01

By Michael Every of Rabobank

Back in early 2020, one of the ‘signs that things were really getting serious’ for the always-astute media was that the latest Bond movie, ‘No Time to Die’, was postponed for release until October. Now it is October, and it has been postponed again until April 2021. Moreover, the UK cinema chain Cineworld is suspending operations because business is not viable as virus restrictions stand; and the global chain AMC apparently only has enough cash for the next six months. In short, the movie industry –how we watch them, and so the money for how they are made, if they are made– could be dying, indicative of a whole key slice of the service-sector economy.

The title of the Bond film is obviously ironic given the backdrop of Covid-19. Doubly so given the film itself looks like it could easily die at the box office anyway when it is released: the trailer looked staggeringly generic, and its plot –about an eco-terrorist who has to kill everyone to save the planet– is totally unoriginal (Spy Who Loved Me? Moonraker?) and already eclipsed by reality around us, from environmental protests to Covid-19.

On which, real life is indeed better than a movie. US President Trump tests positive for Covid-19; seems fine; is then hospitalised; his doctors give North Korea style positive assessments; leaks say things are far more serious; he goes on a Popemobile style drive outside; and he might even be discharged today, after releasing a video in which he certainly looked healthy, even though everyone knows that it is the next few days that are critical with this virus. As Scott Adams might say, if this is all a movie, what is the ending you then project? Not just philosophically, but practically, this is all just about clinging on to narratives.

If the Walter Reed press sessions are a bit too banana republic-y, what can one say about the countervailing media and social media? On my own feed I have comments from leading journalists and economists, intelligent people all, who claim variously that: Trump is not ill and this is all an election ploy; Trump is in fact close to death and all his videos are staged; Trump knew he was infectious long before he was and deliberately tried to spread the disease; and that Trump needs to be replaced by VP Pence via the 25th amendment immediately, even though he may be discharged today. Just to underline, this is all coming direct from the intelligentsia, not the bazaar. Though it is bizarre.

Allow me to add this academic note (Giry, 2020) on conspiracy theories: they “are used to reaffirm the dominant and established values of an in-group while identifying and subsequently portraying outsiders in a negative light. Conspiracy theories express a reductionism that serves and contributes to uphold, promote and reinforce conventional behaviours, while discrediting or delegitimising inappropriate or marginal ones.”) Isn’t that dynamic as evident today from a deeply-rattled neoliberal establishment as it is from the angry populists neoliberalism created?

Of course, all of what we deal with in life is a story – even at work. In markets, you deal with either data or news-feed as the inputs for your decision-making; and if you lift the lid on data or news, you find it is all just a narrative too.

How about ‘hedonic quality adjustments’ on inflation that mean if the price of steak goes up, they assume you buy more chicken instead? The magical thinking on the Aussie labour market, where cities full of jobs come and go every month? That US initial claims suddenly had their methodology changed just as they are needed as a guide for the first time in decades? And I haven’t even mentioned huge backwards revisions that change the story years later. Or underfunded national data services struggling to keep up with structural change in the economy. Or data with Chinese characteristics.

Back to today: how about opinion polls, which sit between data and news? Two just out show Trump is within the margin of error vs. Biden, or beating him in the electoral college; yet an NBC/WSJ survey puts Biden 14 points ahead and set for landslide win. How does one account for this? Either by doing a deep-dive on the internals (sample size; geographic distribution; method of polling and the inherent errors therein; registered voters vs. likely voters; the assumed party mix vs. recent trends in both voter registration and enthusiasm surveys; the assumed demographic mix in times of change in such, etc.)… or by ignoring all that and seizing the poll preferred as one’s narrative.

Likewise, pure journalism is increasingly, deliberately partisan in what it does and doesn’t talk about – because that sells better to those wanting the narrative. As Twain put it, “If you don’t read the newspaper, you are uninformed. If you read the newspaper, you are misinformed.” (And if you read this Daily, you are probably either bored or confused – or very angry, based on some of the replies I get.)

On which, the press is now saying more US fiscal stimulus finally seems likely, probably helped by the sub-consensus payrolls data on Friday, showing economic momentum is ebbing. No time to waste if the recovery isn’t going to die, for sure.

Not so much global coverage today of China’s semiconductor giant SMIC saying that it is finding it hard to get key supplies due to its US blacklisting; or that the US is starting to enforce its long-standing immigration rules that prevent members of the communist party from immigrating there.

So, in short Trump is really sick; or Trump is faking; or Trump is recovering but not out of the woods yet. And Trump is going to lose; or Trump is going to win. And stimulus isn’t going to happen; or stimulus is going to happen. And so risk on; or risk off.

Man makes trades and markets laugh.

(And so do Aston Villa fans: reality really can trump fantasy in 2020, it seems.)

via ZeroHedge News https://ift.tt/30xJqxw Tyler Durden

Regal-Owner Cineworld Could Suspend All US, UK Operations Next Week Tyler Durden

Mon, 10/05/2020 – 08:46

Cineworld, a British cinema company and the world’s second-largest movie theater chain, is expected to close all of its US movie theaters this coming week, after a brief reopening in mid-summer, according to WSJ, citing a source familiar with the matter.

The final decision to close more than 500 US theaters could be announced as early as Monday or Tuesday, the source said. Cineworld operates US theaters under the Regal brand, the largest and most geographically diverse theater circuits in the US, consisting of 7,211 screens in 549 theaters in 42 states. Regal began reopening theaters in July/August as public health restrictions eased, but indoor capacity was limited.

Readers may recall, in mid-September, even though Hollywood released Christopher Nolan’s “Tenet,” that didn’t necessarily mean consumers flocked back to indoor commercial spaces to watch the flick as the virus pandemic showed little signs of abating. Shown below, one Regal theater in Baltimore was a ‘ghost town’ around the release of Tenet.

Potential drivers behind the closures, which by the way, the source said “isn’t definite,” could be due to low foot traffic at theaters; it actually might make sense for theaters to shutter operations, layoff employees, tap the equity or debt markets, and formulate a relaunch plan when a vaccine is commercialized. Otherwise, as seen this past summer, a premature reopening will be perceived by consumers as irresponsible.

Another driver could be the lack of big-budget film releases, with the new James Bond movie, “No Time To Die,” had to postpone its release to 2021. With the lack of exciting films and consumer behavior shunning indoor theaters, there’s really no need to keep theaters open.

According to Reuters, Cineworld warned investors on Sept. 24 that it may have to raise a second round of cash early next year if the coronavirus pandemic persists. The movie theater operator had enough funds to keep operating after reporting a massive $1.6 billion loss for the first six months of 2020 as revenues crashed by 67%.

“There can be no certainty as to the future impact of Covid-19 on the group,” Cineworld said in a statement.

The anemic box office open is more evidence that consumers aren’t ready to step back inside theaters anytime soon. The National Association of Theatre Owners (NATO) outlined smaller theater chains face a bankruptcy wave:

“If the status quo continues, 69% of small and midsize movie theater companies will be forced to file for bankruptcy or to close permanently,” NATO wrote in a written statement.

Suspending operations could be Cineworld’s best bet to survive the virus pandemic. It’s only a matter of time before other large chains do the same.

via ZeroHedge News https://ift.tt/2StRvyY Tyler Durden

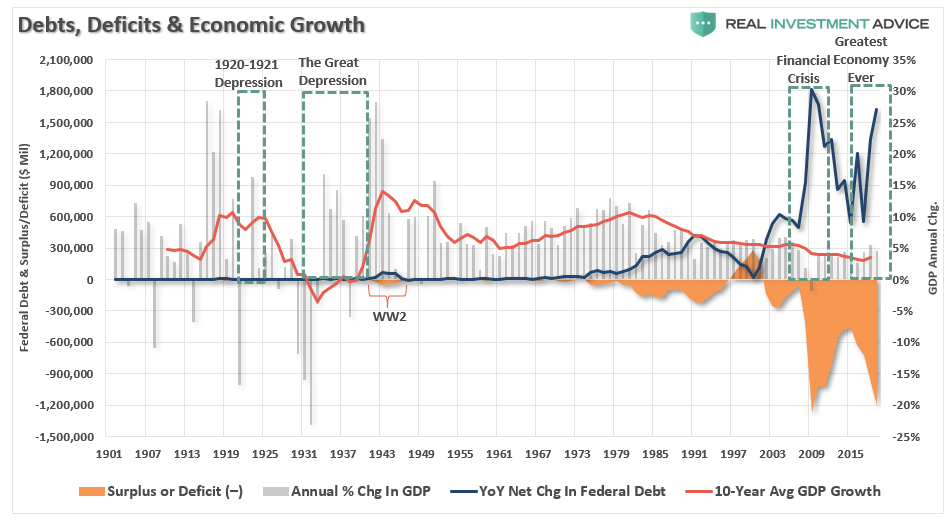

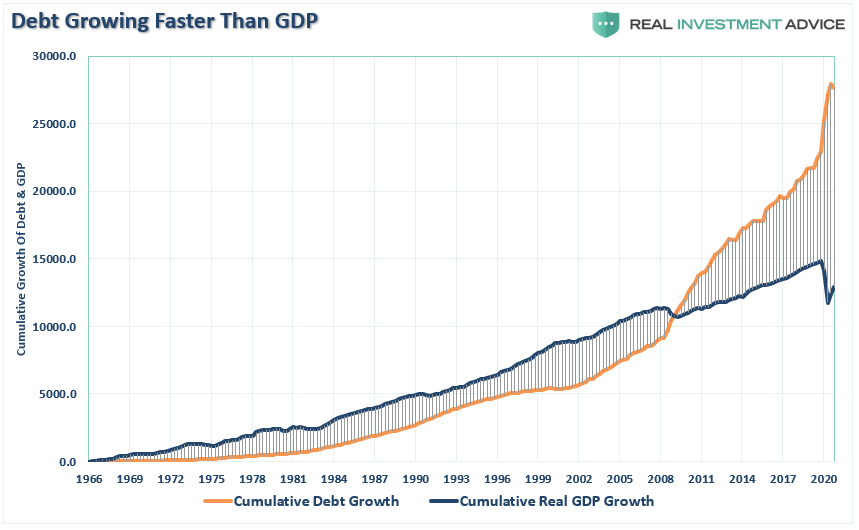

We have frequently discussed the “one-way trip” of American debt and the long, slow slide into the “Japanification”of America.

The amount of outstanding debt, and the subsequent deficit, has long been a problem in the U.S. For the last two decades, policymakers have made annual promises for more substantial economic growth. Yet with each passing year, growth rates weaken, and economic prosperity worsens. As we discussed pre-pandemic in “Economy Should Grow Faster Than Debt:”

“The chart below shows the deficit, 10-year average GDP growth, and the annual change in Federal Debt. The problem should be obvious. Since the Federal government began ramping up debt, and running deficits, growth continues to deteriorate. Such is not a coincidence.”

“The government is already running a massive deficit. It also expects to issue another $1.5-2 Trillion in debt during the next fiscal year. The efficacy of ‘deficit spending’ in terms of its impact on economic growth has been greatly marginalized.”

Spending Without Controls

Since then, Government debt surged n response to the “Coronavirus Pandemic,” to provide fiscal support. Concurrently, the drop in economic activity has dramatically reduced Federal revenues to pay for it all.

Unfortunately, this also means the CBO’s already catastrophic long-term debt forecast has become even more disastrous. It already requires over 100% of all Federal revenues to cover mandatory spending. Such was a point in the most recent Long-Term Budget Outlook report from the CBO.

“Once the effects of decreased revenues associated with the economic disruption caused by the pandemic dissipate, revenues measured as a percentage of GDP will rise. After 2025, CBO’s projections increase largely due to scheduled changes in tax rules. Such includes the expiration of nearly all of the changes made to individual income taxes by the 2017 tax act. After 2030, they continue to rise. But that growth does not keep pace with the growth in spending. Most of the long-term growth in revenues is attributable to the increasing share of income that is pushed into higher tax brackets.” – CBO

Deficits Set To Grow

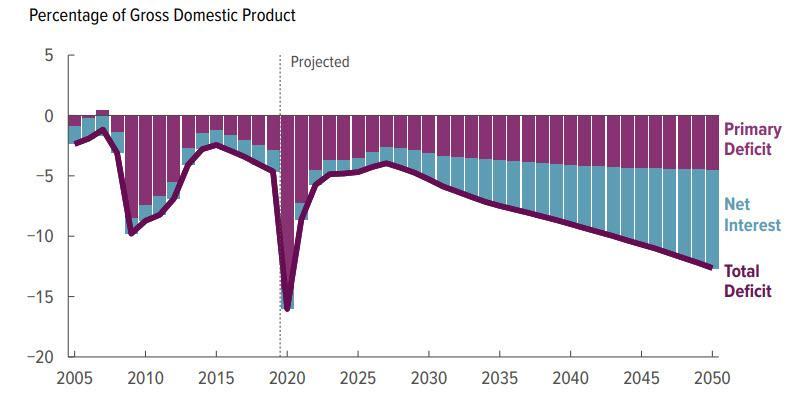

Of course, to fund the excess spending by the Government, the debt burden and subsequent debt service will continue to grow.

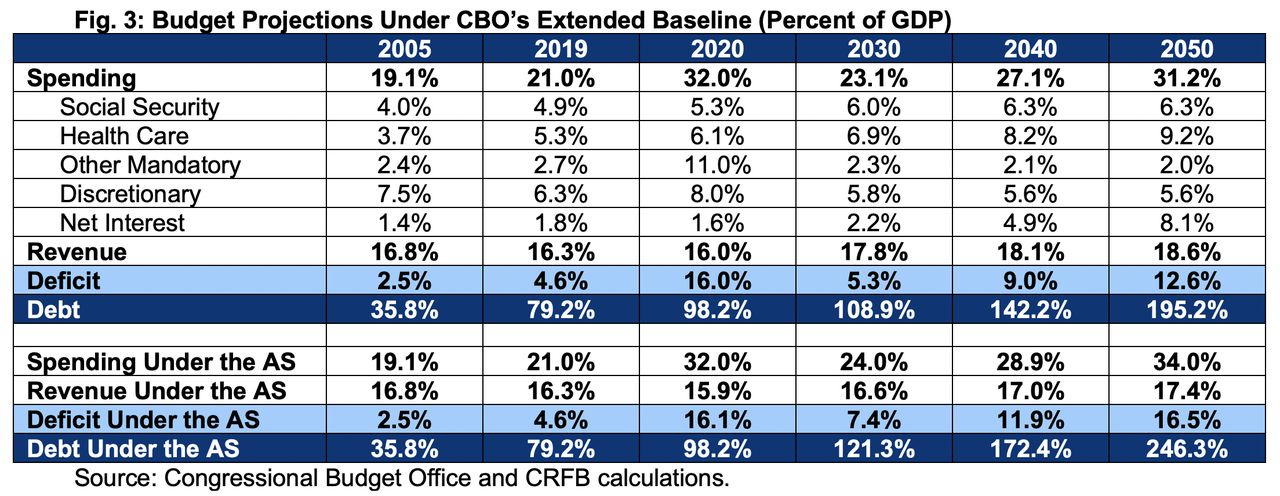

“Deficits increase again in the last few years of the decade, reaching 5.3 percent of GDP in 2030. That level is historically high and more than one-and-a-half times the average over the past 50 years (3.0 percent of GDP).

In the second and third decades of CBO’s projection period, deficits grow from 5.3 percent of GDP in 2030 to 9.0 percent by 2040. They hit 12.6 percent by 2050. Over that 20-year period, deficits average 9.0 percent of GDP, which is higher than their 50-year average of 3.0 percent of GDP.” – CBO

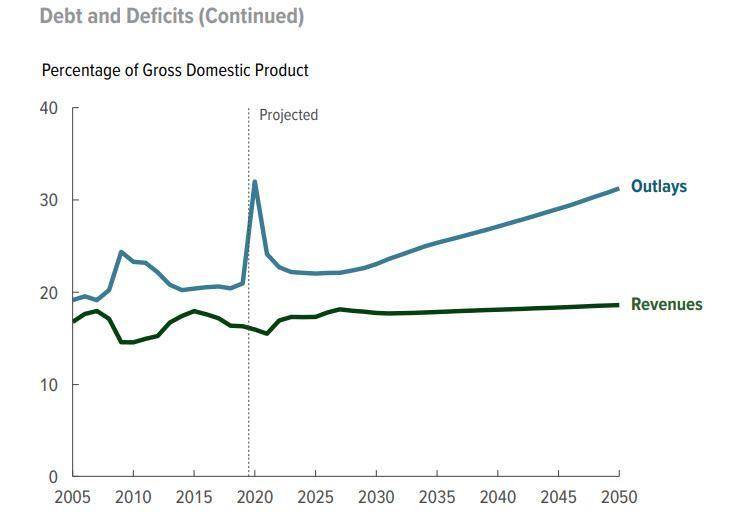

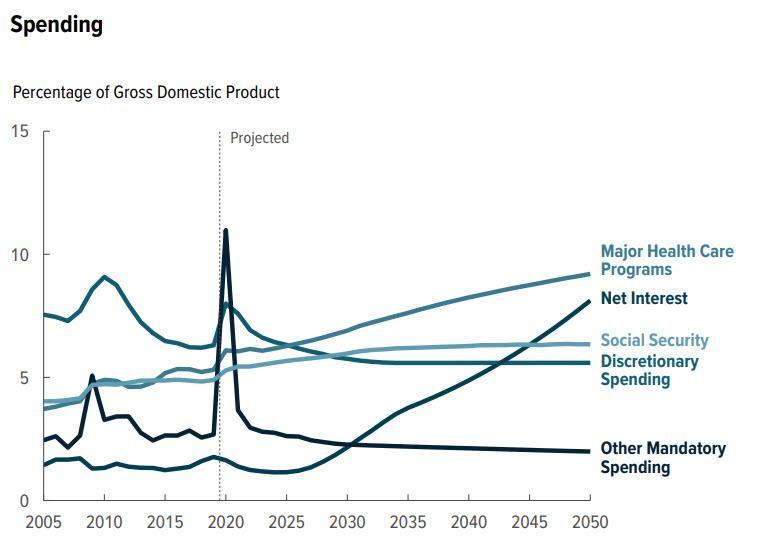

Spending Set To Increase

Note what is driving the deficit. The mandatory spending, comprised of Social Security, Medicare, Medicaid, prescription drug benefits, and the Affordable Care Act, also includes interest on the debt.

Given rising debt levels erode economic growth, as it displaces revenue from productive uses, debt continues to grow to support “mandatory spending” requirements.

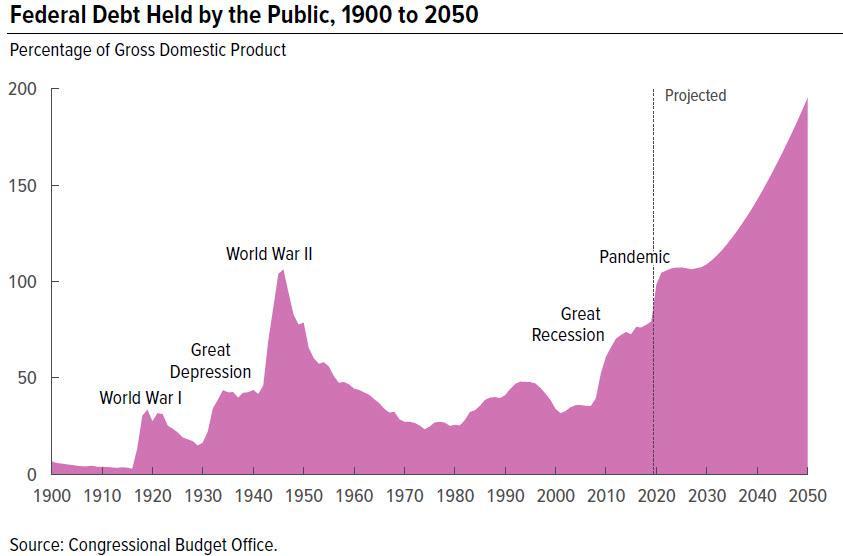

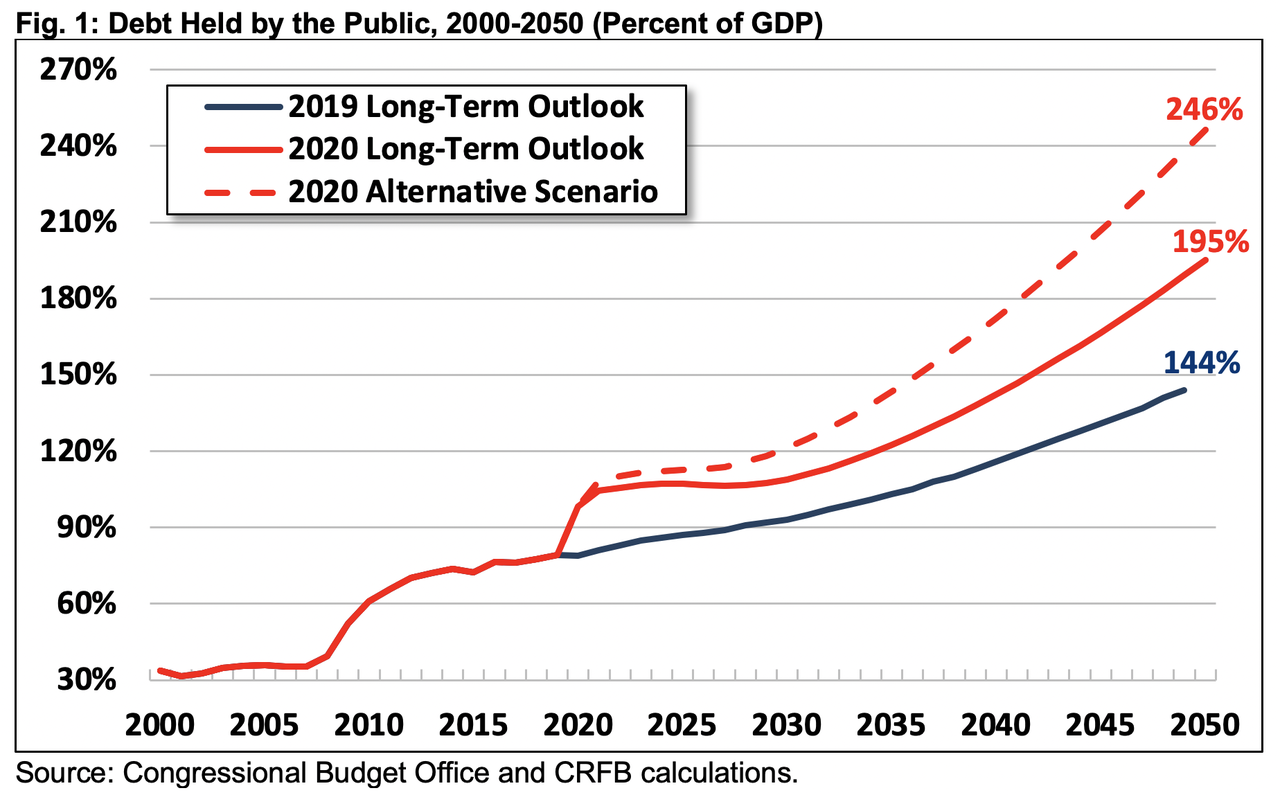

“Debt continues to increase in most years thereafter, reaching 195 percent of GDP by 2050. That amount of debt will be the highest in the nation’s history, and will increase further. High and rising federal debt makes the economy more vulnerable to rising interest rates and, depending on how the debt is financed, rising inflation. The growing debt burden also raises borrowing costs and slows the growth of the economy and national income. There is an increased risk of a fiscal crisis or a gradual decline in the value of Treasury securities.” – CBO

As the CBO further explains:

Debt as a percentage of GDP will increase in most years as the government incurs budget deficits larger than the growth of the economy. If current laws generally remain unchanged, federal deficits will be substantially larger over the next 30 years than over the past 50 years. In CBO’s projections, deficits rise after 2030 as mandatory spending, outlays for the major health care programs, and interest payments grow faster than revenues.

“Projected debt in 2050 is nearly five times higher than the 50-year average of 42 percent of GDP. It will be on track to double the previous record of 106 set just after World War II. In dollar terms, debt will rise from nearly $21 trillion today to $121 trillion by 2050.”

“Actual debt levels could grow significantly faster than CBO forecasts. Under our alternative scenario, debt would reach 246 percent of GDP in 2050.

Even under current law, high and rising debt represents a large fiscal gap. For example, CBO estimates policymakers would need to enact 3.6 percent of GDP in spending cuts and tax increases starting in 2025. Such actions could restore the debt to 2019 levels by 2050. That’s the equivalent of cutting all spending by one-sixth or increasing all revenue by one-fifth.”

Neither of those things will happen.

Spending Will Be Higher

As we showed previously, at the end of 2019, we were already spending more than we brought in.

“Here is the real kicker. In 2018, the Federal Government spent $4.48 Trillion, which was equivalent to 22% of the nation’s entire nominal GDP. Of that total spending, ONLY $3.5 Trillion was financed by Federal revenues and $986 billion was financed through debt.

In other words, if 75% of all expenditures is social welfare and interest on the debt, those payments required $3.36 Trillion of the $3.5 Trillion (or 96%) of revenue coming in.”

The CFRB report expands on this analysis with future projections.

Rising debt and deficits are driven by a disconnect between spending and revenue. CBO expects spending to grow rapidly over the next three decades and revenue to grow gradually.

The 11.7 percent of GDP growth in Social Security, health, and interest costs explains more than the entire 10.3 percent growth in total spending through 2030. Meanwhile, revenue will only grow by 2.3 percent of GDP – failing to cover the rising cost.

Here is the real problem as we advance:

Rising health and retirement costs and insufficient funding also puts trust funds in danger. On a combined basis, CBO estimates the Social Security trust funds will run out in calendar year 2031 and face a 75-year shortfall of 1.6 percent of GDP, or 4.7 percent of taxable payroll.

Slower Economic Growth

The underlying structure of the economy continues to weaken as non-productive debt erodes growth. As discussed just recently in “Debts, Deficits & The Path To MMT:”

“The relevance of debt growth versus economic growth is all too evident. When debt issuance exploded under the Obama administration and accelerated under President Trump, it has taken an ever-increasing amount of debt to generate $1 of economic growth.”

Such reckless abandon by politicians is simply due to a lack of “experience” with the consequences of debt.

However, as the CFRB stated:

“Unfortunately, the actual fiscal situation could turn out to be even worse than CBO projects.

CBO estimates stabilizing debt at 2019 levels would require annual tax and spending adjustments between 2025 and 2050. Such would be equivalent to 3.6 percent of GDP. A carefully crafted package could be phased in gradually, targeted to ask the most from those who can best afford it. It could be designed to improve economic growth and thus reduce the burden of any adjustments. However, there is no magic wand we can wave to fix these problems

While policymakers should prioritize addressing the current pandemic and economic crisis, they cannot and should not continue to ignore our dangerous long-term fiscal situation.”

Ratcheting Growth Down Again

As the CFRB states, ignoring the issue will only lead to longer-term declines in economic growth and prosperity.

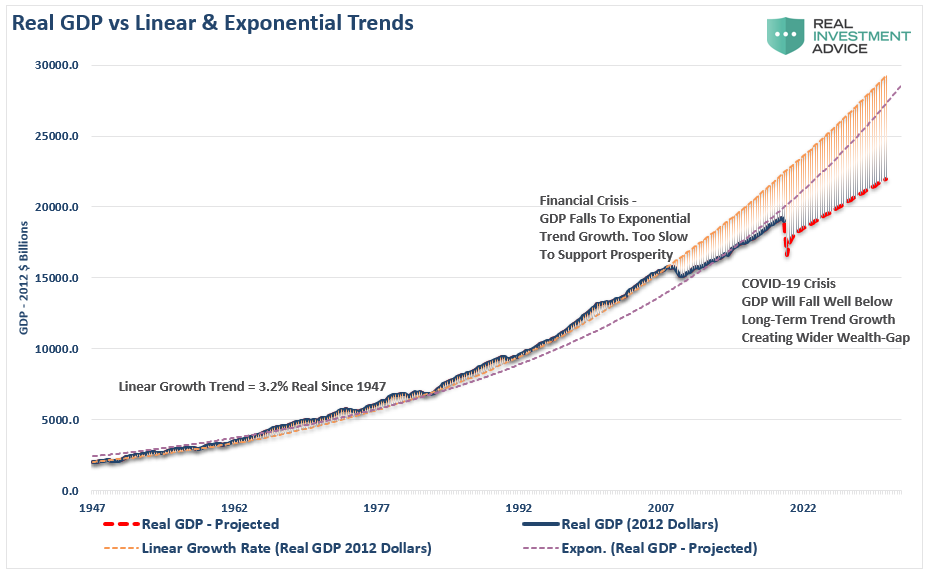

Before the “Financial Crisis,” the economy had a linear growth trend of real GDP of 3.2%. Following the 2008 recession, the growth rate dropped to the exponential growth trend of roughly 2.2%. Instead of reducing the debt problems, unproductive debt and leverage increased.

The “COVID-19″ crisis led to a debt surge to new highs. Such will result in a retardation of economic growth to 1.5% or less, as discussed recently.Simultaneously, the stock market may rise due to massive Fed liquidity, but only the 10% of the population owning 88% of the market benefits. In the future, the economic bifurcation will deepen to the point where 5% of the population owns virtually all of it.

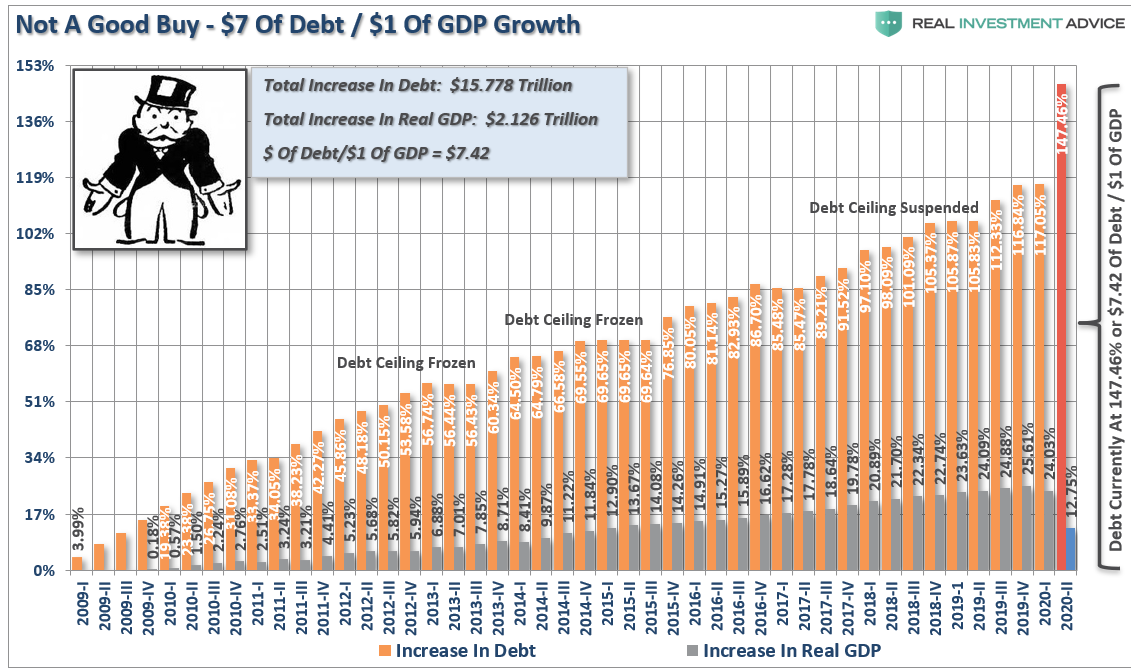

As I noted previously, it now requires $7.42 of debt to create $1 of economic growth, which will only worsen as the debt continues to expand at the expense of more robust rates of growth.

That is not economic prosperity. It is a distortion of economics.

Hypocritical

The CBO’s latest budget projections confirm what we, and the CRFB, have been warning about. The current Administration has taken a path of fiscal irresponsibility, which will take an already dismal fiscal situation and made it worse.

While “conservative” Republicans continually chastised the previous Administration for running trillion-dollar deficits, the Republicans have now decided trillion-dollar deficits are acceptable.

That is entirely hypocritical.

Given the flaws in the CBO’s calculations, their current projections of multi-trillion deficits next year, and exceeding that mark every year after, will likely turn out to be overly optimistic.

Notably, the projected budget deficits in the coming decade are “full-employment” deficits. Such is significant because, while budget deficits can help recessions by providing an economic stimulus, there are good reasons we should be retrenching during good economic times, including the one we are in now.

Conclusion

As President Kennedy once said:

“The time to repair the roof is when the sun is shining.”

Instead, we seem to have just removed the roof altogether.

The fact that debt and deficits had risen under conditions of full employment suggests a more profound underlying fiscal problem existed and has now worsened.

The CBO’s budget projections are a harsh reminder of the consequences of debt and deficits.

“The longer policymakers wait to fix the debt, the harder and costlier it will get. That fiscal gap would grow to 4.4 percent of GDP if action was delayed until 2030, or 5.9 percent if delayed until 2035. Delaying action means the necessary changes will be spread among fewer people. Policymakers will have less ability to carefully target adjustments. And ultimately, it will be harder to phase in new policies or give families and businesses time to prepare and adjust for them.” – CFRB

It is just a function of time until the “bill comes due.”

As we concluded previously, you can make choices today, which may be unpopular, and induce short-term pain for a more robust economy tomorrow. Or, you can wait until creditors force those painful choices upon you all at once.

via ZeroHedge News https://ift.tt/3d1E4jc Tyler Durden

Trump’s Condition Improved Again Overnight, Chief Of Staff Meadows Says Tyler Durden

Mon, 10/05/2020 – 08:15

President Trump’s condition has improved again overnight, according to White House Chief of Staff Mark Meadows.

In an interview with Fox News, Meadows said he expects Trump to depart the White House Monday afternoon.

As we noted earlier, in addition to optimism over a covid vaccine, optimism about the economic recovery, and optimism about a fiscal stimulus, we can now add another category of “optimism” cited by traders to justify overnight futures ramps (at least for the next few days): optimism Trump will be discharged from Howard Reed hospital any day now, perhaps as soon as today, and then stage a full recovery.

Of course, fears that the White House isn’t giving the public ‘the whole story’ will create risks that an errant anonymously sourced report claiming Trump needed another round of supplemental oxygen could send stocks plunging.

Such a turnaround would be remarkably quick, especially for a patient with at least two comorbidities: Trump’s age, and the fact that he’s “slightly overweight”, as Dr. Sean Conley said.

But National Security Advisor Robert C. O’Brien said in an interview with one of the Sunday shows that Trump was “in great shape and firmly in command of the country” while he is being treated from coronavirus.

via ZeroHedge News https://ift.tt/2SsPLpz Tyler Durden

Markets Rally On Optimism Trump May Be Discharged As Soon As Today Tyler Durden

Mon, 10/05/2020 – 08:07

In addition to optimism over a covid vaccine, optimism about the economic recovery, and optimism about a fiscal stimulus, we can now add another category of “optimism” cited by traders to justify overnight ramps in equity futures – at least for the next few days: optimism Trump will be discharged from Howard Reed hospital any day now (perhaps as soon as today), and then enjoy a full recovery. Sure enough, on Monday US index future bounced after doctors said Trump could be discharged from Howard Reed imminently, while sentiment was also lifted amid tentative signs of progress on a new fiscal stimulus.

Late on Sunday Trump released a series of videos in an effort to reassure the public that he is recovering (following by a frenzied tweetstorm on Monday morning), although his condition remains unclear and outside experts warn that his case may be severe. Trump also surprised supporters outside Walter Reed with an impromptu drive through, even as it earned him a fresh round of anger by liberal commentators.

Feeding the improved market tone were comments from House Speaker Nancy Pelosi, who said on Sunday that progress was being made in talks with Treasury Secretary Steven Mnuchin on a new bipartisan package of coronavirus relief measures, although she has said exactly the same thing for weeks now, yet neither party is willing to budge and make the much needed final compromise. Doubts about the scale of further fiscal aid and a slowing economic recovery have weighed on the S&P 500 recently, with the benchmark index in September logging its worst month since the coronavirus-driven crash earlier this year.

At 730am, Dow e-minis were up 206 points, S&P 500 e-minis were up 23.75 points, or 0.72%, and Nasdaq 100 e-minis were up 100.75 points, or just under 1%. This follows a furious short covering spree in NQs last week, as discussed previously.

In premarket trading, Regeneron rallied after Trump was given an experimental antibody treatment made by the drugmaker. Tech gigacaps Apple, Nvidia, Netflix, Amazon.com, Microsoft and Tesla all rose after weighing heavily on the Nasdaq on Friday.

Overhanging the relief rally, however, were concerns that Trump’s case could be more severe than public disclosures suggest, and that more restrictive measures by governments to slow coronavirus infections could harm the economic recovery. Some traders were concerned by doctors’ admission that Trump had been given supplementary oxygen and steroids.

“Many questions remain including the use of the steroid drug … which is usually reserved for those with severe illness,” said Raymond James strategist Chris Bailey in London. “Global cases now top 35 million and various new restrictions in Paris, New York, etc”.

Trump’s infection also comes less than one month before the presidential election on Nov. 3, potentially fuelling more market volatility and making the outcome of the vote even more difficult to predict. “In terms of the impact on the election, we haven’t seen enough polling to assess whether this increases or decreases his chances of winning,” said Deutsche Bank strategists. According to a Reuters/Ipsos poll released on Sunday, Democrat contender Joe Biden opened his widest lead in a month in the U.S. presidential race. However, the same poll inexplicably polled far more Democrats than Republicans, and we all know what happened in 2016 when “polls” did the same.

The MSCI world equity index was up 0.4%, supported by overnight gains across Asia and a positive start in Europe. The pan-European STOXX 600 rose 0.7%. In Europe, consumer companies and banks led a broad advance. A survey on Monday showed the euro zone’s economic recovery faltered last month as new restrictions sent its dominant service sector into reverse. IHS Markit’s final composite Purchasing Managers’ Index fell to 50.4, just above the 50 mark separating growth from contraction, and down from 51.9 last month.

Equities in Asia notched gains, led by materials and finance, after falling in the last session. Japan’s Topix – which actually managed to stay open without crashing for the entire day – gained 1.7%, with Shimachu and Danto rising the most.

In rates, yields on benchmark 10-year Treasuries rose to 0.7138%, with yields higher by 2bp-3bp at long end, steepening 5s30s toward YTD highs above 123bp; 10-year yields around 0.712%, higher by more than 1bp vs Friday’s close. The long end of Treasury curve was cheaper as U.S. trading got under way. Aussie and Japanese bonds fell in Asia session, adding to long-end pressure. Treasury supply this week includes 10- and 30-year auctions Wednesday and Thursday.

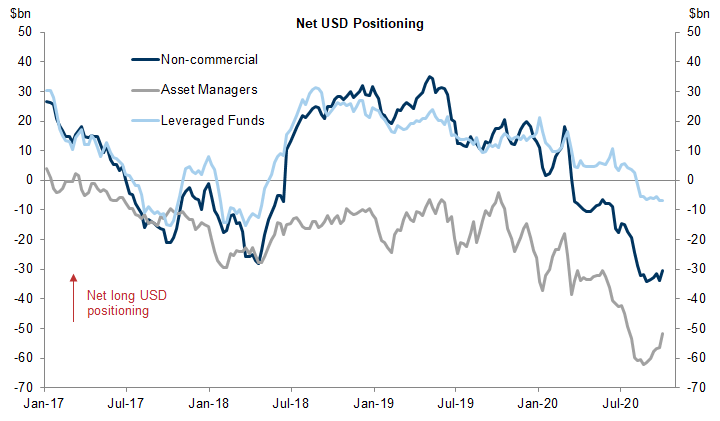

In FX, the dollar slumped, reversing some of Friday’s gains, as investors awaited positive news about U.S. Trump’s health and developments in fiscal aid talks in Washington; one possible upward catalyst for the dollar is that near record dollar shorts have started to reversed.

The yen retreated and Treasuries were steady. The euro advanced, while options capturing the immediate aftermath of the U.S. presidential election remain in demand amid uncertainty over Donald Trump’s condition. The Swiss franc gained amid speculative buying on the back of NEC Corp.’s purchase of Swiss banking software outfit Avaloq Group AG for $2.23 billion. The pound was steady; leveraged funds cut net longs on the pound to the lowest since August, according to data from the Commodity Futures Trading Commission for the week through Sept. 29. The funds increased net longs in the euro to the highest since August.

In commodities, speculation Trump could leave hospital sent oil prices up more than 2%, rebounding from a 3 week low. An escalating workers’ strike in Norway that has shut four of Equinor’s oil and gas fields also helped drive the gains. Brent prices were up 2% at $40.1 a barrel and U.S. West Texas Intermediate added 2.2% to $37.9 a barrel.

Focus later in the day will be on a reading of the US services sector, which accounts for more than two-thirds of the US economy, after data last week showed activity in the manufacturing sector slowed unexpectedly in September.

Market Snapshot

S&P 500 futures up 0.5% to 3,355.75

STOXX Europe 600 up 0.6% to 364.88

MXAP up 1.2% to 171.63

MXAPJ up 1.1% to 563.49

Nikkei up 1.2% to 23,312.14

Topix up 1.7% to 1,637.25

Hang Seng Index up 1.3% to 23,767.78

Shanghai Composite down 0.2% to 3,218.05

Sensex up 0.9% to 39,047.63

Australia S&P/ASX 200 up 2.6% to 5,941.58

Kospi up 1.3% to 2,358.00

Brent futures up 2.3% to $40.17/bbl

Gold spot little changed at $1,899.73

U.S. Dollar Index down 0.1% to 93.71

German 10Y yield rose 0.3 bps to -0.533%

Euro up 0.2% to $1.1738

Italian 10Y yield fell 3.7 bps to 0.581%

Spanish 10Y yield rose 1.5 bps to 0.236%

Top Overnight News from Bloomberg

President Donald Trump briefly left his hospital in a car to greet supporters gathered outside, after posting a video on Twitter saying he was about to make a surprise visit

Volatility eased in U.S. equity futures as optimism over President Donald Trump’s medical prognosis and hopes for fresh economic stimulus put a brake on selling that whipped up Friday

Economists and investors see mixed messages from the ECB’s top policy makers. Most important is a perceived disconnect between President Christine Lagarde’s press conferences after policy decisions, and blog posts by Chief Economist Philip Lane the following day

The stage is set for a showdown on Brexit at a European Union summit next week. French President Emmanuel Macron’s reluctance to make concessions on fish is stirring concern among officials he could sink efforts to reach a wider trade accord as negotiators begin on Monday a two-week period of intense talks

European Commission President Ursula von der Leyen said she is going into isolation after contact with a person who tested positive for coronavirus

A quick look at global markets courtesy of NewsSquawk

Asian equity markets and US equity futures began the week with a constructive tone as the regional bourses reopened from recent holiday closures and participants also digested the positive updates regarding President Trump’s condition, which was said to have continued to improve and he could be discharged from hospital as early as today. In addition, some also attributed the positive tone to the latest polls which showed a widening lead for former VP Biden following last week’s presidential debate. ASX 200 (+2.6%) outperformed with the broad gains led by a surge in energy and financials on the eve of the budget announcement, where Australia’s national debt ceiling is expected to be raised to above AUD 1.1tln and income tax cuts valued at billions are set to be backdated in an effort to provide immediate economic stimulus. Nikkei 225 (+1.2%) traded positively as exporters reaped the benefits of a weaker currency that was spurred by the risk tone and alongside some murmuring of Gotobi demand. Hang Seng (+1.3%) was also upbeat as participants returned following the holidays although mainland China is to remain shut for most this week and won’t reopen until Friday, while there were some weak spots including SMIC shares which have dropped over 6% after the US informed its suppliers they will be subject to additional export restrictions. Finally, 10yr JGBs were weaker amid the gains in riskier assets but with downside stemmed by support near the 152.00 level and with the BoJ present in the market for a total JPY 840bln of JGBs with 1-3yr and 5-10yr maturities.

Top Asian News

How Evergrande’s Billionaire Founder Skirted Latest Crisis

Top India Court Asks Government to Outline Interest Waiver Plans

Credit Suisse Hires HSBC Veteran Oey for Asia Wealth Push

Singapore to Pay Would-Be Parents for Babies as Virus Drags On

European equities (Eurostoxx 50 +0.6%) kicked the week off on the front-foot, before staging a mild pullback, as markets continue to assess updates on US President Trump’s health, the Presidential election and stimulus discussions. In terms of President Trump, it appears that he could be discharged from hospital as soon as today with reports suggesting an improvement in his condition, albeit some in the medical community have raised doubts over the upbeat narrative presented by the administration. Polling is yet to encapsulate the news of Trump’s COVID-19 diagnosis, however, polls detailing the fallout of last week’s debate have moved in favour of former VP Biden who now holds a 14-point lead in the NBC/WSJ poll (prev. 8 point lead); desks have subsequently continued to talk up the possibility of a Democratic “blue sweep”. On the stimulus front, House Speaker Pelosi said that they are making progress on coronavirus relief legislation, whilst Senate Majority Leader McConnell said “we are getting closer” on stimulus negotiations. However, other reports noted that Republicans still give low odds on another pandemic stimulus bill. In terms of performance of European indices, the IBEX (+1.0%) is the main outlier to the upside with gains in the domestic banking sector spurred by reports that the Sabadell (+3.6%) CEO contacted his counterparts from BBVA (+3.2%) and Kutxabank in recent weeks with regards to a merger, according to sources. From a sector standpoint, aside from the banking sector, travel & leisure names lead the way higher this morning despite ongoing concerns about the pick-up in COVID-19 cases (particularly in the UK), whilst strength can also be seen in some of the other pro-cyclical sectors such as oil & gas and auto names. Support has also been seen for UK homebuilders this morning after UK PM Johnson promised to create a “Generation Buy” scheme to help young people enter the property market. The PM has reportedly asked minister to mull a scheme for long-term fixed-rate mortgages with 5% deposits. For individual movers, Cineworld (-31%) are the clear underperformer this morning after confirming it will close all of its cinemas in the UK, Ireland and US this week because of the impact of coronavirus (UK and US closures are to be temporary). K&S (+17.6%) are the best performer in the Stoxx 600 reports noted the Co. is in advanced discussions to sell their Morton Salt unit to Kissner Group for ~USD 3bln. Weir Group (+17.0%) shares have seen notable support after announcing a USD 405mln divestment of its oil & gas unit to Caterpillar for USD 405mln.

Top European News

Europe Tightens Curbs as Leaders Gird for Long Virus Fight

Two- Speed Europe Sees Germany Thriving as Rest of Region Suffers

EU Commission President Von der Leyen Says She’s Self-Isolating

ECB Has a Messaging Problem as Lagarde-Lane Dynamic Muddies View

In FX, a softer start to the week for the broader Dollar and Index, with the latter currently contained within a tight 93.578-832 parameter following the fallout of US President Trump’s COVID-19 diagnosis which could see the President back at the White House as soon as today. Meanwhile, State-side stimulus talks remain with Senate Republican sources giving low odds for another bill, inferring that discussions could extend to after the 2020 Election. DXY tested its 21 DMA (93.646) to the downside, with the 50 DMA seen around 93.270, whilst upside levels see Friday’s high at 94.035 followed by last week’s peak at 94.298. Looking ahead, the docket sees Markit Services/Composite finals, ISM services PMI and potential comments from Fed 2021-voter Evans.

CHF/JPY – The traditional safe-haven FX have seen an early divergence with participants attributing Swiss outperformance to some M&A flows amid reports Japan’s NEC was planning to acquire Swiss software maker Avaloq for USD 2.2bln, whilst some strength may still be garnered from speculation the US currency manipulation report may be postponed until after the US elections, with Switzerland now ticking all three boxes to be labelled as a currency manipulator. That being said, the US Treasury will then offer a period of negotiations, with more drastic measures imposed should discussions fail. USD/CHF briefly dipped below its 21 DMA (0.9163) but matched intraday lows set on Wednesday and Thursday last week (0.9160), with the pair’s 50 DMA residing around 0.9130. USD/JPY resides on the other side of the G10 spectrum with early losses coinciding with gains across APAC stock markets. USD/JPY tests Friday’s 105.66 high with eyes on the 50 DMA (105.74), with the pair failing to close above the MA for the past three consecutive sessions. USD/JPY Opex today includes USD 1.25bln rolling off at strike 105.00.

EUR/GBP – Both on a firmer footing with the aid of a receding Buck, with the currencies on watch for Brexit developments in the aftermath of the videocall between PM Johnson and EC President, which noted that progress had been made but significant gaps remain, albeit the two sides have agreed to 11 days of “intensified” talks ahead of the UK de-facto deadline. Cable saw early sellers which prompted the pair to test 1.2900 to the downside, but thereafter nursed losses to print fresh session highs of 1.2964, with Sterling somewhat supported by surprise revisions higher to Services and Composite PMIs. EUR/USD meanwhile saw little action to revisions higher to final PMIs. EUR/USD retains a 1.1700+ status as it took out several potential resistance levels at 1.1750 (Fri high), 1.1755 (Wed high) ahead of 1.1763 (21 DMA), whilst the NY cut sees EUR 761mln at strike 1.1730 and around EUR 870mln at 1.1700.

CAD, AUD, NZD – All firmer to varying degrees, with the Loonie outperforming the non-US Dollars as it coat-tails on the firmer crude prices, whilst the Aussie eyes the RBA and Aussie budget and the Kiwi eking mild gains but with gains capped on AUD/NZD dynamics. USD/CAD trickles lower below 1.3300 having had tested the level overnight, with a current base at 1.3264, with its 21 DMA at 1.3258 and 50 DMA at 1.3241. AUD/USD meanwhile inches closer towards the 0.7200 mark (vs. current low 0.7157), with its 21 and 50 DMAs residing at 0.7201 and 0.7207 respectively. Finally, NZD/USD remains contained in a narrow 0.6631-54 band as AUD/NZD reclaims 1.0800.

In commodities, WTI and Brent futures open the week on a firmer footing, with early strength coinciding with gains across stock markets overnight after Friday’s pessimism unwound amid weekend reports that US President Trump could be at the white house as early as today. Meanwhile, the conflict between Armenia and Azerbaijan over the disputed region of Nagorno-Karabakh reportedly escalated dramatically. It was also reported that the Nagorno-Karabakh region stated that 18 civilians were killed and over 90 were wounded in a week of fighting – with traders keeping eyes on any potential targeting of oil fields/refineries/ports of the OPEC+ member. Elsewhere, Libyan oil production ticked higher to 290k BPD from last week’s 270k BPD, according to sources. In terms of where we currently stand WTI Nov (USD 37/bbl) trades on either side of USD 38/bbl whilst Brent Dec reclaimed the USD 40/bbl handle (vs. low USD 39.14/bbl). Elsewhere, spot gold and silver are choppy, with earlier weakness in the yellow metal offset by a softer Dollar, with prices now back around the USD 1900/oz mark (vs. low 1887/oz), whilst spot silver attempted a breach of USD 24/oz to the upside – with the latest CFTC data suggesting hedge funds and money managers reduced positions in COMEX gold and increased them in silver contracts in the week to Sept 29th. Finally, LME copper prices are relatively flat having had drifted off highs in tandem with price action seen in stocks.

US Event Calendar

9:45am: Markit US Services PMI, est. 54.6, prior 54.6

9:45am: Markit US Composite PMI, prior 54.4

10am: ISM Services Index, est. 56.2, prior 56.9

DB’s Jim Reid concludes the overnight wrap

I can almost certainly guarantee that wherever you’re reading this from you had better weather than me this weekend. Or at least no worse. It rained from start to finish. Any weekend with the golf course closed is a bad one for me and watching Frozen 2 the twentieth time in two months to fill the time didn’t improve the mood. Then the coup de grace was seeing Liverpool concede 7 (seven – as they always used to type out and put in brackets for unusual scores) for the first time since 1963 last night! Quite astonishing.

The business world continues to be quite extraordinary at the moment too and Mr Trump again dominated the weekend headlines. I’m sure you’ve seen the conflicting and confusing reports concerning his health over the weekend so we won’t go into that here. The latest from yesterday was that his doctors suggested he could be released back to the White House as soon as today. He also appeared on a video last night looking in good spirits. According to the wires this has helped S&P 500 futures to trade up +0.61% this morning but to be honest it could also be because a poll showed that Biden was 14pp up over the weekend (more below). We actually published the EMR almost an hour earlier than usual on Friday and four minutes after it hit inboxes the headlines came through that the President had tested positive. So we will try not to be that efficient again and end up as virtual fish and chip paper as we were on Friday.

In terms of the impact on the election, we haven’t seen enough polling to assess whether this increases or decreases his chances of winning. There was an NBC-WSJ poll released over the weekend showing Biden ahead by 14 points – the biggest lead of the campaign. However this polling was carried out between the first debate last Tuesday and the positive Covid test early on Friday morning. For comparison the last poll from this combination saw at 8pp lead last month. An Ipsos and a YouGov poll have just been released before we go to print and they seem to show around a 10pp and 7pp lead for Biden respectively. These were conducted on Friday and Saturday.

This confirms what was suspected last week, namely that polls were edging further towards Biden even before Friday with the first evidence now coming through that this may have continued. Indeed the recent price action suggests that the market wants certainty more than anything else. Given the realistic options (assuming the polls are not completely out), perhaps the market would currently most like a Democratic clean sweep as this would increase the likelihood of near term certainty. This outcome was edging up in likelihood amongst respected political pundits ahead of Mr Trump’s positive test so Friday’s news brought back all sorts of uncertainties with tail risks increasing in all sorts of direction. The fact that Biden tested negative later in the day seemed to help markets which partly supports the theory above. So this week the market will await more news from the Trump camp and signs of movement in the polls. If Biden pulls away then markets will probably be pretty relaxed. So the batch of polls post Trump’s illness are going to be important.

As we’ll see below the VP debate takes place on Wednesday which is the next major planned event. We’ll also see what the latest on the stimulus package is. It feels like both sides are trying to show that they are doing the best they can to bridge the gap but the reality is that both sides seem to be quite far apart still and it will be an enormous feat to bridge the gap pre-election. Nonetheless, the FT reported yesterday that the US President Donald Trump has issued a call for negotiators to “work together” and complete a deal.

Overnight, Asian markets have started the week on front foot with the Nikkei (+1.20%), Hang Seng (+1.46%), Kospi (+1.18%) and Asx (+2.47%) all seeing strong advances and recovering from Friday’s morning’s shock. China’s markets are closed for holidays. In Fx, the US dollar is trading down -0.11%. In terms of overnight data, Japan September services PMI was confirmed at 46.9 (vs. 45.6 in flash).

Back to politics and onto Brexit. U.K. PM Johnson had the planned VC talk with EC President von der Leyen on Saturday and in a joint statement they instructed their chief negotiators to work intensively in order to try to bridge the obvious gaps that there are and emphasised “the importance of finding an agreement, if at all possible”. On Sunday Johnson reaffirmed that he’d like a deal but said the U.K. could prosper without one. The FT also had an article last night suggesting Barnier is going to hold talks with the impacted EU countries on fisheries which shows some progress and the possibility of negotiation movement. For me it seems like the probabilities of a deal have edged up over the last couple of weeks. In terms of news flow and headlines it’s seems to have been 7 steps forward and only 5 back. We will see. Sterling is broadly flat this morning at 1.2938 ahead of another week of talks.

Onto the virus and the UK reported an extremely high 35,850 new cases over the weekend but these were heavily impacted by around 16,000 previous unreported cases between September 25 to October 2 due to technical issues. Even after taking this into account the new weekend cases stood at 19,850, a higher run rate compared to previous weekends. Meanwhile, the delay in entering those 16,000 cases also means that their recent contacts were not immediately followed up. This will put more pressure on the government.

Bloomberg is also reporting that France may shut down bars in the Paris region and impose other new restrictions in the area. The country reported 29,537 new cases this weekend versus an average of c.25,000 cases over the previous two. In the US, New York City Mayor Bill de Blasio said he plans to close schools and non-essential businesses in nine neighbourhoods in Brooklyn and Queens where there’s been a surge in coronavirus infections. Indoor and outdoor dining will also be closed in these areas. For more details on how the virus is spreading in major regions of the world see the table below. There are a lot of footnotes so please see those in conjunction with the raw data. On the vaccine front, the FT reported the UK government’s head of the vaccine taskforce Kate Bingham as saying that less than half of the UK population could be vaccinated. She said, “There is going to be no vaccination of people under 18. It’s an adult-only vaccine for people over 50, focusing on health workers, care home workers and the vulnerable.”

In terms of this week, outside of the VP debate on Wednesday we’ll get the latest minutes from recent Fed (Weds) and ECB (Thurs) meetings, and also hear from both Fed Chair Powell (tomorrow) and ECB President Lagarde (tomorrow and Weds). The only G20 decision next week is from the Reserve Bank of Australia tomorrow. Our Australia economists expects no change in policy, but we will be watching for clues about whether a rate cut might yet be delivered by the end of the year. The main data highlight will likely be the release of the services and composite PMIs from around the world. Most are today but the U.K. comes tomorrow and China’s on Thursday after holidays. The flash readings showed clear signs of the services sector in Europe being affected by the second wave of Covid-19, with the flash Euro Area services PMI falling to 47.6, which is below the 50-mark that separates expansion from contraction, with both Germany (49.1) and France (48.5) also in contractionary territory. We will see if this trend is confirmed and whether there was any late month deterioration from the initial flash reading. The day by day week ahead calendar is at the end.

Recapping last week now, as we moved into Q4, US equities saw their first positive week since August even with a weaker end of Friday. In a particularly hectic week that started with one of the most raucous US Presidential debates in memory and ended with the sitting US President testing positive for Covid-19 equity volatility jumped. The VIX volatility index rose +1.25pts to 27.63 even as equity prices rose – it was the second largest weekly rise in vol since June. Even with this uncertainty, the S&P 500 rose +1.52% (-0.96% Friday) on the week, breaking a streak of four losing weeks – the longest since August 2019. The NASDAQ rose +1.48% (-2.22% Friday) for the second weekly gain. European equities rose as well with the Stoxx 600 ending the week +2.02% (+0.25% Friday), the third weekly gain out of the last four. The IBEX (+1.90%), FTSE 100 (+1.02%), and CAC (+2.01%) all posted strong weekly equity performances even as their home countries reinstated some restrictions in the face of increasing Covid-19 caseloads.

The dollar dropped (-0.84%) as risk assets generally gained, for just its second weekly loss since the end of August. The drop in the dollar saw gold gain +2.06%, as the precious metal finished the week just under the $1900/oz level. Even though equities gained on the week, oil did not follow suit as worries on global demand saw WTI (-7.95%) and Brent crude (-6.32%) fall sharply and is now down four out of the last five weeks and is at its lowest weekly close since June. Core sovereign bonds were mixed on the week as US 10yr Treasury yields rose +4.6bps (+2.3bps Friday) to finish at 0.701% and 10yr Gilt yields rose +5.7bps (+1.2bps Friday) to 0.25%, while 10yr Bund yields were down -0.7bps (unchanged Friday) to -0.54%. Italian 10yr yields fell -10.2bps to 0.784% – their lowest levels since an all-time low last September.

On the data front, US Nonfarm payrolls rose by 661k (vs. 859k expected) on Friday while August’s numbers were revised up to 1.49 million from 1.37m. The unemployment rate fell 0.5 percentage points to 7.9% (vs. 8.2 expected), though the labour-force participation rate declined by 0.3 points to 61.4%. Meanwhile in Europe, the Euro-area CPI reading showed inflation slowed to -0.3% in August (vs. -0.2% expected) while the core rate set a six-year low at 0.2% (0.4% expected).

via ZeroHedge News https://ift.tt/3nj3Q7j Tyler Durden

Trump Warns “If You Want Massive Tax Increase, Vote Democrat” In Early Morning Tweetstorm Tyler Durden

Mon, 10/05/2020 – 07:06

While the mainstream press was incensed by President Trump’s joyride to greet the “Great Patriots” gathered outside Walter Reed Sunday evening, it was apparently the show of strength and stamina that investors needed to assuage worries about Trump’s condition.

And with futures pointing to a sizable bounce at the open, President Trump has taken to twitter to cheer on the stock market and remind Americans why they should vote for him in a flurry of tweets on everything from the president’s defense of the Second Amendment to the threat that Joe Biden will move to shut down the American economy once again.

The stream of tweets started with a quote from Fox and Friends, one of Trump’s favorite shows…