New Zealand Revives Lockdown 2 Months After ‘Declaring Victory’ Over Coronavirus: Live Updates Tyler Durden

Tue, 08/11/2020 – 08:49

Summary:

Goldman weighs in on US outbreak

Auckland back on lockdown as first cluster of covid cases discovered in 102 days

Russia approves world’s first COVID vaccine

Global COVID total tops 20 million

* * *

Update (0920ET): Here’s an excerpt from Goldman’s latest daily COVID research, which again affirmed that case numbers in the US continue to decline: “The number of new confirmed coronavirus cases has been declining nationally over the past few weeks, but case levels remain elevated in much of the country. The positive test rate has ticked down from its peak in July.”

“But looking at additional testing data clouds the picture somewhat. The US is now performing fewer coronavirus tests nationwide compared to a couple weeks ago, with Florida and Texas contributing much of this decline. In these states and a few others, cases rose to very high levels in the summer virus resurgence and have now fallen sharply. But over the past few weeks as cases declined so did the number of tests conducted, leaving the positive test rate very elevated.”

* * *

They really thought they had it licked.

After surmounting what was at worst an extremely mild outbreak, New Zealand declared “victory” over the coronavirus two months ago, only to see a mild spike two weeks later.

Since the very beginning, New Zealand’s COVID-19 response effort, led by progressive prime minister Jacinda Ardern, was infused with the pinch of “compassionate” social justice, as the island nation focused on using it as an opportunity to look into how to recalibrate society to make more time for leisure by adopting a 4-day work-week.

But in its desperation to establish New Zealand as a liberal (and polar) antithesis to President Trump’s America, Ardern made what now looks to be one critical error: She lifted practically all of the country’s COVID travel restrictions after her sweeping “victory” declaration.

That, and slowly allowing businesses to reopen, has apparently helped give the virus all it needs for another flareup which, however comparatively minor to what’s going on just next door in Victoria, Australia, has forced Ardern to order a new lockdown, just as doubts about the efficacy of such lockdowns are growing.

New Zealand announced on Tuesday it would shut down Auckland, its largest city (though not the capital), after four new cases of the virus were confirmed in the city, the first sign of new domestic spread after 102 days without any domestic COVID cases.

NZ’s Director General of Health Ashley Bloomfield said the four confirmed cases were all within one family living in South Auckland. One patient is in their 50s. The family had no history of international travel. Family members have been tested and contact tracing – which might actually prove pretty effective with such a small body of the infected – is being carried out.

News of the cases sent panic across the country with media reporting people rushing to supermarkets to stack up, and businesses preparing to shut.

Prime Minister Jacinda Ardern said Auckland would return to a “level 3 restriction” beginning at noon local time on Wednesday as a “precautionary approach,” which would mean people should stay away from work and school, and gatherings or more than 10 people would again be restricted. Though, with so few cases, even these economically-constricting decisions might be overkill.

Though fortunately, these restriction would be applied for three days until Friday, which she said would be enough time to assess the situation, gather information and make sure there’s enough widespread contact tracing.

Meanwhile, the world finally crossed a major COVID-19 threshold last night: 20 million confirmed cases, according to JHU. As we reported last night.

As expected, Johns Hopkins has just confirmed that the number of confirmed COVID-19 cases worldwide has surpassed 20 million since the start of the pandemic. Of those, more than 700,000 have died.

It comes just days after the US, the world’s biggest outbreak, topped 5 million, and Brazil, the No. 2, topped 3 million.

Aside from this, perhaps the biggest COVID-related news of the day is coming out of Russia, where Vladimir Putin just hailed the approval of the country’s – and the world’s – first COVID-19 vaccine to be approved by a regulator.

via ZeroHedge News https://ift.tt/2CinKN9 Tyler Durden

Day-Traders Send US Producer Prices Soaring In July Tyler Durden

Tue, 08/11/2020 – 08:40

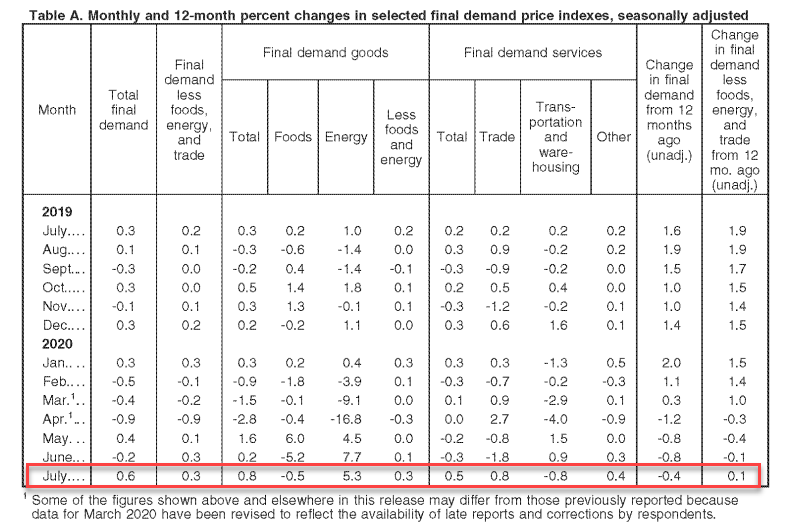

US Producer prices were expected to rise MoM following four declines in the last five months and they did, rising 0.6% MoM (double the expected 0.3% MoM rise). However, this was not enough to unwind the annual deflationary print (PPI -0.4% YoY)

Source: Bloomberg

This is the biggest MoM jump in headline PPI since Oct 2018.

Ex-food-and-energy, the beat was even more impressive with a 0.5% MoM spike vs 0.1% expected which lifted YoY Core PPI off its multi-year lows…

Source: Bloomberg

The biggest driver of this rebound was energy goods as food prices continue to slide.

However, even more stunning was a 7.8% surge in the index for portfolio management was a major factor in the

advance in prices for final demand services.

The indexes for machinery and vehicle wholesaling, automobiles and automobile parts retailing, long-distance motor carrying, legal services, and machinery and equipment parts and supplies wholesaling also moved higher. Conversely, prices for airline passenger

services decreased 7.0 percent. The indexes for automotive fuels and lubricants retailing and for guestroom rental also declined.

Over one-third of the July advance in the index for final demand goods is attributable to gasoline prices, which rose 10.1 percent. The indexes for diesel fuel, home heating oil, electric power, fluid milk products, and industrial chemicals also increased. Conversely, meat prices fell 8.0 percent. The indexes for residential natural gas and carbon steel scrap also decreased.

via ZeroHedge News https://ift.tt/2Ch2Cqq Tyler Durden

S&P Futures Hit All Time Highs On Stimulus, Vaccine Hopes; Gold, Silver Tumble Tyler Durden

Tue, 08/11/2020 – 08:27

S&P 500 futures hit a record high as investors shrugged off continuing U.S.-China tensions and instead focused on news of an approved, if largely unclear, Russian vaccine, and more stimulus optimism as President Donald Trump said he’s considering a tax cut on capital gains. According to Reuters calculations at the current levels, the benchmark index is set to open about 12 points below its Feb. 19 record peak of 3,393.52.

American Airlines and Carnival led a boom in travel shares in the premarket. The S&P 500 closed less than 1% below its record high on Monday as investors extended a rotation into value stocks from heavyweight tech-related names. At 8:00 a.m. ET, S&P 500 e-minis were up 23.25 points, or 0.69%, topping an all-time high of 3,372.25 points last hit on Feb. 20.

A rally in the tech megacaps including Amazon.com, Netflix and Apple that thrived during the shutdowns helped the Nasdaq reclaim its all-time high in June, while the Dow still remains about 6% below its peak.

In Europe and Asia, a broad rally from industrial goods to health-care shares set the Stoxx Europe 600 Index headed for its best increase since mid-June. The Stoxx 600 Europe index rose more than 2% , with auto shares leading the way after a surge in Chinese car sales. Gains for Asian equities ignited a rally in European stocks that lifted Stoxx 50 as much as 2.8% and weighed on bunds, pulling Treasuries along.

Earlier in the session, Asian shares ex-Japan gained nearly 1%, with Japan’s Nikkei rising 1.9% after a Monday holiday. There were hopes Beijing’s sanctions on 11 U.S. citizens may end this round of tit-for-tat moves between the two powers.

“It has left the White House untouched,” said Vishnu Varathan, head of economics at Mizuho Bank in Singapore. “That gives some relief that China is still giving some priority to the (trade deal) dialogue,” he said.

Market participants remain eager to see an agreement on the fifth federal aid bill to help Americans battle with the health crisis was far from over with U.S. cases surpassing 5 million last week. The mood remains cautious as sparring continues in the U.S. Congress over extending fiscal stimulus while economic data such as a steep drop in South Korean exports and a rise in UK jobless rates remain a cause for concern. But upbeat comments by U.S. Treasury Secretary Steven Mnuchin on the prospects for a bipartisan stimulus deal supported Brent crude futures at near five-month highs and kept the dollar index near a one-week peak.

Commerzbank analysts said markets were shrugging off doubts over the legality of Trump’s order and appeared convinced Congress would agree a deal

“Not without good reason, because in the election campaign both parties have an interest in presenting themselves well,” they said. “Who wants to be seen as the stingy bad guy even in times of great need?”

General optimism kept safe haven assets under gentle pressure, with gold falling back under $2000 an ounce, down more than 2%, even as the dollar slumped. Precious metals dropped with spot gold south of $2000 and spot silver just about holding onto a USD 28/oz handle having briefly dipped below the figure. No fundamental news flow coincided with the losses across precious metals but action could merely be a function of tech play alongside some profit taking/stops being triggered. But the most likely reason for the back down in gold prices is that 10Y real rates – which gold has been tracking tick for tick – also dipped from recent record lows.

In FX, the dollar slipped as European stocks follow Asian equities higher, with markets taking encouragement from falling hospitalization rates in California and New York and decreasing new infections in Hong Kong. The euro rose as much as 0.5% after ZEW data revealed investors raised their expectations of a rebound for the German economy in August. Italy’s 10-year yield premium over its German equivalent tightened to its lowest level since February.

In rates, ten-year U.S. Treasury yields were near a two-week high of 0.5870% while German yields likewise rose to two-week highs. Treasury yields were cheaper by 1bp to 2.5bp across the curve led by long end, steepening 2s10s, 5s30s by 1.6bp and 1bp; 10-year yields around 0.60% while bunds, gilts both lag by ~1bp. Ahead of 3-year auction, WI yield is ~0.160%, 3bp richer than July’s record low stop at 0.19%; refunding includes $38b 10-year Wednesday and $26b 30-year Thursday; all sizes are records.

In commodities, WTI and Brent continue to grind higher in early trade, with upside more-so a function of the overall risk tone as opposed to fresh fundamental catalysts, albeit prices remain underpinned by the recent upbeat assessment from Saudi, Iraq and Gulf members alongside the constructive outlook by Saudi Aramco post-earnings. Looking ahead, traders will be eyeing the weekly API inventory release, with expectations for crude stockpiles to decline by almost 4mln barrels, but ahead of the weekly release, participants will pay attention to the EIA Short Term energy Outlook which will include US crude production forecasts for the rest of 2020 and 2021. In terms of base metals, Dalian iron ore futures snapped its two-day losing streak as prices were bolstered by falling portside inventories, whilst LME copper prices saw early downside.

Looking at the day ahead, and data releases out include UK unemployment data for June, the German ZEW survey for August, as well as July’s PPI reading and the NFIB small business optimism index from the US. Otherwise, Fed speakers today include Barkin, Daly and Brainard.

Market Snapshot

S&P 500 futures up 0.6% to 3,371.75

STOXX Europe 600 up 1.8% to 371.07

MXAP up 1.1% to 169.75

MXAPJ up 0.6% to 562.38

Nikkei up 1.9% to 22,750.24

Topix up 2.5% to 1,585.96

Hang Seng Index up 2.1% to 24,890.68

Shanghai Composite down 1.2% to 3,340.29

Sensex up 0.9% to 38,507.25

Australia S&P/ASX 200 up 0.5% to 6,138.65

Kospi up 1.4% to 2,418.67

German 10Y yield rose 1.3 bps to -0.513%

Euro up 0.3% to $1.1768

Brent Futures up 0.8% to $45.33/bbl

Italian 10Y yield fell 0.8 bps to 0.795%

Spanish 10Y yield fell 0.2 bps to 0.253%

Brent Futures up 0.8% to $45.33/bbl

Gold spot down 2.1% to $1,985.04

U.S. Dollar Index down 0.2% to 93.44

Top Overnight News from Bloomberg

Britain’s mounting labor market crisis was underscored by a 220,000 slump in employment during the height of the coronavirus lockdown, the worst decline since the global financial crisis

Even as China continues to hit back at the Trump administration, leaders in Beijing are also signaling they want to ease tensions with the U.S. as the clock ticks down to the presidential election

Lebanon’s political leaders are expected to launch parliamentary consultations to choose a new prime minister after Hassan Diab’s government resigned on Monday over the devastating explosion at Beirut’s port

Hong Kong’s worst coronavirus outbreak is showing signs of coming under control as the city reported the lowest number of new local infections since its resurgence began over a month ago

A quick look at global markets courtesy of NewsSquawk:

Asian equity markets traded higher as risk appetite in the region improved on the tepid performance seen on Wall St where most major indices finished in the green but tech underperformed and indecision lingered amid the ongoing stimulus talks stalemate, mixed views on President Trump’s recent executive orders and ongoing US-China tensions. ASX 200 (+0.5%) was positive as top-weighted financials spearheaded the advances and with the broad sector gains offsetting the weakness in gold miners and tech, while Nikkei 225 (+1.8%) was buoyed on return from an extended weekend helped by a predominantly weaker currency and after bank lending increased by its fastest pace on record. Hang Seng (+2.1%) and Shanghai Comp. (-1.2%) conformed to the upbeat mood after the PBoC upped its liquidity efforts with a CNY 50bln reverse repo injection and although China announced sanctions against officials in retaliation to US sanctions on Hong Kong, they refrained from imposing them on Trump administration officials. Furthermore, casino stocks are red-hot after reports China is to remove the quarantine requirement for Macau effective tomorrow and Next Digital shares surged over 400% in an extension of yesterday’s sharp intraday turnaround as activists piled into the shares in a show of support following the founder’s recent arrest and amid speculation it could sell its listed entity as a shell for other firms to acquire for a back-door listing. Finally, 10yr JGBs were lower and approached 152.00 to the downside as they played catch up to the recent weakness in T-notes and as havens were shunned amid gains in riskier assets, while the lack of BoJ presence in the market also added to the dampened mood for JGBs.

Top Asian News

One of World’s Strongest Rallies Propels Kospi to Two-Year High

Tough-to-Impress Harvard Grad Molds Fortunes of China’s Rich

Singapore’s Economy Posts Worse Contraction in Second Quarter

Iron Ore Futures Gain as China’s Economic Recovery Fuels Demand

European equities trade higher across the board [Euro Stoxx 50 +2.7%], with upside accelerating after the cash open as sentiment improved following an initially bleak APAC handover – prompting DAX cash and Sept futures to gain above 13k, albeit fresh fundamental catalysts remain light throughout the session thus far; some modest impetus coincided with vaccine updates from Russia. Firm gains are also seen across all European sectors, with cyclicals/value clearly outpacing defensives, whilst the breakdown paints a similarly performance, with Travel & Leisure topping the chart, closely followed by Oil & Gas, Autos and Banks, whilst the other side of the spectrum sees Healthcare and Chemicals as the laggards. In terms of individual movers, UK listed Cineworld (+17%) extended on earlier gains and resides at the top of the Stoxx 600 amid reports that the group could go private. BP (+3.7%) coattails on the back of firmer energy prices coupled with source reports the group is said to be mulling the sale of its German chemicals’ unit DHC Solvent Chemie. Mediobanca (+5.9%) extends on opening gains after the ECB gave the green-light for shareholder Del Vecchio to increase his stake in the Co. to 13-14% from 10%.

Top European News

Hungary Inflation Surges, Putting Rate Policy Back in Focus

U.K. Jobs Crisis Worsens as Employment Drops Most Since 2009

Vestas Shares Surge as 2020 Revenue Guidance Reintroduced

Unilever Warns of Dutch Tax Proposal’s Risk for Plan to Move

In FX, another back up in US Treasury yields and mild steepening along the curve into record refunding has underpinned the Dollar to a degree, but a deeper retracement in spot bullion to test support around the psychological Usd 2000/oz level coincided with the DXY marginally eclipsing Monday’s high at 93.729. However, the Greenback has lost momentum against the backdrop of extended gains in global equities that is keeping high beta/cyclical currencies supported and safe-haven demand suppressed.

AUD/NZD/CAD/NOK – As noted above, the Aussie is benefiting from bullish risk sentiment to the extent that declines in NAB business sentiment and conditions have not weighed on Aud/Usd unduly, while the Kiwi is just keeping tabs with 0.6600 ahead of Wednesday’s RBNZ policy meeting even though the bias may be skewed towards a more dovish event compared to the prior assessment and guidance, while NZ reports a local outbreak of COVID-19 cases after a 100+ day run of no infections at all. Elsewhere, elevated crude prices are helping the Loonie and Norwegian Crown remain afloat around 1.3300 and 10.5800 vs the Buck and Euro respectively, with the former now looking for some independent impetus via Canadian housing starts.

EUR/CHF/GBP – All benefiting from the aforementioned Dollar fade, with the index now back under 93.500 again and Euro rebounding between 1.1723-83 parameters following a somewhat mixed ZEW survey, the Franc paring losses within a 0.9168-34 range and Pound maintaining 1.3050+ status, but not quite able to retest yesterday’s best a few pips over 1.3100 in wake of mostly weaker than forecast UK labour and pay data.

JPY – The Yen is marginally underperforming either side of 106.00 on a loss of safety premium and with Japanese markets back from their long holiday weekend, but little lasting reaction to a wider than anticipated Japanese current account surplus.

EM – Oil’s ongoing resurgence is helping the Rouble and Mexican Peso supplement gains vs the flagging Greenback. but the SA Rand has not been deterred by Gold’s meltdown or looming data and has breached key technical resistance in the form of the 100 DMA (17.6240) on the way up towards 17.5400. Similarly, the Turkish Lira is back in recovery mode as tighter CBRT funding conditions prompt some short covering, while Brazil’s Real awaits BCB COPOM minutes from the last meeting.

In commodities, WTI and Brent front-month futures continue to grind higher in early trade, with upside more-so a function of the overall risk tone as opposed to fresh fundamental catalysts, albeit prices remain underpinned by the recent upbeat assessment from Saudi, Iraq and Gulf members alongside the constructive outlook by Saudi Aramco post-earnings. The benchmarks experienced modest downside heading into the European cash open, in which prices briefly dipped below 45/bbl for the Brent Oct contract, whilst WTI Sep tested 42/bbl, before recovering lost ground and some more. Looking ahead, traders will be eyeing the weekly Private Inventory release, with expectations for crude stockpiles to decline by almost 4mln barrels, but ahead of the weekly release, participants will pay attention to the EIA Short Term energy Outlook which will include US crude production forecasts for the rest of 2020 and 2021. Elsewhere, precious metals are under pressure this morning with spot gold south of USD 2000/oz and spot silver just about holding onto a USD 28/oz handle having briefly dipped below the figure. No fundamental news flow coincided with the losses across precious metals but action could merely be a function of tech play alongside some profit taking/stops being triggered. In terms of base metals, Dalian iron ore futures snapped its two-day losing streak as prices were bolstered by falling portside inventories, whilst LME copper prices saw early downside amid the firming USD at the time; albeit, has since nursed losses.

US Event Calendar

6am: NFIB Small Business Optimism 98.8, est. 100.5, prior 100.6

8:30am: PPI Final Demand MoM, est. 0.3%, prior -0.2%; PPI Ex Food and Energy MoM, est. 0.1%, prior -0.3%

8:30am: PPI Final Demand YoY, est. -0.7%, prior -0.8%; PPI Ex Food and Energy YoY, est. 0.0%, prior 0.1%

DB’s Jim Reid concludes the overnight wrap

The last 24 hours has pretty much fit the bill as far as slow news days are concerned in markets. That being said there was a somewhat notable milestone reached yesterday as the S&P 500 surpassed the all-time highs from February on a total return basis. This is a fairly astonishing feat when you consider that in late-March the index was down as much as -33.79% from those highs. In price terms it finished +0.27% yesterday which means it’s just -0.76% lower than its all-time closing high. That move also marked the S&P’s 7th consecutive advance for the first time since April 2019.

While the S&P nudged higher, the Dow Jones saw a much larger +1.30% gain, which is somewhat unusual given the strong correlation between the two indices. Indeed, it’s only the 6th time in the last decade that the Dow’s daily move has been more than one percentage point different to the S&P’s (even if 5 of them have been since the pandemic hit). At the other end of the spectrum though, the NASDAQ (-0.39%) slipped for a rare second consecutive session. At the margin the macro news acted as a bit of headwind and included the news of further Chinese sanctions on US officials after similar measures were announced by the US on Friday, with those sanctioned by China including the Republican senators Marco Rubio, Ted Cruz and Tom Cotton. Chinese Foreign Ministry spokesman Zhao Lijan said yesterday that “China has decided to impose sanctions on those individuals who behaved badly on Hong Kong-related issues”. And in a further sign that US-China tensions are showing no sign of abating any time soon, US Secretary of State Mike Pompeo tweeted yesterday that the arrest of Jimmy Lai under Hong Kong’s national security law was “further proof that the CCP has eviscerated Hong Kong’s freedoms and eroded the rights of its people.”

Meanwhile, markets continue to turn a bit of a blind eye to the lack of any progress on the next US fiscal package with no updates to report of yesterday. Nevertheless there was some more positive coronavirus news from the US, with the number of hospitalisations in New York State at the lowest since the start of the pandemic, and the number of cases in Florida at their lowest in over 6 weeks. California and Texas also reported a fall in hospitalizations. Overall, cases in the US grew by 44,647 in last 24 hours or +0.9% while at the same point last week cases had grown by 46,918 or 1.0%. Globally, the number of cases have crossed the 20 million mark. It is worth highlighting that it took 6 months for cases to reach 10 million after the first infection surfaced in China while the second 10 million took only 6 weeks. On the positive side, China has said that it will resume issuing tourist visas for visitors to Macau which has helped casino stocks rally in the region.

Indeed most Asian bourses have posted strong gains this morning. The Hang Seng (+2.40%) has led the way after underperforming on Monday, while the Nikkei (+1.81%) is up following Monday’s holiday. The Kospi (+1.60%) and ASX (+0.84%) all also up while futures on the S&P 500 are also up +0.26%. It’s been fairly quiet for overnight news, however President Trump did say that he’s “very seriously” considering a capital gains tax cut “which would create a lot more jobs”.

Back to yesterday, and over in Europe the moves were pretty similar to the US in terms of the upward direction for equities, though the STOXX 600 (+0.30%) still remains nearly 16% beneath its own record high in February, with European indices having underperformed their US counterparts since the pandemic hit. Energy stocks led the rally on both sides of the Atlantic thanks to a strong performance in oil prices, and both WTI (+1.75%) and Brent (+1.33%) saw solid gains. Staying with the commodities sphere, it’s worth noting that silver was up +2.93% at a 7-year high of $29.13/oz yesterday, though gold (-0.40%) continued to come down from Thursday’s record high with a 2nd successive decline. Looking at other markets, sovereign bonds advanced modestly in Europe, with yields on 10yr bunds (-1.7bps), OATs (-2.3bps) and BTPs (-0.8bps) all moving lower. Indeed yields on 10yr BTPs were down to 0.918%, their lowest level in nearly 6 months. US Treasuries gave up their gains however, with 10yr yields ending the session up +1.2bps at 0.577%. The MOVE index of implied Treasury volatility did nudge up yesterday however still remains just 2 points off the all-time lows from the end of July. Speaking of volatility, the VIX is now down to 22.13, the lowest since 21 February.

Elsewhere, in terms of data yesterday there weren’t a great deal of releases, though we did get the JOLTS job openings from the US, which rose to 5.889m in June (vs. 5.3m expected). That’s their second monthly increase since their low of 4.996m in April, but still over a million lower than their levels in January and February of just over 7m. On a less positive note however, the New York Fed’s Survey of Consumer Expectations showed that households’ expectations on their employment prospects and year-ahead financial situation worsened in July following two months of improvements.

To the day ahead now, and data releases out include UK unemployment data for June, the German ZEW survey for August, as well as July’s PPI reading and the NFIB small business optimism index from the US. Otherwise, Fed speakers today include Barkin, Daly and Brainard.

via ZeroHedge News https://ift.tt/2XOAeUd Tyler Durden

Last week was a big week for precious metals. Gold broke above $2,000 an ounce and kept climbing, pushing over $2,075 later in the week. Meanwhile, silver blew through $28 and $29 ounce on Thursday and knocked on the door of $30. But even with another week of solid gains, there still seems to be a lot of skepticism about precious metals. Peter talked about gold’s bull run on his podcast and said it’s the most unloved gold bull market he’s seen in his entire career.

On Friday, we did finally got a corrective sell-off. Gold was down about $40 at one point and silver fell back below $28 for a time.

But even with the selloff, gold still closed well above $2,000 and was up 3% on the week. Silver ended up closing above $28 and saw a 15.5% weekly gain. Gold has closed higher for nine consecutive weeks. But as Peter pointed out, there have been down days.

Nothing goes up every single day, and gold and silver are not going to be the exception to that rule. There are no bull markets that are up every day. You’re always going to have down days.”

Peter said it seems investors haven’t figured this out. Gold and silver stocks started selling off Thursday even before spot prices dropped and they continued selling Friday. GDX (an index of gold mining companies) was down slightly on the week. Peter said this tells you a lot about the nature of this bull market and the wall of worry that is has been scaling.

I’ve been talking about this phenomenon on this podcast the entire time – that gold stocks have not really confirmed the bull market even though the bull market is taking place anyway, we haven’t seen it in gold stocks.”

Initially, a lot of people were saying the same thing about silver because it was lagging behind gold’s rally.

A lot of the reasons people were kind of diminishing the significance of the gold bull market was they said, ‘Hey, it’s not being confirmed by silver. Gold is going up but silver is going nowhere, and you can’t have a bull market in gold unless you have a bull market in silver.’ Well, OK. Now we have a bull market in silver. We’ve had a significant breakout in the price of silver. But still, people don’t believe this bull market. I mean, this is probably the most unloved gold bull market I’ve ever seen in my career.”

Peter said the fundamentals are better than any he’s ever seen.

In a CNBC interview, US Global Investors CEO Frank Holmes said he can see $4,000 gold in the relatively near future with G-20 finance ministers and central banks “working together like a cartel and they’re all printing trillions of dollars.”

We’ve not seen this level where central banks are printing money at a zero interest rate. At zero interest rates, gold becomes a very, very attractive asset class,” Holmes said.

Peter said the technical charts look good for gold as well.

So, you’ve got a great chart. You’ve got great fundamentals. Yet still, people don’t believe this bull market. And the proof that they don’t believe the bull market is the gold stocks. They are not rallying the way you would expect. They are being dragged kicking and screaming to new highs by a relentless bull market that everybody assumes is over.”

Peter pointed out that there’s a difference between the buyers of gold and those who buy gold stocks. The buyers for gold and silver are real buyers — individual investors, and in the case of gold, central banks.

The buyers of physical metal are buying as an alternative to fiat money… They are voting with their feet. They are running away from their fiat currencies, and they are running towards a real monetary alternative in gold and silver.”

On the other hand, buyers of gold stocks tend to be stock buyers and speculators. Peter said he thinks the investment community doesn’t believe the gold rally is going to last. They don’t believe gold mining companies are really going to benefit from a temporary rise in gold. Peter mentioned that a lot of people seem to think the rally in gold is simply a function in COVID-19. In fact, the CNBC article highlighting Holmes’ comments cited a coronavirus vaccine as a development that could stop gold’s rally in its tracks. Peter said they don’t understand the fundamentals.

That’s obvious, because every time the price of gold goes up, they expect it to fall. And every time the price of gold falls, they think it’s going to keep falling because they feel that that’s some kind of vindication. Meanwhile, the price of gold keeps going up. … So, the price of gold continues to defy the so-called experts. It continues to quietly make new highs. And this bull market is just going to keep going until ultimately the gold stocks participate — just like silver. How long did it take before silver joined the gold party? It eventually did.

You have to focus on the fundamentals. A lot of investors aren’t doing that.

They’re not looking into the future and realizing the monetary fiscal policies that have already driven gold past $2,000 are going to continue and drive it past $3,000, $4,000, $5,000. So, all of this potential should be reflected in the share price of these stocks, but it’s not. And therein lies the opportunity.”

In this podcast, Peter also talks about President Trump’s ban on TikTok and his recent executive orders. Peter called the EOs bad economics and unconstitutional.

via ZeroHedge News https://ift.tt/2PV73KZ Tyler Durden

Russia declared the vaccine “ready for use” despite “international skepticism,” the Associated Press reported. Putin made the announcement during a “government meeting”, where he also revealed that one of his own daughters had participated in the experimental trials.

“I would like to repeat that it has passed all the necessary tests,” he said. “The most important thing is to ensure full safety of using the vaccine and its efficiency.”

The trials established that a single course of the Russian vaccine is enough to establish immunity to COVID-19, while side-effects were minimal, with slight fevers appearing in Putin’s daughter, and other subjecst.

“As far as I know, a vaccine against the coronavirus infection has been registered this morning (in Russia) for the first time in the world,” the President told members of the government. “I thank everyone who worked on the vaccine – it’s a very important moment for the whole world.”

Of course, it’s worth noting that Russia-linked hackers were accused of spying on and possibly stealing vaccine-related “medical secrets” gleaned form research conducted in the UK.

Putin insisted that vaccination in Russia should only be carried out on a voluntary basis.

“I know that it works rather effectively, forms a stable immunity, and, I repeat, it passed all the necessary inspections,” the President added.

While the west raised alarms about potential safety issues caused by Russian “recklessness”, Vadim Tarasov, a top scientist at Moscow’s Sechenov University, where the trials took place, said Russia the country had a “head start” as it has spent the last 2 decades dedicating significant resources to the virus. The technology behind the Russian vaccine is based upon adenovirus, otherwise known as the common cold, he added. Created artificially, the vaccine proteins replicate those of COVID-19 and trigger “an immune response similar to that caused by the coronavirus itself,” Tarasov revealed.

Nikolay Briko, the Russian Health Ministry’s chief non-resident epidemiologist, echoed these sentiments.”This vaccine wasn’t developed from scratch, the Gamelei Research Center had a serious, significant research base on vaccines,” he was quoted as saying. “The technology of developing such a vaccine was perfected. So perhaps, the process was sped up due to the fact that the vaccine was not created from scratch. It is important that all stages (of vaccine research) are followed and that international requirements are adhered to.”

To try and reassure the Russian public, Putin declared his daughter, who participated in the “experiment” suffered only a mild fever that quickly went away.

“One of my daughters got the vaccine. In this sense, she took part in the experiment. After the first vaccination, she had a temperature of 38, the next day – 37 and that was all.”

The news that Putin administered the vaccine to his own daughter elicited some snickers on Twitter.

Nothing says ‘we have a great vaccine’ than also saying ‘No, you can’t see our scientific data on the vaccine testing’

But believe it or not (clearly, the reporters at the AP are still skeptical), news of the world’s first registered vaccine sent futures higher in premarket trading.

The first doses of the vaccine will be reserved for health-care workers and other vulnerable parties, Putin said. Russia says it hopes the vaccine will be available for mass innoculation early next year.

via ZeroHedge News https://ift.tt/31MkQJk Tyler Durden

Currently, there is much bullish commentary suggesting stocks can only go higher from here. Is the bullishness in the markets justifiable, or is it willful blindness?

“We remain very bullish on this market. You’re going to see money beginning to further move out of the bond market, and it makes all the sense in the world to be positioned in equities.”

This seems a little optimistic given the amount of money that has already flooded into the 5-largest “mega-cap” stocks which have accounted for a bulk of this years market returns.

Nonetheless, it is an interesting question.

From the bulls viewpoint the focus has been the ability for these companies to grow earnings.

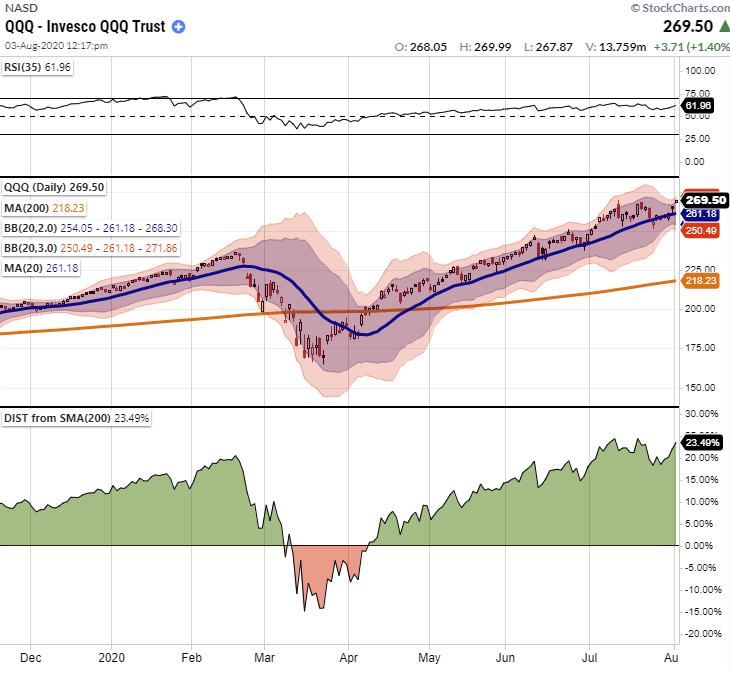

“While the S&P 500 is primarily driven higher by the largest 5-market capitalization companies, it is the Nasdaq that has now reached a more extreme deviation from its longer-term moving average.”

“Moving averages, especially longer-term ones, are like gravity. The further prices become deviated from long-term averages, the greater the “gravitational pull” becomes. An “average” requires prices to trade above and below the “average” level. The risk of a reversion grows with the size of the deviation.

The Nasdaq currently trades more than 23% above its 200-dma. The last time such a deviation existed was in February of this year. The Nasdaq also trades 3-standard deviations above the 200-dma, which is another extreme indication.”

It’s The Fed Stupid

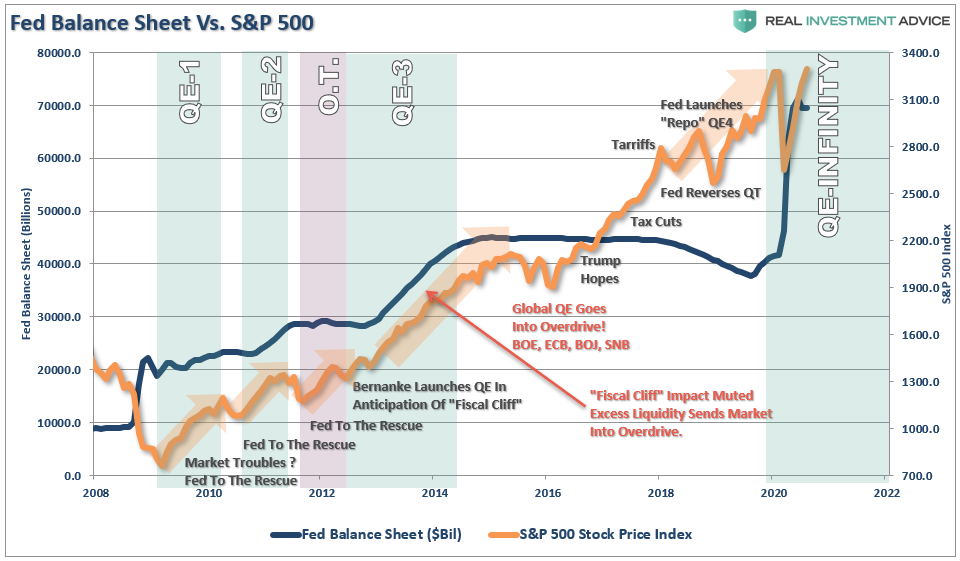

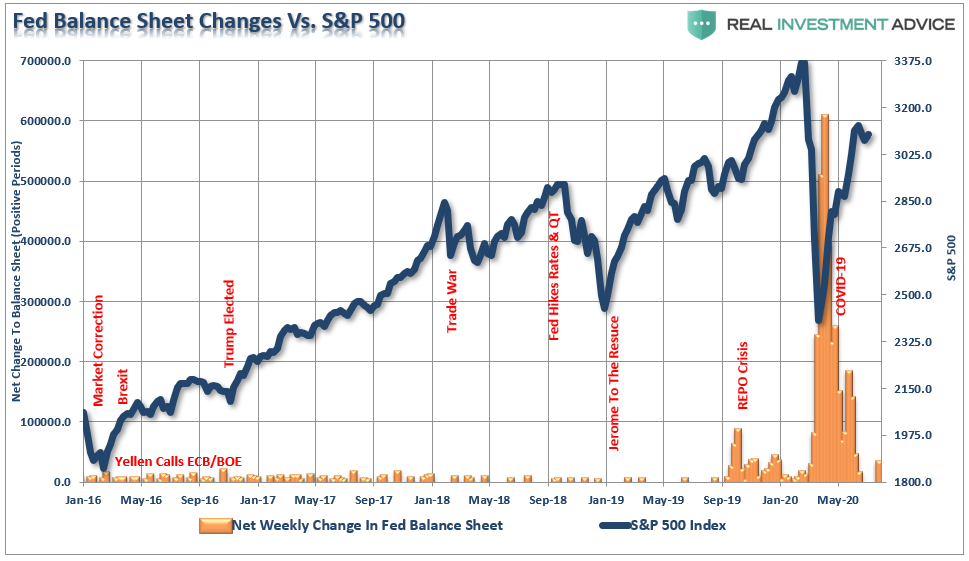

The immediate conclusion is the drive higher in the markets is a function of massive amounts of liquidity being injected into the financial markets by the Federal Reserve. As shown below that was certainly the case during March and April.

However, since then the tapering of the liquidity injections by the Fed has been marked as the slowing uptake of the various programs reduced demand.

While there is indeed truth to the Fed’s impact on the market, it is not solely responsible for the dislocation of prices from the underlying fundamentals.

As shown, the decline in fundamentals didn’t start during the pandemic. The decline in earnings started in early 2019 as economic growth slowed, and accelerated during the pandemic. However, during that same period stock prices rose, which is almost entirely attributable to “valuation expansion.”

Dumb Money All In

E*Trade recently released survey data which showed that despite the market plunge in March, bullish sentiment has returned:

Bullish sentiment returns. Half of surveyed investors (51%) are bullish, rising 13 percentage points since last quarter.

Investors are more likely to believe the market will rise. Over half of investors (51%) believe the market will rise, skyrocketing 20 percentage points this quarter.

But volatility will persist. More than half of investors (56%) believe volatility will continue, gaining nine percentage points since last quarter.

And investors expect a long road to recovery. More than half (54%) believe it will take more than one year to recover from the pandemic, and just one out of five investors (23%) would give the economy an “A” or “B” grade.

You get the idea. Just one quarter after panic selling lows, investors are once again “back in the pool.” Despite the economy just printing a nearly 40% decline in Q2, and earnings having dropped by nearly 40% from their peak, the “dumb money” is back to chasing stocks.

In particular, not only are “retail investors” chasing stocks, they are doing it with increased leverage by using options. As noted by CNBC recently:

“Investors have reentered the market at a record rate following the coronavirus-induced sell-off in March, and as traders look to profit, options volume has soared to an all-time high.

The average daily value of options traded has exceeded shares for the first time, with July single stock options volumes currently tracking 114% of shares volumes.

In other words, the options market is now larger than the shares market.”

We have seen record lows in the Put/Call ratio three times in 2020. All three lead to corrections.

Willful Blindness

Willful blindness, also known as willful ignorance or contrived ignorance, is a term used in law. Being “willfully blind” describes a situation in which a person seeks to avoid civil or criminal liability for a wrongful act by keeping themselves unaware of the facts that would render them liable or implicated.

Although the term was originally used in legal contexts, the phrase “willful blindness” has come to mean any situation in which people avoid facts to absolve themselves of their liability.

“‘Willful blindness’ is most prevalent in the financial markets. Investors regularly dismiss the ‘facts’ which run contrary to their current opinion. In behavioral investing terms this is also known as ‘confirmation bias.’”

As markets rise, investors take on exceedingly more risk with the full knowledge that such actions will have a negative consequence. However, that “negative consequence” is dismissed by the “fear of missing out,” or rather F.O.M.O.

As “greed” overtakes “fear,” investors become more emboldened as rising markets reinforce the conviction that “this time is different.”Ultimately, when the negative consequence eventually occurs, instead of taking responsibility for their actions, they blame the media, Wall Street, or their advisor.

This currently where we are in the markets today.

Value Proves It

Investors know there is a rising risk of loss, but, they are willfully ignoring the facts and and piling into risk because the narrative has simply become “fundamentals don’t matter.” In 2020, investors are again chasing “growth at any price” and rationalizing overpaying for growth.

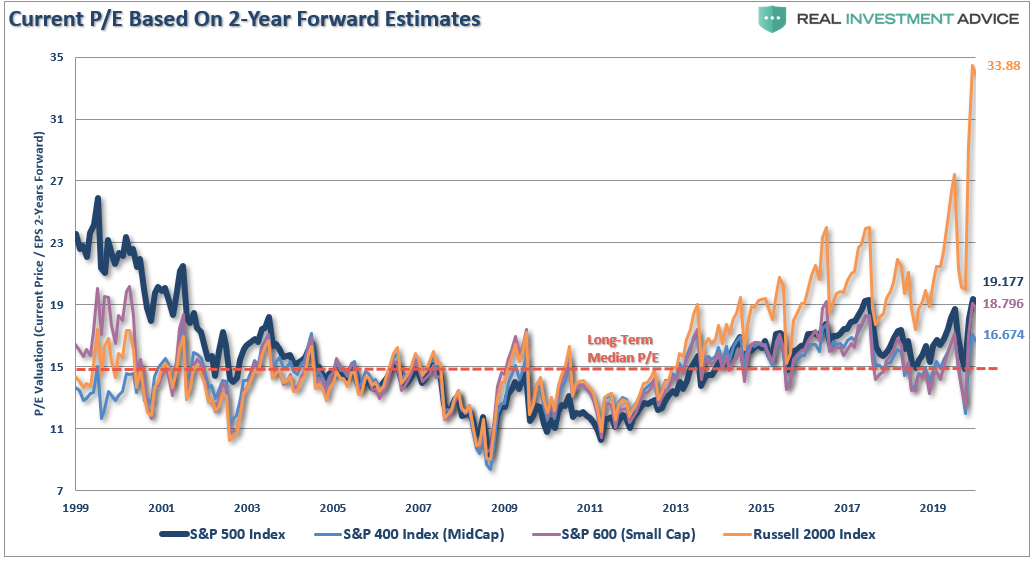

“Such makes the mantra of using 24-month estimates to justify paying exceedingly high valuations today, even riskier.”

There are two critical takeaways from the graph above:

Over the last 90 years, value stocks have outperformed growth stocks by an average of 4.44% per year (orange line).

There have only been eight ten-year periods over the last 90 years (total of 90 ten-year periods) when value stocks underperformed growth stocks. Two of these occurred during the Great Depression and one spanned the 1990s leading into the Tech bust of 2001. The other five are recent, representing the years 2014 through 2019.

In other words, there is high probability that investors chasing “growth” are going to pay a heavy price in the future..

It’s The Economy

The problem, as discussed in “Insanely Stupid,” the ability for stocks to continue to grow earnings at a rate to support high valuations will be problematic. Such is due to rising debts and deficits which will retard economic growth in the future. To wit:

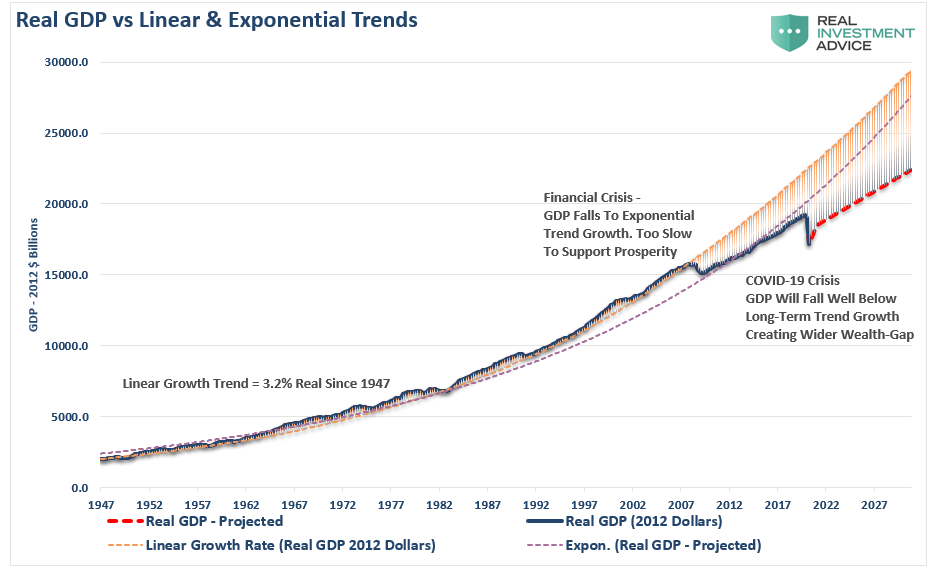

“Before the ‘Financial Crisis,’ the economy had a linear growth trend of real GDP of 3.2%. Following the 2008 recession, the growth rate dropped to the exponential growth trend of roughly 2.2%. Instead of reducing the debt problems, unproductive debt, and leverage increased.

The ‘COVID-19’ crisis led to a debt surge to new highs. Such will result in a retardation of economic growth to 1.5% or less.”

Slower economic growth, combined with a potential for higher taxes, increases the probability that “risk” may well outweigh “reward” at this juncture.

Such doesn’t mean that stocks can’t go higher in the near term, and despite some wiggles along the way, it is quite likely they will simply because of momentum and lot’s of “bullish bias.”

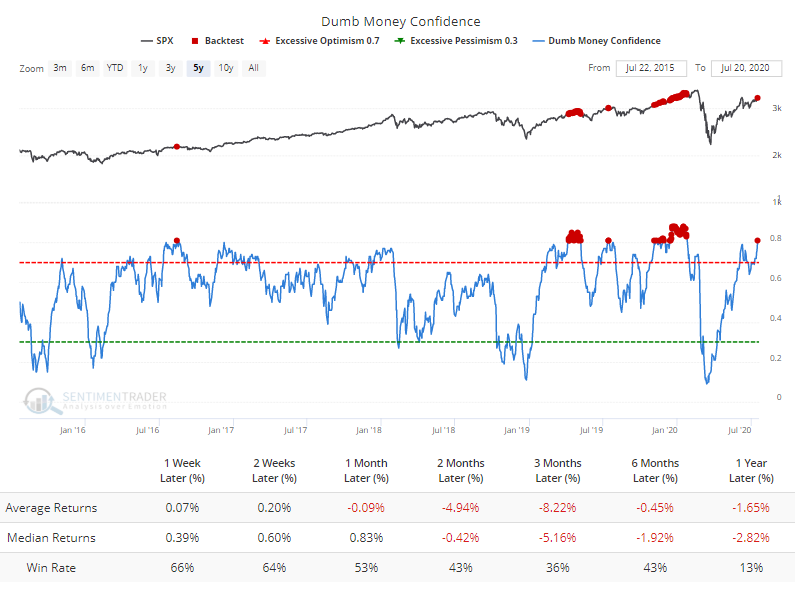

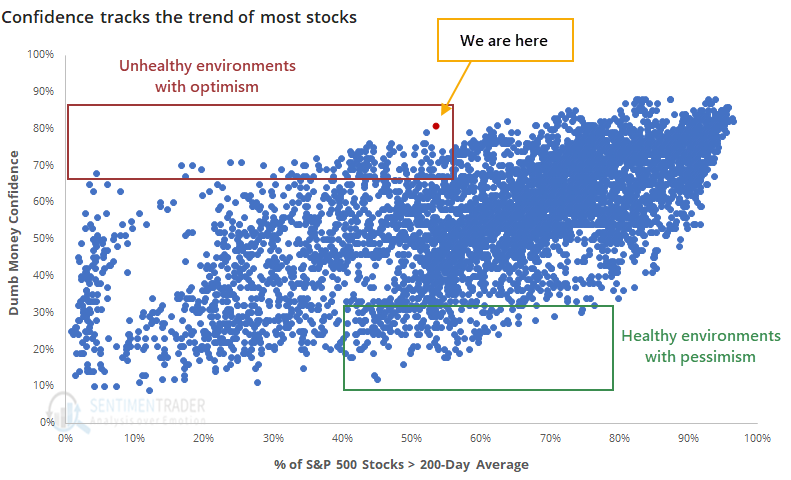

“We’ve often noted that during times of unhealthy market environments, when fewer than 60% of stocks can hold above their 200-day averages, that periods of high optimism tend to lead to below-average forward returns.

We’re seeing that now, to a historic degree. Since we’ve been tracking this data, just over 20 years, there has never been a day when Dumb Money Confidence was at or above 80% while fewer than 60% of stocks in the S&P 500 were trading above their 200-day averages. Until now.” – Sentiment Trader

The Problem Of Eternal Bullishness

The problem of “eternal bullishness” is it leads to the “willful blindness” of risks, rather than having a healthy respect for, and recognition of, those risks. This leads to the unfortunate problem of being “all-in” on every hand which has a devastating consequence when a mean reverting event occurs.

Our job as investors is to navigate the waters within which we currently sail, not the waters we think we will sail in later. Higher returns come from the management of “risks” rather than the attempt to create returns by chasing markets.

I recently quoted Robert Rubin, former Secretary of the Treasury, in “This Is Nuts,” as it defined our philosophy on risk.

‘As I think back over the years, I have been guided by four principles for decision making. The only certainty is that there is no certainty. Second, every decision, as a consequence, is a matter of weighing probabilities. Third, despite uncertainty, we must decide and we must act. And lastly, we need to judge decisions not only on the results but also on how we made them.

Most people are in denial about uncertainty. They assume they’re lucky, and that the unpredictable can be reliably forecasted. Such keeps business brisk for palm readers, psychics, and stockbrokers, but it’s a terrible way to deal with uncertainty. If there are no absolutes, all decisions become matters of judging the probability of different outcomes, and the costs and benefits of each. Then, on that basis, you can make a good decision.’” – Robert Rubin

Focus On Risk

It should be evident that an honest assessment of uncertainty leads to better decisions.

The problem with “Eternal Bullishness” and “Willful Blindness” is that the failure to embrace uncertainty increases risk, and ultimately loss.

We must be able to recognize and be responsive to changes in underlying market dynamics. If they change for the worse, we must be aware of the inherent risks in portfolio allocation models. The reality is that we can’t control outcomes. The most we can do is influence the probability of specific outcomes.

Focusing on risknot only removes “willful blindness” from the process, it is essential to capital preservation and investment success over time.

via ZeroHedge News https://ift.tt/3ac6ZzI Tyler Durden

“More Robust Than Expected”: Promising Preliminary Class 8 Data For July Has Analysts Cautiously Optimistic Tyler Durden

Tue, 08/11/2020 – 05:30

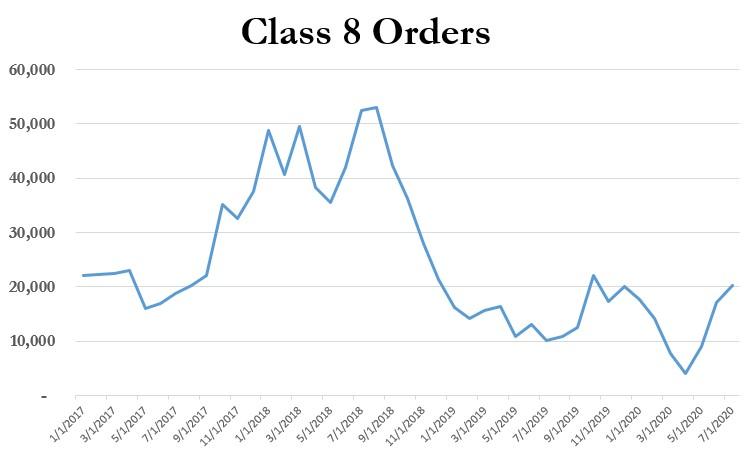

Preliminary data for July shows that Class 8 commercial truck sales may have finally started to rebound.

Stung by both the pandemic and a legacy backlog dating back almost two years that has acted as a constant drag on new orders for the last 18 months, preliminary Class 8 orders were 20,300 units for July, up 27% sequentially and up 98% from 2019’s numbers.

Despite the numbers being nowhere near 2017 and 2018 peak levels, July looks to mark the strongest month of the year for Class 8 orders so far, possibly telegraphing an optimistic second half of the year.

In an August 4 release reported by The Trucker, ACT Research’s Kenny Vieth, president and senior analyst, said: “Preliminary data show that July orders for medium- and heavy-duty vehicles jumped to a six-month high.”

He continued: “The context of rising rates and improving carrier profits adds perspective to what is now occurring in Class 8 orders: Supply matters. With many drivers (and trucks) sidelined, there is now insufficient available capacity for rebounding freight volumes. There is a strong relationship historically between carrier profits and equipment demand.”

He also noted that the positive shift in numbers came despite the additional headwind of a slowing economy during the end of the month:

Vieth noted that during the last week of July, reports showed the U.S. economy for the second quarter of 2020 had dropped 9.5% from the first quarter and was 10.6% below the ending level for 2019.

Jonathan Starks, chief intelligence officer for FTR, says that despite the good month, he is still forecasting a slow recovery: “As we hit the height of summer demand, the freight markets showed strength and resilience and that led to additional orders for trucks. The order activity for both June and July was more robust than expected and is good news for the equipment producers. However, despite the increasing orders, FTR still expects the Class 8 market to maintain a slow, steady recovery.”

He continued: “The freight markets sustained a traumatic decline of volumes at the start of the pandemic and consumer demand, on an absolute basis, will remain weaker as we deal with high levels of unemployment and a Congress that has been unable to foster a bi-partisan solution to stimulate demand. The OEMs received a needed boost from July orders, activity that will help keep the industry moving in an upward direction.”

We will update this article when finalized July data becomes available, which should be in several days.

via ZeroHedge News https://ift.tt/2DwNw0P Tyler Durden

The impact of the global coronavirus lockdown is set to plunge 100 million people into extreme poverty, warns a new report by the Pulitzer Center on Crisis Reporting.

The report appears to pin the blame on COVID-19 itself for the economic impact, yet the actual culprit is discovered to be the “restrictions” put in place by governments in response to the pandemic.

“With the virus and its restrictions, up to 100 million more people globally could fall into the bitter existence of living on just $1.90 a day, according to the World Bank. That’s “well below any reasonable conception of a life with dignity,” the United Nations special rapporteur on extreme poverty wrote this year. And it comes on top of the 736 million people already there, half of them in just five countries: Ethiopia, India, Nigeria, Congo and Bangladesh.”

The report notes that the impact of the lockdown on the poor in countries like India was “so abrupt and punishing” that their Prime Minister, Narendra Modi, begged for forgiveness.

The report will stir up further debate as to whether the global lockdown will prove more deadly than COVID-19 itself, with extreme poverty being directly linked to death and shortened life spans. According to research published by Imperial College London and Johns Hopkins University, around 1.4 million people are expected to die from untreated TB infections due to the coronavirus lockdown.

Experts have also warned that hundreds of thousands or even millions of people could die in the longer term as a result of the lockdown preventing them from receiving treatment for cancer and other serious illnesses.

Given that many of those sunk into extreme poverty as a result of the lockdown live in sub-Saharan Africa, this could also exacerbate mass immigration from that region into Europe.

“It’s a timely reminder that the the main cost of the lockdowns favoured by liberal policy-makers across the world will not be people in the West, but those hovering just above the poverty line in the developing world,” writes Toby Young.

“Thanks to the misguided enthusiasm of Western governments for imprisoning entire populations in their homes, thereby triggering a global recession, tens of millions of people will die of starvation in low-income countries.”

* * *

My voice is being silenced by free speech-hating Silicon Valley behemoths who want me disappeared forever. It is CRUCIAL that you support me. Please sign up for the free newsletter here. Donate to me on SubscribeStar here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown.

via ZeroHedge News https://ift.tt/31IGwG7 Tyler Durden

Italian PM Giuseppe Conte Is Considering Digging A Tunnel Between The Mainland And Sicily Tyler Durden

Tue, 08/11/2020 – 04:15

If there’s one thing the pandemic has done globally, it has been forcing countries to look inward and reassess both their infrastructure and their reliance of products and services on China. The U.S. has already vowed to start making drug components domestically and President Trump has long been proposing infrastructure upgrades.

And in keeping with the trend of upgrading infrastructure – which hasn’t quite been Italy’s expertise anytime over the last few decades – Italian Prime Minister Giuseppe Conte has now said he is considering an underwater tunnel that links Sicily to mainland Italy.

Conte mulled the plans during a speech he gave on Sunday evening in which he announced several plans that appear to be focused on the country maintaining its infrastructure independence. Before building such a tunnel, Conte said that the country would need to improve its internal routes first.

As of today, Sicily is still the only region of Italy which cannot be serviced by the country’s “Eurostar” trains.

The Strait of Messina Bridge has been proposed between the mainland and Silicy for years, but was cancelled in both 2006 and 2013 due to budget constraints. Now that the entire world has collectively decided to ignore budget constraints and allow Central Banks to do whatever they want, it’s no surprise that a project connecting the 576 km between Calabria and the mainland may actually move forward.

At the same speech, Conte also said he wanted to focus on rolling out broadband across the country before reviewing whether or not China should be allowed to supply the country with 5G technology, Bloomberg reported.

“Italy needs a single grid and recent talks will be wrapped up with a clear path by the end of this month,” he said. Given the recent controversy surrounding Tik-Tok and ongoing questions about Chinese hardware and maintaining privacy, our guess is that Huawei may not be leading the list of infrastructure providers to help implement such a network.

But when it comes to the tunnel, there’s one “genius” we can recommend…

via ZeroHedge News https://ift.tt/2CeMw0q Tyler Durden