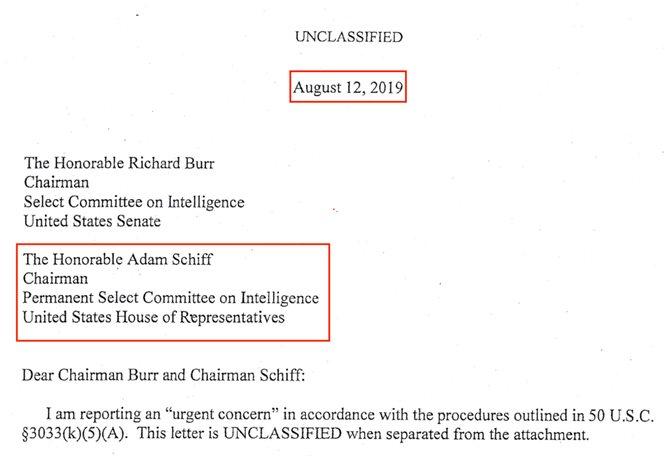

George Soros has responded to recent claims by Trump attorney Rudy Giuliani linking the billionaire financier to a Ukrainian organization accused of meddling in the 2016 US election for Hillary Clinton, as well as another organization whose joint report with BuzzFeed was cited three times in an August 12 whistleblower complaint lodged against President Trump by a CIA employee.

A Monday email from Soros spokesman Michael Vachon with the subject “Ukraine Debunking” reads: “You may have heard (or seen) Rudolph Giuliani’s ranting about George Soros allegedly playing some nefarious role in Ukraine.” The letter then directs people to a Washington Post article authored by Emily Tamkin – who has previously written in Soros’s defense (and loves the word ‘boogeyman’).

Giuliani has come under fire for his recent work to uncover the truth behind several claims regarding Ukraine, including alleged 2016 US election meddling to benefit Hillary Clinton, as well as efforts at the center of a CIA whistleblower complaint to encourage Ukraine’s new president, Volodomyr Zelensky, to investigate former Vice President Joe Biden.

Biden openly bragged last year about strongarming Ukraine when he threatened to withhold $1 billion in US loan guarantees unless a prosecutor investigating energy giant Burisma Holdings – which was paying Biden’s cocaine-addict son Hunter $600,000 to sit on its board – wasn’t fired immediately.

While the CIA whistleblower and initial media reports suggested that Trump was abusing his office to threaten Ukraine, transcripts of a July 25 phone call between Trump Zelensky reveal that Trump applied no such pressure.

In an appearance on Fox News last week, Giuliani said: “What I’m talking about, this, it’s Ukrainian collusion, which was large, significant, and proven with Hillary Clinton, with the Democratic National Committee, a woman named Chalupa, with the ambassador, with an FBI agent who’s now been hired by George Soros who was funding a lot of it” (for more on the situation with Chalupa and the DNC, follow the work of journalist Lee Stranahan).

Rudy Giuliani: “What I’m talking about, this, it’s Ukrainian collusion, which was large, significant, and proven with Hillary Clinton, with the DNC, a woman named Chalupa, with the ambassador, with an FBI agent who’s now been hired by George Soros who was funding a lot of it” pic.twitter.com/nNFyXnHA7r

Ukrainian Ambassador Valeriy Chaly confirmed that DNC contractor of Ukrainian heritage, Alexandra Chalupa, approached Ukraine seeking information on Trump campaign chairman Paul Manafort’s dealings inside the country, in the hopes of exposing them to Congress.

Chaly says that, at the time of the contacts in 2016, the embassy knew Chalupa primarily as a Ukrainian-American activist and learned only later of her ties to the DNC. He says the embassy considered her requests an inappropriate solicitation of interference in the U.S. election.

“The Embassy got to know Ms. Chalupa because of her engagement with Ukrainian and other diasporas in Washington D.C., and not in her DNC capacity. We’ve learned about her DNC involvement later,” Chaly said in a statement issued by his embassy. “We were surprised to see Alexandra’s interest in Mr. Paul Manafort’s case. It was her own cause. The Embassy representatives unambiguously refused to get involved in any way, as we were convinced that this is a strictly U.S. domestic matter.

“All ideas floated by Alexandra were related to approaching a Member of Congress with a purpose to initiate hearings on Paul Manafort or letting an investigative journalist ask President Poroshenko a question about Mr. Manafort during his public talk in Washington, D.C.,” the ambassador explained. –The Hill

Chalupa, who told Politico in 2017 that she had “developed a network of sources in Kiev and Washington, including investigative journalists, government officials and private intelligence operatives,” said she “occasionally shared her findings with officials from the DNC and Clinton’s campaign.“

Giuliani also said that former Ukrainian prosecutor Viktor Shokin, Biden had fired, “dropped the case on George Soros’ company called AntAC,” adding “AntAC is the company where there’s documentary evidence that they were producing false information about Trump, about Biden. Fusion GPS was there,” Giuliani added. “Go back and listen to Nellie Ohr’s testimony. Nellie Ohr says that there was a lot of contract between Democrats and the Ukraine. (via the Daily Wire).

Meanwhile, a footnote in the whistleblower’s August 12 complaint cites a joint report from BuzzFeed and Soros-funded Organized Crime and Corruption Reporting Project (OCCRP) to support their argument – notably leaving the “BuzzFeed” association out of the complaint.

Every page of the OCCRP website features the same bottom section listing the icons of four of the organization’s top funders, including Soros’s Open Society Foundations and the United States Agency for International Development (USAID). Indeed, OCCRP provides a hyperlink to the webpage for Soros’s Open Society at the bottom left corner of every page on OCCRP’s own website.

Soros’s Open Society was listed as the number two donor in most of the annual financial records posted on OCCRP’s website starting in 2012. Some years list Soros as the organization’s top donor.

OCCRP advertises its other funders, including Google, the National Endowment for Democracy, the Rockefeller Brothers Fund and the U.S. State Department Bureau of Democracy, Human Rights and Labor.

According to Breitbart, the whistleblower’s account cites the OCCRP report on three more occasions, to:

Write that Ukraine’s Prosecutor General Yuriy Lutsenko “also stated that he wished to communicate directly with Attorney General Barr on these matters.”

Document that Trump adviser Rudi Giuliani “had spoken in late 2018 to former Prosecutor General Shokin, in a Skype call arranged by two associates of Mr. Giuliani.”

Bolster the charge that, “I also learned from a U.S. official that ‘associates’ of Mr. Giuliani were trying to make contact with the incoming Zelenskyy team.” The so-called whistleblower then relates in another footnote, “I do not know whether these associates of Mr. Giuliani were the same individuals named in the 22 July report by OCCRP, referenced above.”

In short, Soros is so deeply involved in Ukraine that there’s no way he couldn’t be caught up in this whole thing.

Soros explained that Ukraine was particularly important to him because he thought the country’s independence was geopolitically important. “As long as Ukraine prospers, there can be no imperialist Russia,” he wrote.

At the time, Soros’s foundation in Ukraine was supporting a whole network: an institute to train public servants, a foundation to develop legal culture in the country and a center for modern art, among other institutions. He claimed that all of this was important because he wanted “to supply Ukraine with the infrastructure necessary for a modern state — and an open society.” –Washington Post

That said, the Post‘s Tamkin admits that the AntAC-Soros link is a “small kernel of reality buried deep within Giuliani’s conspiracy theory.”

“I asked some of the protesters and anti-corruption groups working at the time if they received Open Society funding. And many, if not most, of them had. But that is different from Soros himself orchestrating efforts against political enemies, which is what their opponents were suggesting.”

In short, just because Soros’s Open Society foundation funded groups which may have meddled for Hillary in the 2016 US election, and are cited by a CIA whistleblower against President Trump, his defenders claim it doesn’t mean his fingerprints are personally on any of it.

Although billionaire bond fund manager Jeffrey Gundlach doesn’t think the U.S. economy is in imminent danger of recession, he does say that there are some worrying signs for President Donald Trump ahead of the 2020 election. How Trump avoids a recession will impact his reelection chances.

As we’ve noted here before, a recession would all but make Trump’s reelection impossible. But if the president can avoid an economic meltdown, the current witch hunt and impeachment rhetoric could very well propel him to another win in 2020. Obviously, we don’t know when the next recession will strike with a vengeance, but that it will and when (not if) it does, it’s important to be prepared for it, as most Americans, currently, are not.

“If you have a recession, a negative sign in front of GDP, especially nominal GDP, that would just be horrific,” Gundlach, the CEO and chief investment officer of the Los Angeles-based DoubleLine Capital, which has $140 billion in assets, told FOX Business.

“I think there is just nothing for Trump to run on if the economy is negative.”

But Gundlach sees only positive signs for the president in the economy, even though many negative indicators have surfaced as well.

The U.S. services sector grew in August for the 115th consecutive month while job growth has remained decently strong and consumer spending remains healthy (but is mostly new consumer debt). In addition, new and existing home sales saw a nice bump in August, probably thanks to a reduction in interest rates in July. But while leading indicators are still positive, they have fallen from 6.6 a year ago to 1.1 in August. A drop below zero could have big implications for the economy.

“There’s [sic] some numbers rolling off in the next few months, it will mean there’s a good risk of the leading indicators going to zero,” he said.

“And the reason why that matters is there hasn’t been a recession in decades of economic tracking, there has not been a recession ever without leading indicators first going negative.”

But, Gundlach concedes that the stakes are high for the president, as a recession, or two consecutive quarters of negative growth, occurring before Election Day could be the death blow that prevents him from winning a second term.

However, some of the “derangement” from the liberal leftists over the recent impeachment proceedings could also help solidify a win.

Gundlach also suggests Trump cut payroll taxes.

“If you cut payroll taxes it absolutely helps the economy because that’s money that’s all at the middle-class level and it’s all going straight into the paycheck,” Gundlach said.

“So that might actually help to put a monkey wrench into these indicators…if the economy is left alone.”

Trump could also do the right thing and stimulate the economy on his own (without the Federal Reserve’s interference) by eliminating his tariffs on Chinese goods.

“What if we just pull all the tariffs in I don’t know March, we just eliminate them?” Gundlach asked, rhetorically.

NY Fed Starts New Quarter With Unexpectedly High $55BN Repo Operation

Many expected the funding shortage sweeping across the US financial community to be mostly a function of one-time mid-September items coupled with traditional quarter-end liquidity: it explained why in addition to three term repos, on the last day of the quarter, the Fed conducted an overnight repo which saw a surprisingly high, $63.5BN uptake on Monday.

Well, it’s now the new quarter… and contrary to clearly erroneous conventional wisdom, the funding shortage still persists. Moments ago the NY Fed reported that in the first overnight repo operation of the quarter, one which saw the maximum allotted size shrink from $100 billion to $75 billion, dealers submitted a surprisingly high $54.85BN in collateral, all of which was accepted by the Fed.

Specifically, dealers tendered $50BN in TSYs and $4.75BN in MBS, as well as a $100MM in Agencies, to boost their liquidity.

The continued demand for reserves, even with $139BN in liquidity locked up in 2-week term repo which expire in the second week of October, suggests that the funding shortage is anything but a calendar event, and confirms that there is an acute reserve shortage, one which the Fed will have to address, most likely by resuming POMO operations to the tune of roughly $20BN per month… which for all the QE denialists, will be the same size as QE1.

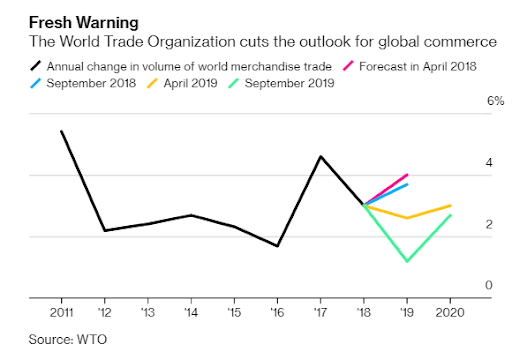

“The Darkening Outlook For Trade Is Discouraging:” WTO Sharply Lowers Global Outlook Amid Trade Conflicts

A synchronized global downturn and an escalating trade war with China has prompted the World Trade Organization (WTO) to reduce its global growth forecasts for 2019 and 2020.

World merchandise trade volumes are expected to only expand by 1.2% in 2019, substantially slower than the 2.6% growth forecast in April. The 2020 global growth forecast is expected to be 2.7%, down from 3% previously.

“The darkening outlook for trade is discouraging but not unexpected. Beyond their direct effects, trade conflicts heighten uncertainty, which is leading some businesses to delay the productivity-enhancing investments that are essential to raising living standards,” said WTO Director-General Roberto Azevêdo.

“Job creation may also be hampered as firms employ fewer workers to produce goods and services for export,” he added.

WTO economists said the global downturn is partly due to President Trump’s trade war, but also “reflects country-specific cyclical and structural factors, including the shifting monetary policy stance in developed economies and Brexit-related uncertainty in the European Union.”

The economists were firm in their global outlook: “Macroeconomic risks are firmly tilted to the downside.”

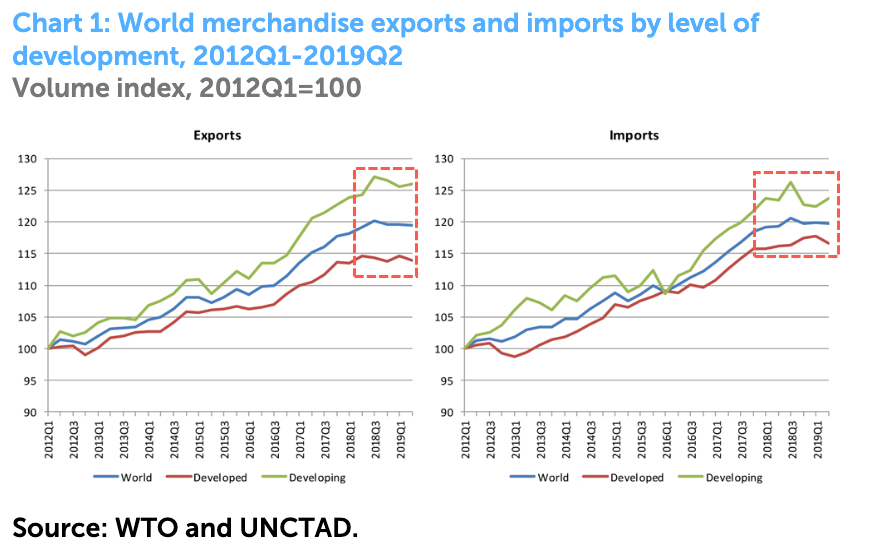

As shown in Chart 1, quarterly merchandise export and import volumes on a seasonally-adjusted basis in the world, developed and developing regions have dramatically stalled since 2018, with no signs of a turn up until next year.

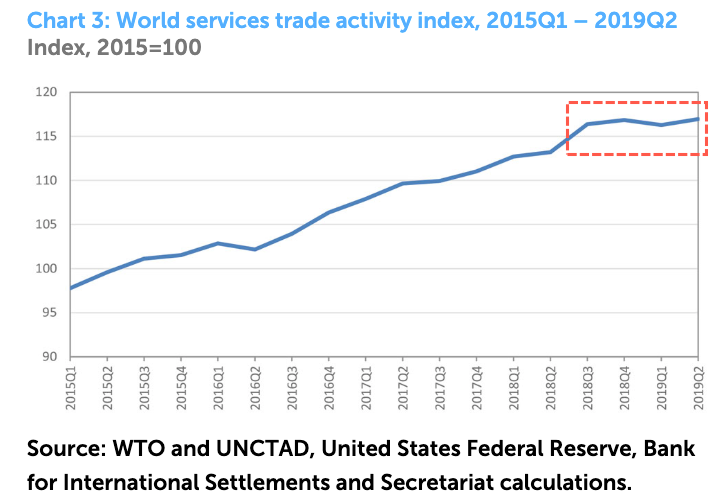

In Chart 3, world services trade has “plateaued” since summer 2018.

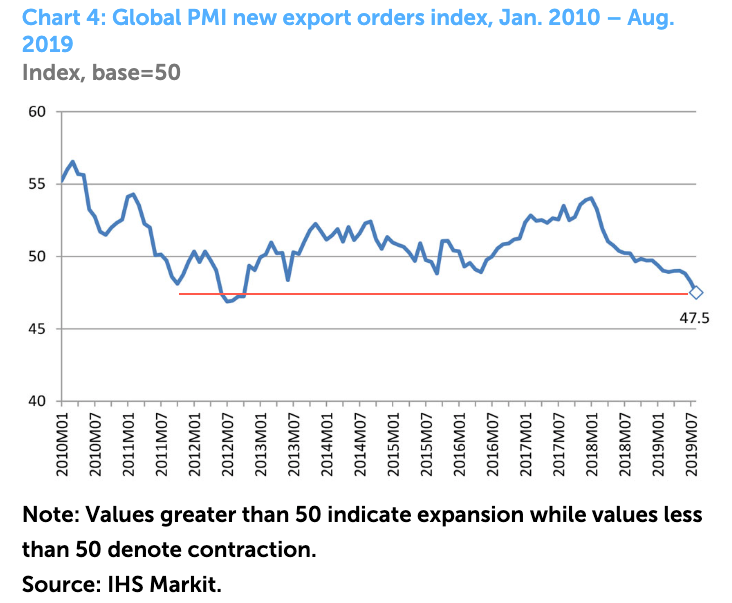

Global Project Management Institute (PMI) new export orders peaked at 54 in January 2018, has since dropped to 47.5 in August, one of the lowest prints since October 2012. Again, there are no signs of a rebound this year according to WTO.

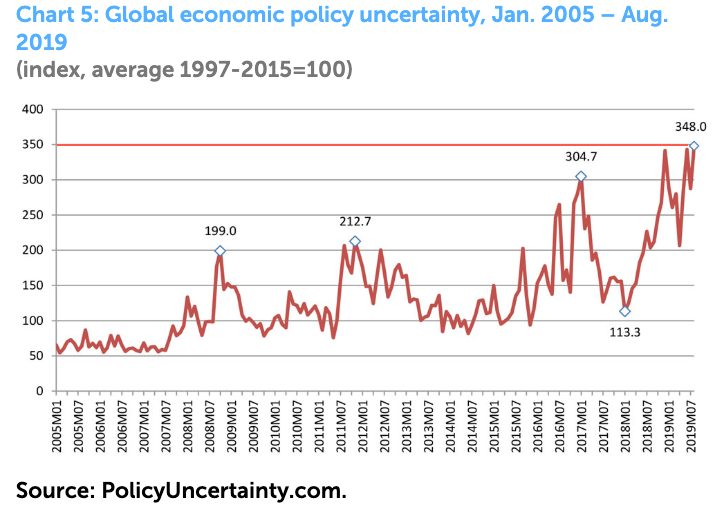

And as we noted on Monday, the global policy uncertainty index continues to soar to a fresh record high. In 2019 alone, the index has jumped from 289 in January to 348 in August.

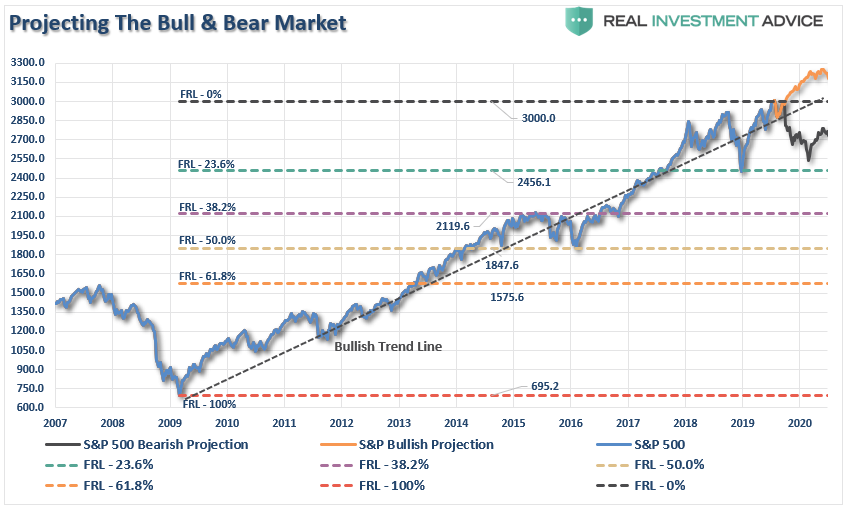

The balance of risk remains tilted to the downside through 2H19. WTO confirms that the economic rebound or “green shoots” Wall Street was predicting for 2H19 is fake news. A growth scare for stocks is nearing; determining the trigger for the next stock market plunge is currently what every concerned money manager is trying to figure out.

“Assuming we are correct, and Trump does indeed ‘cave’ into China in mid-October to get a ‘small deal’ done, what does this mean for the market.

The most obvious impact, assuming all ‘tariffs’ are removed, would be a psychological ‘pop’ to the markets which, given that markets are already hovering near all-time highs, would suggest a rally into the end of the year.”

This is not the first time we presented our analysis for a “bull run” to 3300.To wit:

“The Bull Case For 3300

Momentum

Stock Buybacks

Fed Rate Cuts

Stoppage of QT

Trade Deal”

While I did follow those statements up with why a “bear market” is inevitable, I didn’t discuss the issue of what happens is Trump decides to play hardball and the “trade negotiations” fall apart.

Given Trump’s volatile temperament, this is not an unlikely “probability.” Also, there is more than just a little pressure from his base of voters to press for a bigger deal.

As I noted, China cannot agree to the biggest issues which have stalled negotiations so far:

Cutting the share of the state in the overall economy from 38% to 20%,

Implementing an enforcement check mechanism; and,

Technology transfer protections

For China, these items are an infringement on its sovereignty, and requires a complete abandonment the “Made in China 2025” industrial policy program. This is something that President Xi is extremely unlikely to do, particularly for a U.S. President who is in office for a maximum of 4-more years.

Of course, if talks break down, there are two potential outcomes investors need to consider for the portfolio:

Everything remains status quo for now and more talks are scheduled for a future date, or;

Talks breakdown and both countries substantially increase tariffs on their counterparts.

Given that current tariffs are weighing on Trump’s supporters in the Midwest, and both Silicon Valley and retail’s corporate giants have pressured Trump not to increase tariffs further, the most probable outcome is the first.

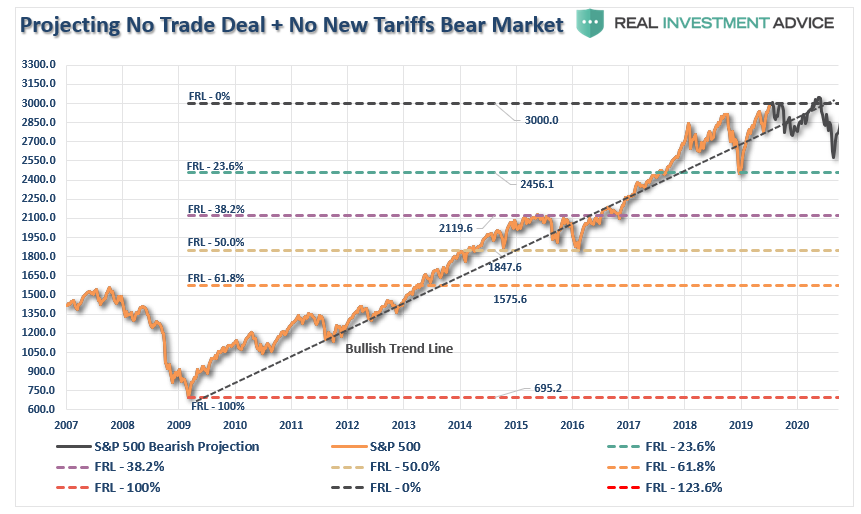

No Trade Deal, No New Tariffs

Unfortunately, that outcome does little for the market in the short-term as existing tariffs continue to weigh on corporate profitability, as well as consumption. Given that earnings are already on the decline, the benefits of tax cut legislation have been absorbed, and economic growth is weakening, there is little to boost asset prices higher.

Therefore, under this scenario, current tariffs will continue to weigh on corporate profitability, but “hopes” for future talks will likely continue to keep markets intact for a while longer. However, as we head into 2020, a potential retracement will likely occur as markets reprice for slower earnings and economic growth.

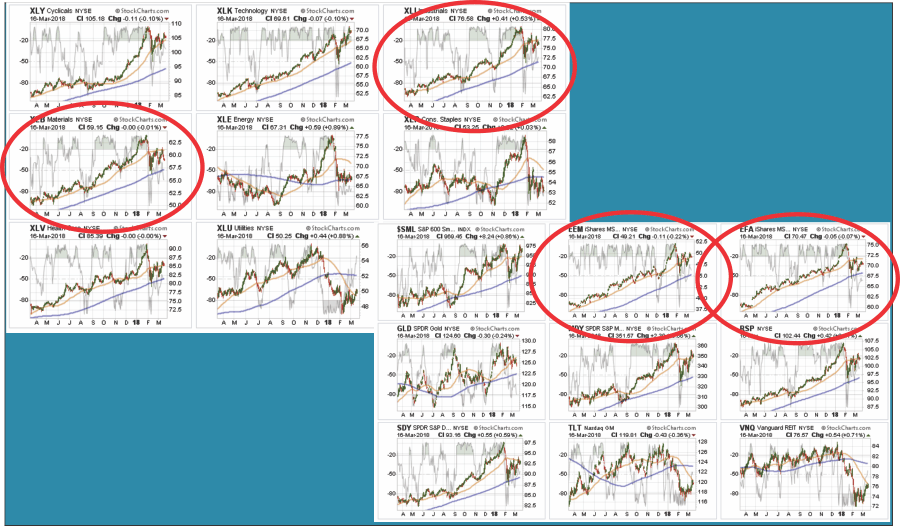

In this environment, we would continue to expect some underperformance by those sectors most directly related to the current tariffs which would be Basic Materials, Industrials, and Emerging Markets.

Since the beginning of the “trade war,” these sectors have lagged overall market performance and have been under-weighted in portfolios. We alerted our RIA PRO subscribers to this change in March, 2018:

“We closed out our Materials trade on potential “tariff” risk. Industrials are now added to the list of those on the “watch, wait and see” list with the break below its 50-dma. Tariff risk continues to rise and Larry Kudlow as National Economic Advisor is not likely to help the situation as his ‘strong dollar’ views will NOT be beneficial to these three sectors. Also, we reduced weights in international exposure due to the likely impact to economic growth from ‘tariffs’ on those markets which have continued to weaken again this week.”

That advice turned out well as those sectors have continued to languish in terms of relative performance since then.

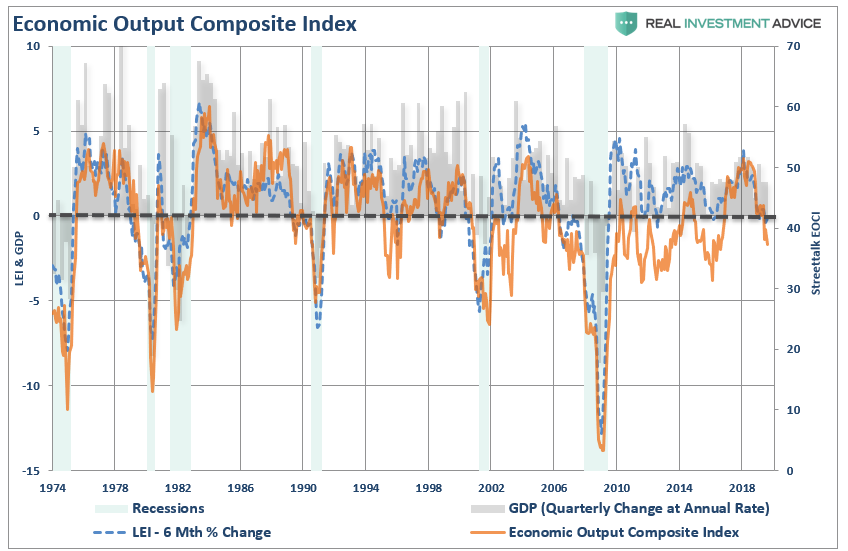

Furthermore, a “no trade deal, no tariff change” outcome does little to change to the current deterioration of economic data. As we showed just recently, our Economic Output Composite Index has registered levels that historically denote a contractionary economy.

All of these surveys (both soft and hard data) are blended into one composite index which, when compared to GDP and LEI, has provided strong indications of turning points in economic activity. (See construction here)”

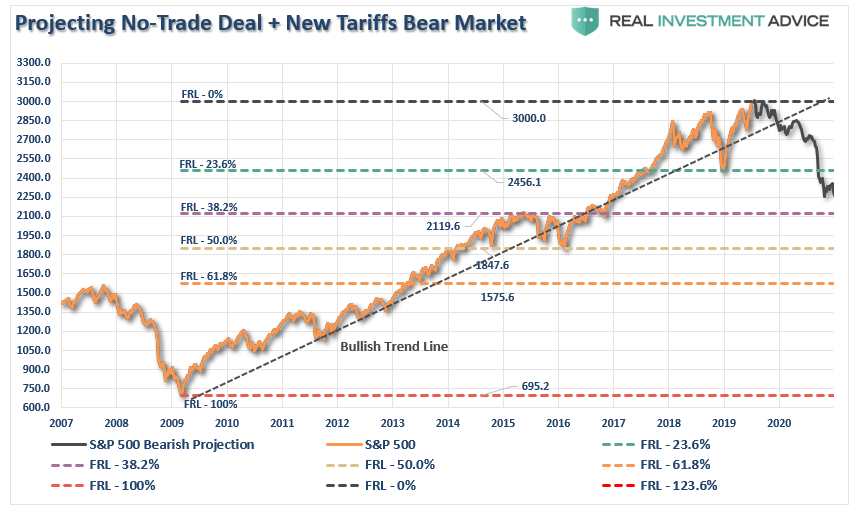

No Trade Deal Plus New Tariffs

The second outcome is more problematic.

In this scenario, Trump allows emotion to get the better of him, and he blows up at the meeting. In a swift retaliation, he reinstates the “tariffs” on discretionary goods, and increases tariffs across the board as a punitive measure. The Chinese, in an immediate retaliation levy additional tariffs as well.

With both sides now fully entrenched in the trade war, the market will lose faith in the ability to get a “deal” done. The increased tariffs will immediately be factored into earnings forecast, and the market will begin to reprice for a more negative outcome.

In this scenario, Basic Materials, Industrials, Emerging, and International Markets will continue to be the most impacted and should be avoided. Because of the new tariffs which will directly impact discretionary purchases, Technology and Discretionary sectors should also likely be under-weighted.

The increase in tariffs is also going to erode both consumer and economic confidence which have remained surprisingly strong so far. However, once the consumer is more directly affected by tariffs, that confidence, along with related consumption, will fade.

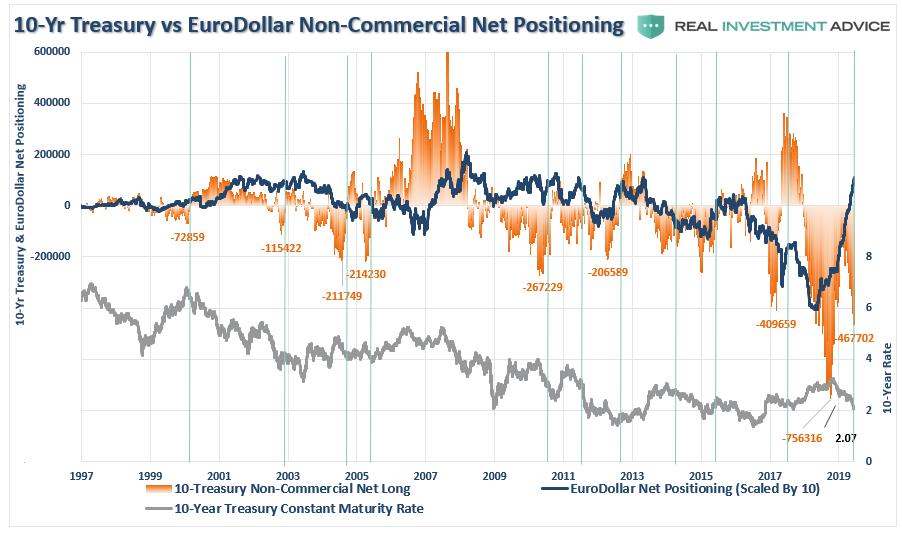

What About Bond Yields And Gold

In both scenarios above, a “No Trade Deal” outcome will be beneficial for defensive positioning in portfolios. Gold and bond yields have already performed well this year, but if trade talks fall through, there will be a rotation back to the “safe haven” trade as equity prices potentially weaken. This is specifically the case in the event our second outcome comes to fruition.

While bond yields are overbought currently, it is quite likely we could see yields fall below 1%. Also, given the large outstanding short-position in bonds, as discussed recently, there is plenty of “fuel” to push rates lower.

“Combined with the recent spike in Eurodollar positioning, as noted above, it suggests that there is a high probability that rates will fall further in the months ahead; most likely in concert with the onset of a recession.”

As I noted, there is no outcome that ultimately avoids the next bear market. The only question is whether moves by the Administration on trade, combined with the Fed cutting rates, retards or advances the timing.

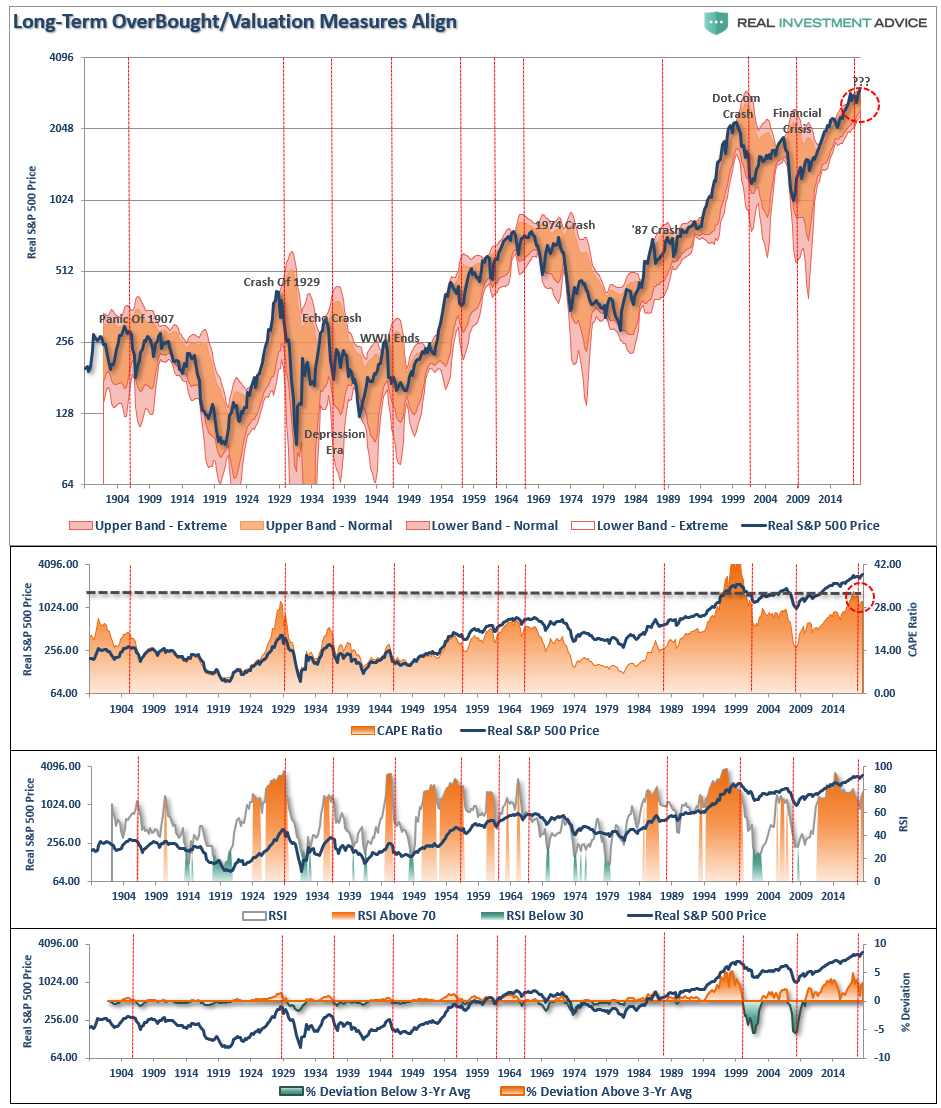

“Furthermore, given the markets never reverted to any meaningful degree, higher prices combined with weaker earnings growth, has left the markets very overvalued, extended, and overbought from a historical perspective.”

Our long-term quarterly indicator chart has aligned to levels that have previously denoted more important market tops. (Chart is quarterly data showing 2-standard deviations from long-term moving averages, valuations, RSI indications above 80, and deviations above the 3-year moving average)

While we laid out the “bullish case” of 3300 over the weekend, it would not be wise to dismiss the downside risk given how much exposure to the “trade meeting” is currently built into market prices.

We are assuming that Trump wants a “deal done” before the upcoming election, which should also help temporarily boost economic growth, but there remains much that could go wrong. An errant “tweet,” a “hot head,” or merely a breakdown in communications, could well send markets careening lower.

Given that downside risk outweighs upside reward at this juncture by almost 3 to 1, in remains our recommendation to rebalance risk, raise some cash, and hedge long-equity exposure in portfolios for now.

This remains a market that continues to under-price risk.

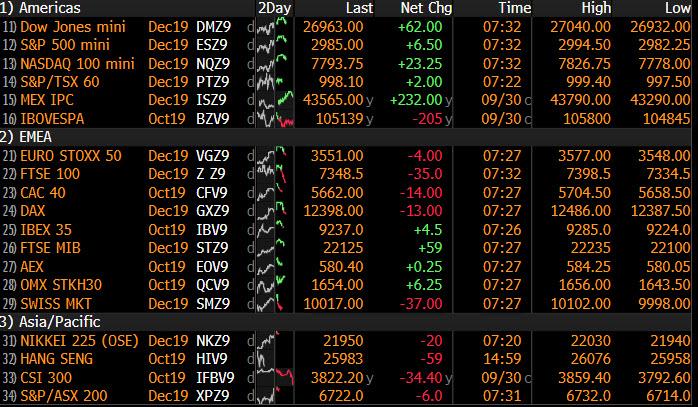

US Stock Futures Levitate, Ignore Bond Market Blowout

In a session market by fireworks in the bond market, stocks were relatively tame and well-behaved as we officially entered the last quarter of the year.

S&P e-mini futures gained on Tuesday as trade talk optimism returned, and ahead of the release of key US manufacturing data as investors looked for fresh signs of domestic demand in the world’s largest economy amid softening global growth. The ISM’s PMI data is expected to show the manufacturing sector rebounded to 50.0 in September after contracting for the first time in 3-1/2 years to 49.1 in August. The US ISM data comes on the heels of euro zone data, which showed manufacturing activity in the bloc contracted at its steepest rate in almost seven years as the global economy flashed clearer warning signs as a wave of data showed manufacturing stuck in a slump, exports falling and sentiment sliding: as the trade war between the U.S. and China rages, industry executives from Japan and Russia to Germany and Italy complained of contracting business, while the World Trade Organization cut its forecast for commerce to the lowest in a decade.

The latest dismal European numbers only added to the gloom for investors facing a laundry list of threats just now, including everything from the drawn-out trade war and Brexit to protests in Hong Kong and an impeachment probe of President Trump; they even barely blinked at the news of the first shot protesters in Hong Kong. Nonetheless, stocks continue to ignore the looming threat in what has been yet another perplexing risk-on start to the week (propelled by more stock buybacks ahead of the blackout period), perhaps because the outcome of each risk seems impossible to predict and the safest assets are looking expensive.

The overnight session started with subdued Asian markets as Hong Kong and China were closed for holidays. Japanese shares rose about 1%, while Australia’s dollar slid after the central bank cut its benchmark interest rate to a record low.

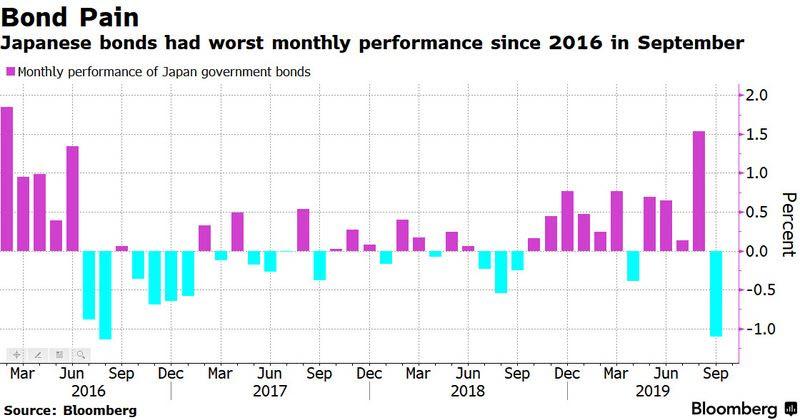

Yet while European stocks slipped amid the disappointing factory and inflation data, global stocks generally ignored the latest dismal manufacturing data, bonds were rather active, and as noted earlier, Japan’s 10Y JGBs suffered the biggest drop since August 2016 on a trifecta of negative developments, following a BOJ warning it would further trim its bond purchases, the GPIF saying it would shift to offshore bond purchases, and the ugliest 10Y bond auction in three years; the violent plunge set off a brief margin call which only made the selloff worse.

Treasuries and bunds then promptly joined the JGB selloff which gradually spread across the world.

The yield on 10-year U.S. bonds headed for the first increase in four days in the wake of the Japanese fiasco.

In FX, the Bloomberg dollar index rose for a second day, while the pound fluctuated as British Prime Minister Boris Johnson prepares to present his blueprint for a new Brexit deal to the European Union.

The Australia dollar tumbled as Australia’s central bank was dragged further into the global easing tide as it cut interest rates for the third time this year, to a new record low, even as it risks refueling excesses that Governor Philip Lowe warned against just weeks ago. The Reserve Bank reduced the cash rate by 25 basis points to a record-low 0.75% and said it may ease even further, venturing deeper into levels where unconventional measures may need to be adopted. The move is in part designed to prevent a rebound in the depreciating currency that might have been triggered if it stood pat while global counterparts eased. “The global race to the bottom is, in a sense, dragging the RBA along,” said Michael Blythe, chief economist at the Commonwealth Bank of Australia. “Failure to participate could see the Australian dollar move higher.”

In other geopolitical news, Chinese President Xi said no force can stop the Chinese people and the Chinese nation forging ahead, must uphold path of peaceful developments. Xi added that the central government would “maintain long-term prosperity and stability of Hong Kong and Macao.”

Gold extended recent declines and West Texas oil climbed.

On today’s calendar, expected data include PMIs and construction spending. McCormick and Stitch Fix are reporting earnings

Market Snapshot

S&P 500 futures up 0.3% to 2,987.25

STOXX Europe 600 down 0.07% to 392.86

MXAP up 0.2% to 156.70

MXAPJ down 0.03% to 501.93

Nikkei up 0.6% to 21,885.24

Topix up 1% to 1,603.00

Hang Seng Index up 0.5% to 26,092.27

Shanghai Composite down 0.9% to 2,905.19

Sensex down 1.6% to 38,050.80

Australia S&P/ASX 200 up 0.8% to 6,742.85

Kospi up 0.5% to 2,072.42

German 10Y yield rose 4.5 bps to -0.526%

Euro down 0.06% to $1.0893

Italian 10Y yield fell 0.2 bps to 0.484%

Spanish 10Y yield rose 4.4 bps to 0.189%

Brent futures down 1.5% to $59.90/bbl

Gold spot down 0.6% to $1,464.37

U.S. Dollar Index up 0.1% to 99.50

Top Overnight News from Bloomberg

British Prime Minister Boris Johnson will present a new plan for a Brexit deal to the European Union within days but there are signs that it may fail. While some purist euro-skeptics in Johnson’s ruling Conservative party are willing to compromise, the Irish government has said his proposals so far for resolving the Brexit impasse are a non-starter

The euro area’s manufacturing sector slumped in September as German factories experienced their worst month since the depths of the financial crisis. IHS Markit’s index for manufacturing in the euro region came in at 45.7 last month, slightly higher than the initial estimate of 45.6, but still the lowest level since October 2012

Police shot tear gas volleys at protesters as simultaneous rallies raged across Hong Kong, including a march through the city center, hours after celebrations for a holiday marking 70 years of Communist rule in China began in Beijing

Gold sank to an eight-week low as investors weighed the impact of a stronger dollar — which traded near the highest level since 2017 — together with unfavorable chart patterns and prospects of renewed, high-level U.S.-China trade talks next week

Japanese bond traders just had a taste of what it’s like when the nation’s central bank and pension fund aren’t there to support them. Bond futures tumbled by the most since 2016, triggering margin calls for investors, after the worst 10-year debt auction in three years. Yields across the curve climbed, while the sell- off also spilled into Treasuries and European debt.

Asian equities traded higher across the board after Wall Street wrapped up the third quarter with a session in the green ahead of principle-level US-Sino trade talks in Washington next week. In terms of Q3 performance, the S&P and DJIA both advanced for a third consecutive quarter, rising in excess of 1% each, whilst the Nasdaq dipped 0.1% Q/Q. Upside in the ASX 200 (+0.8%) was capped as base and precious metal miners bore the brunt of softer prices, whilst Nikkei 225 (+0.6%) cheered favourable currency moves and largely side-lined the planned sales tax hike which came into effect today. Elsewhere, the KOSPI (+0.5%) conformed to the risk appetite despite South Korean exports declining for the tenth straight month and semi-conductor exports slumping 31.5% Y/Y, albeit inflation metrics fell short of forecasts. As a reminder, Mainland China and Hong Kong markets were closed today due to National Day Holiday, although protests were underway in Hong Kong whilst China celebrated the 70th anniversary of the People’s Republic with a military parade. Finally, 10yr JGB futures were softer amid the risk-sentiment, however downside was more pronounced after the Japanese 10yr auction was received poorly as results showed a bid-to-cover at multi-year lows, which pressured UST and Bund futures in sympathy, Japan Securities Clearing Corporation then said an emergency margin call has been triggered on JGB futures.

Top Asian News

Japan’s GPIF Positions Itself for More Foreign Debt Buying

Marubeni Is Said to Sound Out Potential Buyers for Gavilon

Taiwan Dollar Is a Surprise Winner From U.S.-China Trade War

Japan Post Favors CLOs for U.S. Loan Purchases Over Mutual Funds

Major European bourses (Euro Stoxx 50 -0.1%) pared initial gains, following a positive AsiaPac lead, where stocks took impetus from a solid Wall Street session and better than expected Japanese Tankan manufacturing data. The FTSE 100 (-0.3%) is a marginal laggard, amid Sterling strength on renewed Brexit deal hopes and after the second reading of September’s Manufacturing PMI data proved not as grim as expected, while Switzerland’s SMI (-0.4%) is also lower amid weakness in some of its heavyweights. Negative ticks were seen across European bourses (although most pronounced in the DAX [-0.1%]) after the second reading of Germay’s Manufacturing PMI data, which although coming in better than expected, confirmed a deterioration in the sector in the month of September. Amid the initially firmer risk tone, defensives (Utilities (-0.3%), Health Care (-0.6%) and Consumer Staples (-0.9%)) are on the back foot while Tech (+0.3%) is in the lead. In terms of individual movers; MediaSet (+1.3%) was buoyed after posting decent earnings. PostNL (-2.7%) sunk on the news that the Co. is to combine its network with Sandd, in a deal worth EUR 105mln. ASML (+1.8%) advanced after the Co. was reiterated buy at UBS. Ryanair (+3.1%) and Air France (+2.7%) both moved higher after the Co’s were upgraded to buy at BAML. Atlantia (-2.3%) after Italy PM Conte said the process to revoke highway concessions is underway.

Top European News

Euro-Area Manufacturing Slump Deepens in Worst Month Since 2012

Euro-Area Inflation Slows, Adding to Case for ECB Stimulus Move

U.K. Mulls Help-to-Buy Future to Avoid Shock End for Developers

U.K. Factories Extend Slump Even as Brexit Preparations Resume

In FX, it has been a lively start to the new month and Q4 amidst ongoing Greenback strength, but with independent weights exacerbating declines and underperformance. The Aussie rebounded initially after the RBA cut rates by a further 25 bp and inserted a relatively upbeat line in the accompanying statement about a gentle turning point in the economy, but with guidance for further easing retained recovery gains were short-lived and Aud/Usd subsequently slipped below 0.6700, while Aud/Nzd retreated from another test of resistance around 1.0800 even though the Kiwi eventually succumbed to contagion and Nzd/Usd reversed through 0.6250 again to a 0.6220 low following another downbeat NZ business sentiment survey overnight. Meanwhile, the Swedish Krona slumped in wake of a significantly weaker than forecast sub-50 manufacturing PMI that was compounded by a downward revision to the previous month, and its Scandinavian counterpart has fallen in sympathy as Norway’s manufacturing sector only just escaped contraction and decelerated sharply from almost 54.0 in August. Eur/Sek has tested 10.8000 following a breach of technical resistance circa 10.7742 and Eur/Nok rallied beyond 9.9550 from lows of around 9.9080 and just below 9.8850 at one stage on Monday.

USD – The Dollar continues to prosper, partly at the expense of others, but also as US Treasury yields rebound and curves re-steepen with some extra impetus via Fed’s Evans advocating a policy pause after the 2 insurance cuts administered in July and September. Accordingly, the DXY has forged a fresh ytd high and breached 99.500 in the process, at 99.590, eyeing the Markit PMI, ISM and more Fed speakers for further direction.

CHF/CAD/JPY – The Franc has also bowed to disappointing Swiss macro news in the form of retail sales and deeper manufacturing PMI recession, with Usd/Chf up through parity and Eur/Chf crossing 1.0900 even though the single currency is struggling to cope with the aforementioned broad Buck advance and its own frailties. Elsewhere, the Loonie is still pivoting 1.3250 and awaiting Canadian GDP and/or Markit’s manufacturing PMI for extra inspiration, while the Yen appears more attuned to the latest gains in UST yields rather than a post-auction plunge in JGB futures that triggered emergency Japanese SCC margin calls. Indeed, Usd/Jpy has extended gains above 108.00 towards 108.50, with upside chart levels at 108.43 (Fib) and 108.48 (September’s peak) proving tough to break convincingly, thus far.

GBP/EUR – Relative G10 outperformers, or at least putting up a fight against the Greenback with the aid of an unexpected bounce in the UK manufacturing PMI and a steady pan Eurozone final print thanks to a German upgrade from the dire preliminary reading. However, Cable is still not making much headway beyond 1.2300 and Eur/Usd has waned just above 1.0900, with the former down through the 55 DMA (1.2279), Fib support (1.2271) and a late September base before the Brexit re-stocking PMI recovery and latter having another close look at bids at 1.0880 that are protecting a deeper retracement to 1.0864 (strong Fib support).

EM – Blanket losses vs the Greenback, and with sub-50 manufacturing PMIs across the region, bar Turkey, not helping, as the Lira loses more ground amidst rebounding oil prices and further investor disenchantment with the Finance Minister’s latest grand economic plan.

The RBA cut its cash rate by 25bps to 0.75% as expected. RBA reiterated that it is reasonable to expect that an extended period of low interest rates will be required in Australia to reach full employment and achieve the inflation target. RBA added “A gentle turning point, however, appears to have been reached”. The Central Bank noted the low level of interest rates, recent tax cuts, ongoing spending on infrastructure, signs of stabilisation in some established housing markets and a brighter outlook for the resources sector should all support growth, but repeated that the Board will continue to monitor developments, including in the labour market, and is prepared to ease monetary policy further if needed to support sustainable growth in the economy, full employment and the achievement of the inflation target over time.

In commodities, the crude complex is consolidating, with both benchmarks having found support around their 12 September lows around USD 54.00/bbl for WTI and USD 59.00/bbl for Brent respectively, following yesterday’s steep declines which were exacerbated by bearish supply signals re. Saudi Aramco’s recovery to full output. News flow on the Middle Eastern geopolitical front has been light, although reports that Iran has sentenced one person to death for spying for the US could be providing some support to the complex. However, further details regarding who the person is and what the wider implications, if any, may be are scant. Elsewhere, amid continued constructive risk tone and possible technical selling after it convincingly lost its grip on the USD 1500/oz handle yesterday, Gold continues to move lower. The fall in Gold prices comes despite continued escalations in protestor/police tensions in Hong Kong, as markets more broadly remain seemingly unperturbed by developments for now. Meanwhile, Copper futures remain unable to derive support from the more constructive risk tone, and have extended on their overnight declines after broking below short-term resistance around USD 2.572/lbs.

US Event Calendar

8:50am: Fed’s Clarida Makes Brief Remarks at AI Conference

9:30am: Fed’s Bowman Speaks at Community Banking Conference

9:45am: Markit US Manufacturing PMI, est. 51, prior 51

10am: ISM Manufacturing, est. 50, prior 49.1

10am: Construction Spending MoM, est. 0.5%, prior 0.1%

Wards Total Vehicle Sales, est. 17m, prior 17m

DB’s Jim Reid concludes the overnight wrap

Welcome to Q4 and only 85 days until Xmas. Craig has just published the Sept/Q3/YTD performance review. Q3 ended up being relatively positive for global assets with 29 of our 38 asset sample finishing with a positive total return although only 14 did so in dollar adjusted terms owing to the stronger greenback. September saw 23 out of 38 (22 in dollar terms) higher and reversed a tough August where only 18 of the 38 saw positive returns (14 in dollars). See Craig’s full review here .

I am on an advisory board for a research centre at the University of Warwick where I studied Economics (the no.1 place in the UK to study it according to last week’s Sunday Times). It’s called CAGE (Competitive Advantage in the Global Economy) and has published many interesting pieces over the years helping to shape policy and debate. However on a more fun theme it has very recently been associated with a report that debunked an old assertion that winning the lottery doesn’t make you happy. It’s been in a lot of newspapers over the last few days with the new research suggesting (using a much bigger sample than earlier work on this topic) that it absolutely does make you happier and the bigger the better. This made me smile as our new house was commissioned over a hundred years ago by someone that won a small lottery in the UK around the time of WWI. However much of the infrastructure (windows, plumbing, electrics, drainage etc.) hadn’t been touched since and as such I now feel like I’ve lost a lottery renovating it. However I’m blissfully happy living there so I can confirm that spending money you don’t have can also make you very happy – well at these interest rates it can.

One part of the world that’s not very happy at the moment is the global manufacturing sector and today brings the final PMIs/US ISM on this front with Europe’s numbers the most important. Ahead of that, the Chicago PMI yesterday wasn’t indicative of strong activity. Indeed the 47.1 reading for September compared to expectations for an even 50.0 and the print represented a decline of 3.3pts from August. Yesterday’s number tied for the third worst reading in this cycle although it did hit as low as 44.4 in July, although that means the three-month average is just 47.3. More concerning were some of the details though with the employment component at 45.6 which means the quarterly average of 44.1 is the lowest since Q4 2009. Our US economists also made the point that the ISM adjusted for the Chicago PMI was 46.2 and the lowest since 2009.

This comes ahead of today’s September US ISM manufacturing report. A reminder that the August reading fell into contractionary territory at 49.1 for the first time since August 2016. The consensus today is for a slight rebound back to 50.0 and our US economists expect a 50.8 reading. The Chicago number is a worry though.

Ahead of the European PMIs remember that the flash Euro Area reading fell to just 45.6 while Germany hit 41.4. France also only just stayed in expansionary territory at 50.3. We’ll also get a look at the non-core with Italy expected to print at 48.1, while here in the UK the consensus expects a 47.0 reading.

So a rare chance to focus on the data following what feels like nothing but politics for the past few weeks. As for markets, the partial walk back over the weekend of the US restricting capital to China story helped the S&P 500 and NASDAQ to gains of +0.50% and +0.75% respectively last night. Markets got a further boost after Peter Navarro said that the reports about capital controls were “inaccurate.” He’s one of the biggest China hawks in the White House, so his denial carries more weight. On the impeachment front, there weren’t any major new developments, though President Trump’s personal lawyer Rudy Giuliani was subpoenaed by the House Intelligence Committee. Our economists did note, that amid the heightened political noise, the Baker, Bloom, Davis economic policy uncertainty index has risen to 6-year high. Meanwhile, overnight the New York Times reported that President Trump pushed the Australian prime minister during a recent telephone call to help Attorney General William P. Barr gather information for a Justice Department inquiry that Trump hopes will discredit the Mueller investigation.

This morning in Asia markets are largely up in thin trading as Chinese and Hong Kong markets are closed. The Nikkei (+0.76%), Kospi (+0.53%) and ASX (+0.09%) are all higher. Elsewhere, futures on the S&P 500 are up +0.41% while yields on 10yr JGBs are up +5.6bps to -0.170% as a 10yr note auction saw the weakest demand since 2016 in the wake of a steady cutback in bond purchases by the BoJ. Yields on 10Y USTs are also up +3.6bps this morning. As for overnight data releases, Japan’s final September manufacturing PMI came out in line with the initial read of 48.9 while the Q3 Tankan survey results were largely better than expected. Meanwhile, South Korea’s September manufacturing PMI came in at 48.0 (vs. 49.0 last month) while CPI came in at -0.4%yoy (vs. -0.3%yoy expected) and exports printed at -11.7%yoy (vs. -9.6%yoy expected) with imports standing at -5.6%yoy (vs. +0.8% yoy expected).

In terms of markets, Europe also had a good day yesterday with the STOXX 600 (+0.35%) rising to its highest closing level in more than 16 months. It was a quiet quarter end for bond markets with 10y Treasuries and Bunds little changed by the end of play although Treasuries did rally a couple of basis points after that Chicago PMI data. Meanwhile, the dollar rallied (+0.27%; up a further +0.11% this morning) to its strongest level in 29 months, to the disadvantage of both oil (-1.83%) and gold (-1.59%).

Meanwhile on Brexit, Irish broadcaster RTE reported overnight that the UK has proposed customs checks five to 10 miles away from the Irish border with PM Johnson likely to present his plans to Brussels later this week. The Irish finance minister has already responded to the reports and said this plan would be a “non-starter”. The Daily Telegraph reported late last night that PM Johnson will unveil his detailed Brexit plan to EU leaders within the next 24 hours. The report added that the plan is expected to be based on the creation of an all-Ireland “economic zone” which would allow agricultural and food products to move between Ulster and the republic without checks at the border, and on customs the plan is expected to rely on technology and “alternative arrangements,” such as trusted-trader schemes and exemptions for small businesses. Elsewhere, the Times reported that PM Johnson is likely to ask the EU to rule out a further extension as part of a new Brexit deal. Assuming there is a deal agreed which still appears a Herculean effort, this would force MPs to back this deal or risk crashing out with no deal. It would put pressure back on the MPs desperate to avoid no deal. However to get to such a scenario remains a very big ask.

Moving to fiscal, late yesterday Italy released its new budget outlook document which sets a target for a 2020 deficit at 2.2% of GDP and aims to boost growth to 0.6%. This means that the structural deficit will worsen by 0.1pp next year, instead of the 0.6pp improvement that Italy had committed to, while debt will rise to 132.5% in 2019 and start declining only slowly in the following years. Finance Minister Roberto Gualtieri wrote in the outlook document that ”The debt rule would not be satisfied in any of its configurations. But the reduction in the debt-to-GDP ratio in 2022 compared to the previous year would be significant, at 2.2 percentage points.”

In other news, the overnight speech by Chinese President Xi fell shy of delivering any remarks on trade and instead focused on national unity and Xi reiterated the commitment towards China’s complete unification. Meanwhile, Japan’s planned sales tax hike to 10% from 8% takes effect today.

Back to yesterday where the other US data release was the September Dallas Fed manufacturing survey which nudged down to 1.5, albeit slightly better than the consensus for 1.0, but still down 1.2 points. Meanwhile in Europe the data included German retail sales, which were in line with expectations at 0.5% mom, though the previous figures were revised up meaningfully. Also, the German unemployment rate stayed steady at 5.0%, while Italy’s jobless rate fell to 9.5%, its lowest level since 2011, though almost all of the most recent decline was due to declining labour force participation rates rather than higher employment.

Looking at the day ahead, the focus this morning will be on the aforementioned PMIs while other data releases in Europe include September house prices data in the UK and September CPI for the Euro Area. In the US this afternoon we’ve got the September ISM manufacturing, manufacturing PMI and August construction spending. Later today we’re also expecting September vehicle sales. Away from the data we’re due to hear from the Fed’s Evans this morning at a Bundesbank conference while later this afternoon Clarida and Bowman will speak. We’ll also hear from the Bundesbank’s Weidmann this evening.

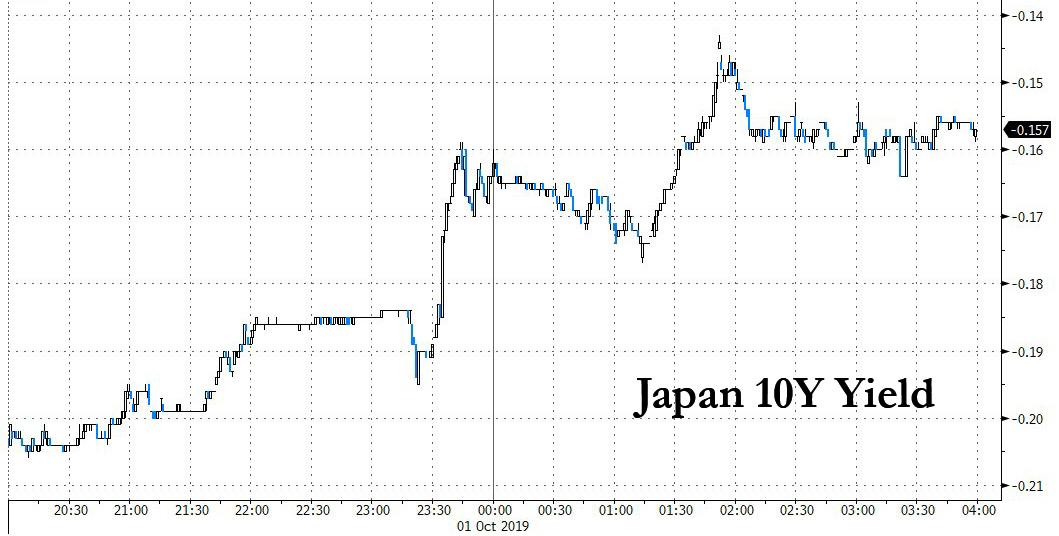

Japanese Bond Crash, Margin Call Sends Shockwaves Around The Globe

For a dramatic preview of what will happen in a flash to all those record low interest rates without the backstop of central banks and ravenous pension fund, look no further than what happened in Japan overnight, where bond futures suffered the biggest one-day crash since August 2, 2016, sliding as much as 0.97 yen to 154.05, and triggering margin calls for investors after the worst 10-year debt auction in three years.

More ominously, once the rout started it quickly spread outside of Japan, because as yields jumped, the sell-off spilled into US Treasuries and European debt.

There were three things behind the swift collapse: the first catalyst was the Bank of Japan’s Monday decision to slash bond purchases in October for the four major maturity buckets in order to steepen the curve and avoid further flattening which Kuroda has repeatedly expressed concern about in the past; the BOJ had indicated it may even stop buying debt of more than 25 years. It also sought to anchor yields from the one-to-three year zone by raising purchases in a regular operation earlier in the day and lifting the purchase band for the sector in October.

“The BOJ is showing its clear intention to correct distortions in the curve through flexible adjustments in market operations,” said Mari Iwashita, chief market economist at Daiwa. “While cutting the lower end of purchases in bonds maturing over 25 years to zero looks shocking, the BOJ will probably cut buying in this zone slowly.”

“The BOJ’s operation change had a huge psychological impact,” said Eiji Dohke, chief bond strategist at SBI Securities in Tokyo. “Investors are reluctant to buy given the risk of the BOJ skipping a purchase.”

Then, there was the announcement by Japan’s Government Pension Investment Fund (GPIF) that it was pivoting toward buying more FX-hedged foreign debt. Specifically, the world’s largest pension fund said it will consider currency-hedged overseas bond holdings as similar to domestic debt investments. That would allow GPIF to buy more foreign debt, as it’s already close to the 19% limit in its current mandate; and while good news for US Treasurys this was bad news for local JGBs.

Takahiro Sekido, a strategist at MUFG Bank, estimated GPIF may allocate more than 30% of its existing JGB holdings to currency hedged-foreign bonds: “There could be many funds following GPIF’s allocation change,” said Sekido, a former BOJ official.

As it turned out, he was right, and as Bloomberg put it, “all of a sudden, investors were left wondering what other changes were in store.”

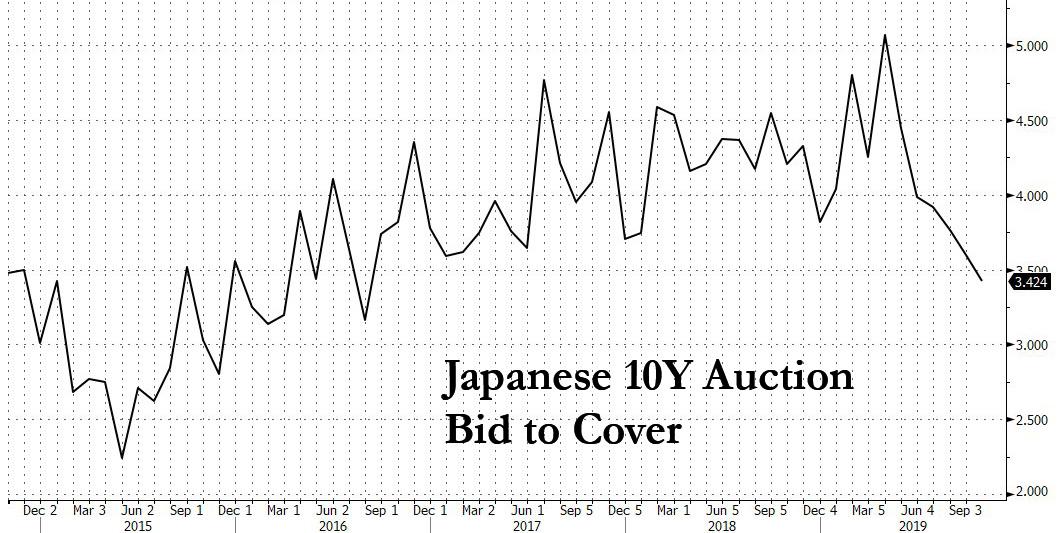

Then the cherry on top came on Tuesday morning, when the latest 10-year JGB auction confirmed the investor panic as the debt drew a bid-to-cover ratio of 3.42, the lowest since 2016, with the cut-off price of 102.33 falling short of the 102.64 estimated by traders, while the 0.29 tail was widest since March 2015. If Japan can ever have a failed bond auction, this was about as close to it as it could get.

The “auction results were much worse than expected amid increased caution after the BOJ cut bond purchases on Monday”, says Eiji Dohke, chief bond strategist at SBI Securities in Tokyo. He noted that the “results reflect caution that the central bank may refrain from buying bonds during one of its regular operations in October” and said that given the weak outcome of Tuesday’s sale, JGB volatility is likely to remain elevated until the BOJ’s policy meeting at month-end and investors will be wary about taking positions.

Following this three-peat of doom for bond bulls, yields on Japan’s 10-year cash bond rose 5.5 basis points to minus 0.16%. The heavy selling sparked a margin call at the Japan Securities Clearing Corp, which then drove prices even lower in a second acute selloff about two hours later.

Tuesday’s rout was merely the latest hit for Japanese sovereign bonds, which were already reeling from a dismal September, when they lost 1.1%, their first monthly drop since April.

And as JGBs dumped, so did Bunds and US Treasurys in a coordinated global move that saw yields in the US and German both spike as a result of tremors started in little, old Japan, confirming that once the central banks lose control, the collapse will be quick and painful (this is for all you MMT watchers out there).

Summarizing this ominous day for Japan’s bond market – and economy – MUFG Bank’s Takahiro Sekido put it best: “Japanese bonds have reached the point where it’s almost impossible to buy.”

For the sake of Japan, the global bond market, and the entire global financial system, he better be wrong.

Credit Suisse COO Resigns Over Spying Scandal; CEO Thiam Spared

As expected, the Credit Suisse board has exonerated CEO Tidjane Thiam, ensuring that Thiam, who first took over the leadership of the Swiss banking giant back in March 2015, won’t be pushed out over a scandal that began as an argument between two neighbors over “suburban shrubbery.”

Unfortunately, another C-Suite executive wasn’t so lucky: COO Pierre-Olivier Bouee was forced to step down after taking the fall for hiring the private security company Investigo to tail former Credit Suisse banker Iqbal Khan, who is on ‘gardening leave’ before starting a new job at cross-town rival UBS.

Pierre-Olivier Bouee

According to Bloomberg, the board said Bouee “acted alone”, and there was “no evidence that Thiam or the board knew about his actions.”

Losing Bouee won’t be easy for Thiam. The executive had been Thiam’s top lieutenant for more than 10 years at three different companies. Bouee submitted his resignation after the board heard ‘more details’ about the ‘surveillance operation’ carried out against Khan – an operation that ended with a confrontation between Khan and three Investigo agents in Zurich.

The bank started spying on Khan early last month over fears that he might be trying to poach bankers and clients from Credit Suisse to boost his profile at UBS.

The investigation was carried out by independent law firm Homburger after the story blew up in Swiss tabloids (though it hasn’t moved beyond the business pages in the English-language press), FT reports.

“The COO said that he alone, in order to protect the interests of the bank, decided to initiate the observation of Iqbal Khan, and that he did not discuss it with Credit Suisse’s chief executive or any other member of Credit Suisse’s executive board, the chairman of the board of directors of Credit Suisse, or the chairman of its audit committee,” the bank said.

With the board’s decision, the scandal will likely fade. However, mere hours before the bank’s announcement, it was reported that the Credit Suisse contractor who had hired the private detectives to tail Khan committed suicide. The contractor, whose name wasn’t given, fatally shot himself one week ago according to reports that first appeared in Swiss media.

CS said it appointed James Walker to replace Bouee as COO. Walker is currently the head of several senior roles in the bank’s finance organization, including as CFO for several critical US subsidiaries. In addition to Bouee, CS’s head of global security services also resigned, the bank said.

Initially, many suspected that the spying scandal might topple Thiam as it played out across the pages of several Swiss tabloids. Yet, several of CS’s largest executives expressed their support for Thiam, and convinced the board to follow their recommendation. Many suspect that the real reason Thiam managed to hang on is because the bank doesn’t have a clear succession plan, and instability at the top could be bad for the share price.

Protester Shot In Chest During Hong Kong ‘National Day’ Demonstrations

An illegal march in Hong Kong held on Tuesday to coincide with the 70th anniversary of Communist Party rule in China had mostly petered out by the late afternoon, as the bulk of protesters left the starting point near Sogo, the SCMP reports.

Still, as has become a pattern in recent weeks, a small but dedicated group of protesters clashed with police, hurling Molotov cocktails and coming to physical blows.

But for the first time since the protests started four months ago, a protester was shot by Hong Kong police officers on Tuesday.

As video circulating online shows, a group of protesters attacked a police van, hurling sticks and other projectiles. Several officers got out and tried to chase them away, but one of the officers slipped and fell to the ground, where he was assaulted by several protesters.

That reportedly led to the firing of several warning shots at the intersection of Waterloo and Nathan Roads in Kowloon. The shots can be heard in the video below:

A video circulating online shows warning shots fired as protesters and police clash at the junction of Waterloo and Nathan Roads pic.twitter.com/8WZPtAFhwC

Two officers suffered head injuries during the attack.

Two police officers fired live-round warning shots skywards in Waterloo road, Kowloon after two police vehicles attacked by protesters. https://t.co/y4RycTJyVV

Shortly after this incident, during a separate scene on Hoi Pa Street in Tsuen Wan, a man was shot in the chest with a live round: First responders and police were seen tending to the victim at the scene, though it’s unclear whether he survived the shooting.

Outside Beijing’s representative offices in Admiralty, police lobbed tear gas at protesters and sprayed crowds with blue-colored water,Reuters reports.

Once again, HK mass transit shut down, with 25 out of 91 stations closed across the city, including the entire Tsuen Wan line.

According to SCMP, five live rounds were fired during Tuesday’s demonstrations. Though police haven’t commented on the shootings, Reuters reports that the police said protesters threw a ‘corrosive fluid’ on officers in Tuen Mun, wounding several officers and reporters.

It’s worth pointing out that the timing of this unprecedented escalation. Beijing has been pushing hard to discredit the protest movement, an effort that has met with limited success. But could this be the ultimate coup by the protesters to win back the sympathy of all Hong Kongers and rejuvenate the movement?

Two countries, the US and UK, both seem to barrel down towards great troubles, hence the title Twisted Pair. When I set it up yesterday, I was going to write an essay combining the two, but it now looks like there’s going to have to be two separate essays. Still, I’m wondering how connected both are, and how they’re connected.

And I don’t mean in the popular Boris equals Trump sense, I find the role of for instance the respective intelligence communities and media far more interesting than such cheap ‘solutions’. That’s for the MSM to sell to you, not me.

Let’s start with the US.

Over the past few days, a series of snippets have appeared that each make me think: can this be true? The first such snippet is that House Intelligence Committee head Adam Schiff supposedly sat on the ‘whistleblower’ complaint for over a month.

By the way, the term whistleblower is a terrible misnomer, but everyone’s using it, can’t undo that anymore. Still, you can’t be a CIA agent, be planted somewhere, leak on what goes on there and then be labeled a whistleblower. That works only if you share CIA secrets.

Niceties aside, it appears that Schiff sat on the complaint since August 12. First question is: why? But there are other questions as well. Two weeks ago, Schiff complained that acting DNI chief Joseph Maguire refused to share the contents of the complaint with Congress. But Maguire did that only after consulting with his legal counsel:

Schiff ripped Maguire for breaching a law that requires him to share with Congress any whistleblower complaint deemed urgent by the intelligence community’s inspector general. He said the confluence of factors led him to believe the complaint involved Trump or other senior executive branch officials.

But DNI general counsel Jason Klitenic insisted in a letter to Schiff on Tuesday that Maguire had followed the letter of the law in blocking the transmission of the complaint to Congress. The whistleblower statute governing his agency, he said, only applies when the complaint involves a member of the intelligence community. Because it was aimed at a person outside the intelligence community, he said, the whistleblower statute does not apply to this scenario.

Under the statute, Klitenic stated, deeming a whistleblower complaint “urgent” is only valid when it applies to conduct by someone “within the responsibility and authority” of the DNI. Therefore, he said, after consulting with the Justice Department, he determined the complaint did not qualify as an “urgent” concern requiring transmittal to Congress.

Note the date. Also note the term ‘urgent’. Which didn’t keep Schiff from sitting on it for 5-6 weeks. And note that Schiff knew what was in the complaint, despite Politico reporting that “the confluence of factors led him to believe the complaint involved Trump or other senior executive branch officials.”

Okay, so why did he sit on the letter? Is it possible this has been a set-up all along? Snippet no. 2 became known on September 24:

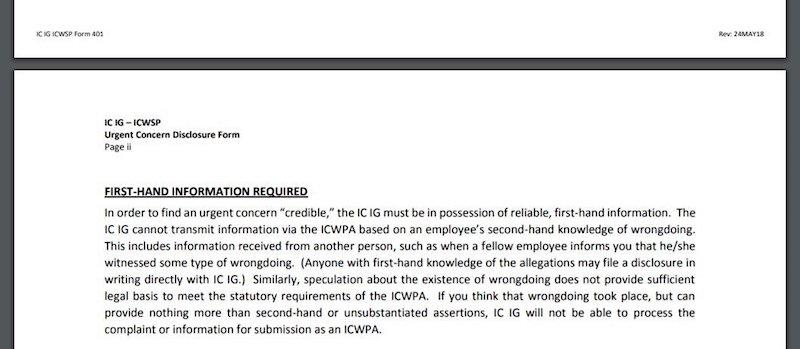

Between May 2018 and August 2019, the intelligence community secretly eliminated a requirement that whistleblowers provide direct, first-hand knowledge of alleged wrongdoings. This raises questions about the intelligence community’s behavior regarding the August submission of a whistleblower complaint against President Donald Trump. The new complaint document no longer requires potential whistleblowers who wish to have their concerns expedited to Congress to have direct, first-hand knowledge of the alleged wrongdoing that they are reporting.

The brand new version of the whistleblower complaint form, which was not made public until after the transcript of Trump’s July 25 phone call with the Ukrainian president Volodymyr Zelensky and the complaint addressed to Congress were made public, eliminates the first-hand knowledge requirement and allows employees to file whistleblower complaints even if they have zero direct knowledge of underlying evidence and only “heard about [wrongdoing] from others.”

The internal properties of the newly revised “Disclosure of Urgent Concern” form, which the intelligence community inspector general (ICIG) requires to be submitted under the Intelligence Community Whistleblower Protection Act (ICWPA), show that the document was uploaded on September 24, 2019, at 4:25 p.m., just days before the anti-Trump complaint was declassified and released to the public.

Here’s what the requirements looked like before the changes:

Why were the changes made? Who authorized them? Can anyone who hears something from their gossipy aunt now become a whistleblower? Can the aunt?

And then a few days ago there was this little tid-bit, snippet no. 3, which seems to fit right into a pattern:

Back in December 2018 CTH noted the significant House rule changes constructed by Nancy Pelosi for the 116th congress [..] With the House going into a scheduled calendar recess, those rules are now being used to subvert historic processes and construct the articles of impeachment. A formal vote to initiate an “impeachment inquiry” is not technically required; however, there has always been a full house vote until now.

The reason not to have a House vote is simple: if the formal process was followed the minority (republicans) would have enforceable rights within it. Without a vote to initiate, the articles of impeachment can be drawn up without any participation by the minority; and without any input from the executive. This was always the plan that was visible in Pelosi’s changed House rules.

Anyone can be a whistleblower, all it takes is for the intelligence community to express an interest in your aunt’s gossip. And then anything anyone says can be used to draw up an article of impeachment. Which can then be voted on by the Democrat majority in Congress, and accepted.

Which has no practical meaning, obviously, because there will be no Senate majority to actually impeach Trump. It’s pure theater. And anyway, impeached for what? For asking Ukraine assistance in investigating 2016 election meddling? Sure, you can rephrase that as “digging up dirt”, but isn’t that phrasing by now a purely partisan thing and hence worthless?

I see two options. A few days ago I wrote: “Pelosi called for impeachment without having seen the transcript or the complaint. That will forever be weird.” If that is true, as we’ve been led to believe by both the protagonists and the press, it is weird indeed. But now there is another option on the table.

Namely, that Pelosi has known the contents of the complaint since August 12, when the ‘whistleblower’ wrote to Adam Schiff, or soon thereafter. And that she, too, sat on it. Urgent or not. And then a few days ago went all-in for impeachment. No matter what the exact details here are, it very much looks like a well-prepared operation, step by step.

I started out with the term Twisted Pair for the US and UK, because both countries raise the question: how are they going to remain governable? Leave or Remain, GOP or Democrat, the trenches are being dug deeper fast. The only way forward appears to be even deeper divides. GOP and Democrats are a Twisted Pair all by themselves.

PS: I don’t get the attention for the whistleblower. The only interesting parties involved are the people who fed him/her their info. Are they also CIA by any chance? Let’s ask them.