“It’s Happening Again” – Traders Store Oil At Sea As Recovery Falters Tyler Durden

Thu, 09/10/2020 – 13:50

Crude prices slid Thursday as the stalled global economic recovery from the virus pandemic triggers a “second wave” of demand fears and sparks renewed interest in floating storage as the oil market flips bearish.

Reuters said a “fresh build-up of global oil supplies, pushing traders including Trafigura to book tankers to store millions of barrels of crude oil and refined fuels at sea again.”

Floating storage, onboard crude tankers, comes as traditional onshore storage nears capacity as supply outpaces demand.

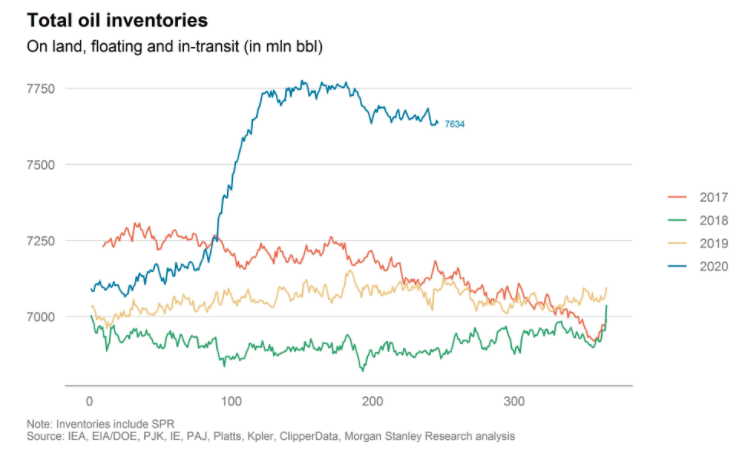

Total Oil Inventories

Refinitiv vessel data shows trading house Trafigura has recently chartered at least five crude tankers, each capable of 2 million barrels of oil.

The inventory build up, driving up demand for floating storage comes as OPEC+ recently trimmed supply curbs from earlier this year on expectations demand would improve. Though with the peak summer driving season in the US now over, demand woes and oversupplied markets are pressuring crude and crude product prices.

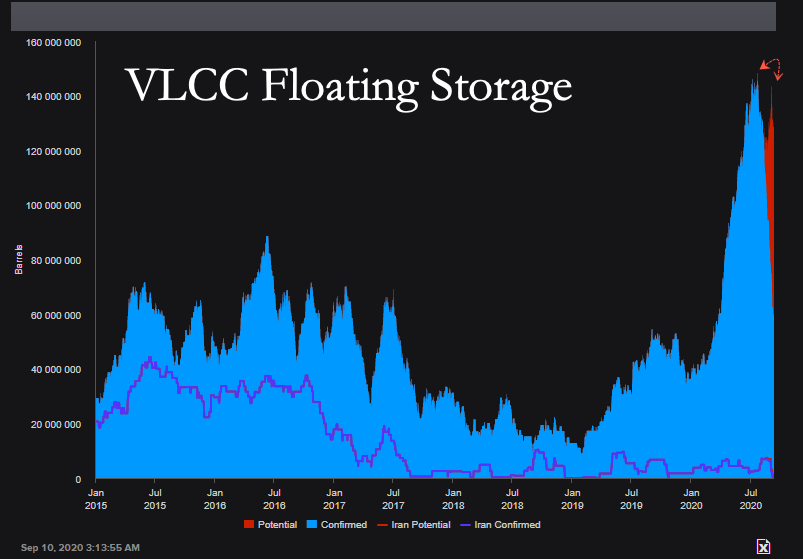

Very large crude-oil carrier (VLCC) storage has started to rise once again.

“Despite the recent slide in oil prices, we think that the OPEC+ leadership will continue to direct its efforts towards securing better compliance rather than pushing for deeper cuts at this stage,” RBC analysts said.

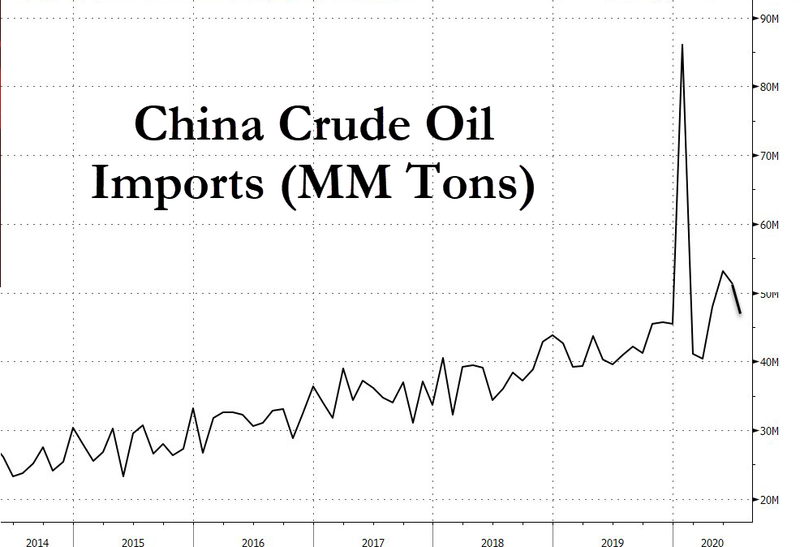

Another catalyst for the bearish tilt in crude markets is that China’s oil imports are likely to subside as independent refineries have reached maximum annual oil import quotas.

Reuters notes, in a separate report, that other top commodity traders are booking tankers to store crude products at sea, including diesel and gasoline.

Refinitiv vessel data also shows Vitol, Litasco, and Glencor have been booking tankers in the last several days to store diesel for the next three months.

“The market is soft and bearish, and floating storage is returning again,” a market source told Reuters.

Morgan Stanley analyst Martijn Rats said in a note that “it is increasingly clear that market fundamentals are not improving as quickly as expected, particularly on the demand side.”

A faltering global economic recovery, combine with oversupplied crude markets and waning demand, is weighing down November Brent crude contracts, down 15% in the last seven sessions.

Americans may finally be waking up, even minimally. A majority of those living in the United States believe that the government is corrupt and unaccountable.

This brings to mind a quote:

“Power tends to corrupt, and absolute power corrupts absolutely.”

-John Dahlberg Acton

That means that anytime you hand power to anyone, their morality will decrease as the desire to control others increases. No one cedes power willingly either. If we have learned anything from 2020 it’s that those in power or authority figures are not in it for us, but themselves.

Seventy-three percent of Americans say that elected officials do not face “serious consequences” for misconduct, according to a new Pew Research Centerpoll.

A closer look reveals that a mere 21 percent of those leaning Democrat and 32 percent of Republicans believe there is some basic justice for delinquent politicians.

This is not the only issue where US liberals and conservatives almost reach a consensus.

Seventy percent of US citizens don’t think the government is “open and transparent,” while 60 percent of both Republicans and Democrats believe that judges aren’t free from the influence of parties and politicians.

However, Americans still think reform is the answer. It’s not. Not allowing others to have power over you is the answer. That means once the system falls (and it will) we replace it with nothing. No more masters and no more slaves. The good news though, is that some Americans are at least finally understanding that corruption is inevitable in every government under any “established rule” over others.

It’s time to figure it out. In fact, it’s past time. We all need to stand up, unite, and stop allowing other people to steal from us, dictate to us, start wars, and use order followers to enforce the “laws.” We don’t need them. They need us. Once we withdraw our consent to be governed (which means controlled) it’s over. We are not their property or their slaves. We all need to realize this quickly.

via ZeroHedge News https://ift.tt/3bMGbqv Tyler Durden

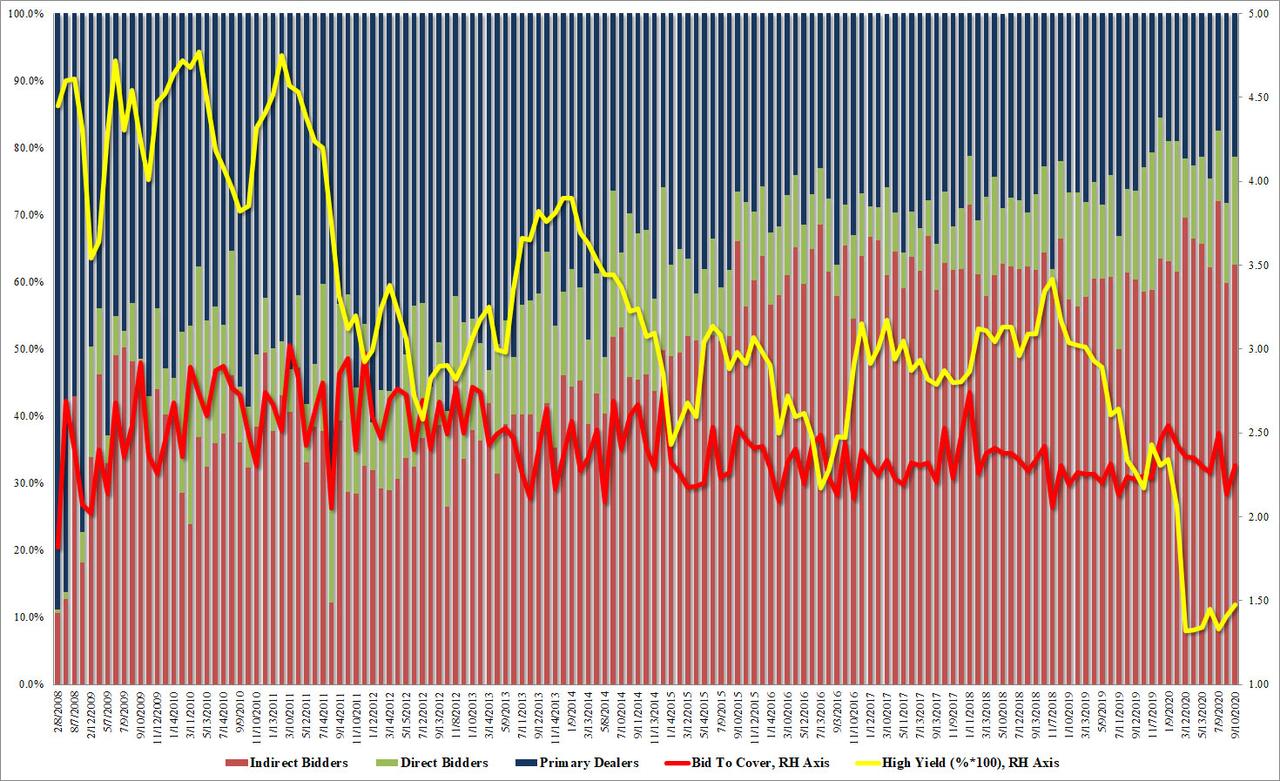

Solid Demand For 30Y Treasury Auction Sends Bond Yields Lower Tyler Durden

Thu, 09/10/2020 – 13:14

After an average 3Y auction, and a subpar 10Y reopening yesterday, moments ago the Treasury completed its sale of coupon bonds for the week when it sold $23 billion (down from $26 billion last month) at a high yield of 1.473%, which was the highest yield on the 30Y since February, although stopping through the When Issued of 1.476% by 0.3bps, demand was stronger than in recent auctions at least superficially.

The Bid To Cover of 2.31 was above the August 2.14 which was the lowest since last August, and was right on top of the 6 auction average of 2.31.

The internals were a tad weak, with Indirects taking down 62.6%m which while above the 59.8% last month was below the recent average of 66.0%. And with Directs taking down 16.1%, the highest since February, Dealers were left with 21.3% just below the 22.6% six auction average.

Overall, another average auction although the lack of a tail was taken as positive by the market, and helped the 10Y yield dip from an unchanged, 0.70% by 1bp to 0.69%, a move which makes sense as stocks are taking on water.

via ZeroHedge News https://ift.tt/3hcLZKY Tyler Durden

Private Equity Firms Use Junk Loans To Fund Dividend Payments Tyler Durden

Thu, 09/10/2020 – 13:09

Back in March, in the aftermath of the Fed’s announcement it would start buying corporate investment grade and some high-rated junk bonds, we pointed out that the bond market had torn in two, with the part of it that was explicitly backstopped by the Fed trading at (or above) par regardless of fundamentals, while “deep junk” issues tumbled as investors shied away from any fixed income issue that did not have a friendly Fed backstop. Since then this decoupling has persisted, especially for issues in the hard hit energy and retail sectors, making capital raising next to impossible for the issuer companies many of which were private equity portfolio companies. Needless to say, this made debt-funded shareholder friendly actions next to impossible.

Yet half a year later, private equity firms have found a loophole: instead of selling junk bonds for which there is still little demand, they are instructing portfolio companies to sell secured loans and use the proceeds to fund sponsor dividends in what Bloomberg called a new round of “aggressive deals.”

Taking advantage of thin supply in the deep junk space, five deals are currently being marketed fund shareholder dividends, accounting for half of this week’s volume, and the most in a week since 2017, according to Bloomberg data. Sponsors are taking advantage of rising loan prices in the secondary market despite continued weeks of outflows.

Of course, with corporate leverage already at record highs, private equity firms are merely piling on even more debt onto their portfolio companies as yield-starved creditors look for sound investments.

Some examples:

Snack maker Shearer’s Foods debt to EBITDA will rise above 7x after a $985 million first-lien loan rated B- is used by the company’s PE investor, Ontario Teachers’ Pension Plan, to recoup most of its initial investment in the business.

TPG-owned cable provider RCN Grande Wave will see its leverage rise to a similar level, S&P said, after borrowing $1.19 billion in term loans and $2.25 billion in bonds. Some of those are rated CCC+.

For those wondering if the new loans continue the tradition of issuing covenant-lite debt, Bloomberg has the answer: “in some cases, sponsors are also asking investors to loosen a key protection that allows the debt to stay in place even if the company is sold to another firm. Power generator Linden, is one such example, marketing loans with exemptions to the change of control provision.“

KKR already successfully circumvented the 101 change in control put earlier this this summer, when the private equity giant squeezed a $560 million dividend in July from Epicor Software through a $2.75 billion loan, only to sell the company to Clayton, Dubilier & Rice the next month.

Continuing this trend, we wonder how long until the first third-lien, PIK loan dividend deal hits the market.

Stepping away from the leveraged loan market, the euphoria in the corporate bond market continues unabated, and on Wednesday, new IG issuance totaled $21.3bn across 16 deals, bringing the weekly total to $41.7bn – in line with the $44.2bn average from the first two days after Labor Day in 2019 and 2018, and a record $1,506.6BN YTD – 65% ahead of last year’s pace.

via ZeroHedge News https://ift.tt/2Zqq50E Tyler Durden

No one predicted that the container industry would be doing this well, this quickly.

“We’ve been scratching our heads a lot, trying to figure out why ocean freight prices have climbed so high,” commented Eytan Buchman, chief marketing officer of Freightos, on Wednesday.

The bullish view is that import demand will continue to surprise to the upside. Ocean rates evidence a U.S. economic rebound. COVID erased demand for some products and services, but increased demand for other products. Storefront sales won’t recover, but e-commerce sales will offset storefront losses. Government support will counter shutdown fallout.

The bearish view is that the economic-fallout shoe has yet to drop. Demand for ocean container transport is being temporarily juiced by the tail end of waning government support, a switch to higher inventory levels — for both defensive and e-commerce reasons — and by bookings brought forward ahead of Chinese Golden Week (Oct. 1-7).

Another dip ahead?

Panjiva, a unit of S&P Global Market Intelligence, reported Wednesday that U.S. seaborne box imports hit an all-time monthly high in August.

“I find it difficult to see this situation as a permanent stable reversal given the underlying economic issues from the pandemic,” opined Lars Jensen, CEO of SeaIntelligence Consulting.

He foresees “another dip for container-shipping volumes” before “getting back on a more permanent upturn.”

According to Buchman, “Demand for ocean freight out of China is still outpacing supply [although] some of the current demand can be attributed to pre-loading ahead of the [Golden Week] break.

“The surge in volumes is leading to equipment shortages in Asia.” he continued. “Some shippers are paying premiums on top of spiking rates to guarantee containers and space. The imbalance is also putting pressure on overwhelmed U.S. ports and importers to process and return empty containers quickly.”

FreightWaves Maritime Expert Henry Byers believes volumes have peaked. “From here, volume will remain on a relatively stable decline through the end of year,” he predicted.

Containers from China are flooding into California ports. (Photo: Jim Allen/FreightWaves)

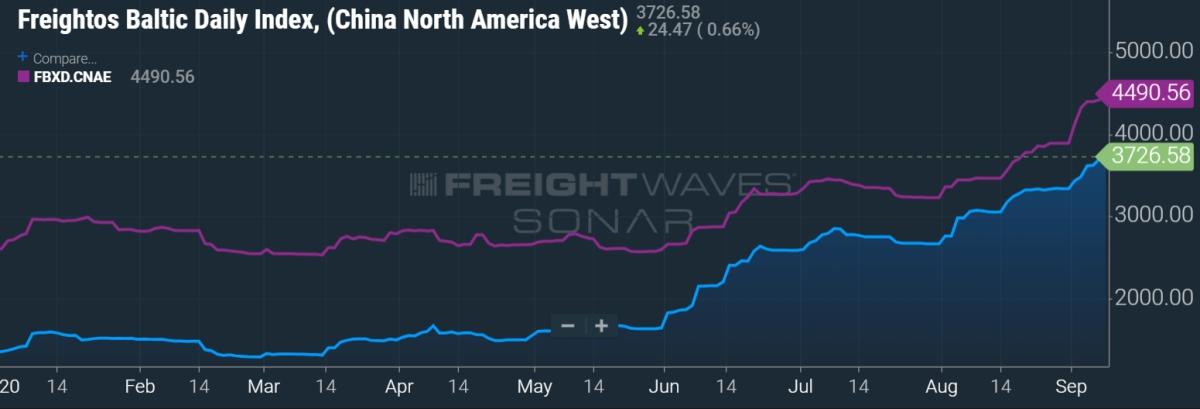

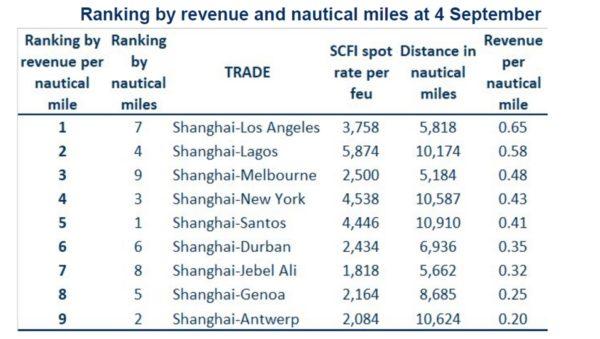

Asia-US rates still soaring

The Shanghai Containerized Freight Index (SCFI) put Asia-West Coast spot rates at $3,758 per FEU for the week ending last Friday. The SCFI estimate for Asia-East Coast spot rate was $4,538 per FEU.

The Freightos Baltic Daily Index shows the same trend but slightly lower numbers. It has Asia-West Coast rates at $3,727 per FEU as of Tuesday and Asia-East Coast rates at $4,491 per FEU.

Trans-Pacific earnings ‘remarkable’

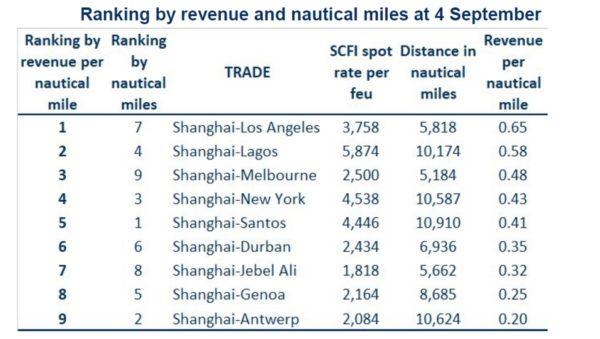

According to Alphaliner, “The recent surge in spot rates from Shanghai to California … has made this route the most lucrative for carriers for exports out of China.”

Alphaliner combined the SCFI numbers with a distance calculator to determine earnings per nautical mile for each route out of China. Shanghai-California came in at 65 cents per nautical mile, Shanghai-New York 43 cents and Shanghai-Antwerp just 20 cents.

“The fact that earnings per nautical mile are more than three times as high on the Asia-USWC [U.S. West Coast] route [versus Asia-North Europe] is remarkable, as carriers need less resources on a shorter trade,” said Alphaliner.

“A typical Far East-North Europe service requires … 12 ships, whereas six ships are sufficient for a Trans-Pacific Southwest [U.S.] loop,” it noted, attributing the rate disparity to “very strong cargo demand on the trans-Pacific.”

Inactive fleet down, charter rates rebound

When coronavirus pummeled import demand in the second quarter, carriers reduced sailings. Carriers idled ships and let charters expire. They booked new charters at much lower rates. Now, carriers are scrambling to lease in as much as tonnage as they can — and they’re paying up for it.

The inactive fleet peaked at over 12% of the total fleet in late May. According to Alpahliner, it was down to just 3.4% as of Aug. 31.

Simultaneously, “the charter market continues its rapid recovery, with charter rates in many cases back to or higher than their pre-COVID-19 level,” said Alphaliner.

Ships carrying 7,500-11,000 TEUs “remain sold out.” The 5,500-7,499 TEU segment “is now sold out” after a recent fixture. Meanwhile, rates for the 4,000-5,299 TEU segment “have gone into overdrive,” said Alphaliner.

Year-to-date total returns of GSL, Costamare and Danaos. Chart: Koyfin

In mid-August, Stifel analyst Ben Nolan called container-ship leasing names the “single most compelling investment opportunity in traditional shipping.”

Asked by FreightWaves on Wednesday whether he still believes so, he replied, “Nothing has changed to dampen my view. The container markets have already moved and some of the [leasing] securities have not.”

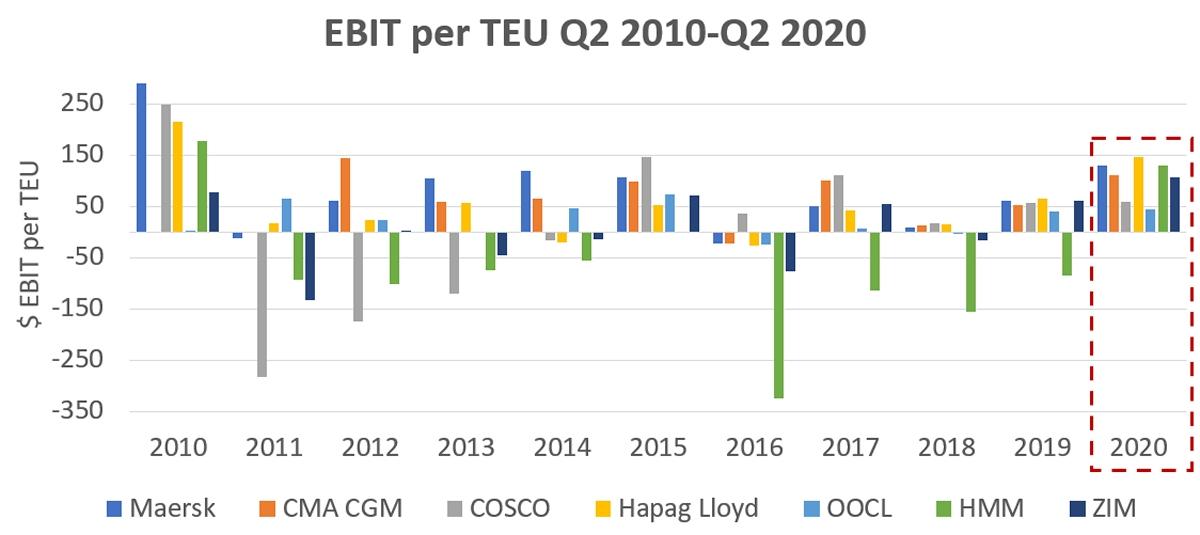

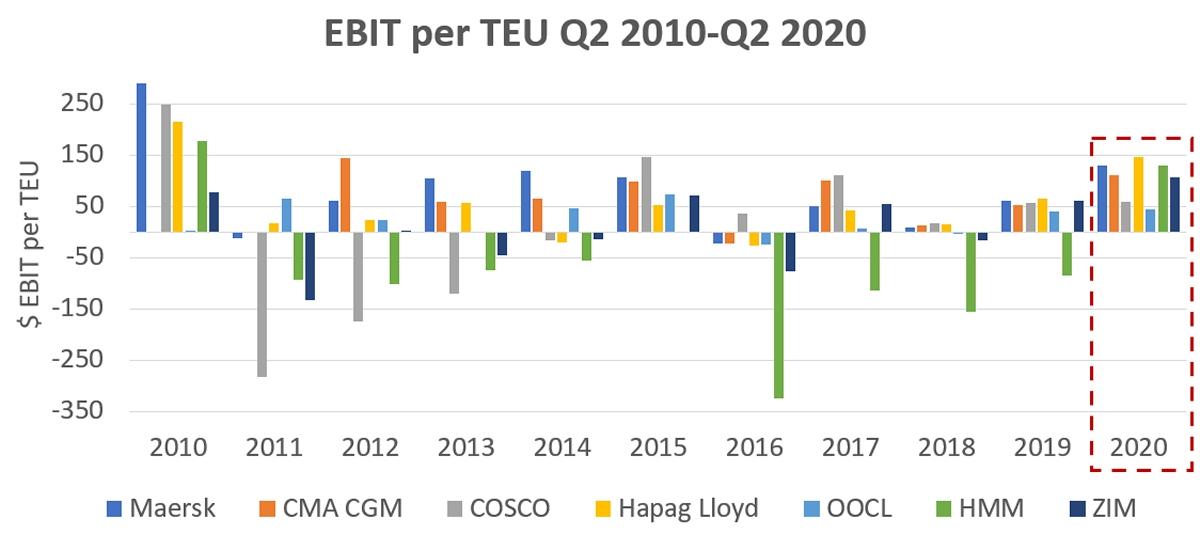

Sea-Intelligence analyzed each liner company’s reported earnings before interest and tax (EBIT) per TEU for the second quarter of 2020 and prior years back to 2010. Hapag-Lloyd led the pack in the latest period, with EBIT/TEU of $146, with Maersk at $129.

According to Sea-Intelligence CEO Alan Murphy, “A positive EBIT/TEU basically means the shipping line is making an operating profit for every TEU transported.” The second quarter of 2020 was “the first time since 2010 that all reporting carriers have had a positive EBIT/TEU,” he said.

Assange Trial Abruptly Halted After US Attorney Exposed To COVID-19: “Courtroom At Risk” Tyler Durden

Thu, 09/10/2020 – 12:30

During the fourth day of resumed Julian Assange extradition hearings the judge has unexpectedly halted proceedings due to one of the lawyers possibly being exposed to coronavirus.

District Judge Vanessa Baraitser said the London hearing has been adjourned until at least next Monday, pending the US government’s attorney awaiting results of a COVID-19 test.

Assange transported from the Old Bailey in London this week, Getty Images.

The judge and lawyers for both sides are said to be in deliberations over what course the hearings should take if indeed the US lawyer is confirmed with COVID-19.

The WikiLeaks founder’s defense team is especially concerned over the fragile health of their client, given he’s been held within the harsh and virus-prone confines of Belmarsh prison:

Assange’s attorney, Edward Fitzgerald, said it had to be assumed that the lawyer had the virus and “COVID will be in the courtroom.”

“Court staff themselves would be at risk, and you yourself may well be at risk,” he told the judge.

“Finally, our client Mr. Assange, who is vulnerable you are aware, would be at risk in court.”

Baraitser then reiterated, for those in video link who didn’t hear, that one of barristers on prosecution team may have been exposed to COVID-19. Testing will occur today. Results expected on Friday. #Assange

The New York Times described the hearing’s pause as having happened “abruptly” after it was made known of the US federal government team’s exposure.

Looking forward to the courtroom sketch of Assange in a glass box with only judge in the room as we all proceed virtually. That’ll be quite appropriate image for this case. #COVID19#AssangeCase

It’s as yet unknown which among the prosecution’s team is undergoing testing, but at this point it’s likely all of them will.

Leaked image of a prior London court appearance months ago, via The Gray Zone.

According to notes from journalist Kevin Gosztola, reporting on the trial live from the Old Bailey courthouse, the US attorney’s test results are expected back Friday.

via ZeroHedge News https://ift.tt/3hmV8R3 Tyler Durden

“One of the best rules anybody can learn about investing is to do nothing, absolutely nothing, unless there is something to do… I just wait until there is money lying in the corner, and all I have to do is go over there and pick it up… I wait for a situation that is like the proverbial ‘shooting fish in a barrel.’”

Perhaps the most important lesson about investing I’ve learned is when there is nothing to do, do nothing. The problem is nothing may actually be the hardest thing to do. We all want to feel like we are being proactive and that requires doing something even when there’s really nothing to be done. So it takes a great deal of discipline to actually resist the urge to do something and commit to doing nothing. In that way, however, committing to doing nothing is probably the most proactive thing to do.

When it comes time to actually do something, to put money to work, you will know by the fact that it is such an attractive opportunity you would be foolish not to take advantage of it. These certainly don’t come around often but when they do they are so obvious they slap you upside the head. As Jim Rogers says, it’s like seeing, “money lying in the corner,” and all that is required of you is bending over and picking it up. That’s what it feels like when it’s time to stop doing nothing and start doing something.

Another way to think about this is to realize that the vast majority of mistakes investors make come out of a feeling of needing to do something, of being proactive, rather than of simply waiting patiently to react to a truly fantastic opportunity. Rather than react only to true opportunity, they react to social pressure or envy when they see their neighbor making a “killing” in dotcom stocks, ala 2000, or residential real estate, ala 2005, or in call options today.

Meanwhile, when a truly terrific opportunity arises they are paralyzed by the fear of going it alone, without the comfort of the company of others, a la stocks in 2009, real estate in 2012 or gold in 2015. Or they just aren’t paying attention. They order Domino’s Pizza every week for decades but never think about buying one of the best performing stocks of the past several decades. They upgrade their iPhone every year or two but are too afraid to buy the stock after Steve Jobs passes away and the stock tanks to its lowest valuation in years.

Right now, due to the extraordinary circumstances in the world, politics, the economy, monetary policy and more, the urge to do something is even greater than normal. However, the opportunity to put money to work is simply not there. At least not yet. But it’s coming. And until it does, the most proactive thing an investor can do is simply commit to doing nothing, understanding that that is not a passive decision but a very proactive one, indeed.

via ZeroHedge News https://ift.tt/2FoBGGB Tyler Durden

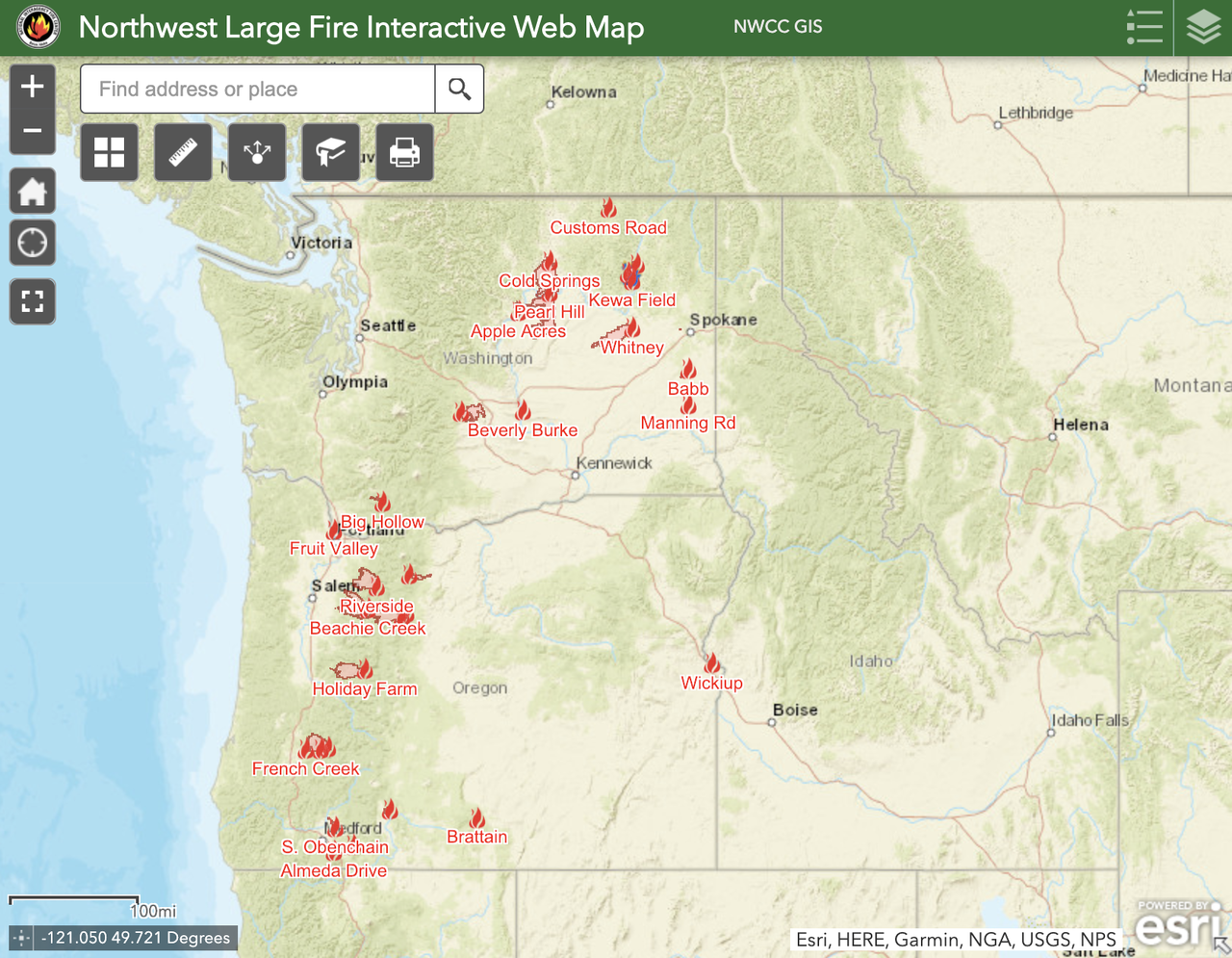

Oregon Faces “Greatest Loss Of Life In State History” From Wildfires As La Nina “Threatens Bigger Blazes, Storms” Tyler Durden

Thu, 09/10/2020 – 11:55

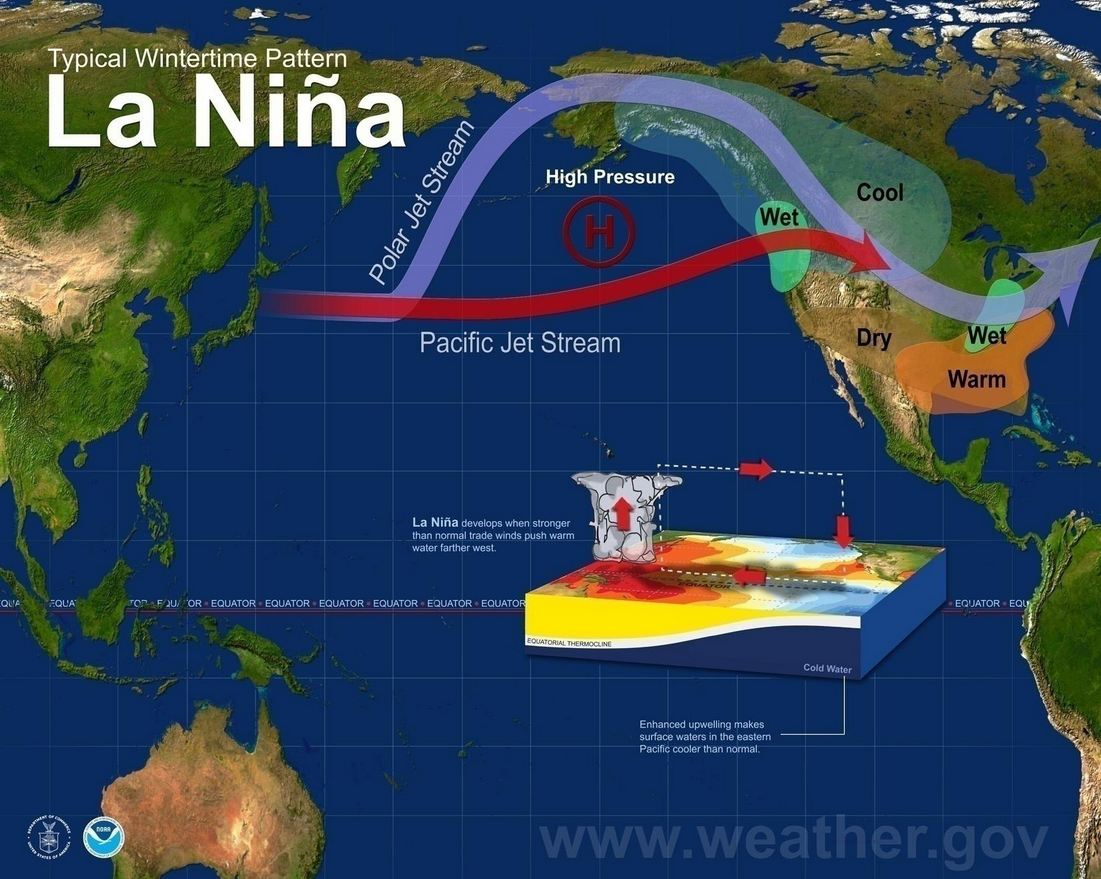

As wildfires move north from California, the state of Oregon is being engulfed in dangerous wildfires – some of the most destructive in its history – as La Nina conditions drive some of the worst wildfires seen in the American West in years.

The weather pattern has also been blamed for the latest string of hurricanes that have hammered Gulf Coast and East Coast states over the past several months.

Gov. Kate Brown said the communities of Blue River and Vida in Lane County had been devastated by wildfires this week, while Phoenix and Talent, in the southern part of the state, have reported “significant damage,” the Portland Tribune reported.

Brown said, “this could be the greatest loss of life and structures due to wildfire in state history. “

The state’s fires remain largely unchallenged Thursday morning as emergency personnel continues to evacuate thousands of people to safety. Doug Grafe, with the Department of Forestry, said the fire situation in the state is “zero percent containment.”

“The largest blaze is the Santiam/Beachie Creek Fire, at 132,450 acres burned east of Salem. It is zero percent contained. The Lionshead Fire has burned 109,222 acres. Fire officials said they expected the fires in the Santiam River area to combine into one large blaze about 3,000 firefighters are deployed,” The Tribune said.

The wildfires burning on Oregon come as “historic” wildfires burn out of control across California. Gov. Gavin Newsom said Tuesday that as many as 3,400 building structures had been destroyed with at least 2.3 million acres burned.

As the following chart shows, air quality across California and Oregon is at an extremely dangerous level…

Volatile U.S. weather this summer could be explained by an ultra-cool water pattern in the Pacific known as La Nina. The U.S. Climate Prediction Center (CPC) confirmed La Nina in the Northern Hemisphere was formed in August.

La Nina “triggers an atmospheric chain reaction that stands to roil weather around the globe, often turning the western U.S. into a tinder box, fueling more powerful hurricanes in the Atlantic and flooding parts of Australia and South America,” Bloomberg said.

The CPC said La Nina produces broad changes to weather patterns that create ‘bigger wildfires’ and more tropical activity in certain parts of the Northern Hemisphere.

“We’re already in a bad position, and La Nina puts us in a situation where fire-weather conditions persist into November and possibly even December,” said Ryan Truchelut, president of Weather Tiger LLC. “It is exacerbating existing heat and drought issues.”

EU Threatens Legal Action, Demands UK Scrap New “Intermarket Bill” By Month’s End As Brexit Talks Suddenly Matter Again Tyler Durden

Thu, 09/10/2020 – 11:38

As expected, Brussels isn’t thrilled about new draft legislation from UK PM Boris Johnson that would effectively invalidate the hated “Irish Backstop” – as the provision in the withdrawal agreement was known before the treaty was ratified – and in a throwback to the thick of the deal talks from the spring of 2019, the latest news on the Brexit front is being blamed for a turnaround in US stocks.

Following a day of deal talks between the UK and EU in Brussels, Commission VP Maros Sefcovic – the lead representative on the joint committee overseeing the withdrawal agreement – threatened legal action and threatened to cut off talks. In an official statement delivered by Sefcovic, the new legislation introduced by PM Johnson and his allies had “seriously damaged” trust between the EU and UK and that “it would constitute an extremely serious violation of the Withdrawal Agreement and of international law”. They demanded that the bill be scrapped by the end of the month “or else”, according to Sky News.

The demand follows an “extraordinary meeting” on Thursday between the EU-UK committee overseeing the deal, led by Sefcovic and Cabinet Office minister Michael Gove. Sefcovic also reportedly told Gove the withdrawal agreement was a “legal obligation” and that the EU “expects the letter and spirit of this agreement to be fully respected”. The meeting was called by Brussels.

The so-called “Intermarket Bill” is London’s attempt to “clarify” the withdrawal agreement. Prime Minister Boris Johnson has defended the Internal Market Bill by claiming it would “ensure the integrity of the UK internal market” and ensure there are no barriers to trade inside the UK after the first of the year, when Johnson has insisted the UK will be exiting the transition period no matter what, either with a free trade agreement or based on WTO rules.

The new bill had its first reading on Wednesday, following a series of leaks over the weekend that first introduced it. Johnson has repeatedly insisted that he wouldn’t extend the transition period for trade deal talks, and that he would have no problem leading the UK out of the bloc.

It outlines a new “safety net” of rules for trade between England, Scotland, Wales and Northern Ireland to prevent disruption to the internal market inside the UK, even in the event that Britain and the EU do not reach an agreement by the end of 2020. The bill would ensure there will be no new checks on goods moving from Northern Ireland to the rest of the UK, and gives Parliament the power to “disapply” rules relating to the movement of goods. It also specifically states that provisions in the law will override parts of the withdrawal agreement, where applicable.

Others have praised it as a coup for Johnson, with Tom Luongo arguing that the EU drew first blood during the withdrawal agreement negotiations, and that this move may be the thing that finally forces Brussels to cave completely even while they fulminate about the Brits “violating international law” by amending a standing treaty.

The news sent the pound lower against the dollar, driving the buck higher, and leading to claims that the move in FX helped catalyze the turn lower in stocks earlier this morning.

via ZeroHedge News https://ift.tt/33mNm54 Tyler Durden

We’ve just come out of a summer period where nothing seemed to matter with markets relentlessly accelerating high to suddenly everything mattering as we just saw the most aggressive correction off of all time highs in the Nasdaq since the 2000 bubble.

A lot of people have written to tweeted @ me in July and August with phrases such as “technical no longer matter”. My response: Technicals still do matter and they matter greatly and there are four charts I want to highlight that show an orchestra of relevance here everyone should pay close attention to in my view.

On Tuesday I had a chance to discuss 3 of these charts in a segment on CNBC Power Lunch. As the segment ran against the clock it was short in time, hence I want to take the opportunity to expand on context of these charts a bit here in this post.

For reference here’s the clip from Tuesday to set this up:

First off let’s recognize we just had a sizable correction off of the megaphone trend line I’ve been highlighting.

This was the original chart I outlined in Bear Capitulation and Panic Buying which pointed to upside risk and resistance:

Here’s the updated chart:

Technicals matter on the upside as well as to the downside. This resistance zone mattered big time as the throw over last week may have forced capitulation, but it was violently rejected and $ES was thrown back inside the megaphone pattern. A furious run from the March lows. Note all of these upper trend line tags have come on the heels of intervention. The January 2018 top on the heels of tax cuts, the early 2020 tag on the heels of hundreds of billions of Fed repo interventions and of course this run here on the heels of $3 trillion in Fed intervention. None came on a fundamental improvement of the economy or growth.

But technicals matter on the downside as well. As you can see the March lows coincided with a tag of the lower trend line and this week’s $ES lows have so far defended the rising trend line that was initial resistance in June and is for now support.

Hence the view that there was confluent support that permitted for a long bounce trade into this correction:

Technicals still work: Lovely bounce play signaled in advance.

But also note the trend is broken. pic.twitter.com/dQnVzGwi6H

And since technicals matter I want to highlight these other key charts.

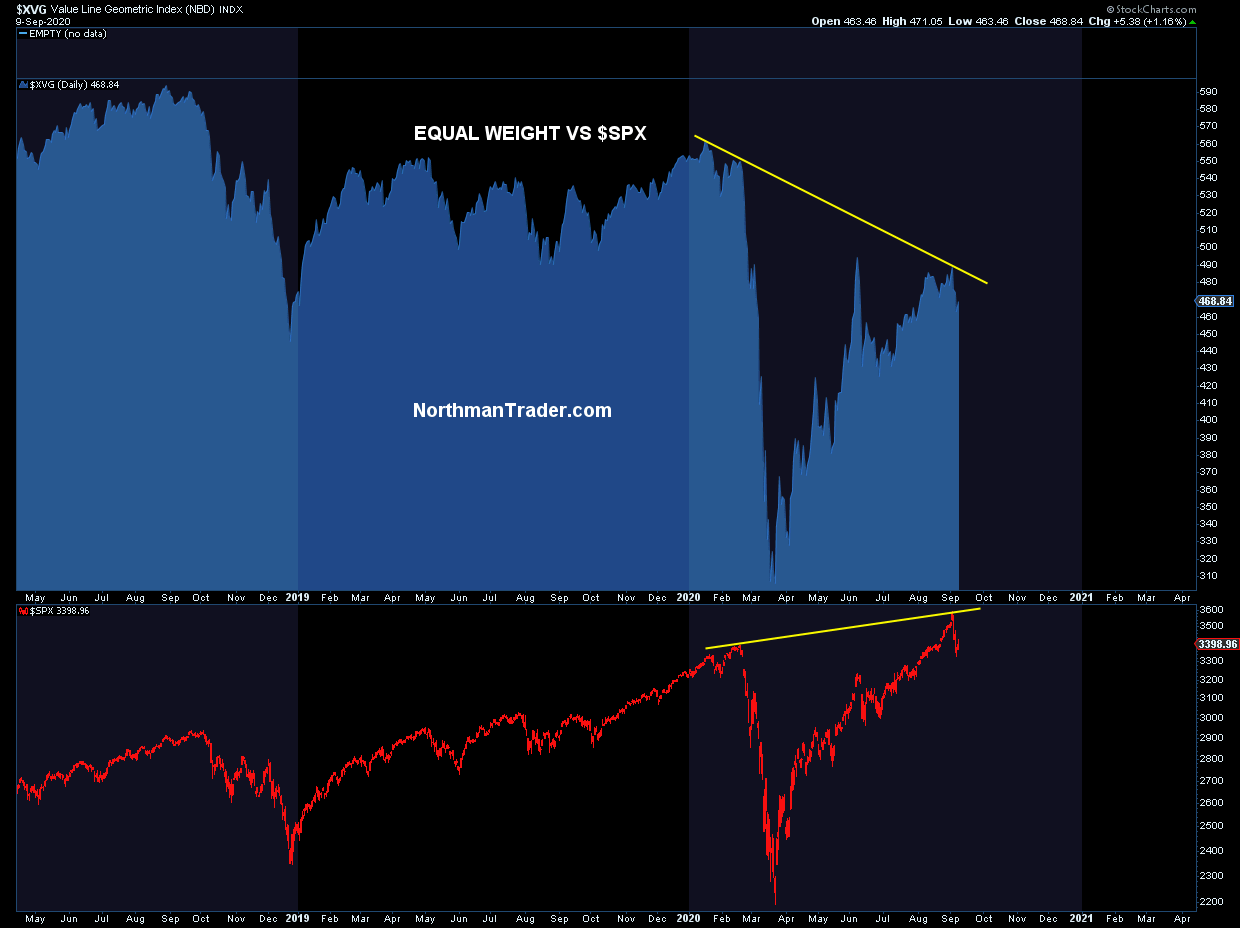

I’ve kept harping about the value line geometric index as a measure of equal weight and it keeps screaming caution and is highly suggesting that all new highs on $SPX and $NDX were literarily driven by those key techs stocks that have jumped to historic valuations:

Even during the recent run above the June highs and to new all time highs $XVG couldn’t even get to its June highs. This is how distorted these markets have become. And note the pronounced weakening that took place way before Covid. The February readings were much lower than the 2018 readings. So small caps, banks, etc, all had shown a negatively divergent market. Unless this equation changes I still consider the broader market to show signs of a bear market rally off of the March lows and the panic buying into high cap tech stocks has provided the illusion of all being well.

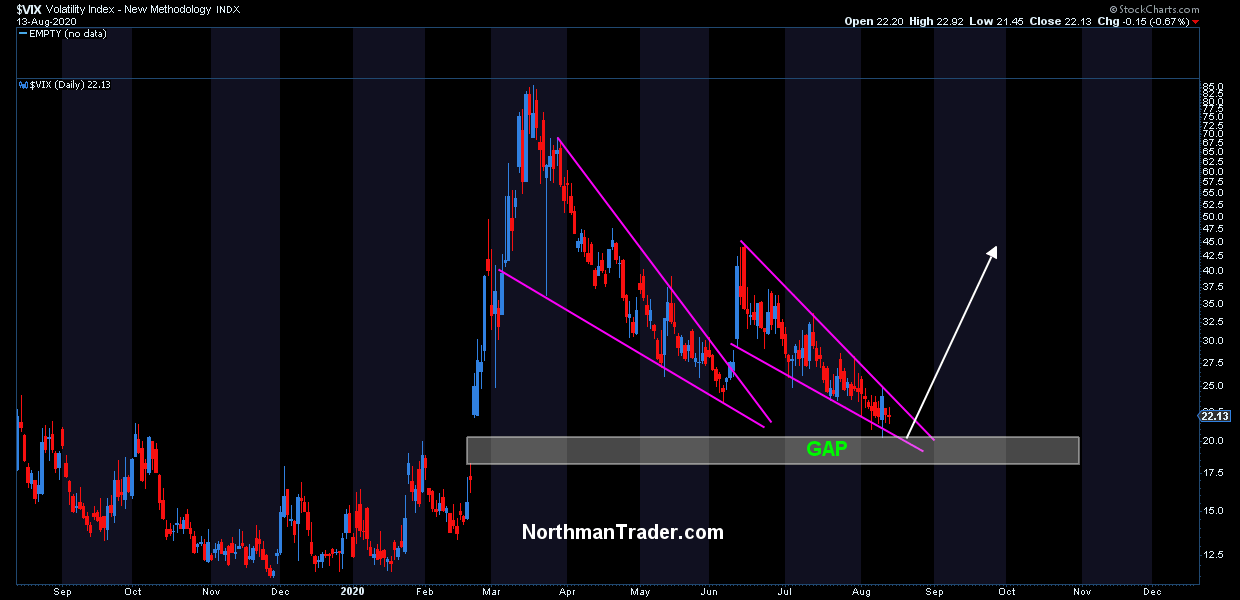

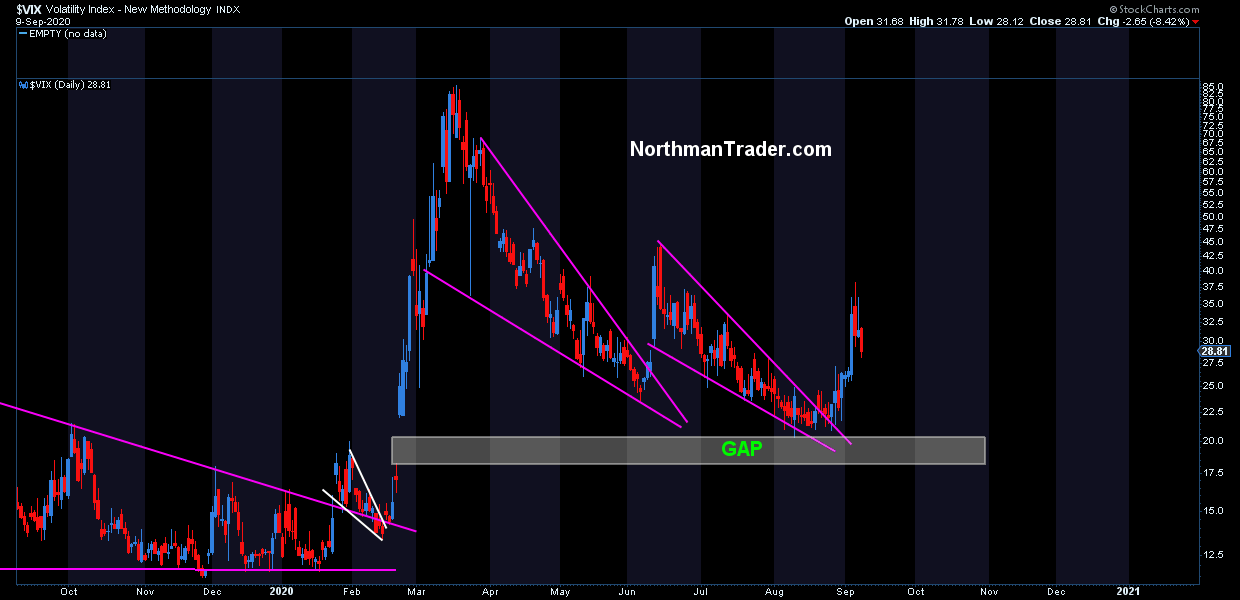

And there’s one chart that support this view and that is the $VIX. In August, with $VIX trading at 22 I highlighted this compression pattern on the $VIX suggestive of another breakout coming:

And the breakout has come to fruition:

It hasn’t reached my 46 target yet, but did manage to break to 38 last week. Whether it reaches the 46 target remains to be seen, but the larger point to highlight: With trillions in interventions and new all time highs on $SPX and $NDX $VIX should’ve have been able to fill its February gap at above 17.5. It hasn’t. Why not? The $DJIA has filled its February gap, so has the $SPX and $NDX obviously. The $VIX hasn’t and that is notable. Things are not calm is the main message.

No, these high volatility readings are supportive of the bear rally argument and the consecutive pattern spikes risk the building of a much larger volatility pattern that could spike far above 46 in due time.

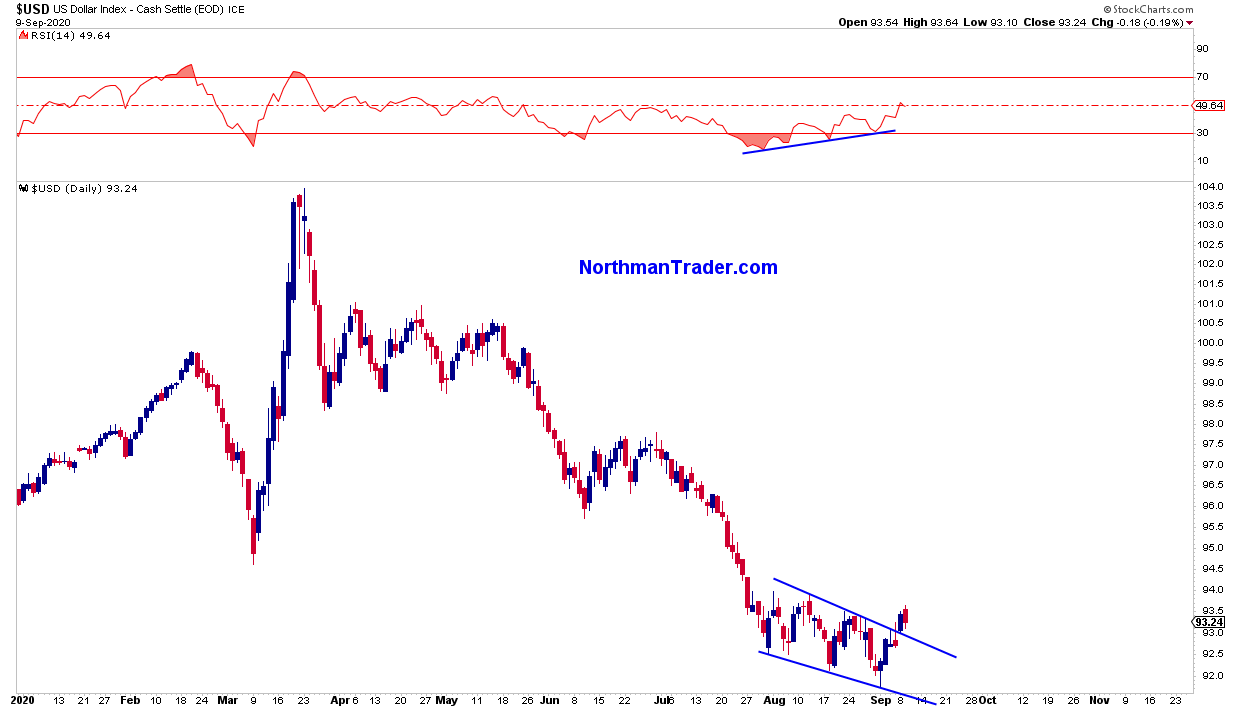

So the $VIX remains a key chart to watch, which brings me to the final chart I discussed in the CNBC interview, and perhaps the most important chart of all: The US dollar.

To the extent much of the rally has been dependent on a declining dollar the technical pattern above shows a recent breakout of the dollar out of a falling wedge pattern, a very clean pattern that has formed during the summer months and has come on a positive divergence.

If the current technical market bounce off of short term oversold conditions can’t force the dollar lower, but rather sees it perhaps retesting the pattern and then move on higher any bounce rally may prove short lived as a major dollar rally is probably least expected at this time as most participants see a long term declining dollar as a given with ongoing Fed intervention and are positioned as such.

Given this backdrop the confluence of historic overhead resistance that was rejected, a questionable internal picture of equal weight, a continued stubborn high volatility index and a potential bullish pattern in the dollar (not to mention valuations and forward multiples) make these 4 charts key to watch in the weeks ahead and make any rallies either of the lower high or even new high kind very questionable.

Technicals still do matter and they keep firing warning signs on a big structural level.

* * *

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

via ZeroHedge News https://ift.tt/3bJEHgF Tyler Durden

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}