Here Comes The Double Dip: JPMorgan Forecasts Negative GDP Next Quarter Tyler Durden

Fri, 11/20/2020 – 12:36

In retrospect, it was inevitable: after European growth hit a brick wall in October and early November after a second round of partial (or full) lockdowns were imposed, with even the ECB warning that Q4 GDP may turn negative after the record rebound in Q3, it was only a matter of time before the US – which is now experiencing a second round of creeping lockdowns across the coastal states – suffered the same fate.

As we showed earlier, the Citi econ surprise index has clearly pointed the way, having swung sharply lower (as one would expect after the biggest – and shortest – economic collapse since the Great Depression) in recent months, as the economy caught up to trendline on the back of trillions in fiscal stimulus.

Furthermore, with the US entering 2021 without any firm commitment for another much needed round of fiscal stimulus – which we hope everyone realizes is the only reason why the economy did not disintegrate in the summer and fall – even as the rising number of covid cases continue to dominate the economic outlook, the time for the realization that a double dip is imminent, was drawing close.

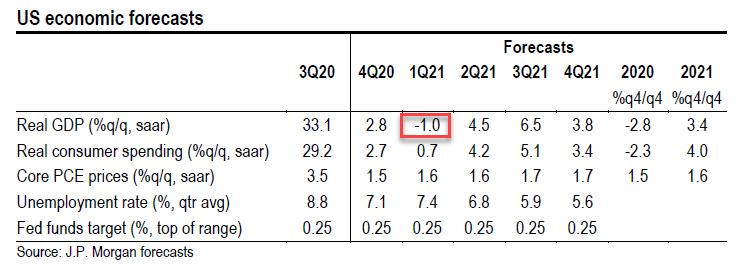

That time came this morning in a note from JPM chief economist Michael Farolil, who writes that while the economy powered through the July coronavirus wave, “at that time the reopening of the economy provided a powerful tailwind to growth. The economy no longer has that tailwind; instead it now faces the headwind of increasing restrictions on activity.” Meanwhile, “the holiday season—from Thanksgiving through New Year’s—threatens a further increase in cases. This winter will be grim, and we believe the economy will contract again in 1Q, albeit at “only” a 1.0% annualized rate.“

In other words, the double dip is about to hit.

The good news is that even without a major stimulus, JPM sees the Q1 recession reverse quickly, because “the early success of some major vaccine trials increases our confidence that such medical intervention can limit the damage that the virus has inflicted on the US economy. (Alas, some lasting damage still seems inevitable.)” As such, JPM expects that by 2Q the vaccine will be available to health care providers, other essential workers, and at-risk populations. JPM then assumes “broader availability to the rest of the population by 3Q or 4Q” which means that while uncertainties abound, “if this timeline is broadly correct, a normalization of activity should give meaningful support to growth in mid-2021.”

And while (the lack of) a vaccine is certainly a downside risk, another potential risk is that the fiscal stimulus which JPM expects will be released next year, also fails to materialize:

By a wide margin, the course of the virus has been the most important factor shaping the outlook. But fiscal policy has been firmly in second place. This year’s unprecedented fiscal support was crucial in jump-starting the current recovery. We expect more fiscal action next year—with a baseline assumption of $1 trillion by the end of 1Q. If realized, this would further support the case for strong growth in 2Q and 3Q.

This assumption appears overly optimistic assuming we enter 2021 with an even more polarized political climate than ever before (which judging by the unexpected Treasury-Fed right overnight is right on schedule) suggesting that the real risk is we get zero (or a token) fiscal stimulus in early 2021, something JPM also concedes is a distinct possibility:

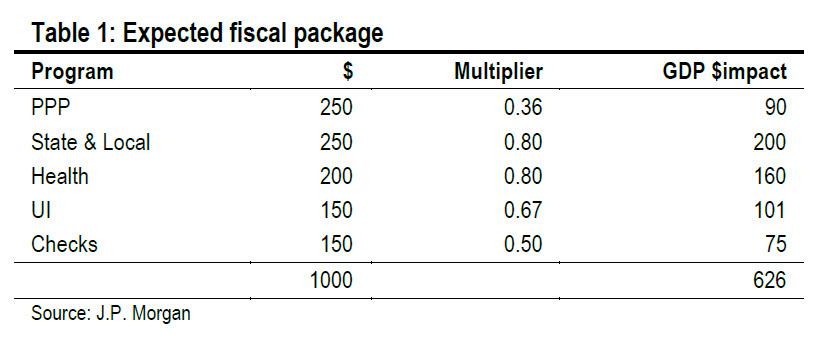

If instead we get no further fiscal support, this year’s massive fiscal thrust is set to turn to fiscal drag. For example, Figure 4 presents the fiscal impact measure developed at the Hutchins Center at the Brookings Institution. If we get the fiscal support we expect, that drag gets dampened and pushed back, allowing a vaccine more scope to boost growth.

In this “fiscal-free” scenario, the question becomes how long after the economy double dips before the Fed sparks the next crisis that will allow it to unleash the next several trillion of liquidity into the market (thus allow stocks to hit JPM’s 2021 target of 4,100 which even the bank admits will happen purely on central bank liquidity).

via ZeroHedge News https://ift.tt/391rG2P Tyler Durden

New Senate Docs ‘Confirm’ Troubling Biden Family Links To China, Russia Tyler Durden

Fri, 11/20/2020 – 12:30

With Joe Biden’s ‘irregularity-filled’ election win all but assured (unless the Trump campaign can pull off several upset legal victories), we now turn our attention back to the Biden family’s ties to Russia and China – a narrative which the MSM will attempt to suffocate out of existence – particularly if Republicans (and their investigative committees) lose the Senate after January’s runoff in Georgia.

In a “supplemental” release to a late September Senate report into Hunter Biden’s international business dealings, Sens. Chuck Grassley (R-IA) and Ron Johnson (R-WI) outlined additional information regarding troubling connections between Hunter Biden’s business associates and the Russian government, as well as ‘millions of dollars’ transferred from a CCP-linked Chinese entity to a Biden business associate who allegedly leveraged his relationship with the former Vice President’s family, according to the Washington Examiner.

“These new records confirm the connections between the Biden family and the communist Chinese government, as well as the links between Hunter Biden’s business associates and the Russian government, and further support the Committees’ September 23, 2020 report’s finding that such relationships created counterintelligence and extortion concerns,” wrote the senators in a five-page report which included 65 pages of evidence.

Elsewhere, they wrote that after their September report was issued, “new sources went public with additional information about business relationships and financial arrangements among and between the Biden family and their business associates, including several foreign nationals … The new information is consistent with other records within the Committees’ possession which show millions of dollars being transferred from a Chinese entity linked to the communist party to Robinson Walker LLC.” –Washington Examiner

A key focus of the supplemental report is Rob Walker, described as “Hunter Biden’s longtime business associate.” Walker is associated with three companies tied to Hunter according to the report, which includes new information from former Biden business associate Tony Bobulinski, who worked with the Bidens and Walker in 2017 to create a business which would establish a joint venture with a Chinese Communist Party-linked business, CEFC China Energy – which was run by a disappeared Chinese tycoon and has since gone bankrupt.

Bobulinski, who was tapped to lead the Biden JV through “SinoHawk”, repeatedly referenced $10 million in startup funding from a Chinese businessman – money which never materialized, yet which Grassley and Johnson conclude some or all ultimately wound up to accounts linked to James and Hunter Biden.

The Senate investigation update noted that in February and March 2017, a Shanghai-based company called State Energy HK Limited “sent two wires, each in the amount of $3,000,000, to a bank account for Robinson Walker LLC” but that “it is unclear what the true purpose is behind these transactions and who the ultimate beneficiary is.” State Energy HK Limited was affiliated with CEFC under the leadership of Ye Jianming, who had “ties to the Chinese Communist Party and Chinese military” and whose deputy, Gongwen Dong, another business associate of Hunter Biden’s, also received funds from State Energy HK. –Washington Examiner

“These transactions are a direct link between Walker and the communist Chinese government and, because of his close association with Hunter Biden, yet another tie between Hunter Biden’s financial arrangements and the communist Chinese government,” reads the Grassley and Johnson release, which also concludes that Hunter “received a $3.5 million wire transfer from Elena Baturina, the wife of the former mayor of Moscow” and that he also “opened a bank account with” Gongwen Dong to fund a $100,000 global spending spree” along with James Biden and his wife, Sara.

William White, former chief economist of the Bank for International Settlements, is taking central banks to task. Monetary policy over the past three decades has caused ever higher debt and ever greater instability in the financial system, says White. Fiscal policy must take over to deal with the current crisis.

William White has seen a lot in his professional life. He worked for central banks for almost fifty years, most recently for the Bank for International Settlements in Basel, where he was Chief Economist until 2008. Back then, he was one of the few officials who had warned of a looming financial crisis.

Today, the Canadian criticizes the central banks:

«They have pursued the wrong policies over the past three decades, which have caused ever higher debt and ever greater instability in the financial system.»

He suggests that the current crisis should be used to rethink in order to build a more stable economic system, one in which fiscal policy plays a greater role and that relies more on productive investment. In this in-depth conversation, White says what should be done – and he demands more humility from decision makers: «We know much less about the economy than we think we do.»

Mr. White, the pandemic has caused the deepest recession since at least the 1930s. How would you rate the reaction of fiscal and monetary policy makers so far?

First, this pandemic again shows how little we know. We’re dealing with a high level of uncertainty about its progression, and we all need a healthy dose of humility. Having said that, I’d say it was the right thing to do to open the fiscal policy spigots to prevent the economy from crashing. I’m more sceptical whether still easier monetary policy is the right answer for a shock of this character. In fact I hope we’ll use this crisis for some serious soul searching on whether the monetary policy of the past thirty years has done more harm than good. But to fight the immediate effects of the pandemic, there was not much else policy makers could have done.

Let’s focus on the fiscal side first: When is the time to withdraw the support?

Certainly not now. There is still room for manoeuvre on the fiscal side and we can still increase that room. Bond markets are wide open. Governments should use the current environment to borrow long and lock in cheap money while they can.

Are you not worried about rising government debt levels?

What I’d like to see is clear guidelines from governments about how they intend to get debt levels down in the future. I’m not talking about a German style debt brake here, but guidance on what types of expenditure cuts and tax increases they would be looking at. They should use this crisis as an opportunity to cut subsidies that often go to special interest groups that don’t deserve them anyway. But let’s be clear, this is not the time for austerity. I’d paraphrase St. Augustine: Lord, give me chastity – but not yet. That was the big mistake after the Global Financial Crisis: Most governments entered the austerity path too early and left it to the central banks to get the economy going. Sadly, that’s been the pattern for the past thirty years.

How do you mean that?

Once upon a time, it was accepted that fiscal policy could play a productive role in dealing with a severe economic downturn. This is what Keynes gave us with the General Theory. But some time in the 1980s, the belief system changed. Fiscal policy needed to be targeted, timely and temporary to be effective, but our legislative processes could not deliver. So fiscal policy grew out of favour. At the same time, starting in 1987 with Alan Greenspan at the Fed, monetary policy grew to be the instrument of choice for all kinds of crises.

And that was wrong?

We’re on a slope where monetary policy has become increasingly ineffective in promoting real economic growth. Every crisis was met with monetary easing that caused debt and other imbalances to accumulate over time, and that caused the next crisis to be bigger than the previous one. The next crisis then needed more punch from central banks. But since interest rates were never raised as much in upturns as they were lowered in downturns, the capacity to deliver that punch was decreasing.

In March of 2020, the financial system was on the brink of collapse with widespread panic in equity and bond markets. The Fed ended that panic by announcing they would buy corporate bonds. Is that not strong proof that monetary authorities are in fact very effective?

This episode perfectly encapsulates my view of what’s wrong with our monetary policy of the past decades. True, the Fed had no choice but to step in to prevent a financial meltdown. But this meltdown only happened because of the monetary policy followed over previous years. You see, by keeping interest rates too low and thereby trying to create economic growth, central banks are inducing corporations and households to take on more debt. To a large part, this debt is not used for productive investments, but for consumption or, especially in the U.S., for the buyback of shares. This creates a debt trap as well as rising instabilities in the financial system. These instabilities broke out in March and the Fed responded adeptly to stop the panic. But my point is: Central banks create the instabilities, then they have to save the system during the crisis, and by that they create even more instabilities. They keep shooting themselves in the foot.

Have central banks reached the end of the road?

Just read what Bill Dudley, the former president of the New York Fed, wrote in Bloomberg a couple of weeks ago. He warns that central banks have run out of firepower, and he warns that the side effects are getting worse. I agree with every word. That is the most dangerous effect of the past thirty years of monetary policy: Debt levels have constantly been building up, and so have the instabilities in the financial system.

Jerome Powell has tried to normalize monetary policy, but he had to stop after a market panic in late 2018. Is the Fed hostage to financial markets?

This is exactly my definition of the debt trap: Central banks know they can’t leave interest rates as low as they are, because they are inducing still more bad debt and bad behavior. But they can’t raise rates, because then they would trigger the very crisis they are trying to avoid. There is no way out but to keep doing what you are doing, but by doing that, you are making it worse. Pretty uncomfortable, right?

After the Financial Crisis, there was a lot of talk about deleveraging the system. Nothing happened. Why?

In 2008, the ratio of global household, corporate and government debt to GDP was 280%. Early 2020, this ratio had grown to 330%. And it’s not just the quantity of that debt, it’s the quality. Most of the new corporate debt is BBB-rated, covenant light, low quality stuff. The reason for that is the ultra easy monetary policy we have seen post-2008. Governments made the mistake of embracing fiscal austerity too early. By that, they left the job to the central banks to frantically try to create economic growth. This is a mistake we must avoid after this crisis. Fiscal policy will have to play a much larger part going forward.

Central banks have argued that their easy monetary policy is needed because inflation was too low. Were they correct?

No, that was a misconception. Starting in the late 80s, we had a series of positive supply shocks to the world economy, most important of all the establishment of China as a manufacturing economy, as well as the collapse of the Soviet Block. Hundreds of millions of workers thus entered the capitalist world economy. At the same time, the members of the Baby Boom Generation grew their way through the Western economies. This manifested itself in a sustained positive supply shock that had a strong disinflationary effect on the world economy.

So central banks tried to fight a disinflation that was in fact benign?

Exactly. There are periods of low inflation or outright deflation that ought not to be of concern for central banks. If prices want to go down because of productivity increases: What’s wrong with that? Productivity increases give you higher profits and lower prices, which is the way productivity gains are shared between the entrepreneurs and the consumers. There is a raft of pre-war literature on the topic of benign deflation, but our central banks have forgotten about it.

And yet, one of the most steadfast arguments for their policy is the undershoot of inflation. The Fed even changed its inflation mandate to achieve «on average 2% over time». What do you make of that?

When you have a lack of demand and high unemployment, then it absolutely makes sense to pursue an easy monetary policy. My problem is that, over many years, central banks have done everything to fight this perceived undershoot of inflation, regardless of its cause. They pulled out all the stops, not least by imposing negative interest rates in the Eurozone, which weakened their banking system. Despite measures of inflation being so imprecise and so unsure, as repeatedly noted by the late Paul Volcker, many central bankers have been willing to pull out all the stops in response to decimal point deviations. That, to me, is hard to justify.

Looking forward, can there be such a thing as normalization in monetary policy?

There is no return back to any form of normalcy without dealing with the debt overhang. This is the elephant in the room. If we agree that the policy of the past thirty years has created an ever growing mountain of debt and ever rising instabilities in the system, then we need to deal with that.

How?

In theory, there are four ways to get rid of an overhang of bad debt. One: Households, corporations and governments try to save more to repay their debt. But we know that this gets you into the Keynesian Paradox of Thrift, where the economy collapses. So this way leads to disaster. Two: You can try to grow your way out of a debt overhang, through stronger real economic growth. But we know that a debt overhang impedes real economic growth. Of course, we should try to increase potential growth through structural reforms, but this is unlikely to be the silver bullet that saves us. This leaves the two remaining ways: Higher nominal growth – i.e. higher inflation – or try to get rid of the bad debt by restructuring and writing it off.

Which way will it be?

Probably a combination, but they are all very hard to achieve. It’s fairly obvious that a number of policy makers will try to inflate the debt away. This was how they did it after World War II, through what we now know as financial repression: Get inflation above interest rates, and then the debt ratio gradually comes down. It’s just very hard to engineer the kind of inflation that is just right for this process.

A number of heavyweight economists are suggesting exactly that: Engineer inflation levels of 4 to 8% over a number of years to inflate the debt away.

Sure, that’s what Larry Summers and Olivier Blanchard are saying. Perhaps that’s possible. My only point is that they are starting with the assumption that the nature of the economy means it is understandable and controllable. But I’m saying we are dealing with a complex adaptive system, full of tipping points, and we should not assume that we can understand and control it. On the one hand, in depressed circumstances, it might prove impossible to raise inflation. On the other hand, given enough fears of fiscal dominance, you might get a lot more inflation than you bargained for.

The period of financial repression after World War II had another prerequisite: capital controls to prevent capital flight. Are they feasible today?

When I started working at the Bank of England in the late 1960s, the biggest department in the place was Foreign Exchange Control. In the modern world, is it really possible for a single government to control the outflow of capital in the way that would be required? I doubt it. Yet, if a number of large governments simultaneously embark on a path of financial repression, it raises the question of where capital might flee to? Gold? Bitcoin? In such an environment, I would be worried if I were Swiss. People might see the Swiss Franc as one of the currencies to flee into. Financial repression has the potential to be a messy process.

What about the fourth way: write-offs?

That’s the one I would strongly advise. Approach the problem, try to identify the bad debts, and restructure them in as orderly a fashion that you can. But we know how extremely difficult it is to get creditors and debtors together to sort this out cooperatively. Our current procedures are completely inadequate.

How so?

Let me give you two examples: It was clear that the best way forward for Greece after their crisis of 2010 was a comprehensive debt relief in return for structural reforms. However, policy makers in Berlin and Brussels never agreed to the level of debt relief that was needed, and so they pushed Greece into a destructive austerity spiral. Or look at government debt in Sub-Saharan Africa today: A lot of it has to be written off. Otherwise these countries are going to be forced to continue to try to pay, and they will do it at the expense of healthcare and so on. That’s a recipe for human disaster. But we are dealing with public, private and Chinese creditors, who are competing to be paid. Why should a Western private creditor give up his claim if the Chinese don’t? Unfortunately, recent legal rulings like NML Capital versus Argentina have taught creditors that it’s best to hold out. So, all over the world creditors don’t agree to restructurings but rather extend and pretend that the debt is still viable. And it’s all made superficially viable by easy monetary policy.

It almost seems the easiest way is to just keep doing what we are doing?

You are right. My colleagues at the BIS and I have been warning of this debt trap issue for twenty years. I am reminded of the economist Herb Stein who once said that, if something cannot go on forever, it will stop. To which Rudi Dornbusch quipped: Yes, but it will go on for a lot longer than you anticipate. One of the reasons for not changing anything is indeed the argument that it has worked so far. What is needed now is agreement that our policies of the past thirty years have created an ever rising level of debt and ever increasing instabilities. Should it be agreed that this path is not sustainable, as it leads to ever bigger crises, it’s an absurd proposition to stay on that path.

Knowing that complex adaptive systems are prone to tipping points: What could derail this system?

I don’t know. One of the conclusions of the complexity literature is that the trigger itself is irrelevant. If the system is unstable, anything could be a tipping point, even if the instability goes on without incident for years. Again, take the episode of March 2020, when these corporate giants in the U.S. were wobbling. The Fed stopped the panic. What if markets at that point had lost confidence in the ability of the Fed? We only know in hindsight that it worked. But we don’t know how the system will react in the future. In fact we know much less than we think we do, which is something that both Hayek and Keynes, commonly described as being at odds, totally understood. Central bankers, indeed all macroeconomists, should be much more humble than they are.

You said that we should use this crisis to build a better system. Apart from dealing with the debt overhang: What do you envisage?

One, I think population aging means we have to build a system that relies much more on productive investment to support both current demand and future pensioners. When I said that fiscal policy has more room in the next few years, it’s absolutely clear to me that there is a lot of potential for good, productive public infrastructure investment, particularly in America and Europe. Again, debt is not a problem as long as it is used for productive investments. Two, we need a corporate system that relies more on equity and less on debt. Managers, particularly in the U.S. and the UK, who took on more debt just to buy back shares to boost their stock options, have acted irresponsibly. Cutting back on capital investment for the same reason is even worse. This bonus culture is wrong. Three, we need a system in which there is more competition and less concentration. Monopolies have been quietly building in the past years, and these monopolies use their extra profits to gain political control. Four, we have to realize that the problems in our political system – populism, alienation, distrust – have their roots in our economic system: in particular, rising inequality. We’ll have to deal with that.

How?

When this pandemic is over, we will see rising marginal tax rates, we will have to talk about wealth taxes, and there must be a much more robust crackdown on the shifting of corporate taxes and criminal tax evasion. And, of course, we’ll have to deal with climate change, a clear and present danger that only people in denial refuse to accept. These are huge tasks.

Are you optimistic that we’ll master them?

I honestly don’t know. We’ll need a paradigm shift in our thinking, and we know from history how difficult that is. I mean, both Copernicus and Darwin delayed publishing their work for years because they knew how much their ideas would upset the establishment. Since the Reagan-Thatcher Revolution of the early 80s we’ve worked with a set of beliefs. And some of these beliefs have turned out to be wrong. These false beliefs need to be changed.

Such as?

The idea that price stability is sufficient for economic stability? Wrong. That easy money always stimulates demand? Wrong. That the economy is self-adjusting, back to a full employment equilibrium? Wrong. That financial markets are efficient and bad things can’t happen? Wrong. That wealth will trickle down to all levels of society? Wrong. These are big beliefs. And false beliefs are dangerous.

You know the saying attributed to Mark Twain: It ain’t the things that you don’t know that get you, it’s the things that you know for sure, that ain’t so! Never forget: We think we know much more than we really do.

via ZeroHedge News https://ift.tt/35PCRcK Tyler Durden

Why The Treasury-Fed Dispute Is Actually Good For Stocks Tyler Durden

Fri, 11/20/2020 – 11:53

Late on Thursday, when we commented on the implications of Mnuchin’s “political” decision to end various emergency facilities jointly operated by the Treasury and the Fed, including the muni liquidity program and Main Street lending program which many Wall Street strategist pointed out “present market disruption risks”, we said that the market is likely completely misreading this analysis, for the simple reason that less support from the Treasury – whether via Fiscal stimulus or helicopter money – means that the Fed will be required to do more, either in the form or more outright QE or expanded duration of existing debt monetization.

Overnight, Ben Emons, head of global macro strategy at Medley shared a similar view, writing that “the Fed may boost Treasury purchases and/or extend maturities of the securities it buys through its main QE program because of the dispute.“

Now, in his morning note, BMO’s chief rates strategist Ian Lyngen agrees with this take and writes that “there is little question that this increases the probability that the Fed pushes forward with an extension of the WAM of QE purchases at the December 16 FOMC meeting.“

Why is this important?

Because when it comes to capital markets, the Fed’s monetary policy – be it QE, YCC, or NIRP – is far more powerful and quick in raising risk prices, whereas any “spending-based” stimulus that goes through the Treasury is not only greatly diluted by the time it hits stock prices (after all it goes through the broader economy first), but it also raises the possibility of inflation. Remember: nothing crushes PE multiples faster than a jump in inflation.

In other words, while Mnuchin’s action may lead to an adverse impact for the broader economy, it is perversely stimulative for the markets. Or at least should be. Which is why today’s downbeat market response is – you guessed it – yet another dip buying opportunity for the army of 16-year-old Robinhood traders and/or Mnuchin’s immediate family which will be able to afford even bigger diamond rings.

Below we republish Ian Lyngen’s full note:

The opposing stances of Mnuchin and Powell on the extension of “the full suite” of bailout facilities has become the market’s primary focus as the weekend quickly approaches. Allowing the expiration of the corporate credit facilities (both primary and secondary) is the headline eyebrow raiser; however, ending the muni liquidity program and Main Street lending also present market disruption risks. We’re sympathetic to both sides of the argument; Powell advocates extending everything over year-end to ensure against dislocations whereas Mnuchin sees functioning in the credit and muni markets as sufficient and the monies would be better used as grants/bailouts. The question of ‘why not both continuing the facilities and providing further fiscal aid?’ falls well into the territory of the political and far afield from the tradition risk/reward calculations in financial markets. Alas, the fact of the matter remains that this debate is very much front and center as investors attempt to navigate the balance of 2020.

There is little question that this increases the probability that the Fed pushes forward with an extension of the WAM of QE purchases at the December 16 FOMC meeting. That said, it’s also incrementally encouraging that Mnuchin’s proposal includes the partial extension of the emergency facilities; perhaps leaving the door open (albeit slightly) for more flexibility with the remaining programs. Any further public comments on this issue in the coming days will allow investors a better sense of the balance of risks into the year-end turn. In the interim, it’s been impressive how limited price action has been in both US rates and global equities. To be fair, the bull flattening in Treasuries has been credited to the risk just such a scenario comes to fruition, thereby forcing the Fed’s hand via extending bond buying further out the curve.

We’re cautious of attempting to extract an overly bearish read on the fact Treasuries haven’t extended the bull flattening on the Mnuchin/Powell showdown, even if it’s tempting to put this episode in the crowded category of buy the rumor sell the fact in Treasury space. Simply concluding the issue has been ‘fully priced in’ at this stage is needlessly glib in light of the array of potential combinations of what programs ultimately get extended and how Congress chooses to utilize any freed up emergency funding. With all the caveats dutifully offered, it’s still encouraging that 10-year yields were unable to dip as low as 80 bp and appear to be stabilizing closer to 85 bp. This price action has occurred despite the building consensus that Fed action next month is much more likely than not and it will, by design flatten the curve and limit any decisive bear steepening.

This reality doesn’t entirely negate the underlying fundamentals that continue to support the potential for gradual upward pressure on yields further out the curve. That said, the prospects for a WAM extension in December and an outright increase in the size of bond buying beyond $80 bn/month at some further point if the situation warrants does limit the degree to which 10- and 30-year yields can back up over the next 12-18 months. This by no means takes 1-handle 10s off the table; in fact, incorporating more official buying further out the curve clears the proverbial deck for an attempt to price in a round of optimism for the year ahead.

It’s a no-data Friday with the overhang (can we stop calling it a benefit yet?) of working from home as the holidays rapidly approach. Cyber deals, coupon codes, free shipping, free returns, and that annoying little countdown clock that implies heavily discounted items are temporary aberrations rather than an initial misprice/overstock are much better positioned to occupy the market than the choppy price action and dueling policymaker headlines. Perhaps we’re just projecting… again. Nonetheless, the weekly closes in 10s and 30s will merit attention, if for no other reason than the technical implications as month-end and the holiday shortened week approaches.

Tactical Bias:

In addition to the unknown of any potential adjustments to the QE program that may be announced at the December 16 FOMC meeting, we’ve been contemplating what the next trend will be in terms of market moving developments over the next several quarters. At present, that designation rests squarely on the path of the pandemic, however as inoculation eventually proceeds and greater collective immunity develops, there will come a time when case counts fade as the timeliest tradable information. It is at this point we suspect the economic data will once again emerge as relevant for rates. Not necessarily as a function of Treasuries responding to the inherently backward looking information, but rather as an update on what hiring, wages, spending and inflation will look like the post-covid novel norm.

As has been exemplified by the collective disinterest in the fundamentals over the past few months, pre-second wave spending patterns are of little consequence when it comes to assessing what the world will look like once a vaccine becomes widely available and adopted.

We are of the mind regardless of the level of government restrictions, individuals will remain reluctant to resume spending in a fashion that was the norm in 2019. This means that presumably at some point in mid-2021, when vaccinations are widespread, the data will capture what growth and inflation – and thus Treasury yields – look like as the second half of the year unfolds and more information is in hand. An extension of the increase in goods spending would follow in such a world. Additionally supportive of this trend is a nuance surrounding the nature of consumption that has been deferred as a result of the pandemic.

Unlike goods spending, many service expenditures will not benefit from pent up demand that has accumulated over the period spent at home. Households will not double the amount of restaurant visits they make or move theater trips they take versus the levels that were the norm before Covid-19. Rather, a return to those levels seems to be a best case scenario given the lingering uncertainty, which in practical terms lengthens the time of the recovery and will ultimately limit the degree to which 10- and 30-year yields will be able to rise.

This doesn’t paint an especially uplifting outlook for the prospects for a trending market in US rates. Instead, the realities imply 1) the curve shape is little more than a directional trade, and 2) the duel between economic optimism and persistent headwinds will leave trading the extremes of the range as the most prudent strategy as the global economy slowly begins to emerge from the pandemic. There will continue to be sectors that are decided winners and losers; even if the prospects for a ‘relatively’ swift return to normal may ultimately save industries that might have been in greater jeopardy had lockdowns persisted for several years.

via ZeroHedge News https://ift.tt/333W7Bp Tyler Durden

Do you remember earlier this year when consumers were feverishly hoarding toilet paper and we were seeing colossal lines at food banks all over the nation during the initial stages of the COVID pandemic? Well, it is happening again. Now that the vote on November 3rd is behind us, the pandemic has once again become the primary focus of the mainstream media, and a lot of people are completely freaking out. Just like earlier this year, store shelves across the country are being emptied because Americans don’t want to be stuck at home without enough toilet paper and hand sanitizer. Each new restriction that gets announced adds to the frenzy, and it has gotten to the point where new restrictions are literally being announced around the nation on a daily basis now. And if the case numbers that we are being given continue to rise, it is inevitable that this new wave of lockdowns will get even tighter.

Over the last several months, Joe Biden has repeatedly told us that we have a “dark winter” ahead. Here is just one example…

“There is a need for bold action to fight this pandemic,” Biden said in Delaware. “We’re still facing a very dark winter.”

Biden, whose campaign against President Donald Trump made the coronavirus a main focus, pledged to “spare no effort to turn this pandemic around once we’re sworn in on Jan. 20.”

Technically, winter doesn’t start until a little over a month from now, but the panic shopping has already begun.

In California, supplies of toilet paper are being voraciously gobbled up by fearful consumers…

Shoppers in Temecula had already emptied the paper and cleaning aisle in a local Walmart by Wednesday morning. Other storefronts, such as Trader Joes in the Silverlake neighborhood of Los Angeles and Ralphs on West 9th Street, were simply running low on such supplies.

A worker at a Costco in Los Angeles, who wished to remain anonymous, said the store was selling out of toilet paper every day, among other supplies, but also said that this could be attributed to the Thanksgiving holiday coming up next week.

In a tweet on Sunday afternoon, KREM photojournalist Roger Hatcher said Target in Spokane Valley was “pretty quiet” but its toilet paper shelves were bare.

I don’t know why there is such a focus on toilet paper. To me, having enough food to eat for an extended period of time is much more of a priority, but when people get fearful they don’t necessarily think rationally.

And certainly there is a bit of psychology to all of this. When people are told that there is a “shortage” of something, many of them inevitably feel motivated to run out and buy some too while they still can. The panic buying has reached such a frenzy that many large chains are once again starting to put purchase limits on certain items. The following comes from CNN…

At Kroger (KR), customers can purchase a maximum of two items when it comes to products like bath tissue, paper towels, disinfecting wipes and hand soap. Giant, a grocery chain in the Northeast, recently put a limit of one on purchases of larger toilet paper and paper towel sizes and four on smaller toilet paper and paper towel sizes.

H-E-B in Texas has implemented similar policies in recent weeks. Some H-E-B stores have instituted limits of two on purchases of disinfecting and antibacterial sprays, while other stores have limited toilet paper and paper towels to two.

This is just one of the reasons why I have always encouraged my readers to get prepared in advance.

If you have a large family, how long is two packages of toilet paper going to last you?

You could try to stretch out your supplies by limiting family members to a certain number of squares per defecation, but you will still run out very quickly.

When you try to prepare for any emergency at the last minute, you are almost certainly going to fall short. One or two trips to the grocery store is not going to cut it, and anyone that thinks otherwise is simply being delusional.

Meanwhile, the decline in economic activity around the nation that is being caused by this new round of lockdowns is creating a renewed surge in economic desperation.

Just the other day I wrote about how some people were waiting in line for up to 12 hours to get handouts from a food bank in Texas, and on Wednesday it was being reported that “hundreds of cars” were lined up to get food in Miami…

Huge lines have been forming at a Florida food bank ahead of Thanksgiving and as the coronavirus pandemic worsened across the United States.

Hundreds of cars were spotted queuing for food boxes at Miami’s Gwen Cherry Park on Wednesday.

The boxes were being distributed by the Miami Marlins Foundation amid the ongoing COVID-19 pandemic that has forced thousands of Floridians out of work.

Sadly, the truth is that this is happening all over the nation, and this new round of lockdowns will continue to make things even worse as we head into 2021.

In so many instances, the people waiting in line at these food banks are wearing very nice clothes and are driving very nice vehicles. This severe economic downturn has come upon them very “suddenly”, but those that have been reading my books were warned in advance that this exact scenario was coming.

Even if this pandemic disappeared tomorrow, I would still believe that we have a “very dark winter” in front of us. If you have not prepared for the extremely challenging times that lie ahead, I would very strongly urge you to do so.

So far this year we have been hit by one major crisis after another, and the “perfect storm” that started in 2020 is only going to intensify during the coming months.

* * *

Michael’s new book entitled “Lost Prophecies Of The Future Of America” is now available in paperback and for the Kindle on Amazon.

via ZeroHedge News https://ift.tt/2UMObjI Tyler Durden

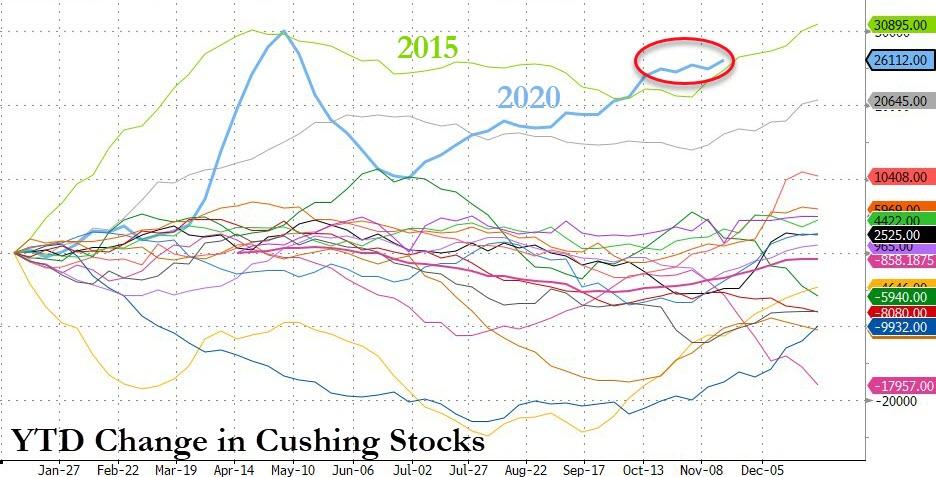

Cushing Crude Stocks Soar At Record Pace, Storage Hub Nears Capacity Tyler Durden

Fri, 11/20/2020 – 11:10

Despite optimism about a vaccine-driven return to normal, the glut in crude oil stocks is getting gluttier once again.

2020 has seen a record increase in stocks at Cushing and while COVID-lockdown Round 1 saw a bigger spike, this second COVID wave is forcing the energy complex into just as ‘glutty’ a situation as before…

Source: Bloomberg

In fact, stockpiles at Cushing, Oklahoma, the delivery point for West Texas Intermediate futures, stood at 61.6 million barrels as of Nov. 13, or about 81% of capacity, according to the most recent U.S. government data. That’s 3.83 million barrels shy of the levels seen in May.

Source: Bloomberg

As Bloomberg reports, though a repeat of the negative oil prices seen in April is unlikely, the mounting supply glut brings home how lockdown measures to contain the Covid-19 pandemic may soon force traders to store oil in every nook and cranny available, including ships and pipelines. Some are already doing that.

“Even as those facilities come back online, we are seeing excess inflows into Cushing overshadowing increased demand,” said Hillary Stevenson, a research director at Wood Mackenzie Ltd.

The reasons behind the buildup are similar to what happened before: Refineries are still coping with lackluster demand as coronavirus cases surge anew.

On top of that, some of them have also been undergoing seasonal maintenance.

This surge in crude stocks has added to the wild swings and speculation in the oil market as the two most influential developments have been Joe Biden’s victory in the U.S. presidential election and Pfizer’s vaccination breakthrough. Both of these events have the potential to significantly impact global oil markets. Then, as we at Primary Vision Network have been warning for months, the second wave of COVID-19 hit, and optimistic estimates of oil demand recovery collapsed.

While all of these events have impacted oil prices over the last few weeks, OilPrice.com’s Osama Rixvi notes that they will also have long-term consequences for oil markets. Joe Biden’s victory will have implications for both the Iran Deal and U.S. relations with China, while the second wave of COVID and vaccine success will significantly impact oil demand and, by extension, OPEC’s strategy in oil markets. Joe Biden’s win has the potential to transform geopolitical and economic policies that directly impact oil prices.

The Iran Deal, formally known as the JCPOA (Joint Plan of Action), is one of the most obvious areas to watch. Among many other promises, Biden has said he plans to “rejoin” the deal, which would involve lifting or easing sanctions on Iran. This would lead to some additional barrels of production from Iran and would directly impact the OPEC+ strategy. With Libyan production already returning and the UAE considering withdrawing from OPEC, an increase in Iranian production would put the fragile OPEC+ agreement under even more pressure. But with new elections scheduled in Iran in 2021, Biden may struggle to keep his promise of rejoining the deal.

Another key factor to watch, as I have highlighted many times, is the U.S.-China trade war. A Biden victory has the potential to ease tensions between these two giants and improve the global economic environment as well as boosting oil markets. It is important to mention here that China will not be able to fulfill its promise of buying an additional $200 billion of products from U.S. If Biden decides to honor the previous agreement and enforce the sanctions snapback clause that was included, the trade war would likely reignite and oil prices would suffer.

The final factor to watch in 2021 is COVID19, the single most important factor for oil markets. While the news of a vaccine did temporarily boost oil markets, there is a long way to go before we overcome the pandemic. A vaccine is going to be vital is we are going to return to a pre-pandemic oil market and economy. But even if the vaccination is effective, its affordability, acceptability, and availability are all key factors is how effective it is.

Moreover, due to the time needed to roll out the vaccine, we will continue to see lower demand for a good part of next year. While we are waiting for demand to recover, the OPEC+ agreement will be vital. The group is currently considering the possibility of extending the agreement for another three to six months. Saudi Arabia even said that the markets can expect additional cuts if required – altering the production cut agreement.

Sources: PVN

According to Mark Rossano of Primary Vision Network (PVN),

“the main issues in the crude markets these days, are:

1) Crude Storage dynamics both onshore/ offshore

2) Crude differentials that promote varying grades

3) The oversupply at the refiners causing economic run cuts making the demand situation worse.”

So while a Biden presidency may change the geopolitical factors at play and a COVID-19 vaccine is providing markets with hope, the oil market will need time to address its fundamental issues.

Biden may have some protectionist tendencies too as he has said he will propose to Federal agencies that they procure only U.S. goods and services. He has also proposed a tax on companies that move their production facilities and jobs outside the U.S. These tendencies alongside his stance on the Senkaku Islands may make it a little difficult for him to seek rapprochement with China.

For the rest of the year, market observers should closely monitor developments related to Iran, China, and COVID, there is no doubt that these will be the three major drivers of oil prices in 2021.

via ZeroHedge News https://ift.tt/2IWko58 Tyler Durden

Under 20% Of COVID-19 Infections Asymptomatic And Far Less Likely To Transmit Virus: Study Tyler Durden

Fri, 11/20/2020 – 10:50

Until now, evidence suggested that up to half of COVID-19 patients are asymptomatic “silent spreaders” of the disease who were unwittingly contributing to outbreaks. Some estimates even pegged the rate of asymptomatic infections as high as 81%.

Now, new evidence suggests that just 17% of those infected with COVID-19 will experience no symptoms, according to Nature, citing a meta-analysis of 13 studies published last month which involved 21,708 people. What’s more, asymptomatic individuals are 42% less likely to transmit the virus than those with symptoms.

The research, spearheaded by lead author Oyungerel Byambasuren of the Institute for Evidence-Based Healthcare at Bond University in Gold Coast, Australia, defined asymptomatic people as those who showed none of the key COVID-19 sysmptoms during the entire follow-up period. The authors only included studies which followed participants for at least seven days, as evidence suggests symptoms typically develop in 7-13 days (during which people are still contagious).

One reason that scientists want to know how frequently people without symptoms transmit the virus is because these infections largely go undetected. Testing in most countries is targeted at those with symptoms.

As part of a large population study in Geneva, Switzerland, researchers modelled viral spread among people living together. In a manuscript posted on medRxiv this month2, they report that the risk of an asymptomatic person passing the virus to others in their home is about one-quarter of the risk of transmission from a symptomatic person. –Nature

That said, the analysis acknowledges that while there is a lower risk of transmission among asymptomatics, they may still present a public health risk due to the fact that they are more likely to be out in the community vs. isolating at home, according to Switzerland-based infectious-disease specialist Andrew Azman of Johns Hopkins Bloomberg School of Public Health, a co-author on the study.

“The actual public-health burden of this massive pool of interacting ‘asymptomatics’ in the community probably suggests that a sizeable portion of transmission events are from asymptomatic transmissions,” he said.

Nature notes that other researchers disagree over the extent to which asymptomatic spread contributes to community transmission. ” Byambasuren, the lead author, says that if the studies are correct that asymptomatic people are a low transmission risk, “these people are not the secret drivers of this pandemic,” as they are “not coughing or sneezing as much” and are “probably not contaminating as much surfaces as other people.”

So, while the ‘silent spread’ factor appears to be far less pronounced than previously thought, and the virus kills less than 1% of those infected under the age of 60, one still has approximately a 10% chance of becoming a “long hauler” – an infected person who essentially suffers from waves of flu symptoms for months on end. Is that worth shutting down the economy over?

via ZeroHedge News https://ift.tt/394pVlg Tyler Durden

Former Secretary of State John Kerry attended a panel discussion at the World Economic Forum during which he asserted that a great reset was urgently needed to stop the rise of populism.

Kerry vowed that under a Biden administration, America would rejoin the job-killing Paris Climate Agreement but that this was “not enough.”

“The notion of a reset is more important than ever before,” Kerry said.

“I personally believe… we’re at the dawn of an extremely exciting time.”

The former Senator made it clear that this “reset,” which is merely a re-branding of the same new world order that has faced stiff resistance for the past two decades, is necessary to extinguish populism.

“I think Europe has to look at that with Brexit and the rising national populism – nationalistic populism,” said Kerry.

“Which is really one of the priorities that we all have to address. You can’t dismiss it.”

Speaking about how Trump increased his vote in 2020, Kerry noted, “What astounds me is that as many people still voted for the level of chaos and breach of law and order and breaking the standards and … I think that, the underlying reason for that is something that everybody has to examine.”

European Commission President Ursula von der Leyen also welcomed the prospect of Biden as a “friend in the White House” to the globalists and said the two entities would work on “a new rulebook for the digital economy and the digital society.”

“The need for global cooperation and this acceleration of change will both be drivers of the Great Reset. And I see this as an unprecedented opportunity,” said von der Leyen.

As we have exhaustively documented, “The Great Reset” is merely the latest incarnation of the agenda to centralize power into the hands of a tiny elite, disenfranchising Americans, lowering their living standards and forcing them to submit to a social credit score system that will eliminate all privacy and personal autonomy.

As we reported yesterday, legacy media outlets like the New York Times are still claiming the “Great Reset” is a “conspiracy theory” even as world leaders openly announce it.

For a full break down of what “The Great Reset” truly represents, watch the interview below.

In the age of mass Silicon Valley censorship It is crucial that we stay in touch. I need you to sign up for my free newsletter here. Also, I urgently need your financial support here.

via ZeroHedge News https://ift.tt/2UMDjSW Tyler Durden

Hedge Funds Go “All-In” As Bears Go Extinct: Shorts Drop To All Time Lows Tyler Durden

Fri, 11/20/2020 – 10:09

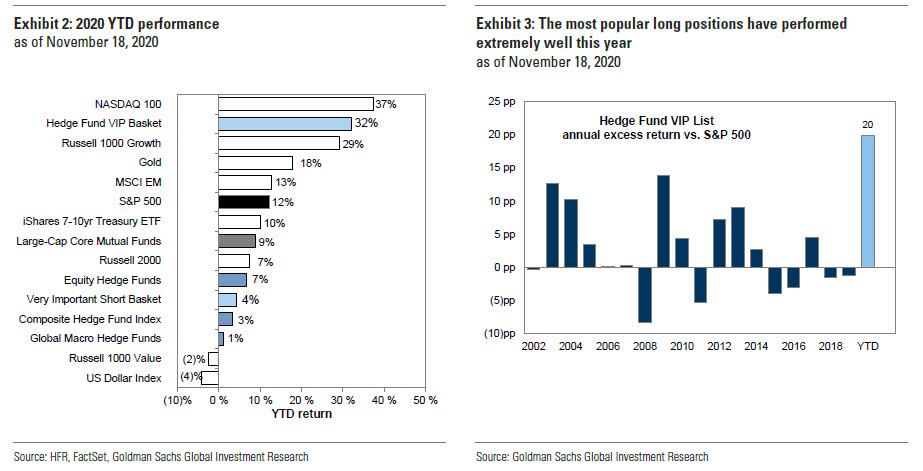

In recent weeks we have read one report after another from JPMorgan’s quants who, in trying to justify their explosive S&P forecast for 2021 and 2022 which sees the S&P rising as high as 4,500, make the false claim that hedge funds are barely invested in the market and have lots of dry powder, i.e., cash on the sidelines.

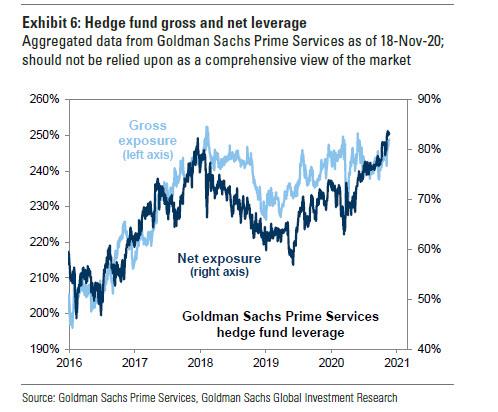

We now hope to bring these lies to an end once and for all, for the simple reason that as of this moment, hedge funds have never been more long stocks on both a gross and net basis.

The reason for that, as Goldman’s Ben Snider points out in its latest hedge fund trend monitor, is that in the third quarter having given up on generating alpha, hedge funds have “increasingly relied on beta to support returns.” Confirming this, Goldman’s Hedge Fund VIP basket, which tracks the most popular hedge fund long positions, has outperformed the S&P 500 by 20% points YTD (+32% vs. +12%). And while it still lags the Nasdaq 100, the basket is now on pace for its strongest annual excess return vs. the S&P 500 on record as shown in the second chart below.

As an aside, following the recent 15-sigma rotation out of growth and into value on the back of vaccine news, Goldman caveats that in recent weeks, the outperformance of the most popular hedge fund long positions has moderated. Since the start of the fourth quarter, VIPs have outperformed the S&P 500 by about 2 percentage points (+8% vs. +6%), as the US elections and vaccine announcements drove sharp rotations within the market.

Ironically, and as we have claimed since 2013, the biggest outperformance came on the back of soaring shorts: as Snider writes in his report, “since the market trough in March the most concentrated short positions have consistently outperformed as funds covered their short exposures in a rapidly rising market.“

Sadly, hedge funds once again were not aware of this, and even as they went long the hedge fund VIP basket which has soared, they were collectively short (as a group) the same handful of names, which has ripped higher, in many cases more than offsetting any gains from the long book.

As a result, hedge funds have resorted once again to the oldest trick in the book – piling leverage upon leverage to chase not alpha, which they have failed to do once again in 2020, but beta.

Indeed, as Goldman notes, “record net leverage has supported hedge fund returns in recent weeks despite the erosion of alpha.”

And here is our – and Goldman’s counter – to anyone who incorrectly claims that hedge funds are not all in: aggregate hedge fund net leverage calculated based on publicly-available data registered 56% at the start of 4Q 2020, tying the record from early 2015. Exposures calculated by Goldman Sachs Prime Services also show extremely elevated net leverage; in fact net leverage has never been higher: as Snider explains: “According to their data, net leverage has risen quickly since the March market trough and is now at the highest level on record.”

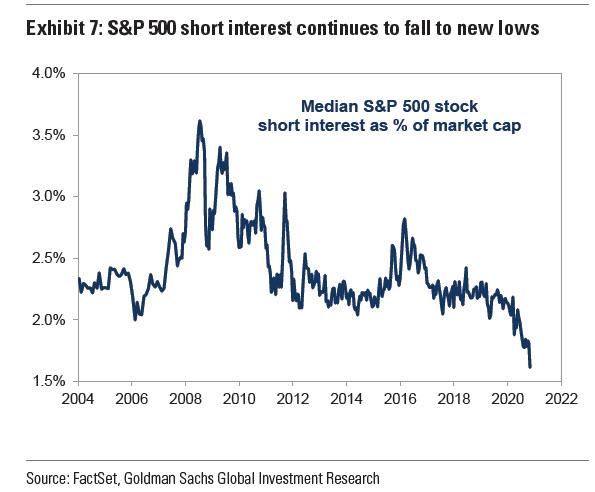

The flipside to the above is that that now that shorts have been absolutely crushed and steamrolled, there are none left.

As Goldman points out, as funds increased length in the rising market (i.e., covered their shorts), “short interest has continued to fall, reaching new record lows.” As shown in the final chart, the median S&P 500 stock has outstanding short interest equating to just 1.6% of market cap, the lowest level in Goldman’s 16-year data history.

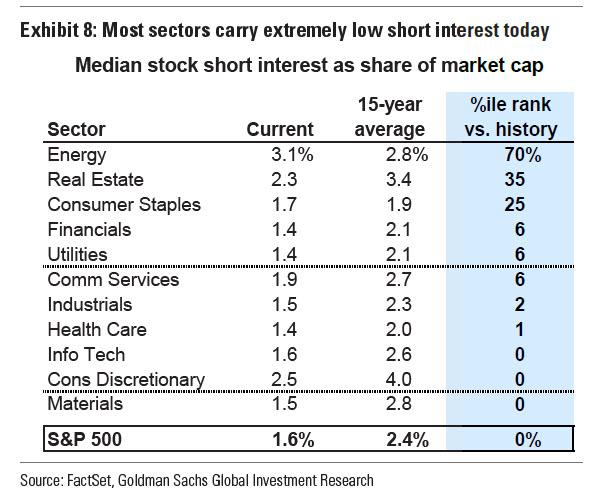

In most sectors, short interest outstanding currently ranks in the bottom decile of the last 15 years, with only Energy sector shorts registering above the historical average.

This means that with no shorts left, the market’s ability to “squeeze” higher is now finished… except for energy where we expect some catalyst to unleash what will soon be the only short squeeze left in the market.

via ZeroHedge News https://ift.tt/390ADJr Tyler Durden

“There’s Plenty Of Firepower Left” – Mnuchin Defends Decision To End Fed’s Emergency Lending Programs Tyler Durden

Fri, 11/20/2020 – 09:50

After the mainstream press accused the Trump Administration of trying to “sabotage” the Biden Administration by closing out a handful of Fed lending programs that were seeded with money from the Treasury earlier this year, Secretary Mnuchin appeared on CNBC Friday morning for a lengthy phone interview with Jim Cramer.

The secretary defended the decision as “a very simple thing” and pointed out the irony that Democrats had initially been skeptical of “giving me $500 million to do with whatever I want”. The program has been “a great success story”, he said. Now it’s time for the money to come back, as Congress intended, he said.

“This has been an incredible success. Let’s not focus on a couple of facilities that were hardly used,” Mnuchin insisted. He also claimed that markets “should be very comfortable” with the amount of ammo the Fed has in reserve.

“Markets should be very comfortable that we have plenty of capacity left,” the Treasury secretary said.

“This is not a political issue,” he added

When pressed by Cramer & Co. about whether his decision to recall the funds was tantamount to shooting Jerome Powell in the back, Mnuchin insisted that he was simply following the process set out in the law, and that the money from these Fed lending programs could be put to better use by making loans to small businesses.

“The intent was this part of it expires in December, let’s go use this money in parts of the economy that need it. We don’t need this money to buy corporate bonds. We need this money to help small businesses that have been hurt, through no fault of their own.”

“The medical emergency may not be over but the financial conditions are in great shape…corporate bonds have come in…mortgages have come in…the stock market has rebounded. I’m hoping that since we’ve been such an effective steward of these tools…that Congress” won’t hesitate to authorize similar programs in the future.

While urging Democrats to come together with the GOP like they did in the spring to pass another round of stimulus measures, Mnuchin revealed that he would meet with White House Chief of Staff Mark Meadows and Senate leader Mitch McConnell. When asked about reaching out to the Dems, Mnuchin said he planned to reach out to Democratic Congressional leaders.

As we reported last night, Mnuchin requested the expiration of the Primary Market Corporate Credit Facility, the Secondary Market Corporate Credit Facility, the Municipal Lending Facility, the Main Street Lending Program, and the Term Asset-Backed Securities Loan Facility by December 31. At the same time, he wants the Commercial Paper Funding Facility, the Money Market Mutual Fund Liquidity Facility, the Primary Dealer Credit Facility, and the Paycheck Protection Program Liquidity Facility be kept in place for an additional 90 days. The Fed responded with a statement claiming it would “prefer” that “the full suite” of measures designed to combat COVID’s impact on the economy be left intact.

When the interviewer pointed out that the next few weeks could be “really ugly,” Mnuchin replied that the administration had shifted its focus from the economy to vaccines, which he said should become available to the first patients in a matter of weeks.

When it comes to negotiations with the Democrats on another stimulus package, the secretary said he would be “redoubling our efforts” to strike a deal, unleashing more optimistic headlines in another effort to pump stocks.

“I had hoped now that we’re past the election that the Democrats will work with us…during the CARES act we had incredible bipartisan support…we’ll be redoubling our efforts to try and get something done.”

When Jim Cramer quoted the NYT which accused Mnuchin of trying to sabotage the upcoming Biden administration, Mnuchin insisted that “what we’re trying to do is follow the law as we’re supposed to…[the program] has been a great success…let’s get it done.”

Asked about his willingness to work with his possible successor, Mnuchin said he would be happy to work with whoever once the certification process related to deciding the official President-Elect is finished.

“There’s a process to certify, and once this is certified of course we will work with whoever we need to work with,” Mnuchin insisted. Asked whether he would be “happy” if former Fed chairwoman Janet Yellen is picked as his successor, Mnuchin demurred, saying it wouldn’t be right for him to comment on the issue…but insisted that he would work with whoever is picked, after the results are made official.

Looking ahead, White House Press Secretary Kayleigh McEnany will hold her first press briefing since the election on Friday at noon. Meanwhile, the torrent of critical op-eds continued, with CNBC publishing a piece of commentary accusing Mnuchin of “removing the life boats from the Titanic”.

Mnuchin’s Fed move is like stripping Titanic of its lifeboats, economist says https://t.co/C7FC79hUoQ