WeWork Abandons SoftBank, Pulls Part Of Rescue Package Over Federal Investigations

With the coronavirus punishing anyone and everyone with exposure to the global financial markets, companies like SoftBank, which was already reeling from last year’s unicorn massacre and the implosion of the WeWork IPO, are finding themselves in an extremely precarious position.

So who could blame them for getting a little squirrelly? Probably not Elliott Management, which now has a vested interest in the SoftBank turnaround.

With that stress in mind, hardly surprising that the company is apparently moving to pull back some $3 billion that it agreed to handover to WeWork insiders as a payoff to allow SoftBank to seize control of the office-leasing company and save it from spiraling into bankruptcy following the collapse of the IPO and JPM-led credit line tied to the offering.

According to WSJ, SoftBank has found a loophole allowing it to reneg on its agreement to purchase shares from WeWork insiders as part of the rescue package, including its agreement to buy shares from founder and former CEO Adam Neumann. Neumann had the right to sell up to $970 million in stock as part of the October deal that led to his ouster from the company’s board and from his CEO spot. The package ultimately allowed him to walk away from the company with more than $1 billion.

However, it looks like he might soon be giving back the bulk of that money in exchange for WeWork shares that probably aren’t worth the paper they’re printed on (it’s an expression).

As WSJ adds, the move doesn’t necessarily mean SoftBank is walking away – the decision could be intended to exert leverage over WeWork’s new management team, which was hand-picked by SoftBank. The deal notably doesn’t affect the $5 billion SoftBank pledged as part of the turnaround effort, some $1.5 billion of which has already been “invested” (i.e. squandered) by the company.

But regardless of SoftBank’s motives, it looks like CEO Adam Neumann, who committed every financial sin imaginable, including badly overextending himself financially by borrowing against his WeWork shares to buy illiquid assets like commercial real estate, might finally be getting his comeuppance for leading the company into the ground.

Market Bottom Indicators #1 – VIX Futures Term Structure

Submitted by Peter Garnry, Head of Equity Strategy, Saxo Bank

Summary: The current VIX level indicates significantly negative returns ahead for S&P 500 and four times the normal volatility on a daily basis. In addition the VIX futures term structure suggests that traders are rewarded for being long and that VIX is expected to be very high even in May. Speculative positions in VIX options and futures suggest that short volatility positions have been cut aggressively but that 15% of open interest is still short.

* * *

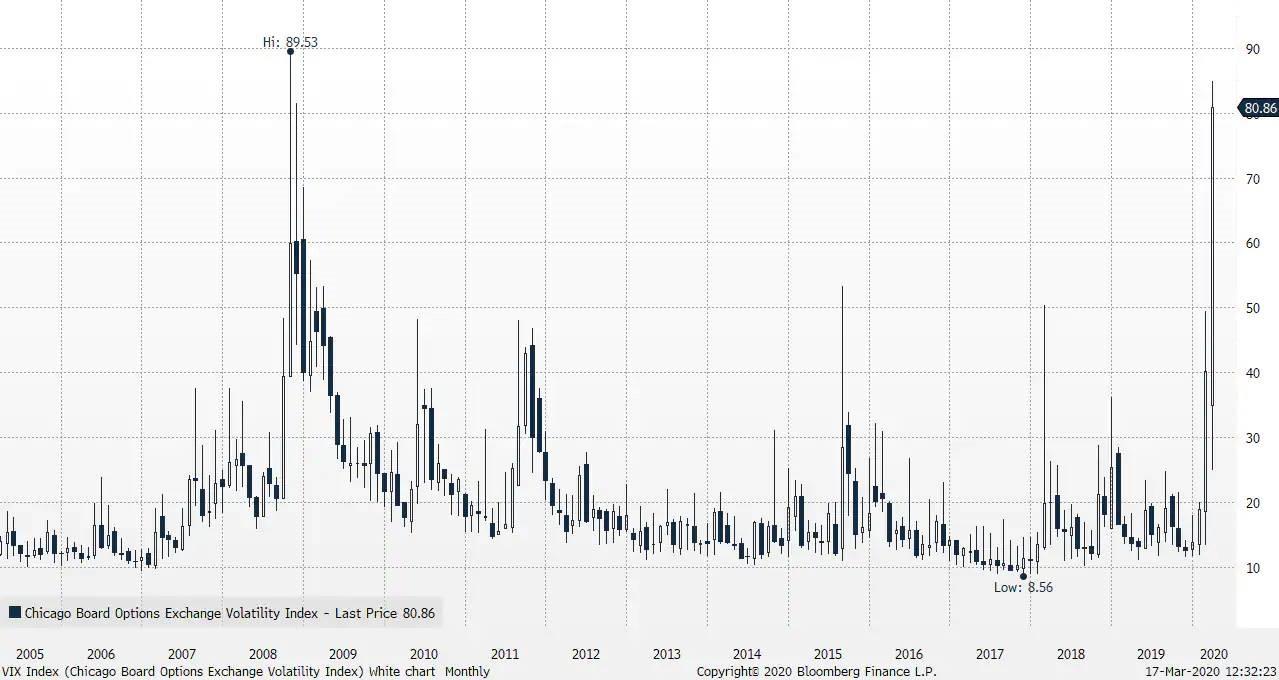

Equity option markets provide investors with valuable information about expectations for volatility and the time value embedded. The VIX Index closed at 82.69 which was a new record close surpassing closing VIX prices during the Great Financial Crisis in 2008. However, the absolute intraday peak of 89.53 in 2008 has not been surpassed yet. Historical analysis of the VIX Index suggest that VIX at these levels puts the market into a state with significant negative return expectations and realized volatility more than four times the normal level combined with extreme large kurtosis. In other words, equities are biased towards more declines from current levels.

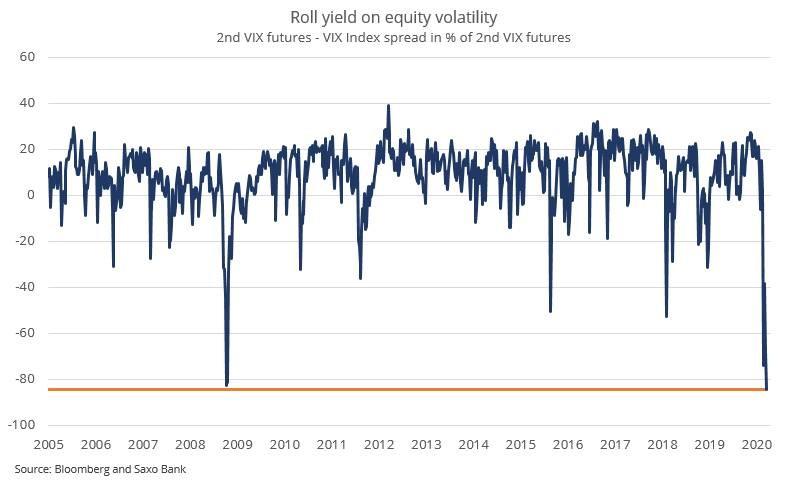

However, hidden in the VIX futures term structure clues for when the equity market bottoms are visible. The term structure of VIX (how the price of future contracts relates to the spot) is normally in contango (upward sloping) meaning that VIX futures have a higher price than the spot. This means that the futures market is pricing on average than volatility will rise from current levels. Historically this premium to spot has been too high relative to the subsequent realized volatility and thus traders have made money by shorting the different VIX futures contracts which then rolls down creating a positive roll yield for being short volatility.

The current spread in percentage between the second futures contract (expires in May) and spot is -84.5% which is lower than during the Great Financial Crisis in 2008. This means that the expecting VIX to fall over the coming months but only to levels around 44 which would still be very high levels. The steep backwardation (downward sloping) creates a tailwind for being long volatility. The Lyxor ETF S&P 500 VIX Futures Enhanced Roll (vool:xetr) is one way to express this. When the VIX futures term structure (2nd VIX contract / VIX Index) has been higher than -10% we typically see positive equity markets. For clients that want to track this spread the VIX Index and the current 2nd month VIX futures contract have the Saxo ticker codes VIX.I and VXK0 respectively.

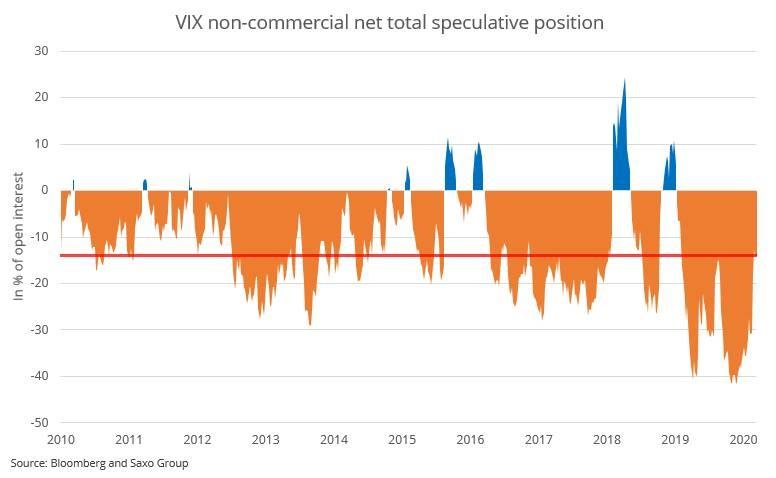

Another way to gauge when the market has exhausted itself is be looking at the speculative positions in VIX options and futures. We have come from the largest short volatility position ever with 40% of open interest being short, that’s yield chasers dominating volatility hedgers. The data is one week delayed but still shows that the short volatility positions have been cut massively but not to zero yet. If speculative positions move into positive then it would be another sign of equity market bottoming.

Boeing Seeks ‘Tens Of Billions’ In Bailouts After Fully Drawing-Down $13Bn Credit Line

A new disclosure on Tuesday afternoon details yet another troubling development for Boeing.

In its latest 8K, the plunging planemaker has completely drawn down its $13.8 billion credit line that it entered in October 2018 as it “navigates current business challenges” exposing just how fast this company is burning through cash.

“As of March 13, 2020, Boeing has fully drawn on the Credit Agreement, consisting of approximately $13.8 billion, which amount includes additional commitments made subsequent to the initial closing date.

For additional information on the terms and conditions of the Credit Agreement, see Boeing’s Current Report on Form 8-K dated February 6, 2020.

We continue to have access to revolving credit agreements entered into on October 30, 2019, which have also been disclosed. These facilities, which to date have not been drawn upon, provide us with additional liquidity as we navigate the current business challenges. For additional information on these credit facilities, see Boeing’s Current Report on Form 8-K dated October 30, 2019.”

This comes just hours after sources told Reuters that Boeing is seeking a bailout of ‘tens of billions’ in US government loan guarantees amid the Covid-19 crisis.

President Trump has already been on record telling airlines that his administration is prepared to pledge $50 billion in support after passenger activity has fallen off a cliff due to the virus scare.

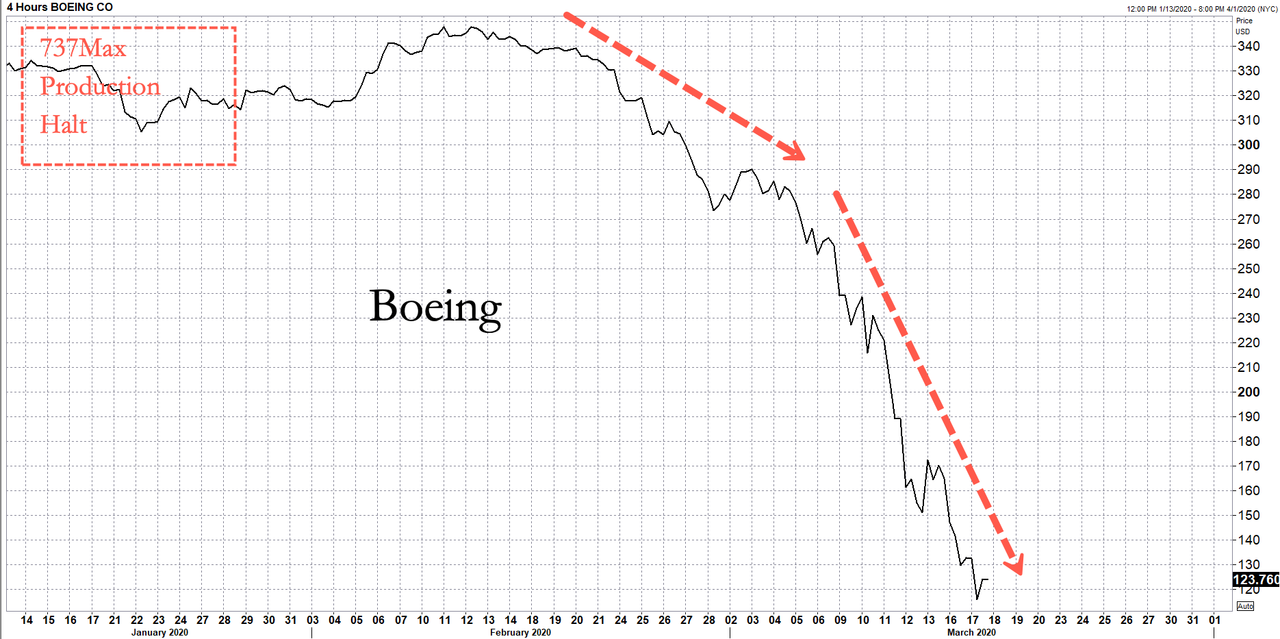

Boeing was struggling before the virus outbreak, dealing with 737 Max groundings, production halts, and cancellation orders.

Boeing shares have dropped 64% in the last 23 sessions.

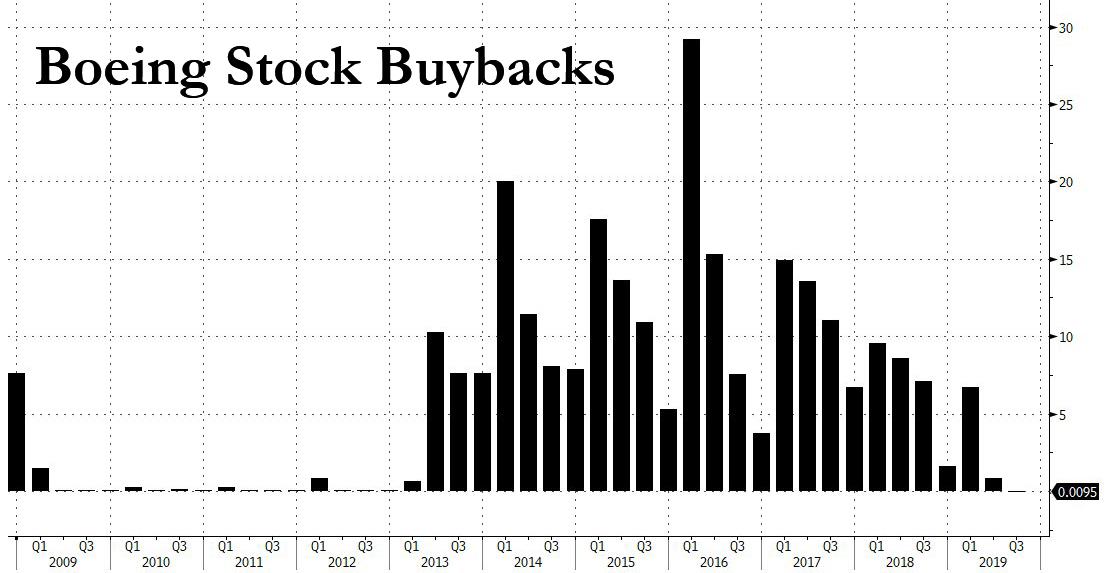

As we raged previously,this bailout demand comes after the company blew nearly $100 billion on stock buybacks since 2013 helping push its stock to all-time highs not that long ago, and instead of selling stock to get liquidity, they’re asking the Trump administration for a massive bailout.

So, no, nobody in their right minds should give Boeing even one penny in “short term aid”. Instead, management and the board should be ordered to sell as much stock as they need – you know, the opposite of buying it back – to maintain the business, even it means sending the stock price crashing far lower.

Because it’s called capitalism, and because there is no reason why taxpayers should foot the bill for a company which instead of saving cash when times were good, was handing it out to shareholders and a handful of executives, and which should now for some insane reason be eligible for a bailout when times suddenly go bad.

No: force Boeing – and others like it that spent billions repurchasing its stock while incurring massive amounts of debt – to sell its stock. After all that’s what a public company’s stock is – a currency – and just as Boeing could repurchase it when it had cash, and lifted its stock price to all time highs, it should now sell its stock and use the proceeds to fund itself, like any other corporation does when it needs funding. Last time we checked, Boeing’s market cap was $73 billion, and it certainly afford to drop much more as the company now does the buyback in reverse.

This is also a warning to Congress and the White House: if chronic stock repurchasers such as Boeing, are bailed out instead of ordered to find their own sources of liquidity, there will be a mutiny in America and rightfully so, because it was Boeing’s shareholders that got rich on the way up, and now it is somehow up to taxpayers to make sure the company, loaded up with record amounts of debt used to fund buybacks, survives one more quarter.

As schools are being closed in my state for the next several weeks, an article published in a local paper this morning stated: “With testing options now expanding, [the state] expects the number of positive cases to increase.”

Even the Orwellian Media is now making the case for shuttering the economywhile, at the same time, Orange Man bad:

Does President Trump have the guts? His initial response to the virus was to underplay it and insist it would be gone before long. He was wrong about that. He has a chance now to rectify that with bold action. Like all leaders who find themselves managing a crisis, Trump is going to infuriate somebody, whether it’s those who think he’s doing too little or those who insist he’s doing too much. He has a short window of time to act before the only possible answer is that he’s doing too little.

In many ways, the daily details are fast-becoming deck chairs on the Titanic. In the terminology of Strauss and Howe’s “Fourth Turning”:

If the 2008 financial crisis marked the Catalyst for this current Fourth Turning and Trump marked the Regeneracy phase, then it appears COVID-19 may be the Climax.

The authors Strauss and Howe defined the Climax as “the death of the old order and birth of the new“.

Indeed, the global reaction to Coronavirus is shaping up to be a watershed societal sea change – similar to 911. A TEOTWAWKI event whereby very little may ever be the same afterward.

The next five years are going to be like skiing down a mountain in a blizzard during an avalanche. Or, in other words, it will be hard to see what’s just ahead and tricky trying not to fall and get buried while navigating a slippery slope.

COVID-19 should have been named Controlavirus. Seriously, isn’t it ironic that “corona” translates to“crown”? Perhaps unsurprisingly, therefore, an Illinois mayor has granted herself the power to ban gun sales and alcohol during the epidemic:

Among the sweeping powers she [Champaign, Illinois mayor Deborah Frank Feinen] gained after signing the executive order was the ability to ban the sale of guns, ammunition, alcohol and gasoline – as well as the power to cut off access to individuals’ gas, water or electricity, according to the Washington Examiner.

The city can also “take possession of private property” and order the temporary closing of all liquor stores and bars.

Paradoxically, the reaction to COVID-19® is about weaponizing the love and civility of the citizenry. In order to protect the most vulnerable, the public will self-regulate.

Coronavirus really has become the new Terrorism. Why? Because it’s time.

It’s surreal how stores are being cleaned out, even in states with very few cases. It was going to happen eventually… but over this? Who knew?

The virus has penetrated the space between folks, even if only in their imaginations – which, in many ways, is worse than the literal virus. Everyone is now suspect. Mission accomplished.

“There [were] certainly some missteps in the beginning regarding getting tests our — some technical issues that slowed down the process, but now the [Food and Drug Administration] and [Centers for Disease Control and Prevention] are working together to get test kits out,” Fauci said when asked about concerns that the Trump administration will not reach its goal of sending 1 million COVID-19 tests as soon as possible.

Seriously, this from a guy who has been the Chief of the Laboratory of Immunoregulation since 1980 and the Director of the National Institute of Allergy and Infectious Diseases (NIAID) since 1984.

…the two most prevalent US testing methods are: antibody, and PCR.

Antibody tests are notorious for cross-reactions. This means factors in no way relevant to a given virus can make the test read positive. In that case, the patient would be falsely told he “has the coronavirus.” But it gets worse. Traditionally, antibody tests reading positive were taken as a good sign for the patient: his immune system had contacted a germ and defeated it. Then, starting in 1984, the science was turned upside down: a positive test was, astoundingly, taken to mean the patient was ill or would soon become ill.

The PCR test (which requires excellent technicians who will not make any number of possible mistakes) takes a tissue sample from a patient which might contain a tiny virus particle(s) much too small to be observed—and blows it up many times, so it can be seen. However, the test says nothing reliable about HOW MUCH virus is in the patient’s body. Why is that important? Because millions and millions of replicating virus in the body are necessary to even begin talking about actual illness. A positive PCR test, nevertheless, will be taken to mean the patient “has the epidemic disease.” —An even deeper issue: where is the PRIOR PROOF that the PCR is testing for a virus that actually causes disease?

The prospect of these two tests being done on Americans is not comforting, to say the least. People will be roped into believing they are “epidemic cases,” and therefore need to be isolated, and treated with highly toxic antiviral drugs.

In the event they become ill, from the drugs, they’ll be told “the coronavirus is doing the damage.” In some cases, this will result in even further dosing with the same drugs, at higher levels—a disaster…

Another consideration: How could any COVID-19 stats be accurate if they only reflect those who’ve tested positive? In other words, the data depends solely upon the number of test kits available. And it appears that more and more are coming; which, in turn, will surely result in more “positives”.

What I also find disturbing regarding the current COVID-19 hysteria is the advent of the newly-coined terminology such as “community spread” –which essentially means they don’t know how the patient got the virus. Or did they? And “flattening the curve” so as to justify people self-quarantining themselves, until the government says it’s safe to leave the house again.

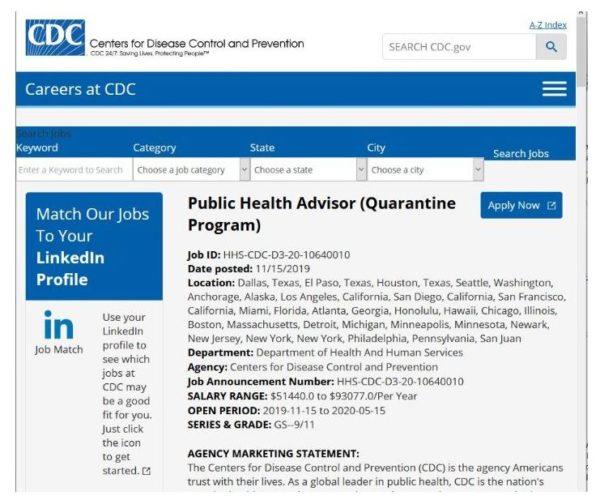

Yes, the exact same government that funds the Centers for Disease Control (CDC) – an organization that has posted a “help-wanted” ad* to fill the following position(s) during the exact COVID-19 window:

(*credit to Hardscrabble Farmer for finding & posting)

That CDC ad was posted on 11-15-2019, or nearly two weeks after both the simultaneously occurringEVENT 201 Exercise in New York City and the Military World Games in Wuhan, China. And the large geographical area, and open enrollment dates, in the CDC ad indicates a broad initiative at exactly the right time.

Conspiracy or coincidence? You’re probably right.

As this article was being typed, churches and schools in my area have been closed and many grocery stores currently contain empty shelves. Certainly, the strange surrealness of the reaction to COVID-19 will exponentially compound; just as a “house of cards” provides an apt visual analogy of supply-chain vulnerability.

Cue the theme song from the movie “Jaws”.

And do you remember in my 2nd Coronavirus article (item # 4) how I discussed the first case of COVID-19 that the Orwellian Media claimed was from an “unknown origin”? They said it had occurred in Sonoma County California but downplayed the fact it was the same county where the Diamond Princess passengers were quarantined at Travis Air Force base.

So… why did the press claim the origin was “unknown”? It’s because they want panic. They are complicit.

Former U.S. Presidential Candidate Ron Paul really nailed it with his March 16, 2020 article entitled “The Coronavirus Hoax”:

Governments love crises because when the people are fearful they are more willing to give up freedoms for promises that the government will take care of them. After 9/11, for example, Americans accepted the near-total destruction of their civil liberties in the PATRIOT Act’s hollow promises of security.

It is ironic to see the same Democrats who tried to impeach President Trump last month for abuse of power demanding that the Administration grab more power and authority in the name of fighting a virus that thus far has killed less than 100 Americans.

Declaring a pandemic emergency on Friday, President Trump now claims the power to quarantine individuals suspected of being infected by the virus and, as Politico writes, “stop and seize any plane, train or automobile to stymie the spread of contagious disease.” He can even call out the military to cordon off a US city or state.

…

The chief fearmonger of the Trump Administration is without a doubt Anthony Fauci, head of the National Institute of Allergy and Infectious Diseases at the National Institutes of Health. Fauci is all over the media, serving up outright falsehoods to stir up even more panic….

…If anything, what people like Fauci and the other fearmongers are demanding will likely make the disease worse. The martial law they dream about will leave people hunkered down inside their homes instead of going outdoors or to the beach where the sunshine and fresh air would help boost immunity. The panic produced by these fearmongers is likely helping spread the disease, as massive crowds rush into Walmart and Costco for that last roll of toilet paper.

…

When the “threat” is over, however, they never give us our freedoms back.

Coronavirus may be the new Terrorism, but it doesn’t mean it’s not real. It’s real because it’s happening.

I know some college students who drove to Florida for Spring Break. They said the bars have been closed and, now, The Controllers are warning of closing the beaches too. The beaches… the salt-water and sunlight… which are probably the most toxic environment for COVID-19 imaginable.

Elizabeth Warren Lays Out The 8 Conditions For A Federal Bailout

Surprise!

While the Trump administration are seemingly working hard to gain consensus in providing money to firms particularly hard hit by the virus – whether they deserve it or not, and picking winners and losers aside – Senator Elizabeth Warren could not help but interject herself into the process with some epic virtue-signaling…

These are the eight conditions she demands for any federal bailout cash to be released…

1. Companies must maintain their payrolls and use funds to keep people working or on payroll.

2. Companies must provide a $15 minimum wage as quickly as practicable but no later than one year of the national emergency declaration ending.

3. Companies are permanently prohibited from engaging in share repurchases.

4. Companies are prohibited from paying out dividends or executive bonuses while they are receiving any relief and for three years thereafter.

5. Companies must set aside at least one seat — but potentially two or more, as the amount of relief increases — on the board of directors for representatives elected by workers.

6. Collective bargaining agreements should remain in place and should not be reopened or renegotiated pursuant to this relief program.

7. Corporations must obtain shareholder and board approval for all political expenditures.

8. CEOs must be required to personally certify a company is compliance and face criminal penalties for violating these certifications.

So… no layoffs, no buybacks, no bonuses, high minimum wage, and union representation on board?

If these rules are to be take effect (which they won’t):

1) no cash is going out anytime soon… and

2) if they do, their business viability would be in question.

But hey, what does that matter – she has signaled the tiny percentage of Americans that voted for her during the Primaries that she is right there beside them fighting the good fight – except she isn’t because they are all getting laid off due to the virus and she is a millionaire.

To contain the economic and financial ramifications of the coronavirus pandemic, Central Banks are going all in.

Jim Bianco, founder and chief strategist of Bianco Research, warns that this time, monetary policy might be unable to stop financial markets from collapsing.

The Federal Reserve brings out the bazooka: It cuts the federal funds rate down to zero and will buy $700 billion in Treasuries and mortgage-backed securities. Additionally, in a coordinated effort with five other major central banks, including the Swiss National Bank, the Fed opens swap lines to smooth out disruptions in overseas Dollar markets.

Still, financial markets seem unimpressed. Futures contracts on the S&P 500 dropped 5%, reaching a «limit down», while stock markets in Asia and Europe started the week with heavy losses.

For Jim Bianco, these actions are the Fed’s last stand:

«This is one of the biggest moments of truth in financial market history. Will last week’s low in risk markets hold? If not, a new era in financial markets may be upon us», says the internationally renowned macro strategist from Chicago.

In an in-depth conversation with The Market/NZZ, he explains why Central Banks are going all in, what happens if risk assets drop further and why closing financial markets may be the only option left.

Mr. Bianco, the Federal Reserve takes massive emergency actions. What does this mean for financial markets?

The Central Banks went all in. They fired all of their ammunition and they’ve got only one goal in mind: They have to stop the decline in financial markets. This started late last week with the Fed’s giant repo operation. You can also throw in the announcements of the ECB and the Bank of Japan. Plus, we have the extraordinary actions taken by European governments to stem the effects of the pandemic. The government of Germany for instance is basically guaranteeing everybody’s job.

However, investors don’t seem convinced. What’s going to happen if markets drop further?

Central Banks need to stop the stock market from falling through last week’s low. I believe if markets fall through those levels and keep going down, the so-called Fed Put is dead. It doesn’t work anymore, so quit trying to find new ways to exercise it. Just understand Einstein’s definition of insanity: Doing the same thing over and over again, and expecting different results.

What are the ramifications if the Fed Put doesn’t work anymore?

Central Banks will need to move on. So if stocks make new lows we’re at a real risk of financial markets being closed. The Fed and other Central Banks have fired all their ammunition and if markets crash through last week’s lows, there’s nothing left. The Fed can’t buy equities outright without a change of the Federal Reserve Act. It would take weeks for Congress to do that. Even if Congress moves with lightning speed it will take them at least a week, and it will be over before that.

What would be the benefit of closing markets?

It took the stock market sixteen trading days to drop by 27% from the all-time highs to Thursday’s lows. We have never seen anything close to that in history. The closest we’ve ever been in history was 1929, when it took 42 days to get from the all-time highs to a 20% correction. The speed in this decline is unprecedented.

Why is it so important to stop this crash?

If it continues, you will get margin calls, involuntary liquidation. Markets will lose their ability to price securities, especially things like high yield bonds and emerging markets securities. Funds in those areas will be unavailable for people to redeem because they won’t have any prices. There will be trapped money. Also, you will get broken covenants in the corporate debt area, and that will force changes of control or restructurings. But the biggest damage will be that pensions will become underfunded. Companies will be forced to pony up billions of Dollars to get their pensions back into funding.

And how would it help if markets were closed?

At this point, we’ve shut down everything else to fight this pandemic. There’s basically nothing else open right now. So why not close financial markets until we get a better handle at the extent of the damage? And then, we can reopen them and look at the possibility of proper pricing.

In the history of the United States, regulators closed the stock market only four times: 1914 when World War I started, during the bank holiday of 1933, after the Kennedy assassination in 1963 and after 9/11 in 2001.

There is still a possibility that what is happening now might work and we can hold the lows from last week. Then closing markets won’t be necessary. But I think Central Banks are thinking exactly the way I am. Their actions are saying: «We have to stop this now. There is no more time to debate, we are all in with everything now. If it doesn’t work now, we don’t care that we’re out of interest rates cuts, and we don’t care that we’ve already blown up the balance sheet.»

So did the Fed the right thing?

I’m going to give Central Banks an «A+» rating in what they have done so far in this crisis. If I was the Fed Chairman this is what I would do. But it looks like it might not work. So I can’t give Jay Powell an «F» because there’s nothing more he could have done than what he has already done. The Fed did the right thing, but in this environment, doing the right thing does not mean it will work. So that leaves one tool left should risk markets continue to fall through last week’s low: Close financial markets before they collapse.

There were also some issues with the Treasury market last week. What’s going on there?

The Treasury market became very dysfunctional in the second half of last week. It looked like all markets were being liquidated: You had stocks declining, bonds declining, commodities declining, gold declining, and you even had a US Dollar shortage since everybody was running into the Dollar. Everything was being liquidated. So the Fed, recognizing this problem, stepped in on Thursday afternoon with the announcement of $5 trillion of repo operations over the next month. On Friday alone, they offered $1 trillion in repo. To put that into perspective: We are talking about the size of QE1 – that was the first quantitative easing program in 2009 – done in one hour.

Yet markets still tanked on Friday initially.

Only $42 billion of the $1 trillion the Fed offered was taken. That’s because there is a myriad of regulations on banks that don’t allow them to leverage their balance sheets because that was the problem in 2008. So the banks can’t take the money that is offered by the Fed because of regulations. That’s why the Fed is engaging in quantitative easing now.

There are rumors about a large hedge fund or another big entity blowing up.

Yes, there are already stories of gigantic losses in the hedge fund community. BlueCrest, H2O, and Bridgewater have all lost around 20%. With market dislocations like this, no wonder there are rumors that somebody is in trouble. Let me tell you, if markets take out the lows of last week and keep going down, then we can start the rumor of who’s still solvent. That’s why they will have to close the markets.

Investment banks like Goldman Sachs predict that U.S. GDP will shrink 5% in Q2. Is this a realistic assumption?

I fear this might look optimistic in a few weeks. Yes, this pandemic-driven economic collapse will be temporary, one or two quarters, but the risk is very real that long-lasting damage is being done that will hamper the economy for years.

You’re been in the investment business for a long time and have seen quite a few crashes. How do you experience this crisis personally?

This is unlike anything we’ve seen in our lifetime. What’s going on in financial markets today exceeds the financial crisis of 2008, it exceeds 9/11, it exceeds the tech peak, and it exceeds the 1987 crash. Maybe 1929 is still bigger, but few of us were alive then. We’re writing a new chapter for American and world history textbooks. We’re only a few pages into it, and we’re not sure how it will end, but our grandchildren will one day learn school about the great pandemic of 2020 and what it meant for world history.

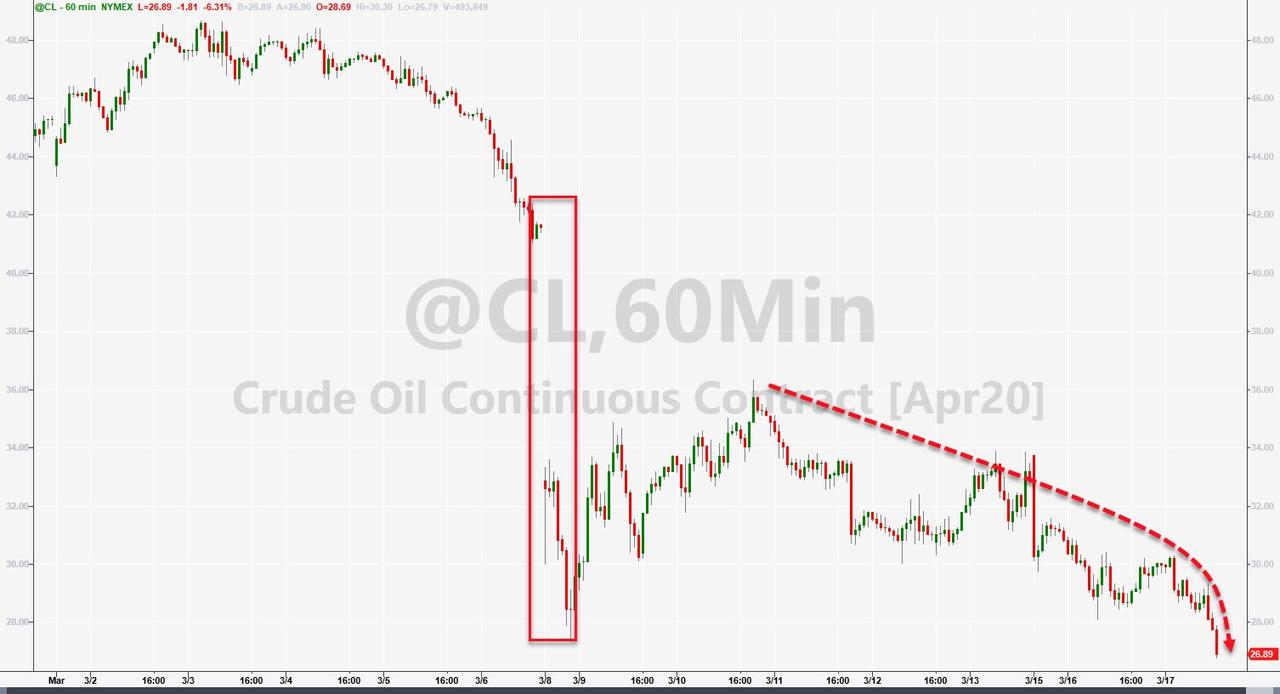

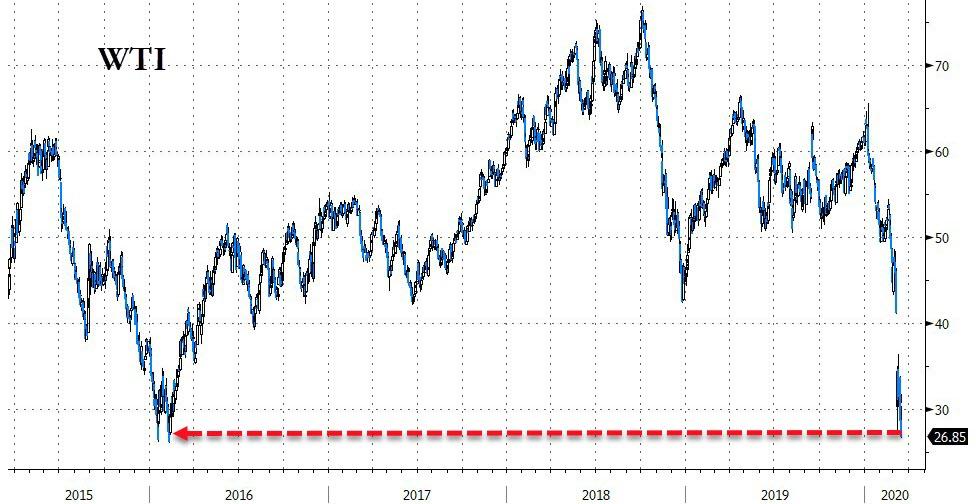

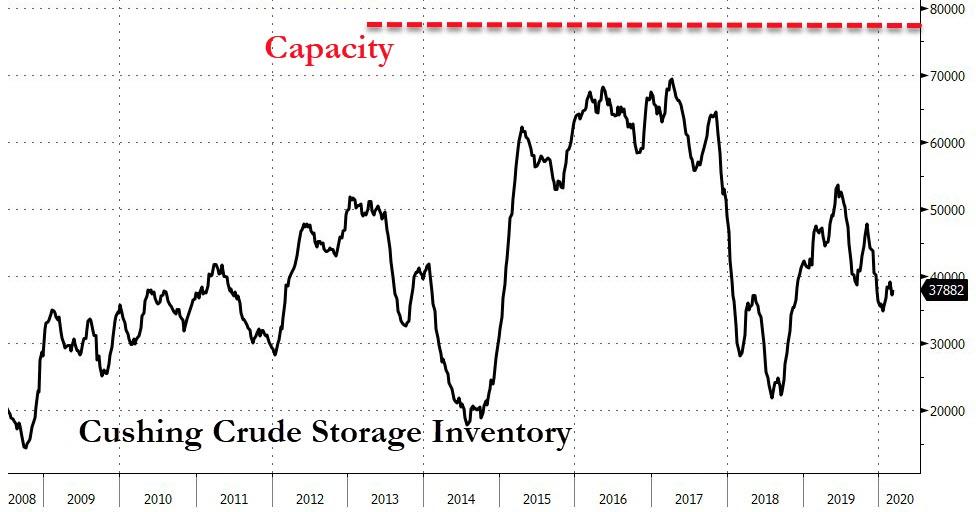

WTI Hovers At 4-Year Lows After Surprise Inventory Draw, One Bank Expects Negative Oil Prices

Oil prices plunge today with WTI back to a $26 handle, the lowest level since 2016, as the coronavirus pandemic threatens to bring the global economy to a standstill, battering fuel demand at a time when crude supply is surging.

“These are dramatic and unheard-of disruptions,” said Pavel Molchanov, energy research analyst at Raymond James & Associates Inc.

“Lockdowns around the world alone would be enough to trigger a bear market for oil. Add in the collapse of OPEC+, those two create an unbelievably toxic combination. This crisis is shaping up to be the worst shock to global demand in modern history.”

So all eyes are once again on inventories to see if the virus effects are beginning to be evident in the data…

API

Crude -421k (+3.1mm exp)

Cushing +66k

Gasoline -7.8mm (-2.4mm exp)

Distillates -3.6mm (-2.3mm exp)

After a seven week run of builds, API reports a surprise crude inventory draw last week and huge product draws…

Source: Bloomberg

WTI was trading around $26.90 ahead of the API print…

And barely budged on the surprise draw…

The supply and demand shocks have dimmed Wall Street’s outlook for oil.

Just this morning, Goldman lowered its Brent forecast from $30 to $20, as the oil market will have to contend with a record surplus driven by a peak c.8 million b/d decline in oil demand and a peak c.3 million b/d rise in oil supplies in the coming months.

While we do not expect this to lead to a breach in storage capacity which still has over 1 billion barrels, it will likely lead to a breach in logistical capacity, meaning ships, pipelines, terminals and processing units. As the market hits these constraints spot prices are likely to separate from forward prices (as the cash-and-carry arb will cease to exist) plunging to levels to force production shut-ins, as more excess crude will simply not be able to be delivered into the system.

As it becomes increasingly clear that Saudi Arabia is likely to maintain output near 12.0 million b/d during 2Q20, we are now shifting to our downside scenario of $20/bbl which is consistent with the market breaching cash costs. There are questions recently around whether Saudi Arabia can maintain 12.0 million b/d during 2Q20 and raise capacity to 13.0 million b/d. We believe that because Saudi Aramco is now a public company and eager to pursue an international offering that the accuracy of their guidance is now extremely important.

As Goldman concludes, rather ominously, the revenge of the old economy is how we have described the underinvestment that has impacted commodity production historically, as in the late 1990s and in the current environment. The recent collapse in oil prices will only accelerate this underinvestment thesis and create supply constraints in 1-3 years that will be extremely binding, which is why we termed the current environment the revenge of the new oil order.

It is not only oil that will be impacted, but metals as well via the negative feedback loop with emerging markets, i.e. lower commodity prices hurt EM demand and drive up funding costs, which in turn drives down prices further, creating a vicious cycle.

However, Goldman are relatively bullish compared to Mizuho’s Paul Sankey wrote today in a note to clients that we may be 15m b/d oversupplied currently, and warned that crude prices could go negative as Saudi and Russian barrels enter the market.

Much of America’s 4m b/d of crude exports are likely to be curtailed as prices fall and tanker rates soar and as Sankey notes, U.S. storage is currently at ~50% capacity and can add 14m bbl/week for 10 weeks until full.

Sankey concludes, a race set up between filling storage and negative pricing “unless U.S. decline rates can outpace inventory builds, which we very much doubt.”

And lending credibility to this admittedly scary scenario, the shale industry is getting desperate…

13 GOP senators are asking Saudi Arabia to rethink its plans to boost oil production: “We urge the Kingdom to assert constructive leadership in stabilizing the world economy by calming economic anxiety in the oil and gas sector.” https://t.co/AN36F4BBSFpic.twitter.com/i3CP3aIRf2

After several consecutive quarters of missing the top and bottom line, the global logistics carrier finally had a good quarter… just as the world is grinding to a halt.

FedEx reported adjusted Q3 EPS that beat the average analyst estimate, which was great, but not so great is that the company suspended its outlook on uncertainty related to coronavirus pandemic.

Q3 adjusted EPS $1.41 vs. $3.03 y/y, estimate $1.27

Q3 adjusted operating margin 2.8% vs. 5.80% y/y, estimate 3.36%

Despite beating sharply lowered expectations, operating results declined due to weaker global economic conditions including the impact of the coronavirus, higher self-insurance accruals, an unfavorable variable incentive compensation comparison, increased FedEx Ground costs from expanded service offerings, the loss of business from a large customer, a continuing mix shift to lower-yielding services and a more competitive pricing environment

However, the big surprise – or perhaps not – in the earnings report was that FedEx was joining so many of its peers in pulling guidance as nobody has a clue anymore what the future holds: “We are suspending our fiscal 2020 earnings forecast for our consolidated and segment results due to the uncertainty caused by the coronavirus pandemic,” CFO Alan Graf said in statement

“To mitigate these near-term headwinds and position the company for future earnings growth, we are attacking costs throughout the company by managing capacity, retiring our oldest and least- efficient aircraft, integrating TNT Express, and lowering our residential delivery costs by having FedEx Ground deliver FedEx SmartPost and certain day-definite FedEx Express packages.”

As a result, while algos initially responded to the big beat sending the stock higher, they have since realized that what happened last quarter is absolutely meaningless in a world where the economy has ground to a halt, and promptly dragged the stock to unchanged.

Jeffrey Gundlach, the billionaire chief investment officer of DoubleLine Capital, is scheduled to conduct his periodic live webcast for his DoubleLine Total Return Bond Fund at 4:15 p.m. New York time. With the webcast coming in a time of markets in crisis, the theme of the webcast today is “The price is right” which this week is a laughable concept when even some of the most “liquid” ETFs saw their NAV tumble far below their stated value, when the Treasury market froze up and when stocks have traded limit up or down virtually every day.

Unlike Gundlach’s annual “Just Markets” webcast in January, the fund-specific presentation will likely narrow the otherwise whimsical scope of the Gundlach’s commentary on broader topics, such as the presidential race, the NFL and public health.

As Bloomberg reminds us, the key takeaways from Gundlach’s January “Just Markets” webcast included:

Top conviction is the dollar will weaken as foreign investors divest from U.S. assets

Commodity prices will likely rise as a consequence of the weaker dollar

Overseas equity markets are likely to outperform the U.S. indexes, which bested most of the world in 2019

Bullish on gold and Bitcoin

Bernie Sanders is the likely Democratic presidential nominee

Two months later, we doubt he will be too happy with on those predictions. Here are some early presentation highlights, courtesy of BBG:

“Lots going on in the market. It’s just incredible” — Gundlach starts off the webcast after thanking everyone for joining.

Gundlach says the webcast title of “The Price Is Right” was chosen because he couldn’t believe how markets were moving before this sell-off.

He’s pleased that unlike a lot of active bond funds, DoubleLine is doing quite well.

Stock market is in a “world of hurt.” Gundlach says he will speak about that in this webcast.

Gundlach expresses concern that Trump’s stimulus plan could be prone to abuse; and says $1 trillion is just the beginning of the fiscal stimulus. “One you start giving cash to business people, I can’t imagine the level of graft and corruption,” he says.

Gundlach then says the Fed’s rate cuts are “obviously an admission we’re not going back to anywhere normal”, and says that we will soon need a $10 trillion Y axis on the Fed balance sheet chart as a result of the latest massive monetary injection.

Gundlach said he was concerned policy makers are in a “rinse and repeat” cycle where stimulus is followed by other intervention over and over.

On the other hand, with the world entering a recession if not depression, central banks may have no other choice, even though as Gundlach notes, the latest forecast chart has a way to go…

… with the billionaire saying that “I would bet dollars to donuts” that the global economic forecasts will drop from what was projected on Feb. 28.” A big reason for this is the collapse in China’s economy, which is 16% of global GDP now…

… and which has fallen off a cliff.

Summarizing the economic situation, Gundlach pronounces that “this is the end of the longest post-war expansion.”

Which means that “we’re in a tricky environment” to trade in, which of course is an understatement.

Gundlach also looked at the spread between the effective fed funds and the 10Y, which as regular readers know well, is where recessions usually begin, and where the yield curve steepens sharply in response.

There is much more in the presentation slide deck below:

‘Helicopter Money’ Sparks Bond Backlash, Stocks Bounce On Fed Bailout, But Bank Liquidity Worsens

US futures traded limit up overnight, plunge back to the lows of the day, soared back above overnight highs, dumped again, ripped again, then slumped… 1000s of Dow points in the swings on the back of various political and monetary headlines of ever-increasing bailouts (and warnings)… that is malarkey!

So, some (brief, perhaps) exuberance in stocks.

BUT…

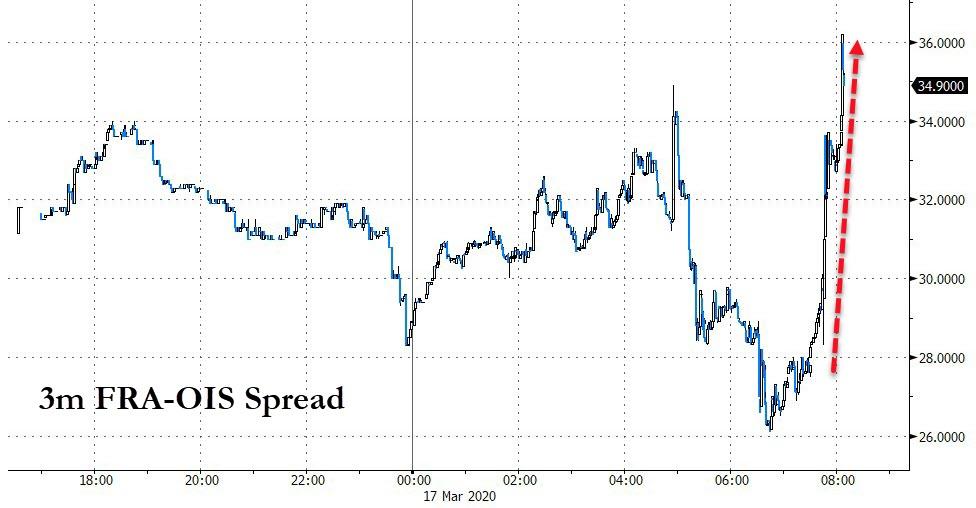

Despite The Fed’s CPFF, banking system liquidity worsened…

Source: Bloomberg

AND…

‘Helicopter Money’ sent the the 10Y Yield soaring back above 1.00% today as yields exploded 30bps higher…

Source: Bloomberg

AND…

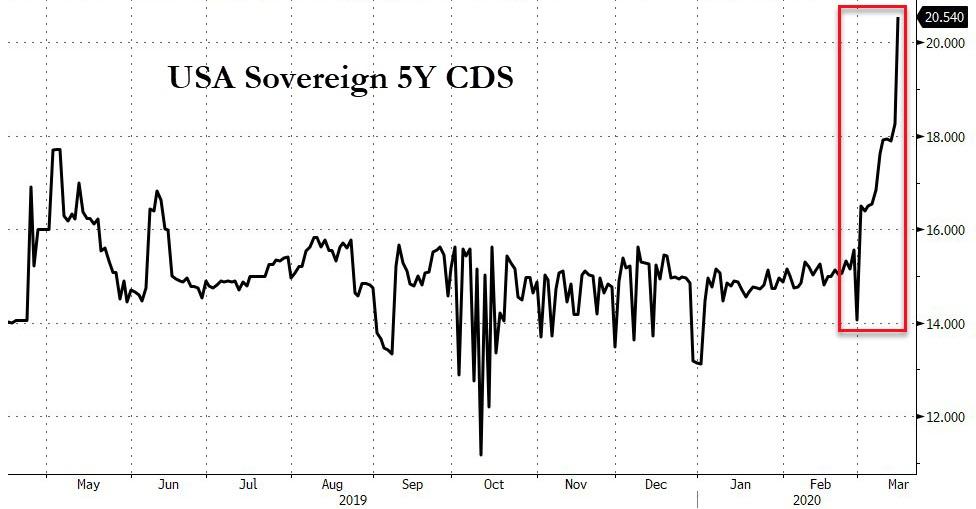

All this chatter of helicopter money has sent USA Sovereign risk is spiking…

Source: Bloomberg

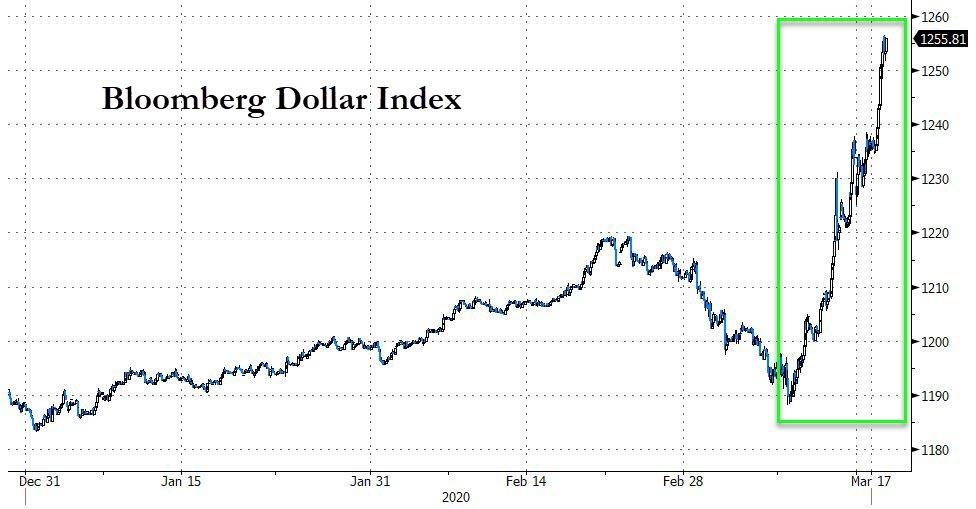

Simply put, it appears the bond market is starting to panic about MMT becoming an imminent reality – not a good sign for The Fed, The Treasury, and all Americans. And while this may lead to dollar-weakness in the endgame, for now, liquidity is all that matters and the dollar soared higher again as the financial system’s liquidity crisis showed now signs of abating. The Dollar is up 6 days in a row…

Source: Bloomberg

Today was the dollar’s biggest daily gain since the flight-to-quality after the UK’s Brexit vote in June 2016 (and the biggest 6-day gain since Lehman).

* * *

Legendary investor Jim Rogers warned that “the next time we are going to have a financial problem it’s going to be the worst…” and right now it appears we are headed toward “the worst financial crisis of our lifetimes” and “we will know in a few months.” However, Rogers noted, the reason behind such market mayhem is “not just the virus, it is certainly much more” than that.

Rather notably, the US equity market has started each day moving in the opposite direction from the previous day’s late-day move every day for two weeks…

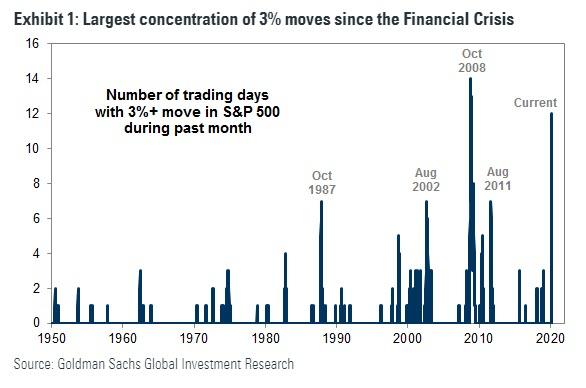

There have been 3%+ moves in the S&P 500 during 13 of the past 22 trading days, approaching the October 2008 experience.

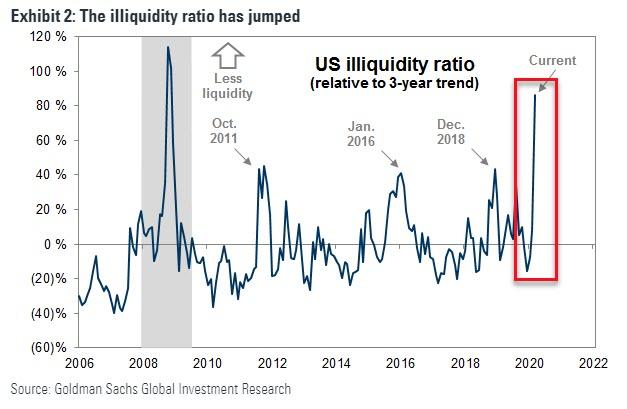

Goldman’s illiquidity ratio, which measures the price impact of trading volumes, shows that liquidity has evaporated within US equities…

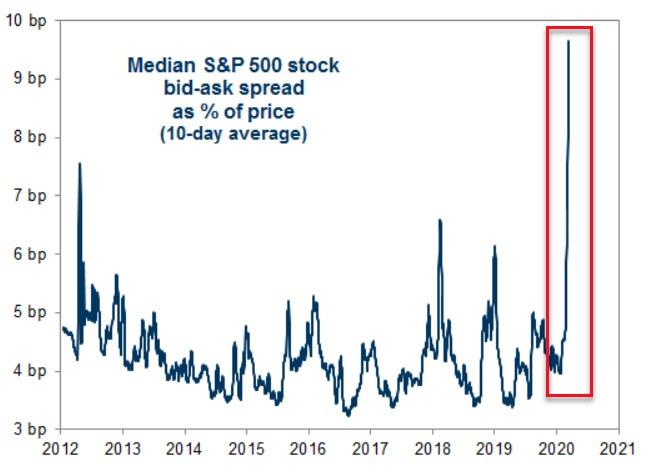

Bid-ask spreads have widened to 8-year highs…

Early in the day, stocks tumbled back into the red but ever-escalating helicopter money headlines and The Fed’s CPFF and extended Repo helped lift the market to a big day, led by Small Caps…(NOTE – the drop around 12ET came after the White House Virus Task Force stated that “we are losing the fight to contain the virus.”

Defensive and Cyclicals rallied today, but cyclicals are dominating the week…

Source: Bloomberg

For some context, this drop in stocks dwarfs the Y2K-post-Fed-liquidity plunge…

Source: Bloomberg

VIX dipped today back below 75, but remains extremely elevated…

There was a bloodbath in bondland today with yields exploding higher across the curve – long-end smashed hardest – 30Y spiked 35bps, 2Y +9bps…

Source: Bloomberg

The ETF liquidity crisis is abating as rates soar…

Source: Bloomberg

US yield curve steepened as chatter increased of the helicopter money-drop in the US…

Source: Bloomberg

This is the biggest steepening since the US downgrade in 2011…

Source: Bloomberg

In the past week, junk-bond investors have suffered through two of the worst days since the collapse of Lehman Brothers. The struggle reflects the spike in economic uncertainty and how many high-yield borrowers will have problems with bank lines. However, junk CDS spreads are pricing in a 43% five-year default probability. That’s high, but in 2009 CDS was pricing a more than 60% default probability, so it can go higher.

Source: Bloomberg

IG credit is even worse, with CDS pricing in a 9.9% default probability, which is extremely high…

Source: Bloomberg

And European sovereign credit spreads are blowing out…

Source: Bloomberg

Cryptos extended their gains today with Bitcoin almost back to even on the week…

Source: Bloomberg

Commodities were mixed today with Gold managing gains as crude and copper were crushed…

Source: Bloomberg

Silver’s continued weakness, and gold’s gains today, sent the gold/silver ratio to another new all-time record high…

Source: Bloomberg

WTI puked to a $26 handle!!

After some serious ugliness yesterday, precious metals rebounded aggressively today as helicopter money chatter hit, BUT that was quickly slapped down by the powers that be… gold and palladium higher on the day (palladium’s jump was biggest since 2001 at its highs), silver and platinum lower…

Source: Bloomberg

Finally, systemic risk continues to soar in deep, dark corners of the financial markets… Implied Correlation is at Lehman/EU Crisis levels…

Source: Bloomberg

But, we suspect this reracking has a lot further to go…