Rabo: In Our K-Shaped World, Some Hum “Wannabe” While Others Air-Guitar “War Pigs” Tyler Durden

Fri, 09/18/2020 – 08:55

By Michael Every of Rabobank

Fifty years ago today a slice of musical genius was released unto the world. Not only does it still sound great today, it still sounds incredibly relevant. I am talking about Black Sabbath’s classic second album ‘Paranoid’, and two tracks in particular – the track of the same name, and ‘War Pigs’. The album opens with the latter, and 2020 is a year which for many reflects that initial air-raid siren over an awesome, spine-chilling guitar groan, building up to a riff that walks up to you and smacks you in the face, the intro to Ozzy’s haunting voice singing these lyrics:

Generals gathered in their masses; Just like witches at black masses; Evil minds that plot destruction; Sorcerer of death’s construction

In the fields, the bodies burning; As the war machine keeps turning; Death and hatred to mankind; Poisoning their brainwashed minds

Oh lord, yeah!

And oh Lord, yeah, indeed! Then there’s ‘Paranoid’ with its own classic riff and lyrics, which many tell me presents itself as a potential theme-tune for this Daily. I think that’s a bit unfair, as I do aim to find the humour in all this as much as I can, but that aside:

Finished with my woman; ‘Cause she couldn’t help me with my mind; People think I’m insane; Because I am frowning all the time

All day long I think of things; But nothing seems to satisfy; Think I’ll lose my mind; If I don’t find something to pacify

Can you help me occupy my brain? Oh yeah

I need someone to show me; The things in life that I can’t find; I can’t see the things that make true happiness; I must be blind

Black Sabbath (or ‘The Sabbs’) were quintessentially English, Brummie, and working class. Their music literally came from the sounds of metal being bashed together, or in the case of lead guitarist Tommy Iommi, of it slicing one of his fingertips off entirely. In his 2010 memoir, singer Ozzy writes: “In those days, the working person’s mentality went like this. You got what little education you could, you found an apprenticeship, they gave you a **** job, and then you took pride in it even though it was a *** job. And then you did that same **** job for the rest of your life. Your **** job was everything.”

With labor markets so very much on the minds of everyone, including central banks, that seems to have as much reverb today as their guitar sound. The difference between then and now, of course, is that first you get an expensive degree in something, and then you get that job; and for too many even the above jobs aren’t for the rest of their lives: in the marvellous, magical gig economy of tech disruption and swipe-rightery, sometimes it is not even for the rest of the week.

The 1970s saw high inflation, by the way. Today doesn’t (Japanese CPI was 0.2% y/y in August and -0.4% core, for example). Want inflation? Think ‘War Pigs.’

On which note, let’s get back to other normal aspects of 2020. For example, the US stating it will imminently be enforcing secondary sanctions on anyone who violates the arms embargo on Iran. The rest of the world may say that the embargo ends in October as scheduled because the US left the Iran nuclear deal, but if they want to act on that belief then they face US wrath – or at least under current management. Or we have the US selling USD7bn of arms to Taiwan in one go, including mines, cruise missiles, and drones, and another US official visiting Taipei against a backdrop of China carrying out military exercises nearby.

Or we have Israel entering a full second lockdown for three weeks (and maybe longer), as 10m in the UK are also told they can’t go to the pubs and restaurants and offices they were actually being paid to go to just a few weeks ago. Or the BOE edging closer towards negative rates, perhaps as soon as February say the markets. Let’s hope they do a better job on the preparations for that than the government has done on its test and trace scheme.

Yet never forget many in markets are not feeling Paranoid or War Piggish at all. Indeed, as they gather in their masses for central banks in their black masses to provide masses of liquidity, they are actually more like….the Spice Girls – another brashly working-class British ‘musical’ act, who encompassed the sugary, credit-driven, globalisation and neoliberalism are great 1990s as well as The Sabbs summed up the grim, 3-day-week-and-power-cuts 1970s. Indeed, the current markets-to-central banks holler-back is more like their first single, ‘Wannabe’:

Yo, I’ll tell you what I want; What I really, really want

So tell me what you want; What you really, really want

I’ll tell you what I want; What I really, really want

So tell me what you want; What you really, really want;

I wanna, I wanna; I wanna, I wanna; I wanna really, really, really

Zigazig ah!

And that is basically what markets want, and basically what they then get, upwards sloping zigazig lines on screens – and as needed, because as The Girls sagely add:

If you want my future, forget my past; If you wanna get with me, better make it fast

Now don’t go wasting my precious time; Get your act together we could be just fine.

So, to summarize, in our K-shaped world some still hum ‘Wannabe’ daily, and not in any ironic way, and others are air-guitaring their way through ‘War Pigs’ to try to find a way to satisfy. Just out of interest, ‘Paranoid’ sold 10m copies back in the days when people actually bought music; the album ‘Wannabe’ was on, ‘Spice’, sold 23m copies.

We few. We lucky few.

via ZeroHedge News https://ift.tt/3kqw5ib Tyler Durden

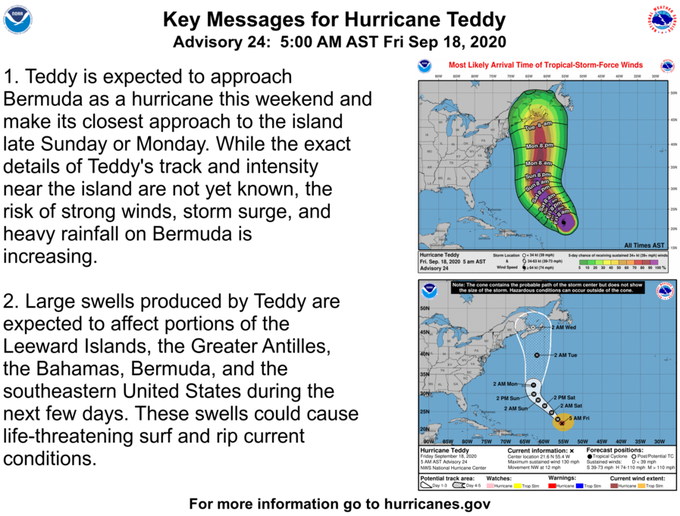

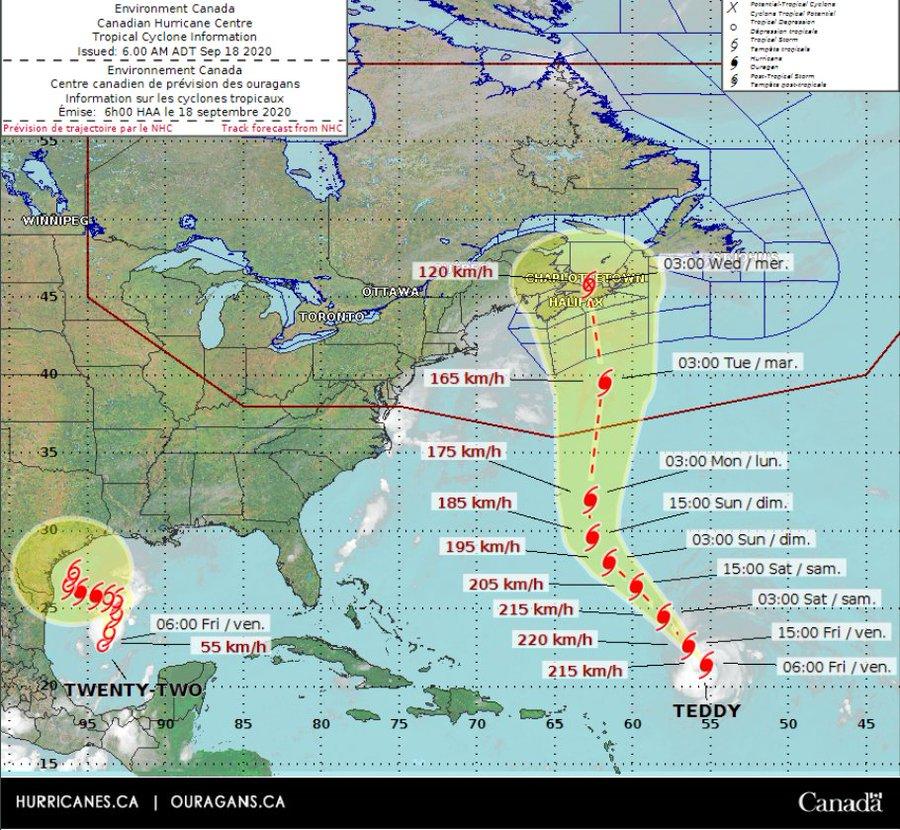

“Powerful” Hurricane Teddy Strengthens To Cat 4 With Canada In Crosshairs; Tropical Depression 22 Forms In Gulf Tyler Durden

Fri, 09/18/2020 – 08:35

The National Hurricane Center (NHC) is closely monitoring “powerful” Hurricane Teddy as it continues to churn in the Atlantic Ocean and could make landfall in Canada early next week.

As of 0500 ET Friday, Teddy is generating 130 mph winds (Category 4) while moving northwest at 12 mph and located about 900 miles southeast of Bermuda. The system is expected to make landfall near Nova Scotia, Canada, as a Category 2, on Tuesday/Wednesday.

Chief meteorologist Cindy Day of SaltWire Network, a Canadian newspaper, said Teddy “would come into Canadian waters late Monday night, and we’d start to get impacted Tuesday afternoon in Nova Scotia, Wednesday in Newfoundland.”

“It’s still quite a distance out and a lot of things could happen between now and then.

“It looks like it’s going to intensify to a 4 maybe by the end of the afternoon (Friday), so it’s a powerful system. The danger with this system is that it’s not tracking over or close to land. When systems do that, the outer bands … when they start to brush up against coastline or land, it weakens the storm system. There’s no land around. It’s out in the mid-Atlantic and it’s just churning and the sea surface temperatures are warmer than normal. So right now, there’s nothing to weaken this system,” said Day.

Day said some weather models have Teddy taking a northwest turn before heading for Nova Scotia, indicating landfall could be between Yarmouth and Halifax.

“That’s how I see the path unfolding, but again a little shift in the system over the Labrador Sea and the high coming in from Quebec and that could get squeezed further to the left or further to right. It looks like there’s going to be some impact, but how significant and where landfall is going to be – it’s a little bit too soon to say just yet.”

As Teddy churns in the Atlantic on Friday, the remnants of Hurricane Sally are moving offshore from the Southeastern/ Mid-Atlantic region.

In another NHC update, Tropical Depression 22 could strengthen into a hurricane over the weekend with models forecasting a South Texas strike.

Americans can’t let Twitter noise overwhelm political reality…

I have been watching a truly curious phenomenon over the past few days.

It seems there is suddenly a movement in media to silence anyone who speaks out against George Soros – and, specifically, his funding of radical prosecutors seeking to change the criminal justice system by simply ignoring certain crimes.

This happened to me personally this week while I was being interviewed on Fox’s Outnumbered. When I brought up Soros’s plan to get pro-criminal, anti-police prosecutors elected across the country, two of the show’s participants interrupted me and forcefully asserted that Soros was not involved.

Host Harris Faulkner, it seemed, was stunned by the interruptions, and did her part to move the show forward after some awkward silence. The next day, she addressed the strange moment during the show and condemned censorship.

Immediately after the show, Twitter and other social media went crazy. People were alleging that any criticism of Soros’s political involvement is automatically false, anti-Semitic, or both.

There are plenty of specific examples of Soros’s work in action.

Dallas County District Attorney John Creuzot, who campaigned on the promise that he would not prosecute a host of crimes—including thefts—admitted his campaign was largely funded through Soros or his groups. He has been so dismissive of crime and police that Texas Governor Greg Abbott has had to send in the Texas State Patrol to police large swaths of Dallas.

Soros gave $333,000 to the Safety and Justice PAC in 2016 to support then-Cook County District Attorney candidate Kim Foxx in Illinois—who is currently presiding over terrible violence and mayhem in Chicago, where murders are twice what they were in 2019.

Soros and his organizations spent $1.7 million to help get Philadelphia District Attorney Larry Krasner elected in 2018. Before being elected, Krasner earned a name for himself by suing the Philadelphia Police Department 75 times. Since he took office, dozens of experienced prosecutors have either been fired or resigned. Criminal prosecutions have plummeted and crime has risen. Philadelphia now has the second-highest murder rate among large cities in the country.

Former Hugo Chavez advisor and current San Francisco District Attorney Chesa Boudin was also funded by Soros and his groups. Boudin has called prison “an act of violence” and has refused to prosecute a slew of illegal acts, from public urination to the public solicitation of sex, which he deems to be “quality of life crimes.” By the way, Boudin is the foster child of Bill Ayers and Bernardine Dohrn, of terrorist group Weather Underground fame. His birth parents were convicted and imprisoned for their involvement in an armed robbery-turned-homicide.

One of Soros’s favored PACs spent $402,000 to support a failed San Diego County District Attorney bid by Geneviéve Jones-Wright.

In 2016, a Soros-funded super PAC donated $107,000 to benefit Raul Torrez in his Bernalillo County District Attorney primary—which he won by a 2-to-1 margin. In fact, Soros’s huge funding prompted the Republican running to bow out because it was just too expensive to run against Torrez.

Soros-backed George Gascon is currently challenging Los Angeles County District Attorney Jackie Lacey, who has been targeted and systematically harassed by Black Lives Matter supporters.

I’m not overly surprised to see the Twitter mob embrace a sudden, near-universal denial of these facts. I am alarmed to see that the force of this groupthink on social media appears to be strongly influencing professional media.

I think the heart of this mass denial is that Democrats and the Left are watching the terrible human cost of their misguided, pro-criminal, anti-police justice policies, and they are beginning to worry that the American people will realize who is responsible for them.

Rather than deal with something difficult—or admit they were wrong—the activists of the radical Left are trying to find some way to scream “racist” and get the media to follow suit.

America will suffer if our professional media continue to be overruled by our social media.

via ZeroHedge News https://ift.tt/3c9cGiR Tyler Durden

Commerce Department Plans To Block Downloads Of TikTok, WeChat In US Tyler Durden

Fri, 09/18/2020 – 07:46

With the White House still ratcheting up the pressure on ByteDance and China, Reuters has just confirmed American millennials’ worst fears: That is, if a deal for American control of TikTok isn’t completed by Sunday evening in the US, the Commerce Department will move to block any future downloads of the apps in the US, a critical step toward shutting them down in the US, as President Trump has insisted.

Moments later, Commerce Secretary Wilbur Ross told journalists that WeChat – another Chinese app targeted in one of Trump’s executive order – will be “shut down in the US” by Sept. 20 if a deal isn’t struck. He also said talks between TikTok and CFIUS are “ongoing”, suggesting that the deal is far from finished.

With deal talks coming down to the wire, the Commerce Department is also reportedly preparing to issue an order on Friday barring anyone in the US from downloading the Chinese-owned apps – both WeChat and TikTok – starting on Sept 20, unless President Trump rescinds the order by late Sunday evening.

According to Secretary Ross, the Department of Commerce will announce prohibitions on transactions relating to both mobile applications on Friday.

“The Chinese Communist Party CCP has demonstrated the means and motives to use these apps to threaten the national security, foreign policy, and the economy of the U.S,” the Department of Commerce said in a statement to the press, released just moments ago.

Though the comments also introduced more confusion, as the administration has apparently kicked the can once again, saying that TikTok will have until Nov. 12 before a total ban, giving the negotiators more space to hash out a deal.

US social media companies like Snap and Facebook rallied on the news. Notably, Reuters reported that the new directive wouldn’t impact US companies interactions with these apps outside the US, a provision that American corporates doing business in China have demanded, since WeChat is the dominant communications platform for people inside China.

The statement also suggests that negotiations will likely drag on past Sunday.

According to the SCMP, ByteDance says a final “deal” has not yet been signed. And even once the US and both companies assent, the Chinese Ministry of Commerce will also have a say in the final plan. So-called “Experts” who spoke to the SCMP said that there’s still potential for China to shoot down the deal.

* * *

The Commerce Department has released a statement about its latest round of “tough on China” actions targeting TikTok and WeChat:

In response to President Trump’s Executive Orders signed August 6, 2020, the Department of Commerce (Commerce) today announced prohibitions on transactions relating to mobile applications (apps) WeChat and TikTok to safeguard the national security of the United States. The Chinese Communist Party (CCP) has demonstrated the means and motives to use these apps to threaten the national security, foreign policy, and the economy of the U.S. Today’s announced prohibitions, when combined, protect users in the U.S. by eliminating access to these applications and significantly reducing their functionality.

“Today’s actions prove once again that President Trump will do everything in his power to guarantee our national security and protect Americans from the threats of the Chinese Communist Party,” said U.S. Department of Commerce Secretary Wilbur Ross. “At the President’s direction, we have taken significant action to combat China’s malicious collection of American citizens’ personal data, while promoting our national values, democratic rules-based norms, and aggressive enforcement of U.S. laws and regulations.”

While the threats posed by WeChat and TikTok are not identical, they are similar. Each collects vast swaths of data from users, including network activity, location data, and browsing and search histories. Each is an active participant in China’s civil-military fusion and is subject to mandatory cooperation with the intelligence services of the CCP. This combination results in the use of WeChat and TikTok creating unacceptable risks to our national security.

As of September 20, 2020, the following transactions are prohibited:

Any provision of service to distribute or maintain the WeChat or TikTok mobile applications, constituent code, or application updates through an online mobile application store in the U.S.;

Any provision of services through the WeChat mobile application for the purpose of transferring funds or processing payments within the U.S.

As of September 20, 2020, for WeChat and as of November 12, 2020, for TikTok, the following transactions are prohibited:

Any provision of internet hosting services enabling the functioning or optimization of the mobile application in the U.S.;

Any provision of content delivery network services enabling the functioning or optimization of the mobile application in the U.S.;

Any provision directly contracted or arranged internet transit or peering services enabling the function or optimization of the mobile application within the U.S.;

Any utilization of the mobile application’s constituent code, functions, or services in the functioning of software or services developed and/or accessible within the U.S.

Any other prohibitive transaction relating to WeChat or TikTok may be identified at a future date. Should the U.S. Government determine that WeChat’s or TikTok’s illicit behavior is being replicated by another app somehow outside the scope of these executive orders, the President has the authority to consider whether additional orders may be appropriate to address such activities. The President has provided until November 12 for the national security concerns posed by TikTok to be resolved. If they are, the prohibitions in this order may be lifted.

The notices for these actions will be posted on the Federal Register at approximately 8:45AM EDT on Friday, September 18, 2020.

Background:

On August 6, 2020, President Trump signed Executive Orders (E.O.) 13942, Addressing the Threat Posed by TikTok, and E.O. 13943, Addressing the Threat Posed by WeChat. In the E.O.s, the President determined that the apps capture vast swaths of information from U.S. users, leaving the data vulnerable to CCP access for nefarious purposes. Commerce, at the Direction of the President, was required to identify transactions within 45 days to protect national security and the private data of millions of people across the country. Today’s announced prohibitions fulfill the President’s direction and mitigate national security risks.

via ZeroHedge News https://ift.tt/3mtYpSJ Tyler Durden

Futures Flat Ahead Of Quad Witching Volume Surge Tyler Durden

Fri, 09/18/2020 – 07:32

US equity futures were flat after trading in a narrow overnight range, and European and Asian markets drifted in a volume-light session ahead of Friday’s traditionally volatile quad witching session, when the expiration of options and futures send volumes soaring as big derivatives positions roll over. As Bloomberg notes, “there may be more attention than usual after a month where the red-hot trade in tech stocks wavered and options activity dominated headlines” however since there are fewer expirations this time, it may mute the impact.

Tesla rose 2.1% in premarket trading after two analysts raised their price targets on the electric carmaker’s shares ahead of its highly anticipated “Battery Day” event next week.

Nasdaq futures rebounded after a sharp two-day selloff in technology stocks while worries about rising coronavirus cases and the economic recovery weighed on S&P 500 and Dow futures. The S&P and Nasdaq have also come under pressure from investors rotating out of high-flying tech-related stocks and into industrial and transportation firms after Powell failed to reassure investors that more monetary stimulus was on deck. Of the 11 major S&P indexes, industrials, materials and energy have gained more than 2% so far this week, while communication and consumer discretionary posted the biggest declines.

Europe’s Stoxx 600 Index was little changed after opening modestly lower, with the gauge weighed down by declines in travel and leisure shares on the threat of wider restrictions to stem the spread of coronavirus. Although activity on major gauges was modest, there were bigger moves in single-name stocks swept up in a bout of M&A.

Asian stocks gained, led by materials and IT, after falling in the last session. Most markets in the region were up, with Shanghai Composite gaining 2.1% and Japan’s Topix Index rising 0.5%, while Australia’s S&P/ASX 200 dropped 0.3%. The Topix gained 0.5%, with Alleanza Holdings Co Ltd and Sysoft rising the most. The Shanghai Composite Index rose 2.1%, with Shuangliang Eco-Energy Systems and Qibu posting the biggest advances.

Investors remain on the lookout for more U.S. fiscal stimulus after the Federal Reserve disappointed stimulus junkies even as it indicated that interest rates will stay low for at least 3 years. Meanwhile, as Bloomberg notes, data continues to show a patchy recovery path around the world as coronavirus infections surge. France’s daily cases rose by more than 10,000 to the highest since the end of lockdown in May.

“The market is somehow uninspired following recent central bank meetings,” said Robert Greil, chief strategist at Merck Finck Privatbankiers AG. “It is waiting for the next support step, be it from their side or regarding the U.S. fiscal program to be agreed finally.”

In rates, treasuries gained led by the long-end of the curve as cross-market flows emerge over Asia session, adding support. Yields were lower by up to 2bp across long-end of the curve with front-end broadly anchored, flattening 2s10s, 5s30s by 1.2bp and 0.8bp; 10-year yields around 0.672% and trading in line with bunds and gilts. The IG credit issuance slate is empty today with nearly $1.6 trillion in deal priced YTD – an all time high; nine deals brought $6.4b Thursday to push weekly volume past $40b projected.

In FX, the dollar was mixed against G10 peers and in tight ranges as traders wait for U.S. data releases amid a thin calendar and low volumes. Interbank desks look to sell dollar rallies versus the euro, the pound and the yen, Bloomberg said citing three Europe-based traders. The pound was little changed around $1.2980 as pressure from Bank of England communique fades given Brexit uncertainty remains; options-related interest in cable circa 1.2950, with sizable bidding interest just below 1.2900.

In commodities, WTI and Brent futures trimmed overnight gains and trade flat during early European hours, with little by way of fresh catalysts to induce the pullback. Still, oil is poised for its biggest weekly advance since early June. Futures in New York are up almost 11% this week as Saudi Arabia ratchets up the pressure on OPEC+ members to adhere to the group’s production cuts.

Looking at the day ahead, we’ll get the preliminary September reading of the University of Michigan’s consumer sentiment index, the August leading index, as well as the Q2 current account balance. In terms of central bank speakers, we’ll hear from the ECB’s de Guindos, Schnabel and Hernandez de Cos, along with the Fed’s Bullard and Bostic.

Market Snapshot

S&P 500 futures little changed at 3,348.25

STOXX Europe 600 down 0.1% to 370.84

MXAP up 0.5% to 173.94

MXAPJ up 0.5% to 570.32

Nikkei up 0.2% to 23,360.30

Topix up 0.5% to 1,646.42

Hang Seng Index up 0.5% to 24,455.41

Shanghai Composite up 2.1% to 3,338.09

Sensex up 0.3% to 39,076.05

Australia S&P/ASX 200 down 0.3% to 5,864.50

Kospi up 0.3% to 2,412.40

Brent futures up 0.2% to $43.39/bbl

German 10Y yield rose 0.3 bps to -0.488%

Euro up 0.04% to $1.1853

Italian 10Y yield fell 1.4 bps to 0.749%

Spanish 10Y yield rose 1.2 bps to 0.276%

Gold spot up 0.5% to $1,953.88

U.S. Dollar Index down 0.1% to 92.86

Top Overnight News from Bloomberg

U.K. Health Secretary Matt Hancock declined to rule out a second national lockdown and said the acceleration of coronavirus cases and hospital admissions across the U.K. represents a “big moment” for the country

The U.K. government said a round of informal EU trade talks this week were “useful,” as European Commission President Ursula von der Leyen told the Financial Times she’s “convinced” a deal is possible

European regulators are moving closer to lifting a de-facto ban on bank dividend payments at the start of next year. Several members of the European Central Bank’s supervisory board, who supported initial requests that banks forgo dividends, see further extensions of the ban doing more harm than good, according to people familiar with the matter

The volume of goods sold in U.K. stores and online rose 0.8% from July, the Office for National Statistics said Friday. It marked a fourth month of growth following an unprecedented slump in April, after the government ordered most stores to close to help fight the spread of coronavirus. Sales excluding auto fuel rose 0.6%, stronger than economists forecast

France’s daily coronavirus cases rose by more than 10,000 to the highest since the end of lockdown in May and Health Minister Olivier Veranwarned that the disease “is again very active” in the country

A quick look at global markets courtesy of NewsSquawk

Asian equity markets were mildly positive after shrugging off the weak lead from the US where the Nasdaq led the retreat once again to extend on the losses following the FOMC policy announcement and heading into quadruple witching. ASX 200 (-0.3%) and Nikkei 225 (+0.2%) were rangebound after failing to build upon opening momentum with strength in Australia’s commodity-related sectors offset by losses in the broader market including the top-weighted financials, while the Japanese benchmark treaded water amid a lack of fresh catalysts to instigate price action and with the latest inflation data all conforming to expectations. Hang Seng (+0.5%) and Shanghai Comp. (+2.1%) were initially indecisive with outperformance eventually seen in the mainland following the PBoC’s liquidity efforts in which it utilized both 7-day and 14-day reverse repos for the first time this month, although some cautiousness remains after recent mixed reports concerning the Oracle-TikTok deal heading into President Trump’s verdict which sources suggested could be within the next couple of days, while substantial pressure was also seen in Tencent shares due to recent underperformance in the tech sector and with its gaming stakes said to draw US national security scrutiny. Finally, 10yr JGBS were higher after recently breaking through the stubborn resistance at the 152.00 level, but with gains limited by the improving risk tone and following slightly weaker demand at the enhanced liquidity auction for 2yr-20yr JGBs.

Top Asian News

Tesla Battery Maker’s Split-Off Angers Korean Retail Investors

Foreign Judge Resigns Amid Hong Kong Security Law Concerns

Taiwan Dollar Rises Most in 6 Months as Central Bank Eases Grip

Thailand Reports First Coronavirus Death Since Early June

Stocks in Europe see a mixed session thus far (Euro Stoxx 50 -0.1%), whilst US equity futures also see no conviction amid a somewhat of a similar lead from APAC, with fundamental news-flow light on quadruple witching day (full schedule available on the headline feed). The regional bourses see a mixed performance, with Switzerland’s SMI (+0.5%) outperforming as the Healthcare sector is propped up by Pharma-giants Roche (+2.1%) and Novartis (+1.8%), with the former announcing its phase III EMPACTA study met primary endpoints in regards to COVID-associated pneumonia, whilst also rolling out a new antibody test for countries accepting the CE mark. On the other side of the spectrum resides Spain’s IBEX (-1.5%), weighed on by the banking sector in the aftermath of the formal merger agreement between Caixabank (-1.5%) and Bankia (-4.3%); with Caixabank’s CEO stating it is out of question that the merger with Bankia will allow for potentially higher dividend. Meanwhile, Banks more broadly saw fleeting upside on reports that EU regulators have moved closer to lifting the ban on dividends in 2021, nonetheless the sector remains in the red. Overall, European sectors trade mixed with no risk profile to be derived. In terms of individual movers, Covestro (+6.9%) holds onto a bulk of its opening gains amid speculation that Apollo is said to be mulling a USD 10bln takeover bid for the group, albeit the Co. said it is not in any discussions. Sticking with M&A, LSE (+0.7%) has accepted Euronext’s (+4.8%) bid for Borsa Italiana, despite it being the lowest offer, but the deal did offer a sweetener as Euronext teamed up with Italy’s sovereign wealth fund CDP and Intesa Sanpaolo (-0.1%) on its bid, with Rome keen to keep a tight grip on Borsa Italiana. Finally, Ryanair (-5.2%) is pressured after cutting its October capacity by a further 20% on top of the already announced 20% in mid-August with similar capacity cuts potentially in the pipeline for winter – also weighing on the likes of easyJet (-8.3%), IAG (-12.1%), Lufthansa (-4.7%) and Air France-KLM (-3.9%) in sympathy, with the airline sector already bearing the brunt of the European COVID-19 resurgence.

Top European News

Tesla Battery Used For First Time to Balance U.K. Power Grid

ECB Moves Closer to Lifting Bank Dividend Ban by Next Year

France Warns Virus ‘Very Active’ as Cases Rise Across Europe

Giant Glencore Coal Mine Faces Threat as Fund Refuses Backing

Hancock Refuses to Rule Out New Lockdown as Covid Surges in U.K.

In FX, the rationale or catalyst is far from clear, but disappointment in wake of NZ Q2 GDP has been relatively short-lived for the Kiwi, and remarks from Finance Minister Robertson overnight noting that the economy is rebounding from contraction may have helped along with his assurance that the RBNZ is committed to maintaining the OCR at 0.25% until Q1 next year when it will reassess the situation. Confirmation of the latter could come from next week’s policy meeting in addition to any response to the latest review of pandemic containment measures in Auckland and the rest of the country. Nzd/Usd has extended its recovery to just shy of 0.6800 vs almost 0.6600 last Wednesday, while Aud/Nzd has retreated through 1.0800 as the Aussie stalls above 0.7300 against its US counterpart following somewhat contrasting comments from Treasurer Frydenberg downplaying Thursday’s stellar jobs data by describing the labour market as still very challenging. Note also, Aud/Usd may be feeling the gravitational pull of 2.4 bn option expiry interest at the 0.7300 strike.

JPY/DXY – Not the biggest index component, but the Yen continues to exert considerable influence on the broad Dollar and DXY as it probes a Fib retracement level ahead and 104.50 following this month’s respective Fed and BoJ policy meetings, even though Japan’s Finance Minister contends that monetary easing has helped Usd/Jpy to stabilise within a 105.00-110.00 range. However, the Buck is unwinding more of its fleeting FOMC gains vs G10s in general and July 31’s 104.20 trough looms as the DXY hovers below 93.000 and not far from last week’s 92.695 base between 92.772-973 parameters.

GBP/EUR – Modest m/m beats on the UK retail sales front may be propping up the Pound, but is appears that Cable’s latest look at 1.3000 and Eur/Gbp’s pull-back from yesterday’s highs are due to renewed hopes of a Brexit trade deal given European Commission President von der Leyen’s purported confidence that an accord can yet be forged. Indeed, the short end of the UK yield curve is still tipped in favour of sub-zero rates after guidance from the BoE, while the Euro is also on a firmer footing against the Greenback, albeit tethered to 1.1850 with decent option expiries capping the upside at 1.1900 and 1.1950, while the 100 HMA is in close proximity at 1.1844.

CAD/CHF – The Loonie has pared more lost ground vs its US rival to straddle 1.3150 before Canadian retail sales, while the Franc is idling just above 0.9100 and looking further forward to September’s quarterly SNB policy review for any tweaks to the language of currency’s valuation.

EM – The Rand has extended post-SARB upside towards 16.1000 vs the Dollar with some extra impetus from the SA Government pledging Zar 10.5 bn extra funds to state carrier SAA, but the Rouble is treading cautiously into the CBR amidst expectations for a 25 bp rate cut and the Lira has slipped to another all time low. Elsewhere, the NBH has launched its first Eur/Huf swap funding facility.

In commodities, WTI and Brent front month futures have trimmed overnight gains to the point futures trade somewhat flat during early European hours, with little by way of fresh catalysts to induce the pullback. Prices yesterday saw support from the Saudi Energy Minister’s commentary, who noted that OPEC does not have to wait until December to react and will be pro-active, whilst warning oil speculators not to bet against the oil producers. Elsewhere, Tropical Depression 22 resides in the western Gulf of Mexico and is forecast to evolve to a Tropical Storm later today; although, current projections show the Depression to become a short-lived hurricane but will steer clear of major oil and gas infrastructures. WTI Nov retains a USD 41/bbl handle but resides closer to session in proximity to the psychological levels, whilst its Brent counterpart trades sub-43.50/bbl having printed a current range of USD 43.12-80/bbl. Elsewhere, precious metals eke mild gains amid the softer Buck, with spot gold meandering just north of the USD 1950/oz mark and spot silver holding onto the USD 27/oz handle. Meanwhile, LME copper hit an over-2yr peak due to the softer Dollar and optimism surrounding Chinese demand, whilst Dalian iron ore snapped a three-session loss streak as industrial data showed that the pace of portside inventory builds slowed.

US Event Calendar

8:30am: Current Account Balance, est. $160.0b deficit, prior $104.2b deficit

10am: U. of Mich. Sentiment, est. 75, prior 74.1; Current Conditions, est. 83.1, prior 82.9; Expectations, est. 67.2, prior 68.5

10am: Fed’s Bullard Discusses the Covid Recovery Challenge

12pm: Fed’s Bostic Discusses Racial Justice

3pm: Fed’s Kashkari Discusses Too Big to Fail

DB’s Jim Reid concludes the overnight wrap

Global equity markets continued to lose ground yesterday as weak economic data coupled with renewed concerns over the coronavirus dampened investor sentiment. In the US, the S&P 500 fell -0.84% in its second straight decline, with 20 of 24 industry groups finishing lower. The NASDAQ saw an even larger -1.27% decline as tech stocks underperformed the broader index. However the two indices were -1.66% and -2.41% respectively at the lows so there was a recovery especially in the last hour of trading. Earlier in Europe the STOXX 600 fell -0.51% as the index came off its one-month high the previous day.

There wasn’t a single headline that sent stocks lower, though a drip-feed of negative data didn’t help. The weekly initial jobless claims from the US through September 12 came in at 860k (vs. 850k expected), while the previous week’s number was revised up by 9k. In addition, both housing starts at 1.416m (vs. 1.488 expected) and building permits at 1.47m (vs. 1.512 expected) came in lower than consensus. Meanwhile in Europe, new EU car registrations fell -18.7% yoy in August, having been down just -5.7% yoy in June and July. With the hard data for August coming in weaker than hoped, this has added to investor jitters about the state of the global economy moving into the winter months in the northern hemisphere.

Asian markets are largely trading higher this morning outside of the Nikkei (+0.02%) and Kospi (-0.04%) which are broadly flat. The Hang Seng (+0.31%), Shanghai Comp (+0.57%) and India’s Nifty (+0.37%) are all up. However, futures on the S&P 500 are down -0.26% while those on the Nasdaq are flat. In Fx, the onshore yuan is up +0.11% to 6.7565 while the British pound is down -0.12% to 1.2958. In terms of data, Japan’s CPI and Core CPI both came in line with consensus at +0.2% yoy and -0.4% yoy respectively.

In overnight news, the Fed has said that it will decide in the next two weeks whether to prolong the limits on dividend payments and share buybacks that it imposed on the biggest US banks. Meanwhile, Bloomberg has reported that the White House has asked gaming companies where Chinese technology giant Tencent Holdings is a major shareholder, to provide information about their data-security protocols.

In terms of the coronavirus, there were further concerning signs out of Europe. Here in the UK, where there’ve been issues with testing capacity, the head of the NHS Test and Trace program said that the numbers calling the helpline and visiting the website were around 3-4 times the number of tests available. It came as a further 3,395 cases were reported yesterday, which sent the 7-day average up to its highest level since May 17. One of the biggest problems in the U.K. is that as people have been encouraged back to school and work they’ve been exposed to more minor ailments that can share Covid type symptoms. As such many have been trying to get tests to rule out Covid and to stop them being forced to self isolate. This has overwhelmed the laboratory system’s ability to process all the tests and therefore tests are effectively being rationed – albeit at relatively high daily levels still but clearly not high enough for demand.This is a warning sign of the type of things to come in the coming months.

Meanwhile in Portugal, 770 new cases were reported, which was the highest number since April, albeit with higher testing now. Over in Austria meetings indoors were restricted to a maximum of 10 people, and the Czech government officials sought tighter social-distancing measures after the country posted a daily record of 2100 new infections. France reported over 10,000 daily cases for the second time in the last week, while the 7-day average of new cases per day has steadily risen over the past month to a pandemic-high of 8800. French Health Minister Veran noted that they are, “now seeing the number of Covid patients in intensive care go up in a worrying way,” though they still remain far behind the initial springtime surge.

In the US, New York City delayed the reopening of classes for in-person learning until September 29 for elementary school students and October 1 for middle- and high-school students. Cases in NY state have been stable since mid-June, with cases increasing by between 0.15% and 0.2% on average per day. Elsewhere, Texas eased some restrictions across much of the state, citing rapidly falling hospital occupancy. Restaurants, retail stores, office buildings, factories, gyms and museums will all be allowed to function at 75% of capacity starting next Monday (Sept 21). There were more worrying signs out of Florida, where weekly cases have risen to 19,300 – the highest since the start of September. The uptick aligns with overall cases in the US rising slightly over the past two weeks after falling for much of the previous two months. These trends are possibly tied to schools and colleges reopening. Meanwhile, Reuters has reported overnight that the US government is planning to authorize more than 6 rapid antigen tests by the end of October in a bid to rapidly increase overall testing capacity to more than 200mn by year end. This will likely enable schools and workplaces to significantly expand testing.

Steadily rising global cases was the backdrop as Moderna released the details of its plan to offer increased clarity into the study of its vaccine. The CEO Bancel noted that they, “want to make sure the general public has trust in vaccines by being transparent.” Bancel added “it is extremely unlikely” everyone in the US could get vaccinated by the end of the first quarter of 2021. Overnight, Bancel told CNBC that Moderna may not be able to examine Phase 3 data until December but added that the most likely scenario currently was an interim analysis to be available in November. Hewrapped up saying “Our best plan is October. I think it’s unlikely but it is possible.” This came as President Trump continued to push that the US would be distributing a vaccine to at least some part of the public by early November or just around the election.

President Trump also made headlines by again pushing Republican lawmakers to take up the $1.5 trillion stimulus bill that was put forth in recent days. Though there was again pushback from leading Republicans, with Senate Finance Chairman Grassley saying the President “better be careful of that because I don’t think that will get through the United States Senate.” While the upcoming election is clearly slowing the process, the recent worsening economic data out of the US may eventually focus lawmakers minds more.

From central banks, the main news yesterday came from the Bank of England’s decision, who unanimously voted to keep policy unchanged. Sterling fell after the announcement however, moving to an intraday low of -0.79% as the minutes showed that the MPC had been briefed on plans to “explore how a negative Bank Rate could be implemented effectively”, and that the BoE and the Prudential Regulation Authority would “begin structured engagement on the operational considerations in 2020 Q4.” So there likely won’t be any moves in that direction this year given talks will only start in Q4, but a sign nonetheless that they’re being considered as an option.

Following the meeting, our UK economist Sanjay Raja has now moved up his call for more QE to November, having previously thought December more likely. This is because tighter social restrictions and increased tensions on Brexit in the coming weeks will offer enough ammunition to pull the trigger on additional stimulus earlier than expected. Speaking of Brexit, sterling reversed its losses following the BoE announcement after an FT headline came out saying that European Commission President Ursula von der Leyen was “convinced” that a trade deal with the UK could still be agreed. The big question now is what happens to the UK’s internal market bill. It’s still going through the House of Commons where the government has an 80-seat majority, but the big question is what will happen in the House of Lords, where the government are likely to face fierce resistance.

Over in fixed income, gilts outperformed following the BoE yesterday, with 10yr yields down -2.6bps. Other sovereign bond yields also moved lower, with yields on 10yr Treasuries (-0.8bps) and bunds (-0.7bps) falling back as well. Separately, oil prices continued to make solid gains, with Brent crude up a further +2.56% yesterday, which brings its advance over the last 3 sessions to +9.21% – the best 3-day performance since May. Crude was helped by comments from both Saudi Arabian and Russian officials critiquing noncompliance of some OPEC+ members to agreed upon quotas.

To the day ahead now, and the data highlights include UK retail sales for August, German PPI for August, and the Euro Area current account balance for July. From the US, we’ll get the preliminary September reading of the University of Michigan’s consumer sentiment index, the August leading index, as well as the Q2 current account balance. In terms of central bank speakers, we’ll hear from the ECB’s de Guindos, Schnabel and Hernandez de Cos, along with the Fed’s Bullard and Bostic. Finally, the Central Bank of Russia will make their latest monetary policy decision.

via ZeroHedge News https://ift.tt/33Gq8XG Tyler Durden

“They Could Have Contained It” – Outgoing US Ambassador Accuses China Of Trying To ‘Cover Up’ Wuhan COVID-19 Outbreak Tyler Durden

Fri, 09/18/2020 – 07:17

Former Iowa Governor and outgoing US ambassador to China Terry Branstad had some harsh words for his one-time friend, Chinese President Xi Jinping. During an interview with CNN, Brandstad accused Xi and China of mishandling the coronavirus outbreak in Wuhan which sparked a global pandemic: “What could have been contained in Wuhan ended up becoming a worldwide pandemic,”Branstad said.

This is one of the harshest rebukes Branstad has ever delivered against China and President Xi, whom Branstad has known since the mid-1980s, when both men were relatively low-ranking government officials. This isn’t the first time Branstad has had to push back against Beijing; in the last few months alone, Branstad has denounced Beijing’s decision to expel American journalists, as well as the forced passage of the Hong Kong ‘national security’ law, and the closure of an American consulate in Chengdu (retaliation for the closure of a Chinese consulate in Texas that was reportedly a “nest of spies”).

This accusation is extremely harsh, and echoes President Trump’s aggressive rhetoric about holding China responsible for the pandemic. President Xi, meanwhile, has pledged to deliver aid – in the form of vaccines, and financial assistance – to poorer countries struggling with the virus.

Speaking to CNN in Beijing on Friday, Terry Branstad, a former longtime Iowa governor, agreed with President Donald Trump that China was to blame for the pandemic, adding that the “Chinese system was such that they covered it up and even penalized the doctors who pointed it out at the beginning.”

Echoing criticisms of the Chinese Communist Party made by US Secretary of State Mike Pompeo and other White House officials, Branstad also blamed China’s system for leading to a spike in tensions and a degrading of one of Washington’s most consequential bilateral relationships.

His departure comes just days after Beijing threatened to impose unspecified restrictions against senior American diplomats after President Trump signed an EO targeting CCP officials and Chinese businessmen allegedly involved with human rights abuses in Xinjiang.

Asked by CNN if he would campaign for Trump, Branstad said he would, if asked.

He told CNN that he was keen to get back home, pointing out that he had been in the role “longer than the previous three ambassadors.”

Asked whether he will campaign on behalf of Trump, who may be relying on Branstad to help swing key Midwestern states, the ambassador said that “if the President asks me to appear at some of his events, I will, as I did in 2016.”

Branstad was one of the first ambassadors appointed by Trump. His decades-old relationship with Xi was cited as a critical to the appointment, reflecting President Trump’s push to build a “personal” relationship with the Chinese president.

However, the administration’s unprecedented and aggressive approach has driven the bilateral relationship between the world’s two largest economies into a new ‘Cold War’. Branstad is set to leave the office by the end of next month, leaving the US without a top diplomat in China during the 2020 presidential vote.

via ZeroHedge News https://ift.tt/3knheF4 Tyler Durden

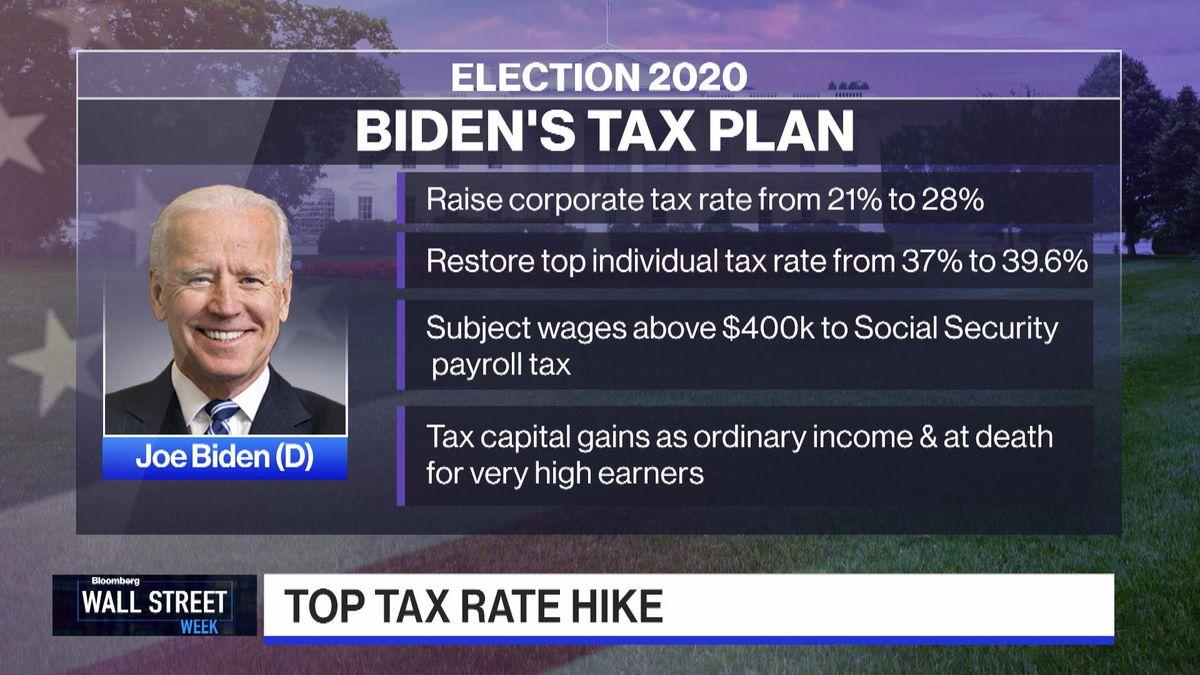

Wall Street Bankers Push For Bonuses Ahead of Possible Biden Win Tyler Durden

Fri, 09/18/2020 – 06:30

Big Wall Street firms may pay out bonuses to employees earlier this year as executives are preparing for a potential scenario where Joe Biden becomes president and a Democrat-controlled Senate would result in higher taxes.

“Employees may ask to receive year-end incentives before the end of 2020 instead of early next year, when they would typically get the bonuses,” said Alan Johnson, president of Johnson Associates Inc., a New York-based compensation consulting firm, who was quoted by Bloomberg.

“You’re going to hear about, ‘This firm did this, and that firm did that,'” Johnson told firms at a virtual industry conference Monday. “You don’t want to be caught unaware.”

A major concern for Wall Street if President Trump doesn’t win is the possibility of higher corporate taxes by a Biden administration. Biden has pledged to roll back Trump’s tax cut legislation, which boosted corporate profits in the last couple of years. If passed, the amount of bonuses Wall Street receives on a per annum basis could be significantly reduced from the roughly $30 billion set aside each year. Biden’s plan also calls for increased taxes for annual incomes over the $400,000, along with higher capital gains taxes.

Johnson has advised firms to prepare for tax increases no matter who wins the election, given the federal government’s desperate need for revenue following the virus pandemic. He said states like New York, New Jersey, Connecticut, and California have already signaled tax increases in the year ahead.

“Firms in the past have accelerated bonus payments in response to changes in tax policy. President Donald Trump’s tax plan, passed at the end of 2017, limited the amount of federal tax deductions high earners could claim for their state and local taxes, prompting some firms to hand out bonuses before the end of the year,” said Fred Farkouh, a partner at New York-based accounting firm Farkouh Furman & Faccio LLP.

Farkouh added, “moving up incentive payments wouldn’t affect finances for many companies, as they would have already planned to record year-end bonuses in their accounting for 2020, even if they were expecting to distribute them in 2021.”

Wall Street appears to be preparing for a possible Biden presidency. If so, does that also mean increased corporate taxes could result in a stock market crash?

RECORD HIGH NASDAQ! It would all come crashing down, including your Jobs, Stocks, and 401k’s, if Sleepy Joe ever became President. China and others would own us!!!

ByteDance Reportedly Has Beijing’s ‘Blessing’ For TikTok-Oracle Deal Tyler Durden

Fri, 09/18/2020 – 06:20

As ByteDance, Oracle and the group of investors scrambled to assuage GOP China Hawks demands to ensure that the CCP will have no access to the personal data of TikTok’s 100 million American users earlier this week, we couldn’t help but wonder whether all these behind-the-curtain negotiations might be in vain.

Not only has Beijing expressed its opposition to a “smash & grab” deal via Chinese state-controlled media, but CCP officials imposed new restrictions on deals involving sensitive AI technology, including the content-recommendation algorithm that lies at the heart of TikTok, and which is said to be its most critical piece of technology, according to Bloomberg.

Finally, Bloomberg has offered us some insight into this question. According to a report published late Thursday night in the US (Friday morning in China), ByteDance has become “more confident” that the deal it has “envisioned” with Oracle (and Wal-Mart, and a smattering of other, mostly American, investors) will receive Beijing’s stamp of approval.

TikTok-owner ByteDance Ltd. is getting more confident its envisioned alliance with Oracle Corp. will pass muster with China’s regulators, a critical step in the political clash over the popular video app, people familiar with the matter said.

While Beijing has asserted its right to block the sale of critical technologies, it is likely to greenlight a deal as long as it doesn’t involve the transfer of the artificial intelligence algorithms that drive TikTok’s service, they said, asking not to be identified discussing a private deal. That’s true even if ByteDance were to cede majority control over TikTok, they said.

ByteDance struck a deal with Oracle and later made revisions put forward by the Treasury Department aimed at addressing U.S. national security concerns, Bloomberg reported Thursday. The proposal calls for ByteDance to own most of a ringfenced TikTok, with Oracle, Walmart Inc. and venture capital investors holding a minority of a new company that will pursue an initial public offering in about a year. But President Donald Trump has the final word and has said he doesn’t want the Chinese parent to retain majority control.

The Trump Administration made clear that it wasn’t comfortable with ByteDance retaining majority control over the new US-based company (which, according to press reports, would be headed for a blockbuster IPO some time next year). By the looks of it, this could be the only route to a compromise. ByteDance might give up majority control of TikTok, but it will be handsomely compensated by American investors. Meanwhile, the spinoff of TikTok’s global business will confer unprecedented clout, while simultaneously filling the ByteDance’s coffers.

The report also included some new details about the Oracle-TikTok plan. Apparently, the two companies have agreed to oversight controls including an all-American board of directors that must be approved by the US government, as well as Oracle monitoring and approving

The plan revised with Treasury calls for the new TikTok to be headquartered in the U.S. with an independent board, approved by the U.S. government and made up entirely of U.S. citizens. The board would include a national security committee – led by an American data-security expert who would be the primary contact with the Committee on Foreign Investment in the U.S. – which would oversee any issues of concern to Washington.

The new terms include 20 pages of detailed provisions over data and national security, the people said. Under the existing proposal, Oracle has power to review the software or source code underlying the TikTok service, but ByteDance maintains ownership.

That technological division could remain even if American investors end up with control of TikTok’s equity. Oracle and ByteDance have accepted Treasury’s conditions, people familiar with the talks have said.

Also, there might be a role in the new organization for former Instagram head Kevin Systrom.

ByteDance executives have also spoken to Instagram co-founder Kevin Systrom about a possible role in the new organization, according to another person familiar with the discussions. It’s not clear if the discussions are advanced, the person said.

If this report is accurate, ByteDance founder Zhang Yiminghas must simply retain control of TikTok’s core algorithm, and Beijing will sign off. That sounds almost…too good to be true, which begs the question: does this represent a kind of capitulation from Beijing?

via ZeroHedge News https://ift.tt/2RF6o0M Tyler Durden

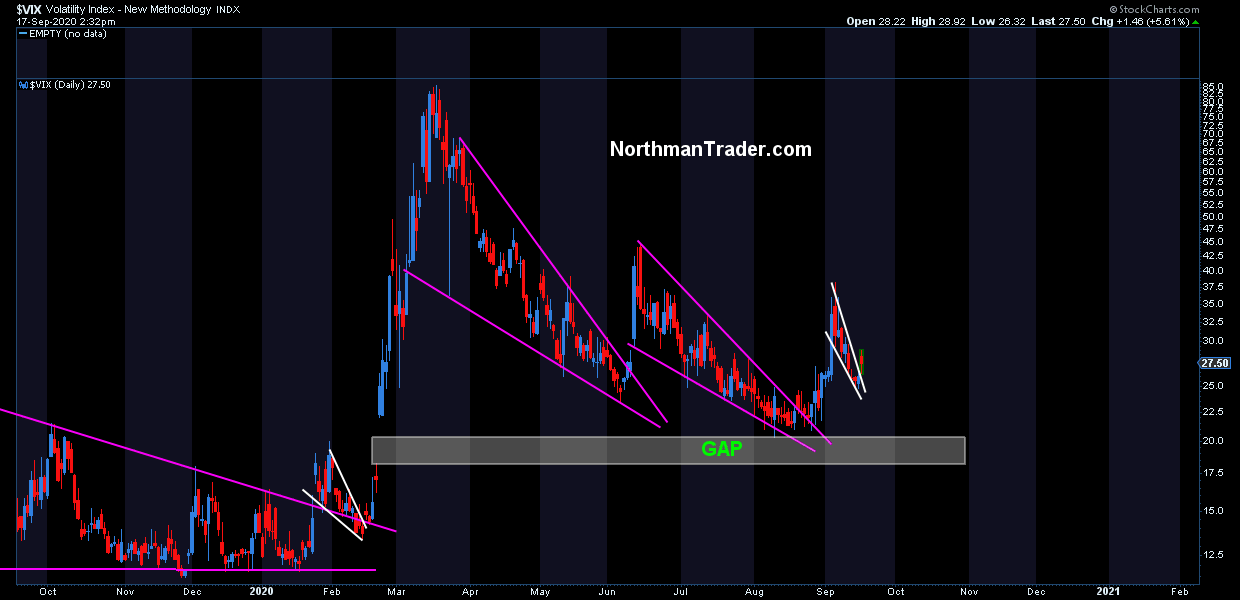

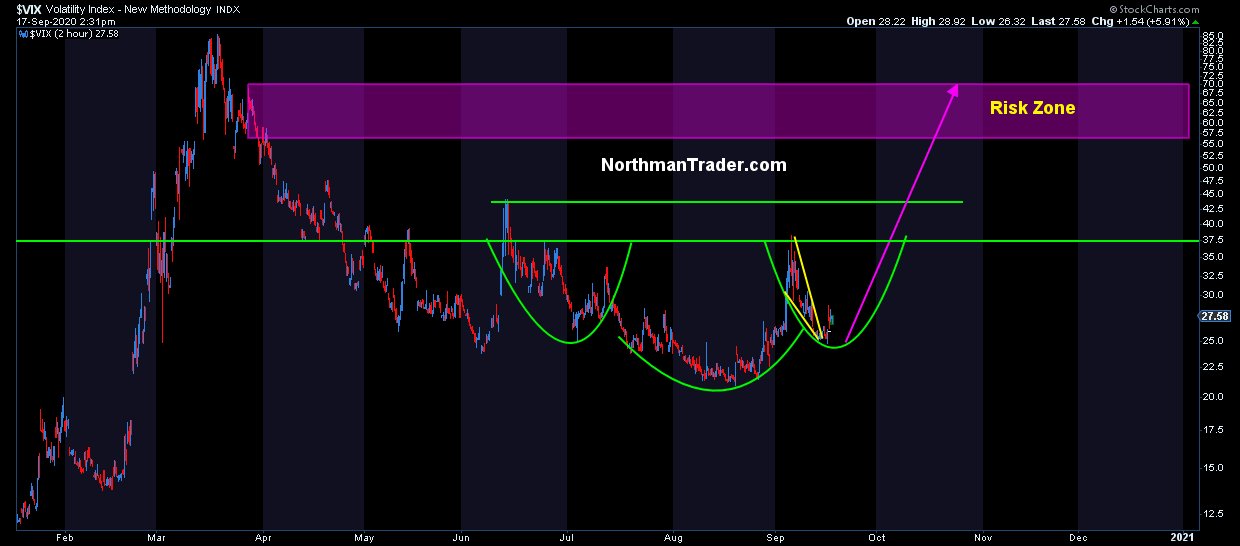

As long time readers know I’m a big fan of $VIX technical structures and compression patterns. Often dismissed as non-chartable I think we’ve successfully to put that argument to bed a long time ago.

Recently in “Key Charts” I again outlined the $VIX as one of the key charts to watch and it’s been interesting to say the least here during this OPEX week and hence I wanted to outline an update as a pattern is forming that suggests a major $VIX uprising may be in the cards this fall.

Yes, $VIX again came under pressure into monthly $VIX futures monthly contract roll-over, but interestingly it didn’t manage to fill the August gap which would have been standard fare if you will:

The good news for bulls may be as now 3 open gaps have formed on the futures contract. As ultimately all $VIX gaps fill there is something to look forward to eventually for bulls. But for now the $VIX keeps telling a larger story that’s a lot more ominous.

In a way I regard the $VIX an expression of central bank control and their self declared mission to “calm” markets. During the most successful times of central bank interventions in recent years the $VIX was very much compressed and contained. Yet, despite trillions of interventions and the deceiving highs on indices such as $SPX and $NDX volatility has remained stubbornly high, all a reflection that perhaps central bank control is not as strong as it appears. The $VIX is anything but calm.

And so we can observe that following the latest breakout of the $VIX (and leading up to the compression phase of this OPEX week) $VIX again broke out of a smaller compression pattern:

In recent months $VIX has gotten crushed during every Friday like clockwork and perhaps it will again this Friday.

That’s not the issue.

The issue is that all of these repetitive structures are forming what could be a much more ominous pattern that could even exceed my previous 46 target.

The structure? A potential larger inverse pattern:

First point to make: This pattern at this stage is unconfirmed and it’s likely going to take some time to build fully. But this week’s low in the $VIX matches up nicely with the July left shoulder and this summer’s low volume rally and summer lows in the $VIX have formed a very clean head structure and the recent surge to 38 and subsequent drop this week have begun the process of forming a right shoulder.

How can this play out? What would confirm it? There are many possibilities of course. Since we’re just at the beginning of the right shoulder formation we may, for example, have a quick spike toward the neckline, and then another rally in markets from there compressing the $VIX again. All of this would ironically firm the structure and make it potentially very potent into the October and November time frame, i.e. into the US election.

The potential fire power of the pattern will have to be monitored as the pattern develops, but currently it suggests a $VIX spike into the 55-70 range if the pattern confirms which would come with a break above the neckline.

This is journey and patterns need time to develop and patterns can of course get invalidated. I suggest everyone keep an eye on a potential $VIX uprising of size. We certainly are keeping close watch for sure.

* * *

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

via ZeroHedge News https://ift.tt/3cavrSR Tyler Durden

The Ultra Wealthy Are Selling Billions Of Dollars In Stock Tyler Durden

Fri, 09/18/2020 – 05:30

As the market has “rebounded” off its lows back in March, the world’s super wealthy are jumping at the chance to offload billions of dollars in stock while global central banks – and most notably the Federal Reserve – keeps a bid under the market and acts as a Mr. Magoo-like counterparty.

Many investors have been prompted to sell by market volatility over the last two weeks, which appears as though it could be signaling an end to the V-shaped recovery. This has likely helped spook the ultra wealthy into take some cash off the table.

Seo Sang-young, an analyst at Kiwoom Securities Co. in Seoul noted: “Stock-market valuations have climbed considerably regardless of fundamentals. Volatility has been increasing.”

Knorr-Bremse AG’s Heinz Hermann Thiele took the bump up in the market as an opportunity to sell about $1.2 billion in stock, while Adyen NV co-founders Pieter van der Does and Arnout Schuijff joined a group of executives that sold $821 million of stock in the payment company, according to Bloomberg. Fortive Corp.’s Mitchell and Steven Rales also sold about $1 billion.

Glovemaker Kossan Rubber Industries Bhd. founder Lim Kuang Sia also sold more than $30 million in stock in August. Lee Wai Keong of glovemaker Riverstone Holdings raised $45 million in a share placement earlier in September. Leslie Wexner of L Brands sold $89 million of his stock in August, as well.

Bloomberg notes that during the week ended September 11, insiders sold $473 million in shares while only buying $9.5 million.

Many of the world’s super rich have their wealth disproportionately tied up in company stock. For example, Jeff Bezos’ Amazon shares are worth $172 billion of his $186 billion net worth. For Mark Zuckerberg, Facebook stock makes up almost all of his $103 billion net worth.

Claire Madden, managing partner of Connection Capital concluded: “It’s the first time most people have lived through something as real, sharp and sudden as this. It does make you reevaluate.”

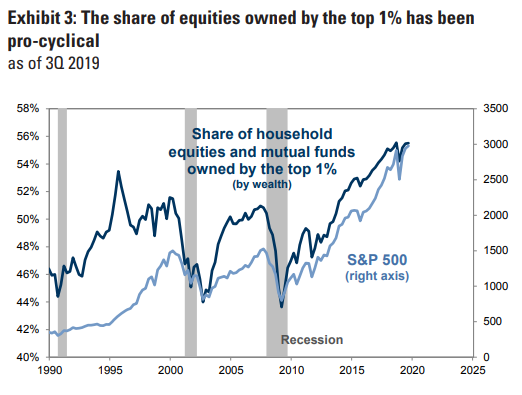

Recall, back in February of this year we wrote a piece showing exactly how the 1% was dumping their stock to daytrading Robinhood millennials with dreams of getting rich. We noted that February was the start of the the point in the bull market where the “smart money” dumps their equities to the unsuspecting and excitable, yet horribly uninformed, retail crowd.

The first chart shows the top 1% dumping as the market falls entering recession. Of late, we can see that selling has happened in spurts by the top 1%:

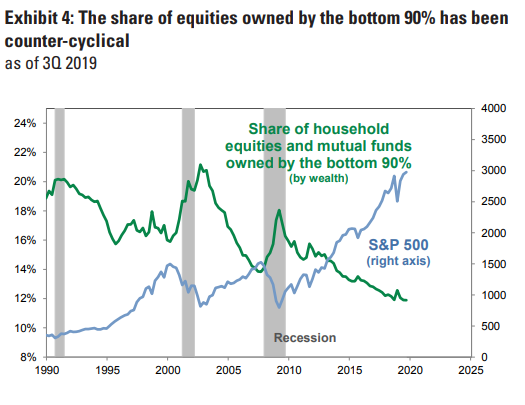

For the bottom 90% it’s just the opposite: the vast majority of unsophisticated retail investor start to chase momentum at the worst possible time, as they buy stocks en masse just as a recession begins, which in turn craters the market. In the Goldman chart below, we can see that the share of equities owned by the 90% jumps just as recession begin.

In laymens terms, the rich dump their stock to the poor just before the market crashes.

The technical term is “distribution.”

via ZeroHedge News https://ift.tt/3iIFgtT Tyler Durden