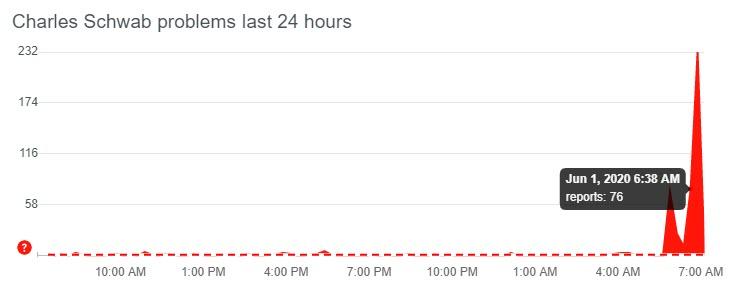

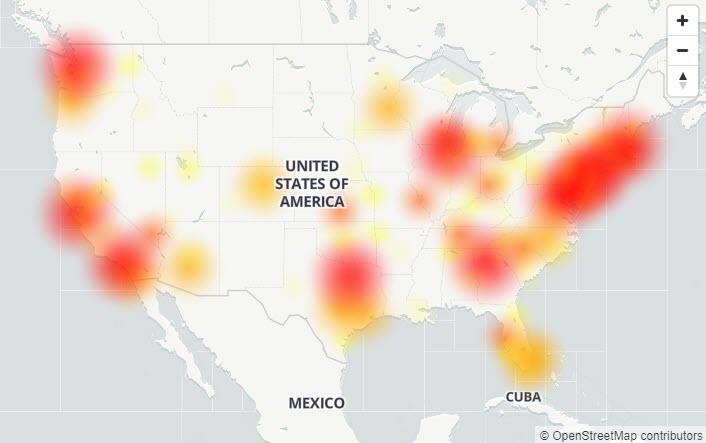

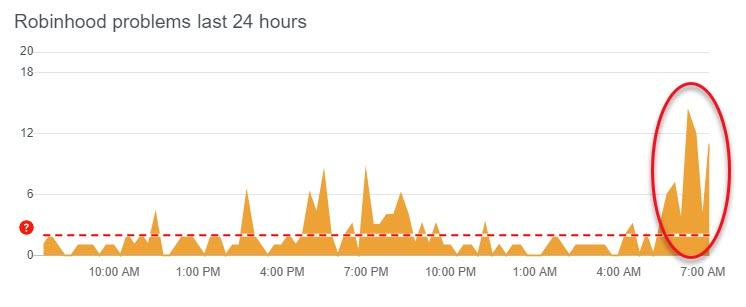

Accelerating losses into and across the open this morning suddenly reversed at around 0938ET… which coincidentally is when Charles Schwab’s website seemed to start having difficulties…

US Manufacturing ‘Soft’ Survey Data Disappoints With Modest Rebound Tyler Durden

Mon, 06/01/2020 – 10:04

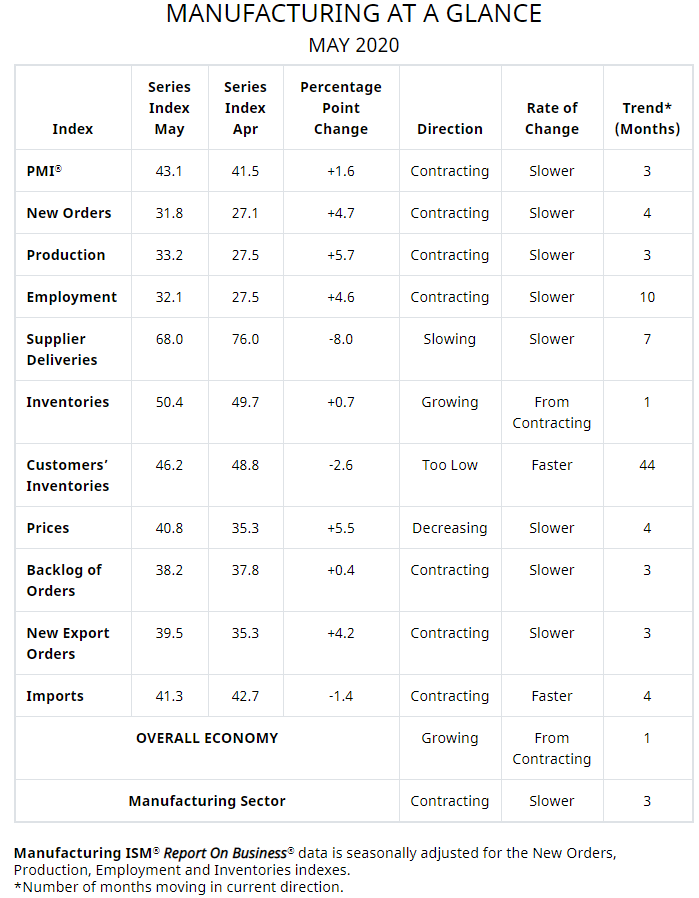

Following May’s preliminary PMI rebound, final ‘soft’ survey data for the US manufacturing sector was expected to consolidate its rebound.

However, while Markit’s PMI held its rebound at 39.8 (from 36.1) it was slightly below the 40.0 expectations and showed no improvement over the flash print.

ISM Manufacturing showed a similar picture – with a modest rebound but disappointingly missing expectations (up from 41.5 to 43.1, but less than the 43.8 exp)

Source: Bloomberg

Markit reports that a marked decline in total sales and negative sentiment towards the outlook for output over the coming year drove employment down, as firms reduced workforce numbers substantially. At the same time, lower input buying and weaker overall demand conditions put pressure on suppliers to lower their prices. Consequently, input costs fell again, in turn helping manufacturers to cut their output charges at a record pace as firms sought to remain competitive.

Under the hood of ISM’s data, things are not pretty…

While most respondents suggested some level of optimism that the corner has been turned:

“Fuel sales demand are beginning to rebound in May as stay-at-home orders are lifted across the country.” (Petroleum & Coal Products)

“Returning to full production for automotive, ramp-up will still depend on speed of automotive start-ups. We have built up inventory to stock. Ready to ship.” (Fabricated Metal Products)

“Business activity remains strong for consumable applications and very weak in durable segments.” (Plastics & Rubber Products)

“We see a lot of positive signs, despite what’s going on. People seem to continue to be building and looking to projects for fall of 2020 and beyond. There is good optimism out there.” (Nonmetallic Mineral Products)

“Despite the COVID-19 issues, we are seeing an increase of quoting activity. This has not turned into orders yet, but it is a positive sign.” (Computer & Electronic Products)

There were a few non-believers:

“Current conditions in the automotive, construction, oil and gas, agriculture equipment, and tube/pipe markets are all adversely impacting our business results.” (Chemical Products)

“We see an issue with suppliers that are affecting production. At the same time, social distancing measures in [the] manufacturing plant and customer demand are impacting the rate of production.” (Transportation Equipment)

“Increased COVID-19 sales in the food business has really stressed our production capabilities.” (Food, Beverage & Tobacco Products)

Digging into some of the pricing details, We see the following “essential” commodities higher in price:

Alcohols; Crude Oil; Freight; Personal Protective Equipment (PPE; PPE — Gloves; and PPE— Masks

But most other commodities are lower in price…

Acrylate Monomers; Aluminum; Base Oils; Copper; Corn; Diesel Fuel (3); Methanol; Nylon; Oil Based Products; Packaging Materials; Plastic Products; Polypropylene; Solvents; Steel; Steel — Carbon; Steel — Cold Rolled; Steel — Hot Rolled; Steel — Stainless; and Steel Products.

“Manufacturing remained in a deep downturn in May, as measures taken to contain the spread of COVID-19 continued to cause production losses, disrupt supply chains and hit demand. Job losses meanwhile continued to run at one of the highest rates in over a decade, and pricing power has collapsed.

“With increasing numbers of companies restarting production, we should see some improvements in the output trend in coming months, and it was reassuring to see signs of the downturn already starting to ease in May, suggesting April was the eye of the storm as far as the production collapse is concerned.

“There remains a high risk that any recovery will be frustratingly slow as ongoing social distancing measures, high unemployment, job insecurity and damaged balance sheets constrain consumer and business spending. The recovery will of course also fade quickly if virus infections start to rise again. For now, however, we focus on the good news that we may be past the worst in terms of the economic decline.”

But, despite all that, The Dow is back to pricing in economic expansion…

Source: Bloomberg

via ZeroHedge News https://ift.tt/2Xk1Oc1 Tyler Durden

Rabobank: “Things Are Getting Real… Everywhere You Look, Decades Are Happening In Weeks” Tyler Durden

Mon, 06/01/2020 – 09:45

Submitted by Michael Every of Rabobank

“There are years where nothing happens, and there are weeks where decades happen.” So said Lenin, who knew a thing or two about revolutionary times. The US faces its worst protests/riots since 1968, which are whipped up by the far right, or the Russians, or ANTIFA –newly-designated as a terrorist organisation by President Trump– depending on what you read. The editor of China’s Global Times has trolled this must be Hong Kong protestors at work – with no Twitter fact-check; certainly Hong Kong’s “If we burn, you burn with us” fits the real rage on display. So should markets think not of the end of lockdown but the start of breakdown? (We have certainly swapped quarantine for curfew in many places.) Perhaps – but 1968 and 1992 were both followed by the usual US exceptionalism. Indeed, the US private sector just sent the first astronauts into space from US soil in a decade, with plans for a moon landing and a trip to Mars. Then again, we are decades further into neoliberal financialisation now, with all the resultant atrophying of previous US strength: the public sector can no longer put a man on the moon; it has to be outsourced.

Re: decades in weeks and breakdowns, on Friday markets –and this Daily– felt a Rubicon was about to be crossed when Trump tweeted “CHINA!” just before a press conference on the subject. However, despite his aggressive rhetoric on the South China Sea and “Wuhan virus”, the conclusion was a bazooka had not been brought to the table. Trump announced: the beginning of the process of ending Hong Kong’s separate legal status from China; a shift in the US travel advisory; action to limit access to US universities; and a working group to protect the US financial system from China; and sanctions on HK and PRC individual. Yet he did not walk away from the phase one trade deal – Trump opted to leave the WHO entirely instead. Equities and CNH both rallied Friday, and Hong Kong was up strongly today. Wrongly.

Loss of US recognition will not directly impact Hong Kong much, as China says, yet:

The shift on visas prevents Chinese nationals studying STEM at post-grad level in the US if they attended a military university (around 4% of the total in the US) OR have links to a firm signing up to Beijing’s policy of ‘Military-Civilian Fusion’: that covers anything larger than an SME.

The working group on financial markets is almost certain to recommend delisting Chinese equities from the US, a process already underway, and escalate restrictions on US capital flows into China, also underway.

We should expect the list of sanctioned individuals to be lengthy and embarrassing. Some will have at least one account with a Western bank, which will have to be closed and moved to a Chinese bank, causing a backlash (last week saw former Hong Kong CEO CY Leung call for a boycott of a bank that could not be more ‘Hong Kong’). Moreover, once Chinese banks are doing that banking instead, US sanctions will then apply to them. We will still end up with restrictions on USD usage in Hong Kong/China that the market think we have dodged.

Trump was never going to walk away from a trade deal even if many observers already see it as dead: why bother? If China sticks to it, great – but it won’t change the political direction of travel; and if they don’t, it’s more fuel on the anti-China fire in the near future.

In short, Trump put US-China decoupling on the table – and STILL pushed the stock market up. Those who don’t see that might want to look at Hong Kong’s money changers, who are having to turn away hundreds of customers due to a lack of USD in the face of massive demand; and this is matched by inquiries over emigration and foreign property purchases. The Hong Kong Finance Secretary has even had to come out and say there are no plans to change the city’s HKD peg to the USD or to impose capital controls: that this had to be said speaks volumes. The South China Morning Post likewise points out Beijing may be holding back on a massive stimulus package because it is keeping its power dry and asks: is it for looming US decoupling? It’s certainly not because the economy is doing well from the latest PMI data (manufacturing 50.6 with new export orders 35.3 and 54% of firms seeing insufficient demand; services at 53.6; and Caixin manufacturing 50.7.)

Meanwhile, the tectonic shift on the US-China front runs through all other markets. Mexico has questioned the US over the phase one trade deal given USMCA Article 32.10 states an FTA with a non-market economy allows the other two parties to terminate or update it. Obviously it isn’t a FTA –it’s barely a deal anymore– but Mexico is stirring the pot given much of the US trade lost to China is likely to be gained by it, underlining the new regionalisation underway.

Far more significantly, Trump postponed the G7 meeting set for June because Germany’s Angela Merkel refused to attend. In response to this slight, as well as the milquetoast EU reaction to Hong Kong, who are still set to proceed with a September EU-China investment summit, Trump has shifted the “out of date” G7 date to September – and invited Australia, South Korea, India, and Russia to join. Yes, Russia used to be in G8, and Australia, South Korea, and India are all in the G20. Yet this overlooks the fact that all of the above except Russia feel threatened by China, and are establishing new national security mechanisms to deal with those concerns, including trading arrangements (India may be buying the Aussie barley China no longer is, for example). Moreover, reverse Nixon-ing to bring in Russia from the cold would be the requisite move to encircle China. That’s realpolitik over liberal ideals.

Please listen to Lenin, Europe (where watches are still set back to 2005). The EU debt/budget debate would have been timely 15 years ago, but the block looks to be drifting into a geo-strategic headache if the US and Russia were to build bridges over the top of it, or if the global architecture fragments, WHO style. Even the UK may opt for the US over an EU FTA (and for Australia, India, etc.). This is a real risk of that building in the British determination to walk away from deadlocked EU trade negotiations within weeks; and in the UK dumping Huawei and angling for a new “D10” (D for Democracy) of countries to unite behind a Western technological 5G alternative; and as the UK says 2.9m Hong Kongers are eligible for British residency – this from a government seen as having won the Brexit debate over immigration.

Everywhere you look, decades are happening in weeks. Are they taking us towards US collapse or renaissance? Towards European solidarity or division and (further) European irrelevance? Towards a Chinese century – or very rapidly away from it?

Does this matter for your market/asset? How can it not?! Bond yields are very low; volatility is very low; equities are very high; and the USD is well off its highs. Not all of these can be correct if those tectonic plates are about to shift: only one can.

via ZeroHedge News https://ift.tt/2TWmBAc Tyler Durden

Key Events In The Coming Week: The Worst Jobs Report Since The Depression, ECB, Brexit And More Tyler Durden

Mon, 06/01/2020 – 09:37

It’ll be a reasonably busy week ahead, DB’s Jim Reid writes (hot in pursuit of a new office desk) with the US jobs report on Friday the highlight, while also of interest will be the ECB’s latest decision on Thursday and whether they’ll announce more policy action, along with the release of PMIs (Monday – manufacturing and Weds/Thurs – services) from around the world. Finally, Brexit will return to the headlines as another negotiating round between the UK and the EU takes place. The most violent US riots in decades may also continue indefinitely.

Looking ahead to the key market moving events this week, for payrolls the consensus on Bloomberg is currently expecting -8000k job losses and the unemployment rate to rise to 19.6%, the highest level since the Great Depression in the 1930s, and up from the 14.7% reading in April. Within this it’ll be worth looking at the sectoral breakdowns for an idea of which industries are being hit the hardest. For example, in April the level of employment in leisure and hospitality fell by 47%. Meanwhile young people are being hit especially hard, and the teenage unemployment rate (for 16 to 19 year olds) rose to an astonishing 31.9% in April. Elsewhere PMIs (and the ISMs) will be important but the diffusion nature makes it incredibly difficult to calibrate to growth at extreme turning points. For the Fed, they meet next week so we’re now in blackout period so don’t expect to hear much from the committee members.

On the ECB meeting on Thursday DB expects large downward economic revisions to the staff forecasts more towards our house view. This supports calls for a doubling of the PEPP to €1.5tn and an extension to mid-2021 (this may be problematic to achieve if the Bundesbank ends up being constitutionally barred from participating in the ECB’s QE). The risk is a soft commitment to increase but no firm numbers until the next meeting on July 16th. There is also a clash between the PEPP being temporary policy and for it to be permanent enough to allow reinvestment. However, a lengthening of the “crisis” period means reinvestment until at least the end of 2022 would be appropriate to avoid a premature tightening of financial conditions. Expect all to be announced on Thursday. Also expect lots of press conference questions on the German Constitutional Court hearing.

Over in the political sphere, Brexit negotiations between the EU and the UK on their future partnership will continue via videoconference from tomorrow to Friday. This is the fourth round now, and thus far there hasn’t been a great deal of progress. Indeed, at the end of the third round in May, the UK’s chief negotiator, David Frost, said that “we made very little progress towards agreement on the most significant outstanding issues between us”. This is the last negotiating round before a high level meeting in June where the two sides will be taking stock of progress. It’s also important as if the two sides want to extend the transition period that concludes at the end of 2020, they only have until the end of June to agree.

Courtesy of Deutsche Bank, here is a day-by-day calendar of events

Monday

Data: May manufacturing PMIs from Australia, South Korea, Japan, China, India, Russia, Turkey, Italy, France, Germany, Euro Area, UK, South Africa, Brazil, Canada, United States and Mexico, Japan Q1 capital spending, May vehicle sales, US April construction spending, May ISM manufacturing

Tuesday

Data: Japan March all industry activity index, final April machine tool orders, Germany June GfK consumer confidence, France May business confidence, US March FHFA house price index, April Chicago Fed national activity index, new home sales, May Conference Board consumer confidence, Dallas Fed manufacturing activity

Central Banks: Reserve Bank of Australia monetary policy decision

Data: May services and composite PMIs from Australia, Japan, China, India, Russia, UK, Brazil and United States, Germany May unemployment change, Italy preliminary April unemployment rate, Euro Area April PPI, unemployment rate, US weekly MBA mortgage applications, April factory orders, final April durable goods orders, nondefence capital goods orders ex air, May ADP employment change, ISM non-manufacturing

Central Banks: Bank of Canada monetary policy decision

Thursday

Data: May services and composite PMIs from Italy, France, Germany and the Euro Area, May construction PMIs from Germany and the UK, Euro Area April retail sales, Canada April international merchandise trade, US April trade balance, final Q1 nonfarm productivity, weekly initial jobless claims

Central Banks: ECB monetary policy decision

Friday

Data: UK final May GfK consumer confidence, Japan April household spending, preliminary April leading index, Germany April factory orders, Italy April retail sales, US May change in nonfarm payrolls, unemployment rate, average hourly earnings, April consumer credit, Canada May net change in employment

* * *

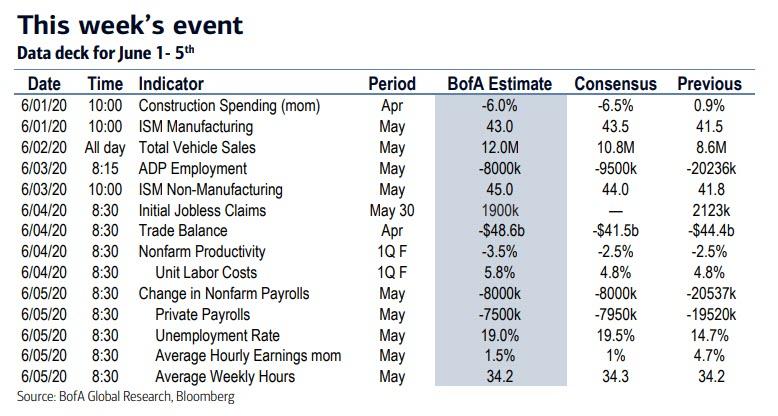

Finally, looking at just the US, Goldman writes that the key economic data releases this week are the ISM manufacturing index on Monday, the ISM non-manufacturing index on Wednesday, the jobless claims report on Thursday, and the employment report on Friday. There are no scheduled speaking engagements from Fed officials this week, reflecting the FOMC blackout period.

Monday, June 1

09:45 AM Markit US manufacturing PMI, May final (consensus 40.0, last 39.8)

10:00 AM Construction spending, April (GS -5.5%, consensus -6.0%, last +0.9%): We estimate a 5.5% decrease in construction spending in April, with scope for broad-based declines in both non-residential and residential construction.

10:00 AM ISM manufacturing index, May (GS 44.5, consensus 43.7, last 41.5): Our manufacturing survey tracker increased by 5.2pt to 38.7 in May, following somewhat stronger regional manufacturing surveys on net. We expect the ISM manufacturing index to rebound by 3.0pt to 44.5 in May.

Tuesday, June 2

5:00 PM Lightweight motor vehicle sales, May (GS 11.8m, consensus 11.0m, last 8.6m)

Wednesday, June 3

08:15 AM ADP employment report, May (GS -6,000k, consensus -9,500k, last -20,236k); We expect a 6,000k decline in ADP payroll employment, reflecting lower jobless claims than in April and higher oil prices. While we believe the ADP employment report holds limited value for forecasting the BLS nonfarm payrolls report, we find that large ADP surprises vs. consensus forecasts are directionally correlated with nonfarm payroll surprises.

09:45 AM Markit US services PMI, May final (consensus 37.4, last 36.9)

10:00 AM Factory orders, April (GS -13.0%, consensus -14.2%, last -10.4%); Durable goods orders, April final (last -17.2%); Durable goods orders ex-transportation, April final (last -7.4%); Core capital goods orders, April final (last -5.8%): Core capital goods shipments, April final (last -5.4%) We estimate factory orders fell by 13.0% in April following a 10.4% decrease in March. Durable goods orders fell sharply in the April advance report.

10:00 AM ISM non-manufacturing index, May (GS 45.0, consensus 44.5, last 41.8): Our non-manufacturing survey tracker increased by 5.6pt to 39.6 in May, following somewhat stronger regional service sector surveys. We expect the ISM non-manufacturing index to rebound by 3.2pt to 45.0 May report.

Thursday, June 4

08:30 AM Trade balance, April (GS -$49.2bn, consensus -$49.1bn, last -$44.4bn): We estimate the trade deficit increased by $4.8bn in April, reflecting a rise in the goods trade deficit.

08:30 AM Nonfarm productivity, Q1 final (GS -2.8%, consensus -2.5%, last -2.5%); Unit labor costs, Q1 final (GS +5.1%, consensus +4.8%, last +4.8%): We estimate nonfarm productivity was revised down by three tenths to -2.8% (qoq ar) in Q1. We estimate growth in Q1 unit labor costs – compensation per hour divided by output per hour – was revised up to +5.1% in Q1.

08:30 AM Initial jobless claims, week ended May 30 (GS 1,800k, consensus 1,800k, last 2,123); Continuing jobless claims, week ended May 23 (consensus 19,039k, last 21,052k): We estimate initial jobless claims declined but remain elevated at 1,800k in the week ended May 30.

Friday, June 5

08:30 AM Nonfarm payroll employment, May (GS -7,250, consensus -8,000k, last -20,537k); Private payroll employment, May (GS -6,750k, consensus -7,650k, last -19,557k); Average hourly earnings (mom), May (GS +1.5%, consensus +0.9%, last +4.7%); Average hourly earnings (yoy), May (GS +9.3%, consensus +8.5%, last +7.9%); Unemployment rate, May (GS 21.5%, consensus 19.6%, last 14.7%): We estimate nonfarm payrolls declined by 7.25mn in May, reflecting a continued increase in temporary layoffs and only a gradual reopening from the coronavirus shutdown. Employment surveys showed month-over-month improvement but remained in contractionary territory, while excess initial claims from regular state programs totaled almost 12mn during the May payroll month. Although alternative data suggest a modest increase in the number of workers at work sites in the May, some of the earliest workers to return to work likely remained on payrolls during the pandemic. We assume the BLS will adjust its birth-death model to capture the impact of some temporary business closures (as it did in the April report); however we believe the adjustment will again understate the true magnitude of nonfarm payroll declines.

We expect that workers that the most of the 8.1mn workers that were employed but not at work for “other reasons” in April will be reclassified as unemployed in the May household survey, providing an almost 5pp boost to the unemployment rate. Furthermore, our real-time unemployment tracker—which forecasts the unemployment rate based on jobless claims—suggests unemployment might have peaked around the May survey week. Additionally, we expect the participation rate to decline a bit further on account of the virus. Taken together, we estimate the unemployment rate rose almost 7 points to 21.5%. We estimate average hourly earnings increased 1.5% month-over-month and 9.3% year-over-year, reflecting a composition shift towards higher-paid workers that is boosted by positive calendar effects.

Source: Deutsche Bank, Goldman, BofA

via ZeroHedge News https://ift.tt/2ZUQ8Oy Tyler Durden

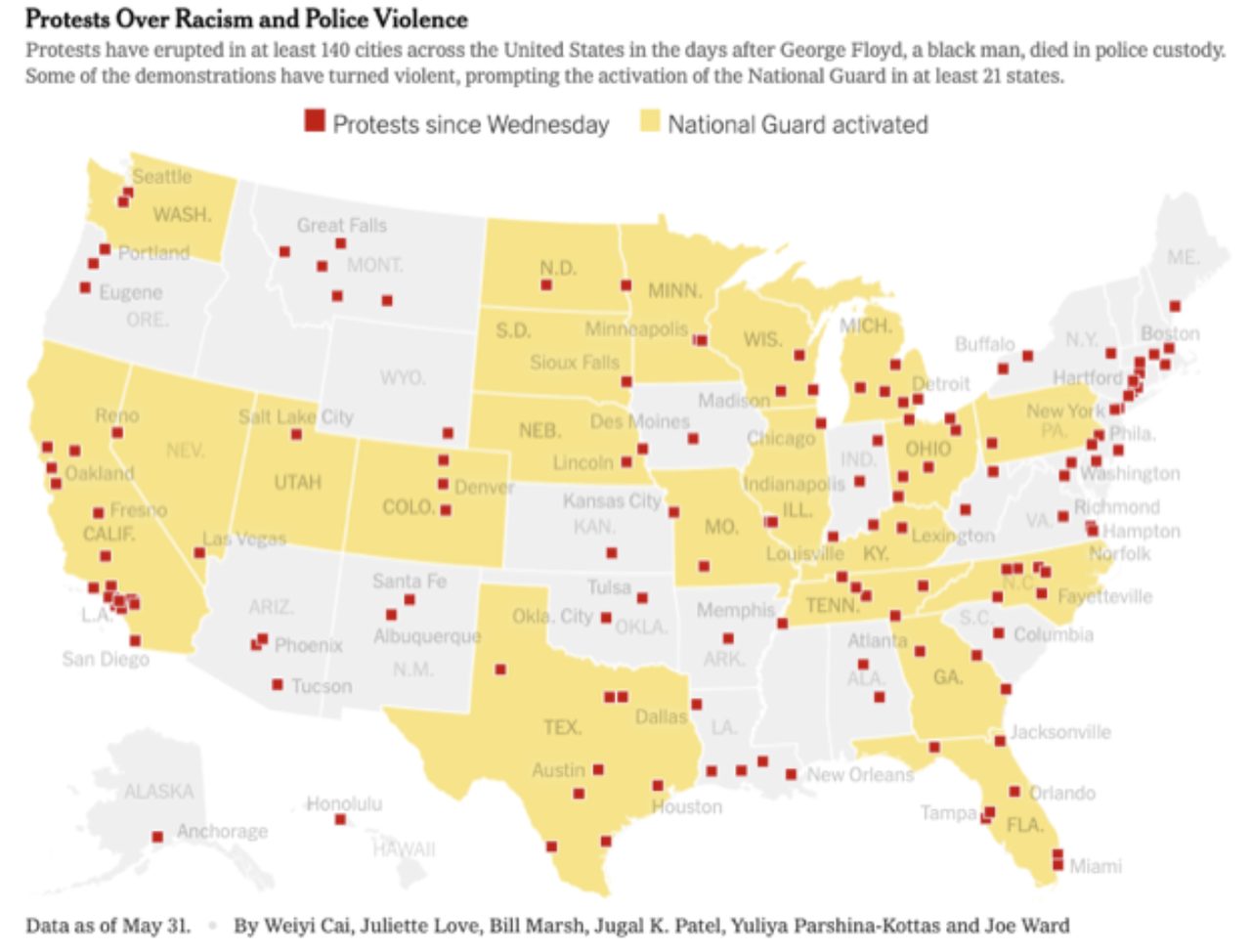

6 Killed, Thousands Arrested As 26 States Called In National Guard To Quell 3rd Night Of Chaos Tyler Durden

Mon, 06/01/2020 – 09:25

Following what was either the third or the sixth night of chaos to sweep across America following the death of George Floyd a week ago, Americans surveying the wreckage are being met by staggering totals. After tens of thousands of peaceful demonstrators, violent anarchists and opportunistic looters commingled for another night of chaos in cities from California to New York, and from Seattle to South Florida.

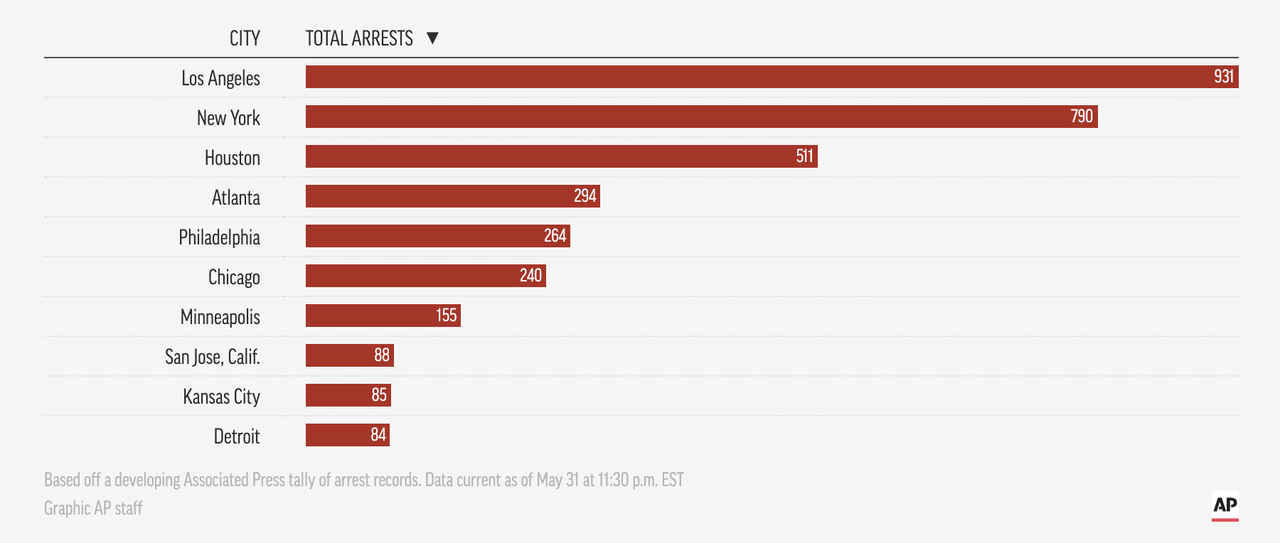

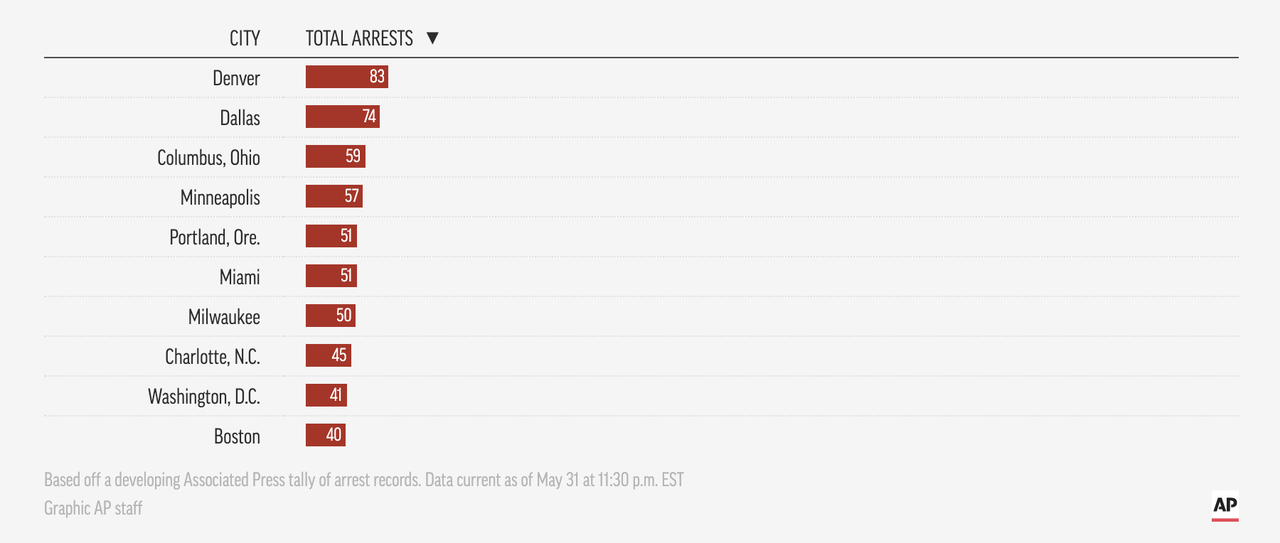

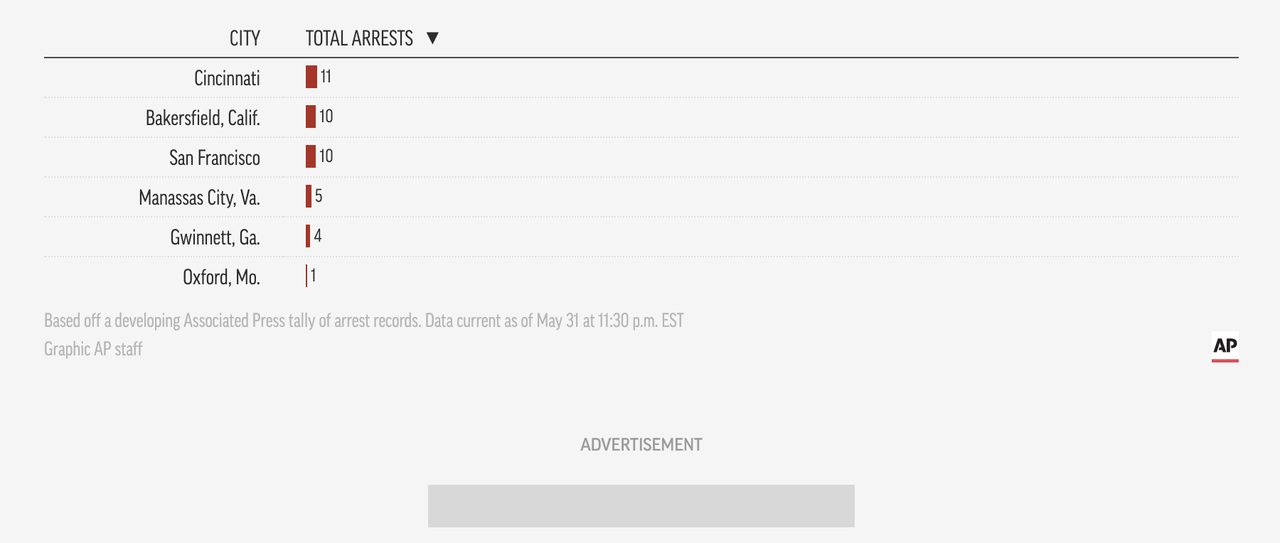

Reports published late Sunday/early Monday revealed that President Trump spent part of Friday in an underground bunker under the White House as secret service fired rubber bullets into crowds of violent and non- violent demonstrators. Over the entire three nights of chaos, at least 4,400 people have been arrested, according to a tally compiled by The Associated Press. Arrests ranged from stealing and blocking highways to breaking the dozens of curfews imposed by cities around the country on Saturday and Sunday as the violence spread, the AP reports.

Curfews were imposed in major cities around the U.S., including Atlanta, Chicago, Denver, Los Angeles, San Francisco and Seattle. About 5,000 National Guard soldiers and airmen were activated in 15 states and Washington, D.C.

One man was shot and killed when police and the National Guard opened fire on a crowd that had reportedly turned violent in Louisville, the city where Breonna Taylor was killed. WaPo reports Metro Police Chief Steve Conrad confirming the Kentucky National Guard and Louisville police were dispatched to the parking lot at Dino’s Food Mart around 12:15 a.m., where a large crowd had gathered, and that as they tried to disperse the crowd, somebody opened fire at an officer.

Minneapolis and St. Paul were largely spared on Sunday evening following early marches that were largely peaceful. Though there was one high profile incident involving a tanker driving into a crowd of marchers on a highway (the driver of the truck was later arrested), the widespread violence that plagued other areas didn’t materialize. As WaPo reports, the city on Monday morning looked like a “ghost town”.

But this relative peace came at a high cost, as the national guard moved to forcefully enforce curfews, even going so far as to fire paint cannisters and rubber bullets at people sitting on porches who ignored shouts to “get inside.”

The gas stations are closed. The grocery stores are dark. And along Hiawatha Avenue in South Minneapolis, one of the only restaurants serving is a McDonald’s, where every inch of the building’s windows are boarded up except for two small holes at the drive-through just big enough to pass along food.

After nearly a week of unrest in response to the death of George Floyd, city and state officials were optimistic Sunday after a night passed without the dangerous fires, looting and violence that have cut a wide swath of devastation through the heart of this Midwestern city.

But it came with a new reality: Thousands of National Guard troops and state and city police officers moving to aggressively – and sometimes violently – regain control of the streets, and a lockdown that has residents under curfew and has closed the major highways at night.

In some neighborhoods, residents stand outside their homes and businesses with guns, fueling a sense of lawlessness, while medical students descend on the scene with supplies to assist those in need, adding to what increasingly feels like a domestic war zone.

Minnesota’s Democratic governor, who has been criticized for not responding forcefully enough in the beginning. Now, he says, his approach might be remembered as heavy-handed – but he doesn’t care.

“There will be critiques of me that this is excessive. Why are you keeping forces on the ground?” Minnesota Gov. Tim Walz (D) said Sunday. It would be “irresponsible” to dial back the state’s response, amid rumors of outside agitators that he and other officials say have come into the city to sow chaos, he said.

In particular, a video of cops and national guard firing at a woman standing peacefully on her porch went viral, eliciting a torrent of criticism. State police leaders defended it

Watch “MINNEAPOLIS COPS AND NATIONAL GUARD FIRE PROJECTILE THAT HITS INNOCENT WOMAN STANDING ON HER PORCH” on YouTube https://t.co/PrrktFKDq8 I think I’m not sure but these all white people getting shot at for being on there front porch

The man in Louisville wasn’t the only casualty of the unrest. As governors in 26 states called in the National Guard and Secret Service agents again clashed with demonstrators outside the White House, media reported that at least six people had been killed in violence across the US, as gunfire rang out from Detroit to Indianapolis to Chicago to Omaha, notably correlating with the sites of notorious police killings.

via ZeroHedge News https://ift.tt/3eBtajG Tyler Durden

Lemon tree very pretty and lemon flower is sweet. But the fruit of the poor lemon is impossible to eat.”

What have we got to look forward to this week?

Around the globe the virus numbers suggest we’re past the moment of greatest danger, but the US riots could well prove a prove a drag on markets and confidence. As I predicted on Friday, Trump’s much anticipated China-bashing speech on Friday proved another lacklustre nothing – providing markets another reason for markets to rally.

But the degree to which soaring markets are diverging from the real economic virus damage, and now rising rage, has become embarrassingly obscene. How can markets set themselves up for new record highs, when hundreds of millions around the globe have been sacked or furloughed and are likely to become long-term unemployment statistics? (Rhetorical question..)

I suspect these riots may be the harbingers of a long-hot summer of discontent – and not just in the US.

To get you started this week, I’m going to recommend a book I have, unfortunately, only half-read. My chums Mark Blyth (a fellow Scot and now rather successful Economist at Brown University) and Eric Lonergan (a fund manager) have just published ANGRYNOMICS. (The copy they gave me to review got left half-finished in the office when lockdown was announced!) The link takes you to the review in the FT.

I’ve been trying to figure out what’s going on and how the current market instability plays out: a dismal outlook and soaring prices. Its complex, but the fact governments and central banks have been able to support markets, bailout businesses and pay salaries has helped with smoothing the initial economic shock. But are all their actions simply creating a deeper delayed crisis? (The answer is yes, and they need to act to avoid it.)

A number of commentators point to burgeoning debt levels around the globe as the metastasising cancer threatening to consume the global economy. I would certainly agree unsustainable debt will prove terminally toxic for many over-levered corporates – and they will need long-term bailouts and support to survive. That is going to fundamentally change the relationship between state and commerce, and we need to figure out how to avoid the private sector simply becoming state ministry of production bureaucracies.

I am also concerned about the increasing risk of sovereign crisis – especially outside the most developed nations, and how defaults across producer/resource nations could create massive, chronic and ongoing instability and potential conflict as nations go bust, triggering supply chain fractures and openings where the Chinese and the West will aggressively compete to seize resource access.

Nations that have borrowed in currencies they don’t own are the most vulnerable – from Argentina to Italy. (Yep.. every Euro member is in trouble..)

But stable sovereigns with stable currencies that can print their own money don’t go bust. They can print money. QE makes it easy. It’s supposed to work by central banks buying debt assets from banks, and the banks then reinvesting that cash into the real economy to fuel growth, jobs, and asset investment.

BUT: As we’ve seen very clearly since 2010 – it doesn’t work that way. Most money created in the financial asset ecosystem by QE remains invested in financial assets.

That’s why QE never created inflation in the real economy. It created massive inflation in financial assets: despite relatively unimpressive growth though the last decade, stocks hit record levels and bond yields fell to record, even negative, rates. That was massive financial asset inflation, and the payback was ever declining yields, forcing investors to assume more and more risk in the search for yield.

QE has become an inescapable trap. The taper tantrum a few years ago when the Fed cautiously tried to start normalisation triggered immediate market instability. It could have precipitated a deeper crisis than 2008 if the Fed had kept going. A market crash would not only trigger recession, but a pensions crisis as thousands of savers saw their futures vanish, and a confidence meltdown.

These are the known long-term consequences of QE and ultralow rates. We now have a global financial system absolutely addicted to it. How do you wean the system off the crack cocaine of QE and ZIRP, without cold turkey destroying the global economy?

One way may be through the magic of Modern Monetary Theory. The way QE works is for a National Treasury to sell bonds in the morning, the government to spend the money by lunchtime, and the Central Bank to buy the bonds in the evening. The result is a liability on the Treasury and an asset on the books of the Central Bank. Quick tap of the MMT wand and the two cancel each other out. The money spent by government remains in circulation. Magic.

Sure, it sounds like madness… but does it matter if central banks show theoretical trillion-dollar losses?

At present, all that money the banks got from central banks for their bonds is immediately invested in more financial assets. We need mechanisms to ensure it’s directed into the real economy – which should be happening through this crisis… but is it? It may be time for Central Banks to start discouraging financial asset investment… Cutting prices by raising bond yields? Transaction taxes?

Shock? Horror! How could anyone be so stupid as to interfere with the functioning of markets. Oh, come on..! QE distortions have seen the invisible hand of markets locked in the deepest darkest dungeon of Chateau d’If these last 10-years. I’m as keen as anyone to see it escape…

Perhaps the only way out of this trap is something very radical? Cancel sovereign debt, create trillions for the IMF to bail out troubled economies, keep interest rates low, and for central banks to buy equity to sustain struggling firms…? (If they do it well, they might even make money..)

How deep do our imaginations go… ?

Meanwhile…

We could always pay for everything by just properly taxing the rich? Why not?

The summers are getting warmer and the weekends are getting madder. Here on the South Coast of England our village was rammed with tourists who clearly think Lockdown is done. (Fair enough – as we learnt from the Andrew Marr show on Sunday, a Chinese survey of thousands of infections found only one case of the virus spreading in the open air!)

Everyone seems to have spent their furlough money buying paddleboards and blow-up canoes – the river was chock-a-block with people, busier than I’ve ever seen it. It was scary trying to manoeuvre the yacht into our mooring past some of the more oblivious ones – I might have got a bit shouty at a couple. (I was advised not to paint little black silhouette paddle boarders on the bow like the black crosses arranged in rows underneath a Spitfire’s cockpit canopy.)

Madness and fury seems to be consuming the US. Space X launching a rocket to the space station was the light comedic distraction as cities in 30 states experienced riots.

I am slightly concerned about the States. When I was young, being brought up on a diet of cowboy films, John Wayne, Star Trek, The Beachboys, The Eagles, and the rest… America was rich, weathly, free and immeasurably more attractive than strife-riven three-day week UK. The American dream looked very real.

Over the last four years, it’s become tarnished very quickly. I can’t help but worry…

Who to blame? Trump… Hell, no.. He’s the product of the times. If anyone can sort it, it’s the Republicans.. If they really want to Make America Great Again, they need to start from the top. (And I can just see the comments rolling in on that one… let me guess.. “lickspittle running dog of the Soros/Rothschild axis…” or some such nonsense..)

via ZeroHedge News https://ift.tt/3dzatgg Tyler Durden

Gilead Falls After Phase 3 Remdesivir 10-Day Trial Failed To Reach Significance Tyler Durden

Mon, 06/01/2020 – 08:45

One week after the New England Journal of Medicine found mixed results in its pivotal study of Remdesivir in covid-19 patients which “found no marked benefit from remdesivir for those who were healthier and didn’t need oxygen or those who were sicker, requiring a ventilator or a heart-lung bypass machine” and only “significantly helped those on supplemental oxygen”, concluding that “given high mortality despite the use of remdesivir, it is clear that treatment with an antiviral drug alone is not likely to be sufficient“, moments ago Gilead announced its own results from a Phase 3 trial of Remdesivir in patients with moderate Covid-19 and which, similarly, appeared to disappoint because while the press release was quick to point out that “patients in the 5-day remdesivir treatment group were 65% more likely to have clinical improvement at Day 11 compared with those in the standard of care group,” this was not relevant, and what did matter is that “the odds of improvement in clinical status with the 10-day treatment course of remdesivir versus standard of care… failed to reach statistical significance.”

The release scrambled to recover the Remdesivir momentum, quoting Francisco Marty, MD, an infectious diseases physician at Brigham and Women’s Hospital, and associate professor of medicine at Harvard Medical School, who said that “our understanding of the spectrum of SARS-CoV-2 infection severity and presentations of COVID-19 continues to evolve. These study results offer additional encouraging data for remdesivir, showing that if we can intervene earlier in the disease process with a 5-day treatment course, we can significantly improve clinical outcomes for these patients.”

In short, anything to save the drug, even if the drug ultimately does not provide much of a benefit compared to placebo. In the end it will be up to the FDA to decide whether said lack of significance is enough to grant Gilead drug approval.

Key efficacy and safety results from the study are included in the table below.

The news sent ES futures lower, with the Emini down 8 points and Dow futures sliding back in the red…

… while GILD stock initially dumped but has managed to rally back some kneejerk losses.

via ZeroHedge News https://ift.tt/3gRLQOe Tyler Durden

‘It’s Out Of Control’ – Brazil Joins US As Only Countries With More Than Half A Million COVID-19 Cases: Live Updates Tyler Durden

Mon, 06/01/2020 – 08:32

With US equity markets set to kick off the month of June in the green in defiance of any rational fundamental analysis, most of the army of journalists who have been covering various aspects of the coronavirus crisis have seemingly been diverted to covering the “protests” that have broken out across the US last night, most of Monday’s big virus related news has come from abroad.

Perhaps the biggest story is British PM Boris Johnson’s decision to push ahead with plans to start easing Britain’s lockdown, even as hundreds of new deaths are reported every day, as the UK outbreak remains one of the world’s deadliest. Several high-profile government scientists spoke out against the government’s plan over the weekend, but on Monday, English primary schools reopened for the first time since they were shut 10 weeks ago, though many parents planned to keep their children at home amid widespread fears.

In addition to re-starting classes for some of the youngest students, up to six people can meet outside in England, outdoor markets can reopen, elite competitive sports can resume without spectators and high-risk patients can spend more time outdoors.

Looking ahead, the UK government’s plan to enact quarantine measures for all international travelers and returning Britons are likely to face a Conservative revolt when they are considered by the Commons later this week due to fears over the impact on the economy, the Telegraph reported.

As the UK starts to ease its lockdowns, India announced another extension over the weekend – nicknamed “lockdown 5” by the people – as the country’s outbreak swelled as the total number of infections approaches the 200k mark. India has reported some if its largest daily numbers of new cases in the last few days as its incredibly restrictive lockdown has been eased.

India has reported 230 deaths in the last 24 hours, bringing its total to 5,394 as the latest extension also includes a three-week plan for reopening that will end when the lockdown does. In reality, the lockdown is being eased in most places except for the containment zones now isolated due to coronavirus outbreaks.

India’s Health Ministry says it has 190,535 cases, placing it in seventh place worldwide.

Across India on Monday, airlines have been ordered to keep the middle seat empty if possible, according to India’s aviation regulator.

Meanwhile, in China, Beijing accused the US of being “addicted to quitting” following President Trump’s decision to leave the WHO.

In Russia, health officials reported 9.035 new cases as Russia became the latest country to see its total number of cases top 400k (with 414,878 total) and 162 new deaths (for a total of 4,855). Singapore, meanwhile, reported 408 new cases and zero new deaths as an outbreak among migrant workers has continued to wane.

Germany reported just 335 new cases and 11 deaths, bringing its twin totals to 181,815 and 8,511, as the country continued its plan of cautious reopening.

In Brazil, the number of cases topped 500k, making it the second country to reach that milestone, after officials reported more than 10k new cases, along with 480 deaths from coronavirus on Sunday, bringing its death toll to 29,314, the health ministry said.

More than half a million people in the country

Russia’s PM has been back in the job for 2 weeks now, but he’s no longer the only PM of a CIS member to contract the virus. Armenian Prime Minister Nikol Pashinyan revealed that he and his family have tested positive for the novel coronavirus.

“I didn’t have any symptoms, I decided to take a test as I was planning to visit the frontline,” he said during a Facebook live video.

Armenia has a population of 3 million, and has so far registered 9,402 confirmed cases of the coronavirus and 139 deaths.

In South Africa, a two month-old coronavirus lockdown has been lifted, allowing people outside for work, worship, exercise or shopping, and allowing mines and factories to run at full capacity to try to revive the economy.

Japan is reportedly planning to allow visitors from countries with low levels of coronavirus infection, including Australia, Thailand, Vietnam and New Zealand.

After weeks of no new cases, Hong Kong’s Center for Health Protection is investigating two new locally transmitted cases of coronavirus – 34-year-old woman and a 56-year-old man. The new cases bring the total number of cases to 1,085 and 4 deaths.

Circling back to Brazil, the Latin American giant now has the second-highest number of cases in the world after the US and the fourth-highest death toll after the US, UK and Italy. According to Reuters, the US has delivered two million doses of the antimalarial medicine hydroxychloroquine to Brazil to fight COVID-19, the White House said, even after Facebook and Twitter took down posts from President Jair Bolsonaro where he touted the unproven but some say promising medication as a “miracle drug”.

via ZeroHedge News https://ift.tt/2Xkyr9u Tyler Durden

Our ruling elites, devoid of leadership, are little more than the scum of self-interested, greedy grifters who rose to the top of America’s foul-smelling stew of corruption.

The Founding Fathers were wary of institutional threats to liberty and the citizenry’s sovereignty, which included centralized concentrations of power (monarchy, central banks, federal agencies, etc.) and the tyranny of corruption unleashed by small-minded, self-interested, greedy grifters who saw all elected offices and positions of government influence as nothing more than a means to increase their own private wealth.

The Founders feared the dominance of self-interested, greedy grifters because they had no concept of the public good: to the greedy grifters, the government existed solely to serve their petty private interests and the interests of their fellow grifters.

The Founders understood that a republic required disinterested leadership capable of looking past petty self-interest to the common good of the people and their nation. They feared the election of self-interested, greedy grifters because once no one served the common good, the republic would fall into a fatal disunity.

We are living the Founders’ nightmare, for America is corrupt to the core. While everyone gorging at the public trough bleats about the “common good,” their single-minded focus is on aggrandizing as much power and private wealth as possible, and feeding their corrupt crew of insiders, lobbyists, “business interests,” bankers and assorted other legalized looters.

America has plenty of law enforcement, prosecutors and prison cells for those who loot a Whole Foods, but none for those who loot the public treasury, commit stock market swindles or financial fraud on a monumental scale. Not only did no one go to prison for the rampant institutionalized fraud of the 2008 looting, a.k.a. the Global Financial Meltdown–the looters were bailed out by the Federal Reserve and Treasury.

More recently, no one was even questioned when a biotech company issued a press release about a Covid-19 vaccine trial that boosted the stock’s price just long enough for insiders to dump millions of dollars of shares on a credulous public and also sell new shares in the company at a premium: a classic looting strategy known as pump and dump.

Members of Congress were caught red-handed in what amounted to insider trading, selling millions of dollars in their stock portfolios based on their secret briefings of the coming pandemic, while they reassured the public Covid-19 was no biggie. The farcical “investigation” found no wrong-doing.

Corruption in our political parties is so endemic nobody even bothers listing it except as a parlor game of pondering which party is more corrupt.

Our ruling elites, devoid of leadership, are little more than the scum of self-interested, greedy grifters who rose to the top of America’s foul-smelling stew of corruption. As for the nation’s infinitely greedy billionaires, if there was any justice left in America, Apple CEO Tim Cook would be rotting in a cell on Devil’s Island for buying back billions of dollars of Apple stock–buybacks were illegal not that long ago.

The cells next to his would be crowded with Big Pharma CEOs who advertised their products directly to consumers–also illegal not so long ago.

America is now a pay-to-play paradise of greed and corruption. The “public good” is a PR cover for legalized looting, much of which now depends on the Federal Reserve’s free money for financiers, parasites and predators.

If you think this is far too harsh on our current crop of greedy grifters and looters, please read historian Gordon Wood’s epic account Empire of Liberty: A History of the Early Republic, 1789-1815, which details the many critical debates between founders with fundamentally different views of what structures and safeguards were essential for the Republic’s survival.

When we look back at the genius of Hamilton, Madison, et al., and Washington’s obsession with ethics and promoting national unity, we are forced to weep for the pathetic, venal scum that passes for “leadership” in America today. The feedback loops the Founders designed to restrain the tyranny of corruption have all failed, as the biggest looters serve their interests under the guise of legality.

The Founders’ weren’t saints; they were flawed as are all humans, and like all humans, they were products of their era. But they did have a keen, abiding sense of the public good, and when they clashed over ideas about banking, the power of the presidency, etc., it was not for personal gain but for their vision of the common good.

If any of America’s “leadership” over the past 30 years had an ounce of concern for the common good, why did they enable financialization and globalization to hollow out the nation’s economy and social order? Why did they enable the frauds, skims, scams, cartels and monopolies that are the foundation of virtually every American billionaire’s “we pay no taxes” empires of greed?

The tyranny of corruption thrives in an amoral cesspool of anything goes and winners take all.

In today’s America, the tyranny of corruption has been so normalized that America’s polarized populaces are blind to the profound corruption of their parties and institutions. As in the last days of the Western Roman Empire, the masses are made complicit with bread and circuses, mimicking their “leaders” debasement of the public good to feeding at the public trough.

These are the troubled years that came before the deluge (Jackson Browne), for as Mr. Dylan put it, a hard rain’s a-gonna fall.