How Much Further Can Markets Fall? Here Is One Bank’s Answer

On Friday, March 6, Goldman’s chief US equity strategist, David Kostin, who bizarrely still holds held the view that the S&P will close the year at 3,200, despite now expecting an earnings recession, and Gldman economists calling for an economic recession in Q2 and a -5% GDP crash in Q2, laid out a binomial “downside case” scenario (i.e., a coin toss because as he admitted, he has no idea if the S&P would go up or go down) that saw the S&P plunging from the mid-2,900 level (where it was trading then) to 2,450 in a “coronavirus recession” case.

One week, and three-limit down sessions later, the S&P traded at 2,401.

So having been stopped out again by the market, Kostin – who realized he clearly wasn’t bearish enough to preserve client credibility – was forced to come up with even more dire downside cases, which he did over the weekend in his latest Weekly Kickstart where he said that while he still expects the S&P to magically rebound to 3,200, he admitted that there is a case where the US stock market could drop to 2,000 and even as low as 1,700, or laughably a 50% drawdown from Goldman’s year-end forecast, a move which Fed-backstopped issuers of subprime loans such as Goldman may afford, but none of Goldman’s clients would be able to live with such a wide range of outcomes.

Here’s more on how Goldman’s top economist comes up with a hilarious 1500 range for the S&P:

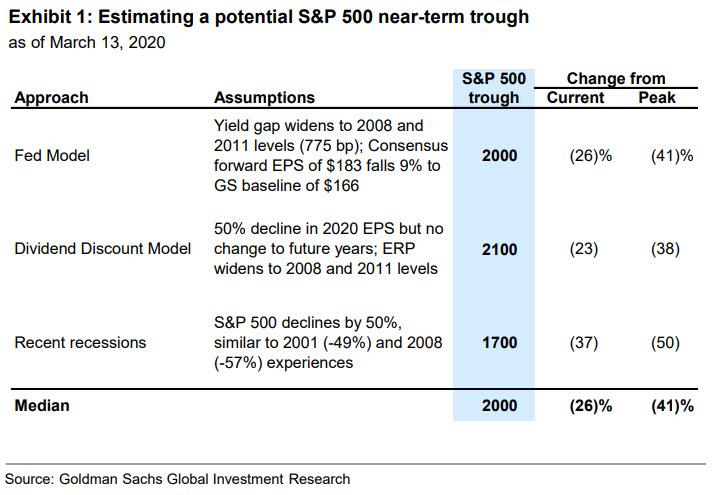

The “Fed Model” is our preferred valuation approach given the low interest rate environment. The yield gap is a proxy for the equity risk premium and measures the difference between the earnings yield and the 10-year US Treasury yield. Based on our macro model, the combination of lower consumer sentiment, higher policy uncertainty, and depressed breakeven inflation corresponds with a yield gap of 665 bp, which would rank in the 99th percentile vs. the last 20 years. Assuming a 10-year Treasury yield of 0.5%, the earnings yield would equal 7.2%, translating to a forward P/E of 14x and a S&P 500 level of 2450.

The yield gap peaked at 770 bp in late 2008 during the Financial Crisis and in mid-2011 during the Euro Crisis. A Treasury yield of 0.5% coupled with a yield gap of 770 bp equates to a earnings yield of 8.25% and a P/E multiple of 12x. Although the absolute P/E multiple bottomed at 9x in 2008 and 10x in 2011, Treasury yields were much higher then (3% and 2%, respectively). Assuming consensus EPS estimates eventually decline by 9% to our top-down forecast, applying a 12x multiple to a blended next-four-quarter EPS of $166 results in a S&P 500 trough of 2000 (26% below the current level and 41% below the high).

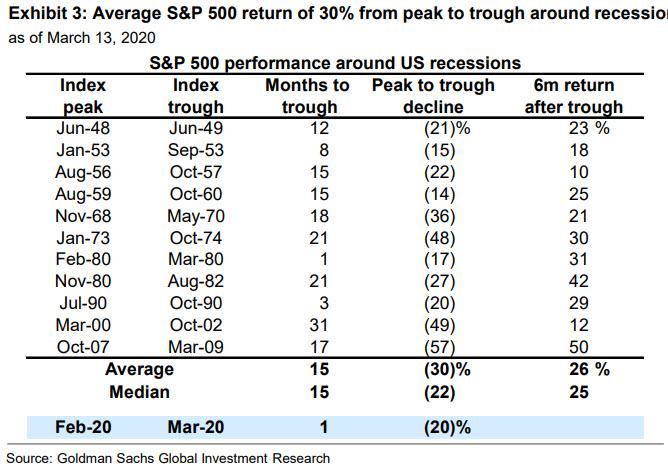

History represents another approach to estimating an index trough. During the 11 recessions since World War II, S&P 500 experienced an average peak-to-trough decline of 30%. A similar-sized decline from the recent peak of 3386 translates into a trough index level of 2370. However, the decline was larger during the last two recessions than during prior downturns. The S&P 500 fell by 49% after the Tech Bubble burst in 2000 and by 57% during the Financial Crisis. These recessions also included abnormally large EPS declines (-23% and -45%, respectively, compared to a median drop of 13% across all 11 recessions). A 50% decline from the February high suggests an index level of 1700, 37% below the current market level. Taking the median of the trough levels implied by the Fed Model (2000), DDM (2100), and historical example (1700) indicates a potential S&P 500 trough of 2000.

The combination of thin liquidity, high uncertainty, and positioning could cause the S&P 500 to fall below our 2450 base case estimate of fair value and closer to a trough of 2000. Investor positioning remained elevated during the first weeks of the correction and explains why we anticipated it would become a bear market. Our Sentiment Indicator, which combines nine different measures of positioning, read +1.7 standard deviations above average at the market’s peak in mid-February and declined to just 0.8 standard deviations below average one week ago. The Indicator has registered between 2 to 3 standard deviations below average at the trough of other major corrections this cycle

And visually?

So what is Kostin’s summary?

Here things get complicated. Here is part one of his summary:

The combination of thin liquidity, high uncertainty, and positioning could cause the S&P 500 to fall below our 2450 base case estimate of fair value and closer to a trough of 2000.

Then there is part two:

“During the 11 recessions since World War II, S&P 500 experienced an average peak-to-trough decline of 30%. However, the decline was larger during the last two recessions than during prior downturns. The S&P 500 fell by 49% after the Tech Bubble burst in 2000 and by 57% during the Financial Crisis. A 50% decline from the February high suggests an index level of 1700, 37% below the current market level.“

And finally, just to make sure he covered absolutely all bases, Kostin is still holding on to this (and yes, it’s all from the same report):

We expect the S&P 500 will end 2020 at 3200 (+18%).

Got all that? Great.

So what was the point of this particular garbage “analysis” which sees the S&P trading between 1700 to 3200 based on this or that? None really, except to show that in a time when the market is moving in a way that nobody has observed in over a decade, i.e., crashing and not even the Fed can halt it, even the smartest people in the room start to sound like idiots.

At least in wartime, the bars stay open.That’s how you know this is a different thing altogether from whatever else you’ve seen in your lifetime. Even those of us who signed up for this trip – that is, who expected a long emergency – may be a little bit in cosmic awe at just how much shit is flying into the ol’ fan. I know I am. The gods must have glugged down a mighty draft of Dulcolax.

Did you get the feeling, as I did, watching the Sanders-Biden debate last night — the inadequate versus the irrelevant — that the world they were blathering about possibly doesn’t exist anymore? The world of institutions that actually function? Like, the ones that conjure up whatever sum of money you demand to keep all the wheels spinning? Remember that Hemingway line about the guy who went broke? Slowly, then all at once. That’s us. Medicare for all now? Really? More like, a year from now every physician in America may be the equivalent of the old country doc toting a black bag around to home visits. Unfortunately, there aren’t enough horses left in America, and the few buggies we’ve got are all in the museum.

The mega financial bubble-of-bubbles is deflating with frightful velocity precisely because of the efforts since 2008 to artificially inflate it. The Federal Reserve gave it one final blast Sunday night — while everybody else was counting their rolls of toilet paper — and the effect was like blowing hot air into a shredded Zeppelin. Stock futures are “limit down” as I write, before the Wall Street open. Gold is getting pounded into the ground like a grape stake and silver is so low it looks like the hedge fund managers are down to pawning grandma’s table service. (Hint, the PMs will bounce back hard; the rest, probably not so much.)

Nobody really knows how deep and how harsh this gets (and perhaps the ones who have a clue ain’t sayin’). But the situation presents two salient questions:

how much disorder is entailed in this ordeal?

And what does the world look like when the convulsion phase of this thing is over?

Americans have never been through anything remotely like this.

The disorders of the Civil War were sharp and horrendous military operations conducted mostly in cornfields, pastures, and woods (yes, and some small cities like Richmond, pop. 38,000, and Atlanta, pop. 10,000). When the smoke cleared, battered Dixieland emerged to numb civil order. Up in Yankeedom, the New York draft riots ran for a week around the small patch of Manhattan island, but everybody else went along with Mr. Lincoln’s program.

After all that, America got on quickly with the lively business of the 19th century: railroads, mines, factories, and all that. The world wars took place in foreign lands, and the home-front scene of the 1940s now looks nostalgically idyllic.

The stresses mounting on the national scene today reflect the extreme fragilities of the way-of-life we constructed since then, and an awful lot of bad choices we made in the process, like suburbanizing the nation and making everybody a hostage to happy motoring. I won’t belabor that point, except to ask how are those vast regions of the country going to manage daily life as the supply chains wobble? I’d say a shortage of toilet paper may only be the beginning of their problems.

The cities — at least, the few that didn’t already implode from the inside out — made assumptions about how big and tall they could grow which don’t jibe with the new circumstances chugging ferociously down the line. Just think what a lockdown of the global economy will do to all those residential skyscraper projects lately hoisted up in New York, San Francisco and Boston? I’ll tell you: They are assets instantly converted into liabilities. And how will these cities even begin to pay for maintaining their complex infrastructures and services when the money for all that no longer exists and there’s no way to pretend that it will ever come back? Answer: They won’t be able to keep borrowing and they won’t manage. These cities will depopulate and there will be battles over who gets to live in the parts that still may have some value, like riverfronts.

I guess just about everybody can now see the idiocy of concentrating the nation’s commercial life in super-gigantic organisms like Big Box stores. It seemed like a good idea at the time, like so many blunders in history, and now that time is over. Any ecology thrives on redundancy — a lot of players doing similar things at the appropriate scale — and America’s chain retail model for a commercial ecology was an obvious fiasco waiting happen. The people who run that, and other people who run other things in our society, must be wondering whether those supply-chains from China will come back. It’s no different than the cargo cults of the Solomon Islanders circa 1947, after the military airplanes stopped landing with all their magical goodies: time to go back to fishing from the dugout canoe.

The foolish, idiotic identity politics ginned up by the Left and their racially-inflamed, sexually-disturbed scribes in the Thinking Class, have successfully destroyed the last shred of an American common culture that held the country together through earlier vicissitudes. So, one concludes that we’ll be left stewing in poisonous tensions, and perhaps some violent conflicts, before those matters head toward some sort of resolution.

Where does this all lead? Eventually, to a land and a people who operate their society in a very different way at a much more modest scale. The task of reorganizing our national life is immense. (There will be plenty to do, so don’t worry about that.) You can forget about the grandiose techno-narcissistic visions of electrified motoring and a robotic nirvana of perpetual sex-crazed leisure. Everything we do has to be downscaled, from whatever manufacturing we can cobble back together to rebuilding commercial ecosystems at a finer grain from region to region — in other words, what we now call small business, geared locally.

Expect giant AgriBiz to founder on a shortage of capital, especially, and expect smaller farms to organize emergently, worked by more humans working together. That is, if we want to keep eating. Expect the small towns in the well-watered parts of the country to revive while the groaning metroplexes spiral down into entropic sclerosis. Consider the value of our vast inland waterway system and the opportunities to move goods on them, when the trucking industry unravels. Consider lending a hand at rebuilding the railroad system in this country.

There will be economic roles and social roles for all those willing to step up to some responsibility. Young people may see tremendous opportunity replacing the wounded economic dinosaurs wobbling across the landscape. It’ll be all about going local and regional and making yourself useful in exchange for a livelihood and the esteem of others around you — aka, your community. Government has been working tirelessly to make itself superfluous, if not completely ineffectual, impotent, and rather loathsome in the face of this crisis that has been slowly-but-visibly building for half a century. Something old and played-out is limping offstage, and something new is stepping on. Aren’t you glad you watched all those debates?

Kudlow Teases ‘Helicopter Money’, But The Market Is Not Impressed

As the administration scrambles to soothe the market during yet another day of trading-halt chaos, Larry Kudlow just tried to jawbone the market higher by raising the prospect of helicopter money.

Of course, the market wasn’t exactly impressed.

Apparently, investors are tired of talk from the administration, and are now waiting until Trump’s economic team starts shot-putting rescue packages filled with prepaid Visa credit-cards.

Essentially, the market’s attitude can be summed up in four words: “fuck you, show me”.

During a presser packed with soundbites, Kudlow said that the administration might offer “100% expensing” for any companies who move production back to the US because of the virus. The G-7 leaders who joined a call earlier in the day committed to doing ‘whatever it takes’ to save the global economy.

Though he acknowledged that the second quarter will be “very difficult”, Kudlow declined to call this a recession.

Because of these economic difficulties, the administration is considering sending cash directly to households to provide some “short-term relief”.

Bottom line: This is a short-term problem, a matter of weeks, not a matter of years.

Kudlow says the #CoronavirusOutbreak is a short term economic problem, a matter of weeks or months not years. He says the fundamentals of the economy are strong. pic.twitter.com/1V1Aod0HFT

The underlying fundamentals of the economy remain strong.

In related news, a group of moderate conservative senators led by Mitt Romney are apparently rallying around a plan introduced via an opinion piece in the WSJ calling for the government to give $1,000 to every American adult to combat the economic fallout associated with the outbreak, per Axios.

Are Democrats just going to sit back and let Romney take the credit for doling out $1,000 to every American after Andrew Yang brought direct cash interventions into the mainstream political discourse.

Shortly after Kudlow’s comments hit the wires and failed to revive the market, the administration lobbed another ‘tape bomb’ with an anonymously sourced insider report claiming the administration is “drafting” a hefty aid package for the airline industry.

How else does one react to the slew of international borders being closed; to the slew of school and businesses within said borders being closed; to reports that elderly people may to self-isolate for months in the UK; that the army may be needed to ensure we get food; that companies are being co-opted by governments to fight the virus as now required (“Build ventilators!” “Make virus tests free!”); that there is talk of supply-chains and virus experts attempting to be poached by the US to work solely for them; and, contra-wise, for key virus-related goods being on-shored or even nationalised, even in Germany?

How else does one react to the scale of staggering scale and breadth of uncosted fiscal packages being rolled out,even in the US (though this has an end-year sunset clause – if you want to believe that). Believe me, those fiscal bills are going to get bigger and bigger. Governments are going to have to support households, the self-employed AND businesses large and small through this all, or we face a domino-style economic collapse. Many are saying they will, or suggesting they will, even the EU’s somnambulant Khrushchev, Angel Merkel.

And what else but war, or utter calamity, would see the Fed not able to wait even a further couple of days to deliver its latest 100bp bazooka cut? (We are now at the zero lower bound again, as our Fed Watcher Philip Marey has been saying all along we would be in 2020.) What else could see the Fed offer up another USD700bn in QE, which on top of the recent liquidity pledges made now mean that USD5.5 trillion is available, if needed (as well as letting banks borrow from the discount window for 90 days and slashing reserve requirement ratios to zero!)? That is genuinely the kind of cash a war usually destroys. Even the smaller central banks are at it: the RBNZ has just slashed rates to 0.25%, once again showing itself more nimble than the RBA (NZD dipped sub-60 for a moment). Indeed, it would seem that with a few exceptions, we are all going to be at the zero lower bound imminently.

Amazingly, China might be one of those exceptions because of the deep debt-and-inflation-and-fear-of-a-CNY-collapse hole that they are already stuck in. Yes, the PBOC has cut its Reserve Requirement Ratio again – but that looks small beer now, especially when retail sales for January AND February, hence flattering the data upwards a lot, was -20.5% y/y (bless those Bloomberg survey respondents whose median guess was -4%!), industrial production was -13.5%, fixed asset investment was -24.5%, and even unemployment was up to 6.2%: who would ever have predicted that China would face problems shovelling in enough liquidity, and perhaps even enough fiscal stimulus, and have a higher cost of capital than the rest of the world?

Yet that certainly doesn’t mean CNY will in any way be pushing USD aside, even if so: quite the opposite. Indeed, alongside this barrage of latest virus-fighting measures we continue to see signs of enormous stress in the markets. Most obviously: S&P futures are limit down following the Fed move, which is hardly a ringing endorsement; while 30-year US Treasuries are back over 1% at 1.26%, vs. just 0.27% for the 2-year, the 10-year is down to 0.65% again, a 31.4bp move today that does not suggest imminent reflation on the back of all this fiscal and monetary fire-power; the superstructure of the global credit markets continues to groan worryingly; FRA-OIS spreads are not where one would want them to be; and cross-currency basis swaps continue to point to a demand for USD. Need I add, the dash for dollars and for cash are again what one would expect to see during a war?

In short, the big policy guns have now all been rolled out and fired. Short of open helicopter money entering playing The Flight of the Valkyries over loudspeaker, there is little left to do already. (“I love the smell of MMT in the morning! Smells like victory!”) And those helicopters are surely coming too if one reads the latest secret UK Public Heath England report obtained by the media, which says that this crisis will not be over in Q2, or even H2. Rather, it is expected to last until Spring 2021, see 80% of the population infected, 7.9m hospitalised, and anywhere from 318,660 to 531,100 deaths – assuming the health service is not over-run and the mortality rate hence stays around 1% max.

So we have an array of monetary and fiscal weapons. But these are likely to face the same fate as 1997’s Starship Troopers did in their first battle with the bugs at Klendathu if they do not understand that nature, not the business cycle, is the most dangerous opponent. (Spoiler: the bugs win big over the arrogant humans.)

Even the jaw-dropping concept of the central banks and governments making everyone whole until this crisis passes, with all the equally mind-bending socio-economic and socio-political implications, is not the real battle. The real battle is the virus. Even helicopter money would just be palliative to keep can-kicking until we can kick the virus.

Further, in a real war markets are right to sell-off. Unlike our recent, comfortable experiences of conflict, fought by people we never meet socially in places we never want to go, the long-run history of war is of blood and tears. Wars destroy economies. They smash currencies. They topple regimes. They remake demography. They shift borders. They rewrite social contracts. They even change national identity and psychology.

If this is a true global epidemic that lasts until we get a vaccine in 18 months (and not due to the “herd immunity” that the UK seems to be chasing away from the rest of the herd), then the cost of fighting it is going to be high for everyone. A whole generation, perhaps two, of market ‘teenage-scribblers’ are unaware what this is really likely to mean: there are still voices out there suggesting this will all be over in weeks and a V-shape recovery will return us to normal: public health officials strongly disagree. Who knows best?

Yes, in the long run one wants to back humanity – science has a great track record when applied during war: the question is how much is lost and destroyed before then. Moreover the alternative logical end-point, no working vaccine and no herd immunity, as with flu, is that we will all have to accept that once we reach old age we probably won’t live that long. Surely no takers there.

However, for now please prepare yourselves carefully – and in markets terms that means ignore Steven Mnuchin and his “I see no recession” call: ‘We can ill afford another Klendathu’.

European Union To Ban Non-Essential Travel Into Europe

The gradual but accelerating “quarantining” of the world into its constituent parts to halt the spread of the Coronavirus just took a major step moments ago, when the FT reported that European countries plan a ban on entry to the 26-state Schengen passport free travel zone in the most radical response yet to the continent’s escalating coronavirus pandemic.

The proposed action – expected to be announced later on Monday – and may be in response to the US ban of all flights from Europe for the next month, would cover all non-essential visits from third countries, with exemptions including for citizens of Schengen countries.

The ban is aimed at non-essential travel to the Schengen area in an effort to curb the coronavirus’s spread across Europe, officials said. The Schengen countries include 22 EU members, as well as Iceland, Norway, Switzerland and Liechtenstein. The five EU states not in Schengen – Ireland, Cyprus, Croatia, Romania and Bulgaria – may also be invited to also implement the restrictions.

In short, virtually all tourism between the US and Europe is now indefinitely halted.

Exemptions to the ban under discussion include for EU citizens, residents and their family members, as well as workers in crucial sectors such as healthcare and transport, officials said.

As the FT adds, EU officials are currently still finalizing the sweeping move, which comes after a sharp rise in cases of infection in Europe triggered a wave of unilateral decisions by member states to all but seal their borders. The plan will still need to be signed off by national leaders, while officials stressed details remained under discussion and could change ahead of the announcement.

Predictably, the status of the UK – which is in a post-Brexit transition period after leaving the EU in January – was not immediately clear.

Diplomats told the FT that the measure was discussed on a phone call this morning between French president Emmanuel Macron, German chancellor Angela Merkel and the heads of the European Commission and Council.

On the call, Macron reportedly attacked national moves to close borders and called for a European response, although it seems he was promptly overruled.

Brussels is set to announce the plan after a videoconference among G7 leaders this afternoon.

Box Office Sales To Plunge 40% In One Week As Social-Distancing Accelerates In US

North American box office revenues are expected to plunge by 40% over last weekend in yet another example of collapsing consumption as people change their habits to avoid contracting coronavirus.

Disney’s “Onward” is projected by Variety to take top spot with $12.5 million in ticket sales – down 68% from its opening weekend. Friday’s take for the family flick was just $3.3 million – a 73% decrease from its March 6th premiere. Typical declines for second-weekend showings are in the 50% range according to the report. Total domestic box office sales are projected to be as low as $60 million for the weekend.

AMC and Regal, two of America’s largest theater chains, announced on Friday that they have cut capacity by 50% in their auditoriums in order to address safety concerns by letting people sit next to empty seats.

“Movie theaters are doing the right thing by reducing capacity in light of the current situation, but naturally this will have an impact on the box office bottom line this weekend,” said Comscore senior media analyst Paul Dergarabedian.

Here’s how the rest of the current releases are doing:

Lionsgate’s faith-based drama “I Still Believe” appears to be the one new release that’s performing in line with pre-release estimates and should finish second with about $11.6 million at from 3,250 venues. It was the top performer on Friday with $4 million, and it garnered an A Cinemascore from opening day audiences.

“I Still Believe” is based on the life of contemporary Christian singer Jeremy Camp (played by “Riverdale” star KJ Apa) and his first wife (Britt Robertson), who was diagnosed with ovarian cancer shortly after they wed. The film is directed by siblings Andrew and Jon Erwin, who also helmed 2018’s “I Can Only Imagine.” “I Still Believe” is the first production by the brothers’ Kingdom Story Company.

Sony’s opening of superhero pic “Bloodshot,” starring Vin Diesel, is heading for third place with an estimated $9.4 million at 2,861 screens, slightly under pre-weekend projections for a $10 million start. Audiences gave it a B on CinemaScore.

Universal has two Blumhouse horror titles battling for fourth with about $6.4 million each — the third weekend of “The Invisible Man” at 3,636 sites and the launch of newcomer “The Hunt” at 3,028 locations. Elisabeth Moss’s “The Invisible Man” is declining by 58%, the lowest decline among holdover titles in the top 10, and will finish the weekend with around $65 million in its first 17 days.

“The Hunt,” a dark political satire portraying elites hunting people for sport, was delayed last year amid backlash over school shootings. The film came in under pre-release forecasts in the $8-9 million range. Opening day audiences were unimpressed, giving the film a C+ on CinemaScore. “The Hunt” carries a $14 million budget.

Paramount’s fifth weekend of “Sonic the Hedgehog” came in sixth with $2.9 million at 3,041 locations, declining by 62%. The video game adaptation will wind up the weekend with $146 million in North America.

Warner Bros.’ sophomore session of Ben Affleck’s addiction drama “The Way Back” was battling for seventh place with Disney-Fox’s fourth frame of Harrison Ford’s adventure story “The Call of the Wild” with $2.5 million each. “The Way Back” slid 70% from its opening weekend and “The Call of the Wild” fell 65% from its third weekend.

Focus Features’ fourth weekend of 19th Century romance movie “Emma” will probably finish ninth with $1.7 million at 1,732 locations. The figure represents a 71% decline. The Jane Austen adaptation will have a total North American take of $10 million by the end of the weekend. –Variety

“You can’t jump into cash. Cash is trash,” says @RayDalio. “You have to have a well-diversified portfolio, you have to be global, and you have to have balance…and you have to have a certain amount of gold in your portfolio.” pic.twitter.com/lZqCnvsqBh

Dalio’s Bridgewater fund is also getting hammered as Dalio admits he was caught wrongfooted during this month’s coronavirus-led market turmoil, as its flagship fund dropped about 20% for the year following sharp reversals in stocks, bonds, commodities and credit.

“We did not know how to navigate the virus and chose not to because we didn’t think we had an edge in trading it. So, we stayed in our positions and in retrospect we should have cut all risk,” said billionaire investor Ray Dalio in a statement to the Financial Times.

“We’re disappointed because we should have made money rather than lost money in this move the way we did in 2008.”

So it is perhaps not entirely surprising that he is laying out what exactly needs to be done to save the world (well, the markets and his fund), proclaiming that what has been done so far “has been inadequate in size, focus, and coordination” and that more massive fiscal malarkey is required… now!

The Implications of Hitting the Hard 0% Interest Rate Floor

While I’m going to pass along my thoughts to you, I want to emphasize that I wasn’t, and still am not, able to anticipate the most important things happening in the markets because of the extremely rare nature of the circumstances. While what I don’t know is much greater than what I know, I will tell you what I think for you to take or leave as you like.

As you know, for some time now I have been concerned that when the next economic downturn would come it would lead to hitting the 0% interest rate floor with a lot of debt outstanding and big wealth and political gaps in the same way that configuration of events happened in the 1930s. The coronavirus was the thing to cause the downturn, which surprised me. While it is an extremely serious infectious disease that will produce many harmful economic impacts, these things alone don’t scare me; however, when combined with long-term interest rates hitting the 0% floor, it really worries me.

Long-term interest rates hitting the hard 0% floor means that virtually all asset classes go down because the positive effects of interest rates falling won’t exist (at least not much). Hitting this 0% floor also means that virtually all the reserve country central banks’ interest rate stimulation tools (including cutting rates and yield curve guidance) won’t work. The printing of money and buying of debt assets that central banks are now allowed to buy almost certainly won’t work much (because bonds can’t be pushed much higher and they are also less likely to be sold to buy other assets of entities that are in financial trouble). Further, with this hard 0% interest rate floor, real interest rates will likely rise because there will be disinflation or deflation resulting from lower oil and other commodity prices, economic weakness, and more credit problems. If that plays out in the typical way, rising credit spreads will raise debt service payments to weaker credits at the same time as credit lending shrinks, which will intensify the credit tightening, deflationary pressures, and negative growth forces. God help those countries that have these things and a rising currency, too.

I am trying to imagine how this will play out. To do that, I (with my great team) are taking existing market prices and visualizing what will happen if things stay exactly where they are. For example, I think about pension funds and insurance companies and others that have long-term liabilities that are funded with these equity and equity-like assets. I do the mark-to-market accounting of what this situation will be like for them by taking the present value of liabilities and looking at the expected returns of the assets that they have to fund their liabilities. They will come up short. I imagine what they will have to do—i.e., sell assets to make payments. I think about oil producers (countries and companies), see that their expenses are much greater than their revenues, and imagine what they will have to do—i.e., slash spending and sell assets. I imagine many others in similar circumstances and what that will mean for economic activity and market prices, and that’s seriously worrisome. These are only a couple of things that I’m thinking about and I’m sure what I’m thinking about is only a small percentage of the financial disruptions that will happen. Remember that most investors and businesses are long (i.e. holding assets hoping that they will go up in price) on a leveraged basis (financed with debt) so that the declines in asset prices that we are seeing will have even bigger financial effects than the unlevered price declines that we are seeing.

Contrary to popular thinking, the markets will have a bigger effect on the economy than the economy will have on the markets. For that reason, calculating who is in what positions and figuring out what they will need to do because they are in those positions (e.g., cut expenses, sell assets, etc.) is most important. That’s what we are struggling hard to do and are doing inadequately.

However, what I’m damned sure about is the following:

Big Fiscal Stimulation with Monetary Cooperation Is Needed, Low-Risk, and Isn’t Yet Happening

Our biggest economic risk comes from the possibility that our elected officials (who are the ones who control fiscal policy) will handle it badly. That is because it’s tough enough to know what to do during a big crisis and then do it boldly even when there aren’t divisive politics. With the divisive politics it might be impossible. While some fiscal stimulation measures are being put into place, they’re not large or targeted enough to neutralize the contagion of the economic and market effects of the virus, and they are being argued about. However, there are some emerging signs that some important policy makers might move to a “whatever it takes” posture. If so, then we will have to see if works given the previously described circumstances being so limiting. More specifically, in a nutshell, here is what is going on:

In the US:

Thus far the fiscal and monetary reactions have been too little too late but there are indications that some parties are moving into the “whatever it takes” mode. What will happen is still being worked out. Things are changing by the minute. Here’s where things now stand.

Thus far, there has been only a very small fiscal response consisting of:

$3 billion for research and development of vaccines, test kits, and other treatments

$2.2 billion for the Centers for Disease Control and Prevention to contain the outbreak

$1.2 billion for the State Department to assist in battling the spread of the virus overseas

$1 billion for medical supplies, healthcare preparedness, and community centers

$1 billion authorized for the SBA to make subsidized SME loans

$500 million for Medicare providers to provide telemedical services

$300 million to ensure vaccines are delivered to individuals at little or no cost

There is talk of a payroll tax cut which isn’t targeted to where the problems are. It’s styled after the 2011-12 cut which was about 0.6% of GDP (a similar cut today is estimated at 0.75% of GDP). However we hear President Trump supports a complete payroll holiday until after the November election (it’s not detailed, but supposedly it encompasses both employer and employee contributions, estimated at ~$500 billion). This plan probably won’t happen because Congressional Democrats and some Republicans don’t support it (because payroll tax cuts are regressive and undermine Social Security funding, and the business part of the cut is considered too business-friendly). It is, however, indicative that president Trump might be in favor of a big stimulation, though there are no signs that it will be targeted where it needs to go most or of a size that it needs to be. Regarding his priority of getting elected, he is in serious risk of doing too little too late, and what president trying to be re-elected wouldn’t love to have big fiscal stimulation going into the election, so I would think that he would move into the “we will do whatever it takes camp.” In time and with further deterioration in conditions, maybe he will support more related tax credits.

For now, there hasn’t been much focus on relatively targeted measures, which I believe are most important because specific areas need the most help for this debt/economic problem not to spread. I’m not saying that nothing was created, because there have been some increased subsidized SBA loans to SMEs, paid sick leave for those affected, coverage of most of the cost of virus treatment for the uninsured (potentially tapping FEMA), and increased funds for state and local healthcare services (by tapping emergency and disaster-related funds via FEMA and its Disaster Relief Fund), extension of unemployment benefits, and increased funding of other direct transfers, e.g., food stamps for those in hard-hit areas. The House voted last week on a set of targeted measures (including free testing for the virus, expanded unemployment insurance and paid sick leave for those affected, and subsidized meals for students eligible for free school lunches). But these measures will be relatively small and offer modest support to those with economic problems. They will need to be much bigger.

Thus far, there has not been much debt support to industries that would go broke due to this shock though President Trump has called for Congress to authorize an additional $50 billion in subsidies for loans to SMEs through the SBA. This could free up a few hundred billion dollars in loans; however, it’s not big enough and it’s not clear whether this measure will garner congressional Democrats’ support. Thus far, meaningful debt supports to industries that would go broke due to this shock have been absent (other than SBA-subsidized loans, which look to be small). Probably the best way to do this is for the fiscal policy makers to guarantee the safety of the banks for new lending of a sort that is needed with government protections on that new lending (a politically challenging move). Accidentally we are seeing a bit of this as troubled companies have tapped pre-existing lines of credit at banks. While this may not be what the banks want (I doubt they want to take on more credit risk when the economy is deteriorating), it is one way that money gets to those businesses that are squeezed. Getting money to targeted businesses is a task the Fed is ill-suited for, but it can provide liquidity to the banks to fund those loans if needed. My suspicion is that we will see more of what I will call “protected lending programs” of the sort that the ECB did (like the TLTRO) in which the Fed provides super-cheap money and protections to the banks that lend it. This big usage of credit lines by businesses has a significant hint of this, even though it’s accidentally stumbled into. All those who control the fiscal levers have to do is protect the banks from going broke. Still, not all of the squeezed companies have pre-existing lines of credit, so large gaps are likely to remain, and they will come with significant costs.

I don’t yet know if the president and other fiscal policy makers have done the stress tests of various companies and various sectors of the economy as we have, or whether theirs show what ours show, but I’m seriously concerned by what I see, which is that a number of companies and industries will have debt problems that will likely lead to restructurings. Perhaps it is expected that these companies will keep operating through the bankruptcy process, though this could be debilitating and would have undesirable knock-on effects because monetary policy will be ineffective and the political fragmentation will be large and potentially volatile. If handled badly, this could become a big political and social issue. If I were in President Trump’s shoes, I’d be generous and empathetic, especially as the news will become increasingly bad at this politically sensitive time. I do expect politics to get in the way of doing the best things for the country as, above everything else, the number one goal of each of the sides is to get into power.

As for the Federal Reserve, it just did about all that it can do in being stimulative without moving to doing what I call Monetary Policy 3 (which is working with fiscal policy makers to monetize their deficits). The first (and preferred) type of monetary policy (MP1) primarily uses interest rates as the control mechanism. When that stops working, they go to the printing of money and buying financial assets which I call MP2. When that no longer works, the central government has to run big deficits and sell the resulting bonds to the central bank (which I call MP3). It takes various forms that you can get an explanation of in my book Principles for Navigating Big Debt Crises (available free at www.economicprincples.org). We are now at that stage in the long-term debt cycle and we will have to see if fiscal and monetary policy makers can coordinate themselves to do that and then see how it works. There’s not much else that can be done. Theoretically the Fed could buy other assets like stocks, but that won’t fly because it’s very controversial, questionable at best under the Federal Reserve Act (it likely requires Congressional approval), and it wouldn’t have much of an impact anyway. As far as I can see, the best path is to do all these things I just mentioned plus provide support to the banks in conjunction with the fiscal authorities providing fiscal protections that will help the credit get to those who need it most.

In Europe:

The European Commission is expected to grant maximum flexibility from the EU rules, most importantly the fiscal rules associated with the Stability and Growth Pact. Consistent with this, the fiscal responses in Europe that have been announced are generally targeted at supporting health services and hard-hit geographies, sectors, and SMEs. The measures include tax and fee cuts, debt service forbearance, and employee compensation for shortened work hours. The hard-hit sectors most mentioned are tourism, transportation, and autos, though supports are likely to be much broader than these. Both France and Italy have been pushing for more concerted efforts at the intergovernmental and supranational level. However, there still is now little consensus on policy direction or a willingness for the mutualization of deficit spending. The European Commission just proposed a modest €25 billion EU investment fund to be used for targeted measures: healthcare, SMEs, and labor-market support. It is funded by the EU Commission reallocating €7.5 billion from its budget (specifically from the Structural and Cohesion funds), which the EIB, in turn, will lever up to €25 billion. Steps toward greater policy coordination are likely to emerge from the next formal meeting of the Eurogroup (EMU finance ministers) on March 16. My guess is that each country will eventually do “whatever it takes” fiscally for itself but not materially help the others and the ECB will be too constrained to help which will cause serious problems. That means that where there are big fiscal stimulation and deficits there will be a lot more bonds that have to be sold so that, without the ECB buying, interest rates will rise. At the end of last week with the German announcement of its big fiscal stimulation we saw that. God help us if that happens.

The ECB can’t do much because it can’t cut rates and it doesn’t have the authority to buy the quantity it needs to buy. While of course its officials won’t directly say that, they are conveying that message as loudly and clearly as they can through their actions and what they are saying. Christine Lagarde did that in her way on Thursday. More specifically, she kept ECB rates at -0.5% and launched a package of measures to alleviate the economic impact of the coronavirus: providing liquidity and a bit more credit by buying €120 billion ($133.9 billion) more bonds by the end of the year and launching a new program to offer cheap loans to banks (at rates as low as -0.75%, below the ECB’s sub-zero deposit rate). But it was made clear that the ECB isn’t going to do anything much other than add liquidity because it can’t. It can’t because it is a justifiable worry that pushing rates lower than where they are now (-0.5%) will be more harmful than helpful, and the Northern Europeans are against lower rates and modifying the limitations on sovereign purchases. ECB President Christine Lagarde said her officials are looking to provide “super-cheap” funding and ensure liquidity and credit don’t dry up. And then she appropriately made clear that the response to the coronavirus needed to be “fiscal first and foremost,” noting that the spending pledges so far from Eurozone governments amounted to only €27 billion ($30 billion) in total, and that central bank measures can only work if governments throw their weight behind them, too, with steps to ensure banks keep lending to businesses in affected areas. I couldn’t agree with her more.

As for what might come next, the ECB is likely to consider raising liquidity for small and medium-size enterprises, possibly by repurposing an existing TLTRO or a new program like that, but that won’t do much. The most important big test of their willingness to “do what it takes” will be in whether or not they raise their bond buying limits to hold interest rates and credit spreads down. A yes on that will buy some time to help fund the deficit but still won’t be enough longer term while a no would be very worrisome.

In Italy:

Thus far, the fiscal stimulus package equals about 0.4% of GDP but they will make it bigger and it should be much bigger. It now contains targeted tax cuts for affected sectors such as transportation, hotels, and exporters; support for healthcare services; and select tax credits for companies that reported a 25% drop in revenues. To me, this is a good policy that other countries should consider their own versions of, because it is the bankruptcies of good businesses and the second-order effects of them that is threatening economic recovery, but it’s not nearly enough. The Italian government is also preparing a structural package of measures designed to encourage FDI and investment but that’s an issue for beyond the time of this crisis. Because these policies are producing political issues, with the opposition saying more should be done, doing more is clearly politically safer on the domestic political stage. Not surprisingly, reportedly the government now seeks to more than double the stimulus size, totaling up to €25 billion (1.2% of GDP), which will bring its 2020 deficit to 3.3% though my guess is that estimate of the size of the deficit is way too low because the tax revenue will be devastated. Although the EU has shown flexibility with regard to Italy deviating from its debt reduction pathway, the amount it borrows will affect its overall debt sustainability. Italy’s finance minister touched on this by asking for the ECB’s support. We will have to see how all the political players (most importantly the European Commission and Italian government) work this out.

In Germany:

The Germans started approaching this crisis with their usual frugality that put not creating a lot of money and credit during times of financial stress above all else, but now they appear to be flipping to doing “whatever it takes” which will significantly increase its need to sell bonds. This put the onus on the ECB to buy them to hold rates down, though there are restrictions, mostly by the Germans, that prevents the ECB from buying them. To quote the statement from the finance ministry “The German government is taking decisive and forceful action against the economic impact of the coronavirus.” It has been agreed that there will be a “far-reaching package of measures to protect jobs and support companies. The government is setting up a protective shield for employees and companies. The goal is to equip businesses with sufficient liquidity that they will be able to make it through the crisis in good shape.” They went on to layout some specifics but a lot more will come. These measures include employee and employer reduced work hours and compensation for these shortened hours and liquidity provisioned via the public investment bank. They also include tax payment deferrals, penalties for late payments being eliminated, etc. It will also create a “protective shield” for businesses that include KD business loans and loan guarantees. To me this looks like an excellent path both in size and focus and it then will require more borrowing to fund it which will put this back in the ECB’s court and the ECB needs to hold rates down and do whatever buying is required to do that, which means that controls will have to be lifted (which is doubtful). It will also be interesting to see how Germany handles its own constraints such as the “black zero” (pledge to maintain a balanced budget) to constrain the size of any potential stimulus over and beyond leveraging automatic stabilizers and drawing down existing surpluses. Also it has to deal with the “debt brake” which is a constitutional provision limiting the structural deficit to 0.35% of GDP. There is, however leeway if a majority of parliamentarians determine additional spending is required to address a “natural disaster or extraordinary emergency situation outside the control of the state,” for which COVID-19 qualifies.

In France:

So far, the focus is on credit payment assistance and various forms of regulatory relief (e.g., credit payment assistance for up to 70% of loans, removal of late payment penalties on public contracts and tax obligations). However, the finance minister has initiated emergency economic measures. The last time such measures were implemented (during the Yellow Jacket protests), they were used to initiate spending and revenue changes of roughly 0.4% of GDP. France has a more centralized institutional structure than Germany and a less stringent strain of fiscal conservatism in its culture. This means that policy barriers to the provision of assistance are weaker, enabling the government to enforce deeper policy cooperation across the sectors of the economy. Governments are also more responsive to people’s screaming (some would say temper-tantrums) so we should expect more as conditions worsen there. However, because France’s budget deficit is already large and in breach of EU fiscal rules (3.2% of GDP), there isn’t yet much talk of a broad fiscal stimulus. I do however expect that will come. We are awaiting announcements.

In Japan:

The government’s fiscal response thus far is targeted to support healthcare services and impacted persons and firms, in particular SMEs. Two recently enacted spending packages totaling ¥450 billion, for example, fund new medical clinics and improvements to medical facilities, provide aid to working parents forced to take leave due to school closures, and support SMEs. In addition, the government is providing ¥1.6 trillion in special financing to aid SMEs and other businesses affected by the outbreak. These look good to me, though not yet enough in light of their total picture. These measures draw on existing “rainy day” government funds. Isn’t it great that they have such a fund? The government is also seeking legislation empowering the prime minister to declare a state of emergency, if needed. These steps are in addition to ¥13.2 trillion in fiscal stimulus already in the pipeline announced in December. That spending is being phased in over several quarters. The government is reportedly considering a fiscal package for April of some ¥10-20 trillion that may include direct cash handouts to households.

The BoJ is being even more squeezed than other central banks because it has the same problems plus the strong currency (which adds to deflationary and negative growth pressures). However, it has more flexibility in what it can buy and in what quantities. Its usual bond purchase it has so far purchased roughly ¥100 billion of equities ETFs on each day it has intervened in the market in March, compared to a previous pace of around ¥70 billion. It has also provided ample liquidity to the market via repo operations. It may increase its annual target for ETF purchases at its March meeting.

In China:

The most targeted and appropriately-sized fiscal and monetary responses are coming from China. That is because it is a country that has a greater ability to coordinate fiscal and monetary policies and cut through political disputes more quickly, and it has very smart economic policy makers.

Thus far there has been a series of announced fiscal measures that have amounted to roughly 1.2% of GDP, excluding infrastructure investment. These include waivers and reductions of social charges (e.g., corporate pensions, unemployment and workplace injury insurance), reduced healthcare insurance contributions, lower VAT taxes for some enterprises, and lower electricity and gas fees for corporate users, among other measures. There has also been a series of smaller fiscal support measures (including subsidies) announced at the local level. At the national level, the government has introduced sets of measures to support select industries, as well as regulatory forbearance (such as delayed recognition of some bank non-performing loans).

The People’s Bank of China has more room to maneuver because of where interest rates are and because it has more levers to pull in order to make lending increase or decrease where it wants to see increases and decreases. It has recently cut rates, cut reserve requirements, provided liquidity and initiated a $79 billion support package for companies hurt by the virus. Additionally it has shifted its official stance to “prudent with appropriate flexibility” and introduced 30 measures to support enterprises impacted by the outbreak (with a focus on SMEs), such as relending and rediscounting funding for banks. It is in my opinion appropriate in light of the full picture.

* * *

In summary, I believe that

1) the 0% interest rate floor and the absence of other effective central bank tools requires much greater fiscal stimulation that is targeted to hit the most important pain points, with the cooperation of central banks holding rates down and providing plenty of liquidity,

2) the response thus far has been inadequate in size, focus, and coordination but that has varied a lot by country,

3) in the last few days there have been signs of fiscal and monetary policy makers moving to much stronger “do whatever it takes” policies, and

4) the wealth and political gaps will test social and political abilities to cooperate and help rather than hurt each other in dealing with these problems.

Bye, Bye Bibi?: Netanyahu Rival Gets Another Shot At Forming A Government In Israel

With a bump of his elbow, Blue & White Party leader Benny Gantz received a mandate from Israeli President Reuven Rivlin to try and form a new ruling government coalition, after a prior attempt by Gantz back in September failed.

As Netanyahu struggles desperately to stay in power at least long enough to avoid being prosecuted for corruption charges, the PM, who is presently leading an emergency unity government as Israel struggles to combat the coronavirus outbreak, has skillfully used the present circumstances to his advantage.

However, on Sunday, 61 members of the Knesset voted to recommend that Gantz be offered the opportunity to form the government. To succeed, he will need to win a majority of votes in the 120-seat Knesset. The problem, is that two members of Gantz’s own Blue and White Party said they wouldn’t vote to back him as PM if the Arab Joint List remains part of the coalition.

According to the Jerusalem Post, currently, the only parties willing to join a Gantz-led government are his Blue and White, Yisrael Beytenu and Labor-Meretz and the Joint List. Legally, 61 MKs must vote for the government at first, even if it ends up being a minority government with less than 61 MKs supporting it.

After the meeting at the presidential palace at noon local time on Monday, a meeting at which Netanyahu was also present to try and convince the president to call for a unity government, Gantz phoned Yisrael Beytenu chairman Avigdor Lieberman and Labor-Meretz chairman Amir Peretz and told them that he intends to form as broad a government as possible to meet the significant challenges currently facing the State of Israel. Both Liberman and Peretz agreed to meet him soon. One of Gantz’s greatest political coups was winning the support of Liberman following a falling out between Liberman and Netanyahu.

But when Gantz phoned Defense Minister Naftali Bennett, the chairman of Yamina, and invited him to meet, Bennett turned him down, saying Gantz should join a unity government led by Netanyahu.

During the 28 days he will have to form a government, Gantz will face a near-impossible mission, per Axios. Although he has 61 recommendations, he may not have 61 members of Knesset to vote in favor of his government, this is because two members of Gantz’s own party said they would vote against a government that relies on votes from the Arab Joint List, claiming the organization, which advocates for more representation for Israel’s Arab minority, supports terrorists.

Israel’s new Knesset will be sworn in on Monday, though swearing-ins will take place three at a time because of virus worries. Meanwhile, Netanyahu is reportedly considering a complete European-style shutdown in Israel as the number of Israelis who have tested positive climbs to 250, with four cases in ‘serious’ condition.

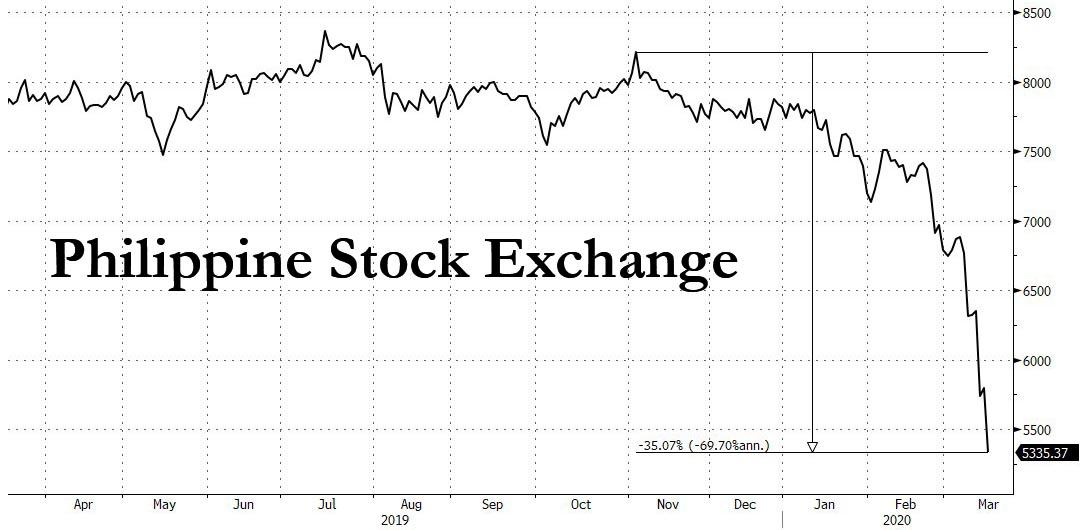

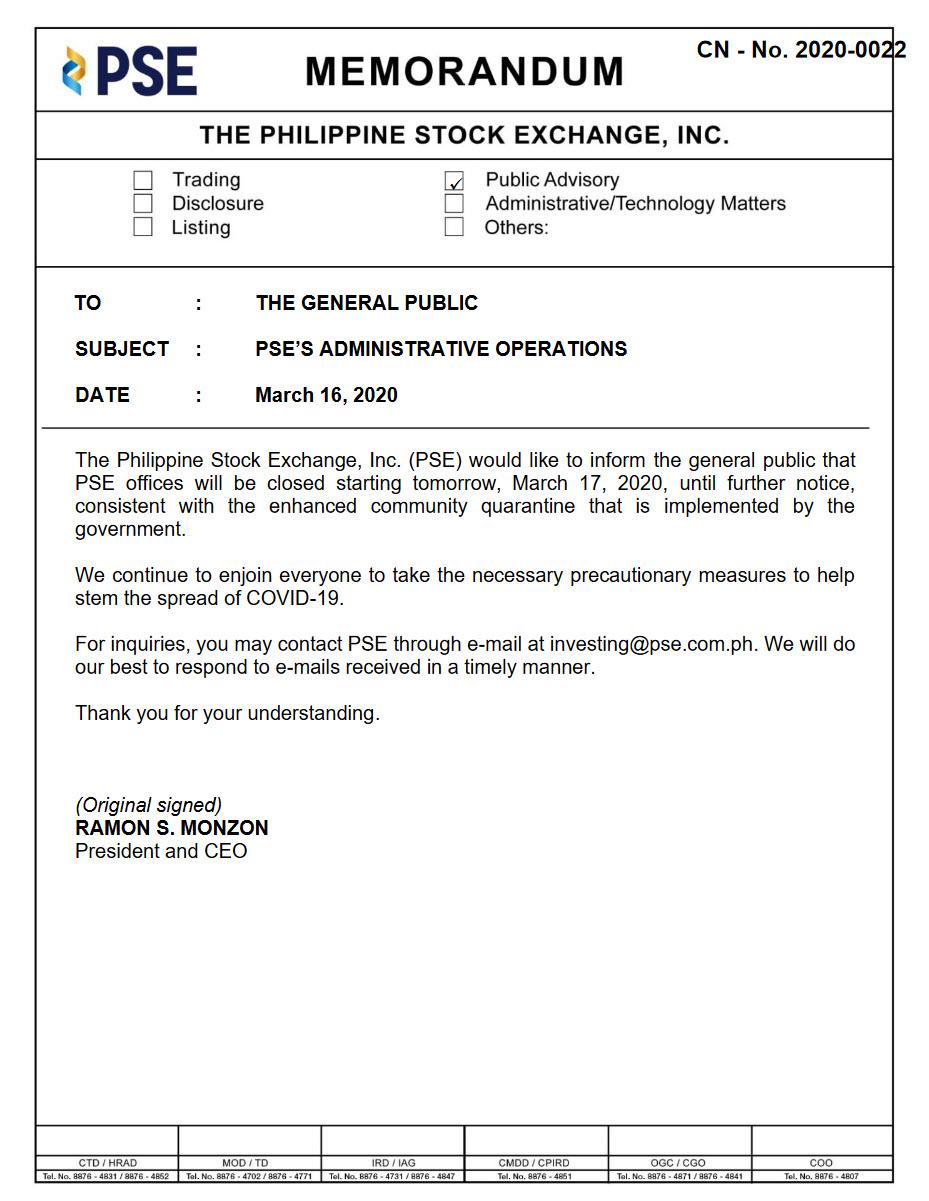

Philippines Is First Country To Halt Its Market “Until Further Notice”

Following two weeks of relentless market turmoil, traders were wondering which country’s stock market would be shut down first. Moments ago we got the answer when the Philippine Stock Exchange announced it is suspending trading “until further notice” after the country’s President Rodrigo Duterte expanded a month-long lockdown to the entire main island of Luzon.

“Mass transport suspension and work suspension in the private sector plus the mandate of the government to stay at home constrained us to suspend trading and clearing & settlement for now,” said PSE Chief Operating Officer Roel Refran, who surely welcomes the opportunity to take a break from the crash in the country’s stock market which has wiped out just over a third of market values in since the November highs.

Earlier on Monday, the CEO of Borsa Italiana, Raffaele Jerusalmi, denied rumors that Italy’s stock market would shut even as the rest of the country is effectively on lockdown, when Ansa quoted him as saying that future decisions on closing stock markets “at aggregate level” are in theory possible but would be up to governments acting collectively. Jerusalmi did not say any such moves were imminent or comment on whether they’ve been discussed at any level.

“If there was a decision at the global level, it could be done, but it is not up to us”, suggesting that the Philippine closure was a rogue decision, although now that one nation’s market is offline it is far more likely that the rest of the world will promptly follow in “coordinated fashion”, especially if Trump fails to spark a BTFD panic with his appropriately timed 3:30pm press conference today, timed strategically to coincide with the traditional last 30 minute market ramp.