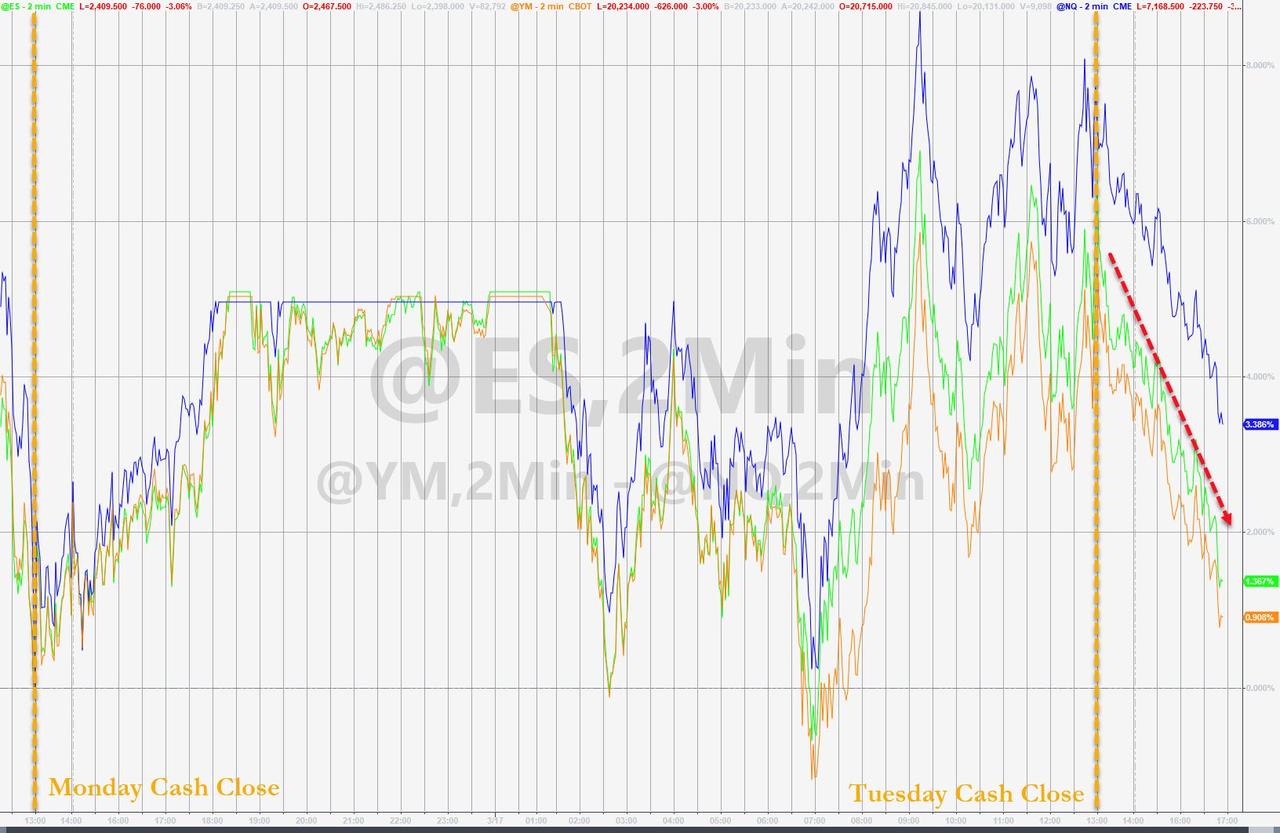

It is unclear what the immediate catalyst is this time – aside from the fact that we are now outside of the stock-trading-machines reach – but US equity futures are plunging in early Asia trading.

Dow futures are down 650 points…

Erasing most of the day’s gains…

“…and suddenly millions of bailout-demanding voices cried out in terror and were suddenly silenced. I fear something terrible has happened.”

How did the Democrats end up with Joe Biden as their presumptive nominee?

After three years of preparatory media fire about diversity and change, and chumming the electorate with promises of free college alongside all the health care-they-care-to-eat, Democrats started with six women, a couple of black people, the gay guy, and progressive ideas ranging from the necessary to the kooky. The full list included 30 players.

They ended up choosing a candidate left over from 1958. Joe Biden is old, he’s tired, he lost the race for president twice already (once for plagiarism and once for lying about his education), and he appears to be in some state of cognitive decline. Between the hair plugs and the botox, he looks waxy, like grandpa putting himself out there for one last fling after Grandma Obama passed away, God rest her soul.

The Democrats’ entire premise is false. They misunderstood Trump’s election as a fluke if not an outright scam. This was sustained by a relatively small group of disconnected people who, through cancel culture, peer pressure, and the need to fill a 24/7 media vacuum, convinced each other they were right.

So when a mediagenic Hispanic woman won a nothing race with few votes cast against a sleepy incumbent in the ever-Democratic Bronx, they told each other they were right and AOC is the living proof. The echo chamber backed them up as they serially proclaimed new saviors, offstage The Squad, onstage Beto! and Pete, though Booker, Harris, Klobuchar, and others were granted mini-moments after a decent debate performance or some minor splash. Some call it the “pundit fallacy,” the belief that Americans are at heart progressives who just haven’t been educated to vote the way they really should.

The problem was that as soon as the actual people were allowed a word, it all fell apart. The primary narrowed quickly. White voters didn’t like the black candidates. Novelties like Yang and Steyer sucked up bandwidth and confused the electorate. Midwesterners were terrified of initiatives aimed at transgender, reparation, and illegal immigrant support blocs that existed only in the minds of those who read The Atlantic and The Nation. Everyone wanted better health care but very few agreed that a massive upheaval of our capitalist economic system was the way forward. The candidates went out of their way to ignore public opinion on these issues and alienate voters, especially purple voters.

Now quick, name a single Biden signature policy initiative.

The second to last man standing, Bernie, was artificial. Unlike everyone else in the field, he started with a pre-built organization, fully formed policies, and cash from 2016. He had a certain glow to him, having been treated unfairly in 2016, but that did not help much when there was no anti-Hillary vote to garner. But while initial power-ups allowed Bernie to survive, he never grew. Voter turnout did increase on Super Tuesday compared to 2016, but most of those new votes went for Biden. Bernie was the rock band still touring behind its only smash hit; the audiences are the same people who loved them in the ’70s, just older now, even as the size of the venues shrinks.

The process of elimination was nudged along by old-fashioned party power plays. Black voters were massed by local pols in South Carolina to come out for Biden. Someone behind the curtain (almost certainly Obama) made the calls to Buttigieg and Klobuchar and told them, as he likely did in 2016 with Biden to clear the way for Hillary, “kid, this ain’t your night.”

That’s how you end up with Joe Biden.

One writer called Biden’s success the product of the “politics of exhaustion.” This sees a Democratic electorate not anxious for change, but just tired of being tired. The unrelenting apocalyptic news cycle burned them out, and all they want is to put someone acceptable enough in charge. When Nancy Pelosi declared the morning of Super Tuesday, “Civilization as we know it is at stake in the 2020 election,” they had had it.

You end up with Joe Biden, running on three things:

1) he’s not Trump;

2) maybe he’ll die in office and his VP will take over early in his term; and

3) Joe’s cognitive decline appears slightly less severe than Trump’s. Not exactly “Hope and Change.”

Biden candidacy also means sweeping three years of Democratic messaging under the bed. The list of once-familiar subjects Joe won’t be able to talk about is a long one. Russiagate imploded on its own. Impeachment centered on Hunter Biden and ain’t nobody on the Democratic side gonna bring that up.

President Bone Spurs?

Biden received five student draft deferments during the Vietnam War, same as Trump. In 1968, when his student status was wrapping up, Biden was medically reclassified as “not available” due to asthma. Yet in his autobiography, he describes an active youth as a lifeguard and high school football player. He also lied about being on the University of Delaware football team.

Trump’s naughty finances?

After leaving the Obama White House, Joe and his wife made more than $15 million, mostly via sweetheart book deals. They made nearly twice as much in 2017 as they did in the previous 19 years combined. The University of Pennsylvania gave Joe $775,000 to teach, and then was nice enough to grant him indefinite leave of absence from actually teaching. Biden charged the Secret Service $2,200 a month in rent for a cottage on his property so they could protect him. Since leaving office, he’s made $2.4 million on speaking engagements, including $10,000 for travel expenses to the University of Buffalo. A speech at Southwestern Michigan in October 2018 included $50,000 in travel expenses.

Taxes?

After failing to close the loophole with Obama, Joe left office to create his own S Corporation. As a result, he receives money for things like book advances and speaking fees not directly, which would cause him to pay Social Security and Medicare taxes as with salaries, but laundered as divestitures from a corporation he owns. As corporate money, nasty personal taxes are fully avoided, and the corporation can claim nearly unlimited “business expenses” to be deducted against those profits. Joe’s S Corp also donated his own money back to his PAC. Legal laundering.

Trump’s sexism and racism?

Young people, Google “Anita Hill” now. You’ll be hearing a lot about her come the fall.

Biden represents to many Democratic voters that they will never see health care reform again in their lifetime (his comeback drove a $48 billion gain for health insurance stock; they know.) They also won’t see a woman president for who knows how many years. Income inequality will remain the salient characteristic of our society. To win, the 77-year-old Biden will have to break the record for oldest man sworn in as president (Trump holds the title now).

But Biden’s worst enemy heading into November will be low voter turnout. His opponent for Democratic votes will be Mr. Just Stay Home. That’s why those polls showing broad dissatisfaction with Trump are pointless. The Trader Joe Moms of Northern Virginia are never going to vote for Trump, but they just might vote for no one. There are ominous signs: polls for states Biden won on Super Tuesday, including Massachusetts, Texas, and several southern states that helped catapult the former vice president into front-runner status, found that young voters did not show up at the rate they did in 2016.

The black voters who saved Biden in South Carolina are notoriously fickle when it comes to turnout. Older Americans, who favor Trump, historically turn out at 30 to 40 percent higher rates than younger voters. The exaggeration of white privilege that became a cornerstone of the Democratic Party—whites are racist, opioid-soaked gun nuts—is also one of the reasons Democrats risk losing the 2020 race, as it leads inexorably to the devaluation of the very voters needed to clinch the Electoral College.

Biden’s new status triggered the mainstream media to drop any talk of the issues that have dominated their agenda for three years in favor of droning on about electability. It makes little sense. Why else vote for someone if not because he represents something you like? You want electability? Run a puppy. Biden represents the endpoint of the idea that anyone must be better than Trump.

That’s betting the whole house on one thin straw. It’s what happens when you settle for Joe Biden.

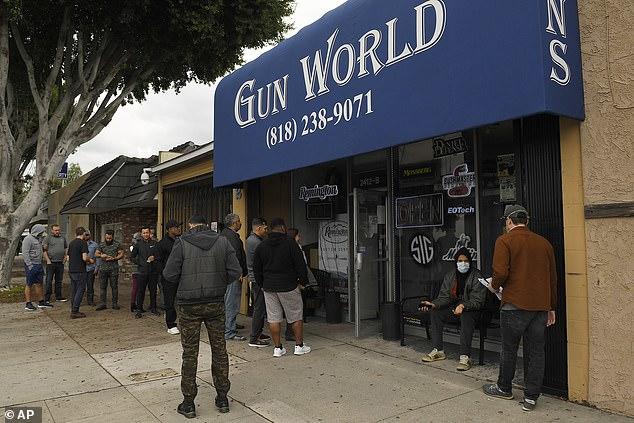

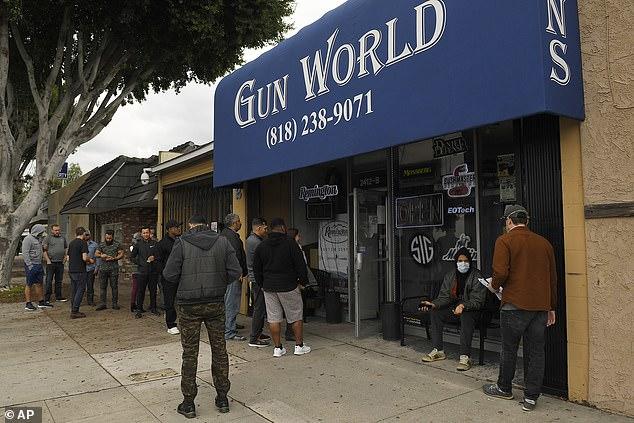

Americans Rush To Buy Firearms As COVID-19 Stokes Fear Of Unrest

First it was food, now it’s guns.

Americans worried about the impact of coronavirus have been lining up at gun stores across the country, arming themselves as fear of social unrest and food shortages have sparked a surge in preparedness.

Gun store in Culver City, California

Lines could be seen stretching around the block at gun stores in California, New York and Washington – the states currently most affected by COVID-19.

Lengthy lines formed outside the Martin Retting Guns store in Culver City, California, on Sunday morning, before the store opened. People said the line Saturday was so long, extending around the block, so they decided to come back and try again. –USA Today

“People are scared,” said Drew Plotkin of Los Angeles. “There’s a lot of panic in the world and people want to be protected for the worst-case scenario.“

And thanks to California’s 10-day waiting period, worried residents – who we can only hope know how to properly handle the guns they just bought – will be without their protection for over a week.

John Gore, 39, who lined up outside the Martin B. Retting store on Saturday, told the LA Times: ‘Politicians and anti-gun people have been telling us for the longest time that we don’t need guns.

‘But right now, a lot of people are truly scared, and they can make that decision themselves.’

Anna – who had never bought a gun before – said: ‘It’s not like an active panic, more a preoccupation with making sure everyone is adequately prepared, myself and family and friends. –Daily Mail

Meanwhile, sporting goods company Omaha Outdoors says they’ve been “inundated with inquiries from out-of-state folks – many from California – asking if we can ship them a gun directly. The answer is, of course, no. Despite what politicians and many in popular media claim, you can’t buy a gun online and have it shipped to your house.”

And my friends who work at other gun stores have seen a crazy surge in gun buying too, with one noting that their one-day sales total exceeded Black Friday by 25%, and that 75% of buyers were purchasing their first gun. He said, in explanation, “People need to protect their toilet paper.” Another friend noted that the amount of brass cased 9mm they usually sell in a month was gone in the first week, and that everything else would be sold out soon too if things continued at this pace. –Omaha Outdoors

Last week we reported that worried Asians in east LA have been loading up on weaponsout of fear they’ll be targeted in COVID-19 related hate crimes. We also reported last week that the first possible coronavirus-related hate crime in America had occurred after an Asian man was stabbed numerous times, all caught on camera, on a Brooklyn, New York street.

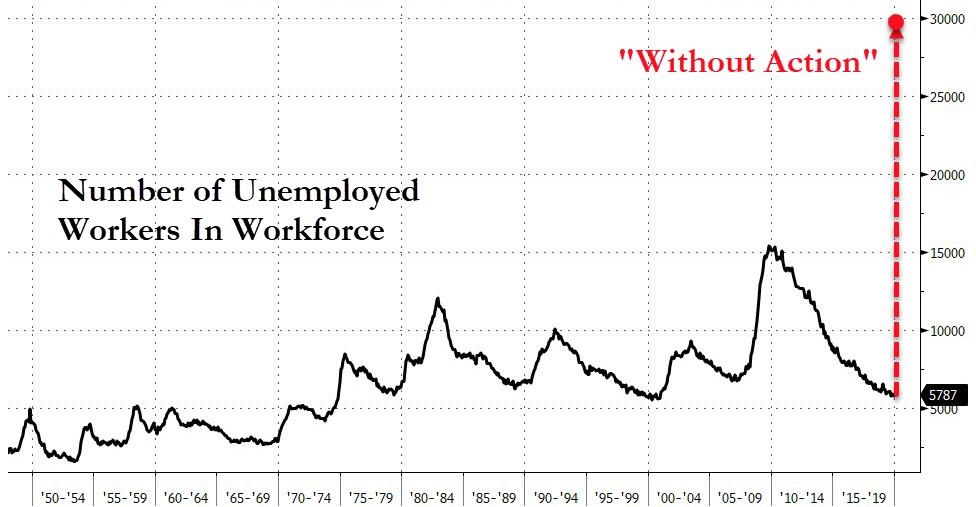

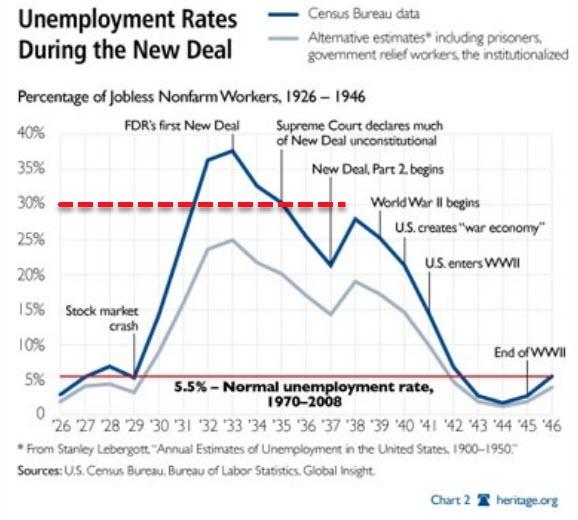

33 Million Jobs Lost: Mnuchin Tells Congress That Without Bailiouts, Depression Era Unemployment Awaits

As Treasury Secretary Steve Mnuchin pitched his trillion-dollar-plus bailout for Americans (and their companies) struggling during the Covid-19 crisis, it appears he has ripped a page right out of the TARP playbook… scare the Senators to death about the consequences of not approving the funds.

Bloomberg reports, according to sources familiar with the matter, that Mnuchin warned the Senate GOP members that without action, the US unemployment rate could spike to a stunning 20%.

With a total labor force or around 160 million, that would mean a sudden spike to over 30 million unemployed Americans

Those are depression-era levels of job losses… which prompted the New Deal and the welfare state the last time it happened…

This time – MMT, UBI, and socialized losses for everyone.

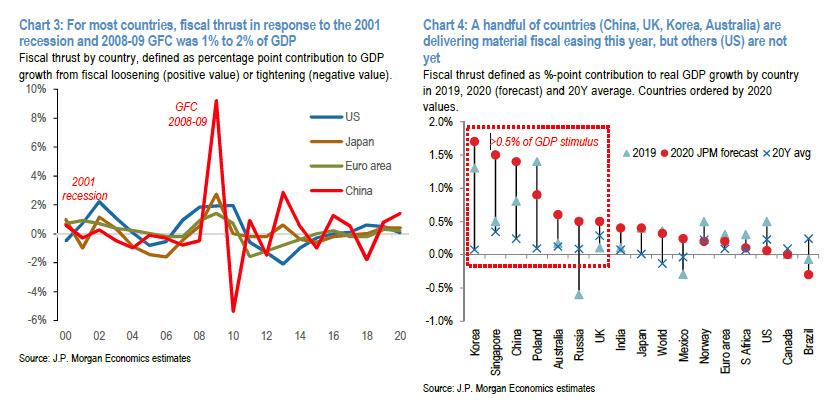

How Much Fiscal Stimulus Will Be Needed To Turn Markets?

Well before the Global Covid Crisis (or GCC) hit, investors always assumed that the next recession would require material fiscal easing to exit, especially since year after year Davos told us that central banks were out of ammo (the Fed’s actions in the past few days have seriously questions that assumption, as the real question is not whether central banks have ammo – they can always print more money – but credibility). And now that the Fed has joined the rest of the world’s central banks in the zero-rate club, announcement of significant fiscal easing seems the most likely catalyst – alongside a peak in the US/European COVID-19 infection rate – for driving a market reversal.

But how to define material? Many countries have delivered fiscal thrust of 1% to 2% of GDP during recessions, so this figure could serve as a benchmark.

Unfortunately, according to JPMorgan’s John Normand, no large country but China come close to this zone. Curiously, the notoriously stingy Europe has also been outpacing the US in terms of its suite of targeted measures such as credit guarantees, wage subsidies and tax holidays, but many of these indispensable measures are tough to quantify, so lack an announcement effect on financial markets.

Meanwhile, until Tuesday, US fiscal easing had been trivial so far, though the legislative process will likely run a few rounds. Furthermore, on Tuesday the Trump administration finally announced a $1.2 trillion stimulus plan – which seemingly was growing by $100 trillion by the hour – and which anticipates sending $1,000 checks to all Americans.

Is that enough? Judging by today’s market’s reaction which send the Dow higher by 1,000 point and bond yields surging the most in decades, traders certainly had a more favorable take on the stimulus plan, and its inflationary impact, announced today compared to the fiasco following the Fed’s Sunday emergency “bazooka” intervention, which led to a record 3,000 point drop in the Dow Jones.

As Bloomberg’s Cameron Crise put it, a putative $1.2 trillion stimulus package represents 5.5% of the U.S. economy. “To put it in context, that’s almost identical to the American Recovery and Reinvestment Act of 2009 (at least the original cost), though it’s less than the combined impact of the ARRA and a prior stimulus bill from autumn of 2008. These are big numbers, and they’re what markets want to see.”

But are they big enough? In a separate article, Bloomberg urges readers to “think of a number, then double it. That’s more or less what Wall Street is telling governments racing to draw up emergency spending plans as the coronavirus brings their economies to a sudden stop.”

Of course, the fiscal response is a process, and the final number will end up being the one that finally stabilizes the market, but the same process does bring up a question: why has policy easing – even globally-coordinated measures – in the first couple of months of a recession or financial crisis usually failed to trigger a sustained market reversal?

The answer, according to JPMorgan, is that there is always a core issue that must be resolved – usually around excess leverage, but this time around an infection’s spread. Until resolution is more advanced, markets tend to price and then maintain a risk premium for several quarters of contracting growth, falling profits, ratings downgrades and rising defaults. Monetary and fiscal easing can limit the extent to which that risk premium tightens financial conditions, aggravates the core vulnerability and turns a manageable shock into a completely unwieldly one, but easier policy rarely obviates adjustment.

Which brings up question #2: given how much pessimism is already discounted in valuations and positioning and how much rightful skepticism surrounds monetary policy, could material fiscal stimulus catalyze a turn even absent a peak in infection rates? It’s possible, especially if Wall Street is accurate in modelling what is coming as the shortest-ever recession of two quarters rather than an average one lasting at least four quarters.

But, here too, we go back to the key question: how much is enough, or said otherwise, “what number is material?”

This is where things get murky as the definition of material fiscal stimulus does not exist, per se.

As JPMorgan notes, most investors have a sense of how much monetary easing is usually required to end a US recession, since the Fed has always had to cut at least 200bp and has cut an average of about 400bp during such episodes since the 1970s. On the other hand, the appropriate amount of fiscal easing is fuzzier, because budget policy isn’t always relaxed deliberately during a recession, beyond the activation of automatic stabilizers like unemployment insurance. When fiscal policy is loosened, it usually comes sufficiently late in the recession (due to the legislative process), that it isn’t obvious how much tax cuts and/or higher spending contributed to the initial bottoming-out process in asset prices.

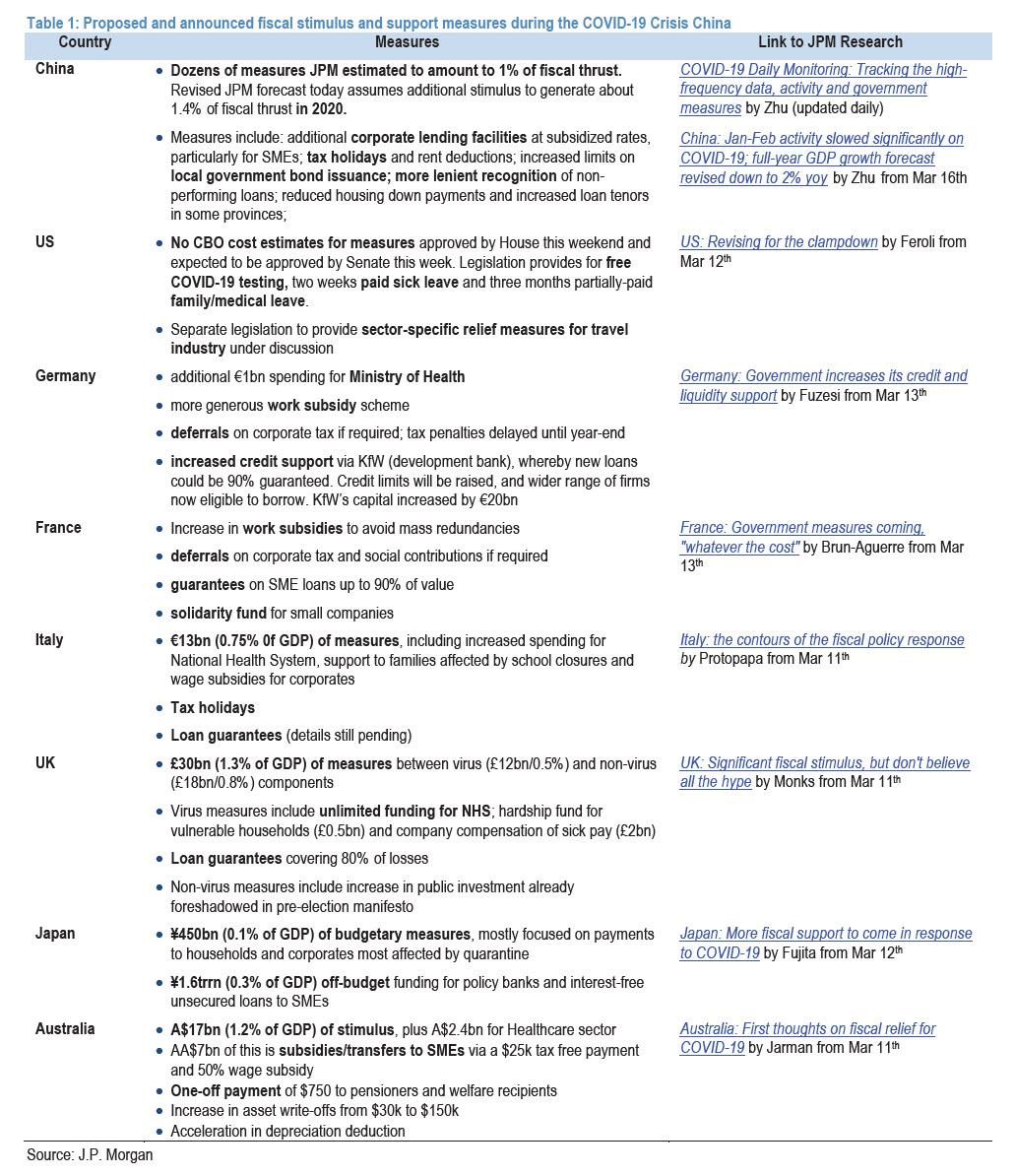

The following two charts, plus table provide a best-guess on what might register with markets as significant fiscal stimulus, and judge how close current efforts are to that threshold. The charts show JPMorgan economists’ estimate of fiscal thrust, which is the percentage point contribution to real GDP growth from fiscal loosening or tightening, over the past 20 years. That sample only covers the 2001 recession and the GFC, but highlights the following principle: Fiscal thrust in the DM economies has tended to aim for 1% to 2% of GDP during recessions, but so far, no DM government has committed to such an expansion. The closest are the UK and Australia, where our economists expected about 0.5% of thrust this year. The US has eased only trivially. The Congressional Budget Office hasn’t scored the COVID-19 relief bill that passed the House this weekend and should pass the Senate this week, but the value of free COVID-19 tests and sick leave will

European measures have been much more comprehensive than US ones, but as noted above, are tougher to translate into a notional amount of fiscal easing. As detailed in Table 1, Europe’s measures are much like China’s in terms of providing a range of targeted credit guarantees, tax holidays, wage subsides and direct payments to households. Some of these programs – like credit guarantees – are backstops rather than stimulus, and their value will only be one when they are tapped rather than ex ante on announcement. Also, funding schemes that apply to new loans would not ease investors’ concerns about the default risk around existing debt when revenue has collapsed.

There is of course the sense that this time government will do something entirely new, i.e., the much-discussed “helicopter money drop”, also known as putting MMT in practice, which would lead to a wholesale change in how government is funded as central banks become de facto branches of the government, meant to monetize debt until hyperinflation is rampant.

“Governments may need to step in to directly guarantee liquidity provision to thousands of corporates and even individuals,” said George Saravelos, Deutsche Bank’s global head of currency research, “This may literally require helicopter drops of money.”

Today’s promise by Trump to send $1,000 to all Americans is just the first step.

Fed Launches Primary Dealer Credit Facility Which Will Accept Stocks As Collateral

Earlier today, when discussing the launch of the “Lehman crisis playbook” in response to the Global Covid Crisis, we listed the alphabet soup of measures the Fed may launch which are a replica of the measures adopted in the aftermath of the Lehman collapse. These included the AMFL, the MMIFF, the TAF and last but not least, the PDCF, or Primary Dealer Credit Facility, which as Rabobank said “would provide overnight funding to primary dealers, similar to the way the discount window provides a backup source of funding for depository institutions.”

Just three hours later, at 6pm ET, the Fed, as expected, announced the establishment of a Primary Dealer Credit Facility (PDCF) “to support the credit needs of households and businesses.” What the Fed really meant is that it is now launching a way for dealers to monetize the stocks they own, as the facility will be collateralized, among others, by “equity securities.”

As the Fed announced, the PDCF “will offer overnight and term funding with maturities up to 90 days and will be available on March 20, 2020” and will be in place for at least six months and may be extended as conditions warrant.

But here is the punchline:

Credit extended to primary dealers under this facility may be collateralized by a broad range of investment grade debt securities, including commercial paper and municipal bonds, and a broad range of equity securities.

This means that as of this moment, equities – which are worth zero in a worst case scenario – are eligible collateral for Fed liquidity.

Here are some more details on the eligible collateral:

Collateral eligible for pledge under the PDCF includes all collateral eligible for pledge in open market operations (OMO); plus investment grade corporate debt securities, international agency securities, commercial paper, municipal securities, mortgage-backed securities, and asset-backed securities; plus equity securities.

That said not all equities are eligible as collateral: “the following equities would not be eligible: exchange traded funds (ETFs), unit investment trusts, mutual funds, rights and warrants”

Who will determine the value of the soon-to-be-bankrupt stocks pledged as collateral?

The pledged collateral will be valued by Bank of New York Mellon according to a schedule designed to be similar to the margin schedule for lending by the Discount Window, to the extent possible.

For those who many not remember, the PDCF was one of the biggest bailout abortions of the financial crisis, one which we discussed extensively in describing how dealers abused the Fed as they pledged totally worthless stocks for which they got “par” value. For more see:

We now look forward to Congress never asking Powell the only question that matters: how on earth are stocks “money good” securities and hard value collateral.

We also look forward to the market asking just which Primary Dealer(s) is in such dire financial straits that it now needs what is effectively a bailout from the Fed (we have a few ideas).

The 2-page term sheet of the PDCF is below (pdf link).

The lesson of it all? The lesson is that lessons are not being learned. Of course the human species has an ingrained problem: We are all born with a blank sheet and have to learn everything from scratch. It would be helpful though if the elders could pass lessons from past mistakes on to the new generation.

But no. So we keep making the same stupid mistakes.

And here we are. Just four weeks after all time highs in markets America is again turning into bailout nation.

Yes coronavirus is an unforeseen shock. So what?

We’re supposed to handle a shock. We’re supposed to be prepared. We’re supposed to have savings and great balance sheets. After an 11 year recovery and marker bull run based on cheap and easy money shouldn’t things be great and shouldn’t we be well prepared for the next downturn?

Is that really too much to ask?

Apparently.

We can’t even go 4 weeks without the Fed going apeshit on cutting rates to zero, launching $700B in QE, making discount windows available and launching $500B, even trillion dollar repos.

We can’t even go 4 weeks without the government launching a proposed $850B stimulus package, tax cuts, free money checks of $1,000 to Americans and suggesting bailouts for $BA and $GE.

That’s how fragile things are. They must be, otherwise the system would be able to handle a temporary shock.

But it can’t. Why?

Well for one our supposed great economy ever has the vast majority of Americans live paycheck to paycheck:

The consumer is doing great:

“78 percent of full-time workers said they live paycheck to paycheck, up from 75 percent last year.

Overall, 71 percent of all U.S. workers said they’re now in debt, up from 68 percent a year ago.” https://t.co/iLgLYRrPYN

That’s a systemic problem. Sure you can blame people for living beyond their means, but in general most people just don’t have the income power to keep abreast with rising medial costs, home prices and all the other fun inflationary items that the Fed simply doesn’t count as inflation. How ignorant they are. PCE deflator. Please.

And then of course the same lesson again not learned that keeps repeating ahead of every bust: Greed and more greed.

When has it ever been a good idea to chase stocks to 150% market cap to GDP or even higher?

The answer is never. Yet they convinced themselves and others that it’s different this time. New flash: It wasn’t.

A lesson not learned and yet they did it. The chart was screaming unsutainability. And here we are 4 weeks later, yesterday closing at 109.5% market cap to GDP:

Reversion to the mean. And it could eventually get much worse.

I showed this chart in Bull Cliffin February and I stated:

“Investors keep piling money into this historically priced market….Central banks can deny all they want that they are not responsible for asset price inflation, but everybody knows better. The denials are not only hollow they are straight out lies.

And having created the Pavlovian effect we now see in the investment community they are leading investors to abandon all sense of risk when risks are mounting ever more around us as valuations and earnings multiples keep expanding as a result of monetary policy. And hence it may be said that central bankers may be leading investors off the cliff.”

Well done. Did anyone listen? I can’t say, but most haven’t. And now they are all in major pain.

It was the same environment of ‘abandon all reason’ during which investors chose to chase stocks like $TSLA going vertical.

“Absolute vertical panic buying, it’s basically a reversion train wreck waiting to happen, technically speaking:”

“This behavior here is dot.com type behavior. Get me in an any price. Market cap added by the tens of billions added every day without an actual earnings story behind it yet. It’s all future projections. What I’m saying is that vertical moves like this are not sustainable and there will be reversion pain.”

Well, here we are a few weeks later:

Investors just made the same mistakes they made in the year 2000 and the same mistake they made in 2007. Chase markets to completely unrealistic valuations and now coronavirus is the most brutal of triggers. Brutal because the Fed made the excess happen with their reckless cheap money policies last year. And now the pain is deeper than it would’ve been.

And now they’re doing even more of the same desperately trying to arrest the markets collapse.

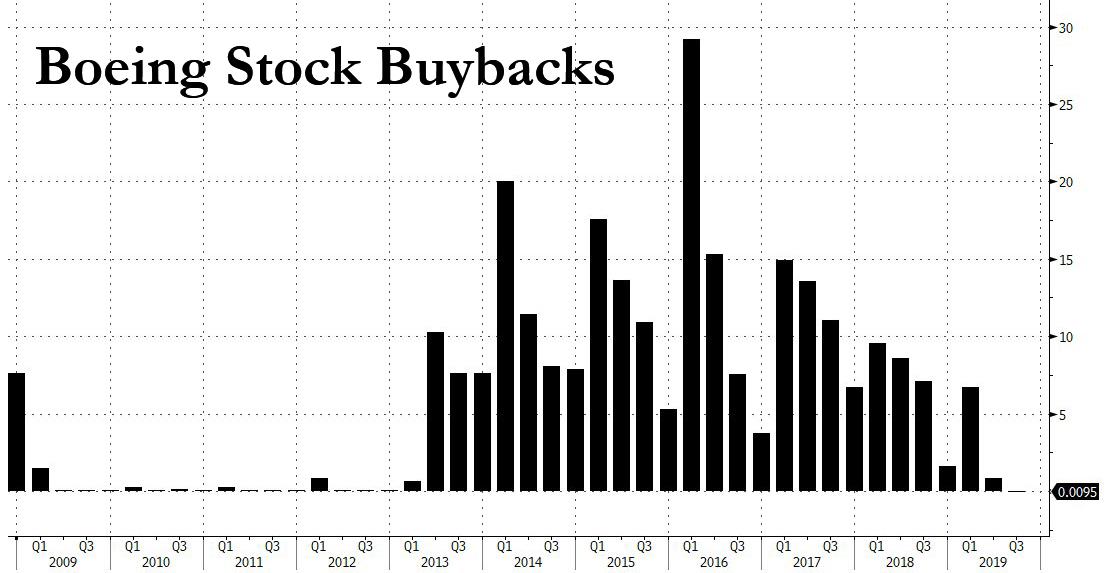

But the best part is yet to come. Let’s bailout companies such as Boeing. Does this all smell like the stench of history?

Why should we bail out Boeing? The company has been responsible for major design flaws on their planes and has taken a major hit on this for the past year. Deservedly so. After all the company was cutting cost corners left and right. Why? Because they were short on cash? No.

The company has blown nearly $45B on buybacks in the past 8 years:

Their choice. And in process they have loaded up on debt. Why should we bail out companies that are so reckless with their operations and financial management? My suggestion:

So now taxpayers will have to bail out companies that loaded themselves up with debt.

You want capitalism? Then no bailouts for companies that spent a single dime on buybacks.

Now the former party of “deficits are bad and we must get the debt under control”, already presiding over a trillion deficit before this new crisis, is pushing for an $850B stimulus package in an economy that will get hit by a massive recession.

I’m not opposed to the government stepping in to help in an emergency. That’s why we have government. What I’m opposed to is the hype, hypocrisy and excess that has preceded it. People got greedy, they piled into stocks at ungodly valuations. Companies that didn’t save or prepare for a crisis, instead were focused on short term market gains to juice up their stock prices. Companies such as Boeing that cut corners and blew money on buybacks for financial engineering purposes to enrich upper management and shareholders.

I say screw them. If you don’t learn the lessons of the past then live with the consequences. And who pays ultimately for the consequences?

And so the larger lesson that nobody wants to confront: We keep creating business cycles driven by debt and cheap money and the consequences get starker each time around because we never address the root causes. We just mask them with ever more debt and ever more cheap money and hope for the best.

And right now they will keep printing and announcing ever more measures until they get markets under control and rally again. But be sure when this is all said and done we’ll end up with $2 trillion deficits, zero rates and a massive trillion debt burden and all we have to show for is a recession.

Oh wait. We already have all that. And we’re doing all this with this being our base line just a mere 4 weeks from all time highs, 11 years into a recovery:

The lesson? We haven’t learned a damn thing. We just keep circling the same drain under the pretense that it’s all consequence free.

Well, some just got an expensive 4 week crash course lesson in market history. See if the lesson sinks in this time. I’m not holding my breath.

* * *

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

WeWork Abandons SoftBank, Pulls Part Of Rescue Package Over Federal Investigations

With the coronavirus punishing anyone and everyone with exposure to the global financial markets, companies like SoftBank, which was already reeling from last year’s unicorn massacre and the implosion of the WeWork IPO, are finding themselves in an extremely precarious position.

So who could blame them for getting a little squirrelly? Probably not Elliott Management, which now has a vested interest in the SoftBank turnaround.

With that stress in mind, hardly surprising that the company is apparently moving to pull back some $3 billion that it agreed to handover to WeWork insiders as a payoff to allow SoftBank to seize control of the office-leasing company and save it from spiraling into bankruptcy following the collapse of the IPO and JPM-led credit line tied to the offering.

According to WSJ, SoftBank has found a loophole allowing it to reneg on its agreement to purchase shares from WeWork insiders as part of the rescue package, including its agreement to buy shares from founder and former CEO Adam Neumann. Neumann had the right to sell up to $970 million in stock as part of the October deal that led to his ouster from the company’s board and from his CEO spot. The package ultimately allowed him to walk away from the company with more than $1 billion.

However, it looks like he might soon be giving back the bulk of that money in exchange for WeWork shares that probably aren’t worth the paper they’re printed on (it’s an expression).

As WSJ adds, the move doesn’t necessarily mean SoftBank is walking away – the decision could be intended to exert leverage over WeWork’s new management team, which was hand-picked by SoftBank. The deal notably doesn’t affect the $5 billion SoftBank pledged as part of the turnaround effort, some $1.5 billion of which has already been “invested” (i.e. squandered) by the company.

But regardless of SoftBank’s motives, it looks like CEO Adam Neumann, who committed every financial sin imaginable, including badly overextending himself financially by borrowing against his WeWork shares to buy illiquid assets like commercial real estate, might finally be getting his comeuppance for leading the company into the ground.

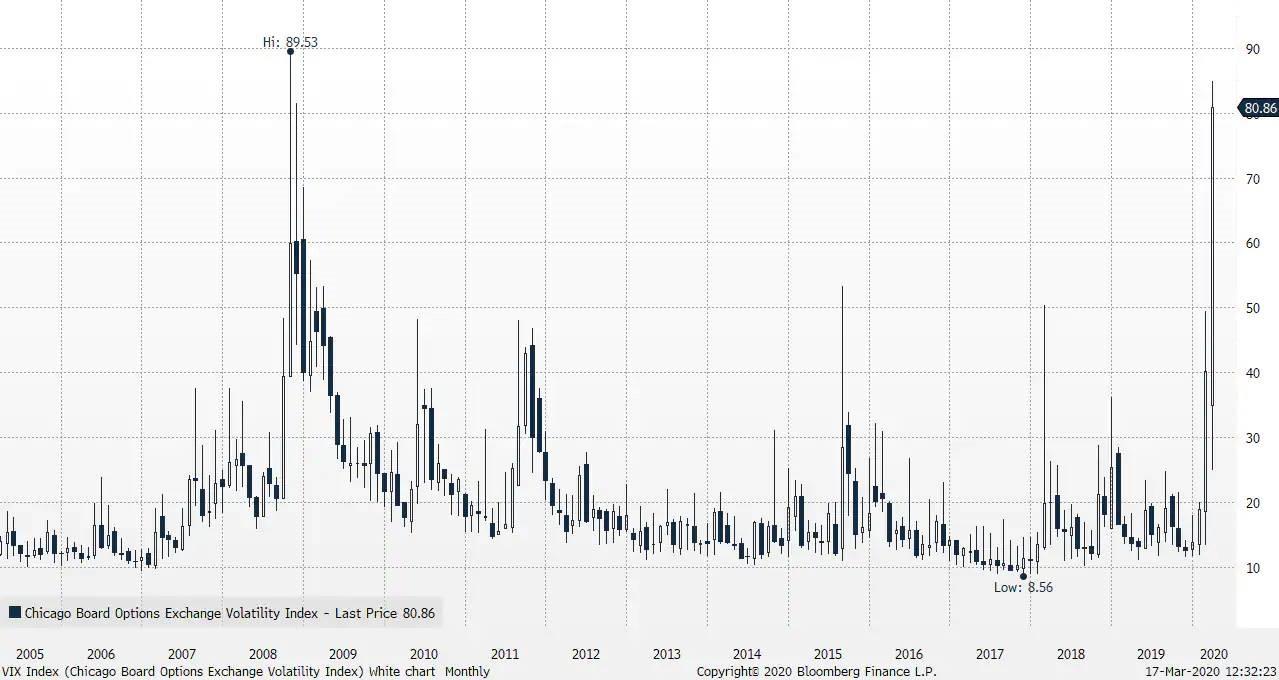

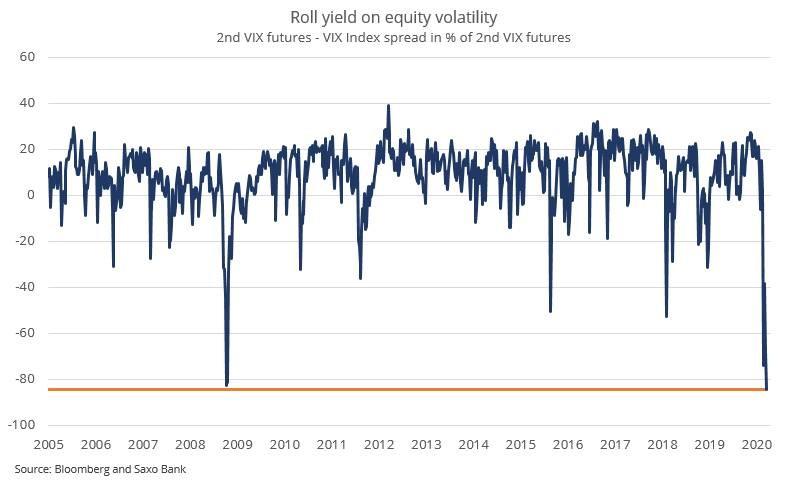

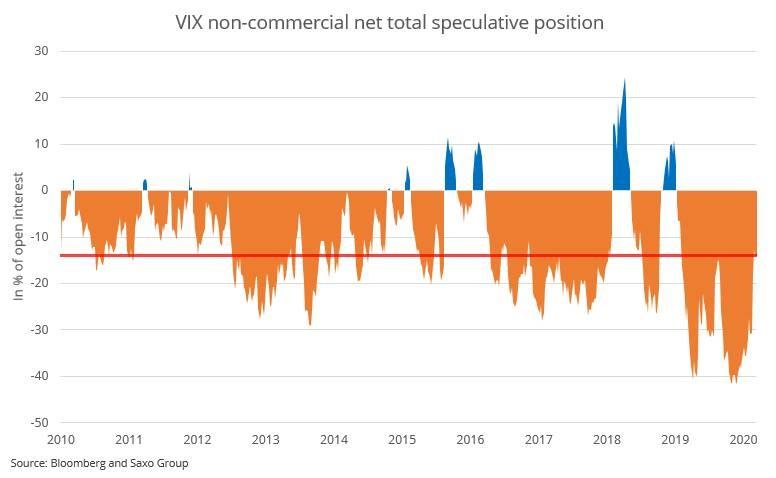

Market Bottom Indicators #1 – VIX Futures Term Structure

Submitted by Peter Garnry, Head of Equity Strategy, Saxo Bank

Summary: The current VIX level indicates significantly negative returns ahead for S&P 500 and four times the normal volatility on a daily basis. In addition the VIX futures term structure suggests that traders are rewarded for being long and that VIX is expected to be very high even in May. Speculative positions in VIX options and futures suggest that short volatility positions have been cut aggressively but that 15% of open interest is still short.

* * *

Equity option markets provide investors with valuable information about expectations for volatility and the time value embedded. The VIX Index closed at 82.69 which was a new record close surpassing closing VIX prices during the Great Financial Crisis in 2008. However, the absolute intraday peak of 89.53 in 2008 has not been surpassed yet. Historical analysis of the VIX Index suggest that VIX at these levels puts the market into a state with significant negative return expectations and realized volatility more than four times the normal level combined with extreme large kurtosis. In other words, equities are biased towards more declines from current levels.

However, hidden in the VIX futures term structure clues for when the equity market bottoms are visible. The term structure of VIX (how the price of future contracts relates to the spot) is normally in contango (upward sloping) meaning that VIX futures have a higher price than the spot. This means that the futures market is pricing on average than volatility will rise from current levels. Historically this premium to spot has been too high relative to the subsequent realized volatility and thus traders have made money by shorting the different VIX futures contracts which then rolls down creating a positive roll yield for being short volatility.

The current spread in percentage between the second futures contract (expires in May) and spot is -84.5% which is lower than during the Great Financial Crisis in 2008. This means that the expecting VIX to fall over the coming months but only to levels around 44 which would still be very high levels. The steep backwardation (downward sloping) creates a tailwind for being long volatility. The Lyxor ETF S&P 500 VIX Futures Enhanced Roll (vool:xetr) is one way to express this. When the VIX futures term structure (2nd VIX contract / VIX Index) has been higher than -10% we typically see positive equity markets. For clients that want to track this spread the VIX Index and the current 2nd month VIX futures contract have the Saxo ticker codes VIX.I and VXK0 respectively.

Another way to gauge when the market has exhausted itself is be looking at the speculative positions in VIX options and futures. We have come from the largest short volatility position ever with 40% of open interest being short, that’s yield chasers dominating volatility hedgers. The data is one week delayed but still shows that the short volatility positions have been cut massively but not to zero yet. If speculative positions move into positive then it would be another sign of equity market bottoming.

Boeing Seeks ‘Tens Of Billions’ In Bailouts After Fully Drawing-Down $13Bn Credit Line

A new disclosure on Tuesday afternoon details yet another troubling development for Boeing.

In its latest 8K, the plunging planemaker has completely drawn down its $13.8 billion credit line that it entered in October 2018 as it “navigates current business challenges” exposing just how fast this company is burning through cash.

“As of March 13, 2020, Boeing has fully drawn on the Credit Agreement, consisting of approximately $13.8 billion, which amount includes additional commitments made subsequent to the initial closing date.

For additional information on the terms and conditions of the Credit Agreement, see Boeing’s Current Report on Form 8-K dated February 6, 2020.

We continue to have access to revolving credit agreements entered into on October 30, 2019, which have also been disclosed. These facilities, which to date have not been drawn upon, provide us with additional liquidity as we navigate the current business challenges. For additional information on these credit facilities, see Boeing’s Current Report on Form 8-K dated October 30, 2019.”

This comes just hours after sources told Reuters that Boeing is seeking a bailout of ‘tens of billions’ in US government loan guarantees amid the Covid-19 crisis.

President Trump has already been on record telling airlines that his administration is prepared to pledge $50 billion in support after passenger activity has fallen off a cliff due to the virus scare.

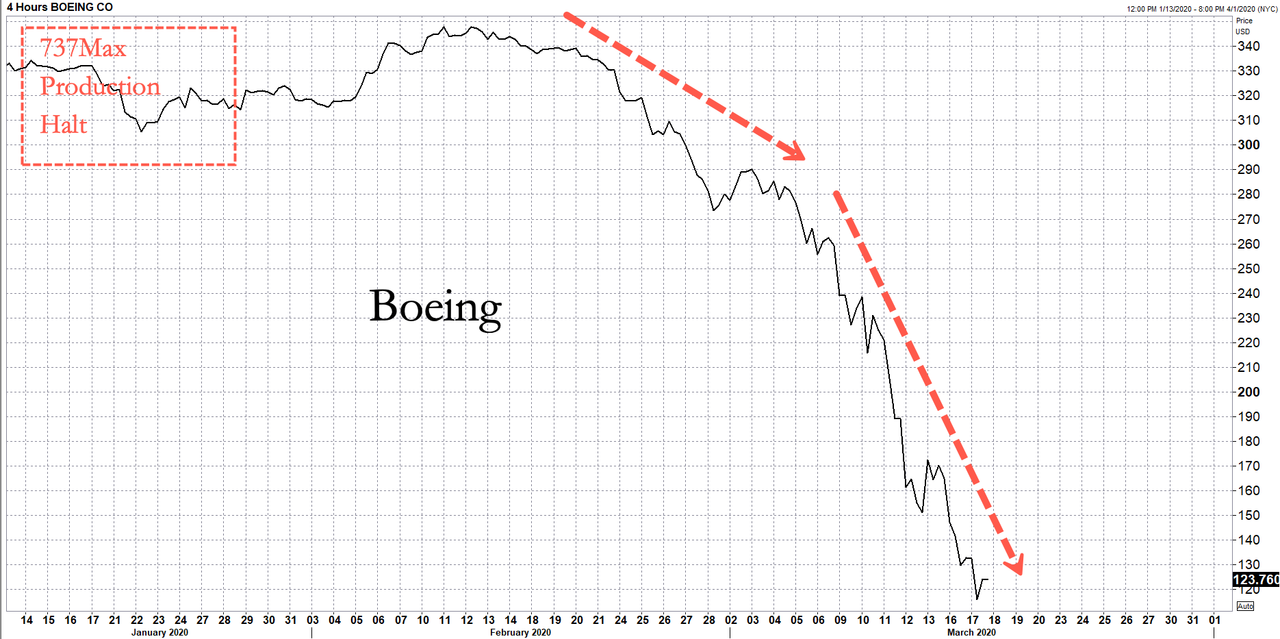

Boeing was struggling before the virus outbreak, dealing with 737 Max groundings, production halts, and cancellation orders.

Boeing shares have dropped 64% in the last 23 sessions.

As we raged previously,this bailout demand comes after the company blew nearly $100 billion on stock buybacks since 2013 helping push its stock to all-time highs not that long ago, and instead of selling stock to get liquidity, they’re asking the Trump administration for a massive bailout.

So, no, nobody in their right minds should give Boeing even one penny in “short term aid”. Instead, management and the board should be ordered to sell as much stock as they need – you know, the opposite of buying it back – to maintain the business, even it means sending the stock price crashing far lower.

Because it’s called capitalism, and because there is no reason why taxpayers should foot the bill for a company which instead of saving cash when times were good, was handing it out to shareholders and a handful of executives, and which should now for some insane reason be eligible for a bailout when times suddenly go bad.

No: force Boeing – and others like it that spent billions repurchasing its stock while incurring massive amounts of debt – to sell its stock. After all that’s what a public company’s stock is – a currency – and just as Boeing could repurchase it when it had cash, and lifted its stock price to all time highs, it should now sell its stock and use the proceeds to fund itself, like any other corporation does when it needs funding. Last time we checked, Boeing’s market cap was $73 billion, and it certainly afford to drop much more as the company now does the buyback in reverse.

This is also a warning to Congress and the White House: if chronic stock repurchasers such as Boeing, are bailed out instead of ordered to find their own sources of liquidity, there will be a mutiny in America and rightfully so, because it was Boeing’s shareholders that got rich on the way up, and now it is somehow up to taxpayers to make sure the company, loaded up with record amounts of debt used to fund buybacks, survives one more quarter.

{kind=link}

{kind=link}