Short Lines Greet Latest iPhone Release In China Tyler Durden

Fri, 10/23/2020 – 12:19

Apple shares slid Friday morning after the release of two iPhone 12 models that went on sale in China earlier in the day. From Shanghai to Beijing, Apple stores saw low-turnout on launch day, due mostly because of the shift to online ordering.

Early preordering of Apple’s new 5G-enabled smartphones had a strong online response by consumers in a post-pandemic world. Unlike some Americans, the Chinese appear smart enough not to gather in long lines as flare-ups of the virus pandemic are being reported in many parts of the world.

Reuters reports Apple stores in Shanghai had limited turnout, while CNN reports stores in Beijing’s Wangfujing neighborhood had “no line out the door as there had been on previous launch days.”

Less than two dozen people waited at a store in Shanghai. One Apple customer told Reuters:

“I feel great being the first customer to get the new iPhone,” said Yan Bingqing, 30, who arrived before the store opened, and was in a line of about 20 people.

The virus pandemic has transformed how consumers shop. On Friday, China’s social media networks had top trending topics related to the new iPhone. JD.Com, a leading Chinese electronic reseller, said more than 500,000 preorders for the iPhone 12 Pro had been seen since last Friday.

Overall, Apple’s announcement a week and a half ago for the new iPhone drew mixed reviews according to a Caijing magazine poll. While 10,000 of those polled voted they would not buy the new iPhone, 9,269 said yes, and 5,400 said they were uncertain.

Some Chinese customers said the iPhone is too expensive, considering it doesn’t come with headphones or a power adapter. There’s also a concern of rising nationalism in the country; as Sino-US relations continue to deteriorate, the Chinese have been gravitating towards domestic brands.

The release of Apple’s 5G-enabled smartphone is more than one year late compared to Huawei’s 5G phone, the Huawei Mate 20 X 5G, launch in summer 2019.

“From the bottom of my heart, it’s a little bit late for Apple to release the 5G iPhone,” Zhu Lin, another Apple fan, who waited in a small line in Shanghai, told Reuters. “I was expecting it last year.”

Recently, research firm Canalys increased its forecast for Chinese iPhone shipments for the fourth quarter to 14% year-on-year growth — from the original 1% decrease.

via ZeroHedge News https://ift.tt/3onqpYT Tyler Durden

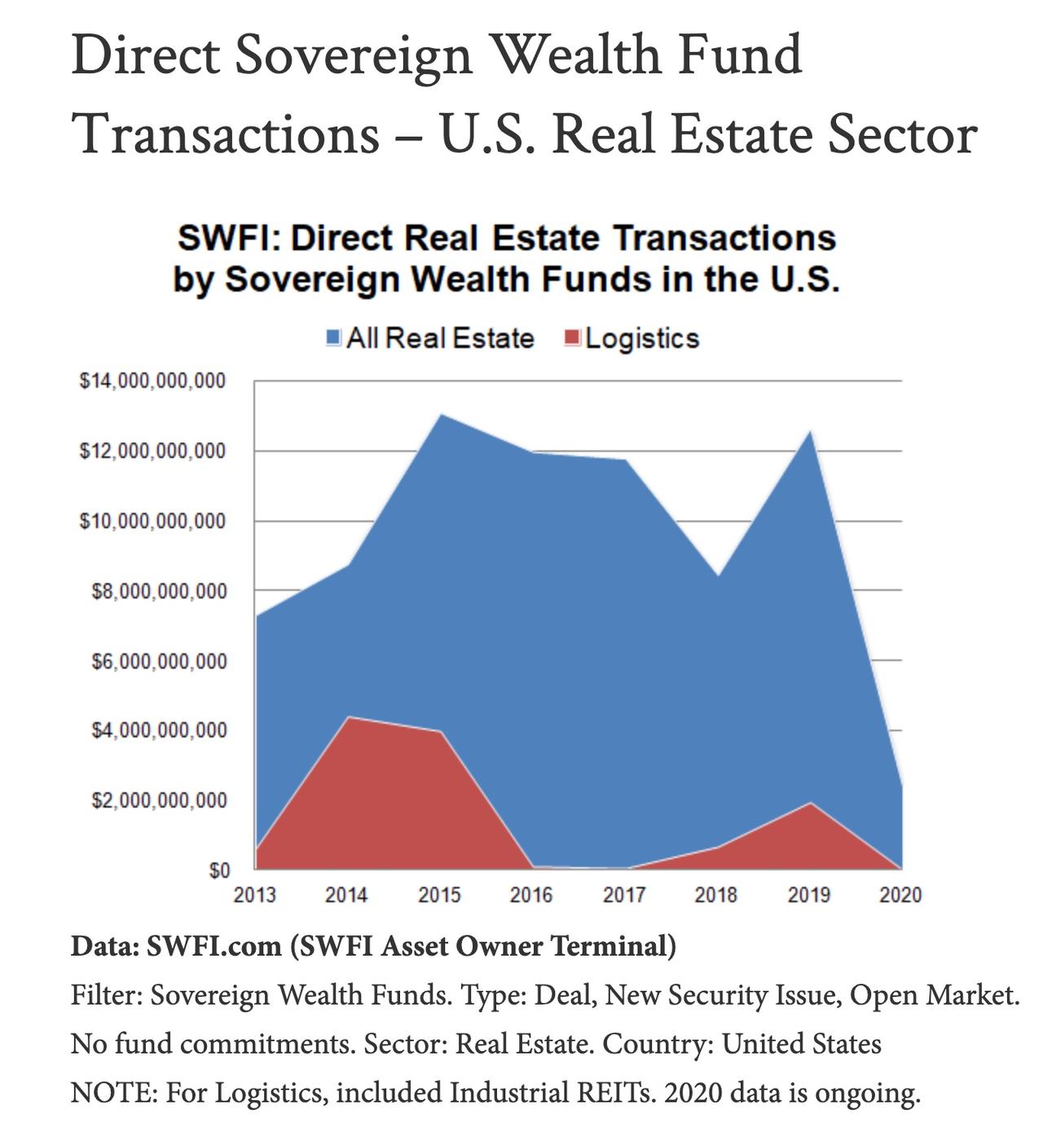

Sovereign Wealth Funds Forestall Real-Estate Investments As COVID-19 Pandemic Bites Tyler Durden

Fri, 10/23/2020 – 11:55

President Trump elicited jeers from New York City’s remaining residents Thursday night when he called their city a “ghost town” during a lengthy riff on the myriad problems created by COVID-19-inspired lockdowns. But a mountain of data shows that Manhattan rents and property prices have tumbled to their most affordable levels in years.

But even more so than residential real estate, commercial real estate has taken a huge hit in the months since the outbreak, as office head counts dwindled and once thriving commercial areas in places like London became veritable ghost towns, so much so that the British government briefly encouraged finance types to return to their offices in Canary Wharf as the shops that depended on their foot traffic struggled.

But on the high end of the CRE market, sovereign wealth funds, which have been an active buyer of real estate in cities around the world, but especially in places like New York City and London, likely won’t be making a return any time soon.

A blog post from the Sovereign Wealth Fund Institute offers more details below:

Direct Sovereign Wealth Fund Transactions – U.S. Real Estate Sector

Filter: Sovereign Wealth Funds. Type: Deal, New Security Issue, Open Market. No fund commitments. Sector: Real Estate. Country: United States

NOTE: For Logistics, included Industrial REITs. 2020 data is ongoing.

The coronavirus pandemic that swept across America in February and March 2020 had a material impact on direct real estate investing by sovereign wealth funds. Cash-rich sovereign investors were paralyzed in their direct investments during this time period, compared to previous years of annual growth in direct property allocations. Sovereign investors are cautious on catching a falling knife in the office and residential real estate sectors, versus the logistics sector – a key beneficiary of the e-commerce theme. A notable deal in 2020, includes GIC Private Limited’s type up with Bill Gates’ Cascade Investment, L.L.C. in becoming major investors in Columbia, Missouri-based StorageMart.

Pre-pandemic, a cadre of Asian and Gulf sovereign funds were active in a wide range of property assets in the United States. For example, on December 12, 2019, Singapore’s GIC Private Limited and NYSE-listed real estate investment trust RPT Realty formed a US$ 244 million retail joint venture. GIC spent US$ 118.3 million to purchase a 48.5% stake in five retail assets in Florida, Missouri, and Michigan and committed up to US$ 200 million of additional capital to the venture for future deals. In the same season in 2019, Marriott International Inc. sold the St. Regis New York for US$ 310 million to the Qatar Investment Authority (QIA).

Furthermore, direct deals in European properties by sovereign wealth investors has come to a near halt compared to other years.

via ZeroHedge News https://ift.tt/35pJKjv Tyler Durden

Stocks Slide To Session Lows After White House Says “Pelosi Making Deal Harter By Not Budging One Inch” Tyler Durden

Fri, 10/23/2020 – 11:30

In the day’s first obligatory round of fiscal stimulus jawboning which just serves to justify why neither party will budge on a deal ahead of the elections despite pretending to “work hard” to get a deal, we first had House Speaker Nancy Pelosi saying on MSNBC that a stimulus bill “can be passed before the Nov. 3 election if President Trump cooperates”, before hedging that Trump has been “back and forth” on a deal, adding he needs to bring around Senate Republicans to back any agreement in the first fingerpointing of the day. Still, she concluded that “the president wants a bill, I really do.”

In response, the White House immediately countered with Press Secretary McEnany saying Pelosi is making it harder by not budging “even one inch” on her stimulus demands.

The market read between the lines, realized that the constant back and forth means no deal is coming, and hammered both the S&P…

… and the Nasdaq.

via ZeroHedge News https://ift.tt/2Hw8huU Tyler Durden

The Bill From MMT: Higher Taxes, More Austerity, Rising Inflation Or Eventual Default Tyler Durden

Fri, 10/23/2020 – 11:20

By Stephen King, HSBC’s Senior Economic Adviser and author of ‘Grave New World’, originally published in the FT,

In a world in which government debt is rapidly rising, it’s hardly surprising that there’s growing interest among investors in Modern Monetary Theory. After all, one of its central claims is that budget deficits are, from a financing perspective, an irrelevance. So long as increased government borrowing doesn’t lead to inflation — and, at the moment, there really isn’t much of it around — we can all afford to relax.

As Stephanie Kelton notes in her book The Deficit Myth, governments with access to a printing press are “currency issuers” (exceptions include, most obviously, members of the eurozone). As such, all their spending could, in principle, be financed via the creation of cash. Taxes may serve other purposes — the redistribution of income and wealth, the discouragement of “sinful” behaviour — but, in the world of MMT, they serve no useful macroeconomic role.

In the real world, however, taxes are crucial. The fundamental difference between government finances and those of companies and households is not access to a printing press but, instead, the coercive power to raise taxes. A company making a severe loss cannot reduce that loss by imposing taxes on everyone else. A government can. A worker receiving a pay cut cannot force others to make up the difference. A government can.

Armed with this knowledge, creditors are understandably willing to accept mostly lower returns on government bonds than on other investments. Put simply, the risk of government default in the face of an adverse economic shock is lower than for other would-be borrowers.

Admittedly, there are limits, dictated largely by the political capacity of a government to raise revenues in difficult circumstances. Emerging markets often end up resorting instead to devaluation, default or inflation. In anticipation, borrowing costs spike.

Still, imagine for a moment that governments embrace MMT. Imagine too, as MMT proponents suggest, that control of the printing press is taken away from unelected central bankers and given to “accountable” elected fiscal representatives. Would we be any better off?

Far from it. Giving elected representatives the keys to the printing press is the equivalent of giving a gambling addict the keys to the casino. For many politicians, the primary objective is to remain in power. As such, they will too often be incentivized to pursue instant gratification at the expense of longer-term stability. In the early-1970s, the UK embarked on what became known as the “Barber boom”, thanks to the efforts of Conservative chancellor of the exchequer Anthony Barber to engineer an election victory in 1974. As it turned out, the Tories lost and, two years later, the UK ignominiously had to accept a bailout from the IMF. Central bank independence provides a useful bulwark against such behavior.

More importantly, inflation and taxes are, in many ways, simply two sides of the same coin. Those governments without access to tax revenues can instead “debase the coinage”. Supporters of MMT claim this will never happen, yet history suggests otherwise: after all, it has been a tried and tested policy of kings and queens over hundreds of years. Too often, those with access to the printing press are prepared to take undue risks in the hope that “this time it’s different”.

In truth, inflation helps solve the financing issues that proponents of MMT claim no longer exist. Negative real interest rates, a result of higher-than-anticipated inflation, serve to redistribute wealth away from private creditors (pensioners, for example) to public debtors. Much the same could be achieved through a wealth tax. At this point, we come full circle: the distinction between the printing press and taxes begins to break down.

Thanks to Covid-19, government debt is rising rapidly and, for that matter, appropriately. In the face of recurring lockdowns, we are better off allowing companies and workers to enter a period of economic “hibernation” in the hope that, once the virus is under control, they can thaw out. The alternative of multiple business failures and mass unemployment is of no use to anyone. In the process, however, we are in effect borrowing from our collective economic futures. At some point, some of us will be presented with a bill which, if hibernation policies succeed, we will be in a reasonable position to pay. The political process will decide whether that bill comes in the form of higher taxes, more austerity, rising inflation or eventual default. That, I’m afraid, is the deficit reality.

via ZeroHedge News https://ift.tt/3ojZb5A Tyler Durden

There Is A New “Biggest Risk On Wall Street”, And This Is How Some Are Trading It Tyler Durden

Fri, 10/23/2020 – 11:04

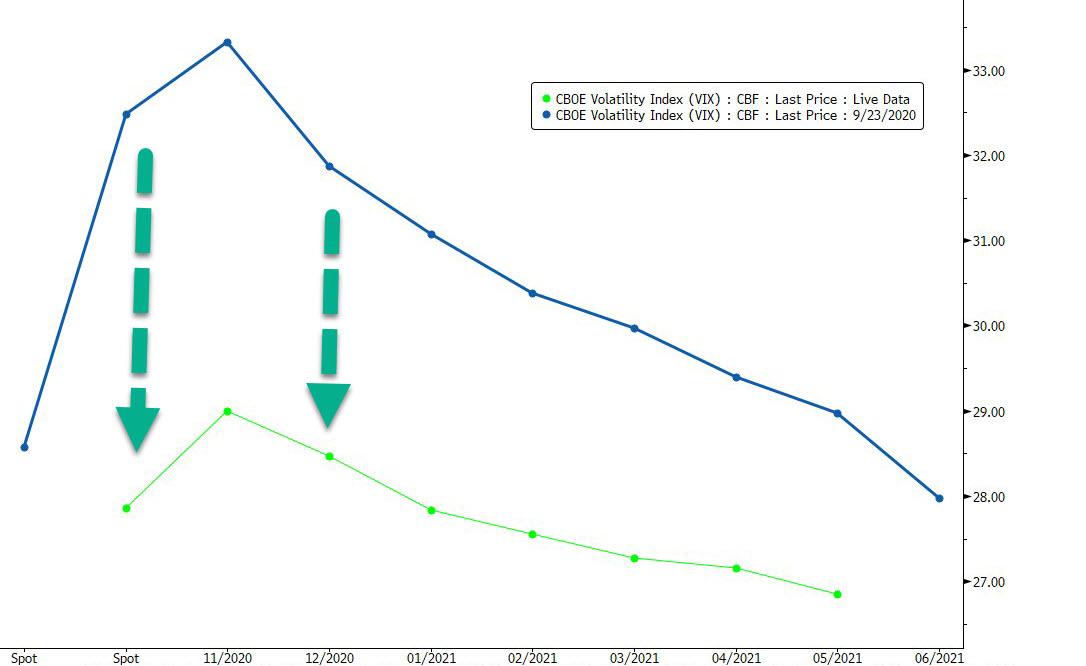

Exactly one month ago, Nomura’s Charlie McElligott suggested that the market was too skittish heading into the election, and that contrary to expectations of a contested outcome, the “risk” for consensus positions was that the kink in the VIX term structure that had emerged around the Nov 3 event would collapse, should there be a decisive outcome on or around Nov 3.

As a result, the Nomura quant concluded that “that some brave vol traders will try to take advantage as a perceived “generational” opportunity to sell this POST-NOV election “richness” (Dec / Jan) – could be a career “maker or breaker,” with the potential to see monster returns if the event were to pass and all that crash is puked back into the ether“, although he also hedged by warning that the opposite could just as easy happen and said returns could “conversely be turned to dust into a God-forbid realization of chaos, with civil disorder, dual claims to the throne etc.”

One look at the shift in the VIX term structure over the past month shows that McElligott has been spot on as implied vol has shrunk considerably across the curve.

Fast forward to today when McElligott follows up on these observations writing that as he had anticipated for the past month, “the consensual buy-in to the ‘election worst case scenario’ meme and thinking calamity could be pushed out post the calendar event and into Dec / Jan (in addition to the likely Dealer dynamic, where in light of the recent March vol shock, Risk Mgmt wouldn’t really allow for anybody to be meaningfully “short crash”) meant creation of an ‘overhedged’ vol dynamic that frankly would require tremendous and SUSTAINED daily market moves in order to realize what was being priced-into markets.”

In other words, the market has continued to anticipate sharp moves in vol even as implied vol has contracted, resulting in big pain for all those who were long the VIX across the curve.

So now that we have seen much of the post election kink/premium begin to soften (see chart above), with more traders now aligning with McElligott in thinking there is potential for a much cleaner election outcome, and as some of that “crash” hedge is then unwound back into the market, the Nomura x-asset strategist writes that “there is a mechanical catalyst for a melt-up into YE (even though there is absolutely still “gamma event” risk between now and then)—thus a lot of folks pushing these VIX 1×2 Put Spreads trading in the market, looking to put this on as their “short vol” trade expression to capture a melt-up.“

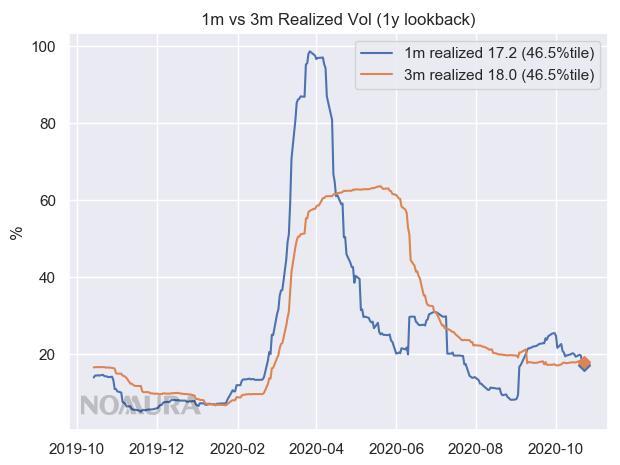

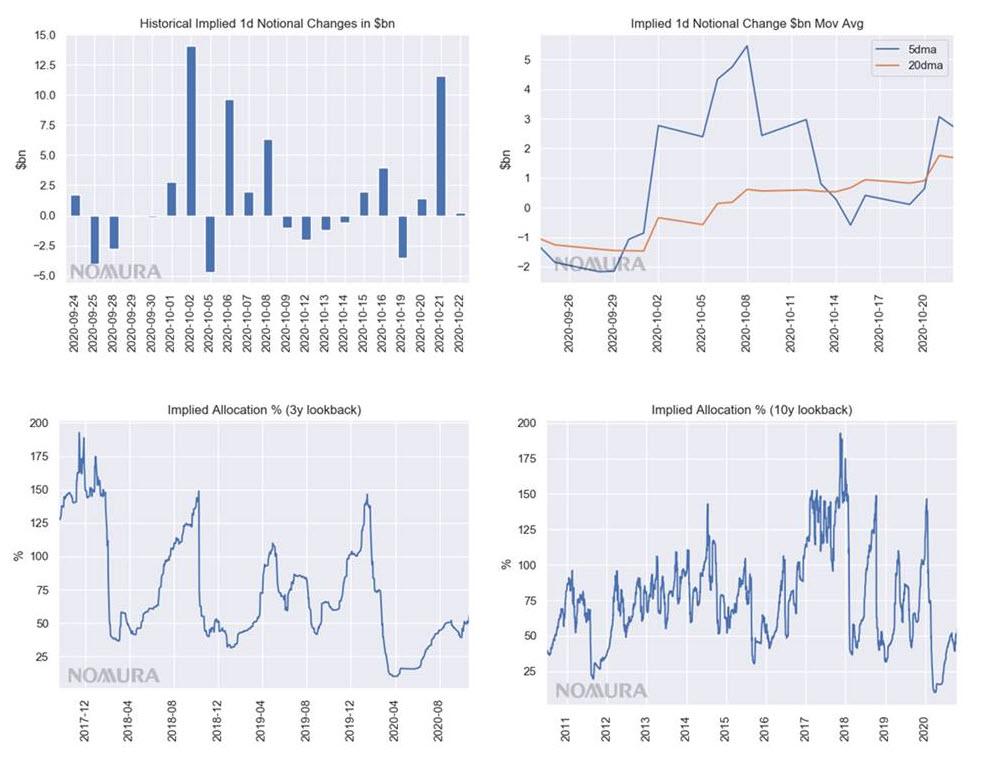

As McElligott then adds, this melt-up scenario gets even more interesting when looking at the recent directional shifts of Nomura’s Vol Control model, which after being a massive and latent buyer to the tune of $90-$100 billion after central banks and governments globally unleashed unprecedented monetary and fiscal policy easing, “then saw the summer vol event in the Equities space dictate a spike in realized, which then meant reversal of part of those prior flows, selling ~ $30B at one point during the past two or so months.“

But now that the previously elevated VIX is sinking again, thanks to the recent “calm”, it has allowed 1-month realized vol (the recent vol input trigger) to average down under the weight of the Aug/Sep blast, which makes 3-month realized vol the new trigger input according to Charlie, as it is the max of the two lookback windows. It is this easing in the VIX term structure that has meant “a recent blast of BUYING per the VC model over 5 of the past 6 sessions (+$13.7B in 5d) which is helping stabilize market against headline shock potentials.“

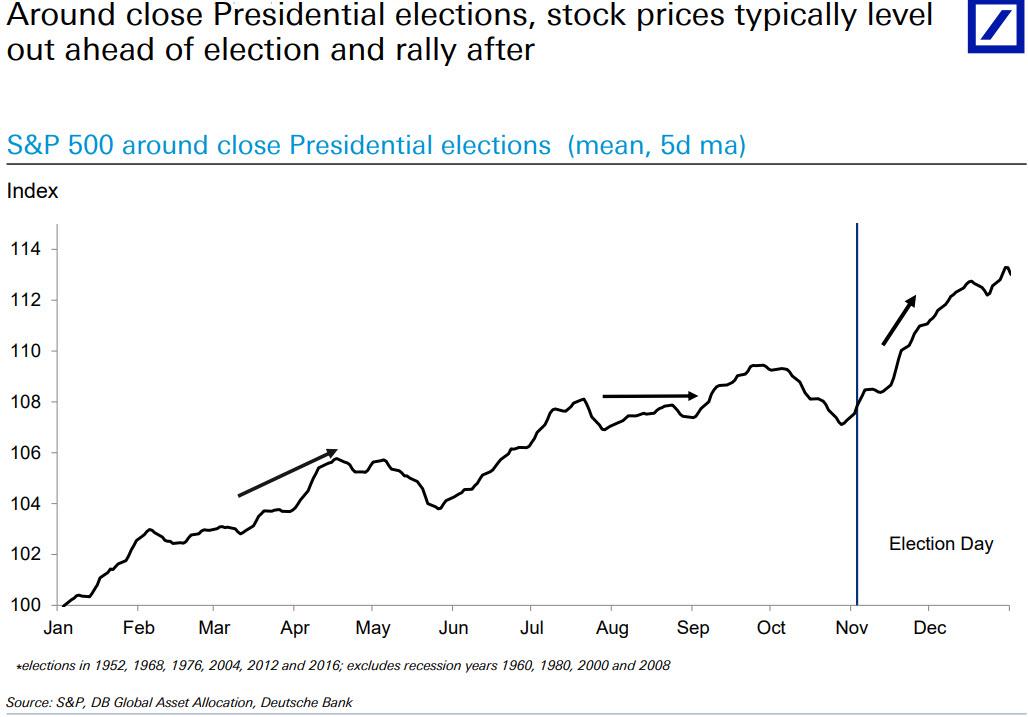

This in addition to all the previously discussed option-linked reasons why the market could blast off higher into year end, in addition of course to the seasonals which heavily skew toward market upside post-election day as the following chart from Deutsche Bank shows:

According to McElligott, the caveat means that the largest risk for the market, which is rapidly reversing its “contested election” bearishness, is this: “NO stimulus between now and the new administration taking-over, which then gets really complicated if the Senate stays Republican as well, who are then emboldened to act as the last line of defense into the Dem House and WH and act as a thorn in their “fiscal largesse” policy plans.”

This, the Nomura quant concludes, is why treasury flattening expressions need to be looked at as hedges for the above “tail” which markets are not priced-for, “because everybody is “set-up” for the bear-steepening/pro-cyclical fiscal stim + deficit spend + infrastructure + vaccine RECOVERY trade.”

This incidentally is also the topic of a Bloomberg article from yesterday, which looks at the market “certainly” that Trump is going to lose the U.S. election next month and his Republican Party may even fail to keep the Senate, and points out “that traders have been burned betting the house on one side before, such as in the last U.S. presidential election in 2016 and the Brexit referendum the same year. The risk that the consensus for a Democratic sweep of power this time doesn’t play out, or the result being contested, is leading some to take no chances with less than two weeks until the Nov. 3 vote.”

As Bloomberg notes, the market’s view has shifted in recent months from worries about a contested election that would spur volatility, to bets on a solid win for Democrat Joe Biden as the polls consolidate in his favor. That has pushed up Treasury yields along with U.S. stocks on the prospect that a Biden administration would usher in bigger fiscal stimulus, especially if the Democrats take the Senate.

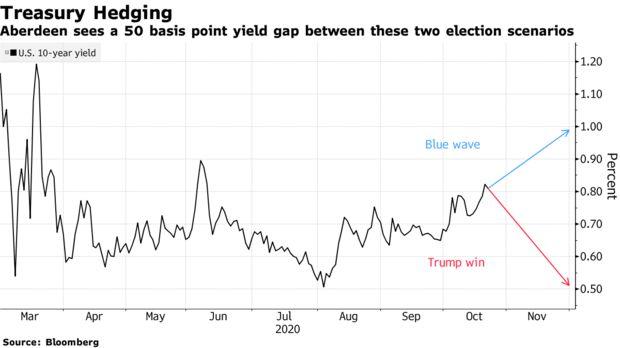

As a result, at least one trader is following the McElligott playbook and loading up on TSYs (and a curve flattener) if the market is once again terribly wrong:

James Athey, a money manager for Aberdeen Standard Investments, has loaded up on Treasuries and has a long position in the dollar and the yen versus riskier currencies such as South Africa’s rand. That’s because he expects these to benefit in the event of a surprise.

“I see a very real chance that the incumbent wins,” he said, looking at social-media sentiment indicators as well as changes in party registrations, both observations we showed first (here and here). “Both suggest more Republican support than the polls.”

Manulife portfolio manager Chris Chapman is another who believes the risk of a delayed outcome is underpriced in the market. He has now reduced his underweight position on 30-year Treasuries to reflect that view.

“For us, duration would be the primary hedge for a contested election, and probably some dollar strength,” said Chapman. “The risk of a contested election does seem to be diminished but the market is probably a little ahead of itself with the blue wave consensus.”

One final point: with a absolutely staggering, and record, number of shorts piling on the long-end, a Nov 3 surprise either in the presidency or the Senate which takes a massive fiscal stimulus off the table and which sparks bond buying and curve flattening, could quite literally result in the biggest bond short squeeze ever.

via ZeroHedge News https://ift.tt/35vBfDw Tyler Durden

This is not the first time I’ve relayed this information. But these days I believe it’s more important than ever to remind readers of its significance, especially in light of the unprecedented credit creation the Fed’s been conducting since March.

Following the Panic of 1907, John Pierpont Morgan was called to testify before Congress in 1912 on the subject of Wall Street manipulations and what was then called the “money trust” or banking monopoly of J. P. Morgan & Co.

In the course of his testimony, Morgan made one of the most profound and lasting remarks in the history of finance.

In reply to questions from the congressional committee staff attorney, Samuel Untermyer, the following dialogue ensued as recorded in the Congressional Record.Untermyer:

I want to ask you a few questions bearing on the subject that you have touched upon this morning, as to the control of money. The control of credit involves a control of money, does it not?

Morgan: A control of credit? No.

Untermyer: But the basis of banking is credit, is it not?

Morgan: Not always. That is an evidence of banking, but it is not the money itself. Money is gold, and nothing else.

Morgan’s observation that “Money is gold, and nothing else,” was right in two respects.

The first and most obvious is that gold is a form of money. The second and more subtle point, revealed in the phrase, “and nothing else,” was that other instruments purporting to be money were really forms of credit unless they were redeemable into physical gold.

So much of the gold market is “paper gold,” not actual gold. This paper gold market is so manipulated, we no longer have to speculate about it. It’s very well documented.

I don’t want to get too deep in the weeds here. But gold leasing is often conducted through an unaccountable intermediary called the Bank for International Settlements (BIS).

Historically, the BIS has been used as a major channel for manipulating the gold market and for conducting sales of gold between central banks and commercial banks.

The BIS is the ideal venue for central banks to manipulate the global financial markets, including gold, with complete nontransparency.

But the entire scheme rests on a tiny base of physical gold. I describe the market as an inverted period with a little bit of gold at the bottom and a big inverted pyramid of paper gold resting on top.

There’s just not that much gold available. But in the paper gold market, there’s no limit on size, so anything goes.

Leasing of paper gold by bullion banks allows them to sell the same gold as much as 10 times over to 10 different buyers. It’s like a game of musical chairs, only with more participants and fewer chairs.

Problems have turned up lately in this market because investors have shown up and said “I want my gold, please,” and the custodian has been challenged to meet all those calls for redemption.

But what if a major institution wants its gold but can’t get it?

That would be a shock wave. It would set off panic buying in gold, driving prices through the roof.

Meanwhile, the physical fundamentals are stronger than ever for gold. Set aside the COVID-related issues for now.

It appears that peak gold production is already here. There are no new gold fields of any significance waiting to be discovered.

There is no new technology that can extract gold from places where it cannot now be recovered. This does not mean gold production stops — just that output does not increase and will start to go down.

Gold exists in minute quantities in everything from seawater to distant asteroids, but the costs of recovery from those sources are astronomical and make no commercial sense.

When it comes to gold, what you see is what you get.

Yet global demand continues to rise from central banks and sovereign wealth funds around the world. With limited output but massive ongoing demand, it’s only a matter of time before a link in the physical gold delivery chain truly snaps and a full-scale buying panic erupts. We could be very close to that now.

You don’t need a Ph.D. to realize that if supply is declining and demand is increasing, then gold prices have nowhere to go but up.

Meanwhile, the Fed has made perfectly clear that it won’t be raising rates for years and is committed to inflation, whatever it takes. It’s hard to imagine a better long-term environment for gold.

If you don’t have gold yet, what are you waiting for?

via ZeroHedge News https://ift.tt/3dSXM10 Tyler Durden

Swing Voters Give Debate Win To Trump: LA Times Panel Tyler Durden

Fri, 10/23/2020 – 10:20

A LA Times panel of 14 undecided voters conducted by Pollster Frank Luntz – most recently in the news for a leaked email exchange with Hunter Biden – thought that during Thursday night’s debate, President Trump was ‘controlled, reserved, poised, con artist and surprisingly presidential,’ while former Vice President Joe Biden came off as ‘vague, unspecific, elusive, defensive and grandfatherly.’

My focus group’s words to describe Trump tonight:

• “Controlled”

• “Reserved”

• “Poised”

• “Con artist”

• “Surprisingly presidential”

Words to describe Biden tonight:

• “Vague”

• “Unspecific”

• “Elusive”

• “Defensive”

• “Grandfatherly”

While all participants felt more disheartened after the debate than inspired, all but two said they would vote for Trump, with one going for Biden and another saying they might not vote at all.

“I am leaning more toward Trump now, however I still don’t feel like I have good answers on the race issues and that’s a very, very important issue to me in this country right now,” said one participant.

“In the mind of the undecided voters, Trump won,” Luntz told CNBC‘s “Squawk Box” following the debate. “But he did not win by a significant margin. It’s not going to change any votes.”

The focus group also wants to know more about Hunter Biden’s laptop. Only two people said they don’t care and they are “annoyed that we’re wasting time on it,” according to RealClearPolitics.

Luntz said that while Trump won the debate, he’ll lose the election.

“You got to give Trump a minor victory because he’ll bring some [undecided] voters home, and it’ll close the race a little bit. But in the end, I think Joe Biden won the war,” said the pollster, who said that even if polls are wrong as they were in 2016, it’s “virtually impossible” for Trump to win at this point.

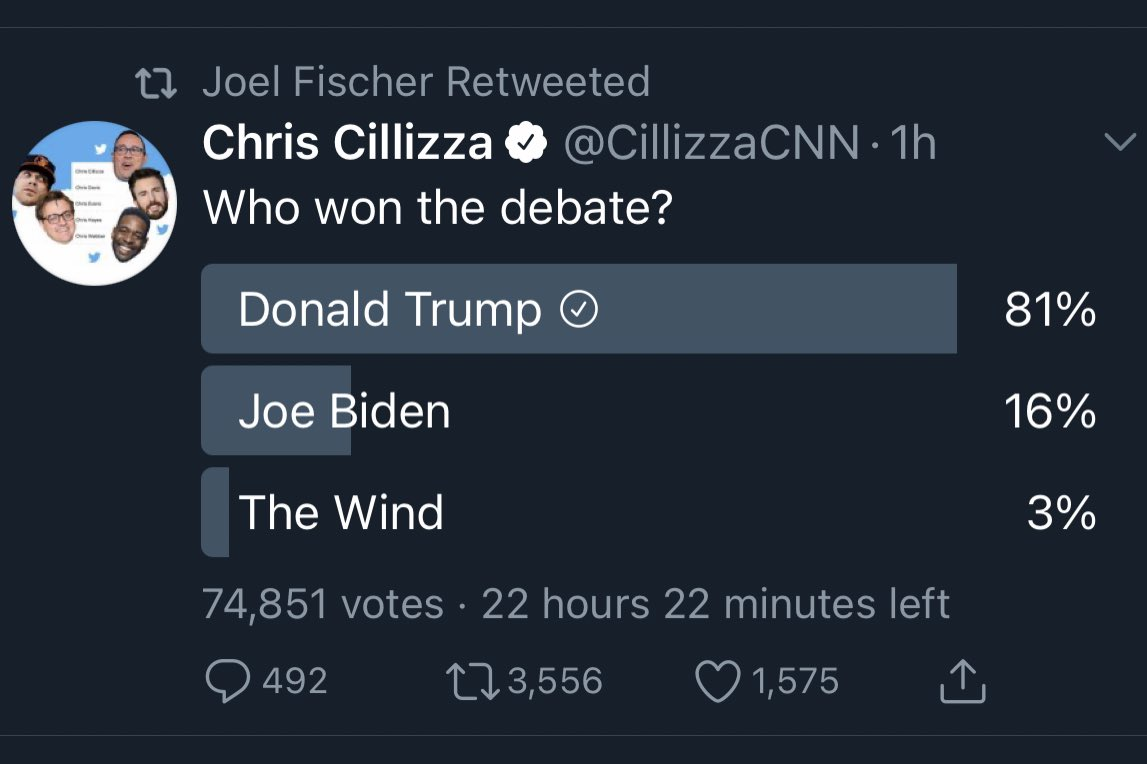

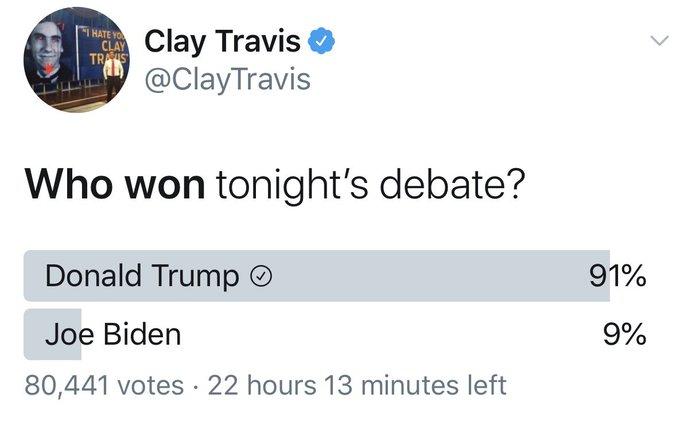

And while three MSM snap polls following the debate found that Biden won, snap polls over Twitter largely favored President Trump.

Ever since the Democratic Party nominated its ticket of Joe Biden and Kamala Harris for the 2020 U.S. Presidential Election, together, with their media operatives, have made it central to their campaign message to brazenly lay at the feet of incumbent President Donald Trump the ‘over 200,000 COVID deaths’ – a spurious claim, by any reasonable standard, that has gone virtually unchallenged by mainstream media and even many Republicans seeking to ‘distance’ themselves from the President.

It’s as if the claim, which borders on insanity and is devoid of any logic or real evidence, has been generally accepted as the truth across wide swaths of the country. The Democrats’ own platform says it in no uncertain terms:

“Make no mistake: President Trump’s abject failure to respond forcefully and capably to the COVID-19 pandemic—his failure to lead—makes him responsible for the deaths of tens of thousands of Americans.“

As early as May of this year, Jeff Bezo’s Washington Post had already rendered its verdict in a ‘death counter’ report with a matter-of-fact headline that read, “Trump’s covid-19 inaction killed Americans. Here’s a counter that shows how many.”

IMAGE: It’s very much the ‘Trump virus’ versus the ‘China virus’ this election season.

If the notion of sending ‘tens of thousands’ of Americans to their death is supposed to conjure up images of some kind of sick death march, that is exactly what Trump’s opponents are hoping to convey to voters in the 2020 election.

IMAGE: New York Governor Andrew Cuomo has presided over one of the worst public health disasters in American history.

Ironically, just a day before the aforementioned WashPo’s journalistic murder conviction of Trump, it was none other than the recently censoredNew York Post that published a scathing rebuke of NY Governor Andrew Cuomo’s disastrous and lethal nursing home policy — a policy that did in fact lead to thousands of dead elderly people in his state’s care.

In a recent episode of the “Conversations with Coleman” podcast, host Coleman Hughes, a Manhattan Institute fellow and contributing editor at City Journal, speaks with establishment academic and author Niall Ferguson, Milbank Family Senior Fellow at the Hoover Institution at Stanford University, and senior faculty fellow at the Belfer Center for Science and International Affairs at Harvard.

Ferguson offers this surprising take on the question of whether the effects of the COVID-19 crisis in the U.S. are Trump’s fault:

“There’s actually very little evidence to support those claims. It’s very clear that the failure that produced bad outcomes in terms of excess mortality […] that those failures were not really and can’t be attributed to the men or women at the top… they were failures of the public health bureaucracy.”

In the current political and media climate, as election day quickly approaches, it would seem that every public health official, including all the ‘white coat’ bureaucrats, along with all the political leaders in every state, county and city in the country have been completely absolved of any responsibility when it comes to the COVID ‘death toll’ — and that’s an incredibly audacious plank of ‘truth’ to stand on.

This is an important conversation to be having at this moment in the country’s history; and yet, amazingly, you can barely find it happening anywhere in the public discourse.

Are the effects of COVID-19 Trump’s fault?Watch:

If we’ve learned anything about the politicization of COVID these past nine months, it’s that media ‘spin’ rooms might as well have padded walls.

via ZeroHedge News https://ift.tt/3okgnb1 Tyler Durden

US Manufacturing Disappoints In Early October PMI Data As Election Anxiety Builds Tyler Durden

Fri, 10/23/2020 – 09:53

After a mixed bag of PMI data from Europe (UK ugly, Services weak compared to Manufacturing), preliminary October data for both segments of the US economy were expected to rise (despite a trend towards weaker macro data for the last two months).

Interestingly, US saw a mirror image of Europe – with Manufacturing disappointing (53.3 vs 53.5 3exp) and Services stronger (56.0 vs 54.6 exp)

Source: Bloomberg

The combination proved enough though to lift the US Composite index to 20-month highs and suggest economic growth is rebounding confidently…

“The US economy looks to have started the fourth quarter on a strong footing, with business activity growing at a rate not seen since early 2019. The service sector led the expansion as increasing numbers of companies adapted to life with COVID19, while manufacturing continued to report solid growth amid rising demand from households and businesses.

“A slowdown in hiring and weaker new order inflows were in part attributable to hesitancy in decision making ahead of the presidential election. More encouragingly, business optimism surged higher, indicating that firms have become increasingly positive about prospects for the coming year amid hopes of renewed stimulus, COVID-19 containment measures gradually easing and greater certainty for businesses a and households after the presidential elections.”

Perhaps most worrying for The Fed however, is that Markit found “Inflationary pressures also eased. Despite a further strong rise in cost burdens, service providers sought to generate more sales and limit increases in output charges.”

Get back to work Mr.Powell!

via ZeroHedge News https://ift.tt/34lKw1G Tyler Durden

US Embassy In Turkey Suspends All Services, Citing Credible ‘Terror Threat’ Tyler Durden

Fri, 10/23/2020 – 09:30

There’s been a huge development out of Turkey at a moment the country is under US scrutiny after conducting major Russian S-400 missile defense system tests for the first time, which have run late last week into this week on the Black Sea coast.

The United States Embassy in Turkey says it has temporarily suspended all citizen and visa services based on a significant security alert.

#Turkey: US Mission Turkey received credible reports of potential terrorist attacks and kidnappings against US citizens and foreign nationals in Istanbul and potentially other locations. Exercise heightened caution where Americans or foreigners may gather. https://t.co/S5Gwb6NQsApic.twitter.com/pHyQoesEuC

According an Oct.23 alert its official website, the embassy “received credible reports of potential terrorist attacks and kidnappings against U.S. citizens and foreign nationals in Istanbul, including against the U.S. Consulate General, as well as potentially other locations in Turkey.”

The statement continues by urging American citizens “to exercise heightened caution in locations where Americans or foreigners may gather, including large office buildings or shopping malls.”

US Embassy in Ankara, via AP

No further details were given, nor were any particular groups or individuals which might constitute a threat named. It’s an alert that’s unusual for Turkey, given it’s a common place of tourism and travel for Westerners. But the security situation for Americans have been of growing concern amid fraying US-Turkey relations of the past few years.

Meanwhile, Turkish President Recep Tayyip Erdogan announced Friday the successful testing of the recently acquired S-400s. He said the Russian S-400 systems “have been tested and are being tested,”according to regional media.

He was further reported to have “shrugged off” US objections and continued threats of Washington sanctions, which is angry over proliferation of advanced Russian equipment by a NATO member state.

Turkey has successfully tested its S-400 air defense system near the city of Sinop …. pic.twitter.com/m0wuAGGTf3

Erdogan said “objection from NATO ally United States on the issue did not matter” according to a translation and paraphrase of the statements by Reuters.

He also attempted to call out what he suggested is a US double standard regarding Greece, noting Turkey’s longtime enemy in the Mediterranean possesses S-300 systems, but that the US has never objected.

via ZeroHedge News https://ift.tt/37uqGn0 Tyler Durden

{kind=link}