Watch Live: Pelosi To Launch “Impeachment Inquiry” Against Trump

Democratic Leader Nancy Pelosi is expected to rally Democratic members of the House for a press conference late Tuesday afternoon to launch an investigation into whether Trump should be impeached.

The House leader will also address other issues facing Democrats and Republicans, including climate control and their electoral strategy for the 2020 vote.

Pelosi said earlier that: “Later today I will make an announcement after I meet with my chairmen, my leadership and my caucus.”

Pelosi has resisted Trump’s impeachment for the duration of his first term, but with the rise of more left-leaning Democrats in the House, it’s looking like an issue that Pelosi can no longer afford to ignore, according to CNBC News.

She is also expected to make a statement at 5 pm ET, following meetings with congressional leadership and her caucus.

More than a dozen Democrats have come out in favor of impeachment within the past week, following bombshell reports that Trump had reportedly asked Ukraine President Volodymyr Zelensky to investigate political rival Joe Biden’s son, Hunter Biden, during a phone call back in July.

Meanwhile, House Intelligence Chairman Adam Schiff tweeted: “We have been informed by the whistleblower’s counsel that their client would like to speak to our committee and has requested guidance from the Acting DNI as to how to do so. We‘re in touch with counsel and look forward to the whistleblower’s testimony as soon as this week,” according to Axios.

We have been informed by the whistleblower’s counsel that their client would like to speak to our committee and has requested guidance from the Acting DNI as to how to do so.

We‘re in touch with counsel and look forward to the whistleblower’s testimony as soon as this week.

Surprisingly, the odds of Trump surviving his first term fell by more than 20 percentage points in recent days as more Democrats turned to supporting the issue, unconcerned about its impact on the election.

But the investigation launch isn’t the only thing happening in Congress: The House will on Wednesday vote on a resolution making clear Congress’s disapproval of the Trump administration’s effort to block the release of a whistleblower complaint, House Democratic leaders said in a statement, according to Reuters.

Pelosi/Hoyer announce a Weds floor vote on a resolution relating to the Ukraine whistleblower complaint.

Nonbinding. Just makes a statement. But it puts Republicans on the spot re: voting to demand the release of the whistleblower complaint. pic.twitter.com/zYoTzQiJbH

Economists are already predicting “the world’s lowest growth in a decade”, but it is beginning to look like what we will be facing will be much worse than that.

In recent days, numbers have been coming in from all over the planet that are absolutely abysmal. The “global economic slowdown” is rapidly transitioning into a new global economic crisis, and central banks seem powerless to stop what is happening. They have already pushed interest rates to the floor (actually below the floor in many cases), and over the past decade they have absolutely flooded the global economy with new money. But despite all of this unprecedented intervention, economic conditions are deteriorating at a pace that is breathtaking.

Let’s start by taking a look at what is happening in India. According to CNN, vehicle sales in India fell a whopping 31 percent in July…

Just two years ago, India’s huge car market was booming and global players were rushing to invest. Now it’s been slammed into reverse.

Sales of passenger vehicles plunged 31% in July, according to figures released by the Society of Indian Automobile Manufacturers (SIAM) on Tuesday. It’s the ninth straight month of declines and the sharpest one-month drop in more than 18 years, SIAM Director General Vishnu Mathur told CNN Business.

Those are numbers you would expect to see if we were in the middle of a full-blown economic depression, and it is being projected that this downturn “could result in a million people being laid off”…

The slump has prompted companies to slash over 330,000 jobs through the closing of car dealerships and cutbacks at component manufacturers, Mathur said, citing data from industry associations that govern those two sectors.

The Automotive Component Manufacturers Association of India warned in a statement last month that its “crisis-like situation” could result in a million people being laid off.

A million jobs is very serious.

And we are talking about just one industry in one country.

How many jobs will ultimately be lost all over the world in the months ahead?

China’s Geely (GELYF) revealed this week that its net profit probably plunged by 40% in the first half of the year as the world’s second largest economy slowed. In June alone, its car sales fell 29%.

That isn’t supposed to happen in China.

For decades, China has been one of the primary engines of global economic growth, but now things have changed dramatically.

Perhaps you can blame the trade war for what is happening in China, but the auto industry is also in big trouble in Europe. In fact, some of the biggest automakers in the world are closing European factories and ruthlessly slashing jobs…

Ford is cutting 12,000 jobs and closing six plants in Europe, including an engine factory in the United Kingdom. Jaguar Land Rover, which is owned by India’s Tata Motors (TTM), is slashing 4,500 jobs. Honda is also closing a plant in the United Kingdom.

If those companies expected the European economy to bounce back in the foreseeable future, they would not be making such moves.

But just like you and I, they can see what is happening to Europe’s economy, and on Monday we just received some more deeply troubling news. The following comes from Zero Hedge…

Weakness in euro-area manufacturing hit a climax this morning as German private sector activity plunged to a seven-year low. The Germany Manufacturing PMI slumped in September, dropping to 41.4, down from 44.7 in August, printing below the lowest sellside estimate (consensus of 44.4); worse, the German manufacturing recession is now spreading to the services sector, where the formerly resilient services PMI also slumped from 54.8 to 52.5, also missing the lowest analyst estimate, and collectively, resulting in the first composite PMI print below 50, or 49.1 to be precise, since April 2013. The rate of decline was one of the sharpest in seven years.

It appears that the German economy has already entered recession territory, and these new numbers are not causing anyone to be optimistic.

Of course the U.S. economy has been slowing down for quite some time now, and if you doubt this, I encourage you to read this list of 28 alarming facts about our economy that I posted earlier this month.

We haven’t seen economic conditions like this in the United States since the depths of the Great Recession, and many believe that what is coming will be far worse than the last time around.

And we may be deep into the coming crisis far sooner than many were expecting. In fact, David Rosenberg of Gluskin Sheff is adamant that there is “a recession coming in the next 12 months”…

David Rosenberg, the Gluskin Sheff chief economist and strategist, is warning that a recession is coming. Rosenberg says economic growth in the United States will turn negative sooner than most investors anticipate and the Federal Reserve is powerless.

Even if the central bank lowers interest rates to zero, a recession will still grip the U.S. within 12 months, Rosenberg predicts. “There’s a recession coming in the next 12 months,”he stated with fact last Thursday on CNBC’s “Futures Now. The Fed just lowered its benchmark interest rate last Wednesday by a quarter-point and Fed Chairman Jerome Powell signaled rates would only be cut again if there’s new evidence the economy is softening.

If things really start to deteriorate in the months ahead, we could be in the midst of a horrible economic downturn by the time the U.S. presidential election rolls around.

Let us hope that is not the case, but right now things certainly do not look good for the U.S. economy or for the global economy as a whole.

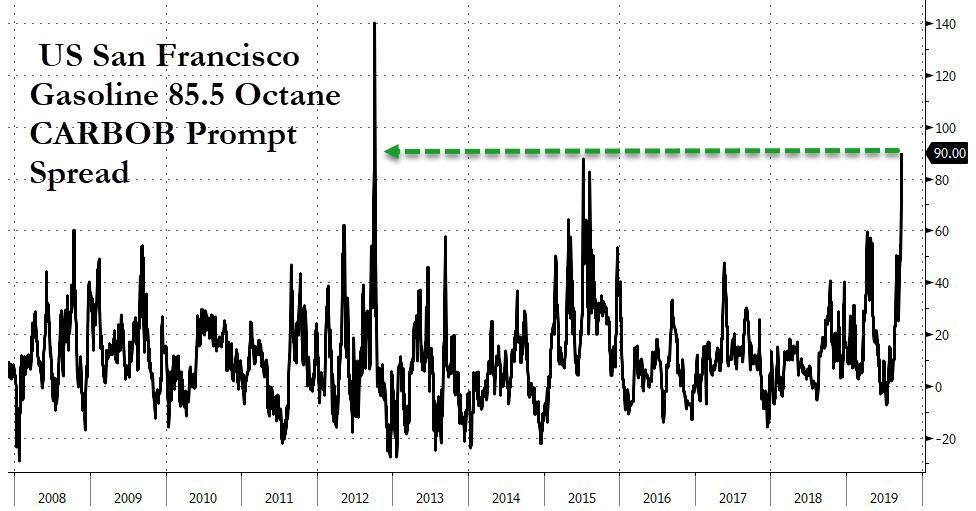

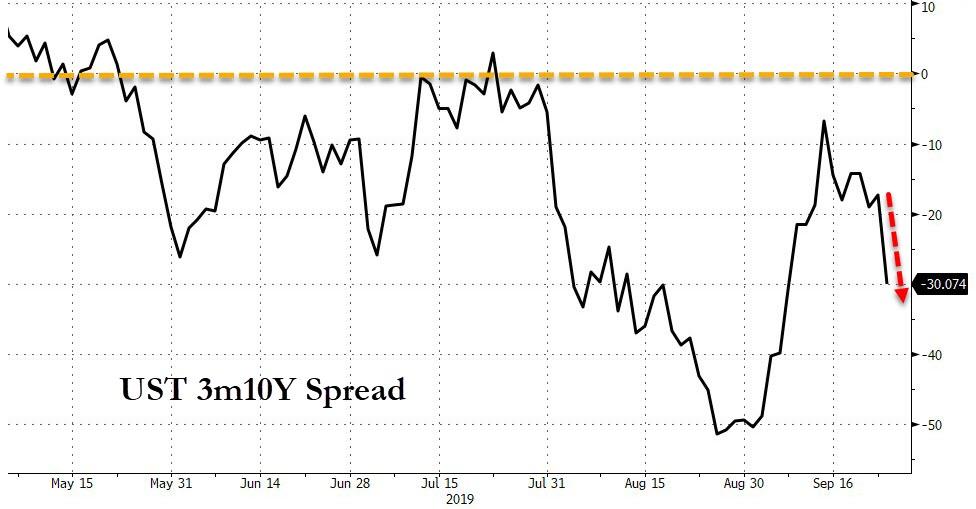

WTI Extends Losses After Second Weekly Surprise Crude Build

Oil prices tumbled today on the heels of Saudi production headlines (supply) and Trump’s negative tone towards China (demand), however, not everyone was buying what the Saudis were selling.

“The current timetable is overly optimistic,” said Joe McMonigle, an analyst at Hedgeye Risk Management and former vice chairman of the International Energy Agency. The kingdom probably won’t achieve full capacity “until the end of the year at the earliest.”

So once again all eyes (and algos) will be on the inventory data…

API

Crude +1.38mm (-600k exp)

Cushing +2.3mm

Gasoline +1.9mm

Distillates -2.2mm

After last week’s surprise crude and gasoline inventory build, analysts have shrunk their estimates for the latest week but were wrong again as API reported a surprise 1.38mm barrel rise in crude inventories. Cushing saw a major rise in stocks…

Source: Bloomberg

WTI hovered around $57 ahead of the data, and extended losses after the second surprise build in a row…

Meanwhile, as Bloomberg details, cash-market San Francisco gasoline traded at near a seven-year high Tuesday and $4/gal retail gasoline “may be on the table” due to refinery issues, Patrick DeHaan, GasBuddy petroleum analysis director, says.

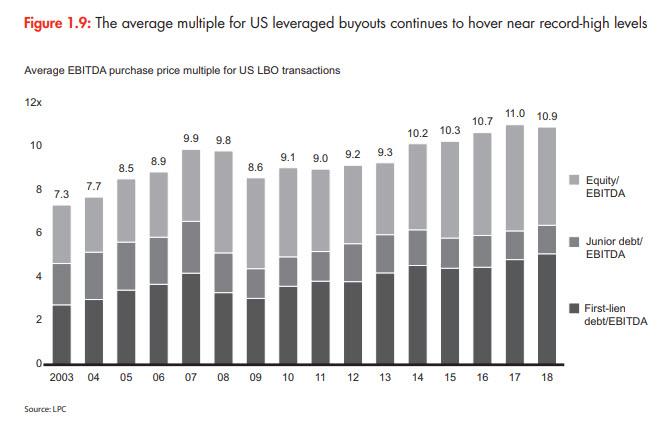

“That’s The Greatest Risk” – Head Of World’s Largest PE Firm Warns Of “Asset Bubble Reckoning”

It’s not just corporate insiders of publicly traded companies who are dumping stocks at a feverish pace: private equity also would be… if of course the equity wasn’t “private.” Stephen Schwarzman, the CEO of Blackstone – the world’s largest private equity firm – warned Monday that the inflating bubble in asset values “could lead to a painful reckoning, particularly for late-stage investors in private technology companies like WeWork parent We Co.”

Speaking to the WSJ, Schwarzman said that orivate valuations are getting “very high”, adding that later-stage funding rounds in companies planning initial public offerings were helping to escalate those values, even for companies that often have little prospect of profitability. Case in point: WeWork, whose disastrous IPO, and whose valuation collapse from $47 billion to less than $10 billion, coupled with mass layoffs, demonstrates what happens when there are no more greater fool.

For those confused, a company went from a $47bn valuation to mass layoffs and CEO termination because it ran out of greater fools

“That’s the greatest risk,” Schwarzman said in response to a question about patterns he sees developing in the market. “These valuations of private tech companies are most probably too high,” he said, adding some people will lose money as a result.

Schwarzman listed SoftBank’s catastrophic investments We and Uber Technologies as examples of overly high valuations, and likened the situation to the dot-com bubble around the turn of the century.

Then again, the bad blood between VCs cashing out from overvalued investments, and PE firms trying to buy (or sell) companies at a time of record high EBITDA multiples is hardly new.

Alternatively, VCs will be happy to counter that whereas their investment create jobs, PE portfolio names merely saddle firms with massive debt loads, forcing them to fire millions of workers as they cut into both the fat and muscle, and strip their investments to the bone. Blackstone however, would have none of it: asked about the battering the private-equity industry has been taking this year by politicians in Washington, D.C., and on the presidential campaign trail, Schwarzman said much of the criticism doesn’t reflect facts.

Arguing that buyout firms “typically invest to grow portfolio companies and improve profitability”, which results in increased payrolls rather than job cuts, Schwarzman pointed out that Blackstone portfolio companies created about 100,000 jobs over the past decade. Of course, here one can point out there some of the biggest defaults in the past two decade have been the mega LBOs which, due to record debt loads, ended up in Chapter 11 or Chapter 7, firing most of their workers, but not before the PE sponsors made out like bandits on their investment.

He added that Blackstone buys an asset to “make it better so it can make more money and grow faster,” he said. “To make a company grow quickly, you don’t cut your way forward. You have to invest.”

Ironically, in a time of collapsing CapEx and massive buybacks and dividends debt deals, nobody is actually investing and everyone is “cutting” their way forward.

Defending his track record, Schwarzman also pointed to the contribution private-equity firms have made to the U.S. retirement system, through managing investments from institutional investors such as pension funds and life insurers. In all, he said, the industry has invested about $3 trillion over the past five years.

It remains to be seen what the IRR on those $3 trillion will be after the coming market crash.

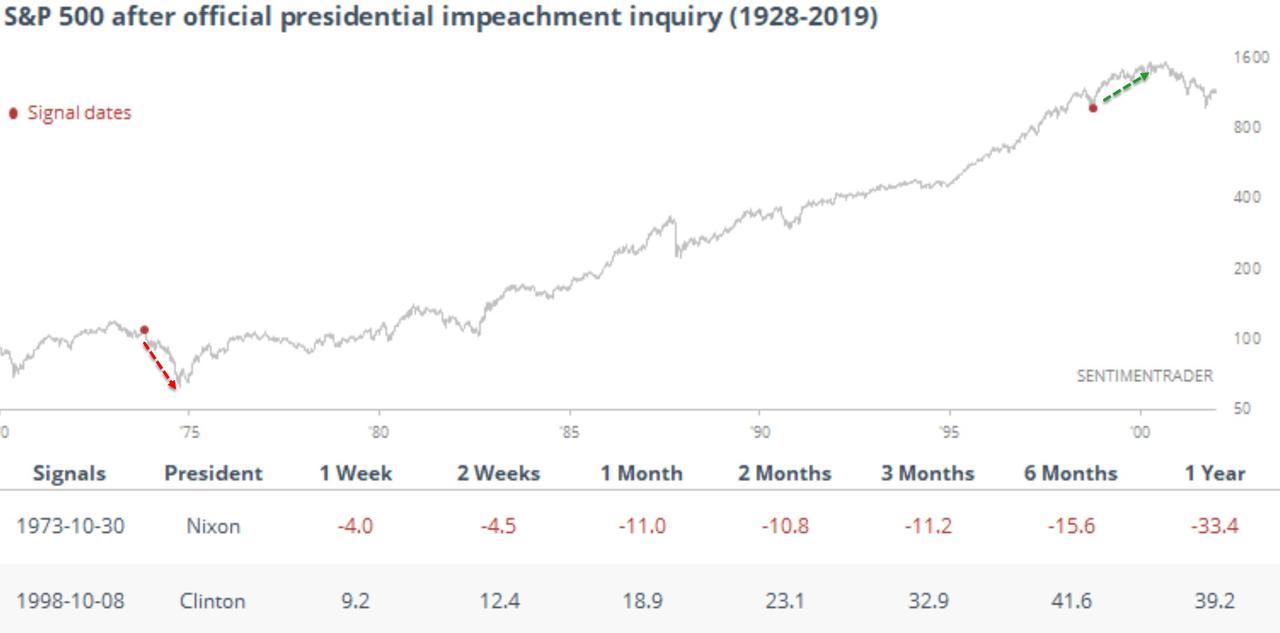

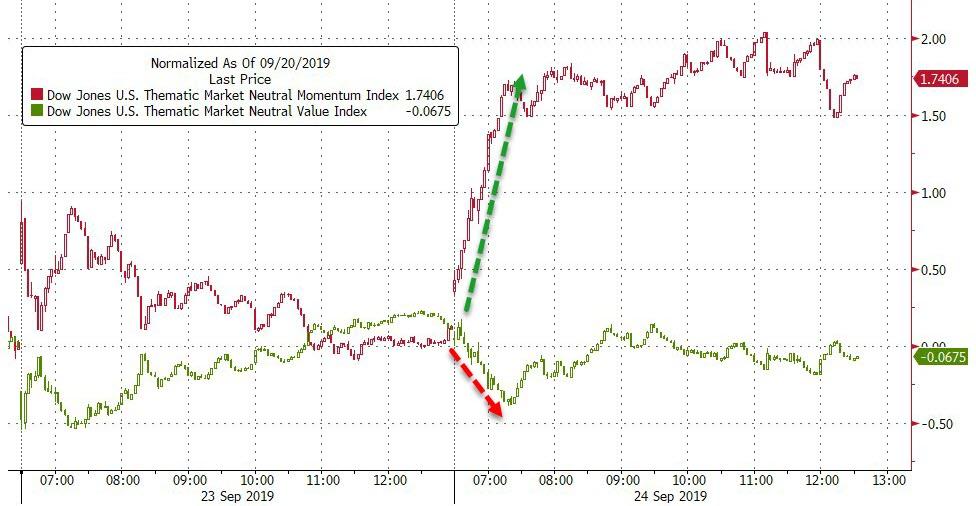

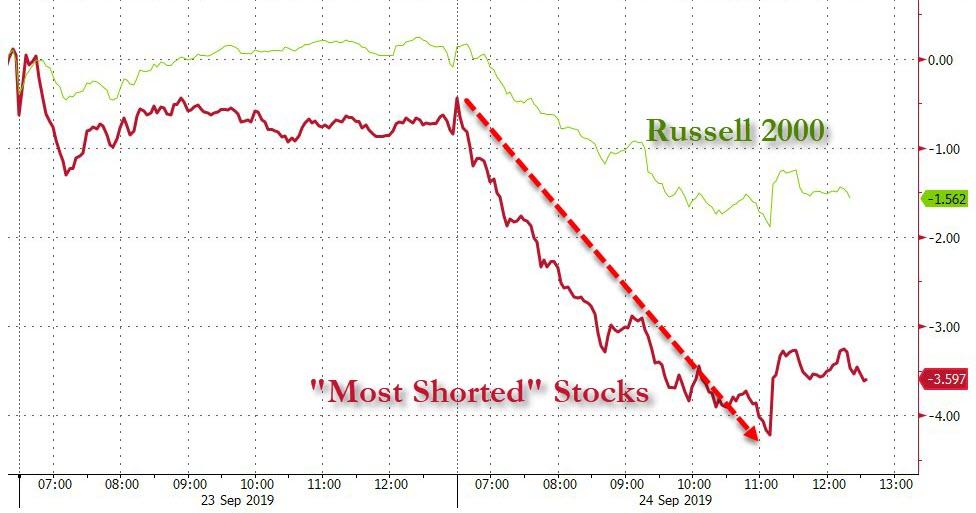

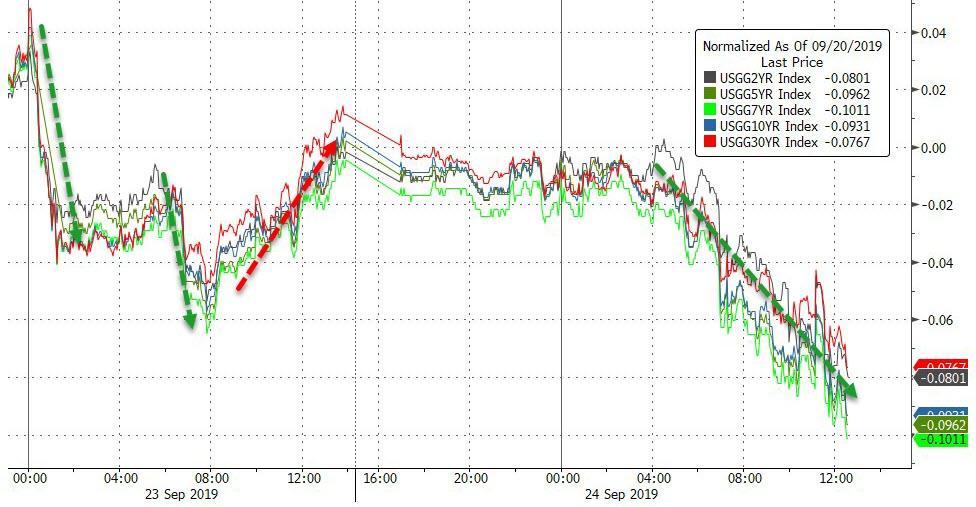

Stocks Slammed On Sentiment Slump, Trade Turmoil, & Impeachment Anxiety

What started off as a positive day thanks to overnight algos liftathon after TSY Secretary Mnuchin spoke on Fox Business and broke old news about China talks, ended up rather ugly as the triple whammy of consumer confidence crumbling, Trump talking down China in his UN speech, and battling impeachment headlines sparked risk-off moves in stocks and a bid for bonds and gold.

What the algos saw…

1605ET BUY – Mnuchin on China Vice Premier talks.

1000ET SELL – Cons Confidence.

1020ET SELL – Trump dissing China at UN

1210ET SELL – Pelosi says she will make an announcement, Impeachment fears rise.

1410ET BUY – Trump to release transcript of Ukraine call, reducing impeachment odds.

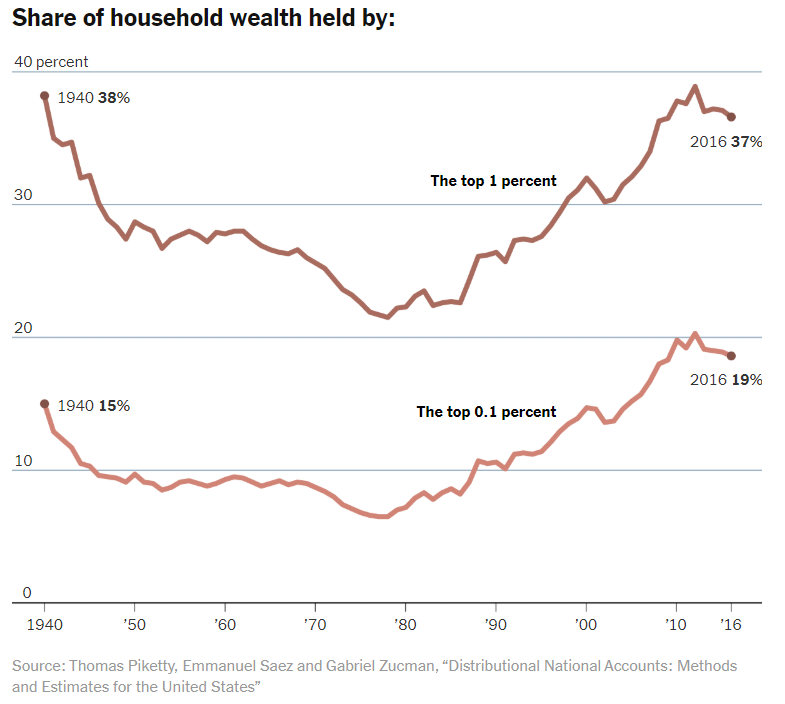

“Billionaires Shouldn’t Exist”: Bernie Proposes Tax To Cut Billionaire Wealth In Half

After spitting venom at millionaires until he became one, Sen. Bernie Sanders (I-VT) has a new target: billionaires.

On Tuesday, Sanders rolled out an ‘ambitious’ plan to tax the nation’s ultra-rich, going far beyond his Democratic primary rival Elizabeth Warren’s proposed wealth tax with what Sanders says would cut American billionaires’ fortunes in half over 15 years.

while Ms. Warren came first, Mr. Sanders is going bigger. His wealth tax would apply to a larger number of households, impose a higher top rate and raise more money.

Mr. Sanders’s plan to tax accumulated wealth, not just income, is particularly aggressive in how it would erode the fortunes of billionaires. His tax would cut in half the wealth of the typical billionaire after 15 years, according to two economists who worked with the Sanders campaign on the plan. Mr. Sanders would use the money generated by his wealth tax to fund the housing plan he released last week and a forthcoming plan for universal child care, as well as to help pay for “Medicare for all.” –NY Times

Sanders’ plan would impose a graduated tax of 1% on assets over $32 million, 2% for households worth $50 – $250 million, 3% from $250 million to $500 million, 4% from $500 million – $1 billion and finally 8% on wealth over $10 billion. Over a decade, the tax would raise an estimated $4.35 trillion (less whatever can’t be recovered from all the money quickly funneled into offshore trusts).

Moreover, the estate tax rate would begin at 45% for assets over $3.5 million, rising to 77% for those with over $1 billion – a proposal which Sanders says would apply to 0.2% of the population.

Sanders’ campaign said his wealth tax would slash U.S. billionaires’ wealth in half in 15 years, “which would substantially break up the concentration of wealth and power of this small privileged class.”

“Enough is enough,” Sanders, a Vermont senator, said in a statement. “We are going to take on the billionaire class, substantially reduce wealth inequality in America and stop our democracy from turning into a corrupt oligarchy.” –Bloomberg

“Let me be very clear: As president of the United States, I will reduce the outrageous and grotesque and immoral level of income and wealth inequality,” Sanders told the Times, adding “What we are trying to do is demand and implement a policy which significantly reduces income and wealth inequality in America by telling the wealthiest families in this country they cannot have so much wealth.”

Asked if he thinks billionaires should exist in America, Sanders said “I hope the day comes when they don’t,” adding “It’s not going to be tomorrow.”

As the Times notes, “As appealing as a wealth tax might sound for the party’s liberal base, enacting it would pose major challenges. Anyone lucky enough to be in its sights has access to top tax lawyers and accountants who can sift through the tax code for a way out, or at least a means of minimizing the hit.”

Warren’s proposal, meanwhile, would impose a 2% tax on wealth over $50 million – or the top 70,000 families in the country. For someone with $100 million in assets, Warren’s plan would cost them $1 million per year. Fortunes over $1 billion would be subject to an additional 1% annual surcharge. Her plan also includes expanding the estate tax – which would begin at 55% and rise to 75%.

The University of California system has announced its intention to completely divest from fossil fuels.

Officials in charge of investments insist that their decision to move toward more “sustainable” and environmentally conscious investments is simply in the practical interest of beneficiaries, rather than a product of political opinion.

In an opinion piece in the Los Angeles Times, UC chief investment officer and treasurer Jagdeep Singh Bachher and chairman of the UC Board of Regents’ Investments Committee Richard Sherman reasoned that “hanging on to fossil fuel assets is a financial risk.”

“That’s why we will have made our $13.4-billion endowment “fossil-free” as of the end of this month, and why our $70-billion pension will soon be that way as well,” the officials explained in the September 17 op-ed.

Sherman and Bachher deny that their decision was “born of political pressure,” or that it is a result of “green movement idealism.” Instead, they insist that it is based on a “sustainable investing” approach.

“Today, we are on track to beat our own five-year goal of investing at least $1 billion in climate change solutions and, by incorporating environmental, social and governance factors — ESG factors — into our investment decision-making, we’ve become better stewards of university funds,” the officials explained.

Sherman and Bachher boast that they drove UC to become the first U.S. public university to sign onto the U.N’s Principles for Responsible Investing, a commitment by institutional investors to act in the “long-term interests” of their beneficiaries by incorporating “environmental, social, and corporate governance (ESG) factors” into investment decisions.

The commitment consists of six principles to guide investment decisions including to “incorporate ESG issues into investment analysis” to “seek appropriate disclosure on ESG issues by the entities in which we invest,” and to “promote acceptance and implementation” of the listed principles.

The investors emphasize that they are not driven by political reasonings, but that they are led to the same decision that they might be if that were the case. Regardless of political motivations, they say that they sold $150 million in fossil fuel assets because they “posed a long-term risk.”

“While our rationale may not be the moral imperative that many activists embrace, our investment decision-making process leads us to the same result. We’re in the business of helping to ensure the financial viability of a great university whose stakeholders frequently come at an issue — even one as terrifyingly consequential as climate change — from different perspectives,” the pair wrote.

Impeachment Holdout Rep. John Lewis Says ‘Time To Begin’ Proceedings Against Trump

Rep. John Lewis (D-GA) added his name to the list of Democrats supporting an impeachment inquiry against President Trump during a Tuesday afternoon speech on the House floor – making 164 members of Congress who say they support the move.

“We cannot delay,” said Lewis. “We must not wait. Now is the time to act. I have been patient while we tried every other path and used every other tool. We will never find the truth unless we use the power given to the House of Representatives, and the House alone, to begin an official investigation as dictated by the Constitution. The future of our democracy is at stake. I believe, I truly believe, the time to begin impeachment proceedings against this president has come. To delay or to do otherwise would betray the foundation of our democracy.”

The new impachment push by Lewis – a frequent bellweather for the Democratic caucus – is seen as a significant step towards a sharply divided House. While some lawmakers say impeaching Trump is the only way to beat him in in 2020, others – such as House Speaker Nancy Pelosi, has long maintained that even if the House votes to impeach – a defeat in the GOP-controlled Senate would ‘exonerate’ Trump and energize his base. Of note, Pelosi will hold a press conference later on Tuesday concerning the matter.

Earlier, seven House Democrats who represent competitive districts are pushing to begin impeachment proceedings against President Trump, if reporting turns out to be true that Trump pressured Ukraine to investigate former Vice President Joe Biden.

“For all seven of us, the idea that a sitting president would use security assistance from the United States to pressure and potentially extort the president of another country into giving him dirt on a political opponent is just beyond the pale,” Rep. Elissa Slotkin of Michigan told NPR’s Morning Edition Tuesday. –NPR

While hesitant Democrats may not have thought impeachment over loose obstruction claims in the Mueller report would go over well, the new push to impeach over allegations that Trump withheld military aid to Ukraine unless the government investigated former Vice President Joe Biden and his son Hunter has emboldened the effort.

“Today I come with a heavy heart deeply concerned about the future of our democracy, and I’m not alone,” said Lewis, adding that he has spoken with constituents who “truly believe that our nation is descending into darkness.”

“Every turn, this administration demonstrates complete disdain and disregard for ethics, for the law and for the constitution, he said. “The people have a right to inquire, they have a right to know… whether they can put their faith and trust in the outcome of our elections… whether the cornerstone of our democracy was undermined by people sitting in the White House today… whether the president is using his office to line his pockets.”

Another Democratic holdout, Rep. Hank Johnson, said “Attempting to coerce a foreign government into digging up dirt on a political opponent, then trying to cover it up by unlawfully refusing to turn over the whistleblower complaint to Congress, crosses a red line.”

Mastercard, one of the big players now looking at this new money, is starting a cryptocurrency team.

“Do you have the desire to work at the cutting-edge intersection of payments and cryptocurrencies,” MasterCard asks.

Those hired will “monitor crypto currency ecosystem trends” and “develop new products and solutions.”

A credit card expert called it “a smart move.”

Bill Hardekopf, CEO of LowCards.com, says Mastercard “sees there’s a lot of activity in this area. Even if it isn’t going to offer its own cryptocurrency, they know it’s important to have people who understand the subject.”

Others Already Playing the Money Game

Mastercard is part of the Libra Association, which includes Pay Pal, Visa, and other big players. Libra intends to create “a globally, digitally native, reserve-backed crypto currency built on the foundation of blockchain technology.”

There were between 2.9 million and 5.8 million users of a cryptocurrency wallet in 2017, according to a Cambridge University study. Most used bitcoin. Four years before that there were between 300,000 and 1.3 million users.

“Mastercard,” says Panda Analytics CEO Bill Xing, is “trying to build a crypto wallet solution, possibly an alternative to Facebook’s Calibra cryptocurrency, which is supposed to begin next year. It is preparing for the situation when crypto (peer-to-peer transaction) is adopted as the mainstream payment solution.”

Direct Transactions without Intermediaries

Peer to peer means that the middleman in today’s traditional transaction could disappear if cryptocurrencies revolutionize money. Cryptocurrencies are decentralized because there is no intermediary; transactions are party to party through electronic addresses without central banks. In fact, they represent a vote of no confidence in the policies of central banks. They see central banks as consistently devaluing money through currencies that aren’t backed by anything but government promises. Critics call this unbacked currency “fiat money.”

Some countries ban alternative currencies. Others embrace them or acknowledge tax them. In 2014 the IRS ruled bitcoin will be treated as property, subject to capital gains taxes.

Today there are hundreds of cryptocurrencies. Bitcoin is the biggest.

These currencies’ value is volatile. Some investors make millions. Others lose big. But the idea of competition between currencies goes back at least to the 1970s. This was an idea explored by economist F.A. Hayek’s 1976 book Denationalisation of Money.

Hayek contended the “government monopoly of money must be abolished to stop the recurring bouts of acute inflation and deflation.” He also argued that the increasingly outrageous overspending of government — which can now be seen in the federal government’s one-trillion-dollar deficit at a time of supposed strong economic growth — would be restricted if the money monopoly was ended.

“The monopoly in money by government,” Hayek wrote, “has relieved it of the need to it keep its expenditure within its revenue and has thus precipitated the spectacular increase in government expenditure over the last 30 years.”

Hayek’s wrote these words back in the mid-1970s. Since then, government overspending, deficits, and debt have progressively worsened. Trillion-dollar deficits are now routinely accepted. Few seem worried about government overspending.

Democrats call for trillions of dollars in new spending. Republicans such as Dick Cheney now defend this massive red ink with the assurance that “Reagan proved that deficits don’t matter.”

But what if the money revolution succeeds? As in any revolution, today’s top dogs have the most to lose.

“In theory,” Xing says, “if these payment companies don’t study new technology around bitcoin or explore new business models, they could be out of business in the next decade.”

So, a revolutionary money is developing. Some governments are trying to stop it for an obvious reason: human nature. Almost everyone would like to be in a monopoly position but competition prevents it in a functioning marketplace. However, governments have the legal power to make competition go away or prevent it from coming back in the cases of goods and services that were once offered privately but are now prevented by the power of government.

Here in New York, where we have the terrible state-run subways, all major pols agree that the state system, no matter how bad it becomes — and millions of subway riders can attest to their egregiousness — must be continued and no privatization allowed. That’s even though, in the earliest period of the subways, when they were considered “an engineering marvel,” and private transportation companies were an essential part of the system. They were later driven into bankruptcy by government price controls. The subway fares, under private companies, were never allowed to raise above a nickel. That’s something that changed quickly once government took over.

More Money Screwups

The movement for alternative money is the result of the history of government monetary mismanagement.

It is a sad story of government central banks and monetary disasters. The Great Depression, of course, happened on the Federal Reserve’s watch.

And most monetary historians agree that the explosion of the money supply in the early 1970s, just before the election of 1972, was a disaster. The easy money policies, designed by Fed chairman and President Nixon appointee Arthur Burns, bolstered the president’s re-election. This created a Potemkin village effect.

The economy grew in the short term, then blew up creating the 1970s stagflation, ruining millions of lives for about a decade. Interest rates went over 20 percent, a nightmare for interest-sensitive industries.

The Fed’s easy money led to low or no growth along with high inflation rates. That was something that Keynesian economists, backed by a devotion to the Philips curve, had previously said would never happen. It happened.

It is logical that many historically literate people want to take away the money-making monopoly from government central banks. Their records of frequent recessions and sometimes depressions, inevitably lead to a boom and bust cycle.

Those governments that want to ban these new money developments may be fighting those who have come up with a better mouse trap. Canute like, the central bankers and their political allies may be trying to stop an inevitable wave.