Stocks, Bonds, & The Dollar Dumped On Dismal-Data & Trade-Tensions

A quadruple-whammy of not-awesome trade-related comments today spoiled the party…

0602ET *TRUMP TO RESTORE TARIFF ON STEEL SHIPPED FROM BRAZIL, ARGENTINA

1035ET *TRUMP WILL INCREASE TARIFFS IF NO CHINA DEAL, ROSS TELLS FOX

1200ET *TRUMP AIDE SAYS IT’S UP TO CHINA IF DEAL WILL BE MADE THIS YR

1230ET *CHINA TO RELEASE ‘UNRELIABLE ENTITY LIST’: GLOBAL TIMES

And then US Macro data poured cold water on China and EU economic hope as construction spending plunged and manufacturing ISM disappointed significantly.

Source: Bloomberg

But that ‘surprising’ surge in a government-provided survey of manufacturers in China was offered up as evidence that (despite US weakness) everything will be ok and the trough is in…

Chinese stocks clung to very modest gains overnight (trade headlines hit after the China close)…

Source: Bloomberg

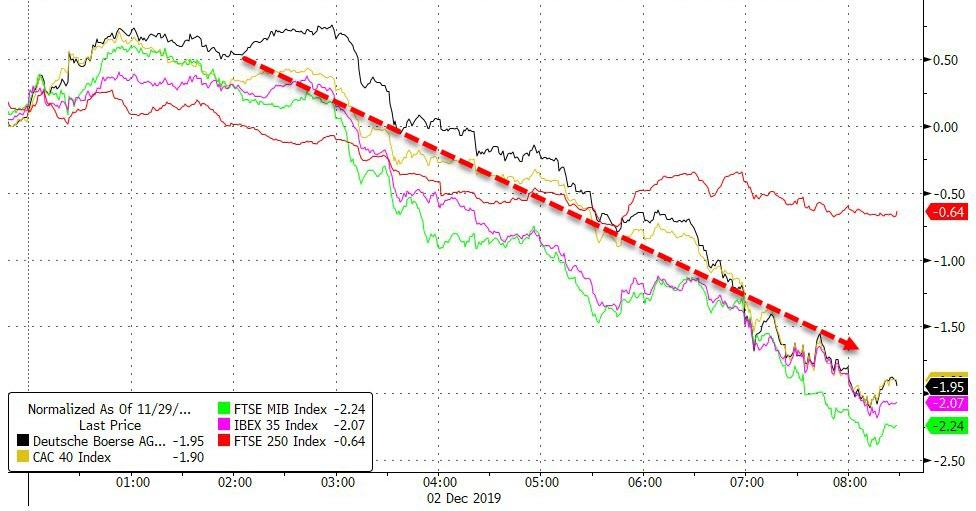

European stocks were hammered on trade turmoil (despite PMIs beating expectations)…

Source: Bloomberg

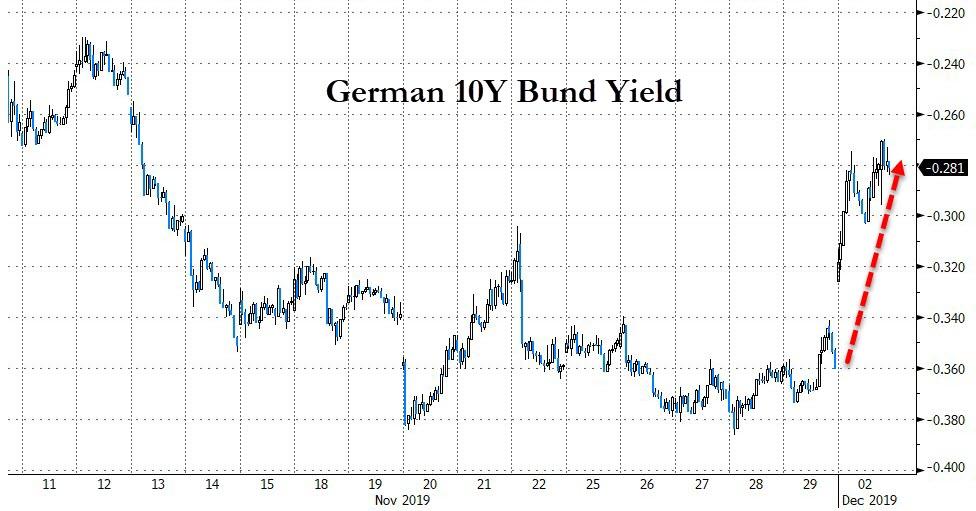

And European bonds were also down (in price) along with stocks (10Y Bunds +8bps)…

Source: Bloomberg

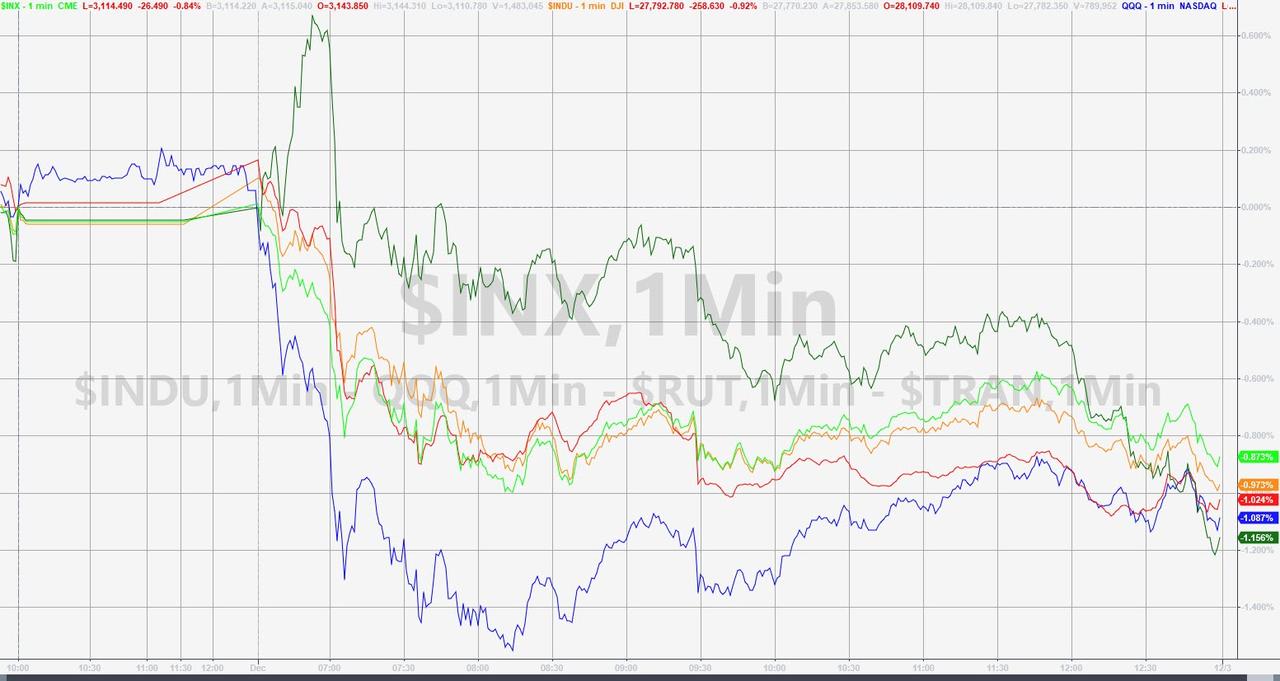

US equities suffered their biggest daily drop in 6 weeks…

Dow futures were down over 400 points from the overnight highs…

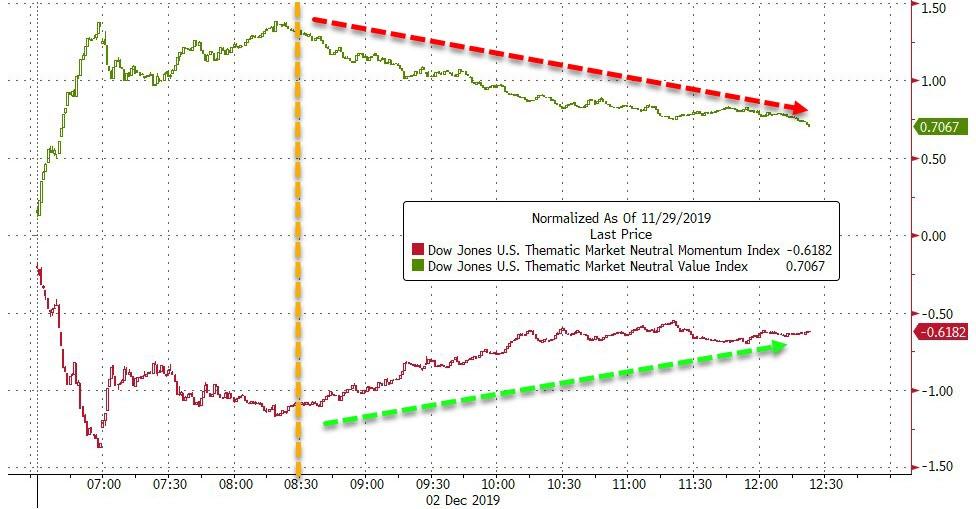

Momo was dumped at the open but the trend in value/momo reversed around the European close…

Source: Bloomberg

VIX spiked above 15 intraday but once again vol-sellers returned after Europe’s close…

Source: Bloomberg

Credit was smashed today (after last week’s insane surge)…

Source: Bloomberg

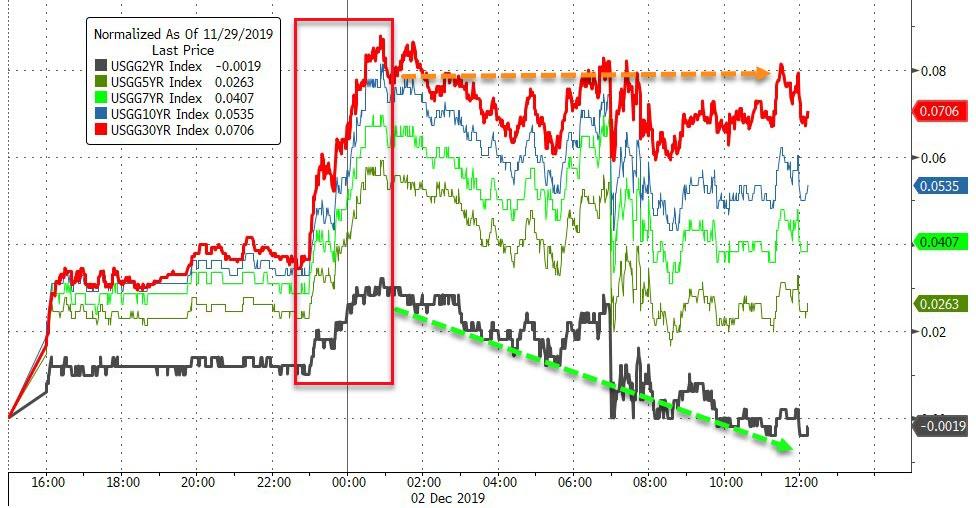

Treasury yields surged on the day, led by the long-end (2Y was marginally lower in yield)…

Source: Bloomberg

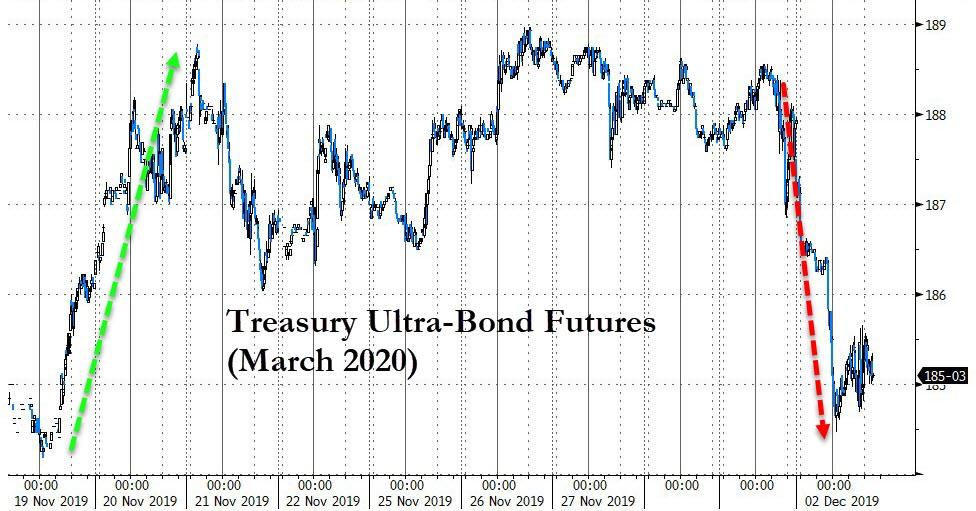

Most notably, the ultra-bond futures collapsed overnight (hitting a 3-point limit circuit breaker)…

Source: Bloomberg

And today saw a major steepening of the yield curve… (the yield curve move has the smell of rate-locks given the underlying macro data, but we will have to wait and see what the calendar looks like – high-grade dealers expect this week to bring $15b-$20b in supply. This is likely to be December’s busiest week, with just about $25b for the full-month in store, according to estimates — that’s $8b more than last year and in line with the $23b that priced in December 2017)

Source: Bloomberg

The dollar was dumped today (biggest daily drop in 6 weeks)…

Source: Bloomberg

…breaking down through its 50- and 100-day moving-averages…

Source: Bloomberg

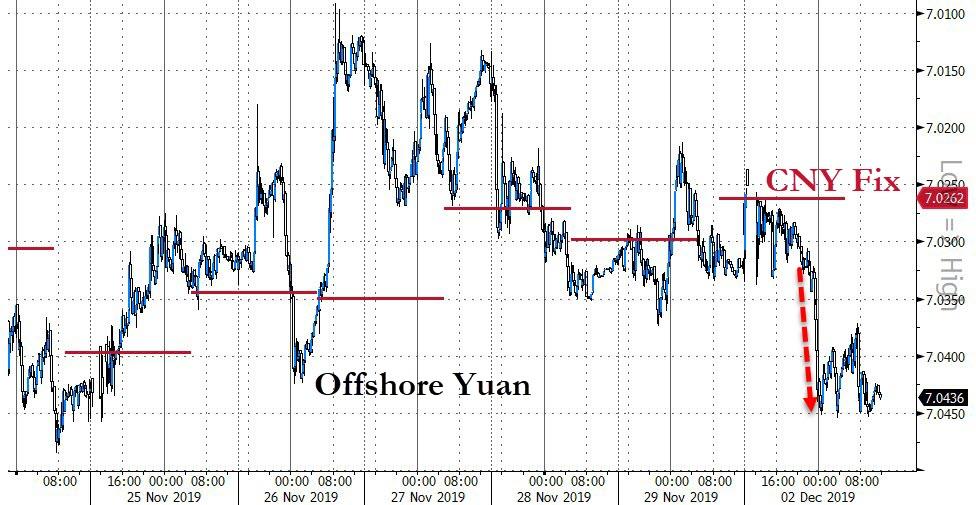

Yuan also lost ground as trade-deal hope faded…

Source: Bloomberg

Cryptos extended losses over the weekend and pushed lower still today…

Source: Bloomberg

Bitcoin has been unable to get back above $7400…

Source: Bloomberg

Gold, Copper, and Silver ended the day lower (despite a tumbling dollar) but oil popped on Saudi calls for more production cuts/extensions at OPEC (as its Aramco IPO looms)…

Source: Bloomberg

But, with regard to oil, it is still a lot lower than before Friday’s plunge…

“This whole week is going to be based on OPEC speculations,” said James Williams, president of London, Arkansas-based WTRG Economics.

All the precious metals are green for 2019, but palladium is by far the biggest winner…

Source: Bloomberg

Finally, today was the worst day for a balanced portfolio of stocks and bonds since mid-August…

Source: Bloomberg

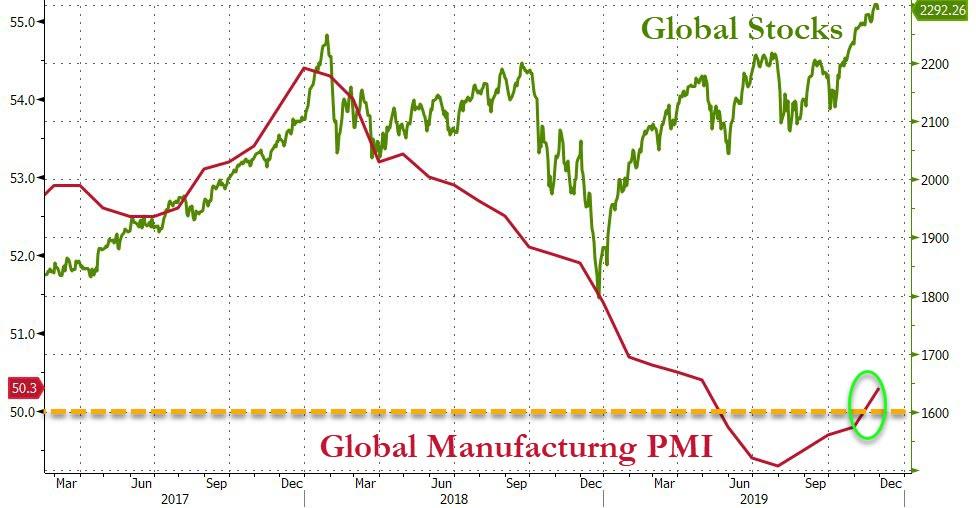

Additionally, as Bloomberg’s Garfield Reynolds notes, global equities are gliding serenely into the end of 2019, even in the face of a dire economic landscape. To justify an exuberance that looks anything but rational, global activity will need to turn around dramatically.

Source: Bloomberg

The 2019 FOMO rally’s resilience has taken it far enough in the face of a cloudy forecast. Any declines from here could get very steep indeed.

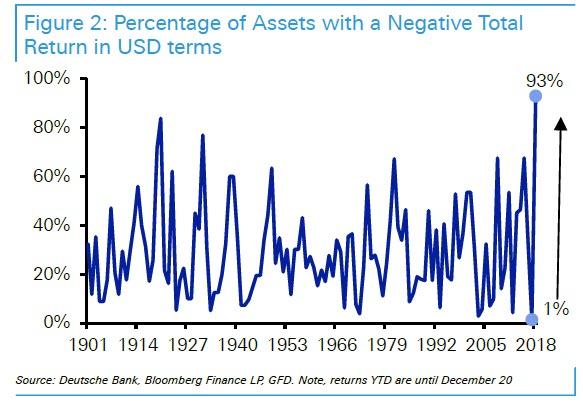

Every Single Asset Tracked By Deutsche Bank Is Up For The Year

What a difference a year makes.

It was last December, which incidentally was the worst December for US equities since the Great Depression, that we showed a remarkable chart: an astounding 93% of all assets tracked by Deutsche Bank were down for the year – worse than even the years of the Great Depression.

2018 would go on to close with a similarly deplorable record: of all assets, only cash posted a positive real return.

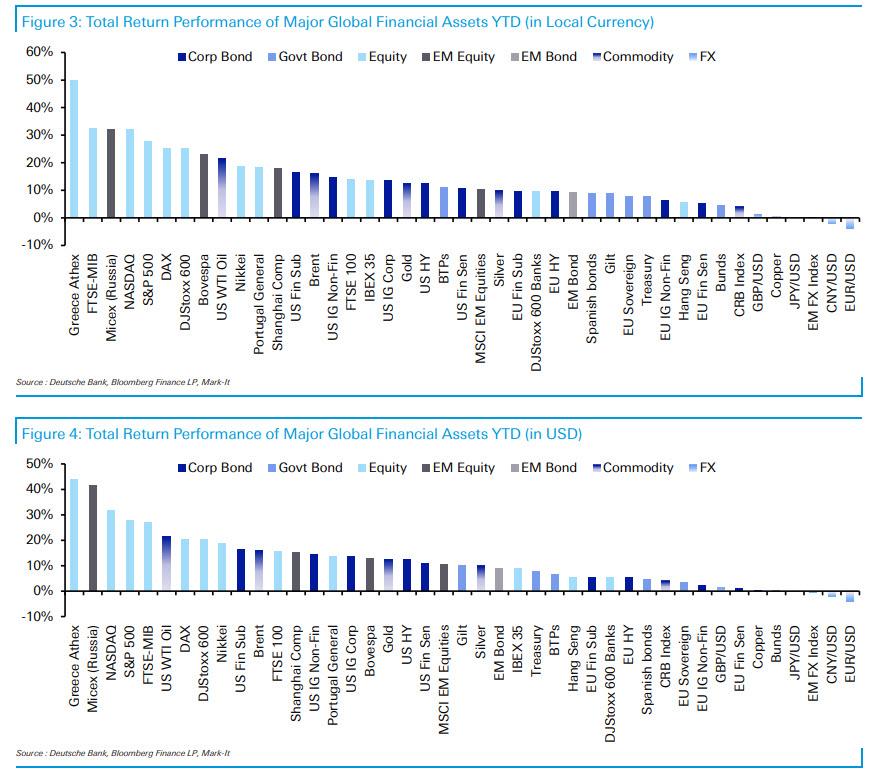

Fast forward 12 months when things couldn’t be more different, and with November now in the history books we have a performance mirror image on our hands: as Deutsche Bank’s Craig Nicol writes today, all 38 assets in its tracking universe have posted positive YTD returns in both local currency and dollar terms.

Equity markets still lead the way with notable mentions for the Greek Athex (+49.8%), FTSE MIB (+32.4%), MICEX (+32.3%) and NASDAQ (+31.9%). Credit markets are up anywhere from +5.2% to +16.5% with USD outperforming EUR. Meanwhile bond market returns continue to be led by BTPs (+10.9%) while Bunds (+4.4%) lag behind.

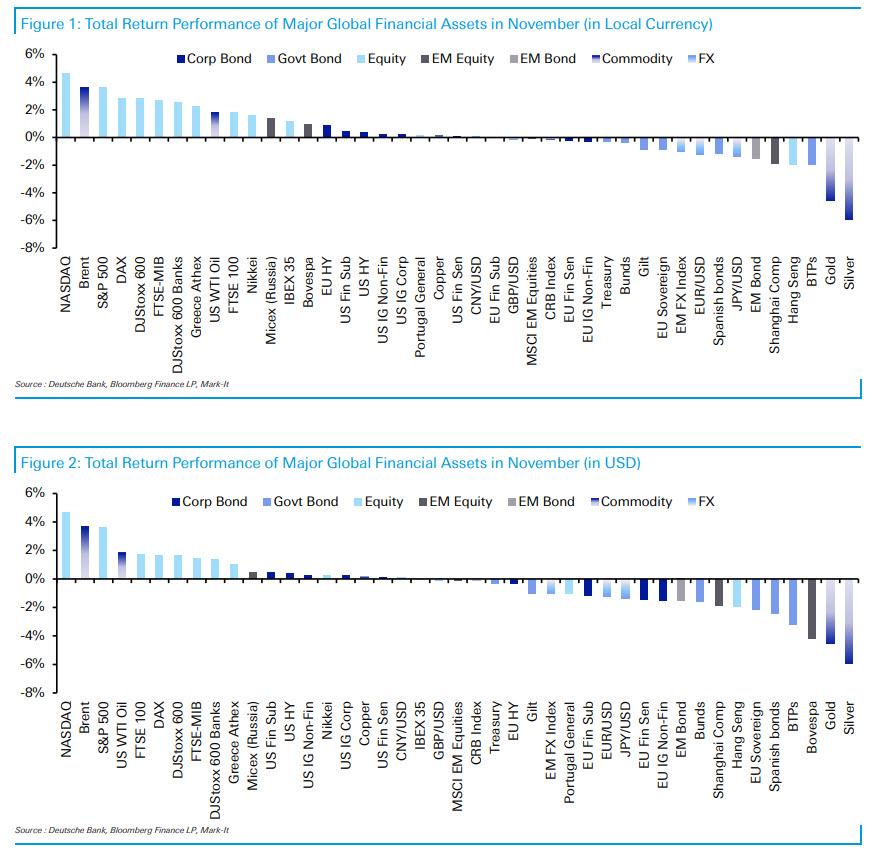

A big reason for this performance was the dramatic gains posted in November, a month which “proved to be another good one for risk assets as tentative signs of progress towards a “Phase 1” trade deal between the US and China fuelled sentiment.” That, and of course, it was the first full month of the Fed’s QE4.

Markets also took hope from the economic data and specifically the stabilization in the PMIs. As such of the 16 equity markets in DB’s sample, 13 closed with a positive total return in local currency terms. That of course included fresh new highs for the major US equity markets.

It was a slightly different story in fixed income markets however where higher bond yields acted as a bit of a headwind to returns. The majority of credit markets closed flat to slightly higher in total return terms however bond markets were broadly negative. As a result, when it was all said and done, out of the 38 assets in the bank’s sample 23 finished with a positive total return in local currency terms while 19 did so in dollar terms with the dollar appreciating versus the euro, yen and sterling.

That said, those assets which underperformed in November such as precious metals, BTPs, China stocks and sovereign bonds had benefited from an impressive return earlier in the year, so their YTD performance was still positive.

In terms of the details, the top of the leaderboard for equities was dominated by the US where the NASDAQ and S&P 500 returned +4.7% and +3.6% respectively. That means we’ve now seen positive total returns for both of these indices in 9 of the 11 months this year.

Meanwhile in Europe we saw the STOXX 600 return +2.9%, DAX +2.9%, FTSE MIB +2.7%, European Banks +2.6% and FTSE 100 +1.8%. Asia lagged with the Nikkei up +1.6% but the Shanghai Comp and Hang Seng down -1.9% and -2.0% respectively with the protests in Hong Kong clearly impeding the latter.

As for fixed income markets, Treasuries (-0.3%) and Bunds (-0.4%) finished with slightly negative total returns while Gilts (-0.9%), Spanish Bonds (-1.2%), EM bonds (-1.6%) and BTPs (-1.9%) suffered heavier losses. That acted as a headwind to IG credit with US IG non-fins retuning +0.3% and EUR IG non-fins -0.3%. High yield fared slightly better, returning +0.9% for EUR and +0.4% for US. Finally, commodity markets book-ended the leaderboard last month with Brent returning +3.7%, while Gold and Silver returned -4.6% and -6.0%. Copper finished +0.2%.

With “trade deal optimism” expected to continue well into 2020 and perhaps until the presidential election, alongside the Fed’s NOT QE, there are few indications that anything can change this trend as we close out the decade.

The early winter holidays are notorious for giving people the blues, but as the last Thanksgiving leftovers slide into the stockpot, the Democratic Party was put on suicide watch. Is the ghost of Jeffrey Epstein in charge? It’s a little late to call an exorcist.

The gun pointed at the Democrats’ head now is a stubby little low-caliber weapon in the person of Jerrold Nadler, chairman of the House Judiciary Committee, who has only grazed the party’s skull in two previous misfirings. The third time, the old saying goes, may be the charm.

When Mr. Nadler entertained Special Counsel Robert Mueller in July, he succeeded spectacularly in discrediting Mr. Mueller, and the inquisition he rode in on. It was the worst public demonstration of aphasia since William Jennings Bryan had a stroke at the Scopes Trial in 1925. Mr. Mueller’s pitiful performance put to rest the last sticky tendril of hope that his tortured report might avail to cast out the arch-demon in the White House. Even the Republicans on the dais seemed to feel sorry for him. True to his character as a schoolyard sap wearing a “kick me” sign on his back, Mr. Nadler just waddled away in a fog of bamboozlement, hitching his pants up to his sternum, to plot his next foolish move.

Which was to haul former Trump campaign manager Corey Lewandowski into the committee in September. Mr. Lewandowski’s performance was the equivalent of watching poor Mr. Nadler get hitched to the rear bumper of a Lincoln Navigator and dragged over several miles of broken Coke bottles. And yet, ever-sturdy, like one of those plastic punching dummies with all its weight on the bottom, Mr. Nadler just popped back up, adjusted his “kick me” sign, and moved on to his next folly: the current comedy of errors around impeachment.

Really, the only question now is what new way will Mr. Nadler find to humiliate himself and mortify his party? Opening testimony this week will be supplied by a panel of Woke constitutional law professors who will attempt to tease out some hermeneutic legal basis for an impeachment other than actual misdeeds. They’ll surely settle on thought-crime, since there is nothing else. Whose idea was it to hit the snooze button just as the curtain goes up on the show?

Next will come a mighty hassle over whether the minority can call witnesses of its own choosing. Ranking member Doug Collins (R-GA) has already asked for an appearance by Adam Schiff, chair of the House Intel Committee, whose procedural shenanigans last month embarrassed anyone with a vestigial memory of Anglo-American due process. Some folks think that Mr. Schiff has got some ‘splainin’ to do about the predicating circumstances of his star chamber spectacle. He is, in fact, a fact-witness to all that, on top of being the issuer today of his own committee’s report on all that, and therefore susceptible to public examination — especially in a train of proceedings as grave as impeachment. If Mr. Nadler enables Mr. Schiff to slither out of testifying, there will be hell to pay, and in the not-so-likely prospect of an actual impeachment trial in the senate, it would be paid there as an unleashed defense goes for Mr. Schiff with pithing needles and thumbscrews of genuine interrogation.

Then there is the “Whistleblower,” this would-be pimpernel of perfidy hiding behind Adam Schiff’s apron under the false assertion that he is entitled to everlasting anonymity. What an idea under our system of jurisprudence! In fact, contrary to Mr. Schiff’s public pronouncements, there is no law that states what he claims — one of several things Mr. Schiff can be called to account for. And that is even if you accept the dishonest proposition that the fugitive who started this fiasco even was a whistleblower, rather than a rogue CIA officer acting on explicitly illegal political motives to interfere in the 2020 election. The CIA, you must know, is forbidden by charter and statute from operating against American citizens, including the president of the United States. Under the circumstances, the so-called “Whistleblower” might fairly be accused of treason.

Has anyone failed to notice that one of the “Whistleblower’s” attorneys, Mark Zaid, tweeted notoriously on January 30, 2017 that “Coup has started. First of many steps. #rebellion. #impeachment will follow ultimately. #lawyers.” Mr. Zaid later explained, “I was referring to a completely lawful process.” Yeah, sure. I think he meant a completely Lawfare process. Of course, the engineered “Whistleblower” escapade was only the latest (perhaps the last) chapter in the annals of nefarious events and actions carried out far-and-wide by several government agencies for three years, and by many officials working within them, and not a few freelance rogues in their service. There is no more accurate way to describe all that except as a coup. The authorities looking into all that have not been heard from yet. The portentous silence is making a lot of people in Washington edgy.

If the various House committees have put the Democratic Party on suicide watch, then something even more deadly is lurking just offstage. Hillary Clinton is making noises about jumping into the 2020 election. She senses opportunity as Joe Biden goes pitifully through the motions of running for office to avoid prosecution for his international grifting operations as Veep. Think of Hillary as the cyanide capsule that the party might actually choose to bite down on as the year ominously turns.

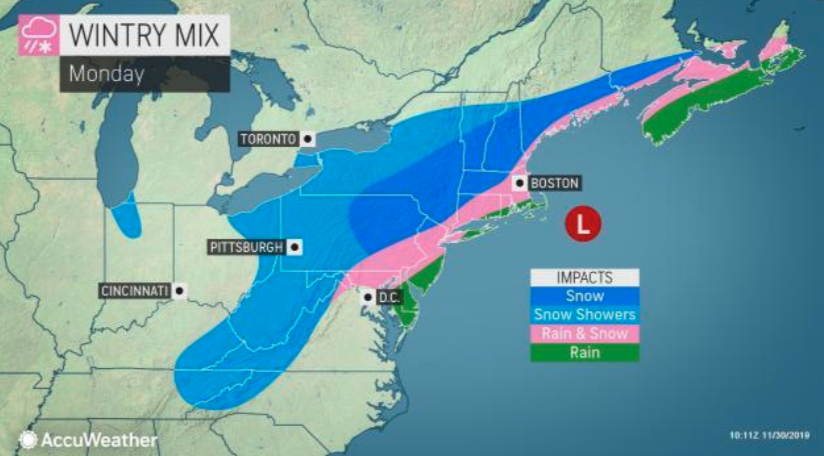

It’s been well over a week since we’ve been reporting on two significant weather disturbances that caused severe headaches for tens of millions of Americans from coast to coast. The latest batch of wild winter weather continues to torment millions in the Northeast. It could make commuting this evening for drivers in Philadelphia to New York City and Boston a living hell.

Evening Commute Nightmare?

Locally heavy snowfall possible tonight in eastern PA, NJ, NYC, and southern New England…

Through the workday, rain and snow showers will switch to snow, could see 1-3 inches in NYC and 4 to 6 inches in Boston by the evening, meteorologist Bob Oravec of the National Weather Service’s Weather Prediction Center told Reuters.

The heaviest bands of snow will be seen this afternoon in Upstate New York, Pennsylvania, northwestern New Jersey, Connecticut, Massachusetts, southern Vermont, southern New Hampshire, and Maine, Oravec said. He added that some regions could receive more than one foot of snow.

“When it’s all said and done, some areas will have over 2 feet of snow from this storm, especially over parts of the Poconos and Catskills,” Oravec said.

Meanwhile, the Mid-Atlantic region has seen a mix of rain, snow, and ice. Mostly rain has been seen in the Baltimore–Washington metropolitan area.

The worst conditions could be seen around the rush hour period for NYC to Boston when the storm is expected to ramp up the intensity. The snow is expected to last through the overnight.

The winter storm is expected to dump nearly a foot on much of Maine in the overnight. The storm is expected to exit the Mid-Atlantic and Northeast regions by Tuesday.

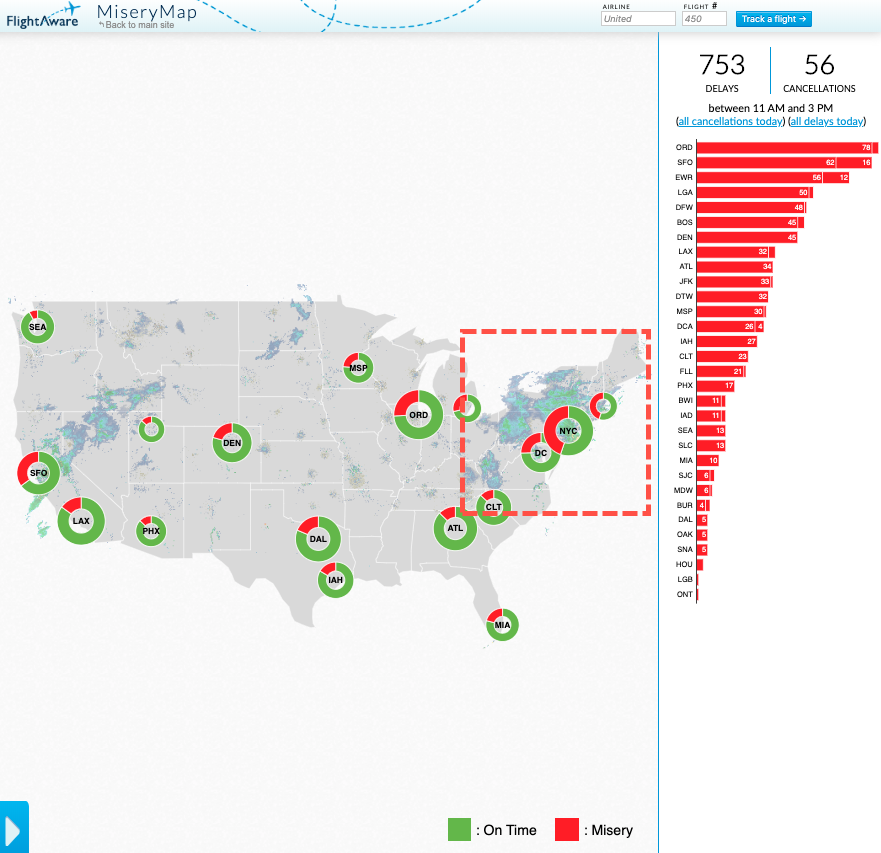

Reuters reports that 1,500 cancellations and delays were posted for airports across the country by late morning. The most affected airports were San Francisco, Albany, Boston, Chicago, and Newark.

As of the early afternoon, Flight Aware posted 753 delays and 56 cancellations across the country. A majority of the delays and or cancellations were seen at Mid-and Northeast airports.

Both storms had huge impacts on the US and came at the worst time during one of the busiest shopping holidays of the year. We assume retailers, who saw foot traffic plunge this year across Black Friday, will blame the weather for their sales slump.

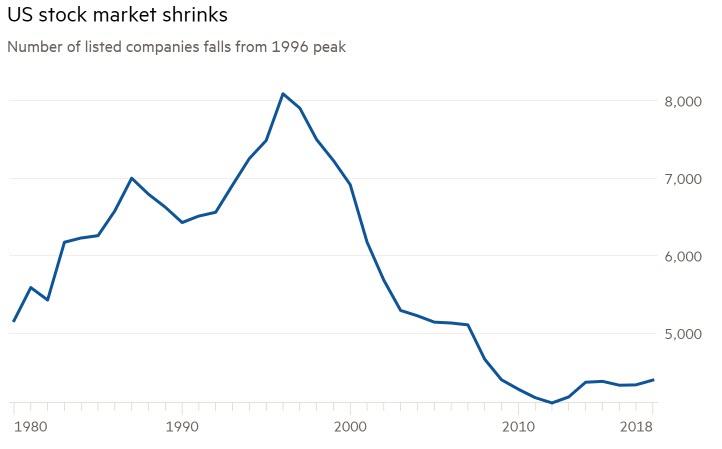

Since the mid-1990s, the number of companies listed on US stock exchanges has been steadily shrinking. There are currently just over 4,000 companies listed, up from the 2012 low but way down from a peak of more than 8,000 in 1996. Europe has not been immune; only 84 companies have listed this year, the lowest in a decade and the lowest by deal value since 2013. European capital markets have always been less equity-centric than the US, but even here the number of listings has shrunk by 29 percent since 2000.

Source: World Bank, Financial Times

In the post–financial crisis period, three factors have driven the retreat of listed equity:

the rise of private equity (an industry that is estimated to be sitting on more than $2 trillion in capital awaiting new opportunities),

the slower pace of new companies launching on public markets (due to the availability of private venture capital),

and mergers of existing listed companies. Behind these factors lies a more powerful force: artificially low interest rates.

In a low–interest rate environment, the appeal of debt financing increases relative to equity. This seemingly benign influence has profound implications for capital markets and the economy more broadly. By means of debt finance, earnings per share can be enhanced without the need for productivity gains. For the executives who direct those companies, the incentive to borrow externally, rather than improve internally, increases as debt-financing costs decline. Conversely, in a rising–interest rate environment these same executives are incentivized to improve the internal efficiency of their enterprises. To this extent, higher financing costs can contribute to improved productivity.

Financing costs have generally been falling since the 1980s. During this same period, executive compensation, especially via the award of stock options, has risen dramatically. Owning call options gives an investor a different incentive from a stockholder. The option holder’s preference is for capital over income; high dividends directly reduce capital value. Executive holders of stock options favor lower dividend payouts and higher earnings per share.

Falling interest rates have also impacted income-seeking investors. Faced with declining returns from fixed- and floating-rate investments, these investors have been forced to accept higher risk in the form of increased duration, greater credit risk, or leverage.

Duration risk is unique to fixed-income investment. All other things equal, the longer the maturity of a fixed-rate bond, the longer the duration — and therefore the more sensitive the price to a given change in the yield to maturity. As short-term interest rates have approached zero, the normally upward-sloping yield curve has flattened. In developed markets, this has been exacerbated by the central bank policy of quantitative easing. By this process, income investors are forced to look elsewhere for returns.

If the return from extending the duration of your portfolio has diminished, an alternative source of yield can be found by the purchase of less creditworthy debt. The insatiable investor’s thirst for yield has been quenched, at least in part, by private equity, venture capital, and leveraged-buyout funds that have securitized their borrowings. Demand has also been met by a wide array of corporate borrowers, many of whom issue debt simply to fund share buybacks. This debt may take the form of fixed- or floating-rate bonds or loans.

For a small group of income investors, the alternative to fixed coupons or floating-rate notes is the outright purchase of equity. In relative terms, this alternative has disappointed; income stocks have generally underperformed growth stocks during the last few years, in part because capital appreciation pushes stock prices higher, which attracts momentum investors. A stronger influence, however, is lower interest rates, which make higher price/earnings multiples more manageable. In addition, low rates encourage expectations of lower returns; they also make investors more fee conscious, favoring index-tracking products over discretionary funds.

Where Are We Now?

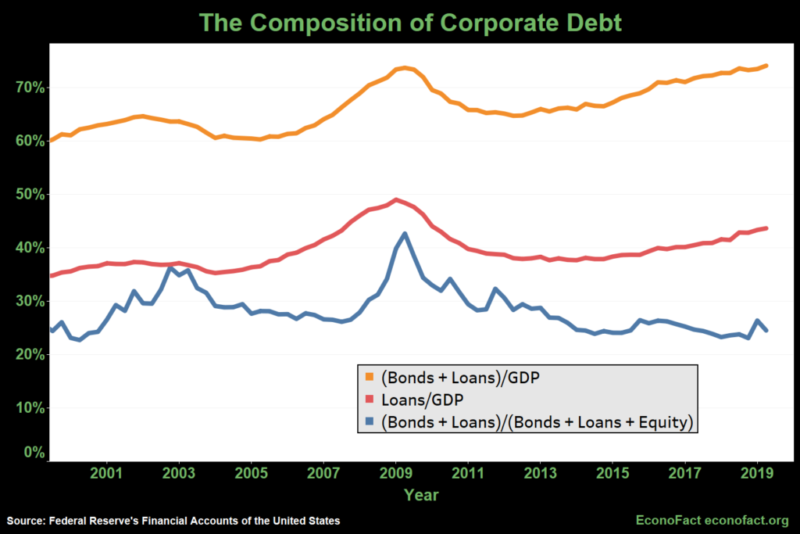

To recap, the breadth of the listed stock market is in long-term decline. Debt finance is cheaper than equity finance. For corporate executives, share buybacks are preferable to capital investment. Corporate debt levels are at or near all-time highs. The credit quality of the outstanding debt is deteriorating.

Further cause for concern is the changing makeup of debt. While corporate bond issuance has been growing, the corporate loan market has been in the vanguard of the expansion. The chart below shows the changing relationship between bonds and loans.

Source: EconoFact, Federal Reserve

The level of debt relative to GDP may be at new highs, but the cost of servicing the debt interest is relatively low, due to historically low official interest rates. The real risk in a recession is that credit spreads widen even as official rates are eased. As growth slows, US Treasury bonds may reach make new highs but lower-rated bonds and loans will still be sold. The credit intermediation process relies on the banks continuing to lend, but banks are notoriously procyclic, pulling in their horns just when they are needed most.

The current environment is not entirely negative. Robust corporate profits, during the long, slow recovery, mean that debt as a share of the total firm-financing mix is much lower today (25 percent) than it was during the 1980s and early 1990s (50 percent). The debt mix has tilted, however, toward floating-rate loans rather than fixed-coupon bonds. The weakest link for financial markets today may be found among leveraged loans and their investors.

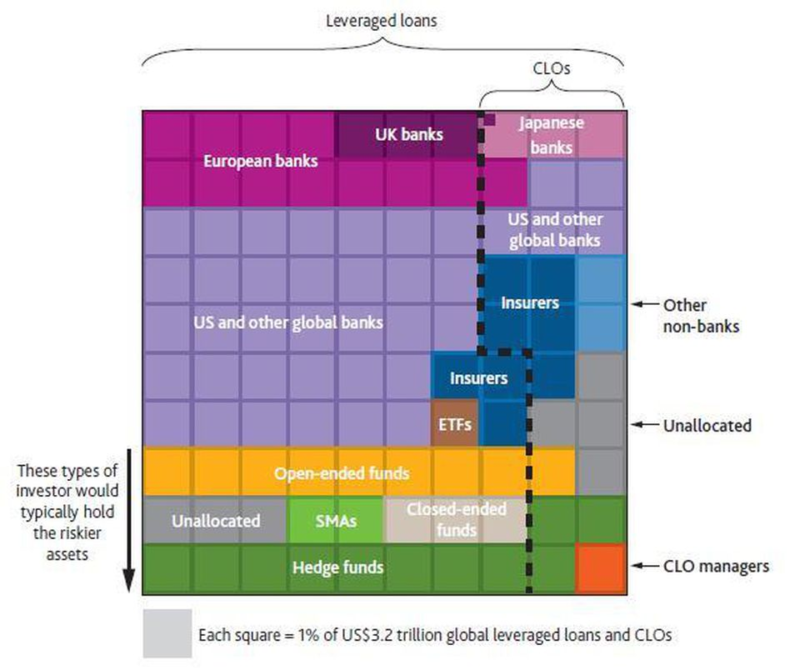

The principal buyers of leveraged loans are banks and insurance companies. The table below shows the current mix.

Source: Bank of England

As the table reveals, many of the higher-risk tranches of loans are purchased by open-ended mutual funds or ETFs, but a substantial proportion, especially those with lower risk, are held in collateralized loan obligations (CLOs). CLOs are, generally, floating-rate tradable securities backed by a pool of, usually, first-lien loans of corporations. Often these loans have poor credit ratings, many emanating from private equity, venture capital, and leveraged-buyout transactions. On their own, these leveraged loans may rank below investment grade, but, by bundling them together with better-quality loans, CLO managers contrive to turn base metal into gold.

If this sounds remarkably like the collateralized debt obligations (CDOs) that harbored covenant-lite subprime mortgages, which precipitated the financial crisis of 2008, then you would not be too far from the mark. CLOs do not contain mortgages or credit default swaps, but they do rely on the assumption that a diversified pool of loans has an inherently lower credit risk than the loan of an individual corporation with the same credit rating. Issuers argue that unlike the individual “liar loans” at the heart of the subprime-mortgage debacle, CLOs contain loans of corporations that have been audited and these corporations are from a wide range of industries. Suffice it to say, auditors can be deceived and recessions sink all ships.

CLOs are also a challenge for investors to value. CLO managers actively adjust their portfolios, and the risk profile is in a constant state of flux. These are opaque investments that are hard to evaluate and difficult to liquidate.

It is not all gloom; despite rating downgrades, CLO defaults are at a seven-year low of 3.42 percent. Investors may not be able to get out, but they should get paid. Or perhaps not. According to an October article in the American Banker,the loans of more than 50 companies have seen their prices decline by more than 10 percent. Moody’s, the rating agency, admits that more than 40 percent of loans are rated B3 or below. While CLOs, by some estimates, hold more than half of all loans, most are not mandated to hold more than 7.5 percent of CCC-rated paper, since CCC is below investment grade.

In a recent post from the Bank of England (“How Large Is the Leveraged Loan Market?”), the authors estimate that there are more than $2.2 trillion of leveraged loans outstanding worldwide, of which $1.8 trillion are denominated in US$. The chart below shows (left-hand side) the speed at which the market has grown and (right-hand side) the increasing leverage of the overall market together with the alarming rise in covenant-lite issuance.

Source: BIS

It is some comfort to know that central banks and financial regulators are cognizant of the potential systemic risk: they may yet contrive to avert a crisis. Covenant-lite loans, however, remain a near and present danger; they constitute 80 percent of issuance, and, by some estimates, as much as 29 percent of investment-grade loans are at risk of downgrade to CCC. If those downgrades come to pass, CLOs’ managers will be forced to liquidate in concert.

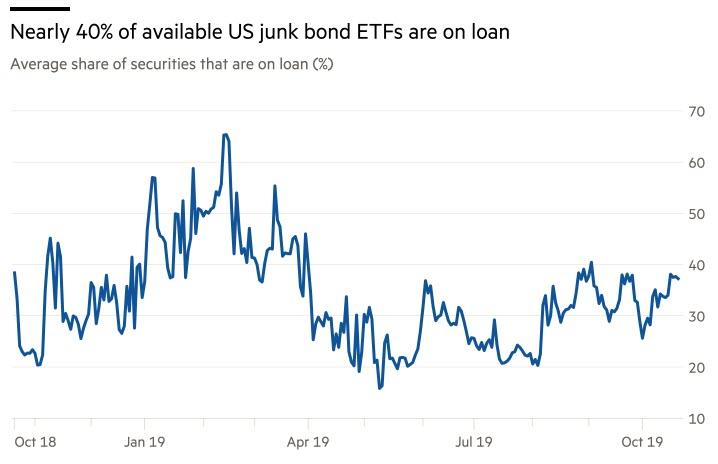

The natural buyers of less creditworthy leveraged loans have been notably absent of late. Leveraged-loan mutual funds and ETFs have seen redemptions for most of the past year. Insurers and banks are mostly full up, and the underwriting banks have been saddled with a large proportion of recent issues that failed to find buyers. Hedge funds are not stepping in to fill the void. Instead they are short-selling high-yield bond ETFs. Short exposure is down from the highs seen in Q1 2019 (which followed the high-yield rout of Q4 2018, when 25 percent of high-yield ETFs were liquidated), but around 40 percent of the market is now out on loan. The chart below highlights the recent change in appetite.

Source: Financial Times, Astec Analytics

The size of the high-yield bond ETF market is small (estimates range from $34 to $60 billion) and the cost of borrowing stock to fund short exposure is relatively high, but there is more than $500 billion of high-yield bond mutual funds that could follow. The liquidity mismatch between the exchange-traded ETFs and mutual funds on the one hand, and the underlying securities on the other , should not be underestimated. The total outstanding issuance of high-yield bonds is around $1.2 trillion, added to which the risk of contagion spreading to loans and CLOs cannot be ruled out.

Back in the loan market, it seems, the rating agencies are finally beginning to confront reality. S&P recently announced that the number of loan issuers rated B- or lower, referred to as “weakest links,” rose from 243 in August to 263 in September. Notwithstanding the significant increase in the number of issuers, this is still the highest figure recorded since 2009.

The Federal Reserve has been proactive, cutting rates even as unemployment data made fresh lows. In the near term, some headline measures of inflation have increased, but the amount of debt is so vast as to be almost self-righting; any hint that the Fed may raise rates to head off inflation will see stocks fall and credit spreads widen. The effect of these market moves on expectations for economic growth will be negative; commodity prices will decline, inflation will stall, and, provided the Fed moves swiftly enough, a full-blown credit crisis may be averted. Nonetheless, as rates approach the zero bound, the central bank has progressively less room for maneuver.

At the risk of repetition, in the longer term the deleterious effect of artificially low interest rates discourages capital expenditure in favor of debt issuance to fund stock buybacks. It undermines productivity and reduces the long-run rate of economic growth.

The number of stock market listings will continue to decline while the sustainable level of price-to-earnings ratios will rise due to the diminishing supply. With interest rates near zero, stocks will be supported: there are few viable investment alternatives in public markets. Income inequality will rise in tandem with the stock market, as will the ratio of debt to equity.

If governments choose to adopt a fiscal rather than a monetary solution to the lack of economic growth (and I am not advocating negative interest rates), they will pile even more debt onto an already over-encumbered marketplace.

Given the demographic headwinds facing most developed countries, consumption demand is likely to remain lackluster for the foreseeable future. Inflation and interest rates are unlikely to rise in this scenario, while corporate earnings growth will be forced to rely on financial alchemy rather than sustainable productivity.

Source: Bloomberg

Artificially low interest rates are hollowing out the productive capacity of the economy. The price of stocks and bonds may remain exalted, but this is not a sign of economic health.

Trader: What We’ve Seen In The Past Two Years Is At Odds With Everything

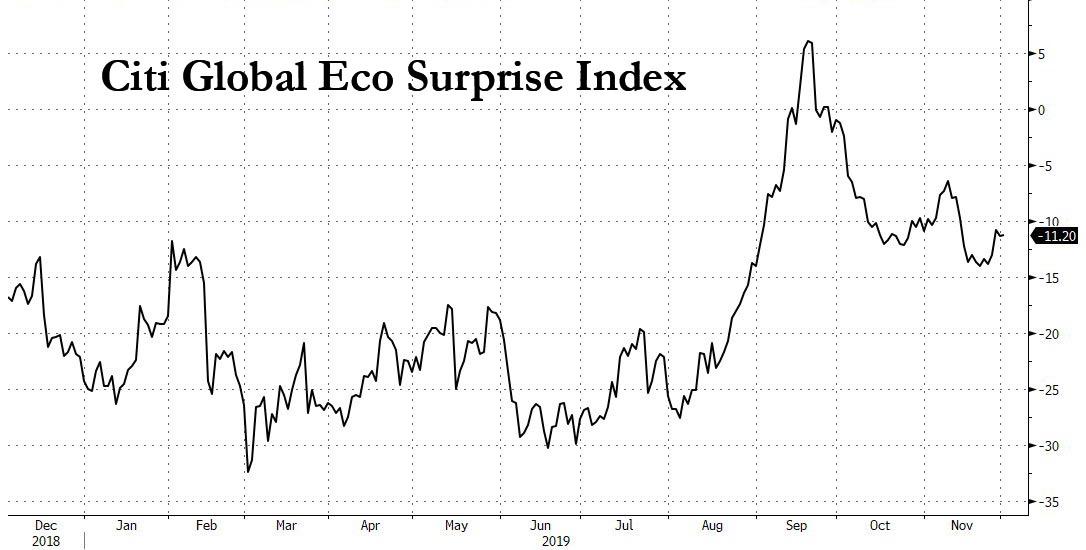

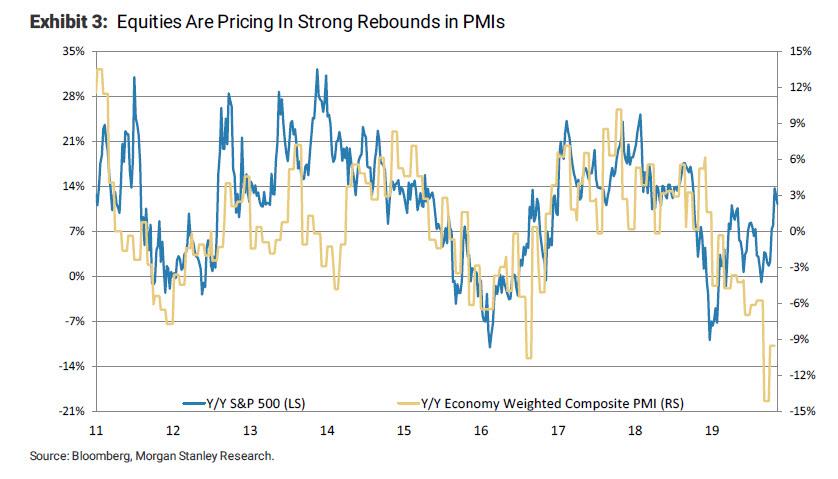

Global equities are gliding serenely into the end of 2019, even in the face of a dire economic landscape. To justify an exuberance that looks anything but rational, global activity will need to turn around dramatically.

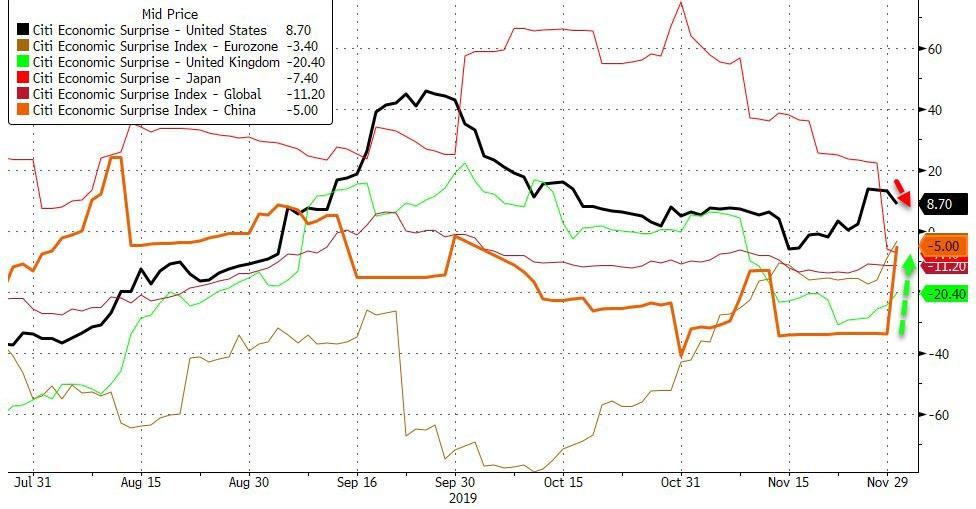

After a brief moment back above zero, Citigroup’s global economic surprise gauge has dropped back into negative territory

Maybe that’s why markets have been so eager to celebrate data beats such as U.S. GDP and China Caixin PMIs, despite indicators remaining at anemic levels. Shockingly poor releases last week like the South Korean and Japanese industrial output, or the Chicago PMI were shrugged off as revealing nothing new. [ZH: today’s dreadful ISM however was not as easily overlooked].

While the overall tone of the data being released is far more stable, the tinge of green in the economic landscape is more redolent of a stagnant swamp than shoots ready to sprout.

Just look at 3Q U.S. GDP. The 2.1% second reading beat expectations, sure, but it isn’t anything to get hugely excited about. Economists forecast the U.S. will expand less than 2% in each of the next two years — the slowest pace since the 2009 recession.

Meanwhile, global GDP sagged dramatically last year as stocks melted down. Since then, activity has stayed depressed even as equities rebounded. This behavior is at odds with past episodes – typically growth and stocks bounce back together after such a decline.

Hence the stubborn bid for bonds, which have been reflecting a fragile global economy all year. That’s why swaps are still pricing in rate cuts for many major central banks.

Recent equity rallies were largely driven by optimism the U.S. and China will reach a phase-one deal, so much of the trade upside has been priced in. A milquetoast accord, or more prevarication could lead to a savage reversal. Even a strong agreement would leave stocks still in need of a data rebound to justify further gains.

If economic prospects darken, central banks are just about out of ammunition. Further Fed easing from here would signal the previous insurance cuts failed to head off recession. The 2019 FOMO rally’s resilience has taken it far enough in the face of a cloudy forecast.

Any declines from here could get very steep indeed.

Have you heard? The Democrats are going to fix the student loan mess! They’ve brought up the issue in almost every Democratic Party presidential debate. All we need is a good government program and we can easily solve this $1.64 trillion problem.

Never mind that government programs caused the problem in the first place.

The student loan bubble continues to inflate. Student loan balances jumped by $32.9 billion in the third quarter this year, pushing total outstanding student loan debt to a new record. Student loan balances have grown by 5.1% year-on-year.

Over the last decade, student loan debt has grown by 120%. Student loan balances now equal to 7.6% of GDP. That’s up from 5.1% in 2009. This despite the fact that college enrollment dropped by 7% between 2010 and 2017, with enrollment projected to remain flat.

In a nutshell, we have fewer students borrowing more money to finance their educations.

Before the government got involved, college wasn’t all that expensive. It was government policy that made it unaffordable. And not only did it manage to dramatically drive up the cost of a college education, but it also succeeded in destroying the value of that degree. Peter Schiff summed it up perfectly:

Before the government tried to solve this ‘problem,’ it really didn’t exist.”

Peter isn’t just spouting rhetoric. Actual studies have shown the influx of government-backed student loan money into the university system is directly linked to the surging cost of a college education.

Millions of Americans carrying this massive debt burden is a big enough problem in-and-of-itself. But it becomes an even more significant issue when you realize the American taxpayer is on the hook for most of this debt. Education Secretary Betsy Devos admitted that the spiraling level of student debt has “very real implications for our economy and our future.”

The student loan program is not only burying students in debt, it is also burying taxpayers and it’s stealing from future generations.”

This is yet another bubble created by government. Despite the campaign rhetoric coming out of the Democratic Party presidential primary debates, it seems highly unlikely Congress will do what is necessary to address the growing student loan bubble. And the Democrats’ solution seems to be to simply erase the debt – as if you can just make more than $1 trillion vanish without serious implications.

Like all bubbles, this one will eventually pop.

The bottom line is that the student debt bubble will ultimately impact US markets and average Americans.

* * *

You can learn more, and how to prepare yourself, in Peter’s white paper The Student Loan Bubble: Gambling with America’s Future. Get the free download HERE.

In Stuttering, Stumbling Address Christine Lagarde Vows To Link QE To Climate Change

In her much anticipated first appearance as president of the ECB before at the European Parliament, Christine Lagarde asked EU lawmakers on Monday to give her time to “learn the ropes” of her new job and to reshape the ECB’s monetary policy in what is likely to be a lengthy policy review, and said the ECB will be “resolute” in restoring euro-zone price stability, while stressing that an upcoming strategy review will be wide-ranging, including climate change as well as inflation.

“The ECB’s accommodative policy stance has been a key driver of domestic demand during the recovery, and that stance remains in place,” she said ahead of her first monetary policy meeting at the ECB on Dec. 12.

Christine Lagarde arrives to testify before the European Parliament’s Economic and Monetary Affairs Committee; December 2, 2019. Photos: Reuters.

Similar to the Fed, the former convicted criminal and IMF chief who left Argentina near bankruptcy, has promised an overarching review of ECB business ranging from how it defines its inflation objective to whether it includes a fight against climate change among its responsibilities.

“I’m indeed trying to learn German but I’m also trying to learn central bank language,” Lagarde, a former lawyer told the European Parliament’s Committee on Economic and Monetary Affairs in a regular hearing. “So bear with me, show a little bit of patience, don’t over-interpret, if I may say,” said a seemingly nervous Lagarde, who often diverged from the text of her prepared speech and stumbled at times, leaving out phrases or repeating herself.

Lagarde said that a key focus of the review would be to determine whether its objective of keeping inflation at close to but below 2% was still valid, given changes in the global economy.

Speaking a day after it was unveiled that the Fed – which is also in the process of reviewing its policies – was considered launching a new rule that would let inflation run above its 2% target to make up for lost inflation, Lagarde also said the review would look at whether the target should by symmetric, meaning it should be used to tackle both low and high inflation and not just the latter, if the ECB should have leeway in reaching that target, or whether there should be a tolerance band around it.

Of course, just like the Fed, the issue for the ECB is two-fold:

i) ignoring soaring asset price inflation which is where central banks have blown the biggest asset bubble in history, and

ii) failing to properly measure consumer price inflation, instead applying a spate of adjustments that make it seem inflation is subdued when in reality for many prices are rising so high, the cost of living is no longer bearable.

Then there is the question of whether targeting higher prices is sensible at a time when the middle class is shrinking across the developed world. As a reminder, back in June, a Bloomberg report looked at the stark disconnect between Fed policy and well, everybody else but banks and the 1%.

While the Fed sees low inflation as “one of the major challenges of our time,” Shawn Smith, who trains some of the nation’s most vulnerable, low-income workers stated the obvious: people don’t want higher prices. Smith is the director of workforce development at Goodwill of Central and Coastal Virginia.

In fact, he said that “even slight increases make a huge difference to someone who is living on a limited income. Whether it is a 50 cents here or 10 cents there, they are managing their dollars day to day and trying to figure out how to make it all work.’’ Indeed, as we discussed in “How The Fed’s New Monetary Policy Will Crush America’s Poorest“, it is the low-income workers – not the “1%”ers, who are most impacted by rising prices, as such all attempts by the Fed to “help” just make life even more unaffordable for millions of Americans.

None of this was a concern to Lagarde, however, who said taht the ECB’s “strategy review will be guided by two principles: thorough analysis and an open mind,” Lagarde told lawmakers. “This will require time for reflection and for wide consultation.”

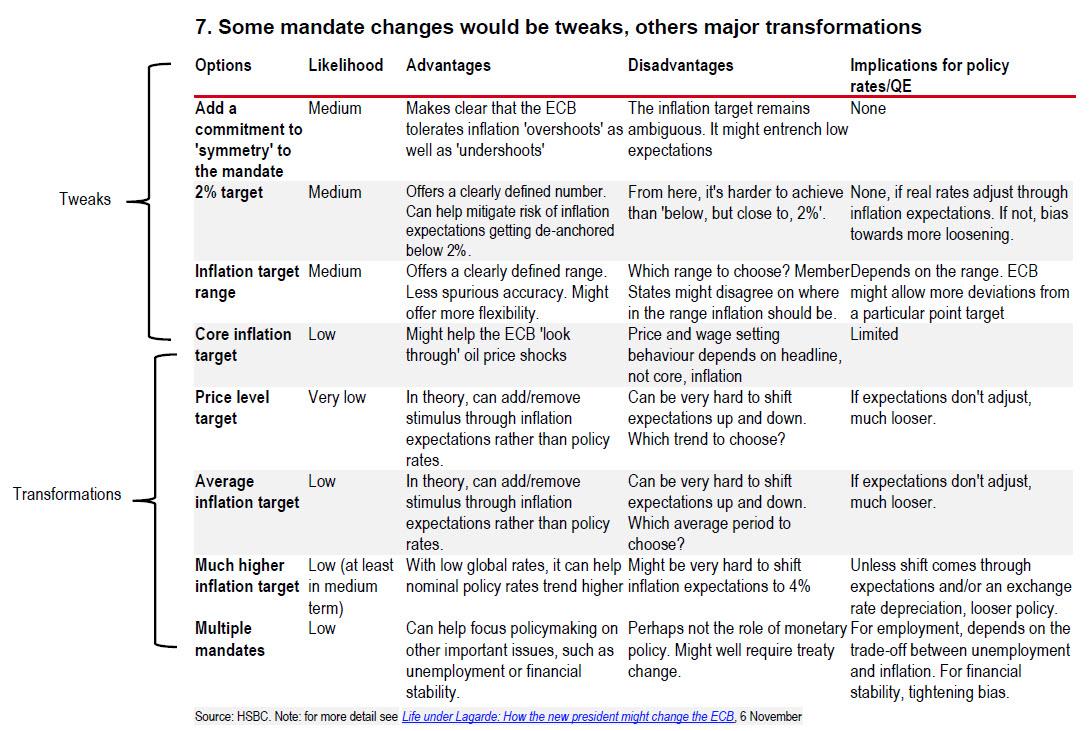

In a recent note, HSBC discussed several options in terms of changing the mandate, from small tweaks to more fundamental changes, which the ECB may pursue. The problem, however, as HSBC noted is that the success of some of these options depends on the degree of confidence in the ECB’s ability to meet it. As a result, the risk of creating a new mandate, only to fail to achieve it as soon as it is implemented, is significant, particularly with policy already so loose and little left in the tank. This was a risk already flagged by Mario Draghi at the September meeting.

These risks, alongside seemingly inevitable compromises in the Governing Council – hawks will likely be averse to any option that risks persistently elevated inflation – lead HSBC to believe that if there will be changes in the ECB mandate as a result of the strategic review, they are likely to be fairly minor. Even moving to a 2% inflation target – removing the uncertainty created by the “below, but close to” – might be too contentious for some.

None of this prevented Lagarde from thinking big. As in climate change big. Because what was more shocking for a central bank which admits it has failed dismally in hitting its price inflation, was its mission creep into seeking to “tame” climate change as well.

Many of the questions at the parliament hearing focused on climate change, an area where the central bank has come under increasing pressure to play a bigger role. In response, Lagarde said that while inflation is the bank’s primary objective, the fight against climate change should be a central part of policy. She said that the ECB’s economic analysis should include the impact of climate change and that its bank supervision arm should also be asking lenders for transparency disclosures and climate risk assessments.

And the punchline: while the ECB’s private sector bond purchases have been market neutral, Lagarde said it was also worth discussing whether climate concerns should impact the ECB’s QE.

How would that work we wonder: “It’s hot outside, so let’s print more money?”

So far the ecofascists have not completely taken over yet, and as we reported previously, German Bundesbank President Jens Weidmann warned against heavy-handed steps such as barring the bonds of polluters from QE, as proposed recently by a group of activists and academics in an open letter to Lagarde. Lagarde said she agreed with Weidmann, but that it doesn’t stop the ECB looking into incorporating climate change into its operations, economic analysis and bank supervision.

To be sure, any mission creep in the ECB’s mandate will only serve to make future monetary easing, well, easier and what better virtue-signaling smokescreen than to use “global warming” as an excuse to print an extra trillion here and there.

Ironically, her linking of QE to climate change took place even as she acknowledged the adverse side effects of the ECB’s ultra-loose policy, and said the review will try to gain a better understanding of how longer-term trends affect what the central bank can control.

One wonders: perhaps the ECB should have conducted such reviews before it bought nearly €3 trillion in assets starting in 2015, long after the European sovereign debt crisis was over, and was merely meant to stabilize risk prices and avoid a market crash.

The take home message however was clear: it is now only a matter of time before the ECB becomes the EcoCB and is “tasked” with a loose, vague and intangible climate change mandate, one which gives the central bank a carte blanche to do virtually anything “in the name of the environment.” Sure enough, at the Parliament hearing, Lagarde said that while the ECB’s primary mandate is price stability, the secondary mandate – to support the general economic policies of the European Union – can cover climate change. European Commission President Ursula von der Leyen has pledged to turn Europe into the first climate-neutral continent in the world by 2050, and green parties made significant gains in recent parliamentary elections.

Finally, reaffirming the ECB’s most recent assessment of the economy, Lagarde added that growth looks weak but that the ECB was determined to use all it available tools to reach its mandate. Asked to predict what the inflation rate will be in eight year’s time when her term ends, Lagarde refused.

“I don’t think that anybody in their right mind would venture to forecast any number, be it growth or inflation, eight years from today,” she said, yet clearly confident it is her job to predict how the climate will do over the same time period.

As COP25 kicks off in Madrid, S&P Global Platts editors take a look at the CO2 impact from OPEC oil production. European gas and nuclear, and IMO 2020’s impact on commodities as diverse as fuel oil and iron ore, are also on the agenda in this week’s pick of charts.

1. OPEC oil-only CO2 output dwarfs EU total emissions

Click to enlarge

What’s happening?OPEC is meeting this week to decide on output quotas, but climate change isn’t on the agenda for the group of 15 major oil producers. OPEC’s total crude output for 2018 would have been responsible for carbon dioxide pollution equal to 5 billion mt, calculated based on average emissions figures for oil from the US Environmental Protection Agency (EPA). That exceeds Europe’s total emissions of the greenhouse gas, from all sources, last year. The cartel currently has no plan in place to mitigate the impact its oil has on global warming despite the growing pressure from consuming nations and business to cut back investment in fossil fuels.

How did we get to these numbers? A barrel of crude weighs about 300 lb, or 136 kg. The CO2 from fuel weighs more than the fuel itself because the carbon element combines with oxygen in the air to form CO2 gas. Carbon-based fuels derived from oil give off CO2 which is on average 3.15 times the weight of the fuel. A standard barrel is 159 liters, and in the US gets refined into 44.1% gasoline, 20.8% distillate fuel oil, 9.3% kerosene-type jet fuel and 5.2% residual fuel oil. So an average barrel of oil will produce at least 317 kg CO2 for just the above four fuels, making the EPA’s average figure of 430 kg seem quite sensible.

What’s next? OPEC and its allies, which pump more than 45% of the world’s crude, are scheduled to meet on December 5 and December 6 in Vienna where a decision on a possible extension to the production cut deal could be taken. The gathering coincides with the 25th Conference of the Parties, or COP, held in Madrid where 200 countries will discuss climate change action as new figures released by the World Meteorological Organization show that green house gas levels reached their highest recorded levels last year.

2. European gas spot prices have risen but December turns bearish

What’s happening? Europe’s benchmark prompt gas contract, the Dutch TTF Day-ahead, crept to a seven-month high last week despite healthy supply. Lower temperatures, reduced storage withdrawals and continued buying combined to tighten the market. The contract has risen Eur6/MWh since October 31, when it dipped below Eur10/MWh. Utility traders are holding onto stocks in anticipation of a greater premium in Q1 2020.

What’s next? While Q1 2020 TTF gas remains over Eur16/MWh, front month December is coming under pressure as Europe’s gas glut looks set to continue. A deluge of LNG is expected to complement already comfortable Russian and Norwegian supply, while gas is seen by market participants as detaching from carbon, and temperatures forecasts have ticked up. Q1 2020 has been more resistant to bearish sentiment because of the risk that transit talks will fail between Russia and Ukraine.

3. French nuclear at record-low lifts December power prices

What’s happening? French nuclear generation is set for a record-low fourth quarter due to maintenance delays and safety inspections at the Cruas nuclear plant following an earthquake. November output averaged 40 GW, down 11% on year, the third month in a row with a double-digit on year decline.

What’s next? 17 of France’s 58 reactors won’t be available at the start of December. French spot power prices are set to hit their highest so far this winter this week despite a generally bearish market, characterized by cheap gas and growing wind output. Colder weather is set to boost demand above 80 GW on Tuesday for the first time this winter with a strike looming as well on Thursday. French gas and coal plants are poised to fill the nuclear shortfall, while stronger hydro and reduced exports should act to ease French price.

4. IMO 2020 sends high sulfur fuel oil cracks tumbling…

What’s happening? Global cracks for high sulfur fuel oil have weakened sharply over the past two months after a year of abnormal strength, reflecting the drastic change in oil products demand due to the International Maritime Organization‘s impending sulfur limit on marine fuels. This month regional prices for HSFO in Asia, Europe, Africa, and the Americas have all reached record discounts to crude as demand falls in the run-up to the IMO 2020 rule limiting sulfur content to 0.5% from January 1, although in some regions they have rebounded somewhat in the past two weeks.

What’s next? Most market watchers believe HSFO prices have now largely bottomed out and are set for a recovery next year. Uncertainty persists, however, over the extent of recovery as pricing economics and uptake of exhaust gas scrubbers – which allow ships to continue burning HSFO – will play a key role in determining HSFO demand. Looking ahead to 2020, the HSFO crack forward curve in Europe is in contango, suggesting regional prices are already set for a recovery.

5. …and complicates shipping costs for iron ore buyers

What’s happening? Iron ore contract buyers this year may be paying as much as $10/dmt more for FOB cargos using industry freight formulas, rather than pricing off spot freight rates. Freight rates are used for invoicing FOB iron ore prices based on benchmark China CFR indices such as Platts IODEX 62% Fe, and Platts 65% Fe fines index. Greater comparative volatility has emerged between spot and long-term industry freight formulas, for Brazil-China Capesize dry bulk rates used to reference contract FOB iron ore prices. Agreeing formulas rather than spot rates may be becoming more complex as bunker oil, a key component in determining long term freight rates under formulas, switches to use lower sulfur marine fuel under IMO 2020 fuel regulations.

What’s next? The extent to which IMO 2020 affects bunker fuel prices and demand for grades consumed, and continued use of industry longer-term freight formulas, remains to be seen. The changes in fuel oil and shipping rates may be discussed by iron ore buyers as they move into new iron ore pricing contracts for 2020 calendar year and fiscal 2020-2021 terms. Some suppliers are already moving contract pricing terms away from formulas to reference spot freight rates, to simplify pricing comparisons with iron ore delivered to markets in China and the rest of the world.

6. Corn prices shoot up in Brazil’s Mato Grosso

What’s happening? Corn prices in Mato Grosso, Brazil’s largest producer, are surging as supplies dwindle and domestic consumption rises, according to Mato Grosso Institute of Agricultural Economics. The state accounts for over 42% of second corn crop, or safrinha, produced in the country. Last week, corn prices in the state hit Reais 29.51 per 60 kg ($116.39/mt), up 53% from the same period a year ago. Strong domestic demand is mainly coming from the ethanol and animal protein industries.

What’s next? As Brazil is the world’s second-largest corn exporter, markets will be closely watching the price movements, as higher corn prices may encourage farmers to expand the crop area for second corn. The second corn planting in the state begins in February. Any increase in domestic consumption is also expected to reduce the supply for exports. The state exported 18.8 million mt of corn in January-October, 54% of Brazil’s total exports of the crop, up from 17.7 million mt in the full calendar year of 2018.

Biden Reinvents Himself, Drags Wife Around Iowa For Massive ‘No Malarkey’ Push

Joe Biden is reinventing himself as he embarks on an eight-day bus tour of Iowa, a key state which he’s largely failed to impress – unlike many of his Democratic competitors angling for the White House in 2020.

The “No Malarkey!” tour got off to an awkward start on Saturday, when Joe bit former Second Lady Jill Biden on the finger as she introduced him at a Council Bluffs kickoff event.

One almost has to feel sorry for Jill. After going out on a high note in 2016, she watched the establishment reanimate her senile husband – only to have clips of him creeping on women and children flood the internet. Then there was Hunter Biden’s rental car crackpipe adventures, Burisma, and now an out-of-wedlock grandchild with an Arkansas stripper. And then Joe bites her finger as they announce the stupidest campaign slogan ever.

“We’re going to go to 18 counties, on a 660-mile trip across the state, and we’re going to touch on what we think is a forgotten part of most campaigns — the rural part of your state, rural America,” said Biden, speaking at the Saturday event.

For months, Biden’s campaign has been dogged by criticism among supporters and critics alike that his Iowa operation was slow to get off the ground. Given the nature of the caucuses, where voters choose the nominee by gathering in public spaces like school gymnasiums, churches and community centers for one night in February, a robust organization that encourages people to participate is critical to success. –Bloomberg

Aside from the eight scheduled stops, Biden will take two side-trips; one in Chicago to raise money – returning to Iowa on Tuesday for a single organizing event in Mason City, and then a jaunt to New York that evening to attend more fundraisers before returning on Wednesday afternoon for more Iowa action.

“I’m running to win. I’m not running to lose. I’m not running to come in third or fourth or fifth or anything like that. So I feel good about it,” said Biden.

No Malarkey?

Seeking to turn Biden into an affable elder statesman after a series of ‘Mr. Magoo’ gaffes, the Biden camp decided to go hard at the depression-era demographic with the slogan “No Malarkey!” – something his grandfather used to say.

As Bloomberg describes it, “The “No Malarkey” theme — emblazoned on the side of Biden’s tour bus — nods at both the candidate’s reputation for truth-telling and Trump’s supposed aversion to it.”

“The other guy’s all lies, so we want to make sure there’s a contrast,” said Biden at one stop.

Biden will be traveling with former Iowa governor Tom Vilsack, who served as Obama’s agriculture secretary. Also joining the tour will be Vilsack’s wife, Christie.

As he stops in small towns, he’s sure to allude to rural values and rural needs and to mention that he’s secured the support of Vilsack, the popular two-term governor, who urged Hillary Clinton’s 2016 campaign to spend more time in rural areas.

“With all due respect to folks who talk about bold, new ideas, the reality is, you’re going to have an incredibly difficult time until the country comes together,” Vilsack told Bloomberg news in an interview in November. –Bloomberg

That said, Vilsack thinks Biden – the current Democratic frontrunner, is best positioned to enact progressive change because he appeals to a much broader audience than other candidates – particularly in swing states.

“The vice president is speaking to a much broader audience than some of the other candidates. I think he’s speaking to the audience that any Democrat is going to have to speak to consistently through this campaign in order to have the people who will decide this election in Pennsylvania and Michigan and Iowa and Wisconsin basically saying, ‘Yeah this guy has been consistent throughout,’” said Vilsack.

If Biden’s attempt to reinvent himself in Iowa doesn’t work as planned, what does it mean for the rest of the 2020 campaign?

{kind=link}