House Intelligence Committee Ranking Member Devin Nunes appears with Maria Bartiromo to discuss two very important issues.

The first is the origination of the “whistle-blower” complaint and new issues surrounding Intelligence Community Inspector General Michael Atkinson.

The second important subject is the background of newly installed FISA Court monitor, David Kris, to oversee the FBI reform promises.

CTH has some explosive new information which has been shared with Mr. Nunes on both issues; but we start with the interview and ICIG Michael Atkinson.

Since our original research into Atkinson, there have been some rather interesting additional discoveries.

The key to understanding the corrupt endeavor behind the fraudulent “whistle-blower” complaint, doesn’t actually originate with ICIG Atkinson. The key person is the former head of the DOJ National Security Division, Mary McCord.

Prior to becoming IC Inspector General, Michael Atkinson was the Acting Deputy Assistant Attorney General and Senior Counsel to the Assistant Attorney General of the National Security Division, Mary McCord.

It is very safe to say Mary McCord and Michael Atkinson have a working relationship from their time together in 2016 and 2017 at the DOJ-NSD. Atkinson was Mary McCord’s senior legal counsel; essentially her lawyer.

McCord was the senior intelligence officer who accompanied Sally Yates to the White House in 2017 to confront then White House Counsel Don McGahn about the issues with Michael Flynn and the drummed up controversy over the Russian Ambassador Sergey Kislyak phone call.

Additionally, Mary McCord, Sally Yates and Michael Atkinson worked together to promote the narrative around the incoming Trump administration “Logan Act” violations. This silly claim (undermining Obama policy during the transition) was the heavily promoted, albeit manufactured, reason why Yates and McCord were presumably concerned about Flynn’s contact with Russian Ambassador Sergey Kislyak. It was nonsense.

However, McCord didn’t just disappear in 2017 when she retired from the DOJ-NSD. She resurfaced as part of the Lawfare group assembly after the mid-term election in 2018.

THIS IS THE KEY.

Mary McCord joined the House effort to impeach President Trump; as noted in this article from Politico:

“I think people do see that this is a critical time in our history,” said Mary McCord, a former DOJ official who helped oversee the FBI’s probe into Russian interference in the 2016 presidential election and now is listed as a top outside counsel for the House in key legal fights tied to impeachment. “We see the breakdown of the whole rule of law. We see the breakdown in adherence to the Constitution and also constitutional values.”

“That’s why you’re seeing lawyers come out and being very willing to put in extraordinary amounts of time and effort to litigate these cases,” she added. (link)

Former DOJ-NSD Head Mary McCord is currently working for the House Committee (Adam Schiff) who created the impeachment scheme.

Now it becomes critical to overlay that detail with how the “whistle-blower” complaint was organized. Mary McCord’s former NSD attorney, Michael Atkinson, is the intelligence community inspector general who brings forth the complaint.

The “whistle-blower” had prior contact with the staff of the committee. This is admitted. So essentially the “whistle-blower” almost certainly had contact with Mary McCord; and then ICIG Michael Atkinson modified the whistle-blower rules to facilitate the outcome.

There is the origination. That’s where the fraud starts.

The coordination between Mary McCord, the Whistle-blower and Michael Atkinson is why HPSCI Chairman Adam Schiff will not release the transcript from Atkinson’s testimony.

It now looks like the Lawfare network constructed the ‘whistle-blower’ complaint aka a Schiff Dossier, and handed it to allied CIA operative Eric Ciaramella to file as a formal IC complaint. This process is almost identical to the Fusion-GPS/Lawfare network handing the Steele Dossier to the FBI to use as the evidence for the 2016/2017 Russia conspiracy.

Atkinson’s conflict-of-self-interest, and/or possible blackmail upon him by deep state actors who most certainly know his compromise, likely influenced his approach to this whistleblower complaint. That would explain why the Dept. of Justice Office of Legal Counsel so strongly rebuked Atkinson’s interpretation of his responsibility with the complaint.

In the Justice Department’s OLC opinion, they point out that Atkinson’s internal justification for accepting the whistleblower complaint was poor legal judgement. [See Here] I would say Atkinson’s decision is directly related to his own risk exposure:

Michael Atkinson was moved from DOJ-NSD to become the Intelligence Community Inspector General (ICIG) in 2018. What we end up with is a brutally obvious, convoluted, network of corrupt officials; each carrying an independent reason to cover their institutional asses… each individual interest forms a collective fraudulent scheme inside the machinery of government.

Michael Atkinson and Mary McCord worked together in 2016/2017 on the stop-Trump surveillance operation (FISA application via DOJ-NSD). Then, following the 2018 mid-term election, in 2019 Mary McCord and Michael Atkinson team up again on another stop-Trump operation, each in a different position, and -working with others- coordinate the House impeachment plan via the ‘whistle-blower’ complaint.

While Devin Nunes is focused on the false statements of ICIG Michael Atkinson, the key is the contact between the ‘whistle-blower’ (Eric Ciaramella) and the House Intelligence Committee via Mary McCord.

There’s a very strong likelihood this entire impeachment construct was manufactured out of nothing.

National Security Council resistance member Alexander Vindman starts a rumor about the Trump-Zelenskyy phone call, which he shares with CIA operative Eric Ciaramella (a John Brennan resistance associate). Ciaramella then makes contact with resistance ally Mary McCord in her role within the House. McCord then helps Ciaramella create a fraudulent whistle-blower complaint via her former colleague, now ICIG, Michael Atkinson…

…And that’s how this entire Impeachment operation gets started.

Howard Marks: Now Is Not A Good Time To Be Investing

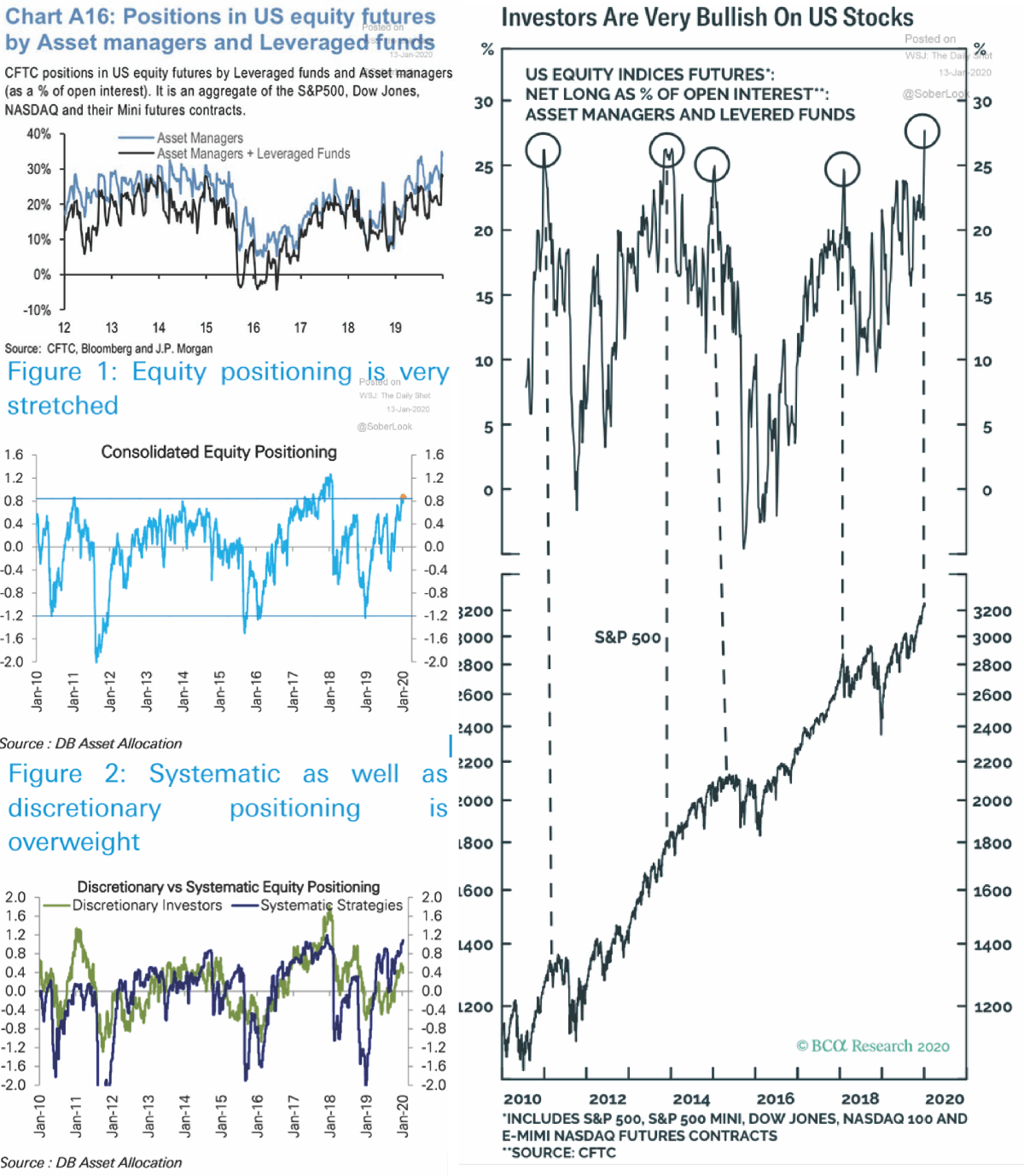

Over the weekend we showed that amid the most violent market meltup since Jan 2018, institutions, retail and systematic investors (i.e., algos, quants, risk parity, CTAs, etc) were now “all on.” And, according to one of the most iconic investors in recent history, they are also on their own.

In an interview on Bloomberg TV with Erik Shatzker, Oaktree Capital’s Co-Chairman, and one of the most respected investors on Wall Street, Howard Marks flat out said that anyone buying stocks here, with the S&P at nosebleed record levels benefiting from the Fed’s $100 billion per month liquidity injection, will likely lose.

Answer a question posted by Shatzker if now is a good time to be investing, Marks says that “it’s not”, and notes that “the market’s been up for 11 years, it’s quadrupled off the low, we’re in the longest bull market, the longest expansion in history, profits are not rising, stock prices are, it’s what we call a liquidity-driven rally, it comes from people having a lot of money to spend,” Marks told Bloomberg Television.

He’s right: as the WSJ noted earlier, US corporate earnings have been down for 4 consecutive quarters – a full-blown earnings recession, and yet the S&P was up almost 30% in 2019. Why? Because of multiple expansion, i.e., the ongoing unprecedented effort by central banks to reflate asset prices:

The US has been in an earnings recession for 4 consecutive quarters: the 29% gain in 2019 was entirely due to multiple expansion https://t.co/RAF2Svxbid

What does this latest artificial surge in stocks mean to the one of Wall Street’s greatest minds?

“It doesn’t mean that the market’s going to go down tomorrow, but it does mean that the odds are not, in my opinion, in the investor’s favor.“

Marks advised that “this is a time to have less risk than you did 3 or 5 years ago”, which is ironic in a market which as DB noted over the weekend, has virtually everyone all in.

The reason: sooner or later securities prices will rise to a levels where they’ll go “over the cliff.” Not just yet thought: even as the S&P 500 has been climbing to new records, spreads on high-yield bonds are again nearing their post-crisis low.

Referring to his latest memo published earlier today and titled “You Bet“, in which Marks discusses his investing life as a “gambler”, Marks said that now more than ever is a time when investors need to be careful, not just where they invest but whom they invest with. The bottom line to Marks is that investing, like gambling, comes down to three things: skill, luck and information, but the distinction between skill and luck is critical, because one is like roulette; the other is like poker.

For example, the market for large-cap equities has become so efficient that, as with roulette, outcomes have more to do with chance than stock-picking ability.

“It’s a luck game,” Marks said. “If you don’t have a manager who has an exceptional skill, and exceptional means rare, then you should go into an index fund, which doesn’t presuppose skill and doesn’t charge for it.”

What Marks doesn’t say is that in a market where the only information one needs is that Fed has made sure there is no downside risk, one doesn’t need luck… or skill, and the best returns come from merely levering up on the S&P500. It also explains why virtually all hedge funds have underperformed the market over the past decade despite charging an arm and a leg for the “privilege” of managing your money.

Ultimately, the question is which markets are inefficient enough – and if any are left – that professional money managers can generate alpha, or excess return, and charge for it. Here one can make an argument that in a world in which there is $16 trillion in excess liquidity, there is no longer any inefficiency and the only thing left is overvaluation. As such the only question is whether one bets alongside central banks, or bets that they will fail. With the S&P at all time highs, we know what the answer is right now.

And while Marks said that in high yield there is still the ability to extract alpha, despite the growing popularity of indexing, and that he believes Oaktree can successfully use credit analysis to cut risk without commensurately reducing returns, we somehow doubt it. If that was the case, Marks would not have cashed out, selling nearly two third of Oaktree to Brookfield nearly a year ago.

Doug Kass’ 15 Surprises For 2020: Biden Tops Trump, Stocks Slump, Auto Industry Dumps

Authored by Doug Kass (@DougKass) via Seabreeze Partners,

Like Diogenes with his lantern, I am, again in 2020, a cynic looking for truth (and an honest investor) – as I engage in my annual assault on the consensus and “Group Stink.”

More than any year in the last decade, the contour of the U.S. stock market will likely be importantly influenced and shaped by politics and profits in 2020. Surprises in the political arena and in corporate profitability are my first two and most important deviations from the consensus.

2020 could be the year of mean reversion – a year of the vanishing Fed (and global central banker) put and a surprising turn in central bank policy (by the ECB), weakening global economic growth and less than expected corporate profits (again), political upsets (again), rising geopolitical risks (and global conflicts), a general recognition of the risks associated with untamed deficits and large debt loads and general market instability.

Remember, my Surprise List is not a set of forecasts. Rather, the List represents events that the consensus views as having a low probability of happening (20% or less) but, in my judgment, have a better than 50% chance of occurrence. In betting parlance this is called an “overlay.”

* * *

Surprise #15 A Credit-Related Event Causes a Market Liquidity Crunch as Covenant-Lite, Leveraged Loans, BBB-rated Downgrades All Pose a Potential Threat to Both the Debt and Equity Markets

Credit conditions tighten with more differentiation between CCC and BBB corporate and consumer credit. More companies fall out of CCC and out of BBB into high yield.

Surprise #14 Market Structure Haunts Our Markets Throughout the Year

The dominance of ETFs and quant strategies (e.g. risk parity) shows its ugly side.

The 2019 movie is in reverse this year – the ETFs and quant products and strategies that delivered a recipe for the relentless advance last year are reversed and, with so many looking to exit, liquidity evaporates. ETF prices, in particular, exhibit greater volatility than the underlying constituent holdings. The dominance of passive strategies is threatened and active strategies begin to garner inflows after a lengthy period of losing market share. Over one quarter of the listed ETFs are delisted.

A “Flash Crash” takes the S&P Index down by over -5% in one day. Volatility rockets to over 35 and stays elevated for most of the year.

Surprise #13 FANG(A) Gets Redubbed FAMG(A) With Microsoft Replacing Netflix

The competition from other streaming services causes Netflix (NFLX) to lose millions of domestic subscribers. The whole pricing power story unravels and market loses faith in the cash burning narrative. Netflix’s shares trade down to $200/share.

Surprise #12A Large Sell-Side Brokerage Firm Abandons its Research Department

Owing to Unbundling of Services and the General Lack of Profitability Associated With Their Efforts

Surprise #11 A Well Known Trader\Investor Who Frequently Appears on Bloomberg, Fox Business and CNBC is Indicted By the SEC For Failure to Disclose His Transactions and Investment Positions In a Proper and Timely Manner

The SEC discloses that many others have failed to fully disclose positions and their trading. The SEC releases a broad edict to all financial media outlets, websites, etc. to adopt new transparency and reporting requirements similar to what is currently required by sell-side brokerage firm’s research departments.

WeWork isn’t the last failed unicorn that tries to IPO itself. The private values on a basket of money losing unicorns falls by over 30%.

Venture capital becomes scarce. There are negative knock on effects throughout the Northern California economy. Late in the year Facebook (FB) , Alphabet (GOOGL) and Amazon (AMZN) begin to show the signs that a chunk of their revenue comes from venture based start-ups – their share prices suffer.

Private equity does not escape the turmoil in venture capital.

Surprise #9 Stock Surprises Abound – Boeing, General Electric, Tesla, ViacomCBS, Comcast, Google, Facebook, Kohl’s, Ford, Square,Twitter, Federal Express, European Banks, U.S. Pharma/Healthcare and U.S. Energy

Boeing’s (BA) shares experience a one day rally of nearly +10% – not because of an earlier than expected return of Max 737 production but because Airbus (EADSY) encounters its own set of major safety issues and problems.

General Electric’s (GE) shares climb to $20/share as the company’s makeover succeeds faster than expected. (Stan Druckenmiller reports that he made $200 million personally on his investment in GE and commits his $0.2 billion personal gain to expanding the reach of Harlem’s Children Zone – Stan is Board Chairman of HCZ).

Tesla’s (TSLA) shares rise to $600/share before it poops out. Elon Musk marries Grimes, his pregnant girlfriend. The couple divorces by year-end.

Old media outperforms new media – ViacomCBS (VIAC) and Comcast’s (CMCSA) shares surprisingly outperform Facebook and Google’s common stock.

European bank stocks are global stock winners – rising by +30% to +40%.

With Democrats gaining control of the Congress and Presidency – healthcare and pharmaceutical stocks are global losers and drop by more than -30%.

Iran waits until the summer and then unleashes physical attacks (through sleeper cells) and cyber attacks in the Middle East, Europe and the U.S. President Trump retaliates. The Strait of Hormuz is closed. The price of oil spikes to over $80/barrel (and stays high through most of the year). Energy stocks run counter to the market’s losses and surprise to the upside in 2020 – with gains of nearly 20%. Several, low-priced energy companies’ share price doubles in price.

A large Enron-like fraud is uncovered (and shocks the markets).

Berkshire (BRK.A) (BRK.B) acquires FedEx (FDX) (see Surprise #7 below).

Jack Dorsey decides to live full time in Africa: In an attempt to improve its position in payments and social media, Google acquires both Square (SQ) and Twitter (TWTR) (beating out Salesforce (CRM) in the process).

Volkswagen (VLKAF) acquires Ford (F) (see upcoming Surprise #4).

Surprise #8 Goldman Sachs Acquires The Vanguard Group (with over $5.3 trillion of assets under management)

In an attempt to expand its retail presence.

Surprise #7 Berkshire Hathaway and Warren Buffett Surprise the Markets – On Several Fronts

Berkshire Hathaway, with over $130 billion of cash, acquires FedEx (for $55 billion) in a spirited bidding contest against Walmart (WMT) . There are several important catalysts to the transaction – Buffett understands FDX’s business and the deal would expand his scale in transportation – where he already enjoys a stronghold in rails with subsidiary Burlington Northern. Moreover, despite the recent Amazon issue, FedEx has a wide business moat with a vast distribution presence and a large fleet of vehicles. Finally, FedEx’ shares have been pummeled (-20%) because of a difficulty in adopting to digital commerce and the company could be purchased on the cheap at under 20x earnings.

Berkshire makes two more large acquisitions – reducing its cash position by $100 billion to $30 billion.

Fires in California grow entirely out of control, shutting down much of the power grid in California – and hobbling the state’s economy. President Trump does not come to the aid of the state until too much damage is done. But Buffett helps and provides bankruptcy financing by Pacific Gas and Electric (PCG) . While it is normally impossible to buy a regulated utility, at the request of regulators Berkshire ultimately takes control of the company.

Contrary to being a “forever holding,” Berkshire unloads a portion of its Apple (AAPL) long investment after the stock becomes too large a percentage of its portfolio.

At the May, 2020 Berkshire Hathaway annual meeting in Omaha, Nebraska, Warren Buffett surprises his shareholders and announces that Ajit Jain will be his successor .

The Oracle of Omaha invites me back to the 2021 Berkshire Hathaway Annual Meeting to ply him and Charlie Munger with tough questions.

Surprise #6 Despite Weakening Economic and Profit Growth the Federal Reserve Does Not Lower Interest Rates This Year

Instead of waiting until the end of Q2 as they currently have planned, the Fed ends the expansion in their balance sheet by February or March. The liquidity spark helping stocks thus ends early.

Foreigners lose their appetite for U.S. corporate debt and government securities and, despite disappointing U.S. economic growth, the 10 year U.S. note yield climbs to over 2.50%.

Surprise #5WithDraghi Gone, ECB Monetary Policy Abruptly Changes and Interest Rates Are Increased

With no more Draghi, the ECB figures out negative rates are a hindrance to growth and has gutted the European banking industry – it normalizes policy. While long term positive, it ends up creating a major disruption in the global bond markets and yields around the world spike. Most European government debt returns to a positive yield. European equity markets rise +20% (compared to a -20% drop in the U.S. indices)

European bank stocks rise by +30% to +40%.

Surprise #4 Watch Out Below!Automobile Industry Sales Plummet and Threaten the Domestic and Global Economies… Ford Is Bailed Out

“Peak Autos” remains in place and the problems facing the industry reverberate in 2020.

At every level there is a ton of automobile loan and securitized debt leverage. A record share of trade-ins last year were upside down on their loans – representing a mirror image of mortgages that existed in 2007.

Retail sales of new vehicles were down by -7% in December, 2019, leading to a retail SAAR of only 14.3 million cars (down from 15 million a year ago and from November, 2019’s 14.8 million rate).

The auto industry falls into a tailspin in 2020 – fueled by burgeoning inventories, record cars going off lease (and entering the used car market), record new car prices (according to J.D. Power and LMC Automotive, the average new care price is now over $35,000), a decline in used car prices, growing and record purchase incentives (of nearly $4,600/unit, a +12% increase from last year), and rising auto loan delinquencies (which hit an all-time high in 3Q2019) causes a substantial amount of damage to the sub-prime auto asset backed securities market in 2020).

The automobile’s sizable role in the domestic economy causes collateral damage to U.S. consumer confidence and spending.

Late in the year, Ford Motor (F) company teeters operationally and financially and the shares fall to under $5/share. The loss-ridden manufacturer is acquired by Volkswagen (VLKAF) .

Surprise #3 The China Trade Deal Falls Apart, China’s Patience With Hong Kong Runs Out and There Is a Global Shortage of Protein

China doesn’t comply with “Phase One” of the trade deal which offers little more than purchasing needed agriculture products and fails to protect U.S. intellectual property.

China’s patience in Hong Kong runs out and it takes action that sets off both a geopolitical and stock market crisis. China’s aggression ends any chance for a “Phase Two” trade deal.

The trade war is reignited and tariffs are reimposed on China.

Capital spending, consumer and business confidence falters.

Speaking of China, the effects of African Swine Fever Virus cause a global shortage of protein. The immediate impact a year ago was wholesale slaughtering, which created a short term surplus. But, now there aren’t enough pigs. Pork prices soar with beef, chicken and fish prices rising in sympathy.

Surprise #2 Disappointing Global Growth, Weakening Corporate Profits, a Fed Pivot and Political and Geopolitcal Instability Produce a “Garden Variety” Bear Market in 2020

As we entered 2020 the almost universal view is that liquidity and the central banks’ put, at the very least, provides a market floor and at the best, will contribute to the next speculative leg of the decade old Bull Market as the market train is supported by the Fed trestle.

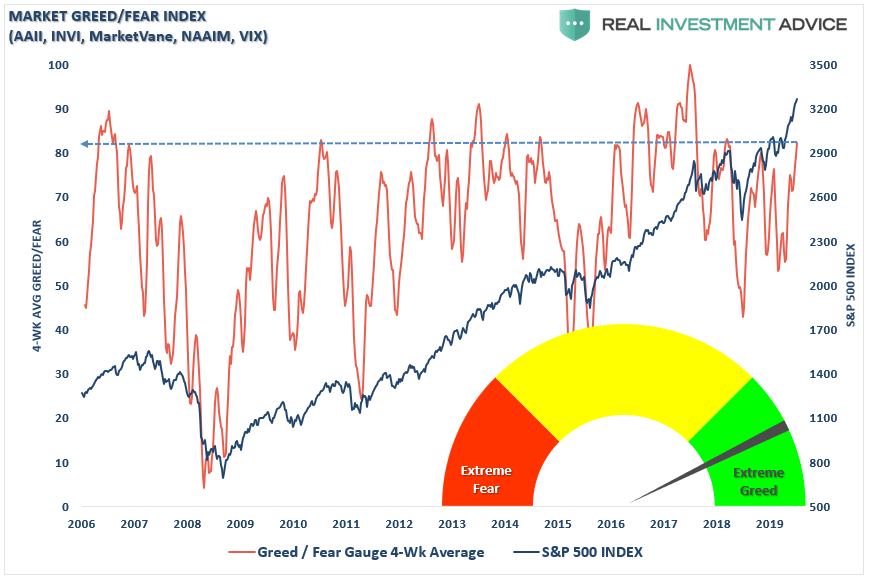

As I finished My15 Surprises for 2020 over the weekend and reviewed the extraordinary nature of the 2019 market — I marvel at the Bull Market in Complacency that seems almost at the polar opposite of the doom and gloom that existed on December 26, 2018, a bit more than 12 months ago. As an example, the CNN Fear and Greed Index was around 2 (!) a year ago compared to 91 (!) this morning. The same applies to the flip flop in AAII sentiment (from very bearish to very bullish – and with the gap between the two moving to over 40).

I would be less concerned with the outlook if the market’s 2019 advance was earnings derived. It was not – like in 2013 it was entirely based on a reset of higher valuations (from a PE of 14.5x at year-end 2018 to approximately 19.0x at year-end 2019). Indeed, consensus 2019 S&P EPS forecasts stood at about $178/share 12 months ago – they are likely to fall in the $163-$164/share level range. As to the 2020 S&P EPS consensus estimates, they, not surprisingly, stand at the same $178/share today! They will likely miss (by an unusually) wide mark, again.

And I would be far less concerned if a changing market structure (the proliferation and popularity of ETFs and the dominance of risk parity and quant products and strategies) coupled with the death of active investing had not served to exaggerate upside price momentum – foiling the natural price discovery many of us “old timers” yearn for.

Meanwhile, as the year concludes, precious metals have made a very “quiet” stealth rally – just look at (GLD) ‘s chart over the last seven weeks. (What are the gold traders seeing that we are not?)

The majority of “talking heads” who hated stocks a year ago are uber bullish on equities this year. (Didn’t we learn from the wrong-footed consensus interest rate forecasts of last December, that self confidently called for a 3.5%+ 10 year U.S. note yield at 2019 year-end?)

Am I concerned? Should investors be concerned? You are damn right. Nevertheless, the consensus remains positive – and the consensus projections shine today with their typical +8% to +10% advance anticipated for the S&P Index.

My view is that next year’s surprise will be a year of mean reversion, but unlike most, I make this surprise without forecast certainty as I recognize that central bankers have lost their collective minds. And so may have many traders and investors.

In 2020, the surprise would be that the “everything bubble” (in which every asset class advanced) is pierced and the notion of mean reversion of returns finally surfaces (just when no one is looking).

Though the third year of the Presidential cycle (2019) was a good one – not so much for the last year of the Presidential cycle (2020).

Despite easing money and an abundance of global liquidity, the rate of growth of the U.S. economy fails to accelerate this year – “The Fed Is Pushing On A String.” Domestic GDP growth slows to under +1% in real terms. Core inflation sits at 2% (but headline inflation is much higher due to rising energy prices). Company share buybacks are sharply diminished as corporate profits disappoint and corporations begin to balk at high stock prices (another surprise)

Though economic growth is slow, interest rates begin to rise in 2020 as the growing U.S. debt load begins to matter. The bond vigilantes slowly return out of hibernation. Higher rates trips up levered corporations and levered consumers. Foreign buyers of credit and Treasuries lose interest in the U.S. debt markets and start selling.

The Fed is stuck and, not wanting to be political, ends its balance sheet expansion and makes no move on interest rates until after the election.

Higher wages and other input costs pressure corporate profits in a backdrop of slowing revenues and domestic growth.

The consensus expectation for 2020 S&P EPS of about $178/share is, for the second year in a row, way off mark as EPS growth falls for the second year in a row because of a continued decline in profit margins that +3% revenue growth can’t overcome. 2020 S&P EPS per share falls to modestly below the $163-$165/share recorded in 2019.

Investors, realizing that corporate profits have essentially been flat since 2014, begin to panic at the “new normal” of subpar economic growth. Another year in which earnings growth fails to recover reverses the valuation upwards reset (so conspicuous last year) as market participants grow increasingly concerned about the real economy’s secular growth prospects.

Much of the more than +25% 2019 reset (higher) of valuations is reversed in 2020 – as price earnings multiples decline by about -15%, producing a modestly larger full year decline (-17%) in the S&P Index. 2020’s market drop is the worst since 2002’s fall of -23%.

The S&P Index closed at 3265 on Friday. The year’s high is made in the first month of the year (at under 3350), the 2020 low in the S&P Index is 2550, and the close is about 2700.

Besides the failure of corporate profits to revive the equity market is burdened by a number of other factors outlined in My 15 Surprises For 2020.

and now…

Surprise #1 Trump Popularity Falters Badly, the Progressive Wing of the Democratic Party Fails to Catalyze Voters, Biden Easily Wins the Presidency and Democrats Have a Clean Election Sweep (As Women and Millennials Show Up in Droves)

According to PredictIt and most of the other polls, the general expectation is that President Trump will narrowly win the November election, the Republicans will retain control of the Senate and the Democrats will keep control of the House.

As in 2016, the (political) consensus proves to be mistaken in 2020.

To summarize, several trends become apparent early in the year, leading to Senator Biden eventually being named the Democratic party’s Presidential nominee. Biden’s lead in the polls climbs and Trump trails by a surprisingly large percentage by early summer. In another surprising election result (much like four years ago) – its a clean sweep for the Democrats – Biden easily wins the November election, Democrats narrowly regain control of the Senate and the Democrats maintain control of the House.

Here is how this and the other surprising political events leading up and into the November election could go down:

Democratic Progressive Presidential Hopefuls Fail and Fall Early – Biden Is The Nominee

Advertising money proves to be a major force in producing candidate support and votes. Both Bloomberg and Steyer climb into the top five Democratic candidates in the national polling as Senator Warren’s popularity wanes.

In the belief that only a centrist candidate can defeat President Trump in November, a surprisingly high number of Democratic voters move to the center (and to the support of non-progressive candidates) during the multiple state primaries on March 3rd.

The progressive left of the Democratic Party moves much lower in the polls and the electability of Senators Sanders and Warren comes into question. Sanders’ “hard ceiling” becomes reality as he finishes in only a weak second or third position in the early February Iowa and New Hampshire primaries. By the end of February, a surging Mayor Pete Buttigieg moves into a virtual tie for second with Sanders (and behind Senator Biden) in the national polls. Warren, seen as talking from both sides of the mouth on campaign financing, after releasing what many consider to be poorly constructed tax recommendations and following modification of some other extreme positions, falters and falls out of the top five behind Biden, Sanders, Buttigieg, Bloomberg and Steyer.

Warren, fearful of a further fall (out of contention), approaches Sanders (who essentially shares the same positions that drags down the Senator from Massachusetts – both are fighting a “rigged system”, “Medicare for all”, tax the wealthy, etc.). She proposes a “prepackaged” progressive ticket and political contract (with Sanders as President and Warren as Vice Presidential candidates – with some shared “Presidential” duties). U.S. stocks briefly tank in response to the possibility of a progressive Democratic Presidential nominee. Sanders initially considers Warren’s offer but rejects it and the contract unravels. Warren, with little money left in her campaign till, falls back further in the polls into seventh place (behind Andrew Yang) and drops out of the race. Surprisingly, many of Warren’s supporters fail to lean towards Sanders and move to the other, more centrist candidates.

Biden never falls behind and maintains his front running status throughout all of the primaries and into the Democratic convention.

Late in the race, Bloomberg and Steyer, recognizing the value of a unified Democratic party against Trump transcend their own personal interests and throw their support towards Biden. Stocks start a steady descent lower as investors view the rising probability of a Democratic President as market unfriendly.

Bloomberg (who is worth $58 billion and is the sixth wealthiest person in the U.S. and 14th in the world) commits “whatever it takes” to help Senator Biden defeat President Trump. In total, Bloomberg eventually spends over $2.5 billion on his Presidential run and later on Senator Biden’s campaign and on the key Senate election contests.

In an uncontested convention Biden is named the Democratic nominee. He selects Amy Klobuchar over Stacey Abrams as his Vice Presidential running mate.

Stacey Abrams delivers a riveting keynote convention address and Pete Buttigieg introduces Senator Biden on the convention’s final day.

The day after his nomination, Republican Senator Mitt Romney endorses Senator Joe Biden .

Trump’s Popularity Slumps Under the Weight of Impeachment and Revelations

In the first half of 2020, just as the impeachment hearings percolate, a New York Times investigation uncovers that President Trump directed the purchase of stock futures by the Fed, the Treasury and other parties (over a lengthy period of months) to buoy the U.S. stock markets and with the stated intent (later disclosed in emails) to improve the chances of his reelection. The discovery and publicity associated with stock futures buying policy (which began to be implemented in late summer, 2019) causes an uproar politically (as leaders of both parties are critical) and Congressional hearings are scheduled – sending markets abruptly lower as there was apparently less to the bull market run than meets the eye.

Though Republicans have a 53-47 majority in the Senate, Senator Susan Collins and four other Republican Senators demand the appearance of witnesses and more than 51 Senators vote to call witnesses in the impeachment hearings despite the threat of Executive Privilege by President Trump. The heated impeachment hearings (which includes Bolton’s explosive testimony which is recounted vividly in his NY Times best selling book), are extended all the way into March, hurting Trump’s popularity.

President Trump avoids being removed from office by impeachment by only one vote in the Senate

Consternation as to the President’s rationale regarding the Iraq military base attack intensifies – further dampening the President’s popularity. Over the past weekend in an interview on “Face The Nation”, the Secretary of the Defense Mike Esper seemed to contradict the President’s statement that there was an imminent threat to four American embassies, saying the justification for killing Soleimani was that it was “probably my expectation” that an attack was imminent. No wonder Republican Senator Mike Lee said Esper’s briefing to Congress was insulting. Pushback that the Administration called for the killing of a foreign leader because it is “probably my expectation” draws increased alarm of both Democrats and Republicans and the voting electorate. Based on testimony and uncovered emails, the evidence mounts that the President’s motivation for the attack was to distract attention from the impeachment trial and because some of the (Republican Senator) jurors in that trial pressured him to do so. (h/t Robert Hubbell) As written in a recent Wall Street Journal column, which chronicles the events leading up to the Iraq attack, the lede is buried deep (30 paragraphs into the analysis). “Mr. Trump, after the strike, told associates he was under pressure to deal with Gen. Soleimani from GOP senators he views as important supporters in his coming impeachment trial in the Senate, associates said.”

The Supreme Court reviews Trump’s assertion that the Supremacy Clause of the Constitution means he doesn’t have to reveal his tax returns. After oral arguments are heard in March, the Court rejects the petition for a writ of certiorari and orders the release of the President’s tax returns. The release of his tax returns clearly shows “questionable” transfers and a significant Russian involvement in his financial affairs (and in those of Jared Kushner and Ivanka Trump).

Jared Kushner and Ivanka Trump return to private life in New York City.

A Washington Post report discloses that Melania Trump and the President have essentially lived in separate quarters since late 2018. The Trumps separate.

Meanwhile, a slowing domestic economy and weakening stock market continue to adversely influence Trump’s polling against the Democratic opponent.

Under the weight of the pressure of running for reelection, a hectic travelling schedule and poor eating habits, President Trump’s health catches up to him. A significant health problem is disclosed in the spring forcing the President to curtail his political appearances for more than a month.

Faced with a unified and financially fortified Democratic Party, extended impeachment hearings, the release of Trump’s tax returns, the stock futures controversy, Russian business disclosures (providing a large amount of loans to Trump and buying inflated homes and condominiums from The Trump Organization), health and marital problems, a weakening stock market and slowing domestic economy – Trump continues to suffer badly in the polls.

Attracted to her recent pro-Trump support which culminated last Monday in a charge that “leading Democrats were mourning the loss of Soleimani” (See Peggy Noonan’s Wall Street Journal story this past weekend and desperate to revive his popularity, Trump dumps Vice President Michael Pence for former ambassador to the United Nations Nikki Haley. (PredictIt has a 90% probability that Pence will be Trump’s running mate).

Voter Turnout Rises Dramatically and Biden Easily Wins the Presidential Election and the Democratic Party Sweeps the Congressional Elections

Voter Turnout rises by over +6% (from 2016) – most of the incremental change is captured by Biden who wins 50.7% of the popular vote compared with 46.3% for Trump – a plurality of over 6 million votes. (That compares to 48% for Secretary Clinton and 46% for President Trump in 2016 – a difference of 2.9 million votes).

Senator Biden also wins a surprisingly large majority in the electoral college (304 to 234).

Though the Republican Party was a huge favorite to retain control of the Senate – the Democrats regain control of the Senate on the coattails of Senator Biden and the widening voter turnout.

Upon winning in November, Biden makes first move and nominates Kamala Harris to the Supreme Court to replace Justice Ruth Bader Ginsberg (who agrees to step down). Stacey Abrams is enlisted to become Attorney General . Pete Buttigieg becomes Secretary of Veteran Affairs. Michael Bloomberg is named Secretary of the Treasury. And, in a move of bipartisanship, Senator Mitt Romney is nominated to the post of Secretary of State.

After the election, there are violent demonstrations around the country by Trump supporters in mid- to late- November. Trump does little to squash or calm down the protests and instead holds a number of rallies against Democrats and the election results.

In December, 2020, President Trump announces his plans to launch Trump TV. Sean Hannity leaves Fox News – assuming a duel role as CEO of Trump TV as well as the station’s chief commentator. Rush Limbaugh and several Fox News commentators join Trump TV.

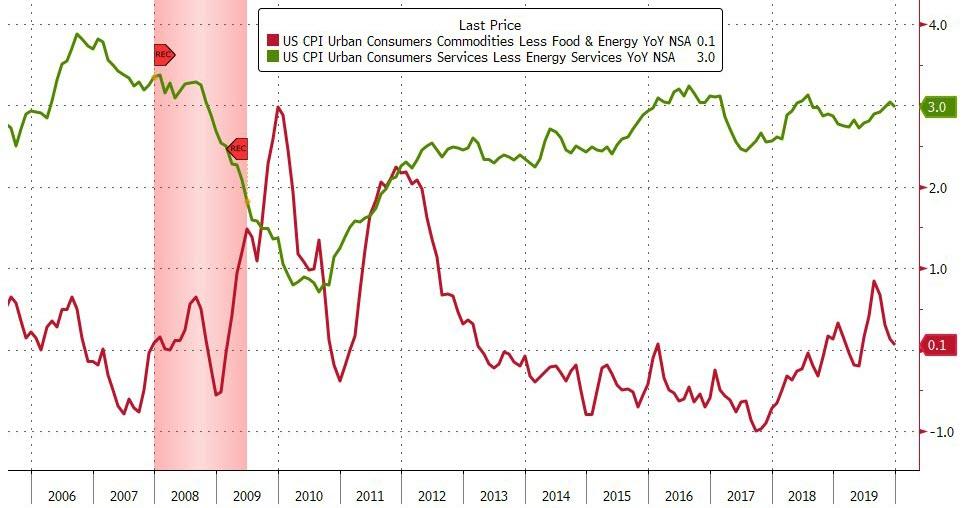

US Consumer Prices Accelerate At Fastest Since Oct 2018

Headline consumer price inflation was expected to accelerate its recent trend higher in December, and it did, but slightly disappointing.

Headline CPI rose 2.3% YoY (below the +2.4% YoY) but above November’s +2.1% and the highest since Oct 2018. Core CPI also rose 2.3% YoY (as expected)…

Source: Bloomberg

Goods prices barely managed to rise YoY in December as Services prices remained up around 3.0% YoY…

Source: Bloomberg

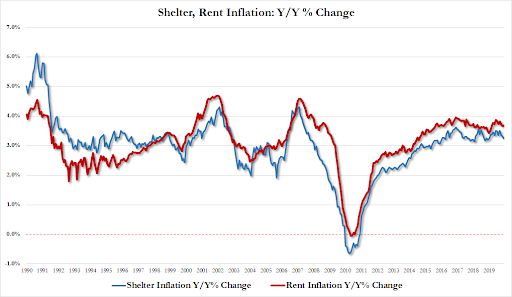

Notably, shelter costs, which make up about a third of total CPI, decelerated…

They rose 0.2% after a 0.3% gain in November, and were up 3.2% year-over-year for the smallest advance since January last year. Both owners-equivalent rent, one of the categories that tracks rental prices, and rent of primary residence climbed 0.2% from a month earlier (up 3.69% YoY – lowest since Feb 2019).

The Labor Department’s CPI tends to run higher than the Commerce Department’s personal consumption expenditures price index, which the Fed officially targets. The core PCE index that policy makers watch for a better read on underlying price trends softened in November, rising 1.6% from the same month in 2018. Core PCE has held below the 2% objective for the better part of seven years.

Having seen all that though, we suspect this push higher in inflation will be dismissed at “transitory” by The Fed as an excuse to keep the liquidity flowing as the asymmetric response function of Powell and his pundits becomes ever more obvious.

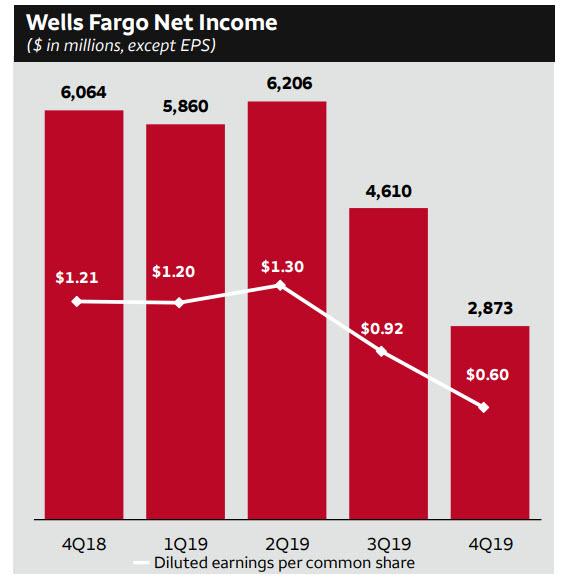

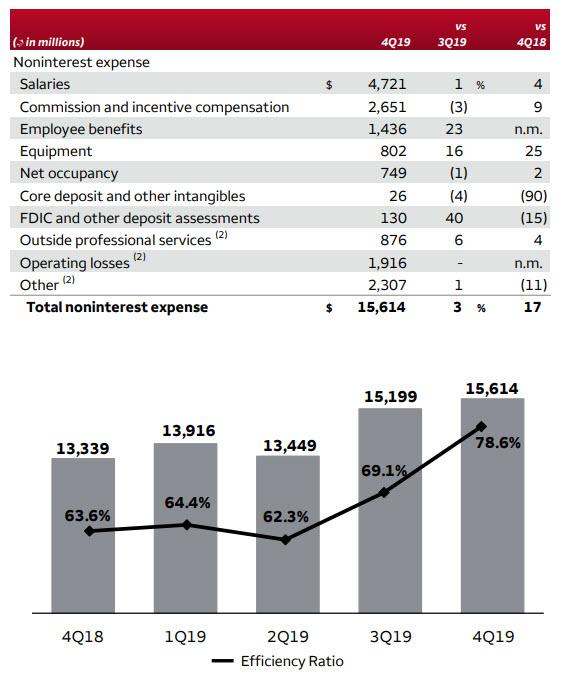

Wells Reports Dismal Q4 Earnings: Huge Earnings Miss, NIM Tumbles As Expenses Soar

If JPMorgan was the posted child for how one should frontrun the Fed’s QE4 (which JPMorgan triggered thanks to the repo market crisis it itself created by pulling liquidity from the market and investing it in risk assets) and report blowout Q4 earnings, Wells Fargo was the polar opposite.

Warren Buffett’s favorite bank reported revenue and EPS which both missed estimates, with Q4 revenue sliding 5.1% to $19.9BN, below the $20.1BN estimate, while Net income of $2.9 billion and diluted EPS of $0.60 (which included the impact of $1.5 billion, or $(0.33) per share, of litigation accruals) also missed estimates of $1.10, even with the one-time adjustment. There were several other adjustments including i) $362 million gain from the sale of our Eastdil Secured (Eastdil) business; ii) $166 million of expenses related to the strategic reassessment of technology projects in Wealth and Investment Management (WIM); iii) $153 million linked quarter decrease in low-income housing tax credit (LIHTC) investment income; iv) $134 million gain on loan sales predominantly junior lien mortgage loans. All this was offset by a $125 million reserve release.

However one defines it, the Net Income trend is hardly Wells Fargo’s friend:

Despite the dismal Q4 results, Wells was proud to announce it returned $9.0 billion to shareholders through common stock dividends and net share repurchases, up from $8.8 billion in 4Q18. Of note, Wells common shares outstanding tumbled 10% to 446.8 million shares, as the bank continued to aggressively buyback shares.

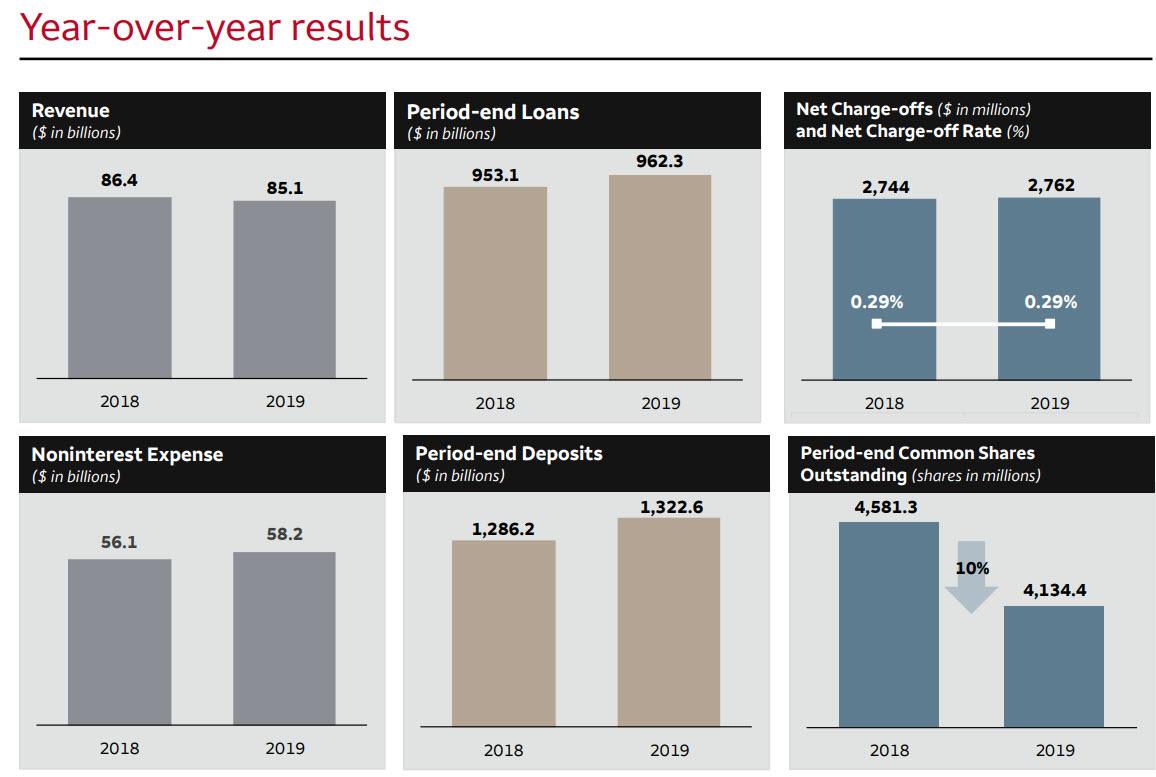

The full year results were not much better, with total revenue shrinking by $1.3 billion to $85.1BN, despite an increase in total loans and deposits, as non-interest expense surged. Not even the 10% drop in common shares outstanding – i.e., thank you massive buybacks – could help the bank’s bottom line.

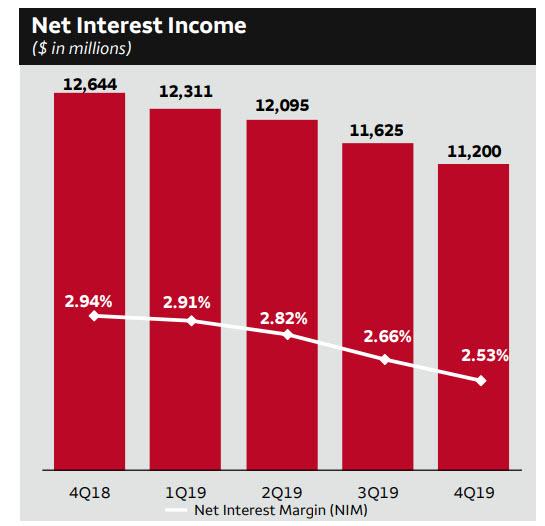

What was the main reason behind Wells’ dismal performance?

As has been the case for the past year, the company’s Net Interest Income just refuses to stop shrinking, and in Q4 it dropped to a new multi-year low of just $11.2BN, down $1.4BN or 11%, largely due to “the impact of a lower interest rate environment.” Not even the impressive increase in earning assets, which rose $18.7 billion Q/Q, could offset the drop: i) Debt securities up $13.7 billion; ii) Loans up $6.7 billion; iii) Mortgage loans held for sale up $1.3 billion; iv) Equity securities up $1.2 billion; v) Short-term investments / fed funds sold down $3.4 billion.

Instead, what was far more notable – and cringeworthy – was that Wells’ Net Interest Margin tumbled to 2.53%, sharply lower than the 2.66% reported last quarter, and missing expectations of a 2.54% print.

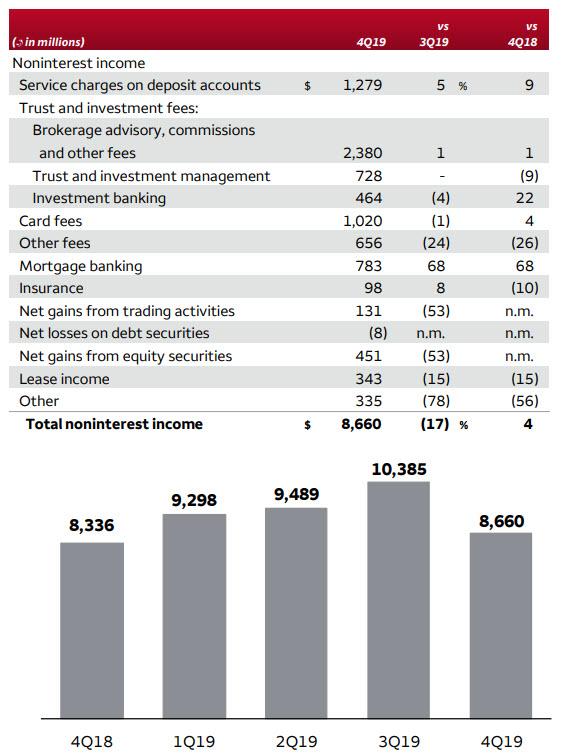

It wasn’t just Interest Income that was disappointing: the bank’s non-interest income barely changed Y/Y at $8.66BN, and down 17% from the prior quarter.

Unlike JPM, Wells’ trading gains were down $145 million from a strong 3Q19

Net gains from equity securities down $505 million “as lower gains from our affiliated venture capital and private equity partnerships were partially offset by $240 million higher deferred compensation gains”

Other income was down $1.2 billion on lower gains from the sale of businesses ($362 million gain from the sale of Eastdil in 4Q19 vs. $1.1 billion gain from the sale of our IRT business in 3Q19), lower gains on the sale of loans ($134 million in 4Q19 vs. $314 million in 3Q19), and $153 million lower LIHTC investment income.

The big problem for Wells is that even as revenues continue to shrink, expenses continue to rise, and noninterest expense was up $415 million Q/Q and $2.3BN, or 17%, Y/Y due to:

Personnel expense up $214 million

Salaries up $26 million

Commission and incentive compensation down $84 million and included lower revenue-related incentive compensation

Employee benefits expense up $272 million and included $258 million higher deferred compensation expense

One reason for the surge in expenses is that this is where Wells lumped the “$1.5 billion of litigation accruals for a variety of matters, including previously disclosed retail sales practices matters, as well as higher customer remediation expense.”

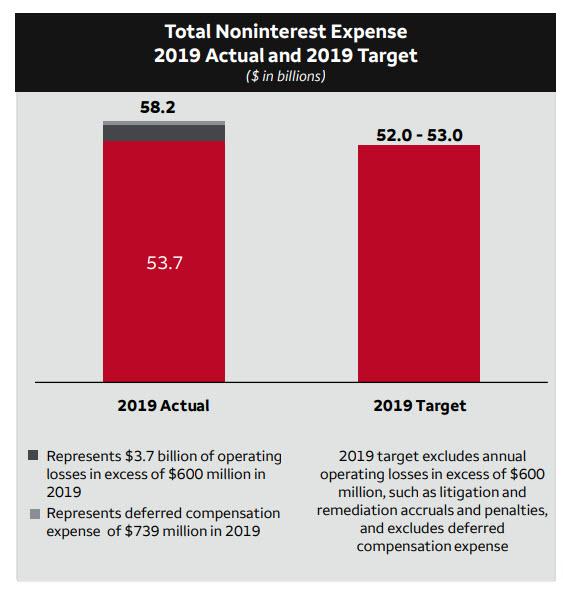

Even Wells notes that its 2019 Actual noninterest expense was $5-$6BN above the internal target, however a lot of this was due to what Wells defined as one-time expenses.

Total noninterest expense in 2019 of $58.2 billion included $4.3 billion of operating losses and $739 million of deferred compensation expense; 2019 noninterest expense excluding $3.7 billion of operating losses in excess of $600 million and excluding; $739 million of deferred compensation expense (P&L neutral) = $53.7 billion

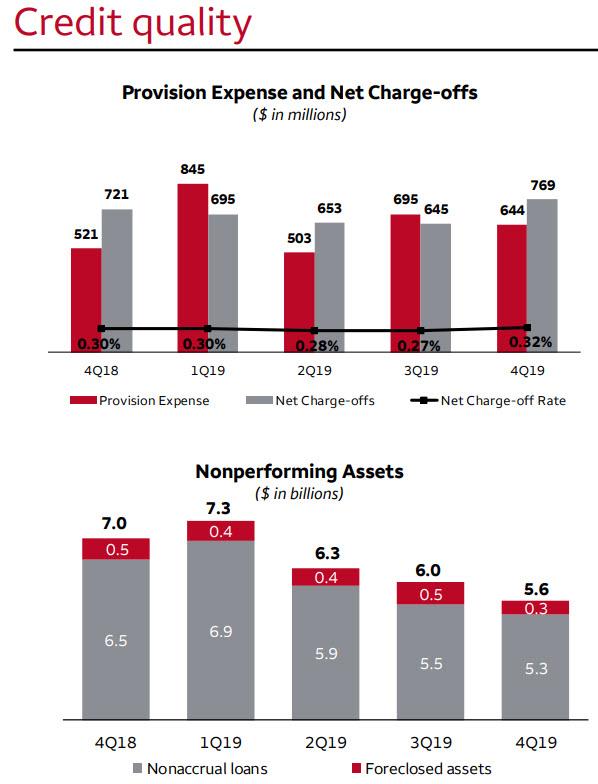

There was some good news in Wells’ credit quality report, where despite jumping 24% Y/Y, provisions for credit losses of $644MM were below the $754MM expected. At the same time, net charge-offs were $769 million, up $124 million from Q3 and the net charge-off rate was 0.32%, up 5 bps.

Also notable, non-performing assets decreased $333 million from Q3, as nonaccrual loans decreased $199 million, including a $141 million decline in consumer nonaccruals reflecting improvement in all asset classes, while foreclosed assets were down $134 million. As a result, Wells recorded a (much needed) $125 million reserve release “on improved credit performance in the consumer loan portfolio and a higher probability of slightly more favorable economic conditions.”

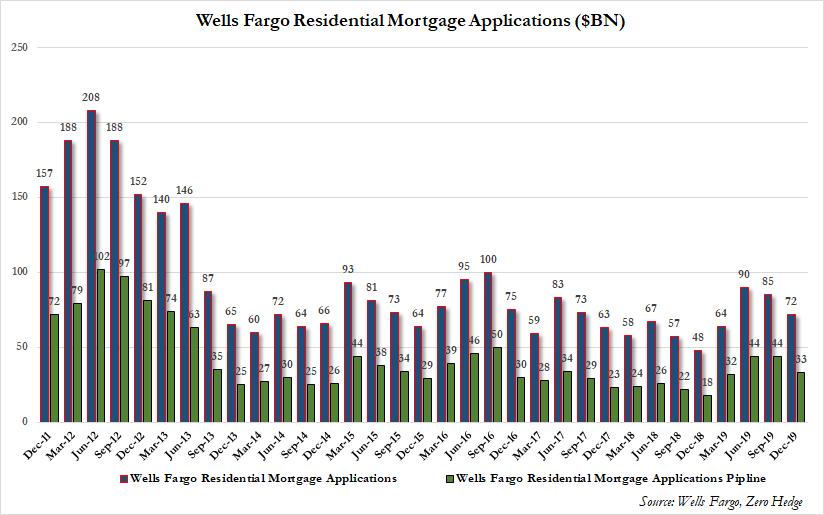

And some more bad news: after Wells Mortgage applications and applications pipeline spiked in Q2 as rates tumbled, this number has since drifted lower for 3 consecutive quarters, as Wells’ “bread and butter” mortgage pipeline appears to be getting clogged again.

Overall, Wells continues to diverge from its trading peers, and as a result of lacking a viable trading desk, Wells continues to get hammered by the ongoing collapse in Net Interest Margin which is depressing the bank’s revenues and earnings. Absent a spike in rates, Wells will likely be the first US “Deutsche Bank” once the Fed cuts rates to negative some time in early 2021. And, not surprisingly, Wells stock is reflecting just these investor concerns as it slides nearly 4% in the premarket.

Apple Responds To AG Barr’s Claim That It Did Not Assist FBI In Pensacola Shooting

Attorney General William Barr requested Apple’s help to extract data from two iPhones that belonged to the Saudi aviation student that fatally shot three US soldiers at a Pensacola naval base last month, reported The Verge.

Barr updated the situation on Monday during a press conference and said Apple had provided no “substantive assistance” in supporting investigators with the unlocking of the smartphones.

“We have asked Apple for their help in unlocking the shooter’s phones. So far, Apple has not given any substantive assistance,” said Barr. “This situation perfectly illustrates why it is critical that the public be able to get access to digital evidence once it has obtained a court order based on probable cause. We call on Apple on other technology companies to help us find a solution so that we can better protect the lives of American people and prevent future attacks.”

In an email to The Verge, Apple rejects Barr’s statement that it hasn’t provided the proper assistance in the Pensacola naval base investigation. It said:

“Within hours of the FBI’s first request on December 6th, we produced a wide variety of information associated with the investigation. From December 7th through the 14th, we received six additional legal requests and in response provided information including iCloud backups, account information and transactional data for multiple accounts.

We responded to each request promptly, often within hours, sharing information with FBI offices in Jacksonville, Pensacola and New York. The queries resulted in many gigabytes of information that we turned over to investigators. In every instance, we responded with all of the information that we had.”

Apple notes that the FBI has asked for more assistance:

“The FBI only notified us on January 6th that they needed additional assistance – a month after the attack occurred. Only then did we learn about the existence of a second iPhone associated with the investigation and the FBI’s inability to access either iPhone. It was not until January 8th that we received a subpoena for information related to the second iPhone, which we responded to within hours.”

Apple also said their engineers were in communication with the FBI to “provide additional technical assistance,” but there was no mention of what that meant.

Apple and other Silicon Valley tech companies have routinely been ordered by the FBI to provide digital keys to unlock encrypted data of customers, and this has been met with fierce resistance from those companies.

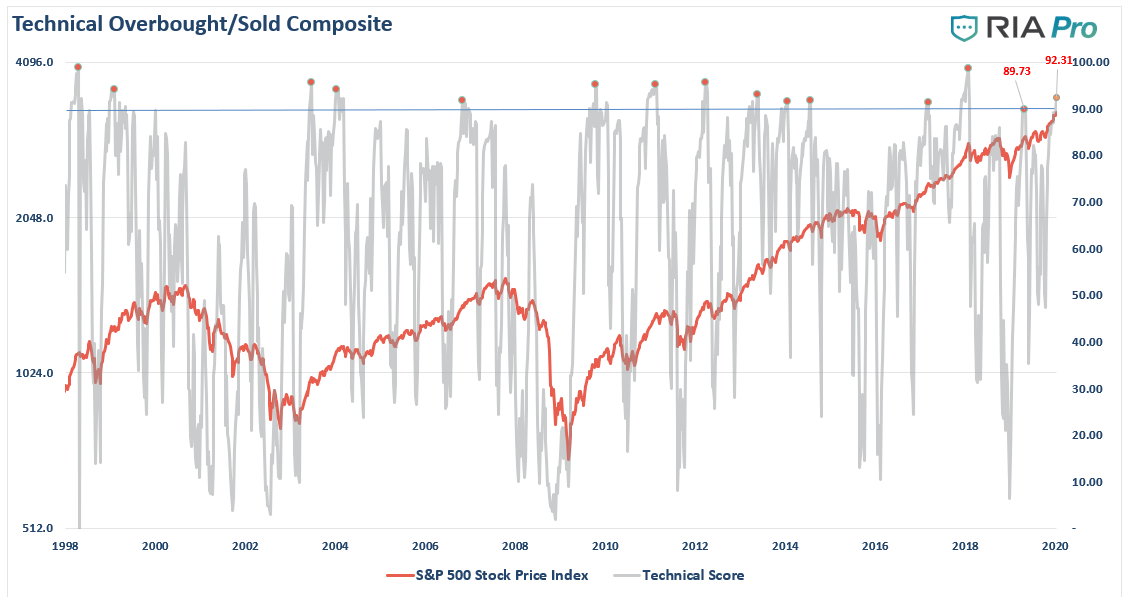

In thispast weekend’s newsletter, we discussed the exceedingly deviated price, and overbought conditions, not to mention valuations, as key reasons why we slightly reduced risk in our portfolios.

“On Friday, we began the orderly process of reducing exposure in our portfolios to take in profits, reduce portfolio risk, and raise cash levels.

In the Equity Portfolios, we reduced our weightings in some of our more extended holdings such as Apple (AAPL,) Microsoft (MSFT), United Healthcare (UNH), Johnson & Johnson (JNJ), and Micron (MU.)

In the ETF Sector Rotation Portfolio, we reduced our overweight positions in Technology (XLK), Healthcare (XLV), Mortgage Real Estate (REM), Communications (XLC), Discretionary (XLY) back to portfolio weightings for now.”

Not surprisingly, I received more than a few emails chastising me for “bailing on the bull market, which is clearly going higher.”

Such is hardly the case. We simply reduced our weighting in some of the companies which have had substantial gains over the last year. We remain primarily long-biased in our portfolios, but given the extreme technical overbought, and deviated conditions, it was prudent to raise some cash and protect our gains.

However, it wasn’t just the conditions we discussed which have us concerned about the markets in the short term. Investor positioning has also reached rather extreme levels. As Bob Farrell once wrote:

“When all experts agree, something else is bound to happen.”

Currently, with investors all extremely long equity exposure, the risk of a correction has become elevated.

Our composite “fear/greed” indicator, which is comprised of investor positioning, shows much the same as “bullish sentiment” has become rather extreme.

Every week, we provideRIAPRO subscribers (Try Free for 30-Days)with the latest updated technical composite score as well. This composite gauge combines extension, deviation, and momentum into a single weekly measure. Readings above 90 (Currently 92.31) are always associated with corrective actions in the market.

With all of these conditions aligned, the “probability” of a short-term correction has increased. Given that risk outweighs reward in the short-term, we decided it was prudent to reduce the numerator of that equation.

Why We Reduced Risk

It may seem irrational that we would reduce our risk exposure as the market continue to rise. Less exposure to equities, means less upside performance of the portfolio, or rather, “opportunity cost.” As I noted:

“While the markets could certainly see a push higher in the short-term from the Fed’s ongoing liquidity injections, the gains for 2020 could very well be front-loaded for investors. Taking profits and reducing risks now may lead to a short-term underperformance in portfolios, but you will likely appreciate the reduced volatility if, and when, the current optimism fades.”

However, the problem for the majority of investors is the inability to predict whether the next correction will be just a “correction” within an ongoing bull market advance or something materially worse. Unfortunately, by the time most investors figure it out – it is generally far too late to do anything meaningful about it.

By reducing risk now it provides us three benefits for the future.

Less equity risk, and higher cash levels, lowers the volatility of the portfolio which will allow us to navigate a correction process, and protect our investment capital.

It gives us capital to reinvest back into positions we currently own at better prices; or,

Buy new positions which have corrected in price.

While it is entirely true that “you can not time the market,” you can do some analysis and make deliberate changes to avoid problems.

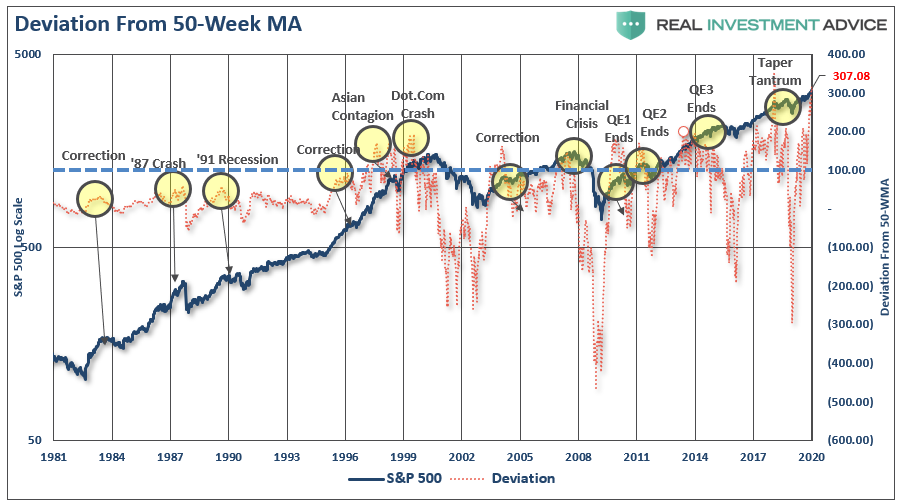

As shown below, price deviations from the 50-week moving average have been important markers for the sustainability of an advance historically. Prices can only deviate so far from their underlying moving average before a reversion eventually occurs.(You can’t have an “average” unless price trades above and below the average during a given time frame.)

Notice that price deviations became much more augmented heading into 2000 as electronic trading came online, and Wall Street turned the markets into a “casino” for Main Street.

At each major deviation of price from the 50-week moving average, there has either been a significant correction or something materially worse. Currently, the deviation from the 50-week moving average is the second-highest level in history, next to the 1999 “dot.com” mania.

How bad could it be?

Measuring The Mean Reversion

Given the current momentum of the market, combined with the Fed’s ongoing liquidity interventions, we only expect a correction of 5-10% to reset the overbought, optimistic, and deviated markets. Such a correction can be used to increase equity exposure and bring equity holdings back to target weights.

However, there is a risk of a larger mean reverting event, yet this is a possibility completely dismissed by the mainstream media under the guise of “this time is different.”

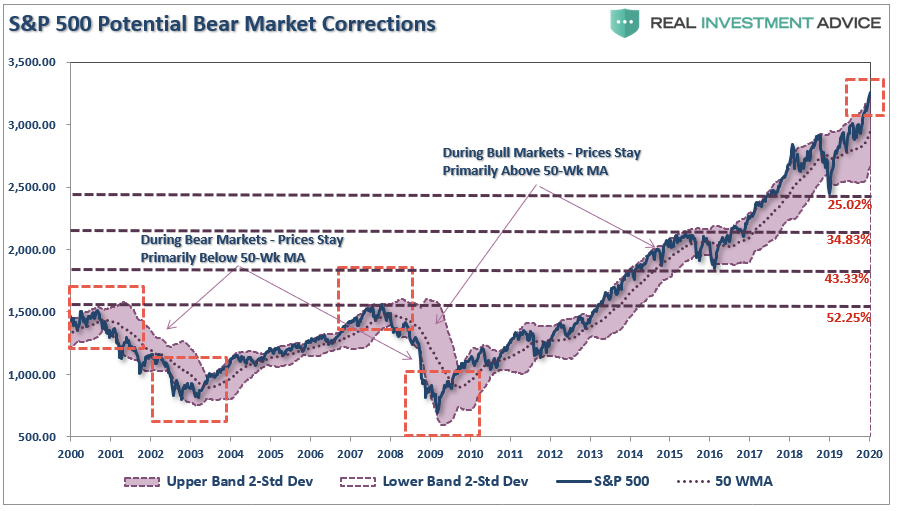

With the market trading more than 3-standard deviations above the 50-week moving average, historical reversions have tended to be more brutal. I have laid out support levels below.

At this juncture, a correction back to the 2018 lows would entail a 25% decline. However, if a “bear market” growls, the 2015-16 highs become the target which is 34% lower. The lows of 2016 would require a 43% draft, with the 2008 highs posting a 52% “crash.”

That can’t happen you say?

We had two 50% declines since the turn of the decade, and the next major market decline will be fueled by the massive levels of corporate debt, underfunded pensions, and evaporation of “stock buybacks,” which have accounted for almost 100% of net purchases since 2018.

Then there is also the other possibility as noted by technical analyst J. Brett Freeze, CFA:

“The Wave Principle suggests that the S&P 500 Index is completing a 60-year, five-wave motive structure. If this analysis is correct, it also suggests that a multi-year, three-wave corrective structure is immediately ahead. We do not make explicit price forecasts, but the Wave Principle proposes to us that, at a minimum, the lows of 2009 will be surpassed as the corrective structure completes.”

Anything is possible, and if he is right, such a decline will eclipse the 85% decline of the Dow following the 1929 peak when stocks last reached what seemed to be a “permanently high plateau.”

We Play The Probabities

The probability is that we will see the 5-10% correction which will be used to increase our exposure.

Just don’t dismiss the possibilities.

“You play the probabilities; but prepare for the possibilities.”

No one knows with certainty what the future holds which is why we must manage portfolio risk accordingly and be prepared to react when conditions change.

While I am often tagged as “bearish” due to my analysis of economic and fundamental data for “what it is” rather than “what I hope it to be,” I am actually neither bullish or bearish. I follow a very simple set of rules which are the core of my portfolio management philosophy which focus on capital preservation and long-term “risk-adjusted” returns.

As such, let me remind you of the 15-Risk Management Rules I have learned over the last 30-years:

Cut losers short and let winner’s run. (Be a scale-up buyer into strength.)

Set goals and be actionable.(Without specific goals, trades become arbitrary and increase overall portfolio risk.)

Emotionally driven decisions void the investment process.(Buy high/sell low)

Follow the trend.(80% of portfolio performance is determined by the long-term, monthly, trend. While a “rising tide lifts all boats,” the opposite is also true.)

Never let a “trading opportunity” turn into a long-term investment.(Refer to rule #1. All initial purchases are “trades,” until your investment thesis is proved correct.)

An investment discipline does not work if it is not followed.

“Losing money” is part of the investment process.(If you are not prepared to take losses when they occur, you should not be investing.)

The odds of success improve greatly when the fundamental analysis is confirmed by the technical price action. (This applies to both bull and bear markets)

Never, under any circumstances, add to a losing position.(As Paul Tudor Jones once quipped: “Only losers add to losers.”)

Market are either “bullish” or “bearish.” During a “bull market” be only long or neutral. During a “bear market”be only neutral or short.(Bull and Bear markets are determined by their long-term trend as shown in the chart below.)

When markets are trading at, or near, extremes do the opposite of the “herd.”

Do more of what works and less of what doesn’t.(Traditional rebalancing takes money from winners and adds it to losers. Rebalance by reducing losers and adding to winners.)

“Buy” and “Sell” signals are only useful if they are implemented.(Managing a portfolio without a “buy/sell” discipline is designed to fail.)

Strive to be a .700 “at bat” player.(No strategy works 100% of the time. However, being consistent, controlling errors, and capitalizing on opportunity is what wins games.)

Manage risk and volatility.(Controlling the variables that lead to investment mistakes is what generates returns as a byproduct.)

The current market advance both looks, and feels, like the last leg of a market “melt up” as we previously witnessed at the end of 1999. How long it can last is anyone’s guess. However, importantly, it should be remembered that all good things do come to an end. Sometimes, those endings can be verydisastrous to long-term investing objectives.

This is why focusing on “risk controls” in the short-term, and avoiding subsequent major draw-downs, the long-term returns tend to take care of themselves.

Everyone approaches money management differently. This is just the way we do it.

Boeing Mocked Lion Air “Idiots” For Requesting Extra Training For 737 MAX

Lawmakers have finally followed up last week’s bombshell release of internal Boeing communications with more extremely damning internal messages exchanged by employees. This time, the messages revealed that Boeing employees successfully persuaded Indonesia’s Lion Air to forego forcing their pilots to use a full flight simulator to train them on the 737 MAX 8.

According to Bloomberg, which published unredacted copies of the messages, offering full flight simulator training to Lion Air would undermine a key selling point of the 737 MAX 8: The fact that Boeing advertised the plane as needing no additional training for pilots and crew, apart from a basic computer-based course.

One Boeing employee wrote in June 2017 – a little over a year before the deadly Lion Air crash in October 2018 that helped inspire the universal grounding of the plane by regulators – that “friggin Lion Air was pushing for a “flight sim.”

However, the Boeing employee promised his co-workers that he would “unscrew” the situation.

“Now friggin Lion Air might need a sim to fly the MAX, and maybe because of their own stupidity. I’m scrambling trying to figure out how to unscrew this now! idiots,” one Boeing employee wrote in June 2017 text messages obtained by the company and released by the House Transportation and Infrastructure Committee.

In response to news about Lion Air’s request, another employee exclaimed that their sister airline, Malindo Air, was already flying the MAX without need simulators.

In response, a Boeing colleague replied: “WHAT THE F%$&!!!! But their sister airline is already flying it!” That was an apparent reference to Malindo Air, the Malaysian-based carrier that was the first to fly the Max commercially.

However, Boeing’s fixation on the bottom line ended up being a penny wise and a pound foolish. After all, in a report on the Oct. 29, 2018 accident, Indonesia’s National Transportation Safety Committee explicitly cited a failure by Boeing to tell pilots about MCAS, a flight control feature that has been implicated in MAX crashes in Indonesia and Ethiopia.

Apparently, it only took Boeing employees, including the company’s chief technical pilot, to convince Indonesia to forego the training.

The communications include a 2017 email from Boeing’s chief technical pilot on the 737 in which he crowed to colleagues: “Looks like my jedi mind trick worked again!” The email was sent two days after the earlier messages expressing alarm about Lion Air potentially demanding simulator training.

Attached was a forwarded email exchange in which the person warned an unnamed recipient against offering simulator training for Max pilots, pushing instead for the computer-based course that regulators had already approved for flight crews transitioning to the Max from earlier 737 models.

“I am concerned that if [redacted] chooses to require a Max simulator for its pilots beyond what all other regulators are requiring that it will be creating a difficult and unnecessary training burden for your airline, as well as potentially establish a precedent in your region for other Max customers,” the Boeing pilot wrote in the forwarded message.

While Lion Air was not identified in the redacted emails, the discussions are consistent with those Boeing held with Lion Air at the time, according to people familiar with the matter.

Once again, lawmakers have released damning communications from internal Boeing employees revealing a glaring negligence that appears to have been a cause, in part, of two deadly accidents that killed a combined 346 people.

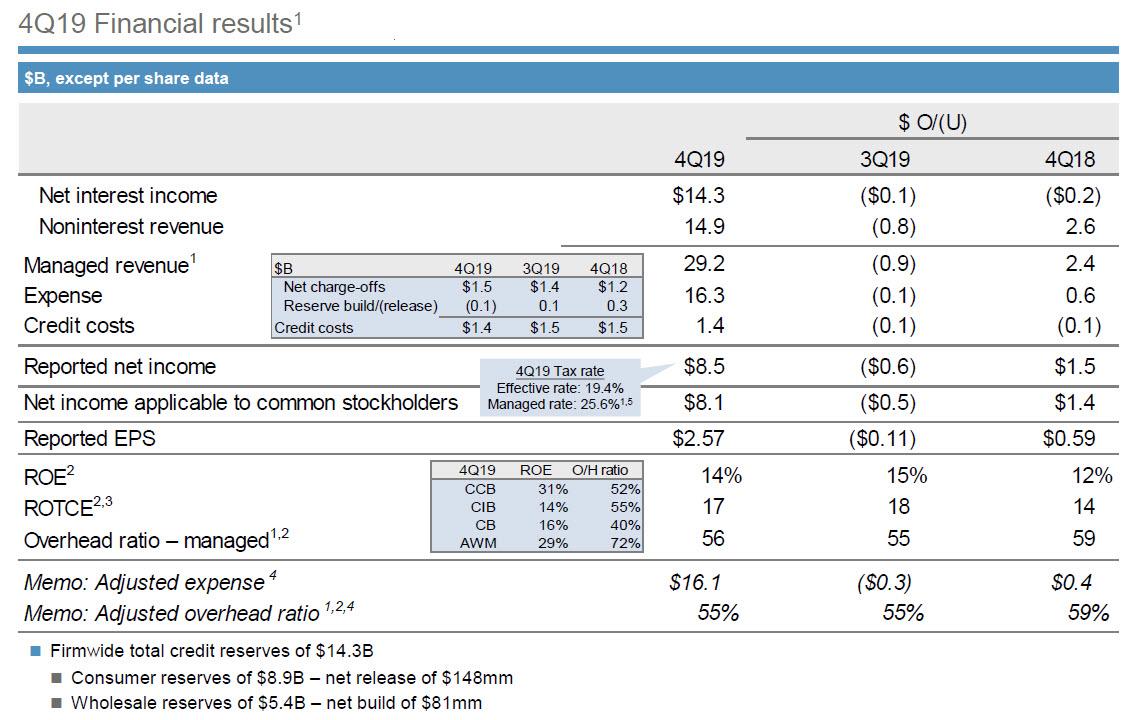

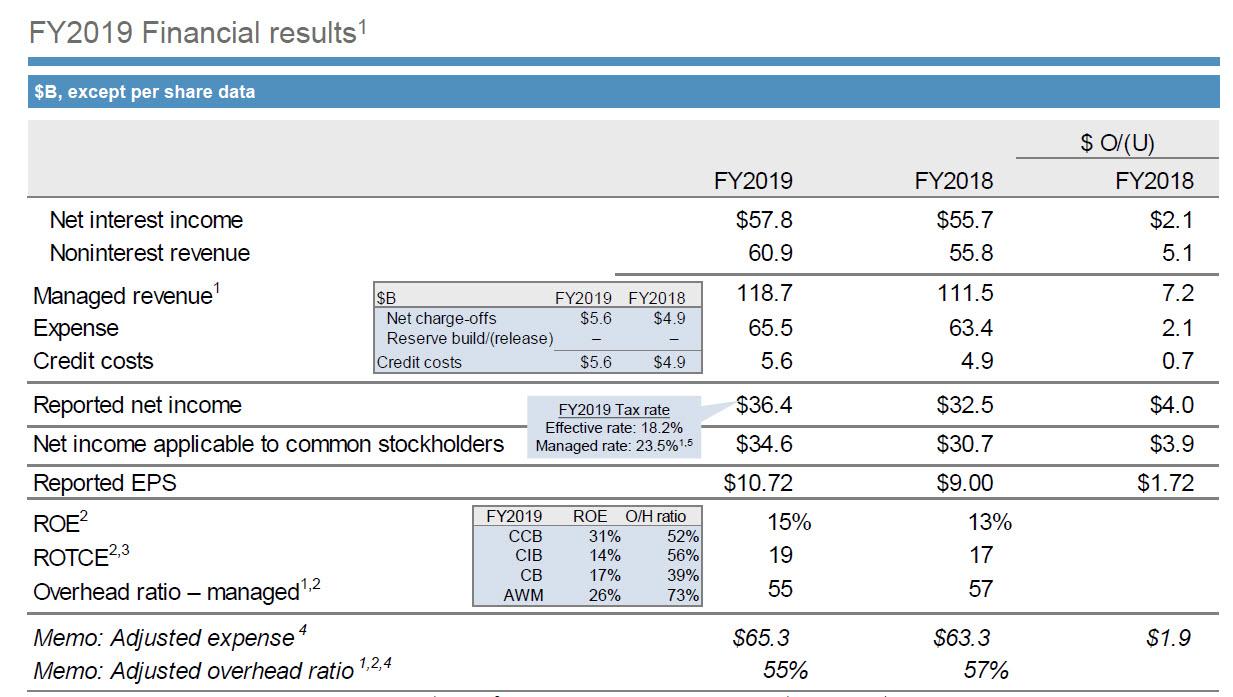

JPM Smashes Expectations: Reports Most Profitable Year Ever Thanks To Massive 86% FICC Surge

Q4 earnings season has officially begun, and once again it has done so on the right foot, with JPMorgan – which as a reminder is the bank that started QE4 in October by triggering the repo market crisis in September – reporting quarterly earnings that as has been traditionally the case for the past year, beat on the top and bottom line.

JPM reported Q4 revenue and EPS of $29.21BN and $2.57, both solidly beating expectations of $27.96BN and 2.30, respectively, and as one can expected, a solid improvement to the dismal Q4 2018 quarter when the bank as well as its peers buckled as the S&P briefly tumbled into a bear market.

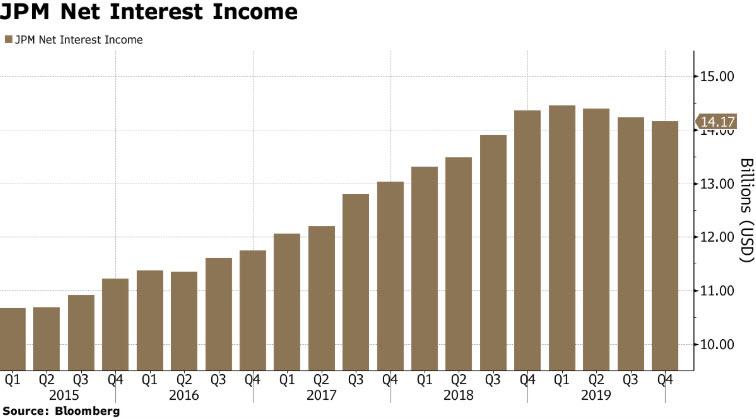

JPM’s revenue rose a total of 9%, up $2.4 billion, even though net interest income declined $0.2BN Y/Y, as non-interest revenue increased a whopping $2.6 billion in Q4.

Net interest margin was 2.38%, slightly above expectations, yet still down from the year earlier and previous quarter figures as the Federal Reserve’s rate cuts in 2019 brought down margins for all U.S. banks.

And while expenses also rose, they did so at a muted pace, with the company’s total expenses rising $0.6BN to $16.3BN. Thanks to a benign base effect, with the company’s earnings disappointing in Q4 2018, EPS was up a whopping 59 cents from $1.98 a year earlier.

For the full year, JPM said profit jumped 21% in the fourth quarter, pushing annual earnings to a record $36.4 billion.

The good news continued on the provisions front, where JPMorgan reported a provision for credit losses for Q4 that beat the average analyst estimate: at $1.43BN, the Q4 provision for credit losses was down -7.8% y/y and below the estimate of $1.53 billion.

Commenting on the results, CEO Jamie Dimon said that “while we face a continued high level of complex geopolitical issues, global growth stabilized, albeit at a lower level, and resolution of some trade issues helped support client and market activity towards the end of the year.” More importantly, the man who singlehandedly launched QE4 said that “the U.S. consumer continues to be in a strong position and we see the benefits of this across our consumer businesses.”

Looking ahead Dimon also said that he continues “to make large investments in technology, including AI, cloud, digital and payments, as well as other investments in innovation, talent, security and risk controls.”

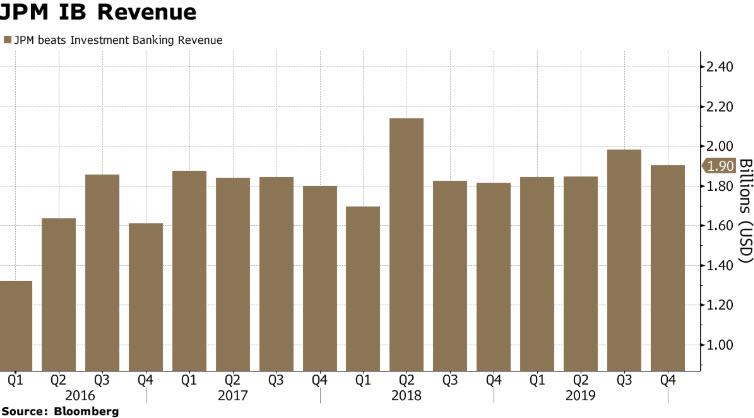

While there was little to note in the bank’s Consumer and Community Banking, and Commercial Banking revenues, of which the former posted a modest gain and the latter dipped Y/Y, the action once again was in JPM’s Corporate and Investment Bank, which surged higher in Q4, with total revenue surging 31% or $2.2BN Y/Y, representing virtually all of the Y/Y total revenue increase, to $9.47BN.

The breakdown between banking and markets was as follows:

IB revenue of $1.82B, up 6% YoY, and just below the $1.84BN expected, “reflecting higher debt and equity underwriting fees partially offset by lower advisory fees.” At the same time, the bank reported Treasury Services revenue of $1.2B, down 3% YoY, with deposit margin compression predominantly offset by higher balances and fee growth. Finally, lending revenue was $325mm, down 6%. Here is the breakdown of IB revenue by segment:

Advisory: $702 million (-3.44% YoY), vs exp. $618 million

DCM: $820 million (+11% YoY)

ECM: $382 million (+10% YoY)

The standout was JPM’s FICC within its Markets and Securities segment, with markets revenue up a whopping 56% to $5BN, thanks to a massive 86% surge in Fixed Income Markets, to $3.4B, “reflecting a favorable comparison against weaker performance in 4Q18 combined with strength in 4Q19.” Of course, a lot of this surge was thanks to last year’s dismal Q4 performance, but even compared to expectations JPM smashed results, with Wall Street expecting $2.44BN in FICC, $1BN below the $3.45 billion reported.

Separately, Equity Markets revenue was $1.51B, up 15%. and also beating estimates of $1.41BN, “reflecting higher revenue in Prime and Cash Equities.” JPM also reported Securities Services revenue of $1.1B, up 3% YoY, with organic growth partially offset by deposit margin compression. Meanwhile, “Credit Adjustments & Other” was a gain of $126mm reflecting lower funding spreads on derivatives.

On the cost side, FICC expenses of $5.2B were up 12% YoY, or $550MM higher, “driven by legal expense, volume- and revenue-related expense, as well as investments in the business.”

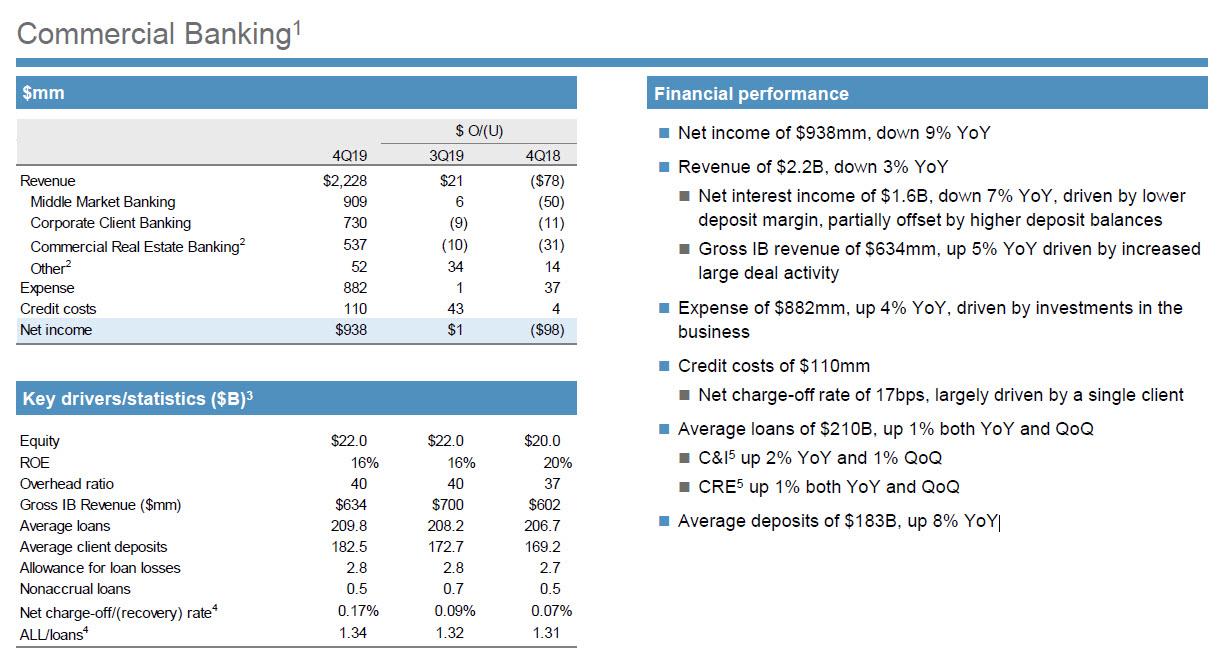

Offsetting the FICC euphoria, JPM’s Commercial Banking group had a quarter to forget, with Net income of $938mm, down 9% YoY on revenue of $2.2B, also down 3% YoY. Net interest income was $1.6B, down 7% YoY, driven by lower deposit margin, and partially offset by higher deposit balances. Meanwhile, gross IB revenue of $634mm, were up 5% YoY driven by increased large deal activity. Some more details:

Average loans of $210B, were up 1% both YoY and QoQ

C&I up 2% YoY and 1% QoQ

CRE up 1% both YoY and QoQ

Average deposits of $183B, up 8% YoY

Despite the revenue weakness, commercial banking expenses of $882mm, were up 4% YoY, “driven by investments in the

business.” And with credit costs hitting $110mm, it is notable that JPM announced that its net charge-off rate of 17bps, was “largely driven by a single client.” We expect questions in the conference call to address who this client was.

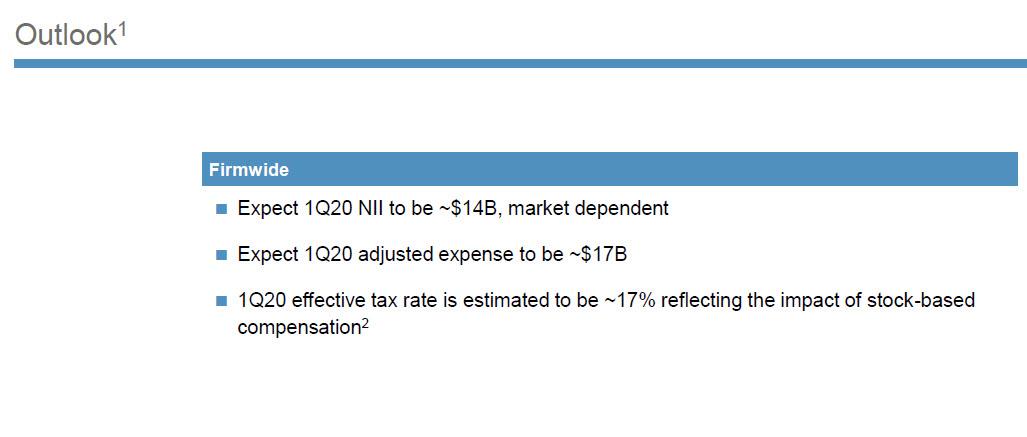

Finally, looking ahead, JPM said that it expects Q1 2020 Net Interest Income to be $14.00BN, just above the $13.95BN expected, so the bank hopes to see some commercial bank stabiliziation after the modest weakness in Q4.