Finance professionals are well aware that when it comes to research, Wall Street has two sets of books: one set, that produced by the official sellside Research division, tends to be perpetually cheerful and is meant to encourage commission-boosting risk-taking among the broader client group; and since this is the research that immediately leaks to the financial media and thus the broader public, it serves to bolster optimism in capital markets and encourage a continuation of a market-levitating status quo. An example of this is Goldman’s David Kostin announcing last Thursday that he is hiking his year-end price target for the S&P500 from 4,300 to 4,700 primarily on lower Treasury yields. While there was little discussion about why lower yields which paradoxically signify a slowing economy and lack of reflation should be bullish for markets, that doesn’t really matter – what matters is that market upside has received a Goldman stamp of approval, and now the rest of Wall Street’s client-facing researchers will scramble to imitate Goldman with their own optimistic upgrades of where “they” think the market will close the year.

But is that what Goldman really thinks?

For the answer of what any bank – be it Goldman or anyone else – believes will happen, one has to step away from the research desk which is manned by bankers whose pay is not determined by whether they are right or wrong, but whether they produce enough convincing work product to validate the prevailing market narrative (in the current case bullish) and also facilitating client meetings with management teams, which is also why most ratings on Wall Street are “Buy” – few CEOs will meet with clients of a bank that just slapped a “Strong Sell” rating on their stock.

As a result, the truth often lies with the unofficial research created by a bank’s Sales and Trading division, which is far more difficult to come by – in fact it usually is not even included in a bank’s client blasts, one can’t directly subscribe to it – and is proprietary to specific traders from either the Flow or Prop desks where it is shared on a direct email basis with a very small subset of generous clients, usually those whose soft dollar commissions surpass a given threshold. Furthermore, since these reports – and their authors – are judged and compensated on the feedback from their clients, and in many cases their own direct P&Ls, the analysis is usually far much more accurate because unlike regular research, if traders are wrong one too many times, they can not only lose their bonus if clients complain, but can also lose their job.

To get a sense of just how different official research is from S&T reports, below we have grabbed the latest note from Goldman’s Tony Pasquariello, head of hedge fund sales at the bank. We urge readers to first skim the summary of Kostin’s hyperbullish market upgrade which we published last week, which sees nothing but smooth sailing in the second half, and compare it to the note below which is far more somber and while admitting the bubble nature of the market, anticipates turbulence once the taper is announced, perhaps as soon as this month’s Jackson Hole meeting: “S&P is trading at P/E levels only seen in the tech bubble … and US Financial Conditions have never been easier … so, yes, the ante will be upped when taper begins.” Furthermore, retail euphoria is a stark reminder that we are in another dot com era: “the US retail investor is long and involved in a way that’s very distinct from the pre-2020 bull market … and, we’ve lived in an era of investor euphoria that’s pushed the multiple up to demanding levels.“

Perhaps most notably, his concern that the “current policy setting” may lead to ruins, but – well – one should never fight central banks, right: “while the current monetary approach may ultimately constitute an inappropriate policy setting, it’s been another year where you’ve been paid to just go with global central banks.”

So without further ado, here is the latest client note from Goldman’s Tony Pasquariello:

Markets/Macro

While preparing for a trip earlier this week1, I dug through some old notes in a markets folder2. Here are a handful of one-liners that stuck out, with a stab at the application to the present day:

i. “as a wise macro manager once said, it’s usually 3-4 big trades a year that drive 90% of your returns” ⇒ Q1 offered a very high quality opportunity set that’s hugely waned; that said, if the US labor market steams ahead, I’m relatively optimistic the back end of the year will offer a few more pitches to hit.

ii. “every macro process begins with a liquidity framework” ⇒ while the current monetary approach may ultimately constitute an inappropriate policy setting, it’s been another year where you’ve been paid to just go with global central banks.

iii. “equities don’t suddenly break because of over-valuation, they typically break when liquidity is tightened” ⇒ S&P is trading at P/E levels only seen in the tech bubble … and US Financial Conditions have never been easier … so, yes, the ante will be upped when taper begins.

iv. “the rally in equities is constantly in question; e.g. at 1250 in S&P, there was no workout in Europe — Greece was going to default and there wasn’t enough capital in the European banking system to withstand it” ⇒ easier said than done, I know.

v. “certain years and certain cycles favor trading over investing, in others it’s the photographic negative” ⇒ in macro, 2021 has clearly favored aggressive trading; in micro, it’s been a mixed bag (investing at the index level, trading at the sector/factor level).

- footnote 1: what stuck out when meeting with corporate clients was enormous focus on two topics: China (most every mention was shot through with some degree of negativity) and ongoing labor challenges (the difficulty of hiring, the friction of RTO and the persistence of COVID).

- footnote 2: one of the journals I re-read was from 2016. it was striking how, eight full years on from the GFC, there was still so much scar tissue in the market narrative (as distinct from the investor euphoria that’s characterized the past 12 months).

Market Direction:

With respect to supply/demand and sentiment:

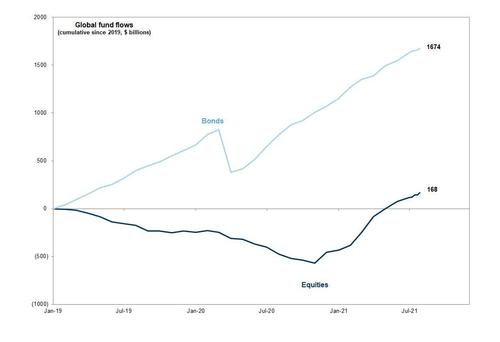

- i. the bullish read: retail activity is off the boil from Q1, but it’s still a story of net demand (see chart 12 below) … corporate technicals are very healthy (all-time high in M&A, $727bn of expected buyback executions and $546bn of dividends from S&P) … there’s still a huge amount of cash sloshing around the global financial system (that’s a clunky statement, but I think you can detect it everywhere) … the put/call ratio on S&P is around all-time highs … and various measures of investor sentiment are surprisingly well balanced (be it Goldman Investment Research or CNN fear/greed).

- ii. the less bullish read: don’t miss the point, following a period of record demand, the US retail investor is long and involved in a way that’s very distinct from the pre-2020 bull market … and, we’ve lived in an era of investor euphoria that’s pushed the multiple up to demanding levels.

Bigger picture, my simple macro process for equities always starts with (1) the trajectory of growth and (2) financial conditions. In an outright sense, current readings are superb (Q3 should market the apex of global economic output, and the GS Financial Conditions Index has never been more accommodative) … While in a comparative sense, the rate of change / second derivative of both factors will almost certainly be less impressive from here.

At the risk of boring you with the same conclusion, I still think that’s a good enough underpinning for US equities — while admitting that the path for S&P from here is more likely to be a grind than a gap (and, that the overriding theme of macro trading is more likely to be “pro-cyclical” than full-throated “reflation”).

I’ll conclude with a reference to point 9 below, which vividly illustrates just how strong the building blocks of shareholder returns are today.

* * *

Quick points, charts:

1. Calibrating China: the amount of ink devoted to China right now is very significant. A few takes:

- i. again, to this point in the game, global equity markets have notably compartmentalized this variable. I’m not speaking of just S&P — the durability of other Asian markets, and EM in general, is a historical aberration: link.

- ii. in a way, that’s a bit reminiscent of the 1990s wedge … I’m not suggesting it will be anywhere close to this magnitude, but note NKY dropped 50% in the decade … whilst S&P ripped 430%.

- iii. should the news flow continue, it’s reasonable to think the repatriation of capital out of the Chinets could be large and sustained. I think it’s worth remembering that — outside of US mega cap tech — the Chinese ADRs felt like one of the only games in town circa ’09-19.

2. Speaking of Japan: despite the Olympics, the domestic equity market is remarkably off the radar of global investors. while admitting my soft spot for Japan-style trading rallies, note the GDP sequencing: Q1 -3.9% … Q2 +0.3% … Q3E +4.0% … Q4E +8.4% (that last estimate is well above consensus). My point here is I can see NKY lining up as great risk/reward again down the stretch should the pro-cyclical narrative reassert itself.

3. Rates: As a colleague put it, 1.25% on 10yr note yields is purgatory for the directional crowd. that said, again viewed through the prism of a stock operator, the ongoing push lower in real yields — both in the US and Europe — is an ongoing tailwind for risk in general, particularly the long duration plays (and, not just tech stocks, I continue to be drawn to healthcare).

4. Infrastructure: given the long runway here, in isolation I don’t think this is a story to plan your risk around, but on the margin our house view for infrastructure stuck me as decently positive: “overall, we continue to expect Congress to approve around $3 trillion over 10 years in additional spending, consisting of around $500bn from the bipartisan infrastructure bill and another $2.5 trillion from a budget reconciliation bill” (link).

5. This benchmark note on the future of work is worth a trip to the printer: For example: in surveying 50k full-time US and 15k UK workers, 20% of people don’t want to work from home at all post-pandemic, while 30% want to work from home five days a week. the remaining 50% of workers are fairly evenly spread between wanting to work one to four days a week at home. so, the biggest groups want either zero — or five days — in the office.

6. I thought this quote applies to many people in our trade: Novak Djokovic said in an interview with the Financial Times that “I can carry on playing at this level because … I like hitting the tennis ball.”

7. While on the topic of being good at your craft, h/t to one Dr. Sancheti, who is retiring after performing more than 55,000 surgeries in his career: link.

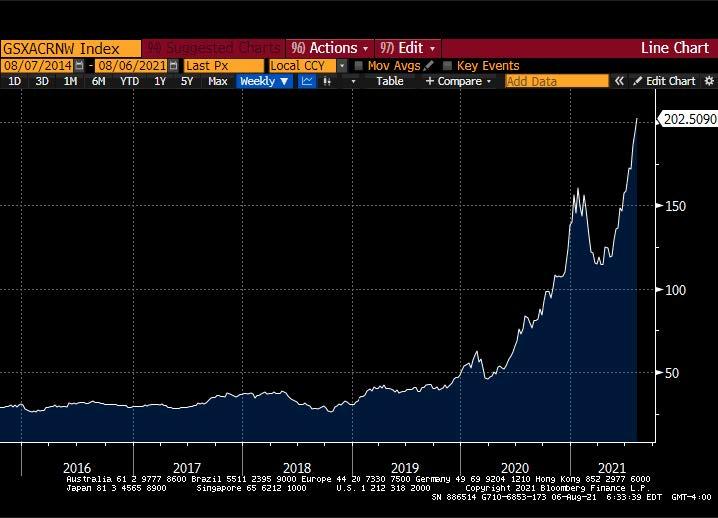

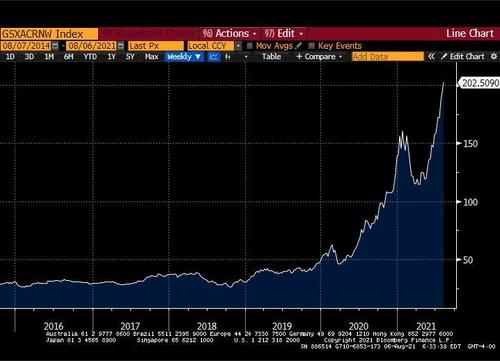

8. Yes, China is mired in a serious bear market. yet, amidst the breakdown, witness the explosive breakout in our China renewables / clean energy basket (you’ll see similar strength in the China innovation basket, ticker GSXACINO). this is also an interesting compare/ contrast with the US, where the domestic renewables basket (GSXURNEW) is 20% off the February highs with S&P ripping:

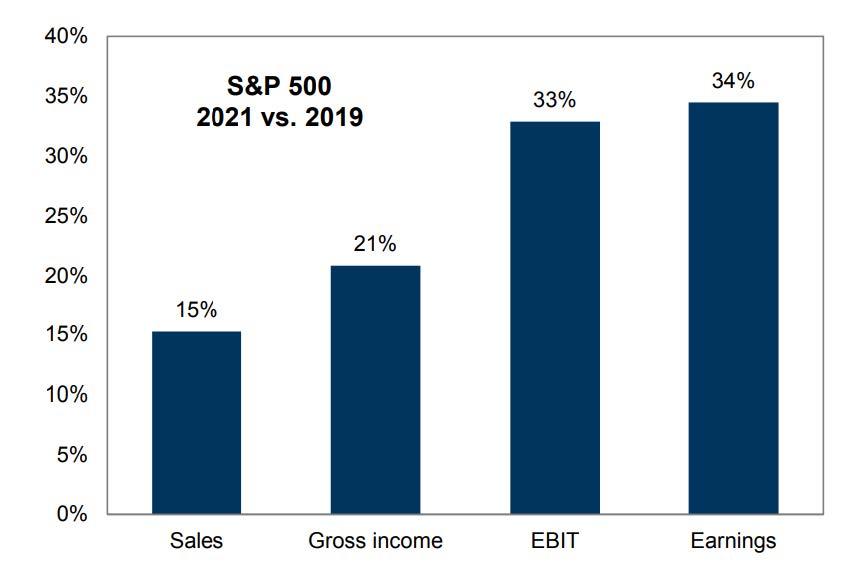

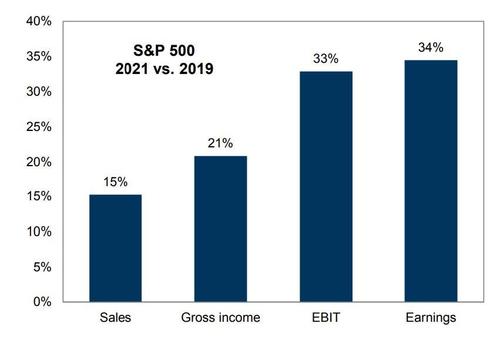

9. US Portfolio Strategy made notable upward revisions to our S&P price targets: YE’21 to 4700 (from 4300) and YE’22 to 4900 (from 4600). within that forecast, our new earnings estimates represent upward revisions of $14 for 2021 and $10 for 2022, reflecting expectations of stronger top-line growth and profit margin expansion. as you can see here, compared to the pre-pandemic levels of 2019, sales, income, EBIT and earnings should be up very meaningfully in 2021.

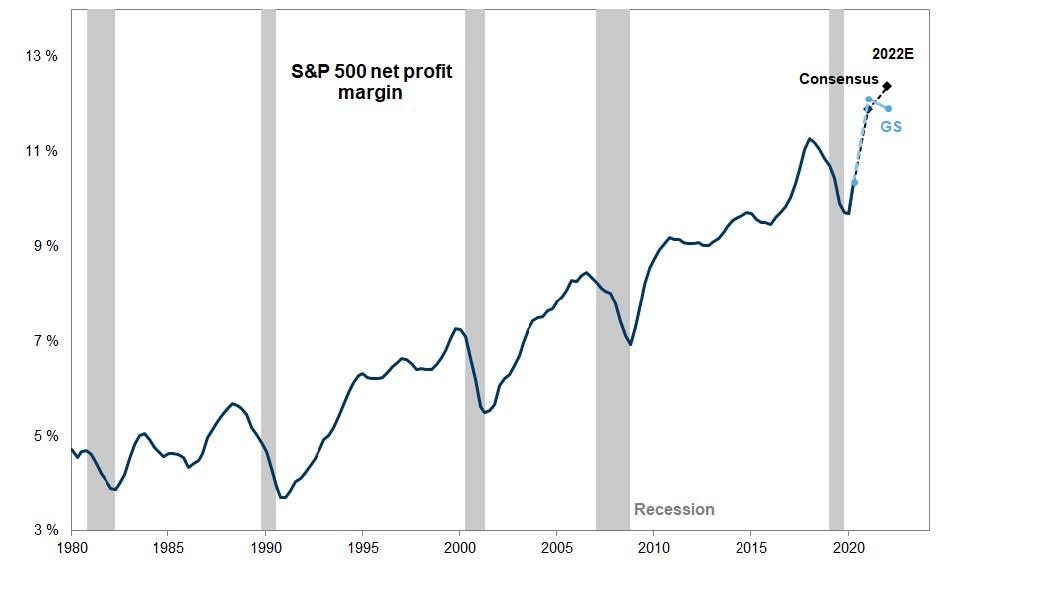

10. While increasingly viewed with ambivalence, the past three decades have seen a remarkable expansion in US corporate profit margins. as you can see here, while margins should make a fresh push to higher highs, in the forward our US Portfolio Strategy team is a bit less bullish than consensus, though this is largely because they assume a version of tax reform is passed by year-end and becomes effective next year (credit to Cormac Conners):

11. Yes, it’s been a huge year for new issues. that said, again as a % of equity market cap, it’s really not so wild:

12. Yes, a tremendous amount of money has flowed into global equities over the past few years. At the same time, demand for Fixed Income remains utterly huge (credit to sales & trading collegue Scott Rubner):