President Trump is refusing to engage and Democrats have concluded they will press ahead anyway, rendering a historic undertaking little more than a foregone conclusion.

Excuse me for pointing out the result was a foregone conclusion whether the White House was present or not.

“That is a tragedy,” said Philip Bobbitt, a Columbia University law professor and a leading expert on the history of impeachment. The framers of the Constitution were careful to design a process for removing a president from office that they hoped would rise above the nation’s petty political squabbles, he said.

Tragedy?

Yes, witch hunts are a tragedy. Republicans found that out when they foolishly went after Bill Clinton.

Boycott the Process

Neal Katyal, the former acting solicitor general under President Barack Obama, called it “deeply dangerous” for the target of an impeachment like Mr. Trump to simply boycott the entire process.

Does the law prohibit a boycott? Does the law require the president to testify against himself? Is it dangerous to accept the advice of legal council?

Rule Book

“The fact is that the House Democrats are essentially giving Trump the same process as previous presidents have received, and it’s Trump who is trying to throw out the rule book” and attack the process at every turn, he said. “Our founders put impeachment in the Constitution as a critical safeguard for the people, and what Trump is trying to do with these baseless attacks is read the impeachment clauses out of the Constitution.”

His response has been an all-out attack on the process itself. He has ordered administration officials not to testify or hand over documents. And he is urging Republicans not to cooperate with their counterparts the way they did during Mr. Clinton’s impeachment.

Excuse me for pointing out that the law is the rule book.

What law has trump violated by boycotting the process?

Shocking?

Of course it is.

Trump continually followed the advice of legal council instead of sticking his foot in his mouth and Tweeting about it.

Click on that link for an amusing video and transcript.

Comments on the Unreal World

Back in the real world, or do I mean unreal world, I get accused of having TDS every time I attack Trump’s idiotic trade policy.

I also get accused of being an extreme Left-Wing nutcase when I defend Trump.

The fact is, I don’t like Trump but I voted for him and would again vs Hillary.

I am a staunch anti-war, fiscal conservative, Libertarian, who does not give a damn about anyone’s race, religion, sex, or age. I believe in equal rights. I also believe in the right to choose. If two women or two men want to get married, I believe it’s none of my business.

I believe that’s a winning platform.

Alas, one cannot get nominated on that platform. Thus, I always have extreme voting compromises to make.

Exxon Mobil Prevails Over “Politically-Biased” New York AG In Major Climate-Change Case

Exxon Mobil has triumphed over New York State and its crusading Attorney General Letitia James in the largest climate-change-related case ever brought against a major energy company in the US.

That Exxon Mobil prevailed is hardly a surprise. Rather than being inspired by investors with genuine complaints, the case was tainted by politics from the beginning. It was brought by New York State’s crusading Attorney Generals, Barbara Underwood and her successor, Letitia James (the current New York State AG), centrist Democrats clearly hoping to punish one of the world’s largest energy companies for purportedly suppressing and misconstruing research about the environmental impact of fossil fuels. Unfortunately, the Manhattan judge who handed down the ruling must have missed Greta Thunberg’s UN speech.

When the case was filed in October of last year, the AG’s office had already been investigating the energy giant for nearly four years. Perhaps James’s office believed they had simply invested too many resources and too much time into the case to let Exxon Mobil walk.

The lawsuit alleged that Exxon Mobil was responsible for $1.6 billion in investor losses by lying to them about the impact of future climate change regulation on its business. Specifically, the company was accused of fabricated a “proxy cost” metric upon which Exxon Mobil based its projections, Reuters reports.

First of all, these “projections” are merely that – estimates, informed guesswork at best. Even these “proxy cost” figures probably won’t be exactly accurate. But the AG’s office thought it had evidence that the company had crossed a legal line by distributing one set of numbers, while using another “more conservative” set of forecasts internally.

By the last day of the trial, it had become clear that the AG’s case was crumbling. During closing their closing statement, the AG dropped the two most damning of four charges without explanation – these were the charges claiming that Exxon’s misstatements were part of a deliberate scheme to mislead investors, and that the data were critical to investors’ decision-making when deciding whether to buy ExxonMobil stock (we’re not lawyers, but having purchased securities before, we can say with some authority that these seems extremely doubtful).

After those charges were dropped, the judge in the case, New York Supreme Court Justice Barry Ostrager, was left to decide whether Exxon had violated New York State’s Martin Act by issuing public statements (in this case, disclosures of the “proxy costs”) that were misleading. Clearly, the judge disagreed.

Here’s a summary of the judge’s comments courtesy of Bloomberg.

“The office of the Attorney General failed to prove, by a preponderance of the evidence, that ExxonMobil made any material misstatements or omissions about its practices and procedures that misled any reasonable investor,” Ostrager wrote in a 55-page ruling. James “produced no testimony either from any investor who claimed to have been misled by any disclosure,” while the company disclosed its use of both the proxy cost and the greenhouse gas metrics no later than 2014, the judge said.

On Oct. 30, former Exxon CEO Rex Tillerson took the stand (many might not remember this; it was easily overshadowed by the latest Brexit deadline delay and the media circus on Capitol Hill). During his testimony, Tillerson alleged that the case was politically motivated, and that the AG’s office was deliberately misleading Exxon Mobil’s intentions. But it shouldn’t take a CEO to understand what’s happening here. Anybody with a background in corporate strategy or finance would probably find the notion that developing a range of internal-only projections is illegal to be disturbing. It’s a widely used practice.

As we’ve mentioned in the past, though it’s commonly applied to insider-trading cheats and embezzlers, ‘securities fraud’ is, in reality, much more vague: Any kind of corporate wrongdoing – or even normal behavior – can be construed as securities fraud if it wasn’t explicitly disclosed to investors.

Investment Grade Credit Faces Party Hangover In 2020

Authored by Bloomberg macro commentator, Sebastian Boyd

Rising corporate leverage will shut down the investment-grade credit party in 2020 after posting a whopping 14% return in 2019. Making money in this space was easy after the 4Q 2018 sell-off and the Fed’s dovish shift at the start of January. Next year will be a very different story.

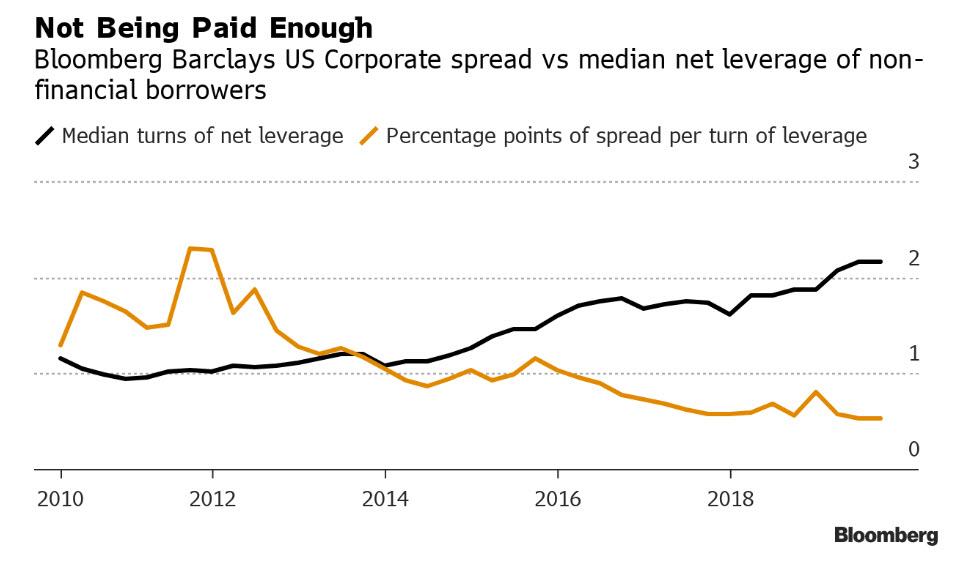

At the end of 3Q, the spread on the Bloomberg Barclays U.S. Corporate index was 115 bps, or 53 bps per median turn of leverage for the non-financial borrowers in it. That’s the lowest in 10 years. Muted expectations for corporate earnings suggest companies may struggle to deleverage.

Spreads haven’t returned to the lows they reached in 2018, but investment-grade yields tumbled. The last time they fell as steeply as they did this year was in 2009 and 2010, just after the Lehman Brothers bankruptcy.

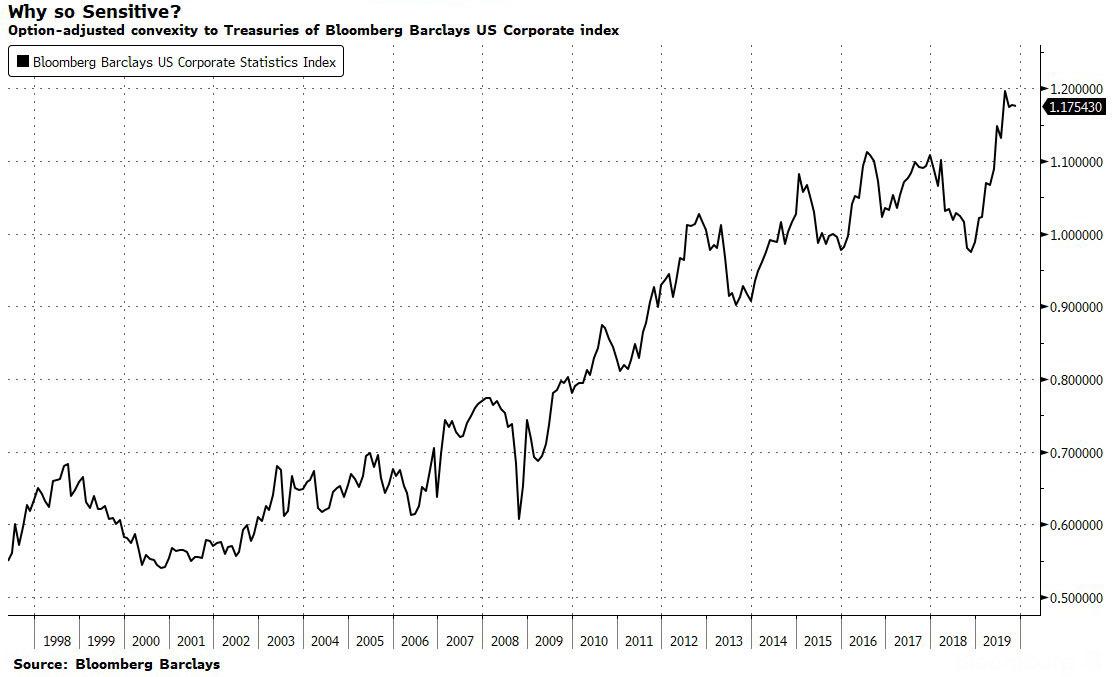

Modified duration in the Bloomberg Barclays index is the highest since the late 1970s, and convexity is the highest in at least two decades. That’s a result of falling coupons and lower yields, and taken together it means high-grade debt is very sensitive to shifts in Treasury yields.

The amount of U.S. corporate bonds maturing in the next 12 months is greater than at any point since 2017, according to the Bloomberg Barclays Short Term U.S. Corporate index — 97% of which is due in a year or less. Supply based on refinancing isn’t necessarily bad news for bondholders, except that it will likely come with lower yields.

While there has been spread decompression in high yield, we haven’t seen the same in investment grade. The gap between BBB and AA spreads is in line with the three-year average. But that’s not necessarily a good thing, since the last three years have been a time of exuberance and spread compression.

On the other hand, the flow story remains solid. In these days of low yields and rising risk, investment- grade credit appeals. Taiwanese life insurers are big buyers of Yankee bonds and are likely to remain a source of demand unless the Taiwan dollar significantly appreciates versus the greenback.

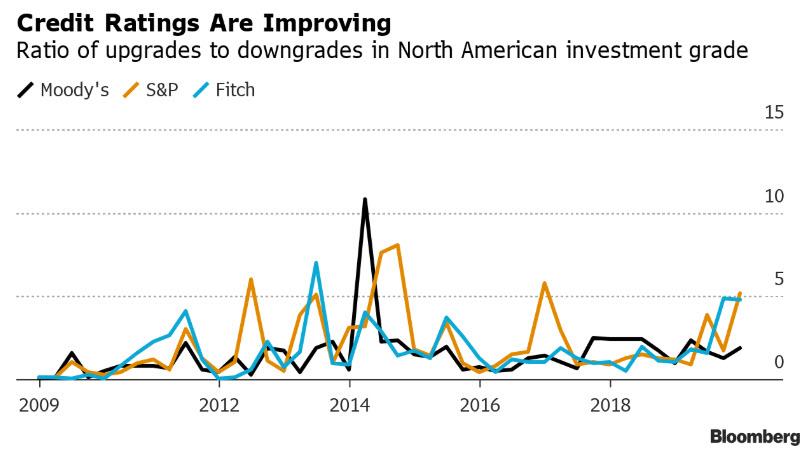

Despite rising leverage among investment-grade companies, cash flow has improved and credit-raters are being generous. The ratio of upgrades to downgrades has risen in recent quarters, which is hard to correlate with either growth or leverage.

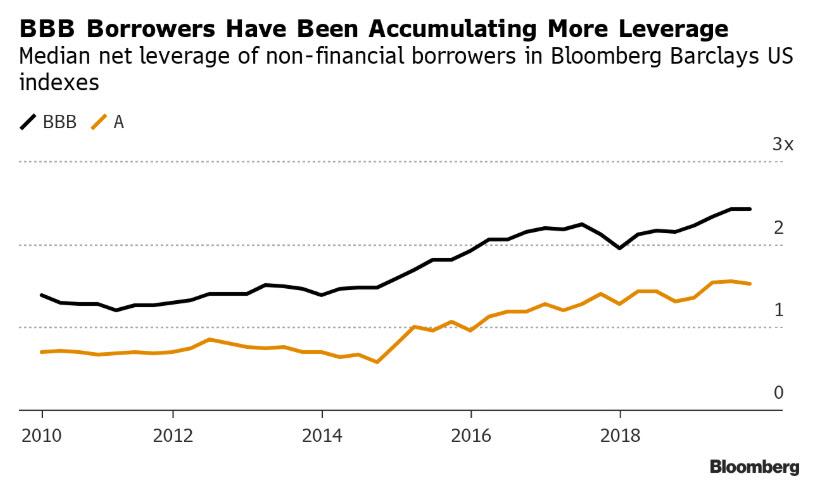

The famous BBB time bomb hasn’t blown up yet. There are reasons to think it might not explode at all, helped by the benign attitude of ratings firms. The chart below shows how the leverage of companies currently rated BBB has been rising. A number of those were downgraded to BBB specifically because of rising leverage, so the picture may not be as bad as it looks. But what it does suggest is that those companies haven’t been deleveraging.

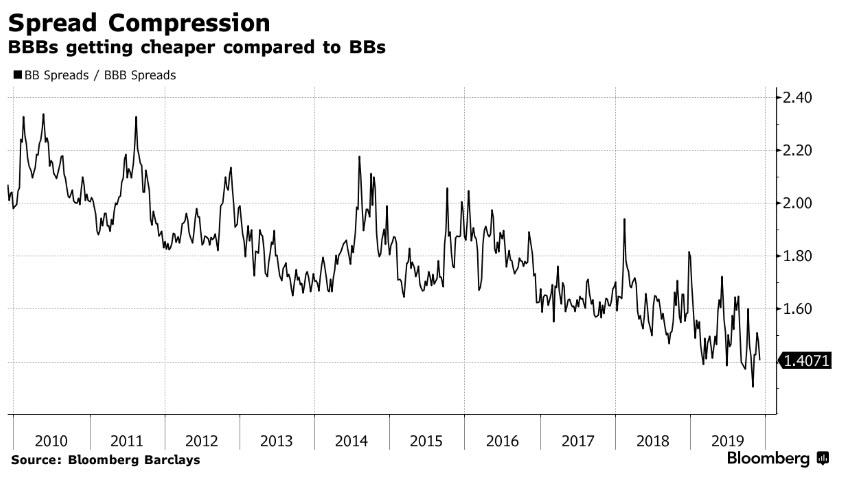

The BBB index paid 62 bps per median turn of leverage at the end of 3Q. That’s low historically but pretty much in line with where it has been since 2Q 2017. You’re not getting paid enough to own that risk, but you haven’t been for a while. On the other hand, the widening of BBBs versus BBs means the higher-grade bonds appear relatively cheap.

Taken together, it’s clear that the story of high-grade debt next year will be told through deleveraging. Yields tumbled in 2019, which helped spur a great year for investors, and borrowing likely will remain relatively cheap in 2020. Some will be able to profit from that. But leverage levels are elevated — and it doesn’t look like companies will have the cash to substantially reduce their debt loads. Without a substantial deleveraging push, it’s hard to see what would enable the market to sustain it’s high.

“It’s About To Get Very Bad” – Repo Market Legend Predicts Market Crash In Days

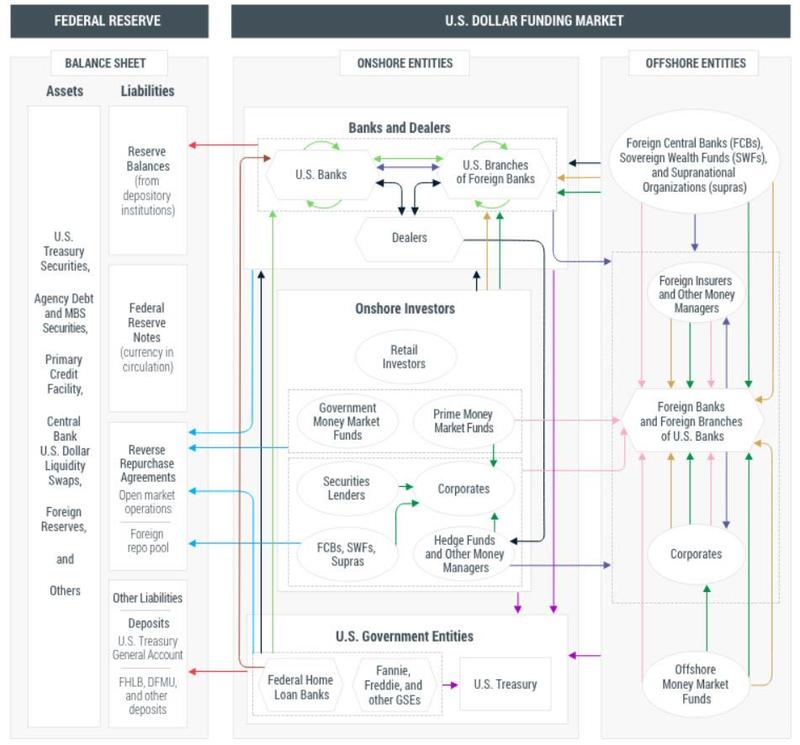

For the past decade, the name of Zoltan Pozsar has been among the most admired and respected on Wall Street: not only did the Hungarian lay the groundwork for our current understanding of the deposit-free shadow banking system – which has the often opaque and painfully complex short-term dollar funding and repo markets – at its core…

… but he was also instrumental during his tenure at both the US Treasury and the New York Fed in laying the foundations of the modern repo market, orchestrating the response to the global financial crisis and the ensuing policy debate (as virtually nobody at the Fed knew more about repo at the time than Pozsar), served as point person on market developments for Fed, Treasury and White House officials throughout the crisis (yes, Kashkari was just the figurehead); played the key role in building the TALF to backstop the ABS market, and advising the former head of the Fed’s Markets Desk, Brian Sack, on just how the NY Fed should implement its various market interventions without disrupting and breaking the most important market of all: the multi-trillion repo market.

In short, when Pozsar speaks (or as the case more often is, writes), people listen… and read.

And since Pozsar moved from the public sector to Credit Suisse in February 2015 to write his market moving (at least for those who can understand it) periodical, “Global Money Notes”, it has been relatively easy to keep track of his thoughts and observations on the repo market as they change over time.

Which brings us to his latest Global Money Notes, #26, published overnight, and in which Pozsar delivers his scathing assessment of the Fed’s latest intervention to stabilize repo markets since the September 16 repocalypse, that sent overnight repo rates as high as 10% in what was previously seen as an impossible event. Of course, as we saw three months ago, not only was the event possible, but it led to a shockwave of confusion as to what caused it, prompting even the BIS to chime in over the weekend with a fascinating theory, discussed previously, that hedge funds were among the causes for the repo fireworks as they scrambled to procure funding to prevent their massively levered relative value trades in which they bought TSYs and sold ‘equivalent’ derivatives contracts, from collapsing.

While Pozsar does not focus as much on the causes of the repocalypse, having previously covered them in depth in his prior Money Notes (and he would know: as noted above, Pozsar is the de facto architect of the modern US repo system), what he does do in his latest note, titled ominously “Countdown to QE4” is explain why the Fed’s interventions to date have failed to reverse the underlying plumbing issues in the banking system, manifesting themselves in a dramatic increase in Treasurys at the biggest US bank, JPMorgan…

… offset by a decline in reserves, i.e. cash…

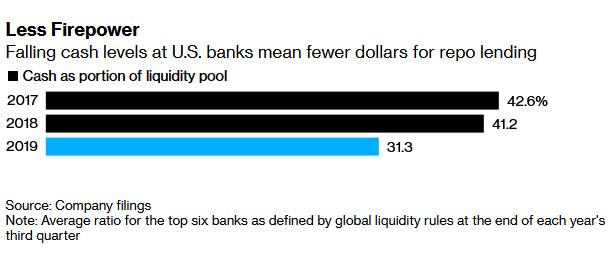

… at the largest US banks, something we addressed previously when we discussed how JPMorgan gamed the financial system to trigger “NOT QE”, and a topic that Bloomberg touches on overnight in “Repo Firepower Reduced by Falling Cash Levels at Big U.S. Banks.”

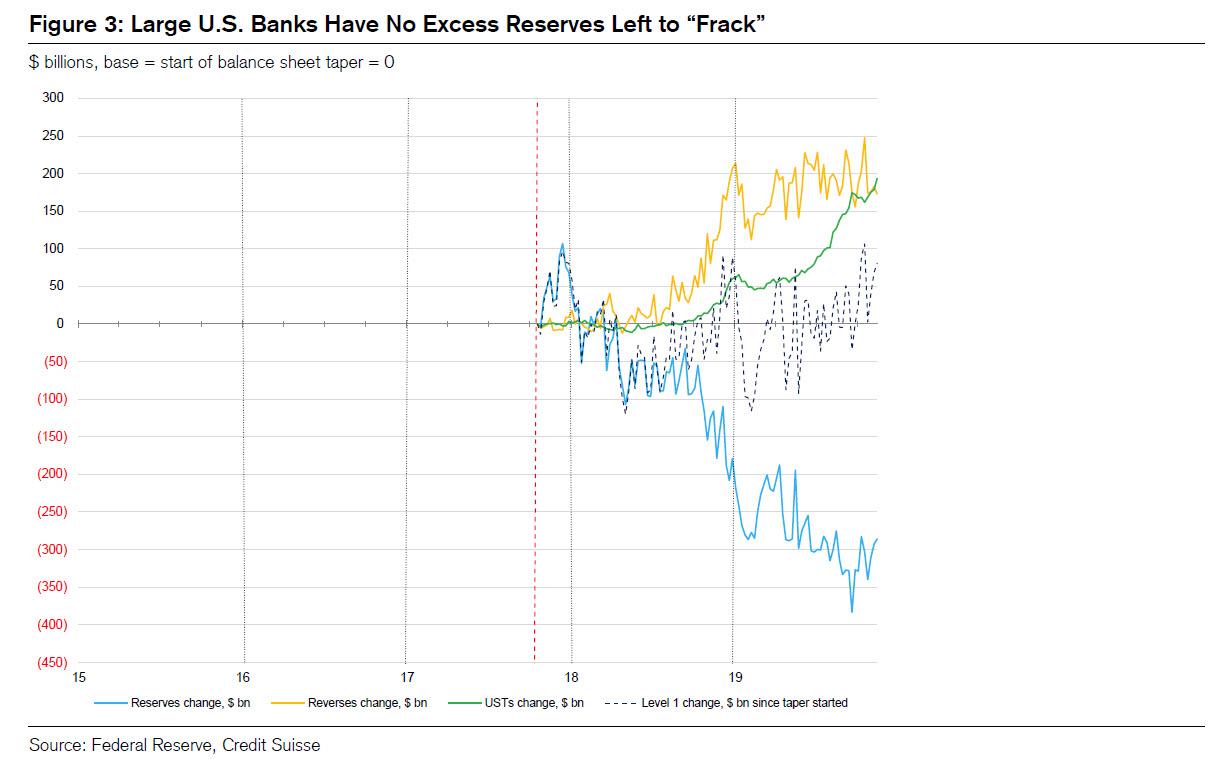

As Pozsar cautions, the core problem at the heart of the repo blockage is that as banks shifted from owning reserves to collateral (mostly Treasuries), for reasons we will address shortly, large U.S. banks like J.P. Morgan that are central to year-end flows spent some $350 billion of excess reserves on collateral since the beginning of the Fed’s balance sheet taper, leaving banks (and especially JPMorgan) dangerously low on reserves.

And while one can debate why banks shifted away from reserves to “collateral”, Pozsar has a simple theory: “dealers and banks loaded up on collateral as a trade – a trade they were supposed to be taken out of by eventual coupon purchases by the Fed.” In other words, here is a former Fed official admitting that banks were purchasing Treasuries as nothing more than a QE frontrunning ploy, something which the Fed has previously sworn was never the intention behind QE. After all, if it emerges that the Fed is essentially facilitating taxpayer-funded and perfectly legal frontrunning, making bank execs even richer in the process, the US central bank would have even fewer fans. And yet, here is arguably the most respected ex-Fed staffer explaining that one of the core roles of QE is just that.

Alas, here a problem emerged, because “the Fed never did that, and for the first time we’re heading into a year-end turn without any excess reserves.”

Indeed, instead of buying coupon bonds as Dealers have been quietly demanding behind close doors, a process which would allow them to sterilize their massive Treasury holdings, the Fed announced in October it would only buy T-Bills in order to not freak out the market that it is officially launching QE 4 (as a reminder, the only semantic distinction between whether the Fed is doing QE or not doing QE is whether it is soaking up duration; the Fed’s argument is that since Bills don’t have duration, it’s not QE. However once Powell starts buying 2Y, 3Y, 5Y and so on Treasuriess, the facade cracks and the Fed will have no more defense that what it is doing is precisely QE 4). And by buying Bills, it is not allowing commercial banks to exchange their coupon holdings for reserves (cash), but merely results in recirculation of sterilized Bill purchases.

Now most people don’t understand this, and instead repeat the old maxim “don’t fight the Fed” which they claim is adding liquidity through repos and bill purchases, and what’s not in the system now will be there on year-end, and the turn will be just fine.

Only as Pozsar says “Not so fast!” and explains:

What we need for the [year-end] turn to go well are balance sheet neutral repo operations, or asset purchases aimed at what dealers bought all year: coupons, not bills – the former to get around foreign banks’ balance sheet constraints around year-end, and the latter to ensure that excess reserves accumulate with large banks like J.P. Morgan. Unfortunately, the Fed is doing neither.

He goes on:

Repo operations are done through the tri-party system which means they aren’t nettable, which in turn means that once balance sheet constraints start to bind around year-end, foreign dealers will take less liquidity from it to lend it to those in need on the periphery: central bank liquidity is useless unless primary dealers have balance sheet to pass it on, and that they’ve been passing it on since September does not mean they will at year-end.

Bill purchases are also ill conceived because banks and dealers don’t own any bills and so don’t have anything to sell to the Fed to boost their excess reserves ahead of year-end. In our view, the notion that bill purchases will force money funds down the yield curve to buy short coupons from primary dealers who would then pay off their repos with banks so that banks build up some excess reserves into year-end involves too many moving parts…

Which brings us to the first of the key observations made by Pozsar: since the Fed’s repos and T-Bill monetizations have done virtually nothing to boost prevailing reserve levels on a sustained basis, “year-end balance sheet constrains will preclude primary dealers from bidding for reserves from the Fed through the repo facility or through repos from money funds. The slope of money market curves suggest that excess reserves won’t build up at banks, and so U.S. banks will not be able to fill the market making vacuum left by foreign banks.”

In other words, the already thin liquidity at year end (which as a reminder, last December 31 sent repo rates soaring even though excess reserves were about $100 billion more than they are now) could get far worse as a result of the Fed’s inability to properly address the reserves (cash) shortage plaguing banks.

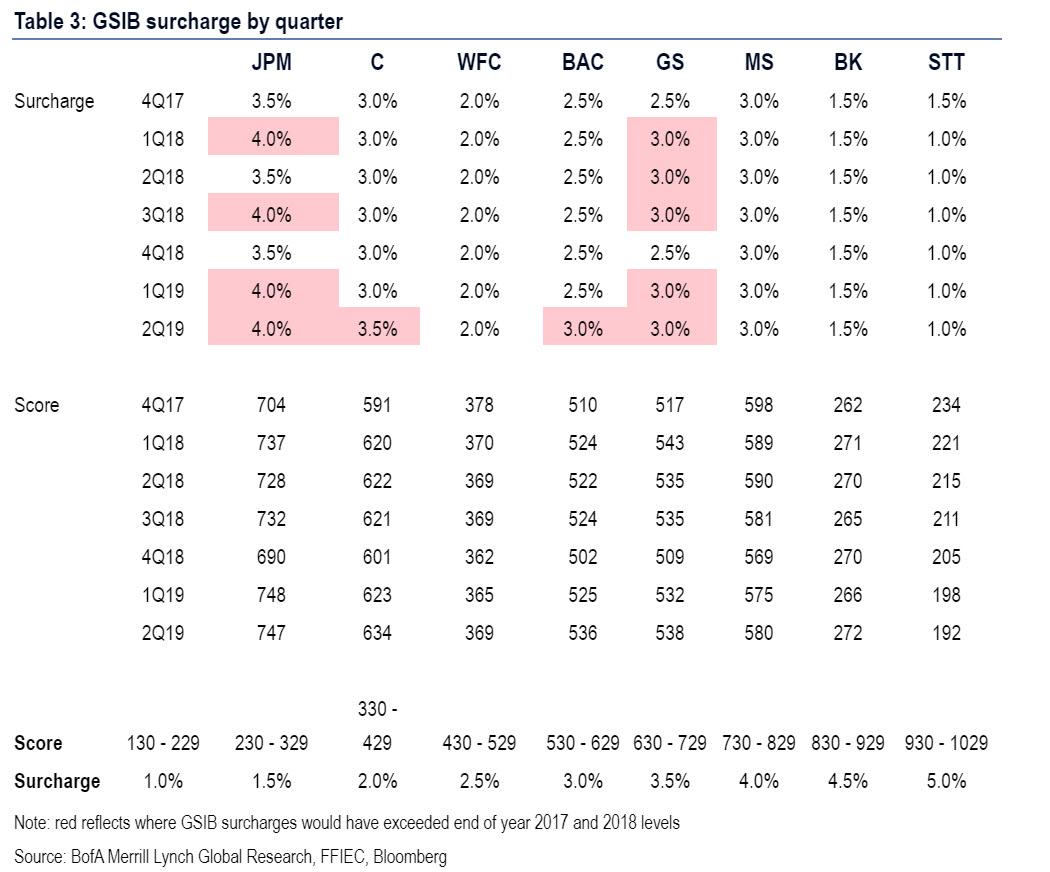

There is another reason why year-end liquidity is likely to get far worse, and it has to do with bank year-end G-SIB surcharges imposed by regulators on US banks on the last day of the quarter and year. As we discussed two weeks ago, and as Pozsar explains, “running low on excess reserves is only one factor that determines how bad the vacuum

in market making can get around year-end turns. G-SIB scores are the other, as they determine what banks can do with whatever excess reserves they have at year-end: lend them through repos, spend them on Treasuries, or lend them through FX swaps, – in that specific order as repos are less punitive for banks’ G-SIB score than FX swaps.”

We previously provided a simple schematic of how bank G-SIB scores are calculated in the following chart…

… but the bottom line is the following: banks seek as low as GSIB score as possible at year end to minimize their period end surcharge:

As Pozsar further notes, “U.S. banks are particularly sensitive to their G-SIB scores this year, as they all moved up to a higher surcharge bucket due to bigger Treasury holdings and a heavier repo footprint: every U.S. bank except Morgan Stanley has an incentive to shrink its score into year-end.“

It is here that a unique paradox emerges: the highest stock prices rise, the higher the implied score (a negative). Some more observations from the repo guru:

G-SIB scores are a moving target as they are influenced by markets. The themes pushing G-SIB scores in the wrong direction this year are the equity market rally and the flat curve:

(1) the rally in equities is inflating scores through G-SIBs’ market capitalization and the value of equities G-SIBs hold as trading assets or available for sale securities;

(2) the flat yield curve is inflating scores through G-SIBs’ bloated Treasury portfolios, which, given auction supply and the equities rally, may grow further into year-end.

While G-SIBs can’t do a thing about the equity market, and, as the largest primary dealers, they also can’t not take down more Treasuries at auctions if there are insufficient bids; but they can do two things to offset some of the factors that are pushing their scores up:

collateral upgrades where they repo equities out to raise some excess reserves, or repo or outright sell some of their Treasuries to raise some excess reserves.

clamping down on market making in the FX swap or sponsored repo markets whereby they’d add to the vacuum in market making triggered by foreign banks

Which brings us to the other key year-end dynamic: when G-SIB scores are too high and banks need to reduce them, they do so by swapping assets for excess reserves. In other words, when banks hold lots of excess reserves their G-SIB scores are relatively low and they have room to lend their excess reserves through repos and FX swaps, and conversely, when banks are low on excess reserves their G-SIB scores are high and that may force them to clamp down on market making.

Well, as we know from the discussion in the first part above, bank excess reserves have collapsed and as a result G-SIB scores are high, “and banks are lowering their scores by swapping assets for reserves to scrape together some excess reserves ahead of the year-end turn – and those scraps are all U.S. banks will have to lend into the market making vacuum left by foreign banks around year-end.”

In the best case scenario envisioned by Pozsar, bank will lend mostly via repos and not FX swaps given their G-SIB scores. “But these flows will be scraps of excess reserves, not bursts.”

As for the worst case scenario, it is one where “collateral upgrades aren’t sufficient and U.S. banks stop making markets in FX swaps and so exacerbate the vacuum triggered by foreign banks.”

Which brings us to the first of Pozsar’s ominous conclusion: “We are on track to realize the worst case scenario, and the market doesn’t price for that.”

Here, Pozsar offers a brief detour offering some practical observations as we enter the year-end period, in which he notes that “according to our conversations with market participants, U.S. G-SIBs rely heavily on Canadian pensions for equity upgrades to accumulate some excess reserves for the turn. Furthermore, some large U.S. banks are selling Treasuries to lower their G-SIB scores and scrape together some excess reserves to harvest higher repo rates over year-end.”

Finally, and most shockingly, the Credit Suisse strategist writes that “at least one large U.S. bank appears to be pricing some of its FX swaps trades such that it misses those trades – a polite way of clamping down market making activities.”

Here some readers may have a “lightbulb” moment because what Pozsar just described is that “at least one large US bank” appears to be gearing for a collapse in the FX swap market, with a very specific intention: to force a market crisis in the coming days and force the Fed to launch full blown QE 4, not just a monetization of T-Bills.

More on that momentarily.

But first, some more observations from Pozsar on how a year-end crisis may play out: “if markets won’t let G-SIBs reduce their scores, G-SIBs will retort to scale back market making, like the one U.S. bank that’s already pricing FX swap trades to miss them. We do not see the pressure from this in FX swap markets yet as foreign banks still have balance sheet to pick up the slack, but pressures will come as we get closer to year-end.”

Pozsar’s point is that the realized year-end turn in FX swap markets “will be worse than what is priced by the market regardless of whether we end up in the best case or worst case scenario.”

This literally means that no matter what the market does from now until year end, there is simply not enough cash and/or liquidity to allow the plumbing of the market to cross into 2020 without a crisis, or as Pozsar puts it, “in our view, the FX swap market is expecting too much similarity between the current year-end turn to last year’s turn. That’s a mistake as last year’s dynamics were different” for the following reasons:

large U.S. banks still had excess reserves to lend, but this year they do not; and

they got a G-SIB relief from a 20% fall in equities, but this year end they do not

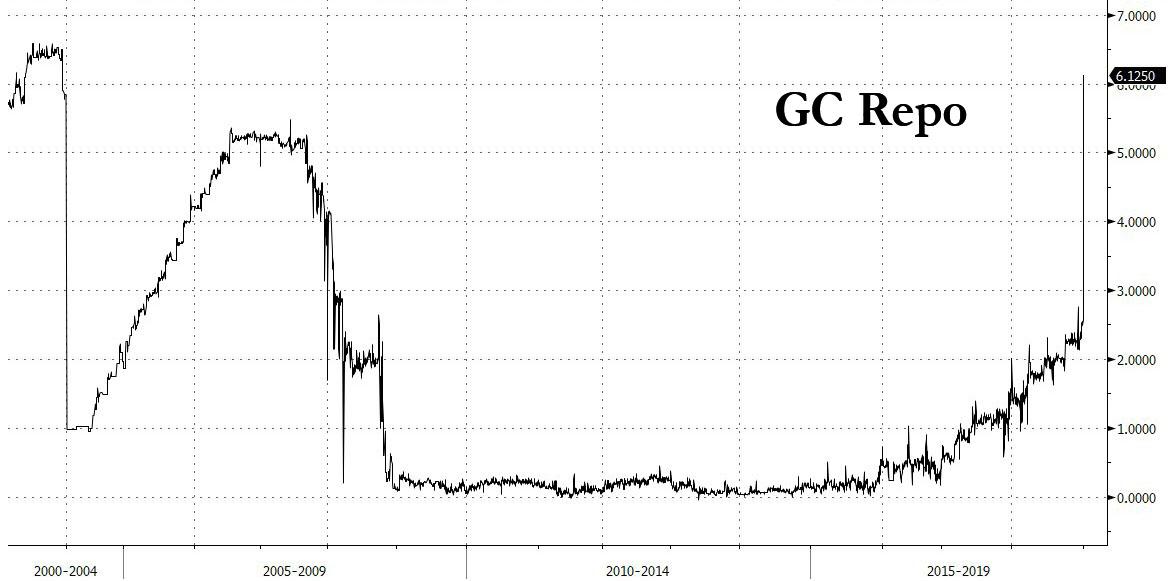

One other key difference from the brief meltup in repo rates last year end: back then, lower G-SIB scores allowed large U.S. banks to spend their hoards of excess reserves on more complex trades like FX swaps, and the year-end turn went down as a non-event – in FX swaps, but not repos. Recall that repo printed at 6.5% on December 31st spot.

This year, Zoltan warns, may be the opposite, as higher G-SIB scores will favor repos over FX swaps when deploying excess reserves, but while FX swaps will be a disaster, repos may still print as bad as last year-end. As for FX swaps, well we’ll leave Pozsar to explain what may happen there:

“FX swaps could end up as the orphaned asset class without an obvious backstop, and that may force banks in some parts of the world to the edge of the proverbial abyss“

As a reminder, this dire warning comes from the man who probably knows the nuances of the US repo market better than anyone else in the world.

But wait, there’s more.

Recall that in its BIS’s recent take on the fireworks in the repo market, the central banks’ central bank pointed the finger at massively levered hedge funds engaging in Treasury relative value trades (think of these as a modern twist on the LTCM trade) as the catalyst for the Sept 16 repo explosion,

“High demand for secured (repo) funding from non-financial institutions, such as hedge funds heavily engaged in leveraging up relative value trades,” was a key factor behind the chaos, said Claudio Borio, head of the monetary and economic department at the BIS.

The BIS’s finding was novel, and surprising, as it highlighted the “growing clout of hedge funds in the repo market” echoing notes something we pointed out one year ago: hedge funds such as Millennium, Citadel and Point 72 are not only active in the repo market, they are also the most heavily leveraged multi-strat funds in the world, taking something like $20-$30 billion and levering it up to $200 billion. They achieve said leverage using repo.

And, as we further discussed, the hedge fund strategy in question involves buying US Treasuries while selling equivalent derivatives contracts, such as interest rate futures, and pocketing the arb, or difference in price between the two. While on its own this trade is not very profitable, given the close relationship in price between the two sides of the trade. But as LTCM knows too well, that’s what leverage is for. Lots and lots and lots of leverage.

We took this detour into how repo affects the hedge fund world, because Pozsar had a rather gloomy prediction about the fate of hedge funds should his dismal forecast materialize. As he writes, “the relative value (RV) hedge fund community is certain that they will have balance sheet to fund their bond basis trades at reasonable rates over the year-end turn. Why?

“Because we have locked up forward settling sponsored repos with dealers over the turn, and market making in sponsored repos is less likely to be scaled back than in FX swaps.”

Well, not so fast:

Forward settling sponsored repos are meant to substitute for the balance sheet that the RV hedge funds will lose from foreign banks around year-end, but their risk is that RV hedge funds don’t know the rate at which they’ll get balance sheet at year-end – forward settling sponsored repos only lock in balance sheet capacity, but not the rate and with all due respect, RV funds are ignoring the incentives of repo dealers.

Fast forwarding to the punchline, the problem is that without having intelligence about the balance between forward settling sponsored repos and banks’ progress to scrape together excess reserves to fund those forward repos, Pozsar warns that relative value funds “don’t know where the rate on their forward settling sponsored repos will print. And given that there are no signs of excess reserves accumulating into year-end, it is likely that the RV community will be taxed excessively to get over the year-end turn.“

The bolded means that massively levered hedge funds may be in for a shock in the coming days, as bank sponsors are woefully low on the reserves that the hedge funds need to perpetuate their RV trades (and leverage) into the new year.

This, too, is a problem. Here’s why:

As the excess reserves missing from bank portfolios will be filled by a small cadre of primary dealers that do not have balance sheet constraints and they’ll fill the hole and keep a lid on repo rates. Sure, let’s assume for a moment that those primary dealers that are not subject to Basel III – Amherst Pierpont Securities LLC, Cantor Fitzgerald & Co. and Jefferies LLC – and three Canadian dealers whose year-end was on October 31st – the Bank of Nova Scotia, BMO Capital Markets Corp. and TD Securities (USA) LLC – will save the day by borrowing enough from the Fed to bridge your needs in repo markets.”

Pozsar’s snarky conclusion to this? “Maybe, maybe not.” We’ll take the latter.

Putting all of the above together, and for those unfamiliar with the nuances of the repo market this summary may be a critical catch up, the risk to the “benign and optimistic view” currently prevailing among market participants, is mostly as related to the FX swap market: given that i) excess reserves are gone and ii) the G-SIB scores bind, “the FX swap market, unlike last year-end, may end up without a lender of next-to-last resort, and so it will likely trade at implied rates far worse than anything that we’ve seen in recent year-end turns.”

If that will indeed be the case, Pozsar envisions a last few weeks of the years in which the handful of Canadian dealers you expect to lend to you to fund your bond basis trades, will instead lend in the FX swap market instead “and you’ll end up short… and you may end up as a forced seller of Treasuries.”

What is even more stunning is that banks themselves may have an incentive to cause this lock up in the FX swaps market: Pozsar’s overarching point is that “a dealer is a hedge fund’s enabler, not its friend, and dealers that co-exist with large bank operating subsidiaries have an incentive to introduce imbalances the repo market to boost the value of their banks’ excess reserves, and dealers that have the balance sheet to take liquidity from the Fed’s repo operations will not necessarily do repos with RV hedge funds if FX swaps offer a much better value.“

* * *

With us so far? Good, because we are finally getting to the punchline.

In this dystopian world described by Pozsar, in which banks have too much “collateral” (Treasuriess) on their books, and not enough “reserves” (cash), where big commercial banks are unable to lend out to the rest of the banking system as they themselves don’t have enough reserves, and where there will be an added pressure to boost reserves in the last days before Dec 31, Pozsar’s big picture conclusion is that “the safe asset – U.S. Treasuries – is being funded o/n and therefore it depends on balance sheet to be held and printed. Balance sheet for the safe asset isn’t guaranteed around year-end and if balance sheet won’t be there, the safe asset will go on sale.”

Translated: “Treasury yields will spike”, Pozsar warns, identifying the trigger of forced sales of Treasuries around year-end as the FX swap market. It gets worse, because the selloff that is triggered by a freeze in the FX swap market will promptly lead to a crash in the bonds market, and spread from there, or as Pozsar puts it, “these funding market stresses will likely pull away capital and hence balance sheet from equity long-short strategies which could spill over into a broader equity selloff… during a Treasury selloff – that’s not the right kind of risk parity Christmas.“

Which brings us to punchline #1: the dismal liquidity situation within the US commercial bank sector is so dire, that the shortage of reserves will start a cascade of liquidations beginning in the FX swap market, progressing to Treasurys, and culminating in stocks… and a full-blown market crash.

When these pressures will show up and how long they will last is the last big question asked by Pozsar and as he answers, “here it’s hard to have a definitive answer: it depends. It depends on how equities do, which depends on the trade deal and other random tweets. It depends on how auctions go, which depends on the equity market and the curve slope relative to actual funding costs.”

One especially ironic development is that higher stock prices in the coming weeks will only make the matter worse! “If the equity market rallies and auctions go poorly, G-SIB scores will keep going higher and the risk that funding market pressures from managing G-SIB scores will show up starting the last two weeks of the year and will last longer than just the spot turn are rising.“

Said otherwise, the dire warning from arguably the top expert on the repo market is that the adverse cascade will begin in the last two weeks of the year meaning that… traders have about a few days to take preventative measures.

That said, there is one potential “out” – the Fed steps in.

Just in case anyone still has a rosy outlook on what the next three weeks may bring, Pozsar repeats his devastating conclusion: “Year-end in the FX swap market is thus shaping up to be the worst in recent memory, and the markets are not pricing any of this. Prices don’t seem to discount the facts that excess reserves are gone and the Fed’s operations still have not added any, and that G-SIB scores are binding and risk large U.S. banks clamping down on market making.”

Worse, another prevailing consensus idea is that the Fed will not cut one more time in December “to deliver slope in the money market curve so that reserves from bill purchases flow up to banks… or that the Fed will actively encourage the use of FX swap lines around year-end to get around G-SIB bottlenecks; or that the Fed will start buying coupons from dealers to inject excess reserves in a balance sheet neutral and G-SIB score-reducing manner.”

What Pozsar is stating in not so many words, is that as has happened on every other previous occasion, the Fed will have no choice but to intervene to reverse the coming crash, only this time with its ammo severely limited, there is just one thing that Fed can do, or as Pozsar says, “something will have to give and the turn has to get very bad before something gives.”

But will things get “very bad”? Well, if Pozsar is right and the Fed loses control over the overnight rate complex, yes, they will, and as we tweeted some practical advice yesterday…

… The question then is what will the Fed do. Here is Pozsar’s answer: “If we are right and the Fed loses control over the o/n rates complex going into year-end – not just around the spot turn but the weeks leading up to it – what else can the Fed do?”

encourage foreign central banks to use of the FX swap lines;

start QE4 by switching from buying bills to buying coupons;

Of the two options, Pozsar believes #2, the Fed launching QE4 (in the next fed days), would be the proper decision:

QE4 would help through the backdoor: by reversing the mistake of balance sheet taper. QE4 would mean buying back from dealers and banks the Treasuries they were forced to buy during balance sheet taper and giving back the reserves they gave up in the process.

QE4 would re-liquefy HQLA portfolios by trading Treasuries for excess reserves: the excess reserves that were always needed to get through to year-ends seamlessly, and which the system’s liquidity profile and U.S. banks G-SIB scores need desperately.

QE4 would re-fill the “Bakken Shale” in an instant: as primary dealers stuck with Treasuries would pay off their repos with J.P Morgan, and that would bring us back to the natural state of the token system, that is, a state, where the distribution of excess reserves is uneven once again, and where J.P. Morgan is the system’s lender of next-to-last resort once again.

That said, as Pozsar concedes in his conclusion “QE4 – as much as it makes sense – won’t happen unless the Fed’s hands are forced.” By which he means there has to be a market crash for the Fed to do the one thing that can alleviate the banks’ terminal reserve problem.

The Credit Suisse strategist admits as much:

“not responding to potential stresses in the FX swap market with the swap lines, may be what forces the Fed’s hands. If it will take the swap lines to help RV hedge funds to roll their positions without the risk of fire sales, not encouraging their use preemptively can lead to fire sales where QE4 goes live as a clean-up “operation” with the Fed buying what the RV funds are forced to sell – and what they could have bought from dealers under normal circumstances as dealers have been politely asking the Fed since September, just like they were asking for a repo facility before that – and we know how that ended…”

In conclusion all we can say here is that 11 years ago, on September 5, 2008, ten days before Lehman filed, there were massive marketwide repo problems (recall the repo market froze in Sept 2008 and only a multi-trillion bailout by the world’s central banks prevented civilization collapse) and almost nobody understood them… with one exception: Citi’s Matt King did and he laid out all the problems in his iconic Sept 5, 2008, piece “Are the Brokers Broken” in which he predicted the collapse of Lehman. Ten days later he was right. Will Zoltan Pozsar be this generation’s Matt King?

“We Totally Failed As A Business”: Unicorn Scooter Impales Investors After Company Goes Hooves-Up

It was a stupid idea at a terrible time; startup company Unicorn thought they could convince people to spend $699 on an electric scooter – as opposed to simply paying a few bucks each time they use one of the ubiquitous e-scooters littering cities across the country.

After blowing all the cash they raised from investors and pre-orders on Facebook and Google ads, CEO Nick Evans said in an email that the company had “totally failed as a business” and would “spread the cost of this failure to you, the early customers that believed in us.”

In total, the company received just 350 pre-orders for the glossy white e-scooters, according to The Verge. And nobody is getting a refund, as “we are completely out of funding.”

Unicorn emerged six months ago as part of a new crop of scooter startups hoping to capitalize on the popularity of dockless rental services like Bird and Lime, while also pitching itself as an affordable alternative to shared scooters. In addition to having a striking profile — the all-white look was really something — the scooter was loaded with a lot of high-tech bells and whistles, like GPS tracking and smartphone-enabled locking. Naturally it included integration with Tile, Evans’ other company, which uses Bluetooth to track lost items, like a wallet, keys, or phone. –The Verge

Evans’ email reads;

We could have continued moving forward and taking more orders and that would continue to fund the business, and if we did that might have been able to deliver the product, but we also may have not been able to sell enough Unicorns, so by doing that we would be risking more people’s orders. So we made the very, very difficult decision to stop.

A large portion of the revenue went toward paying for Facebook ads to bring traffic to the site. A portion also went to our manufacturer in the form of a down payment to build the scooters, but unfortunately that down payment cannot be redeemed for a portion of the scooters that we were planning to order.

Unfortunately, the cost of the ads were just too expensive to build a sustainable business. And as the weather continued to get colder throughout the US and more scooters from other companies came on to the market, it became harder and harder to sell Unicorns, leading to a higher cost for ads and fewer customers.

“We are so, so very sorry,” Evans concludes.

Not good enough, say some investors.

“I am upset he basically robbed everyone of his customers and is closing without delivering any scooters,” wrote hopeful customer Rebecca Buchholtz to The Verge. “This was my daughters Christmas gift and now I cannot get her any gift.”

“I find it shocking that someone like Nick Evans who has name recognition and clout in the tech community due to Tile, would operate in such a fraudulent way,” wrote customer Matt Furhman, who said he’s lost $998 after placing pre-orders for two scooters. He calls Evans a “thief.”

Customers are advised to contact their credit card companies and dispute the charges from Unicorn.

In an email to The Verge, Evans said the company had received only around 350 orders. “I feel horribly guilty that we left people with no scooters and no refunds,” he said. “We are working on something, but, yes, this seems unlikely.” -The Verge

Unicorn is far from alone when it comes to e-scooter fails. Santa Cruz-based Inboard Technology is currently liquidating its assets and IP after trying their hand at electric scooters – laying off all 24 of their employees.

The United States has a total area of 3,796,742 square miles. That makes it the third or fourth-largest country in the world by land area, depending if you count overseas territories. So what’s the point? Despite its size, the U.S. is facing a dilemma of sorts.

According to a new report from The Brookings Institution, regional divergence in the U.S. innovation sector “has reached extreme levels.” The innovation sector, composed of 13 of the nation’s highest-tech, highest R&D industries, is vital to the U.S. economy. The innovation sector accounts for 3% of U.S. jobs, but generates 6% of the country’s GDP, a quarter of its exports and two-thirds of business R&D expenditures. The industries, such as software, pharmaceuticals and semiconductors, consist of workers with degrees such as science, technology, engineering and mathematics.

The report found that job gains in the innovation sector are becoming highly concentrated to a handful of “superstar” metropolitan areas. Boston, San Francisco, San Jose, Seattle and San Diego captured more than 90% of all new jobs in the innovation sector from 2005 to 2017. These cities’ share of the nation’s innovation sector employment increased from 17.6% to 22.8% during this period.

One-third of the nation’s innovation sector jobs are now in just 16 counties, with more than half concentrated in 41 counties. The hardest hit cities, in terms of losing innovation sector jobs over this period, include Chicago, Philadelphia, Dallas and Los Angeles.

One of the other negative externalities the report focuses on is what it calls the “sorting of workers.” This happens as college-educated workers are moving to a handful of cities, leaving those metro areas they’ve moved from with weaker talent pools. This can cause areas of underdevelopment, which in turn, can lead to broader social issues.

So what does The Brookings Institution suggest as a solution to this issue? They believe the U.S. government should counter this divergence by selecting eight to ten new “heartland” metro areas that can be transformed into “regional growth centers.” The report provides a list of 35 metro areas that are ideal candidates for transformation. Madison, Wisconsin, the greater Minneapolis, Minnesota region and the greater Albany, New York region are listed as the most eligible locations. At an estimated cost of $100 billion over ten years, The Brookings Institution points out that it is “substantially less than the 10-year cost of U.S. fossil fuel subsidies.”

As Market Crumbs wrote yesterday, technology companies are expanding, but are increasingly heading to New York City. Doing so doesn’t solve any of the issues The Brookings Institution identifies in its report. If the government takes their advice and tries to develop these regional growth centers, there is sure to be plenty of debate as Amazon’s search for its HQ2 last year showed what happens when governments try to attract corporations.

Gundlach: Trouble Brewing In Debt Markets As The ‘Real Turmoil’ Is Only Beginning

Last week, DoubleLine’s Jeff Gundlach sat down with Yahoo Finance to discuss how US stocks would get absolutely crushed in the next recession. In a continuation piece via Yahoo, Gundlach suggested that trouble is brewing in debt markets as interest rates hover around zero.

Gundlach said the 2020s could exhibit socio-economic chaos as the debt bomb the US is sitting on ignites into the next recession.

“It’s pretty interesting because the 20s in the 20th century, the 20s were super boom times. And weirdly, I think the 20s this time will be very much different than that, with real turmoil,” Gundlach said.

Gundlach said the decades of can-kicking would finally stop in the 2020s, and the US will have to face realities relating to its debt situation.

“[We’re] going to have to face Social Security, health care, all of these things, deficit-based spending — all of that is going to have to be resolved during the 2020s because the compounding curve is just so bad,” he said.

The billionaire investor said interest costs on the debt would soar from 1.25% to at least 3% by 2027. “That’s a big, big increase. And that’s coming,” he warned.

“And when you do that, it kind of says, ‘Hey, GDP is going to be knocked by 2%-2.5% because we have to pay interest,'” he added, which suggests that the 2020s could be a lost era situated in a low growth period with social-economic instabilities.

He said the Federal Reserve understands what’s coming down the pipe, and it’s why everyone is starting to talk about MMT – as it could be the policy prescription pitched by lawmakers and the Fed to lift the US out of the next financial downturn.

Gundlach said, “they [Fed] knows that this problem is going to really hit the headlines when the next economic downturn comes, and I think it’s foolish to believe that there will be no economic downturn for the next ten years considering where we are right now.”

In an earlier segment of the interview, which we covered last week, Gundlach said 2019 was the year when investors could pick “just about anything…Just throw a dart, and you’re up 15-20%, not just the United States, but global stocks as well.” He warns that it could all change in 2020, as a recession is fast approaching.

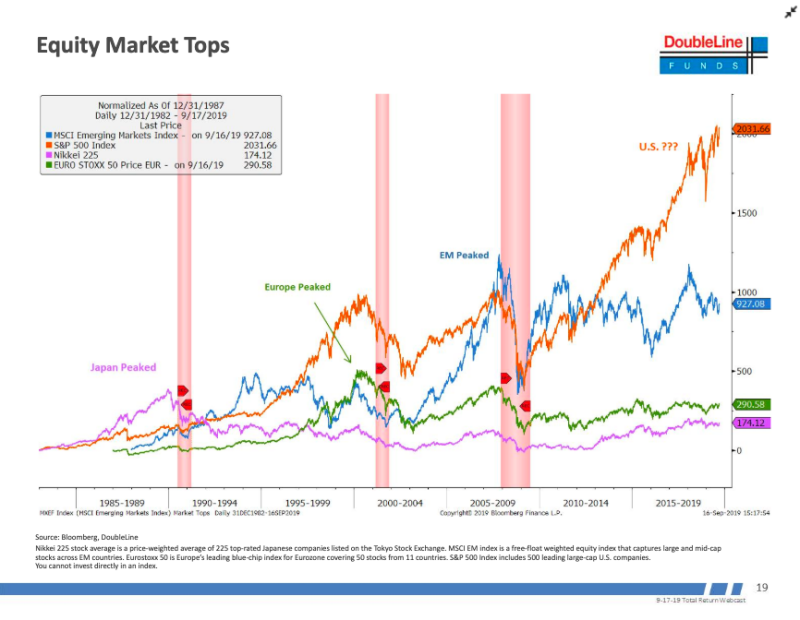

He shared his “chart of the year,” which divides global equities into four regions (the US, Japan, Europe, and Emerging Markets). What it shows is an alarming market top forming in US stocks, similar to what happened with the Nikkei 225 in the early 1990s or the Euro Stoxx 50 Index in the late 1990s or MSCI Emerging Markets in 2007/2008.

“My belief is that pattern will repeat itself,” said Gundlach, who has spent much of 2019 warning of a downturn ahead of the 2020 elections.

“In other words, when the next recession comes, the United States will get crushed, and it will not make it back to the highs that we’ve seen, that we’re floating around right now, probably for the rest of my career, is what I think is going to happen,” he added — suggesting that a recovery won’t be seen for years.

Last month, Gundlach warned about the levels of government debt, and the US equity markets are not sustainable. He told investors that they should brace for significant disruptions.

“The corporate bond market in the United States is rated higher than it deserves to be. Kind of like securitized mortgages was rated way too high before the global financial crisis. Corporate credit is the thing that should be watched for big trouble in the next recession.”

Rabobank: “The Key Reason We Are In This Mess Is Due To Volcker”

Submitted by Michael Every of Rabobank

Tall Tales

Markets were relatively quiet Monday, with key bond yields drifting lower to reverse Friday’s payrolls-induced spike, and the USD likewise reversing some its gain. Even equities ended slightly lower.

Perhaps the most eye-catching news was the sad death of former Fed Chair Paul Volcker. Besides his post-2008 regulatory ‘Volcker Rule’ being infamous to those working in markets, “Tall Paul” is being eulogised as the man “who broke the back of US inflation in the 1980s”. Even before his death others had stated that if there were a Nobel Prize for government serviced that his name would be on that list.

For those weaned on ultra-low rates and central-bank liquidity on demand, it must seem odd that once upon a time there was a Fed Chair prepared to raise rates to eye-watering levels regardless of the cost, who worked for tighter regulation after leaving office, and who publicly wanted to see big banks broken up. By contrast, yesterday saw the current Fed pump in another USD25bn in a 28-day repo operation yesterday – and USD43bn was bid for that USD25bn on offer (so many people so short of cash: is it all really a year-end squeeze?); and let’s not forget the weekend had that USD150,000 banana taped to a wall (up USD30,000 in a day because of the controversy over the first USD120,000 banana being eaten). For all the chatter that Jay Powell ‘was going to be the next Volcker’, the truth is that lower for longer will be lower forever if markets continue to require permanent liquidity support, which they still do a decade after the actual crisis ended.

However to think that we need a Volcker now is a “Tall tale”. Why? Because one also needs to underline that, ironically, the key reason we are in this mess is due to Volcker. He didn’t just break the back of US inflation: he also deliberately broke the back of US labour power. Recall that at the time of soaring US inflation the economy was dealing with the aftermath of an oil shock, the collapse of the Bretton Woods system, the messy end of the expensive Vietnam War, and the start of the US political mania for tax cuts for the wealthy as a cure-all. Most countries would have seen high inflation against that backdrop – and lots of potential policy-combinations might have worked as a palliative. (Tax hikes for the rich, for example, or an early refusal to allow the USD to assume its current global role as absorber of excess global capital and production.)

Volcker decided that the working class needed to pay the price of victory against inflation. He explicitly aimed at breaking the power of organised labour, and just after being appointed as FOMC Chair declared “The standard of living of the average American has to decline”. When looking at the trend of median rea- wage stagnation in the US–something now broadly acknowledged as the root cause of most of our socio-economic problems, and of our distorted markets–this started with the first oil shock, and became entrenched under Volcker. Subsequent Fed Chairs, and indeed most central banks, may no longer be tough on rates and may doll out liquidity like candy – but not to workers, only to banks (and soon, perhaps, to shadow banks). Whatever the Fed does or doesn’t say at this week’s meeting, don’t expect that to change.

Which brings us neatly to the week’s other main event. In the UK, the Labour Party is running on as ‘anti-Volcker’ an economic manifesto as possible, and has been flailing in the polls. However, a viral clip of PM Boris Johnson, a renowned teller of tall tales, refusing to look at an image of a four-year old boy being treated for pneumonia on a hospital floor due to lack of beds is the exact opposite of what a Tory government which presided over a decade of austerity would want to see as the campaign lumbers to the finishing line; it wants the focus on a points-based immigration system post-Brexit (which is moderately ‘anti-Volcker’ in theory, although where used in Australia is still about as Volcker as it gets). Indeed, the Telegraph today claims an internal Tory memo warns Jeremy Corbyn is “much closer” to becoming PM than voters think due to tactical voting – which that viral clip might just encourage. Let’s see if GBP wants to look at the image of PM Corbyn today.

But it’s not just a UK issue. The same Telegraph is also reporting “Germany’s Hard-Left ‘Corbyn Problem’ Is Only Just Beginning”, as the coalition SPD’s base has been captured by hard-Left activists who wish to repudiate key policies such as the Hartz IV labour reforms, and to embrace a 2% wealth tax, a rent freeze, a 30% rise in the minimum wage, a much higher carbon tax, and to shift to massive fiscal expansion on social housing and infrastructure. It goes without saying that these are all also still potentially on the table in the US 2020 election.

Sending a message that suddenly the world is looking fine and dandy–or flagging that that an anti-Volcker tide is rising?–10-year JGBs just popped above zero for the first time since March, taking trillions of USD of negative-yielding debt off the global balance sheet. And in China we saw CPI and PPI, where the former rose to 4.5% y/y, higher than expected, but PPI actually came in stronger than expected at -1.4% y/y, which is useful in pushing real rates lower on both a CPI and PPI basis. One could see the latter as another marginal sign that the Chinese economy is picking up – for now.

Meanwhile, US Agriculture Secretary Perdue that he does not believe the next tranche of USD160bn tariffs will be put in place against China this weekend, even as Jim Cramer of Mad Money tweets he thinks Trump is better off playing the long game and not signing on to a weak phase one deal.

In short, markets can eulogise Volcker while secretly praying we never see his like again. Most central banks also don’t want to be Volckers anymore. They agree there is a risk of global ‘Japanification’ in 2020 despite the recent uptick, meaning even looser policy ahead, and some are girding their loins by reinventing themselves as ‘green champions’ to justify it. But just as they cannot imagine a world where they would have to raise rates like Volcker did, they cannot imagine that they might have to fight a different war if the political climate shifts in a different ‘anti-Volcker’ direction that re-empowers labour vs. capital.

White House, Democrats Reach “Infinitely Better” Deal On NAFTA 2.0

Following months of politicking, and a friendly nudge from Mexicos’ AMLO earlier in the week, House Democrats appear to have satisfied labor’s demands and have agree to ratify the USMCA trade deal that President trump reached last year with Canada and Mexico to replace NAFTA.

The AFL-CIO announced Tuesday it would back the trade agreement, something that would give more cover for Democrats to support it.

“Working people are responsible for a deal that is a vast improvement over both the original NAFTA and the flawed proposal brought forward in 2017,” AFL-CIO President Richard Trumka said.

“For the first time, there truly will be enforceable labor standards — including a process that allows for the inspections of factories and facilities that are not living up to their obligations.”

Speaker Pelosi proudly proclaimed her victory this morning – notably mentioning Trumka numerous times but not mentioning Trump once – that the deal she agreed was “infinitely better” than the original agreement made by Mr Trump, particularly on enforcement of labor standards in Mexico.

The deal is expected to pass with strong bipartisan support in both chambers.

As The FT notes, the move towards a green light on Capitol Hill will be touted as a big win for the White House heading into the 2020 presidential campaign. Trump tweeted this morning:

“America’s great USMCA Trade Bill is looking good. It will be the best and most important trade deal ever made by the USA. Good for everybody — Farmers, Manufacturers, Energy, Unions — tremendous support. Importantly, we will finally end our Country’s worst Trade Deal, Nafta!“

Notably, the peso and loonie barely budge on the news this morning.

It is finally about to happen! After weeks of speculation, guesses, and conspiracy theories, Saudi Aramco’s initial public offering (IPO) is scheduled to begin trading soon. By selling just 1.5% of the company, the Saudi Arabia-owned crude oil juggernaut will receive a valuation of $1.7 trillion, which will make it the world’s largest IPO. The stock is already over-subscribed at home, but foreign investors do not have an appetite for a little bit of the crude bubbly. One reason could be IPO fatigue, especially with the kind of year the market endured.

Class Of 2019 Graduates

After a couple of down years for the IPO industry, it was thought that some of the hottest companies in the United States today would toss a lifejacket for investors underwater in their investments. Uber, Lyft, Pinterest, Slack, and WeWork (the office-sharing company withdrew its IPO) were supposed to save us. Instead, Uber is down 12%, Lyft is up just 1%, Pinterest is down 32%, and Slack is 17% in the red from their IPOs. Even the plant-based Beyond Meat, which had surged 50% from its IPO price, has been carved in half.

Hey, it is not all doom and gloom, though. Peloton, after bearing the brunt of an oversensitive social media mob taking umbrage at a television commercial for its exercise bike, has been one of the surprising bright spots. Even with the 7% loss in the first week of December, shares of the money-losing venture are still up 38% since going public.

That said, the entire situation could worsen over the coming months as the lock-up period – stocks that are eligible to be sold on the open market – of these IPOs are coming to an end. This could add pressure to companies that have already been struggling in their post-IPO sessions. It might also give some future IPOs some consternation about going public.

But why is this happening? Well, it turns out that stocks can no longer rely just on good faith. They need to begin generating a profit.

Goldman Sachs recently published a report that found businesses that went public this year are projected to produce the lowest profits of any year since the dot com bubble. In fact, according to the Wall Street titan, just 24% of IPOs in 2019 will post positive net incomes, which is the smallest percentage in 20 years. With interest rates at historic lows and the Federal Reserve pumping the market with cheap money, these companies can survive the bleeding a little longer.

According to a Bloomberg analysis of listings worth $100 million or more, unprofitable IPOs have raised the most cash of any year since the dot com era. Despite the poor returns of late, investors are scooping up IPOs in the hopes of getting served a plant-based-style burger. Can they be perpetual bulls? If the Fed keeps the spigot running, Wall Street will be there to chug it down.

Bill Gurley, a partner at venture firm Benchmark, recently told CNBC that the IPO process was a “bad joke” for Silicon Valley. He may be right, considering the lackluster performances of these stocks.

Will The Class Of 2020 Get Left Behind?

Either 2020 will be the start of something new or it will replicate 2018 and 2019. The experts are prognosticating that next year will see “global IPO activity pick up.”Forbes magazine is anticipating as many as 40 to 50 IPOs. Right now, the talk on the Street is that Airbnb, Hemptown, Postmates, Robinhood, and Casper will be the biggest businesses to go public.

Like their predecessors, many of these companies have already recorded disappointing quarterly results; Airbnb reported first-quarter losses and Postmates published steep third-quarter declines. HempTown, a company that specializes in hemp production, might be one of the few breakout stars of next year’s class due to a legislative push to ease regulations on hemp in the U.S., thanks to Sen. Mitch McConnell (R-KY).

With Plenty Of Money And You

It has been quite the year for American financial markets. Across the board, nearly every asset class performed well, from the U.S. dollar to precious metals to energy (except natural gas). If you put money in the stock market – whether it was an exchange-traded fund (ETF) or Treasuries – you likely enjoyed a return on your investment. Considering how the Dow Jones, Nasdaq, and S&P 500 each recorded all-time highs in 2019, it would seem counterintuitive that IPOs would drown in an ocean of red ink. But here we are. Unfortunately for the IPO class of 2019, it was the worst of times – can 2020 be an improvement?