PG&E Pleads Guilty To 84 Counts Of Manslaughter Tied To Deadliest Wildfire In California History Tyler Durden

Tue, 06/16/2020 – 15:04

In a landmark development that marks a victory for California citizens trying to hold the state’s largest and most politically influential utility accountable, PG&E pleaded guilty to 84 felony counts of involuntary manslaughter on Tuesday afternoon. The guilty plea marks the end of an investigation into the origins of the Camp Fire, the deadliest and most destructive in California history.

Roughly 18 months ago, we reported on the surreal scenes coming out of the town of Paradise, California, which was swiftly swallowed up by flames as the NorCal ‘Camp’ Fire. That fire eventually became the deadliest wildfire in the state’s history, killing at least 84, including dozens of Paradise residents who failed to flee in time.

An investigation eventually found that PG&E inadvertently started the fire when a transmission line broke from a nearly-100-year-old Pacific Gas & Electric Tower after years of neglect.

In a rare acknowledgment of corporate wrongdoing, PG&E on Tuesday pleaded guilty to 84 counts of involuntary manslaughter for its negligence, ending a two-year ordeal for the families of victims like Ms. Wehe and survivors of the fire, which destroyed the town of Paradise.

PG&E, which had repeatedly failed to maintain the line even though it cut through a forested and mountainous area known to experience strong winds, also pleaded guilty to one count of illegally setting a fire.

In addition to the guilty plea, the California Public Utilities Commission separately fined PG&E almost $2 billion for its negligence in causing the wildfire. What’s more, the company could face additional penalties because its guilty plea represents a violation of a federal probation order placed on the company from a 2010 transformer explosion which started a fire that killed 8 people. The federal judge, William H. Alsup, has the power to impose new penalties on the company for violating its probation, according to the NYT.

As it exits bankruptcy, the company has agreed to pay $13.5 billion to settle claims related to the wildfires (it initially declared bankruptcy last January to try and avoid getting whacked with a massive judgment in the ballpark of $30 billion (or at least that’s what the company feared at the time).

About half of that number will be paid in the form of company stock, leaving roughly 70,000 wildfire victims owning a little more than 22% of the utility once it leaves bankruptcy.

And so ends another saga of corporate malfeasance and abuse.

via ZeroHedge News https://ift.tt/2N2N8Z5 Tyler Durden

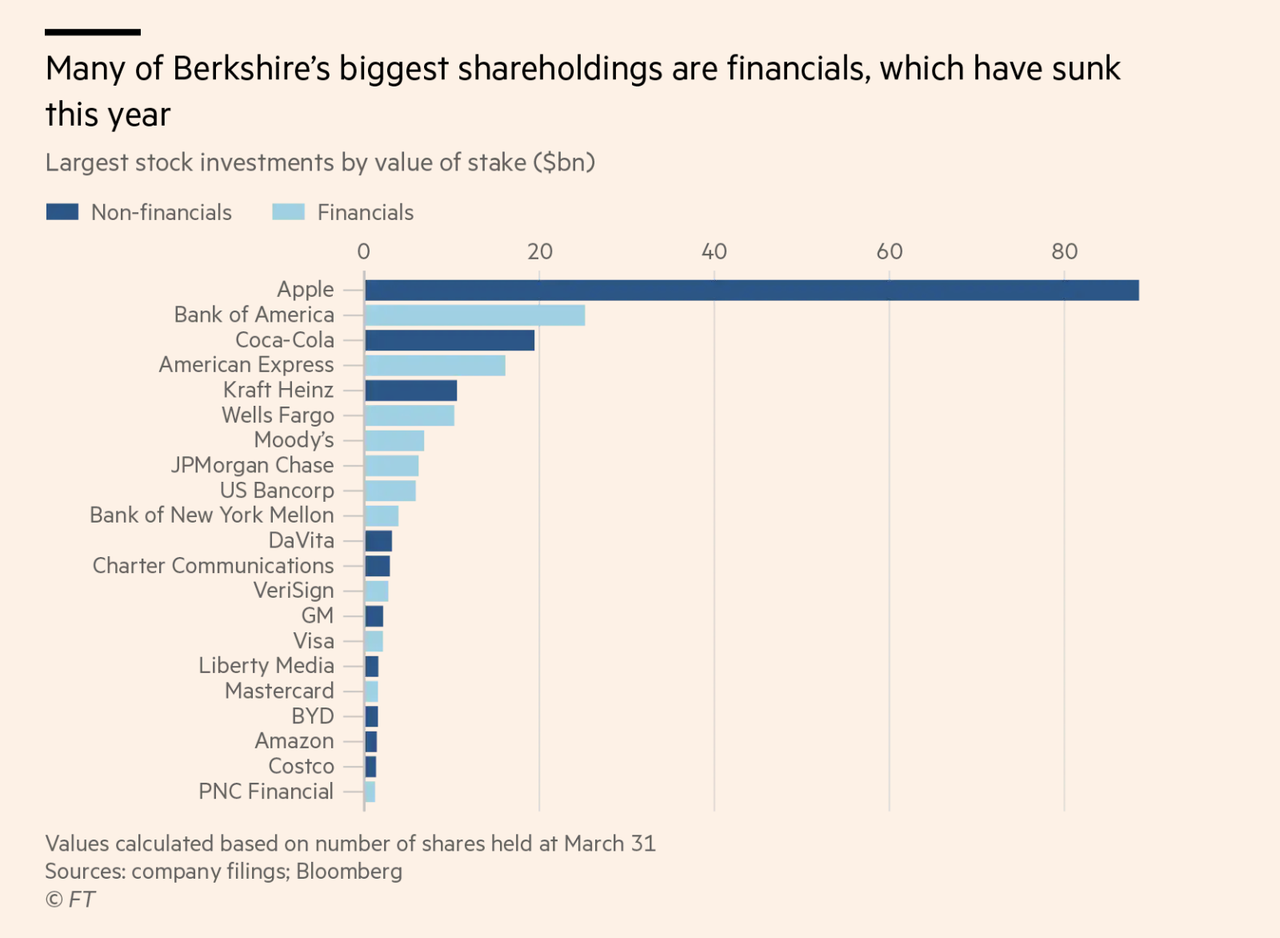

Is The Media Turning On Warren Buffett? Tyler Durden

Tue, 06/16/2020 – 14:50

He’s been the “Omaha of Oracle” since before most of the reporters who cover him were born. But after an unmissable series of missteps, is the financial media finally starting to turn on Wall Street’s favorite billionaire?

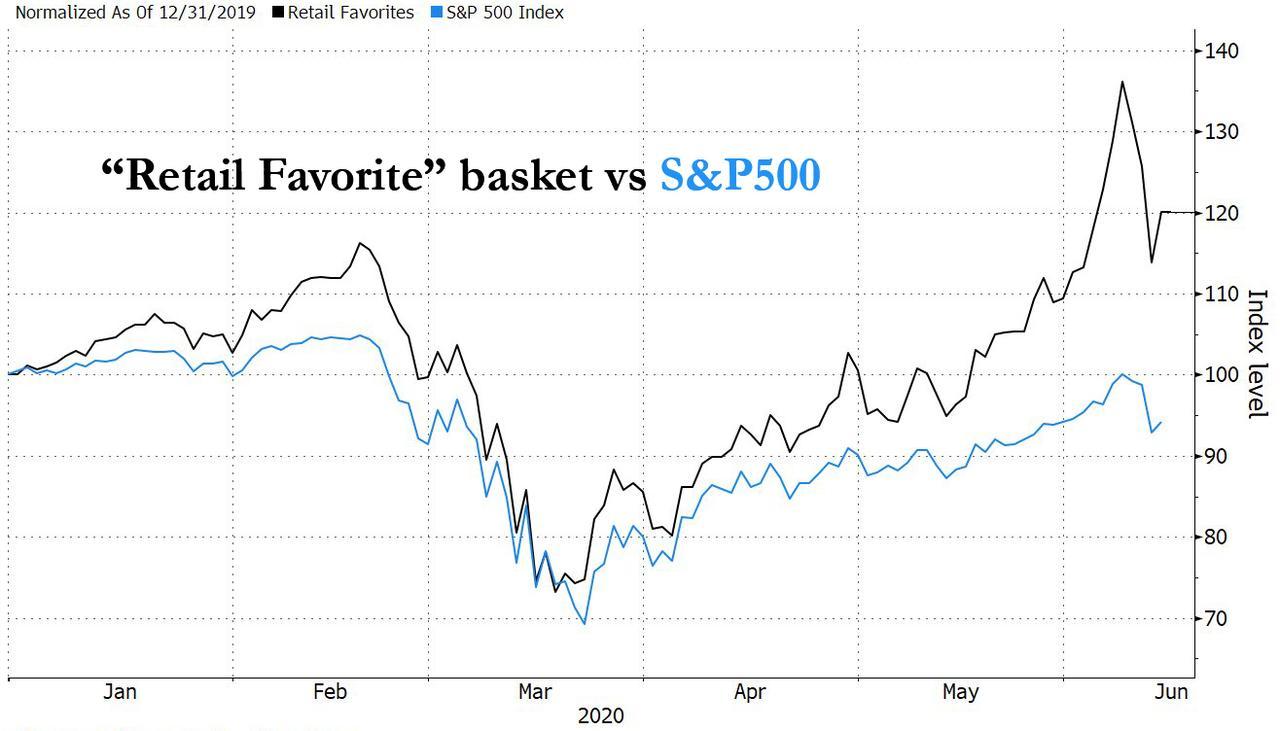

All those ‘serious’ financial journalists who dismissed Dave Portnoy’s torrid affair with day trading as a novelty and/or fad are definitely paying attention now. After Portnoy set the investing community aflutter by proclaiming Warren Buffett a washed-up has-been, the Financial Times has followed up with a piece exploring these theme in greater depth.

More recently, Wall Street analysts who cover the company have started to wonder: Did Berkshire sit out the entire rally?

“I am nervous that he may have missed this whole rally,” said James Shanahan, an analyst with Edward Jones. “If the rally started in late March and he was a net seller in April, it seems like…he missed it all. That’s frustrating. A lot of retail investors were ploughing money into the market and doing better than professional investors. I think you can include Buffett in that.”

If so, Berkshire can probably abandon its hopes of beating the S&P 500 in 2020, after missing the mark in 2018 and 2019 as well. The fact that Buffett, who built his reputation on his keenness for buying companies and stocks during down markets, sat out the drop is enough to question whether his financial genius is still relevant in a world where technology stocks – which Buffett had long shunned before his romance with Apple (which isn’t even a tech stock, according to Buffett) – are king. The Fed’s response ensures interest rates will be mired near zero for years to come. How can one possibly justify keeping so much dry powder on hand, unless one believes, like Gundlach, that the market is going lower, something that seems out of step with Buffett’s perennial bullishness.

Earlier this year, Buffett proclaimed his belief in banking stocks, and skepticism of tech, only for tech to outperform once again, while banking stocks have continued to flounder.

Even Buffett acolyte Bill Ackman dumped his Berkshire stake last month. He later argued in a letter to his investors that Pershing Square was “more nimble” than Berkshire. He essentially told his investors that if Buffett won’t use Berkshire’s cash pile to make investments on shareholders’ behalf, shareholders are going to take their capital elsewhere.

As of end Q1, 30% of Berkshire’s equity portfolio consisted of financials.

In other words, maybe the eponymous founder of Davy Day Trader Global is right: Maybe Buffett really is “washed up”.

Berkshire Hathaway shareholders have more to worry about than Buffett’s skill at playing the public markets. Another sell-side analyst quoted by the FT pointed out that Berkshire’s purchases of major stakes in Kraft Hines (a deal which it helped arranged with Brazil’s 3G Capital) and Occidental may have permanently stained the conglomerate’s reputation.

Berkshire’s “chronic underperformance” requires answers, according to Cathy Seifert, an analyst who covers the company at CFRA Research, particularly in light of some questionable investment decisions in recent years.

The company had written down its holding in food producer Kraft Heinz by $3bn last year, she pointed out, while Mr Buffett’s $10bn investment in oil producer Occidental Petroleum was no longer paying a cash dividend and its stock warrants looked worthless now.

“Those two things, I believe, have really tarnished Berkshire’s reputation for dealmaking,” Ms Seifert said of the two investments. The Occidental deal “was an unmitigated disaster”. On top of this, Mr Buffett increased his shareholdings in America’s largest airlines at the start of the year before selling them at the peak of the coronavirus disruptions in April, crystallising a loss.

Unlike during the GFC, when hard-hit companies (this time around, the group included a preponderance of tech startups) needed to tap the market for emergency cash, they didn’t turn to Buffett; they turned to PE. That’s largely Buffett’s own doing: If you tell everybody who would listen that you don’t really invest in technology companies because you don’t understand them, don’t be surprised when those companies don’t approach you for an investment. But also, Buffett’s ignorance of what some call the “New Economy” – particularly his reluctance to embrace Amazon – is causing some longtime shareholders to seriously question whether Berkshire is primed to succeed in the 21st Century.

Some investors say Mr Buffett must find a way to reconcile his value investing philosophy with what in the dotcom era was called the new economy — which is no longer new. “If Berkshire is to have the prospects of generating the value it has in the past, it has to adapt by buying these companies that will generate significant value over the next 25 years,” said Christopher Rossbach, chief investment officer of J Stern & Co. J Stern manages money for the Stern family, which has held Berkshire shares for decades, as well other investors. “Both Warren and Charlie [Munger, Berkshire’s vice-chairman] have acknowledged that they have missed Amazon and that they should be looking at these companies but they have also said they don’t understand them,” Mr Rossbach said. “They have kept them in the box that Warren has on his desk that says ‘Too hard’. What will it take for them to take these stocks out of the box?”

One of the nice things about finance is that, for all one’s bluster, the proof is always in the pudding. Legendary investors can’t simply rest on their laurels. In finance, if you’re not winning, you’re losing. Buffett dumped airline stocks at a loss, and a million Robinhood traders scooped them up, nearly doubling their money in the span of a few weeks.

Have the times changed too quickly for Berkshire to keep up? Or have Buffett and Munger, by steadfastly resisting change, allowed the conglomerate to lose its sense of relevancy. Either way, the FT’s reporting staff has surely noticed by now that Benjamin Graham’s principles of prudence and responsibility don’t really fit with the millennial investing aesthetic.

Don’t understand? Just take a look at r/WallStreetBets?

via ZeroHedge News https://ift.tt/2YJy8EP Tyler Durden

Pumping up the stock market – supporting corporate bonds will do that – while Main Street suffers is a recipe for sweeping changes to come in the Federal Reserve Act.

We have no doubt a People’s Quantitative Easing (QE) is coming. We had a small taste of it during the COVID crisis response That is a direct credit by the Federal Reserve into individual checking accounts.

Not that we oppose it in political spirit but the economics will be a disaster over the long-term. We can think of much better ways to deal with America’s income and wealth distribution problem but we are already gone down that rabbit hole.

The United States is on the fast track to a Japanese style zombie economy, where the Nikkei 225 is still 45 percent below its December 1989 high, even after massive fiscal stimulus and quantitative easing, which includes direct equity purchases by the central bank. Japan is also a net saver and the U.S. is not.

John Authors of Bloomberg pretty much nails it on today’s Fed announcement,

India Confirms 20 Soldiers Killed In Border Clash With Chinese Forces; Reports Of 43 PLA Casualties Tyler Durden

Tue, 06/16/2020 – 14:19

Earlier in the day we reported that Indian Army officials said that three troops – an officer and two soldiers, to be more precise – had been gunned down by Chinese forces during a “violent faceoff” in Galwan Valley in the Ladakh region Monday night.

In an official follow-up statement, the Indian Army now says as of Tuesday evening local time thatan additional seventeen soldiers were critically injured in the exchange of fire, and since succumbed to their wounds after being “exposed to sub-zero temperatures in the high altitude terrain.” This brings the official Indian death toll to 20 soldiers killed.

With the whole incident still shrouded in contradictory claims and lack of confirmation on potential Chinese casualties from Beijing – even after widespread unverified Indian media reports claimed that up to 43 Chinese People’s Liberation Army (PLA) were killed or injured in the clashes, one thing is for sure — that this is the biggest and deadliest border clash between the nuclear-armed neighbors in a half-century.

India-China Ladakh, Indian media file image.

The only thing approaching an ‘official’ statement from Beijing appears to come via state media. The highly visible editor of state-run Global TimesHu Xijin, who’s often served as unofficial mouthpiece conveying Beijing official sentiment to the West tweeted the following in the aftermath Tuesday, calling it “goodwill from Beijing”:

The Chinese side didn’t release number of PLA casualties in clash with Indian soldiers. My understanding is the Chinese side doesn’t want people of the two countries to compare the casualties number so to avoid stoking public mood.

Importantly, Xijin confirmed that there were indeed casualties on the Chinese side.

Chinese side didn’t release number of PLA casualties in clash with Indian soldiers. My understanding is the Chinese side doesn’t want people of the two countries to compare the casualties number so to avoid stoking public mood. This is goodwill from Beijing.

He stated further: “Based on what I know, Chinese side also suffered casualties in the Galwan Valley physical clash,” in a follow-up tweet.

“I want to tell the Indian side, don’t be arrogant and misread China’s restraint as being weak. China doesn’t want to have a clash with India, but we don’t fear it,” the GT editor added.

It added that “17 Indian troops who were critically injured in the line of duty” and died from their injuries, taking the “total that were killed in action to 20”.

China did not confirm any casualties, but accused India in turn of crossing the border onto the Chinese side.

Chinese foreign ministry spokesman Zhao Lijian said India had crossed the border twice on Monday, “provoking and attacking Chinese personnel, resulting in serious physical confrontation between border forces on the two sides”, AFP news agency reported.

India blamed Beijing for “an attempt by the Chinese side to unilaterally change the status quo” on the border, according to Indian media.

With tensions this high, and no doubt the national medias of each country about to spend days whipping their citizens into a frenzy, there’s likely more to come along the restive and disputed Line of Control (LOC).

We should add that strangely, the Indian army is still claiming as of Tuesday that “no shots were fired” in this latest major clash.

This is of course a not so insignificant detail which has left many observers scratching their heads, but then again, border skirmishes between the two have been known to involve stones, sticks, and fist-fights. Given the high casualty count, gunfire is most likely, or perhaps they fought with bayonets?

via ZeroHedge News https://ift.tt/3fp2vXI Tyler Durden

The Insanity Window Closes: Robinhooders Are Finally Dumping Hertz Stock Tyler Durden

Tue, 06/16/2020 – 14:00

In what is arguably the financial story of the year, late on Friday insolvent Hertz got bankruptcy court approval to sell as much as $1 billion (a number since reduced to $500 million) in stock, targeting the manic retail buyers who had pushed its stock just a week earlier above $6/share. In response, Hertz’ corporate lawyer Tom Lauria, who admitted that the stock is “disconnected from fundamentals”, said that the company immediately start selling the bankrupt shares from its existing shelf “because once the bid disappears, this historic opportunity will be gone too.”

Well, the bid is almost gone (maybe it was the company’s warning that equity holders will most likely be wiped out that caused the dam to finally break).

Not only has Hertz failed to sustain any rally in the past two days, when Hertz started selling stock..

… but in an ominous development for Hertz and potentially other (soon to be) bankrupt company such as Chesapeake which may seek to repeat Hertz’ historic achievement of flipping the bankruptcy process on its head, and whose own Chapter 11 filing is imminent, it appears that Robinhooders have finally googled what “bankruptcy” means, and in the past two days there has finally been the first sustained, if modest decline in Hertz holders on Robinhood.

The problem for Robinhood is that the momentum is now broken (and this without the SEC even daring to chime in on what will end up being catastrophic losses for ordinary investors) and once the daytrader army realizes that the chance for higher highs, and even greater fools is gone, we expect that the number of users holdings the stock will plummet in the next few days, effectively shutting the window for any further Hertz stock sales.

The question then becomes just how much new Hertz stock has been sold by the company to the retail hordes – we expect an update from Jefferies in the next 24 hours – and when do the lawsuits start once the Millennials who have bought the stock in hopes of overnight riches realize they are facing a total wipeout.

via ZeroHedge News https://ift.tt/2YIzOye Tyler Durden

Holdings in gold-backed ETFs charted another all-time high in May as inflows in dollar-terms have already set a yearly record just five months into 2020.

Globally, funds added another 154 tons of gold to their holdings boosting the total to a record 3,510 tons, according to the latest data released by the World Gold Council.

Over the past 12 months, assets in global gold-backed ETFs have nearly doubled.

In dollar-terms, year-to-date inflows of $33.7 billion have already exceeded the previous high seen back in 2016.

Another month of positive inflows in May, coupled with the rising price of gold, also pushed assets under management (AUM) in gold ETFs to a new record high of $195 billion.

North American firms led regional inflows for the second straight month and hit all-time highs in May. Funds based in North America increased holdings by 102 tons. North American funds now hold 1,815 tons of the yellow metal, surpassing the previous highs of 1,736 tons charted in December 2012.

European funds saw inflows of 45 tons. UK-based funds led the way, accounting for about 65% of the regional total for the month.

Asian funds – primarily those based in China – added to their holdings as well, with inflows of 4.8 tons.

Funds in other regions, including Australia, added 2.6 tons of gold to their holdings.

The World Gold Council listed four factors helping drive the flow of gold into ETFs.

The economic and social impact of COVID-19, as most economies remain shut down or are slowly reopening.

Tensions between the US and China continue to escalate.

Labour markets are facing challenges not seen in generations. In the US, the unemployment rate is already at 14% and may soon reach levels last during the Great Depression of the 1930s.

Monetary policy intervention is expanding into asset classes that would have seemed incredibly unlikely even a few months ago, such as high yield (junk) bond ETFs in the US. This has helped push bond yields even lower, reducing gold’s opportunity cost further and adding to market uncertainty as we are in unchartered waters.

Gold was up 2.6% in dollar terms in May. Price volatility was also lower.

At the time of publication, gold has outperformed most major asset classes this year, up by more than 15%. Gold’s performance continues to distinguish itself from the wider commodity spectrum, as broader commodity indices are down 22% – 30% this year and oil (WTI) is down by more than 40%.”

Inflows of gold into ETFs are significant in their effect on the world gold market, pushing overall demand higher.

ETFs are backed by physical gold held by the issuer and are traded on the market like stocks. They allow investors to play gold without having to buy full ounces of gold at spot price. Since their purchase is just a number in a computer, they can trade their investment into another stock or cash pretty much whenever they want, even multiple times on the same day. Many speculative investors appreciate this liquidity.

There are good reasons to invest in ETFs, but they aren’t a substitute for owning physical metal. In an overall investment strategy, SchiffGold recommends buying gold bullion first.

When considering gold-backed ETFs, you should always keep in mind that you don’t actually own the gold. Buying the most common ETFs does not entitle you to any actual amount of the precious metal.

The Fed’s $250 Billion Debt-Buying “Index” Loophole Tyler Durden

Tue, 06/16/2020 – 13:20

In the aftermath of yesterday’s announcement by the Fed that the central bank is starting to buy corporate bonds (not ETFs), something it had said it would do three months ago yet which either the algos or the Robinhooders never quite grasped and which sent stocks soaring even though it wasn’t actual news, some have asked what exactly was the purpose of the Fed’s market-moving press release. As it turns out, there was a very strategic purspose for the Fed to do what it just did, and it involves around the just announced Broad Market Index, which effectively grants the Fed a $250 billion monetization loophole.

BMO’s Daniel Krieter explains below.

What did the Fed do? Initially, the SMCCF was structured to hold two types of investments, “Eligible Individual Corporate Bonds” and “Eligible ETFs”. Yesterday, the Fed introduced a third category: “Eligible Broad Market Index Bonds”. This new category allows the Fed to immediately begin buying individual corporate bonds in much larger volume than previously anticipated. However, while the creation of this category came as a surprise, the announcement that the Fed would buy individual corporate bonds initially came in March.

What are Eligible Broad Market Index Bonds? Bonds that are included in the Fed’s newly created Broad Market Index. These are corporate bonds that, at the time of purchase, (i) are issued by an issuer that is created or organized in the United States or under the laws of the United States; (ii) are issued by an issuer that meets the rating requirements for eligible individual corporate bonds; (iii) are issued by an issuer that is not an insured depository institution, depository institution holding company, or subsidiary of a depository institution holding company, as such terms are defined in the Dodd-Frank Act; and (iv) have a remaining maturity of 5 years or less.

What is the difference between Eligible Individual Corporate Bonds and Eligible Broad Market Index Bonds? Very little. In addition to the requirements for Eligible Broad Market Index Bonds, Eligible Individual Corporate Bonds must also be issued by a company: 1) with “significant operations and a majority of its employees based in the United States,” 2) that has not received specific support under the CARES Act; and 3) satisfies the conflict of interests requirement in the CARES Act. Thus, Eligible Individual Corporate Bonds must meet a stricter set of criteria for purchase by the Fed.

Why is this important? The SMCCF is funded with money from Treasury authorized by the CARES Act, and therefore comes with restrictions. As stated in Section 4003(c)(3)(c) of the CARES Act, any Fed facility to which Treasury makes a contribution shall only purchase obligations or other interests (other than securities that are based on an index or that are based on a diversified pool of securities) from…[businesses] that have significant operations in and a majority of its employees based in the United States.”

The requirement that businesses have significant U.S. operations and a majority of its employees in the U.S. proved problematic for the Fed since the only way the central bank could realistically adhere to this was by having individual corporations certify their compliance with these prerequisites. Having a large percentage of hundreds of American corporations certify compliance was very difficult from an operational standpoint to begin with, and became even more so when certification potentially became stigmatized after credit spreads rallied so significantly. Without certification, the Fed was potentially left with a huge liquidity facility that wasn’t allowed to buy anything but ETFs.

How did the Fed get around certification? By identifying a loophole. Section 4003(c)(3)(c) requires purchases of only companies with “significant operations in and a majority of its employees based in the Untied States” unless the purchases are (emphasis ours) “securities based on an index or that are based on a diversified pool of securities.” This clause was likely included to allow the Fed to buy ETFs. Instead, the Fed created its own index of corporate bonds, the “Broad Market Index,” and will now purchase individual corporate bonds based on this index under this clause. In one swift stroke, the Fed essentially made the entire universe of non-financial corporate debt under five years immediately eligible for purchase.

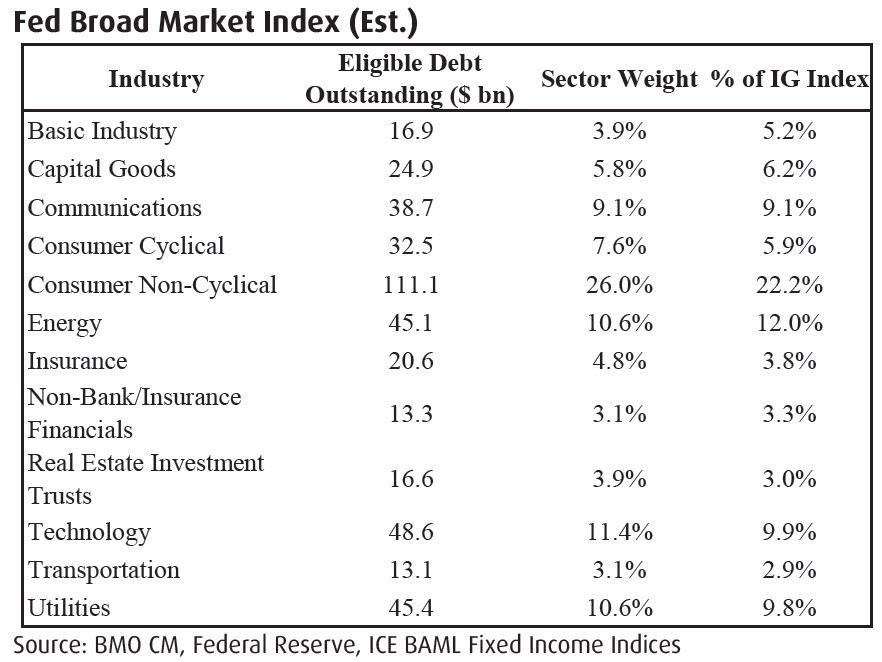

How will purchases work mechanically? The Broad Market Index is intended to track the composition of the broad, diversified universe of secondary market bonds that meet the criteria specified in the Term Sheet for Eligible Broad Market Index Bonds, subject to generally applicable issuer-level caps specified by the Term Sheet. Each time the index is refreshed (approximately every month), the SMCCF will identify all secondary market bonds that meet the criteria for Eligible Broad Market Index Bonds. Next, limits relevant to each issuer, calculated on a par basis as the lesser of the cap of 10% of an issuer’s maximum historical outstanding bonds and 1.5% of the maximum combined CCF facility size, will be applied to generate the index contribution for each eligible issuer. These contributions will then be aggregated, and the proportion of each issuer’s bonds in the aggregate form their weight in the index. Individual issuer weights will form the basis of sector weights, with each issuer mapped to one of twelve sectors (shown below). Purchases will track as closely as possible the sector weights in the index, and any overage or shortfall during a month will be addressed in the following month’s purchases.

It will not be possible for the SMCCF’s purchases to exactly replicate the index at all times. As a result, the primary focus of the SMCCF’s Eligible Broad Market Index Bond purchases will be to track as closely as possible the sectoral weights of the index. Eligible Broad Market Index Bond purchases will also generally track the ratings and maturity profile of the index. However, the maturity profile of the purchases is expected to be several months longer than the index’s maturity profile, as the SMCCF will likely underweight purchases of bonds maturing within six months of the date of purchase.

What are the estimated sector weights? We estimate the total size of the Fed’s Broad Market Index will initially be around $400-450 bn, with our proxy index having a face value of $426.9 bn and sector weights shown below.

Do any individual borrowers benefit from the Fed’s announcement? USD debt of corporations incorporated in the United States but without significant operations or a majority of its employees in the United States theoretically benefit. These bonds are now eligible for Fed purchase, but were originally expected to be excluded. In its FAQs, the Fed defines “significant operations in the U.S.” as a company with greater than 50% of its consolidated assets in, annual consolidated net income generated in, annual consolidated net operating revenues generated in, or annual consolidated operating expenses (excluding interest expense and any other expenses associated with debt service) generated in the United States as reflected in its most recent audited financial statements. However, in reality, we do not expect to see significant outperformace for this type of borrower. While difficult to quantify given difficulty in isolating borrowers that meet this criteria, we do not expect a significant discount ever developed for this type of borrower that would now be corrected.

How big will SMCCF purchases be? The total size of the program (up to $250 bn through Sept 30) gives the Fed plenty of room to ramp up purchases quite aggressively, although the Fed will leave purchases well below the implied maximum pace as long as market conditions remain constructive. As of last Wednesday, the Fed had purchased $5.5 bn in cumulative ETFs through just over four weeks.

We expect the pace will grow as the Fed begins to buy individual bonds, although it will remain dependent upon market functioning. To this point, conditions deteriorated significantly late last week, and this may have been a catalyst for yesterday’s announcement. In normal times, we expect the Fed to purchase around $2-5 bn each week with the potential to ramp up purchases to several times that amount.

Will the Fed still buy “Eligible Individual Corporate Bonds”? Yes. The Fed’s updated FAQs are very clear that the central bank still intends to buy eligible individual corporate bonds. A borrower would need to certify compliance with the significant operations and majority of employees prerequisites in order to be eligible. Upon certification, it appears that the Fed would then buy more secondary market debt of a certified borrower than they otherwise would, according to the Broad Market Index weights. Alongside the PMCCF, these purchases are “expected to become operational in the near future,” according to the Fed’s announcement yesterday.

How can the Fed provide further support to the market, if necessary, with the known corporate buying programs? It is unlikely that any further announcements regarding the PMCCF or SMCCF purchases of Eligible Individual Corporate Bonds result in incremental risk asset performance because these facilities are now truly emergency facilities. We can’t imagine any borrower certifying given associated stigma unless market conditions worsen materially. Therefore, the only thing the Fed can do to existing facilities now is increase/change their size limits. Currently, PMCCF capacity is $500 bn and SMCCF capacity is $250 bn for a total of $750 bn. With the expectation that the PMCCF will not likely get much utilization unless market conditions worsen materially, the Fed could reduce some of the PMCCF’s capacity and add it to the SMCCF. Or, they could increase the aggregate size of the programs.

via ZeroHedge News https://ift.tt/3d6Yupi Tyler Durden

President Trump Signs Executive Order On Police Reform Tyler Durden

Tue, 06/16/2020 – 13:07

In keeping with the Republican plan for tackling police reform, which involves a legislative component being handled by the Senate (an effort led by the only black senate Republican, SC’s Tim Scott), President Trump signed an executive order limiting the use of chokeholds by police across the country and require the creation of a federal database of police misconduct, among other measures.

The EO is part of what could become a spate of several orders as negotiations continue and lawmakers in both parties try to hammer out a compromise plan as Republicans bet that shifting public opinion on police misconduct could create space for a compromise.

According to Axios, the EO is intended to “send a message” to Congress that the president is willing to work with them, as he encouraged lawmakers to pass a compromise plan.

Trump said he had spoken privately with the families of victims of police violence, including Ahmaud Arbery, Botham Jean, Antwon Rose II, Jemel Roberson, Atatiana Jefferson, Michael Dean, Darius Tarver, Cameron Lamb and Everett Palmer, Jr (though notably Floyd’s family was not present).

“We have to find common ground. But I strongly oppose the radical and dangerous efforts to defend, dismantle and dissolve our police departments, especially now when we achieved the lowest recorded crime rates in recent history,” Trump said.

Under the order, police departments that meet certain standards on use of force will be eligible for federal grants, senior administration officials explained Tuesday during a call with reporters. Chokeholds must be banned to earn the certification. The order also moves to create a national registry to track officers with multiple excessive force complaints lodged against them.

The order also includes new programs that would help law enforcement officials to better deal with mental illness, homelessness, and addiction.

via ZeroHedge News https://ift.tt/2N38Bkv Tyler Durden

Last week, Lancet had to retract the most highly-touted hydroxychloroquine study to date, which was used as evidence for entire countries to change their stance on the drug. The study, which was obviously flawed on its face (I commented well before it was exposed that the groupings made no sense), turned out to be produced by a shell company, with unverified data gathered by non-scientists.

But when that study flopped, another study was immediately latched onto. It’s called the RECOVERY trials and was done in the UK. Supposedly, this study was the counter to the fake study published by Lancet.

It was the proof that “well yeah, that other study was bad, but this one got the same results.”

Well, not so much.

Edmund Fordham wrote a piece on what is an emerging controversy, in which it appears the lead of the RECOVERY trial took hydroxychloroquine for another drug, resulting in a high death rate.

Internet sleuths also got to work on the very heavy doses of the drug that were given – 2400 mg in the first 24 hours, a ‘dose fit for a gorilla’ as one critic had it. Quizzed about this, Landray defended the dosage, twice, as being usual for other diseases such as amoebic dysentery. Say again? Hydroxychloroquine is used for lupus and arthritis as well as malaria, but dysentery? As a footnote in medical history, the older chloroquine was used half a century ago in attempts to control dysentery, but Professor Christian Perronne, head of infectious diseases at Garches, France, told France Soir that it had been abandoned before 1976. Was Landray confusing hydroxychloroquine with the hydroxyquinolines, which are used for dysentery?

1,132 patients died in the RECOVERY trial, with general death rates nearly 10% higher than other country’s hospitals (the trial was randomized through Britain’s NHS). Whether giving people 3x the usual dosage of most other studies played a part is now a very real question.

Landray defended himself twice, but is now claiming he’s being misquoted. The French newspaper who quoted him denies that.

Landray explained there was no approved dosing for Covid because it was a new disease. Well, yes, but the toxic dose won’t change depending on the illness. Asked whether the UK had a maximum dose for hydroxychloroquine, Landray wasn’t sure, but opined it would be much larger, say six to ten times the trial’s dose. That makes 24 whole grams. NICE says about 490 mg per day for a 75kg adult. In France 1800 mg in a day mandates hospitalization as a poisoning. Twenty-four grams at one go would be almost certainly lethal, possibly even to a gorilla. So Landray has had notice of some hard questions on dose, which will no doubt be explained in the full report, not yet released.

In the end, though, this study is just another in a long list which completely miss the mark and it’s good that it was canceled. The effectiveness of hydroxychloroquine to fight coronavirus has always been in the early stages because of how the virus works. Doing trials on extremely sick, hospitalized patients is scientifically counterproductive because the viral infection itself is no longer the issue at that point. As the now-debunked Lancet published study counted in their data, giving hydroxychloroquine without adjacent drugs (anti-biotic and zinc) is pointless and using that data in “studies” to claim the drug doesn’t work at all is incredibly misleading. Why is that even being studied and included in any determination of its effectiveness?

Countries and doctors that report success with hydroxychloroquine already know not to give it to late-stage patients and that it’s ineffective when used alone. What they also know is that it does appear to have benefits for early-stage, non-hospitalized subjects when prescribed properly in conjunction with other drugs. Why is it so difficult for some to separate those things and focus on helping people?

The whole thing feels politicized at this point.

via ZeroHedge News https://ift.tt/37E0jsW Tyler Durden

As CHOP Tensions Grow, Seattle Bans Police Use Of Tear Gas, Crowd-Control Weapons Tyler Durden

Tue, 06/16/2020 – 12:39

The Capitol Hill Autonomous Zone (CHAZ), or the Capitol Hill Occupied Protest (CHOP), an area occupied by protesters and is also known as a self-declared autonomous zone, based in the Capitol Hill neighborhood of Seattle, Washington, is breathing a sigh of relief early this week as the Seattle City Council voted unanimously to ban police from using chokeholds, tear gas, pepper spray, and other crowd-control weapons, reported King-5 News.

For readers, here are some of the latest developments in CHOP:

City council voted 9-0 Monday amid new frustrations police officers used tear gas to disperse protesters around CHOP. Council members heard a whole host of complaints from residents forced out of their homes by the gas — even though they were not participating in demonstrations.

Video: King-5’s report on Seattle banning police from using tear gas

Seattle Police Officer Guild President, Mike Solan, said, last week, that officers were forced to use “less than lethal” weapons in the early morning hours of June 8 around the CHOP area to restore public order. These “tools” were mainly tear gas and pepper spray — which were whipped up into the air, in densely packed neighborhoods, and chocked not just protesters, but also residents in their homes.

On Monday, Seattle Police Chief Carmen Best said, “It has been historically known through the evidence and other research that the use of CS gas, otherwise known as tear gas, can often be a less lethal way of dispersing a crowd without having to go hands-on, without using our riot batons. So it has been determined to be less dangerous to do that. That said, it has been very clear to us that people are not wanting us to use the CS.”

Video: Police gas Chop

Best said the police department is speaking with the International Association of Chiefs of Police, exploring other methods to control crowds in the future.

K. Wyking Garrett, the President of Africatown Community Landtrust, a group of real estate professionals in the Greater Seattle region, said he supports the City Council’s decision to restrict how police deploy tear gas.

“It is very unfortunate that people expressing their First Amendment rights have been met with extreme violence and escalation by the police presence,” Wyking Garrett said.

On a federal level, President Trump is expected to sign an executive order Tuesday outlining police reform — it will include efforts to track officer misbehavior, incentivize some departments and involve social workers and mental health professionals on some calls.

CHOP occupants can breathe a sigh of reliefthis week that police will not tear gas or pepper bomb them out of their self-declared autonomous zone.

via ZeroHedge News https://ift.tt/2V5XpIr Tyler Durden

{kind=link}