Hard-working Americans that pay taxes should be more than angry over how little respect the politicians in Washington have for their tax dollars...

An article that appeared on MarketWatch details what people that receive an undeserved 1,200 dollar stimulus checks under the CARES Act should do. The answer appears just over halfway down on the page in answer to the following question;

Question: I believe that my adult son received a $1,200 EIP, via automatic deposit to his checking account, that he was not entitled to because he is my tax-return dependent. Will the IRS go into his checking account and debit it to get the money back?

Answer: No. The statutory language in the CARES Act that set the whole EIP scheme in motion says that anybody who gets more money than they are actually entitled to can keep the excess. I endorse that concept: any money that gets into people’s hands is fair game.

In the above case, it appears the fella received the money in error but I have heard, and I’m also under the impression the same issue exists in the case where a check is sent to somebody that is deceased. The article explains the Feds are using our beloved Internal Revenue Service to distribute these so-called Economic Impact Payments (EIPs). The IRS is not currently processing 2019 returns because the agency is swamped with all the new COVID-19-related tasks it has been given.

The article also states the IRS’s data processing systems were notoriously inadequate even before getting overwhelmed with all these new tasks.

Apparently to those in our government, 1,200 dollars isn’t worth the time it takes to do the administrative job of reclaiming it.

From what I understand we are talking about checks that total several billions of dollars. This type of waste is just another example of why people don’t like paying taxes.

Here Are The Problems WIth Trump’s Plan To Reopen The Economy

On Thursday, the Trump administration released a three-phase plan for reopening the economy.

Each phase would ensue after only a 14-day period to determine the impact on health statistics, so in theory the “new normal” could be achieved in 28 days. If this were to actually happen it would be very bullish for the economy and markets. However the actual pace of re-opening will be determined by the states, not the federal government.

Here are the details:

Phase one: most restrictions remain in place, but “some large public places — including restaurants, movie theaters, sporting venues and places of worship — would be allowed to operate under strict physical distancing protocols. Elective surgeries could resume and gyms could reopen as long as they maintained physical distancing.”

Phase two: nonessential travel resumes, schools reopen and bars open with “diminished standing room occupancy.”

Phase three: this is essentially the “new normal”. Assuming downward trends in cases, allow “public interactions” with physical distancing and unrestricted staffing of worksites, resume visits to care homes and hospitals, and further ease capacity restrictions at bars.

There are problems, starting with the fact not a single state currently meets the criteria for a reduction in new covid cases:

The first criteria for Trump’s reopening plan? States must have a 14-day downward trajectory of COVID-19 cases.

That aside, Bank of America notes three potential roadblocks to implementing this plan.

First and foremost, it is not clear how the US public health system will meet the recommended standards for re-opening. The plan suggests that states looking to re-open should have seen a 14-day downward trend in cases. They should also have: (1) widespread availability of tests, not just for the seriously sick and health care workers, (2) the ability to aggressively track cases and isolate those who may be affected and (3) the ability to quickly and independently supply enough medical equipment and increase ICU capacity to meet surge demand. Alas, all three of these conditions will be challenging to meet.

A second concern is that the 14-day waiting period between phases is too short to determine the impact of the rule changes on the course of the disease. That is the incubation period for an individual case, but in group situations incubation occurs in a rolling fashion. In addition, people might wait a few days to get tested after their symptoms arrive and it takes time for tests to be completed. Therefore, only people who got infected as soon as restrictions were lifted would test positive within a 14-day window. And if a new outbreak occurs, the number of infections would probably be higher later in that window. Given these considerations, we expect states to wait at least a month to move from one phase of the plan to the next.

Third, the devil is in the details. The plan offers very little insight into how social distancing can be practiced in activities that involve large crowds:

How can a bar possibly require that people have masks on at all times and stand at least six feet apart?

How do you get thousands of people in and out of a sports arena without a massive increase in the number of close contacts?

Even if people sit 6 feet apart, they still need to go through turnstiles, visit the bathroom and buy food and drink. The same applies for larger concerts, church services, public transportation, etc.

In summary, private businesses will adopt a conservative approach even if they are allowed to re-open. For example, the MLB is talking about bringing back baseball games only in Arizona (where the outbreak has been relatively contained), with no crowds and players isolated in hotels. The PGA is not planning to resume golf tournaments until at least June.

BofA’s conclusion: the Trump admin plan is a nice outline of the economic side of the reopening process, however, when governors look to implement the re-opening they will need to address all of these issues—adequate testing and tracking, time to assess the impact of policy changes and details of how to maintain six-feet and other social distancing rules.

There is also the “resistance” dimension which has to be considered, namely that it is not unlikely that one or more governors may delay reopening their states just to impair the economy and thus Trump’s chances of re-election. Of course, by doing so said governors also risk a violent public backlash with an increasing percentage of the population demanding a return to normalcy, and as such any forced delays – or fabricated data and/or projections – could end up being a double-edged sword.

In any case, the release of Trump’s ambitious plan does not impact BofA’s economic forecasts, and the bank continues to expect a very slow reopening process, with most of the re-engagement happening in June.

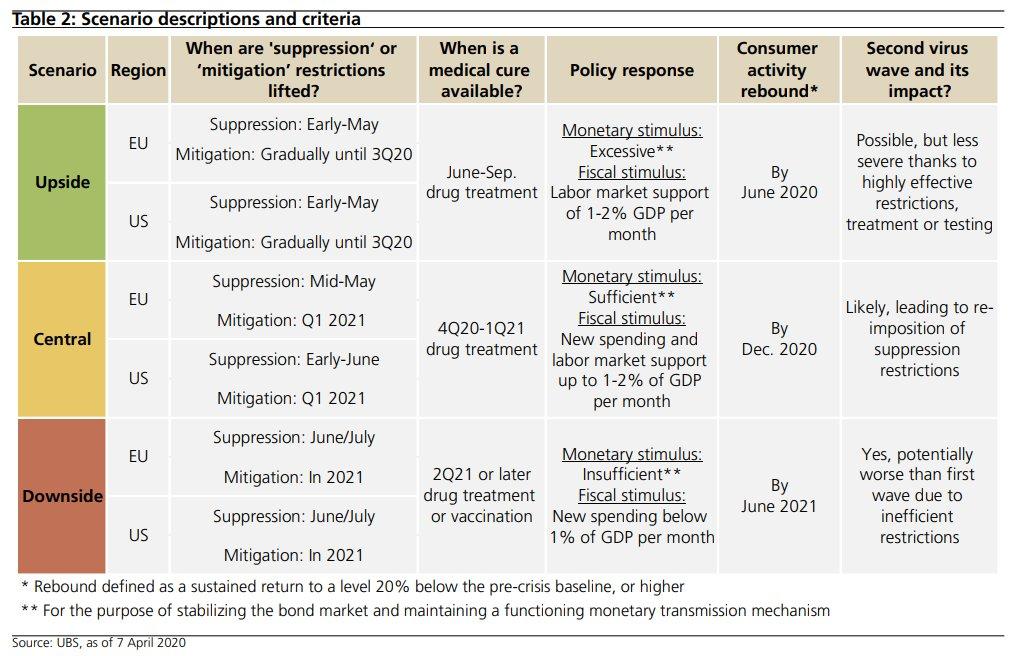

Incidentally, while it remains to be seen how efficient the Trump plan will be, here is a matrix from UBS which lays out an Upside, Central and Downside scenario for a longer-term view of a US reopening…

… which suggests that a return to normalcy may take place anywhere between Q4 of 2020 in the best case, or be delayed as far back as 2021, by which point the US economy – stuck in a nearly two-year depression – will be pale shadow of its former self.

This week’s newsletter will be somewhat condensed as the bulk of our current positioning is based upon the information contained in the two reports referenced herein. The goal of this week’s letter is simply to outline the market ranges which fall within the context of our current Macroview.

With that said, let’s get to work.

In this week’s #MacroView,I reviewed the history of monetary programs and the training of investors to respond to the “ringing of the bell.”

“As each round of ‘Quantitative Easing’ was the ‘neutral stimulus,’ which was followed by the ‘potent stimulus’ of higher stock prices, Not surprisingly, after a decade of ‘ringing the bell,’ investors have been conditioned to respond accordingly.

It is worth a trip back through history to evaluate the relationship between the Fed’s monetary interventions, and the impact on asset prices.”

While the report details the history of repeated rounds of monetary stimulus to offset potential “credit events” that never occurred, the most relevant period to review is 2008, which is most akin to the situation we are currently experiencing. A credit-event coupled with a major economic recession.

“2008: March – Bear Stearns fails, mortgage defaults start to rise, credit conditions worsen, and yield spreads rise. September – Lehman fails and freezes credit markets. Asset prices decline sharply, triggering margin calls, and the Fed floods the system with liquidity. As discussed last week:”

The reality of the economic devastation begins to set in as unemployment skyrockets, consumption and investment contract, and earnings fall nearly 100% from their previous peak, as the market declines 26% into late November. It was then the Federal Reserve launched the first round of Quantitative Easing.

Stocks staged an impressive rally of almost 25% from the lows. Yes, the bull market was back! Except that it wasn’t. Over the next few months, the Fed’s liquidity was absorbed by the “gaping economic wound,” and the market fell another 28.5% to its ultimate low.”

There are currently LOT’S of excuses to rationalize and justify the rally:

The markets are looking past 2020 earnings.

The market is looking at the eventual recovery.

The market is rallying because of the Fed.

Rationalizing fundamentally unsupported advances typically have a “payback” consequence when you least expect it. This is particularly the case when you view the recent rally from a lens of:

Never before seen levels of jobless claims

Depression level unemployment rates

An earnings and profit collapse

The largest single GDP decline in history

A loss of 1/3 of small businesses, which comprise nearly 45% of GDP.

A loss of the biggest driver of asset prices over the last decade – stock buybacks.

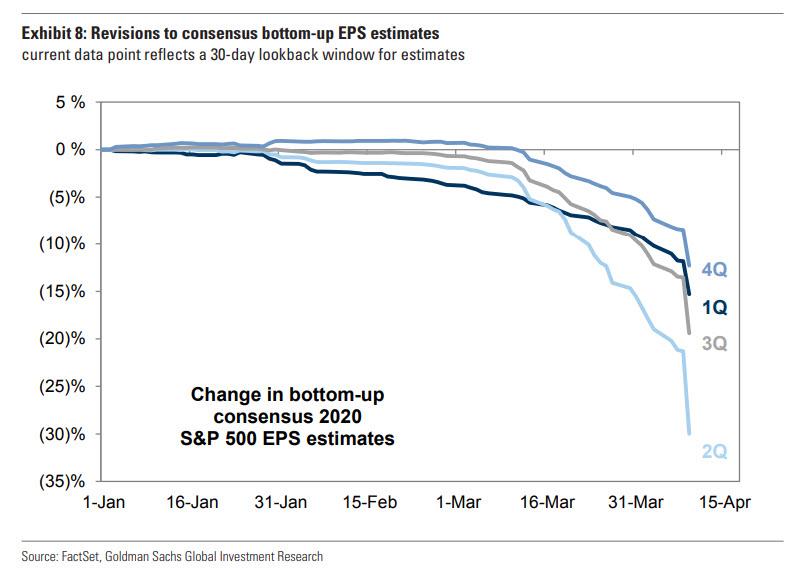

The chart below shows the most current estimates as of April 2020. As you can see, earnings are expected to decline from Q4-2019 levels of $139.47 to $136.18 and $131.09, respectively in Q1 and Q2 of 2020. That is a decline of -2.3% in Q1 and a total decline of -6% in Q2.”

“So, with the entire U.S. economy effectively shut down, 15-20% unemployment, and -20% GDP, earnings are only expected to take a 6% hit?

In 2008, without an economic shutdown, S&P 500 earnings fell from $84.92 to $6.86. That is a decline of 92% from the peak, and earnings did not fully recover until 3-years later in Q3-2011.

Or in 2000, during the “dot.com crash,” earnings fell from $53.70 to $24.69, or a decline of 54%. Earnings did not fully recover until 4-years later in Q2-2004.”

Do you really believe that stocks have priced in a real earnings collapse?

If you honestly think they have, then why is the market trading at 19x forward operating earnings, which is higher than both 2002, and the February 2020 peak?

“While 2008 was bad, the impact from the ‘economic shutdown’ due to the virus will be substantially worse for several reasons:

In 2008, the economy was already slowing down, unemployment was already on the rise, and businesses were adjusting for the related impact to earnings. Also, despite the ‘crisis’ caused in the mortgage market, businesses and consumer activity remained ‘open.’ Outside of the real estate and finance industries, many other sectors were only marginally affected.

In 2020, the shuttering of the economy caught many businesses ‘flat-footed’ and ill-prepared for an involuntary ‘shuttering’ of business.

In 2020, the surge in unemployment, combined with a shuttering of business, will have a substantially deeper impact on gross consumption in the economy than in 2008.

As opposed to 2008, there are many businesses which will never reopen, many more will be very slow to recover, with the rest slow to rehire until demand returns.

The markets are currently rallying on a flush of liquidity, and a massive short-covering rally, which is likely reaching its “exhaustion” stage. Over the next few months, stocks will begin to price in the severity of the economic damage, a substantial decline in earnings, and the realization that hopes for a ‘V-Shaped’ recovery are not likely.”

Whatever rally is left currently in the market is still very likely a “gift” to sell into.

The Ranges

Yes, the economic and fundamental data is pretty discouraging. However, despite the “bearish” backdrop, the market has rallied hard on optimism of getting the country “re-opened,” but, in actually as stated above, more so from the “Pavlov’s response” to the ringing of the Fed’s “liquidity bell.”

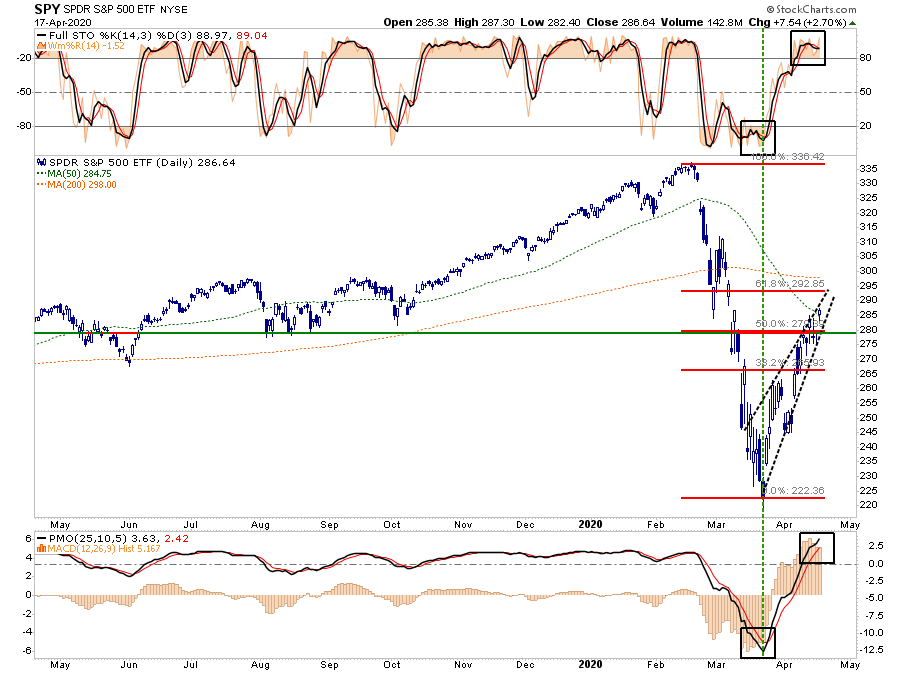

Currently, the market has rallied back to the “target zone” we laid out in mid-March.

On a very short-term basis, the previous “deep oversold” condition that provided the “fuel” for the rally has been reversed. On Friday, all primary “overbought/sold” indicators are now fully stretched back into overbought territory.

One of our ongoing concerns with the rally, has been the lack of participation and the “low volume” rally.

“In eight bear markets across the three indexes since the 90s, the bottom was usually marked with a bang, not a whimper. Trading volume in the first 10 days of the turnaround on all but one occasion (the Stoxx 600 in March 2009) was at least 10% higher than the volume in the bear market as a whole.

This year, all three indexes failed the test. The first 10 sessions after the local low saw average trading volume of ~98% the bear-market average for the S&P 500, ~94% for the Dow Jones and ~104% for the Stoxx 600.

Yet conviction was stronger on the way down than on the way up, and that’s a worrying sign. More study is needed, but on volume alone, this bear market doesn’t appear to be over.” – Eddie van der Walt via Bloomberg,

With the market overbought, this leaves more “sellers” who were trapped during the previous decline with a better opportunity to exit. This will particularly be the case as the data worsens over the weeks ahead.

If we look at our weekly indicators, the recent rally is much less “inspiring.”Both of the primary weekly “sell signals” remain intact suggesting the recent rally will fail. A failure from current levels would suggest a retest of the bullish trend line. (A failure of that trendline will set up a retest of the March 23rd lows.)

I know…I know. I’m being all “bearish and ***” by paying attention to “risk.”

So, here is your short-term “bullish” view.

If we set aside the fundamental and economic data for the moment, the short-term technical backdrop is indeed bullishly biased. The 50% retracement level was taken out on Friday, along with the 50-dma. (This is not a confirmed break unless it holds above those levels through next Friday.)

Friday’s close brings the 61.8% retracement level AND the 200-dma into focus as the next resistance levels. This suggests upside in the market of 4.5% to 7% currently.(Certainly nothing to sneeze at, considering such would normally be considered a decent year’s worth of returns. That just shows how skewed things are currently.)

The downside risk ranges are a bit more disappointing.

-4.7% to the previous 50% retracement level: risk/reward equally balanced.

-12.5% to the previous higher low: risk/reward is mildly out of favor.

-20.5% to the March 23rd low: risk/reward extremely out of favor.

From an optimistic view, a reopening of the economy, a virus vaccine, and an immediate return to low single-digit unemployment rates would greatly expand the bullish ranges for the market.

However, even a cursory review of the data suggests a more “realistic” view. The economic damage is going to be with us for a while, and until earnings estimates are revised substantially lower to reflect the “actual economy,” I have to presume the relevant risks outweigh the current reward.

This doesn’t mean we aren’t long-equities. We are, but we are also carrying a much heavier exposure to cash, and have reduced exposure to fixed income. We continue to be selective buyers of quality companies opportunistically and will continue to prudently build our portfolios.

This is just our approach, and certainly isn’t for everyone. However, after surviving two previous bear markets, experience has taught us much about “managing risk,” which was summed up nicely in a quote on Friday.

“I would say basically we’re like the captain of a ship when the worst typhoon that’s ever happened comes. We just want to get through the typhoon, and we’d rather come out of it with a whole lot of liquidity. We’re not playing, ‘Oh goody, goody, everything’s going to hell, let’s plunge 100% of the reserves [into buying businesses].’

Nobody in America’s ever seen anything else like this. This thing is different. Everybody talks as if they know what’s going to happen, and nobody knows what’s going to happen.” – Charlie Munger.

We agree with Charlie and Warren on this, and it is our philosophy for protecting our clients. We will continue to follow our process until there is actual visibility into corporate earnings and fundamentals.

While it may seem silly, we believe the process of investing is not about “guessing,” but rather “knowing,” what you are buying.

“Under Siege” – Social Unrest Unfolds As Frustrated Americans Demand Reopening Of Economy

We laid the groundwork for readers over the last three weeks that social instabilities could materialize during or after the pandemic. It has become clear that protests in Lansing, Michigan, on Thursday (April 16), was the beginning of the lockdown-backlash that is now unfolding across the country.

Americans are becoming increasingly frustrated with state governments that have closed their economies and issued strict stay-at-home public health orders, resulting in one of the worst economic crashes in the country’s history.

More than 22 million people have lost their jobs in a month, and the true extent of the crash won’t be realized until the second half of the year. The one thing we do know is the financial crash has been so severe that it has forced people to organize on social media to mobilize en mass at their respective state capitol buildings across the country, demanding their governors reopen the economy and return life to normal.

The lockdown-backlash sounds like a revolution is in the making. And, of course, every revolution has a song, and maybe this Nickelback song “Edge Of A Revolution,” already circulating on some pro-Trump feeds, could be it.

As for Saturday’s protests, Infowars’ Owen Shroyer is planning one at the Texas state capitol in Austin. The rally is called “You Can’t Close America,” which is directed at the Texas state government to put an end to the draconian measures that have confined people to their homes for nearly a month.

In Maryland, a protest organization known as Reopen Maryland is already underway in locking down streets around the state capitol building in Annapolis.

“We are the strongest country on the planet and have put a man on the moon, there is no compelling reason why we can’t protect the sick and vulnerable and get our economy back to work,” the Facebook event says.

The group has 13,000 members on Facebook. By Saturday afternoon, dozens of vehicles, presumably from the group, were shutting down streets.

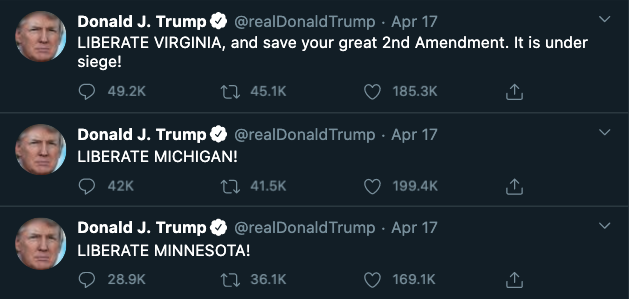

From Oregon, California, Idaho, Minnesota, Michigan, Florida, Virginia, and Maryland, thousands of people are ignoring social distancing rules and are protesting their state governments to reopen the economy on Saturday.

In a series of tweets on Friday, appearing to kick off the protests for this weekend, President Trump tweeted: “LIBERATE MICHIGAN!,” “LIBERATE MINNESOTA!,” and “LIBERATE VIRGINIA, and save your great 2nd Amendment. It is under siege!”

Stephen Moore, a member of President Trump’s council to reopen the country, launched a protest in Wisconsin on Saturday. Here are some scenes from the rally:

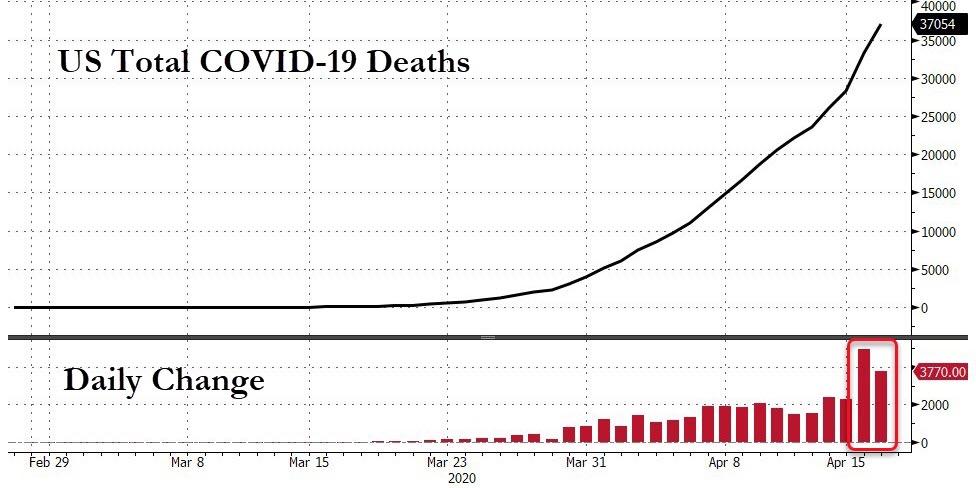

President Trump released plans on Friday to reopen individual states in phases that were currently experiencing a flattening in the cases and deaths.

The president is eager to reopen the economy to save it from a crushing depression. The danger of reopening an economy too soon is that it could spark a second wave.

People are protesting across the country, ignoring social distancing rules and lacking proper health gear, which could result in a further spread of the virus. Nevertheless, the attempt to reopen will be a failure, just look at what’s happening in China… However, we suspect the protests will grow over the next couple of weeks.

Illinois pension plans are in serious trouble. So serious, the states seeks a federal bailout. Cities are in trouble too!

The president of the Illinois State Senate seeks $40 billion to help the pension system, fund unemployment insurance and aid hospitals and cities according to the New York Times.

The letter, sent this week by State Senator Don Harmon, also seeks a $15 billion grant to “stabilize the state’s budget,” $9.6 billion in direct aid to Illinois’s cities, $6 billion for the state’s unemployment insurance fund, and hardship money for hospitals and nursing homes, among other things.

Messages left for State Senator Bill Brady, the minority leader, were not immediately returned on Friday evening. Democrats hold 40 of the State Senate’s 59 seats.

Illinois is Insolvent

I was certain this would happen, but the way this happened is a bit unexpected. Some of the state pension plans will run out of money in as little as 2-7 years.

Many pension funds across Illinois were running out of cash even before the Coronavirus reared its ugly head. Some funds were even on the brink of becoming pay-as-you-go plans, where pensioners are forced to rely directly on employer operating budgets, and not pension fund assets, to get their retirement checks.

The proof is in the collapsing asset-to-payout ratios of most Illinois pensions. That ratio – which is one of the statistics Moody’s Investors Service uses to measure pension health – compares a fund’s total assets to how much it pays out in benefits each year. In other words, it measures how many years a pension plan can make benefit payouts before it runs out of money, assuming no new contributions or investment income.

Illinois’ worst-off funds only had two to five year’s worth of payouts left in 2018. They were among the most insolvent in the country. The COVID-19 market meltdown will have only shrunk their assets further.

Illinois and Chicago Pension Plan Funding

Take, for example, the Chicago firefighter fund. In 2018, its total assets were $1.1 billion and its pension payout for that year was $330 million. That means it had about 3 years’ worth of payouts on hand – an asset-to-payout ratio of 3.4. There are just a handful of funds in the nation with lower ratios than that.

By comparison, the plan’s assets amounted to nearly 10 years’ worth of payouts in 2000.

Chicago’s firefighter plan is now dangerously close to becoming a pay-as-you-go pension plan. That would make firefighters dependent on the city – which is already junk rated and effectively bankrupt – for their retirement checks.

…

It’s not just the firefighters’ fund that’s in trouble. It’s the same thing for Chicago police. Their funds’ ratio was just 4.1 in 2018. Chicago municipal had a ratio of 4.7 years. With the markets and bond yields down significantly, Chicago’s funds are now in a precarious position.

The state’s funds are only slightly better off. Illinois’ biggest fund, the state Teachers’ Retirement Fund, had a ratio of just 8.2 in 2018. At the turn of the century, it had 17 years’ worth of payouts.

The State Employees Retirement System had a ratio of only 7 years.

Worst of all is the Illinois lawmakers’ fund, which had just 2.5 years worth of payouts.

There is much more bad news in the article. Including a look at various cities.

Wirepoint Concludes

If the market meltdown persists for much longer, expect the city of Chicago’s rating to fall further and for the state’s to end up in junk. The consequences of both would be huge. But so far, Gov. J.B. Pritzker and Mayor Lori Lightfoot continue to reject an amendment to Illinois’ pension protection clause.

But soon, they may be forced to choose between either chaos or reforms. Barring state bankruptcy, pension reform is the only way to cut Illinois’ strangling debts and to keep pension fund asset-to-payout ratios from plunging straight to zero.

No Bailout

Illinois does not deserve a bailout. Its pension woes are of it own making, and have nothing to do with the coronavirus.

The state and cities need serious reform starting with the state allowing cities to declare bankruptcy.

Trump could easily have passed national bankruptcy reform in his first Congressional term but he failed to do so. Now Democrats would likely block it.

Two Things

Bankruptcy Reform

Pension Reform

Illinois needs both, and both are up to the state, not the federal government.

Getting Out Of Dodge: After Exiting Loans And Hiking Mortgage Standards, JPMorgan Stops Accepting HELOCs

Earlier this week, JPMorgan reported that its loan loss provision surged five fold to over $8.2 billion for the first quarter, the biggest quarterly increase since the financial crisis (even if its total reserve for losses is still a fraction of what it was during the 2008-2009 crash).

And while Jamie Dimon was mum on how much more losses the bank may be forced to take in coming quarters to offset the coming default surge (something we discussed in Houston: The Banks Have A Huge Problem), it hinted that things are about to get much worse when it first halted all non-Paycheck Protection Program based loan issuance for the foreseeable future (i.e., all non-government guaranteed loans) because as we said “the only reason why JPMorgan would “temporarily suspend” all non-government backstopped loans such as PPP, is if the bank expects a default tsunami to hit coupled with a full-blown depression that wipes out the value of any and all assets pledged to collateralize the loans.”

Then, just a few days later, the bank also said it would raise its mortgage standards, stating that customers applying for a new mortgage will need a credit score of at least 700, and will be required to make a down payment equal to 20% of the home’s value, a dramatic tightening since the typical minimum requirement for a conventional mortgage is a 620 FICO score and as little as 5% down. Reuters echoed our gloomy take, stating that “the change highlights how banks are quickly shifting gears to respond to the darkening U.S. economic outlook and stress in the housing market, after measures to contain the virus put 16 million people out of work and plunged the country into recession.”

In short, JPM appears to be quietly exiting the origination of all interest income generating revenue streams over fears of the coming recession, which prompted us to ask “just how bad will the US depression get over the next few months if JPMorgan has just put up a “closed indefinitely” sign on its window.”

That question was especially apt today, when JPM exited yet another loan product, when it announced that it has stopped accepting new home equity line of credit, or HELOC, applications. The bank confirmed that this change was made due to the uncertainty in the economy, and didn’t give an end date to the pause according to the Motley Fool.

Like in the other previous exits, the move doesn’t affect customers who already have HELOCs with the bank. They’ll still be able to withdraw funds on their existing HELOCs as they wish.

With HELOCs generally seen as riskier for banks than purchase or refinance mortgages as they represent a second lien on the home, it was only a matter of time before the bank – which had already exited new first-lien loan issuance would but up a “closed” sign on this particular product.

In short, JPMorgan wants no part of the shitstorm that is about to be unleashed on middle America, and especially the housing sector which is about to be hammered like never before.

While the U.S. housing market was on a steady footing earlier this year, all hell broke loose as a result of the economic paralysis and deepening depression resulting from the Coronavirus pandemic. And with would-be home buyers unable to view properties or close purchases due to social distancing measures, the health crisis now threatens to derail the sector, especially as banks are going to make it next to impossible to get a new mortgage.

To be sure, as we reported last week the residential mortgage market is already freefalling after borrower requests to delay mortgage payments exploded by 1,896% in the second half of March. And unfortunately, this is just the beginning: last week, Moody’s Analytics predicted that as much as 30% of homeowners – about 15 million households – could stop paying their mortgages if the U.S. economy remains closed through the summer or beyond. Bloomberg called this the “biggest wave of delinquencies in history.”

This would result in a housing market depression and would lead to tens of billions in losses for mortgage servicers and originators such as JPMorgan.

It was autumn 1989. Momentous things were taking place in the world.

The Berlin Wall had fallen. The people of the Eastern Bloc had succeeded at getting to the West through Hungary. The firm line between east and west was wavering. The situation was moving away from the course that Warsaw Pact communist governments had charted: that their populations must remain captive within the borders of the Communist Bloc.

It was unclear whether this social contagion for freedom would spread into Czechoslovakia.

But then November 17, 1989, arrived, a day etched in history. This was Students Day, a legal holiday. Everything had to close under government fiat. People were off school and off work. But some folks were agitated about prior government actions which many saw as abuses.

When the government gave the people of Czechoslovakia that day off, it was like a match to tinder. The small flame grew into a big one.

It was a revolution noted for its bloodlessness. The Velvet Revolution, we call it today, leaning on what the Czechs called it. People, for as far as the eye could see, gathered in a giant square in Prague and called for the ouster of their government.

In the face of the idea that saying the wrong words politically could be toxic to one’s health, much like in America today, some did not resort to speaking words against their government. They merely pulled their keys out of their pockets and jingled them.

The message was clear.

Imagine tens of thousands of people jingling their keys at once.

Imagine the horror that would fill you, as a member of the communist government, looking out the window at a crowd, visible as far as the eye could see, and knowing that this delicate sound being made by each individual, growing into a horrifying sound in unison, called for your ouster.

What could a government minister, sitting at their desk, overlooking the square, even have imagined that sound to have been the first time it arose?

How ominous. How threatening. How deeply horrifying it must have been to peer out that window. The day of reckoning had finally arrived.

At that moment, a question was answered for them: what is the last thought that goes through a tyrant’s head? That is the thought that flashed through theirs as they realized what that sound was: reckoning. It had finally arrived. Were the government ministers thinking those thoughts as the keys jingled below them?

The people of Czechoslovakia remained largely peaceful.

By the end of the year, Czech dissident Vaclav Havel, who had been in prison earlier that year, would be installed in Prague Castle. The beloved Alexander Dubcek, the Slovak hero of the 1968 Prague Spring, would be his right-hand man.

The present-day American state’s response, in ways, goes beyond the communism of even the USSR. The Soviets actually wanted their economy to work. They wanted to beat the West. Churches remained open and remained an important part of society, both for political use, and because the people wouldn’t have it any other way.

But just as the communists of Eastern Europe didn’t back down until they were forced to, the lockdowns of today won’t stop unless government officials fear resistance.

There is a chance right now, with many unhappy Americans and many idle hands, much like Students Day, November 17, 1989, to tell the government “no more.”

Will they be pushed out of office? Will it be peaceful? I don’t know. Time will tell.

But it is time for this to stop. And daily, more people grow angry at being lied to as they witness the mass destruction of their country and culture in the spring of 2020.

It wasn’t the jingling of keys that escorted the evil communists from power in 1989. It was the threat of what all those people jingling keys could do if those in power did not step aside.

Retaining political influence depends dearly on timing. Some of those communists who knew when to step aside, who knew how to apologize, had prosperous careers long after the revolution, some to this very day.

In sharp contrast, the far more stubborn Nicolae Ceausescu of regional neighbor Romania was put to death by a firing squad on December 25, 1989.

We have reached a point where government officials have yet to admit that there is a real cost in terms of life and health that comes with bringing the economy to a standstill. And these same politicians and experts have yet to show that the benefits of their lockdowns are greater than the costs imposed. The models have been shown to be wrong.

Everyone is entitled to a mistake. But to continue making the same mistake repeatedly, destroying lives, amounts to malice.

In my daily life, I am increasingly seeing my country turn into a tinderbox that the disconnected leaders, elected and unelected, cannot imagine and must not toy with. To do so is dangerous for us all.

Not next month, not next week, not tomorrow. Today is the day for the government-imposed lockdowns to stop.

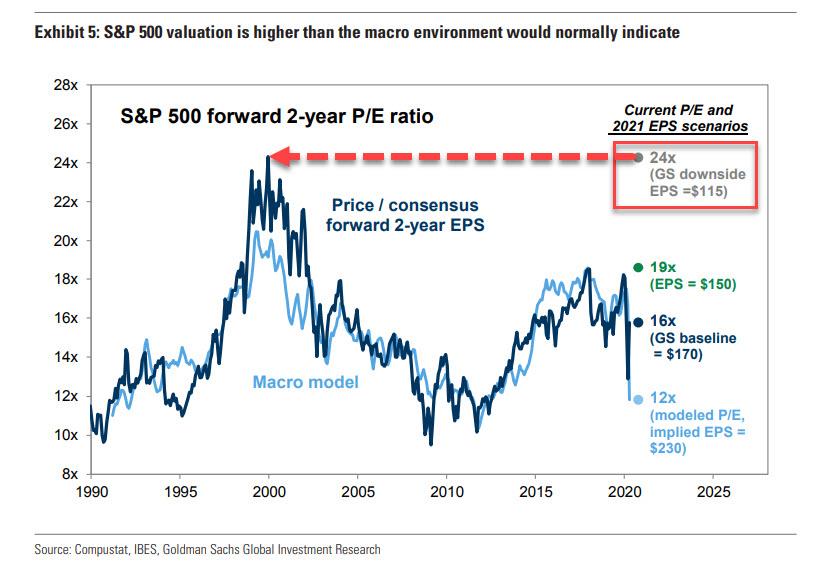

“The Fed Is All The Buyers Have”: The Banks Agree Stocks Have Never Been More Expensive

Late last week, we showed a chart from Credit Suisse which we described simply as “insanity” because it demonstrated that as the US careened into a depression, with GDP crashing and the unemployment rate soaring, between the latest Fed-driven surge in stocks and the collapse in earnings estimates, the PE multiple on the broader market had eclipsed the previous record of 19.0x set during the market’s February all time high, and had now hit a new all-time high of 19.4x. In other words, the market has never been more overvalued than it is right now.

The chart eventually made its way to Jeff Gundlach who yesterday tweeted that “U.S. GDP looks to be down 15%ish, unannualized, from its peak. SPX is presently down a similar amount from its peak. Ergo (and I over simplify to make a valid point) stocks now are back to the Feb 19th highs from a valuation perspective. “In Fed We Trust” is all the buyers have.”

U.S. GDP looks to be down 15%ish, unannualized, from its peak. SPX is presently down a similar amount from its peak. Ergo (and I over simplify to make a valid point) stocks now are back to the Feb 19th highs from a valuation perspective. “In Fed We Trust” is all the buyers have.

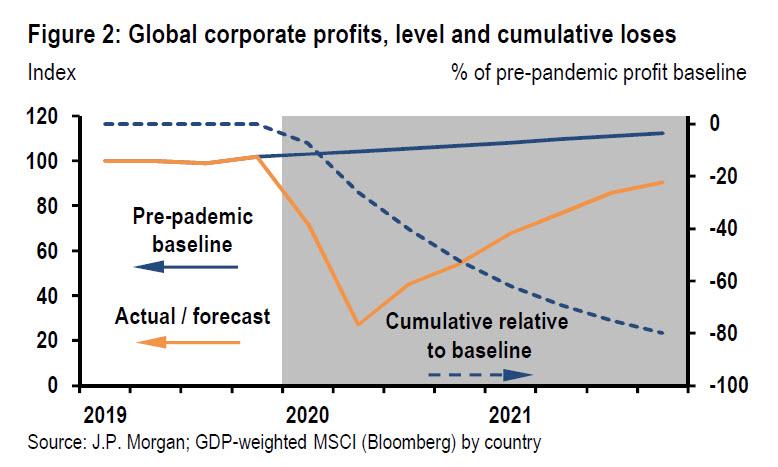

Gundlach’s math is not quite correct because as JPMorgan showed last week, the beta of corporate profits to moves in GDP is about 7x during financial crises. As a result, according to the bank’s chief economist Joseph Lipton, in the current recession in which JPM expects global GDP growth to collapse by the same 9.8%-points in Q2, the bank is applying the same profit drop beta of seven—on par with the global financial crisis– which implies a plunge in corporate profits of roughly 70% in the year through 2Q20.

Meanwhile, with every passing day the fundamental disconnect is getting worse, because as stock prices soar (mostly due to momentum-chasing machine buying while humans sell) earnings estimates are cashing…

… with Goldman calculating that its latest bear case PE multiple (on 2021 earnings no less as nobody is looking at 2020 anymore) is now a dot com bubble-eseque 24x.

Meanwhile, crashing the bulls’ party, or rather their expectations for a V-shaped recovery, JPMorgan also cautioned that corporate profits won’t recover their pre-pandemic baseline until some time in 2022 if not 2023, which is terrible news for Wall Street strategists as it means they will now have to apply even more ridiculous forward multiples from 2023 for their optimistic recos to make any sense.

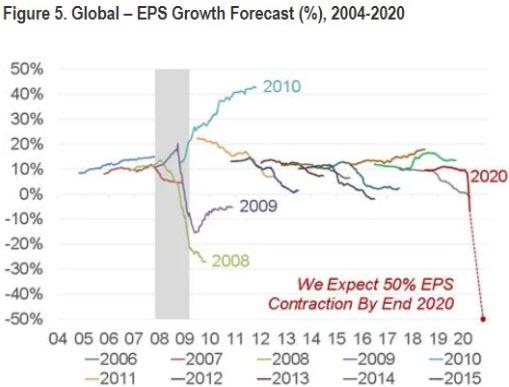

And so as Credit Suisse, JPMorgan and Goldman all point out the schizophrenia in being bullish in a time when corporate profits are set for the biggest – and longest – drop since the Great Depression, late last week two more banks joined the bandwagon with Citi warning that “equities fall the same as EPS in a recession… and reflect that equity markets are currently not reflecting the expected decline of 50% in global EPS in 2020.” Make that 70% according to JPMorgan.

Finally, exactly two weeks after our post on the “shocking” topic of how expensive the market is right now, Bank of America’s Savita Subramanian has also done the math and concludes that as “stocks have rallied, bottom-up consensus estimates for 2020 have fallen”, which in turn has pushed the S&P 500’s forward P/E ratio from March’s low of 13.0x to 19.5x, higher than mid-Feb’s peak P/E of 18.9x.

In other words, using the bank’s reference table of 20 different valuation metrics, “we’re back to elevated multiples on most of the 20 metrics we track” with just three exceptions: lower than average Price to Free Cash Flow, cheaper relative to bonds (equity risk premia frameworks) and – drumroll – relative to gold.

The last one is especially amusing because it means that slowly but surely investors are finally realizing that the biggest winner after the current reflationary surge will not be equities but what the WSJ once dubbed “a pet rock.”

Of course, even in this unprecedented dislocation of a “market”, equity investors still have hope, which is literally is all they have: or as Gundlach puts it, “In Fed We Trust” is all the buyers have” and Citi agrees: “Central bank intervention could cap the downside.”

The Paycheck Protection Program or PPP was funded with $350 billion in the last stimulus bill, this money is now gone. Of the thirty million small businesses in America, only 1.7 million received money from the 2.3 trillion dollar aid package passed to help sustain America during this difficult time. If the government blew through this money and was only was able to help only around 5% of small businesses it is difficult to think another 250 billion dollars will set things straight.

Clearly, because the government made promises it delayed the wave of firing while companies waited for help.

The government has failed to keep its promise so now we should expect unemployment to soar as reality sets in. One of the largest problems facing small companies is they are often underfunded and have difficulty getting financing at reasonable rates. Banks find larger companies much more profitable. The sector of the economy most damaged by the covid-19 shutdown is small business. When this is over America will find many small businesses have been decimated and are not able to reopen. Others will never recover and be forced to close within months. Since small businesses employ over 54 million people in America and their importance in the economy should not be underestimated.

Rest assured government employees and bureaucrats will still continue to get paid but small business, the most productive part of the economy has a knife to its throat. As a landlord and small business owner, I can tell you the program was structured in a way that will be of little help to most small businesses. The government slammed expensive legislation through with no idea of the damage they were doing and how it will cause hundreds of thousands of businesses to close their doors forever. Washington has become so attuned to dealing with lobbyist from mega-companies it has lost sight of the fact small is small, and when this comes to business, this means usually under twenty employees, not hundreds.

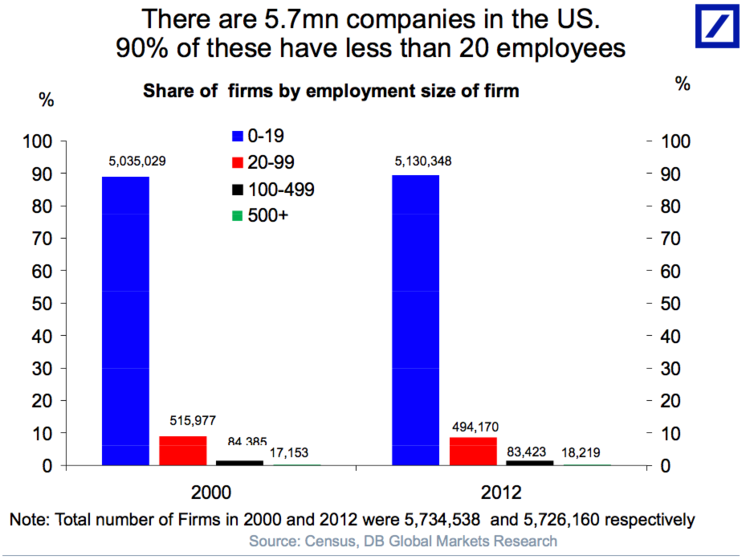

90% Of Businesses Are Small (click to enlarge)

The government’s answer to keeping people employed was to promise small businesses an easy to get, rapid maximum loan amount of two and a half times a company’s average monthly payroll expense over the past 12 months. This loan would turn into a grant and be forgiven if a company did not fire its employees. Sadly, legislators failed to take into consideration that not all small businesses are labor or payroll intense. Some businesses with large or expensive showrooms are getting hammered by rent, others by inventory, or things like taxes, utilities, or even by having to toss products due to spoilage.

The PPP also failed to address the issue of what these employees are going to do while the company has no customers and business barely trickling. In the past, these employees were expected to pursue activities that earned revenue and garnered profits for the business but with no costumers, this is difficult to do. The PPP also ignored the fact that by keeping these employees on the payroll a generous employer is left open to the harsh mandates laid out in the government’s previous bill. The hastily drawn up 110-page federal covid-19 economic rescue package, which Trump fully supported dealt a hard blow to small business. For a small business this is a disaster, the bill requires;

Employers with fewer than 500 employees and government employers offer two weeks of paid sick leave through 2020.

Those same employers must now provide up to 3 months of paid family and medical leave for people forced to quarantine due to the virus or care for family because of the outbreak

As expected, this measure, named “Families First Coronavirus Response Act.” resulted in millions of workers to suddenly lose their jobs. Ironically, it was held before the voters as proof lawmakers could work together during a crisis. By framing the poorly crafted pork-packed bill this way promoters positioned themselves to demonize those unwilling to support it. Remember, this bill is was in addition to the $8.3 billion emergency spending bill first approved to curb the spread of covid-19.

The Private Sector Is Shrinking (click to enlarge)

As government has grown larger it seems to have become totally oblivious to the fragility of many small businesses and how much it can cost a community when they close. By framing these pork-packed bills as bipartisan their promoters imply they are fair and balanced. This is not true, small business is the big loser and hundreds of thousands will soon have to close.With so many tenants looking at foregoing rent small landlords that don’t have deep pockets also face huge problems. We have our heads in the sand if we think companies that exist on events where people gather will overnight regain their luster. It is not like someone can simply flick a switch and things will return to normal.

Reality undercuts the idea of the “V-shaped recovery” theory and the idea after the economy has come to a dead stop it can quickly reboot and be back at full speed in a few months.The government has presented us with an extension of crony capitalism structured to throw just enough to the masses to silence their outrage but in the coming weeks, we will see it failed. Large businesses with access to cheap capital are the winners and the big losers are the middle-class, small businesses, and social mobility.All those people that want a higher minimum wage can forget that ever happening if we don’t have jobs.

As for just how much small business owners make, according to figures from 2015 from the Small Business Administration the median income for self-employed individuals at an incorporated business was $49,804 and $22,424 for unincorporated firms. According to PayScale’s 2017 data, the average small business owner’s income is $73,000 per year. But, total earnings can range from $30,000 – $182,000 per year. This means it varies greatly depending on where and just how big the business is, however, it is important to remember these people have “skin in the game” and most risk losing everything if their business fails.

It is important to recognize that starting your own business has always been about the opportunity to design and build your own future. It is a symbol of freedom not a guarantee of wealth. Many people choose this path proudly, not to make more money but as a way to express their individuality. For these competent and talented people, a job in government or at a large company often offers more security and benefits but far less freedom. Do not underestimate the value of small business and what it contributes to our society. Companies such as Amazon are the anti-thesis of small business making their workers a cog in a machine and stealing their soul.

Based on the government’s promise to small businesses a great many held off on letting employees go but with each passing day in order to survive they are now in the process of letting hundreds of thousands of employees go. This is a ticking time-bomb. By telling these businesses to close and then through its failure to carry out its promise of helping them the government has created a situation with massive negative economic ramifications. To make matters worse, people going on unemployment look to get almost as much as those that do work. Why will anyone want to work, especially government workers when they can get paid to stay home? This is not about wanting more money for small business, it is about the reality that the firings are just beginning.

NYC Housing Activists Urge “Massive Wave” Of Rent-Strikes Because “Landlords Have Gotten Taken Care Of”

The wealth inequality story is not a complicated one to figure out. In essence, tens of millions of Americans were already suffering from insurmountable debts, no savings, and low wage jobs, even before the pandemic unfolded and crashed the economy.

Now the working-class poor are starting to get angry, sitting on their couches in quarantine, as they have recently been laid off, only to watch President Trump at afternoon press briefings tout about his epic bailouts of corporate America and Wall Street, while everyone else gets a lousy $1,200 check.

A “social bomb” is brewing in America – we’ve been documenting how the next crisis could be a social one. The bottom 90% of Americans are getting smarter by the day as they sit in lockdown, now organizing on the internet, and are plotting their very next big move that could be severely disruptive: rent strikes.

New York City housing activists are preparing to unleash a “massive wave” of rent strikes in the next two weeks, reported Bloomberg.

Housing Justice For All hopes to have as many as one million New Yorkers on May 1 participate in a rent strike to pressure Gov. Andrew Cuomo to cancel rent for the duration of the lockdown.

“With so many New Yorkers unable to pay rent for the foreseeable future, the current crisis is unsustainable and demands action,” Housing Justice for All and New York Communities for Change said in a statement Thursday. “Many tenants have no ability to pay rent, and landlords can’t collect rent from tenants who are broke.”

Lena Melendez, an activist who spoke with Bloomberg, said people in her building have organized and will not pay rent on May 1.

Melendez said landlords “have gotten taken care of” by the government, making the case that working-class poor do not need to pay rent.

“They have gotten tax abatements and deferments on their mortgages. And tenants have just gotten a temporary freeze, a pause, on evictions,” she said.

New York City’s Independent Budget Office projects about half a million people will lose their jobs in 2020. The city has been thrown into a recession, if not depression for the 1H20, as a social crisis is brewing…

How long until rent strikes start developing in other large major metros?