Twitter Outlaws Political Satire, Civil Disobedience With Fresh Bans Of Conservative Influencers

Twitter has taken it upon themselves to remove two prominent voices from the public square, once again.

The first victim of Twitter’s ban hammer was Infowars host Owen Shroyer – who was encouraging followers to gather in person at the Texas state Capitol in Austin on Saturday to protest coronavirus restrictions. Shortly after Media Matters wrote about the event, Shroyer was banished from the platform. Apparently the public cant be trusted with decisions concerning their own personal safety, so nanny @Jack stepped in to protect us from Owen’s persuasiveness.

A question, though… How many more people have died in the pandemic because the World Health Organization (WHO) told the public there was no human-to-human transmission of COVID-19 (when Chinese doctors who were silenced by the CCP said otherwise, and their own coronavirus expert disagreed), or not to wear masks, or that travel bans are unnecessary and racist?

How many more people have died or are still battling the effects of coronavirus after Nancy Pelosi told people to come on down to Chinatown on February 24 and mingle – when footage of dead and dying Wuhan residents were all over the internet?

Nancy Pelosi, 2/24/20:

“Come to Chinatown. Precautions have been taken…We think it’s very safe and want others to come.”pic.twitter.com/Pa41NRNf6k

The second conservative influencer banned by Twitter on Thursday was @ALX, a Turning Point USA staffer who dared to parody Joe Biden’s avatar generator with the following picture:

In other words, political satire is now off-limits because, presumably, using humor to point out that Joe Biden has an uncomfortable relationship with China is simply too effective.

Thanks for keeping us safe Jack, and don’t listen to everyone who says you’re shilling for the CCP and the Democratic Party by silencing powerful conservatives that are more compelling – and let’s face it, way funnier than the spoon-fed NPCs on the left.

Professor Luc Montagnier, 2008 Nobel Prize winner for Medicine, claims that SARS-CoV-2 is a manipulated virus that was accidentally released from a laboratory in Wuhan, China. Chinese researchers are said to have used coronaviruses in their work to develop an AIDS vaccine. HIV DNA fragments are believed to have been found in the SARS-CoV-2 genome.

We knew that the Chinese version of how the coronavirus emerged was increasingly under attack, but here’s a thesis that tells a completely different story about the Covid-19 pandemic, which is already responsible for more than 110,000 deaths worldwide.

According to Professor Luc Montagnier, winner of the Nobel Prize for Medicine in 2008 for “discovering” HIV as the cause of the AIDS epidemic together with Françoise Barré-Sinoussi, the SARS-CoV-2 is a virus that was manipulated and accidentally released from a laboratory in Wuhan, China, in the last quarter of 2019.

According to Professor Montagnier, this laboratory, known for its work on coronaviruses, tried to use one of these viruses as a vector for HIV in the search for an AIDS vaccine!

“With my colleague, bio-mathematician Jean-Claude Perez, we carefully analyzed the description of the genome of this RNA virus,” explains Luc Montagnier, interviewed by Dr Jean-François Lemoine for the daily podcast at Pourquoi Docteur, adding that others have already explored this avenue:

Indian researchers have already tried to publish the results of the analyses that showed that this coronavirus genome contained sequences of another virus, … the HIV virus (AIDS virus), but they were forced to withdraw their findings as the pressure from the mainstream was too great.

In a challenging question Dr Jean-François Lemoine inferred that the coronavirus under investigation may have come from a patient who is otherwise infected with HIV.

“No,” says Luc Montagnier, “in order to insert an HIV sequence into this genome, molecular tools are needed, and that can only be done in a laboratory.”

According to the 2008 Nobel Prize for Medicine, a plausible explanation would be an accident in the Wuhan laboratory. He also added that the purpose of this work was the search for an AIDS vaccine.

The truth will eventually come out

In any case, this thesis, defended by Professor Luc Montagnier, has a positive turn. According to him, the altered elements of this virus are eliminated as it spreads:

“Nature does not accept any molecular tinkering, it will eliminate these unnatural changes and even if nothing is done, things will get better, but unfortunately after many deaths.”

Luc Montagnier added that with the help of interfering waves, we could eliminate these sequences and as a result stop the pandemic.

This is enough to feed some heated debates! So much so that Professor Montagnier’s statements could also place him in the category of “conspiracy theorists”:

“Conspirators are the opposite camp, hiding the truth,” he replies, without wanting to accuse anyone, but hoping that the Chinese will admit to what he believes happened in their laboratory.

To entice a confession from the Chinese he used the example of Iran which after taking full responsibility for accidentally hitting a Ukrainian plane was able to earn the respect of the global community. Hopefully the Chinese will do the right thing he adds.

“In any case, the truth always comes out, it is up to the Chinese government to take responsibility.”

‘Secret’ National Guard Unit Ready To Enforce ‘Martial Law’ In Washington DC

Ever since governors started calling up national guard units last month, the Pentagon has insisted that the soldiers remain firmly under the command of the governors that called them up, and that the Pentagon isn’t using the troops to plan for any federal ‘secret missions’ or ‘martial law’, should the crisis spiral out of control and threaten ‘continuity of government’.

Now, a report in Newsweek purports to prove that the Pentagon lied. In reality, a 10,000 soldier strong national guard unit has been deployed to the capital area with a ‘secret’ assignment to enforce martial law in Washington DC and help evacuate lawmakers and top government officials if things go south.

In reality, the joint task force is already 10k strong, and is already on 24/7 alert.

And yet the activation of Joint Task Force National Capital Region, including almost 10,000 uniformed personnel to carry out its special orders, contradicts those assurances. JTF-NCR is not only real and operating, reporting directly to the Secretary of Defense for some of its mission, but some of its units are already on 24/7 alert, specially sequestered on military bases and kept out of coronavirus support duties to ensure their readiness.

Members of the Illinois 106th Aviation Battalion was called up under a federal statute placing them directly under the control of the Secretary of Defense. The soldiers, along with several Black Hawk helicopters, shipped out of Decatur, Illinois armory last month.

The first hints about this “secret mission” were included in a local Illinois newspaper’s report about the call-up of Illinois National Guard forces who were being deployed at Fort Belvoir outside Washington. In addition to their normal mission objectives, the report noted that the unit had also been assigned a bevy of unfamiliar tasks, including: evacuating officials, lawmakers and members of the judiciary aboard 106th Aviation Regiment helicopters.

Here are more details courtesy of Newsweek, including information about the Major General who would effectively be in charge of securing the capital district if martial law were imposed.

Unlike other Guardsmen activated under “Title 32” orders—under gubernatorial control but paid for by the federal government—the soldiers of the 106th were activated under “Title 10” orders, strict federal duty as if they were going to be shipped off to Afghanistan or Iraq. Except that in this case, the battlefield is Washington, DC.

On that battlefield, the Illinois 106th Aviation Battalion’s helicopters would be used to evacuate everyone from Army leaders to the White House.

“We are that quick reaction force that allows us to help mobilize forces within the Washington DC area, evacuate people, or whatever that might be,” says Cpt. Adam Kowalski of the Illinois Guard. “We’re kind of like that big taxicab that makes sure everybody gets where they need to be and keeps the government going.”

The soldiers in the unit, as well as their commanders, have been studying the Joint Emergency Evacuation Plan – the official protocol for moving and protecting senior officials at the Defense Department – and other plans that cover the evacuation of top civilian officials, like lawmakers and the president.

He and his fellow officers have been studying the Joint Emergency Evacuation Plan (JEEP), the national plan to move Defense Department officials to alternative locations outside the Washington area. JEEP is not the only plan. It is supplemented by Atlas as well, which designates the procedures for the movement of civilian leaders, called “Enduring Constitutional Government,” ensuring the survival of the legislature and the judiciary. And above JEEP and Atlas are the highly classified Octagon, Freejack and Zodiac plans that deal with other emergencies, and the movement of the White House and other presidential successors.

The March 16 order that activated JTF-NCR placed all of this planning under the command of Maj. Gen. Omar J. Jones IV. In “peacetime,” the Army Major General commands the Military District of Washington, an Army unit mostly known mostly for its ceremonial and memorial expertise, providing the soldiers at Arlington National Cemetery, the Drum and Fife formations for parades, the grave and precise standard bearers for state funerals. Following post 9/11 organizational changes, Maj. Gen. Jones was also “dual-hatted” as the commander of Joint Forces Headquarters–National Capital Region, an organization created after it became clear that no single command was in charge of immediate response in Washington. There was not even a single military interface with the White House and what’s called “the interagency”, one organization that would be in charge as continuity of government or other disaster plans were implemented.

In peacetime, the Joint Forces Headquarters is merely a coordinator, with each of the military services retaining control of their forces. But once the Joint Task Force is activated, as it has been now, operations and units shift to what the military calls “operational command.” Maj. Gen. Jones is now in charge. He isn’t some martial law commander who takes precedence over any civil authorities, nor is he out in public telling anyone outside his secretive task force what to do. But he is the military man who would be in charge in Washington if civil government broke down.

However, if shit really does hit the fan, these contingency measures might not even be of much help: “No one wants to talk evacuation, especially when there’s nowhere to go,” said one purportedly ‘senior’ military officer who was working on ‘continuity of government’ planning.

Washington DC is in the midst of a spike in new coronavirus cases, and the mayor earlier this week just extended a stay at home order until the middle of next month.

We’ll cover some upbeat earnings reports from GM, Firestone, AT&T and Texaco. The hook: they are from 1929 – 1936. Yes, every company here was profitable in the Great Depression; they cut their workforces until they could earn their dividend (basically the cost of capital back then). Unemployment was a first-order effect of that period, but these financial reports also show less-appreciated impacts: reduced adoption of productivity enhancing technologies (phones and cars) and less public ownership of stocks.

* * *

Regular readers know we have a small but growing collection of Great Depression-era annual reports issued by brand-name American companies, and those are the stars of this week’s Story Time Thursday. They offer a useful historical framework when evaluating the recent unprecedented monetary/fiscal policy responses to the COVID-19 Crisis. What you’ll see in these reports is what happens when policymakers don’t respond to an economic crisis until its effects are widespread.

#1: Firestone Tire’s annual revenues, net profits and dividends (various annual reports, 1929 – 1936, FY ending October):

Takeaway: even in the depths of the Great Depression (1933) and after revenues had dropped by 48% from their highs just 4 years prior, Firestone posted a profit and paid a dividend. How? The only hint comes in the 1930 annual: “by readjusting our organization and reducing our expenses in every phase of our business”. That is what businesses quite rightly do when faced with economic uncertainty: reduce their workforces to protect profits and cash flows.

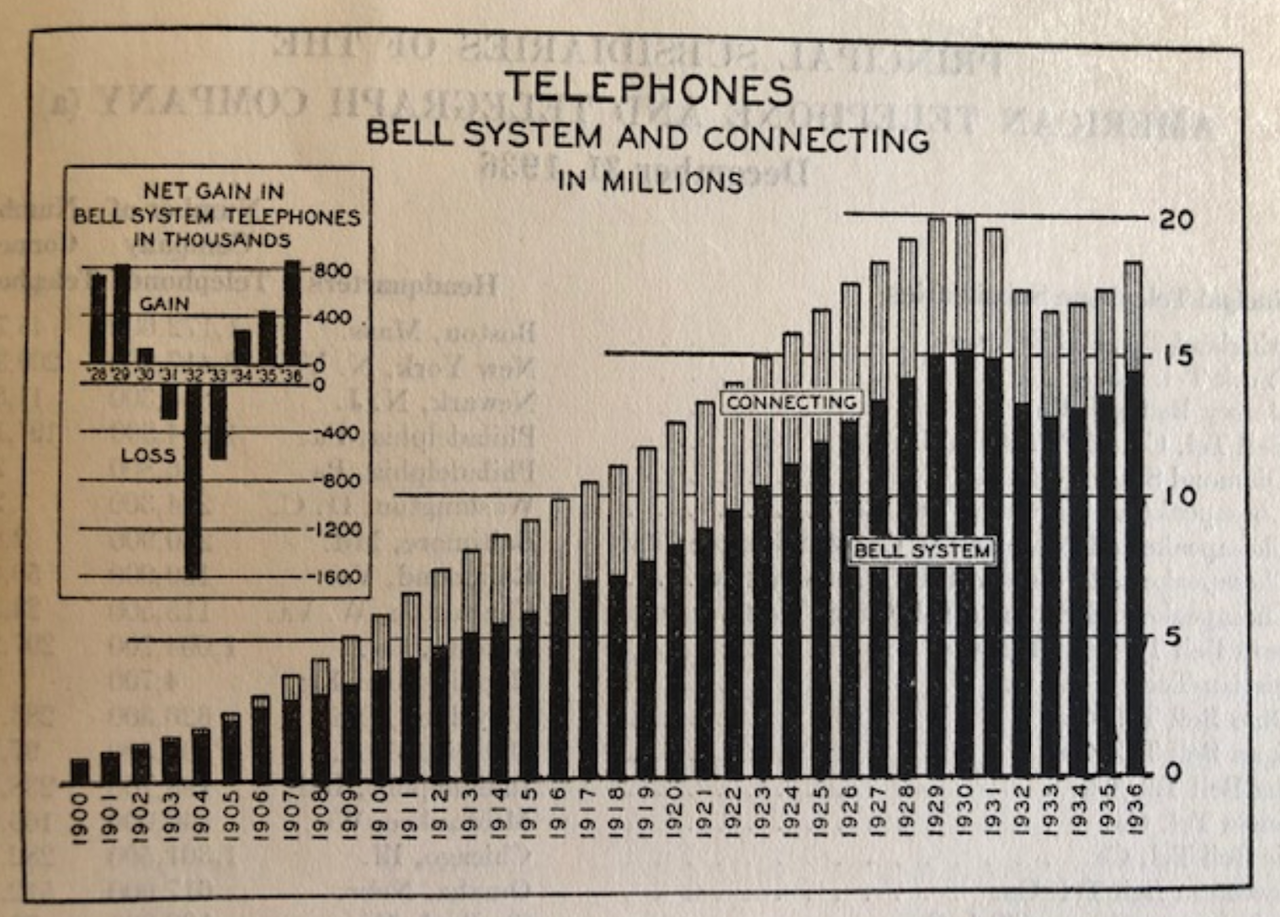

#2: Phone service company AT&T was the Internet of the 1930s, and its 1936 annual report shows the effect of the Great Depression on the adoption of what was then an important and still relatively new disruptive technology:

After 20 years of growth from 1900 to 1929 the number of telephones in America declined by 15% in just 3 years (1930 – 1933) and even when growth resumed there was a lost decade between 1926 and 1936:

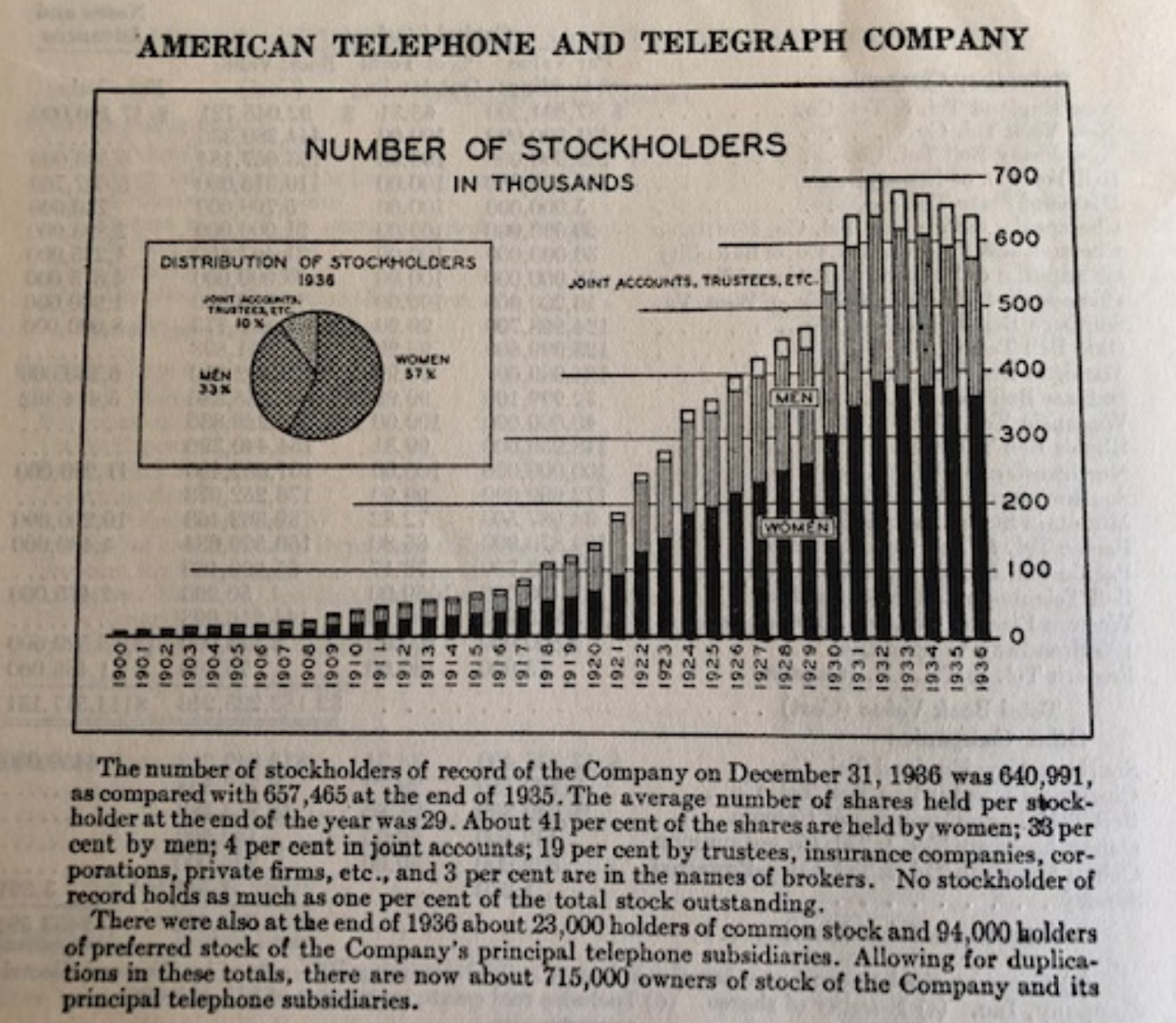

And in a fascinating analysis, the 1936 AT&T annual shows the effect of the Great Depression on the de-democratization of American capitalism: about 10% fewer people owned the stock in 1936 than in 1929. Also worth noting: 41% of AT&T stock was owned by female retail investors versus 33% male ownership, with the remainder in joint or institution accounts.

Takeaway: economic depression has many second order effects, such as reversing the progress of important technological advances and reducing the involvement of the public in capital markets.

#3: General Motors was essentially the Apple of the 1920/1930s; the preeminent purveyor of a wide range of products that gave people personalized access to a wider world. Ford only went public in the 1950s, so we don’t have their numbers. But here is a table of GM’s financial results from its founding in 1909 to 1932:

Takeaway: what you see here is a combination of points #1 and #2. The Great Depression hit GM’s revenues by 71% from 1929 to 1932, which shows what happens to adoption rates for new technologies that happen to be discretionary consumer purchases. And, like Firestone, GM made money in the depths of the Depression and paid common stock dividends as well. Yes, it cost a lot of jobs to make that possible. But imagine how the US might have fared in World War II if GM and Firestone had failed in 1932…

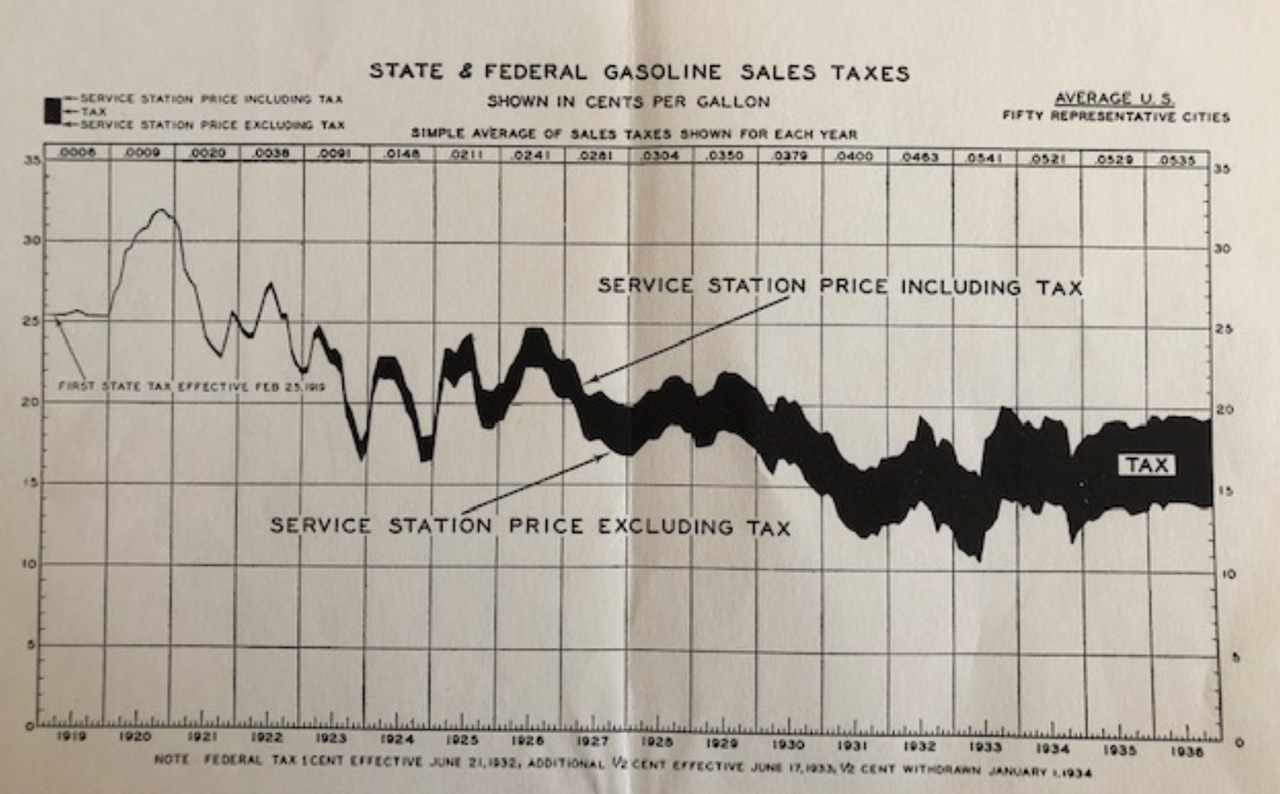

#4: As a final illustration, we turn to the 1936 annual report for The Texas Corporation (a.k.a. Texaco), which included this chart of per-gallon gasoline prices with and without taxes from 1919 to 1936:

Takeaway: in an eerie resemblance to today, pretax oil/gasoline prices per gallon fell by 50% from 1H 1926 ($0.22) to 1H 1933 ($0.11). Part of that was due to reduced demand caused by the Great Depression, especially visible in the chart from 1929 to 1933. But the other piece was the discovery of the East Texas Oil Field in October 1930 using new drilling techniques to reach reservoirs some 3,500 feet below the surface. By 1931 the “Black Giant” field was producing a staggering (even now) 900,000 barrels of oil per day.

Summing up these 4 examples into one framework about the wide-reaching consequences of serious economic contractions:

The first order effects are easy to understand: companies do whatever it takes to survive and keep cutting employment levels until they can make a profit even in the worst of times.

But there’s more to the story…

The Great Depression slowed the adoption of the telephone and automobile, two important productivity enhancing technologies.

It also reduced the population’s ownership of publicly traded capital.

And it endangered key industrial assets that would be needed just a decade later to fight a world war.

Bottom line: deep economic contractions carry far larger societal price tags than job losses and business failures.

Futures Soar On Reopening, Corona Cure Optimism; Ignore Mountains Of Bad News

Even though the Gilead “miracle drug” report was refuted by the company itself, which slammed the market-moving Statnews article (sourced reportedly from hedge funds who were seeking to take profit in GILD) as “anecdotal reports with no statistical power”, and even though Trump’s plans to reopen the country turned out to be far less pressing than expected, with Trump effectively handing power into the hands of states, this morning futures and global stocks have continued their move higher after blasting off last night on the Gilead/reopening speculation, with the euphoria persisting overnight as the small steps toward restarting the world’s largest economy helped investors look past mixed progress on curbing the coronavirus and the latest dismal data from China, where GDP posted its first contraction in four decades, sliding 6.8% or more than expected.

The data from China showed the world’s second-largest economy shrank for the first time since at least 1992 because of the coronavirus woes. GDP contracted 6.8% in the quarter year-on-year, more than expected, and 9.8% from the previous quarter. Retail sales also fell more than expected in March, but industrial output dipped only slightly, suggesting its manufacturing sector at least is recovering more quickly.

As WTI oil slumped, further extending its divergence with Brent…

… the dollar tried to rebound and bond yields were generally unchanged, US equity futures rallied nearly 100 points, or 4%, from the Thursday close and approached the limit-up lock on several occasions, reflecting optimism that major economies will slowly start lifting lockdown restrictions and signs of medical progress against the virus.

The week is ending on an optimistic note after the White House set guidelines to reopen the economy, though it has yet to ensure that widespread testing will be available as many business leaders have urged. The president is under pressure, with 22 million Americans applying for jobless benefits in a month, erasing a decade worth of job creation. At the same time, infections have surged in Russia, Germany and Singapore. Investors also assessed a report that Gilead Sciences is seeing improvements in a group of coronavirus patients being treated with its drug, although the company itself refuted the report. German Chancellor Angela Merkel this week announced tentative steps to begin returning the country to normal.

“The market is a bit optimistic right now,” David Bailin, chief investment officer at Citi Private Bank, said on Bloomberg TV. “Ultimately we have to have really great coordination in order to see any real improvement in the economy.”

Prior to Friday’s cash open, the S&P 500 was up 0.4% this week and set for a second straight weekly gain – its first back-to-back weekly gain since before the market turmoil began in February – despite an unprecedented collapse in the US (and Chinese) economy, and 22 million people laid off in the past month, as investors scour first-quarter earnings to find signs of the novel coronavirus outbreak’s effects on companies’ balance sheets.

In Europe, the Stoxx 600 Index also climbed 2.6%, entering a bull market, after it rose 20% from its March lows, with the travel and leisure sector leading the gains although all 19 industry groups were in the green. Banking stocks helped the Stoxx Europe 600 Index jump to a session high as lenders are said to seek to avert stashing billions for soured loans; the banks subgroup surges as much as 4.3%. European lenders are set to report comparatively small increases in loan loss reserves in the first quarter and plan a similar approach during the rest of the year, Bloomberg News reports, citing senior bankers and regulators.

European countries have “no choice” but to set up a fund that “could issue common debt with a common guarantee”, French President Emmanuel Macron told the Financial Times on Thursday. Failure to do so would lead to populists winning elections in Italy, Spain, and possibly France, he also warned.

Yields on ultra-safe 10-year U.S. Treasuries US10YT=RR and German Bunds rose slightly, while Treasury futures TYc1 and the dollar firmed against the yen JPY=EBS, in another tentative sign of investor optimism.

“The market continues to look through terrible data… on anticipation of economies reopening,” said Steen Jakobsen, Chief Investment Officer at Saxo Bank. “And hopes that a new drug treatment will help lift longer term uncertainty about the COVID-19 pandemic.”

Earlier in the session, Asian stocks gained as traders shrugged off the catastrophic China GDP data noted above, led by IT and materials, after falling in the last session. All markets in the region were up, with Jakarta Composite gaining 3.4% and South Korea’s Kospi Index rising 3.1%. The Topix gained 1.4%, with Riken Technos and Kichiri Holdings & Co Ltd rising the most. The Shanghai Composite Index rose 0.7%, with Zhejiang Xinneng Solar Photovoltaic Technology and Jiangsu Boxin Investing posting the biggest advances.

In rates, the 10Y yield initially bounced sharply from its 0.62% close rising almost as high as 0.69% before reversing virtually all gains. Italian bond markets, which have been under pressure as the country’s virus difficulties push its debt-to-GDP ratio towards 150%, also rallied as France expressed support for joint euro zone debt issuance.

In commodities, spot gold fell 1.5% to $1,692 per ounce too and with investors looking to take on more risk industrial metal copper jumped 4% on track for its best week since February 2019. No such luck for battered oil markets however. WTI futures slumped 8% to an 18-year low after OPEC had lowered of its global demand forecast on Thursday, and Brent crude slipped back under $28 a barrel having been up nearly 3% at one point. OPEC now sees a contraction of global demand of 6.9 million barrels per day (bpd) this year due to the coronavirus outbreak.

“Downward risks remain significant, suggesting the possibility of further adjustments, especially in the second quarter,” OPEC said of the demand forecast.

Looking at the day ahead, the data releases include new car registrations for March in the EU27, the Italian trade balance for February and the final Euro Area CPI reading for February. From the US we’ll also get the leading index for March. From central banks, we’ll hear from the Fed’s Bullard and the ECB’s Rehn.

Market Snapshot

S&P 500 futures up 2.6% to 2,859.50

STOXX Europe 600 up 2.5% to 333.14

MXAP up 1.8% to 144.79

MXAPJ up 2% to 468.07

Nikkei up 3.2% to 19,897.26

Topix up 1.4% to 1,442.54

Hang Seng Index up 1.6% to 24,380.00

Shanghai Composite up 0.7% to 2,838.49

Sensex up 1.8% to 31,166.28

Australia S&P/ASX 200 up 1.3% to 5,487.54

Kospi up 3.1% to 1,914.53

German 10Y yield fell 0.2 bps to -0.476%

Euro down 0.09% to $1.0830

Italian 10Y yield fell 5.0 bps to 1.659%

Spanish 10Y yield unchanged at 0.831%

Brent futures down 0.3% to $27.73/bbl

Gold spot down 1.3% to $1,695.70

U.S. Dollar Index up 0.1% to 100.13

Top Overnight News

China’s gross domestic product shrank 6.8% from a year ago, the worst performance since at least 1992 when official releases of quarterly GDP started and missing the median forecast of a 6% drop

Cantor Fitzgerald is shrinking its workforce, breaking with firms across Wall Street that vowed not to lay off employees during a pandemic that’s unleashed the worst unemployment crisis in decades

The Italian government may set up a 70 billion-euro ($76 billion) package of spending measures in a decree due to be approved on Monday morning, Il Sole 24 Ore reported

More than 15,000 U.K. companies fell into “significant distress” in the first three months of 2020 as the virus shutdown took its toll on the economy, according to a quarterly survey published on Friday by insolvency specialist Begbies Traynor

The Trump administration issued a guideline to governors outlining steps for phased reopening. Some U.S. states and employers may be able to abandon most social distancing practices to curb the coronavirus outbreak within four weeks under guidelines.

The U.S. Treasury Department is in talks with some airlines about accepting their loyalty programs as collateral against government loans to help them weather the virus crisis.

Asian equity markets notched firm gains after tracking the advances in US equity futures following the announcement of reopening guidelines for the US economy and amid hopes of a COVID-19 treatment after positive results for Gilead’s Remdesivir drug in closely observed clinical trials, despite the Co. downplaying the reports. In addition, Boeing shares took off after-hours as the Co. plans to resume commercial airline production in Washington state factories next week. ASX 200 (+1.3%) and Nikkei 225 (+3.2%) surged from the open with corporate updates contributing to the stock rally in Australia including Rio Tinto which posted higher quarterly iron ore output and shipments, while Tokyo sentiment benefitted from the government’s relief efforts including the JPY 100k cash handouts to all citizens, and the TAIEX (+2.1%) was also boosted with chipmakers inspired by strong earnings from global semiconductor giant TSMC. Hang Seng (+1.5%) and Shanghai Comp. (+0.7%) conformed to the broad optimism following reports the PBoC will continue to the guide credit funds to support smaller firms through targeted RRR cuts and with the gains maintained regardless of the slew of mixed tier-1 data which showed Chinese GDP Y/Y at -6.8% vs. Exp. -6.5% Y/Y, although GDP Q/Q was at a slightly narrower than expected contraction. Furthermore, Industrial Production and Retail Sales added to the varied narrative although China’s stats bureau remained optimistic in which it suggested a visible improvement in major economic indicators last month and likelihood of a continued recovery. Finally, 10yr JGBs were pressured amid spillover selling from T-notes with prices dampened as stocks rallied from US reopening guidelines and hopes of progress for COVID-19 treatment.

Top Asian News

Car Inc. Stock, Bonds Soar as Warburg Pincus Unit to Boost Stake

China Stocks Advance as Traders Look Past Poor Economic Data

Indian Central Bank Boosts Liquidity to Offset Virus Hit

RBI Halts Bank Dividends, Injects Cash to Help Indian Borrowers

European equities hold onto a bulk of sentiment-driven gains (Euro Stoxx 50 +3.6%), albeit the region has waned off highs alongside US equity futures. The slight fade in risk appetite follows questions regarding whether reopening the US economy soon will revive an outbreak of COVID-19. Meanwhile, the second catalyst is attributed to Gilead’s treatment showing rapid recoveries among severe cases, but the Co. caveated stating the data does not satisfy safety and efficacy profiles. Traders may also be wary to open/hold onto risky positions heading into another weekend of uncertainty. Nonetheless, broad-based gains are seen across major European bourses as April option expiries provided the region with impetus, with CAC 40 (+3.8%) modestly outpacing peers amid post-earning gains from giants L’Oreal (+2.7%) and LVMH (+4.9%) – which together account for almost 14% of the French index and around 5% of the Euro Stoxx 50. Sectors are in the green across the board and lean towards a risk-on session – with cyclicals outperforming defensive. The breakdown sees Travel & Leisure outperforming whilst the underperformance in Healthcare seems to be more of a risk-driven move. In terms of individual movers, Airbus (+8.7%) shares soar amid reports Boeing (+8.1% pre-mkt) is to resume production at its Seattle factory as soon as Monday next week. Thus, engine makers also gain impetus, with Rolls Royce (+11.3%) and Safran (+8.8%) buoyed. Elsewhere, Rio Tinto’s (+3.3%) iron ore shipment update supports share prices, with peers Antofagasta (+2.9%), Glencore (+9.0%), BHP (+5.1%) and Fresnillo (+2.0%) all higher in tandem. On the flip side, Diasorin (-7%) shares reside at the foot of the Stoxx 600, potentially Gilead seemingly leads the race between the Cos regarding antibody testing.

Top European News

ECB’s Weidmann Tells Governments to Spend Now But Save Later

Europe Autos Jump as Market Optimism Outweighs March Sales Slide

Airbus Chief Says Virus May Require Difficult Jobs Decision

Rate Cut ‘Main Option’ for Bank of Russia Next Week: Nabiullina

In FX, the Dollar is back in demand despite renewed risk appetite for global equities if nothing else on the back of more moves to scale back COVID-19 restrictions and positive anti-virus treatment results. The index has bounced firmly from 99.689 lows to reclaim 100.000+ status and is only marginally shy of Thursday’s 100.300 high amidst almost blanket Greenback gains vs G10 peers.

JPY/NZD/AUD – The Yen continues to resist the Buck’s advances and the bulk of safe-haven unwinding, with reports of Japanese offers into rebounds over 108.00 in Usd/Jpy capping the headline pair, while crosses remain bearish barring extreme bouts risk asset buying. On that note, the Kiwi has regained a degree of stability after yesterday’s RBNZ-related jolt to retest 0.6000 climes and reverse some underperformance against the Aussie, as the cross slips back below 1.0600 and Aud/Usd fades ahead of 0.6400 following mixed Chinese data overnight (GDP contraction not quite as bad as feared overall, retail sales weaker than forecast, but ip vice-versa).

CAD/EUR/CHF/GBP – All making way for the latest broad Dollar upturn, as the Loonie retreats from just under 1.4000 to sub-1.4100 against the backdrop of waning oil prices and the Euro loses more momentum having failed to retain grip of the 1.0900 handle earlier this week. However, the single currency may derive some traction from option expiries again given hefty interest between 1.0835-50 (1.9 bn) and the 1.0800 strike (1.7 bn), in contrast to Usd/Cad that could see 1.9 bn at 1.4000 defended or protected. Meanwhile, the Franc is still caught in the crossfire in terms of weakness around 0.9700 vs the Greenback and strength relative to the Euro as Eur/Chf skirts 1.0500, but Sterling is softer across the board as Cable tops out above 1.2500 and Eur/Gbp rebounds through 0.8700. Note, the former continues to respect the 200 HMA at 1.2525 and latter is prone to almost daily or intraday periods of fix induced volatility. Ahead for the Pound, Moody’s UK ratings review poses downgrade risk to current standing and/or outlook.

SCANDI/EM – Contrasting fortunes for the Sek and Nok, as the aforementioned downturn in crude scuppers the Norwegian Krona irrespective of independent Euro weakness, while the Rub takes note of Brent contagion from WTI and guidance from the CBR Governor to the effect that a rate cut is on the agenda for the April 24 policy meeting.

In commodities, WTI and Brent June futures remain choppy in early European trade, with the former’s June contract quoted given the shift in volume as its front-month expires in the coming days. Due to the colossal contango in the market, WTI May contract trades lower by some 9% (around USD 18/bbl), whilst the June future sees prices in the green on the day above USD 25.50/bbl at the time of writing. Market fundamentals remain unchanged thus far as participants await the OPEC+ pact to go into effect on May 1st, whilst on the lookout for commitments from outside the group. On that front, desks highlight that ConocoPhillips’ announcement regarding 200k BPD to its North American output highlights somewhat meaningful unmandated cuts outside OPEC+. Analysts at ING note “instead, market forces will do the job, with the low-price environment forcing producers to cut back.” Looking ahead to next week, the Texas Railroad Commission (RRC) is expected to revisit the issue on mandated state cuts. Supporters at the prior meeting on the 14th April argued about sever storage shortages and potential record numbers of bankruptcies amid market conditions. The effectiveness of the OPEC+ deal was also downplayed whilst they added that the RRC must do its part. Adversaries contended that the least profitable wells are already being shut and that RRC actions will not solve the crude crisis. WTI June resides towards the bottom end of the its intraday range, having waned off USD 26.78/bbl highs, whilst its Brent counterpart similarly declined from highs near USD 29/bbl. Elsewhere, spot gold remains on the backfoot and trades on either side of USD 1700/oz as DXY reclaims 100.000 to the upside, and with market contacts earlier reporting stops through 1705-1700/oz. The yellow metal thus far printed an intraday base at USD ~1687/oz, albeit remains in the green for the week having opened at USD ~1660/oz on Monday. Copper meanwhile withstands the strength in the Buck and moves in tandem with stocks following a shallower than expected contractions in Chinese QQ Q1 GDP and March Industrial Production, but prices remain capped by resistance at ~USD 2.3675/lb.

US Event Calendar

10am: Leading Index, est. -7.2%, prior 0.1%

DB’s Jim Reid concludes the overnight wrap

Straight to China this morning where Q1 GDP has just come in at -6.8% yoy (consensus -6.0%). The previous weakest quarters (in data back to 1992 on Bloomberg) were the 6% seen over the last two quarters – so an historic moment for modern China. The rest of the activity data was a mixed bag. Industrial production was better than expected -1.1% yoy (vs. –6.2% expected) however both retail sales and fixed asset investment were much weaker than expected at -15.8% yoy (vs. -10.0% expected) and -16.1% ytd yoy (vs. -15.0% expected). So, industrial production got a lot better in March after a disastrous Jan-Feb, but fixed asset investment and retail sales is lagging. Elsewhere, the surveyed jobless rate printed at 5.9% vs. 6.2% last month. China’s National Bureau of Statistics said following the data that it is seeing good progress on work resumption; however added that the external situation is becoming more complicated.

Despite the weaker than expected GDP print the Shanghai Comp (+0.89%) and CSI (+1.23%) are both higher along with other major bourses including the Nikkei (+2.19%), Hang Seng (+2.31%), ASX (+1.87%) and Kospi (+2.96%). Instead, investors appear to be leaning on the encouraging news from the medical publication Stat, that a group of patients being treated in Chicago with a trial of Gilead’s drug Remdesivir were “seeing rapid recoveries in fever and respiratory symptoms”. The report added that most patients showed improvement and were discharged subsequently, with only two fatalities (read our Corona Daily for more on this).

Also helping sentiment this morning was the announcement from President Trump on new guidelines on easing restrictions and reopening the US. He announced that 29 states were in the “ballgame” to reopen soon, with a set of markers needed to be hit before state governors should open their states up. At this point many states are coordination with other states in their regions to coordinate reopening together. Dr. Birx, one of the top public-health experts on the White House coronavirus task force, reiterated that the state leaders will have a leeway based on their own judgement. The recommendations include that states show a “downward trajectory” in cases and flu-like illnesses for at least two weeks. Then they can begin a 3-phase process to reopen. States should then continue to show declining caseloads every two weeks before moving onto the next phase, while any significant “rebound” in numbers could mean needing to bring restrictions back. Schools, daycares and bars would not reopen before phase two, whereas restaurants, movie theaters and sports stadiums could open in phase one under certain restrictions. Regardless of the Presidents announcements, New York Governor Cuomo extended his state’s lockdown until May 15, with New Jersey following suit soon after. S&P 500 futures have gained +3.21% in response, also helped partly by double digit afterhours gains for Boeing following news that the company plans to restart manufacturing in the Seattle area next week.

While President Trump announced guidelines on easing restrictions, a number of other countries moved to extend them. In the UK, it was announced (unsurprisingly) that the lockdown would remain in place for another 3 weeks to early May. This is broadly in line with the timetables that other European nations have outlines in recent days. Meanwhile Japanese Prime Minister Abe extended the state of emergency across the entire country, having previously been just in 7 prefectures. And in Australia, Prime Minister Morrison said that there were no plans to change the baseline restrictions for the next four weeks. On the other end of the spectrum, Switzerland announced it will reopen some businesses and schools in three stages from April 27. For more on all things virus related see our Corona Crisis Daily for much more.

In markets, if yesterday had been a day in January of this year you would have said that it was very volatile as the S&P 500 saw 4 big swings around flat of at least 1.4%. We ended up closing at the top end of the range (+0.58%) as markets started to get excited as to what Trump was going to say after the bell about re-openings. Technology stocks outperformed, with the NASDAQ advancing +1.66%, meaning it’s now down “only” -13.09% from its closing peak back in February, out-pacing the S&P 500 which still stands -17.32% below its previous peak. Technology stocks have benefited from “stay-at-home” narratives and lower interest rates boosting growth multiples. Elsewhere in Europe the Stoxx 600 was -0.19%.

Over in fixed income, the move to safe assets saw both US Treasuries and bunds rally further yesterday. 10yr Treasury yields ended the session -0.5bps at 0.627%, just 8.6bps above their all-time closing low back in early March, while bund yields fell by -0.9bps. Southern European debt also managed to recover slightly yesterday, with the spread of 10yr yields on Italian (-4.2bps) and Spanish (-2.4bps) debt narrowing over bunds. However, those on Greek debt widened by a further +7.1bps.

On a related topic, President Macron yesterday expounded on the importance of a larger virus recovery fund and that without coming together in this crisis the EU will unravel, as Eurosceptism would rise in the countries not supported. France has been the largest country pushing the idea of joint debt issuance. In an FT interview posted as Europe was going home (well maybe commuting from the study to the kitchen) he remarked that, “we are at a moment of truth, which is to decide whether the European Union is a political project or just a market project. I think it’s a political project. . . We need financial transfers and solidarity, if only so that Europe holds on”. These comments come after European Commission President von der Leyen apologized to Italy while painting a picture of a Europe that was coming together, “too many were not there on time when Italy needed a helping hand at the very beginning,” she said. “For that, it is right that Europe as a whole offers a heartfelt apology.” ….The truth is that now Europe has become the true beating heart of solidarity. The true Europe is now standing up.” We will see if all this brings a more specific plan next week at the leaders’ summit.

In terms of data, the weekly initial jobless claims from the US has lost some of its shock value now but we still saw an astonishing reading at 5.245m in the week ending April 11. There’s obviously no sugar coating how bad this is, but markets did have the small consolation that this was the first time in a month that the reading wasn’t quite as bad as the consensus estimate (5.5m). Furthermore, this is the 2nd consecutive week that the reading has fallen, down from a peak of 6.867m. Nevertheless, if you add up the last 4 weeks’ readings, which are the highest in the history of the series, they sum to over 22m, something that is simply unprecedented. For context, the total number of nonfarm payrolls in the US in March stood at 151.8m, so we’re talking well over 10% of the entire US workforce in the space of a month having made jobless claims. Yesterday’s report also means that practically an entire decade of employment growth has been wiped out in a single month. The 10 years of jobs reports from March 2010 to February 2020 saw nonfarm payrolls rise by a cumulative 22.8m. The two series do not completely correspond with each other but I’m sure you see the big picture.

Further hard data for March showed that the pandemic’s impact extended into the housing market, with US housing starts falling to 1.216m (vs. 1.3m expected). The decline of -22.3% on the previous month is actually the biggest monthly decline since March 1984, and comes only 2 months after January’s reading, which saw the largest number of housing starts since December 2006. Meanwhile the Philadelphia Fed’s business outlook survey for April fell to -56.6 (vs. -32.0 expected), which was its lowest level since July 1980.

Here in the UK, the government has refused to ask for an extension of the Brexit transition period. Downing Street added that they’d also refuse if Brussels asked them for an extension instead. The government spokesman said that it was “better to be clear now and minimise the uncertainty for businesses”. Under the Withdrawal Agreement reached with the EU, the UK government have until the end of June to decide whether to extend the standstill transition period past the end of the year, and while they’ve insisted throughout the process that they’d conclude negotiations by the end of this year, speculation has risen thanks to the coronavirus that they could be forced to delay. The next negotiating round is scheduled for next week, and a “high-level meeting” is also scheduled for June to take stock of progress so far. So something bubbling under the surface and something the EU could do without given all that’s going on with Italy.

To the day ahead now, and the data releases include new car registrations for March in the EU27, the Italian trade balance for February and the final Euro Area CPI reading for February. From the US we’ll also get the leading index for March. From central banks, we’ll hear from the Fed’s Bullard and the ECB’s Rehn.

European Car Registrations Crash Most On Record In March

With lockdowns enforced across much of Europe in March, sheltering at home was on everyone’s agenda, and not purchasing a new vehicle (although one wouldn’t know it by looking at TSLA stock). The latest data from the European Auto Industry Association (ACEA) confirmed this after showingnew car registrations plunged 51.8% YoY to 853,077 vehicles for the month, the biggest drop and the lowest number of sales on record.

“With containment or lockdown measures taking hold in most markets from around the middle of the month, the vast majority of European dealerships were closed during the second half of March,” the ACEA said.

Sales across all major EU markets plunged, with Italy hit the hardest by the pandemic – reporting the most significant drop in new car registrations of 85.4%, followed by -72.2% in France, -69.3% in Spain, and -37.2% in Germany.

FCA Group and Groupe PSA saw the largest drop in vehicle sales in the month, with registrations down 74.4% and 66.9%, respectively.

VW Group sales drop 43.6% y/y; ytd down 19.4%

PSA Group sales drop 66.9% y/y; ytd down 34.3%

Renault Group sales drop 63.7% y/y; ytd down 36.1%

Ford sales drop 60.9% y/y; ytd down 37.4%

FCA Group sales drop 74.4% y/y; ytd down 34.5%

BMW Group sales drop 39.7% y/y; ytd down 16.7%

Daimler sales drop 40.6% y/y; ytd down 22.9%

Hyundai Group sales drop 41.8% y/y; ytd down 18.8%

Toyota Group sales drop 36.2% y/y; ytd down 8.2%

Nissan sales drop 51.5% y/y; ytd down 25.6%

The decline in car registrations started well before the virus outbreak.

A decline in registrations will likely roll into April as much of the continent remains in lockdown following confirmed virus cases and deaths the highest in Spain, Italy, France, Germany, and the UK, these countries are the drivers of economic growth, and with a pandemic still underway, an economic recession, if not depression is unfolding, that will continue to impede new car sales through 1H20.

Wuhan Coronavirus Death Toll Revised 50% Higher, Chicago Remdesivir Trial Revives Hopes For ‘Miracle Drug’: Live Updates

Summary:

Wuhan revises citywide coronavirus death toll 50% higher

Beijing blames ‘overwhelmed’ health care system for the error

Foreign Ministry says new numbers “can stand the test of history”

Report on Chicago remdesivir trial stokes hopes for new “miracle drug” to fight the virus

* * *

Shortly after 11pmET Thursday night, a headline came trundling across the wire that caught our eye: Health authorities in Wuhan raised the official death toll from the city’s coronavirus outbreak by 50%, equivalent to 1,290 patients, to a still-too-low-to-be-believed 3,869.

An anonymous city official told China’s Xinhua that the new deaths and newly announced cases (officials confirmed another 325 non-fatal cases, raising the total number of “confirmed” cases to 50,333) were undercounted during the “early stages” of the outbreak, according to the Associated Press.

Echoing NYC Mayor Bill de Blasio’s reasoning for adding thousands of new deaths to the city death toll earlier this week, Chinese officials said the new cases include people who died at home, as well as those who died in a hospital without their deaths being officially added to the toll (during the first weeks after the Wuhan shutdown, Chinese officials refused to include patients who hadn’t officially tested positive in their case numbers, an issue that was supposed to have been fixed by one of the early revisions announced by the Chinese back in February).

The new figures were reportedly discovered after Chinese officials tried to reconcile numbers from their hospital database, with numbers from the city funeral service and its nucleic acid-testing.

The official Xinhua News Agency quoted an unidentified official with Wuhan’s epidemic and prevention and control headquarters as saying that during the early stages of the outbreak, “due to the insufficiency in admission and treatment capability, a few medical institutions failed to connect with the disease prevention and control system in time, while hospitals were overloaded and medics were overwhelmed with patients.

“As a result, belated, missed and mistaken reporting occurred,” the official was quoted as saying.

The new figures were compiled by comparing data from Wuhan’s epidemic prevention and control system, the city funeral service, the municipal hospital authority, and nucleic acid testing to “remove double-counted cases and fill in missed cases,” the official was quoted as saying.

Deaths occurring outside hospitals had not been registered previously and some medical institutions had confirmed cases but reported them late or not at all, the official said.

By adding these 1,290 patients to the rolls, China raised its national death toll to 4,632, from the 3,342 announced by the NHC earlier. After their release, Foreign Ministry spokesperson Zhao Lijian insisted that these new numbers “can stand the test of history.”

Why would China even bother with this latest ‘revision’ – it’s at least the 4th time they’ve tweaked the numbers, and the first time in roughly 2 months – of the Wuhan numbers? Well, it just so happens that the official statistics agency also published the first reading of China’s Q1 GDP, which confirmed a massive contraction, as was expected.

Twitter’s Melissa Chen jokingly compared China’s ‘50%’ revision to when a student purposefully marks wrong answers on their homework to cover up the fact that they’ve been cheating.

When you realize that the teacher would be suspicious because you did too good of a job cheating on your homework, so you threw in some errors:https://t.co/tlHASEudVV

But Wuhan is slightly larger than NYC population-wise, and the outbreak in Wuhan was even more vicious than the outbreak in NYC, which has reported more than 10k deaths. So imagine what that must mean for Wuhan, where the hospital system was completely overwhelmed during the early weeks of the outbreak, leaving some elderly patients to drop dead on the street (something that, as far as we know, hasn’t happened in the US).

The other big news overnight – and the reason why Dow futs are up nearly 800 points in the green Friday morning – has actually been percolating in investors’ minds since shortly after yesterday’s close of cash trading. In the early evening on Thursday, a report claiming ‘miraculous’ efficacy for Gilead’s remdesivir during a University of Chicago study, helped revive hopes that a “miracle drug” might be around the corner. The results were first reported last night by STAT News.

Here’s more from that STAT News report, which we also cited last night.

Remdesivir was one of the first medicines identified as having the potential to impact SARS-CoV-2, the novel coronavirus that causes Covid-19, in lab tests. The entire world has been waiting for results from Gilead’s clinical trials, and positive results would likely lead to fast approvals by the Food and Drug Administration and other regulatory agencies. If safe and effective, it could become the first approved treatment against the disease.

The University of Chicago Medicine recruited 125 people with Covid-19 into Gilead’s two Phase 3 clinical trials. Of those people, 113 had severe disease. All the patients have been treated with daily infusions of remdesivir.

“The best news is that most of our patients have already been discharged, which is great. We’ve only had two patients perish,” said Kathleen Mullane, the University of Chicago infectious disease specialist overseeing the remdesivir studies for the hospital.

However, a statement from Gilead warned that the drug is still in the trial phase, and these results still need to be confirmed. And as we noted earlier this week, officials in China suspiciously shuttered 2 separate trials – one in Wuhan and one in Beijing – of the global remdesivir study, claiming there weren’t enough severely ill patients to run the trials, which sounds like a not-very-believable ruse to us.

Even Gilead, whose shares are up nearly 20% in premarket trade, warned that the U.Chicago trial is just one of many, and these numbers are simply “anecdotal”.

Finally, the number of confirmed cases surpassed 2.1 million during the early hours of Friday in the US, while the number of confirmed deaths neared 150k.

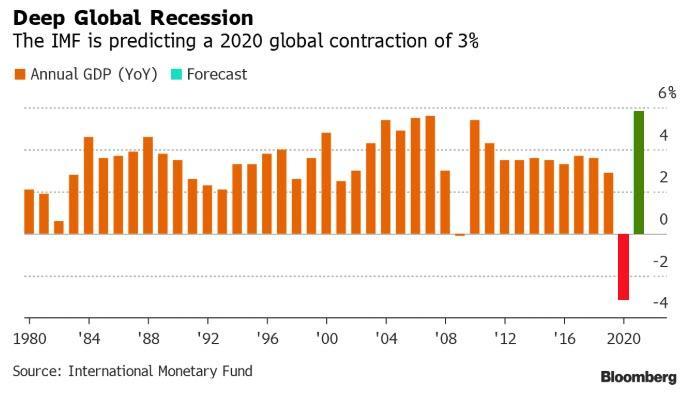

Over Half The World Has Asked IMF For Bailout To Weather “Great Lockdown” Recession

The International Monetary Fund revealed this week that half the world’s countries have requested emergency loans to weather the global coronavirus-fueled financial crisis.

IMF Managing Director Kristalina Georgieva told a meeting of G20 finance ministers and central bank governors on Wednesday that over a hundred countries have approached the D.C.-based international organization for emergency bailouts.

IMF Managing Director Kristalina Georgieva, Getty Images.

Despite just ten countries so far receiving emergency funding, with many more expected to receive lifelines by end of this month, she said the IMF will use its“full toolbox and $1 trillion firepower” of lending.

The comments came after two days prior at the start of the week the IMF direly predicted in its semi-annual report a “Great Lockdown” recession set to be the steepest in nearly a century, forecasting global gross domestic product will shrink 3% this year.

Georgieva also told CNBC in a new interview, “This is an emergency like no other. It is not because of bad governors or mistakes.” She added, “For that reason, we are providing funding very quickly.”

And further, commenting in response to the fund’s reputation for imposing tough conditions on countries seeking emergency loans:

The IMF head said “everything is on the table in terms of measures we can take,” and encouraged central banks to “spend as much as you can.”

“But keep the receipts,” she added. “We don’t want accountability and transparency to take a back seat in this crisis.”

As confirmed global COVID-19 cases soared past 2.1 million on Thursday, Georgieva did add on an optimistic note that should the virus soon be contained and cases begin to recede in the coming months, “the global economy could expand by 5.8% in 2021,” according to CNBC.

“It’s the first time in the history of the IMF that epidemiologists are as important as macro economists for our projections,” the IMF chief said. “We are really hoping our scientists will not disappoint us.”

A CBC News report gives kids advice on how to shut down “conspiracy theories” voiced by their parents about coronavirus being created by China in a lab.

Because apparently that’s the media’s job now.

The presenter laments how somebody’s Dad may drop a message into chat blaming China for “manufacturing the coronavirus” with a “link to a site you’ve never heard of” (translation – a link that’s not, God forbid, mainstream media).

The piece then features a woman from a group that combats “misinformation online” who urges the son or daughter not to get confrontational with their Dad but to accuse him of being accurate and stirring fear.

Is uncle Bob spreading COVID-19 misinformation in the family group chat? This doesn’t have to be awkward. pic.twitter.com/SxX5HVqY9a

— CBC News: The National (@CBCTheNational) April 15, 2020

At one point in the piece, the reporter even suggests that conspiracy theories can be “just as dangerous as a virus.”

“Maybe send an article from a legitimate source quoting credible scientists on why the virus wasn’t manufactured,” states the host.

The suggested article unsurprisingly comes from the CBC and is entitled ‘No, the new coronavirus wasn’t created in a lab, scientists say.’

In reality, as Fox News sources confirmed last night, the coronavirus was indeed leaked from a laboratory in Wuhan, so to say it was “manufactured” isn’t even much of a stretch. The virus was literally created in a lab.

The irony of all this of course is that virtually nobody trusts the mainstream media, so when they attack conspiracy theories it just makes more people believe them.

When social media giants then get involved to censor information about the same conspiracy theories, that also bolsters the notion that they’re accurate because powerful interests are trying to stifle them.

Take the news report below as an example.

A reporter who adopts a stereotypical fake ‘news reporter’ accent which normal people don’t use when they talk to each other tells the viewer that the conspiracy theory linking 5G to coronavirus is false.

A doctor wearing a white lab coat inside what appears to be his own home (to stress faux authority) is then presented to call the conspiracy “completely false.”

The doctor doesn’t even explain why it’s false (he could have pointed out for example that Iran was impacted by coronavirus yet has no 5G network at all), but the news station just expects the viewer to believe him because he’s an authority figure in uniform.

In reality, as the comments below the video prove, the vast majority of people see the news report as desperate and hokey, making them believe the conspiracy theory to an even greater degree.

* * *

My voice is being silenced by free speech-hating Silicon Valley behemoths who want me disappeared forever. It is CRUCIAL that you support me. Please sign up for the free newsletter here. Donate to me on SubscribeStar here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown.

USDA Wants To Purchase Farm Products To Support Food Banks

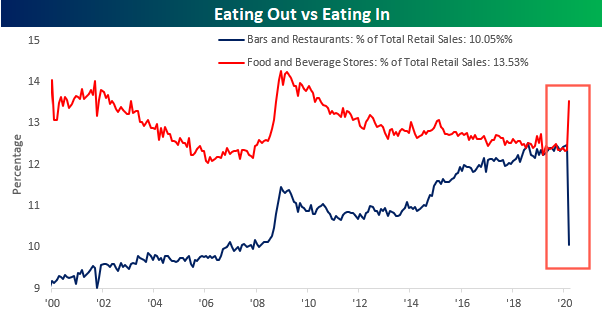

Coronavirus shutdowns have completely disrupted food supply chains from restaurants to supermarkets to distributors to processors, all the way down to farmers. Why is this? Well, America is under government-enforced lockdowns to flatten the pandemic curve, is preventing consumers from eating at restaurants and bars, which has shifted how they source food products to supermarkets entirely. Basically, what happened is that farm products for commercial clients that have yet to be packaged for consumers are being dumped as the restaurant industry folds, which has forced the Trump administration to intervene.

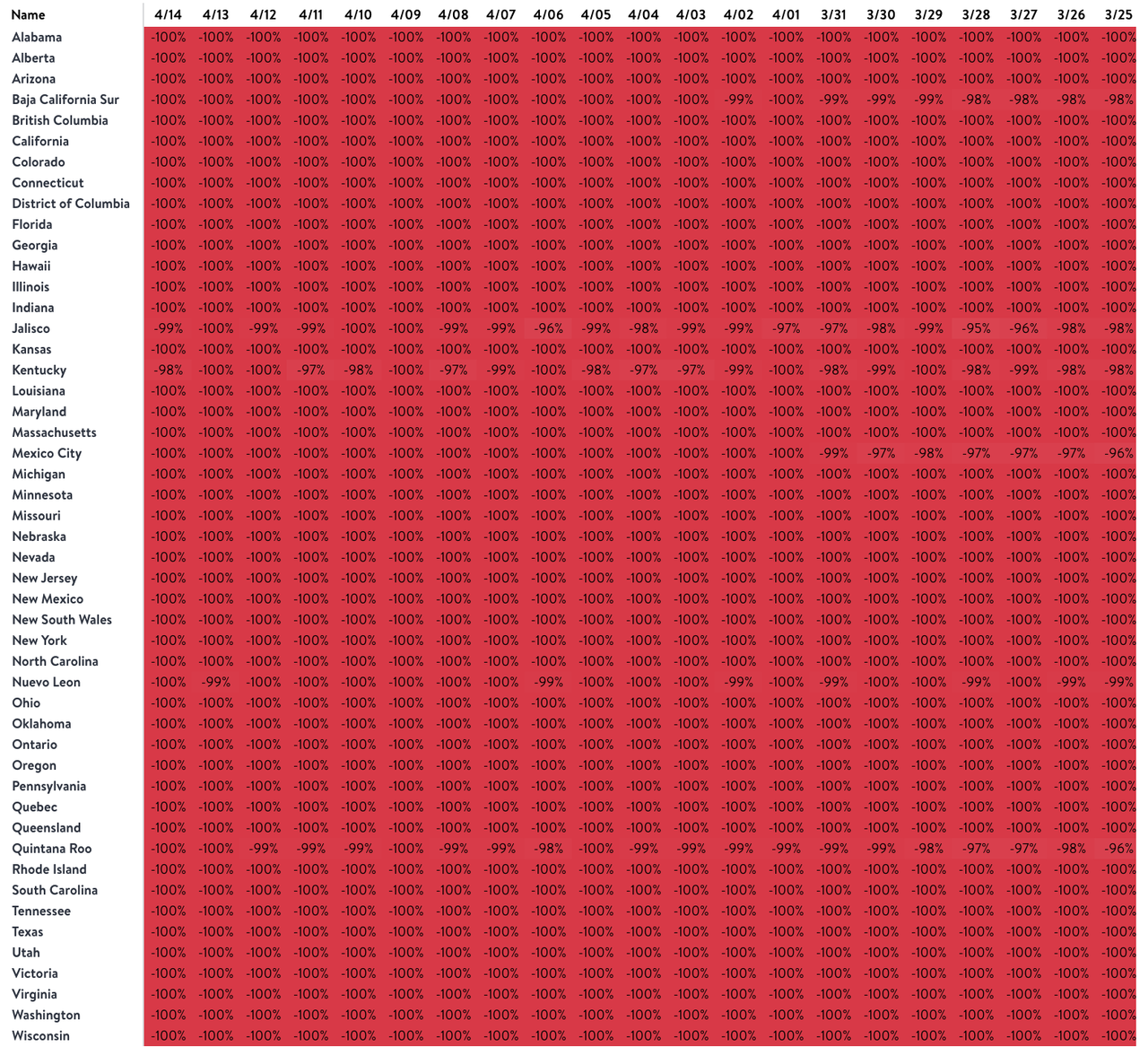

OpenTable data shows restaurant traffic has crashed through mid-April. At the same time, supermarket sales have surged.

OpenTable restaurant traffic data

We documented this seismic shift last week. Countless images poured onto Twitter detailing how farmers dumped tanker loads of milk down the drain as dairy demand via restaurants evaporated in the previous month.

We are dumping milk in South Florida because there is no home for it. We still have to feed and care for our cows, and our farmers are still milking cows, in hopes that we can sell that milk in the future… #stillfarmingpic.twitter.com/tn4dpUBuUa

The collapse of the restaurant industry has quickly rippled down the supply chain, and severely impacted farmers as stockpiles of milk and meat products continue to build, crushing spot prices. The Trump administration has recognized farmers are headed for a world of hurt once more, already reeling from trade war wounds.

Agriculture Secretary Sonny Perdue told Fox Business Wednesday that President Trump would like the USDA to start purchasing milk and meat products as part of a $15.5 billion rescue package for farmers.

“We want to purchase as much of this milk, or other protein products, hams and pork products, and move them into where they can be utilized in our food banks, or possibly even into international humanitarian aid,” Perdue said.

While we don’t believe future food purchases by the government will be transferred into “international humanitarian aid” programs, the likely end destination will be food banks that are experiencing the most significant demand surge ever as 17 million people have just filed for unemployment claims. The Trump administration understands that if food shortages appear at food banks, people will become hangry, and that is one trigger of where social unrest could be sparked.

As part of the coronavirus relief bill, Congress has allocated $23.5 billion in aid for farmers. And of that, it appears around $15.5 billion could be used to purchase milk and meat products that will likely be sent to food banks to support the working poor.

{kind=link}

{kind=link}