Japan Blasts ‘Intolerable’ Chinese Intrusion Into Its Waters For ‘Record’ Amount Of Time Tyler Durden

Tue, 10/13/2020 – 14:10

Top officials in Japan are angrily denouncing an ongoing Chinese incursion in Japanese territorial waters, just off disputed East China Sea waters since Sunday morning.

They are said to be Chinese coast guard ships which have refused to relocate since approaching a Japanese fishing vessel three days ago, AP reports. The ensuing standoff has resulted in formal diplomatic protests lodged to Beijing by Japan.

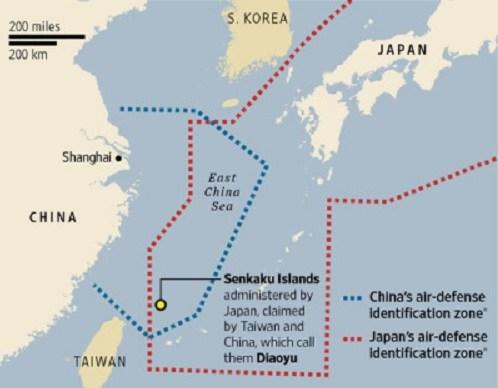

Specifically the area includes the Senkaku islands, which has been the scene of multiple prior such standoffs between Chinese and Japanese vessels.

Senkaku Islands in the East China Sea, via Kyodo News.

Japan’s Defense Minister Nobuo Kishi called the situation “intolerable” and demanded that China “use self-restraint on any action that would escalate tensions.” He also said it’s part of a “continuous attempt to change the status quo by force” in the disputed waters of the East and South China Seas.

China refers to the Senkaku islands as Diaoyu – which Beijing claims as its own. Local reports suggest the crisis may have abated by the Coast Guard ships finally leaving as of Tuesday night (local time); however, it’s still being described as the longest breach of Japan’s waters in almost a decade.

Japanese media recorded China’s justification as involving ‘routine patrolling’:

Meanwhile, China repeated its mantra about the uninhabited islets, saying they are its “inherent territory” without elaborating on why the country’s vessels have remained near the isles for such a long time.

In Beijing, Chinese Foreign Ministry spokesman Zhao Lijian told reporters, “It is China’s inherent right to carry out patrolling and law enforcement in the waters of the Diaoyu Islands, and Japan should respect this,” using the Chinese name of the isles.

The Japanese Coast Guard said the Chinese illegal incursion was for“a record length of time”.

Japanese media reports further that more possibly hostile Chinese vessels are in the area just off Japan’s territorial waters.

“On Tuesday, the coast guard said it also spotted another pair of Chinese vessels sailing in the so-called contiguous zone outside Japan’s territorial waters,” notes Kyodo News of the latest development.

Taiwan is also in the regional mix of those laying claim to the contested islands, also considering the geographic closeness to Taiwan’s coast.

Japan had ownership of the islands since 1895 until WWII. After its defeat by the United States they came under US post-war administration from 1945 until 1972, after which as the US ceded them to Japan as part of the the Okinawa Reversion Agreement.

China, however, claims to have discovered the islands going back centuries, but seems to have taken a more aggressive posture on the issue after discovery of potential undersea oil reserves there in 1968.

via ZeroHedge News https://ift.tt/2FqKkol Tyler Durden

While most people generally understand that the stock market and the economy do not move in lockstep, there is still an underlying belief that a strong market reflects a strong economy. But according to that logic, our current economy must be historically strong. If this strikes you as strange, given that we are in the midst of a destabilizing and polarizing pandemic, and a period of political risk that threatens the foundations of the Republic, that’s just because you don’t understand how the fundamental relationship between the stock market and the economy has changed. Believe it or not, strength on Wall Street is now driven by weakness in the broader economy.

Perhaps the most reliable metric for stock valuations is the Cyclically Adjusted Price to Earnings (CAPE) Ratio, which compares share prices to average earnings over a 10-year period, thereby smoothing out short term conditions. An August 6th Fortune article pointed out that CAPE ratios (which were 31.1 then, and have since moved up to 32.65) have only been as high or higher on three occasions over the past 132 years of available data: in 1929 right before the Great Depression, in 1999 right before the dotcom crash, and then briefly in September of 2018. And while we now know that the optimism that fueled those prior spikes were largely, if not totally, illusory, at least it made some sense that stocks were rallying.(It’s also worth noting that stocks crashed in the immediate aftermath of those spikes).But where’s the optimism that’s fueling the markets now? Sure, Donald Trump may be wildly waving the pom poms, but no serious economist or investor thinks the economy is poised for greatness. Instead, this rally is all about the printing press.

With the Fed now delivering more stimulus than ever, and promising to keep interest rates at zero for as far as the eye can see, many attribute the surprising rally to a “never fight the Fed” bias, which has banished investor fears through the assumption that the Fed will vanquish every dip with even more stimulus. The low rates also “push” investors into stocks because they nearly eliminate the returns available through fixed income. But these forces, which have been with us, off and on, for the past 20 years, don’t fully explain why the current market is so strong. The Covid pandemic has actually created conditions whereby what hurts the economy and Main Street businesses actually helps the S&P 500.

Fed stimulus is particularly helpful to very large publicly traded companies who can borrow by issuing bonds to the public market. Thus, major companies, mostly those that are publicly traded, can actually take advantage of the Fed’s activism in real-time. In contrast, smaller companies typically rely on traditional bank loans, which are often riskier than alternative uses of bank capital. As a result, small businesses are routinely denied credit, or face much higher interest rates, than do public bond issuers.

Low rates also allow large publicly traded companies to refinance their existing higher-cost debt with lower rates, thereby increasing their earnings by lowering their interest expense. This results in the market assigning a higher price-earnings multiple to those enhanced earnings. So, the impact of lower rates delivers a double benefit to these companies both in terms of enhanced earnings and higher valuations.

But private companies, that collectively employ many more people than large public companies, get only modest benefits from ultra-low rates. Smaller businesses, that rely far more on sales revenue than capital markets to meet their funding needs, have seen sales plummet due to forced lockdowns, consumer austerity, worker shortages, and supply disruptions. They can’t turn to Wall Street smoke and mirrors to make up for the shortfall.

In addition, large companies are much better equipped to survive the Covid lockdowns, through greater ability to move business online and to allow employees to work from home. The best-performing companies, like Amazon or Netflix, have online commerce as their core of their business model. These companies may actually benefit from decreased competition from small businesses that can’t transition as effectively. In this environment, it should not be surprising that as of July 31 the S&P 500’s 10 biggest companies by index weight compromise nearly 29% of total market capitalization of the index, the highest level in nearly 40 years. (B. Winck, Business Insider, 8/10/20) As a result, the performance of those companies has a big impact on the market as a whole.

As the “Main Street” economy continues to languish, the Fed will continue the funding available for large business to borrow cheaply even while the pain for small business persists. This means that a bad economy is good for the stock market. Main Street’s pain is Wall Street’s gain.

But to expect that a Main Street recovery will soon take hold to change this dynamic is to completely ignore reality. Those who point to the remarkably strong July home sales numbers as a sign for optimism should think twice. A sober reading of the data suggests that the sales were largely fueled by people abandoning urban areas to buy in the suburbs. If so, the sales do not indicate economic health, but growing fear.

Coronavirus and its attendant economic stagnation are likely to be with us for years to come. Even if a vaccine is found in the next year or so, which is the most optimistic timetable, the damage to the travel, entertainment, fitness and food service industries may be beyond repair. How long will it take for people to once again feel comfortable in large groups? The fear will linger long after the real danger is gone.

Cultural changes that have already taken hold may mean that office towers, retail chains, and theaters may never recover. People and companies are becoming more comfortable with working from home, shopping online, and avoiding crowds. According to an article on Bloomberg on August 23, Goldman Sachs now anticipates that almost a quarter of the 22 million temporary layoffs that began with the first shutdown in March will become permanent. Some 2 million of those individuals could remain unemployed well into 2021. But these near-term problems may be just the beginning.

Many public sector workers across the country have made it clear that they will not return to work unless there is absolutely no danger from Coronavirus. If those demands seem ridiculous, it’s only because you fail to grasp the new idea about work itself. There are those who seem to now believe that an economy can function without work as long as the government is there to foot the bill. The process of producing goods and services has become so remote to most Americans that people don’t understand that something must be produced before it can be consumed, and that production isn’t always easy. This feeling is evident in the rise of concepts such as Universal Basic Income, extended unemployment benefits that pay more than the median wage, and Modern Monetary Theory, which suggests that there is no downside to unlimited money printing.

The trillions that Washington has already spent to help shield people from the ravages of government-mandated lockdowns will be very hard to withdraw once people have come to rely on them. In his first interview since accepting the Democratic presidential nomination, Joe Biden conceded that he would completely shut down the economy again if Covid “was not brought under control.” Of course, he failed to define what “under control” really meant. No doubt it will mean whatever serves his political interest, which seems to be an effort to place government at the center of every facet of life.

It’s not just the possibility of more shutdowns that should be spooking investors. If the Democrats do take over in November, it’s likely that businesses could contend with corporate tax hikes (not only at the corporate level, but also for shareholders through higher taxes on dividends and capital gains), a raft of new environmental mandates, new rules on higher wages and benefits, and increasingly absurd and unworkable diversity and equity requirements that could make compliance and legal costs soar and productivity plummet.

But none of this has dented share prices.

In fact, even as more and more American cities succumb to nightly rioting and paralysis, Citigroup has raised its year-end target for the S&P 500 index to 3,300 from 2,900. Ignoring all the bad news, Citi credited the upgrade to the “unbridled” Federal Reserve monetary easing, negative real rates, and its belief that the Fed will do “whatever it takes to prevent U.S. stocks declining by teen-like percentages.” (C. Mullen, Bloomberg, 8/24/20)

Recently Deutsche Bank came to a similar conclusion, suggesting that in order to make up for the stimulatory “insufficiency” of zero percent interest rates, the Fed’s balance sheet would need to expand by an “additional $12 Trillion” in the near term. (D. Rabouin, Axios, 7/27/20) To put that into perspective, the Fed’s balance sheet expanded by less than $4 trillion as a result of the four years of quantitative easing of 2009-2013. So far in 2020, the Fed has created almost $3 trillion in new money. But Deutsche Bank thinks the Fed will need to pump in 4 times that amount in the near-term just to keep the economy afloat.

As if there were any room left to doubt that the Fed is about to rush further into uncharted stimulus territory, Fed Chairman Jerome Powell recently announced that the central bank will no longer raise interest rates pre-emptively to head off higher inflation. This is really a distinction without a difference as the Fed has no intention of raising rates anytime in the foreseeable future. But this does give it cover to do nothing if inflation does show up in earnest.

As Congress and the President have proven to be absolutely incapable and uninterested in making the difficult economic policy decisions, they have found it much easier to ask the Fed to bail them out with its printing press. Last month, Joe Biden and Congressional Democrats called for changes in the Federal Reserve’s Charter that would require the bank to “aggressively target persistent racial gaps in jobs, wages, and wealth.” How it could possibly accomplish those goals given its limited toolset was left unsaid, but you can bet it will involve printing more money.

So, we have been handed a map of what may be expected over the next few years. The government will attempt to replace an imploded economy with an inflated money supply. This strategy has never worked in the past and it won’t work now. While the dollar has survived similar assaults on its strength before, it has never faced a test of this magnitude. Dollar weakness in recent months have many in the mainstream finally convinced that a reckoning is at hand. Buckle up.

via ZeroHedge News https://ift.tt/33SrEqY Tyler Durden

Trump Brings Tax Return Case To Supreme Court Tyler Durden

Tue, 10/13/2020 – 13:32

It was just a matter of time.

Shortly after President Trump was denied his latest appeal to keep his tax returns private – as if anyone besides a few rabid TDSers still cares about those after the whole thing was leaked to the NYT – on Tuesday the president asked the Supreme Court, which will soon have one more conservative Justice on deck, to block lower court decisions that would give the Manhattan District Attorney’s office access to years of his income tax returns.

Trump’s lawyers filed an emergency application with the Supreme Court asking the court to issue a stay on a grand jury subpoena demanding those tax returns and other financial records from his accountants. The request is pending the filing of his planned request that the high court hear his appeal of the lower court rulings that allowed that subpoena.

And, as CNBC reports, if the Supreme Court agrees to hear his appeal, it will be the second time the court has taken the case. In their filing, Trump’s lawyers said “there is a reasonable probabilty that” the Supreme Court will take the appeal.

Last summer, the Supreme Court rejected Trump’s argument that his financial records from the Mazars USA firm should be protected from the subpoena because of his status as president. But the Supreme Court said Trump could make new arguments against the subpoeana with a federal district court in Manhattan, when a judge in that court ruled against the president after Trump’s lawyers argued that the subpoena was overbroad and issued in bad faith. A federal appeals court then upheld that ruling.

More importantly, with RBG now gone and ACB about to be the latest addition, it will be a true test of just how “conservative” the new appointment will push the court.

As a reminder, Manhattan DA Cyrus Vance Jr. is seeking the tax returns and other records as part of an ongoing criminal investigation of the president’s company, the Trump Organization. Vance is known to be eyeing how hush money payments to women who say they had sex with Trump were accounted for by the company, and according to court filings also could be investigating possible tax crimes, as well as bank and insurance fraud.

via ZeroHedge News https://ift.tt/3nJBWBv Tyler Durden

Which Came First: Loans Or Deposits? An Unexpected Answer From JPMorgan’s Balance Sheet Tyler Durden

Tue, 10/13/2020 – 13:10

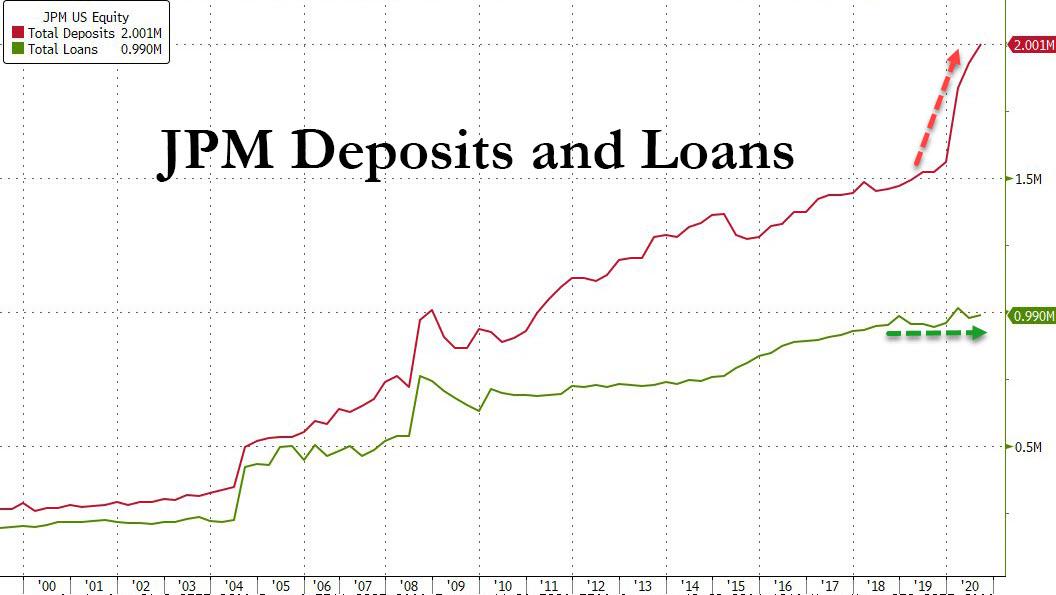

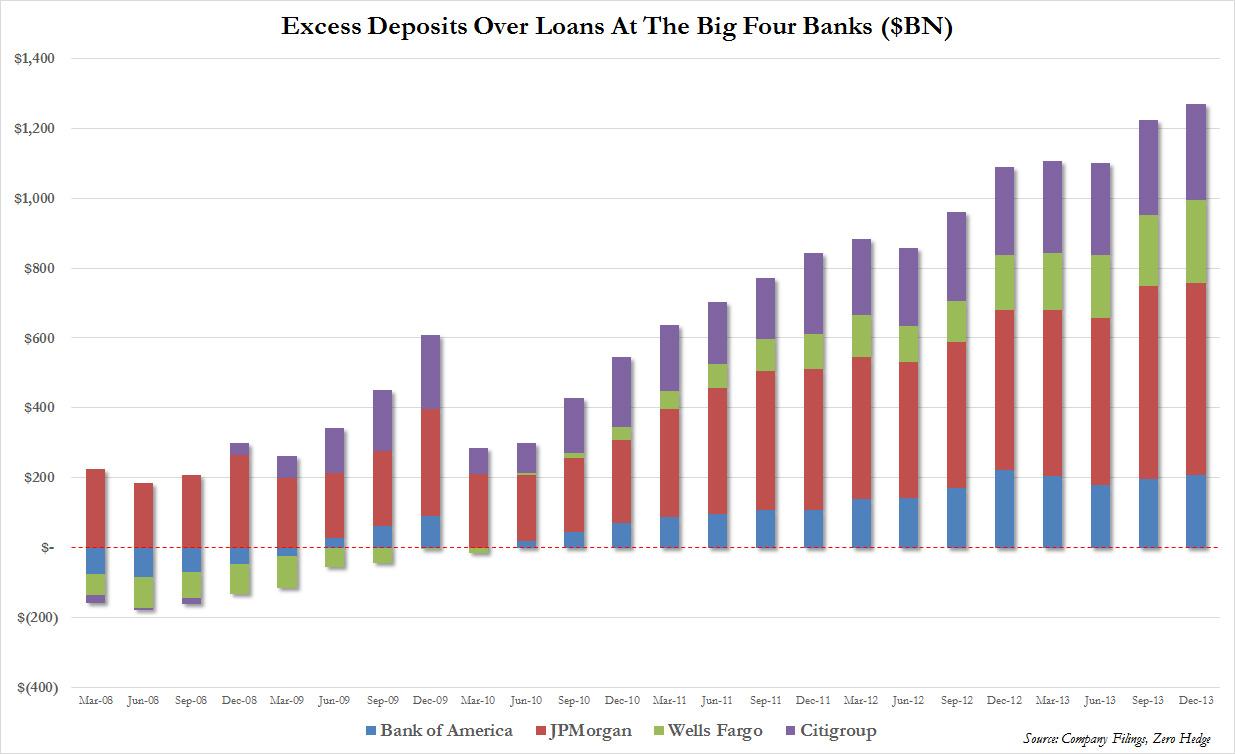

There was a remarkable disclosure in the latest JPMorgan earnings report: the company reported that in Q3, its average deposits rose by a whopping 30% Y/Y, and up 5% from Q2, to just over $2 trillion, even as the average amount of loans issued by the bank were virtually unchanged Y/Y at $991 billion, and down4% from Q2.

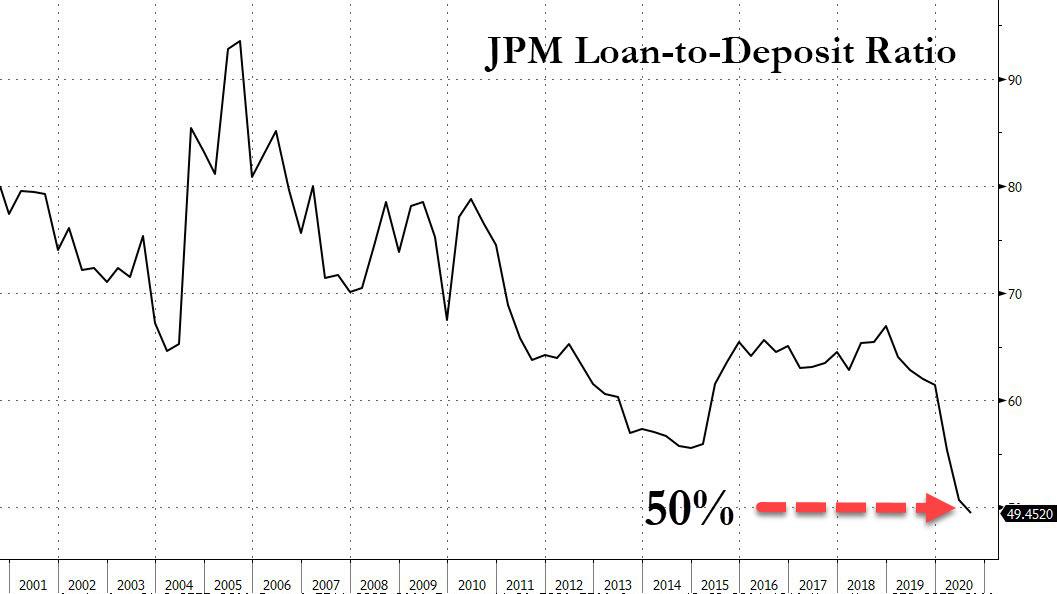

In other words, for the first time in its history, JPM had 100% more deposits than loans, or inversely, the ratio of loans to deposits dropped below 50% for the first time ever:

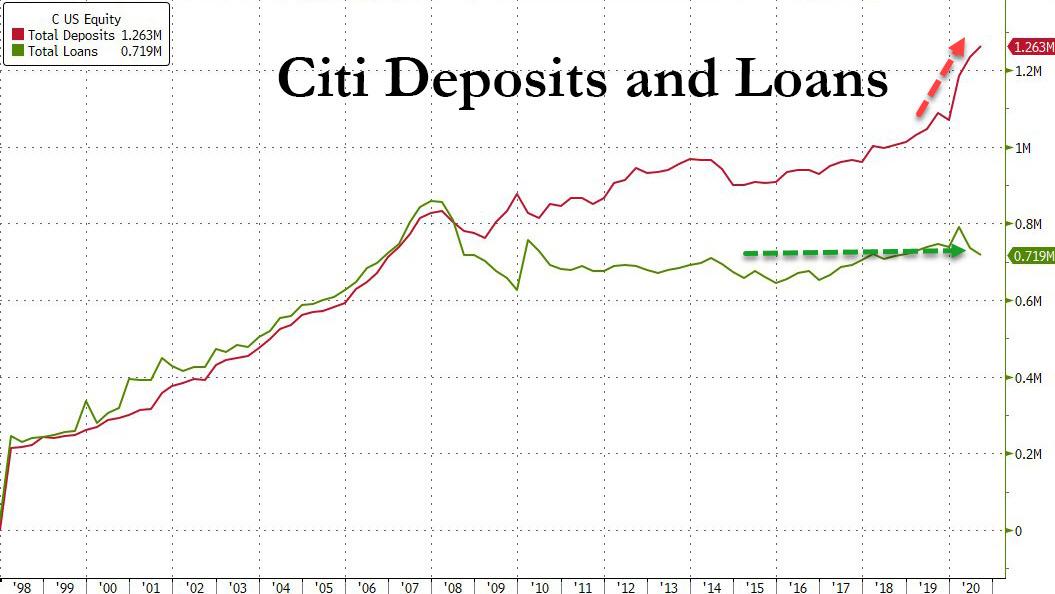

A similar, if not quite as acute pattern emerged at Citigroup, where deposits similarly hit a new all time high, even as the bank’s loans have been virtually unchanged for the past decade.

And while Citi has not quite caught up with JPM in having double the deposits compared to loans, what the chart above reveals even clearer is that the unprecedented divergence between deposits and loans started just as the Fed launched QE1 and has only grown since then.

There are two implications one should draw from the collapsing loan-to-deposit ratio. The first, more superficial one was flagged by Bloomberg today, in that this ratio is “a closely watched metric that measures how much lending a bank is doing when compared to its capacity to lend. For reference, [for JPM] the ratio was 64% this time last year.”

The second, and far more profound implication, the one that Bloomberg did not touch upon, is arguably the most fundamental question in modern fractional reserve banking: what comes first, loans or deposits, in other words do private, commercial banks create the money in circulation (by first lending it out) or is the central bank responsible for money creation.

While we will update this analysis when we get the deposit and loan data from the remaining money-center banks such as BofA and Wells later this week, the pattern is clear: there are now far more deposits than there are loans in the US banking system.

This is a problem because most conventional monetarists will argue that loans always come first, and only then do banks receive deposits. Well, clearly that’s no longer the case, and on its surface, the JPM data would suggest that the conventional process of deposit creation via loans is terminally broken.

Indeed, that’s precisely the case with the missing link being – drumroll – the Fed, as we explained all the way back, in 2014. Here is the punchline of what we said then, when we did a similar analysis observing what was already a record amount of excess deposits over loans:

… how does the record mismatch between deposits and loans look like? Well, for the Big 4 US banks, JPM, Wells, BofA and Citi it looks as follows.

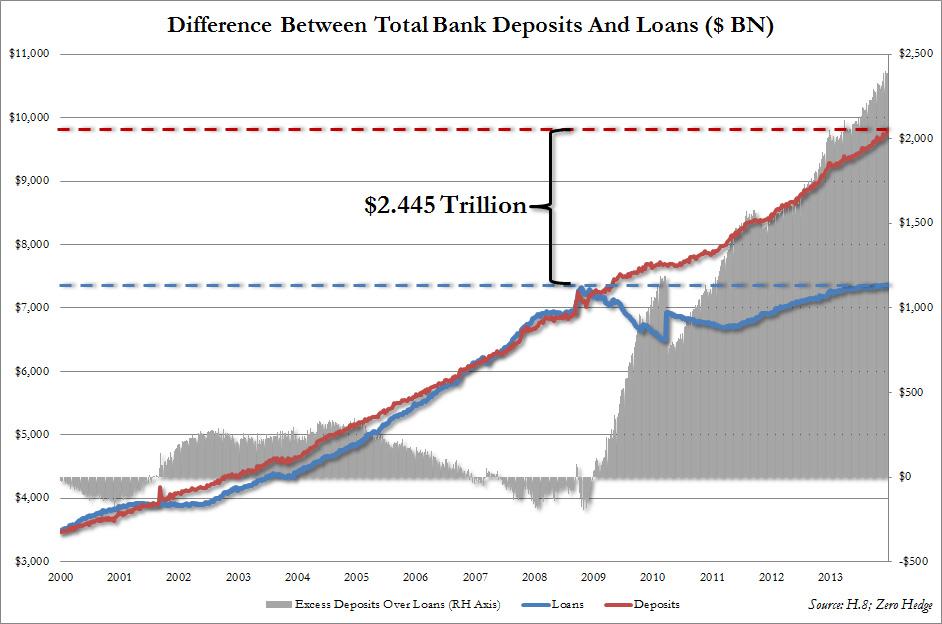

What the above chart simply shows is the breakdown in the Excess Deposit over Loan series, which is shown in the chart below, which tracks the historical change in commercial bank loans and deposits. What is immediately obvious is that while loans and deposits moved hand in hand for most of history, starting with the collapse of Lehman loan creation has been virtually non-existent (total loans are now at levels seen at the time of Lehman’s collapse) while deposits have risen to just about $10 trillion. It is here that the Fed’s excess reserves have gone – the delta between the two is almost precisely the total amount of reserves injected by the Fed since the Lehman crisis.

So what does all of this mean? In a nutshell, with the Fed now tapering QE and deposit formation slowing, banks will have no choice but to issue loans to offset the lack of outside money injection by the Fed. In other words, while bank “deposits” have already experienced the benefit of “future inflation”, and have manifested it in the stock market, it is now the turn of the matching asset to catch up. Which also means that while “deposit” growth (i.e., parked reserves) in the future will slow to a trickle, banks will have no choice but to flood the country with $2.5 trillion in loans, or a third of the currently outstanding loans, just to catch up to the head start provided by the Fed!

It is this loan creation that will jump start inside money and the flow through to the economy, resulting in the long-overdue growth. It is also this loan creation that means banks will no longer speculate as prop traders with the excess liquidity but go back to their roots as lenders. Most importantly, once banks launch this wholesale lending effort, it is then and only then that the true pernicious inflation from what the Fed has done in the past 5 years will finally rear its ugly head.

The above also explains why even as the Fed has pumped trillions in reserves into banks, which by transformation have ended up as deposits on bank balance sheets, the velocity of M2 money has plunged to an all time low (and will soon drop below 1.0x), as loan demand is nowhere near enough to offset the Fed’s forced deposit creation which incidentally ends up not in the economy but in capital markets, resulting in broad – ad wage – deflation and asset price hyperinflation.

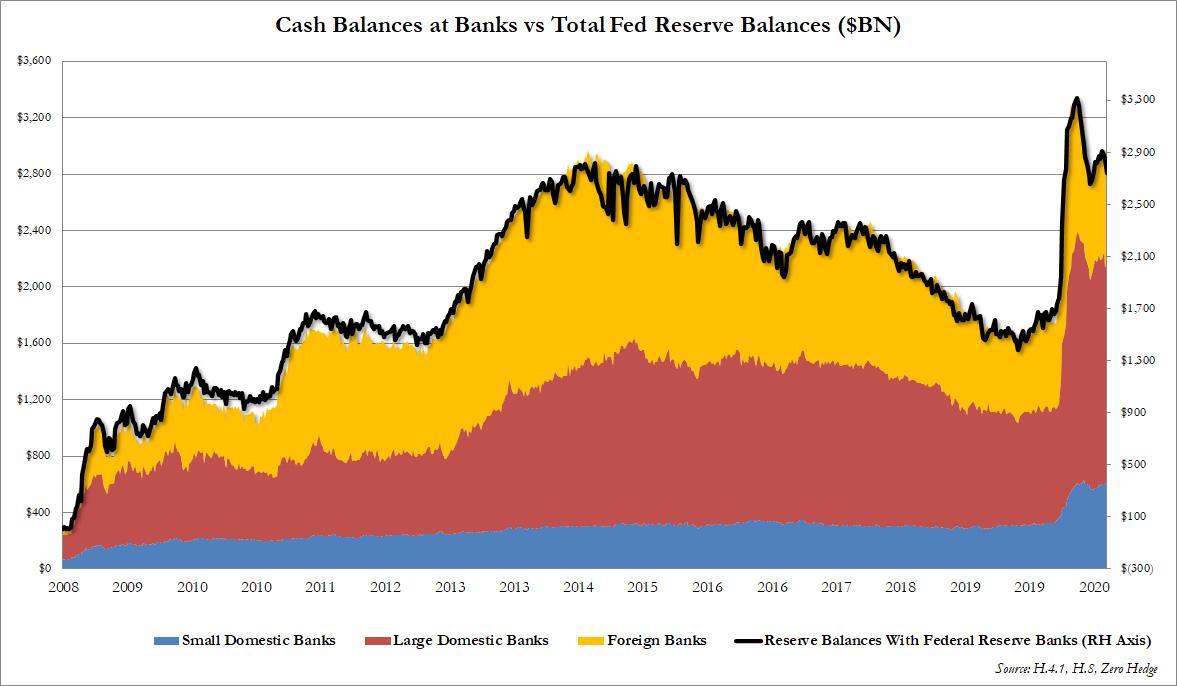

And, as regular readers know too well, it also means that the excess reserves injected by the Fed end up as cash across the US financial system, including both domestic and international commercial banks.

We will update this analysis tomorrow once we have the full bank data, however the take home message for now is that the next time someone says that under fractional reserve banking deposits are always a consequence of loan creation – one of the core pillar of such idiotic theories as MMT – just show them the chart above.

via ZeroHedge News https://ift.tt/3iVOSAK Tyler Durden

It comes as no surprise, that on the same day Apple is set to unveil the new 5G iPhone, a report surfaces via the Nikkei, outlining how key iPhone suppliers have ramped up production of the new smartphone.

Sources told Nikkei that top iPhone assemblers, Foxconn and Pegatron, have been running at “full production speed” in the last couple of weeks, especially during Mid-Autumn Festival and the Golden Week holiday.

Production of the new 5G iPhone began in mid-September, with “more substantial production output,” which started in the first week of October, Nikkei said.

Apple and its suppliers have been dealing with supply chain disruptions this year due to the coronavirus pandemic. Besides the disruptions, Nikkei said 5G iPhone production could be around 73-74 million units this year, which would miss the original estimates of 80 million. Apple expects to make up any shortfalls this year with increased production next year if sales are strong.

At today’s event, Apple will release two 5G iPhones – the 6.1-inch and 6.7-inch models. The Cupertino-based tech giant is locked in a smartphone war with rival Huawei Technologies. Huawei briefly surpassed Samsung Electronics’ as the world’s top smartphone maker this past summer.

Today’s Apple Event starts at 1:00 ET. Watch here:

Chinese sales of 5G iPhones could hit a snag as tensions between Washington and Beijing continue to accelerate ahead of the US presidential elections. If the Trump administration gets their way in banning popular Chinese apps like WeChat or TikTok from the App Store, it could result in a worldwide iPhone shipments plunge.

The Global Times reported in mid-September that Apple could be introduced to the “Unreliable Entity List,” a list of foreign companies accused of mistreating Chinese companies. Other companies the Chinese Communist Party hinted that could join the list are Qualcomm, Cisco, and FedEx.

Will the launch of 5G iPhones support Apple’s lofty valuations?

via ZeroHedge News https://ift.tt/3nO7PZG Tyler Durden

Facebook Bans Ads Questioning Safety Of COVID-19 Vaccines Tyler Durden

Tue, 10/13/2020 – 12:48

Mark Zuckerberg has clearly had enough of being hauled in front of Congress and hectored by a gang of senior citizens and listening to the head of the ACLU slam his company as a vessel for violent hate speech. Because over the past few months, Facebook has done a complete 180 on its position about speech, particularly sensitive political speech. Zuckerberg has apparently been shaken from his non-interventionist approach by announcing that FB wouldn’t accept new political ads during the last week of the campaign, and just yesterday announcing that Facebook would crack down on holocaust deniers on its platform.

The company has also launched salvos against QAnon and election-related misinformation, while taking an aggressive approach toward political advertising, and political content in general.

And as global authorities struggle to convince the public that an eventual COVID-19 vaccine will be safe to take despite the expedited approval process, Facebook has decided to give them a hand by banning all content encouraging users to refuse to take a vaccine. It laid out the new global policy in a blog post published Tuesday.

“Now, if an ad explicitly discourages someone from getting a vaccine, we’ll reject it,” the company’s Head of Health Kang-Xing Jin and Director of Product Management Rob Leathern said in a blog post Tuesday.

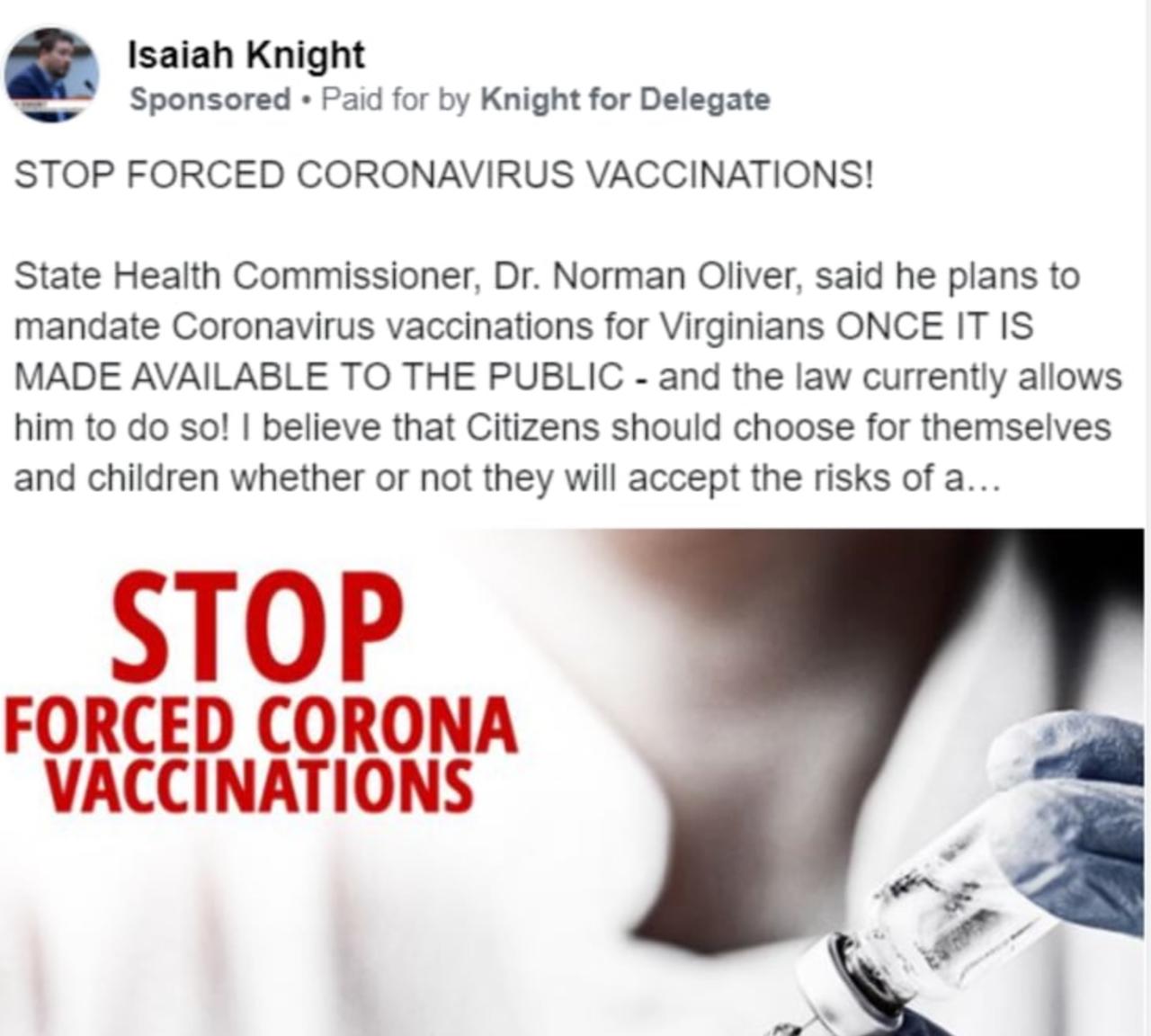

Facebook will draw the line at allowing users who advocate against “mandatory vaccination,” which the company said was a legitimate political position (not an argument made in “bad faith” that some on the left insist), to post as normal. They cited an example of a state lawmaker from Virginia who posted “STOP FORCED CORONAVIRUS VACCINATIONS”.

While the above ad will be allowed under the new rules, ads that explicitly discourage people from taking vaccines by portraying the vaccines as ineffective or unsafe will be banned.

“If an ad that advocates for/against legislation or government policies explicitly discourages a vaccine, it will be rejected,” a spokesperson wrote CNBC. “That includes portraying vaccines as useless, ineffective, unsafe or unhealthy, describing the diseases vaccines are created for as harmless, or the ingredients in vaccines as harmful or deadly.”

Facebook also plans to push directions for all people about how and where to get the flu vaccine.

The timing is no coincidence. In a recent research note, analysts at Goldman Sachs wrote that trust in the vaccine could be a serious barrier to its ultimate eradication. “We think that the biggest challenge to ultimately lowering the disease burden and virus circulation to very low levels will be convincing the broad population to take the vaccine. Our base case assumes such broad uptake but this will likely require a safe and very effective vaccine, trust in the approval and rollout process, no out-of -pocket costs, and effective public and community campaigns.”

And news about JNJ’s latest halt has certainly not been encouraging, especially since the public still hasn’t been informed about whatever is going on with the halted AstraZeneca-Oxford trials in the US.

As we have noted, Facebook’s decision comes as Bill Gates questions the legitimacy of Trump’s FDA, and Kamala Harris tells the American people that she “wouldn’t take” a Trump-approved vaccine.

Would that be banned?

via ZeroHedge News https://ift.tt/3711GU5 Tyler Durden

It looks easy, doesn’t it? Managing a portfolio. Managing a football team.

We all think we could do it, which is why “frustrated money manager” is the core psycho-demographic that supports pretty much all financial media business models. Just like there’s a frustrated GM in all of us, which is why ESPN and sports talk radio exist.

The frustrated money manager is a very different animal than Davey Day Trader Portnoy, who – as best as I can tell – is a showman and impresario (compliments in my book) who uses trading and portfolio “management” to support his brand/media company and tout his direct investments (Penn National Gaming). Same with Jim Cramer.

No, the frustrated money manager is rarely public with his compulsion (or her compulsion, but honestly I think this is almost entirely a y-chromosome thing), unless he’s enjoyed a hot streak and starts bragging to his email buds. Which happens not infrequently in a bull market.

The frustrated money manager is almost always a smart, accomplished professional in his own field who believes VERY much in the existence of The Smart Money.

The frustrated money manager is almost always a liiiittttle bit on the make.

Three years earlier [2015], part of a €528m Vatican portfolio “derived from donations” bought structured notes containing CDS as part of a bet that Hertz would not default on its debts by April 2020, the documents show. The company filed for bankruptcy the following month, giving the Holy See a narrow escape on the investment, which paid out in full.

Other investments made by managers for the Secretariat appointed by Cardinal Becciu include financing the 2019 film Rocketman — a biopic of the musician Elton John — according to fund documents seen by the FT.

The Secretariat also bought multiple luxury residential properties in London’s Knightsbridge, and securitisations partly comprising invoices owed by the Italian state to Vatican-controlled hospitals.

The Secretariat’s investment in the London building known as 60 Sloane Avenue was made through a fund in Luxembourg in 2014 in a deal personally authorised by Cardinal Becciu. In June the Vatican’s state news service reported that Holy See prosecutors believe the investment caused “huge losses”.

It took me a long time to recognize the frustrated money manager within me, including when I WAS a money manager, and a non-frustrated one at that. And to be clear, I said “recognize”, not “eliminate” or something silly like that. No, we are ALL frustrated money managers. The only question is whether we let that dimension of our psychological makeup ruin our lives, like it did Cardinal Becciu and so many others.

Here’s the knowledge that helps me keep it under control in myself. You ready?

There is no Smart Money…

That’s the big secret. That’s the most important thing I have to say to my fellow frustrated money managers. Especially if you ARE a money manager. You can’t eliminate the frustrated money manager in you, but you can control it. Internalize this little nugget and you won’t get taken for a ride to the point where you ruin your life. Please.

via ZeroHedge News https://ift.tt/3nP9DSb Tyler Durden

Virginia Voter Registration Website Crashes On Last Day To Register Before Election Tyler Durden

Tue, 10/13/2020 – 12:20

In the latest localized malfunction of America’s elections infrastructure, the entire statewide voter registration infrastructure of the state of Virginia has just gone offline on the last day to register to vote before the election.

And in a tweet, the Virginia Information Technology Agency claimed that a cable near Route 10 in Chester, Virginia had been mysteriously cut, causing the outage on the final day that voters can register in the state.

Virginia election officials say *this* accidentally cut wire in Chesterfield County is likely why Virginia’s entire voter registration system is down…

The Virginia Department of Elections posted a statement on the registration portal explaining that the system, known as VERIS, was down, and the timeline for its return was unclear: “Due to a network outage, the Citizen Portal is temporarily unavailable. We are working with our network providers to restore service as quickly as possible.”

Technicians are reportedly on-site working to fix the outage.

It’s unclear when the outage is expected to be repaired.

This morning we were alerted by VITA that a fiber cut near the Commonwealth Enterprise Solutions Center was impacting data circuits and VPN connectivity for multiple agencies. This has affected the citizen portal along w/ registrar’s offices.

The outage comes a little over a week after a similar incident left Pennsylvania’s voter registration system down for roughly two days. That issue was traced to a data center managed by Unisys on behalf of the commonwealth.

via ZeroHedge News https://ift.tt/2Focdx8 Tyler Durden

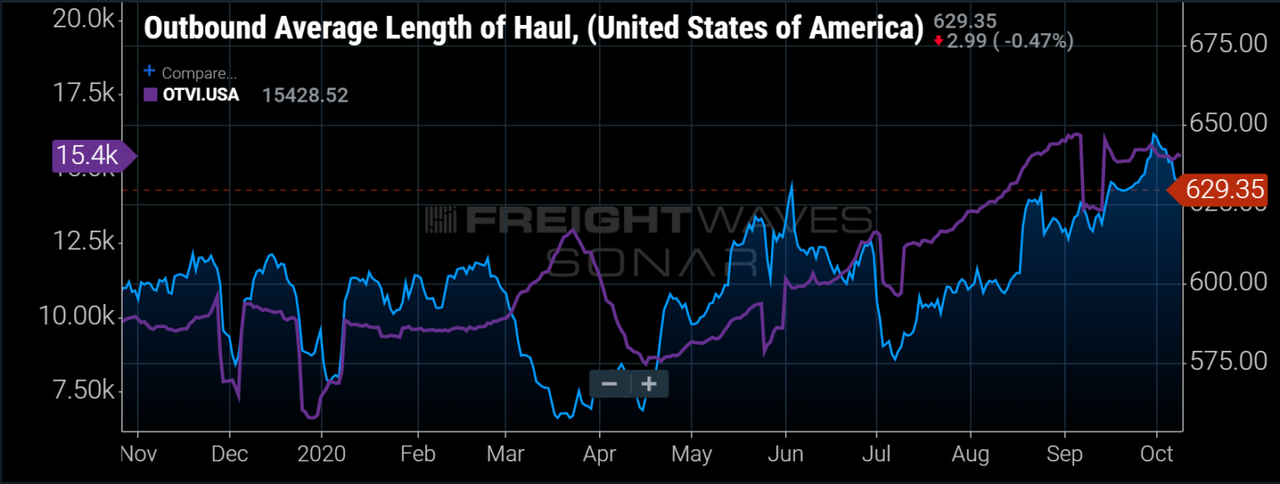

The average length of haul for requested load tenders has increased 6% or roughly 20 miles since the same period last year. This may not seem like a big deal at first, but with accepted volumes being over 20% higher than this time last year, those miles have a multiplier on them — putting a deeper strain on capacity than the tender volumes alone suggest.

Chart of the Week: Outbound Average Length of Haul, Outbound Tender Volume Index

The average length of haul for loads tendered in 2019 was 591 miles through September. Year-to-date in 2020, loads have averaged over 600 miles. Making the 2020 number a little deceiving is the fact it includes the pandemic-inspired shipping spree that saw a boom of short-haul loads in March when the average load moved 568 miles. If we remove March, the average mileage moves closer to 607. So why has the length of haul jumped so much this year?

Freight originating in Southern California has accounted for nearly 8% of the total outbound freight volume in the U.S. over the past two months — currently the first- and fourth-largest outbound markets in the country. The average length of haul for freight leaving the Los Angeles and Ontario, California, markets has been 1,059 and 879 miles, respectively, according to FreightWaves tender data. Accepted volumes have grown over 9% year-over-year in August and September in these markets. So why the growth in this region?

Shippers have been pulling record amounts of freight into the ports of Los Angeles (+18% YoY in August) and Long Beach (+13% YoY in August) over the past few months. A good portion of the imported freight, which ships in international 20-foot and 40-foot containers, gets placed directly onto the rails.

The unexpected surging container volumes have led to the implementation of peak season surcharges for any noncontracted freight that are extremely cost-prohibitive, pushing a lot of the excess volume to trucking. This move exaggerates the already tight truckload market by keeping a lid on overall domestic surface capacity.

The majority of the rail freight moves more than 700 miles, as it becomes inefficient for shorter runs due to the fact most containers need to be transported to their final destination by a truck or drayage provider off the railcar.

In addition to the Southern California freight, other markets like Harrisburg, Pennsylvania, have also seen a notable increase in longer-mileage freight requests. Harrisburg — the third-largest outbound market in the U.S. — saw its average length of haul increase from 434 miles in June and July to 469 miles in August and September.

Lakeland, Florida, loads’ average mileage has jumped 81 miles per shipment over the past year as well. Longer-haul freight tends to correlate with the need for replenishment of inventories as they dwindle. They are also connected to preparation for seasonal demand like the retail peak coming in the next two months. It would appear we are seeing a combination of both, creating a double-up wave effect in the market.

via ZeroHedge News https://ift.tt/377DSy5 Tyler Durden

Of course, BlackRock’s specialty is ETFs. Unlike mutual funds, ETFs trade intraday, giving millennial traders that non-stop rush of trading action that helps to feed their delusions of day-trading glory. BlackRock does that, and so much more the ‘systemic importance of the asset manager/shadow bank was highlighted earleir this year by the Fed’s decision to tap BR to execute purchases of corporate bond ETFs as part of the CBs’ expanded stimulus program.

Largely thanks to his firm’s success, BlackRock founder and CEO Larry Fink has morphed into a CNBC-lebrity, often joining the network’s jornalists to comment on the financial trends of the day, or offer his personal view on where markets are headed.

But on Tuesday, with BlackRock’s latest earnings haul fresh in the headlines, Fink was asked about how retail traders are transforming the asset-management industry. Ignoring the deep economic scarring endured by many, Fink replied that the outbreak is forcing people to rethink how they save and invest.

“Covid and the fear of the future has created probably a higher savings rate — we have people focusing on the long term a little more,” Fink said during the post-earnings call with reporters and analysts. “It’s leading to more savings and more investing for the long term.”

As discount brokerages like Robinhood signed up hundreds of thousands of new customers, BlackRock reported flows into all of its business lines. Retail clients added a net $19.6 billion to BlackRock funds in the period. Buyers of BR’s iShares exchange-traded funds, many of them retail investors but also institutions, took in a net $41.3 billion.

In an interview on CNBC that followed the call, Fink expounded on that point, perhaps without realizing that “FOMO” – or “fear of missing out” – has been an important factor driving markets for a long time.

“The pandemic actually has created that fear of the future, and the response is a higher savings rate in America, and a higher investment rate for the long-term,” Fink said Tuesday during the CNBC interview.

The subtext is clear: to any retail traders watching, instead of throwing your money away on those Nikola calls, maybe think about plunking your tendies into a more staid benchmark-tracking offering from BlackRock at just 3 basis points a year.

According to the latest data, the savings rate in the US has plunged in recent months as we move further and further away from the late summer’s fiscal cliff.

Fink added that this is a global phenomenon, and that retail investors are pouring money into markets in Asia, Europe and elsewhere. In fact, it’s this very trend that has led BlackRock to believe that there’s “even more upside” in the near-term for markets, as more desperate retail investors seek to parlay their meager earnings into more.

“I believe we still have more to go on the upside even in front of probably rising infection rates with Covid-19,” Fink said. “We have a strong conviction that the average investor still is under-invested, and they’re going to have to be putting more and more money to work over the coming months and maybe even years.”

In other words, there’s still some juice to be squeezed from retail traders who, thanks to the advent of payment-for-order-flow no have an outsize impact on market swings.

Fink’s image of the economy was predictably rosy: he confidently suggested that Congress would dole out another stimulus package after the election, and added that Fed stimulus will keep stocks elevated for the time being.

And when it comes to the influx of retail investors, they’re not all going to Robinhood: Fink added that BlackRock has also seen more younger investors putting money to work in its marketplace.

“We are seeing a record amount of retail participation in the marketplace,” Fink said, contending it was more than just novice day traders using online brokerages such as Robinhood. “Across the board, the average investor is putting more and more money to work, which is a good outcome. I do believe that pandemic actually has created that fear of the future and a response is now a higher savings rates in America, a higher investment rate for the long term.”

As far as the long-term implications of the burgeoning federal debt, Fink asserted that investors shouldn’t worry about that right now.

“Monetary policy…creates more income equality because monetary policy lifts financial assets, and it is really mostly the wealthy people who own all the financial assets, and that’s why fiscal stimulus is so important,” Fink said.

“These deficits will matter some time in the future but it is not a problem for this moment,” Fink added. “I do believe the aggressive nature of central bank behavior is basically foretelling us that we should not worry about rising interest rates at this time so let’s focus on rebuilding our economy over the next year or so, and so we have a more broad-based economic growth for everyone.”

{kind=link}