China Folds: For All Its Bluster, Beijing Does Nothing After Trump Signs HK Bill

Just a few hours after Trump called China’s bluff on the Hong Kong bill, it appears the US president won the pot.

After launching a stern verbal protest overnight in which China’s Foreign Ministry said that it would take strong countermeasures if the US continues to undermine Hong Kong’s autonomy after Trump signed the Bill that supports HK protesters, adding that US attempts to interfere in HK are doomed to fail, Beijing has done nothing really, and instead left the door open for a trade deal with the U.S., confirming again that China needs the trade deal with the US just as much as Trump, if not more.

The build up certainly was dramatic: for days after Congress almost unanimously passed the Hong Kong Human Rights and Democracy Act last week, China repeatedly vowed it would take unspecified countermeasures if Trump signed the bill, fueling concerns that President Xi Jinping would scuttle the trade talks to appear tough on the U.S. In the end, China did nothing: Wednesday’s bill signing by Mr. Trump came and went without any real action.

Instead, as the WSJ notes, “Chinese officials shifted their focus to whether the U.S. president would implement any of the bill’s measures, according to officials involved in economic policy-making.” Specifically, to save face, Beijing seized on a sentence in Trump’s statement that emphasized his “constitutional authorities with respect to foreign relations.”

… with respect to foreign relations.” Sources confirm the Phase One deal is being finalized. So let’s see. With @PhilipWen11@Chao_Deng

Or as the WSJ summarized, for all its huffing and puffing, “China’s leadership still wants a deal to help alleviate pressure on its fast-weakening economy”, which incidentally coincides with Trump’s own interest as he hopes to clinch a deal to boost his re-election bid.

Indeed, as the WSJ’s Lingling Wei also notes, Trump “Trump also chose the evening before Thanksgiving to sign the measure, a time guaranteed to get little attention in the U.S. While his signature still makes the bill law, his timing suggests he was trying to play down the political impact at home.

Also good point by @bobdavis187 : Trump also chose the evening before Thanksgiving to sign the measure, a time guaranteed to get little attention in U.S. The timing suggests he was trying to play down the political impact at home.

Trump’s successful gambit was concluded when reporters asked if the bill’s signing would affect trade talks. To this, China’s Foreign Ministry spokesman Geng Shuang didn’t answer directly but demanded the U.S. not implement the law because it would risk “undermining our bilateral relations and cooperation in important areas.” Chinese officials were also reportedly encouraged by Trump’s efforts to emphasize his respect for Mr. Xi. “I signed these bills out of respect for President Xi, China, and the people of Hong Kong,” Trump said unironically in the statement.

And since the actual implementation of the bill wold not take place for over half a year, when it comes to China it is now officially in the rearview mirror as Beijing has moved the goalpost not to responding to Trump’s signing of the bill, but to Washington’s actual implementation.

“It does spoil the mood, but it shouldn’t interfere with the trade talks,” said Wang Yong, a professor of international relations at Peking University, of Mr. Trump’s move. “Both sides have enough reasons to keep trade, Hong Kong and political issues on separate tracks.”

Which means that with both sides now eager to sign a deal, they will ignore any political theater that could potentially jeopardize such a deal:

Some outside experts agree with Beijing’s interpretation that while the U.S. law gives the president broad powers to impose sanctions and travel restrictions on individuals who commit human-rights violations in Hong Kong, the president already had many of those powers—and still has the discretion to not apply them.

“My reading of D.C. is there’s a lot of appetite for talking tough on China, but not that much in terms of actually being tough,” said Andrew Polk, founder of Trivium, a Beijing-based economics and policy consulting firm.

Still, there is a modest risk that Xi will be pressured to offer at least a token response: as noted earlier, China’s top twitter troll, Hu Xijin, editor in chief of the state-run Global Times, said on Twitter that China was considering barring those responsible for drafting the legislation from entering mainland China, Hong Kong and Macau. Trolling Trump’s turn of phrase, Hu said this was “out of respect for President Trump, the U.S. and its people.”

Yet ultimately passage of any trade deal could depend on whether Hong Kong residents escalate their protests in the coming days, emboldened by explicit US support – in that case, Beijing may have no choice but to close the door, if only temporarily, on a Phase 1 deal.

China’s attempts to keep Hong Kong issues and the trade talks on separate tracks might not be universally popular, some analysts say. Shi Yinhong, a professor of international relations at Renmin University, said it could be embarrassing for a phase-one trade deal to progress in light of the Hong Kong law.

Yet despite the various unknowns and risks, the fact that Beijing has so far merely stuck to verbal threats instead of escalating to actual deeds, confirms that for now, Trump’s signing gamble worked out just as the US president expected.

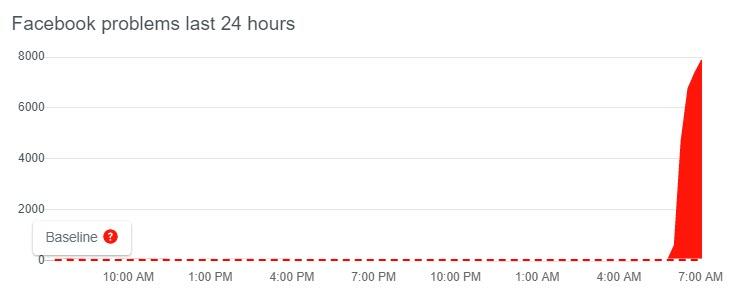

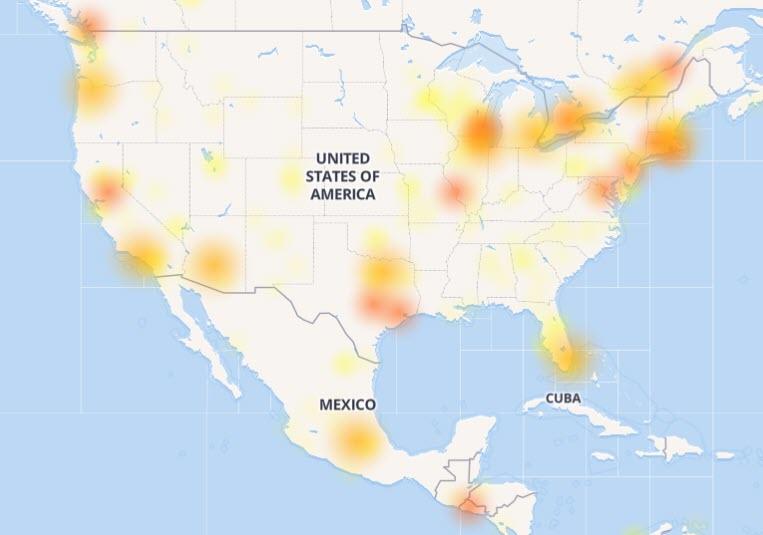

Facebook/Snapchat Is Down For Millions: Millennials Panic As They Face Thanksgiving ‘Alone’

In what could send Millennials across the globe into a tryptophan-inspired cycle of doom, Thanksgiving Day is off to a horrifying start for many as Facebook and Snapchat are reportedly down for millions across the globe.

Users reported outages across both Facebook and Instagram, which are both owned by the same company, but WhatsApp appeared to be unaffected by the issue as yet. All three apps share much of the same underlying infrastructure which can often create a cascade effect when a server goes down.

The latest joy killing decree to be issued from the environmental overlords is that Thanksgiving is canceled because your family meal is killing the planet.

How is it that some sweet potatoes and a pumpkin pie are destroying the Earth? Well, the bastion of all that is pure and good, the aptly named HuffPost has the answer.

“Meat and meat byproducts (cheese, butter and heavy cream, for example) have a larger environmental footprint than plant-based ingredients,” complains Alexandra Emanuelli.

“According to research done by Carnegie Mellon University, the carbon footprint of a 16-pound turkey creates a total of 34.2 pounds of CO2 — the same amount produced by turkey gravy, cranberry sauce, roasted Brussels sprouts, mashed potatoes, rolled biscuits and apple pie combined.” Emanuelli further huffs.

“[P]lant-based foods consistently have been shown to have lower carbon footprints — so those walnuts, chestnuts, mushrooms, etc. are far more efficient to produce in total resources than conventional animal products, especially red meat,” the report continues.

Great… walnut and mushroom soufflé it is then. But no…wait…you can’t actually have a family Thanksgiving at all, unless you all live in a commune and never leave, because traveling is the real evil.

“Researchers at Carnegie Mellon determined that four people flying a 600-mile trip produces 10 times the emissions of the Thanksgiving meal,” the report further whines.

“Driving is less detrimental, but American cars emit close to a pound of CO2 per mile driven. Orchi Banerjee, a recent graduate of the department of Social and Decision Sciences at Carnegie Mellon, said, ‘It may help the environment if [your guests] stayed home and cooked their own meal.’”

So, also canceled are Christmas, Easter, Passover, and 4th of July.

Stay at home alone, in your pod, eating walnuts. Better yet, just eat worms.

Tucker Carlson and his guest Mark Steyn had some choice words for those who want to cancel Thanksgiving:

“‘The Huffington Post’ says you shouldn’t be taking a plane. You shall not be eating a turkey. Eating a Turkey is bad for the planet, even though it is not as bad as one of these flatulent cows that AOC wants to slaughter … instead of having a stuffed turkey, you should have some arugula stuffed with kale or kale stuffed with arugula. Makes no difference, tastes just as lousy either way,” said Steyn.

The pair then pointed out the hypocrisy of liberal jet-setters who preach to everyday Americans about their carbon footprints.

Macron Denies Accepting Putin’s Missile Moratorium For Europe: “Absolutely Not Accepted”

On Thursday contradictory messages were reported out of Europe and Russia after the Kremlin announced French President Emmanuel Macron had told Moscow he was ready to seriously consider Russia’s proposal to impose a moratorium on the deployment of missiles in Europe following the collapse of the Intermediate-range Nuclear Forces Treaty (INF), which formally ended in August. The INF had for decades been effective in preventing just such a ‘new Cold War’ scenario and weapons build-up.

But despite the Russian side touting this new ‘diplomatic opening’ with a lead NATO power, which was initially reported in Interfax and TASS, the declaration appears premature. Hours after the initial claim, Reuters reports the following:

French President Emmanuel Macron on Thursday denied having accepted a Russian proposal to impose a moratorium on missile deployments in Europe, but said it was important the Kremlin initiative not be simply dismissed.

File image via Reuters

The report notes that Macron had been meeting face to face with NATO Secretary-General Jens Stoltenberg in Paris where he stressed that France had “absolutely not accepted” the proposal.

“But we considered that, as a basis for discussion, we shouldn’t just brush it off… Let’s be serious, this is the security of Europe we’re talking about,” he said according to Reuters.

It appears that was enough of an opening for Russian officials to run with, indicating a potential thawing on the issue.

Kremlin spokesman Dmitry Peskov said Macron had was vague but his intention for an opening of dialogue on the issue with NATO was clear: “Of course, (Macron’s) answer is not detailed. But at least, it expressed an understanding of (Russia’s) concern and a readiness for dialogue on this score,” Peskov said.

NATO has maintained that Russia is the main offender which led to the demise of the short to medium-range missile pact, despite the Trump administration being the first to vocalize that it’s obsolete and should be abandoned for a better, more encompassing treaty.

Concerning Russia’s offer for a missile ban in Europe, Reuters points out: “NATO has called the proposal not ‘credible’ and said Moscow has already deployed illegal missiles, something Russia denies.”

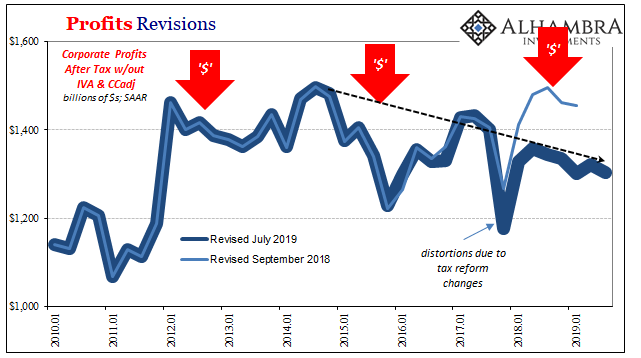

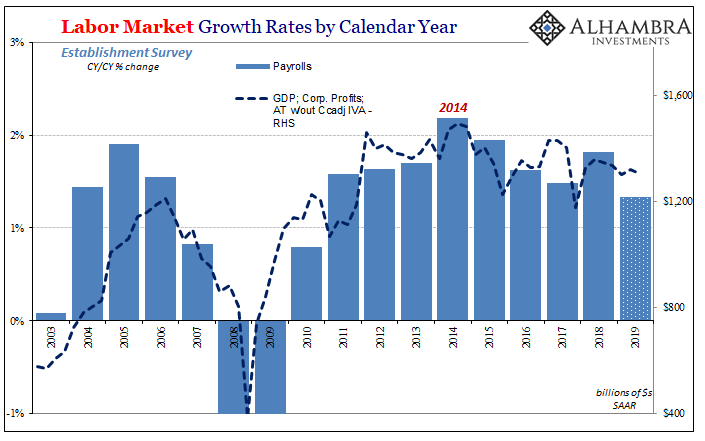

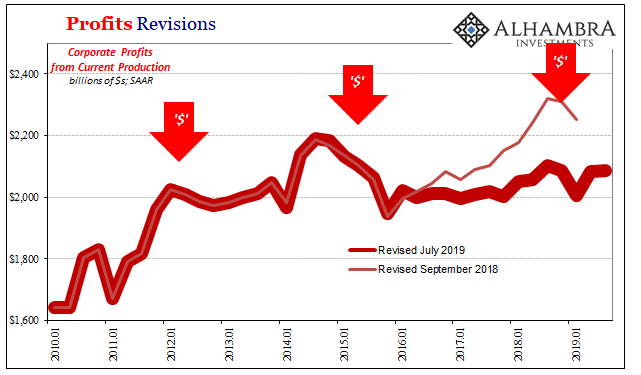

The Bureau of Economic Analysis (BEA) has revised its preliminary estimate of GDP. That can only mean one thing: time to look at corporate profits again. Included along with the recalculated headline output estimate is the BEA’s first run of profit figures. If you are Jay Powell, you aren’t going to like what you find.

First, real GDP in the third quarter was practically unchanged. Revised from around 1.90% (continuously compounded annual rate of change) to a touch above 2.10%, either of those estimates are pretty much equivalent to the unrevised 1.99% growth believed to have taken place in Q2.

Still the slowdown from 2017-18. But what everyone wants to know is, what does this downshift really mean? Did the US economy simply revert to its (already too low) mean potential after a minor reflation high last year? Or is it transiting from reflation into a weaker possibly more dangerous state beyond the simply lackluster? The last time around, four years ago, it was the latter.

Jay Powell and the official position says it is the former. Buoyed by tax reform and slightly more favorable global conditions (he says), 2018 was equivalent to a very small sugar rush. Taking on some unknown but “transitory” cross currents late in the year, as 2019 wears on the unflinchingly strong labor market will more and more support the economy keeping it around average at worst.

In order for that to happen, though, the labor market has to actually be strong. Not just the unemployment rate, either.

That’s where corporate profits come in. As much as anything, the general willingness of businesses in the US (as anywhere else) to add more labor is related to both the top and bottom lines of their income statements. Revenue growth driving profit growth means a lot more net hiring.

No revenue growth and therefore profit problems, a lot less. I’m not really going out on a limb here, illustrating nothing more than the basics you already know quite well.

As economic profits accelerated in the past, the rate of payroll expansions did, too. This isn’t rocket science.

What the BEA’s income accounts have been suggesting is that they aren’t accelerating, having reached a peak rate all the way back in 2014 (which wasn’t all that high, even though it added up to the “best jobs market in decades”). Since, profit growth has been at best stagnant (depending upon the BEA series) and at worst declining.

Unsurprisingly, as you can see above, that near exactly matches what the Bureau of Labor Statistics (BLS) has been consistently reporting for years as far as its Establishment Survey has been concerned. The only difference is that this has gone unreported by the mainstream media which continuously described the situation as “robust” no matter how much it wasn’t.

The labor market is already materially weaker this year than it was in reality last year. And I mean the actual payroll gains which won’t be revealed until this upcoming February. As the FOMC even admitted at its last policy meeting, 2018 wasn’t nearly as good as advertised as far as the labor market was concerned, and 2019 is in all likelihood to be materially weaker still.

The BEA data gives us the reasoning behind it. For all his talk about a strong economy, Jay Powell can’t influence company income statements. And if profit conditions are the way the BEA data puts them, small wonder the labor market in reality is quite different from how it is talked about.

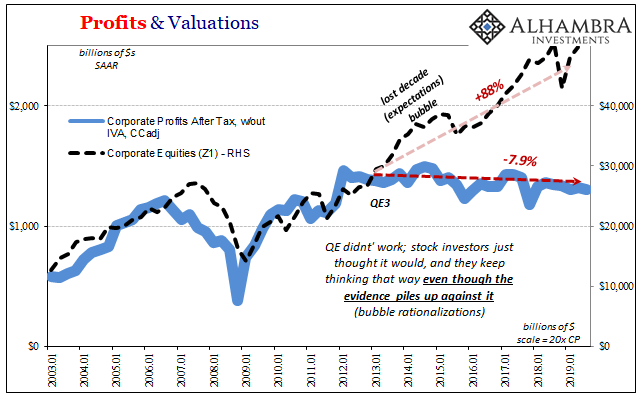

What the Federal Reserve Chairman does influence instead is stock market valuations. At the NYSE, the legend of the “maestro” refuses to die. Partly because of how corporate boardrooms react to his schtick as well as the temporary effects of “tax reform”, buying back shares as fast as possible, in macro terms economic earnings don’t ever rise while share prices absolutely do.

You’ve probably heard by now how this difference is at extremes – the most since the height of the dot-com era. Going by the BEA’s estimates for profits, they are down 8% since the launch of QE3 in 2012. Over the same time span, however, the value or price of corporate equities (taken from the Federal Reserve’s Z1 data, updated through Q2 2019) has exploded, up almost 90%.

By virtue of corporate earnings, the economy hasn’t recovered and isn’t accelerating suggesting more and more it never will. By virtue of stock prices, recovery is still guaranteed to happen…someday.

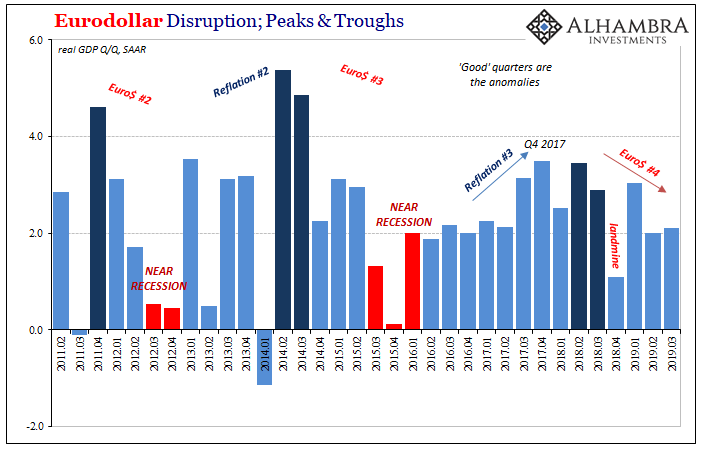

That may be true, but as this fourth eurodollar-related downturn continues to unfold it already means at the very least another multi-year period where it cannot happen. As the best case, if there is going to be a recovery then it has been yet again delayed.

Of course, the more reasonable interpretation is that given now four downturns meaning three false dawns the likelihood of any actual recovery and acceleration is exceedingly small. If it was going to, it would have long before now. One false dawn (Euro$ #2) may be random, two starts to look like a pattern (Euro$ #3), so three (Euro$ #4) cannot be an overly strong labor market which will finally deliver the macro goods in a timely fashion.

At this juncture, what most people usually ask is, if the economy is so bad how can stock prices keep pushing to record highs? The answer is simple; mainly central bankers who have let equity investors fool themselves into believing in QE and how it must have produced a real economic boom over the last several years despite earnings.

That boom will (somehow) create the earnings.

The lack of macro growth and therefore profits, though, has left Corporate America in a precarious position. Top heavy. Without real top or bottom line growth the last half decade, corporate strength has been vastly overestimated. That is why this year and last the sudden mainstream recognition of “zombie” companies who wouldn’t exist if there had been actual growth derived from an actual boom.

Where that becomes a much thornier issue is if or when these zombie-like businesses are forced to confront the reality of their true bottom-line situations – especially if the BEA is right about where those are heading. Recession is a surefire way for that to happen, but it needn’t go that far.

The zombie stock bubble? Perhaps the most fitting description.

There’s good news for American families this Thanksgiving – the cost of a turkey feast has remained stable, rising by a single penny compared to last year. As Statista’s Katherina Buchholz notes, The American Farm Bureau has found that the classic ingredients for a Thanksgiving dinner to feed 10 people will cost $48.91 in 2019. That’s less than $5 per person.

An estimated 46 million turkeys are eaten every year at Thanksgiving, and as is typical, the most costly item by far is the turkey, which this year costs an average of $20.80. Yet, the price of the big bird is at its lowest since 2010. Since most other ingredients on the Farm Bureau’s shopping list have seen slight price increases, the price of the entire meal remained relatively stable this year. In the previous years, the average price of Thanksgiving dinner had actually been decreasing.

The shopping list of the survey includes all ingredients and foods in quantities sufficient to serve a family of 10. 250 volunteers checked prices in grocery stores in 38 states for the Farm Bureau.

According to the American Farm Bureau, U.S. farmers only receive eight cents out of every dollar spent on food for the Thanksgiving feast.

A paper by Scott A. Wolla and Kaitlyn Frerking for the Federal Reserve Bank of St. Louis warns that the Fed’s own policy could lead to “economic ruin.”

The paper titled “Making Sense of National Debt” explains the pros and cons of national borrowing in typical Keynesian fashion. In a nutshell, a little debt is a good thing, but too much debt can become a problem.

But in the process of explaining national debt, Wolla and Frerking stumble into an ugly truth — Federal Reserve money printing can destroy a country’s economy.

So, when does the national debt become a problem?

According to Wolla and Frerking, debt only becomes an issue when it outpaces GDP, or national income, as they call it. If debt grows at a faster rate than income, eventually the debt might become unsustainable.

The federal debt is projected to grow at a faster rate than GDP for the foreseeable future. A significant portion of the growth in projected debt is to fund social programs such as Medicare and Social Security. Using debt held by the public (instead of total public debt), the debt-to-GDP ratio averaged 46 percent from 1946 to 2018 but reached 77 percent by the end of 2018. It is projected to exceed 100 percent within 20 years.”

Note that the total public debt is even higher. Most analysts put the total debt to GDP ratio at around 105%.

As Wolla and Frerking point out, rising levels of debt elevate the risk of default. Normally, investors holding government bonds bear this risk. While governments never have to entirely pay off debt, there are debt levels that investors might perceive as unsustainable.

Enter the central bank. Wolla and Frerking explain how it can step in and “print money” in an effort to rescue the overleveraged government.

While governments never have to entirely pay off debt, there are debt levels that investors might perceive as unsustainable. A solution some countries with high levels of unsustainable debt have tried is printing money. In this scenario, the government borrows money by issuing bonds and then orders the central bank to buy those bonds by creating (printing) money. History has taught us, however, that this type of policy leads to extremely high rates of inflation (hyperinflation) and often ends in economic ruin.”

The process that Wolla and Frerking describe is called debt monetization. And it’s exactly what the Federal Reserve is doing today.

The Federal Reserve will buy $60 billion in short-term Treasury bills each month. According to a statement, the purchases will continue, “at least into the second quarter of next year.” That would amount to around $400 billion worth of Treasurys added to the Fed’s balance sheet.

But the balance sheet will likely expand more than that. The Fed also plans to use interest it earns off its portfolio to buy more Treasurys. And as they mature, it will take that money and buy more bonds, thus pumping up the balance sheet.

Powell insists this is not quantitative easing. When he announced the plan, Powell said, “This is not QE. In no sense is this QE.” But as Peter Schiff said, this is precisely QE – no matter what you call it.

In effect, QE is a fancy term for printing lots of money. The Fed doesn’t literally have a printing press in the basement of the Eccles Building running off dollar bills, but it generates the same practical effect. The Federal Reserve digitally creates money out of thin air and uses the new dollars to buy securities and government bonds, thereby putting “cash” directly into circulation. QE not only boosts the amount of money in the economy; it also has a secondary function. As the Federal Reserve buys US Treasury bonds, it monetizes government debt.

We’ve seen this song and dance before. The Federal Reserve ran three rounds of quantitative easing in the wake of the 2008 Financial Crisis.

When then-Fed-chair Ben Bernanke launched QE, he insisted the Fed was not monetizing debt. He said the difference between debt monetization and the Fed’s policy was that the central bank was not providing a permanent source of financing. He said the Treasurys would only remain on the Fed’s balance sheet temporarily. He assured Congress that once the crisis was over, the Federal Reserve would sell the bonds it bought during the emergency.

That didn’t happen. And now we’re back to QE. In fact, the Fed balance sheet is currently expanding faster than it did during the rounds of QE after the great recession.

Wolla and Frerking assure us everything will be fine here in the US. We don’t have to worry about hyperinflation because we have an “independent” central bank.

You can decide for yourself whether you believe in this mythical Fed independence. Regardless, the central bank can only fool markets for so long. Ultimately, the national debt depends on investor willingness to buy government bonds. Peter said he doesn’t believe the Fed will be able to pull off the ruse again. Investors may expect QE4 to be like QE3, but there’s a big difference.

You see, when the Fed did QE3, investors were still foolish enough to believe that that was the last time they were going to do it. They actually bought the Fed when the Fed said they had an exit strategy, they were going to shrink their balance sheet; they were going to normalize interest rates. The markets were looking forward to that and they thought that what the Fed was doing was working. But it didn’t work. It was an abject failure. That’s why they’re doing it again. But soon the markets are going to discover that QE is permanent and that there’s never going to be a real reduction in the balance sheet. The balance sheet is going to grow into perpetuity and I think we’re going to have a dollar crisis. I think we’re going to have a sovereign debt crisis. I think this is going to end very poorly for people who have been enjoying the paper gains in this stock market bubble.”

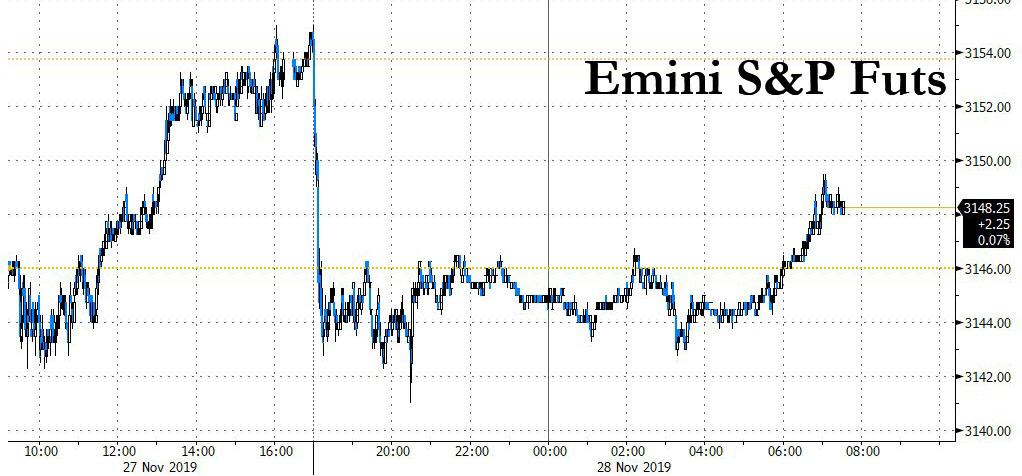

Global Markets Stumble As Fresh Trade Tensions Flare Again

There is a distinct lack of stock market-boosting “trade deal optimism” overnight after Trump signed the legislation that expresses US support for Hong Kong protesters into law. Needless to say, China was furious at Trump’s endorsement of a bill that requires annual reviews of Hong Kong’s special trade status under American law, as well as sanctions against any officials deemed responsible for human rights abuses or undermining the city’s autonomy, and in response China’s Foreign Ministry said US interference unites the Chinese people against Washington’s “sinister intentions & hegemonic nature” and that China country will take strongcounter measures if the US continues this way, adding that US attempts to interfere in HK are doomed to fail.

“The bad news is, the trade war is still on,” Andy Kapyrin, director of research at RegentAtlantic Capital LLC, told Bloomberg TV. “I really don’t see substantial progress on trade with China,” and markets will perceive Trump’s signing of the bill negatively, he said.

All eyes now on whether this impedes “phase one” negotiations, but until then a four-day rally that had lifted world stocks to near-record highs stalled and S&P futures are on the back foot after hitting a third consecutive record on Wednesday, even if they have managed to recoup almost half the overnight losses as traders clearly do not think the HK bill will hurt the trade deal. As a reminder, US markets are closed today for Thanksgiving holiday.

Fading hopes of a deal between the world’s two biggest economies before additional, potentially damaging tariff hikes kick in has lowered risk appetite, pushing the benchmark German 10-year government yield to its lowest since Nov. 1. The safe-haven yen gained against the U.S. dollar, recovering from six-month lows, while London’s FTSE index fell from two-month highs and Europe’s Stoxx 600 index was down 0.2%, led by trade-sensitive sectors such as autos, down 0.6% and tech, down 0.4%.

Euro zone economic sentiment rebounded more than expected in November, with more optimism in the services sector, data from the European Commission showed. Sentiment in industry, among consumers, and in industry all improved but remain below zero. The euro was little changed by the news. Data released on Thursday also showed that bank lending to euro zone companies in October rebounded, after dropping the month before.

Of course, since nothing can interfere with the goalseeked narrative pushing stocks higher, fears as to the extent of Chinese retaliation started to ease during London trading.

“When you see the optics of siding with Hong Kong against the mainland, that would seem at face value to be intuitively antagonist to the prospect of the trade negotiations,” said Jeremy Stretch, head of G10 FX strategy at CIBC capital markets. However, he said, “It may prove to be the case that despite the threat of a Chinese reprisal they may not be quite as significant or dynamic as feared. It is an external headwind but, for now at least, the markets are starting to take a slightly more sanguine viewpoint of the outcome.”

Asian markets mostly traded lower on this news, snapping a four-day rising streak with Indonesia leading declines, while Australia climbed. Technology and industrial shares were among the weakest. Japan’s Topix slipped 0.2%, as Keyence and Honda Motor weighed on the gauge. Japanese retail sales plunged 7.1% in October after a sales tax hike and a super typhoon kept shoppers at home. The decline in retail sales comes at a time when the Japanese government is mulling the size of a fiscal stimulus. An economy ministry official said after the release that sales were also hurt by a drop in overseas tourists, including visitors from South Korea, while car and appliance purchases slid by double-digits.

The Shanghai Composite Index closed 0.5% lower, dragged down by Kweichow Moutai and Industrial & Commercial Bank of China. A scorching rally in pork prices, which pushed China’s inflation to the highest level in seven years, is cooling. India’s Sensex fluctuated after closing Wednesday at a record, as investors awaited the country’s quarterly economic report due Friday.

This kept MSCI’s world equity index flat, after it approached the record reached in January 2018. However, the index is up almost 3% so far in November and is on track for the best month since June as investors flit in and our depending on the trade news.

With 10Y Treasuries closed for trading, European sovereign bonds were mixed, with British and Swiss notes edging up and Italian debt falling.

In FX, the pound held Wednesday’s gain against the dollar following a poll suggesting the U.K. election will deliver a large majority for the Conservative Party. However, the currency failed to build on its gains, trading steady against the dollar at $1.2910. It was little changed versus the euro after surging to its highest in nearly seven months at 85 pence in early London trading. Implementing Brexit by the end of January, as Johnson had promised, would leave him a “miniscule” 11 months to agree a trade deal with the European Union, analysts at Societe Generale told clients.

A drop in Latin American currencies turned into a rout Wednesday as Chile’s peso, Brazil’s real and Colombia’s peso all hit record lows following political unrest in the region.

In commodities, WTI crude oil prices are down -0.43% while, spot gold prices are up +0.16%.

Top US News from Bloomberg

President Trump signed legislation that requires annual reviews of Hong Kong’s special trade status under American law, as well as sanctions against any officials deemed responsible for human rights abuses or undermining the city’s autonomy. A second Hong Kong measure also bans the export of crowd-control items such as tear gas and rubber bullets to the city’s police. China’s foreign ministry reiterated a threat of retaliation without offering any details

Boris Johnson’s Conservative Party is on course to win a large majority of 68 seats in the Dec. 12 vote, according to a YouGov poll, which used a technique that more closely predicted the 2017 election than standard surveys

Japanese retail sales plunged in October after a sales tax hike and a super-typhoon kept shoppers at home, a worse- than-expected outcome the government will need to consider as it mulls the size of a spending package to support growth

Oil fell for a second day after U.S. crude production rose to a record and Trump signed a bill into law expressing support for the Hong Kong protesters

China has ordered local governments to speed up the issuance of debt earmarked for infrastructure projects, so that the proceeds can be invested early in 2020 to help shore up the slowing economy

Major European bourses (Euro Stoxx 50 -0.2%) are broadly lower, with risk sentiment dented in wake of US President Trump’s signing of the Hong Kong Human Rights Bill to the consternation of China, who have threatened counter measures. “While this worsens the negotiation climate for a trade deal” note Danske Bank, “it is still our belief that the sides will be able to keep the Hong Kong issue separate and land a phase 1 deal before the 15 December when US-China import tariffs are scheduled to rise by 15%.” Elsewhere, FTSE 100 (-0.4%) is weighed on as a firmer Pound weighs on large-cap exporters after the YouGov MPR model predicted a healthy Conservative majority at the upcoming election, whilst heavy-weight miners bear the brunt on unfavourable base metal price action. However, Italy’s FTSE MIB (-0.7%) stands as the underperformer thus far, with domestic banks all pressured by unwelcomed action in the Italian fixed income complex. Sectors are mostly in the red, with only Energy (+0.2%) and Materials (+0.1%) modestly in positive territory. Moving on to the stock specific movers; Telefonica (+1.5%) shares advance after the Co. revealed a major overhaul to its business; it will focus more on its domestic market, Brazil, UK and Germany, whilst its remaining 8 Latin American businesses will form a separate unit which could potentially be sold. Moreover, two new businesses, Telefonica Tech and Telefonica Infra, will be created as part of the overhaul, with profits expected to be boosted by EUR 2.0bln by 2022. Elsewhere amongst the gainers, Ambu (+1.2%) and Red Electrica (+1.3%) shares are bid after the Cos received upgrades at Handelsbanken and Citi respectively. In terms of the laggards; declining net earnings and revenue see Remy Cointreau (-3.2%) shares come under pressure. Elsewhere, Proximus (-2.1%) shares are lower after the Co. appointed Guillaume Boutin as its new Chief Executive, effective on December 1st.

In FX, Sterling has extended its recovery rally from recent lows on the back of the latest UK election poll from YouGov that signals a relatively big win for PM Johnson and his Tory party at the forthcoming GE, albeit with the standard statistical error margins that could crimp the actual number of seats predicted to be claimed by the Conservatives. Cable has run into some resistance around 1.2950 and Eur/Gbp support circa 0.8500, but in thinner US Thanksgiving Holiday trade and with more month end models pointing to Dollar selling for portfolio rebalancing 1.3000 remains a realistic objective for the former, while a breach of the round number in the cross exposes 0.8475-70.

EUR/NZD/JPY/CHF – All firmer against the Greenback as the DXY topped out just ahead of 98.500 following yesterday’s post-US data rebound amidst slightly less friendly US-China ties on HK lines compared to the Phase 1 trade accord that is said to be increasingly close to completion. However, the single currency continues to struggle above the 1.1000 level and faces more option expiry-related supply due to 1.1 bn rolling off between 1.1025-30 at today’s NY cut with little impetus via any of the latest Eurozone data ranging from encouraging economic sentiment indicators and M3 metrics to benign German state CPIs. Similarly, the Kiwi is still finding the air rare over 0.6400 even with a more pronounced, while the Yen and Franc are paring some declines from 109.50+ and near parity troughs respectively regardless of contrasting macro releases (Japanese retail sales weak vs stronger than forecast Swiss GDP). Note, Usd/Jpy could maintain its upward trajectory on technical grounds if the pair settles above another Fib (109.37) after breaching 109.20 on Wednesday.

CAD/AUD/NOK/SEK – The G10 laggards, with the Loonie retreating further through 200 DMA resistance towards 1.3300 and Aussie meandering within a 0.6778-60 range following conflicting Q3 Capex figures overnight and as Aud/Nzd hovers near the bottom of 1.0558-24 parameters. Elsewhere, the Scandi Crowns have reversed course after failing to maintain bullish momentum through key chart levels yesterday against the Euro, as Eur/Nok bounces off sub-10.0750 lows to 10.1150+ and Eur/Sek to almost 10.5700 from around 10.5300 at one stage. Soft crude prices may be a factor hampering the Norwegian Krona, but its Swedish counterpart is not deriving any support from decent business sentiment or retail sales.

In commodities, crude markets are lower, with prices weighed by a combination of trade concerns after US President Trump signed the Hong Kong Bill and yesterday’s surprise build in crude inventories and larger-than expected build in gasoline stocks revealed by the EIA. Front month WTI and Brent contracts for now trade just above support in the form of yesterday’s post EIA data lows at the USD 57.50/bbl and USD 62.45/bbl marks. Elsewhere in crude specific news; Russia said that the exclusion of Russian gas condensate production from their output calculations for OPEC+ is going to be a topic of discussion regarding agreements post March 2020 at the upcoming OPEC+ meeting on December 6th, confirming overnight reports. The report noted that given the growth that the country has seen in gas output, condensate production has increased in tandem, leading ING to conclude that “this would help to explain why Russia has failed to fully comply with the production cut deal for much of this year.” Elsewhere, Libya’s El Feel oil field (70k BPD) is said to have resumed production, after violence in the region which disrupted production yesterday. Looking at the metals, gold is slightly firmer, but struggling to gain impetus despite the more downbeat macro backdrop and slightly softer buck; the precious metal is off yesterday’s USD 1452/oz lows, but struggling to break above the USD 1458/oz level, which has capped the price action so far this morning. Meanwhile, the return of Hong Kong related US/China trade jitters has hit copper prices, which have continued to slide during European trade.

US Event Calendar

US closed due to Thanksgiving holiday

Happy Thanksgiving to all our US readers but in reality I hope you’re not reading this and enjoying time with your family instead. I’m in Holland at our annual outlook presentation for Dutch clients that is held on this day every year. Expect markets to be quiet today although the reality is that things have already slowed to a crawl in the last 24 hours.

Having said that, the key headline overnight has been that President Trump has signed the legislation that expresses US support for Hong Kong protesters into law. As we have mentioned before, the bill requires annual reviews of Hong Kong’s special trade status under American law, as well as sanctions against any officials deemed responsible for human rights abuses or undermining the city’s autonomy. China’s Foreign Ministry said in response that the country will take strong counter measures if the US continues this way and added that US attempts to interfere in HK are doomed to fail. All eyes now on whether this impedes “phase one” negotiations.

Asian markets are trading lower on this news with the Nikkei (-0.10%), Hang Seng (-0.24%), Shanghai Comp (-0.38%) and Kospi (-0.28%) all down. Elsewhere, futures on the S&P 500 are trading -0.28% and in commodities, WTI crude oil prices are down -0.43% while, spot gold prices are up +0.16%. As for overnight data releases, Japan’s October retail sales fell by -7.1% yoy (vs. -3.8% yoy expected) as a planned sales tax hike came into effect and a super-typhoon kept shoppers at home. The decline in retail sales comes at a time when the Japanese government is mulling the size of a fiscal stimulus. An economy ministry official said after the release that sales were also hurt by a drop in overseas tourists, including visitors from South Korea, while car and appliance purchases slid by double-digits.

Before this, at 10pm GMT last night, the much anticipated YouGov MRP model was released. This model correctly predicted a hung parliament in 2017, 9 days before the election when normal polls were still showing a Conservative majority. This model covers more than 100,000 potential voters and is much more seat by seat in its projections than normal polls. It projected a 68-seat Conservative majority, with 359 seats compared to Labour’s 211. The model predicts the SNP will control 43 seats and the Liberal Democrats 13 seats. Sterling rallied a few tenths of a percent on the news and it is trading +0.09% this morning. Just before the MRP model, a SavantsComRes Poll showed a Tory lead at 7pts down 3pt since last Thursday, but the market is clearly following the more statistically rigorous poll for now. Interestingly, the press release for the MRP suggested that if the current 11 point lead was cut to 7pt (as a couple of rival polls have shown this week) then it could lead to a hung parliament. So a healthy lead for the Tories but they need to maintain it if they want to win.

Staying with politics, it’s interesting to see that PredictIt now puts Elizabeth Warren’s odds for the 2020 democratic nomination below that of both Biden and more notably Buttigieg now. Warren led both as of just 5 days ago so there’s been a fairly significant shift away from her and towards the two more moderate candidates since her betting odds peaked on October 4th. This move has been mirrored in opinion polls, where Warren has lost 6pp of support since early October (to 15%) while Buttigieg has gained 4pp to (to 9%), while Biden has stayed steady at 30%. Demographically, Warren and Buttigieg draw most of their support from similar groups, namely college-educated white voters, who have apparently shifted their preferences recently. Partially, the fall in support for Warren has been driven by a weaker debate performance in early October, where multiple candidates attacked her over her expensive health care plan. It’s also notable that since her odds peaked on October 4th the S&P 500 has returned +6.83%. That was after markets struggled through August and them limped in September when her support was gaining. There were other things going on but there might be some correlation. All that said, the first primary is still far away on February 3, and the outcome remains tight and changeable.

Also overnight we heard from Bank of France governor Francois Villeroy de Galhau and he said that as a first step in a strategic evaluation the ECB should be clarifying the inflation goal. He said, “First, about the definition of our primary objective of price stability, we have to clarify in particular our various time horizons as well as our commitment to symmetry,” while adding a second step would be that the review should look into whether a separation between monetary and macroprudential policies should be lifted. He also added that third step of the overhaul should be to look at how climate change can be incorporated into the ECB’s monetary-policy analysis. The symmetry line will be the key take-away today.Whether markets believe the ECB could ever achieve this is another matter.

Back to yesterday and at the margin sentiment leaned a bit more positive with the heavy slate of data releases in the end not doing much to change the narrative for the Fed outlook. We’ll come to that further down but just in terms of markets, the S&P 500 and NASDAQ nudged up +0.42% and +0.66% on low volumes, which sent both to another round of all-time highs. For the S&P that also means that of the 19 trading days in November, the index has seen a positive return in all but 5 of those sessions. The positive-leaning sentiment also saw US 10y yields nudge a bit higher, +2.8bps to 1.769% with 2yrs up 4bps, helping the 2s10s curve to flatten -1.5bps to 14.1bps. Meanwhile, in Europe the STOXX 600 gained +0.32%, taking it to just 1.03% away from its all-time high from April 2015. The DAX and FTSE100 both gained similar amounts, up +0.38% and +0.36%. Fixed income was more muted, with bund yields down -0.1bps and OATs up +0.3bps.

In other news, Colombia’s anti-government demonstrations lost steam yesterday as fatigue set in after seven straight days of protests. Elsewhere, the Chile’s peso (-2.39%), Brazil’s real (-0.50%) and Colombia’s peso (-0.92%) all hit record lows yesterday as the region continues to be marred by elevated political risks.

Onto the details of the US data now. In order of relative importance, the preliminary October durable and capital goods orders data broadly beat expectations with most notable being the readings for durable goods ex transport (+0.6% mom vs. +0.1% expected) and core capex orders (+1.2% mom vs. -0.2% expected). The latter helped the six-month annualised trend also bounce back into positive territory while the year-over-year rate also appears to be stabilising, which should encourage the Fed.

As for the GDP data, the second reading for Q3 was revised up two-tenths to 2.1% qoq saar, helped by inventories, business sentiment and slightly stronger consumer data. The lone weakness was Q3 core PCE prices, which were revised down to 2.1%, albeit still growth friendly, while growth in corporate profits essentially slowed to a halt, rising just +0.2% qoq versus +3.8% in Q2. It’s worth noting that corporate profits are now down -0.8% yoy so the trend has been much weaker, even though we’re a long way from the energy crisis lows. It highlights how well the S&P 500 has done to rally hard this year. Although a different subset of firms, the S&P has obviously benefited more from buybacks and liquidity than raw earnings.

Not long after this data we got the November Chicago PMI, which improved +3.1pts to 46.3 even if that was a shade disappointing relative to expectations for 47.0. While this reading is off the lows it still remains weak and the ISM adjusted Chicago PMI at 46.9 is only just above the cycle lows in September. The remaining data was a bit of a wash with softer personal income data for October (0.0% mom vs. +0.3% expected) offset by slightly stronger-than-expected real personal spending data (+0.1% mom vs. 0.0% expected) while the core PCE deflator for October was in line at +0.1% mom, though the yoy figure was weaker at 1.6% versus expectations for 1.7%. That will likely force the Fed to lower their inflation forecasts for the fourth quarter.

Meanwhile, in Germany the October import price index matched expectations at -0.1% mom and November consumer confidence in France ticked up 2pts to 106 (vs. 104 expected) putting it at the highest since June 2017.

Looking at the day ahead, given the holiday in the US, data releases will be focused in Europe with preliminary November CPI due in Germany, October money and credit aggregates data due for the Euro Area and November confidence indicators for Europe. Away from the data we’re due to hear from the ECB’s Villeroy de Galhau, Coeure and Lane.

China May Put US Lawmakers On “No-Entry List” In Retaliation For Hong Kong Bill

Global Times editor-in-chief and notorious twitter troll, Hu Xijin ,tweeted Thursday that China is considering adding those who drafted the Hong Kong Bill of Rights and Democracy Act into law on a no-entry list, banning them from traveling to China’s mainland, Hong Kong, and Macau.

Based what I know, out of respect for President Trump, the US and its people, China is considering to put the drafters of the Hong Kong Human Rights and Democracy Act on the no-entry list, barring them from entering Chinese mainland, Hong Kong and Macao.

“The US now has new and meaningful tools to deter further influence and interference from Beijing into Hong Kong’s internal affairs. Following last weekend’s historic elections in Hong Kong that included record turnout, this new law could not be more timely in showing strong US support for Hong Kongers’ long-cherished freedoms,” Rubio said in a statement.

The Hong Kong Bill of Rights and Democracy Act was first introduced during the 116th US Congress, as a direct response to the Hong Kong extradition bill, also known as the Fugitive Offenders and Mutual Legal Assistance in Criminal Matters Legislation (Amendment) Bill 2019, was a proposed bill regarding extradition of fugitives in Hong Kong to mainland China. The proposal sparked violent protests in the city, now entering the sixth month as the regional economy has crashed into a nasty recession.

The US House bill was sponsored by Jim McGovern (D-MA) and Chris Smith (R-NJ), while the Senate bill was sponsored by Marco Rubio (R-FL).

Co-sponsors for the US House bill included Tom Suozzi (D-NY), Scott Perry (R-PA), Brad Sherman (D-CA), and Brian Fitzpatrick (R-PA).

Co-sponsors for the US Senate bill included Jim Risch (R-ID), Bob Menendez (D-NJ), Ben Cardin (D-MD), Tom Cotton (R-AR), Angus King (I-ME), Ed Markey (D-MA), and Josh Hawley (R-MO).

It’s still not clear which US lawmakers could be placed on the no-entry list, but one thing is clear, Rubio isn’t traveling to China’s mainland, Hong Kong, and Macau anytime soon.

North Korea Launches Missiles Amid Stalled Nuclear Talks With US

North Korea launched two unidentified projectiles on Thursday, in what could be the latest sign that a nuclear disarmament deal with the US might be unattainable unless President Trump offers fresh concessions, reported Reuters.

28-Nov-2019 03:07:57 AM – NORTH KOREA HAS LAUNCHED WHAT APPEARS TO BE A MISSILE — JAPAN COAST GUARD

28-Nov-2019 03:24:02 AM – APPARENT MISSILE APPEARS NOT TO HAVE LANDED IN JAPAN’S EXCLUSIVE ECONOMIC ZONE — JAPAN DEFENCE MINISTRY

28-Nov-2019 03:25:39 AM – JAPAN’S DEFENCE MINISTRY SAYS N.KOREA MISSLE LAUNCHES TO DATE ARE A SERIOUS ISSUE FOR JAPAN, INTERNATIONAL SOCIETY

South Korea’s Joint Chiefs of Staff said both missiles were launched Thursday from North Korea’s east coast.

Japan’s Defense Ministry said, “what appears to be a ballistic missile” fired by North Korea landed outside of its territorial waters.

Prime Minister Shinzo Abe told reporters that the missiles didn’t enter Japan’s airspace or “exclusive economic zone” at sea.

The defense ministry didn’t have any further information on the missile launch.

The latest missile test comes as nuclear negotiations with the US have likely broken down.

North Korean leader Kim Jong-un has told President Trump that he has until the end of the year to offer new concessions, such as removing economic sanctions, to salvage nuclear talks.

Trump has said those concessions will only come when North Korea completely abandons its nuclear weapons, a move that would be political suicide for Pyongyang.

The missile test also comes hours after Trump signed the Hong Kong Bill of Rights and Democracy into law. This move has infuriated China, as it appears the US is set to intervene in Hong Kong affairs. It should be noted that North Korea and China are highly interconnected politically and economically.

{kind=link}