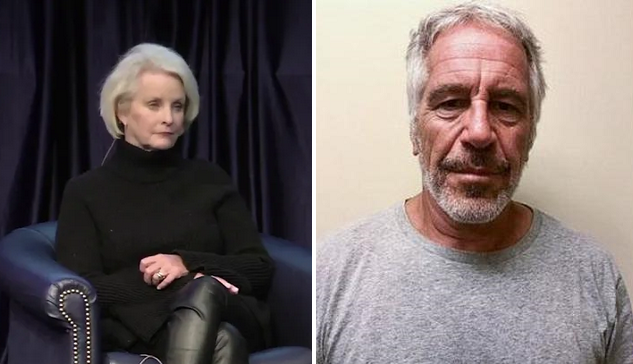

“We All Knew About Epstein” Admits Cindy McCain – Who Did Nothing About It

Sen. John McCain’s widow says “everyone” knew about Jeffrey Epstein’s sex trafficking ring, but were “afraid” to do anything about it.

“Epstein was hiding in plain sight,” said McCain, during an appearance at the State of the World 2020 conference in Florida, according to the Washington Examiner.

“We all knew about him. We all knew what he was doing, but we had no one that was — no legal aspect that would go after him. They were afraid of him. For whatever reason, they were afraid of him.”

McCain said a girl from her daughter’s high school was one of Epstein’s victims and that she hopes Epstein “is in hell.”

Epstein’s massive wealth and his connections to powerful politicians and celebrities allowed him to continue trafficking young women and girls long after many had exposed his devious interests.

Dr. Barbara Sampson, the New York City medical examiner, said Epstein died by suicide at a Manhattan federal detention facility last August. His death and the circumstances surrounding it have created controversy after the former medical examiner of New York, Dr. Michael Baden, told 60 Minutes that he believes Epstein was murdered. –Washington Examiner

While most of the focus in Congress is on the impeachment, Congress has still found time to advance some votes relevant to the potential war with Iran, and are set for some such votes next week.

Two votes are planned in the House, and expected on Thursday. One is from Rep. Ro Khanna (D-CA) prohibiting any funding for a war in Iran without Congressional authorization. The second will attempt to reveal the 2002 Authorization for the Use of Military Force (AUMF).

Image via BBC

The 2002 AUMF was meant to authorize the 2003 invasion and occupation of Iraq. With the Hussein government long gone, many have questioned the relevance of the AUMF, though the administration has at times claimed it authorizes other wars, including military action against ISIS in “Syria or elsewhere.”

The votes are seen not only as a rebuke of Trump’s unilateral action against Iran but a win for House progressives, who have spent years seeking limits on presidential authority. The Trump administration has claimed the 2002 AUMF legally justifies military action against the Islamic State group “in Syria or elsewhere.” — Defense News

While the Iraq AUMF isn’t directly related to a possible Iran War, repealing it would go a long way toward Congress reasserting its war-making powers, and emphasizing that the authorizations aren’t open-ended after the intended war is long over, allowing them to be reinterpreted indefinitely for other operations.

The Senate is not expected to take up any of the Iran War votes this week, though the Senate Foreign Relations Committee will be given a briefing from the State Department on the matter. The State Department had previously canceled this briefing weeks ago.

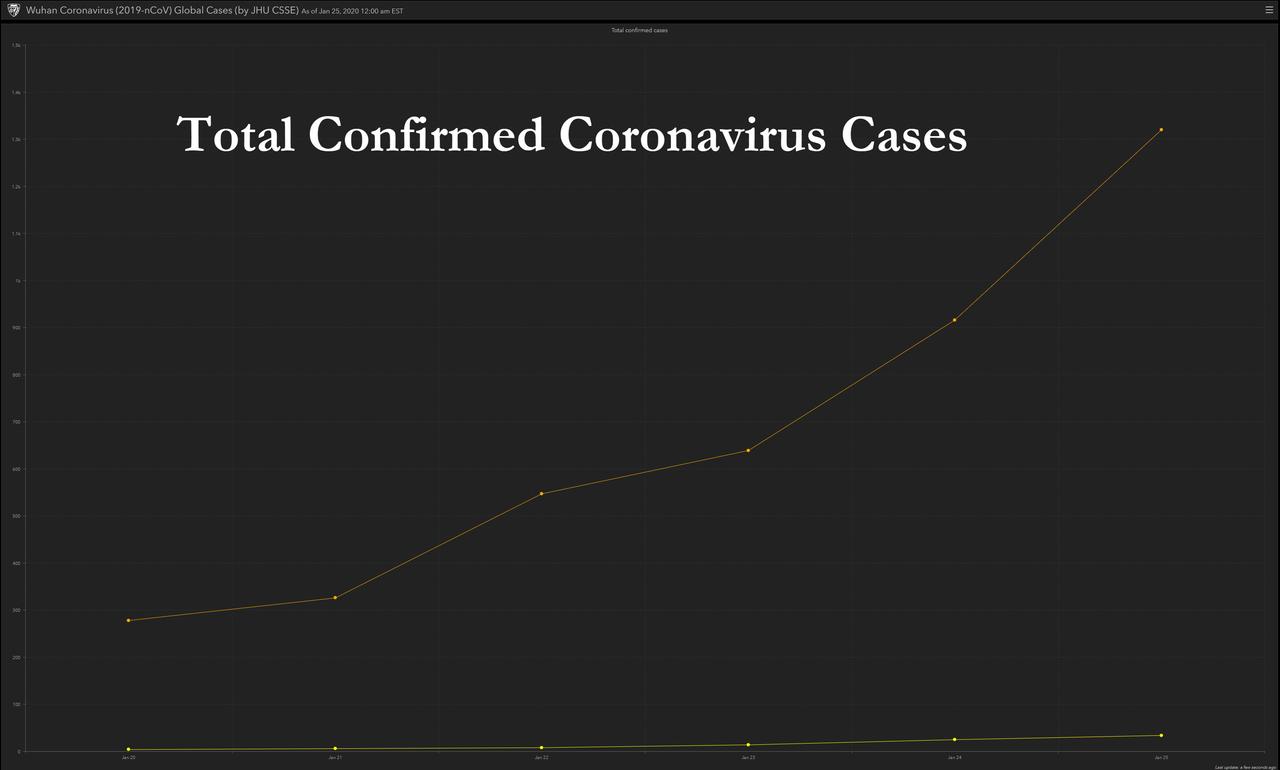

“Thermonuclear, Pandemic-Level Bad” – Harvard Epidemiologist Warns Viral Outbreak Might Get A Lot Worse

As we’ve stepped up our coverage of the nCoV coronavirus outbreak over the past week, some on Twitter have published what we feel are exaggerated criticisms accusing us of fearmongering.

While we understand that the information we’ve shared can be distressing, we’d like to take a moment to remind readers that all of the information and research we have cited is legitimate, having originally been conducted by credible epidemiologists, like the UK’s Jonathan Read. The fact is, the Chinese government hasn’t been nearly as “transparent” as it promised, and it seems like the more we learn about the true scope of this outbreak, the more concerned we become.

The reality is that – as the Architect told Neo in “The Matrix: Reloaded” – denial is the most predictable of human responses. And while the world’s public health authorities certainly still have time to get their arms around this outbreak before it becomes a massive, global pandemic with deadly consequences, the WHO’s dithering response the other day (asserting that they don’t yet have enough evidence of human-to-human secondary transmission to declare a global health emergency) certainly doesn’t inspire confidence.

Now that we have that out of the way – let’s move on to Dr. Eric Feigl-Ding, a public health scientist on the faculty at Harvard.

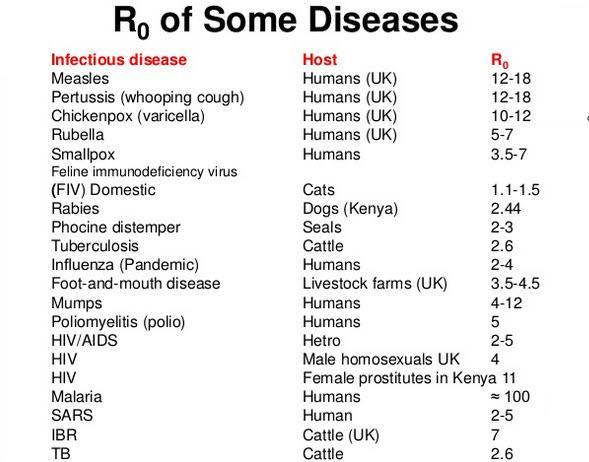

A few days ago, Dr. Feigl-Ding tweeted that he was “really, deeply worried about this new coronavirus outbreak” because the virus seemed to have an”upward infection trajectory curve much steeper than SARS.”

I’ll be honest – as an epidemiologist, I’m really deeply worried about this new coronavirus outbreak. 1) the virus has an upward infection trajectory curve much steeper than SARS. 2) it can be transmitted person to person before symptoms appear — I.e. it is silently contagious! pic.twitter.com/5Kjo6DkbQj

On Friday, the doctor, a well-respected epidemiologist who has worked as an advisor to the World Health Organization, tried his hand at a few projections based on an infection rate much higher than the RO (r-naught) rating of 1.4-2.5 recently estimated by the WHO. As we explained last night, when determining the infectious potential of a virus, arguably the most important variable is RO. This represents the average number of secondary cases resulting from every new infection in an entirely susceptible population.

Of course, government interventions and more vigilant hygiene practices once the public is aware of the threat will help lower the virus’s r-naught variable. But remember, nCoV (the WHO’s name for the virus) has already been quietly spreading among the people of Wuhan for weeks. And as Dr. Feigl-Ding explains, early evidence would suggest that nCoV is contagious before symptoms appear.

Last night, we published the findings of a team of UK epidemological researchers led by Jonathan Read. Read published a paper with four colleagues that estimates transmission parameters for the Wuhan coronavirus and calculates that the true R0 of 2019-nCoV is between 3.6-4.0 or roughly the same as SARS, and reaches a conclusion about spread of the coronavirus epidemic that is frankly terrifying. With an r-naught of 3.8, the virus could eventually cause hundreds of thousands of deaths in China alone.

In fact, it’s not simply terrifying: With an r-naught of 3.8, this virus could be “thermonuclear, pandemic level bad.”

HOLY MOTHER OF GOD – the new coronavirus is a 3.8!!! How bad is that reproductive R0 value? It is thermonuclear pandemic level bad – never seen an actual virality coefficient outside of Twitter in my entire career. I’m not exaggerating… #WuhanCoronovirus#CoronavirusOutbreakpic.twitter.com/6mmxIHL9Ue

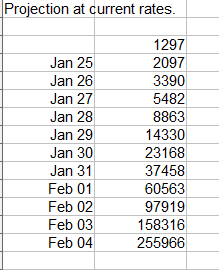

As Dr. Feigl-Ding goes on to explain, using Read’s findings as a jumping-off point, the 4,000 number being kicked around by some scientists as the true number of viral cases in Wuhan might be much too low. By early Feb., the doctor warns that nearly a quarter of a million Chinese could be infected.

2/ “We estimate the basic reproduction number of the infection (R_0) to be 3.8 (95% confidence interval, 3.6-4.0), indicating that 72-75% of transmissions must be prevented by control measures for infections to stop increasing…

3/ … We estimate that only 5.1% (95%CI, 4.8-5.5) of infections in Wuhan are identified, and by 21 January a total of 11,341 people (prediction interval, 9,217-14,245) had been infected in Wuhan since the start of the year. Should the epidemic continue unabated in Wuhan….

4/ we predict the epidemic in Wuhan will be substantially larger by 4 February (191,529 infections; prediction interval, 132,751-273,649), infection will be established in other Chinese cities, and importations to other countries will be more frequent. Our model suggests that..

5/ travel restrictions from and to Wuhan city are unlikely to be effective in halting transmission across China; with a 99% effective reduction in travel, the size of the epidemic outside of Wuhan may only be reduced by 24.9% on 4 February. Our findings are…

To be sure, these findings should be taken with a grain of salt. They are based on a set of assumptions that could change as scientists learn more about the virus. But as things stand, it appears that nCoV has a higher infectious potential than other coronaviruses, meaning it will be more difficult to contain. And the possibility of an unchecked pandemic on par with the 1918 Spanish flu shouldn’t be ruled out yet.

6/ …critically dependent on the assumptions underpinning our model, and the timing and reporting of confirmed cases, and there is considerable uncertainty associated with the outbreak at this early stage. With these caveats in mind, our work suggests that…

7/ a basic reproductive number for this 2019-nCoV outbreak is higher compared to other emergent coronaviruses, suggesting that containment or control of this pathogen may be substantially more difficult.”!!!! #wuhanvirus#CoronavirusOutbreak#ChinaCoronaVirus …

9/ …cannot be stopped by containment alone. A 99% quarantine lockdown containment of Wuhan will not even reduce the epidemic’s spread by even 1/3rd in the next 2 weeks. Thus, I really hate to be the epidemiologist who has to admit this, but we are potentially faced with…

10\ … possibly an unchecked pandemic that the world has not seen since the 1918 Spanish Influenza. Let’s hope it doesn’t reach that level but we now live in the modern world 🌎 with faster ✈️+ 🚞 than 1918. @WHO and @CDCgov needs to declare public health emergency ASAP!

12/ What is the typical R0 attack rate for the seasonal flu in most years? It’s around an R0=1.28. The 2009 flu pandemic? R0=1.48. The 1918 Spanish Flu? 1.80. This new #WuhanCoronavirus reproductive value again? R0=3.8. (Flu reference: https://t.co/ldAWBlFkvA)

13/ …and it gets even worse, the Lancet now reports that the coronavirus is contagious even when *no symptoms*: specifically: “crucial to isolate patients… quarantine contacts as early as possible because asymptomatic infection appears possible”! https://t.co/FZr3Es1VwZ

Even if we assume a much lower r-naught, like, say, 2.8, which is just above the upper band of the WHO’s estimates, the results could still be “pretty bad”.

14/ Let’s pretend the 3.8 estimate is too high (there’s unpublished estimates of 2.5). even if this virus’s R0=2.5, that’s still 2x higher than seasonal flu’s 1.28 (ref above), and higher than 1918 Spanish Flu pandemic of 1.80 that killed millions. So 2.8 is still super bad folks

15) My response to some people who think I’m trying to stoke fear… I’m a Harvard trained scientist with a doctorate in epidemiology (and the youngest dual doctoral grad from Harvard SPH). Here are my response: https://t.co/tdxg3gJQ72https://t.co/AgL4idz8Yc

Based on the above thread, the situation might seem especially dire. But as Dr. Feigl-Ding explains later, actions like China’s mass quarantine of 46 million and other public-health precautions should help to contain the virus and reduce its ability to spread.

Small note: While there were reports of SARS having 0.49 after containment started, a WHO cited experts who said SARS had initial R0 of 2.9 then 2.0-3.5, which which fell to 0.4 after quarantine. But SARS is more symptomatic than this Wuhan virus. To be updated. pic.twitter.com/wNXf3rgcqg

Now, Feigl-Ding’s critics have pointed out that this is only one estimate, and that Read and his team have already revised down their r-naught calculation.

“there is considerable uncertainty associated with the outbreak at this early stage.” & yet you tweeted: “HOLY MOTHER OF GOD”. A Public health scientist should KNOW better than to be an alarmist. https://t.co/2Z5meAFnSx@stgoldst

The doctor repeatedly said as much during the thread, but we suppose there’s something about people tweeting in all-caps that some find extremely off-putting.

Some folks think I’m trying to incite fear. I’m not trying—I’m a scientist. This #coronavirus#WuhanCoronovirus is serious. Over 50 million people are quarantined + case counts will go up much more. Predict @WHO will declare emergency. Let’s hope for the best, prepared for worst. https://t.co/H3UcR9eAjs

And of course this isn’t 1918 – medical technology is far more advanced. In the event of a mass infection, a vaccine could be found to save the day. But that doesn’t mean we should simply dismiss the more dire projections out of hand. This virus could still leave thousands dead before it peters out.

More than 129,000 Illinois public pensioners will see expected payouts of $1 million or more during retirement.

Illinois is home to a small, powerful and protected class of wealth.

Their profits are immense. They bear little to no risk. And the state’s social safety net has been gutted to pay for their privileges, which are closely guarded by politicians.

Sound familiar?

These are Illinois’ pension millionaires.

Among the state’s 12.7 million residents, they constitute the 1%.

More than 129,000 Illinois public retirees will collect estimated payouts of more than $1 million each over the course of their retirements, according to new analysis from the Illinois Policy Institute.

No public-sector worker should be personally shamed for getting a great deal. Those who choose a life of public service deserve honor and praise.

At the same time, it’s crucial that Illinoisans understand these retirement benefits and call for reform. They have resulted in cuts to core services and constant calls for tax hikes across the state for more than two decades. They’re also pushing the pension funds toward insolvency.

Extreme payouts and early retirements are the norm across Illinois’ five state-run retirement systems:

More than 22,000 retirees in the State Universities Retirement System (43%) will receive an expected lifetime payout of more than $1 million, with 42% retiring before their 60th birthday.

More than 31,000 retirees in the State Employees’ Retirement System (51%) will receive an expected lifetime payout of more than $1 million, with half retiring before age 60.

Nearly 75,000 retirees in the Teachers’ Retirement System (68%) will receive an expected lifetime payout of more than $1 million, with more than half retiring before age 60.

The remaining pension millionaires at the state level are spread across the Judges’ Retirement System (nearly 900, or 94%) and the General Assembly Retirement System (more than 200, or 67%).

Meanwhile, the average 401(k) balance nationwide for people aged 60 to 69 is $195,500, according to CNBC.

These numbers can be difficult to believe. So they’re often spun. There are four common “buts” used to justify the status quo:

1) But these benefits attract top talent

In fact, these benefits have made important fields like teaching much less attractive in Illinois. That’s because in order to pay for the extreme benefits promised in the past, new teachers are enrolled in an unfair “Tier 2” retirement plan that is so lousy it will likely result in a lawsuit when the first Tier 2 worker vests on Jan. 1, 2021.

2) But these workers don’t get Social Security

In fact, almost all state employees in SERS are eligible for Social Security benefits on top of their pensions, which average $1.7 million for career workers.

For other public retirees in Illinois, trading million-dollar payouts for a Social Security check would be a serious downgrade. The average Social Security benefit for 2019 is $17,532 per year. And the earliest anyone can qualify for Social Security is age 62, with the full retirement age pegged at 67 for anyone born after 1960.

3) But workers paid into the system

The average state worker or teacher in Illinois retires before age 60, takes home a lifetime pension benefit of more than $1 million and contributes less than 10% of that amount to the system – the rest is covered by taxpayers.

4) But politicians underfunded the system

Illinois pensions were underfunded because they were overpromised. Like a teenage barback trying to front a monthly payment on a Lamborghini, state politicians have kicked the can, borrowed and lied to keep up appearances. Illinois state and local governments now spend the most in the nation – about double the national average – on pensions as a share of their budgets. Consider that the state spends about one-third less today, adjusted for inflation, than it did in the year 2000 on core services including child protection, state police and college money for poor students. During that time, pension spending increased 501%.

Paying more is not an option.

Backing reforms for a fair pension system should be the No. 1 priority for Illinois state lawmakers. And other states can show them how.

A pension constitutional amendment in Illinois that matches states such as Hawaii and Michigan would allow for changes to retirement ages, capping maximum pensionable salaries, and doing away with guaranteed permanent benefit increases in favor of a true cost-of-living adjustment pegged to inflation. All of this can be done without cutting a dime from the checks of current retirees. These changes to “future” benefits have been enacted in Arizona, where they had support from union leaders who realized pensions were in peril.

If Illinoisans work together, commonsense pension reform can ensure state government works for everyone.

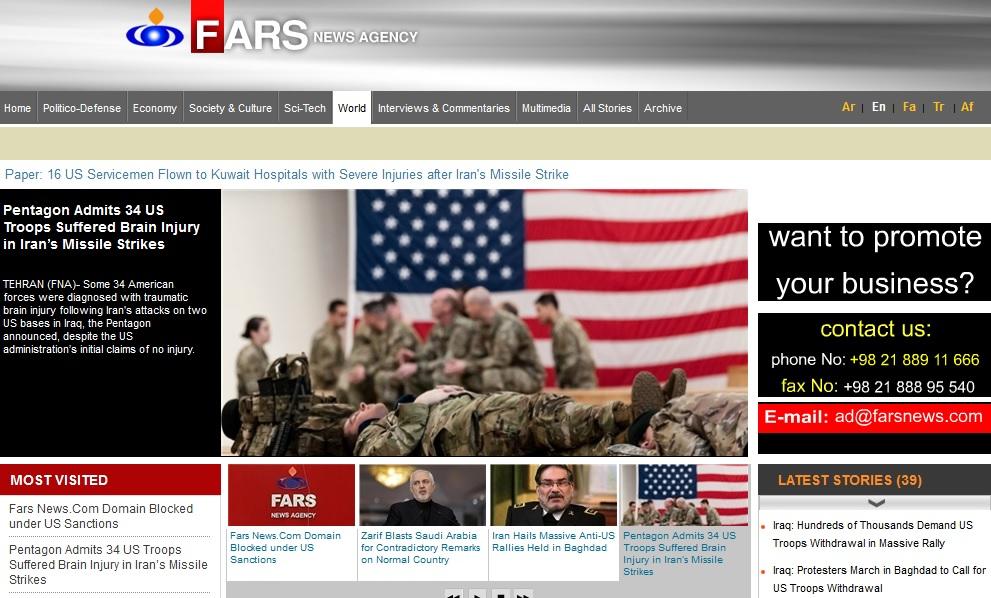

Iran’s Fars News Knocked Off Web By US Treasury Order

Iran’s well-known state media outlet Fars News Agency says US sanctions have knocked it off the internet. As of Friday and into early Saturday the en.farsnews.com domain remained inaccessible while the outlet says it quickly alternately established English content on https://en.farsnews.ir/, which remains live.

Iran says the US Treasury Department shut down international access to its English news site due to new regulations related to US sanctions.

It’s not the first time state-linked Iranian media outlets have had access to Western audiences blocked, with PressTV complaining in recent months about being blocked on YouTube and other popular social media sites; however it’s less common for their domains to be blocked.

Fars outlet issued a Farsi language tweet Friday which reads according to a translation:

“From an hour ago, audience access to the Fars News Agency site has encountered a problem due to being placed on America’s sanctions list, and the technical part of [this] News Agency is working to create access for the audience on the farsnews.ir domain.”

It further said administrators of its state-controlled site were notified Friday that it was being shut down after the US Treasury Department ordered the drastic action it due to sanctions violations.

Fars has since erected a separate domain for its now blocked English language site.

The news agency said that it had received an email from the server company, which explicitly said that the blockage is due to an order by the Treasury’s Office of Foreign Assets Control (OFAC) and its inclusion in the list of Specially Designated Nationals (SDN).

The agency attached to its post a screenshot of its website with the message “www.farsnews.com’s server IP address could not be found.”

In the wake of the Jan.8 Iranian ballistic missile attack on Ayn al-Asad airbase in Iraq, Iranian media outlets were slammed by western analysts for “spreading disinformation” — which initially included claims of multiple American troop deaths and a totally obliterated base.

But in reality both sides could be blamed for sowing war propaganda and disinformation, given the US side initially said “no casualties” — later revised to 11 traumatic brain injuries, and days ago dramatically updated to 34 total head injuries.

Amidst the annual spectacle of the World Economic Forum in Davos, the Bank for International Settlements this week announced that multiple central banks have created a group that will ‘assess potential cases for central bank digital currencies‘.

The Bank of Canada, the Bank of England, the Bank of Japan, the European Central Bank, the Sveriges Riksbank and the Swiss National Bank, together with the Bank for International Settlements (BIS), have created a group to share experiences as they assess the potential cases for central bank digital currency (CBDC) in their home jurisdictions.

The group will assess CBDC use cases; economic, functional and technical design choices, including cross-border interoperability; and the sharing of knowledge on emerging technologies. It will closely coordinate with the relevant institutions and forums – in particular, the Financial Stability Board and the Committee on Payments and Market Infrastructures (CPMI).

The group will be co-chaired by Benoît Cœuré, Head of the BIS Innovation Hub, and Jon Cunliffe, Deputy Governor of the Bank of England and Chair of the CPMI. It will include senior representatives of the participating institutions.

As with every other recent development in regards to CBDC’s, the BIS stand at the heart of the issue. The new central bank grouping comes just over six months after the BIS first established an Innovation Hub for central banks (also known as Innovation BIS 2025) with the objective being to ‘foster international collaboration on innovative financial technology within the central banking community‘.

With the agenda to introduce central bank digital currency gathering further momentum, now would be as good a time as any to ask what the global banking elite are seeking to achieve over the short to medium term.

In 2019 I published around a dozen articles on the subject of digital currency, examining the latest speeches from central bankers and the actions they were taking to formulate the foundations for a cashless society. The Innovation BIS 2025 project is a important pillar to the aspirations of the financial elite. By 2025 they are targeting the completion of reformed payment systems in the UK, the U.S and beyond, systems that will possess the capability to interface directly with Fintech firms that specialise in blockchain and distributed ledger technology (DLT). Both blockchain and DLT would be essential for the roll out of a fully fledged CBDC network.

Like cash, a CBDC could and would be available 24/7, 365 days a year. At first glance, not much changes for someone, say, stopping off at the supermarket on the way home from work. He or she would no longer have the option of paying cash. All purchases would be electronic.

To avoid confusion, there are two variants of CBDC that are regularly discussed by central bank officials. The first is a wholesale CBDC, which would be used to facilitate payments exclusively between financial sector firms. The second option, a retail CBDC, would be for use by the general public.

To quote Carstens from the same speech he made in Ireland:

A CBDC would allow ordinary people and businesses to make payments electronically using money issued by the central bank. Or they could deposit money directly in the central bank, and use debit cards issued by the central bank itself.

This would be a significant departure from the traditional model of commercial banks digitising the money held in people’s bank accounts. To way up the likelihood of this scenario, let’s examine what the International Monetary Fund have been saying.

If digital currencies are sufficiently similar to commercial bank deposits— then why hold a bank account at all?

What if, instead, central banks entered a partnership with the private sector—banks and other financial institutions—and said: you interface with the customer, you store their wealth, you offer interest, advice, loans. But when it comes time to transact, we take over.

Banks and other financial firms, including startups, could manage the digital currency. Much like banks which currently distribute cash.

In this reality, central banks would, according to Lagarde, ‘retain a sure footing in payments‘. By extension, they would also retain autonomy over an all digital financial system.

The IMF expanded on Lagarde’s speech in December 2019 with the publication of an article called, ‘Central Bank Digital Currencies: 4 Questions and Answers‘. Co-written by Tobias Adrian, the Financial Counsellor and Director of the IMF’s Monetary and Capital Markets Department, it asserts that the IMF is now gradually helping countries ‘develop policies‘ as they ‘consider CBDC options and seek advice.’

One of those options is a public-private partnership, which IMF staffed have termed as a ‘synthetic CBDC‘. In the summer of 2019 Mark Carney first raised the prospect of a ‘Synthetic Hegemonic Currency‘ that could be provided by the public sector ‘through a network of central bank digital currencies‘. This would ultimately be at the expense of the world reserve status of the dollar.

The synthetic CBDC model as envisioned by the IMF would see private sector firms like JP Morgan and Barclays issuing digital coins to the general population. Banks would continue ‘innovating and interfacing with customers‘, whilst central banks would ‘provide trust to the system by requiring that coins be fully backed with central bank reserves and by supervising the coin issuers.’ This is worth keeping in mind because as the article confirms, such a set up would ‘preserve the comparative advantages of each participant.’ In other words, global financial institutions and the central banks operating beneath them would work hand in hand with Fintech developers rather than be in competition, creating a state / private lock in that every citizen would be bound by due to the abolition of cash.

The coins the IMF refer to are known as ‘Stablecoins‘, which central bankers routinely discussed throughout 2019. Stablecoins are regarded as a form of crypocurrency, and differ from the likes of Bitcoin in that issuers of the coins would back them using a basket of established fiat currencies. The theory is that this would give the coins stability in terms of their valuation. Stablecoins would be all digital with blockchain and distributed ledger technology central to their make up, meaning payments would be instantaneous across borders.

A few days after the IMF’s article, Lael Brainard of the Federal Reserve addressed an event held in Frankfurt, Germany in honour of Benoit Coeure’s departure from the European Central Bank (the same Benoit Coeure who has now begun his new role heading up the Innovation Hub at the BIS).

This was an important speech because between the lines Brainard set the scene for how central banks could take advantage of the rise in stablecoins. She talked of how the emergence of crypto technology has raised ‘important questions for central banks‘, and that the ‘prospect of global stablecoin payment systems has intensified the interest in central bank digital currencies.’

Facebook’s Libra project is cited by central banks as the bellwether of stablecoins. Whilst Libra has yet to launch, implementation would give it the title of a global stablecoin used throughout multiple different jurisdictions. For Brainard and her colleagues, this brings into question the level of regulation and safeguards that they deem necessary for stablecoins to be rolled out world wide. Without them, Brainard warned, ‘stablecoin networks at global scale may put consumers at risk‘ as well as the financial system as a whole.

There are also questions related to the implications of a widely used stablecoin for financial stability. If not managed effectively, liquidity, credit, market, or operational risks, alone or in combination, could trigger a loss of confidence and run-like behaviour.

Chief amongst the risks raised are money laundering and the financing of terrorism, and it is here where the distinction between a permissioned and permissionless stablecoin network becomes apparent. Central bankers openly advocate for a permissioned network where access must be granted by participants. A permissionless network, according to Brainard, ‘may be more vulnerable to money laundering and terrorist financing.’

One solution mooted by Brainard would be for coordinated regulatory action rather than individual nations determining how stablecoins would be allowed to function. In Brainard’s words, ‘any global payments network should be expected to meet a high threshold of legal and regulatory safeguards before launching operations.’

Elites have been fashioning for decades the narrative that global problems are too large and complex in scale to be remedied at the national level. Their argument has been that more centralisation of powers and the diminishment of the nation state is required to bring about order out of chaos. The seeming regulatory vacuum surrounding stablecoins has given central banks the platform to gradually begin cementing central bank digital currency as a safer alternative, primarily because they would be a ‘direct liability of the central bank.’

As the debate continues around digital currency, the Federal Reserve are quietly progressing with plans to introduce a new payments system called ‘FedNow‘. This will be a platform where users would be able to ‘send and receive payments immediately and securely 24 hours a day, 365 days a year.’

The biggest selling point of digital currency is the convenience factor of national and cross border payments being settled and available without delay. I suspect this is where the banking elite want people to focus their attention, as opposed to how a digital currency network that incorporates central banks and selected private sector players would result in the end of tangible assets.

If you believe what central bankers are saying, then the concept of CBDC’s remain at the investigative stage. Sweden continues to lead the way with the development of an e-krona. The Riksbank has now procured a technology supplier to begin an e-krona test pilot, with the leading objective being to ‘broaden the bank’s understanding of the technological possibilities for the e-krona.’

With the Riksbank being part of the new central bank group working through the BIS, and the IMF admitting that they are now assisting countries in devising policies around digital currency, we are witnessing just how closely they are all collaborating with one another.

One question is whether stablecoins will be used as a stalking horse for CBDC’s, taking them beyond a mere concept. Financial instability has always been an opportunity for the global elite. Stablecoins without sufficient regulatory oversight create an opening for central banks to step in further down the line.

Something to ponder also is how faith could be lost with future stablecoin providers. BIS General Manager Agustin Carstens has said before that trust can be compromised in four particular ways – currency devaluations, hyperinflation, wide-scale payment system disruptions and bank defaults. Naturally, Carstens has positioned central banks as the institutions that can rectify such conflict, even though it has been proven that throughout history it is their policies that have created economic instability leading to collapse.

In relation to what Carstens said about compromising trust, three months prior to the EU referendum Bank of England official Ben Broadbent made a very telling comment in a speech appropriately titled, ‘Central banks and digital currencies‘, about the necessity for currency degradation before the public demand a solution to the traditional monetary model.

Degrade a currency sufficiently, via hyperinflation and collapse of the banking system, and people will eventually look for alternatives. But that’s generally the sort of thing that has to happen. Almost always, these currency substitutions occur only once the existing currency has become deeply compromised. Even then, the thing people naturally reach for is an existing, trusted currency – often the US dollar – rather than some entirely new unit of account.

When currency substitution has occurred naturally it’s almost always done so only after the incumbent currency has been debauched by hyperinflation.

I have warned extensively over the past couple of years of the risk of a global trade conflict triggering higher inflation, the devaluation of currencies such as sterling and the raising of interest rates. It is what would occur afterwards that is of more concern. Would people look to central banks as the saviours in a crisis scenario, giving them licence to digitise all assets through a network of CBDC’s?

As ever, central banks will require sustained geopolitical conflict to shape the future design of the financial system. They are already headlong in devising that very system through the reformation of global payment systems. But with distractions in the shape Brexit and Donald Trump’s presidency still dominating the discourse, potentially up to 2025, how many are even aware of what the central banks are planning?

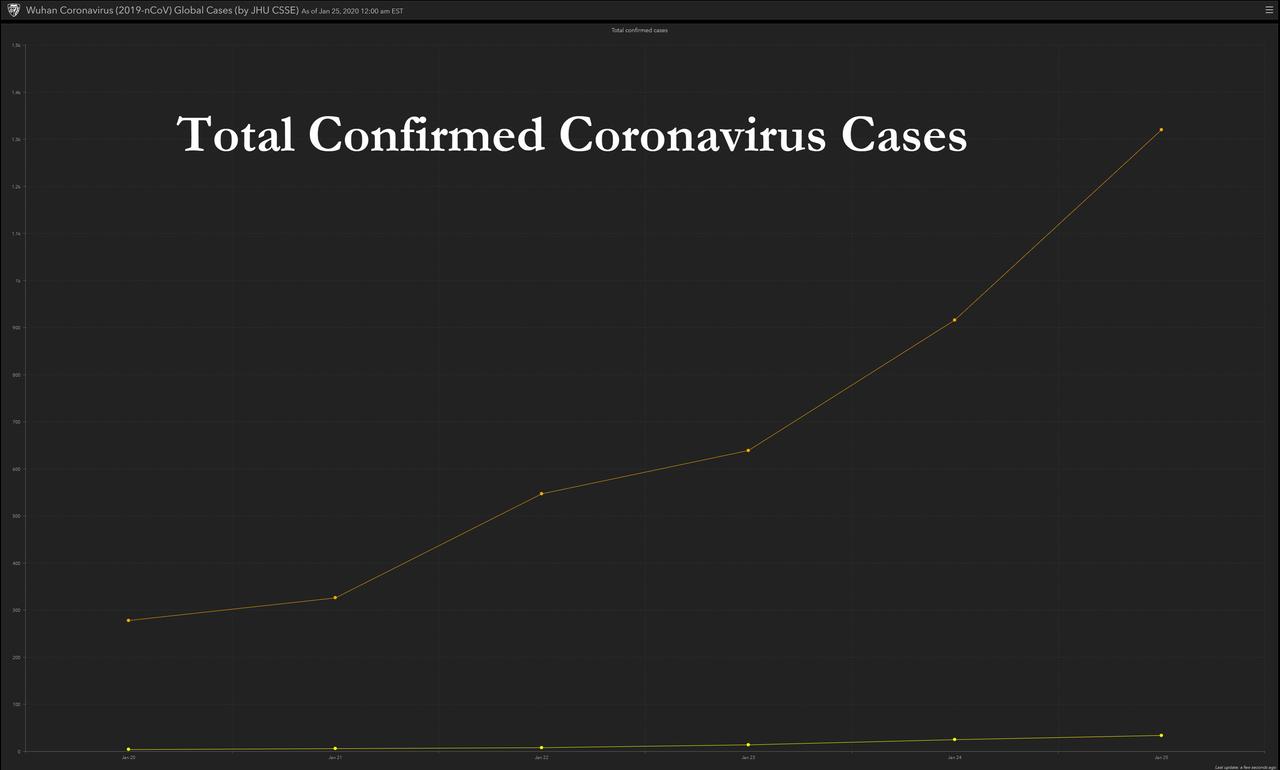

This Is How China Is Hiding The True Number Of Coronavirus Deaths

As the world’s cortisol and stomach acid levels rise every hour in parallel with the number of officially reported Coronavirus infections (and deaths), which as of Saturday morning was roughly 1,400…

… the world has an unpleasant flashback to 2003 when for weeks Beijing would lie and hide the full extent of the SARS epidemic to avoid risking a social panic. To be sure, this time China has done its best to pretend it has learned from the past and it is so transparent, even President Xi Jinping warned that the country is facing a “grave situation”, and that the spread of the deadly virus is accelerating after holding a special government meeting on the Lunar New Year public holiday.

After staying largely silent in public about the outbreak since it first emerged in central China last month, Xi on Saturday convened a special meeting of the seven-member Politburo Standing Committee, calling for a more centralized response to the epidemic and asserting personal responsibility in addressing the crisis.

“When an epidemic breaks out, a command is issued. It is our responsibility to prevent and control it,” Xi said, according to the state-run Xinhua News Agency. He called for the new high-level committee to “address concerns within and outside the country,” indirectly referencing mounting global concern about the epidemic, which Mr. Xi described as a “grave situation” that was accelerating. “We definitely can win the battle to contain the epidemic,” he vowed.

That remains to be seen: as reported earlier, in China – which has put over 56 million people on lockdown quarantine – the coronavirus has killed at least 41 people and infected over 1,400 in China. Ominously, a UK researcher predicted that the Coronavirus would infect over 250,000 people in China in under two weeks, which has sparked a renewed fear that China will once again try to underrepresent the true severity of the diseases until it is too late.

A patient at the Zhongnan Hospital of China’s Wuhan University

The problem is that even as China theatrically pretends to be so forthright about the extent of the epidemic – if only to avoid panic and chaos over allegations it is again hiding the full impact of the disease – it is doing precisely that, and now we know just how it is doing that: instead of putting down coronavirus as the cause of death for an unknown number of Wuhan casualties, China’s coroners and hospitals merely ascribe death to “viral pneumonia”, case closed.

Here’s how the WSJ describes this treacherous “bait and switch”:

A 53-year-old fitness trainer died on Wednesday after checking into a hospital in Wuhan a little more than a week earlier, said his niece. His family had expected the death certificate to reflect the deadly coronavirus, because as his condition deteriorated, his doctors told his family he was suffering from an untreatable virus in his lungs.

Instead, it recorded “severe pneumonia” as the cause of death, she said. The relatives of two other people who died in separate hospitals in Wuhan this week also described similar situations, saying the causes of death had been given as “viral pneumonia.”

Why did the hospital do this? Because as the relatives of all three now dead people said, the deceased hadn’t been included in China’s official count of 41 deaths attributed to coronavirus.

And that’s how China is suppressing the full extent of nCoV’s lethality, and keeping the mortality rate of the coronavirus artificially low: “There are likely to be many times more cases in Wuhan than officially confirmed,” said Neil Ferguson, a disease modeler at Imperial College London, who echoed the forecast of Jonathan Read, and estimated as many as 4,000 people may have been infected in Wuhan. “Clearly, the hospitals are overwhelmed.”

What’s worse is that if there are indeed 4,000 injected already, then the previously discussed catastrophic forecast of 250,000 cases by Feb 4 may be overly optimistic by half.

The official numbers are far lower of course: on Saturday morning, local time, the number of confirmed global infections had risen to at least 1,438, nearly doubling from the previous day. Comically, China has said it would hold officials accountable for any delays or omissions in reporting cases: so far such threats appear to have had precisely zero impact on anyone.

Others have confirmed as much: as the WSJ reports, “some Chinese media with reporters on the ground in Wuhan have said they have found cases that weren’t included in the official reporting. Caixin, a business journal, reported in early January that a doctor in Wuhan had been infected, 11 days before officials confirmed that medical staff had been infected. The Beijing News, a newspaper, reported this week that many patients weren’t officially labeled as carrying the new virus, even though their doctors and nurses said they were.”

Medical staff work to sterilize a hospital in Wuhan, China, on Jan. 24

That said, there may be a legitimate reason why the real number is being underreported, and it has to do with the flood of actual cases which is just too much for local doctors to keep up: China state-run TV cited doctors in Wuhan who said the number of patients with fever was too many to be treated and patients hospitalized couldn’t get the pathogenic test in time, because the samples needed to be sent to the provincial offices of the Chinese Center for Disease Control and Prevention.

That will soon change: China’s health ministry updated its protocol for identifying infections on Thursday with a simplified process for registering cases as suspected or confirmed. An earlier version, viewed by the Journal, required several steps of testing before a patient could be called a suspected case.

Yet despite these mitigating circumstances, it appears that the underlying incentive is to underreport the true extent of the epidemic for as long as possible.

One woman, a 63-year-old retiree in Wuhan, died on Tuesday, her nephew told the WSJ. The death certificate, viewed by the Journal, shows the cause of death as “pneumonia obtained from the community.” Doctors at the hospital that treated her told the family she had the new coronavirus, the nephew said, but she wasn’t counted as a case. The instance has also been reported by the Beijing News.

In another case, a 72-year-old former doctor was in the hospital for three days before he died on Tuesday, his nephew said. The doctors told the family he had caught viral pneumonia, he said. The niece said her uncle, the fitness trainer, first noticed symptoms of what he thought was a common cold in early January, which he believed he had caught at a banquet. He didn’t pay much attention initially, but a few days later, he decided to go to the hospital after seeing blood when he coughed. His niece said he had never been to the food market believed to be the epicenter of the virus.

“The doctor told us repeatedly that he caught the viral pneumonia that no medicine could treat,” she said. A patient’s immune system is the only defense, she said the family was told. “But after he died, the death certificate only said ‘severe pneumonia,’” she said, adding that she had expected the record to reflect the newly detected coronavirus.

The uncle was transferred to the infectious diseases unit on Wednesday, the niece said. Hours later, the family was informed that his condition was critical. Two days after her uncle died, China’s health ministry released the profiles of 39 deaths in Hubei due to the new virus, with two deaths listed in other provinces. She couldn’t find her uncle on the list.

As hundreds if not thousands of Wuhan residents die due to “severe pneumonia” instead of coronavirus, one can’t help but wonder if once the true cause of death is reported, instead of a 4% mortality rate as calculated by Dr. Jonathan Read, the Coronavirus epidemic won’t be in double digits – SARS was 11% – making this one of the most deadly epidemics in history.

A Chinese doctor who exposed the cover-up of China’s SARS outbreak in 2003 has been barred from traveling to the United States to collect a human rights award, a friend of the doctor and a human rights group said this week.

The doctor, Jiang Yanyong, a retired surgeon in the People’s Liberation Army, was awarded the Heinz R. Pagels Human Rights of Scientists Award by the New York Academy of Sciences. His army-affiliated work unit, Beijing’s Hospital 301, denied him permission to travel to the award ceremony in September, Hu Jia, a Chinese rights promoter who is a friend of Dr. Jiang’s, said Thursday.

Dr. Jiang rose to international prominence in 2003, when he disclosed in a letter circulated to international news organizations that at least 100 people were being treated in Beijing hospitals for severe acute respiratory syndrome, or SARS. At the time, the Chinese medical authorities were asserting that the entire nation had only a handful of cases of the disease.

The revelation prompted China’s top leaders to acknowledge that they had provided false information about the epidemic. The health minister and the mayor of Beijing were removed from their posts.

Once again, the mainstream media is pushing the repugnant race card, suggesting that Trump supporters are a bunch of knuckle-dragging xenophobes whose only reason for wanting a wall on the Mexican border is because they suffer an aversion to people with different skin color than them.

What exactly do White Americans – who opened the floodgates to immigration in 1965 – need to do these days to prove they are not natural born racists? Cancel their monthly subscription to Town and Country? Stop walking their dogs, which are, of course, four-legged vehicles of “racial segregation,” or stop attending their evening yoga class, the unsuspecting breeding grounds for white supremacists? Somehow I suspect that even if White people took to burning effigies of Ku Klux Klan members on their manicured front lawns that would not even put a stop to the ugly rumors. Let’s just face it, the only thing that will finally stop the slanderous slurs is if all White Americans publicly denounce their support of the biggest race-hater of them all, Donald J. Trump. And should they refuse the itinerant Liberal Inquisition will be only too happy to do it for them.

Just ask Noah Berlatsky, occasional columnist for MSNBC, whose latest piece was crowned with the zinger of a headline, ‘Trump voters motivated by racism may be violating the Constitution. Can they be stopped?’ Nice leading question there, but the premise that precedes it, that Trump voters are “motivated by racism,” is just one more election-season deceit.

Leftists are angry.

Usually at their own life choices, but “racism, sexism, and social injustice” sounds better.

Berlatsky’s article opens with the conclusion that Donald Trump “ran an openly racist campaign for president,” and that his popular rallying slogan “Make America Great Again” is actually code that can be translated into “America was greater when white people’s power was more sweeping and more secure.” Yet nowhere in any of Trump’s numerous campaign utterances or even Tweets has he ever singled out America’s White population as the intended sole beneficiary of his plans to remake the U.S. economy. In fact, just the opposite. As Trump has made it his goal to return some of the shine to America’s industrial Rustbelt, threatening companies with penalties and public scorn if they relocate their production operations overseas, the unemployment rate among Blacks now stands at 5.9%, down from 7.5% at the start of his presidency. At the same time, the employment rate among Hispanics is at historic highs.

It was exactly three years ago today, January 20, 2017, that I was sworn into office. So appropriate that today is also MLK jr DAY. African-American Unemployment is the LOWEST in the history of our Country, by far. Also, best Poverty, Youth, and Employment numbers, ever. Great!

At this point, the Democrats will invariably mention Trump’s promise to build a wall on the U.S.-Mexican border, a promise that arguably won the real estate developer the White House in 2016. Yet Trump, the Democrats argue, is an unrepentant racist because he admitted to an unsavory truth that even Hispanics living in America agree with: “When Mexico sends its people, they’re not sending their best…They’re sending people that have lots of problems, and they’re bringing those problems with us. They’re bringing drugs. They’re bringing crime. They’re rapists. And some, I assume, are good people.”

Trump was not arguing, of course, that all Mexicans are rapists or criminals. He was arguing that of the many who do make it across the border a disproportionate number do fit the description.

At this point, it needs to be asked why the Democrats deign to show so much care and compassion for those illegals breaching America’s border on a daily basis, at the very same time Democratic strongholds, like California and New York, are already bursting at the seams with tent cities and grinding poverty. Suffice it to consider a comment by a British tourist to San Francisco, the one-time crown gem of the increasingly tarnished, Democratic-controlled Golden State: “I can’t understand how anyone can live in a place where their everyday trip to get groceries or go to work includes a multitude of beggars asking for spare change or a meal.”

Considering that the Democrats can’t even take care of their own burgeoning problems in their primary constituencies, what is the real motivation behind their proposals to open the U.S. border and abolish U.S. Immigration and Customs Enforcement (ICE)? After all, these are the very same people who screamed ‘not in my backyard!’ when Trump threatened to send all apprehended illegals to the so-called ‘sanctuary cities’. Nancy Pelosi skirted the periphery of racism when she called the idea “disrespectful.”

Just out: The USA has the absolute legal right to have apprehended illegal immigrants transferred to Sanctuary Cities. We hereby demand that they be taken care of at the highest level, especially by the State of California, which is well known or its poor management & high taxes!

Would their sham benevolence have anything to do with securing more Democratic voters, or guaranteeing that the Republican Party eventually goes the way of the dinosaurs? Was New York Governor Andrew Cuomo motivated by pure compassion when he signed legislation granting driver’s licenses to illegal immigrants, who may now cast a ‘legal’ vote under New York’s notoriously loose voting laws? Now Democrats are demanding the elimination Voter ID rules, declaring them racist against minorities. This is one of the ways Berlatsky proposes to end so-called “racist voting” now purportedly contaminating U.S. politics.

It’s no secret that Hispanic Americans traditionally vote Democratic, and if that tendency were to change tomorrow you can bet that Chuck Schumer and Nancy Pelosi would be camped out daily at the Mexican border, demanding the necessary funds to finish the project.

In the final analysis, the Democrat’s groundless assertion that Trump supporters are kneejerk racists disintegrates when it is remembered that up to 10 million former Obama supporters – many of them White – switched allegiances to the Trump camp in the 2016 presidential election. Are we really expected to believe that all of those Americans suddenly became hardcore racists with the arrival of the evil ‘orange man’ and his pledge to build a wall? That sounds highly unlikely. The far more logical explanation for this massive change in political sentiment is that Trump’s plan to remedy America’s dangerously porous borders, thereby enhancing the security of all Americans, regardless of skin color, was a welcomed idea across the board.

Nevertheless, the real danger is that the Democrats, entranced by the cult of political correctness and an out-of-control cancel culture, will attempt by some extreme measures to identify and ban so-called ‘racist Trump supporters’ who are just regular Americans looking for a leader who will provide them with a well-guarded country that protects the rights of all its citizens regardless of skin color. Banning undesirable Trump voters from the ballet box may eventually become as easy as censoring right-leaning Twitter users.

Clearly, the Democrats learned absolutely nothing from the mistake of branding Trump supports “deplorables” – to quote Hillary Clinton – and have only worsened their present position by calling these same voters, many of them former Obama supporters, “racist.” Such a gross simplification and misunderstanding of the current American political realities goes far at explaining why the Democrats stand very little chance of beating Trump at the ballot box.

“You Think Americans Really Give A F**k About Ukraine?” – Pompeo Flips Out On NPR Reporter

Democrats’ impeachment proceedings were completely overshadowed this week by the panic over the Wuhan coronavirus. Still, Secretary of State Mike Pompeo is clearly tired of having his character repeatedly impugned by the Dems and the press claiming he hung one of his ambassadors out to dry after she purportedly resisted the administration’s attempts to pressure Ukraine.

That frustration came to a head this week when, during a moment of pique, Secretary Pompeo launched into a rant and swore at NPR reporter Mary Louise Kelly after she wheedled him about whether he had taken concrete steps to protect former Ambassador to Ukraine Marie Yovanovitch.

House Democrats last week released a trove of messages between Giuliani associate Lev Parnas and Connecticut Republican Congressional candidate Robert Hyde. The messages suggested that Yovanovitch might have been under surveillance before President Trump recalled her to Washington. One of the messages seems to reference a shadowy character able to “help” with Yovanovitch for “a price.”

Kelly recounted the incident to her listeners (she is the host of “All Things Considered”) while

After Kelly asked Pompeo to specify exactly what he had done or said to defend Yovanovitch, whom Pompeo’s boss President Trump fired last year, Pompeo simply insisted that he had “done what’s right” with regard to Yovanovitch, while becoming visibly annoyed.

Once the interview was over, Pompeo glared at Kelly for a minute, then left the room, telling an aide to bring Kelly into another room at the State Department without her recorder, so they could have more privacy.

Once inside, Pompeo launched into what Kelly described as an “expletive-laden rant”, repeatedly using the “f-word.” Pompeo complained about the questions about Ukraine, arguing that the interview was supposed to be about Iran.

“Do you think Americans give a f–k about Ukraine?” Pompeo allegedly said.

The outburst was followed by a ridiculous stunt: one of Pompeo’s staffers pulled out a blank map and asked the reporter to identify Ukraine, which she did.

“People will hear about this,” Pompeo vaguely warned.

Ironically, Pompeo is planning to travel to Kiev this week.

The questions came after Michael McKinley, a former senior adviser to Pompeo, told Congress that he resigned after the secretary apparently ignored his pleas for the department to show some support for Yovanovitch.

Listen to the interview here. A transcript can be found here.

NPR’s Mary Louise Kelly says the following happened after the interview in which she asked some tough questions to Secretary of State Mike Pompeo. pic.twitter.com/cRTb71fZvX

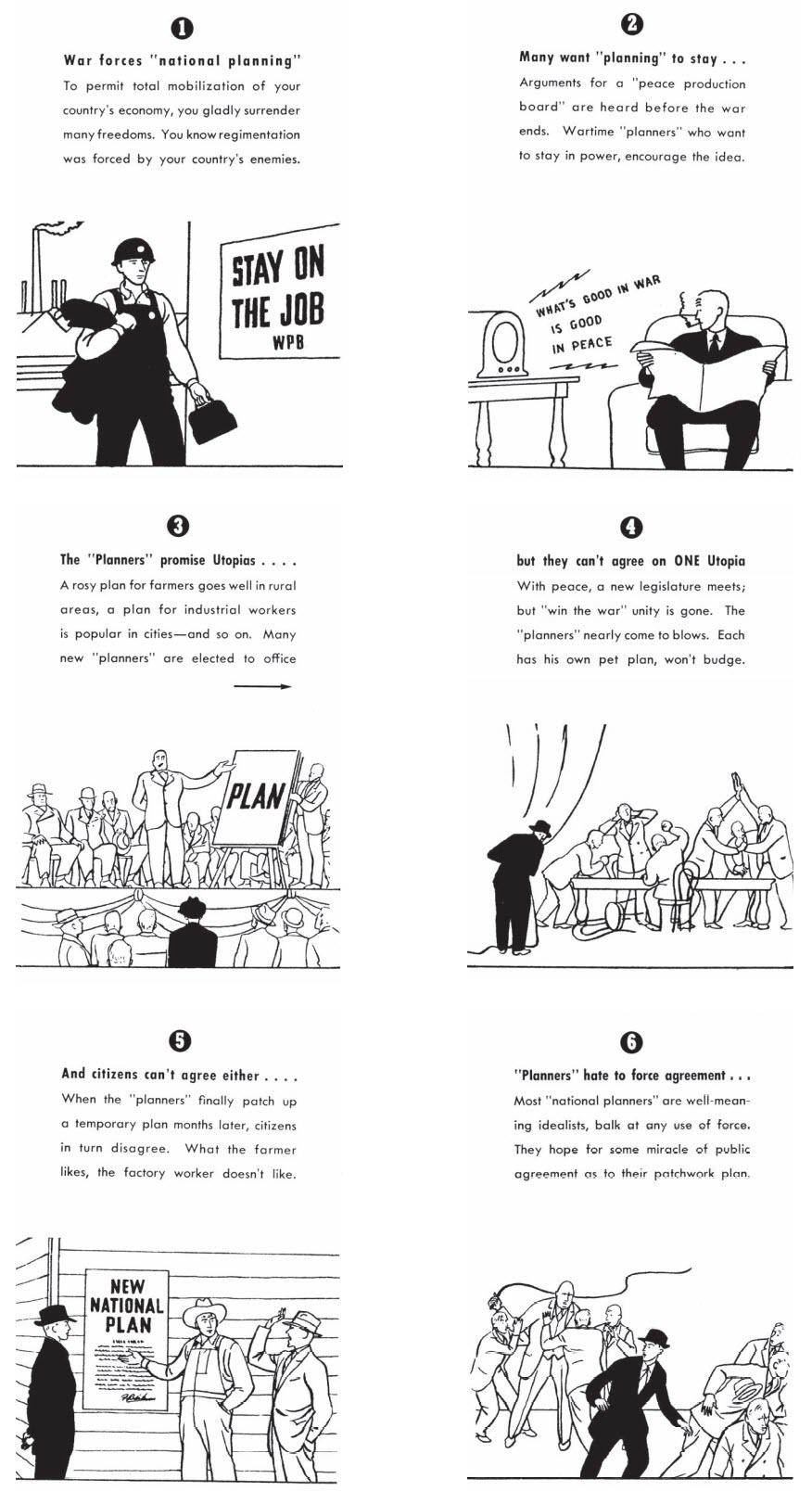

Some years ago, Look, a now-defunct American magazine, published a set of cartoons which attempted to illustrate the basic framework of Friedrich Hayek’s Road to Serfdom. We have published them in other essays. We did it here. And here. And…here. Today we do it again with an excerpt of the first ten ‘steps’. You can see the full range on the Mises Institute’s website.

We keep publishing these cartoons because they are relevant and because they are powerful illustrations of the role of narrative in aiding the concentration of political power. We also think it is valuable to frequently consider forces like this which remain so applicable across time and circumstance.

Yet there is more than one path to serfdom. This is one. In the illustrated scenario, a major event like World War II is used by well-meaning political leaders to establish more long-lasting central control over the planning of economies. They also conjure a Strong Man to see them through. It was a familiar story for mid-20th century Europe and many other times in history. There are other paths. For example, there are paths which run through corporate monopoly power or, say, the Church. These sorts of paths tend to get less attention from those of us who cherry-pick when it comes to Hayek, but that doesn’t make them any less real.

Still, the power of the political Strong Man is a special case. The political Strong Man who seized power immorally or illegally is an even more special case. Yet it isn’t so much the specific case study that interests me so much as the evolution of the road itself. And it has evolved. Seventy-five years after the book that described it was printed, the road to serfdom has gotten shorter. Faster. Those who seek power no longer have to grapple with the kind of public debate that arrested the growth of political movements in the past. Always-on traditional and social media now provide much more powerful tools for missionaries to create common knowledge out of whole cloth. The Widening Gyre has created an environment of identity-based political support ready to muster at will. The methods to summon existential memes to compel compliance are now old hat.

In 2020, all it takes is a critical mass of missionaries to take up the message.

There is a new Road to Serfdom, and I think it looks something like this.

Step 1: Missionary promotes the narrative that “something must be done”about a problem

Step 2:Other missionaries work to establish the narrative as common knowledge, something “everybody knows that everybody knows”

Step 3: Missionaries decry lack of action by traditional mechanisms, need for an unfettered hand to pursue it

Step 4: Missionaries make an explicit play for power

Step 5: Missionaries warn what will happen if they are not given the power

No matter your political identity, I suspect you can think of appealing examples of this pattern. But if you will indulge me, I want to walk you through an especially relevant, present-day example. We are going to explore the evolution of the curious intersection of central banking and climate change over the past four years.

We’re going to do it because I think we are charting a potential new route on the road to serfdom.

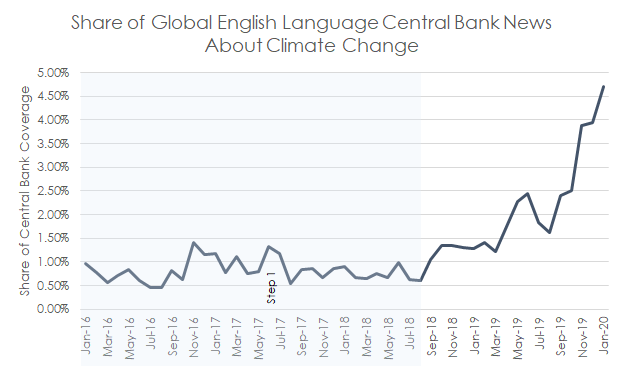

That road starts in January 2016, with Step 1.

Step 1 | Missionary promotes the narrative that “something must be done” | January 2016 – August 2018

Sources: Epsilon Theory, LexisNexis Newsdesk

The title of this graph is a bit of a mouthful. So what, exactly, does it show? In each month between January 2016 and January 2020, it plots a fraction. The numerator of that fraction is the total number of articles with text referring to both climate change AND central banks, where “central banks” means both the term “central banks” or “central banking” as well as the Federal Reserve, European Central Bank, Bank of Japan, Bank of England, People’s Bank of China and the key public-facing officials of those institutions. The denominator of that fraction is just the raw count of central banking articles.

As you’ll note in the first graph above, the first period we charted runs from approximately January 2016 through August 2018. During this first stretch, there was almost no relationship between the way that elected political leaders, unelected political officials, corporate leaders and media members with prominent platforms (collectively in our parlance, “missionaries”) wrote or spoke about central banks and climate change together. These were practically non-overlapping topics. More specifically, between January 2016 and August 2018 about 8 in every 1,000 news articles about the Federal Reserve, Bank of Japan, People’s Bank of China, European Central Bank or Bank of England, or any of their respective key officials, related the activities of those banks to climate change.

You will probably also note a period of modest acceleration in the relationship between these topics between November 2016 and the summer of 2017. This was the result of broad economic pieces published in the wake of the election of Donald Trump, many of which discussed, analysed and expressed opinions on a range of topics, from climate and energy policy to the Fed without necessarily connecting the two. Excluding that brief flurry, articles which related the two concepts were almost entirely related to one of two things:

The PBOC’s establishment of guidelines for the issuance of Green Bonds; and

Statements made by Mark Carney, Governor of the Bank of England and Chair of the Monetary Policy Committee

I am always inclined to ascribe at least some missionary intent to any publication referencing the PBOC, but these are largely perfunctory, logistical and trade articles. Not speeches, finger-waving or “this is how you should think about the environment” propaganda. Green-washing propaganda? Yes, I think that’s a charge you could level. But while it is a lark to talk about actors buying “clean” jet fuel for their G5s in Davos, or the world’s biggest polluter touting its various green initiatives, that isn’t really what we’re talking about here.

No. Instead, what interests us is Goldman alum Carney, the first mission creep missionary. From a June 2016 article in Canada’s Globe And Mail, he was already active establishing the idea that something must be done to create a connection between regulatory policy – more to the point, monetary policy – and climate change. And he did so in a way that was crafted for an audience of institutional investors.

He estimated that global carbon reduction needs imply “somewhere in the order of $5 to $7-trillion a year” in clean-infrastructure investments. “The question is, how much of that is going to be financed through capital markets?” He said that if there is a “global standard” established for green-infrastructure bonds – something the G20 is working on – it would create “a core mainstream fixed-income opportunity.”

He said that China, in particular, has large needs for such infrastructure that could generate relatively high-yielding investment products.

He also argued that a “a consistent, comparable, reliable” global system for corporate disclosure on carbon emissions would better allow equity markets to price in relative risk into company valuations. Mr. Carney has been championing such a system for much of the past year, in his dual roles as the head of the Bank of England and the chairman of the international Financial Stability Board.

“The relative value opportunity in equities is considerable,” he said.

“Having the Governor of the Bank of England here sends a very strong message that it is important that we act now, and that we have a real opportunity for Canadian business,” Ms. McKenna told reporters following the session.

Source: Climate change a $5-trillion opportunity, Globe and Mail, July 16, 2016

Carney’s September 2016 speech in Berlin was a masterpiece in narrative construction, explicitly conflating climate change with terms of art in the world of financial risk management. He begins:

Your invitation to discuss climate change is a sign of the broadening of the responsibilities of central banks to include financial as well as monetary stability. It also demonstrates the changing nature of international financial diplomacy.

Source: Resolving the Climate Paradox, Mark Carney, September 22, 2016

That is, I believe, what we call saying the quiet part out loud. Still, to really appreciate the skill being applied here, take note of the effective redefinition of climate change in the most well-known memes of financial risk. A Minsky moment, indeed.

A wholesale reassessment of prospects, as climate-related risks are re-evaluated, could destabilise markets, spark a pro-cyclical crystallisation of losses and lead to a persistent tightening of financial conditions: a climate Minsky moment.

Source: Resolving the Climate Paradox, Mark Carney, September 22, 2016

In fairness to Carney, at this point he is not advocating the establishment of some grand global central banker-driven policy-making body. In fact, in the speech he delivered at Lloyd’s London to really kick off this whole cycle back in September 2015, he said explicitly that he doesn’t see that as the proper response. His speeches and plans have favored mostly an expansion of accounting standards for carbon reporting, climate change-based stress testing and application of existing risk management tools to this emerging problem. In short, Carney’s vision was an extension of existing central banking tools for measuring, responding to and mitigating systemic shocks that might be the result of climate change. If you see the $10-dollar term of art ‘macroprudential‘ in this note, that’s what we mean by it.

Still, for months, we had a missionary – or perhaps a prophet – alone in the wilderness, shouting that something must be doneto address the risks of climate change through monetary policy.

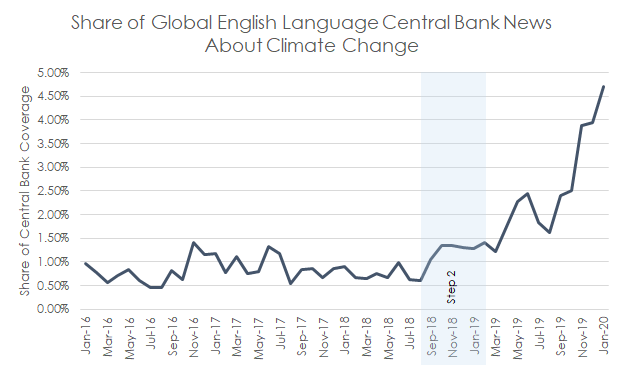

Step 2 | Other missionaries work to establish the narrative as common knowledge, something “everybody knows that everybody knows” | September 2018 – January 2019

Source: Epsilon Theory, LexisNexis Newsdesk

While there were occasional flareups in the discussion over this period – usually prompted by a Carney speech or a related conference topic within the professional environment of economics, it wasn’t until the fourth quarter of 2018 that any acceleration in the intersection of these two topics began. In the build-up to Davos in 2019, other missionaries in the world of economics and economics journalism began to take on the mantle of addressing climate change through financial regulation. Some of the less noteworthy among them clamored already for an unfettered, unelected global power to tackle it.

Here, though, the breakdown in international cooperation and trust becomes really damaging. Ideally, existing global institutions – the IMF, the World Bank, the UN and the World Trade Organization – would be supplemented by a new World Environmental Organisation with the power to levy a carbon tax globally. Even in the absence of a new body, they would be working together to face down the inevitable opposition to change from the fossil fuel lobby.

Source: Larry Elliott, ” Climate change will make the next global crash the worst”, The Guardian, October 11, 2018

There are a lot of ways to write “I want to establish a world body who can tax everyone on the planet, but I’ll settle for some strongly worded letters to the CEO of ExxonMobil,” and this is apparently one of them.

Still, this sort of overzealous shield-banging was the exception during this period, not the rule. The most prominent emerging voices, former officials of the Federal Reserve and some of their associates in the Climate Leadership Council, began a regular flow of Op-Eds to papers and publications around the United States. The flood began in earnest on September 10, 2018 with the publishing of an Op-Ed piece in Fortune written by Janet Yellen and Ted Halstead. The CLC had published its plan almost a year earlier to some acclaim from editorial pages, but had not gotten much traction. This did.

Other economists had similar Op-Eds published in the New York Times, the Boston Globe, the Dallas Morning-News and many other large, metropolitan publications in each of October, November and December 2018. Nobody here was pining for the Fed to have ‘managing climate change risks’ added to its mandate. None looked to take the intersection of monetary policy and climate change beyond macroprudential risk management. None that I can detect (other than including Fed officials as authors) even so much as imply a role for central banks. Most contemplate a set of the CLC’s regulatory policies for addressing climate change in context of traditional political systems governed by elected officials. If you ask me (and you didn’t, but you’re on my website), their proposals and Op-Eds were perfectly sensible and blessedly light on existential memetics.

But from a narrative perspective, whether the proposals were sensible, made in earnest and good faith, or even if they were a good idea, simply doesn’t matter. From a narrative perspective, what is important is that these well-intentioned planners established common knowledge that financial regulation would be necessary to mitigate the negative impact of climate change.

By the end of 2018 and 2019, I think that it was something everybody knew that everybody knew.

Step 3 | Missionaries decry lack of action by traditional mechanisms, need for an unfettered hand to pursue it | February 2019 – October 2019

Source: Epsilon Theory, LexisNexis Newsdesk

Davos in 2019 was…well, it was like Davos always is. It was an opportunity for political and corporate missionaries to scream from a microphone provided by media missionaries for reasons that escape literally every other person on the planet. Still, as irritating as we might find it, the narratives promoted there often take root.

Four days after Davos concluded, the opening salvo of Step 3 was an open letter submitted by 20 Senate Democrats to Jerome Powell telling him that they considered it “imperative” that the Federal Reserve ensure the stability of the US financial system in the face of climate change risks. The letter was directed by a member of the Banking Committee, and a person whose job is, coincidentally, to make and pass laws which could govern just about every conceivable climate policy.

But it wasn’t just congressional leaders who began to float the idea that an independent institution like the Fed ought to more explicitly incorporate climate change into its mandate. It was the Fed itself. In March, a senior policy adviser at the San Francisco Fed wrote approvingly of the latitude some comparable institutions have to influence the relative cost of capital of “green” vs. “non-green” issuers of securities.

This is a Big Deal.

The question of using a central bank’s balance sheet to influence asset prices was controversial and problematic enough when the activity was largely constrained to government debt. It was more concerning when it began to include corporate debt securities and (in some countries) equity securities. Probably half of the content on this website concerns our agitation with these activities, so I won’t belabor their discussion. I will, however, say that the expansion of central banks’ activities to include the open, intentional and unavoidably arbitrary influencing of costs of capital and securities prices for different sectors and companies to reflect some scheme of ‘good’ and ‘bad’ isn’t just a simple next step. It would represent a quantum change in the accepted macroprudential role we cede to central banks under our present social contract.

I think it is important, especially for those who may not deal with these questions every day, to know what is being suggested here. Some economists were – and are – proposing that an unelected body sit in the position of determining by fiat the price at which (and whether!) different companies would be able to access capital based on that body’s assessment of whether that institution was deemed to be sufficiently green. And yes, some of this is already happening.

In a classic economist’s conclusion, the author then lamented the Fed’s more limited present power.

Many central banks already include climate change in their assessments of future economic and financial risks when setting monetary and financial supervisory policy. For the Fed, the volatility induced by climate change and the efforts to adapt to new conditions and to limit or mitigate climate change are also increasingly relevant considerations. Moreover, economists, including those at central banks, can contribute much more to the research on climate change hazards and the appropriate response of central banks.

Climate Change and the Federal Reserve (March 25, 2019)

By April, some missionaries started saying the quiet part out loud again. In a Fortune article published in April 2019, various commentators presented a cynical step-by-step explanation of the application of the “gameplan” that had worked to get central banks engaged in diversity issues that also had proved too problematic to solve via democratic and political mechanisms.

Now, central banks are making a similar case when to comes to addressing climate change…“If you get in with the herd that says climate change is a financial risk, then central banks have all the tools,” says Williams. “I think what you’re seeing is a wave of progress.”

Central Banks are the World’s New Climate Change Activists (Fortune, April 26, 2019)

All that must be done is to change common knowledge. That is exactly what pieces like this do. They change what everybody knows that everybody knows. By the late spring of 2019, everybody at least suspected that others suspected that climate policy was too important to be left to officials and deliberative bodies constrained by pesky consensus-building and politics.

Major financial news outlets began covering the topic from this angle at this time as well, now bringing up the “M” word. Mandate. It simply means the official policy objective(s) to be targeted by the unelected officials of the world’s various central banks. Bloomberg brought up the topic in early April. And yes, the below is theoretically from a news article, not an Op-Ed, but leave that alone for the moment.

Freak weather events blamed on global warming — largely regarded as temporary shocks so far — risk becoming serious impediments to economic management in the future. They could even require a rethink of central-bank mandates at some point

Central Banks Are Thinking Greener as Climate Change Hits Policy (Bloomberg, April 2, 2019)

The idea that subjective regulatory policy, rather than traditional macroprudential activities, ought to be shifted to an unelected body was now mainstream. The related narrative of the need for a central bank mandate for climate change, which in most cases would codify that shift in responsibilities, was now mainstream.

When narratives begin to accelerate, we find that they often manifest in Fiat News. That’s our term for the the use of affected language, opinions presented as fact and obvious issue framing in news articles. The intent is usually to tell you how to think about an issue. Nobody does it better than the New York Times, and here they really go for the gusto. In the lede, no less! I’ll leave you to guess at the author’s opinion.

A top financial regulator is opening a public effort to highlight the risk that climate change poses to the nation’s financial markets, setting up a clash with a president who has mocked global warming and whose administration has sought to suppress climate science.

Climate Change Poses Major Risks to Financial Markets, Regulator Warns (New York Times, June 11, 2019)

In July, the economics research side of a global investment bank published a piece asserting that not adding climate change to the mandate of central banks could be considered an abrogation of fiduciary duties owed by the Federal Reserve to citizens. They added that even if that wasn’t possible, they might have an argument for considering it part of the mandate already given its theoretical impact on employment and prices. Let us conveniently ignore for a moment that extension of this logic would permit the inclusion of literally every molecule between earth and sun in the mandate of central banks.

The real quiet-part-out-loud moment, however, came later in July. It was a widely circulated and shared piece published in Foreign Policy magazine that was later rehashed in an interview with the Atlantic. It was very explicit about the belief not only in the attractiveness of a mandate change, but in a mandate which went wellbeyond the macroprudential authority we have traditionally afforded to our central banks.

As of yet, their response is defensive, focusing on managing financial risks. The rest of us have no choice but to hope that they move into a more proactive mode in time.

Why Central Banks Need to Step Up on Global Warming (Foreign Policy, July 20, 2019)

And that is exactly where the narrative starts to take off from what Carney originally had in mind, and from the narrative the various CLC authors promoted in their Op-Ed push of 2018. The author asserts that central banks need to embrace not only the regular roles of ensuring liquidity and functioning lending markets, but the re-engineering of the economy, where it is growing and where it isn’t.

Taken at face value, the macroprudential approach makes sense. It is better for the financial system to be resilient. But in adopting this approach, the central banks are using the same conservative approach to climate change that proved lacking when it came to financial reform. In the years since the 2008 financial crisis, they have perfected their tools of crisis management but without addressing the root cause of the problem: that banks were too big to fail. More than a decade on, they still are.

Of course, everything possible should be done to make the financial system resilient in the face of climate-related Minsky moments. But why is financial stability the principal concern? Central banks and financial regulators should instead be urgently exploring what they can do to alter the course of economic growth so that the world can rapidly decarbonize and thus prevent worst-case climate change—and the related financial fallout—in the first place….

…If the world is to cope with climate change, policymakers will need to pull every lever at their disposal.

Why Central Banks Need to Step Up on Global Warming (Foreign Policy, July 20, 2019)

Or, as the author put it more succinctly in the Atlantic interview:

Realistic? No. I mean, depends what you mean by realism. The scale of the challenge requires a boldness of action for which there is no precedent.

How Climate Change Could Trigger the Next Global Financial Crisis (The Atlantic, August 1, 2019)

Let’s be really clear about what this is: This is a clarion call for unelected individuals participating in a body with limited transparency and limited oversight to be granted the authority to exert policies to lift up specific industries, companies and individuals, and to bring down specific industries, companies and individuals.

This is Step 9 of the Hayek road.

It is also the culmination of Step 3 of our variant of that road. Its call is always Always ALWAYS the same: We are faced with an existential risk! We simply cannot abide the slowness and inefficiency of open democratic processes! We must vest power in a body with the autonomy and authority to act without debate or politics!

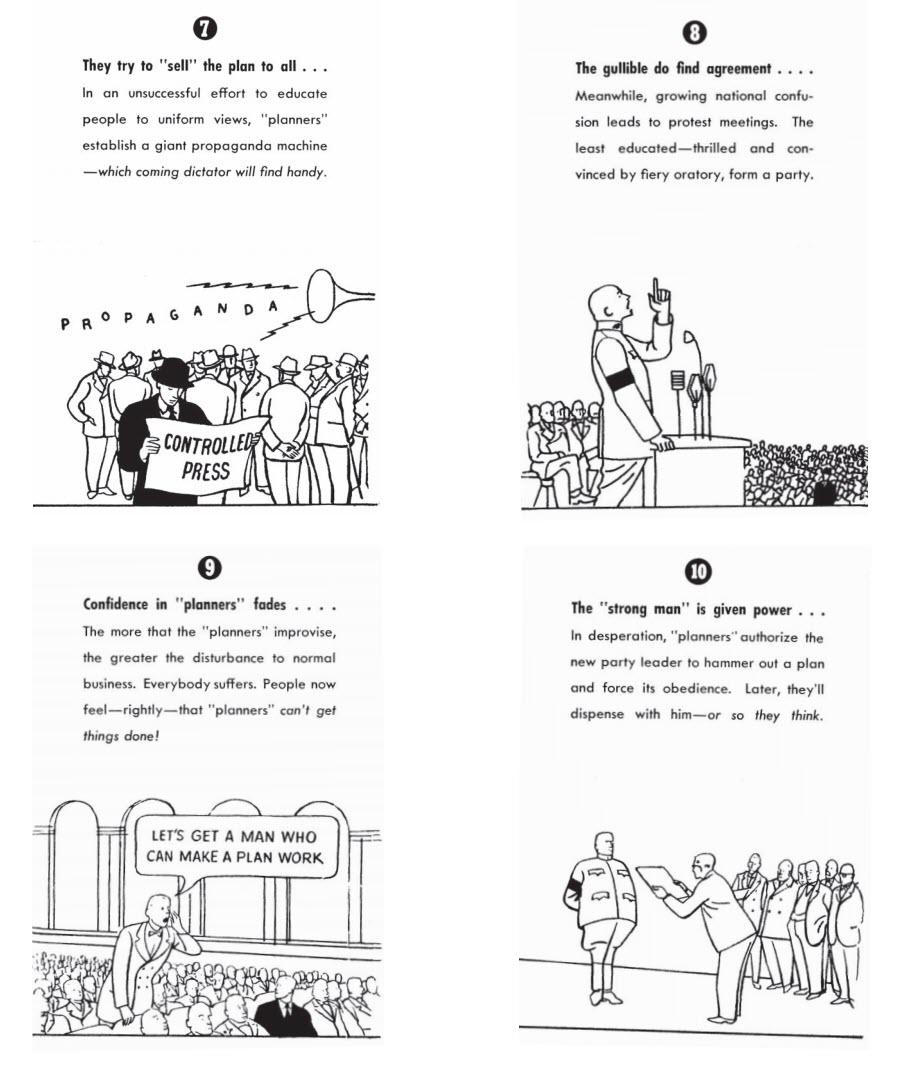

Let’s get a man who can make a plan work.

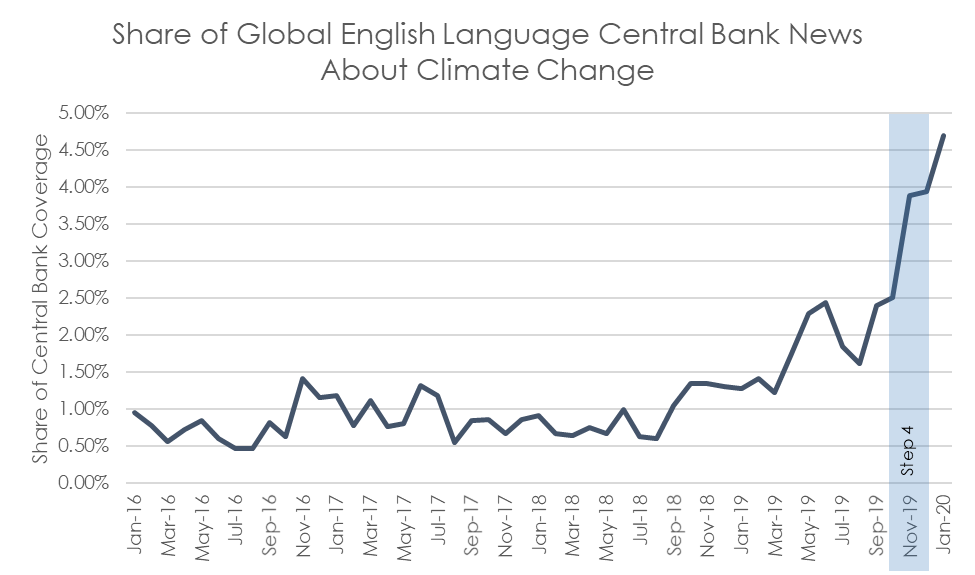

Step 4 | Missionaries make an explicit play for power | November 2019 – December 2019

Source: Epsilon Theory, LexisNexis

The demand for “a man who can make a plan work” is only that – a demand – until its call is heard and taken up. Our next brief period is defined by the taking up of that call. Only it wasn’t a man. It was taken up by incoming ECB President Christine Lagarde. She did so at a time that the intersection of these two topics was reaching a fever pitch.

By then, the narrative pivot so cynically described earlier was no longer a secret. What was once “we need to consider stress testing, reporting requirements and accounting standards for climate-related risks to the financial system” had become “we support the ECB as a lever for climate protection.”

Not just protecting the financial system from unique risks that might be presented by climate change. Protecting the climate. I am not paraphrasing.

“We will support Lagarde as she makes the E.C.B. a lever for climate protection,” said Mr. Giegold, who sits on the economics committee.

Lagarde Vows to Put Climate Change on the E.C.B.’s Agenda (New York Times, September 4, 2019)

In the lead-up to her confirmation, Lagarde was strident in her remarks about the “strategic review” that would characterize climate change as a “mission critical” consideration for the ECB. Media outlets were eager to attach the “mandate” language, although (as Lagarde herself pointed out in her first post-confirmation press conference) a true formalized mandate would require changes from EU’s Parliament. But that is what narrative does. Once an idea like “let’s do it through a mandate change!” becomes common knowledge, it becomes the default framing for all such stories.

Alas, the cat was already out of the bag anyway. Lagarde’s comments consistently embraced the role of the ECB to selectively do exactly what a mandate would require: influence the composition and winners and losers of the economy by manipulating the price of capital of issuers who fit or do not fit a particular standard.