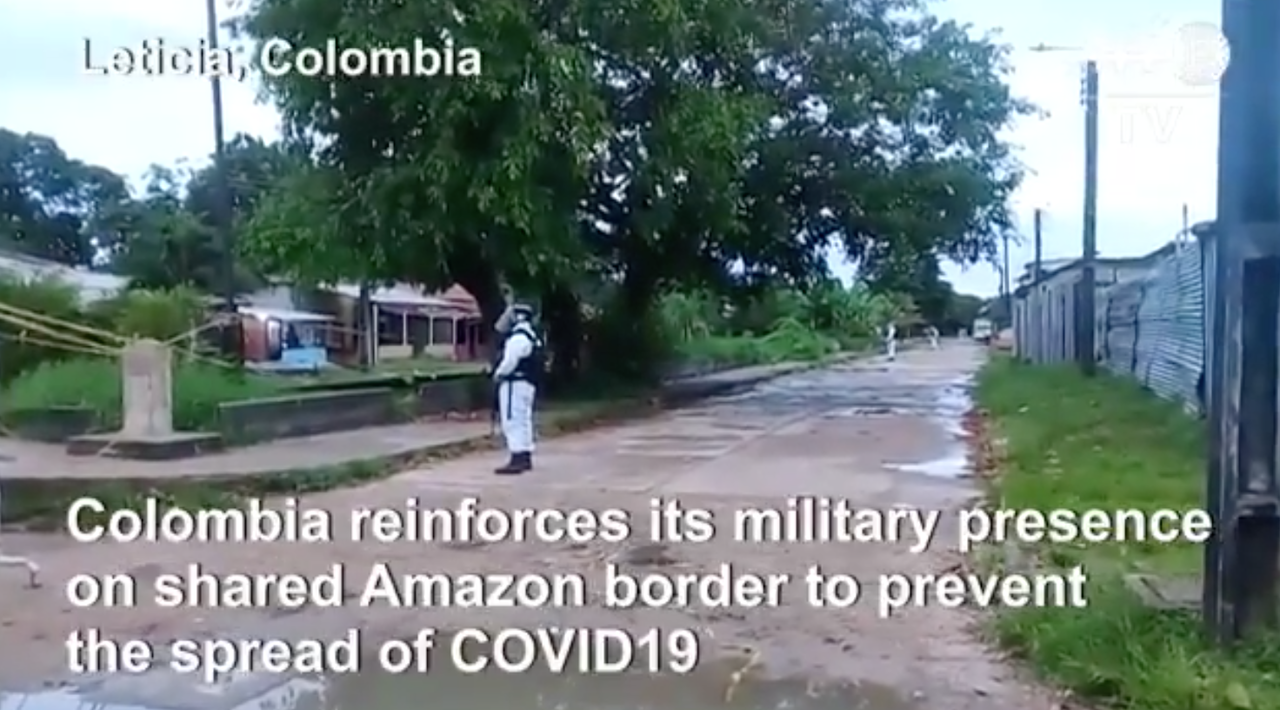

Colombia Militarizes Brazilian Border As COVID Deaths Soar Tyler Durden

Thu, 05/14/2020 – 19:45

A rise in cases and deaths from COVID-19 in Brazil has spooked neighboring countries, resulting in the National Army of Colombia to bolster forces along Brazil–Colombia border, reported Bloomberg.

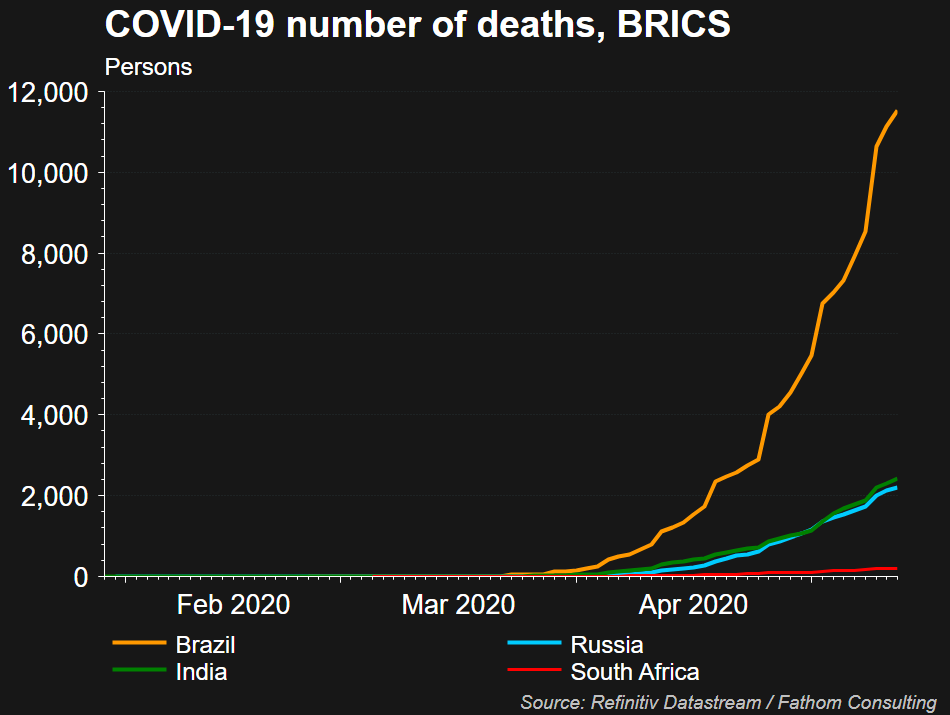

Johns Hopkins University reported the South American country had more than 188,000 cases and 13,000 fatalities on Thursday afternoon. The fast-spreading virus is ravaging the country’s favelas, something we warned about in late March.

Brazil leads BRIC countries in terms of virus deaths

Brazilian President Jair Bolsonaro’s virus response has backfired, due mostly because his administration is concentrated on reopening the economy rather than flattening the curve.

Colombian President Ivan Duque Marquez has had no other choice than increase military presence on its Amazon border that is shared with Brazil and Peru, a move that will hopefully prevent virus carriers from entering the country.

“The decision has been made to militarize, with more presence, all the border points and exercise the respective control to prevent imported cases of floating populations from arriving,” President Duque said Tuesday.

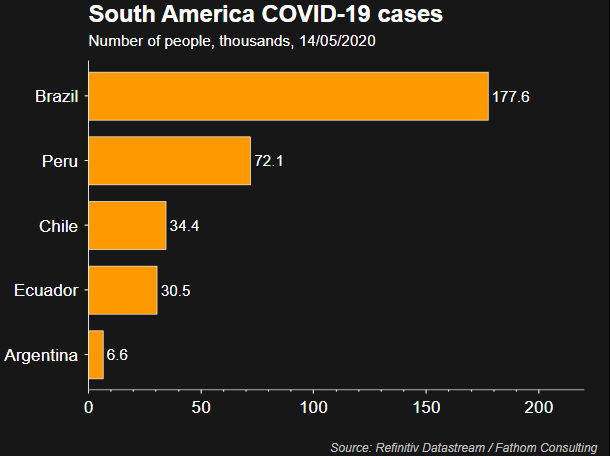

Brazil has transformed into the epicenter of the pandemic in South America. It has the sixth-highest number of infections and deaths globally. On the continent, second to Brazil is Peru, which has more than 76,000 cases and nearly 2,200 fatalities.

Paraguay President Abdo Benitez warned last week that the virus situation in Brazil is deteriorating. He deployed military personnel to Brazil–Paraguay border and enforced checkpoints.

“Brazil is perhaps the place where there is today the greatest spread of coronavirus in the world, and that is a great threat to our country,” Benitez said. “We have to understand that this is a huge threat to the entire effort that the Paraguayan people have been making.”

Argentinian President Alberto Fernandez has also expressed concern and recently said Brazil represents a threat to South America.

Scenes of Heavily armed Colombian troops patrolling Brazil–Colombia border.

VIDEO: Colombia will increase its military presence on the Amazon border, which it shares with Brazil and Peru, to prevent the spread of imported cases of coronavirus from floating populations pic.twitter.com/nqY52tQhvw

… has soared 30% in the past two months, the most likely response is a blank stare: after all nearly 30% of companies have pulled guidance as nobody has any idea what is coming. Not even the Fed in fact: in an interview with MNI, St Louis Fed president James Bullard said the Fed may not have enough clarity on the economy by its June meeting to offer a quarterly forecast.

One thing companies do know, echoing recent similar observations from both Stanley Druckenmiller and David Tepper, is that stocks have run up too far, too fast. And, as a result, CEOs, CFOs and Treasurers are all taking advantage of the tidal wave of liquidity that has propelled many shares back to all time record levels, and are selling stock at a furious pace not seen in almost a decade.

According to Bloomberg calculations, public companies have raised more cash in the past three days – from selling shares – than in any week in eight years. Buyers have been undaunted by warnings from either Fed Chair Jerome Powell, who cautioned about unprecedented downside risk to the U.S. economy, from Goldman Sachs which we first reported said stocks could drop nearly 20% in the next three months, or by investing titans who say this is the most overbought market in history. No, these are retail investors who know better than even corporate management…

… and riding a momentum wave unlike any in recent history, are buying everything companies have to sell.

And while these same amateur traders will point to the strength in equity financing is a promising sign for the broader economy (what they really mean is that Fed backstops actually do work), the reality is that a burst of corporate selling is about as bearish as it gets, as the investors who know their own assets and growth potential best are rushing to sell their stock to a greater fool. Luckily, there is more than enough of those in the US retail investing population.

“Now’s the time to act. The rally is extremely fragile,” said Michael Purves, CEO of Tallbacken Capital Advisors, who spent 12 years advising companies on mergers and capital-raising. “When you’re a CFO or a board director of a company in a capital intensive industry, you raise money so that you don’t lose your job. That’s 100% the right thing to do now.“

Sadly for all those greater, perhaps greatest fools, who bought the shares the rally is now ending, because despite a modest short covering rally on Thursday, the market has double-topped out, unable to rise above 2,950 and is now sliding despite trillions and trillions in central bank liquidity.

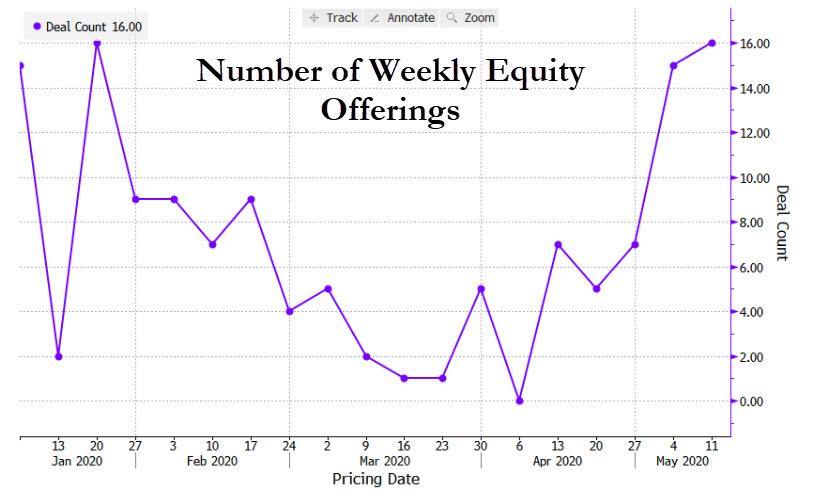

Of course, every short-squeeze in the broader market will be promptly used by companies to sell even more shares. Just int the past three days, investment banks have conducted 16 secondary offerings on U.S. exchanges since Monday in stocks such as Zillow, Equinix, MyoKardia, YETI Holdings, and Q2 Holdings Inc. And according to Bloomberg, through Wednesday that already made for the busiest week of 2020.

In fact, in just the first three days of the week, companies raised more than $17 billion from investors, the most since 2012, thanks largely to PNC Financial Services Group Inc. selling $12.1 billion of its BlackRock shares in the second-largest offering since 2009.

As Bloomberg summarized, “a scarcity of deals during the market’s March meltdown has turned into a geyser after equities recovered and issuers released their first earnings reports since the new coronavirus pushed investors away from risk.”

Since March 1, share sales by public companies and top holders have raised about $35 billion, with this week’s activity comprising half of that volume. Equity-linked offerings are also on the rise, raising $11 billion in the last two weeks – nearly double their haul from the second half of April.

Yet what is even more bizarre is that traders are rewarding these massive at times dilutions (because who cares about such things as shares outstanding at a time of central planning) by bidding their stocks up by an average of 5% from their offering prices even as the Nasdaq has suffered a 2.2% decline in recent days.

”If your stock has done well, you might do a secondary offering here because you know there’s going to be an opportunity to deploy that,” said Jerry Braakman, chief investment officer of First American Trust, in Santa Ana, California, which manages about $1.8 billion. “When people are looking at this current environment, cash is king and equity is a long-term holding.” Because of course equity is a “long-term holding” during a depression when the only liquidity out there is thanks to central banks.

There is just one problem: while it’s safe to say the situation now in the market defies historical comparison, Bloomberg points out that “the record for stocks after big surges in share sales isn’t encouraging” and usually results in broad market selling, something which the companies know too well, and is precisely why there is a firehose of equity offerings now before the window closes. Consider that monthly proceeds from secondary offerings have surpassed $30 billion on only three occasions since 2010. Three months after those spikes, the S&P 500 was trading lower every time (and on most occasions required either small or large Fed bailouts to keep the party going).

Proceeds from this month’s U.S. stock offerings have surpassed $24 billion so far, but are almost assured to cross $30 billion in the next two weeks.

via ZeroHedge News https://ift.tt/2WX3ln1 Tyler Durden

Flynn’s Lawyer Excoriates Obama In Open Letter Tyler Durden

Thu, 05/14/2020 – 19:05

Last week, former President Barack Obama reacted to the DOJ’s move to end its case against Michael Flynn by declaring in a leaked private phone call that the “rule of law is at risk,” and that “there is no precedent that anybody can find for someone who has been charged with perjury just getting off scot-free.”

“That’s the kind of stuff where you begin to get worried that basic — not just institutional norms — but our basic understanding of rule of law is at risk. And when you start moving in those directions, it can accelerate pretty quickly as we’ve seen in other places,” said the former President.

On Wednesday, Flynn’s lawyer Sidney Powell punched back – correcting Obama’s inaccurate diatribe, while managing to drop MOABs on his “wingman” – former Attorney General Eric Holder, Andrew McCabe, Loretta Lynch and others. It’s quite the read.

Re: Your Failure to Find Precedent for Flynn Dismissal

Regarding the decision of the Department of Justice to dismiss charges against General Flynn, in your recent call with your alumni, you expressed great concern: “there is no precedent that anybody can find for someone who has been charged with perjury just getting off scot-free. That’s the kind of stuff where you begin to get worried that basic — not just institutional norms — but our basic understanding of rule of law is at risk.”

Here is some help—if truth and precedent represent your true concern. Your statement is entirely false. However, it does explain the damage to the Rule of Law throughout your administration.

First, General Flynn was not charged with perjury—which requires a material false statement made under oath with intent to deceive.1A perjury prosecution would have been appropriate and the Rule of Law applied if the Justice Department prosecuted your former FBI Deputy Director Andrew McCabe for his multiple lies under oath in an investigation of a leak only he knew he caused.

McCabe lied under oath in fully recorded and transcribed interviews with the Inspector General for the DOJ. He was informed of the purpose of the interview, and he had had the benefit of counsel. He knew he was the leaker. McCabe even lied about lying. He lied to his own agents—which sent them on a “wild-goose-chase”—thereby making his lies “material” and an obstruction of justice. Yet, remarkably, Attorney General Barr declined to prosecute McCabe for these offenses.

Applying the Rule of Law, after declining McCabe’s perjury prosecution, required the Justice Department to dismiss the prosecution of General Flynn who was not warned, not under oath, had no counsel, and whose statements were not only not recorded, but were created as false by FBI agents who falsified the 302.

Second, it would seem your “wingman” Eric Holder is missing a step these days at Covington & Burling LLP. Indelibly marked in his memory (and one might think, yours) should be his Motion to Dismiss the multi-count jury verdict of guilty and the entire case against former United States Senator Ted Stevens. Within weeks of Mr. Holder becoming Attorney General, he moved to dismiss the Stevens prosecution in the interest of justice for the same reasons the Justice Department did against General Flynn—egregious misconduct by prosecutors who hid exculpatory evidence and concocted purported crimes.

As horrifying as the facts of the Stevens case were, they pale in comparison to the targeted setup, framing, and prosecution of a newly elected President’s National Security Advisor and the shocking facts that surround it. This case was an assault on the heart of liberty— our cherished system of self-government, the right of citizens to choose their President, and the hallowed peaceful transition of power.

Third, the inability of anyone in your alumni association to find “anybody who has been charged [with anything] just getting off scot-free” would be laughable were it not so pathetic.

Many of your alum feature prominently in the non-fiction legal thriller published in 2014: Licensed to Lie: Exposing Corruption in the Department of Justice. A national best- seller, it focusses on the egregious prosecutorial misconduct of your longest serving White House Counsel, Kathryn Ruemmler; your counter-terrorism advisor Lisa Monaco; Loretta Lynch’s DAG for the Criminal Division Leslie Caldwell; and Mueller protégé Andrew Weissmann. While they worked as federal prosecutors on the Enron Task Force—under the purported supervision of Christopher Wray—they destroyed Arthur Andersen LLP and its 85,000 jobs; sent four Merrill Lynch executives to prison on an indictment that criminalized an innocent business transaction while they hid the evidence that showed those defendants were innocent for six years. Both cases were reversed on appeal for their over-criminalization and misconduct. Indeed, Andersen was reversed by a unanimous Supreme Court.

Fourth, even if your many alumni don’t remember multiple cases that had to be reversed or dismissed for their own misconduct, Judge Emmet Sullivan should remember dismissing the corrupted case against Ted Stevens. Judge Sullivan is the judicial hero of Licensed to Lie. It is that case that caused Judge Sullivan to enter the strong Brady order the Mueller and D.C. career prosecutors violated repeatedly in the Flynn prosecution.

Fifth, there is precedent for guilty pleas being vacated. Your alumni Weissmann and Ruemmler are no strangers to such reversals. At least two guilty pleas they coerced by threats against defendants in Houston had to be thrown out—again for reasons like those here. The defendants “got off scot-free” because—like General Flynn—your alumni had concocted the charges and terrorized the defendants into pleading guilty to “offenses” that were not crimes. Andersen partner David Duncan even testified for the government against Andersen in its trial, but his plea had to be vacated. Enron Broadband defendant Christopher Calger had his plea vacated. There are many others across the country.

Sixth, should further edification be necessary, see Why Innocent People Plead Guilty, written in 2014 by federal Judge Jed Rakoff (a Clinton appointee). Abusive prosecutors force innocent people to plead guilty with painful frequency. The Mueller special counsel operation led by Andrew Weissmann and Weissmann “wannabes” specializes in prosecutorial terrorist tactics repulsive to everything “justice” is supposed to mean. These tactics are designed to intimidate their targets into pleading guilty—while punishing them and their families with the process itself and financial ruin.

Most important, General Flynn was honest with the FBI agents. They knew he was—and briefed that to McCabe and others three different times. At McCabe’s directions, Agent Strzok and McCabe’s “Special Counsel” Lisa Page, altered the 302 to create statements Weissmann, Mueller, Van Grack, and Zainab Ahmad could assert were false. Only the FBI agents lied—and falsified documents. The crimes are theirs alone.

Seventh, the D.C. circuit in which you reside vacated a Section 1001 case for a legal failure much less egregious than those in General Flynn’s case. United States v. Safavian, 528 F.3d 957 (D.C. Cir. 2008). Safavian sought advice from his agency’s ethics board and did not give them all the relevant info. The jury convicted him on the theory it was a 1001 violation to conceal the information from the government ethics board. The court disagreed: “As Safavian argues and as the government agrees, there must be a legal duty to disclose in order for there to be a concealment offense in violation of § 1001(a)(1), yet the government failed to identify a legal disclosure duty except by reference to vague standards of conduct for government employees.” General Flynn did not even know he was the subject of an investigation—and in truth, he was not. The only crimes here were by your alumni in the FBI, White House, intelligence community, and Justice Department.

These are just a few obvious and well-known examples to those paying any attention to criminal justice issues.

Finally, the “leaked” comments from your alumni call further evinces your obsession with destroying a distinguished veteran of the United States Army who has defended the Constitution and this country “from all enemies, foreign and domestic,” with the highest honor for thirty-three years. He and many others will continue to do so.

1As a “constitutional lawyer,” surely you recall that perjury (or false statements) also requires intent to deceive. In Bronston v. United States, 409 U.S. 352 (1973), the Supreme Court reversed a conviction of perjury. In Bronston, the defendant’s answer was a truthful statement, but not directly responsive to the question and ultimately misled federal authorities. The Court determined: “A jury should not be permitted to engage in conjecture whether an unresponsive answer, true and complete on its face, was intended to mislead or divert the examiner; the state of mind of the witness is relevant only to the extent that it bears on whether “he does not believe [his answer] to be true.” To hold otherwise would be to inject a new and confusing element into the adversary testimonial system we know.” Id. at 359. The FBI agents who interviewed General Flynn specifically noted that his answers were true or he believed his answers to be true—completely defeating criminal intent. Furthermore, General Flynn knew and remarked they had transcripts of his conversations.

Less than two years from when President Trump announced the creation of the 6th major division of the United States Armed Forces, Space Force has launched its first commercial, a thirty-second ad uploaded to the U.S. Air Force and Space Force Recruiting YouTube page.

The ad features a young man staring up at the stars while a narrator opines, “Some people look to the stars and ask, ‘What if?’ Our job is to have an answer.”

A montage flashes images of uniformed personnel, rocket launches, and satellites, while the narration continues:

“We would have to imagine what will be imagined, plan for what’s possible while there’s still impossible. Maybe you weren’t put here just to ask the questions. Maybe you were put here to be the answer.”

A pitch to possible recruits, its final humdinger ends:“Maybe your purpose on this planet isn’t on this planet.”

Since it surged into the cultural zeitgeist in 2018, the U.S. Space Force has been the subject of countless memes, cartoons, and jokes. But behind its public-facing presentation, there is a deadly intensity and momentum. Scarcely over two months ago, the branch received its first offensive weapon, a Counter Communications System (CCS) that functions as a military satellite communications jammer.

GPS satellites gather intelligence, sniff out missile launches, and facilitate precise military hits. The development of satellite communications jammers is part of the new space race taking place between the United States, Russia, and China. Orbital and sub-orbital communication warfare between satellites is widely considered to be first major theater of military space offensives.

“It’s not about putting military service members in space, it has nothing to do with NASA, it’s not about protecting Earth from asteroids or aliens,”said Todd Harrison, Aerospace Security Project Director at the Center for Strategic & International Studies.

Upon signing the 2019 NDAA, which allocated $738 billion in defense spending, President Trump stated: “Space is the world’s newest war-fighting domain.”

However, it’s hard to say what future Space Force missions could eventually include. Right now the Pentagon is rerouting over 16,000 Air Force duty and civilian personnel to Space Force assignments. They’re learning the ins and outs of successful space launches from SpaceX. They’re still figuring out their official uniform, logo, and song.

The actual mechanics and long-term objectives of militarizing space is a murky topic in the already murky depths of the military-industrial complex.

In recent years, NASA considerably bulked up its commercial/PR image. It seems Space Force is coming out of the gate doing the same with its first commercial. And though it’s unlikely that the new Netflix show Space Force (starring Steve Carell) will have any more connection to the reality of its subject matter than Reno 911 did to law enforcement, it will certainly keep the new cosmic military fleet in the pop culture limelight.

Forged in the meme-happy, Netflix-friendly crucible of a divided nation beset by tumultuous culture wars, a global pandemic, and a geopolitical space race, it’s hard to predict what Space Force will look like in 10, 50, or 100 years. But one can be fairly certain it will pack a mean marketing punch.

via ZeroHedge News https://ift.tt/2z0b8s9 Tyler Durden

Real Vision’s Managing Editor Ed Harrison is joined by Roger Hirst to discuss the latest developments in markets, macro, and the coronavirus crisis. Peter Cooper talks about how China, Hong Kong, and South Korea are facing setbacks with a new wave of cases.

via ZeroHedge News https://ift.tt/3dH2iy8 Tyler Durden

Free COVID Testing For Ultra Rich At This Miami Condo High Rise Tyler Durden

Thu, 05/14/2020 – 18:25

It must be wonderful being ultra-rich in South Florida, living in a multi-million dollar flat overlooking the clear blue water. What’s even better about being an elite in a pandemic is that you can receive free virus testing while some parts of the country suffer shortages.

A luxury condo building in South Beach, Florida, somehow obtained a bulk shipment of COVID-19 antibody tests that it plans to offer for free to its residents and employees.

Remember, a little over a week ago, Maryland Gov. Larry Hogan had a planeload of antibody tests flown in from South Korea due to shortages. He then deployed the National Guard to guard the tests at an undisclosed location because there was a risk the federal government would confiscate them.

Forbes’ Amy Dobson says Continuum South Beach, a 522-unit resort-style oceanfront condominium tower, is working with doctors from Mount Sinai hospital and USA Sports Medicine to administer virus testing in the near term.

“We’re redirecting our funds to things that are more important to our residents right now, which is health and safety,” Rishi Idnani, director of operations at the building, told Forbes. “We were able to negotiate a bulk rate for the antibody testing [that] was paid directly by the association as a service.”

Idnani said he did not provide the total number of residents in the building but said approximately 400 have agreed to be tested, along with 120 employees. Management has stockpiled six months of gloves and masks, in preparation for the hurricane season that will start later this summer. The storing was also in preparation for a possible second virus wave that could arrive in fall.

A post-corona world will drive free virus testing for residents in luxury buildings across South Florida. Several miles away on Fisher Island, the country’s most affluent zip code, the community secured test kits, according to Business Insider.

While virus test shortages remain a problem in some regions in the country, President Trump outlined on Monday that tests are plentiful.

via ZeroHedge News https://ift.tt/2LqihEW Tyler Durden

Crisis & 2020 Election: Investors Should Brace For An Earthquake Of Change Tyler Durden

Thu, 05/14/2020 – 18:05

Submitted by Joseph Carson, former chief economist of Allianz

Crisis often produces a dramatic and unpredictable change in economics, finance, and politics. If history is a guide investors should brace for an earthquake of change.

Political change might be the most consequential for investors. History shows that the crisis tends to unleash people’s resentments, grievances, and anger over inequitable policies and bad management. Transformative shifts in electorate preferences produce major changes in the federal government’s economic policies.

Four decades ago, in 1980 the US experienced a watershed election. President Jimmy Carter became the first incumbent president since Herbert Hoover in 1932 to lose an election. The surprising and substantial victory by Ronald Reagan ushered in a new form of government that focused on lower taxes and fewer regulations.

It also resulted in a major change in Congress. Republicans used the strength of Ronald Reagan’s popular landslide vote to gain 12 seats in the Senate and in the process earn their first Senate majority since 1954.

The 1980 election results reflected two powerful forces.

First, there was a strong vote against poor macroeconomic performance and leadership. In 1980, President Carter faced an economic crisis of ever-rising inflation that threatened economic instability. Based on the recommendation of his economic advisors President Carter decided to impose credit controls as part of an anti-inflation campaign.

The economic fallout was abrupt and sharp: people stopped using credit cards and were “scared away from stores”; retail businesses failed as sales plummeted; the economy posted its sharpest fall in the post-war period, millions lost jobs and jobless-rate spiked sharply higher.

Opposition to the credit controls was swift and broad. Credit controls were viewed as “overkill”, worse than the inflation disease. The damage from the credit controls was so sharp they soon became non-binding and President Carter was forced to unwind the credit restrictions within weeks after they were put in place.

The crises of 2020 and 1980 are 40 years apart but there are policy and economic similarities.

To be sure, in 2020 President Trump has been confronted with the coronavirus crisis that threatened the medical well being of the public and economic stability.

Based on the recommendation of his medical advisors President Trump placed federal restrictions on work-life, travel, and social and recreational gatherings as a way to contain the spread of the deadly virus.

The economic fallout and public outcry have been severe and sharp. Critics argued that the “cure cannot be worse than the problem itself”. The federal policy response has become uneven and at times chaotic as policymakers struggle to balance the medical and economic well-being of the general public.

The 2020 election will enable voters to express their opinion on what matters more.

Second, the 1980 election results reflected a fundamental shift in voter’s view of government. A large majority of voters soundly rejected the government programs of social expenditures and the bloated government.

That shift in voter sentiment ushered in a new way of governing with the focus on lower taxes, reduced spending on social programs, and less regulation. There have been fits and starts to this policy over the decades, but there has been a consistent and constant theme on taxes and regulation.

In 2017, the top marginal individual tax rate was lowered to 37% and 21% for business. By way of comparison, in 1980, the top marginal tax rates stood at 70% for individuals and 46% for business.

The 2020 election will enable voters to express their opinion if this shift has gone too far.

2020 presidential elections are less than 6 months away. Polls are not always an accurate barometer of current or even future voter sentiment, but current polling shows the incumbent party has a deep hole to climb. The economy’s performance and the management of the crisis rank very high in the minds of voters.

In 1980 the economy’s performance proved to be the most dominant issue on the electorate mind. With the national polls showing a tie one-week before the election Ronald Reagan ended the final debate with a challenging statement, “Are you better off than you were four years ago”?

The 1980 elections results left no doubt on the answer. Ronald Reagan won 489 of 538 electoral votes, winning 47 of 50 states and 50.7% of the popular vote compared to 41% of President Carter. (Note: an independent candidate John Anderson took 6.6% of the popular vote).

Even before the crisis of 2020, a shift in voter preferences was underway. According to the Census Bureau, 53.4% of the voting-eligible population voted in the 2018 mid-term election, the highest voter turn out since it started collecting voter numbers in 1978. That follows the lowest mid-term turnout vote of 41.9% in 2014.

Those record votes reshaped Congress with the Democrats regaining majority control of the House in 2018 for the first time since 2009 and only the third time since 1995.

The 2020 economic and election parallels to that of 1980 are striking. Investors need to brace for a watershed election. A fundamental shift in politics is underway.

The current crisis has dramatically increased the role of the federal government’s management of the economy and involvement in the financial markets. That increased dual role will come with a heavy price (greater supervisory oversight, more regulation, higher taxes on top wage earners and businesses, and possibly a wealth tax at some point).

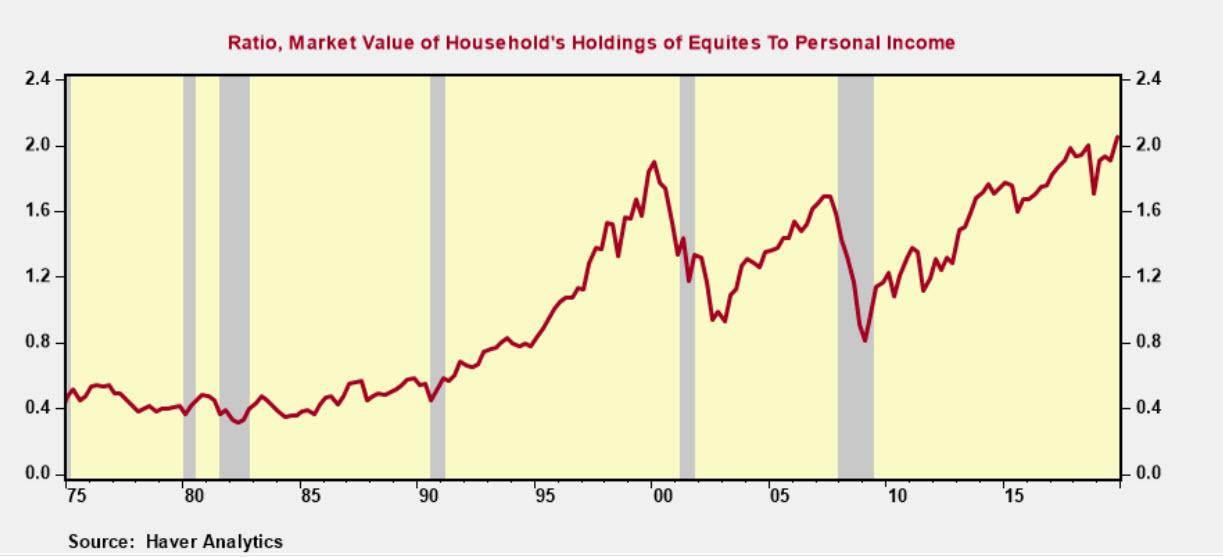

Is a reversal of fortune in the cards? At the end of 2019, people’s holdings of equities stood at 2x times the level of income, twice its long-run average. In 1980, the ratio of equity to income stood .5X times, half its long-run average.

The four-decade rise in the equity/income ratio is over as government policies shift to a less favorable tax regime and more restrictive regulatory and oversight. The question is how fast it reverts to its long-term mean of 1x times, levels that were reached after the 2000 tech bubble and 2008/09 housing crises.

The question for investors is, “Are you prepared for the next four years “?

via ZeroHedge News https://ift.tt/3fP9gTQ Tyler Durden

“These Threats Will Not Be Taken Lightly”: States Mull Crackdown On Intentional Corona Spreaders Tyler Durden

Thu, 05/14/2020 – 17:45

With the country paralyzed by lockdowns and more than 2/3 of Americans afraid to go back to work once they’re lifted, fear of catching coronavirus has grippedlarge swaths of the country.

Playing on that fear are assholes – who have begun threatening to spread COVID-19 to police, retail clerks, grocers, and anyone else they may have a disagreement with, according to Reuters. As a result, several states have begun to mull criminalizing weaponization of the virus.

Florida man James Jamal Curry charged after spitting blood and saliva into police officer’s face while claiming to have coronavirus.

New Jersey, for example, is now considering legislation which would make it a crime to issue a “credible threat to infect another with COVID-19 or similar infectious disease that triggered public emergency,” according to a spokesman for the National Conference of State Legislatures.

A few examples of said threats:

A Michigan man wiped his nose and face on the shirt of a store employee who was trying to enforce a mask-wearing requirement. The 68-year-old man was charged with misdemeanor assault and battery and, if convicted, faces three months behind bars and a $500 fine.

In St. Petersburg, Florida, a man coughed and spit on police and threatened to spread the virus as they responded to domestic violence calls to his home. He faces up to five years in prison on federal charges of perpetrating a biological weapons hoax after his test results came back negative.

A San Antonio, Texas, man claimed in a Facebook post that he paid someone to spread coronavirus at grocery stores. While his threat was deemed false, he too was arrested and charged with a biological weapons hoax. He claimed he was trying to deter people from visiting stores in an effort to prevent the spread of the virus, federal prosecutors in Texas said. –Reuters

In Philadelphia, 27-year-old Jacqueline McBride was arrested and charged with simple assault, terroristic threats and harassment after allegedly spitting on two people in a grocery store.

And who’s against criminalizing this behavior? Advocates for HIV-positive individuals, who say lawmakers need to be mindful not to make the laws so broad “that they punish poor and minority communities,” according to Reuters, which notes that over the last 40 years, at least 26 states have passed laws which criminalize HIV exposure – with crimes ranging from biting to donating blood.

And according to UCLA Law’s associate dean of public interest, Brad Sears, several studies have found that HIV criminalization laws target minorities, and are in response to a negative stereotype of “a predatory gay or bisexual man.”

We’re guessing the percentage of people who thinks that’s nonsense far outweighs those who think criminalizing COVID-19 infection threats.

In New Jersey, Republican Senator Kristin Corrado’s bill to punish anyone convicted of threatening to spread COVID-19 with up to 10 years behind bars and a $150,000 fine was before the Senate Budget and Appropriations Committee this week.

“To those who think it is cheeky to pull a sick prank like this – you will suffer the consequences of your poor decisions,” said Corrado. “These threats will not be taken lightly, and those found guilty will be punished to the fullest extent of the law.“

via ZeroHedge News https://ift.tt/2WVeuEN Tyler Durden

The core problem is the U.S. economy has been fully financialized, and so costs are unaffordable.

To understand the long-term consequences of the pandemic on Main Street and local tax revenues, we need to consider first and second order effects. The immediate consequences of lockdowns and changes in consumer behavior are first-order effects: closures of Main Street, job losses, massive Federal Reserve bailouts of the top 0.1%, loan programs for small businesses, stimulus checks to households that earned less than $200,000 last year, and so on.

The second-order effects cannot be bailed out or controlled by central authorities.Second-order effects are the result of consequences have their own consequences.

The first-order effects of the pandemic on Main Street are painfully obvious: small businesses that have barely kept their heads above water as costs have soared have laid off employees as they’ve closed their doors.

The second-order effects are still spooling out: how many businesses will close for good because the owners don’t want to risk losing everything by chancing re-opening? How many will give it the old college try and close a few weeks later as they conclude they can’t survive on 60% of their previous revenues? How many enjoy a brief spurt of business as everyone rushes back, but then reality kicks in and business starts sliding after the initial burst wears off?

How many will be unable to hire back everyone who was laid off?

As for local tax revenues based on local sales taxes, income taxes, business license fees, and property taxes: the first three will fall off a cliff, and if cities and counties respond to the drop in tax revenues by jacking up property taxes, this will only hasten the collapse of businesses that were already hanging on by a thread before the pandemic.

The federal government can bail out local governments this year, but what about next year, and every year after that? The hit to local tax revenues is permanent, as the economy became dependent on debt and financialization pushed costs up.

Amazon and online sellers don’t pay local taxes, except in the locales where their fulfillment centers are located. Yes, online sellers pay state and local sales taxes, but these sales are for goods; most of the small businesses that have supported local tax revenues are services: bars, cafes, restaurants, etc. As these close for good, the likelihood of new businesses taking on the same high costs (rent, fees, labor, overhead, etc.) is near-zero, and anyone foolish enough to try will be bankrupted in short order.

Now that work-at-home has been institutionalized, the private sector no longer needs millions of square feet of office space. As revenues drop and profits vanish, businesses will be seeking to cut costs, and vacating unused office space is the obvious first step.

What’s the value of empty commercial space? If demand is near-zero, the value is also near-zero. Local government will be desperate to raise tax revenues, and they will naturally look at bubble-era valuations on all real estate as a cash cow. But they will find that raising property taxes on money-losing properties will only accelerate the rate of property-owner insolvencies.

At some point valuations will adjust down to reality, and property taxes collected will adjust down accordingly. If municipalities think they can make up the losses by jacking up the taxes paid by the survivors, they will quickly find the ranks of the survivors thinned.

This doesn’t exhaust the second-order effects: once Main Street is half-empty, the attraction of the remaining businesses declines; there’s not enough to attract customers, and the virtuous-circle of sales rising for everyone because the district is lively and attractive reverses: the survivors struggle and give up, further hollowing out the district.

The core problem is the U.S. economy has been fully financialized, and so costs are unaffordable. The commercial property owner overpaid for the buildings with cheap borrowed money, and now the owner must collect nose-bleed high rents or he can’t make the mortgage and property tax payments.

Local governments spend every dime of tax revenues, as their costs are insanely high as well. They cannot survive a 10% decline in tax revenues, much less a 40% drop.

The metaphor I’ve used to explain this in the past is the Yellowstone forest fire. The deadwood of bad debt, extreme leverage, zombie companies and all the other fallen branches of financialization pile up, but the central banks no longer allow any creative destruction of unpayable debt and mis-allocated capital; every brush fire is instantly suppressed with more stimulus, more liquidity and lower interest rates.

As a result, the deadwood sapping the real economy of productivity and innovation is allowed to pile higher.

The only possible output of this suppression is an economy piled high with explosive risk. Eventually Nature supplies a lightning strike, and the resulting conflagration consumes the entire economy.

The Fed’s Visible Hand: Powell Buys $305 Million In ETFs In Two Days Tyler Durden

Thu, 05/14/2020 – 17:19

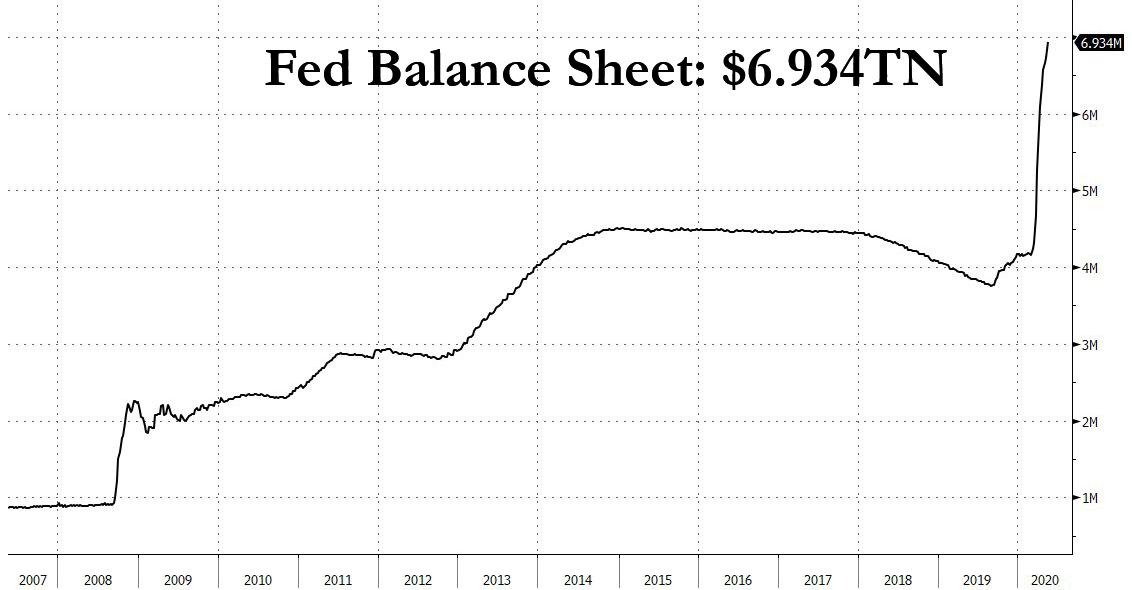

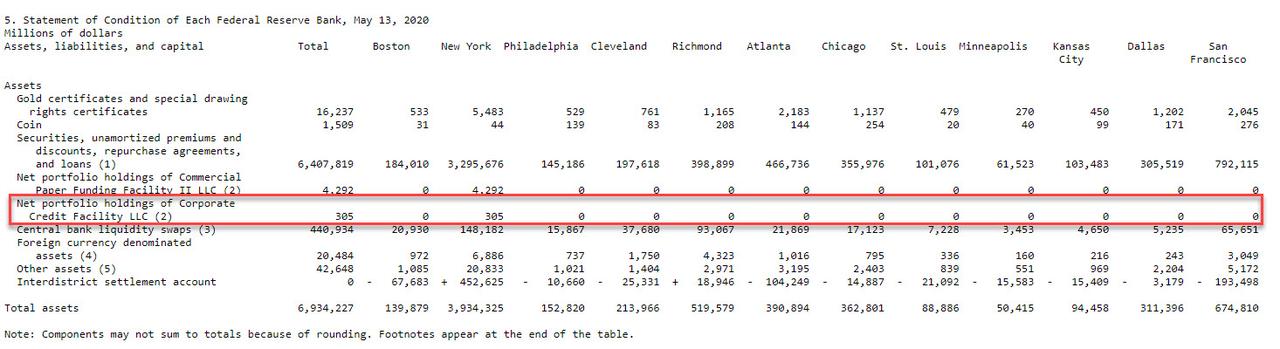

On Tuesday, the US officially crossed over into some bizarro version of a crony, centrally-planned mandated pricing model that is anything but a market when the Fed started buying corporate bond ETFs for the first time ever. Then, moments ago in its latest H.4.1 statement, the Fed – which disclosed that its balance sheet is now a record $6.934 trillion and well on its way to $12 or more than half of US GDP…

… also revealed that in the first two days the program was operational, the Fed purchased $305 million under the Corporate Credit Facility, i.e., the corporate bond ETF buying program, as of EOD May 13, or just two days after the Fed officially gave Blackrock the green light to start waving it in.

Of course, since the transactions were organized by the NY Fed which used Blackrock as agent for the buying, all of the ETFs were parked at the New York Fed.

Bloomberg’s ETF expert, Eric Blachunas, was sure he had observed the Fed in action two days ago when he noticed a jump in both LQD and HYG volumes around mid-day, which appears to be the time Blackrock will be active in the market for all those who feel like frontrunning the world’s largest asset manager, which in turn is frontrunning the world’s largest central bank.

HISTORY MADE: Looks like Fed made good on word as $LQD & $HYG both saw volume jumps today (via some sizable trades mid-day). No way to know for sure it was them, but given what they said yest & non-corp bond ETFs like $AGG, $TLT didn’t see similar jump, there’s good chance IMO. pic.twitter.com/WafG9bwhFk

What is a bit concerning is that even after the Fed bought millions in LQD on the 12th, the ETF closed red. However, Blackrock redeemed itself on the next two days when LQD posted a solid rebound, rising above 128 for the first time since May 5.

What next? Well, those hoping that the Fed’s ETF buying will serve as a stop brake any time there is even a whiff of selling, may want to read the following caveat from Bank of America:

… the maximum amount of ETF purchases may be lower than the $28bn and $8bn we estimated for IG and HY, respectively, as the Fed plans to rely on a number of additional factors to determine eligibility. These include management style (perhaps only passive?), concentration in banks, average maturity, AUM, liquidity and leverage.

So for those who plan on frontrunning the Fed, do it now instead of waiting until Blackrock finds outself out of ammo and a new crash is required to reset the Fed’s buying parameters.

via ZeroHedge News https://ift.tt/2T6HVCI Tyler Durden

{kind=link}