Schumer Asks Trump To Invoke Act For Emergency Medical Equipment; Trump Immediately Orders It Done

President Trump has ordered his administration to immediately prepare to invoke the Defense Production act to “get ventilators and other important medical equipment to those who need it,” after Senate Minority Leader Chuck Schumer (D-NY) asked the president by phone to do so.

“POTUS told Schumer he would, and then POTUS yelled to someone in his office to do it now,” a Schumer spokesman told Politico.

Trump later described the conversation with Schumer as “extremely good” at today’s daily press briefing of the White House coronavirus task force.

“I had a very good telephone conversation, extremely good, with Sen. Schumer a little while ago,” the president said. “We were working on various elements of the deal, and the Democrats are very much wanting something to happen, and the Republicans likewise are very much wanting something to happen. And I think it will.”

Pres. Trump says he had a “very good” conversation with Senate Minority Leader Chuck Schumer amid congressional effort to pass stimulus package.

Trump also says he spoke “at length” with Senate Majority Leader Mitch McConnell (R-KY) – reporting that there exists a “tremendous spirint to get something done,” according to the report.

“So we’ll see what happens,” Trump said, “but my conversation was very good with Senator Schumer.”

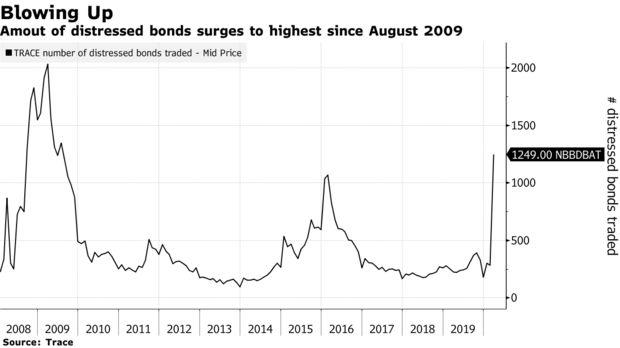

Distressed Debt In The US Doubles In 2 Weeks To $500BN As BofA Expects Surge In Defaults

Last week, in the aftermath of the historic oil price collapse, we warned that the long-awaited “fallen angel” day has arrived, as $140 billion in oil producer (and up to $360 if one includes the mid-stream companies) investment grade debt was on the verge of being downgraded to junk and throwing the entire high yield market in turmoil.

Fast forward to today when Bloomberg calculates that since we published out article, the amount of distressed debt – a term that describes borrowings likely to default – in the U.S. alone has doubled to a half-trillion dollars as the collapse of oil prices and the fallout from the coronavirus shutters entire industries.

While rating agencies have been slow to respond to the total collapse in cash flow generation across most US industries as long as the US economy remains paralyzed due to the spreading lock downs across the nation, markets have been far faster, and the result has been a plunge in the price of countless bonds. As a result, corporate bonds – which according to BofA are no longer properly functioning – that yield at least 10% points above Treasuries, as well as loans that trade for less than 80 cents on the dollar, have swelled to $533 billion. This is more than double from the March 6 total of only $214 billion. And, according to UBS, if one adds across all company debt globally, including loans to small- and mid-sized companies that rarely if ever trade, the distressed pile could top $1 trillion. And yes, that number is only going to surge.

An analysis via Trace shows that the amount of distressed bonds has surged to the highest level since the financial crisis, surpassing the oil/manufacturing recession of 2016.

“We could see this be worse than 2008,” said Bloomberg Intelligence analyst Philip Brendel, in what may be the understatement of the day.

While currently most of the distressed debt comes from U.S. shale companies that have been pummeled by the all-out price war between Saudi Arabia and Russia as most companies are now cash flow negative and unable to service their debt obligations, analysts expect this solvency (and liquidity) crisis to spread to all industries the longer the US economy remains in a state of shutdown.

The amount of the oil and gas sector’s distressed debt now stands at over $128 billion, and is expected to rise substantially higher. One of the biggest casualties has been Occidental Petroleum Corp., which has seen its funding costs skyrocket and its credit rating cut to junk; its bonds due in 2024 now yield 18.6% and trade at just 54 cents on the dollar. In early March, they sold for above par. Meanwhile OXY’s CDS trade as if there is a 65% chance the company will go bankrupt in 5 years.

Energy is just the harbinger however, and the amount of distressed debt in the retail, entertainment and lodging industries, among others, has also surged as economic activity comes to the virtual standstill because of the coronavirus.

“The speed of change is definitely unprecedented,” said UBS credit strategist Matthew Mish. “It’s obviously consistent with the change in investor perception around mobility and essentially the fact that the economy, particularly in the U.S., but globally has ground to a halt.”

Bank of America agrees, and in a report published this morning, its credit analyst Oleg Melentyev says “we think this credit cycle has turned and expecting default rates to rise meaningfully in coming months.”

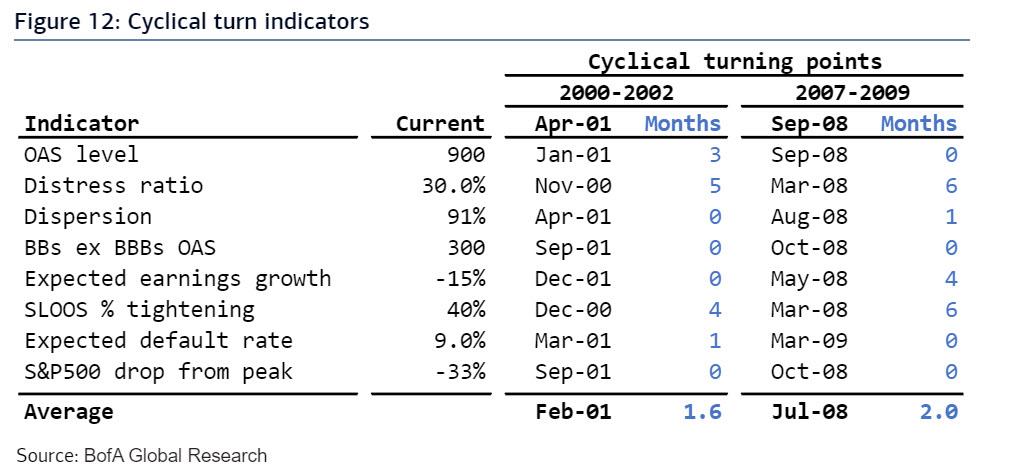

Only a week ago, we summarized all key leading indicators of credit stress in a table below, where we compared the current level on each one of them, to the point in time closest to it going into the two previous credit cycles. Marking Apr 2001 and Sept 2008 as the points of no return corresponding to 1,000bps levels on the HY index, we argued that the whole collection of indicators was about 3-4 months away from such threshold, where a turn in the credit cycle becomes inevitable and irreversible.

BofA’s conclusion: “As things continued to move at lightning speed over the past several days, those same indicators are now averaging only 1.5-2 months of cushion before they reach such a point. Based on those timelines, today’s market environment is equivalent to Feb 2001 and Jul 2008.“

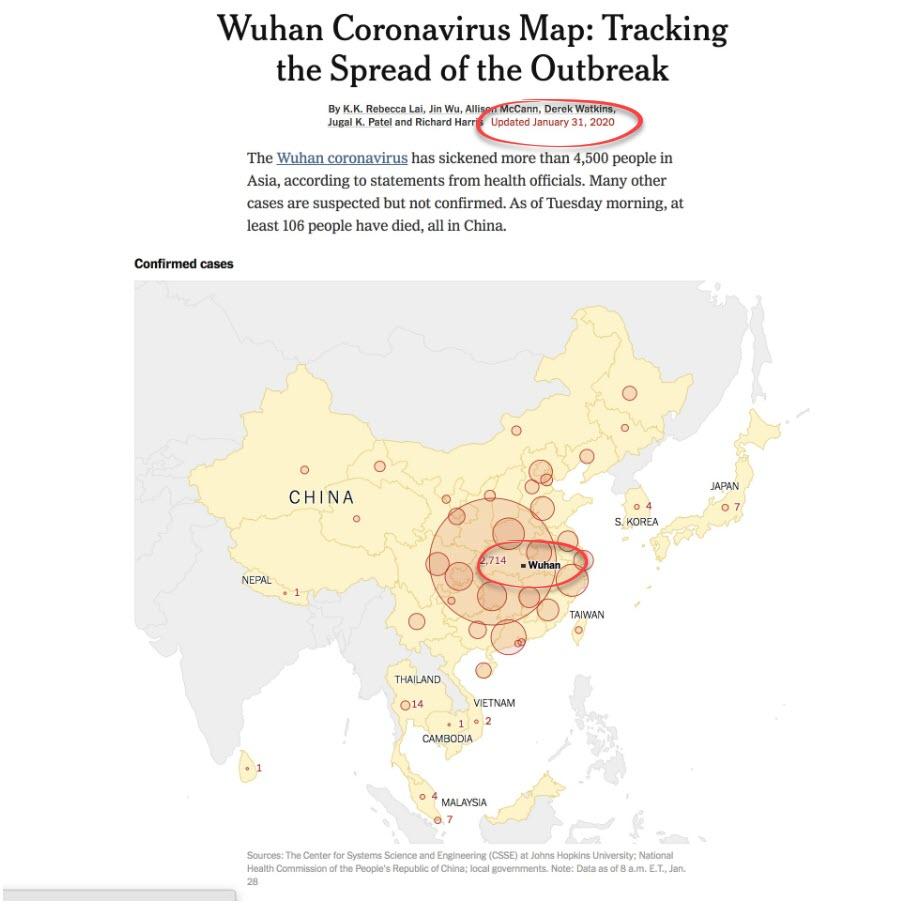

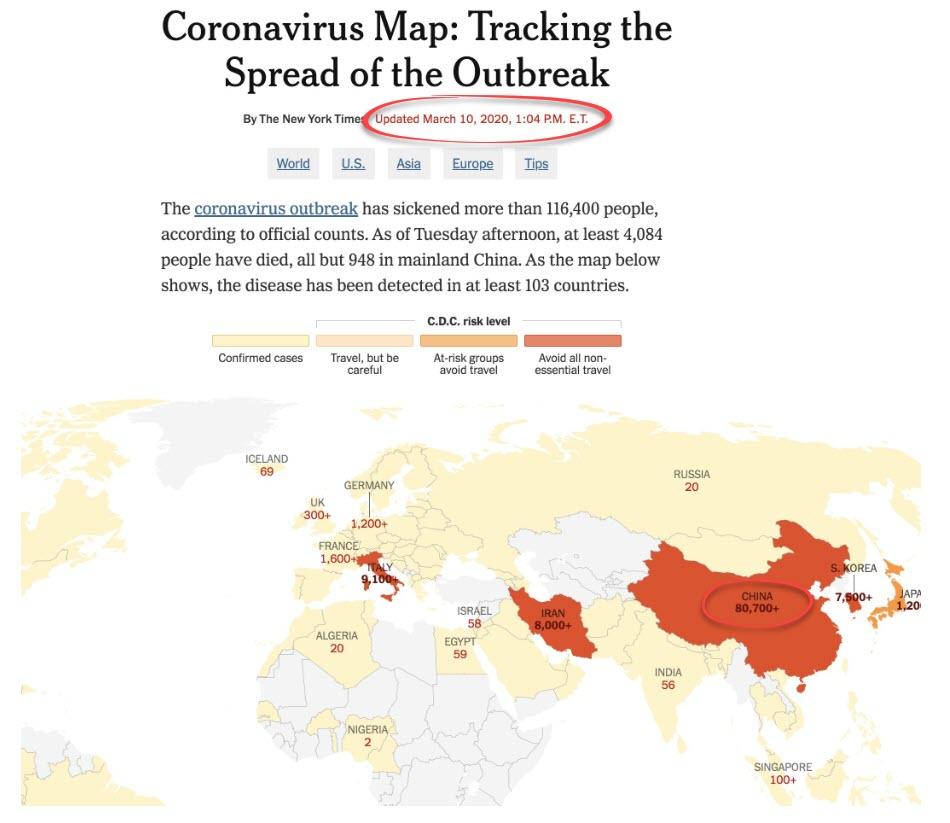

Following a media narrative that President Trump is “racist” for calling COVID-19 the ‘Chinese virus’, the New York Times has now deleted the word ‘Wuhan’ from its coronavirus tracking map.

Trump has repeatedly referred to the outbreak as the ‘Chinese virus’ in an effort to have Beijing take responsibility given that their cover-up of the outbreak in its early months is what rapidly accelerated the current global pandemic.

The media responded, in some instances by directly amplifying Chinese state propaganda, by accusing Trump of “racism” for using the geographically accurate term.

Wow. A reporter from OANN asks Trump a loaded question about whether reporters criticizing his racism are “siding with foreign state propaganda” and Trump uses it as an opportunity to unload on the media pic.twitter.com/tZR7a6T1N5

Now the New York Times has erased the word ‘Wuhan’ from its online coronavirus tracking map in a bid to hide the source of the virus.

BEFORE:

AFTER:

“The Times also altered the name of its map in its February 2 article on the virus, as discovered by independent journalist Jeryl Bier,”writes National File’s Patrick Howley.

Meanwhile, far-left editors over at Wikipedia are desperately trying to change the name of the 1918 Spanish influenza article to remove the word ‘Spanish’ despite it being commonly known as that for over a hundred years.

By removing the word ‘Spanish’, editors obviously hope they can convince the public that naming viral outbreaks after the region in which they originated is not normal, even though it has been virtually since records began.

* * *

My voice is being silenced by free speech-hating Silicon Valley behemoths who want me disappeared forever. It is CRUCIAL that you support me. Please sign up for the free newsletter here. Donate to me on SubscribeStar here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown.

Second Great Depression Begins? Goldman Now Expects A Record 24% Crash In Q2 GDP; Sees 9% Unemployment

On Wednesday we mused that a race had emerged between Goldman and JPMorgan over who can downgrade the US GDP growth rate the most. Up until that point, Goldman held the lead, with its recently announced -5% cut to Q2 GDP. But then JPM’s chief economist Michael Feroli, admitting he really has no idea what he is doing but deciding to do it nonetheless, announced that he now expects Q2 GDP to crater by an unprecedented -14%, a drop the kinds of which have never before been seen.

But Goldman, which just three months ago said the US economy is “nearly recession-proof” (but apparently not depression proof), and instantly lost lost all credibility…

… decided that if it can’t impress its clients with its predictive skills, the least it can do is outshine, or rather outdull, JPM’s forecast which it did moments ago when it slashed its previous GDP estimate published less than two weeks ago, and now sees Q2 GDP crashing at a ridiculous -24% rate, and up from -5% just days ago, which means the US is basically entering a second Great Depression. The trade off, as with JPM, Goldman sees a V-shaped recovery in Q3 but we can likely ignore that: there is no way the country will recover from this kind of “once in a generation” supply and demand shock in 3 months. No way.

While we expect Goldman to take the machete to this analysis as well in the coming days, because if the US economy is indeed paralyzed for at least one quarter, then all of GDP will be lost meaning a -100% annualized print is increasingly likely, here are some of the punchline from the report which will be dramatically revised in just a few days, if not hours.

Over the last few days social distancing measures have shut down normal life in much of the US. News reports point to a sudden surge in layoffs and a collapse in spending, both historic in size and speed, as well as shutdowns of many schools, stores, offices, manufacturing plants, and construction sites. These developments argue for a much sharper drop in GDP in Q1 and Q2.

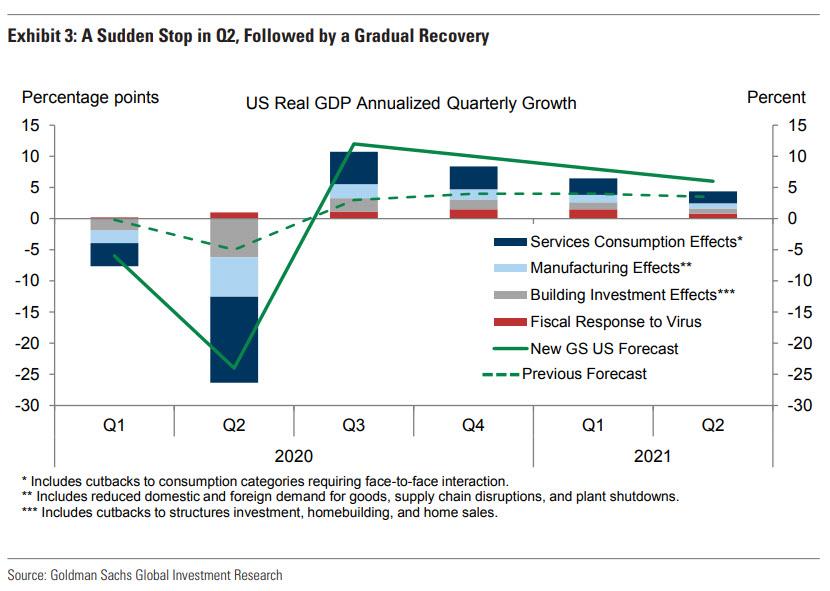

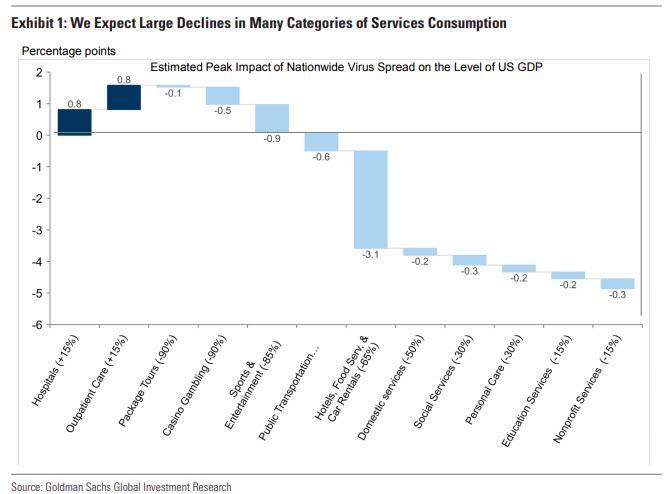

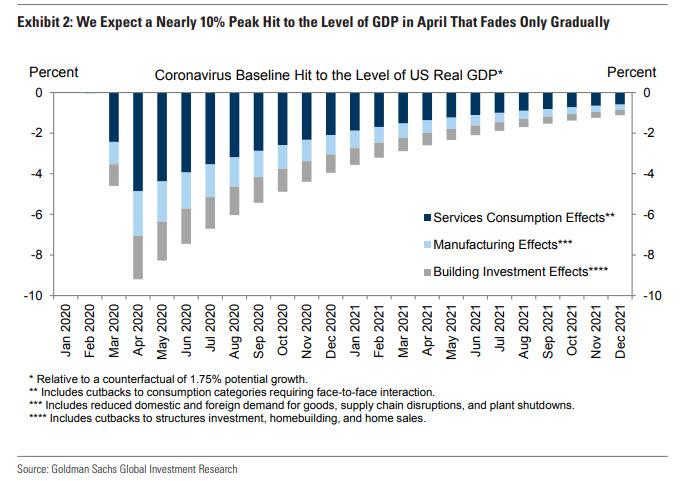

We expect declines in services consumption, manufacturing activity, and building investment to lower the level of GDP in April by nearly 10%, a drag that we expect to fade only gradually in later months. We now forecast quarter-on-quarter annualized growth rates of -6% in Q1, -24% in Q2, +12% in Q3, and +10% in Q4, leaving full-year growth at -3.8% on an annual average basis and -3.1% on a Q4/Q4 basis.

In total, we expect declines in services consumption, manufacturing activity, and building investment to lower the level of GDP in April by nearly 10%. We assume that this drag then fades gradually by 10% each month. While the exact timing is highly uncertain and relapses are plausible, the assumption of a gradual recovery reflects the potential contributions from factors such as effective mitigation and testing actions, weather effects, medical breakthroughs or adaptation by firms and consumers. The slow pace of recovery even in 2021 allows for longer-lasting scarring effects on businesses and workers.

Exhibit 3 translates the monthly path of the level of GDP shown in Exhibit 2 into a quarterly path of GDP growth, adding the impact of the fiscal impulse. We have downgraded our tracking estimate for 2020Q1 to -6% (from -0.2% previously). The largest change to our forecast is in 2020Q2, where we are now forecasting a -24% quarterly annualized growth pace (from -5% previously). A decline of this magnitude would be nearly two-and-a-half times the size of the largest quarterly decline in the history of the modern GDP statistics (-10% quarterly annualized in 1958Q1). It would mean that in only one quarter, the economy would experience an increase in the output gap bigger than that experienced in the entirety of every postwar US recession.

Our assumptions about the gradual fading of the virus drag imply a growth pace of +12% in 2020Q3, +10% in 2020Q4, and +8%/+6%/+4%/+3% in 2021Q1-Q4. Our forecast of full-year growth is now -3.8% on an annual average basis and -3.1% on a Q4/Q4 basis.

Why such an extreme forecast, especially in Q2? The sudden stop in US economic activity in response to the virus is unprecedented, and the early data points over the last week strengthen our confidence that a dramatic slowdown is indeed already underway. In some US states, authorities have now issued statewide shutdown orders to slow the pace of virus spread and avoid overwhelming the health care system, measures that will further reduce the level of economic activity

These unprecedented downgrades to Goldman’s growth forecasts also imply a large upward revision to its unemployment rate forecast as suddenly tens of millions of Americans will be out of a job. Using three approaches—the empirical relationship between GDP and unemployment, the experience of Hurricane Katrina, and a bottom-up analysis of likely job losses by sector and occupation— Goldman estimate a massive 5.5% increase in the U3 unemployment rate to a 9% peak in coming quarters.

What about the $1+ trillion fiscal stimulus, won’t that help?

According to Goldman, the details of the forthcoming fiscal stimulus package could push the unemployment rate in either direction. Unemployment insurance benefits have expanded modestly under Phase 2 of the fiscal package, which became law on March 17. The bank expects a more substantial expansion, including increased benefit payment amounts to cover a greater share of workers’ lost wages, to be included in Phase 3, which will become law the week of March 23. Greater unemployment benefits might make it easier for employers to lay off workers they hope to rehire, knowing that they will receive a higher share of their former wages than employers can pay them.

In the other direction, the Senate Republican proposal for Phase 3 of the fiscal package includes funding for small business loans that would be forgiven if used to finance payroll from March to June, as long as firms pay workers at least 75% of their normal pay. The odds are increasing that such a provision will be enacted as part of Phase 3, but for now a best guess is that more generous unemployment insurance will be the stronger factor, so that on net these two policies are more likely to nudge the reported unemployment rate higher than lower.

Whatever the final outcome, the bottom line is that if unemployment hits 10% in a few months, it would make a Trump’s reelection very complicated.

Watch Live: White House COVID-19 Task Force Holds Friday Meeting

As the number of confirmed cases of COVID-19 passes 14,000, the White House task force is holding its Friday task force, where we imagine we’ll be hearing an update about the Senate’s proposed $1 trillion economic stimulus and ‘helicopter money’ package.

It’s slated to start at 11:45, but we imagine it will kick off at least a few minutes behind.

“It’s a war,” says President Donald Trump of his efforts to contain the coronavirus pandemic, and likening his role to that of “wartime president.”

New York Governor Andrew Cuomo welcomed the president’s claim to his commander in chief role in the crisis and his resolve: “The president and I agreed yesterday… we’re fighting the same war — and this is a war.”

Some measures already taken do call to mind actions in wartime.

Commercial airline flights have been reduced or canceled. Schools have been closed. Universities have shut their doors.

Where Ford, Chrysler, GM and other great auto companies shifted production to jeeps, tanks and bombers in 1942, U.S. auto factories have today been shut down to prevent the spread of the virus.

Bars and restaurants are being closed.

This month, millions of Americans will be added to unemployment rolls, and millions of senior citizens and elderly have already followed government directives to “self-isolate” or “shelter in place.”

There is talk of quarantines lasting not days or weeks, as Americans knew in the days of measles, mumps, chickenpox, scarlet fever and polio, but months.

While a new social solidarity and spirit of self-sacrifice seem to be manifesting themselves in this pandemic, can it endure?

Is the country prepared for months, or years, of social isolation, if that is what is required to win this war?

It is a question that needs to be addressed.

Consider. The Chinese government, whose word is admittedly suspect, claims to have achieved a deceleration in the daily number of new coronavirus infections. The South Koreans say they, too, have broken and reversed the momentum of the spread of the virus.

On March 3, the number of new cases of the coronavirus reported across South Korea was 852. On St. Patrick’s Day, March 17, exactly two weeks later, the count was 85 new cases, a plunge of 90%.

South Korea appears to have “flattened the curve.”

We Americans, however, are far from that.

Exactly how far behind South Korea we are cannot be known until more tens of thousands of Americans are tested, and we learn how many cases of the disease are out there undiscovered and unreported.

But whatever the success of Asian nations in containing the virus, are we politically and socially able to impose the same draconian measures?

Ordering people to “shelter in place” in their own homes, not just for days or weeks but months — can this be done in a free society, as it can be done in the surveillance state of Communist China?

Can mayors and governors of beach towns along the East Coast from Maine to Miami, and the Gulf Coast from Florida to Texas, keep tens of millions from gathering on beaches this summer?

Last week, we saw college kids cavorting on Florida’s beaches, despite warnings that any one among them infected with COVID-19 could transmit it to the rest, leading to grave illness and, in some cases, death.

Moreover, they could become carriers of the disease to parents and siblings. They did not seem to care.

As Prohibition proved, Americans are a rule-breaking people.

Scores of thousands are injured in auto accidents and thousands killed each year from driving under the influence of alcohol, despite tough laws against drunk driving.

Since the 1960s, laws against the use of marijuana, cocaine, heroin, fentanyl, have not halted the rampant ingestion of illegal narcotics and dangerous drugs.

We are endlessly admonished that climate change poses an existential threat to the planet. But have the elites who profess to believe this given up flying in private jets? Have Americans given up their SUVs or ceased to heat their homes with oil and gas?

Are parents going to be able to confine to their homes children whose lives are built around friends on playgrounds? Is the crowd on Martha’s Vineyard going to give up socializing to prevent the spread of the coronavirus?

In the ’60s, we were told that the correlation between cigarette smoking and lung cancer, emphysema and heart disease, is absolute. Yet 34 million Americans continue to risk shortening their lives by smoking.

Seniors and elderly, among whom the mortality rate from the coronavirus is the highest — 15% of those over 80 in one estimate — may shelter in place for months.

But if, in diverse cities, minority communities come out for block parties in summer, are we going to have the police march them back into their homes? Do we have enough cops for that?

A prediction: The longer the orders to shelter in place and self-isolate remain in force, the greater the probability they will begin to be ignored and people will take the risks to end their isolation and be with friends.

Will Americans suffer in social isolation, inside their own homes for months, while a state-induced Great Depression washes over the land?

Trump Nixed Calls For Large-Scale Attack On Iranian Proxies, Citing Covid-19

In what appears the first significant US foreign policy alteration due to the coronavirus pandemic, President Trump reportedly nixed plans for a large-scale attack on “Iranian proxies” in Iraq last week amid a tit-for-tat following rocket attacks on a US base there, which killed two Americans.

The Commander-in-Chief specifically cited coronavirus as reason for holding off on such a major attack, which would surely bog American forces down further in an ongoing battle against Iran inside neighboring Iraq, which Washington fears has long come under the control of the Shia clerics in Tehran. More importantly, the president thought it would “look bad” at the moment of a global pandemic.

NBC reports: “President Donald Trump told his top national security advisers last week that because of the coronavirus pandemic he didn’t think an aggressive response to new attacks on U.S. troops in Iraq by Iranian-backed militias was the right move, according to one former and four current senior U.S. officials.”

Image source: Reuters

He was reportedly being pressed by Iran hawks in the cabinet, of which there are plenty, for a much more muscular attack. Instead US airstrikes on Kataeb Hezbollah locations across southern Iraq on March 12 were limited to to just five militia weapons depots.

Trump rejected the proposals, and stunningly in a rare moment of White House common sense decision-making under pressure, NBC reports:

Trump expressed concern that hitting back hard at Iran at this time would make the U.S. look bad given the extent to which Iran and the rest of the world are struggling to contain the spread of COVID-19, the officials said. They said the president made the comments during a meeting at which his advisers briefed him on possible military responses to the attacks.

If only such concerns of “looking bad” in front of the rest of the world would be even a remote consideration in more normal times, perhaps Washington’s constant foreign policy adventurism could finally be reigned in.

The US has come under intense criticism from Europe and allies across the globe for its severe sanctions on Iran at a moment the pandemic threatens millions inside the economically devastated country.

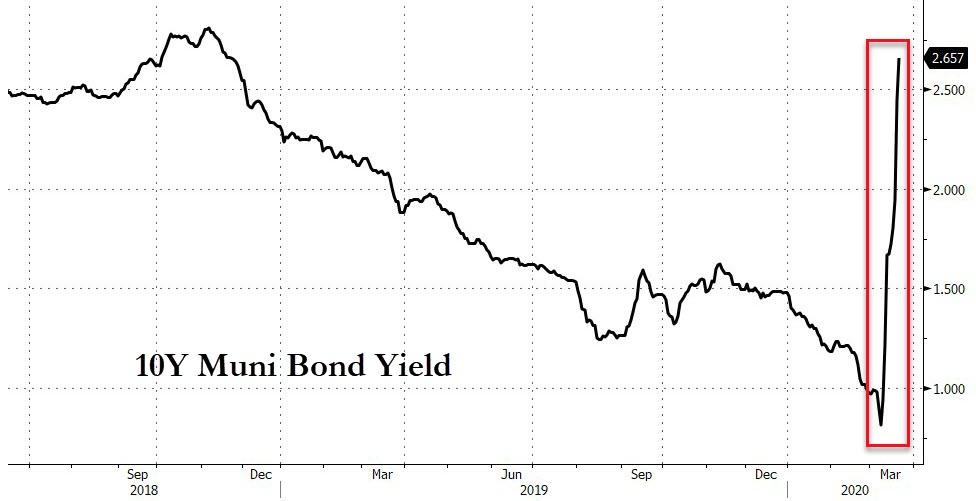

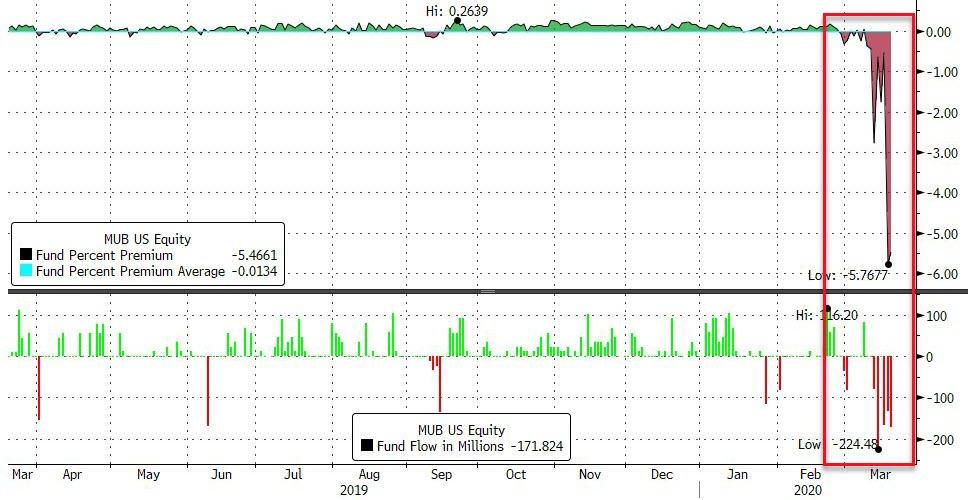

Fed Expands Bailout Facility To Muni Bonds After Market Meltdown

In yet another expansion of The Fed’s intervantionary reach into ‘markets’, The Fed has decided to “expand its program of support for flow of credit to the economy by taking steps to enhance liquidity and functioning of crucial state and municipal money markets.”

This is a move they never played during the Lehman crisis.

This is why – the Muni market is collapsing…

As a reminder, the Muni Bond market had ‘broken’ with investors desperately using the ETFs to hedge…

Completely decoupling the ETF from the underlying due to lack of liquidity…

Fed Statement:

The Federal Reserve Board on Friday expanded its program of support for the flow of credit to the economy by taking steps to enhance the liquidity and functioning of crucial state and municipal money markets. Through the Money Market Mutual Fund Liquidity Facility, or MMLF, the Federal Reserve Bank of Boston will now be able to make loans available to eligible financial institutions secured by certain high-quality assets purchased from single state and other tax-exempt municipal money market mutual funds.

Eligible Collateral: Collateral that is eligible for pledge under the Facility must be one of the following types:

1) U.S. Treasuries & Fully Guaranteed Agencies;

2) Securities issued by U.S. Government Sponsored Entities;

3) Asset-backed commercial paper that is issued by a U.S. issuer, is rated at the time purchased from the Fund or pledged to the Reserve Bank not lower than A1, F1, or P1 by at least two major rating agencies or, if rated by only one major rating agency, is rated within the top rating category by that agency;

4) Unsecured commercial paper that is issued by a U.S. issuer, is rated at the time purchased from the Fund or pledged to the Reserve Bank not lower than A1, F1, or P1 by at least two major rating agencies or, if rated by only one major rating agency, is rated within the top rating category by that agency; or

5) U.S. municipal short-term debt that:

i. Has a maturity that does not exceed 12 months; and

ii. At the time purchased from the Fund or pledged to the Reserve Bank:

1. If rated in the short-term rating category, is rated in the top short-term rating category (e.g., rated SP1, MIG1, or F1, as applicable) by at least two major rating agencies or if rated by only one major rating agency, is rated within the top rating category by that agency; or

2. If not rated in the short-term rating category, is rated in the top long-term rating category (e.g., AA or above) by at least two major rating agencies or if rated by only one major rating agency, is rated within the top rating category by that agency.

How long until corporate bonds… and stocks… are added to the list?

{kind=link}