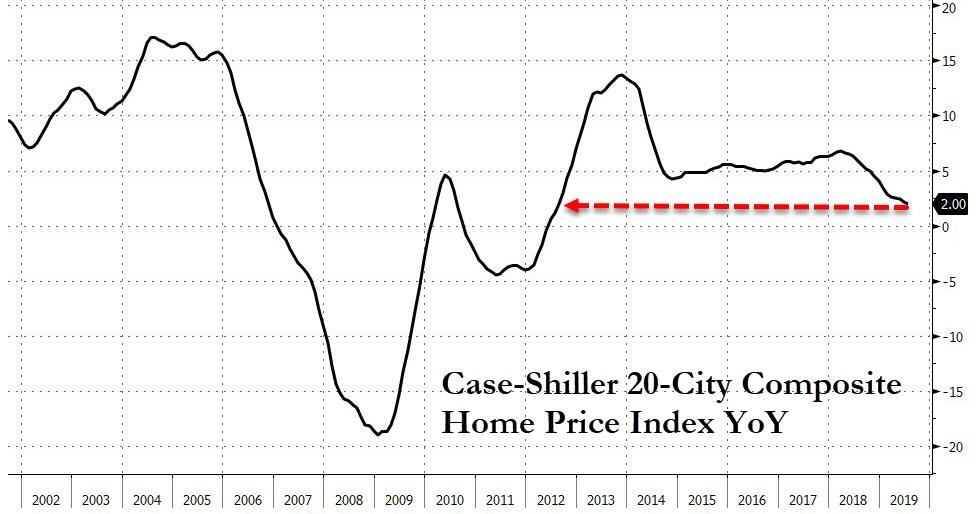

US Major City Home Price Growth Slumps To Weakest In 7 Years

S&P CoreLogic Case-Shiller’s 20-City Composite price index rose just 2.00% YoY in July – the weakest growth since August 2012.

The MoM rise of just 0.02% notably missed expectations of a 0.1% rise and the drop from a revised 2.16% YoY was also a sizable acceleration in the decline.

Source: Bloomberg

Nationally, home-price gains remained steady, rising at a 3.2% pace.

“Year-over-year home prices continued to gain, but at ever more modest rates,” Philip Murphy, global head of index governance at S&P Dow Jones, said in a statement.

“Gains remained positive in low-single digits in most cities, and other fundamentals indicate renewed housing demand.”

With a six-month lag, there is hope though that the collapse in mortgage rates may help home prices rebound once again…

Source: Bloomberg

All 20 cities in the index showed year-over-year gains except for Seattle, where prices were down 0.6% from a year earlier. Phoenix, Las Vegas and Charlotte reported the best annual gains among the 20 cities, led by a 5.8% gain in Phoenix.

In the classic game of “chicken,” two drivers race directly toward each other, and the first to swerve is the “loser.” If neither swerves, both will probably die. In the past, such scenarios have been studied to assess the risks posed by great-power rivalries. In the case of the Cuban missile crisis, for example, Soviet and American leaders were confronted with the choice of losing face or risking a catastrophic collision. The question, always, is whether a compromise can be found that spares both parties their lives and their credibility.

There are now several geo-economic games of chicken playing out. In each case, failure to compromise would lead to a collision, most likely followed by a global recession and financial crisis.

The first and most important contest is between the United States and China over trade and technology.

The second is the brewing dispute between the US and Iran.

In Europe, there is the escalating brinkmanship between British Prime Minister Boris Johnson and the European Union over Brexit.

Finally, there is Argentina, which could end up on a collision course with the International Monetary Fund after the likely victory of the Peronist Alberto Fernández in next month’s presidential election.

In the first case, a full-scale trade, currency, tech, and cold war between the US and China would push the current downturn in manufacturing, trade, and capital spending into services and private consumption, tipping the US and global economies into a severe recession. Similarly, a military conflict between the US and Iran would drive oil prices above $100 per barrel, triggering stagflation (a recession with rising inflation). That, after all, is what happened in 1973 during the Yom Kippur War, in 1979 following the Iranian Revolution, and in 1990 after Iraq’s invasion of Kuwait.

A blowup over Brexit might not by itself cause a global recession, but it would certainly trigger a European one, which would then spill over to other economies. The conventional wisdom is that a “hard” Brexit would lead to a severe recession in the United Kingdom but not in Europe, because the UK is more reliant on trade with the EU than vice versa. This is naive. The eurozone is already suffering a sharp slowdown and is in the grip of a manufacturing recession; and the Netherlands, Belgium, Ireland, and Germany – which is nearing a recession – do in fact rely heavily on the UK export market.

With eurozone business confidence already depressed as a result of Sino-American trade tensions, a chaotic Brexit would be the last straw. Just imagine thousands of trucks and cars lining up to fill out new customs paperwork in Dover and Calais. Moreover, a European recession would have knock-on effects, undercutting growth globally and possibly triggering a risk-off episode. It could even lead to new currency wars, if the value of the euro and pound were to fall too sharply against other currencies (not least the US dollar).

A crisis in Argentina could also have global consequences. If Fernández defeats President Mauricio Macri and then scuttles the country’s $57 billion IMF program, Argentina could suffer a repeat of its 2001 currency crisis and default. That could lead to capital flight from emerging markets more generally, possibly triggering crises in highly indebted Turkey, Venezuela, Pakistan, and Lebanon, and further complicating matters for India, South Africa, China, Brazil, Mexico, and Ecuador.

In all four scenarios, both sides want to save face. US President Donald Trump wants a deal with China, in order to stabilize the economy and markets before his re-election bid in 2020; Chinese President Xi Jinping also wants a deal to halt China’s slowdown. But neither wants to be the “chicken,” because that would undermine their domestic political standing and empower the other side. Still, without a deal by year’s end, a collision will become likely. As the clock ticks down, a bad outcome becomes more likely.

Similarly, Trump thought he could bully Iran by abandoning the Joint Comprehensive Plan of Action and imposing severe sanctions. But the Iranians have responded by escalating their regional provocations, knowing full well that Trump cannot afford a full-scale war and the oil-price spike that would result from it. Moreover, Iran does not want to enter negotiations that would give Trump a photo opportunity until some sanctions are lifted. With both sides reluctant to blink first – and with both Saudi Arabia and Israel egging on the Trump administration – the risk of an accident is rising.

Having perhaps been inspired by Trump, Johnson naively thought that he could use the threat of a hard Brexit to bully the EU into offering a better exit deal than what his predecessor had secured. But now that Parliament has passed legislation to prevent a hard Brexit, Johnson is playing two games of chicken at once. A compromise with the EU on the Irish “backstop” is still possible before the October 31 deadline, but the probability of de facto hard-Brexit scenario is also increasing.

In Argentina, both sides are posturing. Fernández wants a clear electoral mandate, and is campaigning on the message that Macri and the IMF are to blame for all the country’s problems. The IMF’s leverage is obvious: if it withholds permanently the next $5.4 billion tranche of funding and ends the bailout, Argentina will suffer another financial collapse. But Fernández has leverage, too, because a $57 billion debt is a problem for any creditor; the IMF’s ability to help other distressed economies would be constrained by an Argentinean collapse. As in the other cases, a face-saving compromise is better for all, but a collision and financial meltdown cannot be ruled out.

The problem is that while compromise requires both parties to de-escalate, the tactical logic of chicken rewards crazy behavior. If I can make it look like I have removed my steering wheel, the other side will have no choice but to swerve. But if both sides throw out their steering wheels, a collision becomes unavoidable.

The good news is that in the four scenarios above, each side is still talking to the other, or may be open to dialogue under some face-saving conditions.

The bad news is that all sides are still very far from any kind of agreement.

Worse, there are big egos in the mix, some of whom might prefer to crash than be perceived as a chicken.

The future of the global economy thus hinges on four games of daring that could go either way.

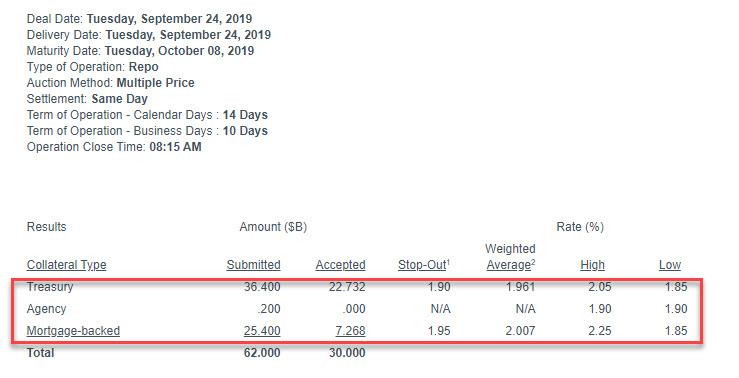

Fed’s Term Repo 2x Oversubscribed As Banks Brace For Quarter End Funding Shortage

The NY Fed’s first term repo operation in over a decade, which has a 14 day term and thus captures the liquidity-draining quarter end period, has just concluded, and it confirmed that banks are hunkering down ahead of quarter-end, by tendering some $62BN in securities for the $30BN operation, making it more than 2x oversubscribed.

And while we await the details of the regular, overnight repo to be printed, which is being held again today, and every day into October, here are some more details on today’s term repo:

The NY Fed accepted $22.7BN of Treasuries at a stop-out rate of 1.90%, with a weighted average rate was 1.961%, both well above IOER and confirming that there was indeed quite a bit more demand than supply.

And while the Fed did not accept agency debt, it accepted $7.27BN of mortgage-backed debt at 1.95%, with a weighted average rate of 2.007%

To be sure, the Fed’s term-repo was always expected to be heavily used, which is also why there are at least two more $30BN term repos this week, which assuming there was just $32BN in additional submissions that did not get access to the Fed’s facility, should be more than met with little need for the third and final term repo. Alternatively, some banks may be simply waiting to get closer to the quarter end before tipping their cards: after all, just like the Discount Window, the repo operation has become the modern “stigmatizing” equivalent, and if reporters or clients get a whiff that a bank is in a dire liquidity state, the consequences could be dramatic.

Furthermore, the closer we get to quarter end, the tighter liquidity will get, and as a result, the overnight general collateral repo rate rose on Tuesday after trading within the Federal Reserve’s target range late last week: according to ICAP GC repo opened at 2.10%/2%, before drifting lower to 2.05%/2.03%; meanwhile term repo rates continue to be in the mid-2% range.

Commenting on the upcoming cash crunch, Wrightson ICAP expected weekly Treasury bill settlements and the “early liquidity- chilling effects” of approaching quarter-end statement date to “start to move repo rates back up this morning”, and that’s precisely what happened.

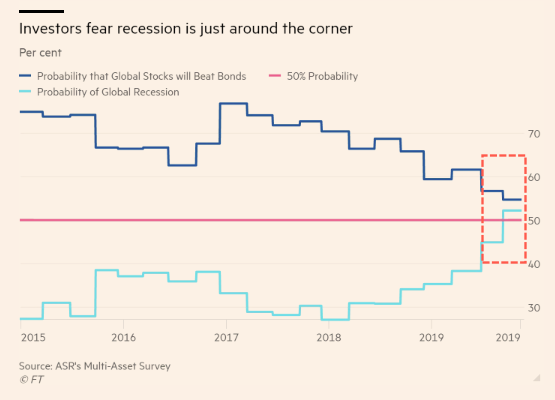

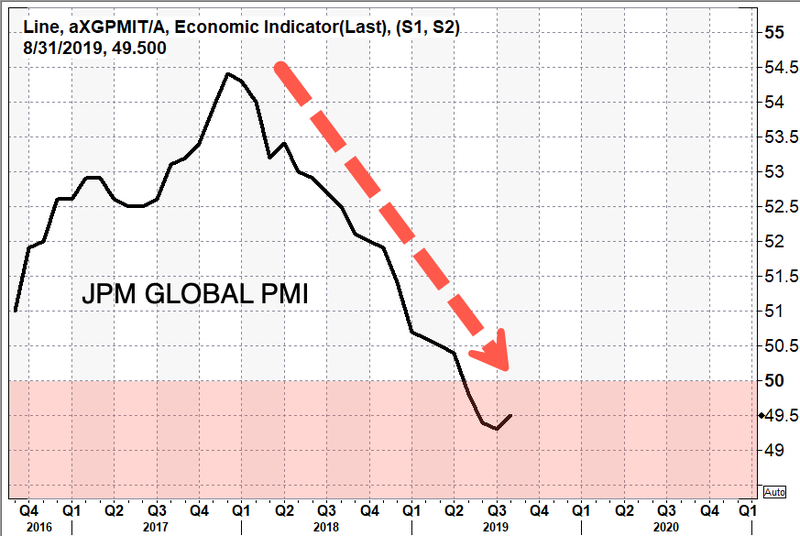

“Bearish Macro View:” Global Recession Fears Grow Among Top Money Managers

Economic data out of Europe and the US on Monday showed that manufacturing recessions are spilling over into services and employment. Global trade volumes are suddenly rolling over, and global central banks are cutting interest rates at the fastest clip since the last financial crisis, more than a decade ago. On Sunday, the Bank for International Settlements (BIS) warned about an impending financial crisis, while billionaire hedge fund manager Paul Singer is building cash to take advantage of the next stock market crash.

Economic storm clouds are quickly gathering across the world, and some of the top money managers are becoming more nervous than ever that economic doom is around the corner, according to Absolute Strategy Research (ASR), first reported by the Financial Times.

Nearly 52% of respondents said an economic downturn could arrive as early as next year — driven by investment uncertainty and trade tensions.

ASR created the survey in 2014, surveyed more than 200 institutions that manage a combined $4.1 trillion in assets, said this is the first time that more than 50% of respondents feel a recession could be imminent.

Many of the respondents expect US unemployment to increase over the next year.

“People have definitely bought into the bearish macro view,” said David Bowers, ASR’s head of research. “When you look at the pattern over the past four or five years, it is definitely quite an important inflection point.”

The ultra-bearish views of more than 50% of the respondents, keep in mind, they manage trillions of dollars, coincide with JPMorgan Global Manufacturing PMI printing sub 50. There’s even fear with respondents that the world is now stuck in a “low-growth trap” – where central banks are powerless to spark inflation.

Despite the doom and gloom, respondents still believed stocks could outperform bonds over the next year.

However, most thought it was less than a 50% chance that stocks will be higher a year from now.

ASR’s survey suggests respondents are hoping central banks can save the world again with unconventional monetary policy.

“They haven’t gone maximum defensive,” said Bowers. “People are thinking the cavalry is going to come quickly to create stimulus to provide that turnaround.”

But as we learned from the European Central Bank (ECB) earlier this month: “The room for monetary policy maneuver has narrowed further. Should a downturn materialize, monetary policy will need a helping hand, not least from a wise use of fiscal policy in those countries where there is still room for maneuver.”

So with that being said, respondents betting that extreme monetary policy will save the day this go-around is unwise.

It looks like they are really going to do it. The Democrats are actually preparing to begin impeachment proceedings, and as you will see below, one senior House Democratic aide is warning that “the dam could break on Thursday”.

That is the day when acting Director of National Intelligence Joseph Maguire is scheduled to testify to the House Intelligence Committee, and Democrats on that committee are going to make it exceedingly clear that they want the whistleblower complaint that is at the center of this latest political firestorm. It is being alleged that President Trump repeatedly pressured the president of Ukraine to investigate Joe Biden and his son Hunter at a time when Ukraine was desperate for military aid from the United States. President Trump has publicly admitted that he discussed Joe Biden’s corruption with the Ukrainian president, but he insists that he never actually pressured him to do anything. Trump is offering to release a full transcript of the call in order to prove his point, but that is not going to satisfy the Democrats. They want the whistleblower complaint, and they want it immediately.

According to Politico, some sources on Capitol Hill are saying that the possibility of impeachment proceedings is “approaching a certainty”, but so much depends on what happens later this week.

Over the course of this week, Democratic leaders are going to do all that they can to get their hands on the whistleblower complaint, and things are likely to come to a head on Thursday when acting Director of National Intelligence Joseph Maguire testifies before the House Intelligence Committee. The following comes from NBC News…

But House Democrats have been pulling together a wide-ranging case to impeach President Donald Trump on a series of alleged past and ongoing crimes against the country — a set of charges that goes far beyond the Mueller report — and all signs point to a possible public inflection point later this week, when acting Director of National Intelligence Joseph Maguire testifies before the House Intelligence Committee.

“The dam could break on Thursday,” one senior House Democratic aide, whose boss has not endorsed impeachment, told NBC News.

Previously, House Speaker Nancy Pelosi had been against impeachment, but now she appears to have changed her tune.

She is insisting that the whistleblower complaint must be turned over, and if that doesn’t happen the New York Times is warning that we should expect “a serious escalation from Congress”…

The fast-moving developments prompted Speaker Nancy Pelosi to level a warning of her own to the White House: Turn over the secret whistle-blower complaint by Thursday, or face a serious escalation from Congress.

By the end of this week, we should have a lot more clarity on what is about to happen.

But at this point, all of the signs are pointing in one direction. The following are 12 quotes that show that the Democrats are getting ready to impeach Trump…

–House Intelligence Committee Chairman Adam Schiff: “I have been very reluctant to go down the path of impeachment, for the reason that I think the founders contemplated, in a country that has elections every four years, that this would be an extraordinary remedy, a remedy of last resort, not first resort. But if the president is essentially withholding military aid at the same time that he is trying to browbeat a foreign leader into doing something illicit, that is, providing dirt on his opponent during a presidential campaign, then that may be the only remedy that is coequal to the evil that that conduct represents.”

–Congresswoman Carolyn B. Maloney: “I first called for impeachmemt back in June. These latest revelations re: POTUS and Ukraine are absolutely outrageous – they take impeachable offenses to a whole new level, and emphasize the urgency for IMMEDIATE action.”

–Congressman Al Green: “”It is time for the Congress to do its job and start the impeachment process, not an inquiry.”

–Representative John Larson: “The Director of National Intelligence must comply with the law on Thursday. If not, the Trump Administration has left Congress with no alternative but for the House to begin impeachment proceedings, which I will support.”

–House Speaker Nancy Pelosi: “The Inspector General determined that the matter is ‘urgent’ and therefore we face an emergency that must be addressed immediately.”

–House Intelligence Committee Chairman Adam Schiff: “This would be, I think, the most profound violation of the presidential oath of office, certainly during this presidency, which says a lot, but perhaps during just about any presidency. There is no privilege that covers corruption. There is no privilege to engage in underhanded discussions.”

–Congressman Al Green: “We are at the crossroads of accountability. Either we will hold the president accountable, or we will be held accountable.”

–Alexandria Ocasio-Cortez: “At this point, the bigger national scandal isn’t the president’s lawbreaking behavior – it is the Democratic Party’s refusal to impeach him for it.”

–Congressman Dean Phillips: “I came to Congress on a mission to clean up corruption and restore America’s trust in our government. The President’s pattern of behavior is corrupt at best, treasonous at worst, and puts our rule of law at risk.”

–Representative Pramila Jayapal: “It is a deeply serious time, and I think we have a constitutional crisis and I think there is only one remedy at this point.”

–Congresswoman Angie Craig: “We have a responsibility to ensure that no one is above the law — particularly our elected leaders. Yesterday, the President and his personal counsel confessed to asking the Ukrainian government to interfere with a political rival. Additionally, President Trump threatened to withhold military aid to our ally if they did not comply. It is clear that the sitting president of the United States placed his own personal interests above the national security of the United States. We must safeguard our electoral process and our very democracy from outside threats. For this reason, the current investigations into corruption must continue. And when there is an abuse of power of this magnitude, it is our responsibility to stand up for what is right. This is why I am calling to open impeachment proceedings — immediately, fairly, and impartially.”

And if impeachment proceedings do move forward, they won’t just be focused on the discussions that Trump has had with the president of Ukraine.

According to NBC News, Democrats are likely to include a whole host of “impeachable offenses” in their charges against Trump…

Democrats are also gathering evidence for possible obstruction of justice charges stemming from Special Counsel Robert Mueller’s investigation — including the eyewitness testimony the Judiciary Committee received from former Trump campaign manager Corey Lewandowski last week. Lewandowski testified that the president twice directed him to tell then-Attorney General Jeff Sessions to un-recuse himself and shut down Mueller’s investigation of Trump.

The other buckets of potentially impeachable offenses include obstruction of Congress, a category that covers a laundry list of efforts by Trump to prevent the House from obtaining testimony and documents from various federal officials, agencies and even people who do not work for the government — like Lewandowski — over whom Trump has sought to limit disclosures by asserting executive privilege.

The latest CNN count has 137 of the 235 Democrats in the House in support of impeachment, but the floodgates have now opened and more are coming out in favor of beginning impeachment proceedings with each passing day.

And with Democrats having a solid majority in the House, there is little doubt as to what the outcome would be.

But the problem for Democrats has always been the Senate where Republicans hold a slim majority. The Republicans currently hold 53 seats, and that always seemed to be an insurmountable obstacle to removing Trump from office.

However, things may have changed due to this latest scandal. At this point, even Senator Mitt Romney seems deeply troubled by what he is hearing…

Senator Mitt Romney of Utah, the Republican presidential nominee in 2012, was more critical, deeming it “critical for the facts to come out” and saying, “If the president asked or pressured Ukraine’s president to investigate his political rival, either directly or through his personal attorney, it would be troubling in the extreme.”

If push came to shove, it is probably likely that Mitt Romney would vote to remove Donald Trump, and if Trump was removed from office that would open up the door for him to make a run for the White House in 2020.

In addition to Romney, there are several other “moderate” Republicans that will be critical to the outcome of any push for impeachment. Many of them are not particularly fond of Trump, and Trump knows it.

Now we are on the verge of a constitutional crisis that could shake America to the core, and either way the end result is likely to leave tens of millions of Americans deeply angry.

Political tension has been rising to a breaking point for a long time in this nation, and this could be the spark that unleashes chaos that nobody is going to be able to control.

So let us hope for peace, and let us hope that the Democrats are not really as serious about impeachment as they appear to be at this moment.

* * *

Pelosi has scheduled a meeting Tuesday afternoon with the chairs of the six committees conducting investigations into Trump, according to a source familiar with the plan. House Democrats have also scheduled an unusual caucus meeting at 4 p.m. Tuesday in the Capitol. The topic remains unclear, but aides speculated it would focus on a path forward on impeachment.

Futures, Global Stocks Jump On “Trade Hopes And Optimism”

It’s time for some trade optimism again to lift stocks again, just in case we haven’t had that every other day for the past year.

Rekindled U.S.-China trade hopes lifted share markets on Tuesday, while the pound spiked after the latest dramatic Brexit twist, when the UK’s top court ruled the government’s suspension of parliament had been unlawful.

And good thing algos had some positive trade news to trade on as one day after a disastrous German PMI print, there was more gloomy data from Germany to contend with too, including the worst German IFO Expectations print in a decade, and which would suggest a -6% GDP print is on deck.

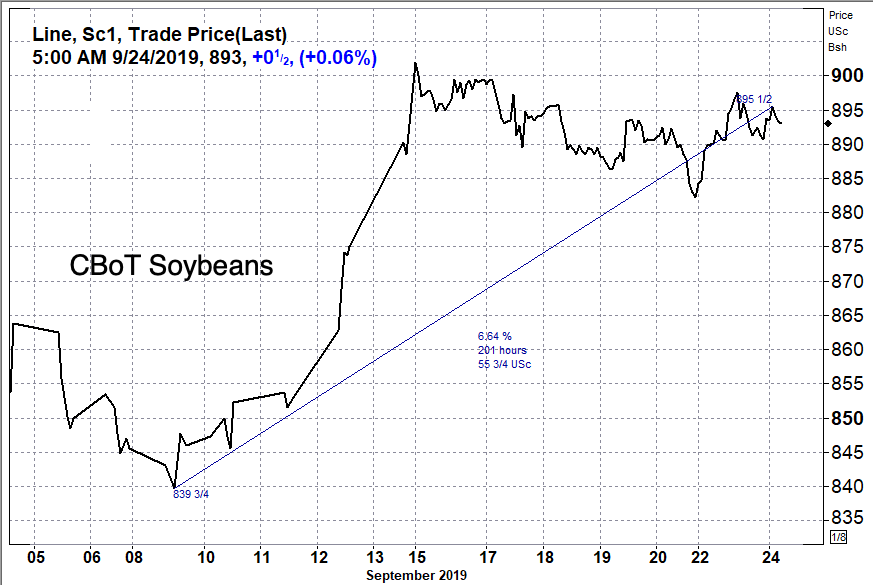

That data, however, was ignored after Treasury Secretary Steven Mnuchin’s and Trade Representative Robert Lighthizer confirmed on Monday that they would meet Chinese Vice Premier Liu He in two weeks’ time, while a separate report that China had granted new tariff waivers for US soybean purchases indicated Beijing may be telegraphing some more goodwill ahead of the negotiations.

“The comments (from Mnuchin on China trade talks) gave a little bit of boost to sentiment, but markets are still not that optimistic, either,” said Masahiro Ichikawa, senior strategist at Sumitomo Mitsui DS Asset Management. “It seems there have been a lot going on behind the scenes,” he said, referring to U.S. President Donald Trump’s questioning a decision by his top trade negotiators to ask Chinese officials to delay a planned trip to U.S. farming regions. That cancellation was seen by markets as a sign of trouble in the U.S.-China talks and sent stock prices tumbling on Friday.

As a result, U.S. index futures advanced with European stocks while Asian shares rose modestly as investors weighed renewed hopes for a trade deal – a catalyst for higher prices since the summer of 2018 – against increasingly recessionary economic data from around the globe. “A perceived lull in U.S.-China trade tensions has eased market fears about an economic downturn,” BlackRock strategists wrote in a note.

Not everyone was euphoric however: “All eyes are on early October, although there’s not a lot of expectation that anything material is going to come out from it,” John Lau, head of Asian equities at SEI Investments Co., said of the trade talks in an interview with Bloomberg Television. “If we get some kind of deal, any kind of deal, that would actually move markets.”

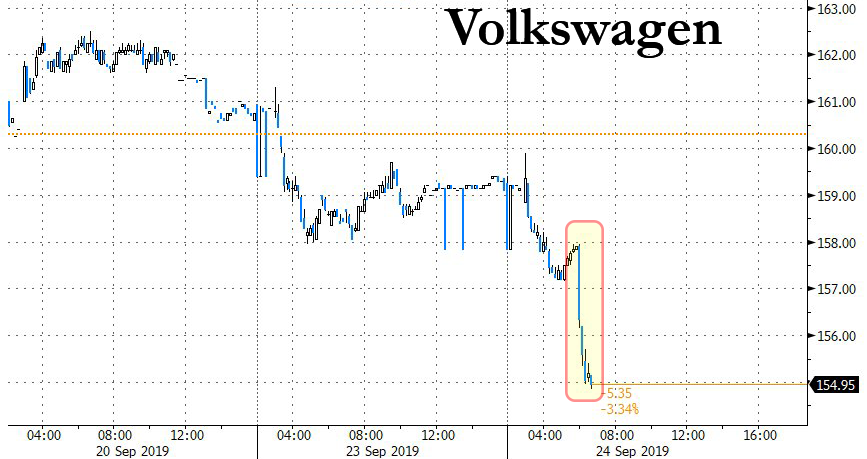

The European Stoxx 600 index rose 0.3%, with the eurozone banking index up 0.6% after it had slumped 2.8% in the previous session. European auto stocks stumbled following news that Volkswagen’s CEO and Chairman were charged with market manipulation over the emissions scandal, sending the company’s stock sliding and hitting the broader auto sector.

Earlier in the session, Asian stocks inched higher, led by energy producers while MSCI’s Asia index rose 0.1%, led by 0.6% gains in mainland Chinese shares after the vice head of China’s state planner said Beijing will step up efforts to stabilize growth. Markets in the region were mixed, with Japan and Singapore leading gains and Indonesia retreating. The Topix climbed 0.4% to its highest since April, with retail giants among the biggest boosts, after a three-day weekend. The Shanghai Composite Index added 0.3%, driven by Kweichow Moutai and Foxconn Industrial Internet. China has an abundant toolkit of monetary policy instruments, the Chinese central bank said in a statement. India’s Sensex fluctuated following its biggest two-day rally in 10 years, as Reliance Industries advanced and HDFC Bank declined.

Also overnight, Japan’s Foreign Minister Motegi said trade deal negotiations with US finished and that he doesn’t see much delay from goal of signing deal by end of the month, while a Foreign Ministry spokesman also said there is still have time to agree to a trade deal with US by end of the month. However, earlier reports suggested a deal may be delayed due to a disagreement regarding the auto tariffs and that an agreement will not be ready to sign when Japanese PM Abe meets US President Trump on Wednesday as it is still undergoing legal checks with the sides to sign separate documents confirming a final agreement.

Currency moves were mostly rangebound with the exception of the pound: traders had waited for a Supreme Court ruling on UK Prime Minister’s Boris Johnson five-week suspension of parliament — a move known as prorogation in Westminster speak — and when it came it was dramatic and blunt. The move was “unlawful”. Sterling initially climbed as high $1.2487 on the view it would help prevent the UK being bundled toward a ‘no-deal’ Brexit at the end of October. But it quickly ran out of momentum and retreated to $1.2460, up a modest 0.2% on the day.

“I wasn’t surprised to see the currency hop higher but I also wasn’t surprised to see cable (pound vs the dollar) run out of steam ahead of $1.25,” said TD Securities’ European head of currency strategy Ned Rumpeltin.

Johnson is now likely to head to his Conservative party’s annual conference at the weekend and rally his troops in preparation for a likely national election which will be a bitter fight over Brexit.

“He is going to have to rally his base and he is going to do that around hard Brexit,” Rumpeltin said. “That will be a moment of clarity for the FX market. It will look at the polling and the Conservatives are leading in the polls.”

In geopolitical news, President Trump said we’re getting along well with North Korea and maybe we will be able to make a deal or maybe not. South Korea spy agency said US-North Korea working level talks will take place in 2-3 weeks and a summit is possible by year-end, while it added North Korea’s leader Kim could attend Korea-ASEAN summit in Busan in November. Trump also said he will discuss Iran in his UN speech today, while he added the US have a lot of pressure on Iran and that he is not looking for a mediator on Iran – Trump is scheduled to speak at 10:15ET. In response, Iran President Rouhani said our message to the world is peace and stability, although there were earlier comments from a senior official that Iran will never yield to the US and the US should lift sanctions if it wants to reduce tensions.

Among the main commodities, oil prices dipped on expectations of subdued demand although uncertainty remained about whether Saudi Arabia would be able to fully restore output after recent attacks on its oil facilities. Brent crude futures fell 40 cents to $64.37 a barrel by 0624 GMT. West Texas Intermediate futures were down 33 cents to $58.31.

“The demand side of the equation is back in focus,” said Michael McCarthy, senior market analyst at CMC Markets in Sydney, pointing to sluggish manufacturing numbers in leading economies in Europe as well as Japan.

Boosting risk sentiment, on Monday, St. Louis Fed President James Bullard who now is clearly gunning for Powell’s chairman seat by coming up with increasingly dovish proposals, said the central bank may need to ease monetary policy further to offset downside risks from trade conflicts and too-low inflation. Not all policy makers are on the same page, though. People’s Bank of China Governor Yi Gang said the country isn’t in a rush to add massive monetary stimulus, while Francois Villeroy de Galhau admitted he opposed the ECB’s decision to restart quantitative easing.

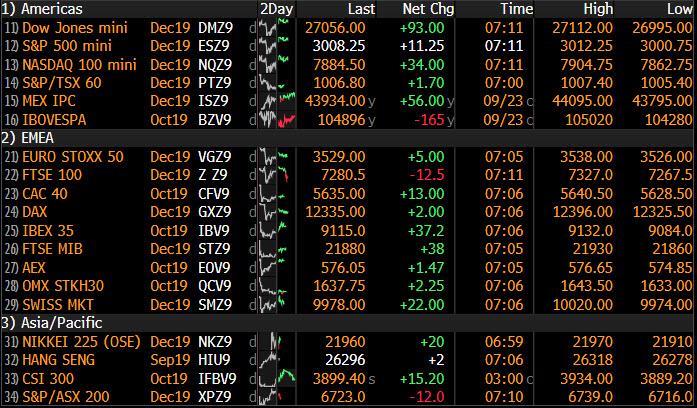

Market Snapshot

S&P 500 futures up 0.2% to 3,003.75

STOXX Europe 600 up 0.2% to 390.44

MXAP up 0.07% to 159.32

MXAPJ up 0.06% to 509.14

Nikkei up 0.09% to 22,098.84

Topix up 0.4% to 1,622.94

Hang Seng Index up 0.2% to 26,281.00

Shanghai Composite up 0.3% to 2,985.34

Sensex down 0.1% to 39,043.39

Australia S&P/ASX 200 down 0.01% to 6,748.87

Kospi up 0.5% to 2,101.04

German 10Y yield rose 0.5 bps to -0.576%

Euro unchanged at $1.0993

Italian 10Y yield fell 9.0 bps to 0.492%

Spanish 10Y yield fell 1.8 bps to 0.131%

Brent futures down 0.9% to $64.20/bbl

Gold spot down 0.1% to $1,520.39

U.S. Dollar Index little changed to 98.64

Top Overnight News from Bloomberg

The U.K.’s top judges dealt an unprecedented legal rebuke to Prime Minister Boris Johnson, branding his controversial decision to suspend Parliament unlawful and giving lawmakers another chance to frustrate his plans for Brexit

German businesses gave mixed signals on economy on Tuesday, a day after a report showed manufacturing stuck in an ever deeper slump; the Ifo institute’s key business sentiment gauge rose slightly more than expected in September, recording its first gain in six months; however, all of the increase was due to the view of the current situation, and a measure of expectations continued to plunge, reaching the lowest level in a decade

The Chinese government has given new waivers to several domestic state and private companies to buy U.S. soybeans without being subject to retaliatory tariffs, according to people familiar with the situation

Japan and the U.S. have finished talks on a trade deal with no indication yet on how the two sides responded to Trump’s threat to slap tariffs on the $50 billion in cars and parts shipped by Japan to the U.S. annually

Anheuser-Busch InBev NV has pulled off the year’s second-biggest IPO the second time around, raising about $5 billion in listing its Asian unit in Hong Kong two months after scrapping the original share sale

The U.K. government has ordered an investigation into the role of Thomas Cook Group Plc’s management in the collapse of the 178-year-old tour operator

Asian equity markets traded indecisively following a similar close on Wall St where the major indices spent the day steadily recouping the opening losses brought on by weak Eurozone PMI data. ASX 200 (U/C) was choppy as outperformance in gold stocks and resilience in financials were counterbalanced by losses across the broader market, while Nikkei 225 (+0.1%) remained afloat on return from the extended weekend but with gains capped by a choppy currency and as officials scrambled to finalize a US-Japan trade deal amid uncertainty regarding auto tariffs. Elsewhere, Hang Seng (+0.2%) and Shanghai Comp. (+0.3%) traded positively after continued PBoC liquidity efforts and as the central bank suggested there was still ample monetary policy tools, although advances were initially limited by the trade-related overhang as participants mulled over the recent ebbs and flows of the US-China trade saga ahead of next month’s high level talks. Finally, 10yr JGBs gained on return from the holiday closure amid the recent temperamental US-China trade headlines and indecisive risk tone in the region, while the BoJ were also present in the market today for JPY 810bln of JGBs in the belly to the short-end.

Top Asian News

PBOC’s Yi Says China Is ‘Not in a Rush’ to Ease Policy Massively

Global Investors Rethink India Stocks on Historic Tax Boost

Xiaomi Unveils First 5G Phone for China in Challenge to Huawei

The Danger When China’s Bull Market Owes So Much to So Few

Major European Bourses (Eurostoxx 50 +0.2%) are modestly firmer, albeit off highs, in tentative trade, following a mixed AsiaPac session. The FTSE 100 is the underperformer, under pressure from sterling strength after the UK Supreme Court ruled UK PM Johnson’s decision to prorogue parliament unlawful and, as such, prorogation voided. While stocks are mostly higher, the more defensive Utilities (+1.0%), Health Care (+0.9%) and Consumer Staples (+0.5%) sectors outperform, indicative of continued apprehension in wake of yesterday’s weak EZ PMI data, although the more risk sensitive IT and Financial are also higher. Materials (-0.5%) and Energy (-0.4%) are the laggards, with the latter pressure by lower crude prices. In terms of individual movers; Aviva (+0.8%) is higher on reports the Co. is looking to sell its Singapore and Vietnam businesses in a deal which could be valued at USD 2.5bln. Ryanair (+2.7%) is up, as the airline sector continues to gain in wake of Thomas Cook’s collapse and with the news that the co.’s cabin crew have voted in favour (approx. 80%) for a four-year Collective Labour Agreement. K+S (-4.3%) is lower after being downgraded at SocGen after the co. cut guidance yesterday, while Royal Mail (-2.8%) is under pressure after a downgrade at Liberum Capital. Finally, Volkswagen (-2.6%) sunk on the news thatGerman Prosecutors had indicted CEO Diess, Chairman Poetsch and the former CEO relating to the Diesel emissions scandal.

Top European News

German Manufacturing Drags Business Expectations to Decade Low

Scout24 Is Said to Kick Off Sale Process for Auto-Trading Unit

Danske’s Ex-CEO in Estonia Has Gone Missing; Police Start Hunt

HSBC Wins EU Court Fight Over $37M Fine for Euribor Rigging

In FX, GBP was firmer after the UK Supreme Court dealt a blow to UK PM Johnson after it ruled the decision as a court matter before announcing that the suspension was unlawful. With prorogation defeated, UK MPs will return to their seats and the parliamentary session will continue as Speaker John Bercow expectedly stated that the HoC should reconvene immediately. GBP/USD touched an intraday high of 1.2487 ahead of its 21 WMA at 1.2490, although the pair then returned to pre-announced levels of around 1.2450 amid unclarity regarding the next steps alongside some profit taking. It is worth nothing that, with parliament back in session, an anti-no deal majority could continue to frustrate government efforts to find a deal with the EU/try to force a no deal. Meanwhile, the Euro had relatively uninspiring day thus far as EUR/USD remains within a tight 1.0984-97 parameter with little impetus derived from the Ifo measures which mostly topped estimates (ex-expectations), although the institute noted that the outlook for the coming months has deteriorated and the domestic economy is likely to shrink in Q3 and stagnate in Q4, a similar comment mate by IHS yesterday. In terms of option expiries, EUR/USD sees 1.3bln at strike 1.10 and 1.1bln at strike 1.1025-30 for today’s NY cut.

AUD – Governor Lowe has aided the AUD to gain a 0.68+ status after noting that fundamental factors underpinning the longer-term outlook for the Australian economy remain strong and economy has reached a gentle turning point, a comment made at the last speech which signals that the Central Bank could stand pat on at the next meeting on October 1st. The Governor reiterated that the Board is prepared to ease monetary policy further if needed to support sustainable growth in the economy, make further progress towards full employment, and achieve the inflation target over time whilst inflation is expected to pick up, but to remain below the midpoint of the target range for some time to come. AUD/USD immediately spiked higher from 0.6784 to 0.6805 ahead of resistance at 0.6810 before consolidating around the 0.6800 mark.

SEK – The Swedish Crown currently stands as the G10 laggard amid slightly more dovish comments from Riksbank’s Governor Ingves who noted that rates are likely to increase at a “very slow” rate over the period ahead (vs. prior “should be possible to slowly raise rates”) whilst also acknowledging low interest rates and weaker sentiment abroad. First Deputy Governor Jansson added further to the dovish fire by highlighting low Swedish inflation numbers and worrying inflation expectations, whilst adding that he sees no appreciable upside for Swedish prices. EUR/SEK, in wake of the governor’s comments, bounced further from its 100 DMA (10.66) to an intraday high of 10.71 (ahead of resistance at 10.73) before retreating below the 10.70 mark.

EM – The Lira is staging another recovery with strength attributed to media reports that the US is said to make a new offer to Turkey regarding F-35s and Patriots system after the two Presidents’ phone call over the weekend. USD/TRY fell from an intraday high of 5.7208 to a current low of 5.6782 ahead of its 55 and 50 DMAs at 5.6779 and 5.6705 respectively. Later, Turkish President Erdogan will make a speech at the UNGA before meeting with his French counterpart Macron and UK PM Johnson and UN Secretary General Guterres

In commodities, WTI and Brent prices are weaker this morning on a rather tentative session thus far on a lack of specific newsflow for the complex, but notably ahead of the UNGA where US President Trump has stated he is to discuss Iran in his speech. He has also added that the US has lots of pressure on Iran, which does follow from the instigation of sanctions on the Iranian Bank by the US; as such, focus today will be on the remarks from Trump and if there is any reference to further sanctions or the prospect of more forceful action. In terms of scheduling proceedings at the UN are to formally begin at around 13:00BST with President Trump scheduled to arrive at the UN headquarters around 14:30BST. Elsewhere, focus turns to tonight’s API release where expectations are form a 0.6mln/bbl draw; though, ING note that the result may surprise market expectations due to the number of storm related refinery disruptions that have occurred recently. In terms of metals, Gold is little changed hovering around the USD 1520/oz mark within a tight USD 1.0/oz range for the session; ahead of risk factors including the UNGA and a number of Central Bank speakers. Separately, copper prices are overall little changed, retaining their non-committal tone from the Asia-Pac session; though the metal does remain comfortably above the USD 2.62/lb mark.

US Event Calendar

9am: FHFA House Price Index MoM, est. 0.25%, prior 0.2%

9am: S&P CoreLogic CS 20-City MoM SA, est. 0.1%, prior 0.04%; CoreLogic CS 20-City YoY NSA, est. 2.1%, prior 2.13%

10am: Richmond Fed Manufact. Index, est. 1, prior 1

10am: Conf. Board Consumer Confidence, est. 133, prior 135.1

DB’s Jim Reid concludes the overnight wrap

Fiscal policy and money printing will inevitably need to be far more joined up in the future and yesterday’s European PMIs pushed us a very small way towards this realisation. The real problem came from the worrying declines in the services sectors in Germany and France, which had previously been the beacon of hope in the recent PMIs. Germany saw the services reading fall 2.3pts to 52.5 (vs. 54.3 expected). That is a nine-month low while there was no sign of improvement in the manufacturing sector, where the reading slumped another 2.1pts to 41.4 (vs. 44.0 expected) and to the lowest in the best part of ten years. That put the composite at 49.1 – the first sub-50 reading for Germany in this cycle and the lowest reading in 83 months, while it’s also worth flagging that the new orders prints were also very worrying including manufacturing new orders at 37.9 being the weakest outside of the peak of the GFC.

As for France, the services reading fell 1.8pts to 51.6 and the manufacturing 0.8pts to 50.3, while for the Eurozone as a whole the manufacturing reading slumped 1.4pts to 45.6 and the services 1.5pts to 52.0. Those are the lowest in 83 months and 8 months respectively. As a result, the composite Eurozone reading is now at 50.4 (vs. 52.0 expected) and the lowest in 75 months. So these services readings are clearly a very concerning sign for Europe and the end result is a barely positive run rate of growth in the Eurozone right now. Let’s see what today’s IFO brings.

Unsurprisingly, bond yields fell as soon as the data was released. By the close of play 10y Bunds finished -5.8bps lower at -0.583%, OATs -6.9bps lower and BTPs -9.3bps lower. Treasuries also rallied post the Euro PMIs but got an added kicker after the US services PMI printed at a weaker than expected 50.9 (vs. 51.4 expected) before reversing the day’s rally late to close unchanged and at the higher end of a 10bps intra-day range. In fairness the services PMI was a 0.2pt improvement from September but disappointed the market at the margin. On top of that, the fact that the employment component declined into contractionary territory at 49.1 (and to the lowest in 10 years) raised a few concerned eyebrows. In fact the two-month decline for services employment is the largest since the crisis. As for the manufacturing PMI, it rose 0.7pts to 51.0 (vs. 50.4 expected) – so a modest bounce but clearly still at low absolute levels.

The moves in equity markets, at least in the US, were more muted. The S&P 500 finished down -0.01% by the closing bell last night with the NASDAQ -0.06%. European equities suffered on the poor data releases however, with the STOXX 600 (-0.80%), DAX (-1.01%) and CAC (-1.06%) all closing lower. European banks led the declines, down -2.76% on the economic weakness and bond rally. Elsewhere, Gold (+0.35%) got a slight lift from the modest risk-off while Oil was +0.95%.

Meanwhile after the US close yesterday, Treasury Secretary Mnuchin said that Chinese Vice Premier Liu He would be visiting for talks next week. Mnuchin also said that “The good news” is that the Chinese have started buying U.S. agriculture products again; “it’s a sign of good gesture,”. He also added that US farmers are important in the China trade negotiations with intellectual property “the most important issue.” The visit can be seen as a slightly positive signal as the Vice Premier was originally scheduled to visit Washington the following week. Also, as we go to print Bloomberg has reported that the Chinese government has given new waivers to several domestic state and private companies to buy US soybeans without being subject to retaliatory tariffs. For now this is likely to increase hopes that trade progress is being made.

Talking of trade, the US and Japan have finished talks on an initial trade deal with Japanese Foreign Minister Toshimitsu Motegi saying after the talks that he would explain more about the tariffs in two days’ time after a meeting of Trump and Japanese Prime Minister Shinzo Abe at the sidelines of the UNGA. He also said that he didn’t think that auto tariffs would be a cause for concern.

This morning in Asia markets are largely heading higher with the Nikkei (+0.14%), Hang Seng (+0.32%), Shanghai Comp (+0.77%) and Kospi (+0.19%) all up. Elsewhere, futures on the S&P 500 are up +0.24% while the 10y UST yield is down -2.1bps. In terms of overnight data releases, Japan’s preliminary September PMIs came out on the softer side with manufacturing standing at 48.9 (vs. 49.3 last month), marking 7 months of contraction this year, while services stood at 52.8 (vs. 53.3 last month) bringing the composite PMI to 51.5 (vs. 51.9 last month).

In other overnight news,the PBoC Governor Yi Gang said in a press briefing, with Finance Minister Liu Kun and National Bureau of Statistics head Ning Jizhe, that China must avoid massive stimulus, keep debt levels sustainable and maintain a prudent monetary policy stance while reiterating the central bank’s policy stance. The statement comes as concerns over China’s growth slowdown are mounting.

Back to yesterday, where ironically, both Draghi and Lagarde spoke post the weak PMIs although neither of their comments were particularly market moving. Draghi mostly repeated his ECB message, including suggesting that EU fiscal rules should be revisited, while Lagarde was asked on the limits of central bank policy but didn’t mention anything particularly ground-breaking. Over at the Fed, we heard from St Louis Fed President Bullard, who was alone in voting for a larger 50bp rate cut at last week’s meeting. He said that “instead of creeping down slowly I would prefer to get to where we need to be”, and voiced support for a further 25bp cut this year. Elsewhere, Williams spoke on the recent repo turmoil and said that it is “important that we examine these recent dynamics and their implications for the liquidity needs in relation to the overall amount of reserves held at the Fed”. Former NY Fed President Dudley also said he thinks the Fed will “strongly consider” a standing repo facility.

As for Brexit, sterling fell –0.39% as chief EU negotiator Michel Barnier made negative comments on a possible deal being reached, describing the UK’s current proposals on the backstop as “unacceptable.” Meanwhile the Labour Party conference rejected calls for the party to back remaining in the EU in a second referendum, instead supporting Jeremy Corbyn’s policy of a wait-and-see approach which translates as 1) get a better deal, 2) put it to a referendum, and then 3) decide whether to back the new Labour deal or remain. It’ll be interesting to see whether their position is a big political gamble or smart sitting on the fence. Given the European election results, I would have more thought the former. At their conference they also pledged to commit the UK to a 32-hour four day week within the decade. If successful I haven’t yet decided which day the EMR will cease to be published.

Looking at the day ahead, data out in Europe this morning includes September confidence indicators in France, the Sept IFO survey in Germany and August public finances and public sector net borrowing numbers in the UK. This afternoon in the US the highlight will likely be the September consumer confidence report, while the September Richmond Fed survey, July S&P CoreLogic house price data and July FHFA house price index are also to be released. Expect there to also be focus on comments from the ECB’s Villeroy and Guindos, while here in the UK the Supreme Court will be ruling this morning on PM Johnson’s suspension of Parliament.

Volkswagen CEO, Chairman Charged With Market Manipulation In Emissions Scandal, Shares Tumble

Four years after the EPA blew the lid off emissionsgate by accusing Volkswagen of selling diesel cars equipped with ‘defeat devices’ to game emissions tests, two of the carmaker’s former top executives have been hit with criminal charges in their native Germany.

The revelation, which quickly erupted into a worldwide scandal, caused Volkswagen shares to erase nearly half of their value in the days over the next few days.

Herbert Diess

Now, Volkswagen AG Chief Executive Herbert Diess, Chairman Hans-Dieter Pötsch, and former CEO Martin Winterkorn have been charged with misleading shareholders. Since there’s a securities fraud angle to most major corporate crimes, it’s not surprising to see prosecutors going with the angle that the executives failed to inform shareholders about their company’s misdeeds, which would soon be disclosed.

According to WSJ, the “surprise” indictment shows prosecutors in Braunschweig, the district that has jurisdiction over Volkswagen’s Wolfsburg headquarters, clearly don’t buy the company’s defense: That its top executives had no way of knowing that the US investigation would lead to such massive losses.

‘Surprise’ indeed. Volkswagen shares were off 3.3% on the news as markets digested the possibility of more legal problems ahead for the carmaker.

China Grants New Tariff Waivers For US Soybean Purchases

Chicago Board of Trade soybean futures have been rising for the past 14 days, a total of +6.64%, on reports, China is granting new waivers to several domestic state and private companies to purchase U.S. soybeans without being subject to tariffs, according to Bloomberg. The companies received waivers for between 2 million to 3 million tons, sources told Bloomberg. Collectively, these firms bought 20 cargoes, or about 1.2 million ton of the soybeans from the U.S. Pacific Northwest on Monday.

It depends on the news source to the exact quantity, Reuters is reporting that Chinese importers only bought 10 cargoes, or about 600,000 tons, expected to be shipped from Pacific Northwest export terminals from Oct. to Dec.

Bloomberg said state-owned buyers Cofco and Sinograin, as well as five other crushers, were awarded waivers this month to purchase U.S. soybeans.

Sources said the waivers were granted after a meeting last week with working officials; purchases of agriculture products like soybeans are seen as kind gestures ahead of a trade meeting between U.S. and China next month.

As shown below, soybeans have enjoyed a wave of buying over the past two weeks on expectations of a similar gesture of goodwill by China and positive trade war news flow.

A trade deal appeared distant late last week after Chinese officials canceled a visit to the Central and Midwest states, but confirmed Monday that the cancellation was non-trade related.

Monday’s 10 to 20 cargoes, or 600,000 to 1.2 million tons of soybeans will leave Pacific Northwest terminals in the coming months. These are some of the most significant soybean purchases since Beijing raised import tariffs by 25% on U.S. soybeans last summer in retaliation for duties on other Chinese goods.

Yet while China is repurchasing U.S. soybeans, Argentina’s Agriculture minister confirmed Monday that China has “approved the first seven crushing plants in Argentina to begin exporting soymeal to the world’s biggest consumer of the livestock feed,” reported Reuters.

Last month, we reported how China wants to build a grains ‘superhighway‘ in the South American country by dredging the Parana River, it will allow large bulk vessels to transport soybeans from the Pampas farm belt to the South Atlantic to the Pacific, and ultimately to China.

While the Trump administration celebrates China’s latest agriculture purchases – keep in mind that China wants to become fully independent from the U.S., in terms of agriculture sourcing, which is why it’s hedging itself with Argentina.

UK Supreme Court Rules BoJo’s Suspension Of Parliament Was Unlawful; Pound Climbs

In a landmark ruling that delivers an unprecedented defeat for Boris Johnson and his Brexit strategy, Britain’s Supreme Court has ruled on Tuesday that the prime minister’s decision to suspend Parliament for five weeks was unlawful.

Now, the Speakers of the Commons and Lords simply need to summon ministers and peers to order and Parliament will be back in session as if it had never been suspended. The Speaker of the Commons is still John Bercow, though he recently announced his plans to resign.

“This was not a normal prorogation in the runup to a Queen’s speech,” said Lady Brenda Hale, the president of the Supreme Court of the UK. The decision did prevent Parliament from carrying out its duties, the court decided. Hale also found that Johnson hasn’t furnished “an explanation” for such extreme action.

It’s unclear what Johnson plans to do once Parliament is recalled – proroguing parliament for five weeks was a desperate gambit to try and strongarm the UK into a ‘no deal’ exit on Oct. 31. But with Parliament back in session, it’s looking very likely that opponents of a no-deal exit will succeed in forestalling it.

The ruling has also denied Johnson the option of suspending parliament to try and force through no deal Brexit.

And as the odds of ‘no deal’ are once again dimming, the pound is on an upswing.

Giuliani Hits Bidens With New $3 Million “Ukraine-Latvia-Cyprus” Money Laundering Accusation

Rudy Giuliani leveled serious new claims at the Bidens in a series of Monday morning tweets. Chief among them is a claim that $3 million was laundered to former Vice President Joe Biden’s son, Hunter, via a “Ukraine-Latvia-Cyprus-US” route – a revelation he claims was “kept from you by Swamp Media.”

Giuliani also says that Obama’s US embassy instructed Cyprus not to reveal the dollar amount.

NEW FACT: One $3million payment to Biden’s son from Ukraine to Latvia to Cyprus to US. When Prosecutor asked Cyprus for amount going to son, he was told US embassy (Obama’s) instructed them not to provide the amount. Prosecutor getting too close to son and Biden had him fired.

Today though it’s the $3 million laundered payment, classical proof of guilty knowledge and intent, that was kept from you by Swamp Media. Ukraine-Latvia-Cyprus-US is a usual route for laundering money. Obama’s US embassy told Cyprus bank not to disclose amount to Biden. Stinks!

Trump’s personal attorney then mentioned China – where journalist Peter Schweizer reported Joe and Hunter Biden flew in 2013 on Air Force Two. Two weeks later, Hunter’s firm inked a private equity deal for $1 billion with a subsidiary of the Chinese government’s Bank of China, which expanded to $1.5 billion, according to an article by Schweizer’s in the New York Post.

Biden scandal only beginning. Lots more evidence on Ukraine like today’s money laundering of $3 million. 4 or 5 big disclosures. Also the $1.5 billion China gave to Biden’s fund while Joe was, as usual, failing in his negotiations with China is worse.

Giuliani then went on to tweet that the Bidens lied about not discussing Hunter’s overseas business.

On Saturday, Joe Biden said he “never” spoke with Hunter about the Ukrainian energy company that Hunter sat on the board of while being paid $50,000 per month. As you’re doubtless aware by now, the elder Biden threatened to withhold $1 billion in US loan guarantees from Ukraine if they didn’t fire the investigator probing the company, Burisma.

Biden says he never talked to his son about his overseas business. Do you think we can prove, with our fact a day disclosures, it’s a lie-a false exculpatory statement. Do we have to prove, or do you already know, it’s a lie, and an incriminating statement.

Hunter, however,admitted in July that the two did speak about his Ukraine business “just once,” telling the New Yorker “Dad said, ‘I hope you know what you are doing,’ and I said, ‘I do’“

Rudy Giuliani: “[Biden’s] family has been taking money from his public office for years, $1.5 billion from China, when our VP is supposed to be impartially and independently negotiating for us? He takes [his son] on Air Force Two to China and the kid … is a drug addict” pic.twitter.com/q8W9ZldwGX

Rudy then lashed out at the Democratic party, which he said would “own” Biden’s scandals if hey don’t “call for investigation of Bidens’ millions from Ukraine and billions from China.”

If Dem party doesn’t call for investigation of Bidens’ millions from Ukraine and billions from China, they will own it. Bidens’ made big money selling public office. How could Obama have allowed this to happen? Will Dems continue to condone and enable this kind pay-for-play?

Here’s what we know about Hunter’s dealings in China based on Schweizer’s reporting via our May report:

Hunter Biden and his partners created several LLCs involved in multibillion-dollar private equity deals with Chinese government-owned entities.

The primary operation was Rosemont Seneca Partners – an investment firm founded in 2009 and controlled by Hunter Biden, John Kerry’s stepson Chris Heinz, and Heniz’s longtime associate Devon Archer. The trio began making deals “through a series of overlapping entities” under Rosemont.

In less than a year, Hunter Biden and Archer met with top Chinese officials in China, and partnered with the Thornton Group – a Massachusetts-based consultancy headed by James Bulger – son nephew of famed mob hitman James “Whitey” Bulger (h/t @Guerrilla_Magoo for the correction).

According to the Thornton Group’s Chinese-language website, Chinese executives “extended their warm welcome” to the “Thornton Group, with its US partner Rosemont Seneca chairman Hunter Biden (second son of the now Vice President Joe Biden.”

Officially, the China meets were to “explore the possibility of commercial cooperation and opportunity,” however details of the meeting were not published to the English-language version of the website.

“The timing of this meeting was also notable. It occurred just hours before Hunter Biden’s father, the vice president, met with Chinese President Hu Jintao in Washington as part of the Nuclear Security Summit,” according to Schweizer.

Perhaps most damning in terms of timing and optics, just twelve days after Hunter and Joe Biden flew on Air Force Two to Beijing, Hunter’s company signed a “historic deal with the Bank of China,” described by Schweizer as “the state-owned financial behemoth often used as a tool of the Chinese government.” To accommodate the deal, the Bank of China created a unique type of investment fund called Bohai Harvest RST (BHR). According to BHR, Rosemont Seneca Partners is a founding partner.

It was an unprecedented arrangement: the government of one of America’s fiercest competitors going into business with the son of one of America’s most powerful decisionmakers.

Chris Heinz claims neither he nor Rosemont Seneca Partners, the firm he had part ownership of, had any role in the deal with Bohai Harvest. Nonetheless, Biden, Archer and the Rosemont name became increasingly involved with China. Archer became the vice chairman of Bohai Harvest, helping oversee some of the fund’s investments. –New York Post

And while Hunter Biden had “no experience in China, and little in private equity,” the Chinese government for some reason thought it would be a great idea to give his firm business opportunities instead of established global banks such as Morgan Stanley or Goldman Sachs.

Also in December 2014, a Chinese state-backed conglomerate called Gemini Investments Limited was negotiating and sealing deals with Hunter Biden’s Rosemont on several fronts. That month, it made a $34 million investment into a fund managed by Rosemont.

The following August, Rosemont Realty, another sister company of Rosemont Seneca, announced that Gemini Investments was buying a 75 percent stake in the company. The terms of the deal included a $3 billion commitment from the Chinese, who were eager to purchase new US properties. Shortly after the sale, Rosemont Realty was rechristened Gemini Rosemont.

“Rosemont, with its comprehensive real-estate platform and superior performance history, was precisely the investment opportunity Gemini Investments was looking for in order to invest in the US real estate market,” said Li Ming, chairman of Sino-Ocean Land Holdings Limited and Gemini Investments. “We look forward to a strong and successful partnership.“

The morning after the car was dropped off, a phone number belonging to a renowned local “Colon Hydrotherapist” called the Hertz. The caller identified himself as “Joseph McGee,” who told the employees that the keys were located in the gas cap as opposed to the drop box.

Amazing how so many countries would scramble to do business with Hunter – a guy with virtually no experience who was discharged from the Navy after testing positive for cocaine – who just happened to be the Vice President’s son.