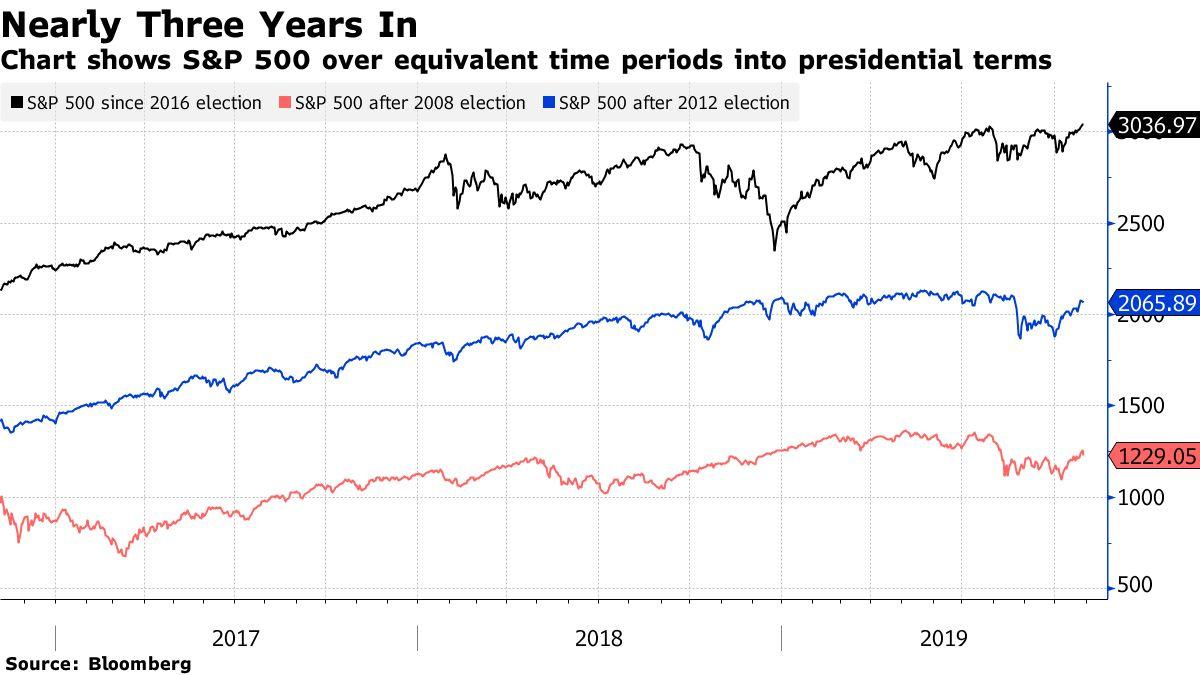

Predictions Of Stock Market Carnage Based On Who’s Elected Are Almost Always Wrong

With recent forecasts of market mayhem if Elizabeth Warren is elected, Bloomberg would like to remind everybody that past predictions of a presidential candidate’s impact on equities are usually wrong.

The S&P 500 will plunge 25% if the Democrat becomes president, says Paul Tudor Jones, the hedge fund manager. Discovery Capital Management founder Rob Citrone says she’s “the single biggest risk for the market” and calculates the downside at up to 20%. Billionaire Leon Cooperman told CNBC earlier this month that the market would drop 25% if Warren or Bernie Sanders win.

That’s a lot of certainty to attach to predictions Wall Street has shown no ability to get right in the past. The confidence sounds particularly rich considering what investors said about the man Warren aims to dethrone, Donald Trump. –Bloomberg

“Strategists predicting the impact of a presidential election are worse than the pollsters,” said equity strategist Matt Maley of Miller Tabak & Co. “It’s one of the best contrary indicators out there.“

While Bloomberg admits that Warren’s plans to rein in Wall Street and corporate America may ‘kill the economy,’ or that the bull market may ‘die of old age,’ evidence suggests that a president’s politics do little to affect stocks – writing: “Variations in equity performance when a Democrat is in the White House are almost negligible when compared with Republicans, according to research from Vanguard that was published before the 2016 election.”

Moreover, strategists were dead wrong about Trump.

Strategists at RBC Capital Markets LLC said prior to Election Day that a Trump victory would send the S&P 500 down 10 to 12%. Barclays had predicted a drop of as much as 13%. The team at JPMorgan advised investors to sell the rebound that materialized just a few hours after Trump won.

It wasn’t just stock handicappers. Two economics professors, Justin Wolfers and Eric Zitzewitz, wrote a paper on the topic for Brookings in October 2016. They analyzed the futures market during the first presidential debate and extrapolated the reaction to conclude a Trump win would send stocks down 10% to 15%. A Massachusetts Institute of Technology economist posited that a Trump presidency would cause a stock market crash and could plunge the global economy into recession. –Bloomberg

According to the report, the terrible market calls related to a Trump win were in part a reflection of polling data. “Since Trump was viewed as a long shot, many predicted investors would be shocked into selling if he won.”

Citigroup strategists, for example, said the S&P 500 could lose 3-5% immediately on a Trump win, in addition to posing long term risks to stocks. While S&P 500 futures plunged 5% in the hours after Trump’s victory was secured, they rebounded almost immediately – while the index has gone on to gain over 40% since Trump’s election.

Strategists were similarly wrong about President Obama’s reelection when he ran against Mitt Romney in 2012. In September of that year, almost 50% of respondents in a Bloomberg survey said that if Obama won again it would be negative for US financial markets despite the S&P gaining 42% between Obama’s first election and his second.

Among prognosticators who muffed the call was Donald Trump, who said in a November 2012 tweet that both the stock market and the U.S. dollar would plunge following Obama’s second victory. The S&P 500 rose almost 50% in that term, bringing his eight-year return to 112%, while Bloomberg’s dollar index gained 21% in the four years that ended in November 2016. –Bloomberg

“The most nay-saying people to Barack Obama will admit that there was not a transformation of our economy in any way that they would’ve feared the day he got elected. Same thing with the Democrats with Trump. There hasn’t been this transformation that was feared,” said Mark Hackett, chief of investment research at Nationwide Funds Group.

“Our economy is bigger than one person or one election cycle.”

US vs China: Unstoppable Force Vs Immovable Objection

Submitted by Michael Every of Rabobank,

Markets were rocked yesterday by further bad news on the trade front. Not only is the APEC venue not available for Trump and Xi to meet, but according to a news report senior Chinese officials have little faith in the US sticking to any deal, have literally no appetite for the large up-front agri purchases that the US is insisting on, and are refusing to contemplate any immediate start on a ‘phase 2’ deal without the States removing tariffs – which isn’t going to happen.

All in all one could almost make the argument that this is case of unstoppable force (the US) vs. unmoveable objection (China), and hence a real trade deal can’t be done. Of course, we have made exactly that projection since before the trade war even started. Indeed, we aren’t compelled to change that view despite both Larry Kudlow and Chinese officials scrambling to let the world press (meaning stock markets) know that the two sides are close to agreement, really.

Do they actually agree? Yes – on their irreconcilable differences. Now just isn’t the time to advertise that agreement to disagree too loudly: but supply chains will keep moving anyway. Consider that US Secretary of State Pompeo and Vice President Pence have both made clear from the US side that China must reform or decoupling, even if undesirable, looms: Pompeo openly talked about “confronting the Chinese Communist Party”. For its part, the Chinese Communist Party’s fourth plenum this week announced “national security” and “rising risks” were the immediate priority, not reforms of the economy.

Meanwhile, politics was again in force as the US House of Representatives officially voted to open impeachment procedures against Trump. From now on depositions will have to take place in public, and there will be a wider range of witnesses called, and far greater Republican involvement. As a result, expect the headlines to get even more colourful than they have been so far; expect nobody to emerge looking very good; and also expect formal impeachment in the House on strictly party lines, which opens up a trial in the Senate. However, don’t expect much focus on the substantive detail of the facts because this all about bare-knuckle politics, and the switchblade issue of quis custodiet iposos custodes; don’t expect the Republican-majority Senate will also impeach Trump to remove him from office, because while it’s possible it’s still the far less likely proposition; and don’t expect Trump won’t run for re-election in November 2020 anyway even if he is impeached or removed from office. Unstoppable forces are unstoppable, just as immovable objections are immovable.

Trump is also wasting no time getting involved in another foreign country, announcing that a BoJo – Farage electoral team-up in the UK would be “an unstoppable force”. Of course, it would make a huge difference to the Tories’ uncertain electoral prospects given the likely loss of some seats to the Remain Lib Dems and others to Scottish nationalists, and hence to what shape Brexit would then take. However, in what is going to be the most uncertain election in UK history there will be many who have an immovable objection to Trump saying what he did – and also that Labour leader Corbyn would be ”so bad for the UK.” It simply isn’t acceptable for foreign leaders to make comments about desired outcomes in other countries’ elections – except when it is the US, when the whole world joins in (which is allegedly why we are where we are on impeachment).

Note that special judgmental role is instead reserved for financial markets: where and while they still can, they get to show who they think would be “so bad” or “so good” for a country.

President Trump Has Plans To Go To UFC 244 On Saturday Night

President Trump will be steering clear of one vicious fight in Washington D.C. to attend another in New York City this weekend.

The President is expected to attend UFC 244 this weekend, according to Bloomberg. The event is being headlined by welterweights Jorge Masvidal and Nate Diaz, who is coming off of a massive unanimous decision win against Anthony Pettis back in mid-August.

And it’s not Trump’s first foray into mixed martial arts, either.

He hosted two major MMA events in 2001 at Trump Taj Mahal in Atlantic City and, in 2016, UFC President Dana White endorsed the Trump campaign and spoke in support of him at the Republican National Convention.

About 10 years ago, Trump even backed Affliction Entertainment, which attempted (and failed) to become a potential UFC competitor.

Trump’s weekend plans will likely be a much needed break from the continued impeachment circus that the Democrats have drummed up in Washington D.C. The President is expected to stay at Trump Tower over the weekend, which could cause significant congestion in Manhattan over the weekend.

Trump has publicly commented that he dislikes coming back to Manhattan because of the trouble they cause the city. “I hate to see the New Yorkers with streets closed,” he said in 2017.

For a long time, people have been trying to tell me that the U.S. economy is headed for a new golden era. They insist that the U.S. will be more powerful and more respected than ever before, and that we will see unprecedented prosperity in this nation.

But despite extremely wild spending by the U.S. government and exceedingly irresponsible intervention by the Federal Reserve, the U.S. economy has not even had a “good” year in ages. As I have pointed out numerous times, we have not had a year when U.S. GDP grew by at least 3 percent since the middle of the Bush administration, and that makes this the longest stretch of low growth in all of U.S. history by a very wide margin. Many believe that brighter days may still be ahead, but all of the economic numbers that we have been getting in recent months make it abundantly clear that a new economic slowdown has begun. I shared 14 of those numbers earlier this week, and I will share some brand new ones with you today.

Source: Bloomberg

Let’s start by taking a look at how U.S. consumers are faring. U.S. consumer confidence has now fallen for 3 months in a row, and this week we learned that the Bloomberg Consumer Comfort Index has just fallen at the fastest pace in more than 8 years…

U.S. consumer comfort suffered its biggest weekly decline in more than eight years on a pullback in Americans’ assessments of the economy, personal finances and the buying climate, possibly signaling more moderate household spending approaching the holiday-shopping season.

The Bloomberg Consumer Comfort Index fell 2.4 points, the most since March 2011, to 61 in the week ended Oct. 27.

How in the world can anyone possibly claim that we have a “booming economy” after reading that?

We also just got another depressingly bad manufacturing number. Experts were expecting a reading of 48.3 for the Chicago Purchasing Management Index, but instead it came in at just 43.2…

The Chicago Purchasing Management Index sank to 43.2 in October from 47.1 in the prior month. This is the lowest level since December 2015. Economists has expected a reading of 48.3, according to Econoday.

Any reading below 50 indicates deteriorating conditions.

We were promised a “manufacturing renaissance”, but instead manufacturing is now the smallest share of the U.S. economy that it has been in 72 years.

But at least we have plenty of government jobs, eh?

In the private sector, things are getting really tough, and we are starting to see lots of big companies lay off workers.

For example, Molson Coors just announced that they will be laying off up to 500 workers as they desperately search for a way to survive in this difficult economic environment…

To further drive efficiency and enable growth, Molson Coors is consolidating and reorganizing office locations. The Denver office will be closed and Chicago will be designated as the North American operational headquarters. Functional support roles currently housed in several offices around the country will now be based in Milwaukee, Wisconsin.

As a result, we expect to reduce employment levels by approximately 400 to 500 employees as part of this restructuring, primarily in our existing United States, Canada and International reporting segments, as well as Corporate.

You know that things are getting tough when even beer companies start laying people off.

Of course the “retail apocalypse” continues to escalate, and we just learned that Forever 21 will be closing most of their stores and laying off most of their employees…

More than 100 Forever 21 stores are slated to close as part of the fashion retailer’s Chapter 11 bankruptcy protection case, according to court documents filed this week.

The family-owned company, which has about 32,800 employees, said it would close “most” of its stores in Asia and Europe and up to 178 stores in the U.S. when it filed for protection Sept. 29.

A similar scenario is playing out for Dressbarn. According to USA Today, all of their 544 stores “will close no later than Dec. 26″…

Liquidation sales at the remaining Dressbarn stores will start Friday, the struggling retailer announced Wednesday.

While the 544 stores will close no later than Dec. 26, the women’s clothing website is expected to relaunch in 2020 with a new owner, the company said in a news release.

It has been hoped that a limited trade agreement with China might bolster the economy at least temporarily, but now we are learning that Chinese officials expect “phase one” of the deal to “soon fall apart”. According to CNN, the Chinese are pessimistic that our two countries will ever be able to “reach a full trade deal”…

Chinese officials have expressed doubts about whether the world’s two largest economies can reach a full trade deal, Bloomberg reported. That is casting a long shadow over the “phase one” agreement that the countries reached earlier in October.

This is consistent with my warnings from previous articles. The Chinese wanted the Trump administration to stop the implementation of any more tariffs, and they were able to achieve that with “phase one”. But in order to move forward with “phase two”, the Chinese are going to insist on the removal of all tariffs…

According to BBG’s sources, this is the bare minimum that Beijing would accept to move ahead with Phase 1: a commitment from the Americans to removing tariffs in Phase 2, and agreeing to cancel the next round of tariffs, set to take effect in December.

This is something that the Trump administration will never agree to, and so that puts us back where we originally started.

The Chinese will continue to “negotiate”, but only for stalling purposes.

There is only about a year left until the 2020 elections, and the Chinese are hoping to run out the clock on the Trump administration with as little disruption to their own economy as possible.

Unfortunately for the Chinese, Trump could possibly win another term, and if either Elizabeth Warren or Bernie Sanders win they could potentially be even tougher on trade with China.

In any event, we should not expect a comprehensive trade deal with China any time soon, and that is really bad news for the economic optimists.

Of course the truth is that everything that I have just shared is bad news for all of us. The U.S. economy is seriously deteriorating, and things are only going to get worse in the months ahead.

Trump Is Officially A Floridian After Address Change

President Donald Trump, born and raised in New York City, announced Thursday on Twitter that he has changed his primary residence to Florida, a move that some think could benefit his re-election campaign.

“I cherish New York, and the people of New York, and always will, but unfortunately, despite the fact that I pay millions of dollars in city, state and local taxes each year, I have been treated very badly by the political leaders of both the city and state. Few have been treated worse,” the president tweeted late Thursday night.

“I hated having to make this decision, but in the end it will be best for all concerned. As President, I will always be there to help New York and the great people of New York. It will always have a special place in my heart!”

….New York, and always will, but unfortunately, despite the fact that I pay millions of dollars in city, state and local taxes each year, I have been treated very badly by the political leaders of both the city and state. Few have been treated worse. I hated having to make….

The president made it clear that his new home is in Palm Beach County, Florida, and he’ll be a “bona fide resident of the State of Florida residing at” his Mar-a-Lago Club.

The New York Times was the first to publish the president’s change of address, citing court documents, as his address changed from Trump Tower in New York City to Mar-a-Lago Club in Palm Beach.

“If I maintain another place or places of abode in some other state or states, I hereby declare that my above-described residence and abode in the State of Florida constitutes my predominant and principal home, and I intend to continue it permanently as such,” President Trump said in court documents.

The filing also specifies the president’s “other places of abode” as the White House and his other private golf clubs across the country.

Bloomberg considers the president’s motivation behind the change to be related to his tax overhaul plan:

“If motivated by tax considerations, it would bolster a point that his political foes have been making for months: His tax overhaul is hurting Democratic-led, high-tax states by prompting the wealthiest residents to move elsewhere.”

As soon as New York Gov. Andrew Cuomo found out about the president’s address change, he tweeted: “Good riddance. It’s not like Mr. Trump paid taxes here anyway… He’s all yours, Florida.”

Shortly after, Sen. Elizabeth Warren accused President Trump of changing his address so he can shield his tax returns from New York officials.

“Donald Trump doesn’t want the state of New York to see his taxes—I wonder why,” Warren tweeted. “Let’s call this out for what it is: Corruption, plain and simple. Under my anti-corruption plan, all presidential candidates would be required to release their tax returns.”

Donald Trump doesn’t want the state of New York to see his taxes—I wonder why. Let’s call this out for what it is: Corruption, plain and simple. Under my anti-corruption plan, all presidential candidates would be required to release their tax returns. https://t.co/0QnsObxV1r

While there could be several causes for the address change of primary residence, one significant reason could be due to Florida is a mecca for the ultra-wealthy as there is no income tax or an inheritance tax in the state.

Potential for the data deterioration theme to pause in the next quarter

Phase 1 US-China deal could pivot Manufacturers from inventory destocking to restocking

Key manufacturers talking about this potential on earnings calls

This underappreciated catalyst could cause a temp bounce in the economic data, lift stocks and curve steepeners even higher – classic end of the cycle melt up

WARNING: This note contains content more positive than the past 10 months and may not be suitable for readers who are expecting a perma bear.

I jest obviously but the theme all year has revolved around the idea of data deterioration. The question from those tired of that notion is always “what would change your view” and the answer is consistently:

1) CB’s adding liquidity

2) China-US trade war progress

3) EU fiscal stimulus

For the first time all year, all three potential catalysts emerging at the same time which risks a Q4 melt up in risk assets and (I hope you are sitting down) an improvement in some of the economic data – mainly the manufacturing sector.

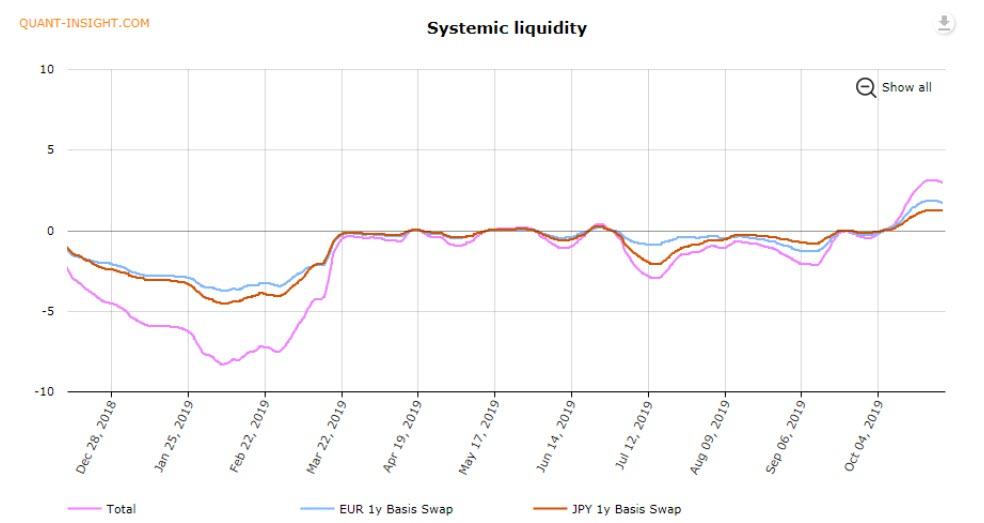

Central Banks pumping liquidity once again

This has been THE driver of the cyclical “up crash” first kicked off around October 8th when Fed Chair Powell noted that the Fed will soon announce steps to add to reserves over time through the purchases of T-bills. Around the same time, as we discussed previously, many Fed officials began setting up the Oct cut which many thought was in question (Rosengren, Evans).

That powerful force of a coming Fed liquidity injection + another Fed cut to sustain the expansion caused a key reversal in the macro landscape where:

USD topped out and depreciated lower

Cyclical equities/commodities bottomed and started to break out higher

Interest rates bottomed and started pricing out future Fed cuts

Yield Curves like 2s10s, that had been dormant, began to steepen

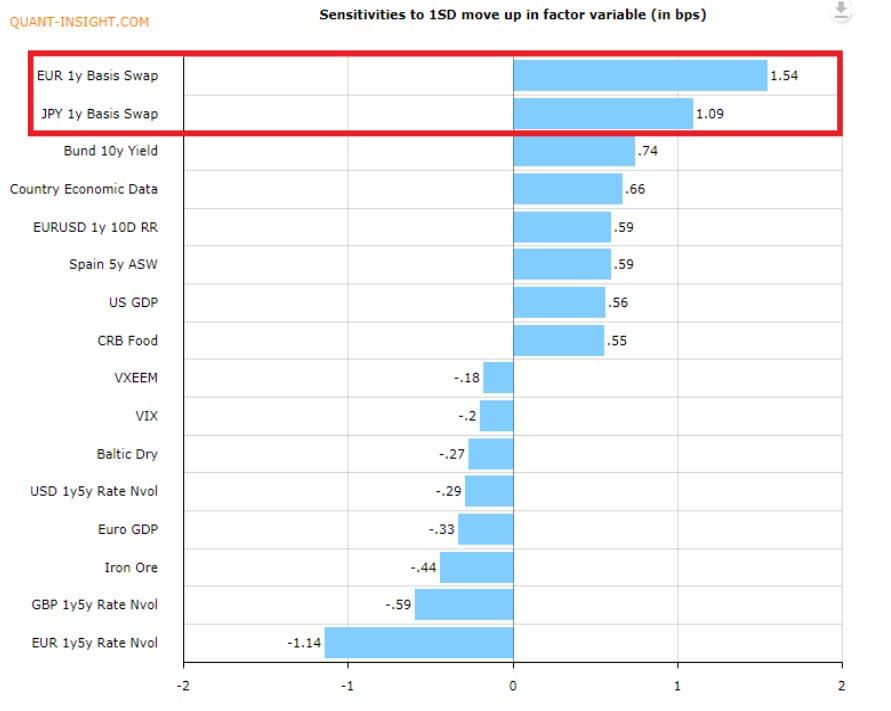

Dollar liquidity got a further boost when Italy for the first time since 2010 issued a $7b USD denominated bond on Oct 9th. That drove the likes of 1yr EU/US basis swaps higher which is atypical into year-end, and a signal that USD liquidity is improving.

Liquidity injection causing a positive cyclical feedback loop

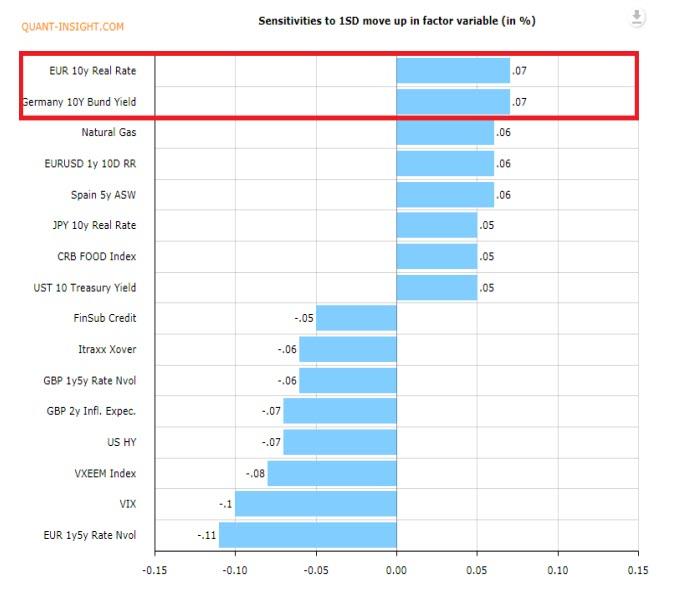

And if you are wondering why yields are rising, basis swap widening is your “tell.” The Fed (and ECB), are adding liquidity and that is driving global yields higher as confirmed in the QI macro PCA model which shows that for both US and China 10yr yields; rising basis swaps (ie: systemic liquidity) are causing nominal yields to rise.

China 10yr yield sensitivities to macro factors indicate basis swaps/systemic liquidity is causing rising yields…

Same story in the US and to show it a different way, the sensitivity to systemic liquidity has been increasingly positive since Oct. 8th…

Then, those rising yields are causing commodities like copper to rise. Copper’s macro sensitivities show rates are the top positive drivers…

And lastly, rising commodities, and the feed through to inflation expectations, is causing the S&P rally and the curve steepening.

So there you have it, the liquidity injection by the Fed’s “don’t call it QE” program is causing a very QE like reaction. Call it a positive cyclical feedback loop.

That’s “the where we have been,” but now let’s look forward. Is there further impetus for this theme to follow through beyond the Fed’s reaction function? YES.

IMPORTANT – Upside growth potential in Q4/Q1

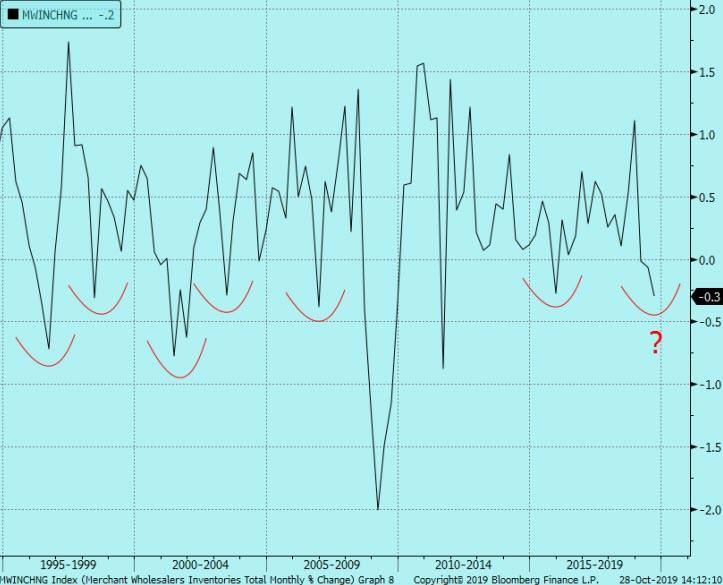

The market rhetoric over the past couple weeks has been stabilizing PMI’s. The Markit Manufacturing PMI for example bounced from a low of 50.3 two months ago to a modest 51.3 now – no big growth surge. However, the main positive in the report was the rise in New Orders and the decline of Inventories. In today’s ISM, we saw New Orders and Inventory both rise. This is the theme I want to highlight today: the potential that destocking in the Manufacturing sector is largely over and the potential for restocking.

As we saw in the Wholesale Inventory data on Monday, the current inventory drawdown is down to levels where you start to see restocking…

What differentiates this note from others is the willingness to do some dirty, bottoms up research like listening to earnings calls. What is MOST notable is that companies are commenting on this inventory dynamic in their earnings calls this quarter which is indication that we have reached a pivot point.

Let’s start with a global chemical company (often thought to be early cycle indicators) offering many different types of chemical products that operates in 30 different countries. They have exposure in North America, Europe, Middle East, and most importantly, China. This is about as good of a read through as you can get for cyclical stocks and on this destocking/restocking theme. What did they say in their earnings call on October 25th?

“We believe that the destocking we reported impacting the first half of the year in polyurethanes is finished most specifically in China.”

“We continue to see customer destocking with such a deep supply chain this business (textiles) has seen more volume pressure than our other businesses. We believe there is little if any destocking left in the chain.”

“Its volume that is hurting the bottom line and I suspect that volume will obviously be coming back as the economy starts to stabilize or even if the economy doesn’t stabilize when you see a lot of the de-inventorying, destocking that is out there taking place.”

”And I think that’s probably the first quarter in the last three quarters or so where we have seen a return to growth in China. So I’m not here to say that China is off to the races and we are going to great guns there but I do think that it has more to do with the idea that we’re done with destocking on a large basis in China.”

“While we’ve experienced real growth within this region demand in China remains well below average and erratic. We believe this will remain unchanged until trade discussions have some form of resolution thereby helping customer confidence and visibility.”

In other words, there is significant upside risk to rebuild inventories if at least some of the uncertainties can be removed, and China growth is better but still not robust.

How about a major global manufacturer of construction machinery…

“In the fourth quarter, we now expect end-user demand to be flat and dealers to make further inventory reductions due to global economic uncertainty.”

“…improved lead times, along with these dealer inventory reductions, will enable us to respond quickly to positive or negative developments in the global economy in 2020.

They are basically saying their dealers are still running down inventory, but if economy picks back up; they are coiled and ready to go.

One more company talking about how they are aggressively reducing inventories is a well-diversified manufacturer of everything from electronics to industrial products to consumer products…

“First, the biggest impact to Q3 margins was the year-on-year decline in organic volume, along with our actions to lower production volumes and reduced inventories to improve cash flow in the quarter.”

You get the idea. Large manufacturers have been running down inventory to build free cash flow. Typical in a slowdown but now will have inventory levels so low, that any improvement in growth prospects will leave them scrambling to rebuild.

Why is this inventory story important?

Critical point -> manufacturing companies have reduced inventories in the face of the China slowdown. Those same companies are indicating that a rate of change improvement in geopolitical risks (Trade Wars and to a lesser extent Brexit) could lead to a restocking. That restocking would give you more than just optimism the market has priced in. That’s real, hard economic growth which the market is not priced for. Dare I say the potential for green shoots.

Since the restocking is reliant on improved geopolitics, let’s address the two biggies.

US-China trade war progress

News last week that China passed a law that will protect IP rights of foreign businesses operating in the country

The fact they passed this is a very positive signal that China is willing to bend on a major sticking point in the negotiations

Pledge to open up Financial Services market

Reports that the Phase 1 deal is basically completed and to be signed Nov 17 in Chile

China requesting the US cancel some of the existing tariffs

Bottom line: a much more positive tone in the talks than we have seen all year. The ball is now in Trump’s court. The size of the reversal in the data will depend on the scope of the tariff roll backs. Most likely outcome is Trump simply does not impose the December tariffs but keeps all the prior tariffs in place until all phases of the deal are completed. That would mean a temporary bounce in the data but the long-term uncertainty will remain. Upside would be a rollback of previous tariffs especially those that hit the consumer.

Ignore the hype in yesterday’s headline regarding a long term deal with Trump. As our China watcher Jessica Sun is pointing out, China would rather make a deal with Trump than Warren, and despite long-term hurdles; China is “forging ahead” to prep for Phase 2.

EU fiscal stimulus

Two thing are driving the rising probabilities of fiscal stimulus currently:

Continued degradation in the German economic data – Manufacturing PMI still printing a depressed 41.9

Angela Merkel’s CDU party losing another regional election to the right wing AfD – the AfD advocates fiscal spending to boost the working class they tend to represent (similar to Trump in the US, Bolsonaro in Brazil etc.)

Bottom line: What used to be a long shot is now moving to possible. Germany, with their current account surplus, has had room to add stimulus but the German public generally has had disdain with running a current account deficit which made fiscal stimulus impossible. That is changing given the poor economy and rising prospects of the CDU losing power.

What does this do to the data deterioration theme?

It could pause it. Or to say it differently; it could cause a tactical economic bounce inside the larger data slowdown trend.

Note that despite the “beat” that the street set the market up for in today’s NFP, payrolls is growing at a 6m average of 155 down from 230 just one year ago. So growth in general is still soggy with the risk that the labor slowdown eventually bleeds into the consumer (strong consumer is THE most consensus thought – at risk).

Does this change the view on duration and curve shape?

In the front end, the Fed just “floored” Eurodollar pricing when Powell said they are not even thinking about hikes as inflation undershoots and AIT comes into their mindset mid-2020. Therefore, Eurodollars are the optimal hedge for cyclical longs as the Fed will not reverse the cuts. Additionally, the ironic thing about this potential economic bounce is if yields (long end) do rise more; it will push the economy right back into the data deterioration theme.

We are already seeing sectors levered to rates like the housing data start to fade (“misses” in Existing Home Sales, New Home Sales, Housing Starts, FHFA Home Price Index this month) so the point is rising yields will once again work to choke off an economy very sensitive to higher yields (too much debt, can’t have that bubble burst). Therefore, avoid shorting the front end and instead look to buy the dip as long-term indications are for further weakness in the US economy (as seen in forward indicators like CEO surveys). Use ED’s as your hedge against a Phase 1 breakdown.

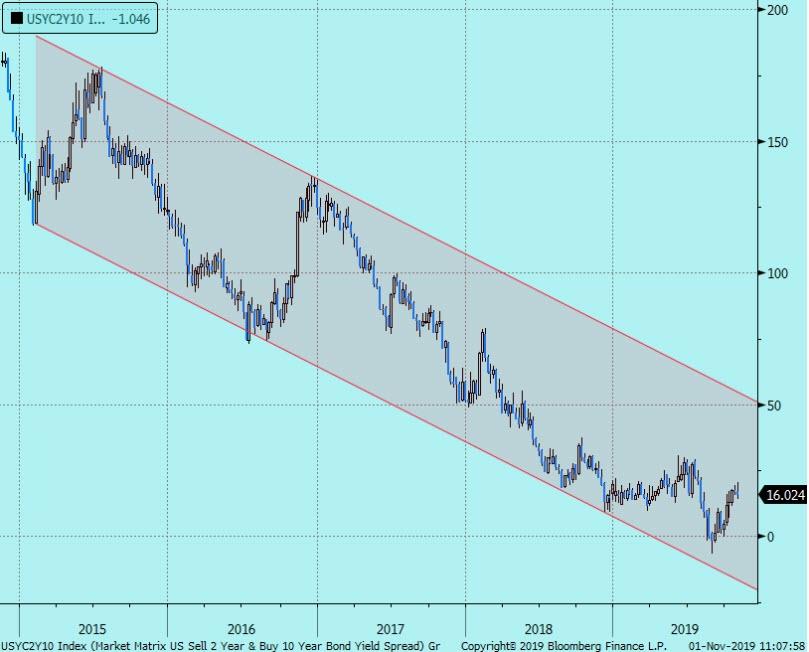

Therefore, the long end is more exposed to a broader correction if the restocking theme does kick in. That obviously argues for additional curve steepening.

US 2s10s: the inverse head and should pattern that formed in the summer is still in motion. The target is 25bps…

Are we being too short sighted though? Given all the catalysts, a larger move to the upper end of the range should be considered – new target 50bps?

Does this embolden the buy S&P upside/cyclical melt up thesis?

Definitely. Most of the positioning data I can find says the market is ill prepared for a rate of change improvement to the economic data. This “offsides” setup was apparent in the technicals which continue to indicate further price gains ahead.

S&P mini’s have broken out of its neckline of its bullish inverse head and shoulder pattern. Target is 3,185…

And obviously you can consider positions that are levered to China including EM equity indices, Euro Stoxx, and Copper.

To succinctly recap:

Inventory levels for the Manufacturing sector have been brought down to a level that makes it susceptible to reverse quickly if there is any surprisingly positive news on trade wars

With a Phase 1 deal looking done, that restocking risk is also growing which would be a near term boost for the global economy – Manufacturing PMI’s bounce

Additionally, German fiscal is finally looking like a possibility

The benefits of lower rates + higher stocks add an additional growth tailwind

That all means upside risk in risk assets and to some extent yields (long end)

Rising yields into the US election cycle (which will add uncertainty in 2020) will make this only a tactical bounce; the data deterioration theme will likely reemerge especially as the more difficult parts of US-China talks drag on

Continue to recommend:

S&P upside (ESH0 3300/3400 call spread)

Hedged with front end upside (2EG0 98.875/99.375 call spread now screening on top)

Sell Fed Fund spreads that have priced out cuts: FFM0/FFU0

Trump-Ukraine Whistleblower Suddenly Won’t Testify; Lawyers Break Off Negotiations Amid New Revelations

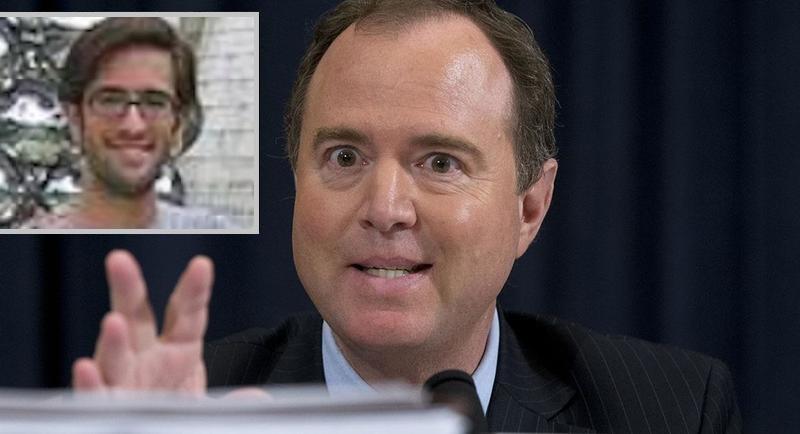

A CIA officer who filed a second-hand whistleblower complaint against President Trump has gotten cold feet about testifying after revelations emerged that he worked with Joe Biden, former CIA Director John Brennan, and a DNC operative who sought dirt on President Trump from officials in Ukraine’s former government.

According to the Washington Examiner, discussions with the whistleblower – revealed by RealClearInvestigations as 33-year-old Eric Ciaramella have been halted, “and there is no discussion of testimony from a second whistleblower, who supported the first’s claims.”

Ciaramella complained that President Trump abused his office when he asked Ukraine to investigate corruption allegations against Joe Biden and his son Hunter, as well as claims related to pro-Clinton election interference and DNC hacking in 2016.

On Thursday, a top National Security Council official who was present on a July 25 phone call between Trump and Ukrainian President Volodomyr Zelensky testified that he saw nothing illegal about the conversation.

“I want to be clear, I was not concerned that anything illegal was discussed,” said Tim Morrison, former NSC Senior Director for European Affairs who was on the July 25 call between the two leaders.

Tim Morrison

And now, the partisan whistleblowers have cold feet;

“There is no indication that either of the original whistleblowers will be called to testify or appear before the Senate or House Intelligence committees. There is no further discussion ongoing between the legal team and the committees,” said the Examiner‘s source.

The whistleblower is a career CIA officer with expertise in Ukraine policy who served on the White House National Security Council during the Obama administration, when 2020 Democratic presidential candidateJoe Biden was “point man” for Ukraine, and during the early months of the Trump administration. –Washington Examiner

In other words, House Democrats are about to impeach President Trump over a second-hand whistleblower complaint by a partisan CIA officer, and neither he nor his source will actually testify about it (for now…).

On Thursday, the House passed a resolution establishing a framework for Trump impeachment proceedings, belatedly granting Republicans the ability to subpoena witnesses, but only if Schiff and fellow Democrats on the Intelligence Committee agree.

Mark Zaid, who along with Andrew Bakaj is an attorney for both the original whistleblower and the second whistleblower, told the Washington Examinerthe legal team was willing to work with lawmakers so long as anonymity is ensured. “We remain committed to cooperating with any congressional oversight committee’s requests so long as it properly protects and ensures the anonymity of our clients,” Zaid said.

On Wednesday, Zaid and Bakaj declined to confirm or deny in a statement to the Washington Examiner that Eric Ciaramella, 33, a career CIA analyst and former Ukraine director on the NSC, was the whistleblower after a report by RealClearInvestigations. –Washington Examiner

In September, House Intelligence Committee Chair Adam Schiff, who lied about contacts with Ciaramella (and hired two Ciaramella associates as staffers) said that the whistleblower “would like to speak to our committee.”

We have been informed by the whistleblower’s counsel that their client would like to speak to our committee and has requested guidance from the Acting DNI as to how to do so.

We‘re in touch with counsel and look forward to the whistleblower’s testimony as soon as this week.

Once Ciaramella’s status as a CIA officer and his links to Biden emerged, however, Schiff backtracked. On October 13 he changed his tune, saying “Our primary interest right now is making sure that that person is protected.”

Attorneys for Ukraine call whistleblower new statement on speculation about the intelligence community employee’s identity. pic.twitter.com/UdsmSQ226P

Meanwhile, once the House impeaches Trump – which it most certainly will – the tables will turn in the Senate, which will hold a mandatory trial. Not only will the GOP-Senators controlling the proceedings be able to subpoena documents and other evidence, they’ll be able to compel Ciaramella, the Bidens, Chalupa and any other witnesses they desire as we head into the 2020 US election.

Nancy Pelosi saw this coming and caved to her party anyway. There isn’t enough popcorn in the world for what’s coming.

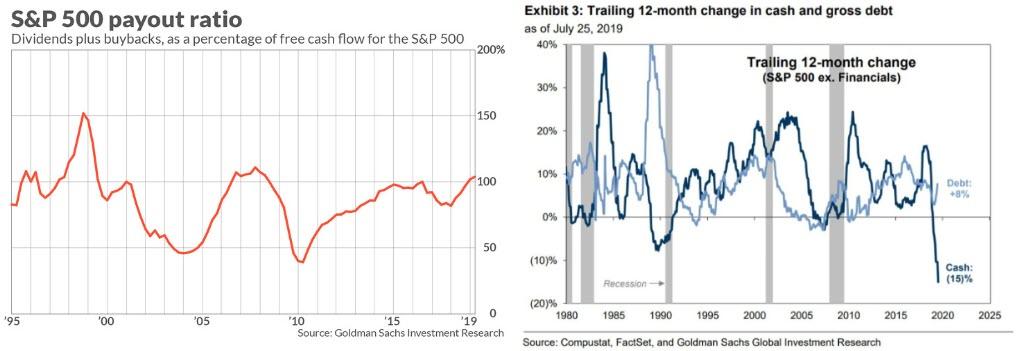

The SPX recorded new highs this week. Investors appear to be excited about the U.S. – China Phase 1 trade agreement, which only goes so far in ending the trade war. Plus, the Fed is cutting interest rates, injecting $100 billion in repo financing over the next month, and embarking on a new round of QE. So, is it clear sailing for corporate America? Maybe companies are not as financially viable as record SPX levels would indicate.

Let’s look at the lifeblood of a company, cash flow. Goldman Sachs analysis of corporate cash flows shows that SPX companies are actually running, in aggregate, negative cash flow at 103.8% while keeping stock buybacks and dividends flowing to shareholders. Debt is up 8% squeezing corporate cash flow to the point where aggregate cash flows are down 15% versus the prior year.

Source: Goldman Sachs – 7/25/19

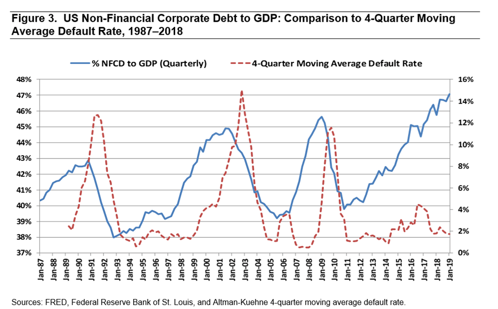

Cash is the lifeblood of a company, but a company can’t borrow money forever without being a viable profitable entity able to pay back debt.

Non-financial corporations have taken on record debt at 47% to GDP. The last time corporations approached this level of debt was during the Great Recession. Yet, default rates have not gone up.

Sources: Federal Reserve Bank of St. Louis, Edward Altman – 8/5/19

Is this time for debt payment defaults different? It would seem this is a ‘benign credit cycle’ when defaults don’t rise. However, a more likely cause is that corporate cash flows are being pumped up by low interest rate loans. This corporate financial cliff maybe one reason the Fed is moving quickly to keep overnight and interest rates low. The Fed has said it is concerned about high levels of corporate debt. What is wrong with corporate debt at 47% of GDP?

The issue is when profits sink due to the trade war or as consumer spending slows, companies will no longer qualify for low interest loans. Banks and investors will hesitate to take on risky loans to companies raking up continuous losses. Without low cost loans to provide needed cash flows, sales decline will result in a freeze on hiring, the layoff of full time workers, and a closure of offices and plants. Management will take these measures to try to keep the company open until sales turnaround.

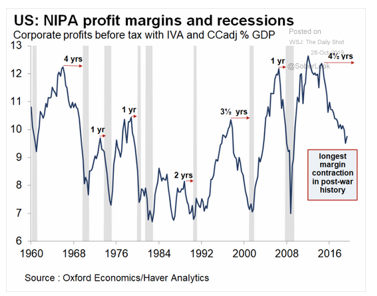

The profit margin squeeze has been happening over the past 4 ½ years, well before the trade war started. Profits were flat for the past nine years, supported by a huge corporate tax cut from the Tax Cut Bill of 2018. The contraction in profit margins has been the longest one on record since WWII. Note how recessions usually follow steep declines in profit margins at 1 to 4 years.

Source: Oxford Economics, The Wall Street Journal, The Daily Shot – 10/28/19

Why have margins been contracting? Margins can be increased by investing in automation, lowering material costs, deploying productivity enhancements, and other efficiencies. Instead of investing in margin increasing activities, corporate executives have been spending available cash from profits and debt on stock buybacks totaling $1.15 trillion in 2018. Stock buybacks are a way to boost corporate stock prices thereby increasing the income of shareholders and executives. Executives have squandered over the past ten years the opportunity to use profits for investments in research, productivity enhancements, raising wages, or cutting costs. Management has focused on short term stock gains at the cost of long term corporate viability. The chickens are finally coming home to roost.

In addition, profit margins are declining due to declining international sales. It is difficult to maintain healthy margins when sales are falling due to base spending for sales, support, and transportation to reach a certain sales threshold of profitability. Major corporations face increasing trade headwinds. For most S & P 100 corporations 50 to 60% of their sales come from overseas with prior growth rates from 15 – 25% per year in emerging markets. The Asia – Pacific region is the fastest growing sales region for many companies. Yet, the accumulating tax of trade tariffs and trade uncertainty is stifling sales growth.

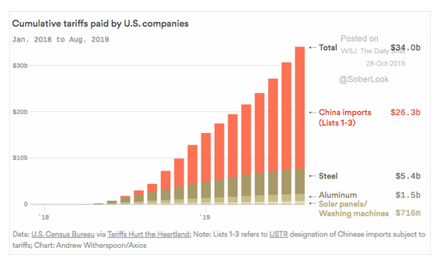

Sources: U.S. Census Bureau, Tariffs Hurt the Heartland, USTR Office, The Wall Street Journal, The Daily Shot – 10/28/19

Since January of 2018, U.S. companies have paid about $34 billion in tariffs. To hold price levels and market share, companies largely paid tariff costs themselves rather than passing them onto customers. Taking tariff costs onto corporate ledgers has squeezed profit margins. The loss of decent margins in high growth markets is creating a huge profit challenge for companies.

While the Phase 1 agreement with China may provide a pause to the trade war, breaking up into two major trade blocks. Corporations will have to navigate selling into two opposing markets with focused sales, support, and product features and pricing. For more details, see our post Navigating A Two Block Trade World to see how companies plan on changing supply chains, and the implications for investors.

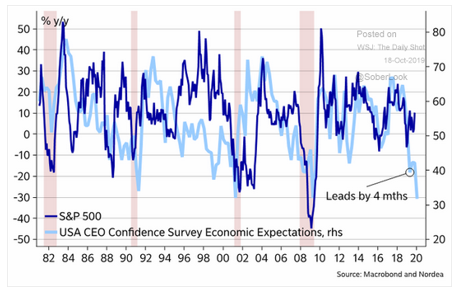

Corporate executives see a loss of profits and margin tightening in the future. A recent CEO survey showed confidence levels of SPX CEOs at recession levels. The survey results indicate a possible SPX decline beginning as soon as four months from now.

Sources: USA CEO Confidence Survey, Macrobond, The Wall Street Journal, The Daily Shot – 10/18/19

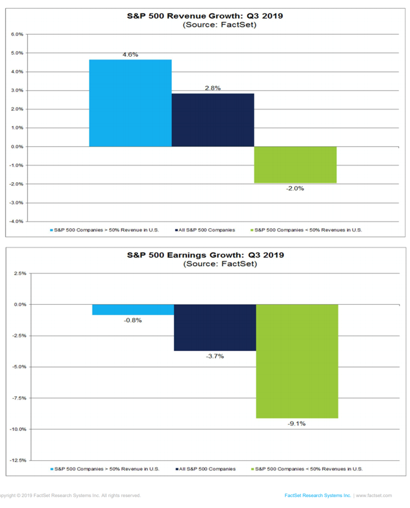

The concerns that CEOs see in revenue and profitability were borne out in 3rd quarter reports of 40% of S &P companies. Companies with more than 50% of sales in international markets report a 9.1% decline in profits and a 2.0% decline in revenue. All S &P companies report a 3.7% slip in earnings thus far for 3rd quarter of 2019.

Source: Factset – 10/25/19

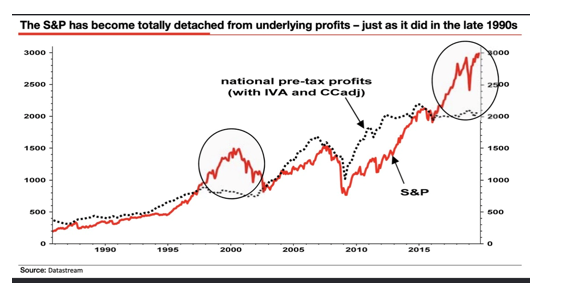

Are equity markets recognizing the decline in profits for corporations? The chart below shows the SPX rising despite flat national corporate profits since 2013, with a huge divergence emerging in the past four years. The SPX soaring to new heights tells us that stock marketcomplacency is at record levels in appraising stock valuations versus actual corporate profits. The chart below shows how wide the gap has become which is about twice the gap size just before the Dotcom decline into 2002 from a peak in 2000.

Source: Soc Gen – Albert Edwards – Marketwatch – 10-28-19

The economic storm corporate executives see on the horizon is likely to be a future economic reality, and not liquidity fueled soaring valuations. Executives are closest to economic reality because they have to make the economic system work for their company day in and day out.A reversion of equity valuations to the reality of falling corporate profits is coming. The only question remaining is: when will the SPX reversion happen?

* * *

Patrick Hill is the Editor of The Progressive Ensign, https://theprogressiveensign.com/ writes from the heart of Silicon Valley, leveraging 20 years of experience as an executive at firms like HP, Genentech, Verigy, Informatica and Okta to provide investment and economic insights. Twitter: @PatrickHill1677.

Netflix Slides After NBC Weighs Free Streaming Service To Everyone

Netflix is sliding into late session after Comcast’s NBCUniversal is “considering giving away the ad-supported version of its streaming service Peacock for free to everyone,” sources told CNBC.

The battle for online streaming services, which includes companies like Netflix, Amazon Prime, Hulu, and Playstation Vue, seems to be heating up as subscriber growth for many of these platforms are peaking.

NBC offering Peacock streaming service for free is a massive blow to Netflix.

WeWork CEO Adam Neumann Accused Of Pregnancy Discrimination

Adam Neumann is apparently still creating problems for WeWork, even after being ushered out of the CEO role by the company’s latest “investors”.

Medina Bardhi, described as “chief of staff” to WeWork co-founder Adam Neumann, is now suing the ousted CEO for pregnancy discrimination, claiming she was marginalized and derided by Neumann after becoming pregnant, according to the New York Times.

In 2016, Bardhi informed Neumann she was pregnant and told him that she wouldn’t be able to accompany him on business trips “due to his penchant for bringing marijuana on chartered flights and smoking it throughout the flight while in an enclosed cabin.”

From there, she is alleging a pattern of discrimination from Neumann, including him calling her maternity leave a “vacation” and “retirement”, according to a complaint she filed with the Equal Employment Opportunity Commission in New York on Thursday. Bardhi’s lawyer said he hoped that the EEOC would file a class action charges against the company.

“Wow, you’re getting big,” another high-level company official, Jennifer Berrent, reportedly said to Bardhi in front of another WeWork executive.

Bardhi was demoted both times she was pregnant while working at the company, the complaint says. She was then fired in early October, shortly after Neumann’s departure, when she was told there was “no longer a role” for her.

The complaint says: “This assertion and supposed justification rings hollow, as Ms. Bardhi already had been pushed out of Mr. Neumann’s office. It is clear that Ms. Bardhi’s firing was motivated by the Company’s sustained discriminatory bias and retaliatory animus against her and other female employees who become pregnant, take maternity leave, and/or complain about gender-based discrimination.”

Bardhi also says in the complaint that the discrimination started at a job interview in October 2013, when Neumann “unlawfully and intrusively” asked if she planned to get married or become pregnant. The question left her “stunned and uncomfortable,” she claims.

After she first became pregnant, three years later, she claims Neumann replaced her with a male employee who was paid more than twice as much. After she got the job back, she became pregnant a second time, and another male employee was hired to replace her. She was “sidelined” when she returned back to work.

“She was given no information about what her new role would be,” the complaint said. “This was obvious retaliation for her taking maternity leave and discrimination against a pregnant employee and new mother.”

“I hope you enjoyed your vacation,” Neumann allegedly said to her while driving back from a meeting on September 16.

The news flies in the face of promises made by Neumann to champion women at the company. “We like to say that right now we’re bringing in the most talented women in the world at an early stage,” Neumann said in 2017.

And over the last year, other women at WeWork have filed lawsuits accusing the company of gender discrimination. Neumann’s leadership has been singled out, as a result, and he has been criticized for maintaining a lavish lifestyle and giving family members, including his wife Rebekah, too much power at the company.

A WeWork spokeswoman said the company “intends to vigorously defend itself against” the complaint.

The statement continued: “We have zero tolerance for discrimination of any kind. We are committed to moving the company forward and building a company and culture that our employees can be proud of.”

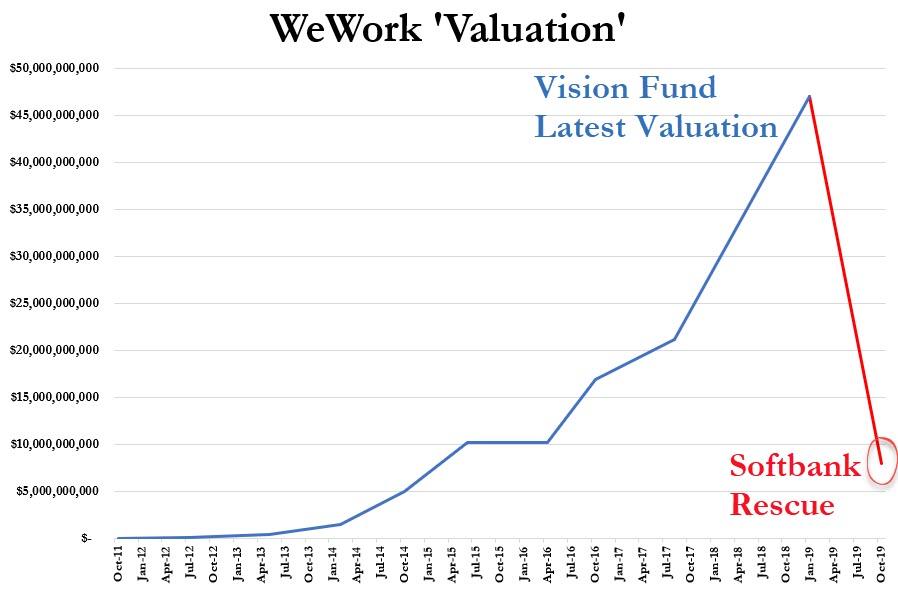

Recall, Neumann stepped down as the company’s CEO in September after its IPO imploded on itself like a dying star. Neumann, on the other hand, will make out just fine. After cashing out over $600 million as CEO, he is now set to receive $185 million to work as a consultant to the company for four years.

{kind=link}