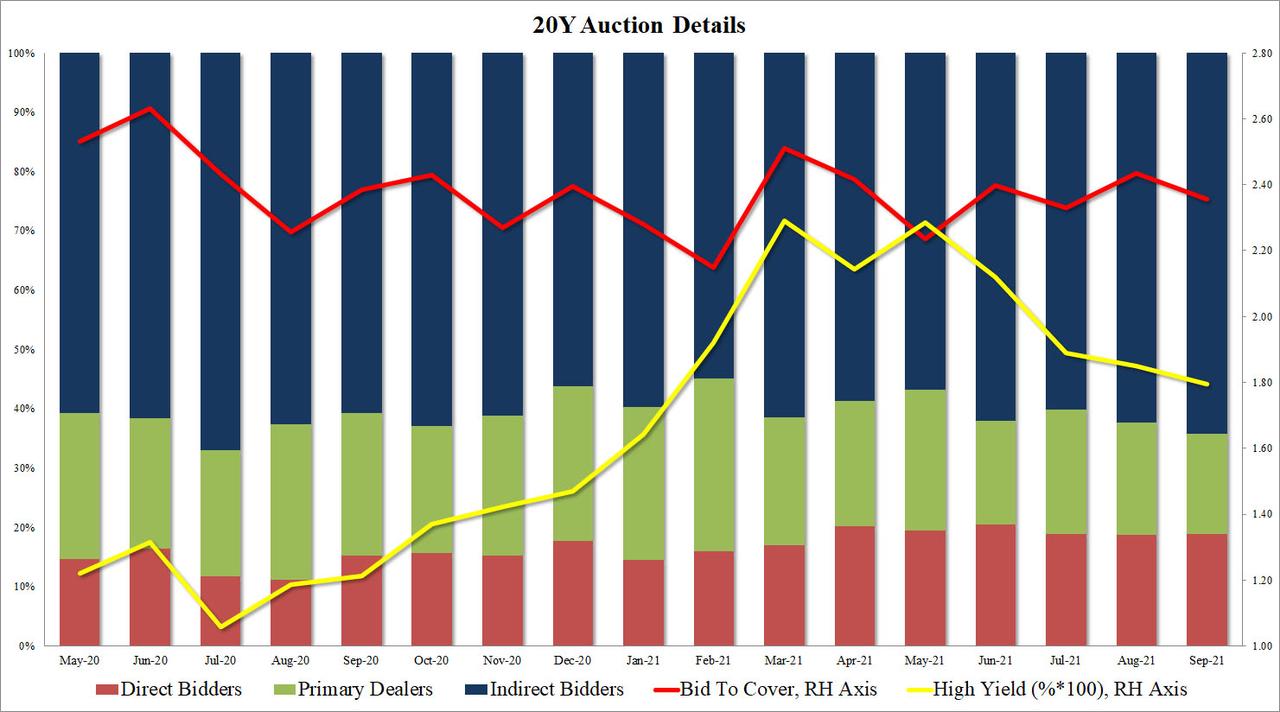

Stellar 20Y Auction Thanks To Second Highest Indirects On Record

With Treasury yields resuming their slide this week on the back of Monday’s sharp risk-off sentiment, and today’s surprise reversal which sent yields back to unchanged even as stocks rebounded, there were some concerns today’s 20Y auction (technically a 19-year-11-month reopening) would face some demand challenges. It did not, and in fact demand for today’s $24 billion offering was one of the strongest since this auction was introduced last May.

Starting at the top, the high yield of 1.795% stopped through the When Issued 1.797% by 0.2bps. It was the lowest yield for the tenor since January’s 1.643%, and well below last month’s 1.850%.

The bid to cover of 2.36 was slightly below last month’s 2.44, and just below the recent, six-auction average of 2.39.

The internals were more solid, with Indirects at 64.2% taking down the most since July 2020 and the second highest on record. Directs took down 18.9%, or in line with the recent average of 19.1% leaving Dealers holding 16.9%.

Overall, a remarkably solid 20Y auction made possible by near-record foreign demand, and indicates that nobody is worried about any hawkish surprises out of the Fed tomorrow.

DraftKings’ $20 Billlion Bid For UK Sports Book Entain Could Trigger Frenzied Bidding War

As sports betting becomes increasingly popular and mainstream across the US (thanks to a shift in state laws that has made the practice legal in a growing number of states), DraftKings, the US fantasy sports/sports gambling company, has made a roughly £16.6 billion ($22.7 billion) offer for the UK-based gambling platform Entain.

Entain confirmed Tuesday that it had received the offer “the consideration for which would include a combination of DraftKings stock and cash.” Per the FT, this is the second time this year a rival has sought to acquire the business and consolidate the fast-growing US market.

The bid, which was submitted in recent days, valued Entain at more than £25 ($34)/share, according to a source with knowledge of the matter who spoke with the FT. CNBC has reported that the offer would consist mostly of stock.

DraftKings isn’t the only recent suitor for Entain. The British firm, which owns brands like Ladbrokes, Coral and Bwin, received an £8 billion (nearly $11 billion) takeover bid from the US casino group MGM in January, roughly half the valuation that DraftKings has assigned. However, Entain already has a joint venture with MGM to offer sports betting in the US via a platform called BetMGM. However, that deal could be scrapped if the DraftKings bid is accepted.

In a filing with the LSE confirming the offer, Entain’s board confirmed that it received a proposal from DraftKings, which would include a combination of stock and cash. The filing did not contain any information on the price of the offer. “A further announcement will be made as and when appropriate,” Entain noted in the filing. “Shareholders are urged to take no action at this time.”

Should DraftKings win the deal, it would dramatically increase its overseas presence as sports betting continues to expand in popularity not just in the US, but around the world.

Since it first went public via SPAC, DraftKings has emerged as one of the most successful companies to list via a SPAC (special purpose acquisition company) and is widely considered one of the catalysts for the subsequent SPAC boom. The company’s market value has risen more than 6x, since it first listed at a $3.3 billion valuation in April 2020 through a merger with Diamond Eagle Acquisition Corp, a Spac led by veteran Hollywood executives Harry Sloan and Jeff Sagansky.

Entain shares soared by double digits on news that DraftKings had doubled MGM’s offer (Entain’s management said at the time that the MGM offer had significantly undervalued the firm, and rejected it).

For what it’s worth, MGM has a say when it comes to the sale of Entain’s US assets.

“Any transaction whereby Entain or its affiliates would own a competing business in the U.S. would require MGM’s consent,” the company said in a statement. “MGM will engage with Entain and DraftKings, as appropriate, to find a solution to the exclusivity arrangements which meets all parties’ objectives.”

DraftKings confirmed the size of the offer Tuesday morning.

The big question now: Will MGM return with another offer raising its valuation for Entain? Or will another bidder come out of the woodwork? Louis Capital Markets analyst Ben Kelly speculated on Tuesday that Las Vegas Sands might make a bid of its own.

Despite the post-pandemic economic improvement and wide expectations that the Fed will begin tapering quantitative easing in the near future, bond yields have remained stubbornly low. Ten-year Treasury yields remain stuck just above 1.3%.

Analysts cited in the Reuters report said the Fed “needs bonds to respond to the end of the pandemic-linked recession.”

ING Bank research analyst Padhraic Garvey told Reuters higher yields would align markets more with the signals coming from central banks.

“To facilitate that, we argue that there needs to be a tantrum. If the Fed has a taper announcement … and there is no tantrum at all, that in fact is a problem for the Fed,” he said.

Analysts say a bond market tantrum would involve yields rising 75-100 basis points (bps) within a couple of months.

What Would It Mean in Practice?

This isn’t just a wonky discussion about interest rates. What we’re really talking about here is a big sell-off in the bond market.

Bond yields move inversely with bond prices. As the price of bonds drops, interest rates rise. Bond prices and yields move in response to supply and demand. Higher supply and lower demand will push the price down and yields up to stimulate buying. Conversely, a lower supply of bonds, or higher demand, will drive the price up and yields will fall.

So, when analysts talk about a bond market tantrum, they mean a bond sell-off that will flood the market with excess Treasuries, drive the price down and push interest rates up.

According to the Reuters article, the Fed not only wants higher yields to “better reflect” economic growth; it also wants to “recoup some ammunition to counter future economic reversals.”

But this analysis completely ignores the elephant in the room – debt – specifically the federal debt.

Why Are Yields So Low to Begin With?

This is a key question the Reuters article never takes on. But it’s the key to understand what is actually going on in the bond market.

The answer is simple. Yields are low because the Fed continues to create artificial demand in the Treasury market by purchasing some $80 billion in bonds every month. It launched this massive QE program at the onset of the pandemic and it continues today unabated. The Fed literally has its big fat thumb on the bond market.

Why?

Because the US government needs the central bank to buy Treasuries to support the bond market in order to finance its multi-trillion budget deficit. Without Fed intervention, the flood of borrowing would tank the bond market and send interest rates soaring.

In a nutshell, the central bank facilitates the federal government’s excessive borrowing and spending by creating artificial demand in the bond market. The Federal Reserve buys Treasuries on the open market with money created out of thin air. This supports bond prices and keeps interest rates artificially low. Without this central bank intervention, there wouldn’t be enough demand in foreign and domestic markets to absorb all of the bonds the US Treasury needs to sell. Interest rates would skyrocket and make the cost of borrowing prohibitive.

Between March 2020 and May 2021, the federal government has added $4.7 trillion to the national debt. In roughly that same time period, the Federal Reserve purchased a staggering $2.44 trillion in US government bonds. In other words, the Fed monetized more than half of the US debt accrued during the first year of the pandemic. No other entity bought more US bonds than the Fed – not foreign investors, not US banks, and not even US corporations and individuals.

The Question Reuters Never Asks

Debt monetization never comes up in Reuters’ analysis. But this is a significant question: how would a bond market tantrum impact US government borrowing and spending? And will the Fed really let this happen?

A bond market selloff would make it more difficult for the US Treasury to sell bonds. Remember, the Fed’s thumb on the market helps make the borrowing spree possible.

And the borrowing and spending are not about to end any time soon. Congress is working to pass a massive infrastructure bill. Along with Biden’s proposed budget, we’re looking at some $6 trillion in spending in 2022. To put that into perspective, total federal spending for fiscal 2021 stands at $6.3 trillion with one month remaining. In other words, the Federal government wants to spend almost as much next year as it did this year.

This means the US Treasury will have to continue selling bonds at a torrid rate. How will it do this if the Fed pulls the plug on QE? How will it continue to borrow if interest rates spike? A bond market tantrum is a nightmare scenario for the US government. This is precisely why Peter Schiff says even if the Fed starts to taper, it will ultimately expand QE.

Last summer, Federal Reserve Chair Jerome Powell claimed the central bank isn’t monetizing the debt. During testimony before the Senate Committee on Banking, Housing, and Urban Affairs back in June, Powell flatly denied the central bank is buying assets in order to facilitate the Treasury’s sale of debt. “That certainly is not our intention,” Powell said.

It wasn’t in any way about meeting Treasury supply, and it continues not to be. We really don’t think about it.”

Powell then claimed that the demand for Treasuries was “robust.”

But as already discussed, the demand for Treasuries was only robust because the Fed was buying Treasuries.

As far as Powell’s claim that the Fed doesn’t “think about” the ramifications of its monetary policy on government financing, I call BS.

The glib assessment of a “bond market tantrum” by Reuters only shows part of the picture. Sure, in some ways, the Fed bankers would like to see bond yields increase. They would like to taper asset purchases. But they haven’t and there’s a reason for it. They have to know the ramification of rising interest rates in a world buried by debt. They have to know the US government needs the central bank’s thumb on the bond market.

The Fed is between a rock and a hard place. Reuters identifies the rock but ignores the hard place.

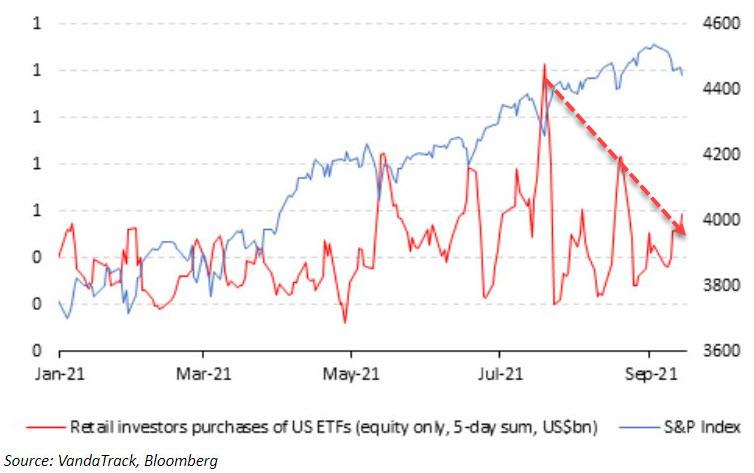

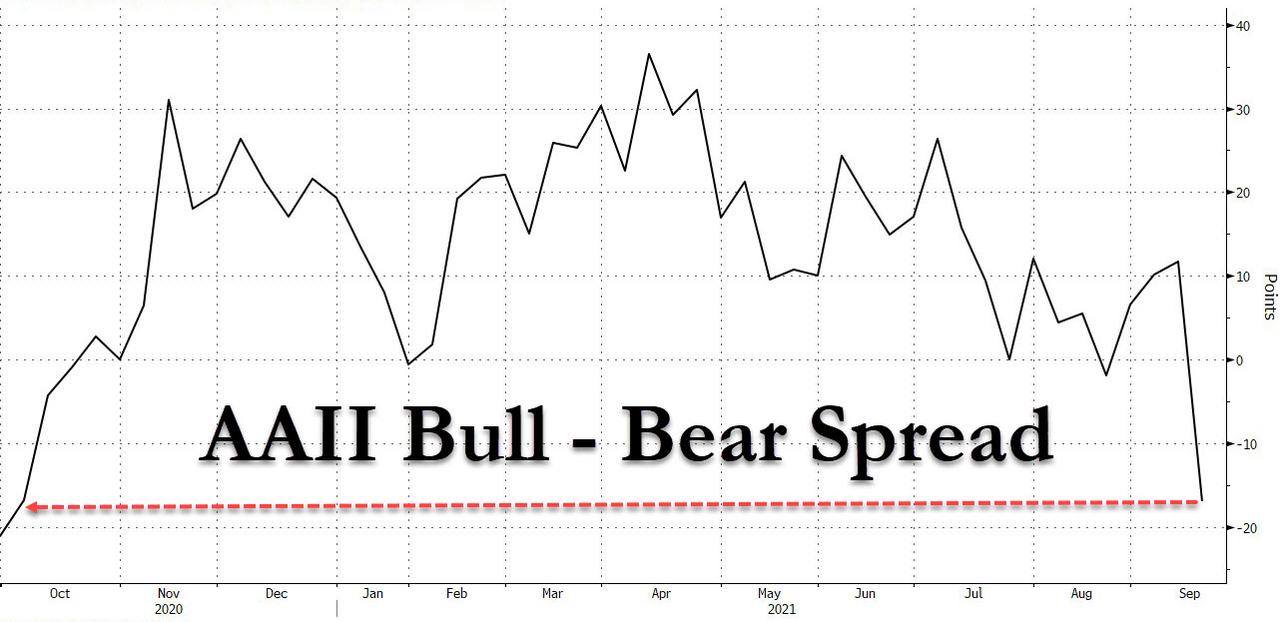

Retail Investors Flooded Into Stocks On Monday Just As Professional Sentiment Turned Most Bearish Since Last October

One week ago, when we last looked at the decline in retail participation in the market, we quoted Vanda Research which said that this trend raised the chances of more serious declines if big investors continue to retreat.

“While we have seen a pick-up in ETF buying this week, the magnitude has been a little underwhelming relative to previous selloffs,” Ben Onatibia and Giacomo Pierantoni wrote. “This diminishing appetite to support the equity rally raises the odds of a larger selloff if institutional investors continue to sell.”

In retrospect, they were right, even if instead of a full-blown 10% correction we just got a modest half “corr“, which saw the S&P suffer its first 5% drawdown since 2020.

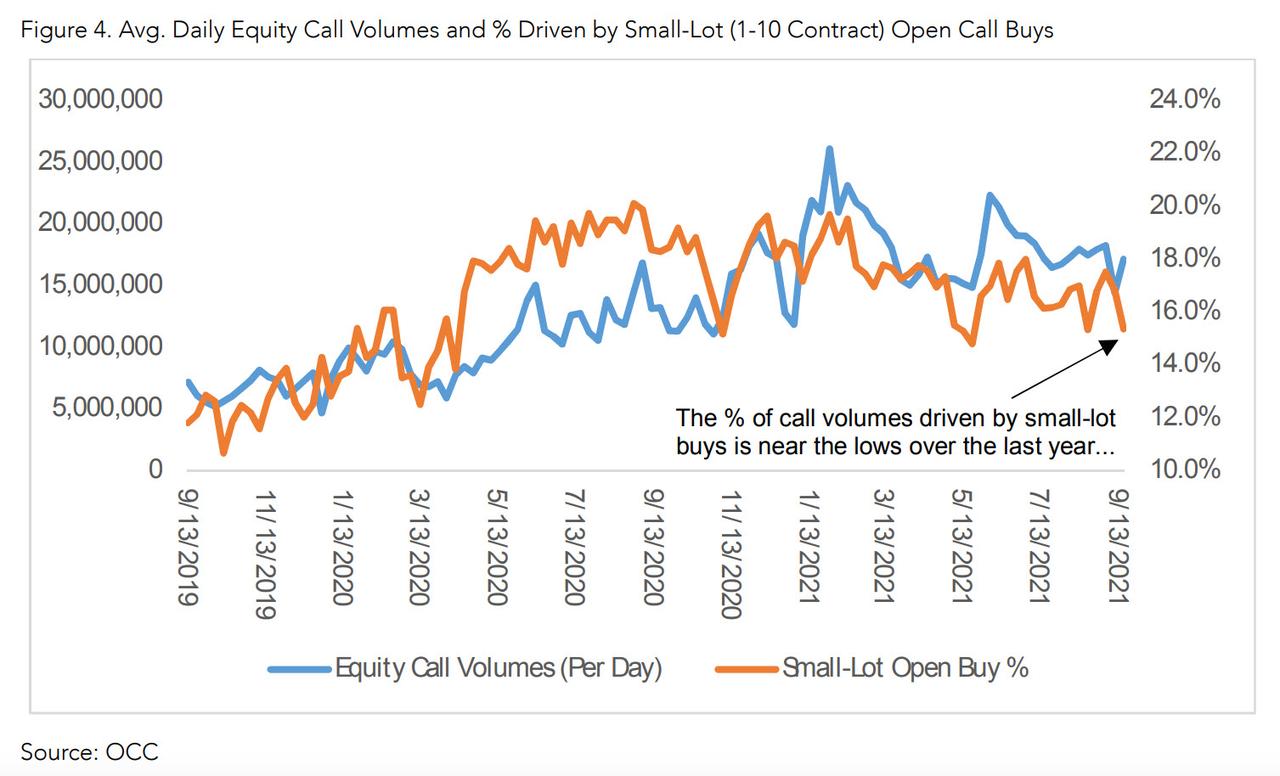

Picking up on this, this morning Susquehanna looking at the latest data from the Options Clearing Corp. and noted that so-called newbie traders – those buying or selling 10 contracts or less at a time – continued to scale back their equity call-option buying to nearly a 17-month low going into the rout…

… a move which according to Bloomberg looked rather smart with the S&P 500 down 1.7% on Monday and bearish bets on the market’s trajectory on the rise.

According to Susquehanna’s Christopher Jacobson, the so-called “dumb money” retail crowd had been scaling back its call-buying appetites along with professional investors, albeit for slightly different reasons. The latter is doing it out of fear that this year’s rally of as much as 21% is losing steam, while the former is chasing a rally in hotter assets like cryptocurrencies. Whatever the reason, the synchronized skepticism may lend optimism to the idea that the selloff’s blow to the market won’t be as severe as it could have been otherwise.

However, there was a sharp divergence between what professional investors and retail traders did on Monday when stocks tumbled amid growing fears of Evergrande contagion: on one hand, there was a bearish options deluge with ~5.3 million bearish contracts on the SPDR S&P 500 ETF Trust changing hands yesterday, the most since June last year, data compiled by Bloomberg show. That as the volume of call contacts reached the highest since 2013.

This was likely due to Wall Street professionals betting that Monday’s slide was just getting started, a sentiment underscored by the latest AAII survey print, which showed that sentiment plumbed lows not seen since 2020 as the gap between bearish and bullish sentiment readings hit the widest level since October 2020… and touched the point that has been historically associated with buying opportunities. Indeed, according to RBC Capital Markets, when the gap was wider than minus-10 in the past, the S&P 500 rallied 86% of the time in the next 12 months, gaining 15% on average.

And while to some, like Miller Tabak’s Matt Maley, the soaring negative sentiment wasn’t sufficient to sound an all-clear – after all we still haven’t had a day when China was back from holiday and we have no idea how Beijing will respond to the Evergrande fireworks – noting that “we’re going to have to see that activity come down and meet the lower level of bullishness before it would signal a change,” retail investors had seen enough, and after treading water for the past few weeks into yesterday’s dump, retail daytraders took advantage of the selloff to pile back into some of the largest U.S. exchange-traded funds and bank stocks, providing a buying boost to sliding stock and bucking worries that the group would let stocks tumble.

According to the latest Vanda research note, individual investors bought a total of $1.93 billion worth of assets Monday, the fourth-largest net buying since the start of the pandemic.

Vanda found that buying from the day-trading crowd was mostly concentrated in popular index ETFs such as the SPY, and the QQQ which saw combined inflows of $337 million, while separate data from Fidelity showed the SPY fund and Apple shares were the most bought assets on its platform Monday.

Large investment banks – such as Citigroup and Bank of America – were also among the most bought companies, while bigger institutional investors were likely selling, Vanda said.

The data suggest that just as professional investors were positioning for further downside by a surge in put buying, retail investors took the other side of the trade, and rushed into the broader markets, particularly in megacap tech stocks, to increase their holdings in spite of a jump in volatility.

There was a surprise in the Vanda data which found individuals sold shares of airline companies like American Airlines Group and Delta Air Lines; Vanda researcher Ben Onatibia wrote. That selling “means institutional investors were on the other side of the trade, building exposure to the reopening trade.”

True to form, daytraders also snapped up shares of meme stocks despite the group’s worst day in months. Favorites like AMC Entertainment and GameStop saw continued interest, but newcomers like SmileDirectClub were also bought, Fidelity data show. The three stocks were among the most traded companies on Monday and edged higher on Tuesday.

Nicholas Colas, co-founder of DataTrek Research, said the return of retail traders buying the dip was an “important observation,” given their impact on stock markets in 2021, and a continuation of what we said in May 2020 when we explained “How Retail Investors Took Over The Stock Market.“

A string of explosions struck Taliban vehicles in Afghanistan’s provincial city of Jalalabad over the weekend, killing eight people, among them Taliban fighters.

ISIS claimed responsibility for the attacks.

The Taliban are under pressure to contain ISIS militants, in part to make good on a promise to the international community that they will prevent the staging of terror attacks from Afghan soil.

There is also a widely held expectation among conflict-weary Afghans that the new rulers will at least restore a measure of public safety.

“We thought that since the Taliban have come, peace will come,” said Feda Mohammad, a brother of an 18-year-old rickshaw driver who was killed in one of September 19th’s blasts, along with a 10-year-old cousin.

“But there’s no peace, no security. You can’t hear anything except the news of bomb blasts killing this one or that,” Mohammad said.

The weekend bomb blasts served as a reminder of the threat the militants pose.

On September 21st, the Taliban said that there was no evidence of Islamic State or al Qaeda militants being in the country, despite the attacks.

Taliban spokesman Zabihullah Mujahid rejected accusations that al-Qaeda maintained a presence in Afghanistan and repeated pledges that there would be no attacks on third countries from Afghanistan from militant movements.

“We do not see anyone in Afghanistan who has anything to do with al Qaeda,” he told a news conference in Kabul.

“We are committed to the fact that, from Afghanistan, there will not be any danger to any country.”

On August 26th, as American and foreign troops completed their withdrawal and frantic airlift from the country, ISIS suicide bombers targeted U.S. evacuation efforts outside Kabul international airport in one of the deadliest attacks in Afghanistan in years. The blast killed 169 Afghans and 13 U.S. service members.

The events have bolstered fears of more violence, as ISIS militants exploit the vulnerability of an overstretched Taliban government facing massive security challenges and an economic meltdown.

“They’re making a very dramatic comeback,” Ibraheem Bahiss, an International Crisis Group consultant and an independent research analyst said of Islamic State. “There could be a long-term struggle between the groups.”

Despite the significant Kabul Airport attack, Mujahid denied the movement had any genuine presence in Afghanistan though he said it “invisibly carries out some cowardly attacks”.

“The ISIS that exists in Iraq and Syria does not exist here. Still, some people who may be our own Afghans have adopted the ISIS mentality, which is a phenomenon that the people do not support,” he said.

“The security forces of the Islamic Emirate are ready and will stop them,” he said.

Biden Tells UN He Still Wants To ‘Return To Full’ Nuclear Deal ‘If Iran Does The Same’

Tehran is signaling that it plans to re-enter Vienna nuclear talks within the “next few weeks” after the negotiations have been stalled since June, which has lately left Biden admin officials in doubt over whether a deal is salvageable at this point.

Iran’s newly installed President Ebrahim Raisi is set to address Tuesday’s United Nations General Assembly (UNGA) via video feed, given he’s currently under Washington human rights sanctions, making physical travel to UN headquarters in New York complicated.

US President Joe Biden, meanwhile, in his speech before the UNGA said that he’s offering a full return to the deal “if Iran does the same”.

Biden didn’t spend much time on Iran in his speech, with critics lambasting him for not using the occasion to go after the Iranian regime on human rights and a track record of oppression. Biden’s key line in the Tuesday speech was as follows:

“The United States remains committed to preventing Iran from gaining a nuclear weapon. We are working with the P5+1 to engage Iran diplomatically and seek a return to the JCPOA. We are prepared to return to full compliance if Iran does the same.”

Within the past weeks there were unconfirmed reports that Iran and world powers could hold negotiations on the sidelines of this week’s UN meeting; however, Foreign Ministry spokesman Saeed Khatibzadeh denied that full multi-lateral talks would take place.

“Iran has no plans to hold multilateral talks during the UN summit,” Khatibzadeh clarified, but there may be talks with individual mediating powers separately.

Today @IranIntl caught trucks protesting #Iran’s President Ebrahim Raisi and members of his administration in Manhattan as he prepares to address #UNGA. It’s the most sanctioned and wanted administration since 1979. pic.twitter.com/jxv4MwdBW4

Meanwhile, Raisi’s newly appointed negotiating team is expected to hold a firmer line compared to the prior “moderates” under former president Rouhani:

A seasoned Iranian diplomat, who was a member of Iran’s nuclear negotiations team in the 2010s under President Mahmoud Ahmadinejad, says new appointments at the Foreign Ministry signal a tougher negotiating posture in nuclear talks.

Washington has in a slow, piecemeal way already relaxed some Trump-era sanctions on Iran, but it’s been Tehran’s consistent position that a restored JCPOA deal is not possible unless an immediate full rollback is in effect.

Hundreds of Navy SEALS are risking being blocked from deployment after failing to get vaccinated, according to a lawyer and pastor counseling them.

As reported by Just the News, the number of SEALS involved in the dispute with the Pentagon amounts to as many as a quarter or more of all active members, a loss that could impact military readiness.

Some SEALS were given a deadline to get the vaccine and have sought a religious exemption.

“My clients include several Navy SEALS who are a small part of a large group of SEALS and other military members who are being asked to choose between their faith and their ability to serve our nation,” R. Davis Younts, a lieutenant colonel in the Air Force reserves and a lawyer representing several of the operators, said.

“They have been told that if they seek a religious accommodation, they likely will no longer be able to serve our country as Navy SEALs and have been given an arbitrary deadline to comply with the vaccine mandate.”

“My clients need time, and we are seeking at least a 90-day extension to [the] vaccine mandate compliance deadline they have been given,” he continued.

Similarly, Pastor Jeff Durbin, who has been ministering to the special operators for weeks, said between a quarter to a third of all active-duty SEALS are involved in the dispute with the Pentagon, including some who already have COVID-19 immunity because they recovered from the disease.

“There are hundreds of Navy SEALs who have not been vaccinated, do not want to take the vaccine, or who have had and recovered from COVID and have the benefit of natural immunity,” Durbin told Just the News.

“A large number of SEALS that I am speaking on behalf of are facing the very difficult decision that even with a legitimate religious exemption that is based upon their commitments to Christ, the Gospel, God’s Law, and the Constitution, they will no longer be Navy SEALs.”

“They are essentially being asked to make a decision between their commitments to the lordship of Christ and their careers as Navy SEALs,” he continued.

“Our country should be very concerned about what this would do to military readiness. Losing hundreds of Navy SEALs because of their legitimate and sincerely held Christian beliefs could be devastating to us as a nation.”

[ZH: Fox News’ Tucker Carlson commented on the situation last night: “To be clear, in case you’re wondering if this is in response to some kind of crisis: We don’t believe a single Navy SEAL has died of COVID. These are some of the healthiest people in the world, the Olympic athletes of the military. Many of them have had the virus and recovered, meaning they have more natural immunity than the vaccine could ever provide.”

“And yet, as of tonight, we’re hearing that hundreds of Navy SEALs face being fired imminently for refusing to take the shot,” Carlson further noted.

He continued, “Keep in mind there are only about 2,500 active-duty Navy SEALs, each of whom costs at least a half–million dollars to the U.S. government to train. Imagine the effect on our country’s military readiness. It’s horrifying. If you love the country, you would not do this. You would also not disable our hospitals by forcing our nurses to resign because they don’t want to take the shot.”]

“Many People Will Be Arrested” – Evergrande Lured Retail Investors Into Billions Of “Wealth Management Products” With Gucci Bags, Dyson Air Purifiers

In our post detailing how Evergrande became a “too big to fail” anchor of China’s shadow banking system, we noted that a key missing piece in the company’s funding was selling wealth management products – i.e., unregulated “shadow banking” products – to outside investors, as well as its own employees and their families, promising returns up to 13%. It is these WMP investors that are currently besieging the company’s offices across the country in hopes of getting some of their principal back, and which include everyone from paint suppliers to decoration and construction companies. To them, Evergrande owes more than 800 billion yuan ($124 billion) due within one year, while it has only a 10th of that amount of cash on hand. It will have even less once the now officially defaulted company makes priority payments to its banks and creditors.

Expanding on this striking funding source, Reuters today writes that lured by the promise of yields as high as 12, “tens of thousands of investors bought wealth management products” through China Evergrande, a transaction which was softened by gifts such as Dyson air purifiers and Gucci bags, not to mention the guarantee of China’s top-selling developer, a guarantee which we now know was worthless.

And now, many investors fear they may never get their investments back after the cash-strapped property developer recently stopped repaying some investors and set off global alarm bells over its massive debt. Some have been protesting at Evergrande offices, refusing to accept the company’s plan to provide payment with discounted apartments, offices, stores and parking units, which it began to implement on Saturday.

“I bought from the property managers after seeing the ad in the elevator, as I trusted Evergrande for being a Fortune Global 500 company,” said the owner of an Evergrande property in the conglomerate’s home province of Guangdong surnamed Du.

“It’s immoral of Evergrande not to pay my hard-earned money back,” said the investor, who had put 650,000 yuan ($100,533) into Evergrande wealth management products (WMPs) last year at an interest rate of more than 7%. That investor is about to learn that in addition to return, there is also risk, a concept almost forgotten in today’s world where central banks and authoritarian governments do everything to preserve the “wealth effect” and avoid social unrest resulting from stock price crashes.

According to a sales manager of Evergrande Wealth, launched in 2016 as a peer-to-peer (P2) online lending platform that originally was used to fund its property project, more than 80,000 people – including employees, their families and friends as well as owners of Evergrande properties – bought WMPs that raised more than 100 billion yuan in the past five years. Of these investments, some 40 billion yuan are still outstanding, and will likely never be repaid. Last week, Evergrande revealed that even Ding Yumei, the wife of billionaire founder Hui Ka Yan, had bought $3 million of the company’s investment products in a show of support.

As the FT adds, Evergrande financial advisers marketed the products widely, including to homeowners in its apartment blocks, while its managers persuaded subordinates to invest, the executives of Evergrande’s wealth management division said.

The publication adds that one executive – who spoke during a meeting with angry investors who went to the company’s Shenzhen headquarters to try to get their money back – suggested the products were too high risk for ordinary retail investors and should not have been offered to them. Of course, it is way too late now.

“My parents put the bulk of their savings, which is Rmb200,000 and not a lot by Evergrande’s standard, into its [wealth management products],” said the daughter of one investor who asked to be identified by her surname Xu. She said an Evergrande financial adviser stationed in an apartment tower built by the company in central China had persuaded her mother to invest. “They wouldn’t have trusted Evergrande’s wealth products had they not bought the developer’s apartment,” she said. “All they wanted was to ease the financial pressure from buying expensive cancer drugs [for Xu’s mother], nothing else.”

Last week, Xu was one of hundreds of people who travelled to Evergrande’s Shenzhen headquarters in hopes of recovering their investment.

One investor named Rosy Chen and her husband, an Evergrande employee, invested Rmb100,000 this year in a product with an advertised 11.5 per cent annual return on the urging of one of his superiors. The cash went to “supplement” the working capital of a company called Hubei Gangdun Materials, according to the investment contract.

“At first we waited, but when we saw we were among the only families in the whole [Evergrande] division not to buy in, we decided to invest too,” said Chen. “We believed Evergrande wouldn’t cheat its own employees.”

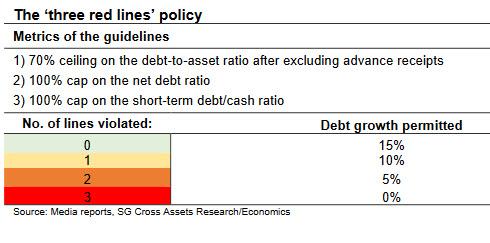

Remarkably, this hit to Chinese investors and resulting social unrest, comes as a time when China’s Xi has launched a renewed pursuit of core Marxism with his “Common prosperity” initiative, which also coincides with China’s years-long effort to deleverage its economy, which has pushed companies to resort to off-balance sheet investments in search of funding. It’s why we said recently that what is happening to Evergrande is a symptom of China’s great deleveraging campaign, which however for a country with 350% debt/GDP is doomed to fail.

The funniest thing about the whole Evergrande fiasco is that it’s due to China pretending it can reduce its debt without a crash.

Guys, ain’t happening: at least the US accepts this and has adopted the idiocy that is MMT to justify perpetual debt increase until it all blows up pic.twitter.com/xdw4F7CTQV

Incidentally China has only itself to blame for the Evergrande crisis. Having allowed unprecedented debt growth for much of the past decade, last year Beijing capped debt levels of property developers last year as part of its “three red lines” policy which limited how much debt growth various tiers of developers can engage in. As a result, the most indebted players like Evergrande – feeling even more pressure to find new sources of capital to ease mounting liquidity stress – ended up moving to the unregulated “shadow banking” market, and turned to employees, suppliers and clients for cash through commercial paper, trust and wealth management products.

Evergrande Wealth started to sell WMPs to individuals in 2019 after a regulatory crackdown led to a collapse of the P2P lending sector, said the sales manager and another Evergrande employee who bought the WMPs. To attract investors, the sales manager offered gifts such as Dyson air purifiers and Gucci handbags to each person who bought more than 3 million yuan of WMPs during a Christmas promotion last year.

A product leaflet provided by the sales manager seen by Reuters showed the WMPs are categorized as fixed-income products suitable for “conservative investors seeking steady returns”. It was anything but.

In an interview with local media, one Evergrande financial adviser said the products were a type of “supply chain finance”. While the money from retail investors may in years past have gone to its suppliers, the Evergrande executives in Shenzhen receiving retail investors said this was no longer the case.

Asked about Hubei Gangdun, one of the executives of Evergrande’s wealth management division said that it was just a shell company. “Proceeds from the WMPs have been used to bridge various funding gaps faced by the parent company,” the executive said. “There is no need to thoroughly examine where the money actually went.

“Some WMP proceeds were used to repay previous products but sales plummeted, making it difficult for the business model to continue,” he admitted.

“Many people . . . might be arrested for financial fraud if investors don’t get paid off,” he said. “Our products were not for everyone. But our grassroots salespeople didn’t consider this when making their sales pitches and they targeted everyone in order to meet their own sales targets.”

Translation: Evergrande used not just Ponzi instruments, but unregulated Ponzi instruments, which are now worth nothing.

In two products sold last November, a construction company in Qingdao was looking to raise up to 10 million yuan with annualized yield of 7% in one and 20 million yuan with yields ranging from 7.8% to 9.5%, depending on the investment size, in another. Minimum investments were 100,000 yuan and 300,000 yuan, respectively.

According to the sale manager, to make its products especially attractive, Evergrande offered additional yield up to 1.8% to certain investors, which would push returns to above 11% for a 12-month investment, an interest rate which in a world of zero rates, indicates funding stress if nothing else. Proceeds were to be used for Qingdao Lvye International Construction Co’s working capital, the documents showed. Repayment would either come from the issuer’s income or from Evergrande Internet Information Service (Shenzhen) Co, a subsidiary that runs Evergrande Wealth and promises to cover the principal and interest if an issuer fails to repay, the prospectus said.

The sales manager said the Qingdao company was working on Evergrande projects and would use the payment from Evergrande upon completion to repay investors.

“It’s a de-facto Evergrande product,” he said.

Other highly leveraged Chinese conglomerates including HNA Group, which declared bankruptcy early this year, and China Baoneng have used similar products. It was the overreliance of China’s giant conglomerates on shadow banking – among others – that prompted us back all the way back in 2018 to predict that after HNA and Anbang, Evergrande would fail next.

Anbang first, then HNA, Evergrande and Dalian Wanda

Earlier this week, Evergrande said that six senior executives would face “severe punishment” for securing early redemptions on investment products after retail investors were told that they would not be repaid on time.

Another big question is whether Evergrande ever included the 40 billion yuan of WMPs among the liabilities on its balance sheet; as the FT notes, the answer “remains unclear.”

“We expect part of it should be included in the total liabilities . . . however, there was no detailed disclosure in its financial statement, so it is difficult to verify,” said Cedric Lai, a senior credit analyst at Moody’s Investors Service.

Nigel Stevenson of GMT Research agreed it was unclear how Evergrande accounted for the WMPs. “Once the lid is lifted on its financials, it’s possible more horrors will be discovered,” he said.

In a petition to various government bodies, a group of WMP investors in Guangdong accused Evergrande of inappropriately using money that should have gone to the issuers to fund its own projects, and not sufficiently disclosing the risks. They also complained that they were misled by the stature of its chairman, Hui Ka-yan, noting that he was seated prominently during a 2019 celebration of the 70th anniversary of the founding of the People’s Republic of China.

“The investors trusted Evergrande and bought Evergrande’s WMPs out of our love for and faith in the Party and government,” they wrote.

US Equity Markets Tumble Into Red, Erase Overnight Gains

After yesterday afternoon’s surge higher, futures markets overnight extended the momentum, lifting US markets up over 1% at their peak around the European open (remember, much of Asian liquidity is on holiday still).

Since then, things have gone downhill and the selling pressure since the US opened has sent Small Caps, S&P, and Nasdaq into the red for the day…

Still wanna buy the dip? Do you feel lucky ahead of The Fed?

The LA County Department of Public Health responded to criticism of the maskless Emmys by claiming the rules didn’t apply because it was a television production event – despite the fact that workers were still made to wear masks.

There was uproar on Sunday as celebrities packed themselves into the Event Deck at LA Live without a mask amongst them as they kissed and hugged all night long.

Irate respondents on Twitter asked why celebrities were exempt from the rules yet their 4-year-old kids had to wear masks in class.

Under Los Angeles County’s Department of Health guidelines, everyone aged two years and older must wear a face covering in “all indoor public settings, venues, gatherings, and public and private businesses.”

However, after it was asserted that the rules don’t appear to apply to the rich and famous, the department was forced to respond.

New: LA County Department of Public Health tells me that the mask-less Emmys were not in violation of the county’s mask mandate because “exceptions are made for film, television, and music productions” since “additional safety modifications” are made for such events. pic.twitter.com/6S105zYjbJ

“LA County Department of Public Health tells me that the mask-less Emmys were not in violation of the county’s mask mandate because “exceptions are made for film, television, and music productions” since “additional safety modifications” are made for such events,” tweeted CNN’s Oliver Darcy.

So apparently, so long as you’re making a television production, COVID-19 recognizes that fact and doesn’t show up for the night, much like it disappears as soon as people sit down to eat at a restaurant, but not while they walk to the table.

Health authorities went further, insisting that the event organizers “exceeded the baseline requirements for television and film productions,” before asserting that the full vaccination of all those present was “one of the most powerful ways to achieve a safe environment” (despite the fully vaccinated being able to pass on the virus).

“The Emmy Award Show is a television production and persons appearing on the show are considered performers,” they added.

So apparently, if you’re a “performer,” or in other words rich and famous, you don’t have to wear a mask.

But if you’re merely a lowly worker drone, you still have to wear a mask, as dozens of staffers were seen doing at the event.

Makes perfect sense.

Meanwhile, San Francisco Mayor London Breed responded to criticism of her not wearing a mask inside a club by saying the “fun police” were making a story out of nothing.